Abstract

This article explores how the impact of the 2022–2023 inflationary episode was managed in Greece, and explains how labour market governance framed public policy responses. Greece resembles other southern European countries in the chronic weakness of its institutional preconditions for managing emerging inflationary pressures in a coordinated manner. Greece is also different, however, in that the previous two economic shocks had left a legacy of drastically diminished collective bargaining, financially vulnerable households and a public debt-to-GDP ratio close to 200 per cent. We show that, in a context of weakened trade unions and collective bargaining institutions, the response of wages to inflation was anaemic, while profits grew strongly, especially in oligopolistic product markets. We also discuss how, in order to ease the cost-of-living crisis, the government resorted mainly to untargeted support measures with a regressive distributional impact. We conclude by reflecting on what our findings imply for Greece’s quest for a more sustainable and more inclusive growth model.

Introduction

After a long period during which it hovered below 2 per cent, inflation in Europe began to accelerate in spring 2021. At the time, unresolved bottlenecks in global supply chains, shifts in sectoral demand linked to the COVID-19 pandemic, and higher than expected seasonal demand for natural gas drove up the headline inflation rate (Matsaganis and Theodoropoulou, 2022; Tsafos, 2022). The energy shock was later exacerbated by Russia’s invasion of Ukraine and the economic sanctions subsequently imposed on Russia, which resulted in restrictions in the supply of natural gas and oil in international markets and a steep rise in their price. Higher gas prices quickly fed into electricity prices, dramatically increasing production costs for firms and the cost of living for households. Moreover, food prices also spiralled up, given that on the eve of the war Russia and Ukraine together accounted for about 30 per cent of global exports of wheat and 20 per cent of corn (OECD, 2022: 3), further adding to inflationary pressures.

The impact of these developments has varied across Europe, as have responses to the shock. National governments, supported by the EU (European Commission, 2022), took measures to mitigate the impact of higher energy prices on households and firms, and to reduce their countries’ dependence on Russian fossil fuel imports. At the same time, the European Central Bank (ECB), and other central banks around the world, abandoned quantitative easing and zero (or negative) interest rates, and tightened monetary policy to keep inflation in check.

In this article, we focus on the experience of Greece. As in other EU Member States, the cost-of-living crisis was the third major economic shock the country had faced since 2010, after the euro crisis and the COVID-19 pandemic. The previous two economic shocks had left a legacy of drastically diminished collective bargaining, financially vulnerable households and a public debt-to-GDP ratio close to 200 per cent. All of these added to the challenges of managing an inflationary shock and its consequences. These can be contradictory: weak unions are poorly placed to preserve real wages as inflation rises, while in contrast uncoordinated collective bargaining institutions militate against wage restraint, at least for some categories. Both imply that more robust government intervention is required to preserve real incomes, especially at the bottom of the income distribution, while keeping inflation under control, a task complicated by limited fiscal space.

We specifically examine how the 2022–2023 inflationary episode played out, its drivers and the responses it elicited from price- and wage-setters. We explain the Greek government’s response by putting it into a broader institutional context, with a special focus on labour market governance, showing how the latter has enabled and/or necessitated some policy options over others. We also explore the distributional implications of the Greek government’s policy response, and reflect on the resilience of the Greek economy and its growth model.

The article is structured as follows. The section ‘Internal devaluation’ examines labour market governance in Greece in the aftermath of the deregulation of the 2010s. The section ‘Industrial relations’ briefly reviews the state of industrial relations and trade unions in Greece on the eve of the recent inflationary shock. The section ‘The recent inflationary episode’ explores the characteristics and drivers of that shock. The following section examines its effects on wages and profits. The section ‘The government response to the inflation shock’ lays out the policy response to the cost-of-living crisis. The following section assesses its distributional effects. The final section concludes.

Internal devaluation

The recent inflationary episode and the resulting cost-of-living crisis caught Greece with much weakened collective bargaining institutions, following far-reaching reforms in the context of the country’s bailouts in the 2010s. While Greece’s trajectory was not dissimilar to that of other southern European countries (see Tassinari et al., 2024), the dismantling of collective bargaining arrangements went further in Greece than elsewhere.

Collective bargaining in Greece underwent substantial changes in the early 2010s. The reforms shifted the system’s centre of gravity away from the national level. Collective agreements at firm level were allowed to overrule industry-level ones. Coordination of wage setting was also weakened, while the automatic extension of collective agreements to non-unionised workers and non-signing employers was abolished. This caused the bargaining coverage rate to collapse from 100 per cent in 2011 to 14 per cent in 2017 (OECD/AIAS, 2023). Moreover, ‘associations of persons’ were allowed to represent workers in firms from which unions were absent. The minimum wage, until 2012 set by social partners in the national general collective agreement, became statutory (Matsaganis, 2013). Such radical developments were unmatched elsewhere in the EU.

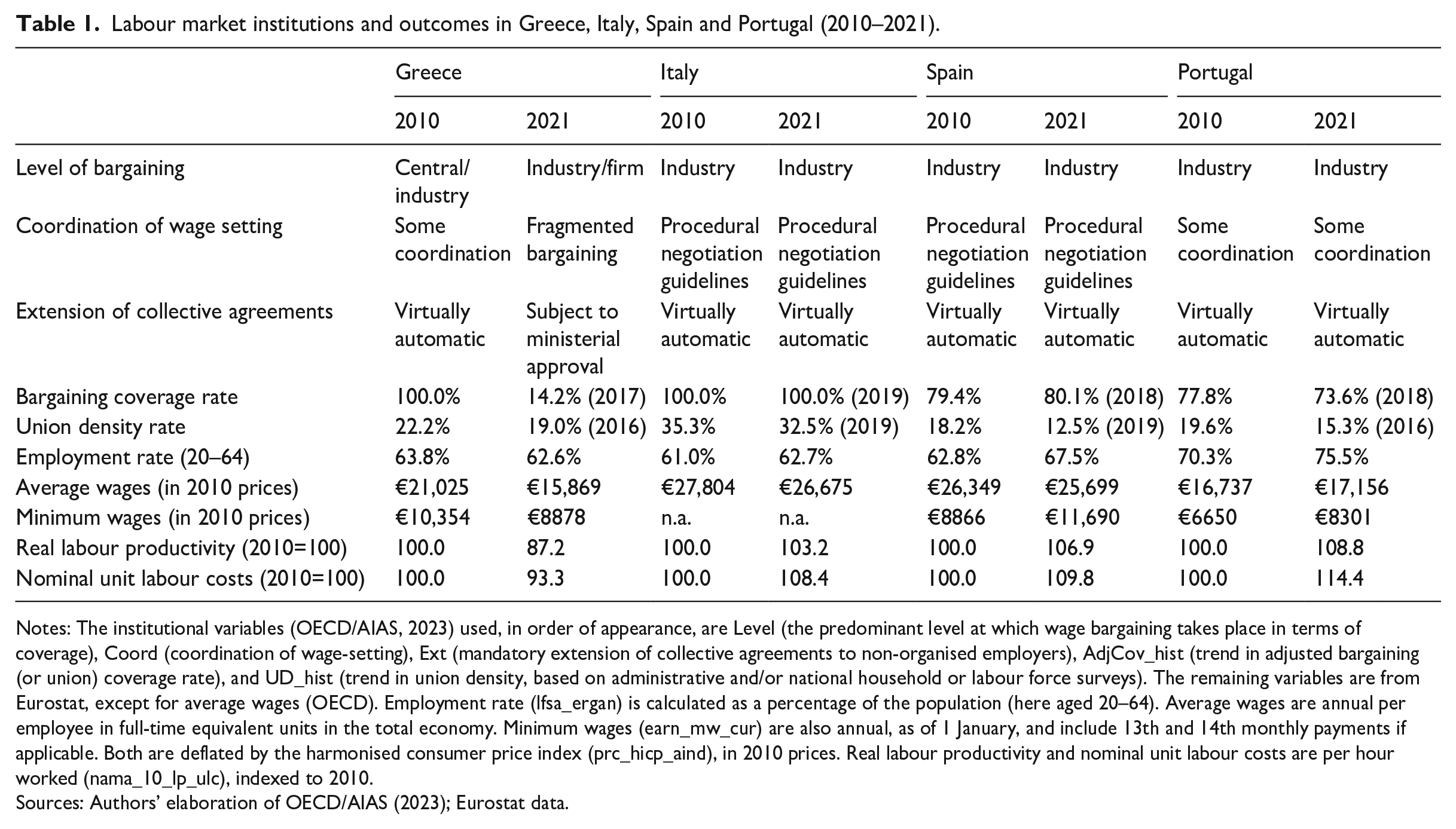

The objective of the labour market reforms of the early 2010s had been to engineer ‘internal devaluation’ (Perez and Matsaganis, 2019), in other words, the simultaneous lowering of wages and prices in order to boost exports in a manner equivalent to a currency devaluation (which, of course, was not possible in a currency union), with the ultimate goal of reversing economic decline by creating new jobs. As it turned out, the employment rate was actually lower in 2021, on the eve of the cost-of-living crisis (62.6 per cent), than it was when the debt crisis erupted in 2010 (63.8 per cent). By contrast, over the same period, in Spain and Portugal the employment rate grew by around 5 percentage points, and in Italy by nearly 2. This is shown in Table 1.

Labour market institutions and outcomes in Greece, Italy, Spain and Portugal (2010–2021).

Notes: The institutional variables (OECD/AIAS, 2023) used, in order of appearance, are Level (the predominant level at which wage bargaining takes place in terms of coverage), Coord (coordination of wage-setting), Ext (mandatory extension of collective agreements to non-organised employers), AdjCov_hist (trend in adjusted bargaining (or union) coverage rate), and UD_hist (trend in union density, based on administrative and/or national household or labour force surveys). The remaining variables are from Eurostat, except for average wages (OECD). Employment rate (lfsa_ergan) is calculated as a percentage of the population (here aged 20–64). Average wages are annual per employee in full-time equivalent units in the total economy. Minimum wages (earn_mw_cur) are also annual, as of 1 January, and include 13th and 14th monthly payments if applicable. Both are deflated by the harmonised consumer price index (prc_hicp_aind), in 2010 prices. Real labour productivity and nominal unit labour costs are per hour worked (nama_10_lp_ulc), indexed to 2010.

Sources: Authors’ elaboration of OECD/AIAS (2023); Eurostat data.

As for prices, they stabilised (rising by a mere 2.5 per cent cumulatively in 2010–2021), but they certainly did not fall, albeit briefly.

Internal devaluation scored its only success in terms of wage devaluation. According to OECD estimates, in 2021 average real wages in Greece were 24.5 per cent below their level in 2010. By comparison, in Italy and Spain the decline of the purchasing power of average wages over the same period was less dramatic – at 4.1 and 2.5 per cent, respectively – while in Portugal average wages in 2021 were 2.5 per cent above their 2010 level, adjusted for inflation.

Meanwhile, the reallocation of jobs to lower-productivity activities (such as tourism), in a context of stagnant employment and significantly reduced wages, caused labour productivity in Greece to fall by 12.8 per cent per hour worked in 2010–2021. In contrast, in the other three south European countries, labour productivity increased over the same period. Because of the decline of labour productivity in Greece, the gain in cost competitiveness, proxied by the decrease in unit labour costs, also per hour worked, was smaller than might have been expected, given wage devaluation: 6.7 per cent in nominal terms (9.0 per cent in real terms) in 2010–2021.

Industrial relations

As trade union power weakened in Greece, so did the ‘carrots’ and ‘sticks’ (Culpepper and Regan, 2014) that unions could deploy when dealing with employers and the government. This was due not only to the labour market deregulation and high unemployment of the 2010s, but also to long-lasting structural and organisational dynamics, as well as to dramatic shifts in Greece’s political landscape, spearheaded by the crisis.

Trade union politics in Greece is highly fragmented and adversarial. Following the restoration of democracy in 1974, competing factions, usually affiliated to a political party, have actively contested union elections at all levels, while the communist faction has gone one step further, creating a separatist ‘workers front’ (ΠΑΜΕ) in 1999, critical of the General Confederation of Greek Workers (ΓΣΕΕ) that covers wage-earners in private firms and public utilities. (ΑΔΕΔΥ, the other peak-level union confederation, covers civil servants and other public sector workers.) Partisan divisions within unions have been reinforced by, and further contributed to, political polarisation.

In the 1990s, ‘highly fragmented and heavily politicized labour and employer organizations, and a reluctance on all sides to engage in political exchange’ made tripartite policy concertation and social pacts to meet the Maastricht criteria less effective in Greece than in the rest of southern Europe (Hancké and Rhodes, 2005: 14). In essence, trade unions proved more accustomed to lobbying the government through confrontation (by calling a general strike or by vetoing government policy initiatives in public enterprises) than by negotiating over tripartite solutions. Lack of trust also meant that even relatively pro-union governments, such as those led by the Socialist Party, held back important policy initiatives from the negotiating table, thus constraining the space for political exchange (Ioannou, 2010). Nor were employers much interested in offering workers productivity-enhancing deals (for example, investment in skills) in exchange for wage restraint (see Hancké and Soskice, 2003; Kritsantonis, 1998).

In the early 2000s, trade unions scored an important victory over the socialist government by first blocking and then watering down a pension reform bill, aiming to bring the entitlements of civil servants and employees in public utilities and banks down to the level enjoyed by most other workers (Matsaganis, 2007). In a similar vein, in the rest of the decade, public utility employees and civil servants were awarded wage rises over and above the rest of the economy (Di Carlo, 2021: 16). Under union pressure, government spending on wages and (especially) pensions spiralled out of control. Such practices reinforced the image of unions going to great lengths to pursue the narrow interests of their most powerful members in secure jobs, while employment conditions in private firms became ever more flexible and insecure (Featherstone, 2003).

As already explained, the EU-ECB-IMF bailouts after Greece’s debt crisis prioritised internal devaluation and labour market deregulation. Both had devastating effects on unions. First, the dismantling of collective bargaining arrangements significantly reduced unions’ institutional power, leaving them with hardly any ‘carrots’ for dealing with the government and employers. On the other hand, the prolonged recession and persistent high unemployment further reduced workers’ bargaining power. As a result, national general strikes, the tool of choice in the past for exerting pressure on employers and government (unions’ ‘stick’) lost any remaining potency as unions failed to mobilise workers facing high unemployment. Thirdly, the tight conditionality of bailout agreements left little scope for lobbying for generous pay awards and pension benefits in the public sector. Lastly, caught between significant income losses and large mortgage debts incurred in more optimistic times, many Greeks became over-indebted, which as historical evidence from France and Sweden suggests (Gouzoulis, 2021), has an additional detrimental effect on the labour share.

When the debt crisis erupted, unionisation was on a downward path, and unevenly distributed across sectors. The union density rate had fallen to 22 per cent in 2010 (down from 48 per cent in 1977 and 38 per cent in 1992), and was due to fall further to 19 per cent by 2016 (OECD/AIAS, 2023). Public sector enterprises (until the late 2000s) and state-controlled banks (until the late 1990s) were union strongholds, with union density rates often in excess of 80 per cent (Matsaganis, 2007; Vogiatzoglou, 2018). In contrast, organising workers in the private sector in Greece was (and still is) a challenge, with large parts of the workforce employed (sometimes informally) in very small firms, or in self-employment (Kritsantonis, 1998; Zambarloukou, 2006). Peak-level union confederations, notably ΓΣΕΕ, have had limited success in mobilising migrant workers and others in precarious jobs (Matsaganis, 2007: 545; Vogiatzoglou, 2018: 122). Economic change, namely the decline of manufacturing and the rise of service employment, has also contributed to weakening union power.

The collapse of electoral support for the two parties that had dominated Greek politics since the restoration of democracy in 1974 had repercussions for unions, too. The Socialist Party, which dominated both peak-level union confederations, saw its share of the vote dwindle from 43.9 per cent in October 2009 to 4.7 per cent in January 2015. Rightly or wrongly, some of the discredit was extended to the official trade unions.

In this void, new militant grass-roots unions, informal workers’ collectives and experimental cooperatives emerged. Some of these, at firm or industry level, had been launched in the 1990s, aiming to organise precarious workers who were (or felt) ignored by official trade unions. Notwithstanding their militancy and innovativeness, these new forms of worker organisation face challenges: among other things, their members are weak vis-à-vis employers, their access to labour market institutions is limited, and their repertoire of actions is small and limited to the workplace (Kretsos and Vogiatzoglou, 2015).

The recent inflationary episode

Like other European economies, the recent inflationary episode struck Greece as it was recovering from the sharp recession that followed the pandemic. In the case of Greece, the pandemic shock had come after a long decade of recession and stagnation, and was amplified by the country’s increasing dependence on tourism (Bürgisser and Di Carlo, 2023: 250). Wages slowly began to rise again: between 2019 and 2021 minimum wages grew by 11.7 per cent and average wages by 2.1 per cent (both in real terms), albeit not sufficiently to make up for the losses incurred since 2010.

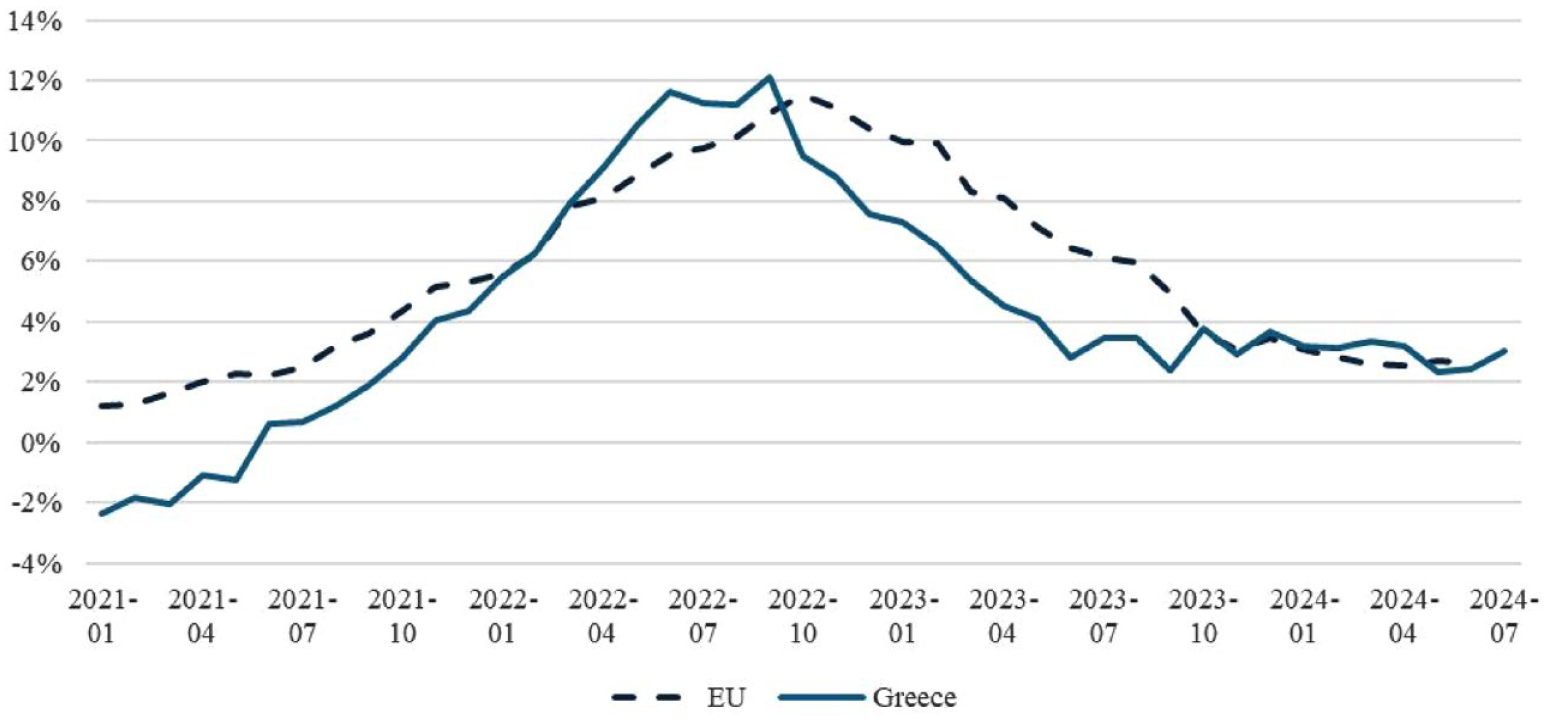

Headline inflation in Greece began to rise fast in early 2021, peaked at 11.6 per cent in June 2022 (a full 2 percentage points above the EU average), then started to decelerate more sharply than in the rest of the EU, falling as low as 2.4 per cent in September 2023 (far below the EU average of 4.9 per cent) and eventually fluctuated around 3.0 per cent until the time of writing (August 2024). This is shown in Figure 1.

Headline inflation in Greece vis-à-vis the EU average (January 2021 to July 2024).

Rising domestic prices in Greece were driven by high import costs, and by high profits in energy and other markets (European Commission, 2023). Energy prices had already started to increase gradually in March 2021 throughout Europe. In Greece, energy costs soared: in October 2021, they were 18 per cent higher than the previous month, and 28 per cent higher than in the same month of the previous year. The country’s vulnerability to the energy shock can be traced to its high dependence on fossil fuels, to a considerable extent imported from Russia. Natural gas, oil and solid fossil fuels accounted for 81 per cent of the country’s energy mix in 2021, about 20 per cent of which was imported from Russia (Nakou, 2023: 3). Energy costs eventually peaked in September 2022, when energy inflation reached 80 per cent year-on-year (compared with 53 per cent in the EU as a whole).

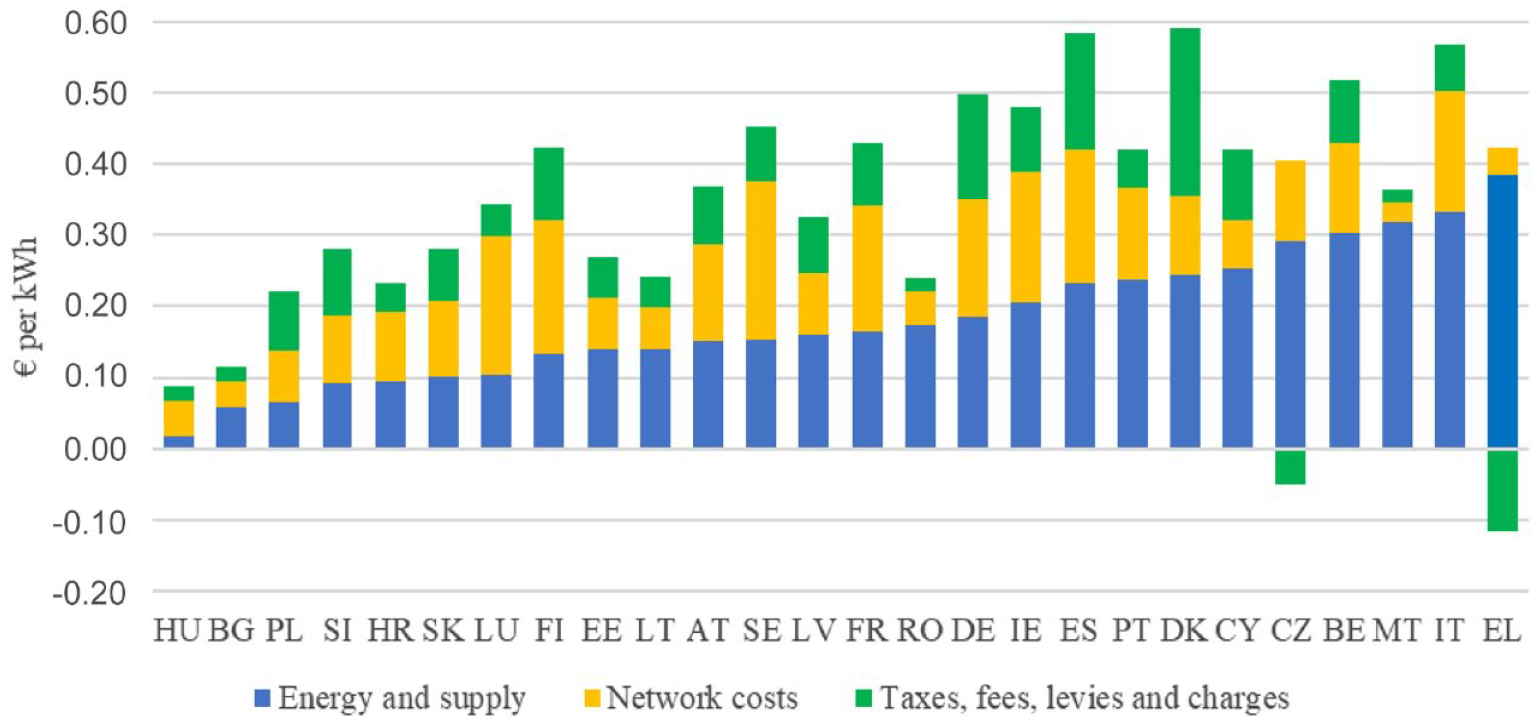

The electricity generation market is highly concentrated in Greece, as three firms account for over 95 per cent of net electricity generation (the lowest number of firms in the EU, jointly with Malta and Slovenia). In natural gas, which contributed around 40 per cent of all electricity production in 2021, the price mark-up reached close to 20 per cent, the second highest in the EU (ACER-CEER, 2022: 62). As a result, Greek households faced the highest pre-tax electricity prices in the EU.

High prices in an oligopolistic market were compensated by the government. Unlike in all other Member States bar the Czech Republic, net taxes on electricity consumption in Greece were negative, as price subsidies more than offset ‘taxes, fees, levies, and charges’. It was because of negative net taxes (and relatively low network costs) that post-tax electricity prices in Greece were below the EU average. This can be seen in Figure 2.

Electricity prices by component (2022).

From September 2022, energy prices in Greece decreased steadily for the following 12 months, eliminating nearly two-thirds of their increase in the previous 12 months. Thereafter, energy prices remained fairly stable. The deceleration was due primarily to the decline in gas prices internationally, but the rising share of renewables in the supply mix for electricity generation also contributed to lowering costs. In January to May 2024 renewable energy sources accounted for 47.2 per cent of Greece’s electricity mix, up from 15.9 per cent 10 years earlier (The Green Tank, 2024). The reduction in carbon prices in Europe also helped, as did the steady growth in electricity self-production on the part of households, firms, farmers and energy communities.

Soaring energy costs, combined with the disruptions of war in Ukraine, and extreme weather elsewhere, soon caused food prices to escalate. Food inflation in Greece remained above 10 per cent for a year and a half (from April 2022 to October 2023), peaking at over 15 per cent year-on-year in early 2023, compared with nearly 20 per cent in the EU as a whole.

Effects of inflation on wages and profits

All inflationary episodes create distributive tensions (Matsaganis and Theodoropoulou, 2022), and the recent one was no exception. Firms react to higher input costs by raising the prices of their products (especially in markets less exposed to competition), while workers and unions demand pay rises to compensate for higher prices. The high inflation of the 1970s and 1980s has often been attributed to such wage-price spirals, although a recent analysis of the historical record by IMF economists (Alvarez et al., 2022: 18) has questioned their importance, concluding that ‘an acceleration of nominal wages should not necessarily be seen as a sign that a wage-price spiral is taking hold’. Be that as it may, this time the response of price- and wage-setters in trying to avert real income losses was scrutinised intensely by policy-makers to ensure that inflation did not spiral out of control.

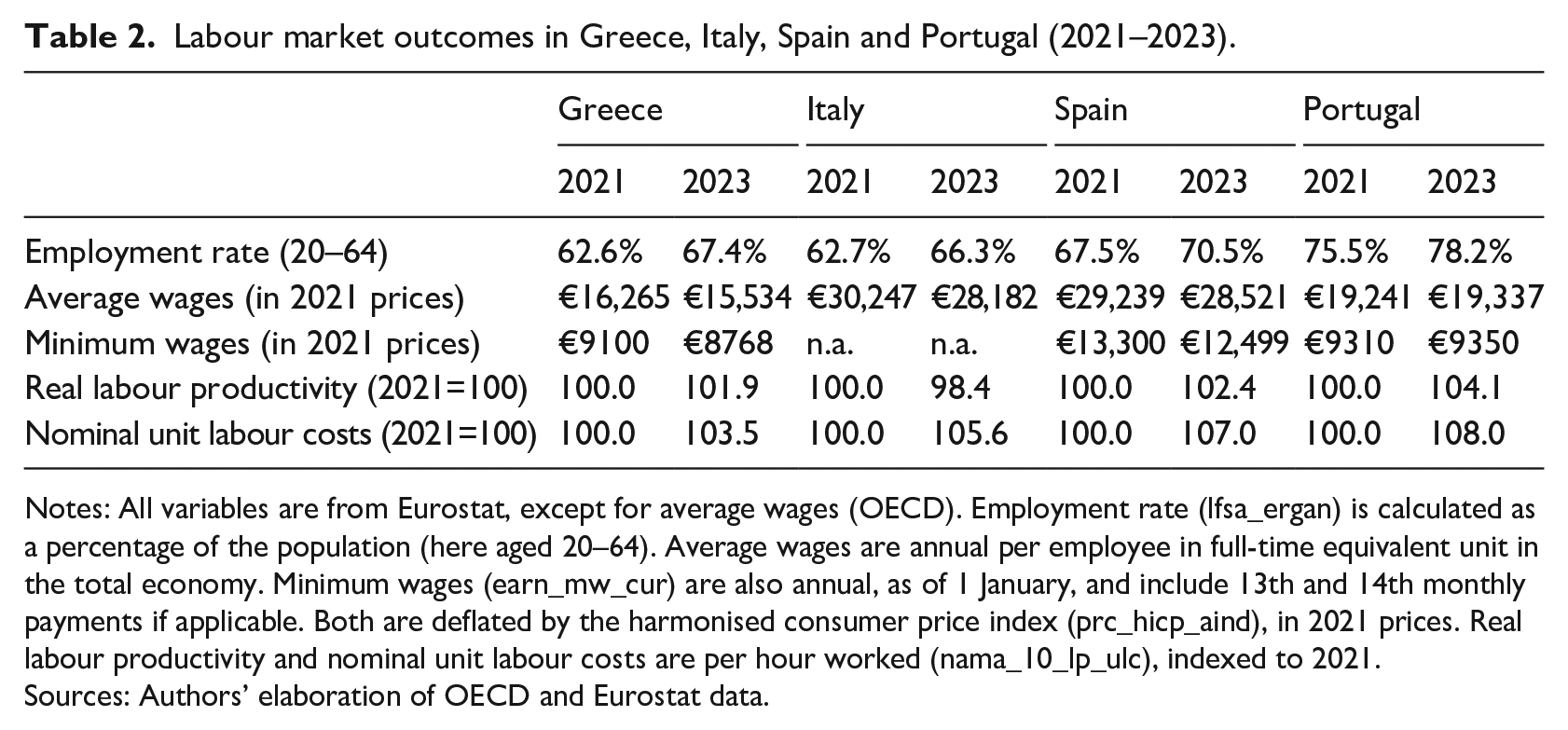

Real wages declined throughout southern Europe in 2022 as prices rose faster than nominal wages. OECD estimates suggest that the erosion of purchasing power was greatest in Greece (5.4 per cent); average real wages fell by 4.1 per cent in Spain, 3.6 per cent in Italy and 1.8 per cent in Portugal. In 2023, nominal wages in Greece rose marginally faster than prices, protecting real wages, but failing to recover their erosion in 2022, not to mention the significant losses of the 2010s. More specifically, average real wages rose by 1.0 per cent in Greece, by 2.4 per cent in Portugal, and by 1.7 per cent in Spain, while they fell again in Italy (by 3.4 per cent). Over the two-year period, average real wages declined by 4.5 per cent in Greece, more than in Spain (2.5 per cent), though not as much as in Italy (6.8 per cent). In Portugal, average real wages actually rose slightly (by 0.5 per cent) in 2021–2023.

Data from collective agreements largely confirm the above picture. In 2022, out of 217 firm-level agreements, only 80 (covering a mere 1.2 per cent of all employees) involved a nominal pay rise of 5 per cent on average. In none of the 80 did the rate of wage increases match the inflation rate (9.3 per cent). In 2023, out of 209 new firm-level agreements, 59 (covering 2.7 per cent of all employees) provided for an average nominal wage increase of 6 per cent, against an inflation rate of 4.2 per cent. Only three such agreements, concluded at the height of the cost-of-living crisis (October 2023), covering a total of 840 workers, provided for more generous nominal pay rises (15.2 per cent).

At industry level, 22 collective agreements were concluded in 2022 (down from 120 in 2009). Of these, 13 involved zero wage growth. In sectors with a significant employment share, only one agreement (in banking) provided for a nominal wage increase (of 2 per cent). In contrast, out of 20 sectoral agreements signed in 2023, 18 provided for wage increases. Oil companies awarded a pay rise of over 21 per cent. In another two cases (accommodation and food services), the pay rise was marginally above inflation. Workers in the tobacco industry, and those in insurance and real estate, received a nominal wage increase of 4 per cent, that is, just below inflation. Pay awards in all other industries employing a significant number of workers, including banking employees (2.2 per cent), were well below inflation. Collective agreements in tourism (accommodation and food services), banks and the tobacco industry were mandatorily extended to non-unionised firms by government decree.

Concerning the statutory minimum wage, since 2019 governments of all colours have made a point of raising it, typically by more than the experts’ committee had recommended. Recent increases were 10.9 per cent in 2019, 9.7 per cent in 2022 (when it was raised twice), 9.4 per cent in 2023, and 6.4 per cent in 2024. In real terms, the increases of the past five years took the 2024 minimum wage 22.2 per cent above its 2019 level. Nevertheless, they made up for only about three-quarters of the losses incurred in the 2010s, leaving the 2024 minimum wage 6.2 per cent below its 2010 level (in real terms).

Labour productivity per hour worked improved somewhat in 2021–2023 (by 1.9 per cent), though less than in Portugal (4.1 per cent) and Spain (2.4 per cent). In Italy, labour productivity fell (by 1.6 per cent). Inflation raised unit labour costs throughout southern Europe, though in Greece, where modest nominal wage increases were partly compensated by the small growth in labour productivity, unit labour costs rose by only 3.5 per cent in 2021–2023, that is, less than in the other southern European countries. This can be seen in Table 2.

Labour market outcomes in Greece, Italy, Spain and Portugal (2021–2023).

Notes: All variables are from Eurostat, except for average wages (OECD). Employment rate (lfsa_ergan) is calculated as a percentage of the population (here aged 20–64). Average wages are annual per employee in full-time equivalent unit in the total economy. Minimum wages (earn_mw_cur) are also annual, as of 1 January, and include 13th and 14th monthly payments if applicable. Both are deflated by the harmonised consumer price index (prc_hicp_aind), in 2021 prices. Real labour productivity and nominal unit labour costs are per hour worked (nama_10_lp_ulc), indexed to 2021.

Sources: Authors’ elaboration of OECD and Eurostat data.

Wage developments in Greece can be understood in the context of the dismantling of collective bargaining institutions described in Section 2, and of the declining power of trade unions, compounded by the emerging divisions among new workers’ organisations and the mainstream trade unions discussed in Section 3. Notwithstanding its diminished resources, ΓΣΕΕ did not refrain from mobilising its members to protest at the erosion of real wages, calling a general strike on 10 occasions from September 2021 to September 2024, three of which were held on International Workers’ Day (1 May) and during HELEXPO, the Thessaloniki International Exhibition held annually in September, at which Greek prime ministers traditionally announce new policy measures. Notably, between February and May 2024, ΓΣΕΕ organised a campaign against cost-of-living increases in several cities across Greece. Needless to say, the success of this activism was limited in terms of protecting real wages.

With unions and workers too weak to achieve pay increases in line with inflation, the much-feared wage-price spiral failed to materialise. On the contrary, Eurostat estimates suggest that in Greece the profit share of non-financial corporations (gross operating surplus as a proportion of gross value added) rose to 49.2 per cent in 2022, up from 45.9 per cent in 2021, and from 39.3 per cent in 2019. Bank of Greece estimates (Bank of Greece, 2024: 115) suggest that profitability fell somewhat in January to September 2023, partly because of the withdrawal of generous government measures to help firms and households cope with the energy crisis.

The government response to the inflation shock

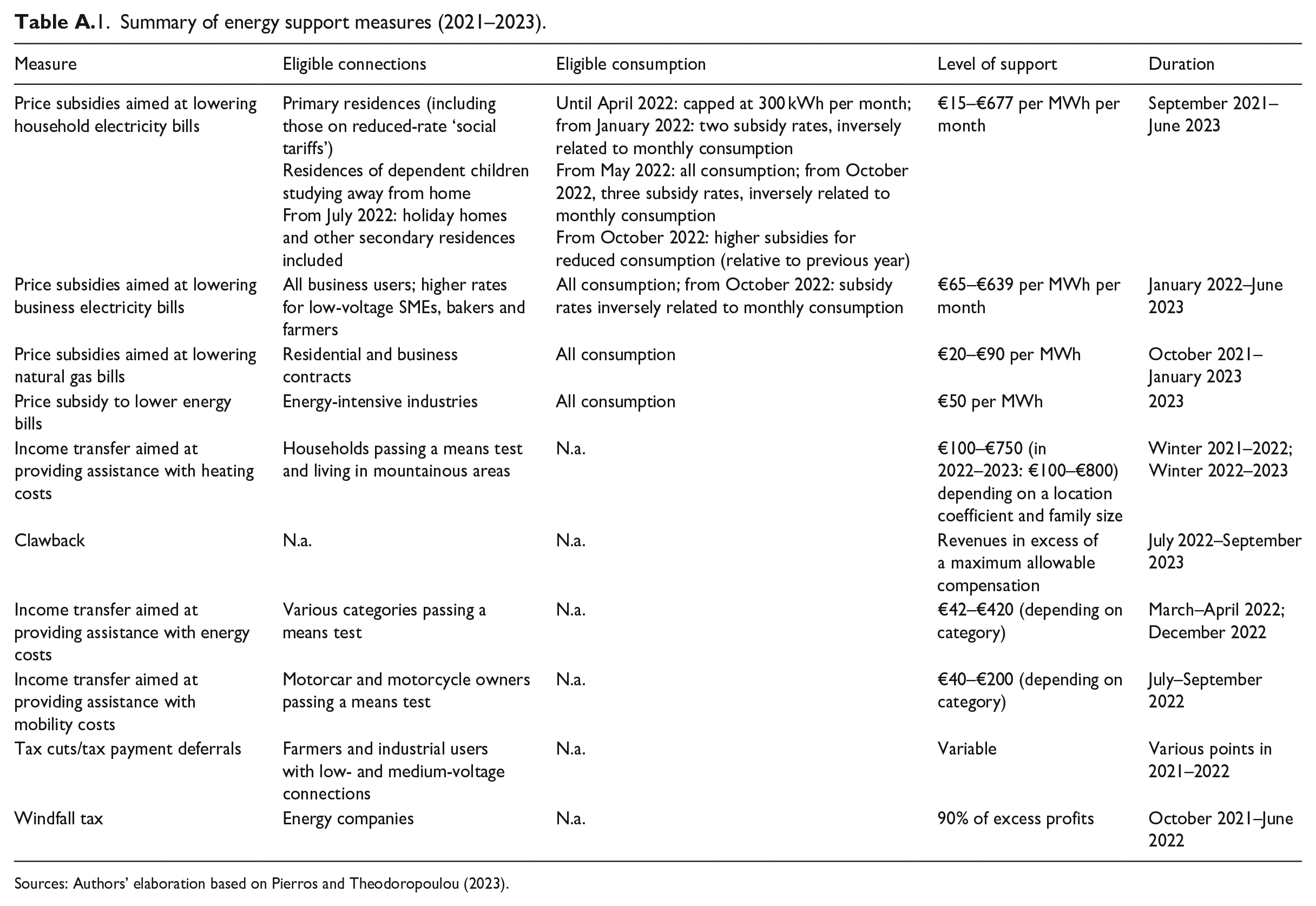

Faced with oligopolistic energy firms charging the highest pre-tax electricity prices in Europe to consumers worn out by a rather difficult decade and a half left the (pro-business) Greek government with no other option than to reach for its cheque book. According to OECD estimates (Hemmerlé et al., 2023), Greece spent as much as 4.87 per cent of GDP in 2022 to soften the impact of steep increases in energy bills on households and firms. That was far higher than in any of the other 40 countries in the study: Italy and Poland, a joint second, spent a mere 2.82 per cent of GDP. For a country with famously mild winters and a notoriously high public debt, the government’s largesse was quite impressive. Equally remarkable was the balance between targeted measures, ‘providing assistance specifically to vulnerable households’, and untargeted ones, ‘offered as broad support to all energy users’. The latter accounted for 85 per cent of all public spending on energy support in 2022. A summary of the main energy support measures can be seen in Table A.1 in the Appendix.

The preferred instrument for supporting residential users against rising electricity bills was a price subsidy scheme, first launched in September 2021. Its level was recalibrated every one to two months to reflect variations in electricity prices. The government’s approach towards eligibility criteria shifted over time. From July 2022, as the energy crisis gathered pace, subsidies began to rise steeply across the board, peaking in September 2022 at €639 per MWh (€677 per MWh for households on the ‘social tariff’). Primary and non-primary residences were all eligible, while subsidies applied across-the-board, irrespective of consumption levels. From October 2022, subsidies began to decline in line with prices, while later incentives were introduced in the form of higher subsidies for households reducing their consumption by at least 15 per cent relative to the previous year. Holiday homes remained eligible (Pierros and Theodoropoulou, 2022).

Electricity subsidies became available to business users from January 2022. Small and medium-sized enterprises with low-voltage connections received higher subsidies from May 2022, gradually extended to farmers and larger firms. At first, these subsidies were applied across-the-board. From October 2022, subsidies became inversely related to the level of consumption (except for farmers), capped at 2 MWh per month. Across-the-board subsidies also became available to natural gas users, whether residential or business (Pierros and Theodoropoulou, 2023). Finally, in line with the EU temporary crisis framework for state-aid measures to support the economy following the war in Ukraine, a subsidy of €50 per MWh was paid in 2023 to firms that had suffered competitiveness losses in energy-intensive sectors.

Targeted income support measures featured less prominently, accounting for a mere 15 per cent of all public spending on energy support in 2022. Such measures included the expansion and increase of the ‘heating allowance’, the introduction of a scheme to support households in arrears with their electricity bills from December 2021 to March 2022, and the launch of a ‘fuel pass’ to compensate low-income consumers for higher mobility costs in April to September 2022.

Furthermore, a mechanism was introduced in July 2022 to recoup excess profits of electricity producers by setting a ceiling equal to the maximum allowable compensation (per kWh), based on actual costs. Revenues in excess of that ceiling were clawed back, and the proceeds used to support households and firms facing rising energy costs. By May 2023, the government reported that total revenues from the mechanism had surpassed €3.25bn or 1.5 per cent of GDP (Hellenic Republic Ministry of Finance, 2023). For the period prior to the introduction of the mechanism, a 90 per cent windfall tax was introduced in November 2022, levied retrospectively on energy suppliers’ excess profits realised between October 2021 and June 2022. The proceedings, estimated at €375m (0.2 per cent of GDP), were also used to offset energy bills. Finally, from August 2022 to September 2023, energy providers were no longer allowed to include an ‘adjustment clause’ in their retail contracts, effectively decoupling domestic electricity prices from fluctuations in international natural gas markets (Amores et al., 2023; Pierros and Theodoropoulou, 2023).

The proceedings of the windfall tax and the maximum compensation mechanism described above were channelled into a special Energy Transition Fund (ETF), created in autumn 2021, to finance energy support measures, with extra funding to the tune of €400m from the government budget. As the government’s response to the energy crisis unfolded and its cost escalated, however, additional sources of revenue were found elsewhere, namely in the auctions of emission allowances under the EU Emissions Trading System (ETS), and in the surpluses of the Special Account for Renewable Energy Resources (SARES). In 2022, revenues reached an estimated 2.8 per cent of GDP (Hellenic Republic Ministry of Finance, 2023), covering about 57 per cent of the total cost of energy support measures in that year.

The government repeatedly argued that, because its energy support measures were funded largely by ETS and SARES, there was nothing to worry about. This argument was flawed on two counts. On the one hand, huge amounts of money were diverted from EU programmes, intended to facilitate the transition from fossil fuels to renewable energy in order essentially to support the country’s current energy consumption and production patterns. On the other hand, despite EU funding, the fiscal cost to the national budget was considerable. Bank of Greece (2024) estimates (p. 165) put the total cost of energy support measures at 5 per cent of GDP (that is, slightly more than estimated by the OECD), of which 2.2 per cent of GDP came out of the national budget.

Furthermore, the government’s preference for price subsidies over income transfers was likely to be inequitable as well as inefficient. Just how inequitable is the subject of the next section.

The distributional impact of energy support measures

As already discussed, the recent inflationary episode erupted while Greeks were still reeling from the impact of the debt crisis and the pandemic. The lingering effects were evident in various metrics. According to Eurostat data for 2022, 18.7 per cent of households could not keep their home adequately warm, 34.1 per cent were in arrears with their utility bills, while 26.7 per cent were facing housing costs in excess of 40 per cent of their disposable income, a share three times as large as in the EU as a whole (8.7 per cent).

These difficulties were compounded by the inherently regressive impact of any inflation increase driven by rising energy and food prices, as low-income households spend a higher share of their budget on these two commodities. A recent study by Claeys et al. (2022) found that at its peak inflation in Greece was as much as 3 percentage points higher for the poorest 20 per cent of households than for the richest 20 per cent.

To neutralise the regressive impact of inflation successfully, energy support measures would have to be well targeted. As seen in the previous section, that was not the case in Greece, where 85 per cent of the total cost of such measures was directed towards untargeted, mostly across-the-board price subsidies. Recent research confirms that, despite their high cost, government policies to help consumers cope with rising prices only partly protected low-income households.

Amores et al. (2023) found that the effect of rising prices before government measures was strongly regressive: it amounted to 15.0 per cent of baseline income for the poorest income decile 1, relative to 5.8 per cent for the richest income decile 10 (7.8 per cent on average across the population). Price subsidies were mildly progressive: they accounted for 6.8 per cent of baseline income in decile 1, compared with 1.4 per cent in decile 10 (2.9 per cent on average), although they were worth 1.7 times more in money terms for decile 10 than for decile 1. Income support measures fared better: they raised baseline income by 4.1 per cent in decile 1, compared with virtually zero in decile 10 (0.8 per cent on average across the income distribution). The combined effects of inflation, price subsidies and income support were regressive: real incomes declined by 3.4 per cent in decile 1, compared with 2.7 per cent in decile 10 (2.9 per cent on average).

A simulation study by two IMF economists (Hua and Shi, 2024) used granular information from the 2021 Household Budget Survey to estimate the distributional impact of inflation and the government response in Greece. That study also confirmed that low-income households, and those living in sparsely populated areas, faced larger losses in purchasing power, but also found that household size and composition mattered: the impact of inflation and policy measures was higher among the elderly, and lower in larger households. The authors concluded that targeted support would have been most effective in protecting vulnerable households, followed by categorical measures (aimed at well-defined population groups, such as families with children, with no income tests); price subsidies were least effective.

All three studies cited above assumed for simplicity’s sake that consumption of energy (and food) remained at the same level before and after the price increases. As a matter of fact, recent data show that, as prices rose, households across the income distribution cut back significantly on their electricity consumption (in kWh terms). Nevertheless, energy is a necessity, so its demand is ‘inelastic’. As a result, the fall in consumption was not sufficient to fully offset the effect of rising prices: spending on electricity (in money terms) went up in all income classes. Low-income households, in particular, spent 20 per cent more on electricity in 2022 relative to 2021, even though they consumed 7 per cent less (ElStat, 2023).

Concluding remarks

The Greek economy proved to be highly vulnerable to the inflationary shock of the early 2020s. This vulnerability can be traced back to its dependence on imported goods, such as natural gas, the high import content of its exports (OECD, 2023), and ultimately to its lasting competitiveness issues (Stockhammer and Kohler, 2022). The latter resurfaced in 2022 as the country’s current account deficit reached 10.3 per cent (Bank of Greece, 2024: 138).

Inflation dealt a further blow to real wages, which lost 4.5 per cent of their purchasing power in 2021–2023, in addition to their 24.5 per cent fall in 2010–2021. The minimum wage, statutory since 2012, fared better: the upwards adjustments in 2019 and 2022–2024 raised its value in real terms and went about three-quarters of the way towards reversing its decline in the 2010s.

The failure of organised labour to protect real wages was not surprising. Union power is much diminished, partly because of the weakening of collective wage bargaining institutions and partly due to persistently high unemployment, compounded by structural issues (service economy, small firm size).

Greek trade unions’ standard tools (calling a general strike, using their political affiliation to put pressure on government) have lost their old potency. High unemployment and wage cuts have limited workers’ participation in industrial action (whose success was variable even in better times). Public sector wage setting, and spending on pensions and other items of interest to the unions, are now subject to tighter constraints and centralised fiscal monitoring, thus removing a field in which unions had been successful in extracting concessions in favour of (some of) their members.

Moreover, official trade unions in peak-level confederations have lost some of their prestige among workers. They have often been associated with the more protected sections of the workforce, mainly in the public sector, whose interests shaped union strategy, and as a result they are perceived as distant from the concerns of ordinary workers in insecure jobs struggling to make ends meet. The gap in representation has facilitated the emergence of alternative, more militant workers’ organisations. Nevertheless, these in turn are too weak, their resources inadequate, and their access to regulatory labour market institutions too limited to be players that a government must reckon with.

In fact, as wage-price spirals failed to emerge, the government did not feel constrained to seek the cooperation of organised labour in order to contain inflationary pressures. In view of that, the government did not turn to the unions to seek their support in managing inflation. Its approach was rather paternalistic: the government attempted to project an image of concern for workers, making a point of extending by ministerial decree key collective agreements to non-unionised firms, in addition to raising the statutory minimum wage in 2022–2024.

By contrast, inflationary pressures derived from the oligopolistic structure of key markets, which allowed firms to raise prices and register high profits. Despite its pro-business stance therefore the government pleaded for price restraint, calling on food distribution firms to refrain from ‘speculative price rises’ (to little effect so far), and intervening in energy markets in order to recoup some windfall profits (and fund energy support measures).

More importantly, to protect households and firms from rising energy costs (and later, price increases in food and other goods), the government resorted to highly costly, mostly untargeted measures, to the tune of 5 per cent of GDP in 2022. Because of their nature, and despite their high fiscal cost, the measures turned out to be relatively regressive and insufficient to protect the purchasing power of low-income families. Furthermore, by privileging across-the-board price subsidies at the expense of targeted income transfers, energy support measures had the further unfortunate effect of blunting incentives for energy efficiency and for a shift from fossil fuels to renewable energy.

Overall, these points speak to the need for a more sustainable and more inclusive growth model. Greece is generally considered to have ‘weathered the storm’ of the debt crisis, and to have achieved a fairly high degree of economic recovery and political stability. Nevertheless, the latest cost-of-living crisis demonstrated that the country is no more resilient to shocks than it was before the debt crisis. Moreover, excessive reliance on tourism has locked the economy in a low-productivity/low-wage equilibrium, combined with the depletion of natural resources. Greece’s predicament is that negotiated solutions away from the current growth model, and towards a more sustainable, more inclusive one, require better industrial relations and stronger collective bargaining institutions than are currently available, following the deregulation of the 2010s.

Footnotes

Appendix

Summary of energy support measures (2021–2023).

| Measure | Eligible connections | Eligible consumption | Level of support | Duration |

|---|---|---|---|---|

| Price subsidies aimed at lowering household electricity bills | Primary residences (including those on reduced-rate ‘social tariffs’) Residences of dependent children studying away from home From July 2022: holiday homes and other secondary residences included |

Until April 2022: capped at 300 kWh per month; from January 2022: two subsidy rates, inversely related to monthly consumption From May 2022: all consumption; from October 2022, three subsidy rates, inversely related to monthly consumption From October 2022: higher subsidies for reduced consumption (relative to previous year) |

€15–€677 per MWh per month | September 2021–June 2023 |

| Price subsidies aimed at lowering business electricity bills | All business users; higher rates for low-voltage SMEs, bakers and farmers | All consumption; from October 2022: subsidy rates inversely related to monthly consumption | €65–€639 per MWh per month | January 2022–June 2023 |

| Price subsidies aimed at lowering natural gas bills | Residential and business contracts | All consumption | €20–€90 per MWh | October 2021–January 2023 |

| Price subsidy to lower energy bills | Energy-intensive industries | All consumption | €50 per MWh | 2023 |

| Income transfer aimed at providing assistance with heating costs | Households passing a means test and living in mountainous areas | N.a. | €100–€750 (in 2022–2023: €100–€800) depending on a location coefficient and family size | Winter 2021–2022; Winter 2022–2023 |

| Clawback | N.a. | N.a. | Revenues in excess of a maximum allowable compensation | July 2022–September 2023 |

| Income transfer aimed at providing assistance with energy costs | Various categories passing a means test | N.a. | €42–€420 (depending on category) | March–April 2022; December 2022 |

| Income transfer aimed at providing assistance with mobility costs | Motorcar and motorcycle owners passing a means test | N.a. | €40–€200 (depending on category) | July–September 2022 |

| Tax cuts/tax payment deferrals | Farmers and industrial users with low- and medium-voltage connections | N.a. | Variable | Various points in 2021–2022 |

| Windfall tax | Energy companies | N.a. | 90% of excess profits | October 2021–June 2022 |

Sources: Authors’ elaboration based on Pierros and Theodoropoulou (2023).

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.