Abstract

On the onset of the year 2020, the unprecedented outbreak of novel coronavirus, initially as a human health epidemic and later as a global pandemic, has wobbled the economies of affected countries across the globe. The consequential unexpected occurrences of supply- and demand-side shocks forced the economies to trim down their growth prospects. The interplay of these shocks has generated spirals of downturns in all major economic sectors, including the financial sector in affected countries. Specifically, the stock markets immediately nosedived, following the outbreak of the global spread of coronavirus disease 2019 (COVID-19). Thus, we examine the behaviour of the selected Asian stock markets amid the huge uncertainties of the corona pandemic and find the occurrences of volatility clustering in these markets. Such volatility clustering primarily occurred, owing to the pessimistic and panic sentiments of investors, and the increase in the number of COVID-19 confirmed cases, changes in oil prices, and exchange rates were found to be significant in channelizing the fears and uncertainties of coronavirus pandemic to cause unexpected nosedives in Asian stock markets.

Introduction

The unexpected outbreak of novel coronavirus contagion has created an unparalleled and devastating hazard to both human health and the socio-economic prosperity across the globe, and the world is yet confused about its severity and span. It has been observed to work through a highly interdependent world with interconnected production networks and financial markets (Sahoo & Ashwani, 2020). The economic fallouts of this pandemic mainly include a strained healthcare system, disrupted supply chain and trade, and plummeted production, consumption and investment activities. The footprints of its impacts are noticed at almost every corner of economies, developed or emerging, primarily driven by demand, supply and financial shocks. While the demand shock resulted in the decrease in consumers’ ability to buy goods and services due to lockdown and shutdown measures, and restrictions on movements, supply shocks have caused a reduction in economies’ capacity to produce due to supply-chain disruptions, restrictions on the movement of labour and the temporary shutdown of some production units as a part of the enforced pandemic containment measures. Besides, the financial shock has resulted in decreased liquidity availability to businesses due to disorders in the cash-flow patterns. The United Nations (UN) Secretary-General on 10 June 2020 1 aptly remarked that the temporary business closures are becoming permanent and unemployment is skyrocketing, and thus, rebuilding to pre-crisis levels of output and employment may take years.

While tracing the epicentre of the coronavirus outbreak and its subsequent spread, the extant literature notes the report of the first four cases in Wuhan, China, on 29 December 2019 (Li et al., 2020), following the report of positive cases in Thailand on 13 January 2020; Japan on 15 January 2020; and South Korea on 20 January 2020 (Cardona-Arenas & Serna-Gomez, 2020). All these cases have been believed to be imported from Wuhan, the epicentre of contagion. The attention of the world was drawn towards such unexpected outbreak when National Health and Fitness Commission (NHFC) of China on 20 January 2020 confirmed that the virus is human-to-human transmissible (Liu et al., 2020). Immediately, next day, the US Centers for Disease Control and Prevention (CDCP) confirmed the first case in Washington. 2 These confirmations were the big news of those days, which immediately exerted announcement effects on the stocks of travel-related companies, including airlines and hotel companies. To mention a few, Cathay Pacific lost 4 per cent, American Airlines lost about 2 per cent, United Air Lines lost 3.3 per cent, Casino companies Wynn Resorts lost 4.4 per cent, Las Vegas Sands lost 4 per cent, Marriott Vacations lost 2 per cent and Marriott International lost 1.9 per cent. 3 Such announcement effects were also observed in other countries and stock markets started displaying volatilities amid the spread of uncertainties and fears of virus spread.

The noteworthy observation is that the virus spread became rapid in China and 20 more countries outside China, mostly Asian, by the end of 30 January 2020. The World Health Organization (WHO) declared the situation as ‘Global Public Health Emergency’ on 31 January 2020 (Oxford Economics, 2020). Subsequently, the virus spread turned to be a pandemic from initial phases of an epidemic with the report of 123,000 globally confirmed cases and 4,578 deaths, 4 and so, WHO formally tagged it as Global Pandemic on 11 March 2020 (WHO, 2020). By this time, the world had already been under panic and pessimism, which caused severe plunges in market indices on the announcement day. For instance, Asia Dow Index lost 4 per cent by midday; Japanese Nikkei-225 fell 3.6 per cent by mid-afternoon; Hong Kong Stock Exchange lost 3.6 per cent by early afternoon; Shanghai Stock Exchange composite index lost 1.6 per cent; Singapore Financial Times Stock Exchange (FTSE) Straits Times Index fell 3.7 per cent by early afternoon; Taiwan’s TSEC (Taiwan Stock Exchange Corporation) fell 4 per cent; and Mumbai Sensex went down by 6.8 per cent on the day of the announcement. 5

The downturns in stock markets deepened when governments restricted domestic and international travels and imposed outright lockdown of affected areas to contain the virus spread. The high value–adding sectors like petrochemicals and garments witnessed shrink in demand and supply due to restrictions on the movement of man and materials. The greatest hits were observed in tourism and hospitality, retail, civil aviation and in labour-intensive and supply chain–based manufacturing sectors, which caused increased layoffs and the consequential rise in unemployment rates. According to Standard & Poor (S&P) Global Rating, the rate of unemployment across Asia-Pacific went up by 3 percentage points by 21 April 2020, as a consequence of the implemented social distancing measures. 6 Bangladesh recorded unemployment figures of 15 million, while India recorded 122 million, Pakistan 18 million and 6 million in Afghanistan due to COVID-led slowdown/shutdown in trade and business in April. 7 In Malaysia, the unemployment rate increased to a level of 3.9 per cent by the first week of May 2020. 8

Besides the adversities on unemployment, the spread of coronavirus also left its footprints in the oil sector. Owing to falling demand in aviation and manufacturing, movement restrictions on people, and due to own structural issues, the major oil indices crashed over 60 per cent as of early May 2020. 9 The crude oil prices plunged, falling to under US$30 per barrel. On 21 April 2020 West Texas Intermediate (WTI) crude score plunged more than 300 per cent. It recorded for its trading at below negative US$40/bbl and settled at negative US$37.63/bbl for the first time in history. 10

The uncertainties of the pandemic also triggered a swift outflow of capital, causing a nosedive in the markets and a rapid fluctuation in the exchange rates across the Association of Southeast Asian Nations (ASEAN) region. As a consequence, about a fourth of the stock market values in Indonesia, the Philippines, Thailand and Vietnam were wiped out. The largest drop was in Vietnam, where the market index fell by 29.3 per cent between end-January to end-March, and in Malaysia, the index fell by 11.8 per cent in the same period. The key currencies such as Thai baht, Indonesian rupiah and Singapore dollar were considerably affected (ASEAN Policy Brief, 2020).

The governments across countries implemented expansionary fiscal and monetary policies to give a timely boost to economies. The fiscal efforts were primarily to give reliefs of various kinds and to generate job opportunities for unemployed. Fiscal boosters also targeted quick recovery in trade and business. Complementing to these fiscal measures, the central banks also responded with policies of quantitative easing, targeting rebuilding faster liquidity and credit flows. 11 For example, Reserve Bank of India reduced the repo rate and reverse repo rate by 75 bp and 90 bp, respectively, on 27 March; Bank of Indonesia reduced the policy rate by 75 bp cumulatively in February, March and June; central bank of Hong Kong adjusted the base rate downward to 1.50 per cent and 0.86 per cent on 4 March and 16 March 2020, respectively; Bank Negara Malaysia reduced the Overnight Policy Rate by 25 bp; The central bank of the Philippines reduced its policy rate thrice in 2020 by a cumulative 125 bp; and central bank of Thailand reduced the policy rate by 75 bp from 1.25 per cent to 0.50 per cent during 2020. 12 Such a downward revision of central bank policy rates can have effects on movements in stock market indices.

In this backdrop, this study examined the behaviour of stock markets in affected countries in Asia amid the devastating economic and financial consequences of the rapid spread of coronavirus. The main research question that has been addressed in this study is ‘how does the sudden outbreak of corona pandemic affect the stock markets in Asian countries?’ This issue has been addressed in three parts—first, whether the uncertainties and pessimism associated with the corona pandemic resulted in the increased stock market volatility; second, whether there is an effect on the abnormal stock returns due to the outbreak of the pandemic; and, third, what are the major factors responsible for the stock market plunges after the outbreak of corona pandemic in Asian countries.

The results support the observations about the announcement effects on stock return movements and presence of volatility clustering in selected Asian markets. The outcomes also provide insights about the factors responsible for stock market plunges in Asia. The significant factors of stock markets’ downturn include the number of coronavirus disease 2019 (COVID-19) confirmed case changes in the exchange rate and the changes in Brent crude oil prices. The remaining of the article is organized as follows: Section II reviews the relevant literature and states the hypotheses of the study; Section III describes the data and methodology used in the study; Section IV analyses the data to generate empirical insights into stock market behaviour amid the uncertainties of the severity and span of corona pandemic; and Section V concludes the article.

Literature Review

Amid the huge implausibility about the severity and span of the novel coronavirus pandemic, an exceptional human health crisis has been caused across the globe (Wang et al., 2020). And, the immediate containment measures adopted by nations to control the virus spread have triggered a global economic slump, driven by both supply and demand shocks (Eichenbaum et al., 2020; Fetzer et al., 2020; Gormsen & Koijen, 2020; Malden & Stephens, 2020). The interplay of these shocks have caused fluctuations in the labour supply, oil prices, commodity prices, income and wages, output, export-import activities, exchange rates, interest rates, share prices, savings, investment spending and availability of liquidity and credit to households and businesses, thereby disturbing the positions of aggregate demand-aggregate supply (AD-AS) curves (Banco, 2020; IMF, 2020; Maliszewska et al., 2020; Pak et al., 2020; World Bank, 2020; WTO, 2020). Such a global macroeconomic disequilibrium has exerted spectacular impacts on different sectors in economies, including the financial markets. The panic and uncertainties of COVID-19 pandemic intensified the global financial instability world over and caused nosedives in market indices (Zhang et al., 2020). Prominent among the financial market segments is the stock market, which weathered spiked volatility, deteriorated liquidity and sharp fall in the prices of equities and commodities immediately after the breakout of the pandemic (Boissay & Rungcharoenkitkul, 2020). As corrective measures, governments and central banks across the globe have responded with fiscal and monetary policy options. While governments implemented cash transfers and other economy-booster packages, central banks eased the money supply by cutting down the policy rates, and they also injected additional liquidity to the financial system (McKibbin & Fernando, 2020). Consequent upon these actions of containing the fallouts from the pandemic, recently, investors’ sentiments have been stabilized, leading to a recovery in most of the stock markets, albeit leaving some degree of volatility in stock return patterns, thereby posturing financial vulnerabilities. The near-term improvements in the job market and manufacturing profiles, and the positivity of the availability of coronavirus preventives/curatives, have all boosted investors’ confidence and put the market indices on the recovery track in the midst of threatening scenarios of rising COVID-19 cases.

The empirical studies addressing the issues of the dynamics of COVID-19-led stock market volatilities are only a few. In earlier studies, Bai (2014) and Baker et al. (2012) argued that the investors feel pessimistic about investment prospects in a given market and sell off that market’s stocks under the outbreak of communicable diseases. Recently, Liu et al. (2020) observed that the adverse effects of increased COVID-19 cases on stock market returns were mainly triggered by the investors’ pessimistic sentiments on future returns and fears of uncertainties. Shanaev et al. (2020) also added that the market sentiment does play a crucial role in explaining the economic and financial implications of the corona pandemic. Across the globe, corona pandemic has impacted economic activities, owing to domestic lockdowns and slowdown in the global trade and growth, which, in turn, generated spirals of uncertainties that transmitted the spillovers of COVID-19 impacts to domestic financial markets, mainly through the channels of finance and confidence. Zhang et al. (2020) showed that the global financial risks have increased substantially in response to the pandemic, and the individual stock market reactions are clearly linked to the severity of the outbreak of the pandemic in each country. Albulescu (2020) noted that the report of new COVID-19 cases in China and outside China have a mixed effect on financial volatility. Corbet et al. (2020) observed that the announcement of corona pandemic caused stock markets to exhibit negative returns and increased volatilities. Haroon and Rizvi (2020a) found a positive association between media induced panic and increased sense of uncertainly in financial markets, evidenced by volatility in indices of several industrial sectors. Huo and Qiu (2020) observed that there were reversals in stock prices of China both at the industry level and at the firm level, primarily due to investors’ overreactions to the announcement of pandemic lockdown. Also, Haroon and Rizvi (2020b) found the existence of an inverse relationship between the trends in the number of confirmed COVID-19 cases and the financial market liquidity. Christensen (2020) observed that the global coronavirus pandemic has caused significant increases in the volatility and deteriorated the market liquidity at industry levels. Piksina and Vernholmen (2020) observed that corona pandemic-related news negatively influenced the market sentiment in Sweden, and thus increased the stock price volatility. Al-Awadhi et al. (2020) found that daily growth in total COVID-19 confirmed cases and deaths have significant effects on stock returns across companies in China. In a study, Mishra et al. (2020) found that all the stock market indices depicted downturn during COVID-19 in India and concluded from the Markov-Switching Vector Autoregressive (VAR) model that the impact is severe on stock returns. However, Ali et al. (2020) observed that the plummets in stock market returns in China were relatively lower than that in the USA, the UK, Germany and South Korea, where market volatilities were larger. Liu et al. (2020) in a study found that the stock markets in major affected countries fell quickly after the virus outbreak, while countries in Asia experienced more negative abnormal returns as compared to other countries.

In continuation to such observations, Baker et al. (2020) unveiled the key factors of unexpected plunges in stock markets and highlighted the role of the enforcement of government restrictions on commercial activities, and voluntary acceptance of social distancing by people for such sudden downturns. The spread of coronavirus and subsequent imposition of restrictions on travel and transport, and closure of manufacturing houses have caused slumps in oil prices, which posed a serious threat to public health, financial system and the economy at large (Apergis & Apergis, 2020). Such slumps in oil prices made the oil market inefficient in deciding the oil prices (Gil-Alana & Monge, 2020), and thus increased stock market volatility (Sharif et al., 2020). The persistent fall in oil prices is primarily due to the loss of people’s confidence towards investment in oil and oil-related products, which led to the people diversifying their investments. A negative association has been empirically observed between crude oil return and stock market returns (Liu et al., 2020; Qin et al., 2020). The negative effects of coronavirus pandemic on oil prices have been found to be stronger when the number of new coronavirus cases increased above the threshold level of 84,479 (Narayan, 2020). The slump in oil prices associated with distortions in the export–import activities also caused domestic exchange rates against the US dollar (USD) to reveal fluctuations in several countries. Thus, exchange rate volatilities are presumed to have sent signals to stock markets of different economies and caused marked plunges in their market indices (Cardona-Arenas & Serna-Gomez, 2020). Moreover, Onali (2020) found that the number of COVID-19 reported deaths have a positive impact on the volatility index (VIX), which, in turn, was found to have a negative impact on stock market returns in the USA.

Furthermore, the likelihood of inflation risks contributing to the stock market plunges in different countries cannot be ignored. Of course, no empirical studies have yet been taken up, including inflation risks as a factor influencing the stock market movements during the COVID-19 pandemic. However, the argument is that the pandemic has made severe disruptions in supply chains in affected countries, which might have generated spirals of commodity market uncertainties to adversely influence the movements in stock market indices. Second, the fiscal measures adopted in affected countries are primarily relief focused and economy boosters. So, these measures are unlikely to be inflationary. Third, the recent monetary policy of quantitative easing is likely to increase the money supply, thereby spreading the panics of inflation risks. Since the main objectives behind the quantitative easing are to make the financial markets function efficiently and provide supplementary credits to businesses for their smooth continuation, the monetary measures such as cut down in central bank policy rates seem to reduce the potential supply shocks. Despite the impacts of inflation and interest rate risks on stock market movements being ambiguous in light of COVID-19 pandemic, we can include inflation and interest rate risks as probable causes of nosedives in stock markets to estimate their impacts and significance.

The unexpected intensity and length of COVID-19 pandemic and subsequent containment measure of lockdowns have increased unemployment rates in affected countries. The sudden surge in unemployment rates in affected countries might have made the investors uncertain about the expected returns on their investments when economic activities almost came to a halt during the phases of lockdowns. This labour supply shock might have also contributed to the plunges in stock market indices. However, empirical studies are also lacking from this point of view. Thus, we have included the unemployment rate in our analysis to estimate its impact and significance.

Based on the perspectives examined in the first section and the review of relevant studies, three hypotheses have been formulated in the study. These are (a) the outbreak of COVID-19 in Asian countries increases stock market volatilities; (b) the information on the announcement of the possibility of the global spread of COVID-19 negatively affects stock market returns; and (c) COVID-19 reported cases and deaths, volatility index, oil price, exchange rate, inflation rate, unemployment rate and central bank policy rate are significant causes of stock market plunges in Asian countries.

Data and Methodology

In this study, we have selected 12 Asian countries based on the degrees of the spread of COVID-19 infections.

13

These countries are China, Hong Kong, India, Indonesia, Israel, Japan, Malaysia, the Philippines, Singapore, South Korea, Thailand and Taiwan. The stock market indices selected from these countries are listed in Table 1. We have used the daily data on COVID-19 reported cases and deaths being compiled from the website

List of Asian Countries, Stock Market Indices and Sample Data Period

List of Asian Countries, Stock Market Indices and Sample Data Period

The econometric methods used in the study are divided into three parts—first, the Generalized Autoregressive Conditional Heteroskedasticity (GARCH) (1,1) model has been used for describing the stock market behaviour in selected Asian countries in which asset returns might have been more volatile due to the outbreak of corona pandemic; second, the event study method has been used to examine the immediate response of the selected stock markets around the event of the announcement that the COVID-19 infection can spread rapidly across the globe; and, third, the panel fixed effect regression model has been estimated to explore the likely factors carrying pessimisms and uncertainties of the pandemic to affect the abnormal returns in the selected stock markets.

GARCH (1,1) Model Specification

We have used the GARCH (1,1) model, comprising the following conditional mean and variance equations:

In the conditional mean Equation (1), Ri,t is the first difference of the stock market closing index value (in natural log), generally interpreted as the stock return, in the stock market i at time t. Second, CVD

i,t

is the percentage change in the COVID-19 confirmed reported cases in the country i at time t. Third, VIX

i,t

is the return based on CBOE volatility index, popularly called ‘fear index’, which is a measure of investors’ pessimistic sentiments, fear and uncertain behaviour and market risks. Finally, ei,t is the residual. In the conditional variance equation,

Event Study Method

We have employed the event study method to determine whether there is an abnormal stock returns effect of the event of the announcement of the global spread of COVID-19 infection under the assumption that the Asian stock markets are information efficient.

15

We believe that the announcement made by Zhong Nanshan, the high-level expert group leader of NHFC of China, on 20 January 2020, about the possibility of spread of novel coronavirus among people across the globe, which became the headlines of the major media, is the event that caused a stir in the markets. Precisely, 20 January 2020 is taken as the event date in our study. Since the event study facilitates observing the economic/financial effects of the event over a relatively short period of time, we have formed six event windows, consisting of 90 trading days from the event date: (0,14), (15,29), (30,44), (45,59), (60,74), and (75,89). The event study method uses an estimation window before the event date to determine the effect of the event on the stock market behaviour. Since the news of the global spread of novel coronavirus created huge uncertainty in the market, choosing a too long estimation window cannot accurately capture the abnormal stock market response. Thus, we have taken two estimation windows (−1,−90) and (−1,−120) to observe the changing trends of the Asian stock markets. The estimation window helps to estimate the expected stock market returns and abnormal stock market returns using an ordinary least squares (OLS)-based market model, specified as follows:

In this specification, Ri,t is the real return of a stock index, Rmt is the real return of a benchmark stock index (we have taken Dow Jones Global Index as the benchmark index), E(Ri,t) is the expected return of a stock index and AR i,t is the abnormal return of a stock index. Then the cumulative abnormal return (CAR) has been calculated for each event window, and its significance has also been determined by employing the t-test. The AR and CAR help in understanding the stock market behaviour in the post-event period. In the event study, we have focused on the significance of the calculation of returns, as most of the variation in the value of the stock market is due to changes in expected returns (Campbell & Shiller, 1988; Shiller, 1981).

Panel Fixed Effect Regression Specifications

The intellectuals would come to a consensus with us that the global spread of corona pandemic has recently created spirals of systematic risks across markets in Asia. And, we can cite the role of supply, demand and financial shocks for such occurrences (Brinca et al., 2020). In order to control the adverse effects of these shocks, governments have responded with the conventional expansionary fiscal and monetary weapons along with other policy responses to protect their economies from plausible recessions. This boils down to the argument that the post-event abnormal returns in Asian stock markets could have been influenced by the supply shocks, demand shocks, financial shocks and policy responses of governments. Therefore, the parameters that represent these shocks and responses need to be examined, while attempting to explore the factors carrying the pessimisms and uncertainties associated with the corona pandemic and influence the stock markets of Asia. We have taken Brent oil price and inflation rate as reflections of supply-side shocks; unemployment rate and exchange rate as indicators of demand-side shocks; and central bank policy rate as the monetary policy response variable. Besides, we have taken stock market return as the proxy of financial shock and volatility index as a mediating variable that reflects investors’ sentiments towards the increase in COVID-19 confirmed cases and deaths.

We have employed panel fixed effect OLS-based regressions to explore the probable factors influencing the abnormal returns in the stock markets of selected Asian countries over the 90-day event window from the event date of 20 January 2020. The following specifications have been used for this purpose:

In the specifications (6) and (7), AR it is the abnormal return of the stock index, CVD it is the log of the COVID-19 confirmed reported cases, DTH it is the log of the COVID-19 death reported cases, Rit is the real return of the stock index, VIX it is the log of the CBOE volatility index, EXR it is the USD-based exchange rate of the domestic currency, INF it is the Consumer Price Index (CPI)-based inflation rate, UEMP it is the unemployment rate, CBPR it is the central bank policy rate and OilP it is the log of the Brent crude oil price. This specification allows for the country and year fixed effects through the use of the hi, rt, gi and lt terms in the specifications (6) and (7). We have selected fixed effects model for our analysis by performing the Hausman test. And, within fixed effects, we have chosen to include both cross-section and period fixed effects on the basis of the redundant fixed effects likelihood ratio tests. The results for random effect models, Hausman test and redundant fixed effects likelihood ratio tests can be made available on request to authors.

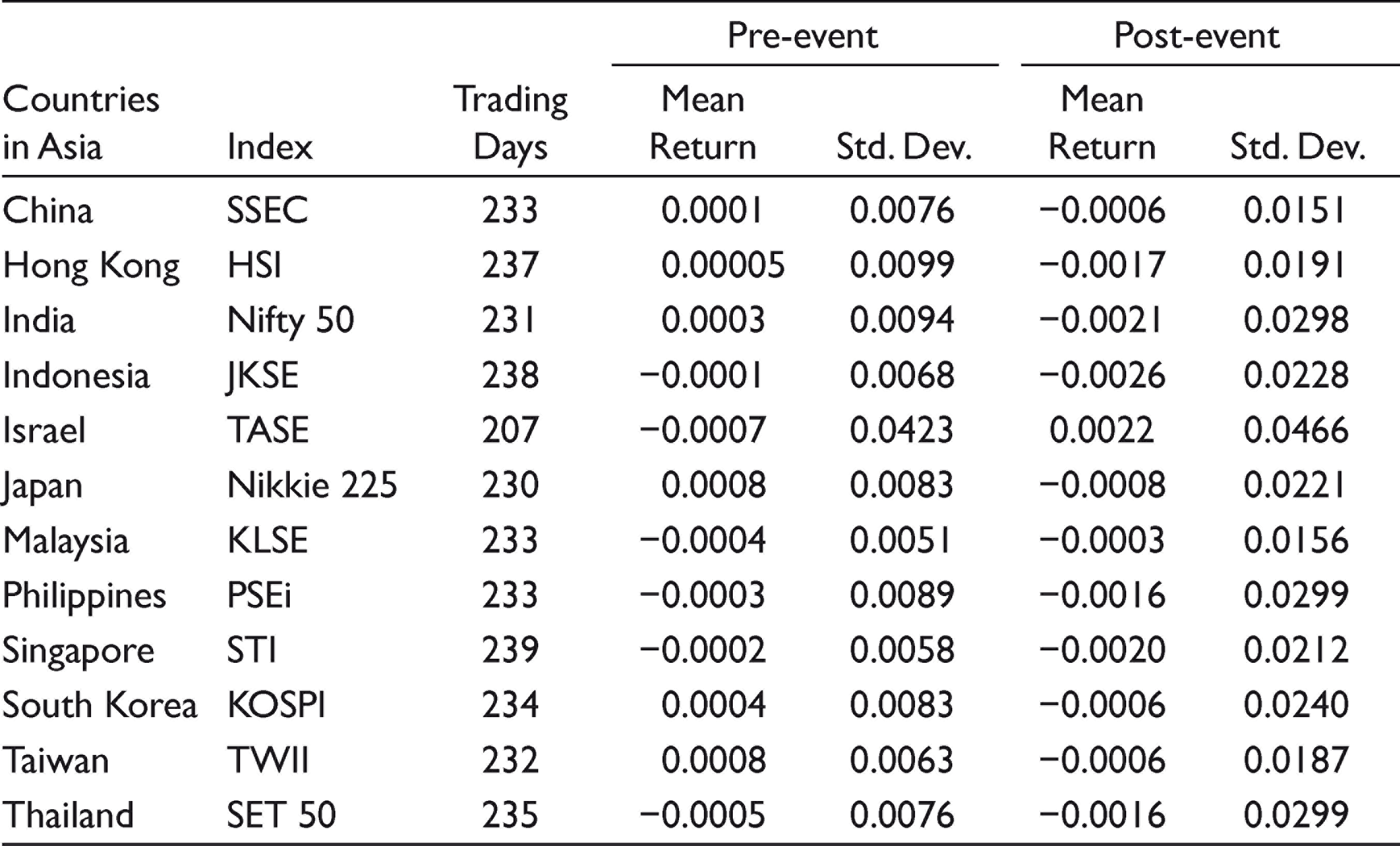

At the outset, the descriptive statistics of the selected stock market indices of Asia are presented in Table 2. It is revealed that the post-event mean returns in all the selected stock markets in Asia are negative, except Israel with relatively larger standard deviations in contrast to that of pre-event period. This is the clear indication of volatility of these stock markets.

Descriptive Statistics of Selected Stock Market Indices of Asia

Descriptive Statistics of Selected Stock Market Indices of Asia

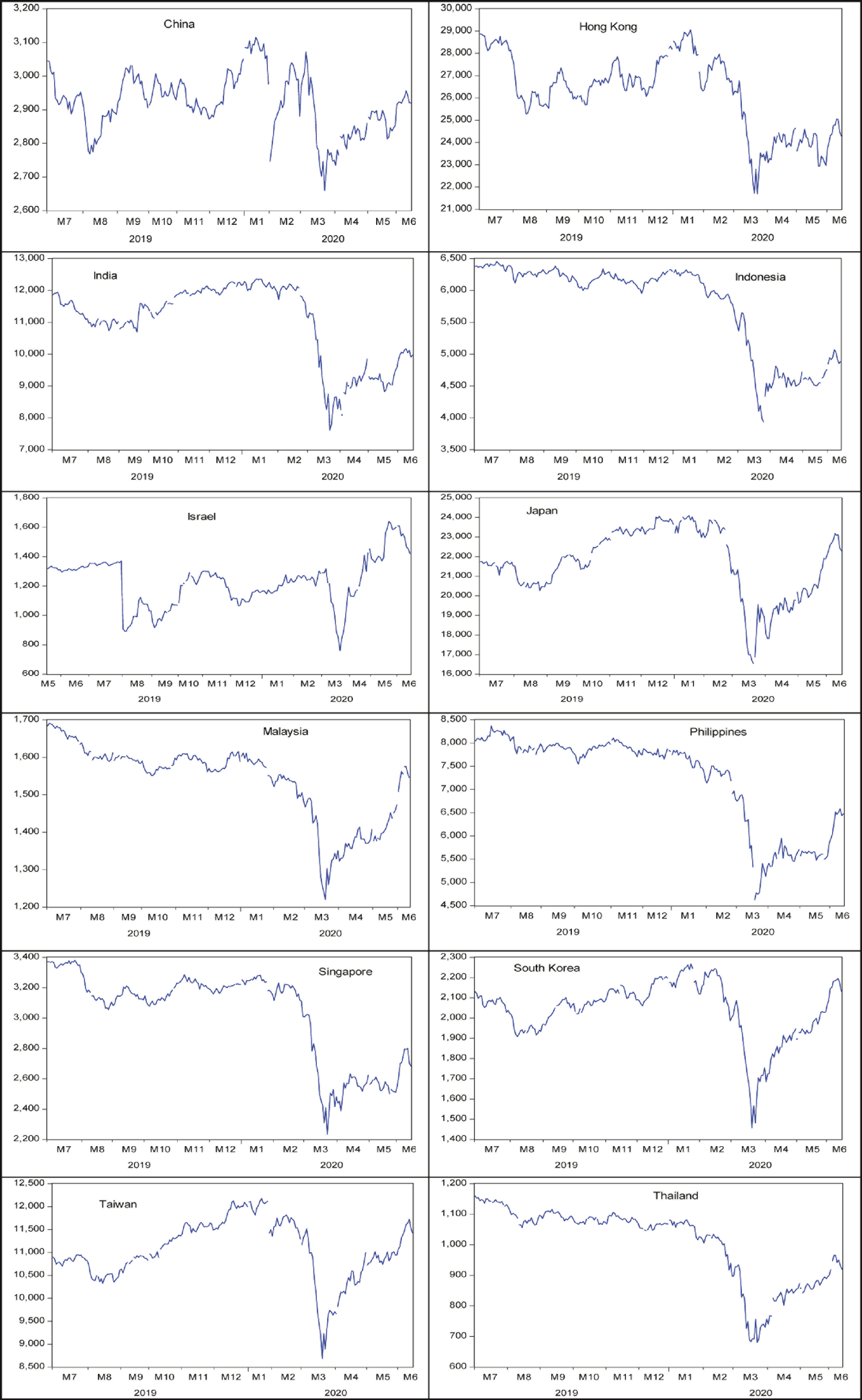

The time-series plot of the stock market return series in Figure 1 reveals the presence of volatility clustering immediately after the event date, except for the stock market of Israel which is relatively stable. In recent days, these return series have been depicting the trends of returning to their pre-event levels. This is the clear indication that investors at the macro level have subsequently accepted the advice of WHO about the learning to live with coronavirus. Furthermore, the recovery trends in stock market indices can also be due to the expansionary effects of fiscal and monetary policies. This sort of optimism in investors’ behaviour is likely to spread quickly to generate forces to bring back the economies of selected Asian countries into the growth phase of business cycle.

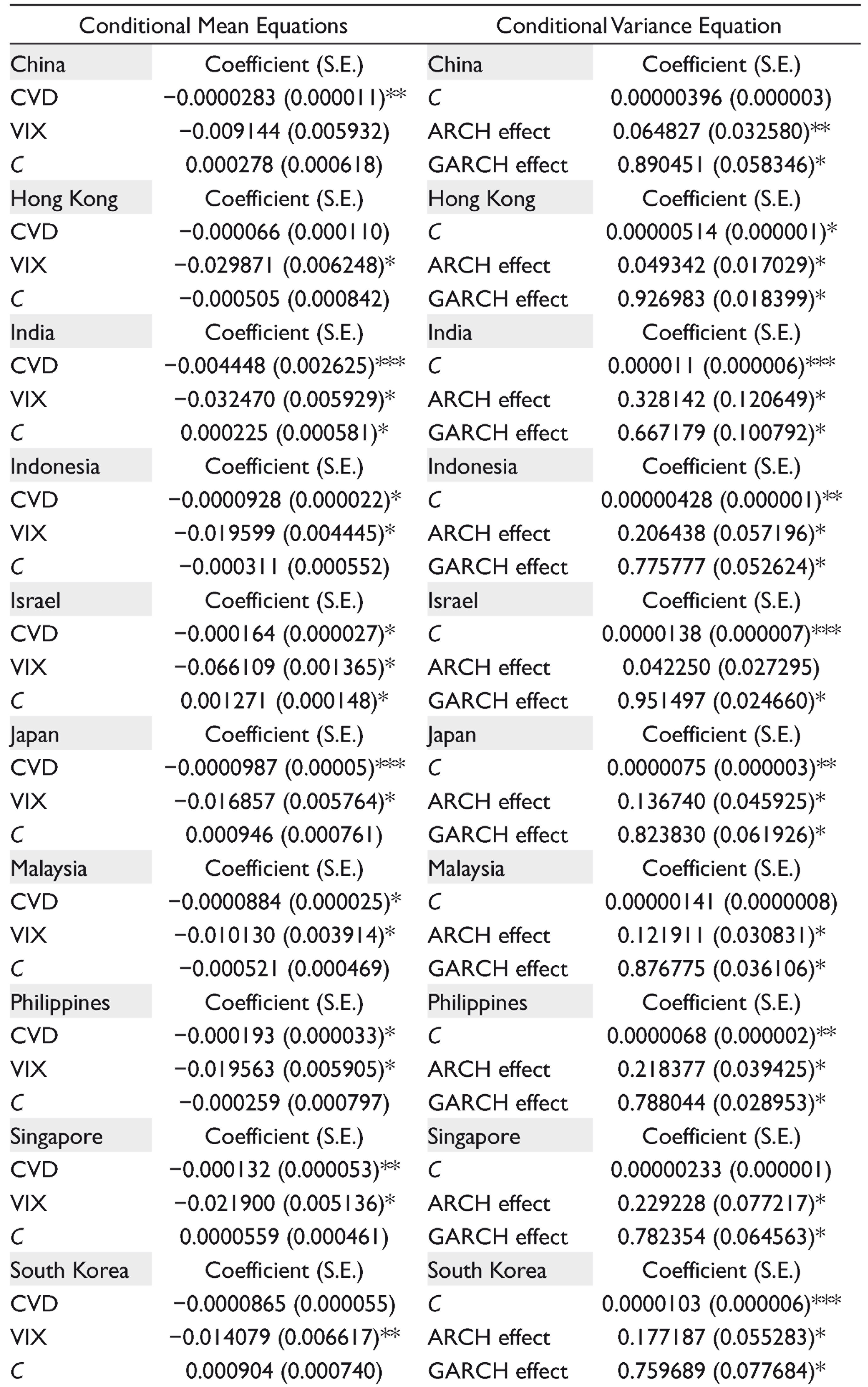

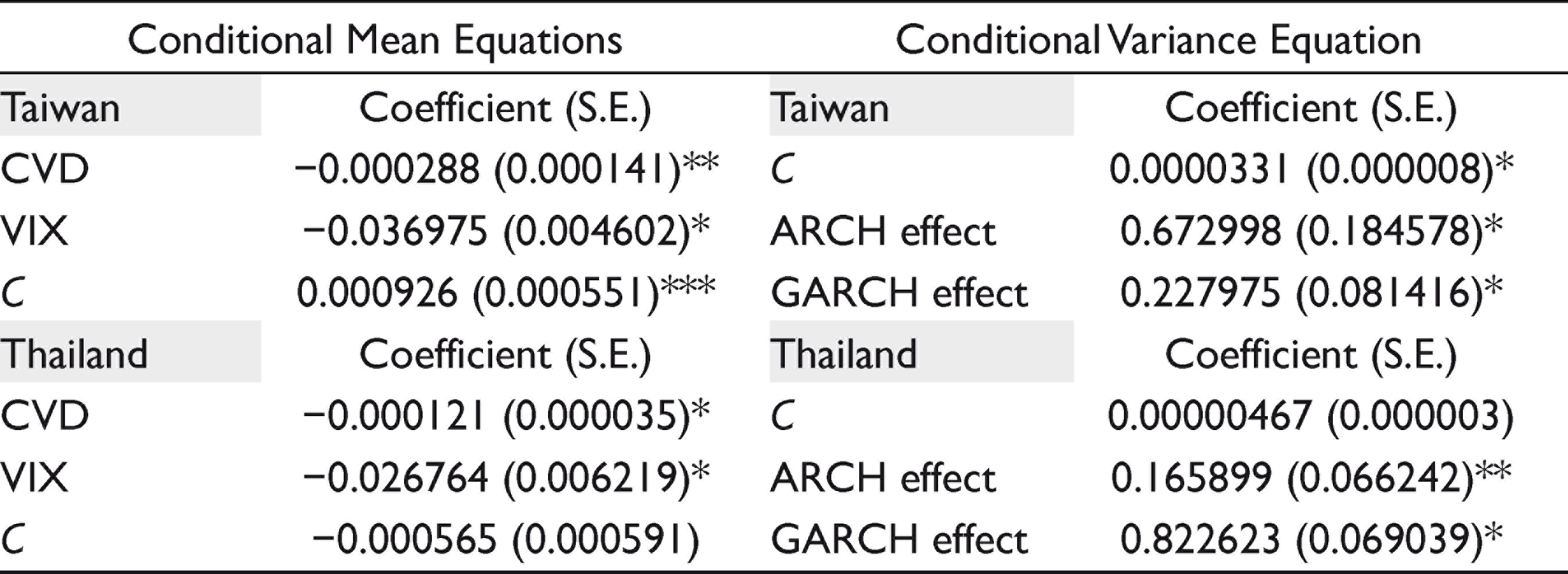

However, for statistical conformity of the presence of volatility clustering of stock return series due to the unanticipated outbreak of corona pandemic, we have performed GARCH (1,1) model estimation—the results are summarized in Table 3. It is observed that the coefficient of CVD term is negative as well as statistically significant in the conditional mean equation (left side of Table 3) for all the stock markets in selected countries, except for Hong Kong and South Korea for which the coefficient is negative but not significant. It lends to support the negative effect of the outbreak of coronavirus pandemic on the stock markets of selected Asian countries. Furthermore, the coefficient of the fear index is negative and significant in all countries, except for China. This clearly indicates that the pessimistic sentiment of investors towards corona pandemic is a significant factor in influencing the movements in stock market indices. China is considered an exception because the pandemic was soon controlled in this country and normalcy resumed.

Results of GARCH (1,1) Model Estimation

Besides, the GARCH effect is positive and statistically significant in the conditional variance equation (right side of Table 3) for all the stock markets in selected Asian countries, which confirms the presence of volatility clustering in the stock return series due to the unexpected global spread of COVID-19. Specifically, a bulk of pessimistic information flows from the previous day’s forecast to make the stock markets volatile, around 89 per cent in China, 92 per cent in Hong Kong, 66 per cent in India, 77 per cent in Indonesia, 95 per cent in Israel (but referring to Figure 1, one can see that this outcome also covers some volatility clustering in the second quarter of 2019–2020, so the entire coefficient is not due to the pandemic effect), 82 per cent in Japan, 87 per cent in Malaysia, 78 per cent in the Philippines, 78 per cent in Singapore, 75 per cent in South Korea, 22 per cent in Taiwan and 82 per cent in Thailand. All these results satisfy the stability condition of the GARCH (1,1) model, that is, the sum of ARCH effect and GARCH effect is ≤1. However, these many volumes of information flow from the past period forecasts need not necessarily be due to the uncertainties created in the post-event period. And, to this extent, the above-mentioned results can be misinterpreted albeit Figure 1 confirming maximum volatility in the post-event period. Hence, we have employed the event study method for analysing the stock market behaviour in the post-event period.

Using the specifications (3)–(5), we have estimated the abnormal returns in all the selected stock markets under consideration for the event day and the immediate next trading day using two different estimation windows, and the results are reported in Table 4. It is observed that the abnormal returns are negative for all the stock markets in both the estimation windows, except for Israel on the immediate next day of the event day. This reflects the pessimistic behaviour of investors towards the global news of the outbreak of corona pandemic, which makes the markets volatile. In order to know the persistence of such negative effect, we have estimated the CAR over six different short-length event windows, covering a period of 90 trading days using two different estimation windows. The results are reported in Tables 5 and 6.

Abnormal Returns in the Stock Markets in Asia

CAR in the Stock Market Indices in Asia

CAR in Sample Stock Market Indices in Asia

For China, using estimation window of (−1, −90), the negative effect of the outbreak of corona pandemic initially persists up to 14 trading days, then reappears between 30 and 44 trading days and further reappears between 75 and 89 trading days. This indicates good resilience of the stock market of China towards the spread of uncertainties and pessimisms. A similar pattern is observed when a longer estimation window of (−1, −120) is used. And, these results are statistically significant. The stock market of Hong Kong also depicts almost similar behaviour to that of the Chinese stock market. In the Indian stock market, the negative effects of the pandemic persist up to 44 trading days and reappear between 60 and 74 trading days in both the estimation windows, and these results are statistically significant. In other words, the event has made the Indian stock market more volatile and caused a market downturn. A similar pattern is also observed for the stock markets of Indonesia, the Philippines and Singapore with statistical significance in both the estimation windows.

In the stock markets of Malaysia, South Korea, Taiwan and Thailand, the COVID-led downturn continued up to 44 trading days, and then the markets recovered. These results are all statistically significant in both the estimation windows. The stock market of Japan weathered the downturn up to 29 trading days due to the negative effects of the spread of coronavirus and such downturn reappeared between 45 and 59 trading days in the estimation window (−1, −90) with statistical significance. But when we estimated using a longer estimation window of (−1, −120), the Japanese stock market was observed to be in downturn trend up to 59 trading days and then recovered with statistical significance. These observations are in conformity with the time-series plots (see Figure 2) using the Japanese index value, which led us to conclude the robustness of the results of the (−1, −120) estimation window for capturing the behaviour of Japanese stock market. The stock market of Israel depicts typical trend behaviour when we look at the time-series plot of index value and the estimated CAR values. In March 2020, the stock market of Israel witnessed a sudden downturn and also very quickly recovered, leaving a little footprint of the negative effects of the spread of coronavirus. Again, towards the end of May 2020, it showed a downturn, but its corresponding CAR is negative and statistically insignificant in both the estimation windows. So, we can say that the stock market of Israel is more shock resistant.

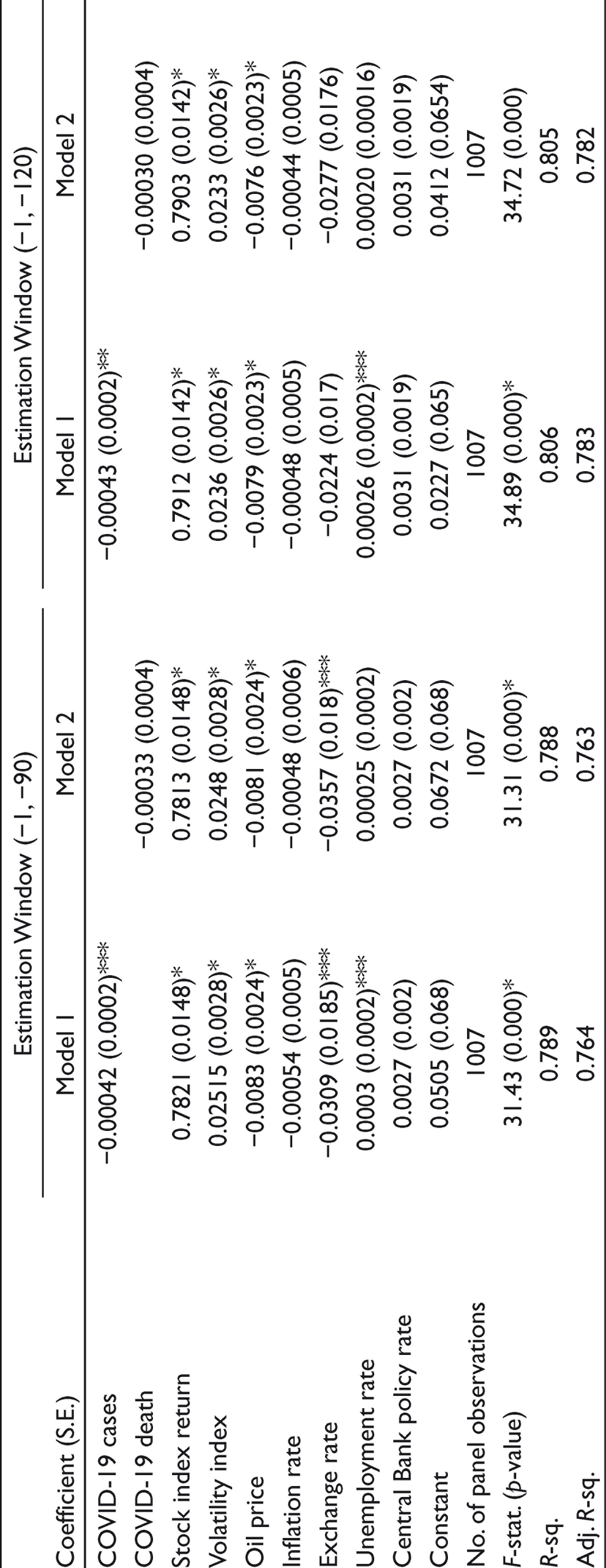

Having studied the response of the Asian stock markets to the news of the unexpected outbreak of the novel coronavirus in terms of the market downturn and recovery pattern, it is crucial to explore the likely factors, which create uncertainties and pessimism, and bring into reflection in terms of market downturn by adversely affecting investors’ sentiments. For this purpose, we estimated fixed effects panel regression Equations (6) and (7) for both the estimation windows, that is, (−1, −90) and (−1, −120), the results of which are presented in Table 7. It is observed from Table 7 that the COVID-19 confirmed cases in Model-1 have significant negative effects on the abnormal returns in the Asian stock markets during the post-event period in both the estimation windows. However, the reported COVID-19 death cases in Model-2 have no significant effects on stock market abnormal returns in both the estimation windows. This might be due to very low fatality rate of coronavirus infections, which investors might not have included in their technical analysis. The stock index return (represents demand and financial shocks because of its wealth effect on households and firms) has a positive significant effect on abnormal returns in models 1 and 2. This may be due to the fact that investors consider the wealth effect of their investments in their technical analysis of predicting stock market returns. Therefore, fluctuations in the returns on the stock index are a mediating factor in determining the abnormal returns in the post-event period. Another observation is that the fear index has a significant positive effect on abnormal returns in both the models and in both the estimation windows. Thus, we can say that the investors might not be that much pessimistic in their analysis of stock return predictions in Asia during the COVID period.

Factors Explaining Abnormal Returns in the Stock Markets in Asia

The effect of oil price on stock market abnormal returns is negative and statistically significant in both models 1 and 2. Primarily due to country-wide lockdowns and restrictions of travels and transports, the demand for oil substantially declined in the post-event period, which considerably reduced the crude oil prices, thereby adversely affecting the abnormal stock returns in Asian economies. Furthermore, the inflation rate has been observed to have negative effects on abnormal returns in the post-event period in both the models, but it is not statistically significant anywhere. Although aggregate demand for durables has been affected greatly due to the containment measures, the demand for necessaries has been affected marginally. This may be the reason why inflation risk has not been significantly transmitted to affect the nosedives of Asian stock markets.

We found the exchange rate negatively influencing the abnormal returns, and such observation is statistically significant in the estimation window (−1, −90), but not in the window (−1, −120). Although the export–import activities have been affected by the global spread of corona pandemic, and forex rates initially witnessed a little fluctuation, exchange rates in Asian countries are not a significant carrier of uncertainties of the outbreak of corona pandemic. In addition, the unemployment rate has been found to have a significant positive effect on the abnormal returns in the post-event period. This may mean that the pandemic triggered unemployment rates are lower than expected in Asian countries. Such a lower degree of actual and expected readings in unemployment rates might be due to the timely announcement of fiscal packages by the governments of these countries to control job losses and income losses. Therefore, the unemployment rate is also not a carrier of pessimism to adversely influence the abnormal stock market returns. The monetary authorities of Asian countries have also responded to counter the economic slowdowns by easing the policy rates. In this perspective, we found that the changes in central bank policy rate have positive effects on stock market’s abnormal returns. However, such observation is not statistically significant in any model.

Therefore, we found that changes in the number of COVID-19 confirmed cases, oil prices and exchange rates are the significant channels by which fears and uncertainties associated with the outbreak of coronavirus pandemic might have been transmitted to the stock markets of Asian countries and caused them to nosedive.

This study investigated the impact of severity of the spread of corona pandemic on the selected Asian stock market returns and their volatilities. The study contributes to the literature by providing empirical insights on how the ongoing pandemic has made investors panic and pessimistic in Asian countries. The finding of the significant negative effect of the rapid spread of coronavirus on Asian stock markets indicates that the pandemic generates the spirals of market uncertainty, which weakens investors’ sentiments and causes market volatilities. However, the degrees of volatilities are different across countries based on the severity of the pandemic. It is important to note that the Asian stock markets were found to be responsive to the global announcement regarding the nature of the spread of coronavirus. It is evident from the finding that stock market abnormal returns became negative immediately on the next day of the global announcement of the possibility of the rapid spread of COVID-19. This also implies that the information flows from the previous day could have caused volatilities in Asian stock markets. Besides, the study brings to the limelight the empirical evidence of the significance of increased COVID cases, oil price plunges and exchange rate fluctuations in adversely affecting investors’ sentiments while deciding about stock market investments in Asia. Therefore, the regulators and policymakers need to safeguard the investors’ interest maybe by providing liquidity and profitability opportunities to businesses. The policy focus should be to gradually activate travel and tourism, manufacturing, constructions and service sectors, keeping in view the severity of infection spread. This would certainly make the investors optimistic about the future earnings, which, in turn, would reduce market volatilities and make way for stable growth of economies. Despite the key empirical insights drawn from this study, scope lies in extending the work by including other relevant socio-economic, demographic, political and policy parameters in the analysis.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.