Abstract

This paper is concerned with the distributional effects of the deregulation and privatization of essential services in Britain since the 1980s, based on a cross-sector study of water, energy and local bus transport. Our approach locates end users within the structures and processes, and prevailing narratives that underpin both production and consumption. This framework highlights the ways that the provisioning of these vital services is contested, contradictory and underpinned by power relations. We show that, at one end, investors in these sectors have made generous returns on their investments but their methods of profit maximization are often not in the public interest. Meanwhile these profits are financed by end users’ payments of bills and fares. Many lower-income households face challenges in terms of affording, and even accessing, these essential services. Regulation has failed to provide adequate social protection. We argue that adverse social outcomes emerge from systemic factors embedded in these modes of provision. A narrative of politically-neutral, technocratic solutions belies the underlying contested nature of privatized monopolistic shared essential services. Moreover, a policy preoccupation with markets and competition obscures the inequality embedded in the underlying structures and processes and undermines more collective and equitable forms of provisioning.

Introduction

Over the past three decades, households in Britain have become ‘revenue streams’ for global finance via their consumption of essential goods and services such as water, energy and transport facilities (Allen and Pryke, 2013; Loftus et al., 2016; Meek, 2012). Some low-income households have suffered disproportionately, in some cases resorting to extreme coping mechanisms (such as ‘self-disconnection’), and many have failed to be protected by social policy. State intervention is dominated by market-oriented ideology, with policies centred on increasing competition or creating pseudo-competitive constraints on monopolistic providers. We argue that these policies have created adverse social outcomes which result from systemic factors embedded in the underlying processes and structures by which privatized services are provided.

In constructing these services in market form, providers and end users have been redefined as investors and customers. For consumers, the process of ‘market-making’ imposes a responsibility to manage access and affordability, ostensibly in isolation from the underlying production processes. The state has multiple and contradictory roles, charged with both protecting the rights of citizens and residents as well as creating an attractive investment climate. As we discuss below, a narrative of neutral technocratic solutions belies the underlying contested nature of private provision of monopolistic shared essential services, and the seemingly technical task of regulation is infused with political judgements.

Our approach connects investors with end users as part of an integrated system with attention to the structures, the core agents and the financial flows as drivers of inequality. This paper begins in the following section with an overview of privatization in Britain, and the way this has developed in practice in each of these sectors. This is followed by three separate sections each devoted to a segment of agents in the system: producers, consumers and the state. These sections are connected by the theme of the revenue stream. The final section concludes.

Overall our analysis shows that provisioning systems for these vital services have been consistently configured in the interests of producers rather than consumers, and high returns to capital at household expense have been tolerated, and even encouraged, for many years. For low-income households this can translate into multiple deprivations, as is demonstrated in these three essential services. Recent regulatory moves towards tighter controls are not embedded in the regulatory process but have emerged in response to political pressure. Elsewhere in the economy, a bias towards capital at the expense of households has been observed in the wake of the 2008 financial crisis. For example, the share of gross domestic product allocated to labour has fallen (Kohler et al., 2018) and the post crisis ‘recovery’ is regressive (Dagdeviren et al., 2020; Meek, 2012). This paper contributes to this literature, indicating that a similar bias in favour of capital can be found in the ways in which basic needs are met in Britain.

Background: The systems of provision approach and privatization in Britain

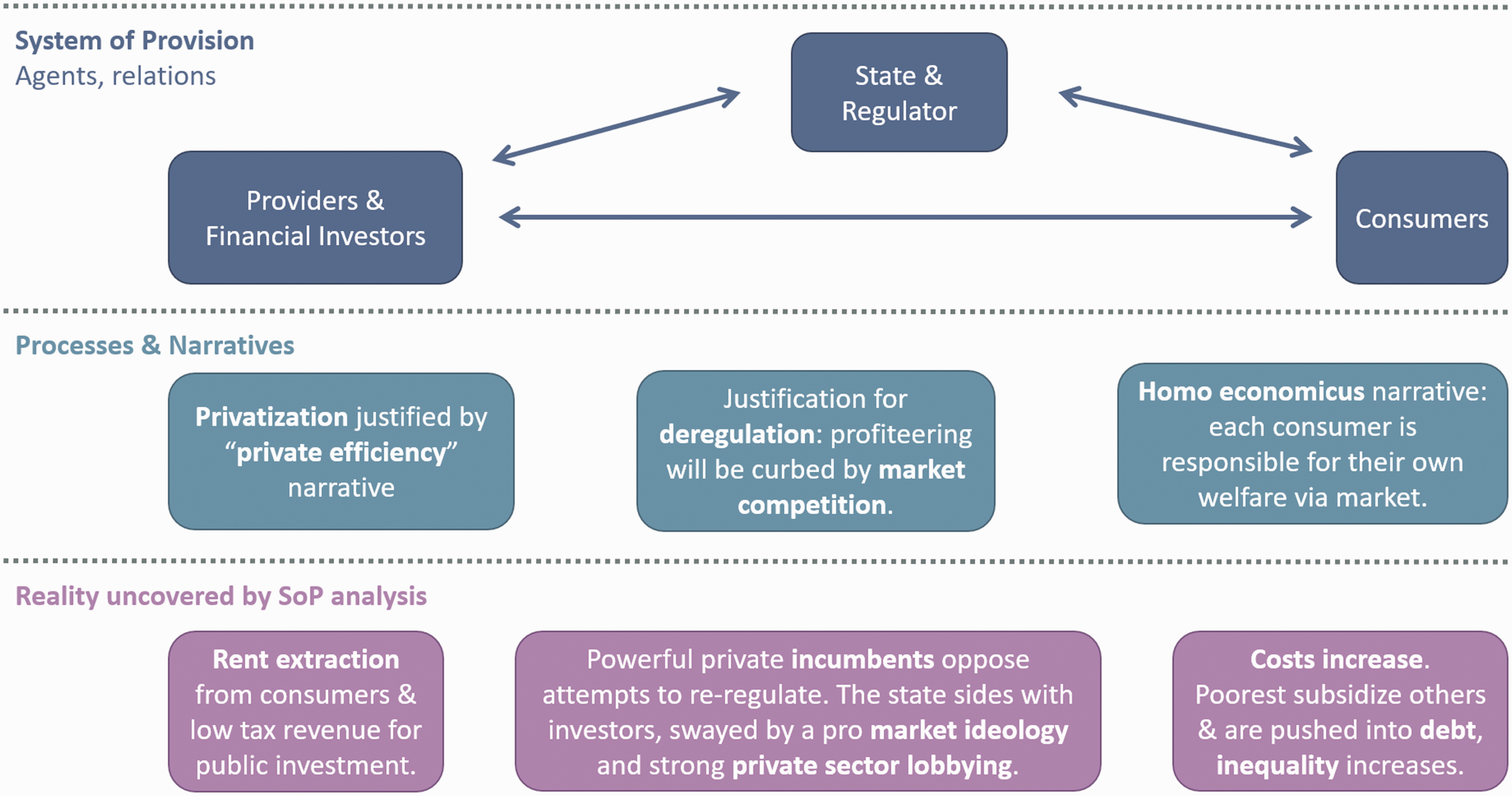

Our analysis draws on the systems of provision (SoP) approach (Fine et al., 2018), which contends that consumption is integrally connected to the ways in which services are provided. As such, agents in the chain of provisioning, including consumers and producers as well as the state (and sub-groups within these) are assumed to have complex and competing priorities, and outcomes are contested. These vertical chains of provision intersect with cross-cutting structures and cultures so that each SoP is highly context-specific and influenced by the materiality of what is provided. Systems are maintained by prevailing narratives. The approach effectively lifts the lid on the social relations which underpin specific consumption outcomes (see, for example, Mattioli et al., 2020 on the political economy of car dependence). In the context of this paper, the approach provides a systematic framework for analysing the complex relations between ‘consumers’ (or end users) and other agents within the system by which essential services are provided (Figure 1).

Schematic depicting the agents and relations studied through Systems of Provision (SoP).

A starting point for the SoP approach is the context within which the system is located. This section provides a brief overview of the spread of privatization and its effects in each sector. While privatization in different forms has been taken up across the world, the style and reach in Britain, originating with the Thatcher Government of the 1980s and 1990s, has been more extreme than elsewhere.

In water, upon privatization in 1989, the 10 public regional water and sewerage monopolies in England and Wales (and some smaller water-only companies) were listed on the London Stock Exchange (LSE). Water in Scotland and Northern Ireland was not privatized. The dispersed ownership of the early 1990s quickly gave way to consolidation as shareholders built their market share. Only three water and sewerage companies remain listed on the LSE, while six are owned by private investors and one (Welsh Water) by a not-for-profit company.

Private water utilities are regulated by a system of periodic price controls, established and enforced by the state regulator, Ofwat. Prices are based on anticipated investment costs and past performance against targets, set in advance for five-year periods. The regulatory process is intended to mimic the market, as private monopolies supposedly become price takers, as they would in a competitive market. Notably, the regulator does not intervene in dividend payouts or corporate structures, deeming these to be market outcomes.

Since privatization, investment and productivity have increased (Frontier Economics, 2017; NAO, 2015), but the record on efficiency gains is mixed (Hall and Lobina, 2008; Saal and Parker, 2001; Saal et al., 2007). Overall, the performance in England and Wales is not significantly better than neighbouring Scotland where water remains in the public sector (Helm, 2020; Thomas, 2019). Financial engineering has boosted shareholder payouts (Yearwood, 2018; Helm, 2020). England and Wales have among the highest bills compared with other European countries (Helm, 2020).

In energy, the gas and electricity sectors in Great Britain 1 have been unbundled, each into four constituent parts: generation, transmission, distribution and retail. For electricity this happened as part of privatization in the 1990s. For gas, the process took considerably longer (Thomas, 2016). Transmission and distribution networks were considered to be monopolistic and these were created into private companies initially by listing them on the LSE. All energy transmission and distribution networks have since been delisted from the LSE and are privately owned. A separate company operates the national grid for both gas and electricity. As with water, these monopolistic parts of the energy sectors are regulated by a state regulator, Ofgem, via periodic price controls.

The generation and retail segments, in contrast, were opened up to competition with free entry and exit of providers. Since 1999 consumers have been able to choose their retail energy provider. Retail prices in energy were originally subject to price controls but these were lifted in the early 2000s (IPPR, 2014). However, the energy market has not operated as planned. As Thomas (2019: 220), puts it: ‘the ideal of a liquid, competitive wholesale market feeding into a competitive retail business with consumers choosing the cheapest supplier has never been achieved.’ Despite the introduction of competition, energy retail has been dominated by the so-called ‘Big Six’ vertically integrated incumbent energy companies, typically providing both electricity and gas. 2 While their market share has fallen from 98% in 2013 to 80% in 2019, still the majority of customers does not switch their provider in response to price signals, and there is extensive mistrust of the energy sector and retail competition (Thomas, 2019). Meanwhile, gas and electricity in the wholesale ‘market’ is primarily sold via ‘self-dealing within the Big Six or long term confidential contracts’ (Thomas, 2019).

Prior to the Transport Act 1985, local bus provision was regulated, and most of the bus industry was owned by (either national or municipal) public companies. The 1985 reforms privatized much of the industry and introduced ‘quantity deregulation’ outside of London. This meant that bus companies became free to provide (and withdraw) services as they pleased, with little more than formal notice to the Local Authorities. This was intended to encourage competition between a multitude of small private operators, with positive effects on public transport provision (Banister, 2002; Wolmar, 1999). In contrast, in London a public agency (Transport for London) retains strategic control of public transport provision, while operations are tendered to private firms.

While there are disagreements regarding the best model of provision for local bus transport (see, for example, Currie, 2016; Mees, 2010; van de Velde and Wallis, 2013), the English deregulated approach is widely considered as a failed experiment. Broadly speaking, bus provision in England has underperformed comparable systems, both in London and abroad, in terms of affordability and supply of services (Campaign for Better Transport, 2019; Preston, 2003), deterioration of service provision due to ‘fragmentation effects’ (O’Sullivan and Patel, 2014), and resulting negative impacts on social inclusion for low-income households (Crisp et al., 2018). Much of the problem results from the rapid consolidation of the market in the wake of privatization, so that a few operators operate as near monopolists in local areas.

The privatization of essential services in Britain went considerably further than elsewhere in the world. Only Chile has fully divested its water services. In energy, while retail competition has been introduced elsewhere, Bulgaria is the only other country in Europe that has divested its networks to foreign owners (ECIU, 2017). In local public transport, the British model of ‘quantity deregulation’ is an outlier among OECD countries (Mattioli et al., 2020; Mees, 2010). Privatization and deregulation were part of a programme, which evolved incrementally in the 1980s with no master plan (Bayliss, 2014). The policies were presented as mechanisms to bring investment and efficiency through competition building on a narrative of poor state performance. While the main public-facing argument was one of better and cheaper services for customers, the full agenda was one of private acquisition of state assets. However, as we discuss, outcomes are complex and contested. In water, there has been extensive investment as intended but this is financed by high-cost debt, which feeds through to household bills. In energy, competition has been effective in driving down prices for some, but this has been financed by those that are less active (and more vulnerable) in the market. In bus transport, initial generous provision and price reductions from competition gave way to inflated prices and curtailment of uncommercial bus routes, although these had been socially valuable. At the same time, private investor profits have soared. Overall, then, the case for privatization and deregulation is far from compelling. As demonstrated in other sectors (Bowman et al., 2014), privatization and deregulation can create industries that do not serve national welfare interests, for example, with the use of extractive business practices such as curtailing investment in order to maximize profits.

Producers: Investors and investment practices

This section examines the investors that own the companies that provide water, energy and bus transport. The section goes on to highlight some of the methods of profit generation (or outright profiteering) practiced by these companies.

Investors

There has been a marked shift in the type of owners of the monopolistic water utilities and energy transmission and distribution networks since the mid-2000s in England and Wales. Traditional infrastructure companies (RWE, Vivendi, Suez) have been largely replaced by financial investors including pension funds, sovereign wealth funds, global conglomerates and private equity investors and investment funds. Some financial investors use intermediary special purpose vehicle (SPV) companies set up offshore to buy utilities. The world’s richest are represented in the high net worths that contribute to the funds of asset managers, as well as the direct shareholders. In some cases the ultimate owners are unknown companies registered in the Cayman Islands (Bayliss, 2014).

The ‘competitive’ retail elements attract a different kind of investor. In energy, mostly these are listed companies (such as SSE and Centrica which owns British Gas) or subsidiaries of companies listed elsewhere (NPower, Scottish Power and Eon). Investors also include state subsidiaries of foreign governments such as EdF Electricity which is majority owned by the Government of France.

For bus companies, rather than de-listing from the LSE, ownership structure travelled in the opposite direction as small-scale private owners, which emerged in the aftermath of the 1985 reforms, expanded before launching on the LSE. Local bus provision is now dominated by a small number of large operators, which are often de facto monopolists in local areas (Competition Commission, 2011). In 2015–2016, three companies, Stagecoach, FirstGroup and Arriva, accounted for more than half of all bus journeys in England (excluding London) (DfT, 2016). These companies are listed on the LSE, and financial investors are strongly represented among shareholders. Also, the German Government has a stake in Arriva via Deutsche Bahn. Deregulation has generated extreme wealth for some. The founders of Stagecoach, Brian Souter and Ann Gloag, share eleventh place in the Scottish Rich List with net worth of £920 m each (Brinded and Colson, 2017).

From business opportunity to exploitation

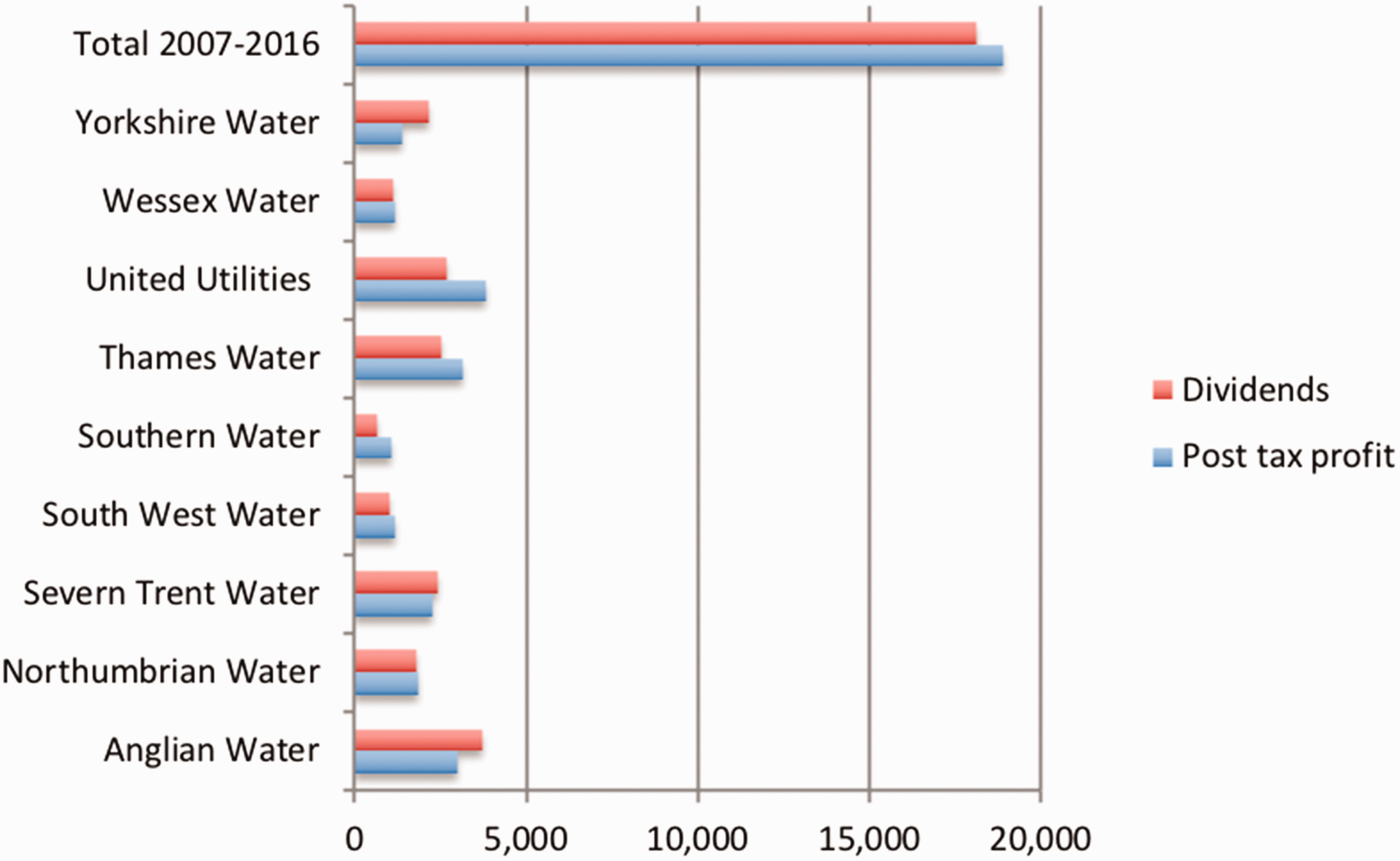

Investors have boosted shareholder revenues through diverse means unrelated to productivity. In water, investment has been debt-financed and almost all post-tax profit was taken out as dividends over the decade to 2016 (Figure 2). Private equity-owned water utilities have securitized future water bills to increase company debts. The increased debt has been used not just to finance investments but also to pay ‘special dividends’ and to refinance so that the ‘acquisition debt’ (i.e. the cost that the investors incurred to buy the utility) is allocated to the regulated utility and financed by consumers (Bayliss, 2014). These companies pay little tax (Bayliss and Hall, 2017). However, the full nature of financial engineering is obscured by the complex water-related financial products and instruments that have been devised to boost extractions as well as opaque corporate structures (Loftus et al., 2016; Pryke and Allen, 2019). Thames Water has been particularly aggressive in its financing structures. Customer bills were securitized for a 50-year period, up to 2062 (Allen and Pryke, 2013) so bill payments will, for decades, be paying off debts used in part to finance dividends paid in the 2000s and 2010s. Such transactions escape regulatory control as capital structures and dividend payouts are deemed by the regulator to be ‘market outcomes.’

Dividends and post tax profits for England’s water and sewerage companies ([£m] 2007–2016).

Similar high returns have been observed in the regulated energy networks where prices are higher than necessary (Helm, 2017). Research by the ECIU (2017) found that the distribution network operators reported net profit margins in the range of 25–39% per annum. They calculate that the average dividend payout was 15% of turnover, equivalent to £13 of the average domestic bill (ECIU, 2017). Research for Citizens Advice Bureau also found that consumers were over-paying for distribution networks by £7.5 billion a year (Wild, 2017). These high returns have in part been attributed to lenient regulation which, for example, has been generous in its estimates of the risk levels companies face (Wild, 2017).

In competitive areas, energy firms have taken advantage of the least proactive customers. A 2015 investigation by the Competition and Markets Authority (CMA, 2016) found that domestic energy price increases for the Big Six created a ‘detriment’ (i.e. the value of overcharging) to domestic customers of around £1.4 billion a year. Higher prices were charged to the 70% of consumers that had not moved to cheaper tariffs (Waddams Price, 2018), although the details of the calculations are disputed (Littlechild, 2017).

In addition, all of the Big Six have been fined since 2013 for ‘mis-selling,’ i.e. trying to attract new customers with misleading information or for poor customer service. Ofgem has continued to fine companies for these offences at regular intervals since retail competition was introduced nearly 20 years ago. In December 2015, Ofgem imposed its largest fine to date of £26 million on Npower for ‘failing to treat customers fairly’ (Ofgem, 2015) in their billing and complaints handling. Rather than indicative of regulatory enforcement, Thomas (2016: 46) suggests that, as this was the eleventh fine imposed on the Big Six in five years for similar violations, it is indicative of ‘Ofgem’s impotence with regard to effecting behavioural change [in producers].’

In bus transport, competition was intended to lower prices and improve services. However, an initial phase – known as the ‘bus wars’ – characterized by overprovision and fierce competition between operators, was followed by rapid market consolidation. Larger companies were able to undercut competitors with low, loss-making fares. Some 34 years after privatization, the bus market is characterized by strong barriers to entry because of the economies of scale from which the big players now benefit (Competition Commission, 2011). Large companies use cross-subsidies to drive smaller competitors out of business but not to sustain unprofitable routes for social purposes (Wolmar, 1999).

Thus, in each of these sectors firms have boosted profits via aggressive and innovative practices unrelated to production. Crucial local services have become cogs of investment wealth generators, subject to decision-making to meet commercial priorities established in distant head offices, segregated from local authority control. In return for high dividend payouts, directors earn high salaries, over £2 million in some cases (Bayliss, 2014) also financed by consumers. These examples of regular practices of rent extraction, translate into systemic upward pressure on prices and downward pressure on standards across this combination of essential services, combined with a collective failure of the state to protect end users, discussed further below.

Consumers

Since the financial crisis, the socio-economic climate in the UK has been dominated by a ‘regressive recovery.’ Government policy has been directly supportive of returns to asset holders, promoting corporate profitability at the same time as cuts in welfare and an increase in precarious and low paid employment have penalized low and middle-income wage earners (Green and Lavery, 2015). Austerity Britain has led to intense hardship for a growing number of households affecting key aspects of everyday life. Indebtedness is on the increase for low-income households, not for indulging in luxuries but simply in order to pay for essential needs, such as food, shelter and key services. Many of these households face difficulties meeting payments across all essential expenditures (Dagdeviren et al., 2020). Policy narratives have shifted the responsibility to individuals for managing the affordability of basic services, masking the structural and systemic causes of increasing deprivation, such as the changes in the labour market, and the welfare system (Dagdeviren et al., 2020). Similarly, access to services is framed in terms of the actions of the individual user with little attention to the social relations and structures that underpin the system by which services are provided. As in other sectors, state policy is blinkered by ‘imaginaries’ of markets and competition (Bowman et al., 2014).

Affordability

While there is no official definition of ‘water poverty’ there are clear indicators that many struggle to pay their bills. 3 Water bills increased by around 40% (after inflation) on average following privatization but have plateaued since 2000 (Bayliss, 2014). However, affordability has declined due to falling in real wages in the wake of the financial crisis (Dagdeviren et al., 2020). Almost a quarter of households in England has difficulty paying their water bills (Ofwat, 2015). This translates into real difficulties for the poorest households. The proportion of calls to National Debtline relating to water debt increased from 4% in 2008 to 16% in 2018 (Money Advice Trust, 2018).

The extractive practices of producers put upward pressure on prices. For the nine Water and Sewerage Companies in England, interest charged increased from £288 million to over £2 billion in the 20 years from 1993 to 2012 (in 2012 prices) as debt levels rose. In the 2010–2015 period, around 27% of the average bill went to return on capital (i.e. interest and dividend payments) (Bayliss, 2014), all of which is funded by bill payers. In London, an additional separate investment, Thames Tideway, a massive sewerage development, was ultimately funded by an additional levy on Thames Water consumers. This arrangement was needed in part because of Thames’s high existing debt levels (Loftus and March, 2019).

Energy bills are among the most significant expenses for households. In 2016, energy costs accounted on average for around 8.4% of the household income for those in the lowest decile compared 4% for all households (Money Advice Trust, 2018). Overall bills in 2017 were 39% higher in real terms than bills in 2001 (Money Advice Trust, 2018). Many struggle to pay. The proportion of calls to National Debtline that related to energy debt problems increased from 9% in 2008 to 17% in 2017 (Money Advice Trust, 2018). In England, 2.5 million households (11%) were classified as being in ‘fuel poverty’ in 2016 (BEIS, 2018). 4

The past decade has seen a fall in the number of energy customers that are behind on their bills and rates of disconnection for non-payment have fallen (Money Advice Trust, 2018). However, the proportion of customers on energy prepayment meters has doubled from 7% in 1996 to 16% in 2015 (CMA, 2016). When a customer runs into financial difficulty, the supplier can obtain a warrant to force installation of a prepayment meter and customers are often required to pay for the warrant process, further exacerbating their debt (Ofgem, 2018). For years, those on prepaid meters were charged a higher tariff than other consumers until a cap on prices was introduced in 2017 (see below). However, prepaid customers are still penalized because they do not have access to the cheapest tariffs available.

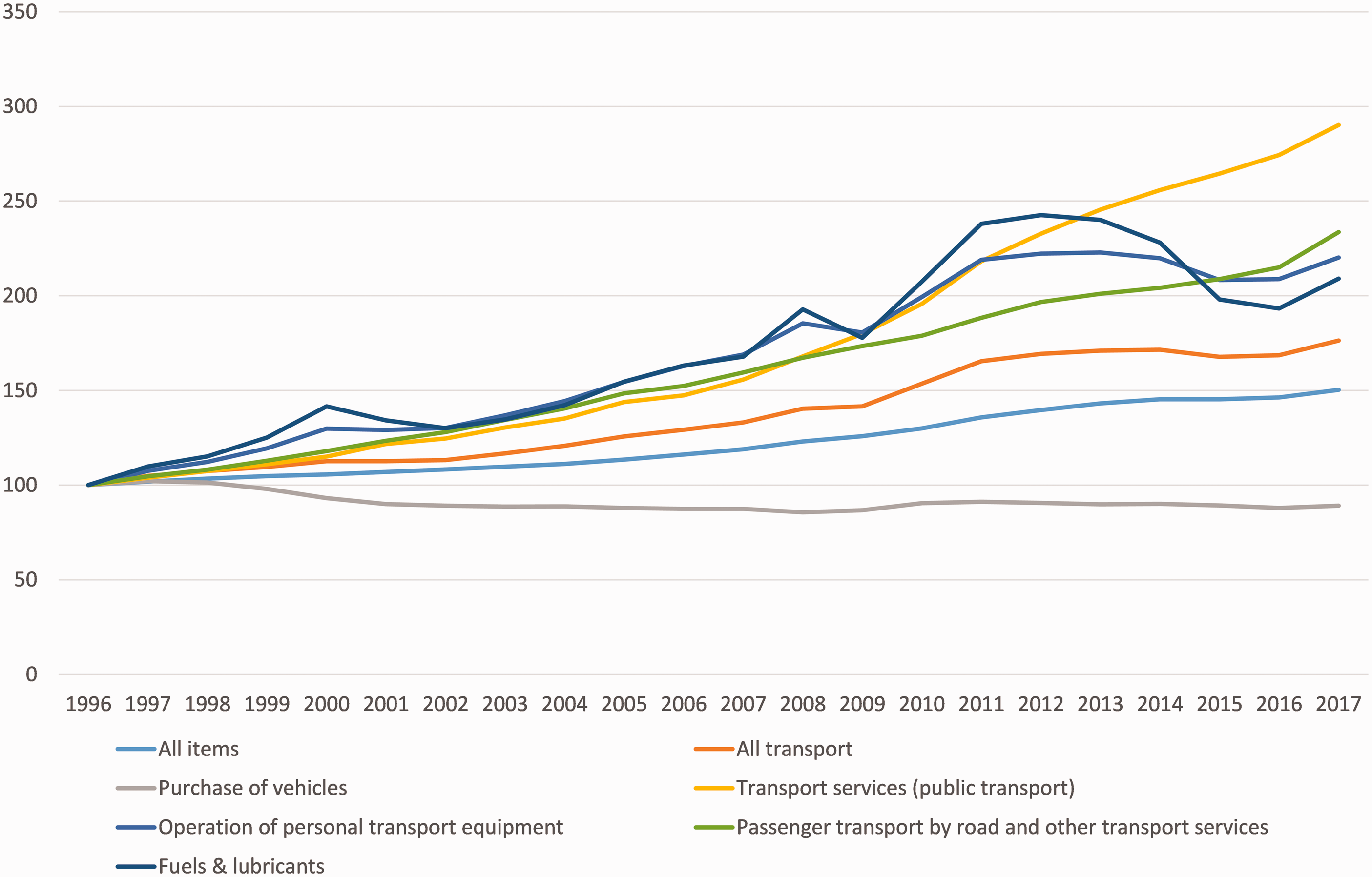

In bus transport, deregulation has been linked to significant fare increases (Banister, 2002; Preston and Almutairi, 2013) and the real cost of public transport has increased more rapidly than other items of expenditure since the 1990s (Figure 3). Deregulation is associated with a reduction in bus travel in part because companies find it more profitable to cut peripheral services leaving many areas with a ‘patchwork quilt of zones where operators may be operating in near-monopolistic conditions’ (Crisp et al., 2018: 52). Furthermore, bus routes are fragmented and uncoordinated with other transport operators (O’Sullivan and Patel, 2004). As Mees (2010) argues, in a competitive market there is no incentive for operators to implement cross-subsidies or coordinate between different modes, routes and operations. Deregulation, then, provides incentives to boost financial returns by ‘reducing or eliminating more peripheral services while concentrating on core corridors’ (Crisp et al., 2018: 53). This penalizes those travelling for reasons other than commuting, as well as commuters with shift patterns in the flexible economy and/or needing access to outlying business parks (as many low-income workers do). Overall, this results in greater car dependence, discussed below.

ONS CPI index for different items of expenditure 1996–2017.

Responsibility as the customer’s burden

With these sectors depicted as markets rather than social or public services, there is increasing emphasis on the savvy consumer to be responsible for their own welfare. In the water and energy sectors, the ethos of the market imposes specific behaviours. These services have become commodities, requiring the user to act as a rational, utility-maximizing, fully informed shopper – in line with the mainstream economic caricature of ‘homo economicus’ (Raworth, 2017). In the energy sector, the consumer is required to seek out the ‘best’ deal from a complex array of tariffs. However, as mentioned, the majority of the population does not change their supplier regularly. The combination of impenetrable information, search costs, inertia, uncertainty and the potential short term of the financial gain mean that not changing tariff could be seen as an entirely rational consumer response (Antal, 2020; Costa et al., 2016).

Lower-income households are penalized by the structures of the energy retail ‘market.’ Those that switch tend to be from higher social grades, have higher incomes, be younger, pay their bills by direct debit and are owner-occupiers or private renters (Ofgem, 2017). Those who are highly disengaged are more likely to be from a lower social grade, to rent social housing, to be non-white and not to speak English as a first language (Ofgem, 2016). Households with limited resources disproportionately avoid behaviours, which might upset their tight financial control, such as switching providers or payment methods or moving to electronic rather than paper billing (Davies et al., 2016). Many on low incomes are effectively excluded from the market due to poor credit history, a lack of access to information and being on prepaid meters (Middlemiss and Gillard, 2015).

In water, metering is seen as an important element in reducing demand to achieve environmental objectives (DEFRA, 2019) and new technology such as the introduction of smart meters in water and energy are promoted as providing greater control of consumption. These provide data and have inspired nudge style practices for example with displays to compare with consumption of other households. However, there are concerns that vulnerable customers are least likely to be able to take advantage of improvements (Waddams Price, 2018). In addition, meters play a role in creating new ‘financial subjectivities within the home’ characterized by ‘disciplined responsible behaviours’ to ensure a continued revenue stream to the financialized entities that depend on them (Loftus et al., 2016: 329).

Where consumption is metered, firms are paid according to units consumed, and therefore benefit from high consumption levels. Yet, demand reduction is essential for sustainability in our water-stressed future. This potential impasse has been overcome by setting ‘demand reduction’ as a performance target for companies (Ofwat, 2019). Thus, if per capita water consumption falls in a specified price review period, the company will be rewarded with a higher price increase in the subsequent price review period. For the consumer, reducing consumption will only save money in the short term and in the end is charged more for consuming less.

While we observe a clear narrative of customer self-responsibilization in the energy and water sectors, the situation is different for buses. Here, reduced bus provision tends to result in greater car dependence for low-income households. For these households, the consumer choice is often equivalent to a ‘choice’ between severe social exclusion and the enforced reliance on a durable good that is expensive to purchase and to run, discussed below.

Coping mechanisms

In the three sectors, consumers deploy coping strategies to deal with high costs and/or reduced services. These include indebtment, self-rationing of consumption, and the shift to other systems of provision, all of which have clear negative consequences for social inclusion. In water, households cannot be disconnected for non-payment of bills. However, water debts are rising and arrears on water bills is the most common type of debt for low-income households (JRF, 2018).

While formal disconnection for non-payment of energy bills has fallen, customers on prepayment meters in financial difficulty are known to self-ration. Ofgem (2018) cites research from the Citizens Advice Bureau, which estimates that 16% of prepayment customers (some 600,000 households) self-disconnect at least once per year by not topping up their meter. Of these, 50% included someone with a mental health condition, 33% had a young child and 87% were in receipt of benefits. Severe self-rationing can cause or exacerbate existing health problems, with potentially devastating results. Research suggests that over 9600 frail and vulnerable were dying in the winter months due to cold homes (NEA, 2017). Qualitative research in the North of England has found that some of the poorest households have literally disconnected the gas supply from their house in order to avoid paying a standing charge and, as a result, have no access to heating. 5

The downward trajectory of local bus transport outside of Greater London since 1985 has arguably contributed to increasing car dependence and an increase in the incidence of ‘forced car ownership’, where low-income households are effectively forced to own and operate cars, despite their substantial cost, because of the lack of practicable alternatives (Currie and Senbergs, 2007; Mattioli, 2017). The number of cars per household in England increased from 0.82 in 1985 to 1.22 in 2017 (DfT, undated), while the percentage of the UK population agreeing that the car is a ‘necessity that adults should not have to do without’ doubled between 1983 (22%) and 44% (2012) (Mack et al., 2013).

Research indicates that 7% of UK households (12% in the lowest income quintile) own cars despite being in ‘material deprivation’ (i.e. not being able to afford at least three necessities), and can thus be described as ‘forced car owners’ (Mattioli, 2017). These households typically have high levels of debt, and suffer from fuel poverty within the home, which may be the result of high expenditure on car ownership, and use leading them to curtail other areas of expenditure. They are also likely to be particularly vulnerable to increases in the price of motor fuel, which has been volatile in recent years (Figure 3). Furthermore, there is evidence that households with low incomes and high motoring costs are unable to reduce their car use when fuel prices go up, with resulting economic stress (Mattioli et al., 2018b).

The widening and deepening of the private sector across essential services represents a major reconfiguration of the relations between households, private capital and the state. Market rhetoric suggests that individuals have agency but this is restricted by the ways that services are provided, and, in some cases, coping mechanisms are leading to (self) exclusion from services. While there is a superficial appearance of individual autonomy, options are narrowed by the structures of the SoP, which are conditioned by producers and the state. This section shows that the situations of households, struggling under welfare and labour policies, are exacerbated by the privatized and financialized provisioning of essential services which have been structured to benefit global private capital. Thus, it is not just that affordability is impinged by lower income levels, but the bills themselves are boosted by profiteering practices, and routes out of poverty are blocked by cuts to transport services that are not commercially viable.

Role of the state

The state consists of many different agencies, from the political party through to civil servants. These may have different, conflicting objectives and influence in policy and practice. Ultimately the state has a responsibility for ensuring that essential needs are met. Yet, wider narratives of private provision, combined with cuts to local government funds have left major gaps. As the UN Rapporteur for Extreme Poverty writes, following his visit to the UK in 2018 (Alston, 2018: 11): Abandoning people to the private market in relation to services that affect every dimension of their basic well-being, without guaranteeing their access to minimum standards, is incompatible with human rights requirements.

Social policy

The state has established social policies in each of these sectors. In water, the WaterSure tariff caps water bills for low-income families with more than three children or with a medical condition, which requires significant use of water. In addition, water companies are required to set up social tariffs for disadvantaged consumers. There are certain restrictions to this. The tariff has to be ‘cost-neutral,’ meaning that the revenue that a company loses by offering a social tariff must be balanced elsewhere, for example by a decline in debt recovery costs (Ofwat, 2011: 4). In addition, since the social tariff is funded by other residential bill payers (nonhousehold customers do not contribute to the social tariff), the subsidy to disadvantaged households must be acceptable to the customers paying for it (DEFRA, 2012). Households are consulted about their views on suitable beneficiaries and appropriate levels of social tariffs, which inevitably draws judgements about deserving and undeserving poor (Bayliss, 2017). Social policy in water, then, is oriented around the business impact of non-payment. The social tariff is associated with a specific understanding of fairness which is more akin to charity, and infused with morality, rather than progressive redistribution.

In energy, there are a number of social initiatives. There is some support for vulnerable customers, for example with the Priority Services Register (PSR) and the Under the Warm Homes Discount. 6 Winter fuel payments are available for older customers but is not means tested. These measures ensure security of supply and improve affordability for some customers although there are concerns that some measures are poorly targeted (Boardman, 2010; Hills, 2012; Preston et al., 2013).

In bus transport, with the 1985 reform, local government retained the power to subsidize unprofitable services that are deemed socially necessary. The national government also subsidizes bus use through the Bus Service Operators Grant (a fuel duty rebate) and the ‘concessionary travel scheme,’ whereby disabled persons and people of pensionable age have a right to free off-peak travel. This intervention, as with energy social policy, is poorly targeted (Crisp et al., 2018; Mattioli et al., 2018a; Shaw and Docherty, 2014; Titheridge et al., 2014). Both of these measures benefit older people (regardless of need), while other disadvantaged categories (e.g. the unemployed) receive little or no assistance. In addition, where social tariffs are funded by taxpayers, these can be seen as a public subsidy to profit-making private operators, and a bad investment for the public purse (HoC, 2018; Mees, 2010; Preston, 2003). Bus operating revenue coming from concessionary bus fare reimbursement rose from £0.63 billion to £1 billion between 2004–2005 and 2017–2018. This is due to wider coverage, as the scheme moved from a local authority to a national scheme, to increased eligibility and a larger proportion of elderly in the wider population (DfT Bus Statistics, 2017–2018). According to some estimates, concessionary bus passes account for 45% of bus operators’ revenues (HoC, 2018: 22).

Across each of these sectors, the levels of social tariff are far from sufficient. At the end of 2017–2018, the number of customers receiving support through water company social tariffs came to just 393,143, while a further 158,454 were on the Government’s WaterSure programme. This amounts to around just over 2% of customers, far fewer than the 5.6 million that find their bills unaffordable (CCW, 2018; Money Advice Trust, 2018). In energy, the social provision is woefully inadequate in view of the levels of deprivation demonstrated by the extent of self-rationing and self-disconnection, above. In bus transport, deregulation provided the occasion for a large reduction of direct public subsidies for the provision of non-profitable routes in 1980s and 1990s (Preston, 2003). Mostly as a result of austerity policies, local authority spending on supporting buses has fallen again by 43% in real terms between 2009–2010 and 2018–2019 (Campaign for Better Transport, 2019). This has resulted in over 3000 local authority supported bus services being cut or reduced between 2009 and 2019 (Campaign for Better Transport, 2019), with dramatic impacts on accessibility for households without cars, notably in rural areas (Bawden, 2018).

The scope for social provision is diminished due to cherry-picking by investors. When private companies close rural bus routes that are not commercially viable, these are left to the state to provide, but without the scope for cross-subsidy from more lucrative areas of activity which remain with the private sector. Strategic bodies such as local authorities have very limited powers to set or oversee key aspects of the public transport system. Local authorities can tender bus services where private operators alone do not run them but these tend to be poorly integrated with commercial services (Crisp et al., 2018). Indeed, councils need to seek alternative funding sources for rural bus services such as through levies on new housing developments (Smith, 2018).

Viewed through the SoP lens, these measures are effectively tweaking around the edges of a system that is structured in favour of investors. While these measures may lead to some small improvements for some consumer groups, the extractive methods of provisioning by producers are largely unchallenged. Conceiving of these sectors as markets reduces scope for more progressive and collectivist financing mechanisms.

Regulation: Contestation and conflict

Regulation in water and energy has become increasingly complex and is something of a ‘moving target’ (Allen and Pryke, 2013: 426). Increased complexity increases the scope for regulatory capture. Each water sector price review has added roughly two new regulatory mechanisms to the process (Helm, 2020). In energy, critics have highlighted a narrow technocratic approach to policy, attending more to delivering markets rather than energy specific goals (Kuzemko, 2016; Thomas, 2019).

The state, via the regulator, is required to mediate between the conflicting interests of consumers, investors and voters. In the water sector, for example, Ofwat is called upon, on the one hand, to set conditions that will facilitate low-cost investment (DEFRA, 2019: 3). On the other hand, the regulator has faced criticisms due to the high returns made by investors. Tighter price controls are proposed for the 2020–2025 Price Review period. But this action by the regulator resulted in the down grading of the credit ratings of highly geared companies (Moody’s, 2018), which risks increasing financing costs for companies. The regulator has to navigate these conflicting pressures.

Price-setting inevitably involves winners and losers. For some years, the overall regulatory climate in Britain has been remarkably supportive of private investors. According to the Chief Executive of Ofwat ‘over the past twenty years, the direction of error has been consistently in favour of companies rather than customers’ (Ofwat, 2017: 2). Furthermore, the regulator’s consistent overestimation of financing and taxation costs led to windfall gains for water companies of at least £1.2 billion between 2010 and 2015 (HoC, 2016). The effects of the securitization of water bills escaped regulatory scrutiny (Allen and Pryke, 2013) until it reached the media and the attention of politicians (Gove, 2018). As with water, shareholder returns in energy have been boosted by biases in assumptions made by the regulator which has consistently overestimated the level of risk that investors face, resulting in higher bills for customers (Wild, 2018).

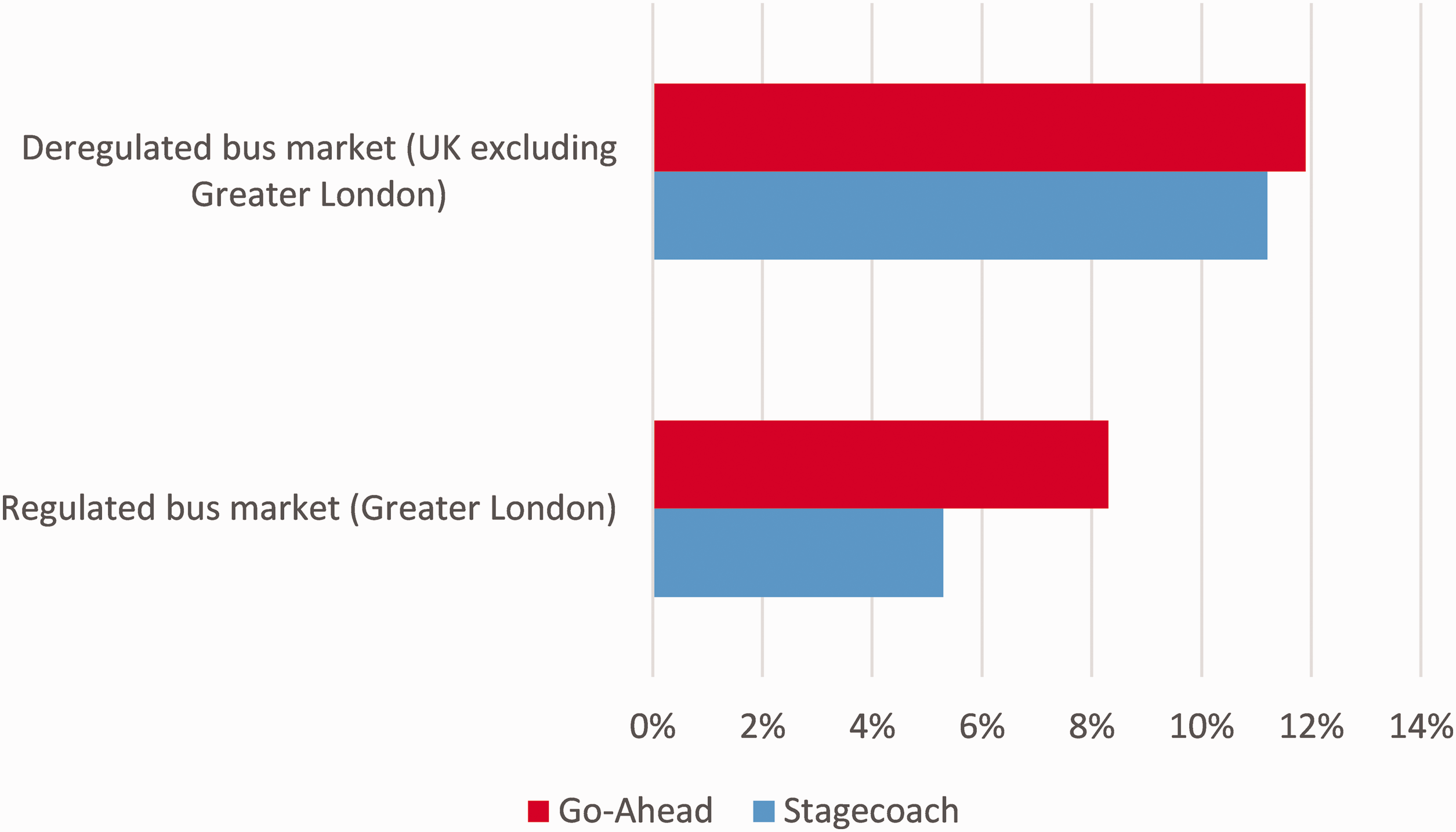

Conventional narratives of regulation underestimate the weight of investor interests as compared with those of consumers. Powerful corporate interests have been successful in steering interventions in the interests of investors. In bus transport the problems of fragmentation of services are well known, and reforms have been debated since the mid-1990s. Yet, private operators have fiercely opposed attempts to re-regulate the market. The profits generated from operating in London’s publicly controlled tendering system (see below), are much lower than in the deregulated environment in the rest of Great Britain (Figure 4 – see also Knowles and Abrantes, 2008; Wolmar, 1999) (Figure 4).

Operating profit margins of two major bus operators in the regulated and deregulated markets in the UK in 2018.

Privatization and deregulation create powerful incumbents, which benefit from the status quo and oppose attempts to re-regulate the sector. This form of lock-in means that these reforms, once enacted, are much more difficult to reverse.

While official policy is strongly wedded to the ethic of competition and markets, the state continues to play a strong role, and this has been expanding in some areas. In the energy sector, following the evidence of overcharging in the CMA review, the government took the radical step of imposing a cap on retail prices. Initially this was just for those on prepaid meters, but was then extended to all customers on default standard variable tariffs from winter 2018–2019 (Ofgem, 2018). Critics point out the limitations of this in terms of social policy. For example, there is nothing to stop firms overcharging in other ways (such as on existing arrears) (Hannah, 2017). Furthermore, for customers on low levels of energy consumption facing affordability constraints, the cap is not going to make much difference (CAP, 2018). And these price caps are temporary and will last no longer than 2023 (BEIS, 2018: 21). But this is a remarkable increase in state intervention, and is effectively recognition of the failure of private competition to meet social needs.

Competitive tendering in the bus transport sector

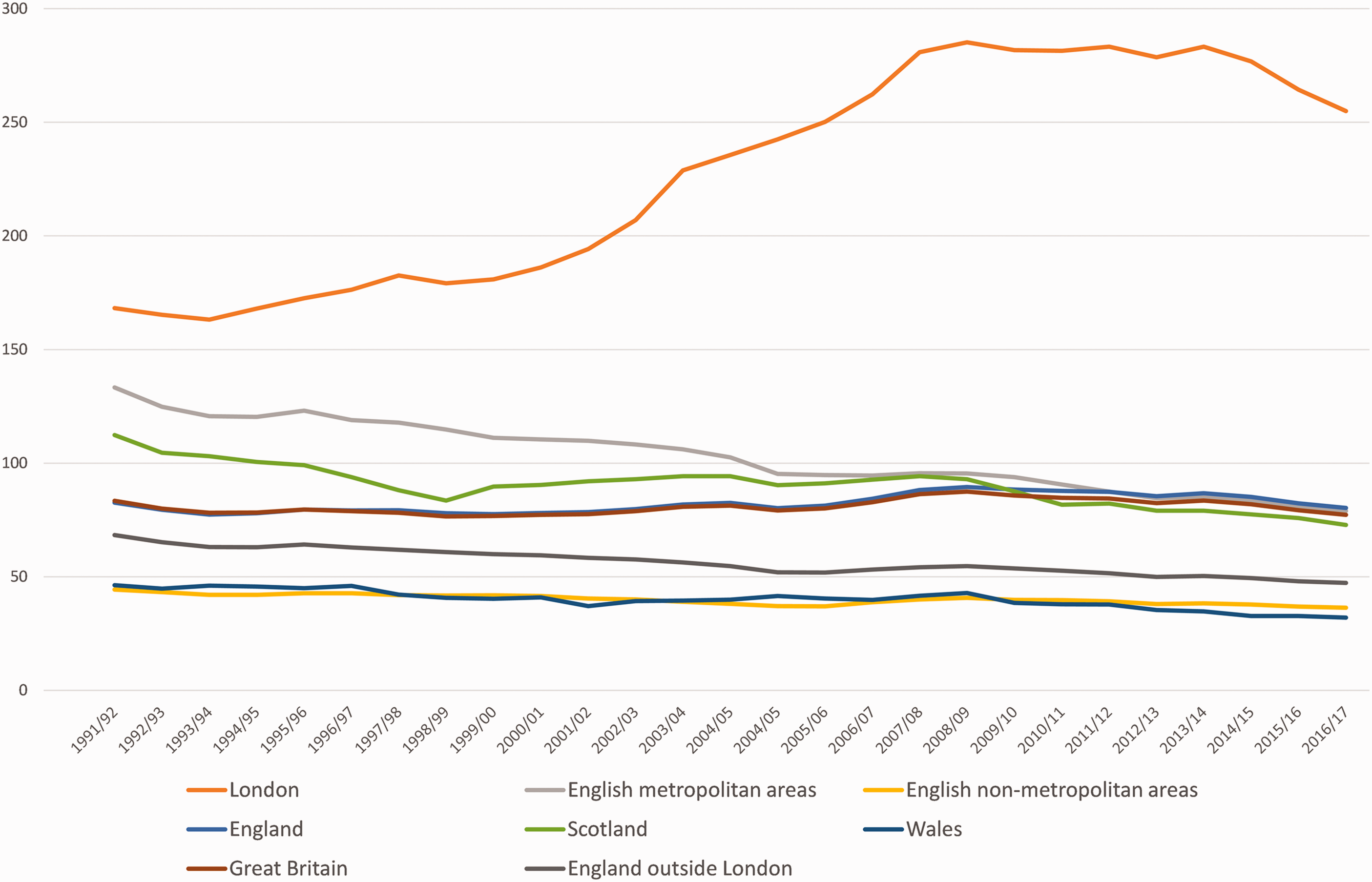

In contrast to the rest of Britain, bus and other public transport in London is coordinated by public agencies (Buehler and Pucher, 2011; Buehler et al., 2018; Koch and Newmark, 2016). London bus routes are established under coordinated public planning and then tendered to private companies by a public agency, TfL, which retains control of the strategic and tactical aspects of public transport provision (Mees, 2010). The simultaneous introduction of competitive tendering in London, and of the more radical deregulation in the rest of England, provides a natural experiment of sorts on the impacts of different models of public transport provision. The results could not be clearer: while bus travel per capita has rapidly increased in London between 1990 and 2010, it has declined in the rest of Great Britain, notably in other metropolitan areas (Figure 5). Meanwhile, bus companies extract lower profits from the London ‘market’ than in the rest of the country (see above) (Figure 5).

Passenger journeys on local bus services by metropolitan area status and country per head of population 1991–2017.

Other cities are seeking to follow the example set by London. The newly introduced ‘Bus Services Act’ (DfT, 2017) enables Mayoral Combined Authorities (i.e. eight major city-regions in England) to re-regulate the sector and be provided with ‘equivalent powers to those available in London’ (p. 4). To date, only Greater Manchester has initiated the complex legal process required for re-regulation (GMCA, 2019), and is facing the opposition of private bus operators, which have threatened legal action. It is widely expected that other city-regions will follow suit if Greater Manchester’s attempt is successful (Bounds, 2019). The case of TfL suggests that if the engagement of the private sector in public transport provision was relegated to the level of private tendering for planned and regulated provision, then some of the adverse effects of deregulation could be mitigated.

Conclusion

This paper applies the SoP approach to the water, energy and bus sectors in the UK, connecting end users with the underlying systems by which these services are provided. The analysis reveals how consumers, as they meet their basic needs, are unwittingly moulded to meet the imperatives of investors, representing global capital. The state, tasked with mediating between the two, has tended to side with investors. Consumers have no alternative but to comply as best as possible. However, in some cases, those that cannot fulfil the revenue requirements are disconnected from vital services, and may suffer severe deprivation while they appear to quietly peel away. On paper, excessive profiteering should be curbed by competition and/or by regulatory intervention. But, as Bowman et al. (2014: 11) point out ‘markets and the actors within them never work quite as expected and unintended negative social consequences proliferate.’

An important question is why these outcomes occur and why the regulator does not intervene further to protect poor households. The SoP analysis suggests that this is due to a combination of factors. First there is an inevitable trade-off inherent in balancing the contested interests of stakeholders, and the balance has tipped in favour of investors. Second, there is a strong ideological commitment to market-led solutions, with narratives framed in terms of efficiency and competition rather than equity and public service. Hence, policy is focused on market-making. Third, with these sectors understood as markets, consumers can be treated separately from the underlying biased structures by which services are provided, and the inequality inherent in the system goes unnoticed. Finally, these distributional outcomes are below the radar for the majority of the population and there is little political pressure to challenge the existing structures. Opinion polls showed considerable support for the public ownership of essential services in the 2019 national election, but the opposition (Labour) party was defeated on other issues and the window for nationalization has all but closed (Hall, 2020). While there are debates around the details of regulation, there has been little significant challenge to the structures created by privatized modes of service provision.

The SoP framing suggests that the market narrative presents a convenient screen for rent extraction. Thus, social policy is framed in terms of individual affordability and consumer choices, while the inequalities in the underlying SoP are ignored. In water for example, social policy is reduced to small cross-subsidies between households while the millions paid to directors and billions paid to shareholders are considered to be the work of the market. Similarly, the closure of unprofitable bus routes is seen as a market, rather than a social outcome. Policy is dominated by an intense preoccupation with superficially technocratic interventions. Continuing to see these sectors as markets, and consumers as utility-maximizing individuals, occludes more collectivist responses (Van der Zwan, 2014: 113).

The couching of these structural shifts in terms of market narratives has echoes of austerity more generally. Policy responses to the financial crisis have been associated with a narrative of greater moralism, blaming individual responsibility rather than private profiteering. For example, a lack of financial literacy is blamed for increased indebtedness. Dagdeviren, et al. (2020) and Green and Lavery (2015) also point to the entrenchment of an ethos of ‘moralistic disciplining,’ for example, in workfarism. Van der Zwan (2014: 112) points out that ‘the financialisation of the everyday has been facilitated by discourses of risk-taking, self-management and self-fulfillment … individuals today encounter a world of risk in which they themselves are responsible for dealing with the uncertainties of life.’ Similar discourses prevail in water and energy, where the individual is responsible for the affordability of, and access to, essential services.

Conceiving of such outcomes as market failure suggests that a more market-like structure offers the solution, but this approach has consistently failed to benefit low-income households, while revenue flows to shareholders continue. The result has been a sustained and systemic structural assault on households in general, and low-income households in particular, across essential services. As Meek (2012: 1) puts it, ‘the privatisations are joining up’ and so are the inequalities. In the same way that the state has developed a punitive and precarious system of welfare provision for low-income households facing choices between debt and hunger (Dagdeviren et al., 2020), privatization and deregulation have also penalized low-income households. These are the ones that are forced on to prepayment meters for energy, that pay over 5% of their household income in water bills, who face poor connectivity from public transport services with resulting car dependence. In the provision of essential services, as elsewhere, the state has orchestrated the transformation of the political economy of Britain, channelling funds into privileged sectors while imposing deflation on others (Green and Lavery, 2015).

Policy responses to poverty and inequality tend to focus on fiscal measures such as tax and welfare, or educating and even punishing poor households, as though their poverty were the outcome of lack of information or bad behaviour. However, this paper reveals that in Britain, inequality is built into the fabric of everyday life, emerging from the way in which basic needs are met. Regulation has not been able to provide social protection. Rather, in order to address these highly inequitable social outcomes, attention is needed to the underlying structures and processes of the SoP. The current policy narrative of markets and competition needs to be replaced with one of equitable and universal provision.

Footnotes

Authors' Note

Julia Steinberger is also affiliated with Institute of Geography and Sustainability, University of Lausanne, Switzerland.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported through the Research Leadership Award to Julia Steinberger for the project ‘Living Well Within Limits’ (LiLi) (RL2016–048) funded by the Leverhulme Trust.