Abstract

In recent years the pharmaceutical industry has been accused of prioritising profits from patents at the expense of the wellbeing of patients. Many argue that this transition reflects the full-scale financialization of the industry, whereby an increasing focus on shareholder value and financial performance has resulted in cost-cutting, outsourcing and novel forms of competition based on securing new patents and intellectual property rights through mergers and acquisitions (M&As). The aim of this article is to explore the variegated financialization of the pharmaceutical industry through the analysis of M&A data. Acknowledging M&As as a key tenet of pharmaceutical financialization and drawing from a sample of 1805 deals between 2001–2020, we reveal an uneven geography of acquirers and targets across the global, national and city scales. While we uncover a global rise in the value and volume of M&A deals, this activity is concentrated across a limited geography, with the US the largest market by value and China the largest by volume. Analysing these two countries in depth reveals the importance of institutional and regulatory conditions in not only shaping the implementation of M&As but fundamentally constituting the nature, causes and effects of financialization. These findings allow us to develop a relational conceptualisation of financialization which adds novelty to geographical debates around its uneven causes, processes and outcomes.

Introduction

It is no exaggeration to say that the survival of the human race depends on pharmaceutical firms. For centuries these firms have been at the vanguard of developing life-saving medicines, curing the incurable and, albeit unevenly, improving standards of living around the world. The importance of these firms has only been further enshrined by the Covid-19 pandemic, with ‘big pharma’ (Pfizer, AstraZeneca, Novartis, Johnson and Johnson, amongst others) central to the vaccine rollout. In fact, if you are reading this article then there is a very high chance that you have been injected with the product of one of these firms. These firms are also likely to have helped you soothe a migraine, survive a cold or recover from a more serious illness. The point is that pharmaceutical firms are important to everyone everywhere, without exception.

But what happens when pharmaceutical firms become less interested in saving lives and more interested in generating returns to shareholders? Many commentators argue that this has been the case for decades now, with the pharmaceutical industry undergoing a process of financialization (Fernandez and Klinge, 2020; Froud et al., 2006; Gleadle et al., 2014). Defined as the growing importance of financial motives, markets, actors and institutions on society, financialization has become a defining characteristic of 21st century life (Epstein, 2005). It highlights the permeation of financial logics throughout the economy, politics and society, resulting in seismic shifts in how national economies function, how firms are governed and how households spend their money and save for the future (French et al., 2011; Langley, 2007). In the context of pharmaceutical firms, financialization has partly but not exclusively incentivised cost reductions, the outsourcing of production, the monopolisation of intellectual property rights (IPR), growth through mergers and acquisitions (M&As) and increased shareholder value orientation (Busfield, 2020; Danzon et al., 2007; Fernandez and Klinge, 2020; Gleadle et al., 2014).

While all aspects of financialization are important to our analysis, we are principally concerned with M&As. All pharmaceutical firms producing the Covid-19 vaccines as of late 2021 are the product of M&A activity, with Pfizer and AstraZeneca prime examples. Both of these firms have used M&As to extend their product portfolios, access new knowledge and develop the manufacturing, research and logistical capacities which have proven central to vaccinating billions of people. On the one hand, financialization has birthed pharmaceutical behemoths capable of rapidly developing vaccines which have saved countless lives. On the other, and thinking beyond just vaccines, this financialization has come at a cost, as other areas of medicine have been neglected due to a short-term pursuit of profits, shareholder value and market capitalisation which prioritise financial performance ahead of social utility.

With few exceptions (Froud et al., 2006; Rafols et al., 2014), geographically framed studies on the pharmaceutical industry remain limited. While research on the financialization of pharmaceuticals has identified its role in transforming the business models, market structures and competitive dynamics of the industry, much less focus has been devoted to exploring the spatiality of these transformations and their geographical causes and effects. Some research has explored the transnational nature of big pharma (Rafols et al., 2014; Fernandez and Klinge, 2020), but these studies focus on a small number of firms and pay less attention to the global and relational geographies of pharmaceuticals which extend beyond the leading companies. This neglect of geography means that we know comparatively little about where the financialization of pharmaceuticals is taking place and even less about where it is not, and why. These empirical gaps are aggravated by deficiencies in our understanding of financialization, including its uneven geographies (French et al., 2011), homogenous characterisations (O’Brien and Pike, 2017) and actual existence based on genuine empirical evidence (Christophers, 2015).

The overarching aim of this article is to explore the variegated financialization of the pharmaceuticals industry through the analysis of M&A data. Variegated financialization refers to the uneven, contingent and contested enactment of its logics and processes across different spatial settings, as firms respond to its challenges and opportunities in novel ways (Appleyard et al., 2016; Keenan, 2020). Drawing from a sample of 1805 M&A deals between 2001–2020, we reveal the changing landscape of acquisitions across spatial scales. At the global scale, we show how the vast majority of deal value and volume is concentrated in Asia, Europe and North America. Beyond providing a comprehensive global picture, and in order to meaningfully analyse the variegation of financialization across geographical scales, we focus on two examples: the

These findings allow us to make new empirical and conceptual contributions. Empirically, we show that the financialization of the pharmaceutical industry is spatially variegated. We present fresh empirical insights which support the argument that the pharmaceutical industry has become increasingly financialized but show that the geographical causes and implications of this transformation are highly uneven. While contributions revealing the uneven, contested and contradictory nature of financialization are now well versed, our article advances an original relational understanding of financialization based on acknowledging the causal and constitutive role of geography. The inherent nature of M&As, with decision-making power moving between firms and places, allows us to conceptualise the relational spaces of financialization. This is because M&As are the principal corporate mechanism through which financialized activities can reach new places and enrol new actors, while avoiding others and creating a limited and exclusive geography. This relational conceptualisation gives geography an active rather than a passive role, as geography does not just mediate financialization but fundamentally constitutes what it is, where it is and how it collides with new spaces (Klinge et al., 2021; Harvey, 2006). Ultimately, we argue and empirically demonstrate that the where of financialization is as important to understand as the what of financialization.

The rest of this article is structured as follows. We start by providing a critical overview of the literature on financialization and pharmaceuticals, focussing on empirical and conceptual gaps. In the next section we outline the research design, data collection processes and our M&A-based approach to analysing financialization. We start our analysis by providing a global overview of pharmaceutical M&As. This is followed by analysis of the US market which reveals the contrasting positions of New York and San Francisco. We then analyse the growth of the Chinese market and the limited financialization of its firms. Conclusions are reached in the final section where it is argued that the financialization of pharmaceuticals is inherently variegated.

Moving from the what to the where of financialization

Financialization is commonly defined as the ‘increasing role of financial motives, financial markets, financial actors and financial institutions in the operation of the domestic and international economies’ (Epstein, 2005: 3). It reflects the transformative power of finance throughout contemporary capitalism but, similar to globalisation and neoliberalism, is constantly being reworked and redefined to match disciplinary contexts and empirical foci (Aalbers, 2015; Engelen, 2008). From a geographical perspective, financialization research can be placed into three categories; the macro analysis of a structural shift in capitalism towards a finance-driven regime of accumulation (Boyer, 2000), the meso analysis of corporate and firm-level financialization (French et al., 2011) and micro analysis concerned with the sociocultural impacts of the financialization of everyday life (Appleyard et al., 2016).

Most important to our analysis is research undertaken at the meso scale on corporate financialization, defined as the deepening interconnections between firms and financial intermediaries, institutions and markets (French et al., 2011). Research into corporate financialization has uncovered the rise of shareholder value generation (Van Treeck, 2009), downsize-and-distribute strategies (Lazonick and O’Sullivan, 2000), the rise of debt (French et al., 2011), short-term financial targets and metrics (Dodig et al., 2015) and assetization (Birch, 2017) in rendering a growing number of non-financial firms ‘increasingly beholden to the logic of finance’ (Hall, 2011: 3). These core constituents of corporate financialization (Keenan, 2020) have created novel forms of financialized competition, whereby firms compete in new ways to meet the demands of financial markets and institutions (Williams, 2000). This creates challenges and opportunities for firms and has resulted in the restructuring of business models, corporate governance structures, production networks and entire industries (Pike and Pollard, 2010). To name a few examples, empirical studies have revealed the role of financialization in the outsourcing and offshoring of manufacturing (Berghoff, 2016), the prioritisation of financial over physical investments in global retailing (Baud and Durand, 2012), the stretching and ‘distancing’ of agri-food chains (Clapp, 2014: 797), the concentration of production in global brewing (Keenan, 2020) and the uneven geography of investments in infrastructure (O’Brien and Pike, 2017).

These empirical insights demonstrate the variegation of financialization, whereby its processes unfold unevenly across spatial contexts (Brown et al., 2015). Political economic, institutional and cultural conditions present across all geographical scales have been shown to shape and mediate the forms and effects of financialization. While there are common and recognisable tendencies to financialization (Lapavitsas and Powell, 2013), made evident through its core constituents at firm-level (Keenan, 2020), geography necessarily intertwines with these tendencies and underpins how they manifest, unfold and evolve in novel ways (Pike and Pollard, 2010). Space and place are therefore central to processes of financialization, partly determining who is involved, the powers they have, and the intersecting challenges and opportunities they face (French et al., 2011).

Much of this research has been framed at the national scale, with studies exploring how some countries are more susceptible to financialization than others (Christophers, 2012). Highly neoliberalized countries such as the US and UK are said to facilitate greater forms of financialization through institutional frameworks promoting financial deregulation, shareholder primacy and short-term profit maximisation (Dixon, 2011). In contrast, more coordinated economies such as Germany and Japan place limits on financialization through patient capital and stakeholder modes of corporate governance (Peck and Theodore, 2007). More complex cases exist such as China, where rapid financial expansion combined with authoritarian state capitalism has resulted in financialization with ‘Chinese characteristics’ (Petry, 2020: 213). Cases such as China require further study, as they provide greater insights into the intersecting roles of public and private actors in managing what, where and how financialization unfolds as part of non-Western contexts (Pan et al., 2021).

While this research helps ground and contextualise the variegation of financialization, there are legitimate concerns around methodological nationalism. Framing analysis at the national scale leads to oversimplified and exaggerated accounts which fail to account for subnational variegation in institutional frameworks and heterogeneity in firm behaviour (Dixon, 2011; Peck and Theodore, 2007). To address these concerns, more finely grained and comparative studies are required to show how place-based conditions encourage or discourage financialized activities. As shown by Van Loon (2016) in his comparison of real estate development in the Netherlands and Belgium, financialization results in uneven qualitative transformations at firm-level even throughout the same industry and countries with relatively similar economic structures.

Several studies have outlined the role of financialization in the pharmaceutical industry in partly but not exclusively incentivising the outsourcing of production, R&D and clinical trials (Busfield, 2020), M&A activity (Danzon et al., 2007), and the prioritisation of shareholder value generation (Fernandez and Klinge, 2020). Central to explaining how and why these activities have become more prevalent is understanding the fundamental importance attached to patents, intellectual property rights (IPR) and the commodification of knowledge throughout the industry. In pharmaceuticals, the ability to generate value for shareholders and meet the expectations of financial markets is underpinned by the acquisition and monopolisation of IPR (Fernandez and Klinge, 2020).

Up until the early 2000s the biggest pharmaceuticals firms relied on a small range of ‘blockbuster drugs’ which were patent-protected and ensured huge profits in the medium-to long-term (Gleadle et al., 2014: 68). These drugs, protected by patents lasting at least 20 years, facilitated strong financial performance and returns to shareholders. However, recently, this model has come under intense pressure due to a gradual decline in the discovery of New Molecular Entities (NMEs). NMEs are the core chemical ingredient in pharmaceuticals products which, if proven by regulatory bodies to be novel, form the foundations of a new patented drug (Gleadle et al., 2014). It is believed that a slowdown in the discovery of NMEs is the result of an R&D crisis, whereby the rapid approval rates of patented drugs in the 70s and 80s have created modern day scarcities and significantly increased the R&D costs and time attributed to the confirmation of each new patent (Haakonsson et al., 2013; Rafols et al., 2014). Many of the biggest pharmaceutical firms are therefore facing patent cliffs (Kaitin, 2010), which threaten their most valuable revenue streams (Danzon et al., 2007).

With no immediate replacements of NMEs and with R&D increasingly viewed as a ‘financial gamble’, pharmaceuticals firms have had turned to M&As to maintain their patent pipelines and uphold expected levels of financial performance (Gleadle et al., 2014: 76). Heightened financial competition and lower patent approval rates have incentivised the use of M&As, with firms in possession of or even showing the potential to attain exclusive IPR deemed to be valuable ‘commodities on a marketplace’ (Fernandez and Klinge, 2020: 11). For example Pfizer, one of the most active firms in pharmaceutical M&As, acquired Warner-Lambert in 2000 to gain ownership of Lipitor, and Wyeth in 2009 to gain ownership of Prevnar. While M&As have always been part of the industry, recently many of the larger pharmaceutical firms have begun to target smaller biotech firms in their acquisitions (Gleadle et al., 2014). Biotech firms emerged in the 1970s specialising in biologics and the development biologically-as opposed to chemically-based drugs (Busfield, 2020). Pharmaceutical firms are becoming increasingly dependent on these smaller and innovative firms, whose R&D is often publicly funded, to develop new patented drugs (Gleadle et al., 2014). This has created uneven power geometries throughout the industry, as publicly funded research is increasingly being captured and monopolised by the larger private firms through M&A activity (Fernandez and Klinge, 2020).

More recently, and partly attributed to M&A activity, NME approval rates have risen (Ma et al., 2013). Due to the fragmented nature of pharmaceutical innovation, whereby patented drugs are made up of several compounds from numerous firms, M&As have supported this process by merging smaller firms together and supporting them with technological, regulatory and business expertise (Ascher et al., 2020). While M&A activity will have contributed to this uplift in approval rates, improvements in the regulatory review process have also played a key role (Ma et al., 2013). The Covid-19 pandemic raised critical questions around drug development and coordination, supporting faster approval processes through a reduction in bureaucracy (Mullard, 2020). Ultimately, the financial logic instilled by financialization have firmly established M&As as centrally important to the long-term development of pharmaceutical firms (Fernandez and Klinge, 2020). They have become the key mechanism for appropriating value as part of the assetization of IPR throughout the industry (Birch, 2020).

Importantly, financialization does not provide a universal explanation for growing M&A activity in the pharmaceutical industry. While financialization has increased the incentives for M&As, the motivations behind them are inevitably complex and contingent (Green, 2018). M&As are not purely about financial performance, as they allow firms to respond to new regulatory frameworks, adapt to changing labour market conditions, grow their market share and access new technology, knowledge and skills (Rompotis, 2015). M&A motivations can be broadly classified as market-, efficiency- and technology-seeking (Motis 2007). Market-seeking deals occur when firms attempt to access new markets, efficiency-seeking when cost savings are the primary motivation, and technology-seeking when new assets are required to enhance production, innovation and research and development (Lee, 2017).

These distinctions raise questions concerning the causality of financialization in terms of wider transformations witnessed throughout the industry. Financialization may increase cost reductions, outsourcing, and the monopolisation of IPR (Busfield, 2020; Danzon et al., 2007; Fernandez and Klinge, 2020; Gleadle et al., 2014) but it is not the only or in some cases even the principal driver of these transformations. Just like M&As, pharmaceutical firms may restructure their activities for other strategic reasons aside from financial performance and shareholder value. As suggested elsewhere, caution must therefore be exercised when using financialization to explain economic transformations, with our analysing remaining sensitive to the multiple and intersecting factors which encourage and discourage financialized activities (Krippner, 2011).

While research has shed light on the financialization of pharmaceuticals, significant gaps remain. The focus of most research has been towards understanding the what and when of financialization, as opposed to the where. Aspatial studies mean that we know very little about the uneven geographies of pharmaceuticals financialization and the role of different regulatory frameworks and patent regimes in shaping firm behaviour. In terms of M&As, while there is broad consensus that acquisitions have increased in value and volume, there is little knowledge of where the acquirers are, where the targets are and what this geography means for how, when, where and why life-saving and other drugs are, or more importantly are not, being produced and consumed. Relatedly, we know little about the concentration of corporate control in the global pharmaceuticals industry and how the relational geographies between different centres of pharmaceutical activity evolved over time.

These empirical gaps relate to conceptual deficiencies in our understanding of financialization. A longstanding critique of financialization studies is that they remain ‘insufficiently attentive to space and place’ (French et al., 2011: 800). While research has begun to address this criticism by exploring the variegation of financialization, an understanding of the causal and constitutive role of geography remains underdeveloped (Pike and Pollard, 2010). There has been limited focus on causality, with the majority of studies less reflective on the ‘spatial organisation and geographical embeddedness’ of actors which not only modifies financialized activities but fundamentally constitutes their nature, magnitude and intensity (Klinge et al., 2021: 2). There is also an implicit focus towards exploring where financialization occurs rather than exploring where it does not occur, and why (Van Loon, 2016). This bias leads to uncritical accounts which fail to recognise spatial and temporal contingency (Christophers, 2015; O’Brien and Pike, 2017). Research must therefore prioritise the relational and multiscalar forms and effects of financialization which unfold unevenly and are shaped by an intersecting dialectic between space, place and social agency (Keenan, 2020).

Analysing the financialization of pharmaceuticals through M&A data presents an opportunity to address these empirical and conceptual gaps. Answering the call for a ‘spatial turn in corporate financialization’, the inherent relationality of M&As allows us to accommodate a shift in thinking from ‘abstract space to relational space’ (Klinge et al., 2021: 15; Harvey, 2006). M&As reflect the ‘inescapable geographic construction, context, and rootedness’ of financial activities, allowing us to show how geography actively shapes the what, when and where of financialization (Pike and Pollard, 2010: 38). Moreover, the relational connections forged by M&As allow us to interrogate the footprint of financialization, with corporate control concentrating in some cities and not others.

Researching the financialization of pharmaceuticals through M&A data

We analyse all domestic and cross-border M&A deals valued at or above US$10m involving pharmaceutical firms on either or both sides of the transaction between 2001–2020. Our sample of 1805 deals were collected from Zephyr, a world leading source of M&A data, before a long and rigorous process of geocoding took place which identified the headquarter address for every firm included in the database. This meant that for each deal we have geographical data on the acquirer and target firm down to the city-level, allowing the analysis of trends and patterns in deals over time and space. Our definition of the pharmaceutical industry, based on the North American Industry Classification System (NAICS), includes all firms from NAICS codes 3254 ‘Pharmaceutical and Medicine Manufacturing’ and 541714 ‘Research and Development in Biotechnology’ (see Appendix 1). This definition is necessarily broad to comprehensively cover the entire industry, but we do not suggest that each subindustry experiences financialization in the say way.

We build on a ‘narrative and numbers’ approach to analysing the financialization of pharmaceuticals (Froud et al., 2006: 122). Thus our quantitative analysis of the numbers and values of M&As is combined with the qualitative analysis of the narrative of M&As interrogated through company accounts, market analysis and industry reports. While this helps to triangulate and contextualise our findings, the industry narratives of pharmaceutical M&As are analysed with circumspection. This is because disparities exist between the prospect and reality of M&As in relation to financial performance (Trujillo et al., 2020). M&A announcements may provide short-term financial rewards through increasing share price valuations but do not always deliver in the long-term (Demirbag et al., 2007). We therefore do not suggest that all M&As are universally successful nor that they inevitably deliver in terms of the core constituents of financialization.

Central to our approach is also acknowledging the variegation of capitalism and understanding firms as ‘social institutions’, shaped but not inevitably defined by the political economic conditions in which they are embedded (Peck and Theodore, 2007: 738). This definition fits our multiscalar approach to analysing M&A deals, as we start by addressing the global scale before analysing national- and city-level trends. The global scope of our data and analysis helps address a persistent criticism that most quantitative studies on corporate financialization focus on a small number of advanced and western economies (Klinge et al., 2021). This limited spatial focus has underpinned the inaccurate conceptualisations of financialization as a ‘universal process, which articulates itself similarly in different institutional contexts’ which our analysis aims to critique (Engelen, 2008: 114).

Throughout the article we analyse both the number and value of M&A deals. As we will demonstrate, these two measures tell contrasting stories. While we acknowledge that increased M&A activity is a signifier of financialization (Fernandez and Klinge, 2020), we aim to provide more nuance in our analysis through recognising that a deal worth $10m is very different to a deal worth $10bn. Considering this important distinction we focus more on deal values than volumes. While analysing the number of deals helps identify geographical patterns, analysing value fits better with our focus on financialization, as higher deal values are more likely to reflect the underlying tenets of financialization based on shareholder value, market capitalisation and the concentration of corporate control and decision-making power as part of global production and financial networks.

We believe that the number and value of M&A activity provides a useful proxy for measuring the extent of financialization throughout the pharmaceutical industry. Corporate financialization research has drawn from several indicators for analysis. While Froud et al. (2006) draw from perhaps the most comprehensive mixture of qualitative and quantitative data, other studies have drawn from various firm-level financial indicators to explore its forms and effects. To name a few, this has included the share of financial assets to total assets (Baud and Durand, 2012), the share of debt to equity and capital (Fernandez and Hendrikse, 2020), net debt (Yrigoy, 2016), dividends (De los Reyes, 2017) and returns on revenue, assets and equity (Baranes, 2017). M&As remain a novel and understudied indicator in the analysis of financialization. While including a wider range of firm-level indicators could have enriched our analysis, this would have limited our global focus and reduced the size of our sample. Accepting that M&As are by no means the perfect indicator, they allow us to create a global, comprehensive and novel picture of pharmaceuticals financialization, with their inherently geographical and transactional nature central to developing a relational conceptualisation of financialization.

The global market for pharmaceutical M&As

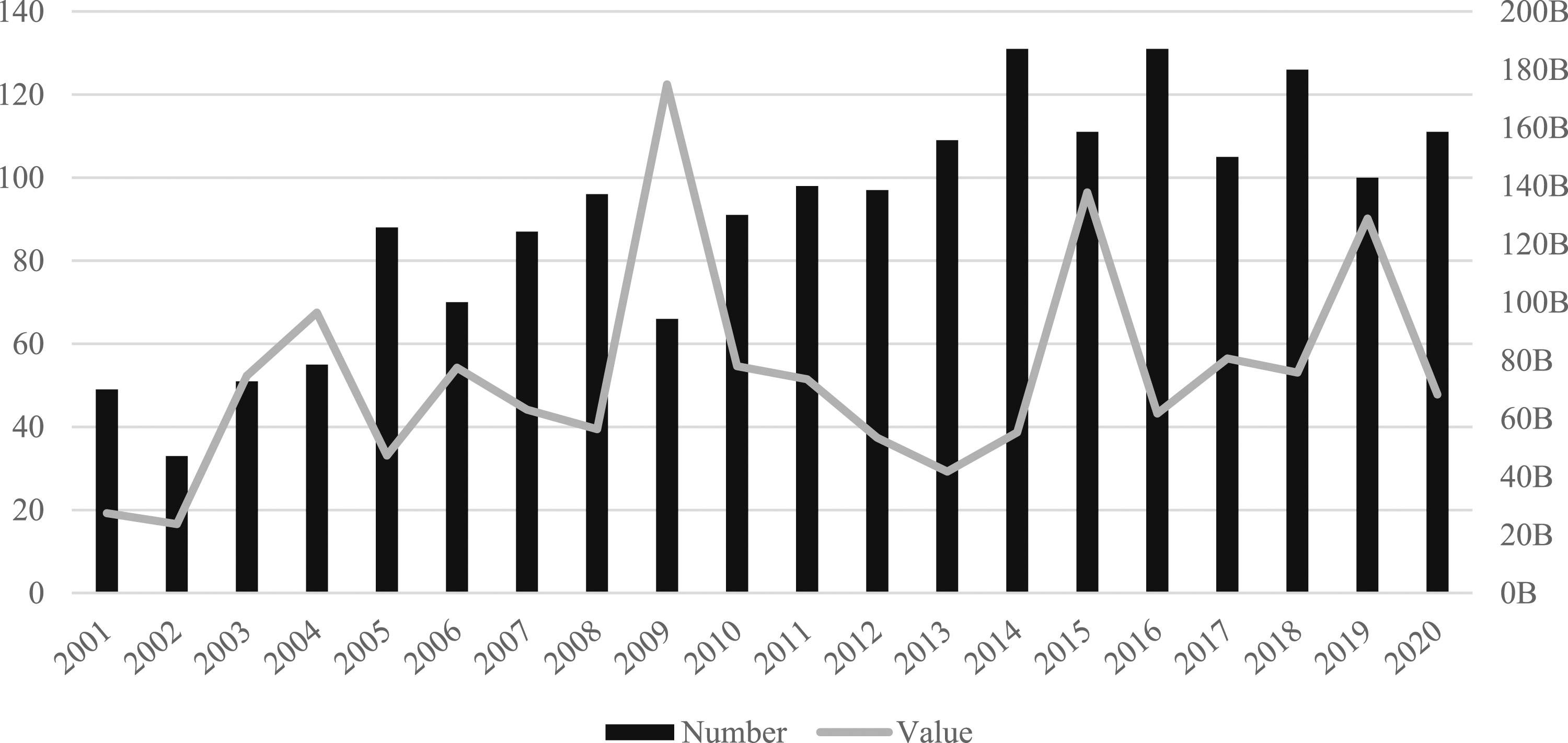

Much has been made about the rise in the number and value of M&As throughout the global pharmaceutical industry. We unravel this M&A activity across geographical scales, moving from the global to the national- and city-level. Figure 1 starts by documenting the total number and value of pharmaceuticals M&As between 2001–2020. It shows a consistent growth in the number of deals, which more than double from 49 in 2001 to 111 in 2020, accompanied by a much more turbulent evolution in the value of deals. Greater fluctuations in deal value can be attributed to large one-off deals. For example, in 2009 Pfizer acquired Wyeth for $68bn and in 2019 Bristol-Myers Squibb acquired Celgene Corporation for $74bn. Number and value (US$bn) of all deals (2001–2020).

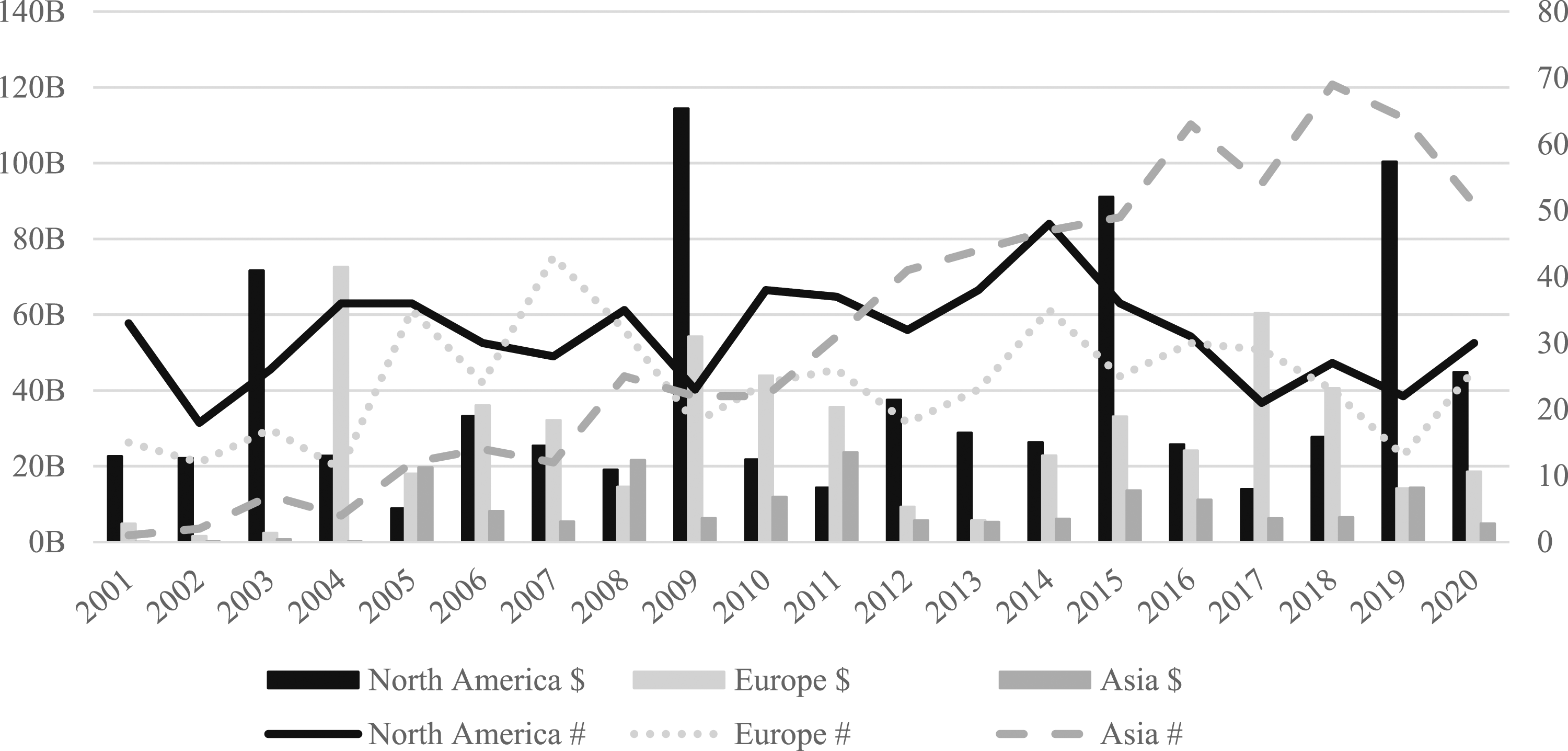

Behind this global picture lies a complex and uneven geography. Throughout the 20-year period, 99% of deal value and 97% of deal volume is located in Asia (11% of value and 35% of volume), Europe (36% and 27%) and North America (52% and 35%). This highlights the paucity of pharmaceuticals M&A activity in Africa, Oceania and South America. With this in mind, Figure 2 highlights the evolution of deal value and volume in Asia, Europe and North America. Number and value (US$bn) of deals in Asia, Europe and North America (2001–2020).

Over time, the most notable trend is the growth of Asia as it moves from 2% of deal volume in 2001 to 48% in 2020. However, this is not matched by value, as annual deal value in Asia rarely exceeded $10bn. This is likely the result of lower firm valuations due to the historical size and strength of pharmaceuticals in western countries and relative differences in technology, R&D investments and patent regulations. While deal value is considerably higher in Europe and even more so in North America, neither of these regions experienced a similar rise in volume over time. Importantly, and as discussed in the methods section, these trends highlight clear differences in the value and volume of pharmaceutical M&A deals.

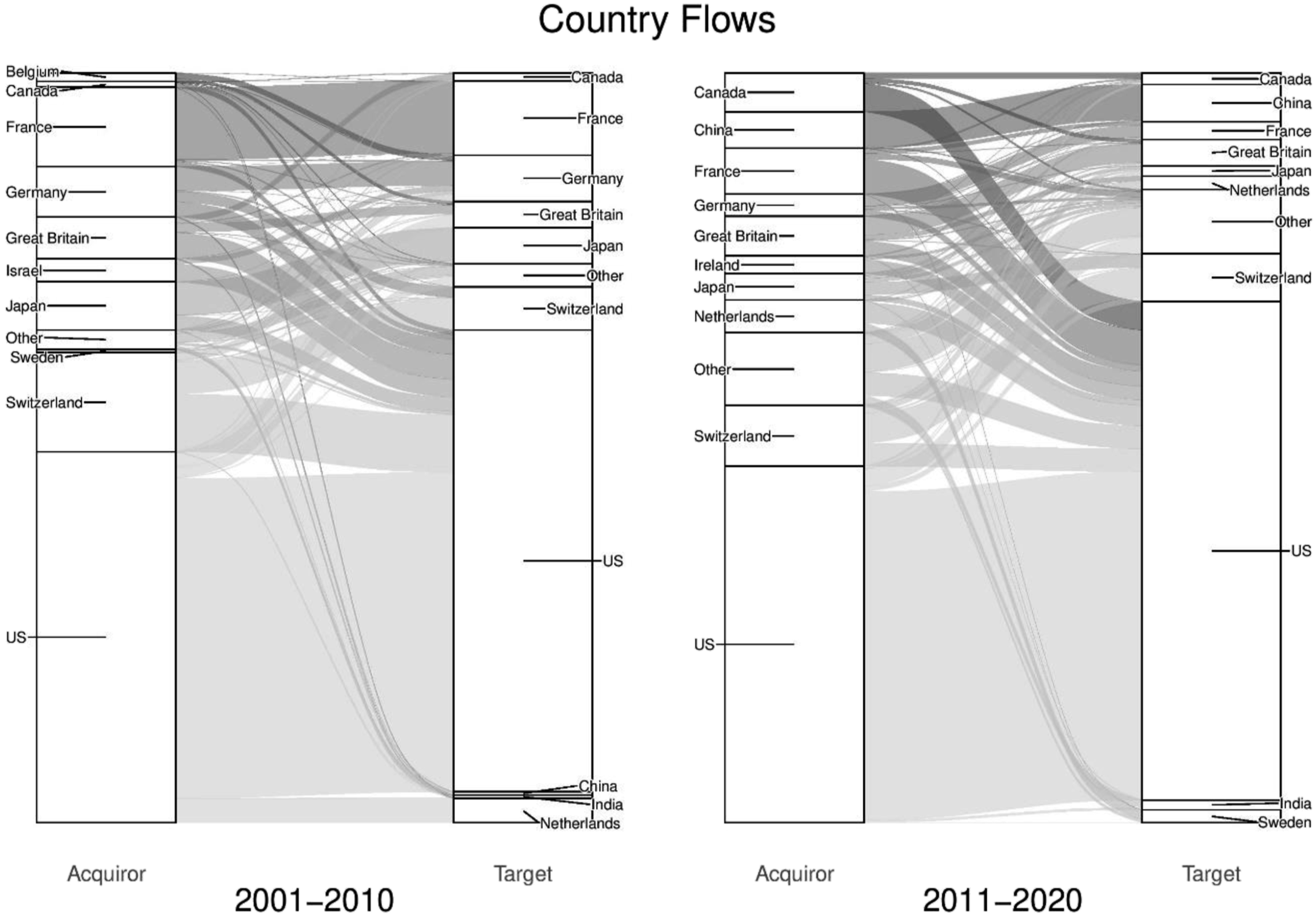

Homing in further on this global picture, Figure 3 highlights the most significant country-level trends. Based on deal value, it reveals the top 10 acquirer and target countries (left to right) and how these positions have changed over time (left panel to right panel). The value (US$bn) of all deals at country-level (01–10 and 11–20).

In the first decade, the US made up 50% of all acquisition and 62% of target value. European countries in the top 10 accounted for 38% of acquisition value, with Switzerland (13%), France (11%) and Germany (7%) all in the top five acquirers. Asian countries are represented through Japan (6%) and Israel (3%) among the top acquirers, with India (less than 1%) and China (less than 1%) among the top targets. In the second period, the US share of acquisition value declined slightly (48%) but target value increased (67%). Switzerland remained the second largest acquirer which can be attributed to its unique political and economic position in Europe, in addition to its world class R&D functions which have supported the development of a dynamic pharmaceutical industry (Gautam and Pan, 2016). The largest risers in terms of acquisition value are Canada and China, both of which increased their shares from less than 1% to 5%, although the vast majority of Chinese activity is domestic.

In overview, Figure 3 reveals several characteristics of the global geography of pharmaceutical M&As. First, it highlights the size and strength of the US as the world’s largest market for pharmaceutical M&A value. The scale at which the US leads as the world’s largest target is striking, showing the extent to which firms from other countries are attracted to the US market due largely to the quality and quantity of innovation and R&D, as well as opportunities for profit through unregulated drug prices (Tulum and Lazonick, 2018). Second, and as many of the acquisitions of US firms come from European firms, Figure 3 also highlights the strength of European countries engaging in cross-border activity. This is no surprise given the historical size of pharmaceuticals markets and level of R&D investments across Europe. At present five of the top 10 largest pharmaceutical markets are in Europe and specifically Germany, France, Italy, the UK and Spain (IQVIA, 2020). Third, India appears as a special case as the only country among the top targets in both periods without ever being a top acquirer. The rise of India as an international target can be attributed to financialization, as pharmaceutical firms from developed countries are increasingly outsourcing R&D functions and clinical trials to India as a cost-cutting mechanism (Rafols et al., 2014). Finally, Figure 3 highlights the domestic orientation of many of the largest acquirers and targets. Across all deals and over both decades, domestic deals accounted for 63% of value and international for 37%. Acknowledging the contingent nature of M&As, this probably reflects the uneven national regulatory landscapes for healthcare and drug manufacturing, as well as growing incentives for national governments to protect the autonomy of their domestic pharmaceutical functions in the wake of the Covid-19 pandemic.

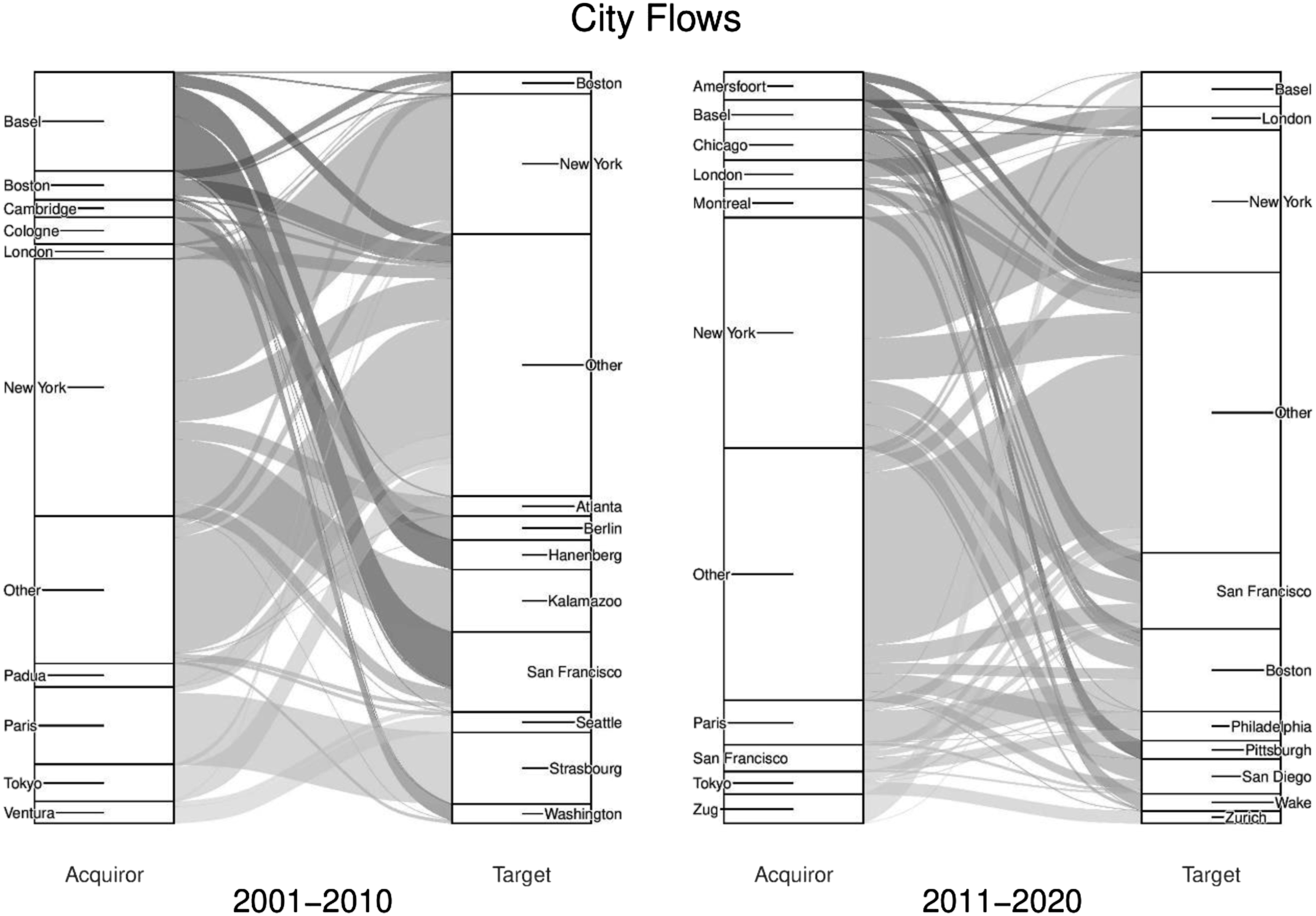

Building on country-level analysis, Figure 4 reveals the top 10 acquirer and target cities (left to right) and how these positions have changed over time (left panel to right panel). Based on deal value, it underscores the concentration of activity across US and European cities. In the first decade, New York is the top acquirer and target, with 34% of acquisition and 19% of target value. Basel is the largest European acquirer, with 13% of all acquisition value, driven by Roche – the world’s second largest firm by market cap – and Novartis – the fifth largest (Deshmukh, 2021). US cities in the top 10 make up 41% of acquisition and 49% of target value, with European cities accounting for 35% of acquisitions and 17% of targets. Tokyo is the only Asian city to feature with 5% of acquisition value and this reflects the relative strength of Japanese firms in terms of generating high revenues from the sale of generic drugs while also investing heavily in R&D to support new drug discoveries (Umali, 2010). The value (US$bn) of all deals at city-level (01–10 and 11–20).

In the second decade, New York remained the largest acquirer (31%) and target (19%). Paris (6%) replaced Basel (4%) as the second largest acquirer, although Switzerland grew its presence with Zug (4%) entering the top acquirers and Zurich (2%) the top targets. US cities were still the most attractive targets, with Boston (11%), San Francisco (10%) and San Diego (5%) making up the rest of the top four alongside New York. Importantly, we see growth in the Other category, moving from 19% to 34% of acquisition value and 35% to 37% of target value, suggesting that concentration in the market for corporate control is decreasing at the city-level.

Overall, while there are changes, Figures 3 and 4 paint a picture of inertia in the distribution of pharmaceutical M&As, with no seismic shifts in the geography of acquirers and targets over two decades. We see a core group of dominant North American and European cities alongside very limited activity throughout Asia. While analysing deal volumes would have revealed a more dynamic picture, particularly a rise of China, this relatively stable geography of deal value highlights the concentration of corporate control and a high degree of spatial stickiness in decision-making throughout the global pharmaceutical industry.

US pharmaceuticals and the search for biotech

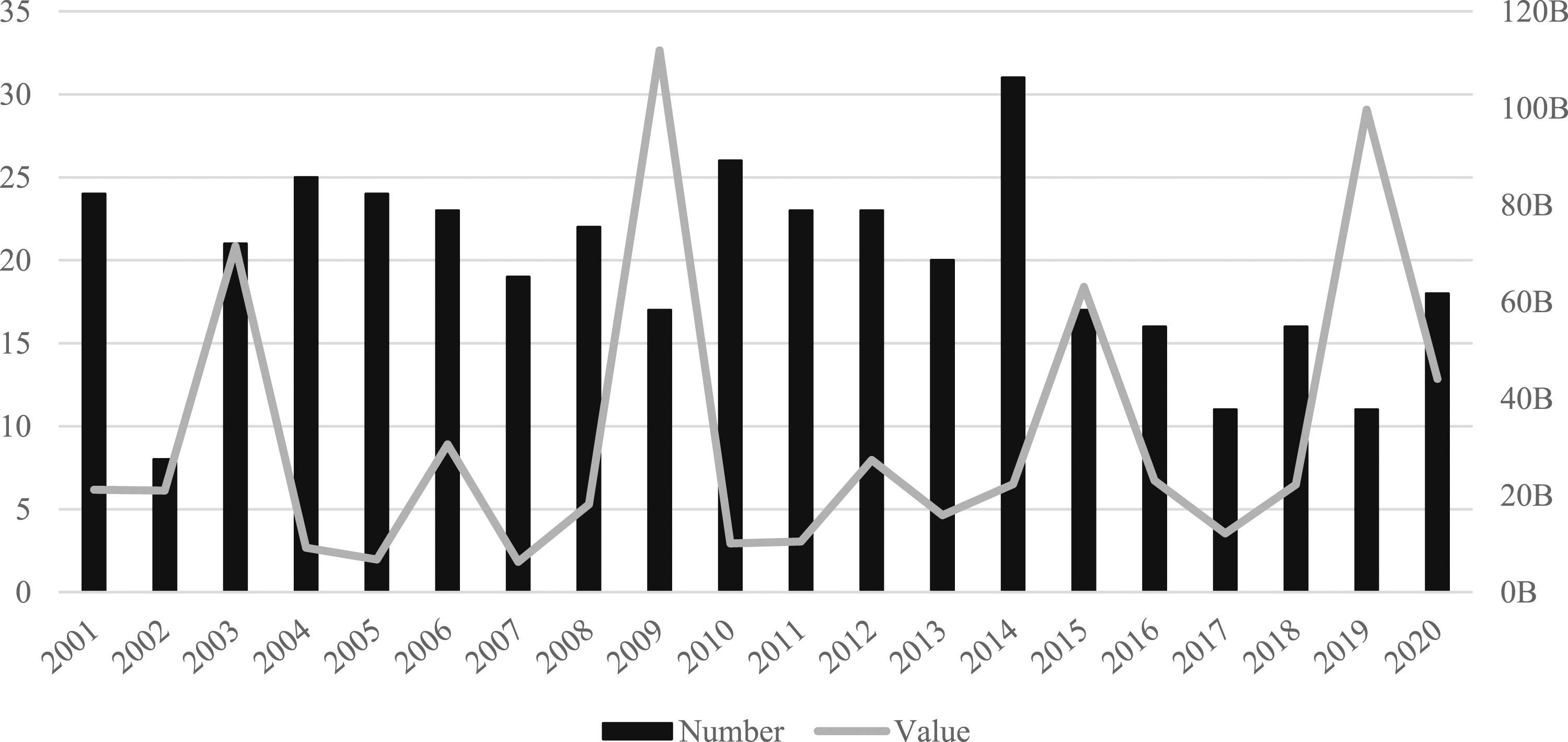

The US is the world’s largest pharmaceutical market with sales over $533bn in 2020 (IQVIA, 2020). In terms of M&As, the US is the largest market by value and the second largest by volume. Over the last two decades US firms engaged in 395 domestic deals (35%) worth $647bn (69%) and 119 (17%) international acquisitions worth $78bn (14%). Importantly, US firms were also the most popular international target, making up 196 (29%) deals worth $313bn (57%). Based on value, the leading US firms were Pfizer with $185bn worth of acquisitions, followed by Bristol-Meyers Squibb ($110bn), Schering-Plough ($54bn), Johnson & Johnson ($40bn) and Amgen ($35bn). Showing domestic deals only, Figure 5 reveals the size of the US market by value and volume. Interestingly, there are no obvious trends over time, with the market sustaining a high level of value and volume across the entire period. Number and value (US$bn) of domestic deals in the US (2001–2020).

Equally important to understanding why M&A activity increases under financialization is understanding how the conditions for financialization emerge in the first place. Driven by shareholder value orientation, the monopolisation of IPR and competition through M&As, the US pharmaceuticals industry is viewed as the archetype of financialization (Tulum and Lazonick, 2018). While the emergence of contemporary financialization more generally is often tied to the US and neoliberal reforms implemented by the Reagan administration in the 1980s (Engelen, 2008), the financialization of US pharmaceuticals can be explained through the particularities of its institutional and regulatory environment which provide “unique advantages” for the production and sale of drugs (Tulum and Lazonick, 2018: 282). There are four key features of this institutional environment which support the financialization process.

First, and most important, is the patent regime. Patents are what allow pharmaceutical firms to monopolise new knowledge, generate rent incomes and provide value for shareholders (Fernandez and Klinge, 2020). The first ever US drug patent was registered in 1796 by Samuel Lee Jr for bilious medication (Young, 1960) and since then US institutions have been at the centre of strengthening pharmaceutical patents both at home and abroad (Townsend et al., 2018). Proponents argue that patents spur investment and drive innovation through ensuring long-term profits which cover the high costs attributed to developing new drugs, whereas critics argue that they lead to the production of a narrower range of drugs with higher opportunities for profit and limit access to medication throughout developing countries (Feldman et al., 2021). Handled by the Food and Drug Administration (FDA), pharmaceutical patents in the US grant exclusivity rights to new drugs for up to 20 years, with the option for ‘evergreening’ strategies enabling firms to extend patent exclusivity following modifications to the drug (Townsend et al., 2018: 90). Perhaps most importantly, the US is currently the world’s leading country for the protection of patents and IPR (US Chamber of Commerce, 2021).

Second is the quantity and quality of R&D, underpinning the discovery of new patented drugs. The US has some of the best conditions in the world for pharmaceutical R&D, with access to world class talent, investment capital and a diverse range of private and public research institutions (Tulum and Lazonick, 2018). The US government has played a significant role in cultivating these conditions and actively supporting the private appropriation of public knowledge. In 1986 and as part of the Federal Technology Transfer Act, the Reagan Administration implemented the Cooperate Research and Development Agreement (CRDA), which incentivised collaboration between public and private research enterprises by allowing private firms to easily acquire and monetise new ideas and technology made through collaboration with public bodies (Tulum and Lazonick, 2018). This paved the way for private pharmaceutical firms to patent drug discoveries made in partnership with public agencies. In addition, the US government also supports pharmaceutical R&D through the National Institutes of Health (NIH), a research agency founded in 1887 which provides over $30bn worth of public funding each year to support health-based research and medical innovations (NIH, 2021).

Third is the financial environment. The nature of pharmaceutical and biotech innovation is invariably risky, meaning that investors and financial institutions must match this appetite and exposure to risk. The financialized nature of the US economy and the prevalence of venture and risk capital provides suitable conditions for start-up firms to finance innovations. Considering European countries such as Germany, which on the whole represent risk-aversive investment communities, there are financial incentives for pharmaceutical and biotech start-ups to move their operations to the US, particularly at earlier stages of development.

Finally, the US is the only advanced economy which does not regulate the price of pharmaceutical drugs, resulting in US drug prices being the highest in the world. A study comparing US drug prices with 32 other OECD countries found that on average drugs in the US are over 2.5 times more expensive (Mulcahy et al., 2021). This substantial difference in price means that pharmaceutical firms can be much more profitable in the US than in other countries, providing an explanation as to why the US is the highest target in international M&As. The scale of this difference, and the opportunities for profit, are made evident when comparing sales revenue across countries, with the US market worth $533bn in 2020 and the combined sales revenue of the 9 other countries in the top 10 worth $629bn (IQVIA, 2020).

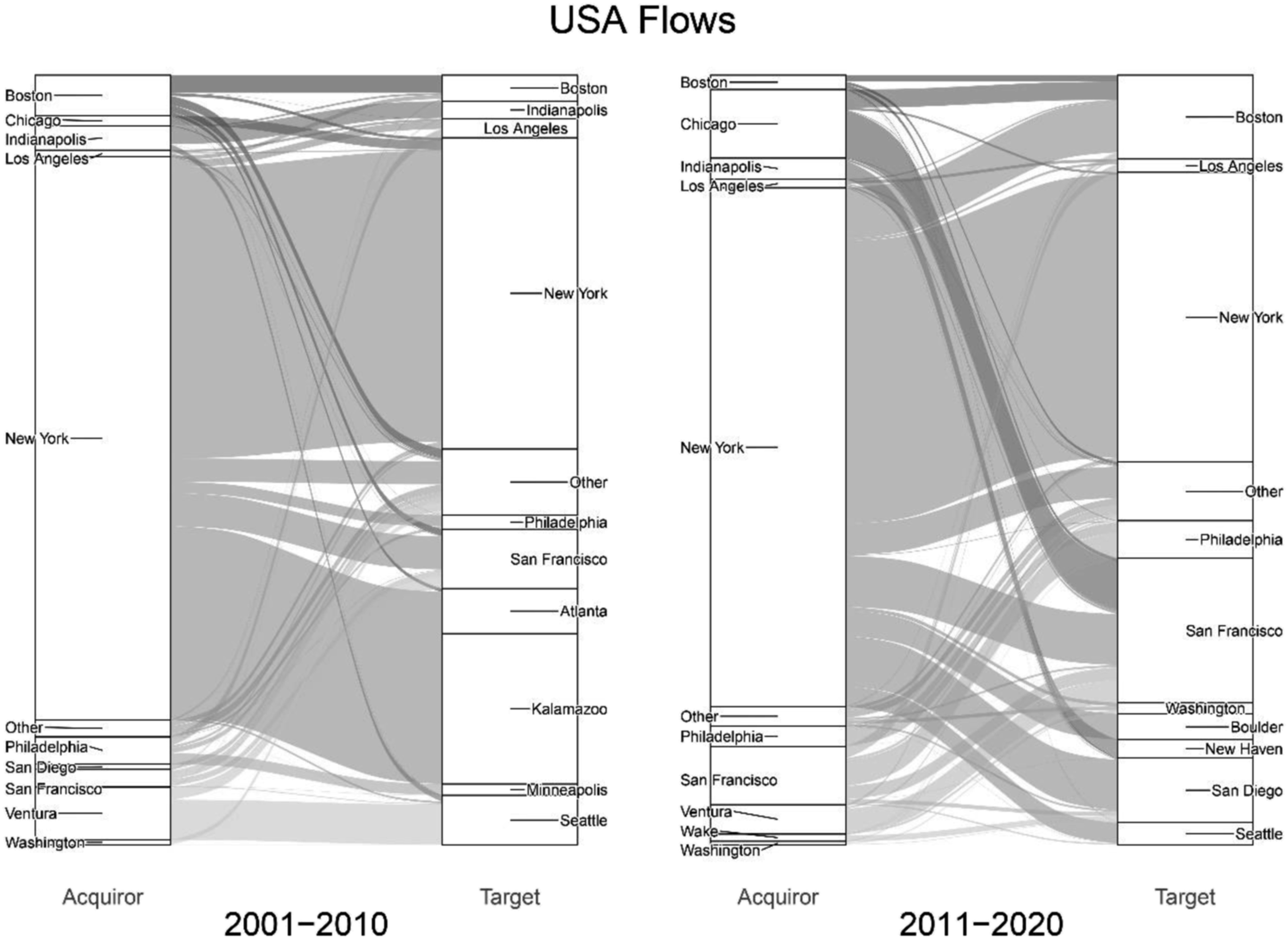

This institutional environment has not only facilitated but actively incentivised and accelerated the financialization of pharmaceuticals. While these conditions allowed some pharmaceutical firms to grow and provide enormous value for shareholders, the model has recently come under pressure due to declining patent approval rates, patent expiration cliffs and an R&D productivity crisis (Gleadle et al., 2014). This has increased the number and value of M&As, resulting in an uneven geography of acquirers and targets. Focussing exclusively on domestic deals, Figure 6 shows the top 10 acquirer and target cities in the US (left to right) by value and how these positions have changed over time (left panel to right panel). The value (US$bn) of domestic deals in the US (01–10 and 11–20).

Figure 6 underscores the leading position of New York, with 73% of acquisition and 39% of target value in the first decade. However, the position New York weakens over time, particularly in terms of acquisitions with its share of value falling to 67% in the second decade. Notable is growth in Chicago, which increased its share of acquisition value from 1% to 9% mainly through AbbVie’s $21bn acquisition of Pharmacyclics. Perhaps even more important is the rise of San Francisco, which grew its share of acquisition value from 2% to 8% and target value from 8% to 19%.

San Francisco is an important example demonstrating the growing reliance on biotech acquisitions by US pharmaceutical firms (Fernandez and Klinge, 2020). Described as the ‘birthplace of biotechnology’, San Francisco is the largest biotech hub in the world with over 200 firms and close links to leading universities and R&D institutions (City of South San Francisco, 2021). Biotech firms in San Francisco have become some of the most sought-after targets in the world, as firms faced with patent expiration cliffs are actively seeking biotech acquisitions to bolster R&D productivity (Gleadle et al., 2014). The concentration of corporate control in New York over the last two decades has played into this and created an unbalanced market structure whereby firms in New York depend on M&As to compete, grow and maintain certain standards of financial performance. On the other hand, cities which do not house any of the world’s largest pharmaceutical firms or have close links to leading financial institutions depend on smaller innovative firms to develop new technologies and discover new patent opportunities before eventually being targeted as an exit strategy (Danzon et al., 2007). Importantly, this process is not limited to San Francisco, as growth in Boston, San Diego and Seattle has created a landscape of biotech competition (Blankenship, 2021).

Financialization and high levels of M&A activity are therefore compounding divisions of labour and economic specialization in the research, production, and distribution of US pharmaceuticals. While larger firms in New York with access to world class financial support are growing through strategic acquisitions and consolidating corporate control, smaller firms in San Francisco and other parts of the country are growing through innovation and publicly funded research before being enrolled into this M&A-based form of competition. Importantly, this spatial variegation and the emerging competitive landscape at the city-level has been shaped by the wider national institutional environment, demonstrating the geographically uneven causes and effects of financialization.

Chinese pharmaceuticals and the awakening of a sleeping giant

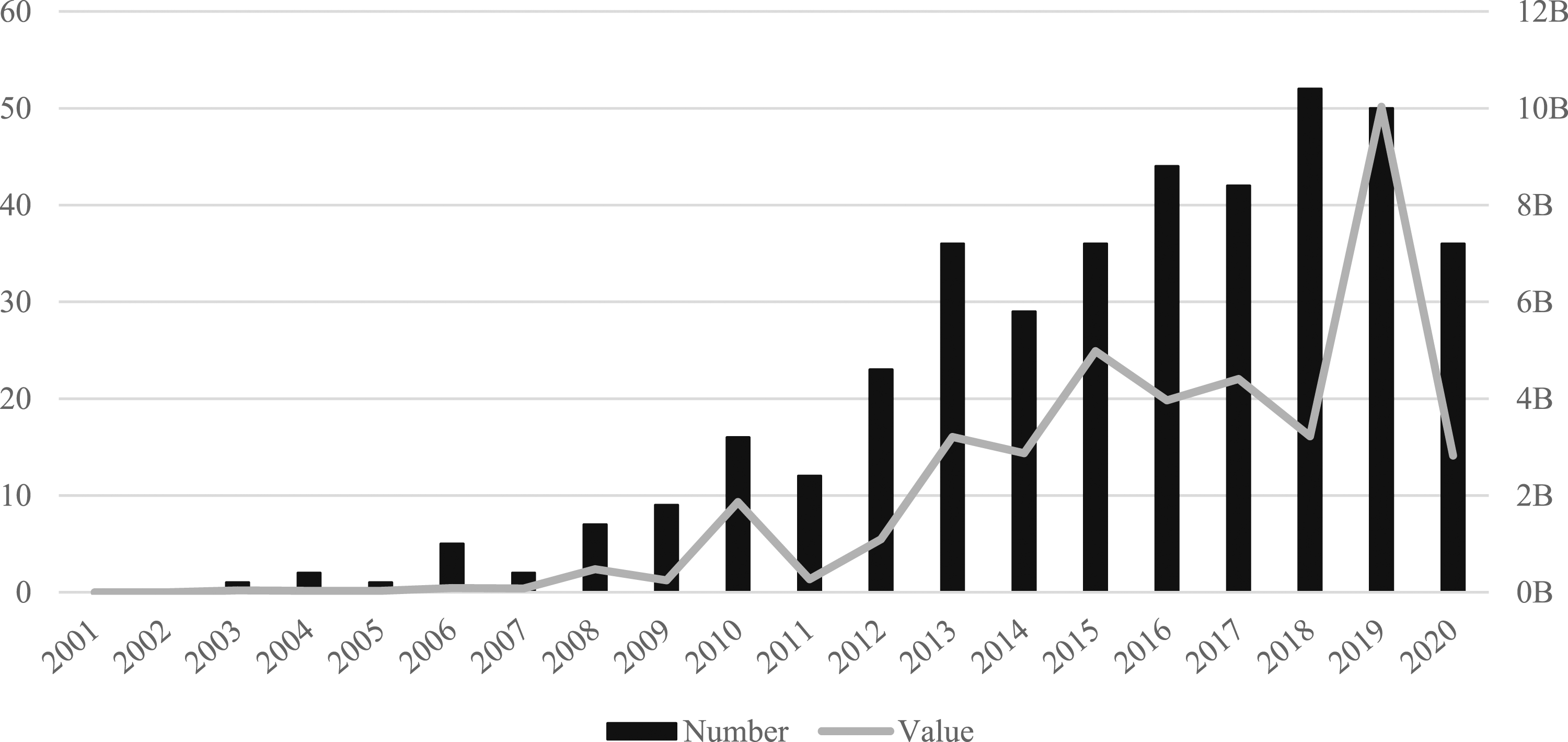

China has the second largest pharmaceuticals market in the world, with annual sales worth $93bn in 2020 (IQVIA, 2020). Huge growth in recent years can be attributed to the role of the Chinese government in reforming pharmaceutical legislation, widening access to healthcare insurance and rapidly developing the country’s hospital and primary care infrastructure (Daxue, 2021). While these efforts have increased the demand for pharmaceutical products, the pharmaceutical industry remains highly fragmented, especially in comparison to advanced economies (Barbieri et al., 2017). As shown by Figure 7, this fragmented industry has experienced a significant rise in both the number and value of pharmaceutical M&As. As the largest domestic market by volume and the fourth largest market by value, Chinese firms engaged in 403 domestic deals (36%) worth $40bn (4%). With very few deals between 2001–2007, M&A activity began to rise rapidly in 2008 and continued in an upward trajectory until reaching a peak in volume of 52 deals in 2018 and value of $10bn in 2019. Number and value (US$bn) of domestic deals in China (2001–2020).

The most distinctive attributes of the Chinese pharmaceutical M&A market are its relatively lower valuations and overwhelmingly domestic orientation. Both attributes are partly the result of China’s patent regime. Over 97% of drugs sold by Chinese firms in the domestic market are generic and have no IP rights (Chen et al., 2018; Daxue, 2021). The pharmaceutical patenting process in China has been described as unclear, overboard, and lengthy, with the Chinese government enforcing strong regulations on foreign entrants and imports (Chen et al., 2018). All domestic and foreign products are subject to approval from China’s National Medical Products Administration, a regulatory body which approved only 100 new drugs between 2001 and 2016 (New York Times, 2018). In comparison, the US FDA approved 438 new drugs during the same period (Food and Drug Administration, 2021). While new regulations are being introduced to speed up the approval process (Han et al., 2021), China’s historically low levels of drug approvals are the result of it not recognising foreign clinical trials and international testing certifications, as well as forcing all imported products to align with its own specific manufacturing standards (Wu and Hsu, 2018). These conditions have encouraged the production of easily replicable generic drugs by domestic firms and deterred foreign entry into the market as opportunities for profit are limited by the time, risks and costs attached to monetising patents (Zhong and Ouyang, 2020).

In this sense, China’s patent regime exists as an ‘implicit non-tariff trade barrier’, which provides a form of institutional protectionism that has reduced the outright ownership of Chinese pharmaceutical firms by foreign competitors (Wu and Hsu, 2018: 753). Combined with much lower levels of R&D investment which has hindered the pace and sophistication of pharmaceutical innovation (Chen et al., 2018; Zhong and Ouyang, 2020), Chinese firms have traditionally lacked the capacity to acquire foreign firms and are themselves often perceived to be unattractive targets. This is evidenced by the fact that despite being the second largest pharmaceuticals market by sales revenue (IQVIA, 2020), over the last two decades Chinese firms made only and 11 (2%) international acquisitions worth $1bn (less than 1%) and were only targeted by foreign competitors 21 times (3%) worth $2bn (less than 1%). While there have been different types of international collaboration and joint shareholding (Wu and Hsu, 2018), these conditions have essentially sealed off the market and prevented the spread of financialized restructuring through foreign ownership. With unique shareholder arrangements, made evident by the large presence of state-owned shares in all listed companies (Wang, 2010), pharmaceutical firms have typically remained smaller and private entities which are shielded from the expectations of institutional investors and international financial markets. For example, China’s most valuable pharmaceutical firm by market capitalisation – Jiangsu Hengrui Medicine – is positioned 20th in global rankings, in stark contrast to US pharmaceutical firms, which account for approximately 45% of global market capitalisation and make up 6 out of the top 10 firms (Deshmukh, 2021).

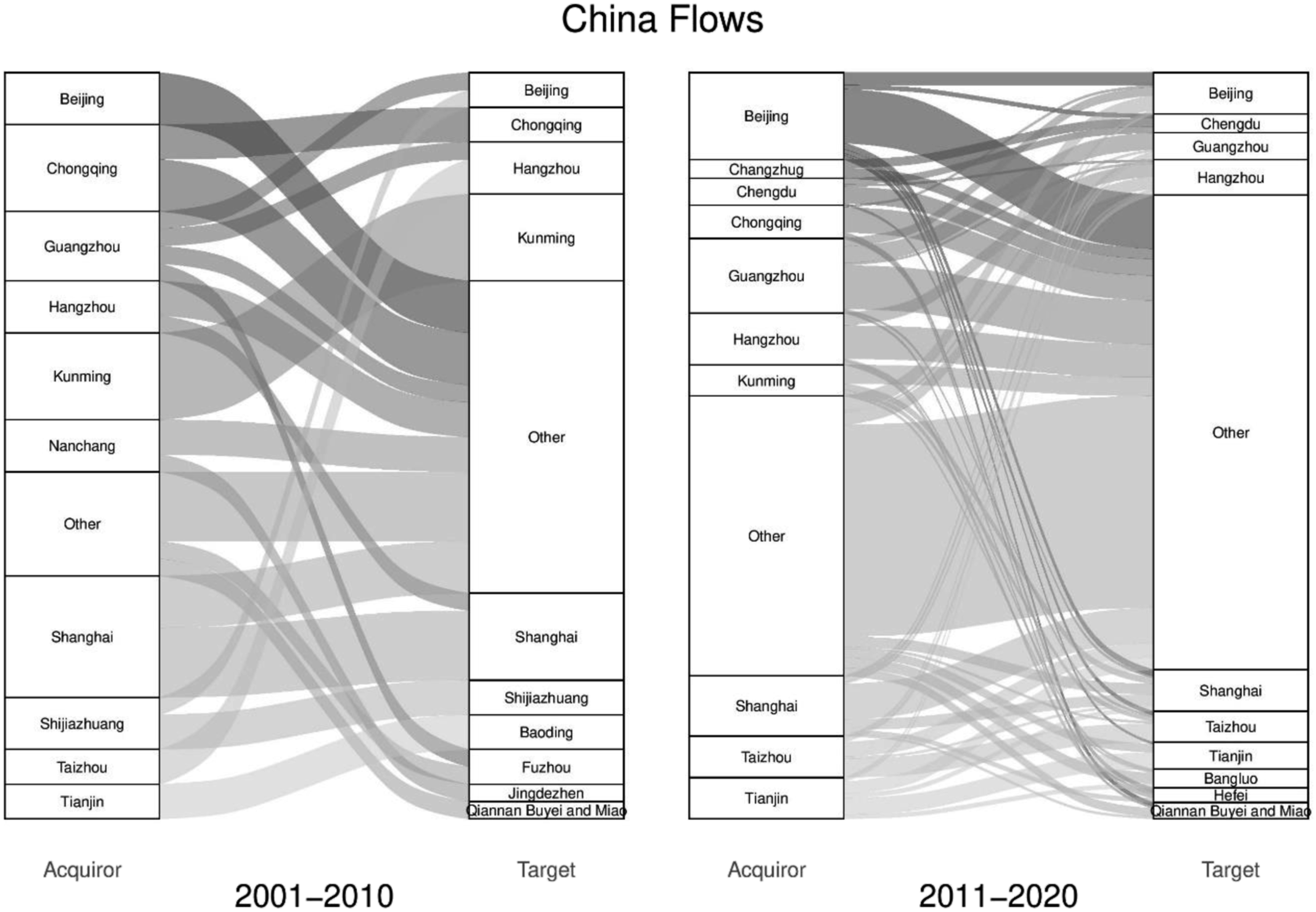

While international activity has been limited, Figure 7 does however reveal a huge rise in the number of domestic M&As. With over 5000 pharmaceutical firms, many of which are small to medium sized, the Chinese government has actively encouraged consolidation through M&A activity (Daxue, 2021). Identified as a priority industry in China’s 13th Five-Year Plan of Strategic Emerging Industries, the government is seeking to mobilise M&As as a way of restructuring the industry, increasing competitiveness, and supporting the development of national champions which will have the capacity to compete with the world’s largest firms (Barbieri et al., 2017). On top of this approach, new production regulations such as the Good Manufacturing Practices and longstanding difficulties surrounding the patenting process have increased costs and reduced opportunities for profit, subsequently increasing the attractiveness of M&As to navigate economic challenges (Wu and Hsu, 2018). As shown by Figure 8, the state-led promotion of pharmaceutical M&As has created an uneven landscape of acquirers and targets. While pervious figures have been based on value and given that China is the largest M&A market by volume, Figure 8 focuses exclusively on domestic deals and reveals the top 10 acquirer and target cities (left to right) by number and how these positions have changed over time (left panel to right panel). The number of domestic deals in China (01–10 and 11–20).

The scale and pace of deals evolved rapidly over the last 20 years, growing from 43 deals in the first decade to 360 in the second. The landscape of M&As takes shape in the second decade and begins to reflect general patterns of economic development in China, with cities on the eastern cost including Beijing, Guangzhou, Shanghai and Hangzhou emerging as the top acquirers. Over both decades, Beijing is the leading acquirer with a total of 45 acquisitions and Shanghai the leading target with 25 deals. Interestingly this has parallels with the subnational geography of the US and the relationship between New York and San Francisco. Beijing is the political and to a growing extent the financial capital of China, whereas Shanghai is increasingly seen as the leading city in terms of high-end R&D, innovation and crucially, biotech. While biotech in China is still transitioning away from generic drugs and starting to align with new regulatory reforms, early signs suggests that innovations in this sector will be central to the development of pharmaceutical firms and to some extent shape future M&A activity (Han et al., 2021).

Crucially, this increased M&A activity has not resulted in the emergence of highly leveraged publicly listed firms driven by the expectations of shareholders and financial markets. This is the main reason as to why the value of the Chinese M&A market remains much lower than the US, as government intervention has influenced stock markets with repeated attempts to keep speculative bubbles under control. M&As have been mobilised by the Chinese government to restructure the domestic market and facilitate improvements to the research, innovation and production of pharmaceutical products (Barbieri et al., 2017) but other conditions such as the strict patent regime and lower R&D standards have limited international M&A activity and the permeation of financialized corporate logic (Chen et al., 2018; Zhong and Ouyang, 2020). This finding supports existing claims that while China has become increasingly financialized, this process has been heavily steered by its authoritarian form of state capitalism and managed in ways which support the state development objectives (Petry, 2020). While the Chinese government has encouraged M&As, its control over the financial system through state-owned banks and financial institutions means that other forms of financialization have remained limited throughout the pharmaceutical industry (Pan et al., 2021).

Essentially, and somewhat paradoxically, the institutional and political economic conditions in China have simultaneously encouraged M&As while preventing the financialization of pharmaceuticals. This is a key finding considering that M&As are seen as a central component of pharmaceuticals financialization. In the case of China, more M&As does not necessarily mean more financialization. This apparent paradox demonstrates how understanding the where of financialization is equally important to the what, as the underlying processes of financialization are constituted by the political economic, institutional and cultural conditions in which they are enacted.

Conclusions

The aim of this article was to explore the variegated financialization of the pharmaceutical industry through the analysis of M&A data. Drawing from a sample of 1805 M&A deals between 2001–2020, we reveal a geographically uneven landscape of acquirers and targets across the global, national and city scales. Our analysis uncovered that 99% of deal value and 97% of deal volume was concentrated within Asia, Europe and North America. Within these continents and at the country-level we revealed the central role of the US, Switzerland and France as key acquirers, with a notable rise in the position of China over time. Analysis at the city-level underscored these trends, with the central position of the US reinforced by New York being the world’s leading acquirer and San Francisco the leading target. While international acquisitions were some of the most valuable, findings also uncovered the domestic orientation of many of the largest pharmaceutical M&A markets, with close to two thirds of all deals occurring within countries.

Our analysis of the US and China added depth to these findings by revealing the importance of institutional and regulatory conditions in shaping the incentives and outcomes of M&As. In the US we uncovered the central role of the state in creating the conditions for the financialization of pharmaceuticals, mainly through enabling the private appropriation of public knowledge, as well as the role of M&As in compounding spatial divisions of labour. While the Chinese state also played a significant role in accelerating pharmaceutical M&As, most notably through their aim to establish national champions, different institutional conditions limited the extent to which these acquisitions are driven by financialization. Overall, this comparison highlights the contingent nature of M&As as part of the financialization of pharmaceuticals. Rather than increased M&A activity necessarily and inevitably leading to greater forms of financialization, contrasting institutional and regulatory conditions played a key role in shaping the scale, pace and outcomes of their implementation.

These findings allow us to make empirical and conceptual contributions. Empirically, we have provided fresh insights into the spatially variegated financialization of the pharmaceuticals industry. By uncovering spatial disparities in the value and volume of M&As, as well as identifying dynamic landscapes of acquirers and targets across geographical scales, we can better understand the how the financialization of pharmaceuticals unfolds unevenly. Importantly, and while we discovered some shifts in trends over time, most notably the significant rise of China in terms of deal volume, we uncovered no seismic transformations to the geography of pharmaceutical M&A deals. This is a striking finding considering that our analysis stretched two decades. It highlights a high level of inertia and helps us understand the limited and exclusive geography of pharmaceuticals financialization.

Conceptually, our findings advance debates around the geographies of financialization. Our novel M&A-based approach has allowed us to develop a relational conceptualisation of financialization, whereby geography is causal and constitutive in terms of what financialization is, where it unfolds and how it collides with new spaces. Considering that M&As are the primary mechanism through which financialized business models fuse with others, our analysis has allowed us to capture where and why financialized activities reach new places. This key finding, along with the comparison of the US and China, demonstrated how geographical, institutional and regulatory conditions do not only shape the processes of financialization but fundamentally constitute what they are and how they are enacted. While we acknowledge that M&As are key tenet of pharmaceutical financialization, we uncovered a paradox whereby more M&As in China did not translate into more financialization. This crucial distinction suggests that solely analysing the what of financialization may be misleading. In the case of pharmaceuticals, understanding the where of financialization, and namely the institutional and regulatory conditions which shape firm behaviour, is equally important.

While our M&A analysis has generated fresh empirical insights, important questions remain unanswered and further research is required to develop more finely grained explanations of the financialization of pharmaceuticals. In the context of de-financialization, what regulatory measures can be taken to ensure the prioritisation of patients and healthcare systems over corporate profits? How uneven are the outcomes of pharmaceuticals financialization, particularly in terms of patient wellbeing but also in terms long-term investments in R&D and innovation? How do the geographies of some of the other key tenets of pharmaceuticals financialization, such as shareholder value generation and R&D outsourcing, compare with the geography of M&As? Addressing these questions will not only generate new perspectives on the pharmaceutical industry but also reveal much more about the variegated nature of financialization.

Footnotes

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by funding from the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation program (grant agreement No. 681337). All errors and omissions are the sole responsibility of the authors.