Abstract

This article discusses the multi-faceted and changing role played by trade unions in providing unemployment benefits in Sweden, a country using the so-called Ghent system. As an important institutional feature explaining the high rate of unionisation in the Nordics, the system has been much debated. This article provides a comprehensive account of the retrenchment of the state unemployment benefit system (UBS) and the development of occupational and private UBS pillars providing complementary protection. It also introduces an ongoing reform discussion where the social partners are proposed to govern the unemployment insurance system via collective agreements, while retaining the union-linked insurance funds. The core institutional feature of the Ghent system – voluntary membership of a union-linked insurance fund – is turning out to be highly resilient despite frequent attempts to weaken the union power stemming from it. However, the system’s role in providing unemployment protection has changed due to its development into a multi-pillar structure, meaning that its future prospects are uncertain.

Introduction

In Denmark, Finland and Sweden, as well as Belgium, unions are greatly involved in the administration of unemployment benefits. In the literature, this system is named after Ghent, the Belgian city which in 1901 started subsidising local unions’ unemployment funds (Vandaele, 2006). The Ghent system of state-subsidised but union-administered unemployment funds became widespread in Europe in the first half of the 20th century, with Rasmussen and Pontusson (2018) counting 10 countries with such systems, among them France (1905–1950), the Netherlands (1916–1952) and Spain (1919–1936). However, the Ghent system was abandoned in most of them in connection with the Second World War, to be replaced by a mandatory, state-run unemployment benefit system (UBS) (Alber, 1981). The Ghent model was discontinued in most countries due to its inherent inability to achieve large-scale risk-pooling covering the entire workforce, in contrast to the mandatory state insurance programme.

The Ghent system has survived in Belgium and three of the Nordic countries. However, the Belgian system is a hybrid one where the state collects unemployment insurance contributions while the unions administer the payment of benefits to the unemployed (Vandaele, 2006). This is different to the Nordic countries which have mainly retained voluntary systems, i.e., individuals decide themselves whether they want to join the unemployment fund and pay contributions. As these payments only partly cover the quite generous benefits, the state finances the lion’s share through taxes. However, Denmark is the only country with a completely voluntary scheme, while the Finnish and Swedish systems include a basic flat-rate benefit not requiring fund membership (Jokivuori, 2006; Kjellberg, 2009).

While the Ghent system is strongly associated with the Nordic region and cherished by the unions and social democratic parties, the system can be seen as an anomaly within the Nordic social democratic welfare states (Esping-Andersen, 1990), as it has characteristics befitting a liberal rather than a social democratic regime – risks are pooled only within occupational groups/unions, while the state subsidies can be regarded as a sort of a ‘help to self-help’ (Goul Andersen, 2012). From a social democratic point of view, one would expect the first-order preference to be a universal compulsory benefit system where the risk of unemployment is pooled across the entire workforce. Following Goul Andersen, whether a Ghent system fits into a more universal welfare state despite retaining voluntary fund membership depends on several criteria: the strictness of eligibility, to what extent benefits replace income losses, the parity of contributions between funds, and finally to what extent the state subsidises the system. All these factors are open to state intervention within the Nordic Ghent systems, and, consequently, politically contested (Gordon, 2019; Lindellee, 2018).

In addition, as well described in the literature, the Ghent system is very much linked to high union density (Clasen and Viebrock, 2008; Høgedahl, 2014; Lind, 2007; Rothstein, 1992; Scruggs, 2002; van Rie et al., 2011; Western, 1997). In an international comparison, all Nordic countries have high densities: peaking in the 1990s at around 80 per cent, it has declined in recent decades – in 2019 down to 67 per cent in Denmark and Finland, and 65 per cent in Sweden. By contrast, Norway, a non-Ghent country since 1946, had a significantly lower rate of 50 per cent in 2019. Iceland, on the other hand, has a very high union density (91 per cent), despite abolishing its Ghent system in 2006.

The importance of a Ghent system as a power resource for unions and social democratic parties has also meant that it has come under frequent attacks from right-wing parties attempting to weaken the union influence stemming from the system. While in Denmark and Finland insurance funds not affiliated to unions have become widespread, Sweden is unique in that union-linked unemployment insurance funds continue to dominate. Conservative attempts to weaken the Ghent effect in Sweden took a different path, preferring not to meddle directly with the link between the unions and insurance funds (Bandau, 2017; Høgedahl and Kongshøj, 2017; Kjellberg and Lyhne Ibsen, 2016).

This article focuses on Sweden, how its Ghent system has changed since the great economic crisis of the 1990s and the unique ways in which Swedish unions responded to UBS retrenchment. According to several scholars, in recent decades Sweden has adopted a neoliberal trajectory, weakening union power and splitting the labour market between insiders and outsiders (Baccaro and Howell, 2017; Berglund et al., 2020; Gordon, 2019). Against this background and confronted by declining union membership, the Swedish trade unions have managed to retain and partly reinvent their role in the governance of the unemployment benefit system, employing more diversified strategies to protect the unemployed. Despite still fighting the retrenchment of the Ghent system in terms of benefit levels and the coverage of the earnings-related benefits, the unions have played an important role in the development of a multi-pillar benefit system offering complementary benefit schemes to top up benefits paid by the state UBS (Lindellee, 2018, 2021a).

We start by providing an account of past changes in Sweden’s UBS, going on to describe the various pillars of today’s UBS. We then discuss an ongoing reform where the social partners are trying to gain greater control over the financing of the unemployment insurance programme and the rules governing it, via collective agreements. We end by discussing how important – despite all the changes and ongoing political struggles revolving around the UBS – the voluntary membership of union-linked unemployment insurance funds still is for the Swedish unions, and how the rigidity of this particular institutional feature influences the system’s political sustainability.

Changes in the Swedish Ghent system

The Swedish unemployment insurance programme is dependent on individual workers’ voluntary membership of an insurance fund, in contrast to the compulsory systems found in most other European countries where unemployment insurance is part of the general social security system. To receive earnings-related unemployment benefits, workers need to actively become a member of an unemployment insurance fund. There are currently 27 such funds, with several of them having a history stretching back to the 1890s when they were financed and governed by unions and their members. At that time, however, affordable benefit levels were very low, and funds risked bankruptcy when too many members became unemployed (Edebalk, 1996).

Much later than Denmark (1907) and Norway (1906), the Swedish government started to subsidise unemployment funds in 1935. While there are several reasons for this late introduction of the Ghent system, one important one was union hesitance due to the perceived risk of losing control over the funds, for example over eligibility criteria for benefits or the possibility to use fund resources for other purposes such as complementing strike funds (Edebalk, 1996; Wennemo, 2014). However, influential social democrats at that time argued that having unions run and the state subsidise unemployment funds would in the long run serve union interests (Wennemo, 2014). Over the following decades, state subsidies gradually increased, allowing more generous benefits and in turn increasing union acceptance (Rothstein, 1998). At the same time, the unions regained influence over unemployment protection policies through the introduction of corporative institutions, in particular the Swedish National Labour Market Board.

The unemployment insurance funds are by law defined as legal bodies independent of the unions. Their resources cannot be used for any other purpose than paying unemployment benefits. Under the 1997 Unemployment Fund Act, they are obliged to treat all members equally (IAF, 2018; SOU, 2015). Though their work is now (since 2004) supervised by the Swedish Unemployment Insurance Board (IAF), the unions retain a certain amount of influence in the governance of the funds, as the majority of fund management boards include or are even chaired by union officials (IAF, 2018).

The relationship between fund membership and union membership – the core of the so-called Ghent effect – is not so clear-cut. Right from the start in 1935, there was no requirement to be a union member in order to be eligible for unemployment benefits (SOU, 2015). Moreover, a union-independent unemployment fund – the Alfa fund – has existed since 1998, offering an option to workers with no intention of joining a union. In most cases, Olson (1965)’s theory of collective action and the mechanisms of selective incentives are used to explain the Ghent effect. Both Rothstein (1992) and Scruggs (2002) emphasise negative selective incentives as the main mechanism determining why workers choose to become members of both a fund and a union. According to the authors, twin membership reduces the risk of unequal treatment when eligibility criteria are applied, when finding a suitable job, or when re-entitlement starts following a period of unemployment. Consequently, the close relationship between unions and funds is seen to put non-union fund members at risk of not being equally treated. However, this explanation has lost credibility over the decades, with new laws and regulations greatly circumscribing fund powers and transferring some of their tasks to state authorities such as the Public Employment Service and the IAF. Indeed, the latter audits funds’ application of the rules and even has the authority to suspend state funding (Lindellee, 2018; SOU, 2015).

A more probable explanation for twin membership is the close association perceived by workers to exist between unions and funds. A recent IAF (2018) report points out that many unions and their insurance funds work closely together, for instance sharing office space and board mandates, or that insurance funds are involved in union recruitment. Nine of the 27 funds have their membership fees collected by the unions, though in some cases it is not clear what part of the contribution is the fund membership fee and what part the union membership fee, blurring the distinction between the two organisations. The same report also describes how several insurance funds make the decision to approve an application for membership dependent on whether the applicant is a member of the associated union, and how unions and their insurance funds collaborate in recruiting members (IAF, 2018: 25–28). In union recruiting campaigns, the income insurance scheme is always highlighted as a key advantage of membership. In a previous study, this blurred situation was considered an important explanation for twin membership (Clasen and Viebrock, 2008). Similarly, a recent survey revealed that many still think that union membership is a prerequisite for access to unemployment benefits (Calmfors et al., 2021: 6–7).

Unions’ initial concern of losing control over the governance of unemployment insurance to the state has in many ways come true. Alongside their unemployment fund contributions, workers also need to fulfil certain work-related criteria to be entitled to earnings-related benefits, e.g. the minimum qualifying period. These criteria are decided by the state. Moreover, the replacement rate cap is set by the government, as well as several other rules determining when sanctions can be imposed on benefit recipients.

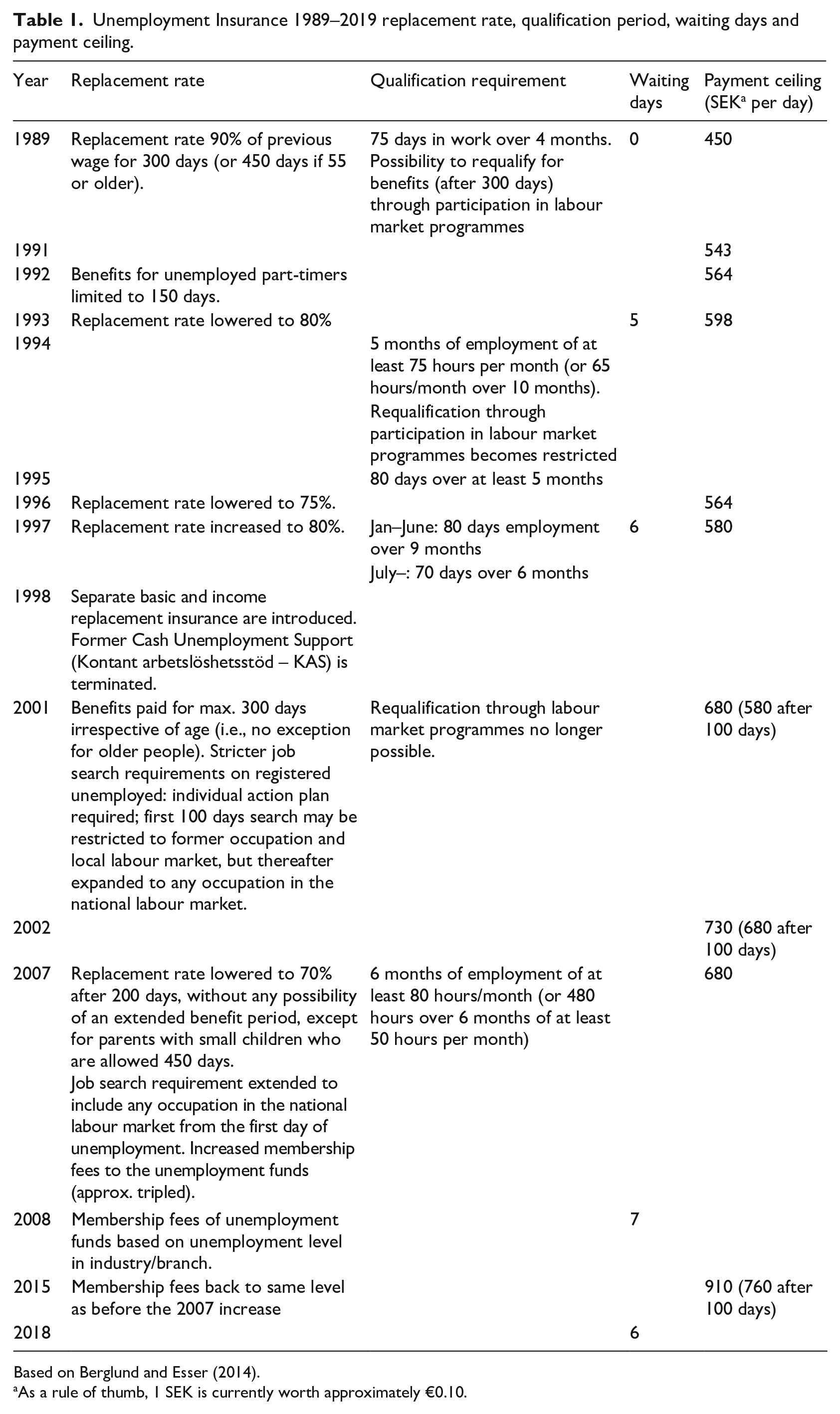

Table 1 lists the key changes in eligibility criteria and replacement rates since 1990. Generally speaking, right-wing governments tend to tighten requirements. For example, in 1994, under the Bildt government, calculation of the qualifying period was changed from days to months, making it harder for part-time workers to meet the criterion, while the centre-right Alliance government (2006–2014) reduced the replacement rate and further tightened the qualifying rules. Despite loosening some of them, social democratic governments have not reversed many of the changes introduced. As a result, over the last few decades unemployment insurance has moved in a direction that can only be called neoliberal, becoming less generous, tightening criteria, and putting more pressure on the unemployed to find a new job (Bengtsson and Berglund, 2012; Gordon, 2019).

Unemployment Insurance 1989–2019 replacement rate, qualification period, waiting days and payment ceiling.

Based on Berglund and Esser (2014).

As a rule of thumb, 1 SEK is currently worth approximately €0.10.

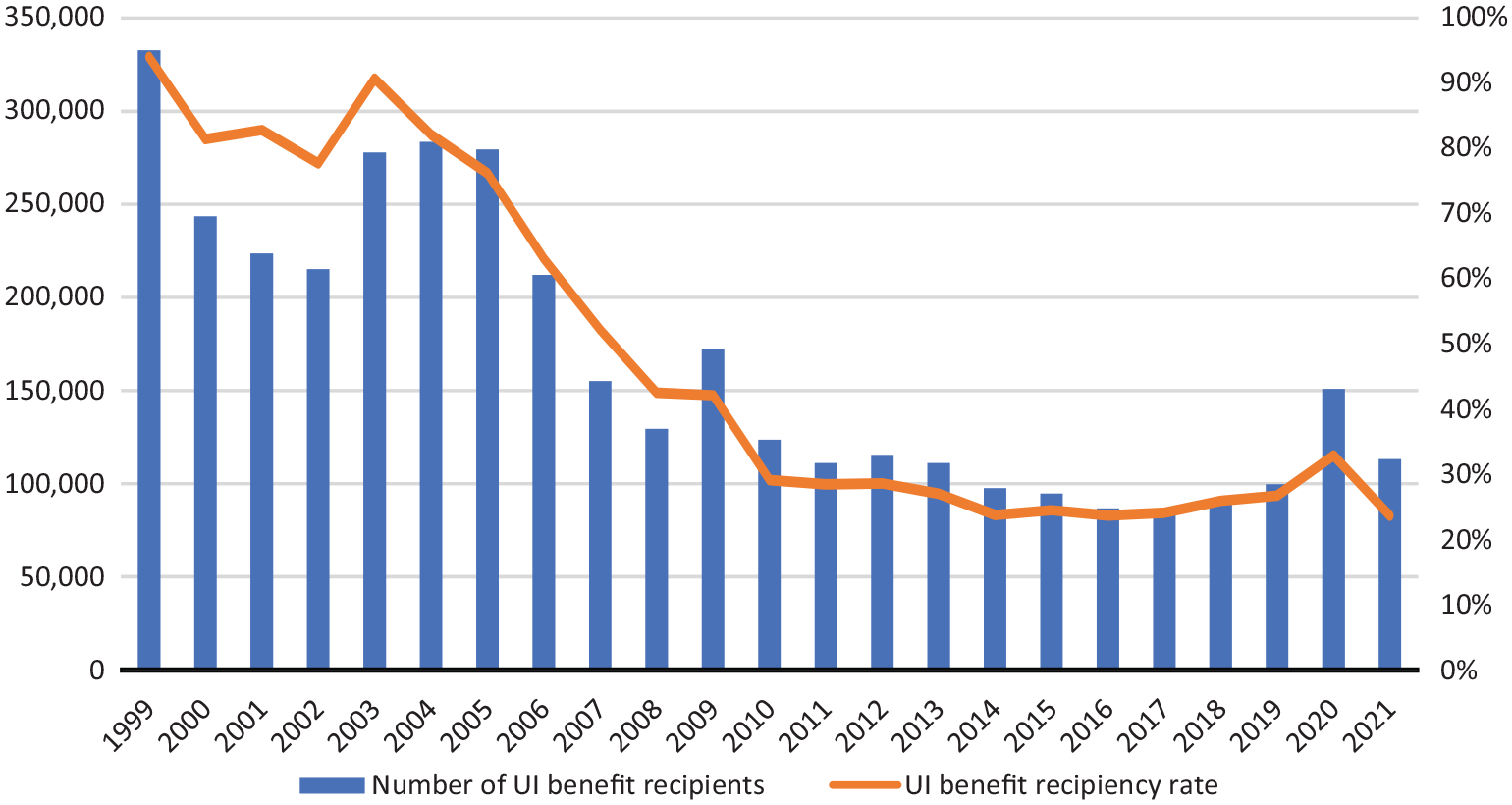

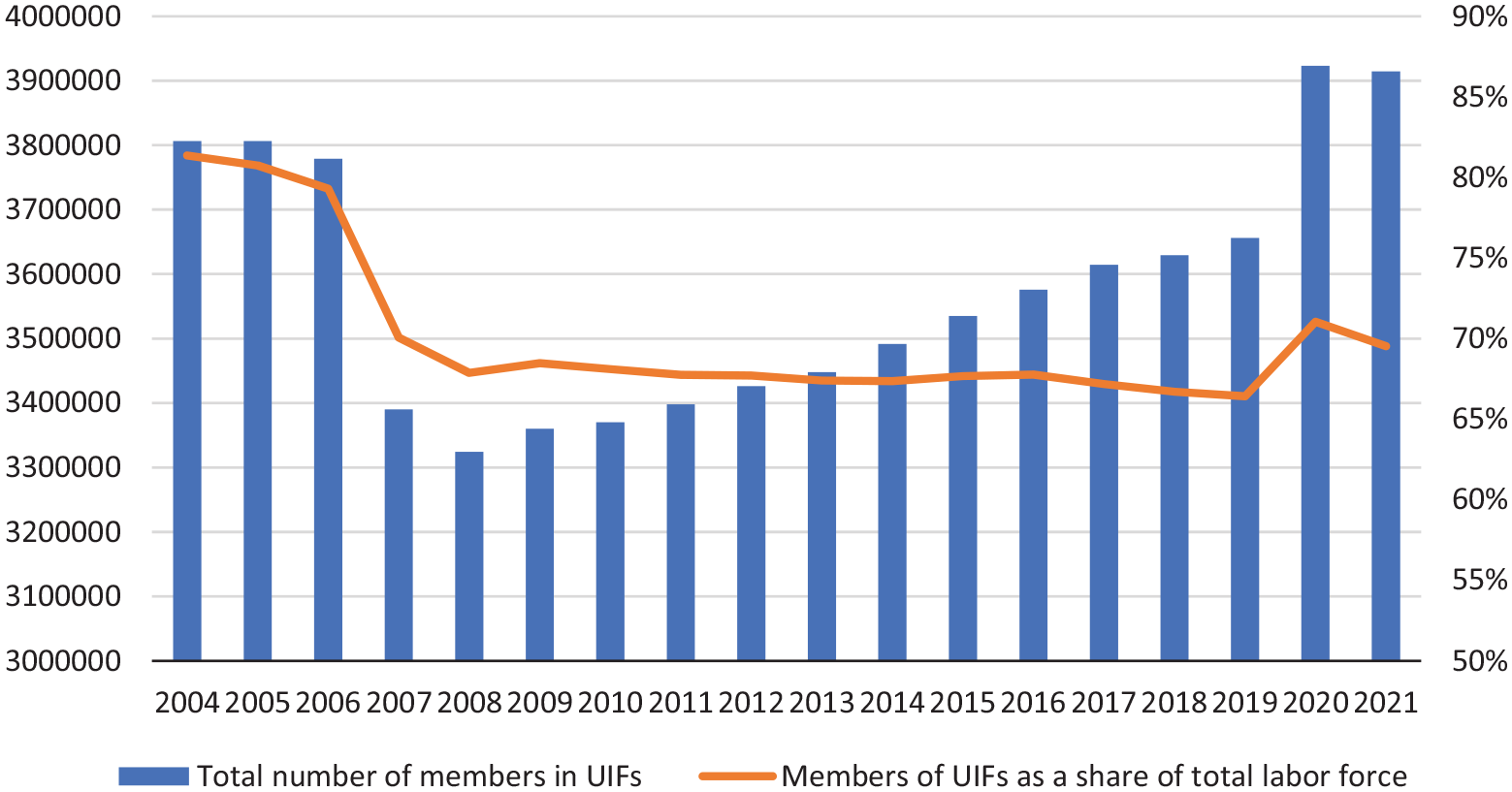

This steady retrenchment has meant that the number of benefit recipients has declined greatly since the mid-2000s (Figure 1). Reforming the UBS in 2006, the centre-right Alliance government effectively reduced state subsidies, first by raising the funds’ fees to the state, and second by abolishing the possibility for workers to deduct fund membership fees from tax. 1 Moreover, fund membership fees became differentiated, with the aim of tightening the relationship between the unemployment risk of a given fund’s members and its membership fees. This led to huge differences in fees between funds and in turn to dramatic drops in the membership of funds with high unemployment risks (Kjellberg, 2009). Though absolute membership numbers have steadily increased since the big drop in 2007, this constitutes no real recovery in light of the increase in the size of the total labour force (see Figure 2).

Changes in the total number of unemployment insurance beneficiaries and as a share of total number of unemployed (recipiency rate), 1999–2021.

Changes in the total number of members in Unemployment Insurance Funds (UIFs) and as a share of the total labour force, 2004–2021.

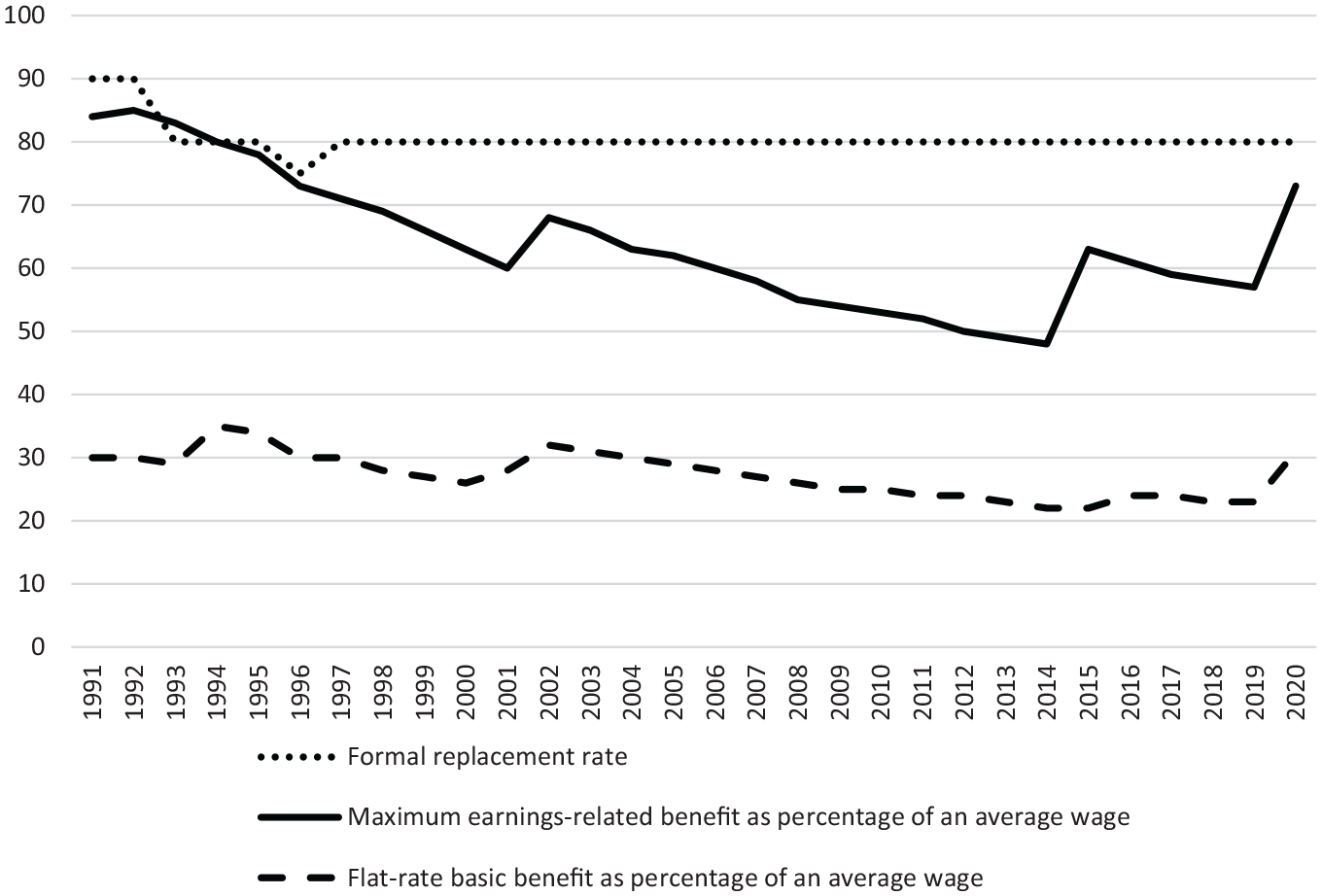

As shown in Figure 3, benefit generosity has decreased almost constantly since the 1990s (except for 2002, 2015 and 2020 when the ceiling was raised, albeit temporarily), as the maximum amount of insurable income (the ‘ceiling’) was not indexed to wages and prices. Although the gross income replacement rate has remained at 80 per cent since the late 1990s, benefits were thus de facto de-linked from wages as of the mid-1990s.

Changes in the formal, maximum and minimum replacement rates in Swedish unemployment insurance benefits, 1991–2020.

The decrease in income protection for the unemployed in Sweden becomes clear when looking at comparative data, for instance the OECD’s net replacement rate for the initial unemployment period (two months) of a single person without children (OECD, 2021). In 2002, the Swedish rate was 67 per cent, placing Sweden among the more generous OECD countries and giving it the highest replacement rate in the Nordic region. By 2014, the rate had fallen to 42 per cent, the eighth-lowest OECD replacement rate and even lower than in the US (45 per cent). Just before the COVID crisis (2019), the replacement rate was 49 per cent but had started to fall again since the increase of the wage ceiling in 2015 (see also Figure 3).

Changes during the pandemic

When COVID-19 arrived in Sweden in February 2020, a momentum developed for the Social Democrat-led government to initiate several reforms to mitigate its consequences. A furlough scheme was swiftly put in place (Müller and Schulten, 2022), together with other measures mainly aimed at helping small businesses survive the downturn. Moreover, changes were made to health insurance, another highly contested policy area. Though most of these changes were to be temporary, many have been extended several times due to the continuing crisis (Lindellee, 2021b).

A range of changes were made to the state unemployment insurance programme as well, making it more accessible for the unemployed. Qualification requirements became more generous and the waiting period was scrapped. Moreover, the benefit ceiling was raised by 30 per cent, meaning that workers on higher wages are better protected. The following is the detailed list of changes (Regeringskansliet, 2021a).

The minimum 12-month unemployment fund qualification period for the earnings-related benefit is cut to three months.

The minimum number of hours to be worked to qualify for the earnings-related and basic benefit is changed (60 hours per month instead of 80, or 420 hours for six months instead of 480), making it easier for part-time workers to qualify.

The basic benefit is raised from 365 to 510 SEK per day.

The maximum amount of earnings-related benefit is raised from 910 to 1200 SEK per day for the first 100 days of unemployment.

The six-day waiting period is temporarily abolished.

Rules allowing the self-employed to become eligible for unemployment benefits are relaxed (basic activities can continue while receiving the benefit).

Made swiftly without much political opposition, these temporary changes were initially intended to be in place until January 2021. However, in September 2021 the government decided to extend the changes until at least 2022 (Regeringskansliet, 2021b). They have led directly to an increase in insurance fund membership (see Figure 2 for 2020 and 2021). Moreover, the Ghent effect seems still to be in place, as union membership has also increased, both for blue-collar workers (2 per cent increase between 2019 and 2020) and white-collar workers (3.1 per cent increase) (Kjellberg, 2021). Overall union density increased from 68 per cent in 2019 to 69 per cent in 2020.

Given the long-term trend of declining benefit levels and tightened qualification criteria, the pandemic and its impact on the labour market can be seen as an external shock which led to radical and swift changes in many aspects of the unemployment insurance programme. It remains to be seen whether this will be a critical turning point in the development of Sweden’s UBS.

Sweden’s multi-pillar UBS and evolving union roles

The above-discussed retrenchment of the UBS provoked union collective bargaining action, with unions trying to alleviate the negative impacts on workers in different ways. Several complementary unemployment benefit schemes have been developed, turning the Swedish UBS as a whole into a very complex multi-pillar system. The term multi-pillar is used here to highlight the fact that there are different loci of unemployment benefit provision. However, a holistic picture is seldom painted by scholars. While the term ‘multi-pillar’ has been used first and foremost in pension discussions over the last few decades, its use is not common in describing the UBS.

One way of understanding the development of Sweden’s multi-pillar UBS is to view it as a way of collectivising risks in the face of the retrenchment of state welfare provision (Johnston et al., 2011, 2012; Trampusch, 2007). Viewed in this light, the emergence and development of a complementary insurance system can be seen as the unions’ attempt, in agreement with the employer organisations, to take over the responsibility of re-collectivising the risk of income loss through unemployment, at least for the growing part of workers’ wages not covered by state unemployment insurance.

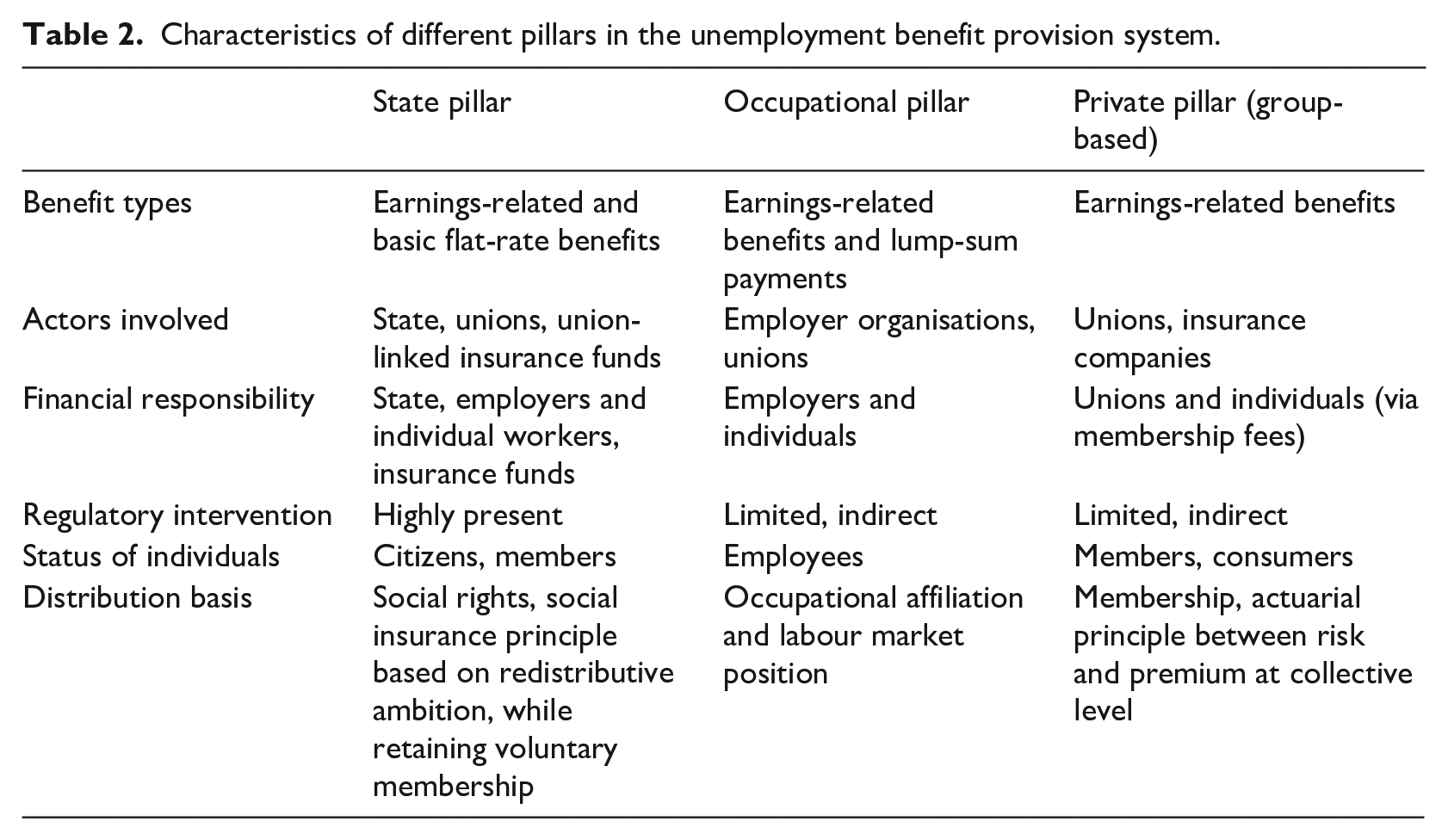

There are three co-existing pillars: the state pillar, the occupational pillar and the private pillar. They involve different types of unemployment benefits (earnings-related, flat-rate or lump-sum) and different sets of collective actors, though unions are involved in all three. They differ also in terms of how financial responsibility is shared between the state, employers and workers, to what extent they are subject to regulatory interventions, and how workers’ roles can be characterised. Generally speaking, one can say that the pillars follow different distributional paths with different exclusionary patterns, with outcomes ultimately dependent on where workers work, in what form of employment, and whether they are union members. Table 2 summarises the three pillars (Lindellee, 2018: 175, modified).

Characteristics of different pillars in the unemployment benefit provision system.

Swedish unions are involved in all three UBS pillars. The state pillar consists of the Ghent system described in the sections above, with voluntary membership in a union-linked insurance fund giving access to earnings-related benefits. However, unemployment risks are pooled among the whole workforce, with a flat-rate basic benefit paid to non-affiliated workers. The programme is subsidised by the state via employers’ labour market contribution fees.

Within the occupational pillar, either lump-sum or earnings-related benefits are paid to unemployed workers whose previous workplace was covered by a so-called Employment Transition Agreement (ETA), a collective agreement negotiated between the social partners in different industries. Managed by private foundations jointly owned by the employer organisations and the union confederations, these agreements are financed by a payroll fee. Initially established for private-sector white-collar workers in the 1970s, the coverage of this pillar has increased rapidly since the 2000s, in particular following the changes to the state UBS between 2006 and 2008 (Gordon, 2019). As of 2017, ETAs cover most workers in the Swedish labour market. The four major agreements cover state employees (The Job Security Foundation), local and regional government employees (The Transition Fund), private-sector blue-collar workers (The Employment Transition Fund), and private-sector white-collar workers (The Employment Security Council). In many of these agreements, both eligibility for and the size of benefits depend upon a worker’s age, the number of years employed and the employment type (e.g. permanent employment required) (see Lindellee, 2021a: 112 for the list of existing ETAs and coverage figures).

Looking at the private pillar, the unions provide complementary income insurance schemes to their members, topping up benefits from the state and occupational pillars (Lindellee, 2018, 2021a; Jansson and Ottoson, 2021a). These schemes are provided in collaboration with private insurance companies, meaning that they are run on the basis of actuarial principles and resemble commercial insurance policies more than social insurance schemes, albeit at a collective level (i.e., group insurance). In 2017, these union-provided schemes covered approximately half of the working population (Lindellee, 2018). Apart from civil law, there are few regulatory provisions governing this pillar. Though no official coverage statistics are publicly available, some scholars have used the number of union members as a proxy variable for estimating coverage (Davidsson, 2014; Lindellee, 2018; Lindquist and Wadensjö, 2011). The law on unemployment insurance benefit stipulates that the maximum replacement rate (80 per cent) in the state pillar is not to be exceeded through top-up payments from a group insurance. However, the gap between the ceiling (e.g. 910 SEK per day) and 80 per cent of former wages (see Figure 3) renders many employees not reaching the 80 per cent level, creating the opportunity for unions to offer complementary options targeting in particular the many white-collar workers with salaries often much higher than the ceiling. Within this pillar, individuals are first and foremost union members. Yet they are also consumers, as different unions – by advertising their complementary income insurance schemes – compete to attract more members. Moreover, most white-collar unions provide the option of raising the insurable amount of one’s salary or extending the benefit period, against an extra fee.

Consequently, risk-pooling is based on collective, non-market means in the state pillar, while the private pillar entails more individualised and market-oriented practices. From a distributional point of view, the larger the complementary pillars become, the more regressive distributional consequences are to be expected for the unemployment benefit system as a whole. This is because labour market ‘insiders’ with relative secure positions are likely to have access to the better protection provided by the complementary pillars, whereas outsiders with gaps in their employment history, not belonging to a union or insurance fund, etc. are least protected in the multi-pillar system (Gordon, 2019; Lindellee, 2018). As illustrations, permanent employment or a certain minimum length of employment is a prerequisite for all major ETA schemes, while private-sector blue-collar workers only have access to lump-sum benefits and not to the earnings-related complementary insurance benefits found in the ETAs covering public-sector employees and private-sector white-collar workers.

The unions’ entrenched role in Sweden’s UBS illustrates their fundamental stake in protecting the unemployed, and thereby offsetting downward pressure on wages. While the Ghent system, with its strongly state-subsidised unemployment funds, remains highly cherished by the key collective players, the unions – at least those organising white-collar workers (SACO and TCO) – have actively engaged in developing complementary pillars to compensate for the retrenchment in the state pillar. Paradoxically, the deteriorating benefits from union-linked unemployment funds have created leeway for unions to regain control over unemployment insurance, using it to recruit members (Lindellee, 2021a). The next section of this article discusses a new phase of this trajectory, with the social partners proposing new UBS governance arrangements and calling for greater control over UBS funding and regulation.

The latest development: a new proposal for a bilaterally regulated unemployment insurance system

Sweden is going through a turbulent period in the wake of proposals to reform the Employment Protection Law (EPL). These also cover the UBS. The current Swedish government made up of the Social Democratic Party (SAP) and the Green Party took office in January 2019, after lengthy coalition talks following the September 2018 election. Without a majority in the Riksdag (the Swedish parliament), this government has to rely on the support of two other centre-right parties (the Liberals and the Centre Party), at the cost of a deal struck with them after long and very difficult negotiations. The so-called ‘January agreement’ listed 73 political reforms that the government needed to implement to gain the support of the two parties for the rest of its term of office. This has led to government policies exhibiting a rather eclectic amalgamation of different ideological preferences, especially regarding a range of socio-economic issues. Item 20 of the deal concerned a liberalising EPL reform, though it also included a clause opening up the possibility for the social partners to reach a collective agreement on employment protection in line with the spirit of the January deal. For the Social Democrats, this was a much better option, as a liberalisation of the EPL would have gone against the labour movement’s core values. Consequently, the government pressured the social partners via a series of new legislative proposals based on a government-led inquiry, including a relaxation of the seniority rule when dismissing workers (‘last-in-first-out’), to be adopted unless the social partners reached agreement (SOU, 2020).

In December 2020, an agreement on ‘Security, transitions (omställning) and job protection’ was concluded between the Confederation of Swedish Enterprise (SN), PTK (the council for negotiation and cooperation for salaried employees in the private sector, representing 25 unions), and two of the most influential LO unions, Kommunal (union of public employees) and IF Metall (PTK, 2021). However, the umbrella LO union confederation was not initially party to the agreement due to strong resistance from several LO unions (this has since changed, with LO becoming party in November 2021). According to Kjellberg (2021), the agreement has the potential to be at least as important as the 1938 Saltsjöbad agreement and the 1997 Industry agreement.

The agreement between the social partners included a radical proposal: a comprehensive reform of the UBS governance structure under which the social partners, via collective agreements, would run the state UBS for the majority of workers (those in companies covered by collective agreements) (Johansson et al., 2020). In the minutes of the negotiations, the decision in favour of the proposal figures prominently in paragraph 3, with both parties seeing several advantages – a ‘win-win’ situation – in fully taking over the UBS. Looking first at the employers, they perceive their present contribution to financing the UBS, the so-called labour market fee, as a hidden tax rather than a fee. According to the parties, between 2010 and 2019, total labour market fees collected far exceeded the state’s expenditure on benefits. Calculated at approximately 62bn SEK, the surplus flowed directly into the state budget. With an insurance scheme governed by collective agreements, the employers see the potential to decrease the fee and their contribution.

Turning to the unions, they see a possibility to regain control over unemployment insurance with regard to eligibility criteria and benefit levels. While Kommunal and IF Metall hope to change the criteria to make it easier for their members to qualify for the benefit, especially for groups experiencing difficulties in qualifying (e.g. temporary workers), the white-collar unions want to increase the income ceiling, thereby enabling more of their members to attain the 80 per cent income replacement level.

One explicit goal of the proposal is to reduce political influence on the UBS. The proposal makes it clear that the current labour market fees should be replaced by the contributions to the collective agreement-based UBS, run for instance by a new foundation established by the social partners. Moreover, the social partners – i.e., not the state in the form of the IAF – would decide on the detailed UBS rules and would be responsible for supervising the insurance funds. The union-linked unemployment insurance funds responsible for administering the payment of benefits and collecting membership fees would remain in place. The main motivation for this proposal is that a UBS regulated by collective agreements would become more stable in the longer term and would strengthen the Swedish model of labour market regulation by the social partners.

While the proposal outlines a UBS based on collective agreements solely for the private sector, the upcoming government inquiry agreed in the summer of 2021 will look not only into the feasibility of the social partners’ proposal, but also into whether such a scenario could be extended to the public sector. 2 The inquiry will, inter alia, study the reasons why the social partners want to change the UBS, and how a collectively agreed insurance scheme would relate to the legislation governing the state budget, and especially how a fund-based system would tie in with the strict budgetary discipline required by current budget legislation. The last question is important as the proposed system would require that the government be prepared to step in with funding in the event of an unemployment crisis overstretching the resources paid in by the social partners (i.e., fees from employers and union members). This seems to be one of the most crucial questions for any new system. A further tricky question is whether the state is prepared to give up the tax revenues generated by the current system.

Discussion

The Ghent system is in many ways an ‘ugly duckling’ in the otherwise mainly universalistic and state-centred Nordic welfare states, as it relies extensively on ‘civil society’, with the unions and their insurance funds acting as ‘private’ providers of social security (Goul Andersen, 2012). While the Ghent model was introduced very early in Norway and Denmark and much later in Sweden, the system’s liberal features – a government supporting unions’ solidarity measures for their unemployed members – have over time become more state-controlled, in a way confirming the initial fears voiced by union leaders on introducing the Ghent system. In the Swedish case, the UBS has become a battleground for partisan politics over the last few decades, illustrating the Ghent system’s key function as a power resource in the labour market. As the Ghent effect – the blurred distinction between unions and funds – still seems to exist, the income protection that comes with fund/union membership is a key union power factor. Consequently, and paradoxically, the ugly duckling seems to be of essential importance in the battle for an encompassing welfare state.

Unemployment benefit generosity increased until the 1990s. Conservative governments have since invested great effort in weakening union influence on the UBS. Examples include the Bildt government’s failed 1994 attempt to abolish the Ghent system altogether, and the Reinfeldt government’s 2007 hike of fund membership fees resulting in a major drop in fund and union membership. Social democratic governments have left several changes in place – and added some themselves –, leading to stricter entitlement requirements and less generous income protection. Together with changes in other key labour market institutions – the wage bargaining system (Baccaro and Howell, 2017), employment protection legislation (Emmenegger, 2014) and active labour market policies (Bengtsson and Berglund, 2012) – the direction of the changes can only be described as neoliberal, exposing workers more to market forces (Lindellee, 2018).

At the same time, the UBS has become more dualised. This is firstly an effect of tightened eligibility criteria, making it harder for temporary and part-time workers to qualify for the state unemployment insurance benefit. Moreover, the increase in fund membership fees in the period 2007–2014 led many workers to quit funds, leaving them without any income-related protection at all. In addition, the erosion of the income replacement ceiling in the state pillar has greatly impacted benefit levels for the large majority of employees – with ambiguous consequences. On the one hand, it has created opportunities for unions to develop complementary income insurance schemes conditional on union membership and thus incentivising workers to become union members. On the other hand, the UBS pillars tend to solely protect workers with a strong attachment to the labour market – mainly white-collar workers, especially in the case of the ETAs. Consequently, the development of complementary insurance schemes has been beneficial for member recruitment in unions (above all, TCO and Saco) organising those workers with salaries generally much higher than the replacement ceiling in the state scheme and therefore with a stronger incentive to take up complementary earnings-related insurance schemes.

The latest social partner proposal for a collectively agreed unemployment insurance is a radical new step in the development of the Swedish UBS. The proposal itself is highly illustrative of the social partners’ continued involvement in the governance of Sweden’s UBS and ties in with observations that it is in countries like Sweden, with its ‘organised corporatism’, where occupational welfare can be developed most (Riva and Rizza, 2021). Similar to the way Swedish unions preferred to provide severance pay via collective agreements rather than via company-based schemes (Ozkan, 2019, 2020), the new initiative can be regarded as an attempt to strengthen incentives for a high degree of organisation among both employers and unions. While the previous development of complementary benefit schemes can be partly understood as a reaction to the retrenchment of the state pillar, the new proposal of a UBS regulated by collective agreements highlights, in a sense, the even bolder social partner ambition to run the UBS more directly than today.

However, it is difficult to assess the distributional outcomes of the proposed system. This depends, for example, on whether public-sector workers will be covered, and on the possibilities for workers not covered by collective agreements to access benefits. Should the unions succeed in attracting new members and covering areas of the labour market that are hard to organise – i.e., becoming encompassing organisations –, then the proposed governance structure will probably provide better protection than today’s system. In the event of failure, however, the insider-outsider divide on the Swedish labour market may become even more salient.

The win-win situation foreseen by the social partners may turn out to be a zero-sum game, with just marginal gains (e.g. eligibility criteria, ceiling etc.) requiring complicated and tough negotiations. Moreover, the related EPL changes included in the social partners’ December deal have reduced unions’ bargaining power. How this will spill over onto the governance of the UBS cannot yet be predicted. Side-effects may also materialise in the other UBS pillars, in particular when employer incentives to continue contributing to the occupational pillar are weakened as a consequence of the proposed, collectively governed unemployment insurance scheme and of EPL liberalisation. Concerning the latter, some researchers regard a strict EPL as a key condition providing unions with the necessary leverage in negotiating Employment Transition Agreements and similar agreements (Engblom, 2018: 892, 900–901; Jansson and Ottoson, 2021b: 16).

Conclusion

Over the last few decades, the Ghent system in Denmark, Norway and Sweden has come under pressure. In both Denmark and Finland, low-cost funds not requiring union affiliation became alternatives for many workers wanting to escape the costs and ideological alignment inherent to union membership (Kjellberg and Lyhne Ibsen, 2016). In Sweden, however, the introduction of the non-union-affiliated Alfa fund in 1998 did not affect the Ghent system in a similar way. Instead, conservative governments have repeatedly tried to weaken the system from within, particularly in 2007 when the sharp hikes of fund membership fees led to a significant decline in union density, but also to large numbers of unemployed without adequate income protection. Despite being hurt by the various policy changes, the unions found new opportunities to safeguard the Ghent effect. The multi-pillar development of the UBS, with its group-based private insurance schemes and employment transition support governed by collective agreements, has provided new incentives for union membership, albeit with the side-effect of mainly benefiting white-collar unions and risking an accentuation of the insider-outsider divide with regard to both protection and worker representation.

The difficult parliamentary situation in Sweden in recent years seems to have created a new momentum for the social partners to retake the initiative. Despite strong pressure from the government, the EPL negotiations have resulted in an agreement putting the social partners back in the driver’s seat. If, as they foresee, the agreement also results in a new UBS governed via collective agreements, the potential offered by a reinforced Ghent system may materialise. However, the risks inherent to such a system – increased dualisation of protection, a conflict-ridden unemployment benefit system and, in the event of a deep recession with high unemployment, the risk for a full state-takeover – need to be considered.

Footnotes

Funding

This research was partly funded by the Swedish Research Council for Health, Working Life and Welfare [dnr 2016-07204].

1

Prop. (2006/07:15) En arbetslöshetsförsäkring för arbete [An unemployment insurance programme for work].

2

Dir. 2021.64 Kommittédirektiv. Förutsättningar för en ny kollektivavtalad arbetslöshetsförsäkring. Regeringskansliet. Arbetsmarknadsdepartement.