Abstract

Impact investing has emerged as a topical subject-matter for scholars working at the intersection between finance and social policy. By and large, it is seen as a product of financialization: some argue that the social is colonized by financial actors and methods, others see it as a site where boundary work produces a state of value plurality in which competing values—social and financial—co-exist. This article takes the latter perspective further and unpacks the endogenous dynamics underpinning the creation of social values in impact investing programs. It analyzes how high-level organizations in the field prescribed specific social impact valuation processes and mechanisms for collecting, measuring, and reporting data about value creation. It argues that the social values circulating in the impact investing field emerge from the interplay between a wide array of stakeholders, impact investors included. The social impact accounting tools that capture them materialize therefore as sites of political battles and negotiations between stakeholders, with both emancipatory but also exploitative potential. This has consequences upon our understanding of how financialization travels and how the social dynamics underpinning accounting devices (re)draw boundaries between competing values and fields.

Introduction

In 2013, Social Ventures Australia—a not-for-profit organization whose self-described mission is to alleviate disadvantage—raised A$7m from a consortium of 60-odd investors, including high-net-worth individuals, superannuation funds, and family foundations, to fund a social program designed to restore children in out-of-home care to their parents by fostering safe family environments (SVA, 2013). The program was underpinned by an outcome-based contract known as a Social Impact Bond (SIB), whereby repayments of the investment were tied to hitting specific performance targets called outcome or impact metrics. Once a minimum was hit—in this case, a proportion of at least 55% of children restored to their families compared to a counterfactual—investors received an additional interest payment ranging from 5 to 15% over the full term depending on the overall outcome performance achieved. The SIB built on the track record of the service provider, UnitingCare, but 2 years into its deployment, doubts about its accounting infrastructure started emerging. One issue was that while investors were receiving payments for restorations, not all restorations were locked in, with some descending into “reversals,” that is, children eventually returned into foster care. In this context, UnitingCare resolved to open up the accounting black box and amend the metrics used, but this raised fundamental questions about the possibility to re-negotiate the balance between social and economic returns mid-way through a social program. This was an issue especially given that it required the unanimous approval of investors, who furthermore stood to have their projected interest rate reduced from 15.08% to 8.92% (Tomkinson, 2015). To the relief of UnitingCare, after discussions with investors who were presented with the amendment but also with the option to sell their investment, they all conceded to the changes. Why was it so uncontentious for investors to concede to changes to the impact valuation process? Was this episode an exception or is there something distinctive about the interaction between stakeholders in the design and roll out of social impact programs? This article seeks to answer these questions.

Not long ago relegated to arcane and technical discussions between proponents and practitioners, impact investing (or social finance)—the mutual pursuit of social impact and financial return—is increasingly garnering attention within academic circles too. While a great share of scholarly work on social finance, in particular when it comes to emerging financial instruments such as SIBs, approaches it in the context of the global entrenchment of austerity policies ensuing the global financial crisis and the advancement of the ideology of neoliberalism (e.g., Broom, 2020; Harvie and Ogman, 2019; Lilley et al., 2019; Lavinas, 2018; Tse & Warner, 2018; Dowling, 2016), recent studies have focused also on the importance of the “boundary work” (Gieryn, 1983) at play in the field of social finance (e.g., Langley, 2018; Berndt and Wirth, 2018; Chiapello & Godefroy, 2017). Drawing demarcations from other fields is particularly important in the context of an emergent, “pre-paradigmatic” practice (Nicholls, 2010) that seeks to carve out a space of intervention at the intersection between other established domains of socio-economic activity, especially ones that are seemingly inherently hostile (Zelizer, 2000), such as the pursuits of social versus financial value creation.

Initially, studies on the shifting boundaries between finance and the social looked at the outsized role of financial actors, instruments, and processes in social impact programs and gauged social finance as a form of financializing the social (e.g., Bryan and Rafferty, 2014; Chiapello, 2014; Fine, 2012). This entailed transforming social policy into a source of financial extraction and allowing the social to be invaded by the language of finance, with social programs considered, for instance, as activities that must provide a (social) return on investment. However, when looking at the value infrastructure underpinning social finance, it was becoming increasingly clear that what emerges is value plurality (Barman, 2015), with competing values co-existing on the same plane and with boundaries beyond which financial processes and values do not travel. Langley (2018), for instance, contends that social finance “folds” social upon market logics and is able to mobilize them simultaneously to arrive at mutually beneficial outcomes in the spirit of liberal pluralism. This then constitutes a “liberal ethics of investment,” where private investment, facilitated by the novel calculative tools of valuation that gauge outcomes in social impact programs and “complement” traditional tools of portfolio managers, is able to pursue both financial and social value creation by harnessing, rather than rejecting, “value dissonance” (Langley, 2018: 12–13; also Barman, 2015).

This phenomenon of simultaneously pursuing a plurality of values, also referred to as “double bottom-line” or the “blended value proposition” (Emerson, 2003), has done much to refine our understanding of how financialization processes redraw boundaries within the social field. At the same time, a lot remains to be settled with regards to the calculative tools of valuation that buttress the social finance field and are crucial for preserving or safeguarding the social in the face of the advance of finance. How do these calculative tools appear and persist in the social finance field? What is novel about them and what do they actually measure? On whose terms are they fashioned and whose input goes into their creation? These are important questions to explore, for they can reveal battle lines and power dynamics hidden behind the seeming harmonious mutual pursuit of social and financial values implied in a liberal ethics of investment.

This article will then take a deep dive into the social impact accounting infrastructure built by the organizations sustaining and promoting the field of social impact investing, thus underscoring their role in the delineation of social finance as a legitimate space of socio-economic activity. That accounting is a crucial enabling factor of financialization more generally is well noted (Hiss, 2013), but in the field of social finance this mechanism becomes more complex. This paper will thus scrutinize the way in which the organizations that have taken upon themselves the task of promoting, standardizing, and institutionalizing the field of social impact investment prescribe the steps that need to be taken to define, measure, and report social impact creation. These steps demarcate what counts as proof of impact and whose input goes into impact assessment and calculation. It is important to explore this not only because financial return is predicated on its result, but also because it can reveal the extent to which financialization actually engrosses the social and what, if any, mechanisms are there in place that might derail it.

Loosely defined, the field of social impact investing can be assumed to have been in operation for some three to four decades. However, a sustained effort to create an institutional framework that would support the creation of standardized impact investing products began only with the advent of the various social impact investment task forces set up in the UK after 2000 and the launch of the first Social Impact Bond in 2010 (Social Finance, 2016; Young Foundation, 2011). It is thus the decade around the year 2010 that many organizations got involved in building the socio-material infrastructure for social impact investment and delineating this field from mainstream investing or from cognate fields such as socially responsible investing. This paper will therefore look at reports issued around this time (2005–2015) where the recommendations regarding the process of defining, measuring, and reporting social value creation are laid out. The approach adopted for analyzing the reports entails attempting to delineate a unified picture of how social impact is supposed to be gauged, using, where necessary, an abductive reasoning approach which accounts for intriguing findings and then reflects them back onto the existing scholarship and systematically reviewed documentation to check for reliability and logical consistency (Morse et al., 2016). The choice of organizations was based on their relative weight in the construction of the market, as visible in the number of citations and cross-references their reports accrued in various other sources describing the functioning of the market for social impact investment, including policy documents, third-sector evaluations, news pieces, secondary literature, and within the reports themselves. In total, seven organizations have been identified as crucial in the development of the impact investing. 1 While in some instances these entities collaborated in delineating the field of impact investing, at other times they operated independently of one another or even acted as regulatory competitors (Kurunmäki & Miller, 2011). Either way, for the purpose of this paper they will be treated as being part of the same epistemic community which determines the paradigmatic organization of this field. The choice of these organizations does not imply that they are solely responsible for the birth of the social impact sector as an institutionalized field. However, their reports paint a consistent picture of the inputs that are required in impact evaluations and should be indicative of the implications these have on the process of financializing the social sector.

The paper continues as follows: the section (Impact) Accounting technologies as social processes places the issue of (social impact) valuation in its social context and discusses how the social processes underpinning it can disclose important insights regarding the mechanisms behind financialization. The section Contextualizing social impact investing provides a background to the notion of “social impact,” while the section Defining and measuring social impact looks at how high-level organizations in the industry went about institutionalizing this field. This is followed by the section Discussion exploring the implications of the analysis, and a final part which concludes, emphasizing the porous nature of impact assessment and calculation at the heart of social finance and stressing how social impact accounting practices can be a double-edged sword for financialization processes.

(Impact) accounting technologies as social processes

In the field of impact investing, there are various accounting tools that measure social value creation. But social value cannot simply be presumed; rather, it is the result of a valuation process. During the past couple of decades, the issue of valuation as a social process emerged anew as a topical subject-matter central to the understanding of the construction and functioning of markets of all sorts (Helgesson and Kjellberg, 2013; Stark, 2011). It has been emphasized in various ways how markets and money mobilize a complex social structure that goes beyond the isolated spaces of the production site or the individual consumer and how this process involves, crucially, various systems of worth, evaluation, counting, ranking, rating etc. that constitute the plumbing of markets and are part and parcel of its pragmatics. This is to a certain degree in contradistinction with an understanding of value as “the way people represent the importance of their own actions to themselves” (Graeber, 2001: 45), emphasizing rather the (supra)structural and interactive or conflictual nature of valuation processes, particularly as it relates to attempts to shoehorn value multiplicity into narrow understandings, for example, financial value.

This is reflected also in accounting practices, which mirror social relationships (Hopwood, 1974), and are often “used to articulate and promote particular interested positions and values” (Burchell et al., 1980: 17). The valuation process is an arena for political battles and claims to expertise and jurisdiction, and the resulting accounting system expresses the resolution of these social entanglements. Value added accounting, for instance, was the expression of the need to re-envisage the nature of the firm as a cooperative endeavor where concerted efforts benefited a wider range of stakeholders (Burchell et al., 1985). But the fact that it ended up being only a short-lived initiative suggests that accounting systems are far from constituting stable objects, and that as easily as new ones arise, equally easy can they be undone. This essential “plasticity” of accounting valuation (Mennicken and Power, 2015) means that value is a “contested and provisional judgment” (Carruthers and Kim, 2011: 253) subject to fragile and shifting social relations which lie behind metrics and quantified information. Given these dynamics, it is worth asking: if there are various social constellations underpinning particular accounting systems, which one is the one lying behind social impact accounting and what does this tell us about the financialization process?

In the field of social finance, the valuation process occurs at two levels: at the level of the service delivery, as part of every social impact program, and, initially, at the level of the market promoters, as part of the institutionalization of the impact market itself. It is the market promoters—in this case, the organizations identified above—that define the conditions of possibility or the playing field where impact programs will unfold. They are the ones that recognized, defined, and negotiated the rules of the game in an environment of “value complexity” (Barman, 2015). A financialization of valuation narrative would suggest that this tension is resolved through the seizing of the social by financial valuation processes (Chiapello, 2014; Martin et al., 2008). However, this is not the only way to resolve the issue of hostile worlds. In some cases, such as accounting control in aircraft production, a process of hybridization occurs between imperatives of economization and technological performance standards (Harrigan, 2014). Blended value, as the interaction between social and financial value creation, is a contender for hybridization events. On the other hand, as in the medical profession in the UK which has generally operated as a “professional enclosure,” the issue of value complexity has not been resolved, but has resulted in preserving competing accounting demands between medical expertise and accounting management practices (Kurunmäki and Miller, 2008). Blended value is, yet again, a contender for being a channel for the preservation of competing demands. As this paper will argue, what actually occurs in the field of social finance is somewhere in the middle, with stakeholders from across the financial and social divide deciding on the make-up of social impact valuation processes, but also with financial values kept flatly separate.

Contextualizing social impact investing

Initially, impact investment was not a self-explanatory investment class for financial actors to simply come in and buy into it. It was unclear what the notion of “impact” even referred to. A survey of major investors in the market found in 2012 that a fifth of investors had already engaged in one form or another with impact investing before 1995 (GIIN 7 January 2013 et al., 2013). That said, the results were not conclusive: one of the main issues was that what exactly “impact” was meant to capture was opaque. Indeed, impact investing was placed by some on the same plane with similar concepts such as socially responsible investing (SRI), ethical banking, corporate social responsibility, or even Islamic finance.

SRI and social impact investing do share the imperative of being mission-driven as a common denominator. All forms of responsible investment, by utilizing negative screening, essentially promote some sort of value, be it at the very least economic (in the guise of employment) or moral (through stigmatization and avoidance). However, what really set impact investing apart from SRI was that while the latter does possess some tools for measuring standards of investment, these are generally secondary and remain underdeveloped. From the outset, social impact investing had as its goal the delineation of social value creation as an intentional and evidential objective. Thus, it had to actively engage with two aspects: the social dimension of investment and the elaboration of appropriate tools or metrics for measuring the impact on that social dimension. It therefore stressed non-financial returns not only as a filter through which illegitimate, noxious investments can be sifted out, but also as an investment rationale and essential factor through to financial return would be connected.

Social impact investing is also linked to venture philanthropy, popularized by the nouveaux riches of Silicon Valley (Abélès, 2002), as well as social entrepreneurship and social innovation (Nicholls and Murdock, 2012). These latter practices were closely connected through the idea that activities that strive to bring about social change were grossly inefficient and stood to learn a few things from the gradual but constant improvements that entrepreneurship had benefitted from during the past decades. Successful entrepreneurs, driven by the imperative of efficiency quantified in monetary returns, could make for useful models in the field of social intervention. Last, impact investing also benefitted from a host of financial innovations such as securitization, equity-type investments, credit enhancements, crowd sourcing, and social impact bonds, as well as a plethora of new institutions such as capital aggregators, secondary markets, social stock exchanges, venture philanthropy organizations, online portals, conversion foundations, or funding collaboratives (Salamon, 2014). These instruments allowed organizations engaging in social programs to tap into the vast pools of global capital markets and magnify their limited resources (traditionally, operating income) by leveraging from institutions such as pension funds, mutual funds, investment banks, insurance companies, or from the savings of high-net-worth individuals.

Defining and measuring social impact

Impact investing emerged thus against the backdrop of all these developments. But the first obstacle that needed to be tackled was the lack of consensus regarding the meaning of “impact.” As mentioned above, within the sister practice of SRI, the social dimension of impact was considerably underdeveloped, and the notion of utilizing metrics to measure impact was, with some exceptions, virtually absent (Fiestas et al., 2010). Even within microfinance, a practice that also strove to foster capital market funding for social or developmental programs, the social dimension was generally underspecified. Fenton notes, for instance, that “of all the metrics listed on mixmarket.org—the main resource for Micro Financial Institutions (MFI) data—none directly, if at all, indicate social performance or attempt to measure impacts on poverty” (2010).

But the notion of “impact” as used in impact investment was meant to go beyond this and was supposed to be coeval with the practice of measuring said impact. However, it was laden with ambiguity. Many organizations that utilized and promoted the notion of impact investment (e.g., The Global Impact Investment Network (GIIN), The European Venture Philanthropy Association (EVPA), The International Association for Impact Assessment (IAIA), JPMorgan) still did not always employ a common or strict understanding of what it is exactly that impact entails. For instance, IAIA, one of the most prominent non-profits developing standards and principles for impact assessment, initially defined impact as “the difference between what would happen with the action and what would happen without it,” and the procedure of assessing impact as “the process of identifying the future consequences of a current or proposed action” (IAIA, 2009). In a more analytical vein, the innovation charity NESTA qualified the notion of impact by distinguishing it from output and outcome: “impact” would thus be the effect on outcomes attributable to the output (2012: 5). On the other hand, when looking specifically at the kinds of concrete outcomes that may form part of successful interventions, these were understood as “changes” to one or more of the following: people’s way of life; their culture; their community; their political systems; their environment; their health and wellbeing; their personal and property rights; their fears and aspirations (IAIA, 2003: 8). As much as a definition of the foundational notion of “impact” was slowly being teased out, due to its persisting ambiguity its operationalization in particular impact programs remained elusive. This was further compounded by the difficulty of assigning attribution to a designated action: how could one be sure that an outcome was the direct result of an intervention and not of some other, unrelated social dynamic (EVPA, 2013)?

Social impact programs thus took place in a complex social arena where causalities were hard to pinpoint. At the very least, EVPA recommended to potential venture philanthropists to calculate the outcomes of their investments while acknowledging (and where possible adjusting for) where other programs could have contributed (e.g. the effect of the welfare state in developed countries) or where there may be negative effects, i.e. those factors that increase or decrease impact (2013: 46–47).

In other words, impact assessment had to adequately account for all these aspects: agency (is there some identifiable agent to whom the impact can be attributed?), time (how does the impact develop over time?), space (how are other entities outside the scope of the intervention affected by it?) etc. This was a tall order, and rather than becoming a rigorous process governed by clear conventions, often a rule of thumb was an acceptable practice for delineating what counts in impact assessment. But most importantly, it pointed to the fact that social impact programs were highly specific and singular undertakings that had to be accounted for by appealing to their own, localized context, and not to general formulae. And in particular, it was the stakeholders involved in the impact programs that were perceived as being best located to “resolve” the ambiguity of impact and define the scope of a program should have.

Negotiating social outcomes

Industry promoters envisaged social impact creation as taking place not only in a highly specific and localized context, but also in a negotiated manner. Alongside social finance professionals, stakeholders—the target population specifically—would be invited to voice their concerns and decide what impact should be. This was evidenced in the way the G8 Social Impact Investment Task Force (SIITF) 2 explained the process of impact measurement. In one of its subject papers, it divides the typical measurement process in four general phases, each with its own specific activity: Plan, Do, Assess, and Review (SIITF, 2014). The negotiated nature of this procedure seeps through its guidelines.

The “Plan” phase is the most dynamic and contestable of all the phases. As such, it requires investors and investees to agree upon two aspects: the impact to be achieved and the instruments to evidence it (metrics). The articulation of the specific impact sought requires the joint elaboration of an investment thesis or a “Theory of Value Creation” (ToVC) in order to “form the basis of strategic planning and ongoing decision making and to serve as a reference point for investment performance” (SIITF, 2014: 8). There are no set criteria for establishing what counts in value creation; this is left to parties involved to decide. The desired impact will thus form the reference point upon which the entire project will reflect back. The choice of impact metrics, also part of the Plan phase, as described by SIITF, is similarly open to negotiation between stakeholders, and it can involve either a choice of a measurement framework from the myriad of already existing frameworks, or the elaboration of a new one, tailor-made to suit the circumstances of the project at hand. The second phase, “Do,” includes the gathering of data together with its validation. As such, it involves the mobilization of processes for making sure that the streams of data collected flow from investees to investors in a transparent and organized manner, as well as the review of the collection of data to assess, by cross-checking calculations and assumptions, whether data is gathered in a complete and accurate fashion. Like the first phase, it is also meant to involve communication, negotiation, and contestation between the parties involved. In the third phase, “Assess,” the data gathered is reviewed and analyzed with an eye for understanding and assessing to what extent the quality, scope, and depth of the impact is on track with the desired goal. Last, the “Review” phase involves reporting data and making strategic management decisions.

Two aspects can be inferred from this description of how a typical impact assessment should unfold: first, the progress of the investment project is shared with a variety of stakeholders to inform their decisions regarding the effectiveness of the project; second, and importantly, feedback from these stakeholders is taken into account both at the outset and throughout, with the purpose of delivering and integrating recommendations regarding the appropriateness of the ToVC established at the beginning and the extent to which this is mirrored in the project itself. The phases of the impact measurement process are, therefore, dynamic and flexible, something that is acknowledged by SIITF itself: performance measurement processes and the outputs of each step will interact and evolve continuously. The sequence, frequency and timing of each activity will also vary. Implementation of these guidelines will be unique to every organization, as they are likely to have their own measurement goals, resource constraints and stakeholders to consider (2014: 8).

The social impact sought, therefore, results from a negotiated process that includes various stakeholders’ voices, who thus interact with the service deliverers and funders. Debating where to draw the lines between the scope of a particular social investment project and what should lie outside it is, consequently, conceived as an elastic process that allows room for contestation and change.

Choosing social metrics

As part of the elaboration of a specific approach to social value creation, the parties to the contract are required to agree on the metrics employed in the social impact program. To the social investor, this is what matters most: the long-term measurable net social change that can be attributed to the service operator’s designated program scope. This is the case, of course, because the data regarding social return is correlated contractually to a specific degree of financial return accruing to investors. Impact metrics, thus, as far as the investors are concerned, are the bedrock of social investment. But the role of the target population is central in this case too.

A few industry-driven initiatives stand out in this regard. An early one is The Global Reporting Initiative (GRI), established in 1997 with the mandate to help businesses and governments apprehend and report the impact their actions have on sustainability issues. Similarly, the Global Impact Investing Network (GIIN) was conceived in 2007 with the remit of building critical infrastructure and supporting the expansion of a coherent and consistent impact investing industry. Around the same time, the Rockefeller Foundation became a central player who marshalled resources in order to establish impact investing as both a socially-oriented financial practice and a properly functioning market for international investors who sought to create not merely financial returns but “blended value” (Emerson, 2003).

In a 2009 report, for instance, the Monitor Institute (funded by the Rockefeller Foundation) identified as the biggest concern of investors precisely the nebulousness of the notion of social impact and the inability of financial valuation instruments to provide an appropriate representation and estimate of the latter (Monitor Institute, 2009). There was a perceived need for basic market instruments like the ones available for commercial investors, such as GAAP, Moody’s, or portfolio management tools, but these were deemed unsuitable for the nature of value encountered in social finance (Brandenburg, 2012). Therefore, a parallel market infrastructure needed to be constructed, structured around calculative tools specifically designed for the valuation of social impact, and with local stakeholders as their central input-providers.

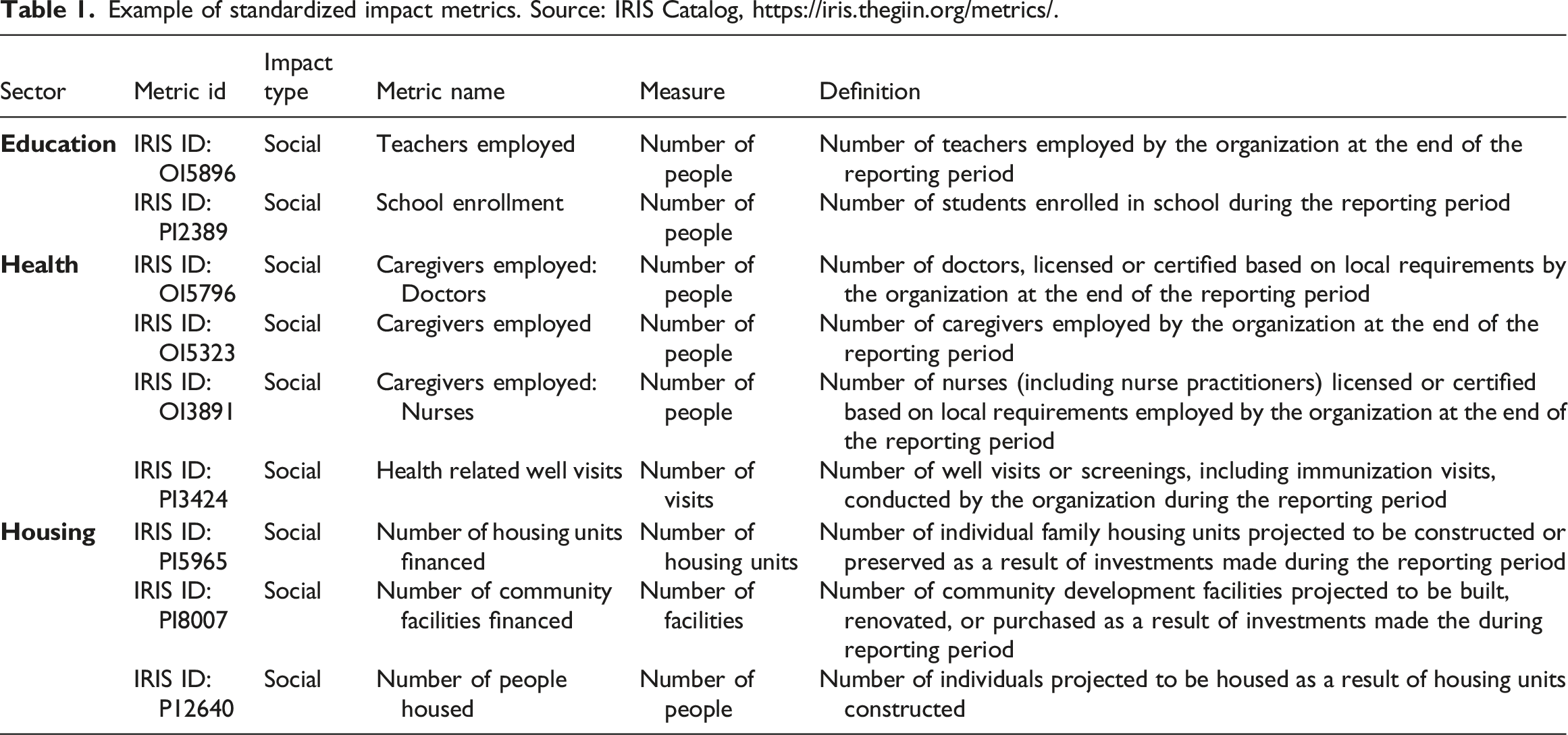

Example of standardized impact metrics. Source: IRIS Catalog, https://iris.thegiin.org/metrics/.

The second tool essential to the valuation infrastructure was GIIRS, a ranking system that was meant to evaluate and rate investment opportunities across the social finance spectrum according to the impact social enterprises created (GIIRS, 2010). Like credit rating agencies such as Moody’s or S&P’s, GIIRS provides arms-length judgments on the performance of social enterprises, which are evaluated and then ranked based on a specific scoreboard. 3 GIIRS, however, is unlike IRIS in that it reduced the plurality of meaning to a few common denominators constituting the building blocks of the rating system: governance policies, status and treatment of employees, policy toward the environment, policy toward the community and goods and services provided (GIIRS, 2010). These dimensions were believed to be flexible and encompassing enough in themselves to allow for multiple paths to impact. In other words, behind categorization still lied the multiplicity and specificity of local social value creation.

What this essentially means is that, incentivized by industry regulators, a large spectrum of metrics is now available for use in social impact programs. And what is interesting about these metrics is not only that they measure different forms of values being created, but that some metrics measure the same values but make different epistemological assumptions regarding those values and allow a different degree of stakeholder integration. Indeed, the metric frameworks present in the field of social finance can be divided into three different categories: positivist, critical, or interpretive (Nicholls et al., 2015). These categories can be perceived as a spectrum ranging from more technocratic (emphasizing expert knowledge as a road to outcome legitimacy) to more participative (emphasizing stakeholder and target population as important actors in outcome legitimacy), which thus permits stakeholder voice to be integrated to a higher or lower degree. The positivist view assumes that the act of measuring captures and represents the experiential social reality without other hindrances beside the extent and complexity of the reality it must grasp. Impact is produced in a linear manner, stemming from a series of inputs to a series of outputs and eventually outcomes. The mechanics behind the link between inputs and outputs is one of simple causality, based on a stripped-down logic of “if…, then…” (SIITF, 2014). The evaluator endeavors to establish or uncover positivistic relationships between inputs and outputs, and devises the most efficient strategies for collecting the data required to establish if the impact project is on track to achieving its target. These can range from participatory observation and interviews to surveys and official statistics, but what is important is that the final outcome turns on the interpretation of the expert-evaluator and is filtered through their expertise. Under this category one can find methods as varied as: cost–benefit analyses; experimental methods of choice modeling (e.g., Randomized Control Trials); or behavioral models (e.g., stated preferences—asking people how much an outcome is worth to them, or revealed preferences—examining past choices to infer how much various options are worth to people).

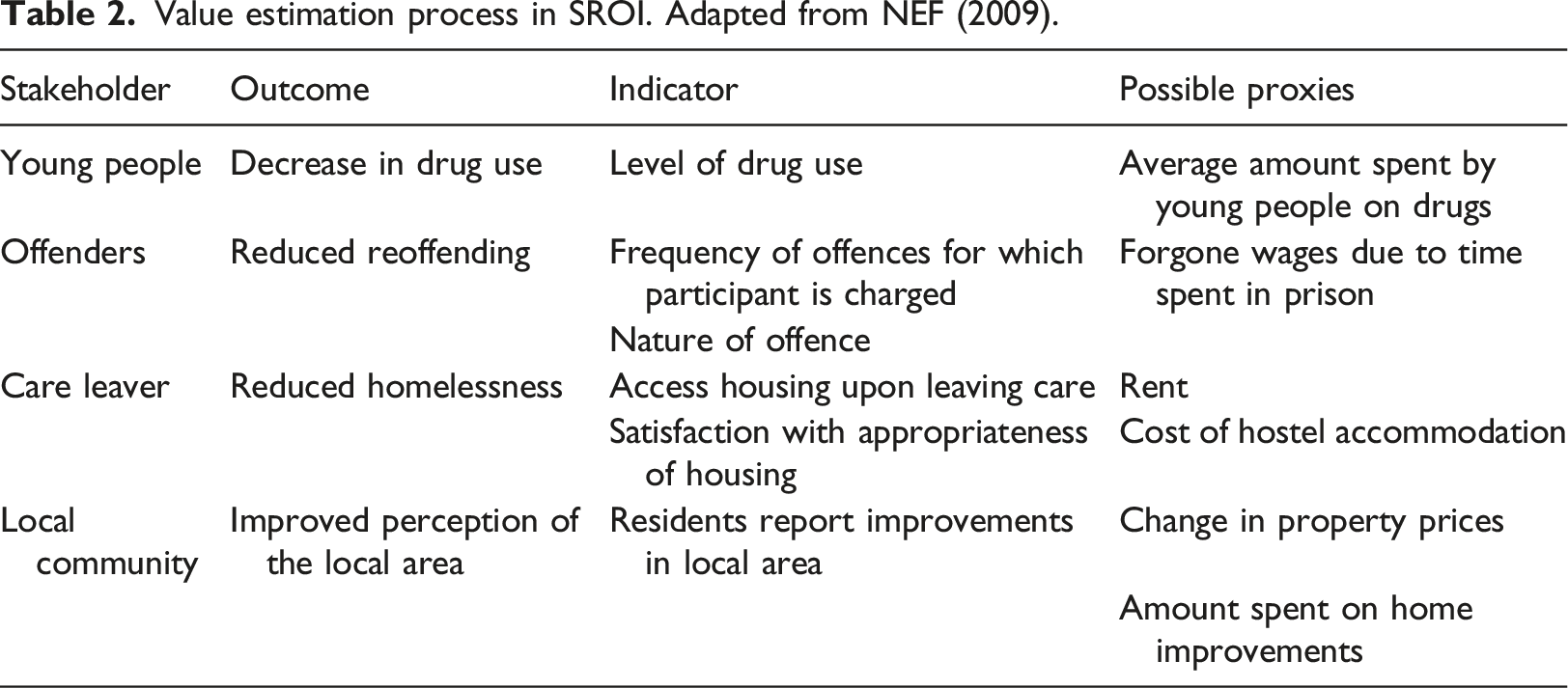

Value estimation process in SROI. Adapted from NEF (2009).

Other methods that fall under this heading are “strategy approaches” with metrics such as balanced scorecards and strategy maps, or dashboards (Kaplan and Norton, 1996). Balanced scorecards were initially conceived as a counterbalance to the dominance of financial concerns at the top, and were meant to reinforce or “assail” performance interpretation with data from the ground (Nicholls et al., 2015). Similarly, dashboards provide a wide-ranging view of performance data from disparate sources. All in all, critical approaches highlight the foundational power relations that lie at the core of impact assessment and attempt to overcome it through, mainly, participatory methods and a more holistic approach to stakeholder inputs. Some accounts, for instance, describe SROI even as a “new rationality that can offer emancipation via new forms of communicative action” (Nicholls, 2018). The target population’s inputs play a central role in these approaches.

Lastly, the third metric framework is the interpretive one. This approach abandons the assumption of power relationships but takes the participative drive even further, integrating stakeholder involvement at an even earlier stage in the process, but also throughout. As such, it privileges communication and debate among concerned parties with regards to the goals of the project, the nature of the intended value creation, its extent, as well as the best way to grasp and represent it. This way, the grassroots participants can aid both in designing the intervention and constructing the appropriate metrics for accounting for it. At the same time, given ongoing stakeholder participation, this means that the metrics associated with this framework also create feedback loops that can validate or contest the accuracy of the data being reported, or indeed create another layer of impact simply through this involvement (Nicholls et al., 2015). The Outcomes Star model is one such example. It is a metric framework that maps desired outcomes in a star-shaped form with degrees of attainment (e.g., from 1 to 10) on each branch of the star. There are various iterations of the Outcomes Star model suited to the specific sector of which the impact program is part, but the mechanism behind it is the same: both the service deliverer and the service user (the beneficiary) plot how the latter is doing on their way to the stated goals. This is done in a collaborative manner, through the worker and the user deliberating and identifying together the step where the user is on the outcome ladder, at various times throughout the project (every three, six, or 12 months, depending on the project length) and by assigning a numerical score through which the tracking is made easier and more recordable (MacKeith, 2009). The data can then be used not only for tracking or measuring the outcome achieved by the entire project, but also for benchmarking it with national or international averages or even modifying the strategy for achieving impact along the way. All in all, regardless of their variations in form, these frameworks for impact assessment emphasize grassroots stakeholder priority, engagement, and collaboration. Seeing the beneficiary’s judgment of the service as the ultimate source of legitimate knowledge, they attempt to extract as much data as possible from this level.

There is certainly no lack of metrics and methodologies for quantifying the amount of impact a specific project has on a target population. But impact assessment, as prescribed by the regulatory entities operating in the field of social impact investing, transpires as a flexible process that is not beholden to rules as strict as for instance financial reporting would be. Indeed, there are no precise guidelines as to what “impact” means, and in most instances this ambiguity is meant to be resolved through what can be called discretionary action: stakeholders can decide which metric or framework to utilize based on their unique circumstances—indeed, they can pick from the available ones or they can fashion their own. Furthermore, when it comes to the metrics themselves, what has been prescribed by industry regulators was not a narrowing down or standardization of the diversity of metric frameworks, but rather an acceptance of their heterogeneity and in some cases malleability. And even though there are frameworks that are more inflexible or “technocratic,” by and large the metrics that have emerged endogenously are characterized by a significant amount of plasticity and are to a great degree participative.

Discussion

There is much enthusiasm surrounding social impact investing, and many of the organizations operating in this field see it as being on track to delivering a genuine new asset class for financial actors to invest in (US SIF, 2018). Nevertheless, the institutionalization of the field has not necessarily followed the typical route of providing clear prescriptions for how data should be collected, measured, and reported. On the contrary, the process has unfolded differently: industry-led regulatory processes have resulted in the prescription of a particular leeway given to service deliverers often in conjunction with the target population of the social program initiated and even the investors involved regarding how the process of impact assessment should take place. In other words, what they prescribed were distinct spaces of valuation where local negotiation and discretionary action are required for resolving the inherent ambiguity present in the notion of “impact creation” and for deciding upon an appropriate metric from the panoply of metrics and metric frameworks that already exist (or fashioning novel ones if it is deemed the impact program so requires). This and not exogenous financial forms of valuation is what constitutes the bread and butter of the social impact investment field and what financial actors must contend with.

Various perspectives have thus been outlined to understand financialization and the growing role of finance in contemporary society (Van der Zwan, 2014; Nölke et al., 2013; Engelen, 2008). Because of this polysemy, Christophers (2015: 196) has gone so far as to question the usefulness of the notion of “financialization,” suggesting that “it remains unclear what financialization “is” and, relatedly, how it can most productively be conceptualized and analyzed.” The approach adopted here, however, sought to look specifically at the valuation processes sustaining the expansion of finance and the role of financial actors in the elaboration and choice of impact metrics. This mechanism has sometimes been understood in a unidirectional manner, with financial actors simply capturing valuation processes occurring in non-financial realms and dictating the terms of engagement. The perspective sketched here, however, reinforces the view that in cases of value plurality, there are boundaries beyond which financial terms do not travel. This is the case because what can be encountered in social finance is a proliferation of endogenous methods and metrics, which are tasked with grasping and accounting for social value creation as distinctly separate—though not independent—from financial value creation. This unfolds to a degree in a shielded manner, with stakeholders playing a much bigger role—depending on the accounting framework chosen—in the valuation process. Financialization, in this case, provides the impetus for the creation and safeguarding of limiting spaces which the financial actors and financial imagery cannot easily access. In this sense, the notion of financialization is embraced as useful, at least insofar as it can disclose limits to how far along finance can travel into the social.

Several observations can further be made regarding the proliferation of non-financial spaces as a result of the financialization of social policy. First, the process of valuation of impact investment projects, as indicated by industry regulators, is meant to be distinct and specific: it is supposed to rely on a particular understanding of how social change happens in society. The Theory of Value Creation (ToVC), for instance, is meant to be decided upon mostly at the level of the service providers or social enterprises, and less so at the level of the financial organization providing capital. ToVC, furthermore, relies often on subjective inputs and inter-subjective collaboration mechanisms and consensus building at the level of the social enterprise. This latter point would not be very different from, say, a regular decision-making process regarding allocation of capital at a regular investment bank, were it not for the fact that social enterprises cannot cash in on so-called “hard economic data” like mainstream banks, and must rely on more elusive notions and deeply held beliefs regarding “the social” and its dynamics. It is at this exploratory level that local negotiation is expected to occur in order to decide upon the scope and meaning of social value creation, which will ultimately be tied to financial return calculations.

Second, the process of gathering performance data about impact is similarly envisaged to be reliant upon a specific degree of discretionary action, with inputs in this regard coming from across the stakeholder board. As illustrated above, the creation of a metric repository, IRIS, did not reduce the multiplicity of metrics and metric frameworks, and there are similarly no clear guidelines as to who should be involved in reporting impact data and which metric is required in which context. There are thus more participative metrics that are more prone to the beneficiaries’ voices or indeed biases, and more technocratic ones that are more amenable sometimes to adventurous quantitative reporting. Regardless, the crux of the matter is that inputs about the impact that is tied to the financial rewards the social investors reap come from various actors, be they beneficiaries, service providers, NGOs involved, or public agencies. This negotiated nature of impact reporting makes the valuation process much more socially dynamic and unique in its various guises, as well as amenable to contestation. Valuation of impact interventions can be, as a result, a quasi-political endeavor implicating various actors and multi-faceted power struggles. In this respect, the social dynamics underpinning accounting for social values are closer to those that the short-lived value added accounting was trying to capture (Burchell et al., 1985), even though the latter was still meant to be the trade of expert accountants and was therefore much more technocratic than participative. Social impact accounting tries to capture value added to stakeholders, but only whilst considering it to a great extent on the terms of those stakeholders.

Third, much has been made of the issue of attempting to reconcile the “hostile worlds” of financial versus social value (Zelizer, 2000). In the healthcare domain, for instance, there has been a persistent reluctance to mix the particular knowledge-sets of the various actors involved and competing accounting guidelines regarding value creation have been imposed by various regulatory agencies (Kurunmäki and Miller, 2008). On the contrary, in the field of social impact investing, resting on the notion of blended value as conceived by the industry itself, a degree of negotiability and hybridization was baked in that allowed financial returns to accrue according to the amount of social value created but independent of the epistemological framework adopted by stakeholders as to the nature of social value. This was perceived to be the most efficient avenue for resolving the issue of hostile worlds. By allowing stakeholders to participate in the social value measuring process on their own terms, in their own understanding and perception, then this could at once make the project more efficient, provide a more encompassing narrative and account of social value creation, and lead to perhaps a higher degree of financial return.

Fourth, what became the strength of this sector—its proclivity for malleability and inclusiveness—could also prevent it from achieving its stated aim: becoming a legitimate asset class. While industry regulators set up entities like IRIS and GIIRS to ensure commensuration and comparability for investors to make informed decisions, these entities still do not operate like their homologous institutions (say GAAP and S&Ps). For instance, the quest for institutionalizing and standardizing metrics, which has been the main mission of a platform such as IRIS, has been met not with a reduction in the multiplicity of approaches of quantifying impact, but with an explosion of different metric frameworks and indicators. While the response of IRIS and similar initiatives has been to sanction each reliable metric, the very specificity of each intervention meant that more and more service providers have constructed their own metric systems which they have reported or not to be catalogued alongside the others.

This implies that, in theory, a comprehensive register of indicators is conceivable, though impractical. The continued existence and creation of proprietary metrics means that the process of valuation of specific social impact progress will be subject to the various needs and goals of particular organizations and target populations. If the valuation process lying behind social impact accounting practices will indeed remain as “liberal” as indicated by the high-level organizations supporting the expansion of this field, then it is perhaps harder to envisage the process of financialization taking hold as deeply as it has in other fields like housing or education. If, on the other hand, the valuation process becomes a battleground where stakeholders compete to have their own epistemic position prevail, then this might open the possibility for regressive outcomes due to power asymmetries and narrower or tendentious understandings of value(s). This certainly seems to be the case in some social finance projects, as Cohen and Rosenman (2020) point out when analyzing how social values were reshaped to fit the needs of financial actors in public schooling and affordable housing programs across multiple US sites. Other metrics employed in social finance projects “on the ground” have also been evaluated as refashioning, for instance, the target population according to the neoliberal precepts espoused by service providers (Cooper et al., 2016) or indeed by the states that promote social finance projects (Berndt and Wirth, 2018). But even so, as outlined above, there is nothing inherent in the design of impact investing programs that would prevent, at the same time, an opening for a wider variety of stakeholders to feed back their own experiences and aspirations, as many of the social valuation processes constructed so far are intended to be negotiable. A specific degree of socialization of finance and multi-stakeholder relationality is thus inscribed in impact investing through malleable impact accounting infrastructures, albeit it sometimes results in social value being defined on the terms of the more “persuasive” actors involved in the programs.

Conclusion

As the UnitingCare example in Australia suggests, accounting for social value creation in the impact investing sector is a more exploratory process that allows room for stakeholder intervention and negotiation. While in that case the accounting black box was opened as the program was unfolding, in other cases this might occur at the design stage. This paper has sought to examine these processes in the emerging field of impact investment, particularly by looking at the way industry regulators attempted to institutionalize it in the context of the financialization of social policy. By analyzing how the impact assessment process was prescribed by these organizations, it has tried to show that social impact valuation was understood as a mechanism resting on specific endogenous social dynamics that deal with the meaning and scope of “social value creation” and undertake localized negotiation and discretionary action when it comes to social accounting frameworks, and do not necessarily rely on exogenous types of valuation. Thus, it is still social impact accounting practices that facilitate the process of financialization, but only via the creation of non-financial forms or spaces of valuation. Furthermore, it appears that in as much as we can talk of a process of financializing the social, so can we detect the obverse: that impact investing re-socializes finance and to an extent shields social value from some of the deleterious consequences of financialization. This should come as no surprise, given that one of the foundational aspects of social impact investing is that of resolving the issue of “hostile worlds”—accumulating financial returns at the same time as creating social value. How this is accomplished, though, is through the creation of a particular form of valuation that underpins the impact measurement process. This way, more leeway is prescribed to stakeholders to interact, negotiate, and ultimately decide upon what social value creation should be and how data should be collected, measured, and reported.

Thus, various meanings and forms of value indeed co-exist in the field of social investment, and actors operating in the field have no qualms in pursuing, to varying degrees, one alongside the other. But “the social” that is safeguarded from financial processes of valuation in impact programs is also one that is open to a wider array of stakeholders, impact investors included. The social values circulating in the social finance field emerge therefore from the dialectical imbrication between, for instance, impact investors, social enterprises, and the target population, and as such the social impact accounting tools that capture them materialize as sites of political battles and negotiations between stakeholders. As the social impact investment sector continues to grow, it is thus important for future research to pay heed to these power dynamics underlying the seemingly objective and reflective social valuation devices in assessing the emancipatory or exploitative potential of social finance.

Footnotes

Acknowledgments

The author is grateful to Andrea Mennicken, Mike Power, Peter Miller, and all the AC500 seminar participants in the Accounting Department at the LSE where two versions of this article were probed. The author would also like to thank Anastasia Nesvetailova, Stefano Pagliari, and Amin Samman, who commented on an earlier draft. The usual disclaimers apply.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the UK Economic and Social Research Council under grant number ES/T008687/1.

Author’s Note

Andrei Guter-Sandu is a Lecturer in International Political Economy at the University of Bath. He works on sustainable finance, central banking, and public governance of grand challenges.