Abstract

Extending the growing literature within international political economy, this article puts forth the notion of transnational state capitalism, taking into account the anaemic growth gripping the global economy since the 2008 economic crisis and China’s massive efforts to export infrastructure following the launch of the Belt and Road Initiative (BRI) in 2013. Focussing on the agencies, practices and outcomes of the Jakarta-Bandung High Speed Rail, one of the largest infrastructure undertakings in Southeast Asia since the BRI’s inception, this article explores how and to what extent state capitalism has shaped the political economy of a rising China in Indonesia. We identify three characteristics of an emerging transnational state capitalism in Southeast Asia: state-centric in its overall direction and operation; simultaneous pursuit of economic-cum-geopolitical interests; and an inability to stem structural weaknesses associated with statist economic directives (which have been further complicated by its intertwining with host state dynamics). Our central argument is that although this project was initially conceived as a business-to-business arrangement, it has increased the appeal of state intervention in a transnational context. The driving forces include Indonesia’s political economy and the Chinese state-owned enterprises’ dual agenda of seeking profits and advancing geopolitical goals. We also argue that the project’s statist nature has brought about some side-effects such as inefficient resource allocation and incumbency bias, thus raising concerns about the vulnerability of state capitalist models. Our findings highlight the importance of conceptualizing the transnational state against the backdrop of a globalizing China, going beyond parochial understandings of this increasingly salient phenomenon.

Keywords

Introduction

Recent transformations in the global economy have reignited interest in the role of the state. Such transformations include a resurgence of various forms of state-led development, especially in the Global South (Alami and Dixon, 2020; Bremmer, 2008; Kurlantzick, 2016). One of the most enterprising research out of these works is how China, as the pacesetter in the developing world, is challenging established market conceptualizations. For Massot (2021, 534), China’s emergence is upending market belief in three ways: ‘the continued resilience of China’s authoritarian state-led capitalist economic model, China’s positioning around notions of power and fairness in the global economy, and China’s mixed preferences regarding global markets’. She further contends that these features are difficult to interpret ‘within the confines of three conceptual straitjackets that limit our capacity to think creatively about markets: the free-market ideal-type, the market-state dichotomy and the notion of a natural progression towards a market system’ (Massot, 2021, 552). It is here that comparative capitalism studies have ‘the potential to become a major approach in the field of development studies in the future and relieve comparative political economy from some of its Western centrism’ (Schedelik et al., 2021, 514; see also Feldmann, 2019).

Scholars have proposed various ways to remedy the deficiencies in addressing the implications of a rising China in the existing frameworks of global and capitalism studies. Massot (2021, 552) proposes ‘an institutionally grounded definition of markets’ by emphasizing the ways in which markets vary along ‘different institutional features such as the behaviour of market stakeholders, its shape, the nature of the interactions among market actors, its governance structures, power relations and embeddedness features’. Similarly, Andreoni et al. (2019) argue that it is almost impossible to reduce examination of industrial policies to a mere ‘technical problem’ using a market economy lens. They suggest incorporating a wider range of institutions into the analysis than what is normally discussed, especially for developing countries (such as China) yet to establish a mature market economy (Chang, 2002a). This context-rich viewpoint is useful in assessing tensions arising from their industrialization process, not least when their economic influence is increasingly noticeable in the global arena (Andreoni and Chang, 2019). Robinson (2015) calls for a paradigmatic shift in focus to decipher the increasingly prominent role of Brazil, Russia, India, China and South Africa (BRICS) in international affairs. Opting for a break with the nation-state/inter-state framework, he forwards a global capitalism perspective that sees the world not in terms of nation-states struggling for hegemony through competition and coalitions, but ‘in terms of transnational social and class forces that pursue their interests through national states and other institutions’ (Robinson, 2015, 2).

Building on such works, this article advocates a ‘transnational state capitalism’ framework to discern how state activism is moving across borders and shaping development outcomes. It challenges the state-market dichotomy and market primacy assumptions, unearthing the unconventional manners by which developing economies promote their overseas interests. The article also analyses how a wide range of stakeholders and institutions collaborate and compete with one another in infrastructure development, a pivotal issue for developing countries, distinguishing itself from earlier studies (e.g. Harris, 2009, 2013) that focus on financial institutions such as sovereign wealth funds and their investment in emerging market equities and in other investments abroad. As will be argued later, a transnational state capitalism with three key characteristics is emerging: it is state-centric in that major decision-making and resources allocation come from the government and/or state-owned enterprises (SOEs); it is driven by both an economic logic of expanding market share and profits and a geopolitical agenda of boosting Chinese influence; and it is tied to a set of inherent dilemmas (such as inefficient resource allocation) that are exacerbated by its complex intertwining with the host economy’s politics.

An alternative interpretation of China’s economic development is especially important in the wake of severe crises such as the 1997 Asian Financial Crisis (AFC) and the global economic crisis of 2008. Making things more complex is the speed (relative to mature economies) with which China revived its economy in 2008 (Nölke, 2014; Petry, 2020). As Chinese firms, not least the SOEs, faced a fast-declining export market in the advanced economies during the 2008 crisis, aggressive stimulus spending to create demand within China was rolled out expeditiously (Wang, 2014).

While a meltdown was avoided then, overcapacity and soaring government debt, amongst other issues, have reared their ugly heads by the mid-2010s and hampered economic expansion. Indeed, Chinese politicians, bureaucrats and economists have gradually come to terms with the realization that annual gross domestic product (GDP) growth will slow to between 7.0% and 7.5% from the double-digit levels in recent past (Wang, 2014). According to Ye (2020), this overaccumulation and secular slowing down is one of the major factors undergirding the announcement of the Belt and Road Initiative (BRI), seen in many quarters as arguably China’s most crucial engagement tool with the rest of the world.

Although there exist multiple interpretations on how the BRI is to be defined and operationalized, there is a consensus that the export of capital-intensive infrastructure constitutes a key component of the initiative (Camba, 2020; Rana and Ji, 2020; Yan, 2021; Liu et al., 2022). However, what exactly happens when Chinese firms carry out these projects overseas? How and to what extent is Chinese state-business relations transmitted across borders, especially into a fellow country in the Global South? What differences, if any, does the participation of Chinese actors make in the shaping of the host state’s pre-existing infrastructure development practice? What are the implications for a better understanding of an emerging transnational state capitalism as well as its related boon and/or bane in the context of infrastructure export at a time of growing Chinese influence in Southeast Asia and beyond?

Exporting railway projects to the Global South

With the above as a backdrop, this article focuses on the much-touted USD5.5 billion Jakarta-Bandung High Speed Rail (HSR) project, arguably the highest profile BRI project in Southeast Asia. 1 Subject to intense jostling between China and Japan, the project was eventually won by the state-owned China Railway Group Limited (CREC) in September 2015. In winning the bid, CREC received a loan from the China Development Bank (CDB), another Chinese SOE, to finance 75% of the project cost over 40 years. The remaining cost is covered by Kereta Cepat Indonesia China (KCIC). KCIC is a China-Indonesia joint venture, with 40% equity owned by a CREC-led consortium and the balance 60% owned by PT Pilar Sinergi BUMN Indonesia (Dharma Negara and Suryadinata, 2020; Lampton et al., 2020). 2

The Jakarta-Bandung HSR represents a key thrust of the Joko Widodo (Jokowi) administration (2014 to present) – which is clearly promoting infrastructure development (that requires patience in terms of duration of return on investment) and by extension, an enhanced role for state activism (Kim, 2020). Another oft-cited reason contributing to CREC’s winning bid is its promise that it could complete the project before Jokowi’s re-election campaign in April 2019. This proved vital to Jokowi, who wanted to show voters that he had fulfilled his promise of improving Indonesia’s infrastructure when he was first elected as President in 2014 (Kratz and Pavlićević, 2019). However, perhaps because of its high-profile, the 150 km railway linking Indonesia’s largest and third largest cities, respectively, has elicited defensive political responses.

This article’s central argument is that the project has forwarded the appeal of state intervention in a transnational context, notwithstanding the Indonesian government’s initial preference of a business-to-business arrangement and other hurdles and contradictions. In line with the characteristics of transnational state capitalism alluded earlier, we make three observations. Firstly, host state elites (led by Jokowi) have facilitated CREC’s entry to a costly infrastructure project with a longer-than-normal payback period in the Jakarta-Bandung HSR, shunned otherwise by the private sector and some members of the Jokowi administration. Jokowi’s determination to undertake infrastructure projects with large development externalities (in this case, the HSR) reinforces state activism in Indonesian industrialization. Secondly, CREC has simultaneously pursued its commercial interests while advancing Beijing’s broader foreign policy objectives. Yet, official credit has been disbursed rather cautiously. CDB’s prudent approach in financing the Jakarta-Bandung HSR underlines the importance of market incentives even in such a high-profile BRI undertaking. CREC’s and CDB’s behaviour is seemingly a by-product of the Chinese economic system, where public and private interests are not easily separable. More to the point, their internationalization process is characterized by a continuous search for functional forms of state-business relations outside China. Thirdly, the Jakarta-Bandung HSR’s statist nature has brought to the fore a set of inherent dilemmas associated with state capitalism (such as resource misallocation), exposing the model’s vulnerability. In addition, the project’s ‘state-ness’ and ‘Chinese-ness’ has compounded bureaucratic frictions in Indonesia and invoked fears of the alleged promotion of Communism.

Interview and fieldwork information.

The article first examines the dynamics of the transnational state and identifies the gap in knowledge, especially the lack of studies on how Chinese capital exports are crossing national borders and impacting host state development (and vice versa). The subsequent section focuses on the Jakarta-Bandung HSR, unfolding the agency of key political and economic players. More specifically, it analyses the meshing of Chinese firms with the Indonesian political economy – centred on state activism, market behaviour, and structural weaknesses associated with state capitalism. The article concludes by summarizing the main arguments and outlining implications for future studies.

When China ‘goes out’: Of transnational state and global development

The history of development shows us that catching-up has almost entirely been enabled by an activist state, through both direct and indirect means (Chang, 2002b; Gerschenkron, 1962). According to Nölke (2014), China rising is termed as ‘state capitalism 3.0’ as it is merely following in the footsteps of the ‘1.0’ (mid- to late 19th century US, Germany, and Japan) and ‘2.0’ variants (US and Soviet Union after the Great Depression and the post-World War II East Asian developmental states). Relatedly, due to the rapid growth since its 1978 ‘Reform and Opening-up’, the Chinese economy has received arguably the most attention from analysts unpacking state capitalism.

Although nominally a socialist economy, post-1978 China is firmly founded on a market economy as private firms (both domestic and foreign-owned) thrive alongside the powerful SOEs (Naughton and Tsai, 2015). Most of the agents, even when state-owned, are driven to maximize profit, relying heavily on market forces in their sustained pursuit of international comparative advantages (Lin and Wang, 2017; Naughton, 2010; Nolan, 2014). There is also a blurring of boundaries between public and private interests, with the state regularly intervening in ways that create spillover for broader socioeconomic stakeholders, and in certain cases private parties well-connected to politicians. This complex mix of the state and market implies that short-term economic loss is acceptable so long as long-term political goals are attained (Huang, 2008; Ye, 2020). For Li (2015), this translates to the grooming of a ‘national team’ of giant modern SOEs, especially in the ‘commanding heights’ of the economy, through decades of corporate experimentation and policy learning. The wellbeing of the ‘national team’ is important not only to generate employment and economic output, but also to further technological know-how. This state of affairs also means that the government retains considerable administrative prerogative in shaping enterprise development, including but not limited to the outright banning of activities deemed sensitive to national interests (Starrs, 2017).

However, this model is not without flaws, with doubts cast over its sustainability. According to Liu and Tsai (2020), the preponderance of SOEs has compromised the overall competitiveness of the corporate sector. In addition, foreign direct investment (FDI) has been courted to plug technological shortfall, but in turn creates even more dependence on the former. Their work resonates with comparative research on state-activist strategies of various emerging economies. The overall prognosis is that merits such as a more rigorous push for industrial upgrading and economic redistribution must be balanced against side-effects ranging from weakened accountability, incumbency bias, resource misallocation, to debt pile-up (Chatterjee, 2020; Wade, 2018).

Despite its insights, the scholarship detailed above examines the Chinese economy in almost entirely the domestic context. Yet, this situation has to be reconsidered, especially if one takes into account China’s emergence as a large outward investor since the early 2000s (Ye, 2020). Outward FDI flows received a further boost in 2013 after the BRI was announced. This development means that Chinese capital and its associated modes of operations have increasingly crossed national borders, generating ramifications that are relatively less understood compared to earlier decades (where Western and Japanese firms were the two largest investors in the world). For one, the state’s heavy imprint means that Chinese capital export is markedly distinct from the more developed Western and Japanese outward FDI, which is largely owned by private enterprises (Bremmer, 2008; Kurlantzick, 2016). Blurring the boundaries between private economic interest and state-building efforts, the motivations of the Chinese business groups venturing overseas are driven both by a desire to seek profit as well as promote Beijing’s foreign policy (Oh and No, 2020; Liu 2022a, 121–140). This perspective is especially salient in infrastructure export, where China is said to leverage capital and technology vis-à-vis smaller nations to support its rise as a global power (Oh, 2018; Tritto, 2021). Contrarily, Lauridsen’s (2020) research on the Sino-Thai HSR project interlinking Bangkok and the rural, north-eastern provinces, found that the project has been driven predominantly by economic motivations. Although he does not deny Chinese foreign policy and geopolitical objectives, Lauridsen argues that what matters more in the Sino-Thai HSR project is the market-seeking directives of its infrastructure and engineering firms, many of which are suffering from overcapacity and domestic business slowdown as a result of the deceleration of the Chinese economy following years of rapid growth.

This is not to imply a lack of research on Chinese firms ‘Going Out’ in general. Babic, Garcia-Bernardo, and Heemskerk (2020), in their study on transnational state-led investment, show that states employ two basic strategies when they invest capital abroad. On one hand, statist economies (led by China) pursue a control strategy by creating ownership ties that grant them majority control of overseas firms. Contrarily, more liberal or ‘Western’ economies (e.g. Norway and Canada) seek to receive return on investments through portfolio investment (financial strategy) (Babic et al., 2017). Perhaps because of its preoccupation with a macro-level dynamic, there is a relative lack of analysis on actual, on-the-ground affairs. Relatedly, stakeholders, especially those in the host economy, and their agency are often given short shrift. Such research gap brings about a conflation (or even confusion) of intention with outcomes, leading to possible misunderstanding of the development impacts of Chinese capital exports on the host economy.

What is needed is a more circumscribed exploration of the imbrication between transnationalizing state capitalism and development outcomes. Indeed, there is a small, but growing, corpus of scholarship covering this perspective (e.g. Camba, 2020; Gu et al., 2016; Kratz and Pavlićević, 2019; Liu and Lim, 2019). Analysing project-level outcomes is Lim (2018), who illustrates that – despite paying a premium to acquire Canada-based Nexen in 2013 – state-owned China National Offshore Oil Corporation (CNOOC) has found it difficult in adapting to local conditions. In 2015, CNOOC’s acquired unit failed to comply with safety and regulatory standards when its freshly installed pipeline spilled more than 31,000 barrels of unprocessed effluent into the environment, hitherto the largest such spill in the history of Alberta, Canada. Taking on a more international political economy viewpoint, Kutlay (2020) demonstrates that the Turkish ruling elites, leveraging warmer ties with both China and Russia, appear to be gradually shifting from a Western-oriented liberal model towards a variety of ‘state capitalism’ as an alternative development paradigm. Kutlay underlines his argument by shedding light on how three interconnected and reciprocal mechanisms – ideas, material interests, and institutions – have adopted increasingly illiberal, extractive features.

Chinese business groups in Indonesia: Merits, discontents and outcomes

State activism across borders

Ascending to the Presidency in 2014, Jokowi pledged to uplift Indonesia’s creaking infrastructure, making it one of his key mandates. Therefore, big ticket projects like the Jakarta-Bandung HSR are critical to his legitimacy. However, Jokowi, unlike past Presidents, is not a member of the nation’s political, business and military elites. Despite access to the national budget and the SOEs, Jokowi’s modest background meant that he has to contend with politico-bureaucrats who guard the relevant ministries (Syailendra, 2017). To alleviate this gridlock, Jokowi has taken two broad approaches.

Firstly, Jokowi has steadily increased the stature of the SOEs, primarily through indirect finance disbursed through development financial institutions. Kim (2020) illustrates that indirect financing allows the Jokowi administration to sidestep (albeit not completely) the obstacles it faced when it attempted to support the SOEs directly. Jokowi was also helped by a fortuitous drop in energy prices, giving him the opportunity to slash fuel subsidies, thereby freeing up cash for the SOEs (Kim, 2021). Jokowi builds on the state-activist momentum generated during the second term of his immediate predecessor, Susilo Bambang Yudhoyono (2009–2014). Emboldened by a strong electoral mandate and eager to counter the headwinds stemming from the 2008 economic crisis, Yudhoyono promulgated aggressive reflationary measures in his second stint as President. One of his landmark policies was the Masterplan for the Acceleration and Expansion of Indonesian Economic Development 2011–2025 (MP3EI) (Sato, 2017). Despite some reform measures, the MP3EI was limited by several factors, especially fiscal commitments and Yudhoyono’s reluctance to more aggressively mobilize SOEs. As detailed by Warburton (2016), Indonesian legislative restrictions on the size of its fiscal deficit (under 3% of GDP) and large fuel subsidies constrained Yudhoyono’s policy space. Yudhoyono primarily saw SOEs as vehicles to provide tax and dividend payment to the government. Relatedly, Yudhoyono’s unwillingness to more actively mobilize SOEs can be explained by a scandal implicating construction SOEs run by his clique, which undermined public confidence in the administration (Kim, 2021).

Secondly, Jokowi courts Chinese business groups aggressively. Their speed-to-market, and reasonably high quality, amongst other factors, are helpful in pushing projects with long gestation period. While receptive to foreign capital regardless of nationality, Jokowi has acted quickly in capitalizing on Chinese President Xi Jinping’s announcement of the ‘21st Century Maritime Silk Road’ (the maritime component of the BRI) in the Indonesian parliament in October 2013. 3 Important bureaucratic measures include the setting up of a special desk dedicated to attracting Chinese investors by the Investment Coordinating Board (BKPM) in May 2016. This team provides consultation, facilitation and information service in Chinese language for investors from China. Relative to the pre-Jokowi era, the BKPM has more actively conducted investment promotions in China in partnership with China’s banks and business association (Dharma Negara and Suryadinata, 2021). In April 2021, Jokowi elevated the bureaucratic status of the BKPM into the Ministry of Investment. As a fully fledged line ministry, it now has extra powers to issue decrees and create regulations (Medina, 2021).

Both approaches were evident in the coming together of the Jakarta-Bandung HSR. To reiterate, four Indonesian SOEs were mobilized to form the KCIC consortium with CREC. This state-state alliance interlinking the SOEs of China and Indonesia, from its financing (by CDB) to on-the-ground implementation (by KCIC) can be interpreted as a sign of increased state intervention in the economy. In pushing this transnational collaboration, Yudhoyono’s MP3EI is effectively ‘inherited’, or even enhanced, by Jokowi. With Jokowi commencing his second term after winning the Presidential election in mid-2019, this state activism is no longer a transient development. It similarly underlines Indonesia’s democratic transition following the end of Suharto’s regime in 1998, which ushered in a series of short-ruling Presidents until Yudhoyono’s emergence in 2004. A more stable Presidency also implies that industrialization efforts and economic strategies can be formulated more consistently.

Nevertheless, the Jakarta-Bandung HSR has experienced multiple hiccups, achieving only intermittent progress at the time of writing. The planned completion in late 2018 and operation commencement in early 2019 have both failed to materialize. One of the major reasons, ironically, is the project’s ‘state-ness’ and ‘Chinese-ness’. With regards to the former, it has been argued that Indonesia’s decentralization and bureaucratic politics have hindered the railway’s implementation (Lampton et al., 2020, 162–167; Lim et al., 2021). Furthermore, the Jakarta-Bandung HSR’s state-state alliance and its related assemblages remain circumscribed by Indonesian legislative requirement to cap fiscal deficit at under 3% of GDP. Recent reports highlight an increase in Indonesian SOE debts, with some of them defaulting on their creditors (Rahman R, 2020). In April 2020, S&P Global Ratings even downgraded Indonesia’s sovereign credit rating outlook to ‘negative’ from ‘stable’, indicating the rising financial risks associated with the SOEs’ debt.

When it comes to the Jakarta-Bandung HSR’s ‘Chinese-ness’, it is worth mentioning that the project has been opposed by influential interest groups who believe that dependence on China would circumscribe Indonesia’s strategic autonomy. One of the most strident voices originate from the powerful military. In particular, conservative factions are suspicious about the alleged threat of China’s Communist ideology to Indonesia. 4 BRI projects such as the Jakarta-Bandung HSR are frowned upon because of an alleged alliance between the Chinese and their Indonesian peers, which could jeopardize national interest (Interviews with academic researchers, business executive and think tank analysts, 22 to 24 March 2018, Jakarta). This ‘red scare’ has been spread to society-at-large by organizations associated with the military. Some of these organizations have staged protests to warn of Communism’s potential ascent in Indonesia (Priyandita, 2016). Their anxiety relates to several widely circulated media reports alleging corruption, poor construction quality and unregulated welcoming of Chinese labourers into Indonesia (e.g. Syailendra, 2017; Danubrata and Suroyo, 2017). In addition, the military claimed that the HSR’s construction has encroached into the Halim Perdanakusuma airbase in East Jakarta. The then Air Force Chief of Staff suggested the relocation of one of the HSR stations as he claimed that the project could jeopardize the military’s air transportation duties (Kompas.com, 2020). The impasse was resolved only in July 2018 after KCIC handed over a new set of houses to the affected military personnel (Zuhriyah, 2018). Furthermore, the complexity of ‘Chinese-ness’ lies not only with the Chinese state, but also with the presence of a large number of ethnic Chinese businesspeople in Indonesia and Southeast Asia. Some of them have seen their fortunes rise through their institutionalized engagement with China. Amidst the growing significance of the BRI, this group of businessmen will likely play an increasingly pivotal role in actualizing transnational Chinese state capitalism (cf. Ren and Liu, 2022).

KCIC’s dispute with the Indonesian military and its broader politicking arguably emboldened Prabowo Subianto, a former commander of the Army Strategic Reserve Command who challenged Jokowi for the Presidency. Using fiery (and arguably primordial) rhetoric, he invoked negative sentiments targeting CREC and its supporters in his Presidential election campaign. Attempting to distinguish himself from Jokowi and capture conservative votes, Prabowo promised to conduct a thorough review of prominent BRI projects, in particular the Jakarta-Bandung HSR, if he became President (Salna and Aditya, 2019). Despite the General Elections Commission declaring Jokowi as the winner of the Presidential election on 21 May 2019, Prabowo has refused to budge as he challenged the election result in court (Santoso and Yasir, 2019). On 23 October 2019, in his first cabinet reshuffle after being re-elected, Jokowi has seemingly closed ranks with Prabowo, appointing the latter as Minister of Defence. Despite these challenges, stemming from the project’s ‘state-ness’ and ‘Chinese-ness’, progress has still been made.

Playing geopolitics with (quasi-)market means

As mentioned earlier, the Jakarta-Bandung HSR was awarded to state-owned CREC in late 2015 after an intense bidding war that involved Japanese railway builders. Despite initiating a Japanese government-sponsored feasibility study as early as 2009 and promising to finance 75% of the project cost with an interest rate on the loan of 0.1%, in addition to endorsement from key Japanese politicians, the Japanese railway consortium failed to stave off CREC’s belated entry (Harner, 2015). The Chinese bid was picked primarily because of its financial structure – CREC had not required any Indonesian government financing or a government guarantee (Dharma Negara and Suryadinata, 2020). CREC’s proposal, unlike the Japanese offer, transforms the project into a business-to-business venture, shifting the burden of financing from the public to the corporate sector.

Additionally, Jokowi leveraged the project to reduce Indonesia’s reliance on Japan. Japanese firms, supported by their national government, are amongst the biggest investment and aid contributors in Indonesia, especially since the Japanese Yen’s appreciation in the aftermath of the 1985 Plaza Accord (Kratz and Pavlićević, 2019). Fieldwork showed that Japanese economic packages tend to come with conditionalities, which occasionally went against the interest of stakeholders within the Indonesian establishment. Some of the conditionalities are rigid reporting standards and requirement for sovereign guarantee on borrowed money. The interviewees believed that letting CREC win the project would not substantially alter Indonesia’s existing ties with Japan, whilst providing Indonesian policymakers with another option in the form of China (Interviews with academic researchers, business executive, and think tank analysts, 22 to 24 March 2018, Jakarta; Telephone interview with academic researcher, 18 May 2019, [Singapore to] Jakarta).

China’s geopolitical ambition in overseas railway development is underpinned by several factors, ranging from the pursuit of political and economic cooperation, enhancement of inter- and intra-regional connectivity, to export of ‘China Standard’ in critical infrastructure and engineering systems (see, for example, Chan, 2016; Lampton et al., 2020; Liao and Katada, 2021; Yan, 2021). The Jakarta-Bandung HSR, courtesy of Indonesia’s status as the largest economy (GDP of about USD1.2 trillion) as well as most populous country (close to 270 million people) in Southeast Asia, is thus a ‘must-win’ for a rising China. This view was underlined by the manners in which the project received the attention of top office bearers within the Chinese government. For example, as China’s ‘HSR Salesman’ and the second-highest ranked politician, Premier Li Keqiang travelled extensively across the world, including Indonesia, to press for contracts (China.org.cn, 2014).

Perhaps more important to CREC’s winning of the Jakarta-Bandung HSR project is the visit by Xu Shaoshi, then head of China’s powerful National Development and Reform Commission (NDRC) on 10 August 2015, merely weeks before the winner of the bid was announced. In an unprecedented move, Xu was sent as special envoy of President Xi Jinping to meet Jokowi, delivering to the latter a feasibility report and a five-point cooperative proposal for the project (Ma, 2015). Recognizing the importance of the HSR to Chinese geopolitical ambitions, CREC has been forthcoming with its support to the political leadership. This can be gleaned from Yang Zhongming’s (Managing Director of CREC) public declaration of support to state-centric objectives such as ‘setting the tone for the BRI in Southeast Asia by making the Jakarta-Bandung HSR an early success story in the region’ and to promote ‘minxin xiangtong’ (people-to-people connectivity; one of the five major priorities of the BRI) (Zhongguowang, 2018).

While Japan has utilized (and continues to utilize) official development assistance to pursue foreign policy, Tokyo has, as a rule, avoided taking equity stake in grooming Japanese business groups (a trend which started even before World War II). With the private sector as the main engine of growth, Japanese SOEs play only a relatively minor role in the economy; they usually participate in highly regulated, non-tradable industries such as utility provision. This state of affairs imply that Japanese firms cannot tolerate as high a risk as their Chinese counterparts as the former is ultimately responsible to private shareholders. Indeed, the financial risk for CREC is heightened by the waiver of a financing commitment or guarantee from Jakarta, a concession that the Japanese political and commercial establishment refused to meet. In other words, CREC is seemingly forgoing short-term monetary gains (or disregarding monetary incentives) to achieve more far-reaching political goals. This development can be explained by the manners in which capitalism has been cultivated in China. CREC’s (and the broader economy’s) growth has been undergirded by a state that retains substantial administrative authority and a blurring of boundaries between state and market, a thesis made by Liu and Tsai (2020) as well as Huang (2008). This implies that CREC has reasons to align its decision-making with state preferences, especially in a critical overseas project such as the Jakarta-Bandung HSR.

However, beneath the geopolitical manoeuvring, the situation was more complicated. CREC has had to source more business abroad as Chinese railway development was maturing by 2015. Furthermore, there were talks in March 2015 about a mooted merger between CREC and its long-time rival, China Railway Construction Corp (CRCC) (Ye, 2015), but this failed to materialize eventually. It could be argued that CREC was ‘pushed’ to internationalize because the Chinese economy was already suffering from overcapacity not only in labour-intensive traditional industries, but also in so-called high value-added emerging industries where Chinese expertise is increasingly recognized (e.g. railway development and renewable energy) (Insights from participants in public fora, 17 January 2019 and 10 May 2019, Singapore).

Even accounting for all the push and pull factors motivating CREC to bid for the Jakarta-Bandung HSR, the reality is that SOEs like CREC do not have substantial operating experience outside China (Interview with European banking executive, 12 September 2017, Beijing). Interviews suggest that one of the main problems besetting CREC’s overseas expansion was their inability to adapt to the political environment outside of China. More specifically, inside China, these SOEs are used to dealing with just a handful of state organs who can make binding decisions at the start of the project. This in turn creates a relatively stable state-business relations which sets expectations and limits uncertainties once the project kicks off. However, this institutional setting is not commonly found outside of China (Interviews with business executives and think tank analysts, 18 to 20 September 2017, Beijing). Local authorities often do not possess the same level of authority like their Chinese counterparties, resulting in frequent changes of operating terms, which cause delays and even project cancellation.

Largely because of the above reasons, CREC and its partners have found conditions in Indonesia challenging. Two inter-related issues continue to plague KCIC – its limited cashflow and the tricky process of land acquisition. The latter would have been easier to surmount if KCIC had a stronger cashflow, but the four Indonesian SOEs are limited in terms of cash and can only contribute to the joint venture’s equity in stages. KCIC’s challenges have been compounded by the CDB’s guarded approach in loan disbursement. Originally, CDB was expected to disburse a USD4.1 billion loan (amounting to 75% of project cost) by March 2017 (Desfika and Trimurti, 2017). However, CDB was reluctant to do so, releasing the first loan package only in April 2018. Furthermore, only USD170 million was provided to KCIC, which amounts to a mere 4.1% of the total loan value of USD4.1 billion (Silaen, 2018). As of September 2020, only about 55% of the loan has been released (Gunawan and Azka, 2020). It was reported in April 2021 that the Indonesian side wanted to reduce its 60% share in KCIC, but the outcome remains unclear (Diela, 2021).

CDB’s caution seems to stem from its interpretation that the loan is de facto a profit-motivated one as the Chinese government had waived off the need for an Indonesian government guarantee during the bidding phase. Although the authors did not directly interview CDB executives on this matter, the information triangulated suggests that the state-owned bank had to hedge its risk in disbursing a loan of such magnitude. This means that it will only disburse loan moneys on a staggered basis, and they are contingent on the completion of land clearing by KCIC (Interview with European banking executive, 12 September 2017, Beijing; Insights from participants in public fora, 17 January 2019 and 10 May 2019, Singapore). CDB’s prudence implies that market incentives, rather than political considerations (i.e. the project’s importance to the BRI and commandeering by another SOE in CREC), are the main factors in deciding when (and by how much) to lend. CDB’s reliance on market signalling in an overseas project extends the studies of Naughton (2010) and Nolan (2014), both of whom highlight that the majority of Chinese market participants are driven to maximize profit. However, their analysis was derived almost exclusively in a domestic setting, precluding research on how these actors behave when they conduct business outside of China. More prosaically, the findings here reflect how China’s policy banks – CDB as one of the two – are facilitating overseas projects. Rather than subsidizing firms’ international business through direct allocation of fiscal revenue, Chinese policy banks play an indirect role in enhancing the creditworthiness of projects, in effect making them more ‘bankable’ (Chen, 2020).

Intertwining of politics with economics

Considering the scale and complexity of the project, it is only natural that disagreement emerge within Jokowi’s cabinet. More worryingly, the ensuing fallout raise the spectres of weakened accountability, incumbency bias, and resource misallocation, issues identified in the broader scholarship of state capitalism (e.g. Chatterjee, 2020; Wade, 2018). Take Rini Soemarno, for example. An ally of Jokowi, the (until late 2019) Minister of SOEs had been a key figure in advancing the project and in ensuring that it was awarded to CREC. 5 Rini’s main objective was to promote HSR development at a competitive price, while increasing the capacity and efficiency of SOEs under her command (Warburton, 2016). According to McBeth (2017), Rini pushed for China’s involvement from the start, even though the Japanese submitted the first feasibility study during the Yudhoyono administration in 2011. There were also significant differences between the Japanese proposal with that of the one eventually awarded to KCIC.

Ignasius Jonan, then Minister of Transportation, was more concerned with the technical and physical feasibility of the Jakarta-Bandung HSR, including but not limited to safety standards. Jonan’s team has also been discussing with Japanese firms on other public transportation projects (Lim et al., 2021). Unhappy with Rini’s manoeuvring, the ministry announced – 5 days after the Jakarta-Bandung HSR’s ground-breaking ceremony – that it had not issued the building permit. The Ministry of Transportation justified its action, claiming that it had not received the required paperwork from KCIC. Moreover, the concession agreement was withheld because it was still negotiating several important issues (e.g. default risk management and safety assessment) with KCIC (Susanty, 2016). This public brickbat did not end well for Jonan, who was soon sacked by the President in July 2016 (Parlina, 2016). However, Jokowi seemingly backtracked, appointing Jonan to the position of Minister of Energy and Mineral Resources, about 3 months after the latter’s initial termination. 6

Rather than engaging constructively with issues raised by Jonan, Jokowi’s axing of the former opens up possibility that institutional checks-and-balances might have been circumvented, leading to power centralization at the Presidency. Additionally, the fact that Jonan was so swiftly installed as the Minister of Energy and Mineral Resources raises more questions than answers. By not revealing the exact rationale behind Jonan’s removal from and subsequent recall into the cabinet, Jokowi has seemingly undermined public confidence in the Presidential office. 7

Perception of incumbency bias – towards Jokowi’s clique – has also been compounded by the close ties between Jokowi and Rini. For example, some Indonesian parliamentarians believe that Rini’s actions had undermined the Ministry of Transportation (Dharma Negara and Suryadinata, 2020). Despite Jokowi’s backing, Rini has failed to maintain harmonious ties with the leadership of his party, the Indonesian Democratic Party of Struggle (Partai Demokrasi Indonesia Perjuangan). Its matriarch, former Indonesian President Megawati Sukarnoputri, has privately and publicly attacked Rini’s credentials, even to the extent of calling for her removal from cabinet (see Kim, 2018; Warburton, 2016). Such pressure was to no avail as Jokowi kept his faith in Rini for the entire duration of his first term.

Reminiscent of Kutlay’s (2020) examination of Turkey’s institutional transformation to engage more closely with Chinese-Russian state capitalism, the ‘political settlements’ highlighted here add another layer of financial and technical burden to the Jakarta-Bandung HSR, generating potential resource misallocation. The project’s necessity has been questioned from the start. Its touted ability to cut travel time between Jakarta and Bandung to about an hour does not look wholly impressive when travelling by car, under light traffic, consumes slightly over 2 hours (Guild, 2020). Critics also argue that, as far as railway development is concerned, priority should be channelled towards improving conventional railways rather than installing new generation technology like HSR (Oh, 2018). Relatedly, more spillover could arguably be generated if the money had been spent to better connect Jakarta and Surabaya. Spanning close to 800 km, more economic activities and agents could be stimulated, especially considering Surabaya’s status as Indonesia’s second largest city (Salim and Dharma Negara, 2016).

More prosaically, the latest estimate of the HSR’s cost has been revised upward to almost USD7.9 billion (from USD5.5 billion), translating to a hike of about 44% (Reuters, 2022). Furthermore, the project’s overall completion rate stood at only 79.9% as of January 2022, up from 5% in mid-2018 (ANTARA, 2022; Desfika, 2019; Mu, 2019; Zuhriyah, 2018). The Jakarta-Bandung HSR was initially granted a deadline extension to 2021, following KCIC’s inability to complete it by mid-2019. However, this extension came to nothing as the onset of the COVID-19 pandemic in early 2020 shuttered most work places and disrupted supply chains. Indeed, the Ministry of Transportation announced as soon as April 2020 that the completion of the HSR would be further delayed (Rahman DF, 2020). The latest estimated completion date, announced by Jokowi in early 2022, has been set to June 2023 (ANTARA, 2022).

Conclusion

Analysing the Jakarta-Bandung HSR, this article has shed light on arguably the highest profile Chinese undertaking in Southeast Asia to-date. It has explored the intertwining of politics with economics and the hitherto underexplored impact of the increasingly heavy presence of Chinese capital exports in the global arena. The article’s central thesis is that the Jakarta-Bandung HSR deal – notwithstanding some challenges – has enhanced the appeal of state intervention across national borders. It has also illustrated that market primacy assumptions about the nature of the economy and the state are difficult to sustain.

First and foremost, CREC’s entrance has supported state activism in Indonesia, whereby SOEs are mobilized by President Jokowi to undertake costly infrastructure development, otherwise undersupplied by market forces. If anything, Jokowi is not only taking Yudhoyono’s MP3EI to heart, but also participating far more actively in pushing infrastructure projects through large, capital-intensive joint ventures between both Chinese and Indonesian SOEs. Although the Jakarta-Bandung HSR does not necessitate direct government financing or a government guarantee from Indonesia, one of the main reasons CREC defeated its Japanese rivals, the reality is that the key business groups behind this supposedly business-to-business venture are very much statist. More pointedly, CREC’s entrance into Indonesia signifies a state-state capital alliance, fuelled by both the welcoming of Chinese (state-owned) firms and the mobilization of Indonesian SOEs to carry out mega infrastructure projects. However, the project’s ‘state-ness’ and ‘Chinese-ness’ has meant that it is susceptible to decentralization and bureaucratic politics as well as ‘red scare’ allegations. It also faces a most important legislative hurdle safeguarding Indonesia’s macroeconomic health – the directive to cap the country’s fiscal deficit at under 3% of GDP.

Secondly, CREC has simultaneously pursued its commercial interests while conforming to Beijing’s foreign policy objective in the Jakarta-Bandung HSR. However, in a project that not only promotes China’s budding engineering expertise, but also arguably limits Japanese clout in a key regional economy, official credit has been disbursed carefully by CDB. The policy bank’s caution illustrates the importance of market signals. This deference to market forces can also be seen when one considers the ‘push’ factor driving CREC to ‘Go Out’, not least a slowing Chinese home market and overcapacity in key industrial goods. While geopolitics is an important calculus for the Chinese political and commercial elites promoting the Jakarta-Bandung HSR, the project’s manifestation thus far highlights that it is a far more complex issue than the oversimplified, politically expedient image oft-paddled in the popular media and/or the state-market dichotomy dominant in certain academic and policy debates (cf. Massot, 2021).

Thirdly, the Jakarta-Bandung HSR’s statist nature has unearthed a set of dilemmas associated with state capitalism (e.g. weakened accountability and resource misallocation). In the spirit of Andreoni and Chang (2019), a parallel argument can be made that these dilemmas are merely structural tensions, bottlenecks that a late developer faces when it pursues industrialization. The onus, therefore, is on the state to manage conflicting interests, alongside its policy entrepreneurial function. Notwithstanding Jokowi’s occasionally perplexing ways of handling the numerous opponents of the Jakarta-Bandung HSR, the project has been pushed forward – albeit in a gradual pace. While a detailed examination of how Jokowi’s government has managed interest groups standing to gain (or lose) from the project (e.g. local firms, labourers and non-governmental organizations) and how their jockeying has led to particular development outcomes falls outside the article’s remit, recent comparative political economic research by Lim et al. (2021) and Liao and Katada (2021) shows that the Indonesians appear to have extracted somewhat better terms from the Chinese business groups, at least in comparison with other Southeast Asian economies that also engaged the Chinese in pursuing railway projects. Nevertheless, the implementation speed of the Jakarta-Bandung HSR lags that of the other projects.

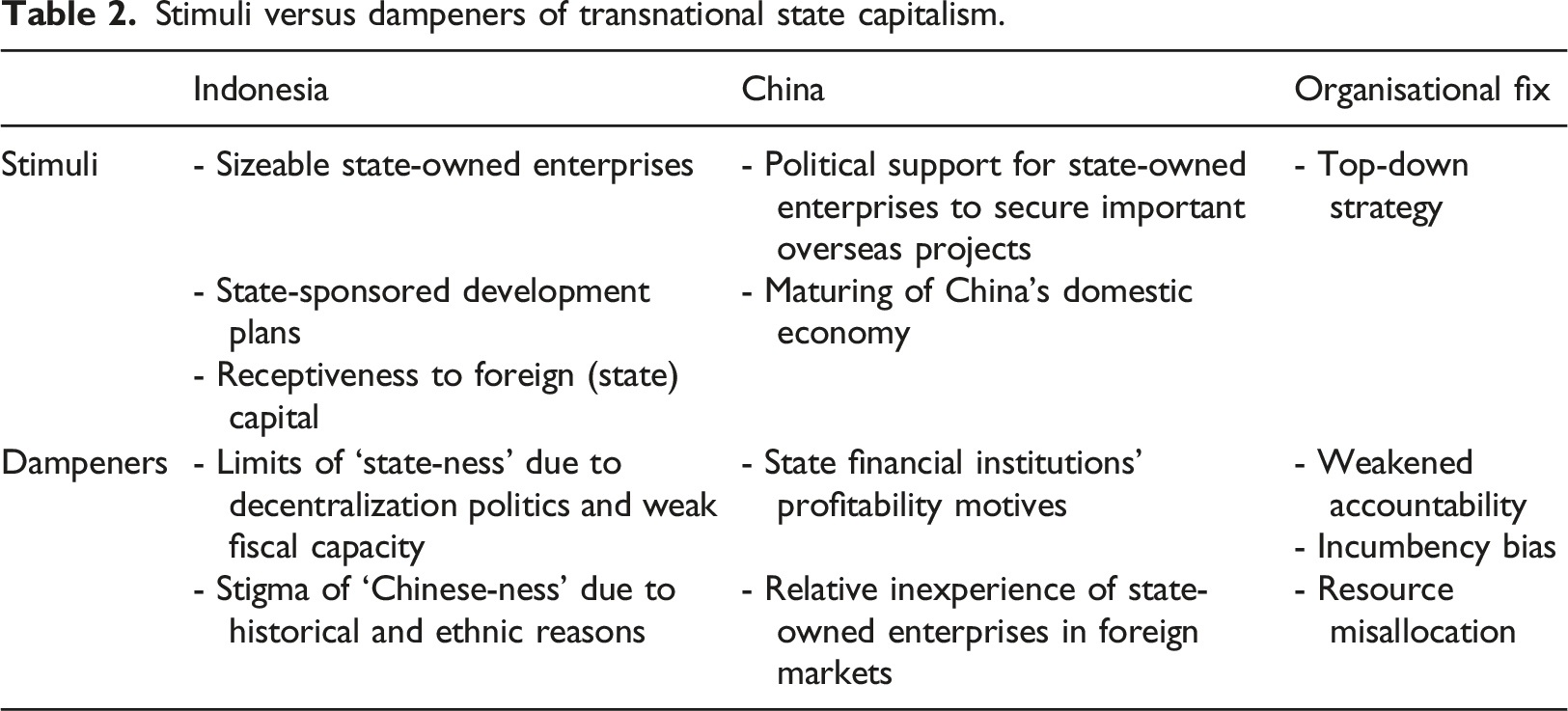

Stimuli versus dampeners of transnational state capitalism.

In Southeast Asia at least, the general political sentiment towards China has been relatively benign. One of the main factors buttressing China-Southeast Asia ties is the region’s longstanding shortfall in infrastructure provision. Scarred by the meltdown induced by the 1997 AFC, policymakers within the region have insisted on running current account surpluses that are arguably stronger than optimal, accumulating foreign exchange to shore up their economies’ external position (Khor et al., 2021). Such an overly conservative strategy is not without drawbacks because public spending, including those related to infrastructure, has been curtailed. This also implies that infrastructure demand will likely remain high in the near to medium term, opening up opportunities for Chinese firms eager to grow their market share in the region. However, economic shocks, such as COVID-19, have complicated matters. Another cause for concern is the deteriorating US-China relationship in recent years. Sandwiched by these two behemoths, it is likely that some of the Southeast Asian economies, especially those involved in border disputes with China, will be pressured to take sides (Lee, 2020).

Recent research adds weight to this article’s conceptualization of transnational state capitalism. While recognizing China’s growing heft in the global economy, Goodfellow and Huang (2021) stress the importance of examining the coming together of business, geopolitics, and development goals at the local level. This means that plans and designs are subject to mediation and politicking, leading to contingent outcomes that inadvertently dilute ‘Chinese-ness’ and its assemblages. Advocating a historical perspective on China’s engagement with the Global South, Liu (2022b) argues that it is important to not lose sight of the fact that China has been keen to uphold the legacy of the 1955 Asian-African Conference (also known as Bandung Conference). Gathering delegates from a total of 29 countries spanning Asia and Africa, the conference catalysed the emergence of what is to become the Global South, of which China and Indonesia remain key members. In addition to offering an alternative development paradigm to that professed by the advanced economies, it also sought, amongst other things, to deepen knowledge transfer within the Global South. More importantly, the Bandung legacy has continued to thrive, with its spirit and ideals continually invoked by various political leaders of the Global South.

With the rise of non-Western economies such as China and other BRICS countries over the past decade, it is imperative to go beyond Western-centrism and investigate new economic dynamisms and market mechanisms associated with the emerging economies (see Liu, 2022b; Neubert, 2022). This trend is likely to persist in the near to medium term as increasingly more emerging economies band together to forge larger common markets such as the Regional Comprehensive Economic Partnership, which took effect in early 2022. By focussing on China’s increasing economic influence and its engagement with Indonesia, the fourth most populous country in the world, it is hoped that our study represents a modest attempt to better understand the changing dynamics and growing importance of the transnational state in the Global South, and by extension, the international political economy.

Footnotes

Acknowledgements

The authors are grateful to the anonymous reviewers and editors of Competition and Change for their constructive suggestions which have helped improve the final version of this article. The authors are solely responsible for the views and any remaining errors.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Hong Liu would like to acknowledge funding support from Nanyang Technological University (04INS000103C430 and 04INS000132C430).