Abstract

In India, the coronavirus (COVID-19) pandemic-induced country-wide regulatory lockdown and consequential supply-chain disruptions and market instability have all posed serious challenges before the regulators and policymakers. Amid the pandemic, the stock market showed return volatilities primarily due to the unexpected investors’ behaviour. One of the behavioural biases is herding, which has the power to wreck the market equilibrium and shatter the market efficiency. Given that the pandemic has generated unprecedented spirals of uncertainties across the globe, thereby creating interruptions in the pattern of stock market investment decisions, this study examined the herding behaviour of 54 stocks of banking and financial services sectors listed in the national stock exchange. In the quantile regression framework, the study provides evidence of the presence of herding for public sector banking and financial services under the bull market conditions during the pandemic in the 90th quantile of the return distribution. This finding has implications for the mispricing of financial assets in these sectors. So, the study suggests removing information asymmetry among the market participants and devising policy initiatives for ensuring market stability.

Introduction

Since the exceptional outbreak of the novel SARS-CoV-2 virus in late December 2019 in the Wuhan city of China that causes COVID-19 infection, it has spread to more than 213 countries and territories around the world, resulting in socio-economic and human health devastations (Chang et al., 2020). As of 20 May 2021, about 164 million people have been infected and 3.41 million have succumbed to this ongoing pandemic across the world. The pandemic has been observed to trigger a massive spike in uncertainty, quickly transmitting itself from healthcare to the macroeconomy (Bouri et al., 2020) and has been a real threat to the global economy and financial markets (Barro et al., 2020; Ramelli & Wagner, 2020). On 31 January 2020, owing to the World Health Organization (WHO’s) declaration of COVID-19 spread as Global Public Health Emergency, the Dow dropped more than 2% during the day on COVID-19 fears, thereby wiping out all the gains of January (Mnif & Jarboui, 2021). Further, on 11 March 2020, owing to WHO’s labelling of COVID-19 spread as a Global Pandemic, Asia Dow immediately lost 4% by mid of the day (Mishra & Mishra, 2021) and Mumbai Sensex went down by 6.8% (Shu, 2020).

Arin et al. (2008) predicted that financial investors are induced to exit the unstable market in search of more stable financial investment avenues when unexpected disastrous events take economies into the grips of uncertainties and pessimism. And, markets loom under fear, leading to plunges. However, such an adverse market reaction has been observed to be short-lived, and eventually, markets return to the rising track when market participants get accustomed to the macroeconomic fundamentals and regain confidence (Gormsen & Koijen, 2020). This hypothesis was proved in the case of the Indian capital market during the COVID-19 pandemic. In India, the two crucial bourses Bombay Stock Exchange (BSE) Sensex and CNX NIFTY 50 depicted nosedives from 41,952 and 12,362 points on 14 January 2020, to 25,981 and 7,610 points on 30 March 2020, along with the subsequent recovery through 31,327 and 9,154 points on 24 April 2020 (Ravi, 2020). The primary reason for such a quick recovery is that each market fall provides investors with an opportunity to enter the market and earn a higher return (Ravi, 2020).

Nonetheless, this market entry of investors for higher returns often posit a behavioural bias and/or market anomaly, called herding behaviour, when market entry decision is taken based on collective actions of other market participants, while ignoring personal rational decisions (Banerjee, 1992; Christie & Huang, 1995; Hirshleifer & Hong Teoh, 2003). Riaz et al. (2020) made it clear that well-informed and rational investors have no intentions to follow the masses and, thus, do not contribute to herding effect. The less informed and less confident investors rely more on the decisions of better-informed and more confident investors to minimize risks and optimize returns (Easley & Kleinberg, 2012; Goodfellow et al., 2009). In doing so, these investors contribute to the herding effect. Espinosa-Mendez and Arias (2021) pointed out that the less informed investors being driven by fear and uncertainty tend to follow the path of more informed investors during extreme market conditions like the ongoing COVID-19 pandemic.

The ongoing biological disaster of COVID-19 pandemic, by damaging human health and creating socio-economic disruptions, has been observed to lead to spillovers and market reactions (Mnif & Jarboui, 2021) through a highly interdependent world with interconnected production networks and financial markets (Sahoo & Ashwani, 2020). During the first wave of the pandemic, the prolonged regulatory lockdowns, worldwide economic downturn and disruptions in demand and supply have severely affected both real and financial sectors (Chakraborthy & Thomas, 2020; Guru & Das, 2021; Kizys et al., 2021). The COVID-19 pandemic has caused fear to investors in financial markets of a global credit crunch (Chang et al., 2020) and profit loss (Wu et al., 2020), which undermined their ability to determine optimal portfolios (Shehzad et al., 2021). In such a pessimistic environment, COVID-19-induced herding effect may exist when investors faced with the decline of the economy along with rising medical and social uncertainties, abandon their beliefs/information and consider what others are doing to maintain and/or invest in capital markets without analysing the rationality of objectives (Espinosa-Mendez & Arias, 2021). This herding effect can deviate the prices of securities from the equilibrium, thereby making the market inefficient (Chauhan et al., 2020; Yousaf et al., 2018) and causing abnormal losses and/or returns in the market (Bui et al., 2018).

Recent empirical studies reveal that the first wave of the COVID-19 pandemic has induced a decrease in asset prices and an increase in market volatility in affected countries (Ali et al., 2020; Apergis & Apergis, 2020; Gil-Alana & Monge, 2020; Narayan, 2020; Salisu & Sikiru, 2020). Studies established that excess market volatility induces herding behaviour (Bekiros et al., 2017; Kabir & Shakur, 2018; Youssef & Mokni, 2018). In recent studies, stock markets of Asia, including that of India, have been observed to depict high levels of return volatilities, owing to the pessimistic and panic sentiments of investors, increase in the number of COVID-19 confirmed and death cases, changes in volatility index, changes in oil prices, inflation rates, interest rates and exchange rates (Mishra & Mishra, 2020, 2021). In another study, Dhall and Singh (2020) found evidence of an industry-level herding effect in the Indian capital market during periods of extreme market conditions amid the pandemic. In an earlier study, Kabir and Shakur (2018) stated that investors in India follow herding behaviour during both high and low levels of market volatility.

Dey and Siddiqui (2020) stated that the ongoing pandemic has posed a sizable impact on different sectors in India albeit the magnitude of the impact varies from sector to sector. Agarwal (2020) mentioned that the financial services sectors are no exception to the impacts of COVID-19 because of its association with the broader economy and its activities, and link to all other sectors. Demirguc-Kunt et al. (2020) employed daily stock prices data in 53 countries, including India, to assess the impact of the pandemic on the banking sector, and they found a systematic underperformance of banking sector stocks relative to that of the corporate sector at the onset of the pandemic between March and April 2020. By late March 2020, the stock prices of banks dipped to less than 60% of their initial levels of the year, and thus, the abnormal returns on bank stocks became −6.6 and −3.2 percentage points during March and April 2020, respectively. Further, it was observed that the public sector banks suffered greater reductions in their stock returns relative to that of private sector banks.

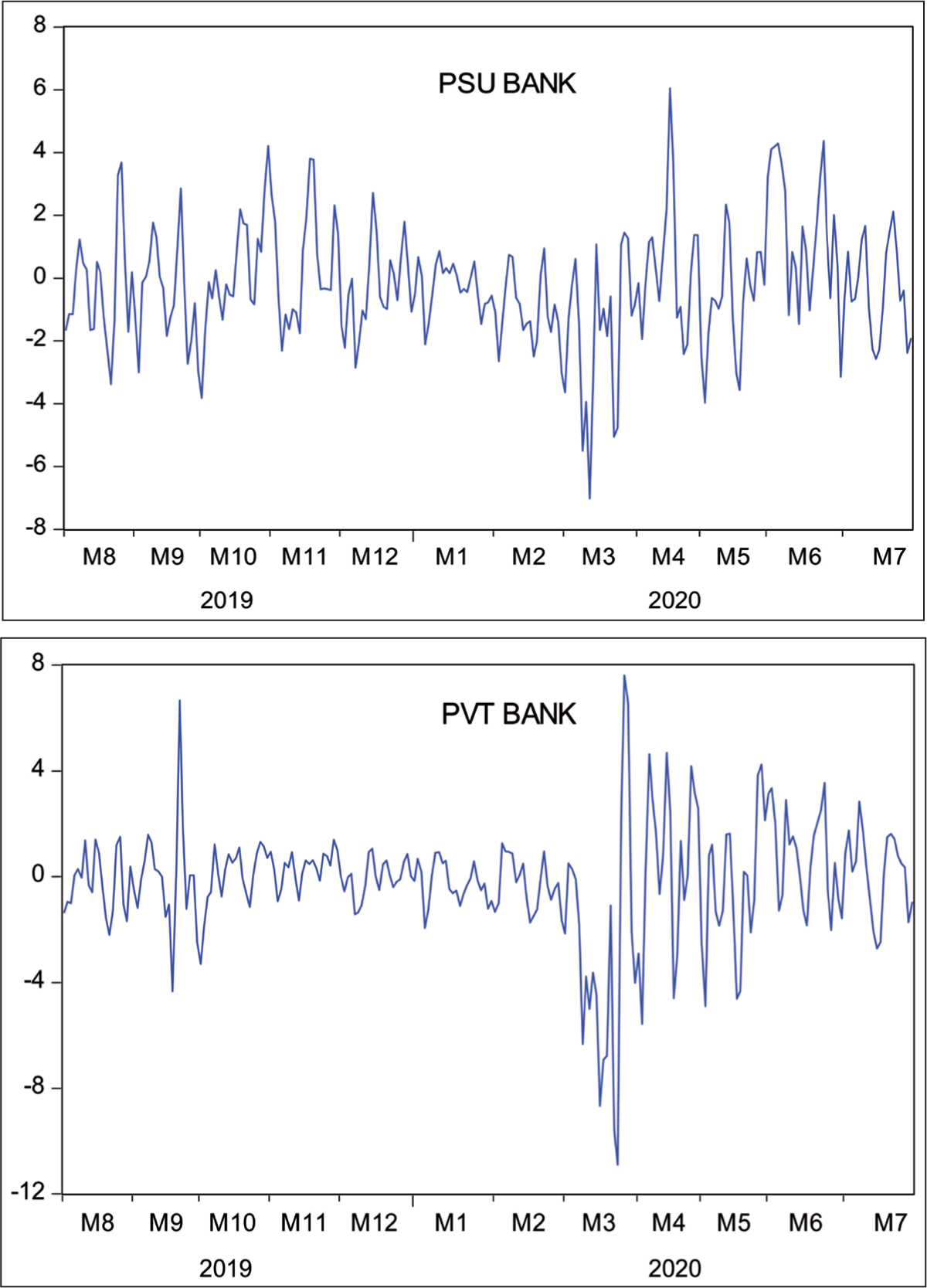

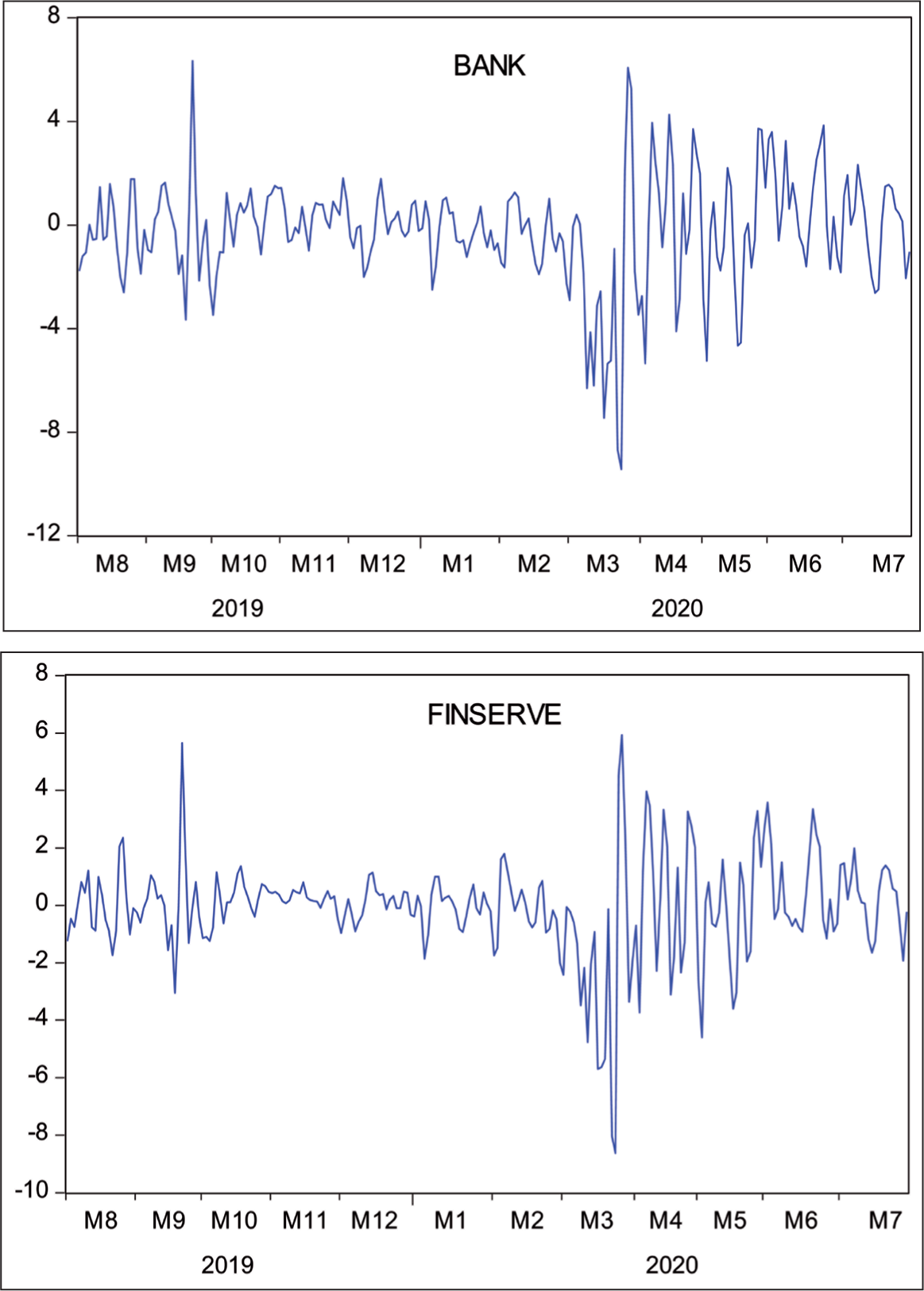

Such observations indicate the presence of a high degree of return volatility in the banking and financial services sectors. In the context of India, Figure 1 presents the occurrence of return volatilities in the stocks of banking and financial services amid the pandemic. Thus, in line with these observations based on the extant literature and time-series plot of average market returns, we hypothesize that the banking and financial services sectors portray the presence of herding effects in investors’ behaviour during the COVID-19 pandemic in India. Specifically, the study focuses on the analysis of herding behaviour in banking and financial services sectors, assuming that these sectors are primarily online-based and were allowed to function during countrywide lockdowns. Additionally, this sectoral-level study is justified on the ground that the fundamental as well as the technical analyses of investment decisions are made by the asset managers, market analysts and researchers based on the information that is diffused mostly at the industry/sectoral level. Also, the sector-specific stock index is calculated based on different stocks of banking and financial companies, and the investors more often make decisions in favour of individual stocks or sectors. Thus, studying the herding behaviour at the sectoral level can better reflect the investors’ psychology.

Therefore, this study tries to explore whether Indian investors revealed a herding behaviour, suppressing their own beliefs, logics, information and judgements, about the market conditions in the periods of pandemic-induced market distress in India. First, it examines the likelihood of the presence of return volatility in the banking and financial services sectors. Second, it examines the possibility of the presence of herding behaviour in the pre- and post-COVID-19 outbreak phases. Third, it examines the herding during different market conditions—Bullish and Bearish markets—in the post-COVID-19 phase in India. The study documents (a) the presence of pandemic-induced return volatility clustering in the banking and financial services sectors in the Indian capital market; (b) no evidence of herding effect in the pre- and post-COVID-19 outbreak phases in the banking and financial sectors; and (c) the evidence of herding effect under bull market conditions for the public sector banking and financial services sectors when the market returns reach the 90% level in the right tail of the return distribution. Thus, the findings of the study consider investors’ herding behaviour as a significant risk factor in the public sector banking and financial services for price discovery and consequential market inefficiency. The novelty of this study is that it discusses the possible presence of herding behaviour in India over the entire return distribution during the COVID-19 pandemic and, thus, contributes to the literature the evidence of its presence in extreme market conditions during the crisis period. This study is perhaps the first one to discuss investors’ herding behaviour amid the pandemic, using the quantile regression approach, which is considered robust to ordinary least squares (OLS) when the data set is not normal. The remaining part of the article is structured as follows: Section II reviews the extant literature to line up the entire study; Section III makes a note of the data and methodology used in the study; Section IV makes the analyses and discusses the findings; and Section V concludes the article.

Literature Review

In analysing the mechanism of the operation of the financial markets in price discovery and return optimization, investors’ behaviour plays a crucial role. The traditional economic theory as put forward by Bachelier in 1900 assumes rationality in investors’ behaviour (Dimson & Mussavian, 1998), while irrationality has been assumed in modern behavioural economics as advocated by Keynes (1930, 1936, 1937). The former, called Efficient Market Hypothesis (Fama, 1995; Malkiel & Fama, 1970), argues that the investors’ behaviour is always rational, and stock prices rapidly adjust to the new information to enable the investors to make the best investment decisions based on all available information. The latter, called animal spirit by Keynes (1930, 1936, 1937), argues that investment is often based on how people feel about the overall economy rather than on unbiased, rational analysis of facts. Since financial markets are mostly guided by the animal spirit, some investors fail to process the new information logically, based on their beliefs, critical thinking and judgements, when faced with high levels of volatility, which prompt them to follow the behaviour of other market participants. Latter this has been called ‘herding behaviour’ in the financial investment literature (Banerjee, 1992), the term being coined following Trotter (1916).

This herding behaviour entails that the investors tend to follow the behaviour of other groups of investors, mostly large investors while making investment decisions in financial markets (Hwang & Salmon, 2004; Parker & Prechter, 2005; Yousaf et al., 2018). Investors indulge in herding when they lack sufficient information to make appropriate asset choices for trading (Lee et al., 2021; Spyrou, 2013), they intend to invest a larger amount of capital by minimizing risks (Riaz et al., 2020), financial markets depict large stock price fluctuations or excess volatility, falling prices, calendar effects, asymmetric effects in stock returns, the imbalance between prices and fundamental variables (Bekiros et al., 2017; Golarzi & Ziyachi, 2013; Kabir & Shakur, 2018; Mobarek et al., 2014; Tan et al., 2008; Youssef & Mokni, 2018), they sell and buy the same assets simultaneously (Lakonishok et al., 1992) and/or when they lack confidence due to severe market stress, crises and uncertainties (Bouri et al., 2020; Chiang & Zheng, 2010; Christie & Haung, 1995; Devenow & Welch, 1996; Forbes & Rigobon, 2002; Rahman & Ermawati, 2020). In all these, the objective is the protection of investments against market risks and uncertainties, and to optimize returns on investments.

In the presence of the herding effect, the returns on individual investments tend to move in the same direction as the market portfolio, thereby making risk diversification difficult (Chang et al., 2000; Hwang & Salmon, 2004). The existing literature predicted several outcomes of the herding effect, including errors in stock pricing or pricing inefficiencies, increased stock price fluctuations, increased return volatilities, disrupted risk-return trade-off, creation of additional market risks, speculative bubbles and crashes leading to market destabilization (Bekiros et al., 2017; Bikhchandani & Sharma, 2000; Blasco et al., 2012; Chang et al., 2020; Javaira & Hassan, 2015; Kabir & Shakur, 2018; Sihombing et al., 2021).

The extant literature provides empirical evidence that the herding behaviour is more prevalent during severe market conditions in emerging markets (Chang et al., 2000; Economou et al., 2011; Lao & Singh, 2011; Tan et al., 2008). Chiang and Zheng (2010) found an increase in the intensity of herding during the financial crisis, whereas Galariotis et al. (2015) found its existence in the financial market when governments announce macroeconomic policies. Chang et al. (2000) supported the presence of herding behaviour in Asian countries because investors’ decisions mostly rely on the macroeconomic information due to their palpable economic conditions and non-availability of firm-level information in these countries. Lao and Singh (2011) observed the existence of herding in the Indian stock market during rising market conditions, whereas Fu and Lin (2010) found the existence of herding in the Chinese stock market during the down-market conditions. Tan et al. (2008) provide evidence of the presence of herding in the Chinese stock markets during both bull and bear market conditions. Bhaduri and Mahapatra (2013) provides evidence of herding behaviour in the Indian stock market during extreme market conditions.

The ongoing COVID-19 pandemic has caused devastations in all the economies across the globe and severely affected both real and financial sectors. Specifically, the pandemic has made economies unstable by disturbing their healthcare system, supply chain, trade and investment activities (Mishra & Mishra, 2020, 2021). All these generated the spirals of panics and uncertainties among market participants, making the investment decisions formidable. In this context, several studies have been conducted to examine the possibility of the herding effect in financial markets in different parts of the globe. The findings of Chang et al. (2020), Abdeldayem and Al Dulaimi (2020), Abd-Alla (2020), Espinosa-Méndez and Arias (2020, 2021), Bouri et al. (2020), Wu et al. (2020), Riaz et al. (2020), Rahman and Ermawati (2020), Mnif et al. (2020), Lee et al. (2021) and Kizys et al. (2021) support the presence of herding effect during the COVID-19 public health crisis. Particularly, the findings of Bouri et al. (2020) reveal the presence of a strong herding effect in emerging stock markets, and thus, it depends on the development status of an economy. The findings of Espinosa-Méndez and Arias (2020) establish that the herding effect is significant during extreme market conditions.

The capital market of India witnessed nosedives, followed by a V-shape recovery, while depicting return volatility (Mishra & Mishra, 2020, 2021; Mishra et al., 2020) in the initial phases of the pandemic. The existing literature argues that such a crisis-led volatile market can weaken investors’ confidence and spread market pessimism. Thus, investors prefer to move along with the market consensus, leaving apart their own beliefs about market conditions. In this pretext, Selvan and Ramraj (2020) provide evidence of herding behaviour in the Indian capital market amid the pandemic. In another study, Dhall and Singh (2020) found the evidence of herding effect amid the COVID-19 pandemic in extreme market conditions at the industry level. The extant literature further argues that in the presence of such behavioural bias, markets can depict heightened return volatilities, leading to unstable market conditions, thereby causing market inefficiency (Javaira & Hassan, 2015). The analysts observed that the ongoing pandemic has posed a sizable impact on different sectors in India albeit the magnitude of the impact varies from sector to sector (Dey & Siddiqui, 2020). In the same line of argument, Demirguc-Kunt et al. (2020) found a systematic underperformance of banking sector stocks relative to that of the corporate sector at the onset of the pandemic between March and April 2020 in a sample of 53 countries. It was further observed that the public sector banks suffered greater reductions in their stock returns relative to that of private sector banks. Agarwal (2020) mentioned that the financial services sectors are no exception to the impacts of COVID-19 because of its association with the broader economy and its activities, and link to all other sectors in India. It is interesting to note that the announcements of regulatory initiatives to reduce the rate of transmission of COVID-19 infection and to give a boost to economies (Ashraf, 2020; Baker et al., 2020; Sharma et al., 2021) have impacts on investors’ behaviour. Demirguc-Kunt et al. (2020) observed that the policy initiatives such as borrower assistance announcements, liquidity support initiatives, countercyclical prudential measures and monetary policy initiatives have all contributed to the large abnormal stock returns, especially in small banks and public sector banks.

Given the aforementioned theoretical and empirical observations, and the footprints of the unexpected outbreak of novel coronavirus, the following points justify why a study on herding behaviour is required amid COVID-19 spread outs: (a) the sudden outbreak of the pandemic had made the investors panicky in the initial phase and, thus, caused a sudden downfall in the performance of stock indices in India; (b) the pandemic has created a wide range of crises such as health, economic and financial crises in the country; (c) as the pandemic containment measure, governments at the centre and state levels announced and implemented several socio-economic and financial measures apart from the health-specific measures, which may have impacts on investment decision-making; and (d) amid the pandemic, Indian stock market has witnessed both the bull and bear market conditions. Further, a study on herding behaviour is significant from a policy point of view because its existence has adverse effects on stock market movements (Haritha & Uchil, 2019; Jaiyeoba et al., 2018), the volatility of asset returns (Demirer & Kutan, 2006) and on market efficiency (Yousaf et al., 2018). Therefore, this piece of work is an effort to examine the herding effect amid the ongoing COVID-19 pandemic.

Data and Methodology

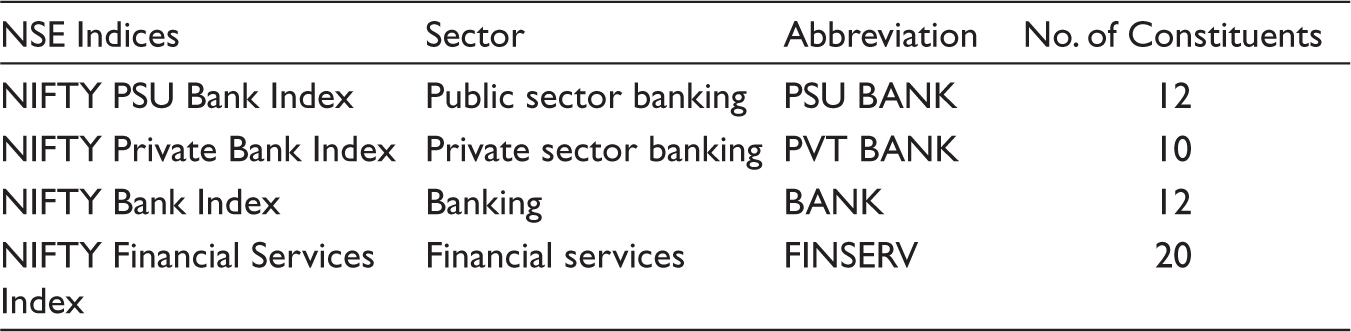

This study examines the investors’ herding behaviour in banking and financial sectors in the Indian stock market amid the devastating economic and financial consequences of the rapid spread o COVID-19. This issue has been addressed in two parts—first, we have examined whether the uncertainties and pessimism associated with the COVID-19 pandemic resulted in the increased return volatility in the banking and financial sectors, and second, we have investigated whether these sectors depict the herding behaviour of investors amid the pandemic, including the era of extreme market conditions. For this purpose, we have considered the National Stock Exchange of India. The study uses the daily closing prices of stocks of the constituent banks and financial service companies of the banking and financial sector indices of National Stock Exchange—NSE (for details, please refer to Table 1) because the level of herding is more evident when daily data are used (Tan et al., 2008), as this market behaviour is short-lived in nature. We have taken public sector banking, private sector banking, banking as a whole and financial services sectors for our analysis because NSE publishes separate indices on these four sectors.

Banking and Financial Services Sector Indices

Banking and Financial Services Sector Indices

The daily data on the closing prices of 54 stocks of the constituent banks and financial service companies were compiled from the NSE website of historical prices. Besides, daily data on the volume of 54 stocks traded and NSE volatility index (VIX) were also compiled from the NSE website. The period of these data spans from 1 August 2019 to 28 July 2020. On 30 January 2020, the WHO declared the COVID-19 1 as a Public Health Emergency of International Concern to alert about the unexpected consequences of the spread of COVID-19 across the Globe. Therefore, we have subdivided the full sample period into two sub-samples, the first being from 1 August 2019 to 29 January 2020 and the second from 30 January 2020 to 28 July 2020.

First, we have computed the daily return of a stock using the formula:

Stock Market Volatility

First, the generalized autoregressive conditional heteroskedasticity (GARCH) (1,1) model has been used for describing the sector-specific stock market behaviour, assuming that the asset returns might have been more volatile due to the unprecedented outbreak of the COVID-19 pandemic.

GARCH (1,1) Model Specification

We have estimated the GARCH (1,1) model, comprising the following conditional mean and variance equations:

Conditional mean equation:

Conditional variance equation:

In the conditional mean Equation (1), Rm,t is the average of stock returns in the sector i at time t. Second, CVD

t

is the percentage change in the COVID-19 confirmed reported cases in India at time t. Third, VOL

i,t

is the average traded volume of stocks in the sector i at time t. Fourth, VIX

t

is the return based on NSE volatility index, popularly called fear index, which is a measure of investors’ pessimistic sentiments, fear and uncertain behaviour and market risks. Finally, εt is the residual. In the conditional variance equation,

Herding Effect During the Coronavirus Pandemic

The quantile regression approach has been used to examine the herding behaviour in the banking and financial sectors, assuming that investors are more likely to follow the crowd by suppressing their information in periods of market distress like during COVID-19 spread outs.

Quantile Regression Model Specification

We have formulated the following baseline quantile regression model:

Here, ψ2 is the coefficient of the market return (Rm,t) of the sector i in the τth quantile, and ψ3 is the coefficient of the square of the market return (

In our quantile regression model, CASD is the cross-sectional absolute deviation as proposed by Chang et al. (2000) to measure securities dispersion from market returns. CASD is a measure of the dispersion of the stock returns around the market returns and indicates less than proportional decrease or increase in equity dispersions with the market return (Chang et al. 2000; Thirikwa & Olweny, 2015). The CASD is given by

Since the existence of herding behaviour can cause an increase in the correlation of stock returns, the relationship between individual stock return and the market return is a non-linear one (Henker et al., 2006; Mertzanis & Allam, 2018), and thus, we have formulated non-linear quantile regression model for our analysis. Under a rational asset pricing model, ψ2 is expected to be significantly positive, indicating the effect of stock exposures, relating to the equity dispersion. However, a significantly negative value of ψ3 indicates the presence of herding behaviour in the stock market (Economou et al., 2011, 2016).

Herding Behaviour During Extreme Market Conditions

We have also estimated the quantile regressions to examine the asymmetric stock behaviour in the extreme market phases like bull and bear market conditions amid the rapid spread of COVID-19, assuming that market conditions were unstable after the outbreak of COVID-19.

Quantile Regression Models for Unstable Market Conditions

When market conditions are unstable, for instance, due to the outbreak of COVID-19, stock behaviour may be asymmetric, thereby fuelling herding in the market (Camara, 2017; Fu & Lin, 2010; Tan et al., 2008). Market conditions are unstable when the rate of increase in the dispersion of aggregate market returns is higher in bull market conditions as compared to that in bear market conditions. Thus, asymmetry in the stock market herding behaviour has been examined separately for the bullish (Rm,t > 0) and the bearish (Rm,t < 0) market conditions using the following quantile regression models:

In the quantile regression models (4) and (5), significantly negative values of ξ3 and ξ3 indicate the presence of herding behaviour. The asymmetry in the herding behaviour is indicated from ξ3 ≠ ξ3.

At the outset, the descriptive statistics of CSAD and average market return of each sector for the full period and sub-periods are calculated and summarized in Tables 2 and 3. Since the mean values of CSAD in three different cases are all greater than one in Table 2, the non-existence of herding behaviour in the Indian stock market is indicated. Since the values of the standard deviation of the average market return in all the sectors show an increasing trend through the pre- and post-COVID-19 outbreak periods in Table 3, the increase in stock return volatility due to the pandemic is also indicated.

Descriptive Statistics of Cross-sectional Absolute Deviation (CSAD)

Descriptive Statistics of Cross-sectional Absolute Deviation (CSAD)

Descriptive Statistics of Average Market Return (Rm,t)

However, for conformity of these observations, we have employed sophisticated time-series econometric methods. Since the use of time-series econometric methods requires the testing of stationarity of each variable, we have employed the Phillip–Perron unit root test in which the null hypothesis is ‘non-stationary of the variable’ with intercept and trend. The results are presented in Table 4. It is observed that the null hypotheses for all the variables of interest are significantly rejected, thereby indicating the stationarity of these variables at their levels. Therefore, the estimation of GARCH (1,1) and quantile regression models are well justified. Additionally, it is inferred from Tables 2 and 3 that the variables CSAD and average market return (Rm,t) are not normal as indicated by the values of kurtosis. This finding also justifies the use of a semi-parametric quantile regression model.

Results of Unit Root Tests

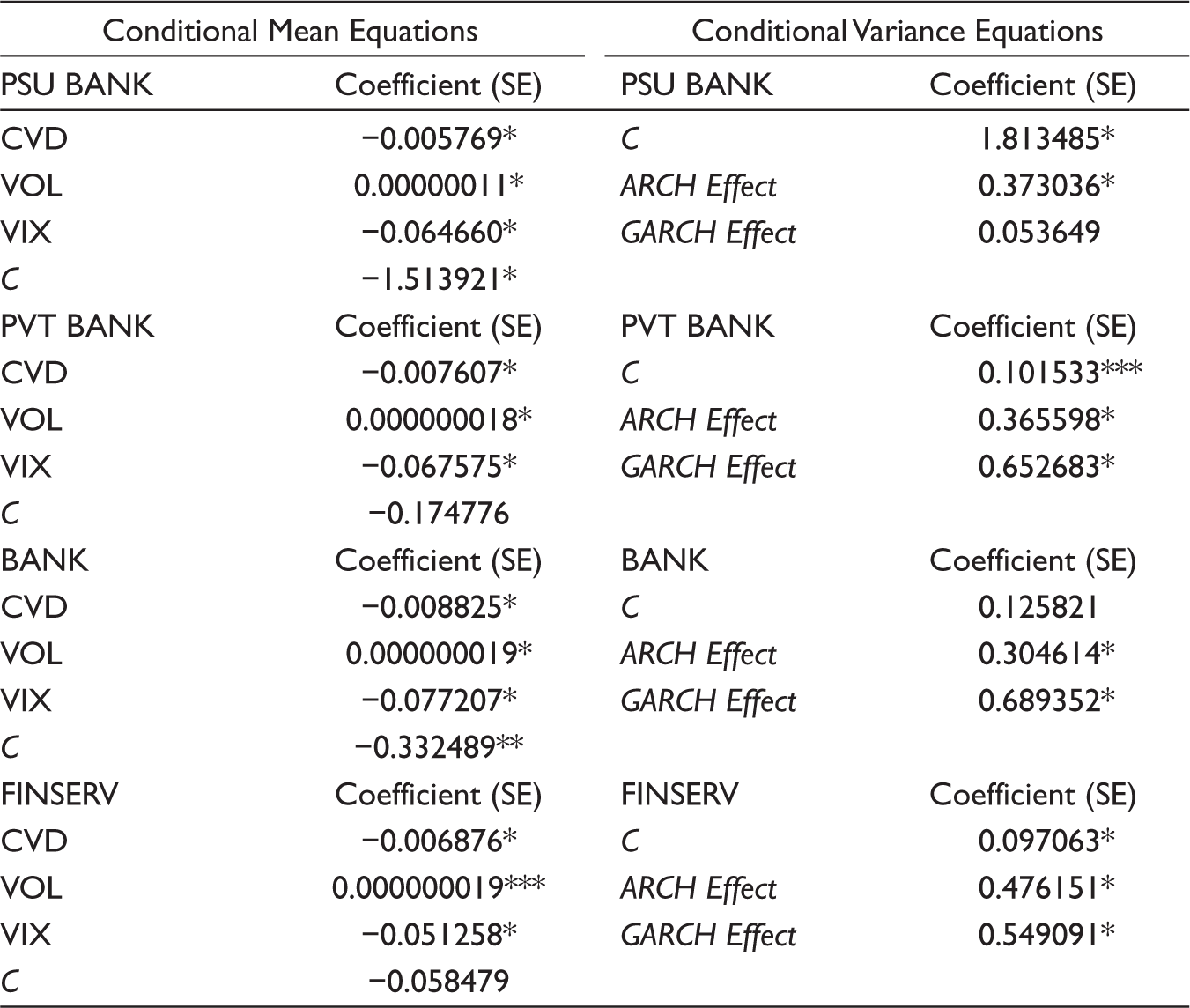

Now, to examine whether the uncertainties and pessimism associated with the COVID-19 pandemic resulted in the increased return volatility in the banking and financial sectors, we have estimated the GARCH (1,1) model specifications (1) and (2), the results of which are summarized in Table 5. It is observed that the coefficient of the CVD term is negative as well as statistically significant in the conditional mean equation (left side of Table 5) for all the sectors under consideration. It lends to support the negative effect of the outbreak of COVID-19 pandemic on the stock market indices of banking and financial service sectors in India. Furthermore, the coefficient of the fear index, VIX, is negative and significant in all these sectors. This indicates that the investors’ pessimistic sentiment towards the COVID-19 pandemic is a significant factor in influencing the movements in the stock market indices of banking and financial service sectors. Besides, the GARCH effect is positive and statistically significant in the conditional variance equation (right side of Table 5) for all the sectors, except for PSU banks, which confirms the presence of volatility clustering in the stock return series of these sectors due to the unexpected global spread of COVID-19. Specifically, a bulk of pessimistic information flows from the previous day’s forecast to make the stock market volatile, around 65% in private sector banking, 68% in banking and 54% in financial service sectors. All these results satisfy the stability condition of the GARCH (1,1) model, that is, the sum of the ARCH effect and GARCH effect is ≤1. However, these many volumes of information flow from the past period forecasts need not be necessarily due to the uncertainties created in the post-event period. And, to this extent, the above-mentioned results can be misinterpreted albeit Figure 1 confirming maximum volatility in the post-event period.

Results of GARCH (1,1) Model Estimation

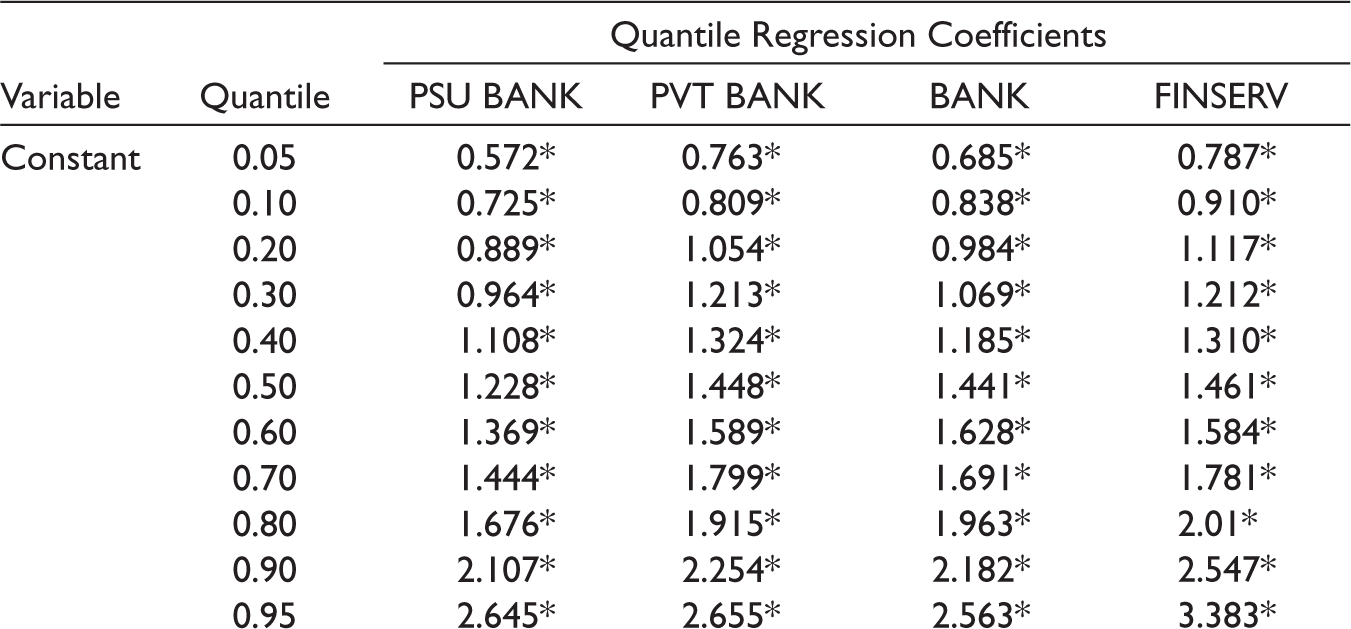

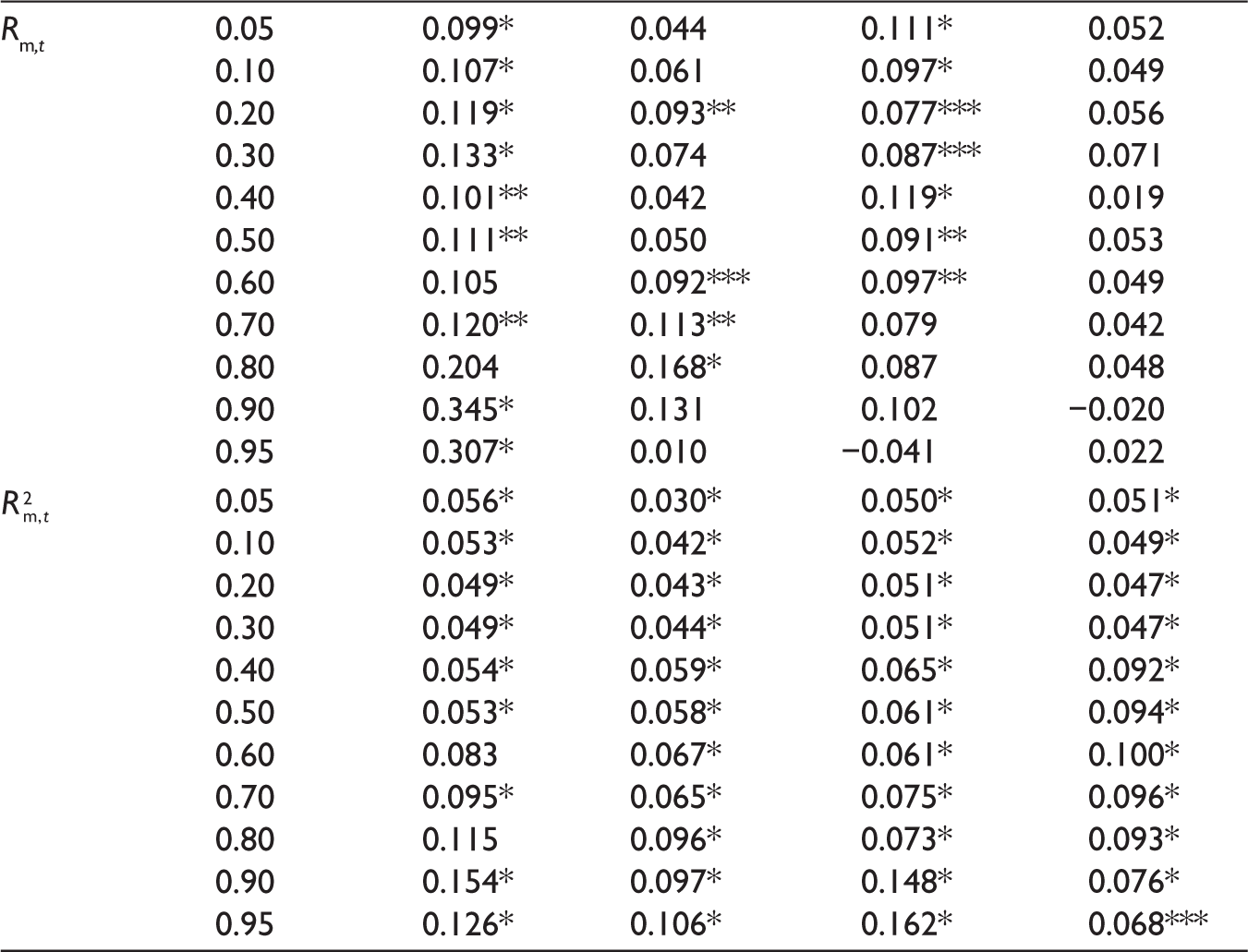

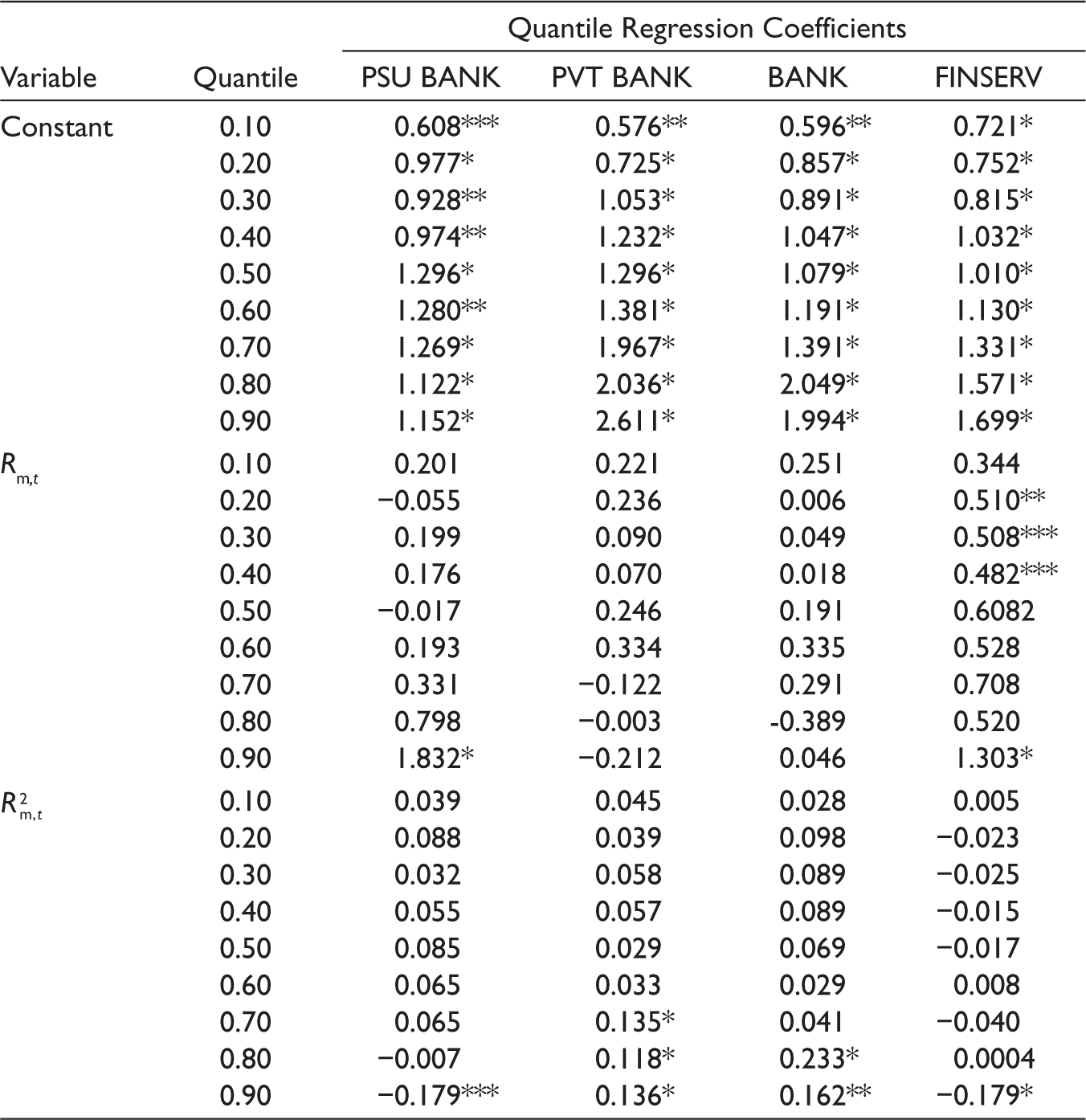

After the presence of volatility clustering is identified, we have examined whether these sectors depict the herding behaviour of investors amid the pandemic. For this purpose, we have estimated the quantile regression for the whole sample period, pre- and post-COVID-19 periods using specification (3), and the results are presented in Tables 6–8. In this quantile regression framework, it is evidenced that neither banking nor financial services sector exhibits herding behaviour as none of the coefficients of

Results of Quantile Regression: Full Period Sample

Results of Quantile Regression: Pre-COVID-19 Period

Results of Quantile Regression: Post-COVID-19 Period

Since the herding effect has been observed to last for a short duration, and investors are prone to be indulged in herding behaviour during bull market conditions (Tan et al., 2008), it will be justified to test it for the era of economic recession triggered by the COVID-19 pandemic in its initial phase in 2020. Chiang and Zheng (2010), Ouarda et al. (2013), Angela-Maria et al. (2015), Litimi (2017), Youssef and Mokni (2018), and Bouri et al. (2020) added that herding behaviour is more apparent during crisis periods. Bekiros et al. (2017) and Mnif and Jarboui (2021) opined that studying the presence of the herding effect during the period of crisis can help detect market bubbles and market crashes.

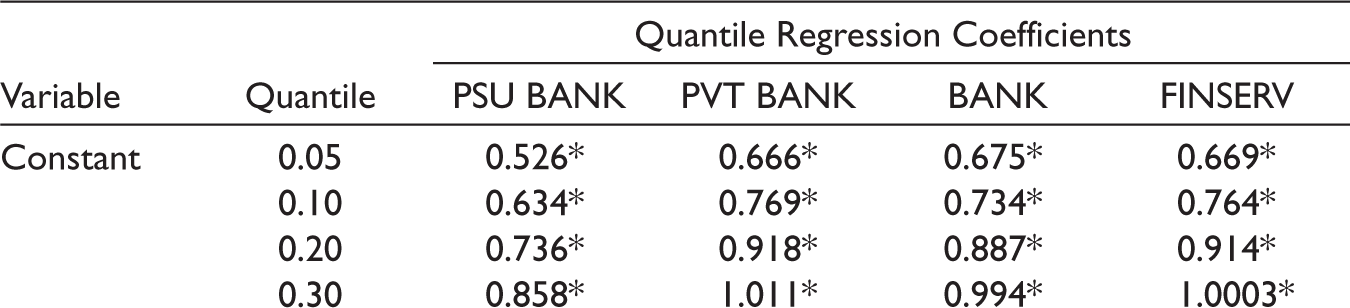

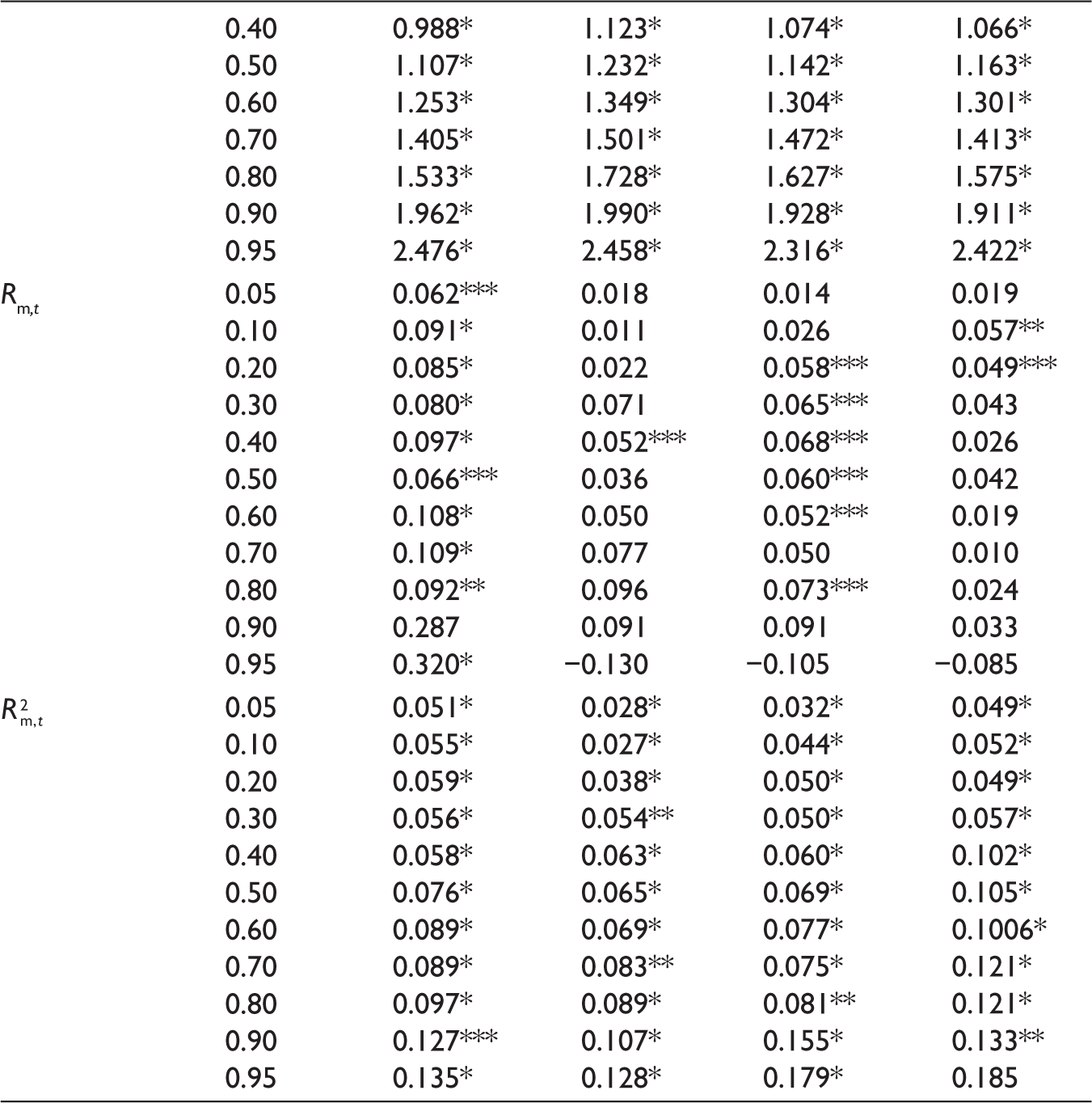

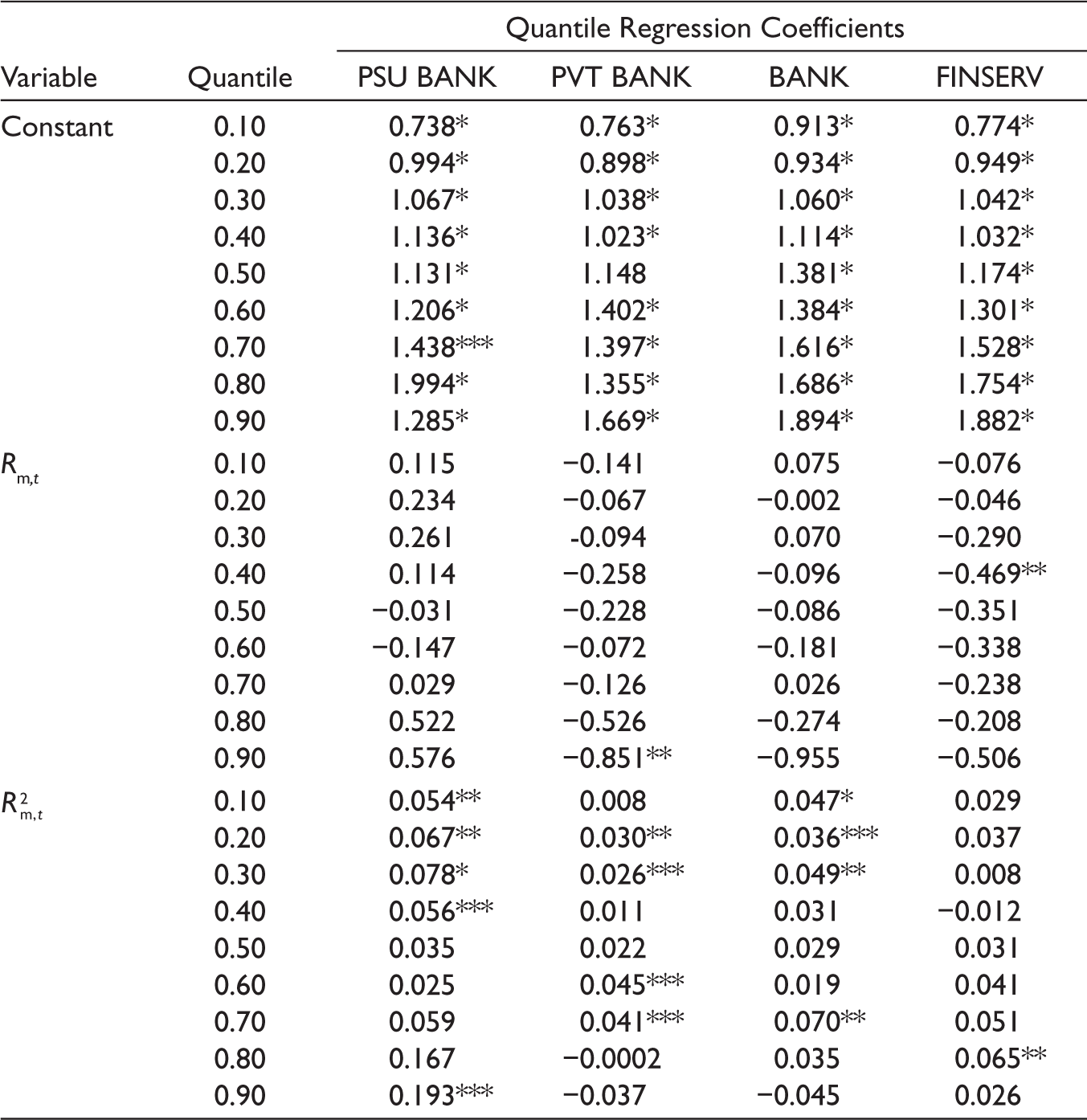

Therefore, we have examined the likely presence of the herding effect in the extreme market conditions of the post-COVID-19 era and present the quantile regression results for the extreme market phases, viz. bullish and bearish phases in the post-COVID-19 period in Tables 9 and 10. Since the coefficient of

Quantile Regression Results: Post-COVID-19 in Bullish Market Condition

Quantile Regression Results: Post-COVID-19 in Bearish Market Condition

This finding of the evidence of herding effect in the bullish market condition corroborates the findings of Chang et al. (2000); Lobão and Serra (2007); Hwang and Salmon (2004); Kassim and Duasa (2008); Barros (2009); Zhou and Lai (2009); Zaharyeva (2009); Demirer et al. (2010); Leite (2011); Bonfim and Kim (2012); Laih and Liau (2013); Chiang et al. (2013); Jlassi and Naoui (2015); Hwang et al. (2016); Vinh and Anh (2016); Zheng et al. (2017); Mahmud and Tinic (2018); and Nath and Brooks (2020), but it contradicts the findings of Lao and Singh (2011); Ganesh et al. (2016); Kumar et al. (2016); Dutta et al. (2016); Mertzanis and Allam (2018); Sharma (2018); and Chaffai and Medhioub (2018). Considering the COVID-19 pandemic era, our findings match that of Espinosa-Méndez and Arias (2020), Dhall and Singh (2020), Wu et al. (2020) and Sihombing et al. (2021). The presence of herding behaviour in bullish market conditions may indicate the presence of excess volatility (Kabir & Shakur, 2018), which can negatively impact the optimal portfolio determining ability of investors during the crisis period (Shehzad et al., 2021) as it can lead to error in the pricing of stocks (Sihombing et al., 2021). In such a situation, investors feel panicked, which may force them to go by the market consensus (Lee et al., 2015). Besides putting the market efficiency at risk, the presence of herding behaviour can reduce the possibilities of portfolio diversification (Bouri et al., 2020). Thus, policy changes are needed to maintain financial sustainability and assist the investors to deal with future crises.

The sudden outbreak of novel coronavirus across the globe has caused unprecedented vibrations in national economies having its footprints in almost all the sectors, including banking and financial services. The ongoing COVID-19 pandemic has weakened the sentiments of stock market investors by generating spirals of market uncertainties. In this context, this study examined the volatility and herding behaviour in the banking and financial services sectors in India using stock market data. The study was based on two hypotheses—first, the COVID-19 pandemic leads to sector-level stock return volatility due to investors’ week sentiment, panic feeling towards the rapid surge in COVID-19 confirmed cases and market pessimism, and second, the disordered psychology of investors prohibits them to rely on their information and induce them to show herding behaviour by following the decisions of other investors, especially during extreme market conditions amid the pandemic. The empirical outcomes lend to support the first hypothesis that the COVID-19 outbreak increased stock return volatility at the sectoral level. The study did not detect herding behaviour when the full market returns data were used. However, the herding behaviour was detected during the bullish market conditions amid the pandemic in the public sector banking and financial services at high quantiles (90%). The reason might be that the investors with impaired sentiments may have scares to make an investment decision in the high-return phase based on their information and beliefs and, hence, might be following the crowd as a shield against the unexpected loss of returns. Another reason may be the presence of asymmetric information, that is, the individual investors may be less informed about the market conditions and other fundamental relative to that of institutional investors, and thus, the former might have followed the latter. The presence of such herding bias, on the one hand, implies market inefficiency in the bull market condition during the pandemic phase and, on the other hand, implies the presence of market uncertainties and information asymmetry at the sectoral level. However, one positive implication of the evidence of the herding effect in the bullish market condition is that when both individual and institutional investors indulge in herding, gradually, their confidence will increase due to positive expectations and general optimism in the market. This directly contributes to quick market recovery from the crisis of heightened volatility as was observed in the capital market from late April 2020 onwards.

Since the presence of herding behaviour during extreme market conditions and during the crisis period can contribute to significant asset mispricing due to asymmetric information flow in an imperfect information market, it is crucial to reduce the degree of information asymmetry among the market participants by ensuring fair and cost-free disclosure of all pertinent information. The governmental bodies and market regulators can issue advisory for increasing the confidence level of investors to help them stay away from the traps of herding behaviour. Since the herding effect is more observed in the case of individual investors relative to that of institutional investors, the former can be given relevant awareness training about the techniques of investment analysis using fundamentals. The public authorities need to work for reducing multidimensional uncertainties surrounding the crisis to boost investor confidence and spread market-wide optimisms.

However, the study is limited in the sense that it does not explore the determinants of herding effect during the crisis period like the COVID-19 pandemic. Therefore, further research can be conducted to determine the factors influencing herding behaviour in the time of COVID-19 pandemic, as asset selection and investment decisions are taken, considering both macroeconomic and industry/sector-specific fundamentals, including government policy announcements.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.