Abstract

The compromise that emerged from the lengthy debate on European unemployment insurance (EUI) involved the establishment of a ‘European Unemployment Reinsurance Scheme’. However, it was not until the shock waves of the COVID-19 pandemic were felt that any specific measures were actually taken to establish such a scheme. The reasons for such prevarication were, first, doubts as to whether moral hazard can be kept under control and, second, the huge diversity of EU Member States’ coverage and level of social protection. This article offers a third reason for this protracted stalemate: the neglect of moral assurance as a countervailing force of moral hazard. It argues that the concept of unemployment insurance itself needs to be fundamentally revised. Modern labour market policy must cover not only income risks related to unemployment, but also other serious income risks related to critical transitions over the life course. Finally, this article proposes the extension of the European Social Fund to create a European Employment and Social Fund with elements of work-life insurance and a reinsurance mechanism for shock absorption.

Le compromis qui a émergé du long débat sur l’assurance-chômage européenne (EUI) impliquait la création d’un “régime européen de réassurance-chômage”. Il a néanmoins fallu attendre les ondes de choc de la pandémie du COVID-19 pour voir apparaître des mesures spécifiques visant à mettre en place un tel système. Ces hésitations étaient liées, d’une part, aux doutes quant à la possibilité de maîtriser l’aléa moral et, d’autre part, à la grande diversité de la couverture et du niveau de protection sociale dans les États membres de l’UE. Cet article propose une troisième raison à cet enlisement prolongé : le fait de négliger l’assurance morale comme contrepoids à l’aléa moral. L’auteur soutient que le concept d’assurance-chômage lui-même doit être fondamentalement révisé. La politique moderne du marché du travail doit couvrir non seulement les risques de revenus liés au chômage, mais aussi d’autres risques de revenus, importants et liés à des transitions critiques au cours de la vie. Enfin, l’article plaide en faveur d’un élargissement du Fonds social européen, avec la création d’un Fonds social et de l’emploi européen qui comporterait des éléments d’assurance vie-travail et un mécanisme de réassurance destiné à absorber les chocs.

Nach einer langen Debatte über eine europäische Arbeitslosenversicherung tauchte eine europäische Arbeitslosenrückversicherung als Kompromiss auf. Konkrete Schritte in diese Richtung wurden jedoch erst unter dem pandemischen Schock von COVID-19 als Katalysator unternommen. Zweifel, ob “moral hazard” unter Kontrolle gehalten werden kann, sind ein Grund für dieses Zögern, die enorme Diversität von Deckungsgrad und Niveau des Sozialschutzes in EU-Mitgliedstaaten ein anderer. Dieser Essay hebt einen dritten Grund für das lange Patt hervor: die Vernachlässigung von “moral assurance” als Gegengewicht von “moral hazard”. Er argumentiert, dass das Konzept der Arbeitslosenversicherung selbst einer fundamentalen Revision bedarf. Moderne Arbeitsmarktpolitik sollte nicht nur Einkommensrisiken bei Arbeitslosigkeit decken, sondern auch andere ernsthafte Einkommensrisiken bei kritischen Übergängen im Lebensverlauf. Er schlägt vor, den Europäischen Sozialfonds zu einem Europäischen Beschäftigungs- und Sozialfonds mit Elementen einer Arbeitslebensversicherung und einer Rückversicherung für Schock-Absorption zu erweitern.

Keywords

Introduction

We must also do more to support those who lose their jobs because of external events that affect our economy. This is why I will propose a European Unemployment Benefit Reinsurance Scheme. This will protect our citizens and reduce the pressure on public finances during external shocks. (von der Leyen, 2019: 10)

This proposal by the new President of the European Commission echoed an idea which, at the time, had gained common ground among the vast majority of researchers who were interested in strengthening Europe’s social dimension (Beblavý and Lenaerts, 2017; Beblavý et al., 2017; Dullien et al., 2018; Luigjes et al., 2019). ‘European Unemployment Reinsurance’ (EURI) subsequently replaced the original concept of a genuine European unemployment insurance (EUI), which had lost all support during the decades-long debates (Andor, 2016; Dullien, 2015; Schmid, 2019a).

Yet, it was not until the sudden shock of the coronavirus pandemic, whose effects were far more severely felt than originally anticipated, that any specific steps towards such a scheme were taken. The COVID-19 pandemic served as a catalyst for the establishment of a temporary unemployment reinsurance scheme called SURE, a €100bn fund for ‘Support to mitigate Unemployment Risks in an Emergency’. SURE loans are intended to help EU Member States to preserve employment, either in the form of short-time work (STW) or similar schemes (part-time unemployment) as an alternative to lay-offs or redundancies. SURE was immediately welcomed as a first step towards developing a genuine EURI scheme (Vandenbroucke et al., 2020).

Both ideas, however, give rise to a number of problems. Whereas EURI limits the European dimension of social protection to the stabilisation function of unemployment insurance, even the proposal for a genuine EUI – albeit one that goes beyond the current EU legal framework – fails to address the broader issues of social protection in modern labour markets. Despite the emerging common sense policy trends and good political intentions, it also remains unknown to what extent SURE can help prevent mass unemployment – in particular long-term unemployment – in the long run, and whether it serves to shape the institutional contours of a sustainable EURI model. Moreover, to date, EURI has been considered as an institutional device intended only for the eurozone and not for the entire EU-27.

Against this backdrop, I shall propose a pragmatic yet radically different approach to strengthening the EU’s social dimension with a view to the establishment of a European Social Union (Ferrera, 2018; Vandenbroucke and Vanhercke, 2014). This proposal takes into account both the stabilisation function and the social protection function of job loss, while building on the established EU institutions and their respective experiences. The concept of unemployment insurance itself, however, needs to be fundamentally revised: modern labour market policy must cover not only income risks related to unemployment, but also other serious income risks related to critical transitions over the life course. Work should pay, but so should transitions between various employment relationships; social protection institutions should enable people to adapt to the market, but the market should also adapt itself to the changing needs of workers over their life course. This opens up the perspective of ‘work-life insurance’ which places the emphasis on moral assurance, i.e., enhancing individual autonomy, rather than on moral hazard, i.e., controlling the exploitation of insurance. 1

This article contributes to this vision in two respects: first, it outlines the theory of moral hazard and moral assurance, and elaborates the principles involved in effectively covering the growing variety of social risks over the life course and reshaping social security institutions in order to meet these norms; second, it proposes that, in order to cover a broader spectrum of social risks, the best solution in the current political stalemate would be to enhance and extend the existing European Social Fund (ESF) to create a European Employment and Social Fund (EESF), one which includes elements of work-life insurance as well as a reinsurance mechanism for shock absorption. The article then goes on to discuss the features of such a fund before summarising with some concluding remarks.

Moral assurance: the forgotten feature of social insurance

How should income from dependent work, i.e., wages or salaries – often still the only source of income for ordinary workers – be protected in the event of involuntary unemployment? Should the mechanism providing a ‘bridge’ between the job that has been lost and the new job be based on flat rate benefits financed by taxes and covering – at least in principle – all citizens of working age, or should it be based on previous earnings financed by proportional contributions and paid only to those with some work history (i.e., employee/employer contributions)? For a long time, these two opposing views informed the debate on social protection systems in Europe (Esping-Andersen, 1990). Although not strictly ‘coded’ in any guidelines, contribution-based regimes without means-testing are usually denoted as ‘Social Insurance Schemes’, whereas tax-based regimes with means-testing tend to be called ‘Social Assistance Schemes’. Meanwhile, existing social protection schemes began to combine elements of both, showing a trend towards institutional convergence (Clasen and Clegg, 2011). A reason for this might be the progress made towards economic integration in the EU and the principle of free movement of labour (Bruzelius et al., 2016). Thus, the debate on ‘Social Europe’ should focus on consistent political norms and economic functions designed to fulfil those norms (Schelkle, 2006). To that end, explicit consideration of such norms and functions in connection with social protection against labour market risks is essential.

Several arguments call for the maintenance and enhancement of the social insurance principle (Atkinson, 2013; Barr, 2001; Schmid, 2017, 2018: 129–148). Ex ante risk-sharing (Schmid, 2015) involving a degree of solidaric redistribution is the essence of social insurance, which has at least seven significant advantages compared to ex post, flat-rate and means-tested social security: Social insurance benefits are better protected than means-tested benefits against discretionary political decisions, due to targeted individual or employers’ contributions establishing a kind of property right (Schmid et al., 1992: 88, 248). This is also important as more and more people from outside the European Union work on the EU labour market acquiring such entitlements through paying contributions.

2

Contribution systems are often complemented by fiscal budgets legitimising explicit redistribution to overcome the tendency of contribution systems to be overly selective in favour of standard employment relationships due to the required contribution history. Yet the strong rationale for relying heavily on contributions remains.

3

The shift of tax bases away from earnings and social security contributions would weaken the nexus between the costs and benefits of social security perceived by workers and the direct link to labour costs that can be used for political exchanges in social pacts and collective wage agreements, e.g. wage coordination and wage restraints. The weakening of this link is likely to lead to the loss of the traditional political support of the social partners (Schelkle, 2006: 252–253). Individual and wage-related benefits can be calculated more easily, transparently and fairly than benefits that have to be means-tested; even if these benefits are flat rates (no calculation needed), the means tests afford a significant amount of administrative discretion, often leading to a high number of appeals (for the case of Germany, see Schmid, 2018: 147, 258). The employment incentives of work-related social insurance benefits are stronger than for means-tested benefits, not least due to the entitlement effect, which can completely eliminate the moral hazard problem in job searches (Zhang and Pan, 2017). The macroeconomic stabilisation impact of wage-related replacements is higher than that of (usually lower) means-tested benefits (Dolls et al., 2011). Generous short-term unemployment benefits – up to about nine months of unemployment – also have positive external effects: decent benefits ensure liquidity for low or medium wage-earners during unemployment, thus maintaining effective demand and reducing cut-throat competition between insiders (covered by insurance) and outsiders (not covered by insurance). They also provide individual workers with the choice to reject non-standard work, especially in its precarious forms, and they protect people from resorting to costly consumer credit (Chetty, 2008; Gangl, 2004; Hsu et al., 2014; Lalive et al., 2015). Jobless people covered by unemployment or work-life insurance remain healthier and more self-confident than jobless people without such benefits or with only means-tested benefits due to the provision of income and employability security (López-Casasnovas and Maynou, 2018; Rodriguez, 2001).

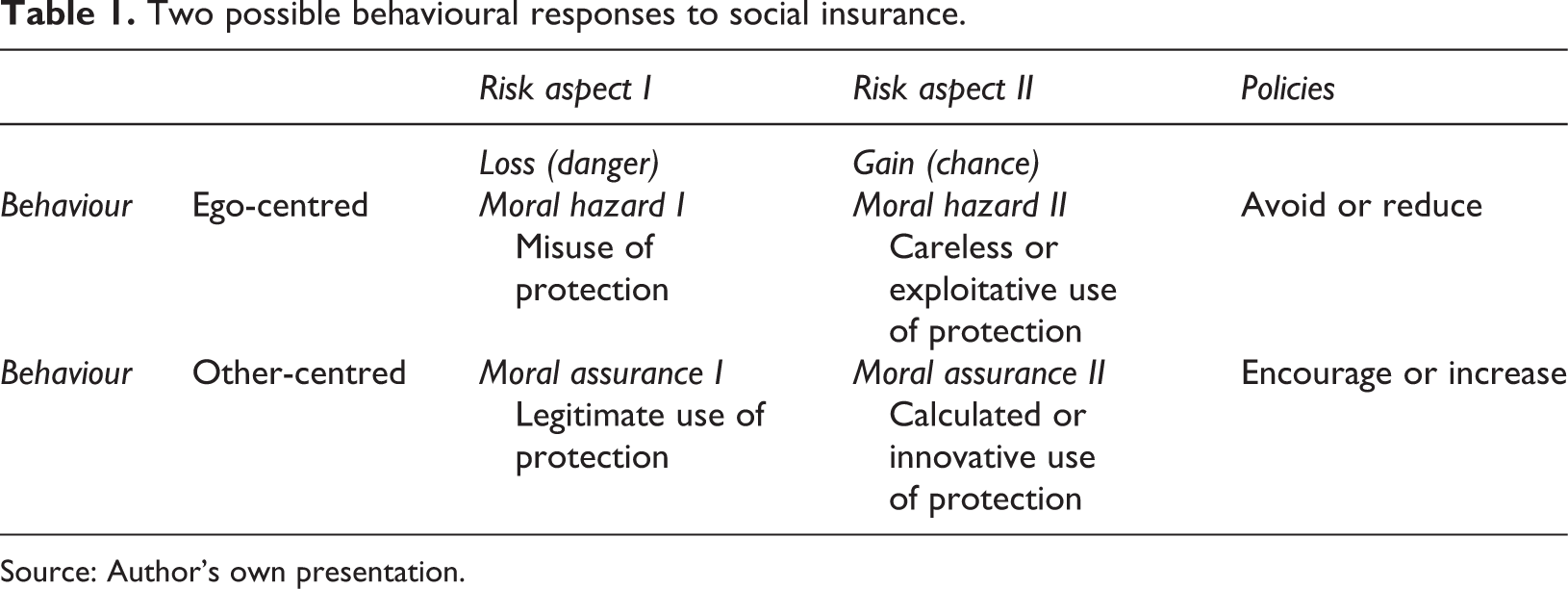

Moreover, a general theoretical argument can be made in support of these particular advantages to the effect that social security benefits also have a productive function (Acemoglu and Shimer, 2000). Mainstream economists often neglect or even deny this function by focusing solely on costs and on possible negative behavioural impacts of any kind of social protection or insurance, namely ‘moral hazard’ (Rowell and Connelly, 2012). They disregard or omit the positive counterpart of moral hazard, namely ‘moral assurance’ stemming from the other-centred behavioural response to risk exposure. 4

As Table 1 shows, risk always consists of two aspects (Bernstein, 1996): the potential loss in case of misfortune, which reflects the dangerous element of risk; but also the potential (and often greater) gain in case of good fortune, which reflects the chance or opportunity element of risk. Furthermore, people can respond to these two aspects in one of two ways. If ego-centred behaviour dominates, moral hazard occurs in two forms: misuse of protection and careless or exploitative use of protection. In the first instance, workers may claim benefits fraudulently or by quitting their job voluntarily; in the second instance, workers may make very little effort to find a new job, or employers, in the knowledge that their workers are well protected, may more readily dismiss them. If other-centred behaviour dominates, moral assurance leads to a legitimate use of protection in case of involuntary loss of employment or enforced reduction of working time (short-time work or partial unemployment) and related income, which contributes to social cohesion and trust; it may, however, also lead to calculated or even innovative use of protection in case of risk taking for potential large gains.

Two possible behavioural responses to social insurance.

Source: Author’s own presentation.

In other words, if workers can rely on social protection in case of misfortune, they will overcome their innate risk aversion and have the courage to take calculated risks, e.g. to change jobs and invest in continuous vocational training, thereby contributing to mobility, innovation and structural change. Moreover, they will be more inclined to cooperate with colleagues and demonstrate loyalty to their employers because they have trust in fair redistribution in case of misfortune. Both aspects of moral assurance enhance productivity and economic prosperity if the other possible behavioural response to social protection (moral hazard) is effectively controlled.

The appropriate core response of social insurance systems to the new risks of modern labour markets is the establishment of new social rights and new social obligations on both sides of the behavioural risk portfolio depicted in Table 1. 5 The new social rights would be new in that they cover subjects unfamiliar to industrial wage-earners on which the traditional standard employment relationship is built: rights to education and training, to appropriate working hours including the right to request shorter working hours, to occupational redeployment, retraining or vocational rehabilitation, and – last but not least – to a flexible employment guarantee through the state (Atkinson, 2015: 140–147). The scope of new social rights would also be new since they would cover not only ‘standard’ wage-earners but also the ‘non-standard’ part-time workers, the self-employed or semi-self-employed, the temp-agency and marginal workers and even zero-hours contract workers. One example would be to include the risk of reduced earnings capacity in a way that is analogous to short-time work (of full-time workers) covered by work-life insurance: the income loss caused by reduced working time (due to, for example, unpaid care obligations) could be compensated for by part-time unemployment benefit or – as in the case of Germany (Schmid, 2019b) – a wage-related parental leave allowance. Such an insurance benefit would also be helpful in response to the increasing demand for care for the frail and elderly. The new social rights are new in nature because they often take the form of vouchers, social drawing rights or personnel accounts, which provide transition securities from one labour contract to another and allow workers to rely on solidarity within defined and perhaps collectively bargained limits when exercising their new freedom to act (Korver and Schmid, 2012).

As these new rights enhance the range of individual choices, a corresponding new field of individual responsibilities opens up (Sen, 2009: 19). The new social obligations arising from the extended freedom to act would be new in that they cover aspects unfamiliar in the traditional employment relationship: obligations to provide training and retraining both for employees and for employers so as to maintain employability and management capabilities; to search actively for a new job or accept a less well-paid job under fair compensation rules; to promote healthy lifestyles and occupational rehabilitation; to make reasonable workplace adjustments that reflect the capabilities of workers or to change working times either to meet the needs of the individual life course or to keep pace with the volatile market demands for goods and services. The scope of new social obligations would also be new since they would cover not only certain categories of workers or employers but also the core workers in open-ended contracts and all firms irrespective of size and function. For example, the exemption of civil servants or the self-employed from contributing to social security (especially pensions and unemployment insurance), as is the case, for instance, in Germany, would not be justified under the regulative ideal of inclusive labour contracts. The new social obligations would be new in nature since they often take the form of a ‘voice’, residing in the willingness to negotiate at individual, firm, regional and branch level in order to reach mutual agreements and to seek compromises that reconcile different interests: in other words, ‘negotiated flexicurity’ at all levels (Schmid, 2008: 317–322).

Two specific strategies follow from this relaunch of social insurance and ex ante risk-sharing. First, it is not enough that work should pay: transitions should also pay by extending social insurance principles beyond the risk of unemployment to include, in particular, volatile income risks associated with critical events over the life course (school-to-work transitions, job-to-job transitions, working time transitions and work-to-retirement transitions) reflected, to some extent, in non-standard forms of employment. Second, it is not enough that workers are able to adapt to the market: the market also needs to adapt to the workers (Gazier, 2003) through capacity building of employers and employees to enable them to adjust to uncertainties (Deakin and Supiot, 2009), in particular through enhanced investment in human capital and the workplace environment.

What implications do these principles have for the debate on European unemployment insurance (EUI)? Should it be, in essence, a genuine and uniform system, possibly with extra benefits and coverage depending on national traditions, or should national social security systems remain at its core but with EU-enhanced institutional capacities? 6 In this article, an argument will be made for the second solution, one which leads to the proposal of extending the European Social Fund to create a European Employment and Social Fund. However, in the light of the current volatile situation, we must first take into account the immediate policy impact of the COVID-19 pandemic.

The rationale behind extending the European Social Fund (ESF) to create a European Employment and Social Fund (EESF)

In response to the COVID-19 crisis, the EU introduced a new instrument for temporary Support to mitigate Unemployment Risks in an Emergency (SURE), which provides low-interest loans of up to €100bn to Member States to finance short-time work schemes. Accordingly, rather than an ‘unemployment (re)insurance scheme’, this instrument actually serves as a ‘job insurance scheme’, which is an essential element of the proposed work-life insurance system set out in this article. In supporting national unemployment benefit schemes in the EU, SURE has the potential of substantially keeping down the number of unemployed compared, for instance, to the United States where the unemployment rate increased from February to April 2020 by 10.3 percentage points to 14.7 per cent. Equally important is that SURE is based on Article 122 TFEU and funded as a European instrument backed by €25bn guarantees committed by Member States to the EU budget to leverage its financial power. Proponents of this scheme were quick to welcome SURE as a ‘specific “plug in” to an encompassing European unemployment insurance scheme, ready to be installed immediately in the context of such exceptional emergencies’ (Vandenbroucke et al., 2020).

Yet it soon became apparent that this kind of support in the form of soft loans was not enough to prevent a sharp increase in levels of public debt in hard hit countries such as Italy and Spain. Consequently, on 18 May 2020, Macron, Merkel and von der Leyen stepped in with an initiative proposing that the EU borrow on the financial markets in order to disperse some €500bn through grants plus €250bn in loans to European economies hit hardest by COVID-19. This proposal, however, is contested by some Member States that see the initiative as a Trojan horse towards the EU’s becoming a transfer union: the Member States receiving the funds would not need to repay the cash, and so liability for the debt would instead be added to the EU budget, to which Member States contribute according to the size and prosperity of their economies; the European Commission would borrow the money on behalf of the EU. Indeed, should the proposal receive the endorsement of the 25 other EU Member States, it would amount to a significant move towards a new level of risk-sharing involving fiscal transfers firmly opposed during past crises.

Reasons for extending the ESF

As the outcome of the negotiations taking place at the highest levels in Brussels, including the discussions on the mid-term financial plan (2021–2027), is not known at the time of writing, this article must rely on conceptual considerations as to how the architecture for a new European employment and social protection strategy might look. The main reason for the stalemate surrounding EUI before coronavirus hit was the enormous diversity of national unemployment insurance (UI) systems and the fact that the UI regimes in place in many EU Member States are poorly developed (Clasen and Clegg, 2011; Esser et al., 2013; Leschke and Finn, 2019). In many Member States, unemployment insurance benefits cover a fairly limited range of workers. Moreover, many have not only poor capacities for employment promotion but also scarce resources for wage replacement. This latter dimension of UI is usually largely underestimated if not overlooked by neoliberal economists. Yet it is a grave mistake to consider unemployment benefits merely in terms of a ‘passive’ transfer, rather than the ‘active’ promotion of jobs and requested skills. To both workers and employers, reliable and generous unemployment benefits are anything but passive. They offer not only a fair offsetting of individual risk for workers who become unemployed through no fault of their own, but also an ‘active’ investment in their productive job search. Empirical studies show that unemployed workers endowed with generous wage replacements in the first six to nine months find more productive jobs than unemployed workers receiving no or only marginal benefits. Even more importantly, these jobs are more sustainable. Generous short- and medium-term benefits avoid or mitigate revolving door effects, i.e., quickly out of and quickly back to benefits (Acemoglu and Shimer, 2000; Gangl, 2004). Moreover, unemployment benefits link jobless people to employment services and employment promotion measures. In the absence of accessible unemployment benefits, it can be difficult to reach out to those facing multiple barriers to employment, who therefore risk being left behind; thus, achieving good benefit coverage can be essential to make an activation strategy effective and sustainable (OECD, 2018: 185–210). 7

Effective employment services and sensible dismissal protection are therefore essential elements of inclusive work-life insurance schemes; they are also vital for overseeing the moral hazard inherent in any system of insurance, including institutional moral hazard (Vandenbroucke et al., 2016). Evaluation studies unanimously emphasise the importance of implementation capacities for the effectiveness and efficiency of ‘active’ labour market policies, which are underdeveloped in most of the Southern and Eastern European EU Member States. The lack of such capacities also limits the potential impact of important EU initiatives, such as the Youth Guarantee (Escudero, 2018). Effective employment services, in combination with inclusive unemployment insurance, can also support those enterprises forced to respond to large-scale structural changes with staffing measures in order to maintain or improve their competitiveness. Such services, moreover, can also help to prevent long-term unemployment through targeted labour promotion measures. National unemployment insurance systems, which prudently balance support and control, increase the capacity of inbuilt stabilisers as well as the capacity of interregional redistribution aimed at comparable European standards of living, thereby also reducing the pressure of migration.

Support for institutional capacities is already an element of the ESF, albeit on a minuscule scale. This function could be developed beyond the current interim instrument of SURE and oriented on a permanent basis in two directions. First, national unemployment insurance schemes could be helped to include employment risks over and above unemployment, in a move towards work-life insurance. Reasons for including such risks are increasing individualisation (e.g. increase in the number of single parents), demands for greater inclusion in the labour market (e.g. of the disabled or the elderly) and greater working time flexibility over a person’s lifetime (e.g. caring for children or the frail and elderly); a further reason concerns the increasing interdependencies between EU Member States and EU policies, in relation, for example, to joint ventures for green jobs or combating climate change, which might cause structural disruptions.

Such an enhancement of institutional capacities would – apart from strengthening the subsidiarity principle – improve the inbuilt stabilisation function of national insurance systems. In emergency situations, however, this would not suffice. The uncertainties of globalisation demand more, as the COVID-19 pandemic – while being an exceptional case – has proven convincingly. The second element, therefore, to be added to the envisaged EESF is a fiscal capacity to enhance the stabilisation function of national unemployment insurance schemes, since deep economic recessions usually inflict asymmetric shocks on national economies. The provision of low-interest loans to national insurance schemes in deficit would enable them to maintain their ability to overcome such critical situations. Alternatively, and in line with the US model, an emergency fund could provide financial assistance, particularly in a symmetric shock situation like that caused by COVID-19. To that end, it could be used to ensure wage income security and thereby uphold effective demand, instead of responding with pro-cyclical reactions such as benefit reductions or even increased contributions or taxes.

Features of the EESF

A whole set of institutional requirements would have to be met before a fund of this kind could become operational. From the outset, minimum standards for national insurance systems would need to be set (Luigjes et al., 2019). European law lays down three relevant (albeit contested) principles that might provide guidance in selecting the instrument – in the form of European directives – needed as a basis for such standards. First, according to Article 153 TFEU, ‘the Union shall support and complement the activities of the Member States’ in the field of, inter alia, ‘social security and social protection of workers’. Second, Article 352 TFEU allows the Council (‘acting unanimously on a proposal of the Commission and after obtaining the consent of the European Parliament’) to adopt appropriate measures to attain the objectives set out in the Treaties, such as full employment, a high level of protection, social progress, justice, cohesion and solidarity (Article 3(3) TEU). Although the ‘European Pillar of Social Rights’ still lacks formal legality, it can be used as an argument for legitimacy (European Commission, 2017). The Pillar not only proclaims new social rights, such as a minimum income guaranteeing a decent life, the right to adequate social protection irrespective of the kind of employment relationship, and the right to lifelong learning; it also states that, for them ‘to be legally enforceable, the principles and rights first require dedicated measures or legislation to be adopted at the appropriate level’ (Article 14).

With respect to unemployment insurance, these standards should, in particular, ensure an appropriate coverage and level of income security for involuntary unemployed that would have to be developed in a consultation process (for specific suggestions, see Luigjes et al., 2019; Schmid, 2018: 184–192; Schmid, 2019a). The EESF could furthermore support national systems with repayable loans if they run into deficit, thus enhancing the stabilisation function of national insurance systems. Rules of allocation and possibly automatic triggers would have to be negotiated in order to ensure this stabilisation function. In emergency cases, especially in the event of symmetric shocks – such as in 2008/2009 and during the current coronavirus pandemic – additional and direct funding could come from an emergency fund, to ensure a swift response and prevent a vicious circle of income loss and demand deficiency from developing. The US example shows that, in deep recessions, emergency unemployment benefits plus supplementary unemployment benefits (possibly targeted towards low-income workers) funded directly by the federal government made a real difference in the stabilisation of effective demand (Luigjes et al., 2019; Schmid, 2018: 172). Such emergency benefits could be financed from the reserves held by the EESF or the European Monetary Fund. Apart from their social function, the rationale for such benefits is again their investment function in relation to market externalities. 8

In the long term, an independent fiscal capacity for financing the EESF would be desirable. Whether the resources of this capacity would stem from new EU taxes (e.g. a plastic tax, CO2 tax, digital tax or corporate tax) or from a targeted levy remains a matter of political discretion. Targeted national levies would have the advantage of protecting the EESF from permanent political disputes over financing; they could be constructed in such a way that they build up reserves in good times to be used in bad times. A conservative estimate of the size of the levy would be 0.2 per cent of GDP, which would create a fiscal capacity of about €30bn per year. 9 Part of this budget (0.1 per cent) would be allocated to the reinsurance function according, for example, to rules that have been developed by Dullien et al. (2018); the remainder (0.1 per cent) would be targeted according to the ESF+ rules, yet with a stronger focus on institutional capacity building and on measures along the lines of work-life insurance.

Could such a proposal win Europe-wide support? The long-drawn-out (and, as of August 2020, still ongoing) debate on the mid-term EU budget 2021–2027 demonstrates how difficult it is in the present political climate even to keep the budget at the same level, let alone negotiate an urgent and much-needed small increase. The previously agreed fiscal centralisation of 1 per cent gross national income (GNI) is readily seen as a ‘fetish’ (Andor, 2018). Two indications might help raise hopes for more generous budget resources in the medium or long term. First, it is hard to imagine that the ambitious plans formulated by the new President of the European Commission can be realised without a budget that extends beyond the current MFF proposal: in addition to the Green Deal, her proposals include a European Child Guarantee, a Just Transition Fund and a tripling of the Erasmus+ budget (von der Leyen, 2019). Second, the political stance of the ‘net contributors’, according to which any increase in the budget (apart from the required compensation for the UK’s net contribution of about €7.5bn) would increase their relative burden and therefore be unjust, seems to be questionable in view of the real cost-benefit-relationships of the EU in economic terms. One study has found that, on average, EU citizens’ per capita welfare gains from the Single Market amount to €840 per year; however, these gains are vastly heterogeneous: countries and regions in the geographic core of the EU see gains of up to €3600 per capita, while gains in some peripheral regions can be as small as €150 (Mion and Ponattu, 2019).

Thus, in addition to the impetus provided by the coronavirus pandemic (e.g. SURE), hopes are justified that the 1 per cent benchmark fades into oblivion. An independent fiscal capacity for the EESF, as proposed above, would indeed require a change to the EU Treaties. It would, however, also be necessary to ensure that both functions for the envisaged system of European work-life insurance – reinsurance and social insurance – are adequately covered. Such a system would, moreover, be worthwhile in view of the fact that it would – in connection with corresponding budget sovereignty for the European Parliament – encourage national citizens to identify more closely with Europe. Furthermore, it would intensify the exchange of experiences and good practices between national labour administrations, and the current system of European placement services (EURES) could be extended to create a genuine European Employment Agency.

Even if the transfers of the proposed EESF were to remain quite small in its embryonic phase, the symbolic value of a genuine transnational employment and income security institution should not be underestimated. Europe would become more tangible for its citizens. Studies show that employees of transnational institutions quickly develop supranational identities, which reduce regional or national idiosyncrasies and ego-centred interests. In its initial phase, the EESF should prioritise capacity building and employment promotion. The speedy development of a European matching service (EURES) should be the first step, followed by targeted mobility promotion (financial and linguistic support, help in finding housing) for unemployed workers willing to move to other regions or even to another country for a new job. Targeted employment promotion for young people would be the second priority, e.g. employment support in small and medium sized enterprises (SMEs) through a combination of cheap investment loans (from the EU’s investment and structural funds) and recruitment subsidies. In the current critical situation, and given that short-time working measures can, for many workers, serve only as a bridge to new jobs, a bold wage cost subsidy programme could be open to enterprises who hire workers from the pool of unemployed in regions with special employment problems. It was Nicolas Kaldor (1936) who earlier hinted at this option: if employment cannot be boosted by devaluing currencies, wage cost subsidies for each additional or reasonably maintained job would be a functional equivalent. Subsequently, short-time work to maintain skilled labour should not be ruled out, especially when combined with upskilling and reskilling (Cahuc, 2018; Schmid, 2015).

Such transfers would not only ensure cyclical stabilisation, by maintaining effective demand in the regions badly affected by the crisis, but would also promote social inclusion, by preventing long-term unemployment and relieving the pressure on skilled workers to emigrate. Certainly, more regional mobility is necessary for a well-functioning European labour market, and such mobility is also welcome among some segments of the European population, especially young people. This potential flexibility, however, is limited for a number of reasons, and is not desirable in any shape or form, particularly not for adult and elderly skilled workers. In the long term, a European system of work-life insurance should not content itself – apart from wage flexibility – with the balancing mechanism of labour mobility often enforced by frictional unemployment, as the neoliberal logic implies. The logic of work-life insurance also implies keeping the labour force – if not in the same companies – at least in the local or regional area, through supported further training and working time flexibility, i.e., bringing work to the workers instead of bringing the workers to the work. Such a strategy would also encourage a multi-national and inclusive striving to feel at home in Europe, instead of the currently prevailing nationalist and exclusionary call for ‘Heimat’.

Summary and conclusions

What can pull Europe back from the brink? At present, a European Social Union (ESU) is not on the official EU agenda. Yet the need to take the issue of solidarity – between the Member States and all European citizens – more seriously is clearly reflected in the growing body of literature on EUI. All historical reviews of proposals for transnational unemployment insurance schemes, however, have dampened any hopes in this regard. Moreover, the observation made by Maurizio Ferrera should be taken into account: the formation of such pan-European solidarity in the EU will be very different to – and probably even more difficult than – transnational welfare state development in existing federal states such as the United States, Canada or Australia. The reason is quite simple: the creation of an ESU must take place in the context of ‘extensive nation-based welfare states’, which are endowed with considerable variations and their own distinct institutional backgrounds. For this reason, proposals for a genuine EUI are currently ‘off the table’ and, in line with the principle of subsidiarity, are not considered a priority.

This article proceeded to argue for a relaunch of the established European Social Fund (ESF), moving towards a European Employment and Social Fund (EESF) which combines elements of social insurance with elements of reinsurance. These two pillars would gradually develop and ultimately be financed by a specific budget, and – possibly – implemented by a separate pan-European agency. Moreover, this article argued that even the more modest proposals for reinsurance of national UI schemes should be approached with caution. This is chiefly because they overemphasise the macroeconomic stabilisation function and fail to meet the three core objectives of modern (un)employment insurance: first, to provide reliable and generous income security for all workers (including those in non-standard jobs) and for a sufficient period to allow them to find a suitable new job; second, to support this function through an effective employment service including the provision of job-creation assistance aimed at preventing long-term unemployment; and third, in the spirit of transitional labour market theory, to cover the growing variety of social risks related to critical transitions over the life course.

Could such a pragmatic yet, at its core, radical proposal win the support of European citizens? Maurizio Ferrera argues that the Euroscepticism common among the political and intellectual elite might be misguided: there is potentially a ‘silent majority’ in support of a larger EU budget aimed at promoting economic and social investment, helping people in severe poverty and providing financial help to Member States experiencing rising unemployment (Ferrera, 2018: 28–29). This speculation has recently been corroborated through rigorous empirical analysis based on a public opinion survey conducted in 13 EU Member States. Findings included not only indicators for a shared European identity distinct from national identity, but also an unexpectedly high willingness to support European policies that would imply redistribution across national boundaries. For instance, more than half of all Europeans would be willing to provide financial assistance to countries in need from their own pocket in the form of an additional tax (Gerhards et al., 2020: 6). A further study demonstrates that it is also important to address issues in the right way: EU citizens are ready to share the risk of unemployment, and they prefer packages that are generous, yet require countries to offer education and training to all their unemployed citizens. In most countries, support is stronger if the implementation of risk-sharing is decentralised and co-determined by the social partners (Vandenbroucke et al., 2018).

These findings corroborate the argument put forward in this article that one should not try to build a genuine European unemployment benefit scheme, but rather a reinsurance scheme that supports national benefit systems with lump-sum transfers during recessions, combined with an enhancement of national insurance schemes that include elements of risk-sharing over the life course. In all countries, support – even for redistribution – increases if risk-sharing is combined with both conditionality and opportunities, in other words with social investment policies such as training, education, job-creation assistance, support for workplace adjustment and working time variations. Apart from effectively controlling ‘moral hazard’, such investments enhance individual autonomy, i.e., they provide ‘moral assurance’ in case of risk taking. Finally, but just as importantly, when expressing their preferences, European citizens seem to pay less attention than policy-makers to the issue of how tolerant the scheme should be with regard to cross-country redistribution. In other words, and to sum up, practical and effective policies to mitigate and tackle all major income risks over the course of individuals’ work-life and to reward individuals willing to take social risks such as parental leave, job-to-job transitions and retraining are decisive as an argument in favour of moving towards a European Social Union.

Footnotes

Acknowledgements

The author would like to thank the three anonymous referees for their insightful comments; further thanks go to Georg Fischer, Bernard Gazier, Martin Kronauer, Janine Leschke, Frank Vandenbroucke and Bart Vanherke for their encouragement during the various stages of writing this article; the author is also grateful for the guidance that was provided by the editors.

Funding

This research received no specific grant from any funding agency in the public, commercial, or not-for-profit sectors.