Abstract

While growth in India stayed relatively stable over the last decade, Brazil fell into deep recession and a fundamental political and economic crisis. Why did these two countries, despite their similarities, diverge so massively within only 10 years? Through a paired comparison, this article probes two alternative approaches to capitalist diversity to explain the divergence among two rising economic powers and ‘state capitalisms’. It finds that through the lens of a firm-centred supply-side approach, one largely sees institutional stability in both economies, while a focus on the demand side and respective growth models makes visible fundamental destabilization in Brazil. The fragility of domestic demand, the vulnerability of global economic integration and the erosion of key social coalitions, we contend, are key to unpack the divergence between Brazil and India. This study thereby not only sheds a new light on emerging market capitalism but also discusses further possibilities for the analysis of state capitalism within comparative political economy.

Introduction

Over the past two decades, the rise of large emerging economies has become a highly debated feature in the transformation of the global political economy. The economic dynamism of particularly Brazil, China and India spurred notions of a ‘BRICS’-challenge to the Western economic model of liberal capitalism through forms of state capitalism (Alami and Dixon, 2020; Bremmer, 2009; Kurlantzick, 2016; Musacchio and Lazzarini, 2014; Nölke, 2014). Despite doubts about that challenge’s longevity as well as the stability and coherence of the BRICS as a group (Helleiner and Wang, 2018; Sharma, 2012), observers have also noted a deepening of state capitalist institutions, at least in China (Lardy, 2019), which intensifies tensions in the contemporary global political economy (Samuelson, 2019). Hence, the current conjuncture is framed as a ‘clash of economic systems’ (Crowley, 2019; Kalinowski, 2019) or even a ‘New Cold War’ (Ferguson, 2019). In this ‘chaotic mélange’ (McNally, 2020) of the post-liberal order, the stability of capitalism in emerging economies, its economic performance and institutional trajectories will be a crucial issue for the time to come.

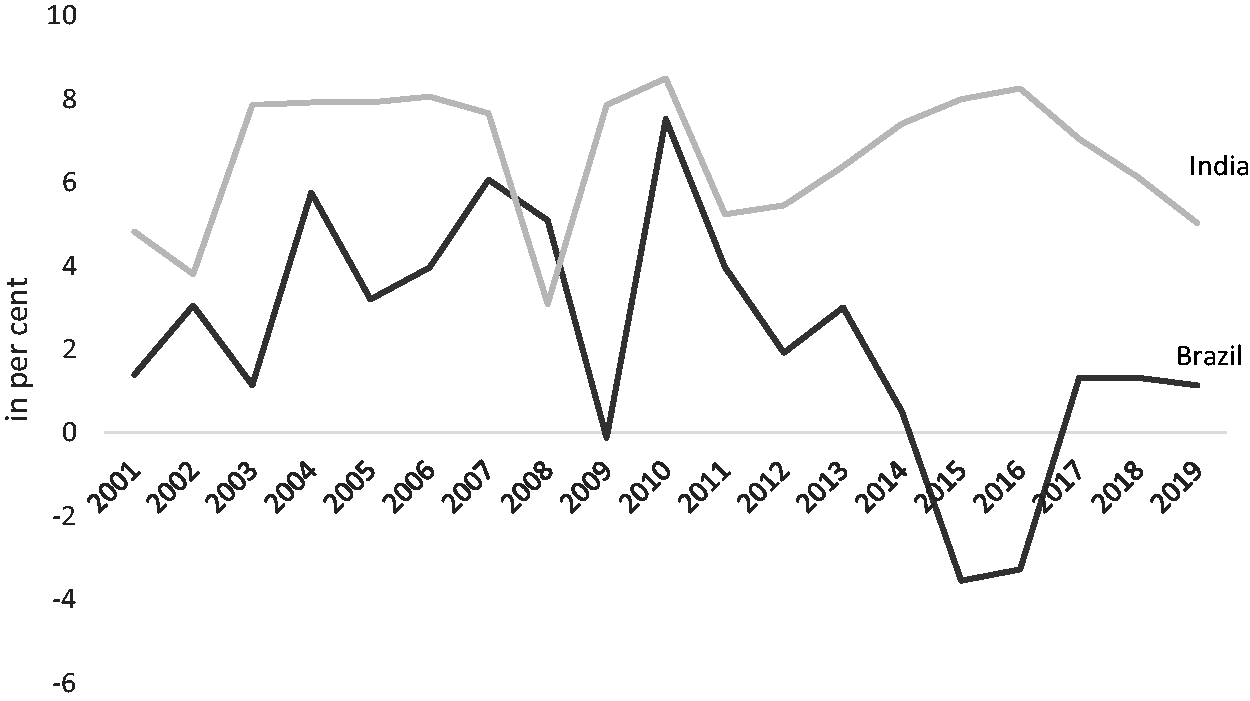

Against this background, we identify a puzzling divergence between two key emerging economies, Brazil and India, in recent years. Substantially, both countries are considered as two of the most democratic emerging capitalist economies, who became two of the ten largest economies globally in the 2000s. Both countries are highly unequal, their economies substantially inward-oriented and with a considerable influence of the state in the national business landscape. Both shifted from a centre-left government in the first decade of the 2000s to a right-wing populist government in the 2010s. However, Brazil encountered the most massive and enduring recession of its history, whereas India only a mild downturn (Figure 1). How can we explain this drift apart?

Annual growth of GDP in Brazil and India, in per cent, 2000–2019.

In order to understand the causes of the fundamental destabilization in Brazil compared to the relative stability in India, we turn to theories of capitalist diversity: the first highlights the role of firms and supply-side institutional domains in the long-term trajectory of capitalist economies and is often associated with the lenses of Varieties of Capitalism or the Business Systems-approach (Hall and Soskice, 2001; Whitley, 1999); the other, mainly associated with the Growth Model Perspective, employs a demand-side, international and macroeconomic focus, from which to analyze more volatile capitalist dynamics (Baccaro and Pontusson, 2016). While providing different explanations for the fate of political economies and their macroeconomic performance, which we aim to test in this article, neither is concerned with seemingly frequent changes induced by government change or with the continued existence of capitalism tout court. Instead, both provide a mid-range perspective on ‘models of capitalism’, which follow specific institutional and political logics.

Such a perspective is fundamentally at odds with existing accounts of the destabilization of emerging economies in general (The Economist, 2020) and of Brazilian capitalism in particular (Prengaman et al., 2017). Usually, commentators have linked the destabilization of emerging market capitalism during the mid-2010s to external factors such as the tapering of quantitative easing policies by the US Federal Reserve, declining revenues from commodity exports and, in the case of Brazil, the Petrobras corruption scandal. Often, they call for deeper economic liberalization and the adoption of Western economic models to avoid future crises (e.g. BBC, 2017; ECB, 2016), although this might induce further instability because it increases economic vulnerability against external pressures (Nölke et al., 2020).

We believe that assessing the divergent fates of two rising economic powers through such a lens contributes to the existing literature in several ways. Whereas we can find many studies comparing the economics and politics of advanced economies (see e.g. Baccaro and Howell, 2017; Beramendi et al., 2015; Soskice and Iversen, 2019; Thelen, 2014), recent comparative studies on the political economies of Brazil and India are scarce. Although research on emerging market capitalism has made great advances during the last years (Fainshmidt et al., 2018; Nölke et al., 2020; Rougier and Combarnous, 2017; Witt et al., 2018; Wood and Schnyder, 2020), the focus so far has been on the identification of (ideal-typical) models of capitalism in the South, but not so much on analysing internal trajectories of change (but see, e.g. Becker, 2013; Zhang and Whitley, 2013). Here, our perspective links up with discussions about institutional change (Mahoney and Thelen, 2010; Streeck and Thelen, 2005), considering the possibility of the destabilization of whole models of capitalism instead of single institutions (Amable, 2017; Streeck, 2009). While advanced capitalist countries are usually strongly institutionalized systems which allow for a high degree of ‘managed' change (e.g. through corporatist arrangements, robust international regime integration and most of all, strong complementary institutions), emerging economies have regularly experienced deep crises and existential erosions of their economic order (Bresser-Pereira, 2009; Ghosh, 2005). Those include frequent debt or liquidity crises that are rare for Western economies but whose remedies are often driven by Western-controlled organizations such as the IMF (Frieden, 2015; Wade, 2001). However, many studies highlighted how liberalization regularly coexisted with statist elements of the ‘old' economic order – particularly in India (Mazumdar, 2014), Brazil (Boschi, 2014) and China (ten Brink, 2019).

Finally, we aim to advance our understanding of the stability and destabilization of what is often referred to as ‘state capitalism’ in emerging economies. Several students of comparative capitalism (CC) have identified this type of capitalism in Asia, Latin America and Africa (Carney and Witt, 2014; Fainshmidt et al., 2018; Nölke et al., 2020; Rougier and Combarnous, 2017; Walter and Zhang, 2012). However, the changing trajectories of state capitalism have so far inspired in-depth country case studies (Amable, 2017; ten Brink, 2019), less so comparative and theory-oriented ones ( but see, e.g. Becker, 2013; Ornston and Vail, 2016; Zhang and Whitley, 2013; on the limits see Alami and Dixon, 2020). Similar to CC studies on advanced economies, liberalization, financialization and transnationalization are identified as major sources of change in capitalism in emerging economies (Fine and Pollen, 2018; Zhang and Whitley, 2013). Yet, state capitalism often remains a descriptive category which has seen it being applied to postwar France (Schmidt, 2003) as much as to contemporary China. Much of the literature on state capitalism uses an eclectic mix of indicators that stand for ‘the state’, ranging from corporate ownership, economic policy or degrees of authoritarianism (see e.g. Sallai and Schnyder, 2020; Wright et al., 2021). However, as Alami and Dixon point out, ‘the CC literature has done a good job at explaining the maintenance or persistence of state capitalism [but] does not say much about its resurgence, renewal and reinvention’ (2020: 78–9), despite the intensive discussion about diversity and change within CC. Hence, the study of state capitalism still lacks a thorough understanding of which elements are crucial in accounting for change. Our analysis aims to contribute to this endeavour by applying two dominant theoretical approaches in CC to two diverging cases of emerging market state capitalism. As we will see, the GMP might be in a good position to include the dynamics of ‘statehood’ into the comparative analysis.

We suggest that the best way of unpacking the divergence is to reflect on these political-economic patterns when testing the two key perspectives on capitalist diversity. Methodologically, we apply a ‘paired’ (Tarrow, 2010) or ‘controlled’ comparison (Slater and Ziblatt, 2013) that allows us to evaluate their respective abilities to explain recent developments in Brazil and India without privileging one approach over the other on the basis of both correlational and process-tracing evidence. Given that this approach is well suited for a theoretically informed combination of variation and control in closely matched cases, we should clarify the basis for our comparison. First of all, both countries share a number of economic and structural similarities which relate to the commonalities of emerging market capitalism. As part of the BRICS group, Brazil and India have gained similar economic and political strength that have given them a status as ‘rising powers’ as well as a position among the ten largest economies globally (Carranza, 2017). Both have earned this position via a trajectory of import-substituting policies, followed by economic liberalization and policies to attract FDI on the grounds of large domestic markets while retaining public control over its economies and the financial sector in particular. Thus, they occupy an intermediate position among emerging economies between the more liberal Mexico or South Korea and the paradigmatic state-dominated economy of China (Armijo and Echeverri-Gent, 2014; Sirohi, 2017). And despite the strong persistence of class and status inequalities, both Brazil and India are considered as two of the most consolidated democracies among developing and emerging countries (Heller, 2019). We believe that these commonalities provide sufficient justification for a mid-range, cross-regional comparative approach. Nonetheless, there are limits to this comparison that do not only stem from different resource endowments, colonial histories as well as population and country size, but also from some contrasting developmental experiences in terms of unemployment and poverty reduction that go beyond our initial puzzle of growth performance. These are important to keep in mind before drawing strong inferences.

In order to employ a comprehensive CC perspective in this comparison, we first investigate the established institutional domains of the supply-side, firm-centred approach such as corporate governance and finance, industrial relations, education and innovation and probe their explanatory power against both qualitative and quantitative data. We then move on to identify the sources of demand and how they relate to the mode of integration into the global economy and the extent of socio-political support to probe the growth model perspective (GMP) analogously. Based on this theory-led approach, our comparison points towards the importance of a broad and stable coalition of national actors in order to organize a successful growth project, of measures to safeguard a stable volume of demand for domestic products and warns against a premature opening towards global financial markets.

Applying the firm-centered, supply-side CC-framework: Same as it ever was?

We refer to a firm-centred, supply-side CC framework that not only contains the VoC program but all approaches that use the distinction of institutional spheres (corporate governance, financial system, industrial relations, education and innovation), institutional complementarities and cross-cutting coordination mechanisms as explanatory concepts. We probe the framework for explaining the drift between Brazil and India by assessing the recent dynamics within its institutional spheres.

Corporate governance and finance

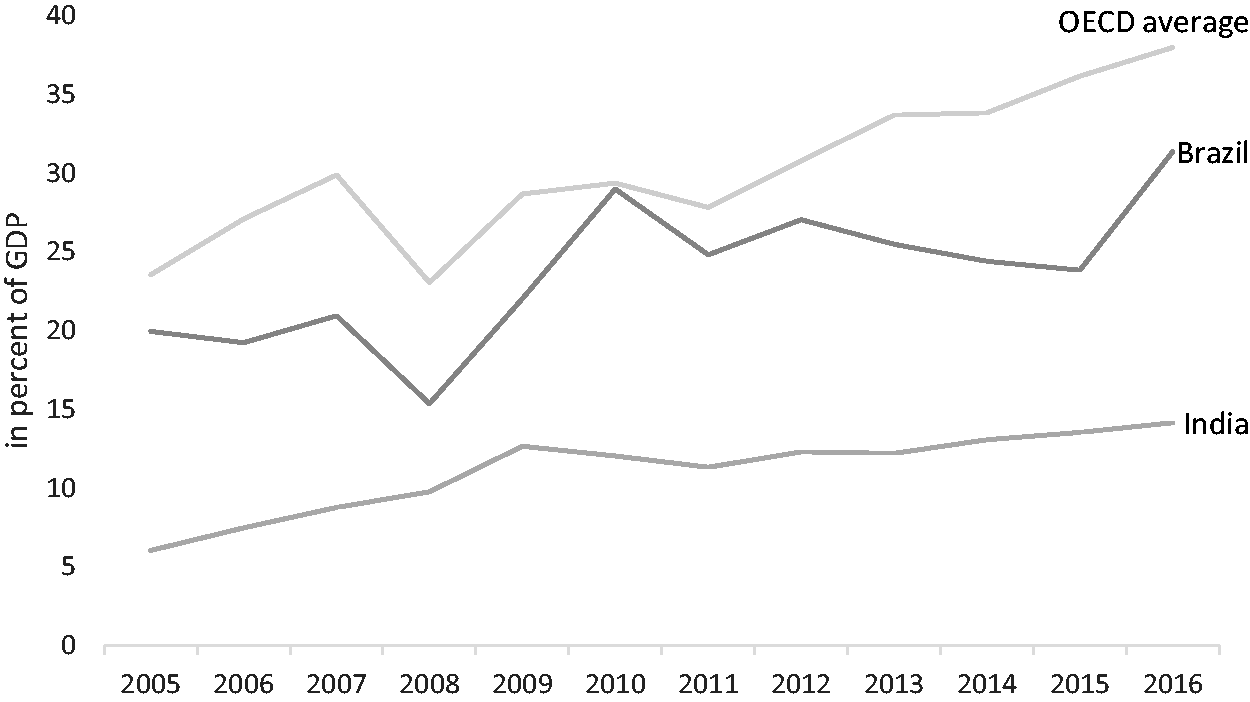

One of the intricate features of Brazilian and Indian capitalism has been a high level of insider control through national capital, enabling long-term investment strategies. This means, corporate ownership is usually concentrated with well-connected families, business groups and the state, mitigating the short termism of global capital markets and dispersed ownership – even though in the past relatively high inflation rates fuelled short-term economic decision-making in both countries. Brazil has also tended to be more open to foreign ownership than India, but continuously below the average of advanced industrial countries (see Figure 5). In the same vein, corporate finance is usually independent from international finance but dominated by internal funds or public bank credit. Hence, there is a strong role for the state for the provision of firm financing, complemented by policies to potentially restrict cross-border financial flows and limit volatility (Allen et al., 2010; Gallagher, 2014).

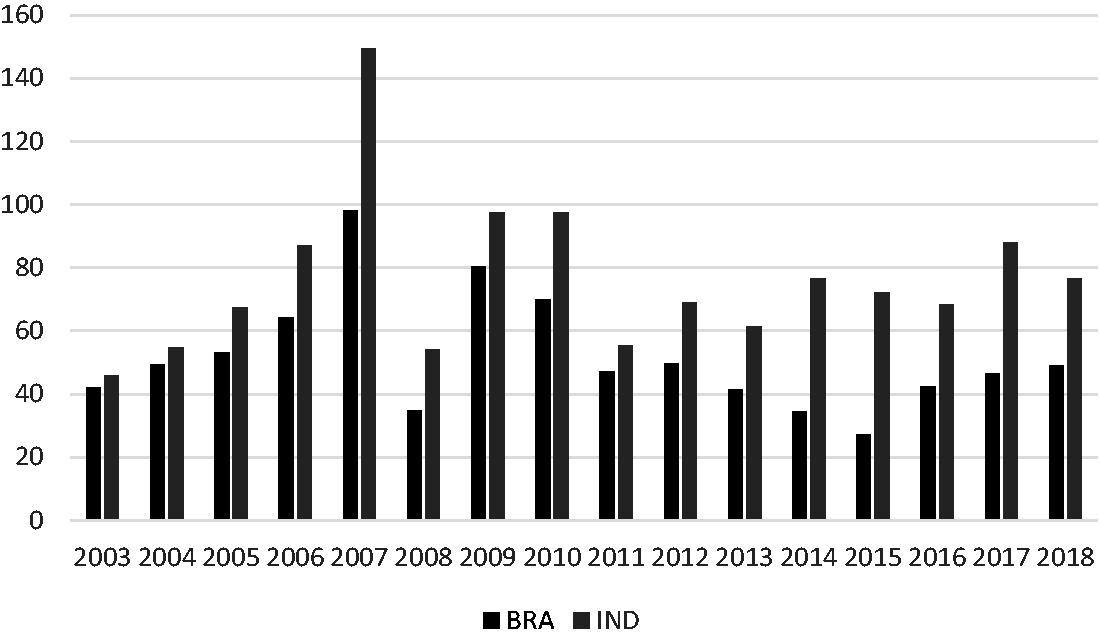

Two factors could indicate for change in these patterns: a loosening of that particular insider control of domestic firms, eventually giving rise to a shareholder value logic and relatedly, to a departure from the closed domestic bank-based system. If corporate control were to become more liberal, we would have to observe a movement towards dispersed ownership and increased market value of domestic firms. Figure 2, however, conveys a different picture: corporate control patterns have remained relatively stable in both Brazil and India. Market capitalization did not increase significantly in Brazil. The overall GDP downturn is actually not an argument against but rather in favour of higher market capitalization: In crises, private firms are usually undervalued and the state tends to sell its shares in firms in the light of fiscal stress. This is not to say that corporate governance reform in both countries was idle, but it remained limited with regard to outcomes. 1

Market capitalization of listed domestic companies (% of GDP).

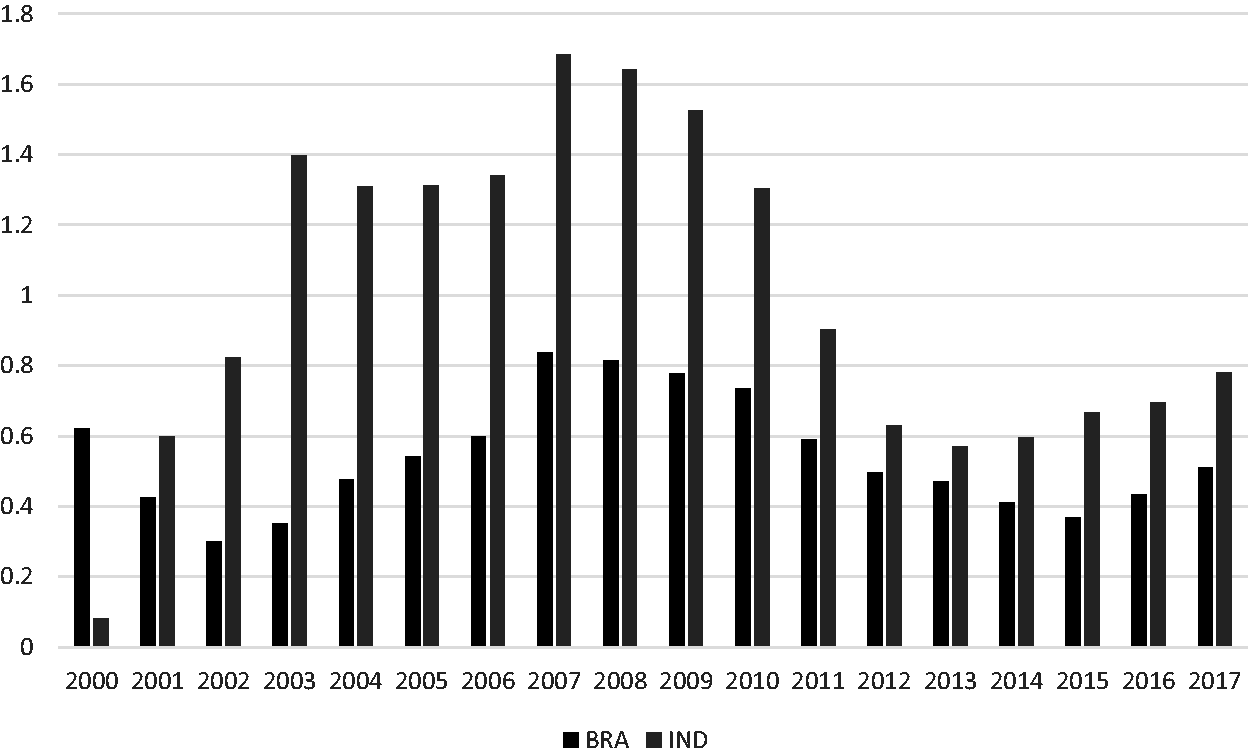

Secondly, has there been an identifiable change from the strong bank-based towards a more market-based system, i.e. have the institutions that support the state capitalist financial system been destabilized? Again, we do not find evidence for this hypothesis. Figure 3 displays the ratio between domestic bank credit and the total value of stocks traded (both in % of GDP). Instead of a shift towards market-based financing – despite some incremental change (see Kaltenbrunner and Painceira, 2018) – we rather see a reinforcement of the traditional bank-based credit system. Thus, the corporate governance and finance landscape seems to be relatively stable even through the years in which Brazil faced a dramatic crisis.

Ratio bank credit to stock market traded value.

Below, we account for Brazil's more open stance towards foreign investors and a weakening of state control via BNDES in Brazil, which both played a considerable role over the last years. However, these are factors of economic policy which supply-side CC – as often criticized – does not account for and are therefore not tested here.

Industrial relations, education and innovation

Given that most demand in emerging markets is fuelled by first-time consumers who value affordability and functionality, the domestic industry heavily relies on these low-end market segments (BCG, 2014). This turns into a considerable competitive advantage, making emerging economies to lead markets for ‘good-enough’ products (Herstatt and Tiwari, 2017; Nölke et al., 2020). Low-waged, predominately low-skilled and highly flexible labour is the precondition for price competitiveness. Most workers are effectively excluded from formal labour codes, employed as contract workers or under other non-standard forms of employment – if not even fully informal. These labour relations are complemented by a highly segmented education system: masses of easily dismissible low-skilled workers on the one hand and a high-skilled labour elite on the other (Nölke et al., 2020: 187–190). Again, if the recent trajectories of Brazil and India were to be associated with the erosion of the institutions of its state-led capitalism, this should be visible in the relevant data. Particularly, we would expect a move towards a more organized industrial relations systems and substantial skill upgrading in Brazil. However, union density rate in both countries remains roughly constant over the last 10 years (OECD, 2020; Visser, 2019). In Brazil, approximately 20% of the total workforce are collectively organized (12% in India) and worker unrest increased slightly in recent years – in contrast to India (ILOStat, 2020).

Crucial for the state of industrial relations and the prospects of collective bargaining, however, is the continuity of informal labour relations. During the 2010s, informality remained stable at 38% in Brazil but increased in India from 75% in 2010 to 80% in 2018 (ILOStat, 2020). Although non-standard and informal employment is lower in Brazil than in India, high rates of job turnover exist nonetheless, as employers can dismiss workers easily even in regular employment contracts (ILO, 2016a: 60). Hence, the marginal differences and changes in the sphere of industrial relations do not yet amount to a critical threshold of altering the present low-cost regime towards a more corporatist one in Brazil, let alone in India where the system-defining element of informality is not fundamentally challenged by recent reforms of labour relations (Kuruvilla, 2019: 233–234). The characteristic features of industrial relations in state-led capitalism do not seem to have changed significantly.

This also applies to the institutions of education and training which are central to a firm-centred supply-side perspective on capitalism. A thorough upskilling of the domestic workforce could mark a departure from the existing low-wage model. Given that most of today’s emerging economies have accomplished fairly high levels of secondary education, an important step towards a higher skilled workforce would be the provision of technical as well as broad-scale tertiary education (Aziz, 2012; Bruns et al., 2019; Doner and Schneider, 2019). Both countries expanded access to higher education significantly between 2000 until 2018 (UNESCO, 2020), but that does not amount to a highly skilled workforce on a broader level because education expansion still has to be matched by substantial increases in quality (Bruns et al., 2019). As a consequence, the strong divergence between the two countries cannot sufficiently be explained by a thorough movement towards a high-skill and high-growth education regime. Consequently, there are no signs for a transition to a novel production regime based on different kinds of innovation. Strikingly, there are strong initiatives in both countries to upgrade the innovation system but with only limited impact on domestic industries (Dominguez-Lacasa et al., 2019).

Summing up, we see considerable dynamics in the institutional configuration of state-led capitalism. However, these represent incremental changes at best but not a transition to a new kind of capitalism. More important to our question: there are hardly any differences between Brazil and India. Apparently, the institutionalist toolkit has been useful for the identification of the stability of state capitalism in Brazil and India but does not seem to be suited for measuring the factors that could cause the divergent trajectories of these two countries. If supply-side institutions were causal factors for the stability of capitalism, we would logically have to detect significant changes in the institutional setup of Brazilian capitalism that could explain why this arrangement is not working anymore. We therefore move on to test the explanatory potential of the GMP.

Applying the GMP: Change amidst volatility

The GMP starts from a post-Keynesian perspective on capitalist variation not by the assertion of different capitalisms as such but of growth models. From its analysis of contemporary European economies, it highlights two complementary growth models: a debt-financed consumption-driven and an export-driven growth model. Hence, it accounts for the consolidation of particular macroeconomic trajectories that prove ‘sticky' on the one hand but also malleable by macroeconomic dynamics on the other. Three aspects especially shape the form of a growth model: first and foremost, the patterns of aggregate demand, the forms in which these patterns are related to an economy’s international integration and the way how social coalitions support a particular growth model. We take these aspects in turns.

The fragility of domestic demand: Limits to debt-led growth in Brazil

A GMP analysis looks first and foremost at the sources of demand in an economy. Unlike the neoclassical paradigm, it does not assume universal demand for goods and services. Instead, different demand types (for instance export-led and domestic consumption-led demand) impinge on the function and logics of the economy. Previous analyses showed that both Brazil and India have been characterized by a consumption-led, rather than an export-led growth model (Bizberg, 2014: 14; Nölke et al., 2020). Against a widely shared misconception, Brazil’s economic fortunes does not primarily depend on exports: even in 2011, still at the height of the commodity boom fuelled by Chinese demand, Brazil's export share in GDP (12%) has been the lowest of the top 10 global economies – lower than similarly closed economies of Japan (15%) and the US (14%) and much behind export-led economies such as Mexico (32%) and Germany (50%; World Bank, 2020). Thus, ‘growth in Brazil is still largely made in Brazil’ (Canuto et al., 2015: 3), much different to the ‘extractivist’ export-driven models dominating other Latin American economies such as Chile and Venezuela (Jäger et al., 2014).

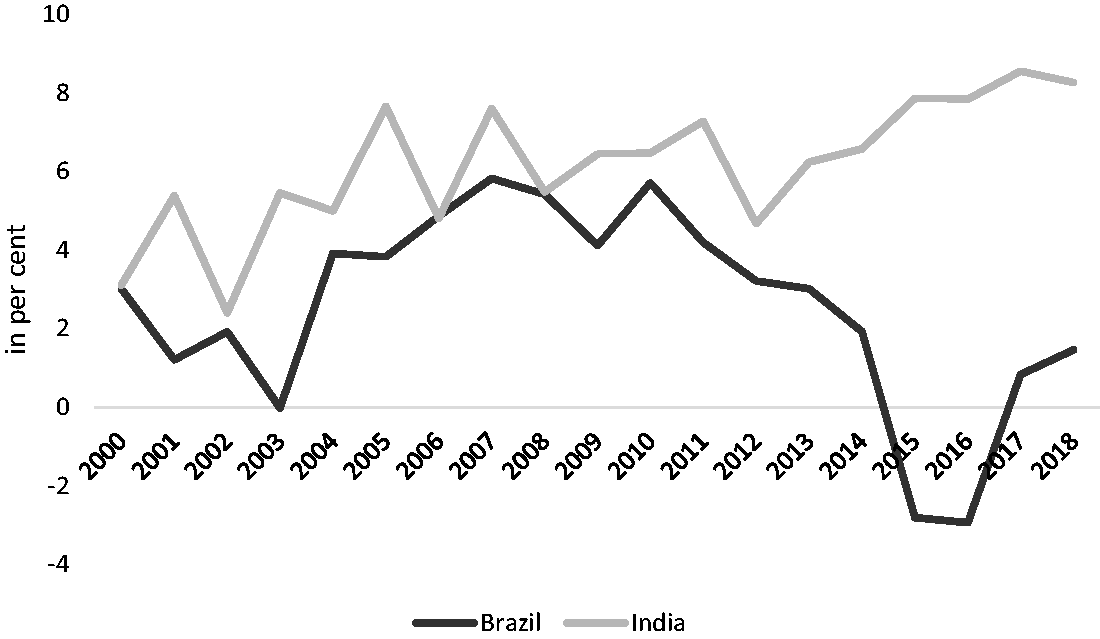

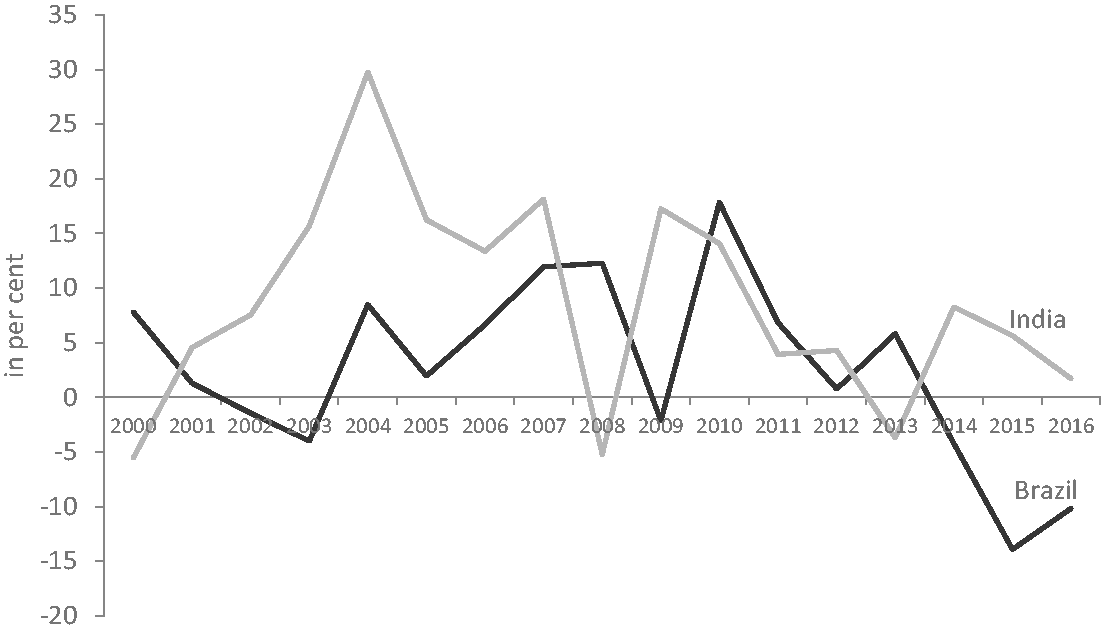

Large domestic markets based on private consumption and investment have served as a backbone for economic growth in both Brazil and India since the late 1990s (Nölke et al., 2020). It is here that we see a major discrepancy between Brazil and India (Figure 4). In Brazil, for instance, pro-poor social reforms were crucial ingredients of demand stimulation. The steady increase of private consumption between 2003 and 2009 has been based on a stable labour market, the creation of new formal jobs, substantial social transfers and wage increases (Melleiro and Steinhilber, 2012: 219). Average real income rose during those years and increased the demand for local products and services. According to the IMF, ‘consumption – both public and private – has accounted for almost all the growth in Brazil’ (2013: 15). The same applies to India – to the discontent of the World Bank which suggests that the Indian export share of 10% of GDP should be increased to the ‘normal' 30% (Livemint, 2019).

Final consumption expenditure, annual growth, 2000–2018.

For the same reason, however, a slowdown of domestic demand can have massive repercussions on economic growth in such relatively closed economies. Comprehensive analyses confirm that the slowdown in Brazilian growth between 2011 and 2014 was overwhelmingly triggered by a sharp decline in domestic demand rather than a fall in exports or external financial conditions (Serrano and Summa, 2015). A comparison with India demonstrates that all major financial sources of domestic demand were affected simultaneously. The first is the substantial divergence in average wage growth (ILO, 2016b, 2020). Real wage growth halted from 2012 onwards and turned negative in Brazil in 2015 (–3.7%), whereas it remained positive throughout in India – despite decreasing levels between 2008 and 2012. Thus, one can observe a shrinking base for domestic demand in Brazil for which, in a domestically oriented economy, resources have to be mobilized endogenously.

As real wage growth in Brazil could not support this pillar of the economic model, the country gradually moved on to a growth regime based on domestic debt (both public and private; see Lavinas et al., 2019), which yet proved fragile due to emerging financial constraints. Public social spending in Brazil, for instance, both eased soaring inequalities and bolstered consumption among low income and poor households. When Brazil moved into recession, it stood at over 15% of GDP – a high value for emerging markets and more than double the level of India (OECD, 2014: 3). A sharp increase in government debt since 2014 (IMF, 2020), combined with political opposition to tax increases, continuously high interest payments and declining revenues from commodity exports limited fiscal possibilities while external indebtedness increased financial vulnerability (IMF, 2013: 49–57; Dierckx, 2015: 153).

However, stimulating demand by increasing external debt has also been off the agenda. In Brazil, external debt has grown significantly since 2011 and is approaching values of the early 2000s (before PT rule), whereas India displays a much more modest development (World Bank, 2020). This difference can partly be accounted for by the strong presence of multinationals in Brazil and thus higher levels of inter-company debt, but it is nonetheless associated with more vulnerability through global financial markets and exchange rate movements (FSB, 2016, 2017; see also below).

The final lever to stabilize domestic consumption, like in many advanced capitalist economies, would be increasing household credit. Here again, the Indian case displays not only a much lower level but also a more modest growth dynamic. Household debt in India levelled at 9–10% of GDP but rose from approx. 15 to 25% in Brazil between 2006 and 2017 (IMF, 2020). In fact, Brazil had made use of bolstering domestic demand through credit expansion, which, however, slowly exhausted with the economic slowdown – not because of an absolute threshold on maxing out household credit but because real wage growth turned sour and banking on social benefits as collateral became increasingly difficult (Lavinas, 2017). Correspondingly, Brazil’s reliance on debt-financed growth became a burden.

In sum, the demand focus of the GMP reveals a major factor explaining the drift apart between Brazil and India: the breakdown of the financial underpinnings of domestic consumption. Although arguing primarily from a macroeconomic point of view, the GMP stresses that demand regimes always depend on their international and political context. Without these two factors, growth would simply be a result of macroeconomic flows. Hence, it is important to study two additional factors that are necessary for the establishment (or absence) of growth models: the international integration of the two economies and the political stabilization – or lack thereof – by dominant social coalitions.

International economic integration: Vulnerability via subordinated financial integration in Brazil

A GMP-based comparison of the international economic integration of Brazil and India reveals similar developments in the field of trade, but divergent ones in international finance, with massive repercussions on the national currency and subsequently the fate of Brazilian industry. In both countries, state capitalism in the first decade of the 2000s has been based on a commitment by the state and its agencies towards the protection of domestic industry against external competition. The aim was to nurture a domestic market with a particular demand structure that would best be served by incumbent industrial firms. That ‘stable protectionism’ stance intensified in India, which actually increased the number of non-tariff measures of protection such as sanitary requirements and technical barriers to trade (as used by Brazil) as well as anti-dumping measures and quantitative restrictions (used by India; WTO, 2021). Similarly, the simple average applied tariff remained stable at 11.6% in Brazil and even increased slightly to 14.3% recently in India (WTO, 2021). These data suggest at least a continuation, if not an intensification of protectionist measures to support domestic industries. For sure they prove that neither Brazil or India turned into an export-led growth model, despite considerable efforts to boost the international competitiveness of selected ‘national champions’ through equity injections and export financing (Hennart et al., 2017).

However, as we mentioned earlier, emerging economies are relatively vulnerable against fast movements of external capital, credit and sudden currency fluctuations. Hence, it is necessary to take a closer look at Brazil and India's external financial relations – a perspective that is also usually not part of the supply-side CC framework. We first look at inward foreign direct investments (FDI). Despite increasing over the past two decades, inward FDI stock in India remains with 14% of GDP at a modest level. Although foreign investors increasingly engage in Indian firms, there is no evidence yet for a destabilizing effect for established ownership structures. In Brazil, by contrast, FDI increased strongly after 2008 as well as after 2015. Thus, the overall trend over the past decade indicates a greater openness for FDI inflows amounting to foreign capital stock levels similar to OECD countries (Figure 5).

FDI stocks, inward, in per cent of GDP, 2005–2016.

Correspondingly, particularly large Brazilian non-financial companies seem to increase their financing through international capital markets (Kaltenbrunner and Painceira, 2018), but the general image is rather mixed. First, banking systems in both countries appear relatively stable, with a slightly growing market share for domestic (public) banks and a marginal role for foreign financial institutions and stock exchanges for investment finance (FSB, 2016, 2017; Tara and Dhamija, 2018). Second, the entry of investment funds in Brazil has not led to a profound change in corporate control or finance because most of them participate in the traditionally highly profitable treasury bond segment, feeding into the specific (state-led) trajectory of Brazilian financialization (Bin, 2016; Lavinas et al., 2019). In effect, most Brazilian firms cannot easily circumvent the limitations of the bank-based system (not least due to the retrenchment of BNDES as a major credit source) by tapping on external market-based credit. India, in contrast, although opening up for foreign firms over the last years, has remained stable with regard to its preference for national control, in spite of the change of government in 2014 (Jayadev et al., 2018).

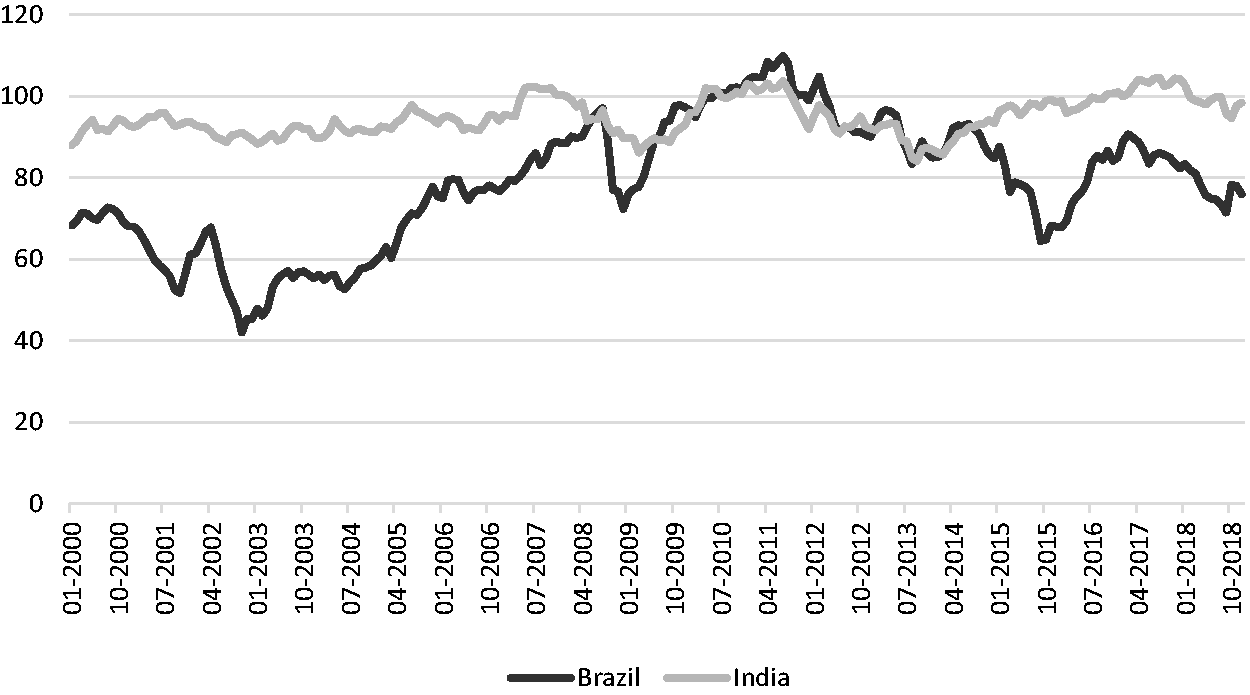

While this is an argument about the importance of foreign capital stocks, the volatility of capital flows is crucial for emerging economies as well. Against this background, Brazil and India have developed protective means against fluctuations on global currency markets through the accumulation of substantial currency reserves. Similarly, both countries also have instated diverse forms of capital controls (Gallagher and Prates, 2016). Brazil, in addition, temporarily introduced a tax against speculative financial flows, which, however, remained haphazard (Alami, 2019; Dierckx, 2015: 154). Yet, Brazil had limited means against global financial speculation. High interest rates – implemented by the independent central bank to avoid a return to previous periods of hyperinflation – are an expression of the public bond-based financial incentive regime and have attracted massive carry trades, leading to a strong overvaluation of the Brazilian currency. Already in April 2011, the Brazilian Real was already heavily over-valued in relation to its long-time optimal value (Nassif et al., 2011). This overvaluation of the domestic currency is seen as one of the major causes of the Brazilian economic record, particularly in manufacturing (Nassif et al., 2015: 1314–1315). Companies in the services sector (because of the non-tradable nature of their products) and in commodities (as their production costs are below world market prices) can survive steep currency appreciation very well (Schneider, 2013: 150). However, domestic manufacturers have suffered tremendously under the weight of currency appreciation, weighing heavy on the domestic consumption model (Schneider, 2013: 168–169). On the other side, financial fluctuations have also worked in the opposite direction during the crisis of confidence in the Brazilian economy. Here, massive capital outflows led to a sudden devaluation of the Real in 2015 (Figure 6).

Real effective Exchange rates of Real and Rupee, 2000–2018.

While a devaluation does increase price competitiveness, sudden currency swings are, however, poisonous for long-term investments (Kaltenbrunner and Painceira, 2015: 1301). India, in contrast, suffered much less from carry trades and, due to the more closed nature of the financial system, has not been affected by sudden stops. As Figure 6 shows, Brazil experienced three major slumps in the external value of the Real: 2002, 2008 and 2014. In each of these episodes, it decreased by 25 to 30% within several months, only to appreciate at similar speed afterwards. Obviously, such volatilities in the currency regime pose problems for firms and policymakers, especially in an environment characterized by inflationary pressures and corresponding interest rates.

In sum, these developments have given financial interests a much greater role in the Brazilian economy that comes with a greater exposure to interest rate volatility, capital flows and credit crunches. Although both Brazil and India have continued their trajectory of ‘stable protectionism’ in foreign trade, the openness towards global financial markets and the related currency movements have put massive pressures on the Brazilian industry, leading to a loss of competitiveness, deindustrialization and decreasing real wages. Still, this development is a gradual one but growth contracted very sharply in Brazil after 2013. This brings us to another factor highlighted by the GMP, namely the importance of a stable social coalition to support the growth model.

Stability of growth coalitions: Stronger paralysis by anti-corruption movements in Brazil

The GMP does not predispose the existence of permanent country-specific types of capitalism but allows for changes between growth models within a country, because macroeconomic variables may change more quickly than institutional factors. Therefore, the political determinants of growth model stability become highly important. The GMP sheds light on the politics between economic sectors and leading politicians. For EU economies, it claims that ‘social blocs’, comprising of ‘[d]ominant social groups, i.e. those whose demands are taken into account in the definition of public policy’ (Amable and Palombarini, 2009: 129), are crucial for the attainment of a particular growth regime (Baccaro, 2019).

The consolidation of socio-political support for a particular growth model is, however, different from EU countries. First, explicit political support through parliamentary majorities (as e.g. put forward by Amable and Palombarini, 2009) prerequisites strong liberal institutions and a history of corporatist organization. Second, due to the much higher level of informality of politics in large emerging markets such as Brazil and India (Hammer, 2019), the collaboration of state actors with representatives of domestic business is based on close interpersonal connections and norms of reciprocal favours rather than through consultation in the process of policy formulation. Therefore, the exertion of control over economic activity is mainly network based (Nölke et al., 2015: 543). In the absence of well-working formal institutions (for instance, sectoral or regional business associations), informal institutions such as family ties help to solve agency and information problems. Close collaboration between state agencies and domestic capital allows for the development of a coherent strategy of industrial development. In contrast to the East Asian developmental states, however, this coordination does not take place through centralized top-down channels but in decentral coalitions between businesses and bureaucracies, for example on the regional level. Arguably, contemporary state capitalism is strongly characterized by such a ‘permeation’ of economic institutions by the state. This goes deeper than direct control of firms and industries or their economic support (Musacchio et al., 2014). At the same time, the state-capitalist social bloc, expressed through ‘growth coalitions’, is not necessarily based on broad political support but on the joint commitment of economic and political elites.

The importance of these growth coalitions became obvious when both countries encountered major corruption scandals that challenged the nature of this close collaboration. An anti-corruption movement shook Indian politics during the late phase of the last Congress Party government with a series of mass protests (Riley and Roy, 2016: 89–91). Since 2013, the left-leaned anti-corruption Aam Aadmi Party continuously won the elections in New Delhi, while the corruption issue has been central to the electoral campaign (and eventual victory) of the nationalist Bharatiya Janata Party (BJP) under Narendra Modi in 2014 on the national level. The societal mobilization against corruption made it increasingly difficult to maintain the traditionally smooth mechanism of informal coordination in the Indian political economy. Close informal interactions between representatives of state and business came under the general suspicion of corruption. Even liberal voices concluded that anti-corruption measures in India have had negative short-term repercussions: Corruption produces bad decisions; concern over corruption produces indecision. […] Mines and other assets lie idle as courts dither over how crooked their owners are. Faced with this mess, private firms have cut investments [which] is one reason why GDP growth has slumped to 5%, the lowest level for a decade. […] Few senior people go to jail; but officials fear being accused of malfeasance, so many think the safest course of action is to make no decisions at all. (The Economist, 2014: 3)

Subsequently, the breakdown of informal state-business coordination due to comprehensive anti-corruption campaigns resulted in decreasing private and public investment. In India, several major investment projects that have been cast into doubt due to anti-corruption operations (Solomon, 2013: 911–913). Although these refer to typical one-off auctions of licenses and infrastructure projects (in contrast to the issues at the heart of the Brazilian corruption scandal), GDP growth in India slowed down during the heydays of the anti-corruption campaign (World Bank, 2015: 5; see Figure 1).

In Brazil, however, the effects of anti-corruption measures on economic growth have been worse, as the development of gross capital formation shows (Figure 7). Petrobras had to scrap massive investment plans and to lay off more than a third of its workforce. Many of the major Brazilian companies were involved in the corruption scandal and therefore banned from doing business with the government. This did not only affect companies in the oil and gas sector but also in engineering and construction, with Odebrecht as the most prominent case. Anti-corruption operations in other sectors followed, for example against the world’s largest beef and poultry exporters, JBS and BRF. As in India, ongoing anti-corruption operations led to a general climate of mistrust and state officials did not dare to make investments decisions anymore. This hampered the efficiency of local growth coalitions. While growth already had slowed down between 2010 and 2013 (due to the reasons discussed in the previous sections), the Brazilian economy fell into its deepest recession in history in 2014 (Felter and Labrador, 2018; see also above). As witnessed in India, anti-corruption operations – via an increase of ‘economic policy uncertainty’ – mainly affected real investment which has contracted by around 30% between early 2014 and late 2016 (Krznar and Matheson, 2018).

Gross domestic investment in Brazil and India, annual growth in per cent, 2000–2016.

At the same time, the public development bank BNDES, which had been reinvigorated by the PT government and stepped up its activities following the global financial crisis, underwent several constraining reforms after the centre-right Temer government came to power. While cutbacks on its funding from the treasury and the workers’ pension fund (FAT) creates pressure on its overall credit operations, the marketization of its interest rate through the new benchmark rate TLP will remove its key competitive advantage vis-à-vis other banks. With a drastically downsized BNDES, which traditionally attracted capital to support a developmentalist strategy (Bril Mascarenhas, 2016), a key pillar of Brazilian state capitalism is lacking for the time to come.

Arguably, the main reason for the instability of the social bloc in Brazil has been a lack of consensus regarding the national development trajectory: A deep ideological rift between a liberal and a state-capitalist faction existed from its inception, both within the governing coalition as well as between the government and large groups of outward looking-domestic capital (Taylor, 2020). Only growth and soaring corporate profits held this heterogeneous social bloc together, spurred by cheap state lending, rising domestic demand, public infrastructure investments and household financialization. When growth faltered and government demand stimulus waned, powerful business groups such as the São Paulo Federation of Industries and the Brazilian Agribusiness Association deserted the social bloc and actively supported the impeachment process of Dilma Rousseff (Morgan et al., 2020: 8). Whereas anti-corruption movements also led to a short period of declining investment rates in India, the social bloc remained largely intact, thereby limiting economic damage. Even if we too see rivalries among industrialists and state authorities in India, there is a broad consensus among growth coalitions on the overarching importance of catch-up development under national control of the economy.

To conclude, massive anti-corruption campaigns have led to a temporary paralysis of public investments and a dip in growth figures. In comparison, this problem has affected Brazil later and more substantially than India, where the anti-corruption investment paralysis has faded after 2013. Given the importance of (public) investments and the related domestic demand for the state capitalist growth model, anti-corruption operations can destabilize the latter for extended periods, a prime reason for the dismal growth in Brazil over the last years.

Conclusion

The initial puzzle was the strikingly different development of the Brazilian and Indian economies during the last decade, in spite of substantial institutional commonalities. Whereas both countries encountered a downturn of growth, Brazil fell into the worst recession of its history, whereas India suffered only a minor dip. Since the divergence cannot be attributed to government change, we turned to comparative political economy for possible explanations, specifically a supply-side oriented framework and the demand-side focused GMP.

The supply-side CC categories could not sufficiently explain the divergent developments of the Brazilian and Indian economies. The categories provided by the GMP proved to be much better suited for an explanation of the collapse of Brazil, compared to the stability of India. Whereas domestic demand remained stable in India, it was severely weakened in Brazil. All major drivers of domestic demand during the previous decade – rising real wages, increasing public investment and the extension of credit to private households – simultaneously turned sour. These factors met a Brazilian industry that was already weakened by an overvalued currency and eventually the collapse of the growth coalition in the context of anti-corruption campaigns.

In strategic terms, our paper alludes to the notion that large emerging markets have developed a distinctive state-led economic model based on different institutions than in Western capitalism. The case of India demonstrates how this model can be relatively stable for many years. However, a haphazard commitment towards this model produces several contradictions that may undermine its stability over time. In the case of Brazil, these contradictions include an openness to the global financial system, leading to destabilizing currency relations, limits to the support of domestic manufacturing via demand stimulation, for example based on the exhaustion of fiscal resources and a lack of consensus on the importance of catching-up development under national economic control.

The different experiences of Brazil and India seem to indicate that a fuller embrace of state capitalism, based on a wage-led demand growth model, works better than a partial adoption of this strategy. This implies that Western calls for even greater liberalization and further transparency may backfire in the case of large emerging capitalist economies, first in terms of economic growth, but fundamentally also in terms of social progress.

In a more theoretical and methodological vein, our contribution has highlighted the usefulness of a comparative political economy toolkit for understanding the economic development of Brazil and India, complementing the more economic policy-oriented and country-specific accounts dominant in much of (heterodox) economics. Among the comparative accounts, the GMP seems to be better suited for the explanation of mid-term economic change than firm-centred accounts – not least because it can partially accommodate the impact of the state. Most institutionalist CC approaches as well as the GMP itself have been designed to explain developed capitalisms, with the consequence that ‘statehood’, which is arguably a decisive factor in state capitalisms, is absent as an analytical category. The GMP offers an entry point to account for the state or the political level which does not necessarily have to be limited to electoral aspects but is able to incorporate the crucial role of state-business relations that have been proven significant in previous research on (Asian) developmental states (Evans, 1995; Maxfield and Schneider, 1997). Obviously, much more work is needed to fully develop the analytical potential in this dimension (Alami and Dixon, 2020).

Therefore, our findings do not mean that firm-centred institutionalist CCs is obsolete. The two approaches rather complement each other and can be fruitfully combined: whereas the supply-side oriented approach is better suited for making sense of the long-term firm-centred set-up of national economic institutions, the GMP rather provides the means to incorporate short-term macro-economic developments, international interdependencies and the political dynamics supporting stable economic models. Yet, as a fairly new research program, its concepts and causal explanations need to be developed further in order to yield better insights on emerging economies, particularly with regard to the much higher level of informality as well as the particular structure of the state.

Footnotes

Acknowledgements

We would like to thank the anonymous reviewers for their constructive engagement with the manuscript. Earlier versions of this article were presented at ISA (4-7 April 2018), AFEP-IIPPE (3-5 July 2019), SASE (18-20 July 2020) and the ‘Growth Models in the Global South Network’ (17 December 2020). We are grateful to all commentators and discussants.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This project has received funding from the German Research Foundation (DFG, Grant agreement no. 218893009).