Abstract

The global economy has been severely paralysed, owing to the unprecedented crisis triggered by the COVID-19 pandemic, and different studies have indicated that the crisis is relatively more maleficent to the lower-income and middle-income economies. Methodologically, this study relied on the review and analysis of the grey literature, media reporting and data published by the Asian Development Bank, United Nations Conference on Trade and Development (UNCTAD), United Nations (UN), World Bank, International Monetary Fund (IMF) among others. The article begins by describing the impact of the pandemic on low-income and middle-income countries, and it discusses how they have responded to the crisis. While discussions have surfaced regarding whether COVID-19 will reverse the process of globalization, what will be its impact on the low-income country like Nepal? The study also highlights that with foreign direct investments speculated to shrink and foreign assistance and remittance taking a hit, how is Nepal struggling to keep its economy afloat? Analysing the new budget that the government unveiled in 2020, this study concludes with a note that instead of effectively implementing the plans and policies directed by the budget, Nepal is unnecessarily engaged in political mess and is needlessly being dragged into the geopolitical complications.

Introduction

In July 2020, Nepal rose up to a ‘lower-middle-income’ country from a ‘low-income’ country. According to the World Bank’s country classification by income-level report, Nepal’s gross national income (GNI) per capita rose to US$1,090 in 2019, exceeding the required threshold of US$1,036. In 2018, Nepal’s GNI was US$960 (Prasain, 2020, July 3). It came as good news for Nepal, whose economy has not remained unscathed from the impact of the global pandemic. Still, as per the same study, economists believe that it would be short lived, and Nepal is likely to fall back to the status of low-income country because of the high level of unemployment riveting the Himalayan country (2020) and also because factors such as economic growth, inflation, exchange rates and population growth influence GNI per capita (Serajjudin & Hamadeh, 2020). Also, as the foreign direct investment (FDI) is dwindling and foreign aid and the inflow of remittance are projected to decline, this article aims to assess the impact of COVID-19 pandemic on the Nepali economy. As the economies of the major industrialized countries are severely affected, it is obvious that the flow of foreign aid and FDI from the developed countries to the developing and underdeveloped countries will be affected. FDI source countries for Nepal include India, China, Singapore, Bangladesh South Korea (Nepal Rastra Bank, 2018) and the European Union (EU) member countries, and the USA, which shows that FDI flows to Nepal is not only from the developed countries but also from the developing countries (Adhikari, n.a.). But, today, while both the worlds are severely impacted, economically, Nepal’s reliance on FDI may be hazardous amidst the spread of COVID-19. Similarly, remittances have been a major source to economically stabilize post-conflict societies in Nepal. But, today, while the oil economies in the Gulf region have faced crisis as the price of oil has plummeted, and migrant workers hailing from the developing and underdeveloped countries like Nepal have been repatriated, it has severely impacted the remittance-driven economies like Nepal.

Governments in different parts of the world have perceptively failed in their endeavours to downsize the explicit impacts of the economic crisis, prompted by the onset of the COVID-19 pandemic. Also, the conventional forms of reciprocity and interdependence are affected, foregrounding the larger probability of the ‘reversion’ of the entire process of globalization. And, amid the prophesized decline in the faith in democracy, it has become quite clear that the ongoing global pandemic has shaken the roots of global political economy. While predictions are being made on how this could set a course for a new structural change in the global political economy, joint responses and effective exit plans for the economic recovery seem to be missing from the side of the governments (OECD, 2020). Mere calculations are being drawn, estimating the impact the global pandemic has on the global economy. Although the overall analysis of the impact of the pandemic on the global economy can be made, only after the dust settles, the International Monetary Fund (IMF) in the middle of April had estimated that the global economy will contract by 3% in 2020 (Winck, 2020). But the IMF’s June report projected global growth at –4.9%, which was 1.9 percentage points lower than the April forecast. In 2021, the global growth, according to the IMF’s June report, is projected at 5.4%, leaving 2021 gross domestic product (GDP) some 6.5 percentage points lower than in the pre-COVID-19 projections of January 2020. The impact on low-income households of the developing and least developed countries is more adverse, jeopardizing the series of achievements in combating poverty and underdevelopment in the world since the 1990s (IMF, June 2020). Recent projections of the World Bank are even more gruesome. As per its latest Global Economic Prospects report that came out on 8 June, the pandemic is set to shrink the global economy by 5.2% (World Bank, June 2020). In its ominously titled report ‘the downside scenario’ predictions are marked at 8%, which is much higher than the IMF predictions. This comes as the biggest economic hit since World War II (Putz, 2020) as ‘per capita incomes in the emerging market and developing economies (EMDEs) are likely to shrink this year, sliding millions back into poverty’ (World Bank, June 2020). Two of the most powerful economies are expected to be hit hard. The US economy is expected to contract by 5.9% this year and unemployment to rise by 10.4%, while China will witness the lowest economic growth rate since 1976, with estimates of the economy expanding by just 1.2% this year (Chan, 2020). For the Fiscal Year 2020, India’s economy will contract by 3.2%, owing to the COVID-19 pandemic and the multi-phased lockdown (The Times of India, 2020). These three countries are Nepal’s major development partners and important foreign aid providers. According to the Ministry of Labor, Employment and Social Security of Nepal, remittance makes up to more than 25% of the country’s GDP (2020), but dropping oil prices that have hit the Gulf Cooperation Council (GCC) economies have resulted into job cut and loss of employment as more than 80% of the labour migrants from Nepal are GCC and Malaysia bound (Mandal, 2019). Owing to the same, this article aims to appraise the impact of the global pandemic on the inflows of remittance, FDI and foreign aid to Nepal. Here, the Himalayan country represents all those countries, where lower middle class are dependent on remittances, and infrastructure development is driven by foreign aid and FDI. Defining the characteristics of low-income and middle-income countries, Section I discusses the impact of pandemic on low-income and middle-income countries. Section II discusses the responses of low-income and middle-income countries in containing the impact of COVID on their economies are outlined. Section III, taking Nepal as the representative state, discusses the impact of the pandemic on globalization and its repercussion on Nepal as a low-income country is highlighted. Section IV discusses the impact of COVID-19 on the inflow of remittance, FDI and foreign aid to Nepal is explained. Finally, in Section V conclusion is drawn from how political problems and geopolitical implications riveting Nepal have procrastinated the implementation of new plans and programmes pledged by the new budget, eventually aggravating the economic crisis.

Defining Low-Income and Middle-Income Countries

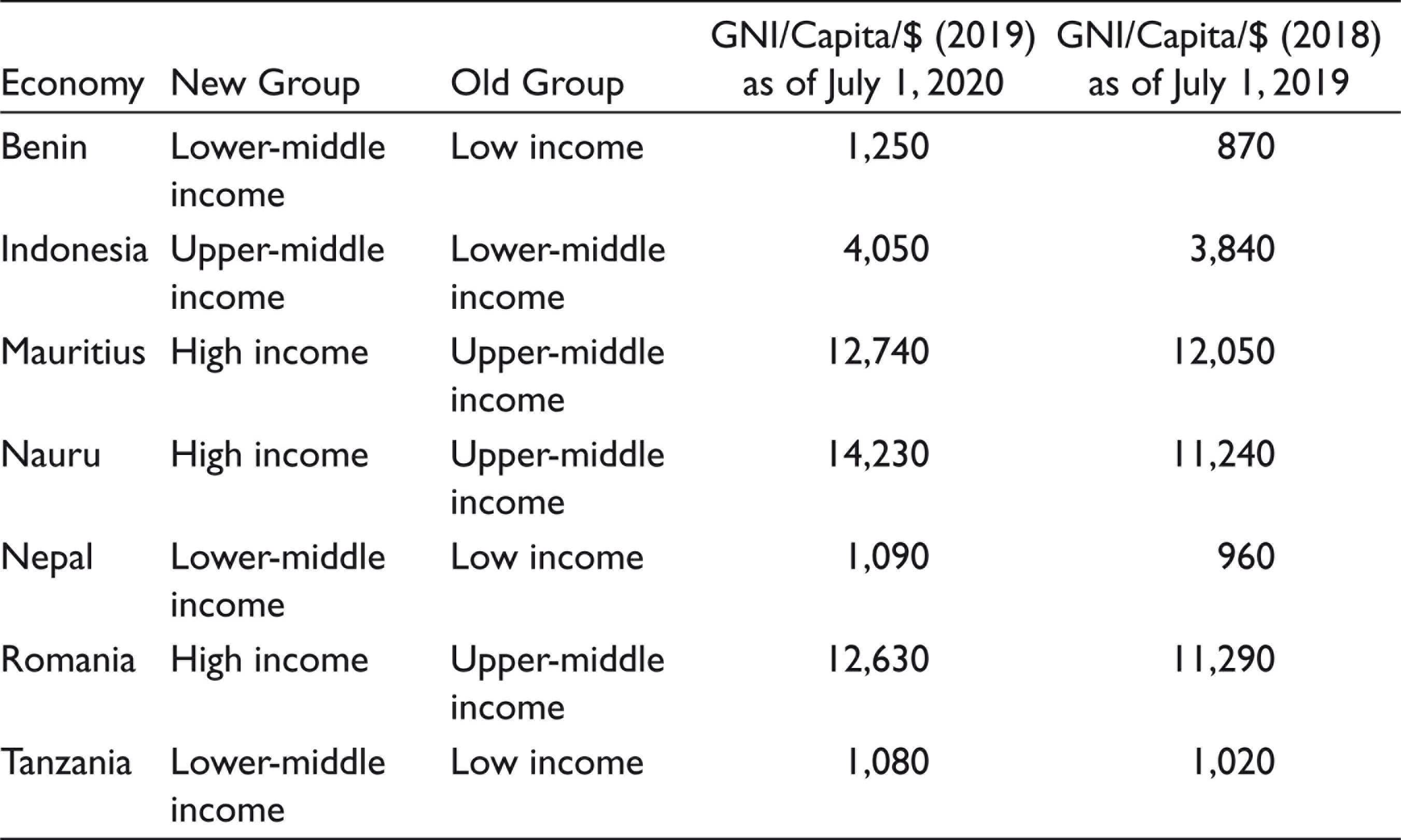

The World Bank has classified the world’s economies into four income groups, which are low-income, lower-middle-income, upper-middle-income and high-income countries. The classifications are based on GNI per capita (Serajjudin & Hamadeh, 2020), which is the country’s annual income divided by population. According to the World Bank, countries with a GNI per capita of US$12,535 are considered high income, while upper-middle-income status countries have a GNI per capita of US$4,046 –12,535. Similarly, the lower-middle-income category includes countries with a GNI per capita of US$1,036–4,045, and countries with a GNI per capita of less than US$1,036 are considered low-income countries (2020). Factors including economic growth, exchange rates, inflation and population growth influence the GNI per capita in each country. But, in order to keep the income classification thresholds fixed in real terms, the World Bank study states that they are attuned annually for inflation (World Bank, April 2, 2020). The new threshold has been mentioned in Table 1.

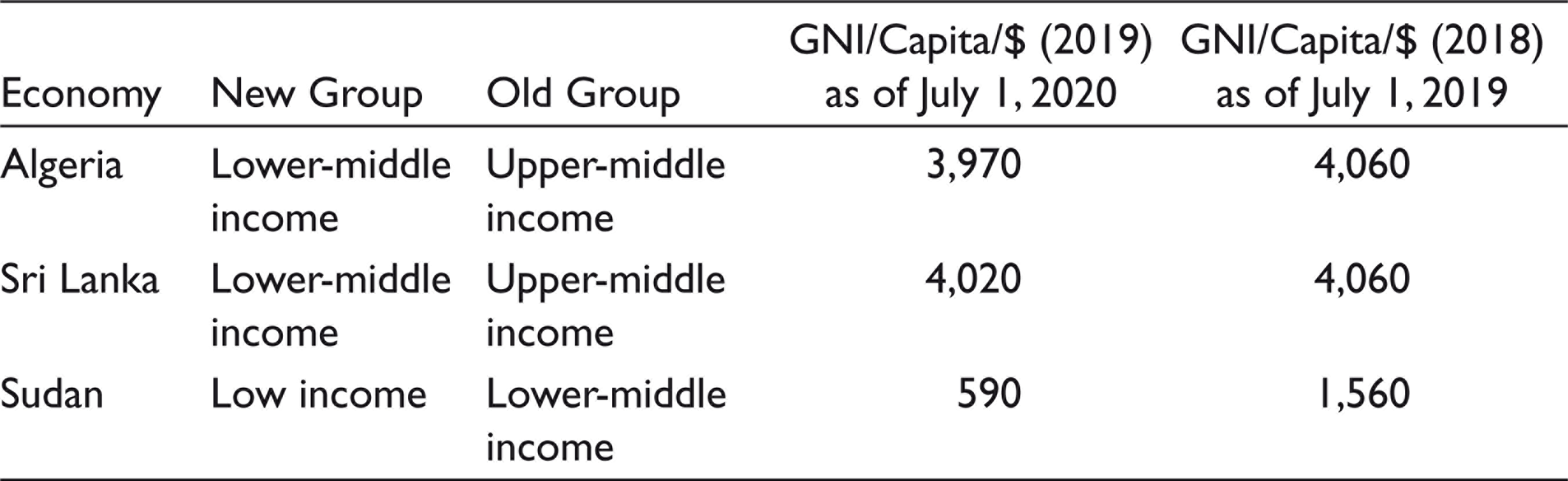

Updated each year on 1 July, the GNI numbers that are used for this year’s classification do not yet reflect the impact of COVID-19. Therefore, economists have been claiming that with the economic recession, and a high level of unemployment in the wake of COVID-19, the countries that have shown improvement in their financial situation are likely to return to the erstwhile status. Table 2 and Table 3 list out the economies moving to the higher category and lower category, respectively. In the Nepalese context, the sharp falls in exports and remittance inflows, which have already upended the country’s economy as the upshot of the existing crisis triggered by the global pandemic, and as incomes at home and abroad are expected to fall sharply, Nepal is also likely to return to the status of low-income country (Prasain, July 3, 2020). World Bank’s Global Economic Prospects, made public in June 2020, has already estimated Nepal’s economic growth to fall to 1.8%, while, for the next fiscal year, the bank has projected Nepal’s growth to 2.1% (ibid).

World Bank’s New Country Classifications by Income Level (2020) Comparing with the Previous Thresholds (2019)

World Bank’s New Country Classifications by Income Level (2020) Comparing with the Previous Thresholds (2019)

Economies Moving to Higher Category (New Group) as of July 1, 2020 from the July 1, 2019 (Old Group) Category

Economies Moving to Lower Category (New Group) as of July 1, 2020 from the July 1, 2019 (Old Group) Category

Low-income and middle-income countries have closed their national borders and imposed travel restrictions to contain the spread of the virus. The protracted lockdown has already weakened their economies. Markets have not fully opened. Public transportation is yet to resume fully. Industrialization, manufacturing of goods and trade have been severely affected. Because of the travel restrictions and uncertainty of the resumption of the international flights, foreign employment is impacted. In the remittance-driven economies, repatriation of the migrant workers has further aggravated the problem. Different international financial institutions have been doling out support to these countries with an aim to stabilize their economies. The IMF has provided emergency financial assistance and debt relief to different low-income and middle-income countries. The Executive Board of the IMF approved US$ 121.1 million in emergency assistance to the Kyrgyz Republic, US$739 million disbursement to Kenya, US$214 million disbursement to Nepal and US$65.6 million in disbursements to Dominica, Grenada and St. Lucia to address the COVID-19 pandemic (IMF, April 9, 2020). Also, the World Bank announced, in March, a financial package, providing grants and low-interest loans from the International Development Agency (IDA) for low-income countries and loans from International Bank for Reconstruction and Development (IBRD) for middle-income countries, using all of the Bank’s operational instruments with processing accelerated on a fast-track basis (World Bank, April 2, 2020). Meanwhile, the United Nations (UN) Secretary-General also established a dedicated COVID-19 Response and Recovery Fund to support efforts in low- and middle-income countries (UNODC, 2020). Besides, the pre-existing problems of poverty, insecurity, weak governance and fragile infrastructure in low- and middle-income countries (UNDP, 2020) have made it further difficult for these countries to effectively implement its economic recovery plan. Provided the unprecedented challenges posed by COVID-19, the World Bank Group aims to deploy up to US$160 billion over the next 15 months, starting from April, to help countries protect the poor and vulnerable, support businesses and boost up economic recovery. In addition to the projects of the World Bank (March 3, 2020), the emergency financing also includes US$8 billion from the International Finance Corporation (IFC), to support the private sector cope with the impact of pandemic, to keep the companies solvent in saving jobs and limiting the economic damage.

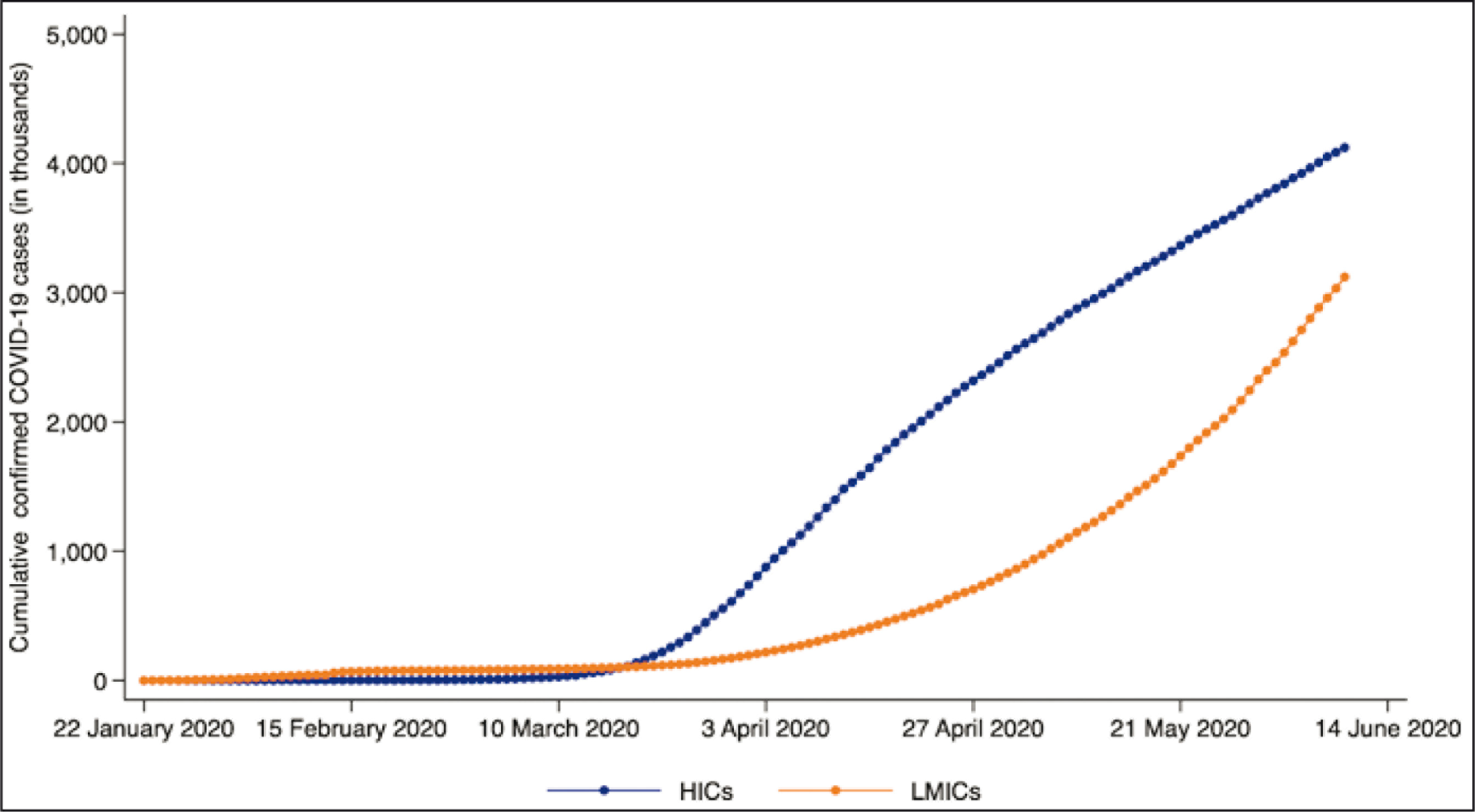

Unlike the early months of the pandemic, when most cases of infection and deaths due to COVID-19 occurred in high-income countries, they have surged up in the low- and middle-income countries too. Figure 1 presents the data over the same from the Johns Hopkins University Center for Systems Science and Engineering (CSSE) are illustrated. It argued that insufficient testing could have led to an underestimation of true infections in those countries. In Figure 1, HICs mean high-income countries while LMICs mean low- and middle-income countries (Gupta et al., 2020).

Because of more infection and deaths, they are still not prepared for a full-fledged resumption of markets, transportation, entrepreneurship, businesses and commercial activities, crippling the national economy. Although a crippling economy obligated India to ease the lockdown, the largest democracy has faced a surge in the cases. Mumbai, the financial capital; New Delhi, the national capital; and Ahmedabad, a hub of trade, commerce and industry have been badly hit by the pandemic (Kazmin, 2020). In the South Asian context, the World Bank’s (April 11, 2020) regional review on South Asia projects that the regional growth is expected to fall to a range between 1.8% and 2.8% in 2020, down from a 6.3% growth projected before the crisis. The deteriorated forecast is also likely to linger into the year 2021, with growth projected to hover between 3.1% and 4.0%. Since 2016, Nepal, the South Asian economy, was attempting to rebuild its fractured economy, and the country had aimed to achieve a target growth of 9.6% before the pandemic. But the pandemic did not let it happen (Budhathoki, 2020). Now, with the drop in the inflow of remittance, FDI and foreign aid, Nepal’s economy may further sink.

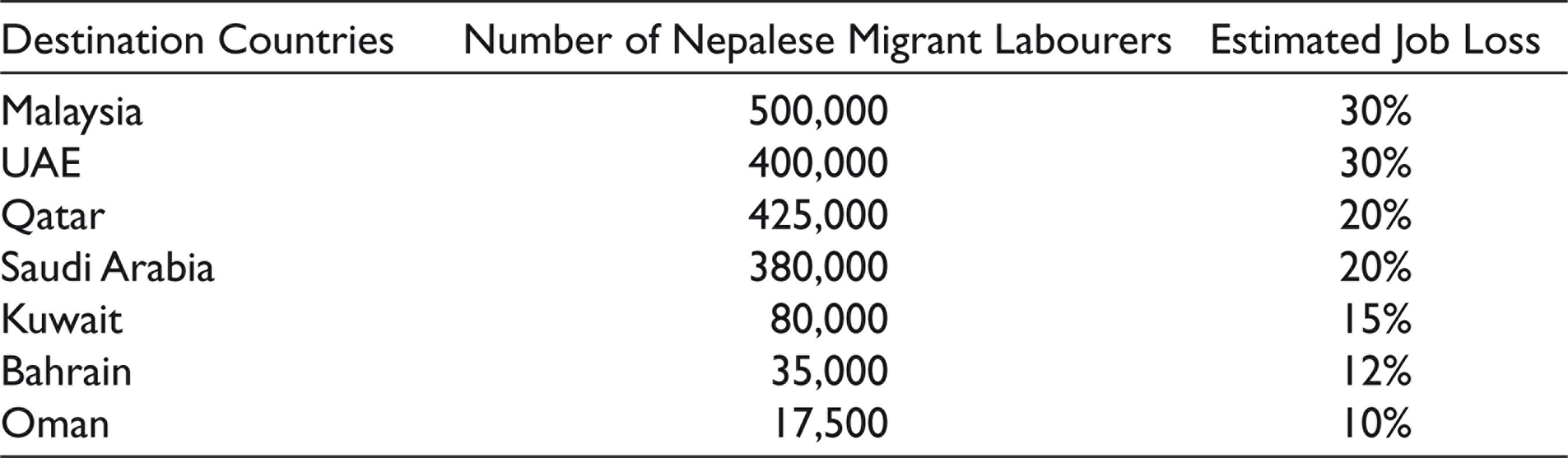

Remittance income has played a vital role in the economic development of Nepal. According to the yearly migration review by the Ministry of Labour Employment and Social Security (2020), Nepal issued over 4 million labour permits for the Nepalese who were seeking to migrate for foreign employment in the past decade with 3,888,035 males and 211,891 females. Nepal received US$8.79 billion in the Fiscal Year 2018–2019, which accounted for 28% of GDP for that year. Other than India, the top destinations for Nepalese migrant workers are Qatar, Malaysia, Saudi Arabia, the United Arab Emirates (UAE) and Kuwait (Mandal, 2018). According to a joint report by the Nepal Labour Force Survey (NLFS) 2017–2018 and International Labour Organization, there are approximately 3.2 million migrants abroad, including those who migrated for work, education or other reasons. The same study estimate suggests that over 37% of the total Nepalese migrants are in India (2019). Because of the pandemic, millions of workers have lost their work, income and faced reduction of salary, as businesses and economic sectors, especially smaller enterprises, have been severely affected. The pandemic has already affected almost 2.7 billion workers, representing approximately 81% of the world’s workforce (ILO, September 23, 2020). In March 2020, the UN’s International Labour Organization stated that because of COVID-19, some 25 million jobs may be lost, and migrant workers are likely to be extremely affected (ILO, March 18, 2020); further worsening inequality between the world’s richest and the poorest (Gu, 2020). According to the Nepal Association of Foreign Employment Agencies, the global COVID-19 pandemic has taken away the Nepalese migrant workers’ jobs in the Persian Gulf and Malaysia, which are Nepal’s top labour destination countries. A total of 10–30% of jobs held by the Nepalese in Malaysia and the Gulf are gone, affecting their lives and livelihood. Being penniless, they are stranded and are waiting for the Nepal government to take them home. About 20%–25% of the estimated 3 million Nepalese workers abroad are likely to return home, mainly because of two reasons: first, the work tenure of about 60 %of the Nepalese workers is over and, second, a large number of workers have lost their jobs due to the pandemic (Mandal, May 21, 2020). There are also the cases of Nepalese migrant workers not being paid, even in the time of the pandemic. Hundreds of Nepalese migrant workers went on a strike in the UAE after their employers did not pay them salaries for over 2 months. About 500 workers terminated their work at an oil and gas company in Ruwais, Abu Dhabi, protesting against their employer for not paying them (Mandal, September 23, 2020).

2019 Data of Nepalese Migrant Workers to Major Destination Countries, Juxtaposed with Estimated Job Loss Triggered by Covid-19

2019 Data of Nepalese Migrant Workers to Major Destination Countries, Juxtaposed with Estimated Job Loss Triggered by Covid-19

Moreover, the COVID-19 pandemic has foiled the processes to apply for and get residence and work permits, as government offices are either closed or have reduced their services (European Commission, 2020) . Even the post-COVID-19 world may possibly introduce a manufactured crisis, playing on the distrust and fears of the receiving state, severely influencing the output of the migration industry and propelling safe and orderly migration into irregular pathways (Yayboke, 2020). Approximately 127,000 Nepalese migrant workers, whose contract terms are over, and stranded without jobs, and those who have applied for general amnesty in the country where they are working, are anticipated to return home immediately, after the travel restrictions are lifted. Also, about 500,000 Nepalese workers are likely to return home due to the COVID-19 pandemic (Giri, 2020).

While migrant workers have been the engine of the globalized economy, the inability of labour to move efficiently will undeniably impact the remittance economies like Nepal, wherein societies are heavily dependent on remittances from migrant workers. But with the impact of the global pandemic (COVID-19), the sources of income for families across the developing world are affected (Yayboke, 2020). According to the UN, ‘[migrants] and their families are often part of marginalized and vulnerable groups that are already experiencing economic hardship as a result of containment measures’. Before the pandemic struck the oil economies—the major destination countries for Nepalese migrant workers—remittance always had a positive impact on the Nepalese economy through savings, investments, consumption, growth and reduced poverty and income distribution.32 But with the pandemic, and decline in inflow of remittance to Nepal, the economy of the Himalayan country is likely to face economic crisis. The World Bank’s Migration Brief states that global remittances are expected to fall by about 20% to US$445 billion in 2020 from US$554 billion in 2019 because of the economic crisis brought about by the COVID-19 pandemic. In the rural areas of Nepal, remittances have been the backbone of rural families and uplifted them out of poverty, particularly through investment in critical sectors, including education, health and land. Also, remittance in Nepal has a positive impact on government revenue, and it has also helped to increase liquidity in the banking system. But, since the pandemic, these sectors in Nepal have been facing a severe crisis.

Remittances proved to be of invaluable support whenever Nepal confronted a crisis in the past. Remittances have helped disaster relief, following the 2015 earthquake that struck Nepal. But, in the present context, the migrant workers themselves are being repatriated, owing to the job loss triggered by the pandemic. According to the World Bank, remittances to Nepal are expected to fall by 14% in 2020, as thousands of Nepalese migrants who work in the oil-rich Gulf countries and Malaysia have been laid off, and the never-ending pandemic may force the remaining workers to return home. The income from remittances totalled US$8.1 billion last year, which is more than a quarter of Nepal’s GDP (Prasain, July 3, 2020). In 2019, remittances had contributed 27.3% to the country’s GDP. A large number of migrant workers have already returned to their villages and are unable to return because of the lockdown and uncertainty about the resumption of international flights. Consequently, Nepal will lose the urgently required hard currency. Unemployment will rise, and many households may fall below the poverty line. Unlike the impact of the global financial crisis of 2008, when remittances had recovered quickly, it has been more severe this time. With oil prices at unusually low levels, employment opportunities in the oil economies of GCC countries have been affected. While even India, a perpetual choice for the Nepalese migrant workers, is affected by the economic slowdown, Nepal’s economy has started to suffer, with uncertainty and not knowing how long the crisis will remain (Pant, 2020).

Impact of COVID19 on the Inflow of FDI to Nepal

With the unprecedented impact on globalization, the COVID-19 pandemic has negatively impacted the inflows of FDIs in developing and underdeveloped countries. A study carried out by the UN Conference on Trade and Development (UNCTAD) indicates that global FDI flows are expected to contract between 30% and 40% from 2020 to 2021. Amid such a contraction in global FDI, developing and underdeveloped countries will be hit the hardest, as the FDI inflows are going to drop when they need it the most. Such a drop has been triggered by the disruption in global supply chains, as the result of the pandemic (Seric & Hauge, 2020).

Nepal’s twin goals of becoming a middle-income country and meeting the Sustainable Development Goals (SDG) by 2030 have been challenged by the impact of COVID-19 on the inflow of FDI to Nepal. With Nepal already facing a financial crunch before the outbreak of COVID-19, the COVID-19 pandemic has further worsened the situation. In June 2019, the National Planning Commission (NPC), the apex body that frames the country’s development plans and programmes, projected that Nepal will face a financing gap of US$4.96 billion per year to meet the SDGs (The Himalayan Times, 2019). Even though Nepal hosted the third Nepal Investment Summit in 2019, and 15 memorandums of understanding (MoUs) were inked with investors from different countries, fewer outcomes surpassed the commitments. Thus, amid such an unfavourable situation, further exacerbated by the global pandemic, no initiatives have been undertaken to revive the FDI. While unveiling the budget for the Fiscal Year 2020–2021 in May, Finance Minister Yubaraj Khatiwada merely stated that US$12.19 billion in FDI has been pledged through the Investment Board, Nepal (The Himalayan Times, 2020). He did not elaborate on the areas that could attract foreign investors because the goal to achieve the SDGs by 2030, the required investment, estimated before the COVID-19 pandemic, stood at US$17.202, 024.8 billion. It was approximately 47.8% of the GDP. Of the total investment requirement, poverty accounts for 7.5%, while inclusive growth (mainly labour and tourism), agriculture, health, education and gender account for 2.8%, 5.8%, 6.6%, 15.5% and 0.7%, respectively (The Himalayan Times, 2019). Thus, already before the pandemic struck, a realization was developed that the government needs to work on assorted macroeconomic policies, and make them more investment-friendly, and should leave no stone unturned to win the confidence of investors. As a result, before the pandemic, FDI pledges had increased by 315.3% to US$1.61 billion, and most of the foreign investment commitments were from China (Shrestha, March 15, 2020). But, the impact of the pandemic may delay them further. Since the outbreak of the COVID-19 pandemic, the Department of Industry, which is responsible for registering industries including those with foreign investments, has not received even a single foreign investment application (Shrestha, March 15, 2020). In addition, if Nepal fails to endorse the Millennium Challenge Corporation (MCC) grant from the USA, consisting of US$500 million to the energy sector and US$130 million to roads sector, it will definitely have a negative impact on the endeavours to bring more FDI from the developed countries. It may send a bad message to the investors that the investment climate in Nepal has not been favourable yet. It cannot be denied that Nepal’s FDI process is slow and ineffective. Usually, approvals consume more time. But, at present, while the need for capital is urgent, Nepal must opt for an automatic route for foreign investment, so that jobs would not be lost before the foreign capital comes to the bank. Gocher (2020) reports that the investment opportunities brought about by the pandemic in the health sector, online shopping and payment systems also cannot be ignored.

Impact of COVID-19 on the Inflow of Foreign Aid to Nepal

With the pandemic ravaging the global economy and emptying the coffers of the aid disbursing countries, Nepal will definitely see a reduction in foreign aid. Nepal had received a foreign aid of US$1.79 billion from multilateral and bilateral donors, and INGOs from 2018–2019. Of the total share, bilateral donors accounted for 60% of the foreign aid to Nepal (Shrestha, April 1, 2020). But, now, with almost all the bilateral donors, including the USA, Europe and China, bracing for a recession, foreign aid for Nepal is expected to shrink, particularly China-led Belt and Road Initiatives (BRI) projects (Bhattarai, 2020). But to what extent it will fall depends on how much impact the pandemic has on the aid-providing countries and how these countries act on their moral responsibility towards the low-income countries. Regarding BRI, because of the pandemic and its fragile economy, Nepal may not be in a position to take loans from China to finance the BRI projects, while China itself is also not in a position to give grants to BRI projects in Nepal (Bhattarai, 2020). Although the UN had set a target for the developed countries in 1970 to contribute 0.7% of their GDP to the poor countries, as development assistance, only few countries have met the target. Now, they have the pandemic to further excuse themselves from contributions. In addition, as UN is unwilling to lose its influence in Nepal, there are chances that some of the traditional development partners may not cut their aid to Nepal. Nepal gets bilateral aid mostly for infrastructure development and capacity building; if the aid doled out for infrastructure are cut, development efforts will be severely impacted. Aid cuts on capacity building will have a severe impact on Nepal’s governance, transparency and accountability.

Multilateral donors had committed funds before the pandemic for a period of 3–5 years. Hence, the foreign aid coming from multilateral donors may not be much affected in comparison to the funding from the bilateral donors. For instance, On 10 June 2020, the World Bank approved a US$450 million ‘Nepal Strategic Road Connectivity and Trade Improvement Project’ to financially assist Nepal in improving its roads and set the course for post-COVID-19 economic recovery through regional road connectivity, cross-border trade, new job creations and better road safety (World Bank, June 10, 2020). The project is expected to enhance road connectivity by improving the Nagdhunga–Naubise–Mugling Road and upgrading Kamala–Dhalkebar–Pathlaiya Road for Nepal’s connectivity and trade with India and other countries (2020). Although Nepal may not lose the foreign aid from the multilateral donors, it may not be enough for the development efforts. Because of the drop in aid receipts, the government has fallen short of meeting its revenue collection targets.

In addition, a sharp decline in aid from INGOs is projected, as the Ministry of Finance has already stated that aid pledges from INGOs for 2020–2021 are around 13% less than their pledges for 2019–2020. They have pledged US$183.41million for 2020–2021. For 2019–2020, their pledges stood at US$210.302 million. In Nepal, most of the INGO focus on sanitation, education and heath, through advocacy and service delivery programmes, in order to raise awareness and strengthen accountability at the local, provincial and federal levels (Shrestha, July 3, 2020). There is also the prospect of international aid from INGOs getting reoriented towards health sectors (ibid). In 2018–2019, INGOs disbursed US$215 million to various projects in Nepal, which was almost double of what they had spent—US$110 million—in the previous fiscal year (ibid). But, as global pandemic has plunged the global economy into the gravest recession since the Great Depression, the disbursement of many INGOs have also plummeted. For instance, Britain has already decided to merge its foreign and commonwealth office and the Department for International Development (DfiD), the latter being the major contributor to the INGOs (ibid). The repercussions of economies of major Eastern and Western development partners have plunged dangerously low, leaving this Himalayan country with no promises in foreign aid at least until these countries stabilize their economies. However, it is also observed that Nepal and similar low-income economies have to structure their investment environment as well as policies to attract FDIs according to the new dynamics that will guide the economies post the pandemic. This also applies to setting their priorities accordingly.

Political and Geopolitical Implications Aggravating Crisis

Despite the sharp fall in the inflow of remittances, FDI and foreign aid to Nepal, severely impacting Nepal’s lower-income and middle-income households, industrial activities, banking sectors and development activities, political stakeholders are not much concerned about addressing the larger impacts at the socio-economic fronts, triggered by the economic downfall. Owing to the travel restriction that was followed scrupulously till August 2020 and some restrictions still in place, uncertainty about the resumption of the international flights for tourists and hotel bookings hitting a record low, the tourism sector has come to a halt. The Nepal government put off Visit Nepal 2020 and cancelled all climbing expedition permits (Aryal, 2020) for nearly 5 months, fearing the spread of the COVID-19 pandemic. The country lost its revenue from the spring climbing season when the government banned all expeditions in March. When the ban was lifted on 21 July, it raised hopes across the sector as the autumn climbing season starts in September and lasts till November (Lama, 2020). With only two expeditions currently in progress, the government has issued new guidelines for tourists arriving for mountain expeditions, which is set to open for foreigners only around mid-October. However, the tourism industry is wary of the government’s lack of recovery plan and unprepared decision-making, leading to ambiguity among the tourism operators and leaving the entire economy dependent on tourism in limbo (Prasain, September 2, 2020). Unfortunately, the implementation of new plans and programmes pledged by the new budget has not gained momentum, owing to the political problems caused by the power struggle inside the ruling communist party and geopolitical implications triggered by the new map row between Nepal and India. Such unnecessary engagements have further aggravated the economic crisis deepening in Nepal.

Also, as the stranded migrants from GCC and Malaysia are being repatriated, and while the thousands of migrant workers from India have already started going back to Nepal, providing jobs and opportunities to them in Nepal is a Herculean task, unless a risk-managing and risk-minimizing development policies are introduced. Centred on the creation of new jobs, Finance Minister Khatiwada’s budget speech for the Fiscal Year 2020–2021 mentioned about government allocating budget to repatriate the Nepalese migrant workers and creating new jobs for them through the Prime Minister’s Employment Programme, Poverty Alleviation Fund, through the establishment of Employment Service Centre at the local levels, by imparting skills and trainings at the provincial levels, promoting collective farming and setting up land bank to promote agriculture. Although the budget appears encouraging in job creations and employment opportunities to the returnees, it has clearly failed to do so, and migrant workers are travelling back to India as their savings have dwindled and the promise of local employment has proved to be a fallacy. The sentiments are similar among those who have been repatriated from other destination countries as well (Khadka, 2020). Although plans and policies are in place, the problems lie in the institutional capability of implementing them. While the country was mired in challenges facing different sectors, including public health, employment, education, transportation, agriculture, trade, investment, tourism among others, the pandemic had also provided an opportunity for the ruling communist government to initiate socialist reforms as enshrined in the constitution. To combat the threats emanating from the pandemic, the leftist government was actually anticipated to come up with the budget for the Fiscal Year 2020–2021. But, even though daily wage labourers, small and medium enterprises, corporate houses and several informal sectors are struggling, no bold reform agendas were introduced in health, education and agricultural sectors. Although the Prime Minister Employment Programme (PMEP) and Prime Minister Agriculture Modernization Project (PMAMP) are still believed to be most promising, government policies and programmes have not been able to internalize the approach: whether to continue with neoliberal behaviour or pursue the socialist goals, as directed in Nepal’s new constitution. The economic issues have been almost suspended by political manoeuvring and geopolitical ambitions. Although the government’s plans initially included casting a social safety net to help the vulnerable class who have lost their jobs and any other sources of income, generating new jobs and reviving agriculture and prioritizing cash crops, they have not been implemented. Economic concerns, especially stabilizing the dwindling economy left in the wake of a global pandemic, have taken a backseat while the nation is desperately pushing itself towards a geopolitical quagmire. Actions and policies required to deal with the economic crisis have not been seriously drawn, and the few in place lack efficient implementation. The power tussle has overshadowed the issues of national priority at the moment. Active public health response has been compromised, which may lead to additional economic burden.

This article has attempted to explain the impact of the decline of the inflow of remittances, FDIs and foreign aid, during the global pandemic, to lower-income countries like Nepal. It has been observed that while protracted lockdown has already taken a toll on the lower- and middle-income countries, the sharp decline of remittance, FDI and foreign aid has pushed the economies further in crisis. Despite the grave economic crises looming large over the Himalayan nation, the entire country has been held hostage by the power struggle in the ruling party, undermining government capacity to deal with the economic downfall, when it should be focused in making collective efforts to address the economic crisis through the implementation of required containment policies and strategic reopening of the economy. The government has not been able to assess the opportunities and challenges brought by the repatriation of the large number of migrant workers who have lost their overseas employment. Even though it has been argued by the development thinkers and planners that multilateral aid would not decline in comparison to the bilateral aid, Nepal has not made any policy-level preparations to attract more multilateral aid for the economic recovery.

From the very beginning, Nepal’s recovery plan seems to have lacked the strategic direction. Already, Nepalese policymakers have missed an opportunity to transform the crisis into opportunity. Crisis resilience should have been the policy priority of Nepal, preliminarily addressing the informal economy and its linkage with the vulnerability of workers during the lockdown. Same applies to Nepal’s foreign employment. But because of the ruling party’s misplaced priorities, the economic recovery plan of the Himalayan country lacks a strategic coherence, upsetting already fractured sectors, including tourism, agriculture, remittance, FDIs and foreign aid. Thus, before it is too late, the Nepal government should mull over using the skill and technology of repatriated migrant workers on the productive sectors of the economy. Also, Nepal should introduce a concrete road map in attracting more FDI by improving the investment environment than being over-dependent on foreign aid. The investment commitment on the energy sector has increased recently, from the foreign investors, even during COVID-19. Thus, Nepal should leave no stone unturned in tapping such opportunities, which may eventually transform the crisis into opportunities.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.