Abstract

The notion that the international monetary system is hierarchical has become increasingly common, but the nature, causes, and shape of international monetary hierarchy remain vague. In this article, we develop a monetary theory of international hierarchy based on the “key currency” approach. We perceive the international monetary system as a world-spanning payment system that is inherently hierarchical because it needs central nodes for clearing and settlement. The centrality of the US-Dollar (USD) as global key currency places the US at the apex and makes the Federal Reserve (Fed) the system’s hierarchically highest institution. Other monetary jurisdictions are pushed into peripheral positions and rely on both using and creating USD-denominated credit money instruments “offshore.” Based on this approach, we explain international monetary hierarchy through different mechanisms to supply emergency USD liquidity from the Fed to non-US central banks. Currently, there are three different public mechanisms for non-US central banks to access the Fed’s balance sheet and attain emergency USD liquidity. The first-layer periphery may receive emergency USD liquidity via the Fed’s central bank swap lines. The second-layer periphery can make use of the Fed’s new repo facility for Foreign and International Monetary Authorities to access emergency USD liquidity. The residual mechanism for the third-layer periphery to access emergency USD liquidity is the Special Drawing Rights system, administered by the International Monetary Fund, in which the Exchange Stabilization Fund acts as gatekeeper for the Fed.

Keywords

Introduction

Multiple fields of research have come to describe the international monetary system as hierarchical. International monetary hierarchy is a theoretical position that stands in contradiction to the world of the Mundell Fleming model (Mundell, 1960; Fleming, 1962), which implicitly assumes that the international monetary system is “non-hierarchical.” This traditional approach perceives the international monetary system as comprised of hierarchically equal autonomous states as building blocks (Avdjiev et al., 2015) which issue their own money, co-exist next to each other, and have “monetary sovereignty” in a Westphalian sense (Murau and van ’t Klooster, 2022). Contrary to this notion, ideas of international monetary hierarchy can be found in various fields such as International Political Economy (IPE), for instance in Strange (1971), Cohen (1977, 1998) and Kindleberger (1970, 1974), post-Keynesian literature (Andrade and Prates, 2013; Bonizzi et al., 2012; Kaltenbrunner, 2015; Terzi, 2006), development economics (Alami et al. 2022; Arauz 2021; Fritz et al., 2018), scholarship in a Marxist tradition (Alami, 2018; Koddenbrock, 2019, 2020), the Money View (Mehrling, 2012, 2015; Pozsar, 2014), critical macro-finance (Gabor and Vestergaard, 2018; Gabor, 2020; Murau et al., 2020), legal scholarship on money (Pistor, 2013), or recent publications of the Bank for International Settlements (BIS) (Aldasoro and Ehlers, 2018; McCauley and Schenk, 2020).

The existing literature goes a long way in explaining the complex social relations that define international monetary hierarchy. Conceptions of hierarchy are typically linked to the international role of state-issued currencies, with the US-Dollar (USD) placed at the top, and other currencies following below (Cohen, 1998; Strange, 1971). Empirical measures such as central banks’ foreign exchange (FX) holdings (Eichengreen et al., 2017) or global FX market turnover (Fritz et al., 2018) have helped refine our understanding of a country’s respective position in the hierarchy by pointing to the use of its currency as a reserve currency or vehicle currency. More generally speaking, currency hierarchy is usually seen as evidence of the uneven geopolitical distribution of power amongst states in the international system. Here, the US and formerly the British Empire are typically posited as hierarchically highest states, followed by some competitors among the “developed” countries and surrounded by many subordinate “developing” countries. Views differ on the causes of international monetary hierarchy. Some see it as the result of intergovernmental policymaking (Strange, 1971), imperialism (De Cecco, 1984; Koddenbrock, 2019), or class relations (Alami, 2018). Others perceive it as an endogenous result of demand-driven market processes (Cohen, 1998; Kindleberger, 1975). Collectively, geopolitics and market mechanisms have given rise to a complex hierarchical system.

Despite many merits, the existing literature does not put forward a thoroughly monetary theory to explain the nature, causes, and shape of international monetary hierarchy. In focusing on factors such as the geopolitics of the existing currency order or its outright contestation through a rising hegemon, the literature tends to locate the politics of international monetary hierarchy outside of the monetary mechanisms that constitute the international system itself. In contrast, we emphasize the monetary character of hierarchy by attributing an internal tendency to credit money systems to form hierarchies, precisely because such systems need central nodes for clearing and settlement (Aglietta, 2018; Mehrling, 2012, 2015). How such credit money hierarchies are institutionally configured and mediated is the result of inherently political decisions. As we show below, a focus on the monetary character of hierarchy will help reveal more clearly where power is located in the system, how hierarchical structures and institutional arrangements coevolve, and why private actors gain privileges through a higher position within the hierarchy.

Although the hierarchical construction of credit money has primarily been explored in a domestic context, our theoretical contribution is to bring a key currency approach (Williams, 1934) into IPE to expand the analysis to the international level. We perceive the international monetary system as a global payments system in which money flows are settled mainly through interactions of private financial institutions. In its current shape, the international system is best understood as an “Offshore USD System” (Murau et al., 2020) as global transactions are heavily dominated by the use and creation of USD-denominated credit money instruments “offshore,” outside the US. The USD’s centrality as global key currency places the US monetary jurisdiction at the apex of the global payments system and pushes all other monetary jurisdictions into a peripheral position. In what follows, we discuss hierarchy within the context of the Offshore USD System.

In normal times, global access to USD liquidity is shaped by private credit markets. In times of crisis, when private credit money endogenously implodes, the role of the Federal Reserve (Fed) as international lender of last resort for emergency USD liquidity becomes paramount. Access to mechanisms through which non-US central banks can obtain emergency USD liquidity from the Fed determines the shape of international monetary hierarchy below the apex. We approach the different mechanisms through which non-US central banks can access emergency USD liquidity through non-market mechanisms as constituting three peripheral and hierarchically distinct layers in the Offshore USD System. The first-layer periphery can receive emergency USD liquidity via swap lines through which the Fed stands ready to create new USD-denominated central bank deposits on demand while accepting deposits of the partnering central banks as collateral. The second-layer periphery can make use of the Fed’s repo facility for Foreign and International Monetary Authorities (FIMA) to access emergency USD liquidity. First set up in March 2020 and made permanent in July 2021, the Fed creates new central bank deposits on the spot against US treasury bonds which non-US central banks have to accumulate beforehand and pledge as collateral. For the third-layer periphery, the best option to access emergency USD liquidity is via the Special Drawing Rights (SDR) system, set up in 1969 and administered by the International Monetary Fund (IMF), which allows indirect access to the Fed via the Exchange Stabilization Fund (ESF).

In analyzing the institutional features of emergency USD liquidity provision in the Offshore USD System, the empirical contribution of this article thus lies in shedding light on the asymmetric and hierarchical role of the Fed as an international lender of last resort in a precise and systematic manner. A key insight is that emergency interventions retain significance that transcend the moment of crisis itself: while the mechanisms discussed here are typically seen as a way to supply emergency USD liquidity or bridge funding gaps, they have broader effects on the constitution of the international monetary system. The mere existence of a credible backstop mechanism has a significant impact on market behavior, as implicit liquidity guarantees shape expectations around the availability of crisis support also in normal times. In providing a competitive edge for financial actors from those monetary jurisdictions with more secure access to emergency USD liquidity, the international backstop arrangements supported by the Federal Reserve thus have broader consequences for the distribution of financial power between non-US financial actors. In highlighting the importance of the Fed in shaping monetary hierarchy, we further clarify the functional relationship between the Fed and the IMF in the Offshore USD System. We stress the paramount importance of the Fed as the only central bank which can create new emergency USD liquidity without limits, while attributing merely a subordinate role to the IMF. This allows bridging the gap between so far disconnected strands of literature on the international monetary system that focus primarily on either one institution or the other.

Further, the integration of swap lines, the FIMA repo facility, and the SDR system into a consistent conceptual framework advances current debates about the nature, shape, and causes of international monetary hierarchy. One advantage of this approach is that it offers a more detailed analysis of the evolving institutional design of the international monetary landscape. In placing the focus of analysis on the institutional mechanisms that allow access to emergency USD liquidity, we highlight how international monetary hierarchy is constituted through pragmatic adaptation in institutional design, governance, and policymaking—a process akin to what Grabel (2017) has called the “productive incoherence” of global financial governance. Another advantage is that in highlighting the constitutive role of institutional mechanisms in shaping the place of a monetary jurisdiction within the Offshore USD System, our analysis brings to the fore the political economic significance of discretionary decisions on the part of the Federal Reserve regarding which country acquires access to specific funding mechanisms, such as central bank swap lines (e.g., McDowell, 2016, 2019; Sahasrabuddhe, 2019).

The remainder of this article is organized as follows. The Key currency theory and international monetary hierarchy section develops our explanation of the nature, causes, and shape of international monetary hierarchy from a key currency theory perspective. The International monetary hierarchy in the contemporary offshore US-dollar system section analyzes the three mechanisms for providing international emergency USD liquidity in the contemporary Offshore USD System. The final section concludes.

Key currency theory and international monetary hierarchy

Key currency theory is a conceptual perspective on the international monetary system that has undeservedly held a minority position in debates on international monetary organization. Williams (1934, 1943, 1944, 1949) is generally credited with founding this approach. He used his work on the intricacies of monetary management in the interwar years to argue against the Bretton Woods compromise during the 1940s, expounding his positions in multiple critiques of the Keynes and the White Plan and in a statement before the US Congress. In this context, the key currency theory is sometimes taken to contain Williams’ alternative vision for a post-war monetary order (James, 1996: 65–66), in which Williams called for a gradual pragmatic evolution of international monetary relations, as conceived by the 1936 Tripartite Agreement, rather than by establishing genuine international monetary institutions (Williams, 1943: 657). Subsequently, discussions of key currency theory featured in the Princeton economics debates, for instance in contributions from Machlup (1962), Lindert (1969), or Swoboda (1968). Another important and prolific user of the key currency concept was Kindleberger (1970, 1972, 1983) whose writings on the global dollar system continues to exert a strong influence on contemporary scholarship (Ito and McCauley, 2018; McCauley, 2020; Mehrling, 2022).

Although international monetary hierarchy features in most contributions to the key currency literature, the concept is typically used ad hoc, without a clear exposition of its nature, causes, and shape. The lack of clarity extends to the concept of key currency itself. For instance, Williams typically referred to his own thinking as a “key country” approach, but it was ex post labelled as one on “key currencies.” Hence, despite the intuition that the international system is organized around some “key” features, the precise nature of hierarchy in it remains vague. Moreover, as it is not always clear if hierarchy is an analytical term or something that is consciously constructed (Endres, 2005: 64), its causes and shape are not sufficiently explicit. Still, key currency scholarship provides a fertile soil for a monetary conceptualization of international monetary hierarchy. To achieve this, we present four tenets of key currency theory that logically build on each other and explain why the international monetary system is hierarchical, what the nature of this hierarchy is, and which factors determine its empirical shape. Our approach also helps to clarify the relationship of a key currency approach in relation to reserve currency or vehicle currency approaches.

The first tenet of a key currency approach to international monetary hierarchy is to perceive any monetary system as a payment system where public and private institutions, just as households and individuals, transfer credit instruments to each other that they accept and use as money. Any payment system may be imagined as a web of interlocking balance sheets, and as such it has an inherent hierarchy of participating balance sheets as well as the instruments they create, hold, and transfer. Hierarchically higher institutions create instruments as their liabilities which hierarchically lower institutions or individuals use as money assets. As such, the need to clear and settle payments already inherently creates a hierarchical structure within any domestic payment system. In a simple model of a traditional banking system, private commercial banks issue deposits as their liabilities when making a loan. The banks’ counterparties—from households and individuals to firms and states’ treasuries—hold deposits as their assets and use these to make payments to each other. If the households and firms have their accounts at different banks, those banks clear the payments on their balance sheets, typically by netting flows that go in either direction. Should an imbalance remain after clearing, the two banks will settle it with each other using the hierarchically highest form of money, reserves. These are provided as liabilities by the hierarchically highest institution in the payment system—the central bank (Aglietta, 2018; Hodgson, 2015; Mehrling, 2012).

The monetary instruments used in this payment system—in our example commercial bank deposits and central bank reserves—must be denominated in a currency, such as the USD, the British pound, or the Euro, which serve as a unit of account. The unit of account is a metric that allows commensurability of the different monetary instruments and their connection with the world of goods and services. In a smoothly functioning domestic payment system, there is only one unit of account. The units of account that are in practical use for the denomination of credit money in payments system are connected to states. Although this is not a logical necessity but the result of historical path dependence (Helleiner, 2003), it makes central banks the issuers of those instruments which are the hierarchically highest representation of a given unit of account (Murau and Pforr, 2020).

The second tenet of a key currency approach is to reject the widespread belief that the real-world international monetary system is an institutional arrangement that has been agreed upon among different states and is operated by a genuine international organization. By contrast, the key currency idea is to think of the international payment system as the extension of a country’s domestic payment system beyond its territorial and legal boundaries (Williams 1934, 1949: 333). Through this extension, it integrates actors and institutions from other monetary jurisdictions into its own payment system and determines one monetary jurisdiction in which clearing and settlement of cross-border payments occurs—we may think of this as the foundation of the international monetary hierarchy. The extended national monetary system forms the apex of the hierarchical international monetary system, its national currency takes over the role of the international “key currency,” and all other monetary jurisdictions and their currencies are pushed into a peripheral position. The apex represents the financial center in which the ultimate clearing and settlement of international payment flows take place (Kindleberger, 1983). The hierarchically highest institution in the international payments system is the apex central bank.

Such an apex of an international payment system can have regional scope or in some cases even be global. The first example of a global key currency was the Pound sterling in the heyday of the British Empire (De Cecco, 1984). International payments were ultimately cleared and settled in the City of London. Although the international monetary system of the time is commonly referred to as the Classical Gold Standard, it was—as Williams (1934) explains—in fact a Sterling standard. The “rules of the game,” which kept the Gold Standard operational (Eichengreen, 1992), were imposed by the Bank of England, which had a hegemonic position among all central banks that were part of the Gold Standard. Along those lines of thinking, the Bretton Woods System—forged in the last years of the Second World War—was less a restoration of the Gold Standard but mainly the establishment of a key currency system around the USD. Williams (1943, 1949) criticized the position that there was a genuine international system operated by the IMF. Instead, he regarded it as the essential challenge to stabilize the relationship between the new key currency, the USD, and the old key currency, the Pound Sterling. Such collaboration had already gone awry in the interwar years when Britain and the US could not provide an effective international monetary management. In particular, the Bank of England had failed its role as international lender of last resort in 1932 when it abandoned the Gold Standard and had thrown the international financial system into chaos (Kindleberger, 1973, 1983).

The third tenet is that—to be able to participate in the key-currency-based international payment system—instruments denominated in key currency are not only used but also created outside of the apex, offshore, in peripheral monetary jurisdictions. This aspect, which is more central to later key currency scholarship (e.g., Swoboda, 1968; recently McCauley, 2020), implies that peripheral banks create deposits not only denominated in their domestic currency but also in the key currency. The key-currency-denominated offshore deposits created by peripheral banks are formally constructed as promises to pay key-currency-denominated onshore deposits of banks in the apex, either on demand or in the near future (Mehrling, 2015). This results in an additional layer of hierarchy between peripheral banks and apex banks. Peripheral banks hold limited key-currency-denominated deposits as quasi-reserves for their offshore deposits. The peripheral banks’ business models depend on the ability to match the inflow and outflow of such payment commitments. Peripheral banks and their counterparties—whether households, firms, or treasuries—use key currency-denominated deposits for the purpose of cross-border payments, either to balance sheets in another peripheral monetary jurisdiction or the apex. Seen from this angle, the key currency functions as vehicle currency—following the terminology proposed by Lindert (1969) or Swoboda (1968)—or as a trade invoicing currency (Gopinath and Stein, 2018).

Offshore Pound sterling creation was common prior to the First World War (Harrod, 1952) but is statistically less well-documented (Lindert, 1969) than offshore USD creation in the Offshore USD System. The origin of offshore USD creation is the Eurodollar market, which came into existence in 1957 when banks in the City of London started dealing in USD-denominated bank deposits (Einzig, 1964). Originally used by socialist state banks from China and the Soviet Union that were interested in making USD-denominated transactions outside of the purview of US authorities, US banks soon discovered the advantages of the Eurodollar market for their own purposes and began to shift activities to the Eurodollar market to circumvent New Deal banking reforms such as reserve requirements and interest rate ceilings (Helleiner, 1994). Although the City of London remained the geographical heart of the Eurodollar market, offshore USD deposits soon started to be created in many other parts of the world in the 1970s (Braun et al., 2021).

The fourth tenet is that the apex central bank has to act as lender of last resort for key-currency-denominated instruments in the international payments system, including those issued offshore (Kindleberger, 1983). It is the access to emergency liquidity from the apex central bank which determines hierarchy below the apex and thus the actual empirical shape of international monetary hierarchy.

In normal times, international transactions in key currency do not require the involvement of central banks because settlement takes place in private markets. Yet any payment system is naturally prone to crises, understood as the initiation default of some promised payments to banks by their counterparties. As banks’ good loans turn bad, their balance sheet position changes. Losing some promised cash inflows of their assets, they may no longer be able to satisfy their own cash outflow commitments (Minsky, 1986). In any payment system, hierarchically higher institutions act as lenders of last resort to lower-ranking institutions to compensate for missing cash inflows in order to prevent a default contagion. As the central bank is located at the top of the hierarchy and issues the ultimate representation of the unit of account, it does not face any constraints in issuing new money. Peripheral banks may face a situation when some of their cash inflow commitments in key currency default and their customers insist on having their key currency deposits redeemed on demand. They could try to obtain emergency liquidity in key currency from banks located in the key currency jurisdiction which act as lenders of first resort (Mehrling, 2015). In some instances, however, this mechanism is insufficient—for instance, peripheral banks may find the borrowing conditions in private money markets too prohibitive, or apex banks may themselves be in crisis and unwilling to lend. Peripheral banks then have to rely on liquidity support from their domestic central bank (Kaltenbrunner, 2010).

For peripheral central banks, it is of profound difference if their domestic banks need instruments in domestic or key currency. If the shortage is in domestic currency, they can create unlimited emergency liquidity simply by expanding their balance sheets. If the shortage is in key currency, however, they can only on-lend the key-currency-cash balances previously accumulated in their FX reserves. This is one of the main reasons why the key currency is also the main reserve currency. However, the USD or the historical Pound sterling were not central because most central banks held them predominantly in their reserves, but rather central banks had to hold them in their reserves because of their key currency status. In a large systemic crisis, the volume of key currency instruments in peripheral central banks’ FX reserves will be lower than the key-currency-denominated claims outstanding and hence insufficient to prevent a default contagion. Then they need to borrow key-currency-denominated instruments from other balance sheets, and in the last instance the apex central bank (Kindleberger, 1974, 1983).

Key to the shape of the international monetary hierarchy below the apex are thus the mechanisms the apex central bank offers to peripheral central banks for emergency liquidity in key currency. Different privileges in cross-border lender of last resort arrangements induce a hierarchy among peripheral central banks and, by consequence, a stratification of countries and their monetary jurisdictions. The mechanisms for emergency liquidity provision in key currency provide an outside spread for peripheral banking systems, which is a competitive edge over other monetary jurisdictions. The more generous the mechanisms are for emergency liquidity provision, the more the distinction between the national and the international LOLR provision disappears. Therefore, to understand the empirical shape of today’s international hierarchy from a monetary perspective, we must analyze the mechanisms through which peripheral central banks are able to receive emergency liquidity in key currency from the apex central bank.

International monetary hierarchy in the contemporary Offshore US-dollar System

In the contemporary shape of the international monetary system as Offshore USD System, peripheral central banks can access the Fed’s balance sheet to receive emergency USD liquidity via three mechanisms: swap lines, the FIMA repo facility, and the SDR system. These three mechanisms induce a clear hierarchical layering among non-US monetary jurisdictions. The specific shape is the result of continuous institutional evolution. In their contemporary use, the Fed’s swap lines emerged during the 2007–2009 Global Financial Crisis and were re-affirmed and refined during the COVID-19 Crisis. The pandemic response also introduced the second mechanism, the FIMA repo facility. The third mechanism discussed here—the SDR system—has a longer historical lineage though it has grown in significance more recently due to two new rounds of SDR allocations in 2009 and 2021.

Our analysis focuses explicitly on those mechanisms that offer direct access to USD liquidity, at a timescale that justifies their classification as a form of emergency response, and that lack the type of conditionality often seen in IMF lending programs. Based on this approach, we exclude several mechanisms typically discussed in the literature on the global financial safety net. For instance, regional swap lines such as those belonging to the Chiang Mai Initiative typically provide funding in local currency, rather than in USD (Perks et al., 2021). More generally, regional financing arrangements—although they can serve a useful function in economizing on foreign exchange reserves—typically do not provide sufficient USD at the scale or speed necessary to meet emergency liquidity demands (Mühlich and Fritz, 2018: 990). As such, they play a supplementary role in attaining USD liquidity. IMF lending programs equally involve lengthy negotiations that disqualify such assistance from playing an effective role during liquidity crunches (McDowell, 2016). Hence, we argue that for those countries that have not been granted direct access to the Fed’s balance sheet via swap lines or which cannot procure the collateral needed to access the Fed’s FIMA repo facility, the SDR system offers the next-best option to access emergency USD liquidity and tap the Fed’s balance sheet indirectly, using the ESF as a gatekeeper.

The Fed’s central bank swap lines

The first-layer periphery of the Offshore USD System consists of monetary jurisdictions whose central banks are in an exclusive position to receive emergency USD liquidity from the Fed via central bank swap lines, which offer flexible access and low borrowing costs. This mechanism is only available to a select group of central banks which are relatively closely allied to the US. The more privileged central banks in the first-layer periphery are part of a standing, unlimited swap line network. This network comprises the US, the Eurozone, Japan, the United Kingdom, Switzerland, and Canada (“C6”). A second group of central banks have non-permanent swap lines which the Fed has so far activated whenever it found necessary. This extended network includes Australia, Brazil, Denmark, Mexico, New Zealand, Norway, Singapore, South Korea, and Sweden (“C14”).

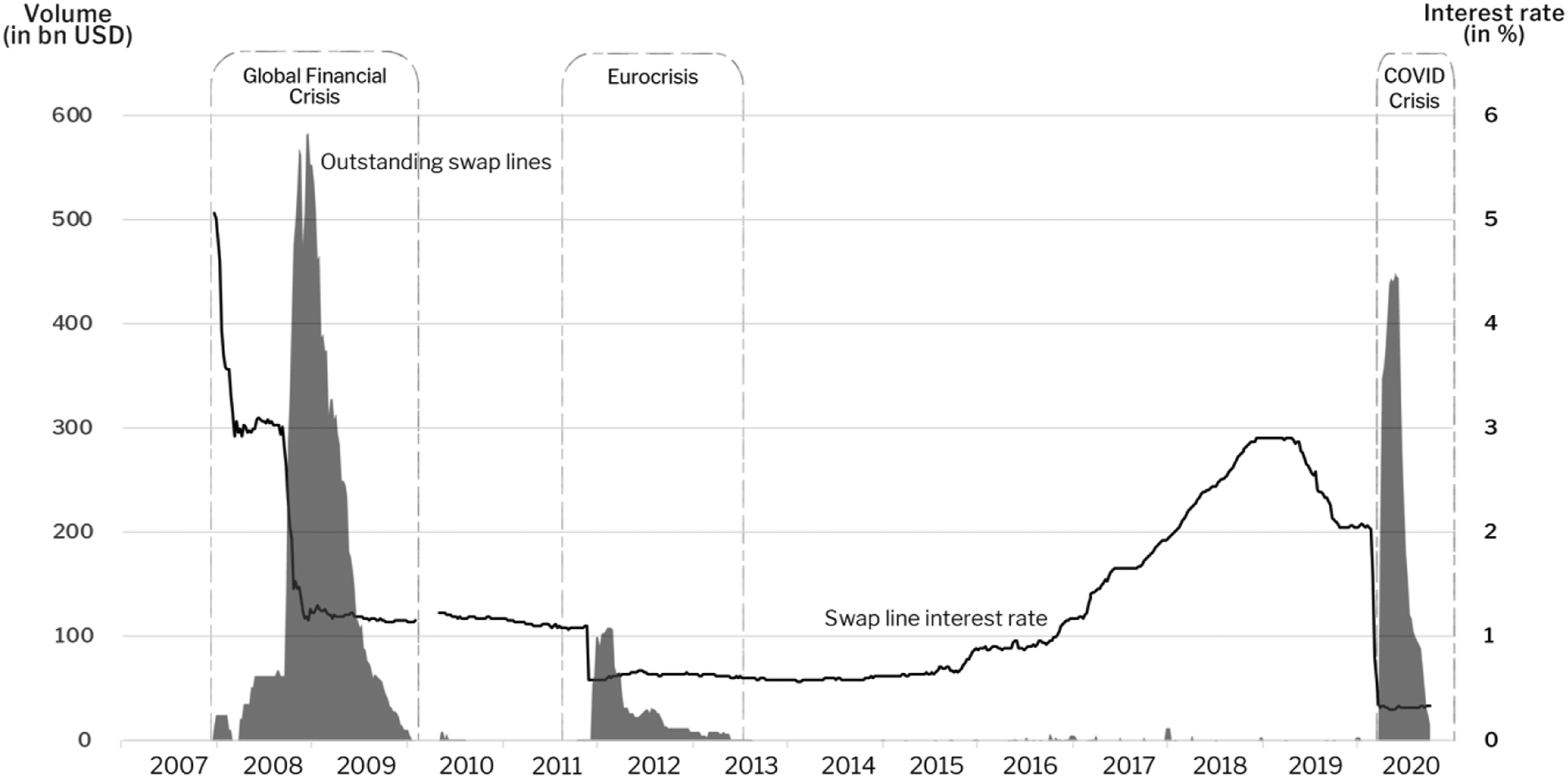

The Fed’s swap lines acquired their contemporary role during the Global Financial Crisis. They were designed to channel emergency USD liquidity through foreign central banks to foreign banks and counter an acute USD funding shortage in the Eurodollar market that was threatening to disrupt US money markets as well. The first swap lines were set up in December 2007 with the ECB and the Swiss National Bank (SNB) and were capped at 20bn USD and 4bn USD, respectively (Goldberg et al., 2010). After the failure of Lehman Brothers, they were doubled in size, and new lines with the Bank of England (BoE), Bank of Canada (BoC), and Bank of Japan (BoJ) were added, bringing the total allotments to 247bn USD. As funding disruptions spread further, the Fed extended these lending agreements to a total of 14 swap lines with ever larger volumes. The scale of the crisis swap operations is difficult to overstate. Already on 13 October 2008, the swap lines to the BoE, the ECB, and the SNB became unlimited in size to accommodate any quantity of USD funding demanded. They provided emergency USD liquidity far in excess of existing FX reserves, which had been estimated at a total of 294bn USD in mid-2007 for the Eurozone, Switzerland, and the UK combined (McGuire and von Peter, 2009: 20).

The crisis swap lines were terminated in February 2010 but resurrected only three months later in a modified form between the Fed and five major central banks—the ECB, the SNB, the BoE, the BoJ, and the BoC. In 2011 and 2012, swap drawings continued especially by the ECB as European banks experienced further funding troubles amidst the intensifying Eurocrisis. In November 2011, the swap lines were converted into a network extending bilateral swap lines between each of them. In October 2013, this network was announced to be made permanent and unlimited, putting in place an indefinite backstop. In March 2020, during the COVID-19 Crisis, the Fed reactivated the C14 swap lines as temporary and limited arrangements. Outstanding swap drawings peaked at 449bn USD in May and helped alleviate acute USD cash-flow problems in international funding markets. Unlike in 2007–2009, however, most drawings were not from the ECB, but from the BoJ, indicating a shifting pattern of global USD funding needs (Pape, 2022).

The initial crisis swap lines were exclusively USD swap lines designed to supply USD to foreign central banks, such as the ECB. The agreements stipulated that the ECB should pay interest on the proceeds of any swap transaction calculated at the rate of the applicable Overnight Indexed Swap (OIS) Rate plus a 100-basis-point spread. The Federal Reserve Bank of New York (FRBNY), by contrast, did not pay interest and did not invest but simply held the funds on its accounts (Fleming and Klagge, 2010). A reciprocal swap line—allowing the drawing of either currency—was only established on 30 November 2011 between the Fed and its five counterparts.

Figure 1 shows the volume and price for swap lines during the Global Financial Crisis, the Eurocrisis, and the COVID-19 Crisis. The terms of the swap contract have been amended several times. The spread over OIS was first reduced from 100 to 50 bps on 30 November 2011 and further lowered to 25 bps on 15 March 2020. Transcripts of Federal Open Market Committee (FOMC) meetings in 2011 indicate that the initial repricing was intended to encourage greater uptake of swap lines during the Eurocrisis and to discourage foreign banks from drawing funds from the Fed directly via their US-based branches (FOMC, 2011). Although FOMC transcripts are not yet available for 2020, it is likely that similar considerations to limit the use of the Fed’s domestic facilities were at play during the COVID-19 Crisis. As swap lines are offered in varying maturities and the Fed uses matching OIS (e.g., one-week swap is priced off one-week OIS rate), swap prices are variable, which is not reflected in the graph. Federal Reserve swap line drawings and interest rate (2007–2020).

Swap line agreements can be understood as contingent assets and liabilities that represent a mere potentiality for peripheral central banks to receive emergency USD liquidity without depending on pre-existing FX reserves. Once the swap line is activated, “actual” assets and liabilities emerge. The FRBNY creates a new USD-denominated liability that it deposits into a special account for the partnering central bank, which holds it as an asset; and vice versa the other central bank creates a new liability credited to the FRBNY account. This process increases the amount of FX reserves on central bank balance sheets “out of thin air” (Coombs, 1976: 76). The establishment of unlimited swap lines between the C6 in 2013 thus effectively implies that the Fed stands ready to provide expansions of its balance sheet in indefinite quantities to meet the USD needs of these central banks.

For the first-layer periphery, the Fed’s swap lines are a flexible mechanism for providing emergency USD liquidity at rapid speed. For this reason, swap lines are credited with restoring confidence in the USD and calming international markets during periods of crisis (Goldberg et al., 2010). At the same time, the Fed’s swap lines have been criticized for their selectiveness and opaqueness, giving power to technocratic central banks rather than multilateral political agreements (Sahasrabuddhe, 2019). As studies on the politics of swap line access show, the explicit division of Federal Reserve swap lines into a “core,” standing network and several additional, temporary swap lines creates two tiers within the first layer periphery of the offshore USD system. Drawings and total amounts for temporary swap lines remain limited and typically must be approved in a way that the core swap lines do not. Here, the Federal Reserve maintains significant political leeway in granting or refusing swap line access to countries (McDowell, 2012; Sahasrabuddhe, 2019). Although the politics of access and the resulting differences between swap line recipients are significant, we maintain that access to a swap line (whether conditional or unconditional) offers countries a strategic advantage in attaining emergency USD liquidity over those who are unequivocally denied access to this mechanism. For this reason, we categorize all swap line recipients as first-layer periphery.

The Fed’s FIMA repo facility

The second-layer periphery in the Offshore USD System is made up of monetary jurisdictions whose central banks do not have access to the Fed’s balance sheet via swap lines but who can interact with it via its foreign repo facilities. The prerequisite is that those non-US central banks have an account at the Fed and hold enough US treasury bonds in stock to pledge as collateral. Although this mechanism is comparable in flexibility with swap lines, repo transactions are less attractive as central banks require previously accumulated US treasury bond holdings. The group of monetary jurisdictions that belongs to the second-layer periphery is more difficult to define than first-layer peripheral countries since the binding constraint is their holdings of US treasury bonds, which is not always known and fluctuates over time. We may contend that it includes those monetary jurisdictions with a high degree of global financial integration that have not received a swap line, possibly for political reasons, such as China.

The Fed announced the creation of a temporary repo facility for foreign and international monetary authorities (FIMA repo facility) on 31 March 2020. Taking up operations on 6 April, the FIMA repo facility allowed non-US central banks and other monetary authorities that have an account at the FRBNY to conduct repurchase transactions with the Fed and to pledge US treasury bonds as collateral to receive USD-denominated central bank deposits, which can then be made available to institutions in their respective monetary jurisdictions. The explicit goal of the facility is to smooth the functioning of key segments of both domestic and offshore USD markets, including the US treasury bond market (Federal Reserve, 2020). On 27 July 2021, the FIMA repo facility was made permanent (Federal Reserve, 2021).

The Fed decided to introduce the FIMA repo facility due to disruption in the US treasury market. The March 2020 market turmoil saw a sudden “dash for cash” by global investors whose usual income streams collapsed due to pandemic shutdowns. Driven by the sudden unwinding of hedge funds’ leveraged trades and the liquidation of large treasury portfolios by foreign official reserve managers, the treasury bond market witnessed a sudden bout of unprecedented volatility. In this context, the new FIMA repo facility allowed non-US central banks to access emergency USD liquidity without having to sell into a falling market, potentially exacerbating instabilities (Setser, 2020). For the US, the primary purpose of the facility thus is to act as a backstop: the implicit purpose is to discourage panic-selling of US Treasury securities by providing a credible outside option for foreign monetary authorities. By making the facility permanent in July 2021, the Federal Reserve thus enshrined a novel mechanism within the institutional architecture of the Offshore USD System.

From the perspective of foreign monetary authorities, the FIMA repo facility offers a way to ease strains in global USD funding markets, thereby mirroring the function of the Fed’s swap lines. Unlike swap lines, however, it does not use foreign currencies as collateral but US treasury bonds. The difference is important. Although foreign central banks can create their own currencies as a liability on the spot, access to the FIMA repo facility is limited by the amount of US treasury bonds accumulated beforehand (Federal Reserve, 2020).

The FIMA repo facility thus expands the scope of interactions between the Fed and non-US central banks. Central banks usually maintain deposit and custody accounts between each other to facilitate cross-border payments as well as to invest, settle, and hold currency reserve balances. Although such investment services allow foreign central banks and public reserve managers to invest liquid dollar holdings with the Fed directly, most FX reserves continue to be invested in private markets, such as in the FX swap market or in US treasury bonds, leaving open the possibility of treasury bond market volatility amidst large-scale liquidations (Rommerskirchen, 2020). The introduction of the FIMA repo facility seeks to redress this situation by allowing non-US central banks to exchange their Treasury bond holdings against cash outside of the private market mechanism. The Fed, just as in the case of swap lines, creates new USD-denominated central bank deposits out of thin air.

The idea that repo transactions backed by US treasury bonds is a “second best” option next to swap lines finds expression in discussions by the FOMC as early as October 2008. During the Global Financial Crisis, just after Lehman Brothers had collapsed, FOMC members considered extending swap lines to EMEs. Keen to offset any repayment risks, the FOMC decided to grant swap lines to only four EME countries—Mexico, Brazil, South Korea, and Singapore—that all had large USD-denominated reserve holdings, followed generally prudent monetary policies, and had roughly balanced current account and fiscal positions. Yet even amidst these favorable conditions, the FOMC took comfort in the broader “set-off rights” of the FRBNY: as these foreign central banks already held part of their USD-denominated FX reserves on accounts with the FRBNY, in case of non-repayment the Fed would be able to simply confiscate the assets already on its books (FOMC, 2008: 19). Ultimately, the FOMC rejected the idea of lending officially to other central banks against US treasury collateral on the basis that this might be considered stigmatizing (McDowell, 2016).

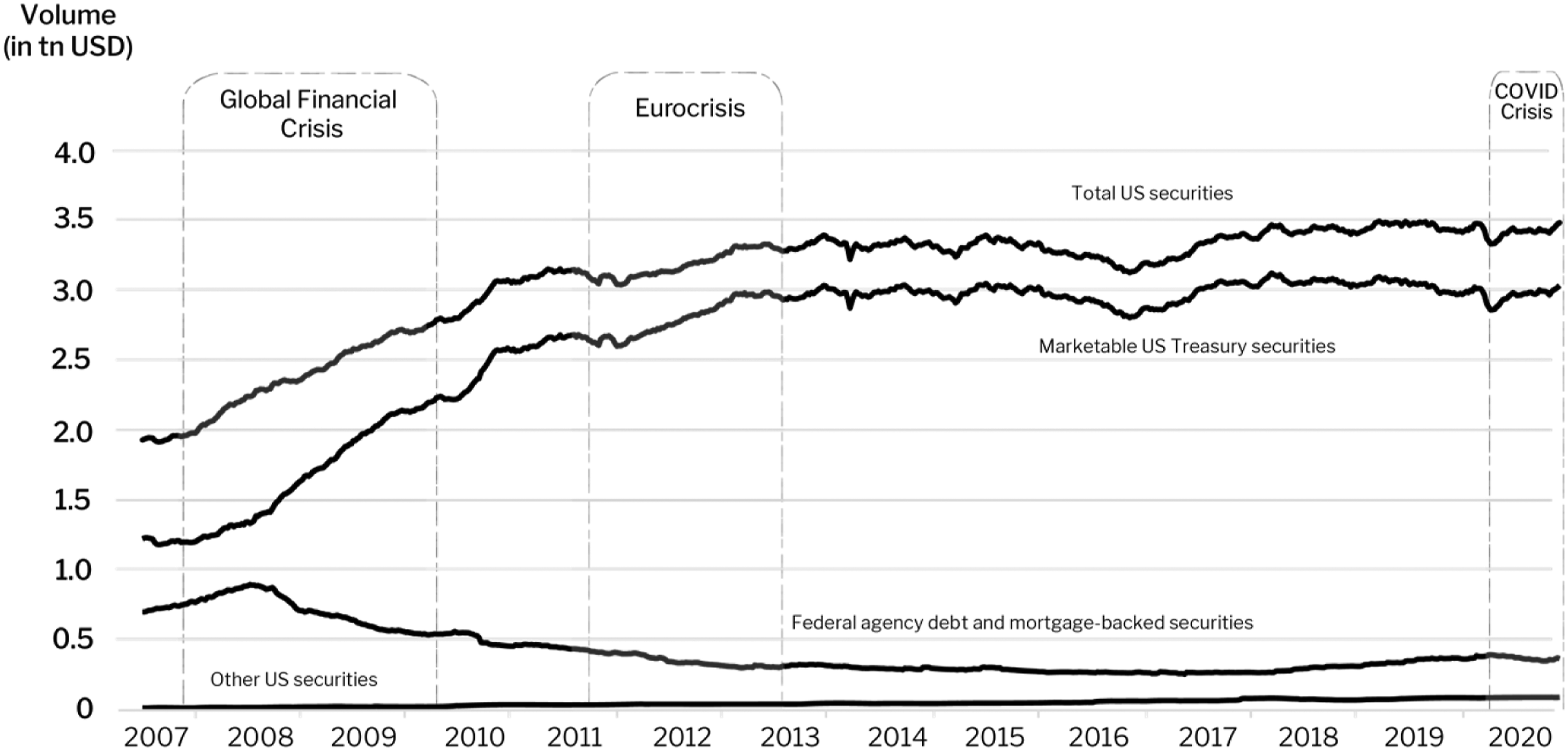

With the introduction of the FIMA repo facility in March 2020, the Fed revived this idea by providing mechanism to supply emergency USD liquidity for central banks with sufficient US treasury bond holdings, which we summarize as second-layer periphery. Who belongs to that group is less straightforward to determine than in the case of swap lines: On the one hand, the holdings of US treasury bonds by non-US central banks is confidential information. Individual central banks tend to publish only aggregate volumes of their FX reserves without specifying exact instruments and denominations. Vice versa, US authorities publish information about the total volume of US treasury bonds held by non-US central banks but do not specify individual institutions (see Figure 2). On the other hand, even if these positions were known, there is no clear-cut definition for how many treasury bonds need to be held in order to be included in membership of the second-layer periphery. US securities holdings of non-US central banks (2007–2020).

In summary, the second-layer periphery is defined by the FIMA repo facility—the latest innovation in the global financial architecture, single-handedly introduced by the Fed during the COVID-19 Crisis in March 2020. It allows channeling emergency USD liquidity from the Fed’s balance sheet to that of non-US central banks facing a shortage of liquid USD instruments in their FX reserves. Although the facility has rarely been used, its mere existence offers a pertinent liquidity insurance that helps to calm market sentiments in those monetary jurisdictions without access to swap line funding. As a “second best” alternative to swap lines, the FIMA repo facility serves those monetary jurisdictions that do not entertain close geopolitical ties with the United States—most notably, China, which holds a large reserve position in US treasury bonds, but also other monetary jurisdictions such as Taiwan, Hong Kong, or India (Setser, 2020).

The Special Drawing Rights system

The third-layer periphery in the Offshore USD System consists of monetary jurisdictions whose central banks neither have access to the Fed’s swap lines nor do they have sufficient holdings of US treasury bonds to use the FIMA repo facility. The remaining mechanism available to them to receive emergency USD liquidity outside of private markets is the SDR system. Third-layer-periphery central banks can use the SDR system to borrow usable currency—first and foremost denominated in USD—from other members of the SDR system. Access to the Fed is only indirectly possible, with the Exchange Stabilization Fund (ESF) functioning as a gatekeeper. Instead, most emergency USD liquidity in the SDR system is provided by central banks of the first and second-layer periphery. The SDR system is a small payment community that currently comprises 206 members: one institution per IMF member country called “Participant,” typically the central bank (Ocampo, 2017: 61), and only rarely treasuries or off-balance-sheet fiscal agencies such as the ESF (Henning, 1999); the IMF itself, which is represented in the form of the General Resource Account (GRA); as well as 15 Prescribed Holders such as the BIS, the ECB, and multilateral development banks. The SDR system is administered and operated by the SDR Department, a sub-balance sheet of the IMF.

Created in 1969 as an attempt to rescue the crumbling Bretton Woods System, the SDR system is based on idiosyncratic accounting rules that are the result of a French-US compromise and it is notoriously opaque. Although there was a shared interest to create a new international reserve asset in addition to gold and USD-denominated instruments, the US wanted the new asset to be a non-interest-bearing instrument or “outside money” such as gold, while the French wanted it to be interest-bearing credit or “inside money” such as drawings under IMF quotas. The SDR system that got adopted is the attempt to provide a mix of both positions (Kindleberger, 1975). It is only possible within this accounting logic to see how the SDR system, which was designed for the Bretton Woods System, serves as a mechanism for supplying emergency USD liquidity to peripheral monetary jurisdictions in the Offshore USD System (Pforr et al., 2022).

In these accounting rules, the label “SDR” simultaneously denotes two types of financial instruments and a unit of account. The instruments are properly called “SDR holdings” (a tradable asset) and “SDR allocation” (a non-tradable liability) (Galicia-Escotto, 2005). These instruments are denominated in SDR as a unit of account. We use the international ISO 4217 currency code “XDR” when we refer to the SDR as unit of account. Upon introduction of the SDR system in 1969, the XDR was identical with the USD. Only in 1974, after the collapse of the Bretton Woods System, did the value of XDR become determined by a currency basket that fluctuates against other units of account, including the USD (Kindleberger, 1975).

Special drawing rights instruments are created on the balance sheets of the Participants in an SDR allocation. A new round of SDR allocation must be agreed upon by the IMF Executive Board, which also stipulates the amount of new SDR creation. Once approved, the general amount is divided among the participating institutions according to the quota shares of IMF members. Hence, IMF members with the greatest quota will receive the most SDR holdings and SDR allocation. Historically, there have been four rounds of SDR allocation: in 1970–72, 1979–81, 2009, and 2021. Today, the total volume of SDR holdings and SDR allocation stands at 660 bn XDR. After an SDR allocation, the amount of SDR holdings and SDR allocation is inelastic in the SDR system. Importantly, an SDR allocation affects neither the balance sheet of the IMF nor that of the Fed. Each Participant receives interest on its SDR holdings and has to pay interest on its SDR allocation. As both are compensated with the same interest rate, no interest is payable as long as the institution’s SDR holdings are equivalent to its SDR allocation. The interest rate is calculated as a blended average of the key interest rates of the basket currencies (IMF, 2018: 86).

After an allocation, the SDR system allows Participants to sell their SDR holdings in exchange for usable currency to other Participants or Prescribed Holders. This mechanism—called “transactions by agreement”—is how Participants can use the SDR system to obtain emergency USD liquidity. Although it is open to all participants, it is most attractive to central banks in the third-layer periphery. Once the third-layer central bank decides to sell its SDR holdings, it has to choose the usable currency it wants to receive in return. Although no official data exist about the share of USD obtained through transactions by agreement, it stands to reason to assume that the USD makes up the largest share. It typically takes around eleven workdays from an expression of interest to convert SDR holdings until USD-denominated instruments are received by a third-layer central bank (IMF, 2018: 104). This makes it slower than the other mechanisms for effective emergency USD liquidity provision.

Transactions by agreement may look like the sale of an asset that has previously been provided as a “free lunch” by the SDR allocation. However, only the creation of SDR holdings and SDR allocations is free of charge. The usage of SDR holdings effectively is a loan. As soon as a third-layer central bank has converted its SDR holdings into usable currency, it will have to pay interest on the difference between its remaining SDR holdings and its original allocation, whereas its counterparty receives interest payment on the excess of its SDR holdings over the original SDR allocation, whereas the cost of borrowing via transaction by agreement involves only the nominal SDR interest rate, the usage of other IMF lending channels also incurs additional fees and charges (“SDR adjusted rate of charge”) (IMF, 2018: 89, 95). The SDR department administers the transfer of payments.

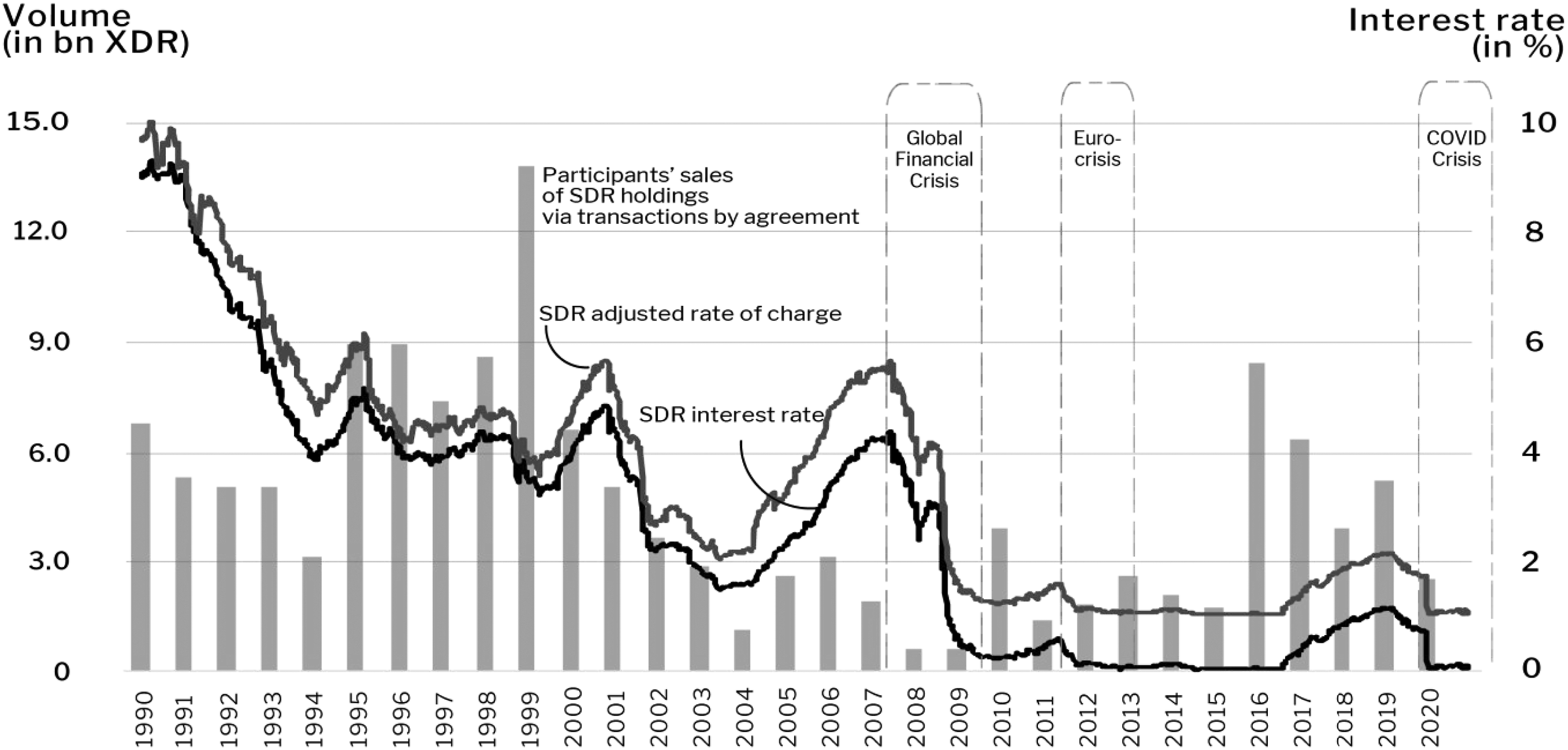

Figure 3 shows the volume of usable currency that Participants obtained via transactions by agreement from 1990 to 2020 as well as the SDR interest rate and the SDR adjusted rate of charge. These data—based on IMF Annual Reports—do not reveal which currencies have been borrowed. Although it shows comparatively high borrowings in the 1990s, there were relatively low borrowings in the context of the Global Financial Crisis or the COVID-19 Crisis in 2020. This may be explained by the fact that least developed countries in the third-layer periphery who would be most dependent on emergency USD liquidity through the SDR system receive the smallest allocations and had drawn over 80% of their SDR allocation before the 2009 allocation (Ocampo, 2017: 61–62). Similarly, the new borrowing potential after the 2021 allocation can only influence future sales of SDR holdings. SDR holdings sold via transactions by agreement and SDR interest rates (1990–2020).

When the third-layer central bank sells SDR holdings, it obtains emergency USD liquidity from a counterparty which acts as a “market maker” in the SDR system as it has a Voluntary Trading Agreement with the SDR Department. In most cases, this will be a first or second-layer central bank, which does not create new USD-denominated instruments but sells those previously held in their FX reserves. The situation differs when the ESF is the counterparty and the third-layer central bank receives emergency USD liquidity directly from the apex. As before, selling SDR holdings entails that the central bank and the ESF exchange SDR holdings against USD-denominated deposits held at the Fed. In a next step, the ESF can issue “SDR Certificates” which are acquired by the Fed, thereby creating new USD-denominated central bank deposits (US Treasury, 2019: 72–73). In this case, the Fed creates new USD liquidity that it channels into the SDR system. The third-layer central bank was able to access the Fed’s balance sheet, albeit only mediated by the ESF, which in this regard has a gatekeeper function.

Although the first lending channel via central banks in the first and second-layer periphery appears to be more widely used than the second channel via the apex (Ocampo, 2017: 63–64), the ESF is nevertheless a net supplier of USD-denominated instruments via the SDR system. As of January 2022, its SDR holdings of 163.5bn USD exceeded its allocation of 159.8bn USD by 3.7bn USD. This difference was financed by an outstanding volume of SDR Certificates at 5.2bn USD (US Treasury, 2022: 2). In theory, the maximum level of SDR Certificate issuance amounts to the total volume of SDR allocations (Special Drawing Rights Act of 1968, Sec. 4a). Even though the issuance of SDR Certificates occurs at a comparatively low level since the 2000s—the last time any issuance occurred was in response to the 2009 allocation, which saw the creation of an additional 3bn USD SDR certificate—this mechanism was extensively used during the 1980s and 1990s (FRED, 2022). Hence, we seem to see a dynamic at play where the Fed is the potential lender of last resort within the SDR system whereas the market-maker central banks of the first and second-layer periphery are lenders of first resort. However, this lender of last resort function so far has never been fully put to the test.

It is true that third-layer central banks can also access public sources of emergency liquidity other than the SDR system, which creates a further differentiation among them. This includes bilateral swap lines, regional financing arrangements, and IMF lending programs. Through each of these mechanisms, individual countries can improve their respective liquidity position within the global monetary system (Mühlich and Fritz, 2018). These mechanisms are best thought of as supplementary—not only because they are unable to establish any sort of connection to the apex central bank but also because they tend to lack the speed and scale necessary to meet emergency USD liquidity needs. For instance, despite the proliferation of bilateral swap line agreements in recent years (McDowell, 2019), one factor that tends to limit these agreements is that they are typically not denominated in USD. The only exception here are the bilateral swap lines of the Japanese Treasury and India’s swap line to the Maldives (Perks et al., 2021: 17). Similarly, IMF lending and regional financing agreements typically are not available at short notice and may carry additional conditionality requirements. Compared to all these options, the SDR system also tends to be the cheapest source of funding available to these countries (Perks et al., 2021).

Overall, the importance of the SDR system lies in the fact that it provides a public last resort mechanism for all those countries which do not have access to the Fed’s swap lines or FIMA facility. SDR holdings function as a de facto credit line for this purpose. In that sense, the SDR system parallels central bank swap lines (Ruhlmann and Holmberg, 2017: 6). To use this mechanism, non-US central banks must have a sufficiently high SDR allocation and a sufficient level of SDR holdings remaining in their FX reserves. As the mechanism is less preferential than swap lines or the FIMA repo facility, it is most useful to central banks in the third-layer periphery whose domestic banking systems enjoy worse implicit USD liquidity guarantees than those of hierarchically higher monetary jurisdictions.

Conclusion

This article has presented a novel monetary conceptualization of the nature, shape, and causes of international hierarchy by focusing on different ways of supplying emergency USD liquidity from the Fed to non-US central banks. By highlighting the institutional characteristics of the Offshore USD System, our framework allows us to connect the established IPE literature on monetary hierarchy with scholarship on the Fed’s role as international lender of last resort and studies on the politics of swap lines. Moreover, we offer a way to integrate the SDR system into the picture and stress the significance of SDR Certificates, thus shedding a new light on the interconnection between the Fed and the IMF with regard to international monetary hierarchy.

The article advances both a theoretical and an empirical contribution. Regarding the former, we show that monetary hierarchy results from the need for some ultimate means of clearing and settlement. As payments systems based on credit money are inherently hierarchical, there tends to be one institution which issues this ultimate means of settlement. In the modern context, this institution is the central bank. International monetary hierarchy is the result of a national payment system stretching across borders and integrating other monetary jurisdictions into its orbit. When one country’s unit of account is heavily used in the payment systems of most other countries, we can speak of that country as being at the apex of the international monetary system and its central bank becomes the apex institution of the global monetary system. In today’s institutional structure, these roles are played by the USD and the Federal Reserve, respectively. Regarding the latter, we shed a precise and systematic light on asymmetric mechanisms for the provision of emergency USD liquidity, highlighting the key role of the Federal Reserve policymaking in shaping hierarchy through the pragmatic adaptation of institutional mechanisms within the Offshore USD System.

Our approach to international monetary hierarchy leads to several important insights that can guide future research. First, our institutional analysis offers a novel lens for understanding monetary power. By highlighting access to the Federal Reserve as a key metric, we showcase the power of the Fed to determine whether a country is granted the status of first layer periphery. In emphasizing institutional design, our analysis offers a potent framework to conceptualize the enduring inequality in the international monetary system. We argue that the existence of emergency mechanisms confers a special advantage onto private finance even during non-crisis times, as they can rely on established backstopping arrangements. As commercial banks in hierarchically higher peripheral monetary jurisdictions can receive emergency USD liquidity at more favorable rates, they face structurally cheaper borrowing conditions in the Eurodollar market (Mehrling, 2015), which provides them with a competitive advantage. How reliable such access is, and how (geo)politics are tied up with access, has long been part of the literature on central bank swap lines. Recent events—such as the freezing of Russa’s FX reserves as part of the economic sanctions following the invasion of Ukraine—highlight how the institutional structure of the international monetary architecture confers exorbitant monetary power on the US.

Second, our approach also yields insights into currency competition. As the history of the interwar years shows, a change in key currency—such as the one that took place from the GBP to the USD— is likely to be preceded by a failure of institutional mechanisms at the very apex of the system. The granular analysis of the institutional mechanisms that underpin the stability of the USD-centric international order can therefore usefully be extended to analyze questions of currency competition. Current debates about RMB internationalization, for example, rarely consider the payment mechanisms that would be needed to sustain and underpin such an expansion and challenge to the existing international order. Without widely available public backstops, a possible challenger currency is unlikely to usurp an existing key currency.

Finally, our approach shows the importance of analyzing USD borrowing and lending in the SDR system, an institutional feature of the international monetary system that is typically overlooked or dismissed as irrelevant. Following a dramatic expansion of existing SDR resources after the pandemic, our framework thus helps situate debates about the role and purpose of the SDR system in the contemporary international monetary system.

Footnotes

Acknowledgements

For reading and commenting on this manuscript at various stages, we are deeply indebted to Iñaki Aldasoro, Torsten Ehlers, Frederik Vitting Herrmann, Elizaveta Kuznetsova, Perry Mehrling, Mathis Richtmann, Zoltan Pozsar, and Jens van ‘t Klooster. We also wish to thank two reviewers for their excellent feedback. All remaining errors remain naturally our own.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: S.M. acknowledges financial support by the German Research Foundation (DFG, project number 415922179). F.P. was supported by the UK Economic and Social Research Council (grant number 1912377).