Abstract

Contemporary tax research is split into two camps: comparative approaches emphasize continuity and cross-country differences, while the globalization literature stresses similar changes across countries. Counter the continuity thesis, this paper finds that neoliberal dynamics were at play in a case considered largely resilient to such dynamics: German governments implemented a series of corporate tax reforms which radically curbed business taxes and added a short-term and cost-cutting component to investments and corporate finance. While these changes point towards neoliberal change, they were distinct from the trends we see in other economies: crucially, the German reforms did not follow the common trend of reducing taxes for individuals and entailed a particular emphasis on enhancing multinational’s access to international capital – but did not liberate financial incomes from tax in general. Based on archival documents from the Bundestagsarchiv, this paper traces the process of German tax reforms and finds that neoliberal dynamics were at play but received a local (export-oriented) colour through processes specific to the German polity. Because consensual institutions granted power to a specific business coalition, radical change was long blocked. Reforms could only be implemented once the state forged a new coalition. Making sense of the mediation of neoliberal dynamics through state institutions can contribute to a better understanding of the variegated nature of neoliberalism.

Introduction

Tax systems critically shape the resource allocation between different sectors of an economy and thereby determine the type of economic growth that evolves (Haffert and Mertens, 2019; Prasad, 2006, 2012). State actors have to decide whether they want to levy a higher tax burden on consumption or investment (Huo, 2020), and whether they want to support certain business groups over others (Berry, 2016). By making these decisions, policy makers determine the type of growth strategy they want to pursue. So far, the tax literature has either highlighted tax reforms driven by neoliberal dynamics and globalization leading to a convergence of tax regimes towards the liberal model (Cerny, 1997; Strange, 1996), or stressed how institutions in coordinated regimes ensured resilience (Hall and Soskice, 2001; Mares, 2006), or incremental change within the larger framework of collective organization (Thelen, 2014, 2019). With this emphasis on globalization and institutions, the state as an active ‘economic player’ (Zysman, 1983: 75) has moved to the backburner of the analysis. This paper analyses neoliberal dynamics in the German case which, because of its collective organization and export-orientation, was for a long time considered the case that was resilient against neoliberal trends.

Can an export-oriented tax regime be neoliberal? In broad terms, neoliberalism can be defined as ‘a set of economic ideas and associated policies that have a constant goal (to enlarge the realm of the market) and a variable one (to carry out upwards redistribution)’ (Ban, 2016: 4). In the realm of taxation, scholars have shown that neoliberal reforms usually combine low tax rates and high levels of tax neutrality. More specifically, the goal of neoliberal tax reforms is to minimize the distortion of markets which comes about through taxes on corporate profits, individual incomes and capital incomes (dividends, interest and capital gains) (Hakelberg and Rixen, 2020: 4). According to this definition, the German tax regime has gone through a neoliberal transition and yet the transformation critically differed from outcomes in liberal regimes. First, German neoliberal tax reforms came surprisingly late. In the 1980s, when governments in the Anglo-Saxon world implemented radical corporate tax reforms (Martin, 1989, 1991; Swank, 2006), the German tax regime retained most of its post-war features including support for large exporting businesses (Prasad, 2006; Zohlnhöfer, 2003) and ‘patient capital’ – a system of long-term finance (Gourevitch and Shinn, 2010: 162; Lütz, 2000: 150). Reforms were implemented only in the late 1990s, and they differed in several respects from their Anglo-Saxon counterparts: Even though corporate tax rates were reduced and patient capital dismantled – adding short-term and cost cutting elements to investment and corporate finance – export businesses remained the main beneficiaries of the reforms: They benefited from significant (and uneven) rate reductions and a new dividend tax system which facilitated corporate finance in international capital markets.

This paper inquires how this unusual pattern of German neoliberal tax reforms came about. It draws on state-centred approaches to argue that neoliberal tax reforms originate from the state’s active involvement in the economy and are critically shaped by the state’s relations with businesses. I develop a heuristic of state entanglement which encapsulates both movements at the same time: When pursuing growth strategies, the state may find the support of some economic actors – the winners of reform – but will also encounter considerable backlash by entrenched interests which lose out from a new strategy (Zysman, 1983). Navigating through these structures of resistance of entrenched interests, the disentangling of existing relations and building of new ones can be critical to facilitate and shape neoliberal reform. By investigating the role of entanglements between state and economy, this paper explores how state-business relations mediate the outcomes of globalization pressures on domestic institutions.

The paper shows that much of the entanglement of the German state with businesses was shaped by electoral institutions. Federalism and consensual institutions – proportional representation and multiparty governments (Basinger and Hallerberg, 2004) – entangled the interests of business groups and policy makers in three different ways. First, federalism aligns the regional economic interests of state governments and economic interests. Second, coalition governments represent several different business interests which become entangled with parties’ interests in federal government. Finally, state actors’ dependence on certain business groups can entangle their interests with these actors: In the German, case federal states depended on the services of the savings banks. These entanglements and the state’s attempt to break them up critically shaped the outcome of neoliberal reform. The German case helps explain why neoliberalism is not a ‘one-size-fits-all’ process of convergence, but produces variegated outcomes depending on the institutional structure within the state.

The paper uses systematic process analysis to examine the step-by-step falling apart of the old tax regime and its replacement with a new regime. Process tracing allows for an in-depth investigation of interests of several actors in the policy process, the relations of businesses and the state and the strategies of the state which led to change. This method is applied to documents from the archives of the German Bundestag (Bundestagsarchiv) which include statements by officials, parties and business associations on corporate tax reforms.

The paper proceeds as follows: The next section introduces general trends in neoliberal tax reforms across countries and the unusual pattern observed in the German case. Section three debates the existing scholarship on tax reforms and the benefits of reviving insights from the state-centred approach. Section four will outline the process-tracing technique and the archival research. Section five will engage with the empirical evidence starting with a historical background of the post-war German tax regime and mapping out actors, relations and interests during the critical reforms of German corporate taxation. It then compares two periods of tax reform, one in which the tax system remained largely unchanged (1988–1998) and one in which radical change came about (1999–2000). The final section will draw the conclusion that state entanglements and attempts to supersede them can shape the outcomes of neoliberal reforms.

Neoliberal tax cuts and the unusual pattern of reform in Germany

Neoliberal ideas, policies and institutions have spread across advanced Western democracies since the 1980s placing tax cuts to the forefront of fiscal considerations (Ban, 2016; Blyth and Matthijs, 2017; Simmons et al., 2006). Neoliberal tax reforms often entail two critical features: radical rate reductions and enhanced tax neutrality, i.e. minimizing selective tax benefits for specific economic sectors. Tax rates often targeted to fall were corporate income tax rates (CIT), top personal income tax rates (PIT) on individual incomes and profits of unincorporated businesses, and capital income on dividends, interest and capital gains. According to supply-side theorems, these rates distort the efficient allocation of resources in the economy – as opposed to consumption tax which is generally viewed as least distorting (Hakelberg and Rixen, 2020: 4). The overarching goal of this type of tax policy is to enhance investment conditions, reduce costs of production and improve the incentives to work and save (Musgrave, 1959: 246).

Neoliberal tax structures first emerged in the late 1970s and early 1980s in the liberal market economies under Thatcher and Reagan who dramatically changed the functions, instruments and goals of taxation in the U.K. and the U.S. In the preceding Keynesian model, taxation contributed to the overall goal of state management of the economy: Tax rates were generally high, but investment credits, grants and exemptions incentivized investment in certain economic sectors (Howard, 1997; Steinmo, 2003). Progressive income tax rates contributed to demand stimulation and limited private investment when resources were needed for alternative societal goals (Martin, 1991: 22). This model came into crisis after productivity growth had slowed in the 1960s, and supply-side notions, suggesting that coupling high tax rates with exemptions was unfair, complicated and inefficient, increasingly influenced the thinking of economists and policy makers (Brownlee, 2018; Prasad, 2012). Under the additional pressure of businesses threatening to leave jurisdictions for cheaper production sites (Ganghof, 2006; Streeck, 2010), many finance ministers and economic advisers in OECD countries came to view taxation as a critical hurdle for productive investment (Swank, 2006).

Many OECD countries followed the liberal model and implemented corporate, top marginal and capital income tax rate cuts (Ganghof, 2006; Hakelberg and Rixen, 2020). Many governments radically reduced the top statutory corporate and income tax rates, and curbed investment tax credits for specific economic sectors (Swank, 2006). After mobile (high-income) individuals and profits of multinational corporations contributed to a massive outflow of taxable profits in the 1990s, OECD countries also specifically reduced taxes on financial incomes (interest income, dividends and capital gains) (Hakelberg and Rixen, 2020: 11). For instance, several countries – which traditionally taxed interest within the general income tax schedule – introduced lower rates to curb cross-border tax evasion (Genschel and Schwarz, 2011: 359).

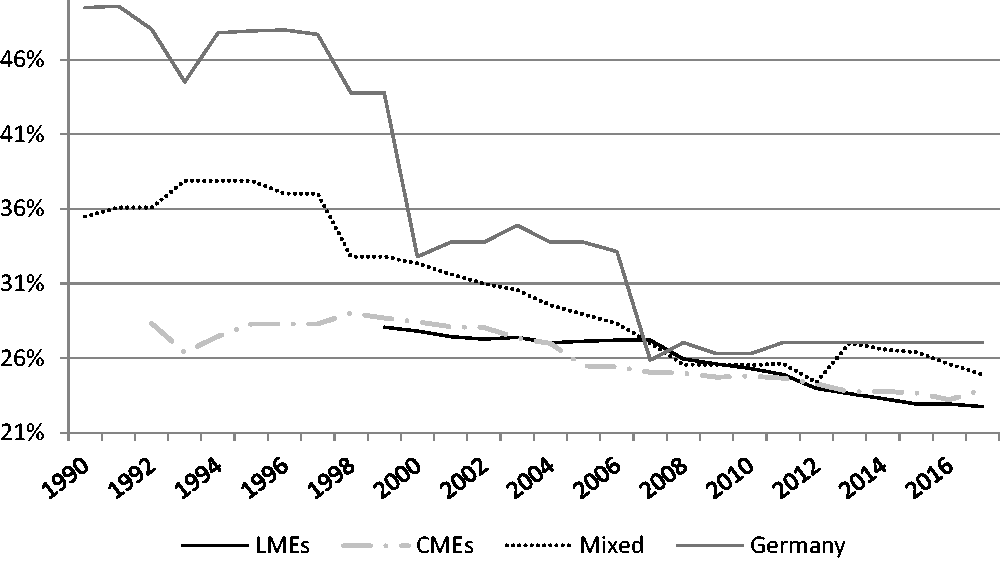

While many OECD countries followed the liberal model, German reforms differed in several respects. Throughout the 1990s, German governments only achieved incremental reductions in corporate tax rates resulting in unusually high effective average corporate tax rates (AETR) compared to liberal and other coordinated market economies. Then, in 2000, a radical reform cut CIT rates to OECD levels within one year (the rates fell from 43.7 to 32.8 per cent) (Figure 1). Moreover, the composition of the German reform differed from the general trend. German policy makers cut CIT rates but retained high personal income tax rates. For instance, the cuts in statutory CIT – paid by corporations – were much more pronounced (fell to 25 per cent in 2000) than the reductions in the top marginal PIT rate for small businesses (fell to 42 per cent in 2000) (Bach et al., 2014: 119). Moreover, top rates for individuals were almost fully retained. Compared to the US, where effective rates for the top 0.01 per cent fell to 23 per cent in 2002 (CBO, 2008), German top income taxation almost did not change: the top 0.01 per cent still paid 39.8 per cent in Germany in 2002 (Corneo, 2005). Finally, while many governments reduced taxes on financial incomes, German reforms focused on facilitating investments into corporations. The most significant reform elements in the area of financial incomes were a new dividend tax, the elimination of tax support for savings banks and the elimination of capital gains taxes on block-shares which dismantled traditional finance structures and facilitated corporate finance in international capital markets (Sørensen, 2002). In short, German reforms contained some neoliberal elements by adding a cost-cutting component for corporations and enhancing access to foreign investments and yet they differed from the neoliberal model by selectively supporting corporations over individuals and SMEs.

Average effective corporate tax rates; country groups and Germany.

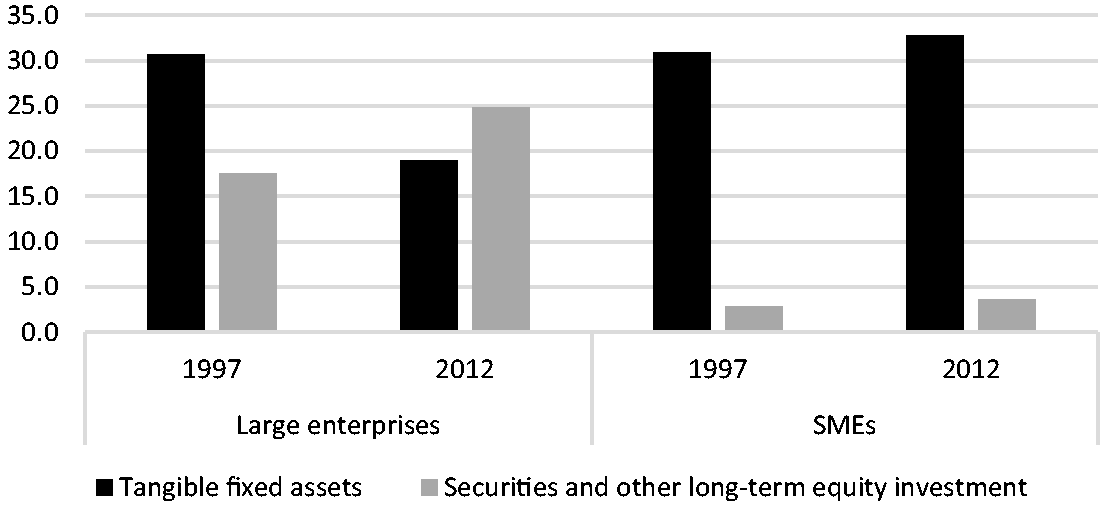

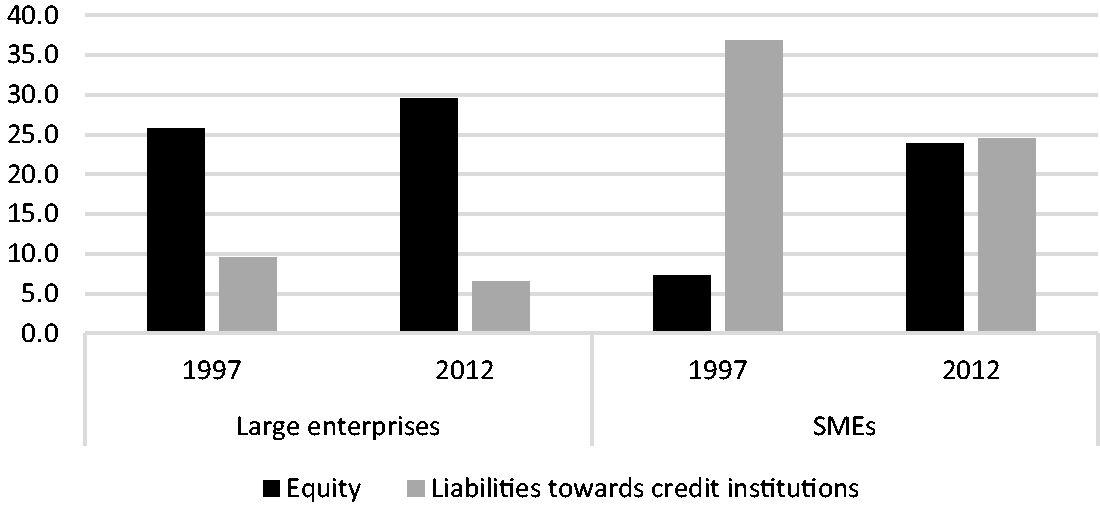

The consequence of this one-sided approach of tax reform was a divergence in investment and finance opportunities of different types of German businesses. Figure 2 shows that large corporations invested more in securities and long-term equity and less in tangible assets – German corporations also reportedly accumulated rising levels of profit since the late 1990s (Braun and Deeg, 2020), while equity investment for small and medium-sized businesses (SMEs) remained at a low level. At the same time, as Figure 3 shows, loans – one of the traditional elements of German organized capitalism – declined as a source of corporate finance for both SMEs and large corporations, while finance through retained earnings and capital markets increased. Unfortunately, there are no data which distinguish equity into internal and equity finance, but data on all firm types show that there has been a general trend of deleveraging and profit retention in the German economy between 2000 and 2015 (Bundesbank, 2018), internal finance made up a roughly stable share of 70 per cent of new finance, while equity finance made up about 10 per cent between 1997 and 2012 (Braun and Deeg, 2019: 8). At least for large corporations, it is likely that this indicates a stronger short-term orientation of corporate finance.

Assets of NFCs as a percentage of the balance sheet total.

Liabilities of NFCs as a percentage of the balance sheet total.

If this tax reform triggered some neoliberal elements but remained distinct from the Anglo-Saxon type of liberalism, could it be characterized as ordoliberal? Blyth (2013: 133) calls ordoliberalism a ‘peculiar form of liberalism’ which differs from neoliberalism in that it stresses the role of a more interventionist state which sets framework conditions to enhance the effectiveness of markets. Ordoliberalism developed in 1920s and 1930s Germany but was based in the experience with an interventionist state during late industrialization in the 19th century and the loss of credibility of liberalism after the stock market crash in the Great Depression (Allen, 1989). Ordoliberalism promoted a strong state, one that curbed the uninhibited power of economic agents and instituted collective forms of economic organization (Bonefeld, 2012: 643). Since the German tax reforms stripped away important elements of the collective organization of the German post-war system – including patient capital, the case at hand rather represents a reorganization of the German economy along laissez-faireism than ordoliberalism.

Explaining neoliberal tax reforms: Tax competition, coordination and the role of the state

Much has been written about the convergence of tax systems after the radical reforms in the U.S. and the U.K. put pressures on Western economies to follow their example and radically reduce CIT and PIT rates. Many studies have argued that rising capital mobility and trade integration instigated tax competition and critically limited the room to move for revenue collection and redistribution in European welfare states (Genschel, 2002; Genschel and Schwarz, 2011; Radaelli, 1999). More specifically, some studies pointed out that tax optimization and tax arbitrage of multinational corporations forced governments to radically reduce statutory tax rates because transfer pricing activities rendered capital movements uncontrollable by governments (Devereux et al., 2008; Slemrod, 2004). While many economies radically reduced taxes on corporate, individual and financial incomes (Béland, 2006; Swank, 2006), the general tax competition argument cannot explain why German reforms emerged much later and differed in their composition from the reforms in liberal economies.

While comparative accounts – loosely connected with the Varieties of Capitalism (VoC) approach – have since developed a comprehensive theoretical framework which explains different outcomes of tax policy across countries, these approaches expect that coordinated market economies (CMEs) like Germany are either ‘resilient’ (there is no change) or subject to ‘drift’ (incremental change) under globalization pressures. Initial ‘resilience’ accounts argued that the coordinated nature of the German economy prevented liberal-market reforms because these did not suit the long-term orientation of patient capital, industrial relations and skill formation which support high-quality production (Hall, 2007; Hall and Soskice, 2001; Mares, 2006; Martin, 2014; Reisenbichler and Morgan, 2012). While a second strand of the literature focused less on the complementarity of institutions and stressed the historical origins of contemporary tax structures (Gould and Baker, 2002; Prasad, 2006, 2012; Prasad and Deng, 2009; Steinmo, 2002), both approaches share a static view of institutional development which leave the radical changes in the German tax system unexplained.

Following the critique of scholars who found a significant erosion of the German coordinated market economy (Höpner and Beyer, 2004; Streeck, 2009), and a dualization of insiders and outsiders which left some protected and others unprotected (Emmenegger et al., 2012; Häusermann and Kriesi, 2015), comparative scholarship increasingly incorporated the changing conditions of the German economy. Thelen (2014) develops a new ‘political coalition model’ which argues that with the pressures of economic liberalization, different trajectories of liberalization evolved. While liberal market economies entered ‘deregulatory liberalism’ resulting in the displacement of institutions of collective organization, the conservative Christian Democratic countries – like Germany – entered ‘dualising liberalisation’. They maintained strong levels of coordination, but the changing economic context (a rising service sector) eroded coverage and insider-outsider cleavages emerged. Change in the latter type of liberalization follows a pattern of ‘drift’ because there is no direct attack on the old institutions (see also Thelen, 2019). While going beyond the dual nature of the original VoC approach and recognizing liberalization dynamics, the literature largely stuck to known country groups – Thelen (2014, 2019) splits CMEs into conservative European and Scandinavian countries, but these groups are expected to develop coherent responses towards liberalization along existing institutional frameworks (for a critical response see Clift and McDaniel, 2019). Moreover, ‘drift’ is a rather incremental form of institutional change which does not match the radical nature of German corporate tax reform.

To make sense of the varieties of neoliberal tax reforms, this paper turns to the literature which stresses the role of the state in economic reforms (Evans et al., 1985; Mann, 1984; Skocpol, 1985). Instead of viewing the state as a mere regulator or provider of institutional frames, these approaches see the state as ‘an economic player’ which actively shapes economic outcomes (Zysman, 1983: 75). States pursue what Martin (1991: 17) calls ‘growth strategies’: strategies of economic development that are loosely organized around a dominant growth model which shapes economic relations between the state and businesses. Once relations of the state and businesses have developed, economic policy change becomes difficult to enact because of the considerable distributional consequences of new growth strategies: they will likely strip resources from entrenched interests which will resist reform (Hall, 1986; Zysman, 1983). Change most likely comes about during an economic crisis which drives a wedge between existing coalitions, generates conflict within the institutional structure and incites state actors to forge new coalitions (Gourevitch, 1986; Gourevitch and Shinn, 2010).

A useful heuristic which allows us to examine the specific mechanisms underlying economic relations is ‘state entanglement’. Entanglement can be defined as the intertwining of interests of the state and businesses in institutions and social networks which are difficult to reverse (Grabowski, 1998: 110). The concept was first introduced by the developmental-state literature which viewed it as a source of state power: business support for state strategies mobilizes resources for economic development (Grabowski, 1998). 1 A similar concept has been developed by the literature which investigates the role of central banking for financialization. Braun (2018) defines infrastructural entanglement as the increasing mutual control of state and market actors through market-based central banking. By providing an infrastructure for markets, the state enhances its steering capacity of the economy, but this will in turn also generate power for the financial market as the state increasingly depends on functioning markets (see also Konings, 2007; Walter and Wansleben, 2019). This mutual expansion of power of state and economy is also important in this study, but electoral institutions play the critical role for state entanglement.

Electoral institutions can contribute to entanglement in three distinct ways: First, the dispersion of interests across smaller regional political entities in federalism might lead to the entanglement of interests of regional political actors with regional economic actors. Federalism contributes to the fragmentation of interests across regions, while more centrally organized polities will face more homogenous interest representation (Martin and Swank, 2012: 20). If interest formation is dispersed across geographic areas, there is a high chance that regional political actors will share the interests of regional economic interests (Lütz, 2000; Verdier, 2003). The German case presents a good example because of the type of federalism which is present in Germany: cooperative federalism. Contrary to systems of dual federalism where legislation in the federal and local sphere are relatively separated from one another, cooperative federalism requires that the federal and state level work together closely in many areas of legislation (Börzel, 2001). Because representatives in the second chamber (the Bundesrat) not only represent central partisan positions but also regional economic interests, voting may diverge from the first chamber and present effective veto points protecting regional interests in federal policy making.

Second, the system of proportional representation (PR) can contribute to the entangling of interests of business groups and parties. While majoritarian electoral systems often generate single-party governments (which represent a selected group of business interests), PR systems favour multiparty governments (Prasad, 2006). These multiparty settings enforce consensus not only among multiple parties but also the economic actors each party represents. This consensual nature of PR contributes to continuity in legislation because several actors have to agree on a new initiative (Gourevitch and Shinn, 2010) and change will be rare (Verdier, 2003). We can see this dynamic in the German case. Each party represents some business interests more than others – the Free Democrats (FDP) represent small businesses, the Christian Social Union (CSU) represents farmers and the Christian Democratic Union (CDU) represents small and medium enterprises (SMEs). When these parties enter into government – as they did in 1981, they needed to find agreement among all those business interests (Gourevitch and Shinn, 2010; Schmidt, 2002, 2009). The fact that the coalition lasted for 16 years, but implemented few radical reforms, demonstrates the obstacles that consensual political organization poses for change.

Finally, the economic relevance of some market actors may contribute to an entangling with state interests. For instance, if the state depends on a specific public good provided by a market actor, this might lead to entangling. The German semi-public savings banks represent such an economic actor. Partly owned by the federal states (Länder) and critical for state-level economic and structural development for most of Germany’s post-war development, these institutions held a particularly powerful position in the German polity. Savings banks provided cheap loans for housing and local economic development (Johnson, 1998: 11; Seabrooke, 2006). They received special tax treatment in corporate income tax, local trade and wealth tax to facilitate the provision of loans small savers, small and medium enterprises (Mittelstand) and structural support for financially weak regions (Gärtner, 2008; Koschorreck, 1969). Additionally, partial ownership by the states ensured an indirect representation in the second chamber of the German parliament (Bundesrat). As a consequence, these semi-public institutions found considerable support in the German parliament once the conservative government proposed to curb some of their benefits to finance tax cuts for corporations.

Methodology

To capture the role of local institutions and state entanglement for radical tax reforms, this paper uses a systematic process analysis approach after Hall (2006). Processes reveal how strategic interactions of actors and specific events shape institutional change. With a focus on chain of events, researchers can unveil the micro-level mechanisms of historically complex macro-causal relations (Hall 2006: 30). In the German case of tax regime change, process tracing can uncover the concrete historical dynamics of interest formation and how the state used these to forge coalitions for change.

Two reform periods were selected to trace change over time. The first spans from 1990 to 1994 and contains the two largest tax cuts implemented under Helmut Kohl; The Tax Reform Act 1990 and the Location Preservation Act 1994. In the reform period under Gerhard Schröder (1998–2001), the Tax Relief Act 1999/2000/2002 and the Tax Reduction Act of 2000 were passed. In both periods, government strategies to revive economic growth and forge business coalitions are analysed from statements of officials in hearings and parliamentary debates. Business interests are extracted from letters to the parliament and statements in hearings. The archival material stems from the Bundestagsarchiv in Berlin and contains all protocols of hearings in the Finance, Economic and the Mediation Committee, all written statements of businesses, civil society groups and trade unions on the four relevant tax reforms. The total population of documents analysed encompasses about 3400 pages.

The evolution of a new growth strategy in German tax reforms

This section lays out the empirical findings in three parts. It will first introduce the historical background of the German growth strategy and map out the key actors, their relations and interests. This will help to introduce the context within which long-term blockage and eventual overhaul took place. Sections two and three will introduce the empirical process of resilience in the 1990s and the process of change between 1999 and 2000, respectively.

Historical background, actors, relations and interests

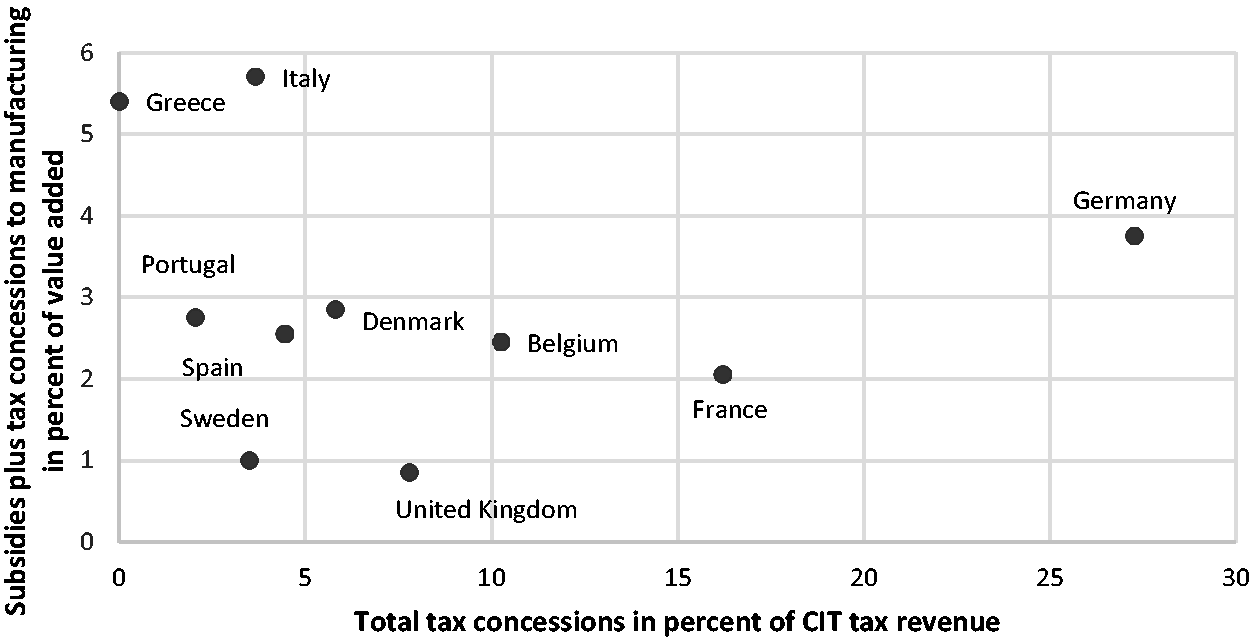

The German post-war corporate tax regime was characterized by the institutional structures of federalism and the dispersion of power of the central German state initiated by the Allied forces. One consequence of this structure was that states held independent rights to spend which rendered control of the federal state over fiscal resources insecure. In order to ensure sufficient revenue sources, post-war governments implemented very high corporate and income tax rates (Katzenstein, 1987; Shonfield, 1965; Zysman, 1983: 255). Since high tax rates impaired the potential recovery of the German economy, tax concessions became an integral part of the German fiscal structure and supported the reinvestment of profits in machinery, fixed assets and inventories. Critical in this respect was the accelerated depreciation schedule, the degressive Afa which shifted resources from declining to growing sectors of the economy (Zysman, 1983: 257). 2 The state’s support for reinvestment contributed to the orientation of the economy to long-term investment and long-term employment enabling high-quality production (Streeck, 1991; Zysman, 1983: 256). While selective subsidies and tax concessions in manufacturing were rather minor, West Germany had unusually high levels of general tax concessions reaching an average of 27 per cent of total tax revenue of the corporate income tax revenue (Figure 4).

Subsidies and tax concessions in European economies, average 1993–1997.

The state also supported a long-term loan structure, so called ‘patient capital’, through tax instruments. The German post-war finance regime was characterized by a pattern of relational banking in which bankers held seats on corporate boards and block shares of their clients to exchange information and build trust (Gourevitch and Shinn, 2010: 162; Lütz, 2000: 150). Tax concessions were critical for cross-shareholding as the ‘major shareholding privilege’ (Schachtelprivileg) exempted all dividend income from shareholdings of more than 25 per cent of a firm’s shares (Höpner and Krempel, 2004: 346). Moreover, tax concessions protected the house bank relationship of the credit institutions of the public right (savings and state banks) and German SMEs. The savings bank privilege (Sparkassenprivileg) was a special tax concession for the public savings- and state banks (Sparkassen und Landesbanken) which ensured the availability of cheap loans for SMEs, local consumers and structural regional development (Koschorreck, 1969). In short, the German tax regime supported credit-based and long-term-oriented corporate finance.

We can identify three larger groups of actors relevant in the debates over German tax reforms: businesses (interested in tax cuts), state governments (interested in balanced budget and support for savings banks) and federal governments (with new growth strategies). While all important business groups requested tax cuts, there were significant differences in the specific cuts each group proposed. Large manufacturers – often multinational corporations (MNCs) – represented by the Federation of German Industry (Bundesverband der Deutschen Industrie BDI) requested a radical CIT cut and the liberalization of German corporate finance. 3 Medium-sized businesses represented mostly by the Association of German Chambers of Industry and Commerce (Deutscher Industrie- und Handelskammertag DIHT) supported radical CIT and PIT tax cuts because many SMEs pay PIT. Moreover, since SMEs often depended on loan finance from savings banks – which they found increasingly expensive – they requested tax cuts on retained earnings to self-finance. Because self-finance is not an option for small firms and farmers, the German Confederation of Skilled Crafts (Zentralverband des Deutschen Handwerks ZDH) and the German Farmers Federation (Deutscher Bauernverband DBV) defended loan-finance through savings banks. The financial sector and commercial banks, on the other hand, requested its dismantling and more support for shareholders and the German stock market.

Because every German party represents some business interests more than others, the conservative-liberal coalition government (CDU/CSU and FDP; 1981–1998) developed complex tax plans. The CDU tended to represent the Mittelstand (SMEs), but the CSU and FDP represented farmers and small businesses. The tax plan tried to integrate all requests at once: CIT and PIT reductions coupled with cuts in tax concessions for all business groups to finance the reform. Together with the initiative to liberalize corporate finance and strengthen the German stock markets, the overall goal of the program was to support investment and offer capital-market finance to MNCs.

But these tax initiatives were frequently blocked in the second chamber: state governments including those governed by the FDP and CDU/CSU feared reforms would negatively affect state finance. Moreover, state governments wanted to secure the position of the savings banks and rejected proposals to raise revenue through new taxes which burdened these entities.

Throughout the 1980s and 1990s, the Social Democratic Party (SPD) and the Green Party blocked reforms in order to protect the old system of long-term finance and investment, but this changed in the late 1990s when continued decline in growth rates and rising levels of unemployment put pressures on the German economy. Growth rates had been unusually low especially since unification and businesses, politicians and the public increasingly attributed this to the outdated tax system (Lieberman, 2000; Streeck, 2009). Once in office, in 1998, the so-called ‘modernisers’ won increasing support in the red-green government and pushed for a tax plan in support of MNCs and finance (Rademacher, 2017: chapter 7). The new strategy was to liberalize corporate finance for large MNCs to allow for self-finance in SMEs and to dismantle patient capital which limited growth prospects in venture capital markets.

Savings banks as guardians of patient capital (1990–1999)

Much of the existing literature explains the continuity in the German corporate tax system as a result of the complementarity of the German institutional mix of long-term loans, industrial relations institutions and corporate taxation (Hall and Soskice, 2001; Mares, 2006). This section will demonstrate that continuity in the tax system was less a function of complementarity, but of the entanglement of interests of economic and political actors in German electoral institutions.

Since the 1970s, businesses in the export sectors – metal, automobile and chemical sectors – had publicly debated the role of high German corporate tax rates for increasingly diminished productive investments and product innovation (Lieberman, 2000). In response, the Kohl administration proposed two larger tax cuts which planned to support investment. The Tax Reform Act 1990 proposed a moderate reduction of CIT for retained earnings – from 50 to 45 per cent – and a top PIT rate reduction on business income – from 56 to 53 per cent. The Location Preservation Act 1994 planned another 5-percentage point CIT reduction on retained earnings and a 4-percentage point reduction in the top PIT for business income (Prasad, 2006; Zohlnhöfer, 2001). Additionally, the government planned to eliminate the financial transaction tax (Börsenumsatzsteuer) to strengthen the German stock market (DIP/11/2157). Since state governments worried about their budgets, the government proposed to raise DM 4–5 billion extra revenue through a new 10 per cent withholding tax on interest income (Findling, 1995: 173).

This proposed tax rate on interest income was the first measure which encountered considerable resistance by economic actors entangled with the state. While the government presented this tax as one that was predominantly closing loopholes of tax minimizing practices of German commercial banks (PA/XI71/A2/18, pp. 24), the 10 per cent withholding tax on interest income was also to be levied on operations of savings banks. In the early stages of the deliberation process (in February 1988), the entire banking sector – private and public banks – lobbied against it arguing that the tax would hurt the German loan market, raise the cost of finance and curb available resources in the capital market (PA/XI71/B2/39; PA/XI71/B2/42).

Once the debate moved to the Bundesrat, the arguments of the public banks were adopted by state governments. Representatives argued that placing taxes on banks of the public right was not an effective approach of revenue recovery because it indirectly raised costs for federal states and municipalities. A majority in the Bundesrat suggested to exempt these banks from the tax entirely. The institutes of the public right had after paragraph 5 section 2 income tax law ‘special responsibilities’ which included support of the housing market, improving the regional economic structure, and strengthening local competitiveness (PA/XI71/A2/17, 570. Finance Committee, 14.04.1988, pp.82, 83). Moreover, municipalities held silent partnerships in the public mortgage banks (Hypothekenbanken) which would get more costly if these entities had to pay higher tax (PA/XI71/A2/17). The fact the Bundesrat argued that these institutions should be excluded from the tax (PA/XI71/A2/18, pp. 52), indicates how difficult it is to disentangle institutions which generate shared interests of the state and economic sectors.

Commercial banks and the financial sector did not hold comparable ties in the Bundesrat. The Federal Association of German Banks (Bundesverband deutscher Banken) wrote several letters to the Bundesrat arguing that commercial banks required protection from the competition of the advantaged savings banks and could not bear further preferential treatment for those entities. While the overall rate reduction for businesses – the top PIT rate reduction from 56 to 53 per cent and the corporate income tax from 56 to 50 per cent – evened out the traditional favouritism of the savings banks-because private banks mostly grant credit to corporations and savings banks cover SMEs, the planned additional unfair tax treatment of interest income would reinstate unfair competition between the two sectors (PA/XI71/B2/42). But the savings bank privilege remained untouched.

Similarly, although the government planned to abolish a financial transaction tax to enhance wealth building in the German economy, this element of the tax plan did not pass the Bundesrat. The government argued that the tax hindered the mobility of financial capital which generated economic disadvantages for finance in Frankfurt. The Bundesrat almost unanimously (10 of 11 votes) rejected the proposal arguing that the costs of losing revenue of DM 600 million – a rather minor figure – outweighed the benefits of enhancing the German financial market (PA/XI71/A2/17, pp.112). Baden-Wurttemberg, Berlin and Bavaria argued ‘it is desirable but currently not affordable’ (PA/XI71/A2/18, pp. 70).

The second source of gridlock were the entangled relations of the governing parties with business interests. The individual representation of SMEs, small firms and farmers in the coalition required an inclusive approach to reform. The small firms and farmers were disappointed that corporations received a larger tax reduction than smaller firms which filed taxes as individuals – the top PIT was only reduced from 56 to 53 per cent. Thus, to get the support of the FDP and the CSU in the Bundesrat, the Finance Minister Stoltenberg had to offer a compromise in the finance committee. He added special depreciation allowances for SMEs, a cut in the wealth tax of small firms and improvements in the treatment of pension schemes for freelancers and small firms. These amendments won support of sufficient votes in the Bundesrat but reduced the revenue recovery from DM 19 to 9 billion (PA/XI/71/A5/113).

While much smaller, the Location Preservation Act of 1994 also planned to raise revenue through reductions in tax concessions. DM 8 billion were supposed to get recovered through a reduction in the degressive depreciation schedule (degressive Afa) (DIP/12/4487, pp. 31). This reform provided greater benefits for SMEs through a significant top PIT rate reduction (from 53 to 44 per cent), but big businesses were losing out from the Afa reduction. Small businesses, for instance the crafts-business association ZDH, ‘fully backed’ tax cuts (PA/XII66/A3/58, pp. 1), but the BDI and the DIHT (large and medium-sized firms) viewed reductions in the degressive AfA as ‘a serious problem’ (PA/XII66/A3/58, pp. 2). Again, entangled interests made it difficult for the government to implement reductions in tax concessions. The opposition and a number of CDU-led governments voted against the reductions in the degressive AfA (PAXII/242/A1/6, pp.20–22) since the bill only raised 3 billion instead of DM 8 billion in extra revenue, the scope for further rate reductions was significantly curbed (BMF, 2014: 74–76).

Finance and the export sector as promoters of a liberalized system (1999–2005)

The literature on German corporate finance has shown that increasing capital market finance of MNCs instigated an erosion of the German system of patient capital (Beyer, 2003; Höpner and Beyer, 2004; Höpner and Krempel, 2004). However, this trend not only changes the economic sphere, but also opened political opportunities. When the Red-Green government proposed radical corporate tax reforms in the late 1990s, it forged a new coalition of the financial sector and large internationally operating corporations. Thus, instead of bringing all business groups into their tax coalition, the new government selected specific interests which received benefits, while broadening the base among the outsiders of the coalition.

The new growth strategy under the red-green government aimed at radically reduced tax rates and a new system of corporate finance to attract investors and generate capital for young high-tech firms and start-ups in the software and biotechnology sectors (Spiegel, 2000). Two reforms radically reduced the CIT on retained and distributed profits from 45 and 30 per cent to 25 per cent (Bach et al., 2014: 119). Moreover, the Tax Reduction Law 2000 entailed a very focused programme to support MNC finance which simultaneously dismantled patient capital. Revenue recovery was composed of the cutting of several tax concessions for SMEs – the co-entrepreneur waiver, and the swap assessment – and the elimination of the savings bank privilege (von Rosen, 1999: 654; PA/XIV/16/B3/96, p.6).

One of the key instruments of the Tax Reduction Law 2000, which generated strong business support for the project, was the plan to implement a new system of dividend taxation which provided systematic shareholder relief – especially for foreign investors. The former imputation system deducted the corporate income tax from the income tax of the shareholder which benefitted domestic investors who paid German income tax but rendered foreign investors subject to double taxation (PA/XIV154/A6/111, pp. 11). The government considered the imputation system an obstacle for the attraction of foreign investment and the growth of German export businesses because it repelled foreign investors and complicated joint-ventures (PA/XIV154/A4/88, pp. 54). The new half-income system was supposed to attract investments from abroad and open international capital markets to German corporations (Brühler Kommission, 1999). The systems change was complemented by changes in capital gains taxation: Capital gains from the selling of corporate shares became tax free when shares held in a firm were below the threshold for significant participation – effectively abolishing the block-shareholding in the Deutschland A.G. (PA/XIV154/A6/111, pp. 9–11).

Resistance formed in the parliamentary discussions among the traditional coalitions of the SMEs, the savings banks and the federal states. Business associations representing SMEs – the ZDH, the German Crafts Association and the DIHT – argued that the capital gains tax cut unevenly benefitted corporations (PA/XIV154/A4/88, pp. 133; PA/XIV154/A4/88, pp. 50). Smaller businesses also worried that by eliminating the savings bank privilege, loans would get more expensive (PA/XIV154/A4/88, pp. 51). Since the CDU supported SMEs and the CSU and the FDP were close allies of smaller businesses, conservative state governments blocked the proposal in the Bundesrat (PA/XIV154/A4/88, pp. 139; PA/XIV154/A2/40; PA/XIV154/A6/111; PA/XIV154/A6/103, pp. 44). The Bavarian government complained that farmers and forestry received the smallest benefits but suffered significant losses from the reductions in special tax concession for SMEs (PA/XIV/A1/2, pp. 125).

To work against gridlock, the government engaged in a divide and conquer strategy and ‘split existing coalitions’. While strengthening the coalition of SMEs and federal state governments, it excluded the savings banks from the arena of deliberation. Most relevant in this respect was the setting up and staffing of the ‘tax reform commission’, which brought representatives of BDI (MNCs), DIHT (SMEs) and the federal states together and made the DIHT tax expert Alfons Kühn the chairman of the commission (PA/XIV154/A6/111, pp. 9; PA/XIV154/A4/88, pp. 57). The effect of this setup was that the DIHT (SMEs) increasingly felt responsible for the interests of other important business interests represented in the commission, most notably MNCs, while letting go of the alignment with the savings banks (PA/XIV154/A4/88, pp. 79). Statements like ‘various mergers with German firms could not take place in Germany because we have the full-income system’ (PA/XIV154/A4/88, pp. 79) and the system change could double the number of shareholders which ‘enhanced the risk and shareholder culture in Germany’ (DIHT, 2000) are a testimony to a shift in interest towards capital market liberalization.

The outcome of this strategy was a tax plan which incorporated the interests of the MNCs and SMEs. The commission developed a plan which supported capital-market finance (requested by MNCs) and self-finance (requested by larger SMEs) while further curbing tax support for loan finance (PA/XIV154/A6/111, pp. 9; XIV154/A4/88, pp. 57). The DIHT summarized its mission as making corporations and SMEs independent from the German hausbank relationship and ‘turn firms [themselves] into savings banks’ (PA/XIV154/A4/88, pp. 133). Capital gains tax on the selling of block shares would be eliminated to ‘break up the encrusted German shareholder structure’ (PA/XIV154/A4/88, pp. 133), and a system change in dividend taxation would increase investments of foreign investors into German corporations (PA/XIV154/A6/111, pp. 9; PA/XIV154/A4/88, pp. 57). Lower tax rates on retained and distributed earnings allowed for ‘let[ting] profits sit in the corporation, cumulate and through the realisation of earnings through the selling of shares make a good cut’ (PA/XIV154/A4/88, pp. 133).

The second strategy to limit the power of the existing coalitions was to introduce outsider interests and to ‘forge new business coalitions’. The German Shareholder Institute (Deutsches Aktieninstitut), an association which had not played a role in previous tax reforms, was introduced as one of the main players in the debate. It was highly supportive of those elements of the reform which promised a restructuring of German firms. For instance, by reducing the co-entrepreneur waiver and the swap assessment – tax concessions which helped larger SMEs to expand and produce abroad – the Mittelstand had strong incentives to restructure which opened up new capital sources to capital markets (PA/XIV154/A4/88, pp. 134; PA/XIV154/A4/88, pp. 131). Moreover, the association argued that the capital gains tax reform liberated capital locked-in in the Deutschland A.G. with positive effects on international financial markets (PA/XIV154/A4/88, pp. 133). This sentiment was shared by BDI which confirmed that the tax reform proposal had created ‘phantasies’ among investors abroad which led to a soaring of share prices (PA/XIV154/A4/88, pp. 133).

The third state strategy was to ‘disentangle’ the interests of the federal states and the savings banks. Initially, the states opposed the radical CIT cuts because with the existing imputation system, which credited the CIT against the PIT, the states which collected 50 per cent of the latter would have suffered significant revenue losses (PA/XIV154/A4/88, pp. 79). For instance, the minister president of North-Rhine Westphalia argued in a hearing that: ‘If you want to keep the imputation system, but at the same time support the definitive taxation of the CIT with 25 per cent, this is unaffordable’ (PA/XIV154/A6/111, pp. 12). To gain the support of the federal states, the government presented the half-income system as one that recovered much of the revenue loss of the federal states. There were estimates that the half-income system would limit the revenue loss from the CIT cut by 2.5 billion for the federal treasury and 2.3 billion for the federal states (PA/XIV154/A6/111, pp. 7; DIP/14/2683, pp. 103).

Another powerful budgetary argument was that the former imputation system was particularly prone to tax evasion. Under the imputation system, foreigners could engage in so-called dividend stripping, a practice in which foreign investors sold their shares to German residents at a predetermined buyback price. Both financial actors benefitted, but the treasury incurred significant losses. The government tied the argument in favour of the system change to the goal to reduce such practices (von Rosen, 1999: 658; PA/XIV154/A6/111, pp. 9–11). It argued that it included a reduction of the significant participation from 10 to 1 per cent into the tax plan, for the very reason that the simultaneous reduction in tax rates on distributed and retained earnings allowed for tax saving models (PA/XIV154/A4/88, pp. 133).

These strategies generated very high levels of support for the bill in the Bundesrat. The vote margin in favour of the reform was 41:28 and thus included a significant share of votes from opposition governments (Ganghof, 2004: 101). It resulted in a large tax cut – volume of DM 31 billion – which entailed a significant reduction in the CIT (BMF, 2014: 113–117).

Conclusion

This paper started from the puzzle that after a long period of resilience in the German corporate tax regime, a radical reform was implemented which shifted tax support from savings banks and SMEs to MNCs and finance. Aside from the general reduction in corporate tax rates, the reforms facilitated capital-market finance of large export businesses. This distinguishes German reforms from the general trend in OECD countries, in which tax reductions for MNCs were accompanied by significant tax cuts for individuals and financial incomes.

This unique process and structure of German corporate tax reform provides us with a useful case to test this special issue’s question of contested neoliberalism. The special issue argues that neoliberalism is contested not just because of the many interpretations that developed in 40 years of academic debates, but also because of neoliberalism’s nature, its contextual occurrence and local variegation. The special issue finds that neoliberalism is a consequence of common economic pressures of globalization but becomes localized within the state. The state responds to and embodies neoliberal transformations. This dual nature of neoliberalism has contributed to its theoretical and conceptual elusiveness. On the one hand, the classical thesis that neoliberalism instigates a convergence of Western capitalism to one liberal model did not materialize. Today, scholars largely agree that local differences between domestic regimes prevailed. However, the comparative literature’s conclusion that coordinated market economies were resilient (Hall and Soskice, 2001; Mares, 2006), or that the process of neoliberalization would be confined to incremental processes of ‘drift’ and ‘erosion’ (Streeck, 2009; Thelen, 2014, 2019), make it difficult to understand radical but variegated changes in domestic economies. This special issue intends to highlight radical change but acknowledge local implementation.

Applying this approach to the German case of corporate tax reform, this paper finds that radical reforms originate from state actors’ active involvement in economic development and are shaped an array of ‘economic relations’ between the state and businesses. In the German case, economic relations consisted of an entanglement between businesses and parties in consensual institutions of federalism and proportional representation. This structure is particularly hostile to change because governing parties represent certain business groups in parliament. The process of breaking up entanglement shaped not only the pace of reform but also its outlook. Successful tax cuts could only be implemented once the red-green government ‘split’ existing coalitions, ‘forged new coalitions’ and ‘disentangled interests’. The resulting new coalition of MNCs and finance supported the new structure which granted large exporters greater freedom to finance in international capital-markets.

This finding has implications for our understanding of the role of neoliberalism in contemporary capitalism. The fact that German neoliberal tax reforms came late and differed from the liberal model does indicate that neoliberal dynamics vary. The case invites us to rethink the interaction of globalization with institutional context and sheds light on the constraints imposed on officials and their strategies to supervene these to implement new growth strategies.

Supplemental Material

sj-pdf-1-cch-10.1177_1024529420985174 - Supplemental material for The entangled state: How state-business relations shaped the German corporate tax regime

Supplemental material, sj-pdf-1-cch-10.1177_1024529420985174 for The entangled state: How state-business relations shaped the German corporate tax regime by Inga Rademacher in Competition & Change

Supplemental Material

sj-pdf-2-cch-10.1177_1024529420985174 - Supplemental material for The entangled state: How state-business relations shaped the German corporate tax regime

Supplemental material, sj-pdf-2-cch-10.1177_1024529420985174 for The entangled state: How state-business relations shaped the German corporate tax regime by Inga Rademacher in Competition & Change

Footnotes

Acknowledgements

I have presented an earlier version of this paper at the workshop ‘Economic policy-making institutions at the state/market frontier’ where I received very helpful comments by Matthew Watson, Craig Berry and Florence Dafe. I also presented the paper at a workshop at King’s College ‘The Return of Intervention? Industrial Capacity of the State after the Financial Crisis’ where Scott Lavery, Manolis Kalaitzake, Neil Dooley and Victoria Stadheim commented on the paper. I would also like to thank Betsy Carter and Engelbert Stockhammer for reading the manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Appendix A

Documents used for the empirical analysis (alphabetical order):

DIP/11/2157 – Deutscher Bundestag: Gesetzentwurf der Fraktionen CDU/CSU und FDP. Entwurf eines Steuerreformgesetzes 1990; 11.04.1988; 11. Wahlperiode; available at ![]() .

.

DIP/12/4487 – Deutscher Bundestag: Entwurf eines Gesetzes zur Verbesserung der steuerlichen Bedingungen zur Sicherung des Wirtschaftsstandorts Deutschland im Europäischen Binnenmarkt (Standortsicherungsgesetz – StandOG); 05.03.1993; 12. Wahlperiode; available at: ![]() .

.

DIP/14/2683 – Deutscher Bundestag: Gesetzentwurf der Fraktionen SPD und BÜNDNIS 90/DIE GRÜNEN Entwurf eines Gesetzes zur Senkung der Steuersätze und zur Reform; 15.02. 2000; 14. Wahlperiode; available at: ![]() .

.

PA-DBT 3107 Finanzen XI/71 Bd. A2 lfd. Nr. 17.

PA-DBT 3107 Finanzen XI/71 Bd. A2 lfd. Nr. 18.

PA-DBT 3107 Finanzen XI/71 Bd. A5 lfd. Nr. 113.

PA-DBT 3107 Finanzen XI/71 Bd. B2 lfd. Nr. 42.

PA-DBT 3108 Wirtschaft XII/242 Bd. A1 lfd. Nr. 6.

PA-DBT 3107 Finanzen XII/66 Bd. A3 lfd. Nr. 58.

PA-DBT 3106 Haushalt XIV/154 Bd. A2 lfd. Nr. 40.

PA-DBT 3107 Finanzen XIV/154 Bd. A4 lfd. Nr 88.

PA-DBT 3002 Gemeinsamer Ausschuss XIV/154 Bd. A6 lfd. Nr. 111.

PA-DBT 3111 Agrar XIV/154 Bd. A1 lfd. Nr. 2.

PA-DBT 3107 Finanzen XIV/16 Bd. B3 lfd. Nr. 96.

PA-DBT 3108 Wirtschaft XIV/154 Bd. A6 lfd. Nr. 103.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.