Abstract

Ghana has gained international attention due to a controversial deal, which it has entered with the Chinese Sinohydro Corporation Limited. Sinohydro is investing $2 billion in infrastructure development, in return for refined bauxite over a 15-year period. When it comes to resource-backed loans between China and African governments, these types of cooperation are widely known as the Angola Model. Besides the criticism of resource-secured lending, in some African countries, these practices are declined, while in others it continues, but also evolve. For example in Guinea and in Ghana. This article takes a closer look at the structure and concerns regarding Ghana’s Sinohydro deal in comparison to the Angola Model. The main difference appears to be (a) the established para-state company charged with managing the extraction of bauxite and (b) the plans to develop an integrated bauxite–aluminum industry within Ghana. On the other side, environmental concerns regarding bypassing regulations or possible pollution remain the same.

Introduction

Over the last few years, trade between African countries and China has rapidly expanded, due in part to China’s fast-growing economy, which has led to an increasing demand for energy. By 2011, China had become the world’s largest energy consumer (Vasquez 2019), and in 2014, the country surpassed the US as the world’s largest oil importer and positioned itself as an alternative market. Due to low oil prices after 2008, African oil became available at competitive prices, and so China engaged increasingly more with oil-producing countries in the continent (Arriagada, Espinasa, and Baragwanath 2014; Dollar 2016). To take advantage of these opportunities, China used investment, lending and political agreements to expand its oil frontiers (Vasquez 2019), with its banks and major companies investing in selected countries in exchange for oil. The financial presence of China is exemplified in two major ways: (a) as foreign direct investments or (b) as loans in exchange for future payments in oil; for example, Angola and Sudan secured significant loans with oil. However, Brautigam and Hwang (2016) point out that of the five largest recipients of Chinese loans in the period 2000‒2014, only Angola and Sudan secured their loans based on oil, while Ethiopia used sesame seeds as collateral, the DRC used copper and Kenya secured a loan for building a railway against future revenues from rail traffic. Vasquez (2019) noted that certain voices framed these outcomes as an orchestrated policy by China (e.g. Kong and Gallagher 2017; Taylor 2006), while others played down these negative assumptions (e.g. Brautigam 2009; Economy and Levi 2014; Gonzalez Vicente 2013).

Nevertheless, trade and diplomatic relationships between African countries and China have rapidly expanded, as well as the discussion about so-called resource-for-infrastructure swap agreements. According to Singh (2019), resource-backed loans make up approximately one-third of China’s monetary advances to African nations. Brautigam and Gallagher (2014) name Angola, Congo-Brazzaville, the Democratic Republic of Congo, Equatorial Guinea, Ethiopia, Gabon, Ghana, Nigeria, Sudan and Zimbabwe as recipients of commodity-backed finance in Africa. This large-scale Chinese financing scheme has been widely known as the Angola Model (Foster et al. 2009), Angola Mode (Alves 2013) or China–Angola Investment Model (Begu et al. 2018). The Angola Model involves an exchange of natural resources for national infrastructure through direct investments by China in both mining (in the case of Angolan oil) and infrastructure, and it dates back to 2004 when Angola signed several financing packages with China for public investment projects. Mihalyi, Adam, and Hwang (2020) illustrate that the finance structure, also labelled the Angola Model, has become relatively commonplace in resource-rich countries in sub-Saharan Africa, Latin America and beyond. Lenders are mainly state-owned development banks from China. In general, these resource-for-infrastructure deals have been criticised for leading to certain economic as well as ecological risks for the host country. However, they are also recognised for the fact that they enable the financing and development of infrastructure, desperately needed by African countries. Habiyaremye (2016, n.d.) argues that Africa’s ability to sustain the high growth rates of its lion economies, in the long run, will depend on its capacity to mobilize the profits from the natural resource sector so that they can yield sufficiently large surpluses for investment in a modern manufacturing sector. Since resource-backed loans also come with challenges, Mihalyi, Adam, and Hwang (2020) reveal emerging new modes of financing, citing contracts in Brazil 2017, Guinea 2017 and the Sinohydro deal in Ghana 2018 as examples in this regard.

The latter is an agreement between the Sinohydro Corporation, a Chinese state-owned enterprise (SEO) specialising in infrastructure development, and the Government of Ghana. Sinohydro arranged loans to fund infrastructure projects, while Ghana uses revenue from refined bauxite to repay the loan. However, the bauxite–aluminum sector in Ghana is not particularly well developed, plans for extraction at the Atewa Forest Reserve (eastern region of the country) have gained international media attention (e.g. Washington Post 2019 or Oteng-Yeboah 2019). According to Johnston (2019), the Sinohydro deal is actually a step-around debt trap and not far away from the widely used Angola Model. Furthermore, in 2017, the Chinese Exim Bank called for a long-term, stable and sustainable financing mechanism and promoted government–private capital cooperation (Exim 2017).

Ghana’s Bauxite Industry

Ghana is rich in oil, gold, manganese, diamonds and bauxite; however, gold is currently the key resource for the country’s economy (Ayee et al. 2011), making it the largest producer in Africa. Over time, the country has managed to exploit its resources; however, for several reasons, this has returned little in sustained development value to the economy (Ayee et al. 2011). Despite the rich reserve base and Ghana being the third-largest producer of bauxite in the African continent (Knierzinger 2018), the raw material has only been mined at one site since 1942. Besides, its exports accounted for 0.6% of total minerals exports and 0.22% of total merchandise exports in 2014 (Oxford Business Group 2017). Ghana’s bauxite gained importance between World War I and World War II, and it played a major role in the Volta River Project, which included a hydroelectric dam, an aluminum smelter to process Ghanaian-mined bauxite, new cities, a deep-sea harbour and other infrastructural investments (Miescher 2014). The project, during the years of Ghana’s first President Kwame Nkrumah, became a symbol of sovereignty and promised an economically independent Ghana as a result of rapid industrialisation and reducing the country’s dependence on cocoa exports (Agbolosoo 1991). After the coup in 1966, Britain showed little interest in the development of a bauxite–aluminum industry, and bauxite production in recent years has fluctuated on account of the country’s inadequate railway system for transporting ore from the mine to the coast. After Western companies withdrew from the sector, Chinese investors took their place and began to revive the old vision. Following the plans posited by the First Republic of Ghana, the country’s bauxite deposits are to be further developed in terms of an integrated aluminum production strategy. The proceeds from this project will serve to finance many needs, such as infrastructure, electricity, schools and water supply, and realise, according to President Akufo-Addo, a Ghana Beyond Aid: My government is going to implement an alternative financing module to leverage our bauxite reserves, in particular, to finance major infrastructure program across Ghana. This will probably be the largest infrastructure program in Ghana’s history without any addition to Ghana’s debt stock (Akufo-Addo 2018, n.d.). However, currently, only two major actors are active in the bauxite–aluminum industry: the government, which holds a 100% share in the VALCO smelter at Tema and 20% stake in the Ghana Bauxite Company. As well as the Bosai Minerals Group, which holds the other 80% in the Ghana Bauxite Company, operating at the only bauxite mine in Ghana, namely Awaso (Figure 1).

Research Design and Methods

Mihalyi, Adam, and Hwang (2020, 2) argue that RBLs have become relatively commonplace in resource-rich countries in sub-Saharan Africa, Latin America and beyond. Meanwhile, the Sinohydro deal has been recently labelled as a new finance model and a promising alternative to the widely used Angola Model (e.g. Johnston 2019). This article elaborates on the differences between the Angola Model and Ghana’s Sinohydro deal and considers whether the deal offers a more promising model for Chinese investments in Africa.

I contend in this article that there are differences between the Sinohydro deal in Ghana and other resource-backed loans made by China, particularly highlighting (a) a privatisation shift and (b) the collateral itself; using refined bauxite, not raw bauxite, which enables Ghana to add value to their resource and may increase therefore the local economic impact. This deal illustrates a shift that may be becoming more visible, that is, the diversification of the Chinese finance mechanism.

Herein, I first expand on the Angola Model, its origins and operational characteristics, following which I provide a brief overview of resource-backed loans in the African continent. The first section ends by describing the shortcomings of the Angola Model. In the following section, I outline the origins and operational characteristics of Ghana’s Sinohydro deal. Thereafter, the deal in Guinea is briefly compared to the Sinohydro deal. Both loans were negotiated during the same period, and both with bauxite as collateral. Building on the mentioned shortcomings of the Angola Model, I discuss if and how the Sinohydro deal does things differently. A conclusion, as well as ongoing concerns and challenges, end the article.

Research for this article is based on the analysis of secondary and primary literature, including official government documents, press statements by NGOs or governments, presidential speeches and research reports on resource-backed loans and the environmental impacts of aluminum sector projects. During field trips in March 2019 and March 2020, additional material, such as Sinohydro deal documents, were collected. Relevant contacts were the local NGO A Rocha Ghana, Minerals Commission, VALCO and the Environmental Protection Agency (EPA). However, all relevant information used in this article is now published, which is why interviews are not included in this article. Information in sections entitled ‘Origins of the Sinohydro Deal’ and ‘Operational Characteristics’ on the Sinohydro deal can be found in the original documents. These were made available to me, but they have now been published on the Parliament of Ghana’s server.

The Angola Model

Origins of the Angola Model

In 2002, the Movimento Popular para a Libertac¸a˜o de Angola (MPLA) government in Angola was ready to rebuild the country after a 27-year civil war. The IMF offered loans to fund a large-scale infrastructure reconstruction program, albeit insisting that Angola had to achieve a healthier fiscal situation first, which implied cutting public expenditure, lowering inflation and increasing transparency. Angola’s government did not agree with these conditions and instead decided to negotiate with China. At that time, on the one hand, China’s export-oriented industries and manufacturing demanded more and more natural resources, especially oil (Burgos and Ear 2012). On the other hand, the commencement of war in the Middle East made it necessary for China to diversify its imports. In 2004, China’s Exim Bank offered the first loan to Angola (Corkin 2011), and both countries were able to secure their national interests using this strategic financial mechanism (Kiala 2010).

Brautigam and Hwang (2016) define two financing models: strategic partnerships with major Chinese companies and commodity-secured package finance. Strategic partnerships offer financial support to national champion firms, usually in the form of five-year plans, while commodity-secured packages offer individual project loans and a line of credit secured by resource exports. Zongwe (2010) argues that the Angola–China contracts are the first major example and archetypes of resource-for-infrastructure contracts between China and the African continent. An investment contract is distinguishable from a trade agreement. While a trade transaction characteristically consists of a one-off exchange of goods and money, an investment deal initiates a long-term relationship (Dolzer and Schreuer 2008). The World Bank, in its report entitled Building Bridges (Foster et al. 2009), first framed the term Angola Model, the fundamental assumption of which is that African Countries want China to invest in their infrastructure, and China needs to import Africa’s mineral and oil resources (Begu et al. 2018). Foster et al. (2009) point out that the China Exim Bank increasingly uses the Angola model for countries that cannot provide adequate financial guarantees to back their loan.

Operational Characteristics

When Angola negotiated with the IMF for loans in 2003, the government also received a counteroffer of a $2 billion advance from China’s Exim Bank. The deal came with an interest rate repayment of 1.5% over 17 years, including a grace period of 5 years (Corkin 2011). At first, 10,000 barrels per day of crude oil should be supplied, but later this should increase to 40,000 barrels per day (Taylor 2006). The Angola government has granted a licence to extract the resource to Chinese oil companies, which provide payment for the loans. Also, indicates the Angola Government the infrastructure projects to Chinese construction companies. Meanwhile, Chinese construction companies receive financial support from the Exim Bank, which holds the exclusive mandate to extend concessional loans that fall under the official development aid (ODA) category, albeit, in the case of Angola, they are extended on a more commercial basis (Alves 2013). The bank has been a key instrument in facilitating expanding economic cooperation between China and Angola. The Export–Import Bank of China is one of China’s three policy banks established in 1994 (the other two are the China Development Bank and the China Agricultural Development Bank), which remain tools of the government and allow Beijing to allocate preferential or targeted finance through a mix of planning and market means. Both the Exim Bank and the Development Bank are key instruments in China’s foreign economic policy and cooperation with Africa, with the former providing concessional finance and loans for infrastructure development in the majority of countries in the continent (Corkin 2011). In addition, loans are tied, because involved companies (usually construction businesses) are generally Chinese in origin. Furthermore, these Chinese companies carry out infrastructural projects and are reimbursed by the Exim Bank, which deducts construction expenses from the value of resources that African countries transfer to the Chinese government (Tan-Mullins, Mohan, and Power 2010). Vasquez (2019) stresses that the China Development Bank (CDB) and the Export–Import Bank of China (China Exim Bank) are mainly involved in lending money, but to a much lesser extent than commercial lending institutions. As part of the loan mechanism, the proceeds from the exported resources are deposited in an escrow account at a Chinese bank, which draw from it to repay the loan (Brautigam and Gallagher 2014).

Alves (2013) claims that the Angola Model is the product of a timely convergence of interests between China and African countries. On the one hand, China is home to many rapidly expanding industries, and on the other hand, African countries have infrastructural deficits. It is also important to point out that while the IMF or Western countries tend to be more careful about investments, China was ready to take a risk in Angola, a country that had recently stabilised after civil war. Landry (2018) highlights that risk calculations are an important aspect in determining the interest rates applied to development finance. Especially African countries in post-war circumstances had difficulties accessing the capital market but were rich in natural resources. Therefore, using natural resources as collateral to access sources of finance for investment came as a welcome solution. China loans were provided without political conditionality and at a much lower interest rate than any international financial institution might offer (Begu et al. 2018). This was also a more favourable deal for the African political elites (Konijn 2014). After all, the Angola Model made it possible to leverage natural resource wealth for infrastructure development. Additionally, Halland et al. (2014) claim that such finance models reduce the risk that revenues from resource extraction will be spent elsewhere, mismanaged or get other prioritisation. In some way, resource-backed loans’ inherent precommitment mechanisms may reduce such risks (Halland et al. 2014). Kabemba (2012) reported that the Congolese government failed to secure investments from Western countries and turned to China. Similarly to Angola, the money used for infrastructure did not go to the government, thereby enabling quick investment in infrastructure and preventing other types of political spending or mismanagement.

In the case of Angola, in 2004, a $2 billion loan from the Chinese Exim Bank was used to finance the reconstruction of infrastructure damaged during the nation’s long-lasting civil war (Konijn 2014). The Angola government now uses Chinese credit, backed by oil-based guarantees, to finance national infrastructure. In addition, Chinese companies are largely contracted to undertake projects and are paid directly by China Exim Bank. The loan is repayable at LIBOR plus 1.5% over 17 years, including a grace period of 5 years (Corkin 2011). Investments appear not as money that is directly transferred to the government of Angola; rather, in the case of Angola, a Chinese oil company provides payments for new loans to the Chinese Exim Bank, which in turn provides financial loans for infrastructure projects to a Chinese construction company. Therefore, instead of transferring funds to African governments, they are transferred directly to the companies undertaking the construction work (Corkin 2011). The aforementioned Chinese construction companies are selected by Exim Bank and the Chinese Ministry of Commerce and have to be approved by the African government (Thompson 2012). The Government of Angola prioritises the importance of certain infrastructure projects to the Chinese construction company and then grants a licence to the Chinese oil company to extract natural resources. The company then guarantees the repayment of the loan through the export of the natural resource. As long as China receives oil from Angola, the Exim Bank is willing to invest in the African country. At the same time, China is investing in many countries around the world, in order to be independent of Angola’s oil. In 2018, the Government of Angola announced it was moving beyond its heavy dependency on Chinese capital and diversifying its funding sources (Sato 2018).

Examples of Implementation

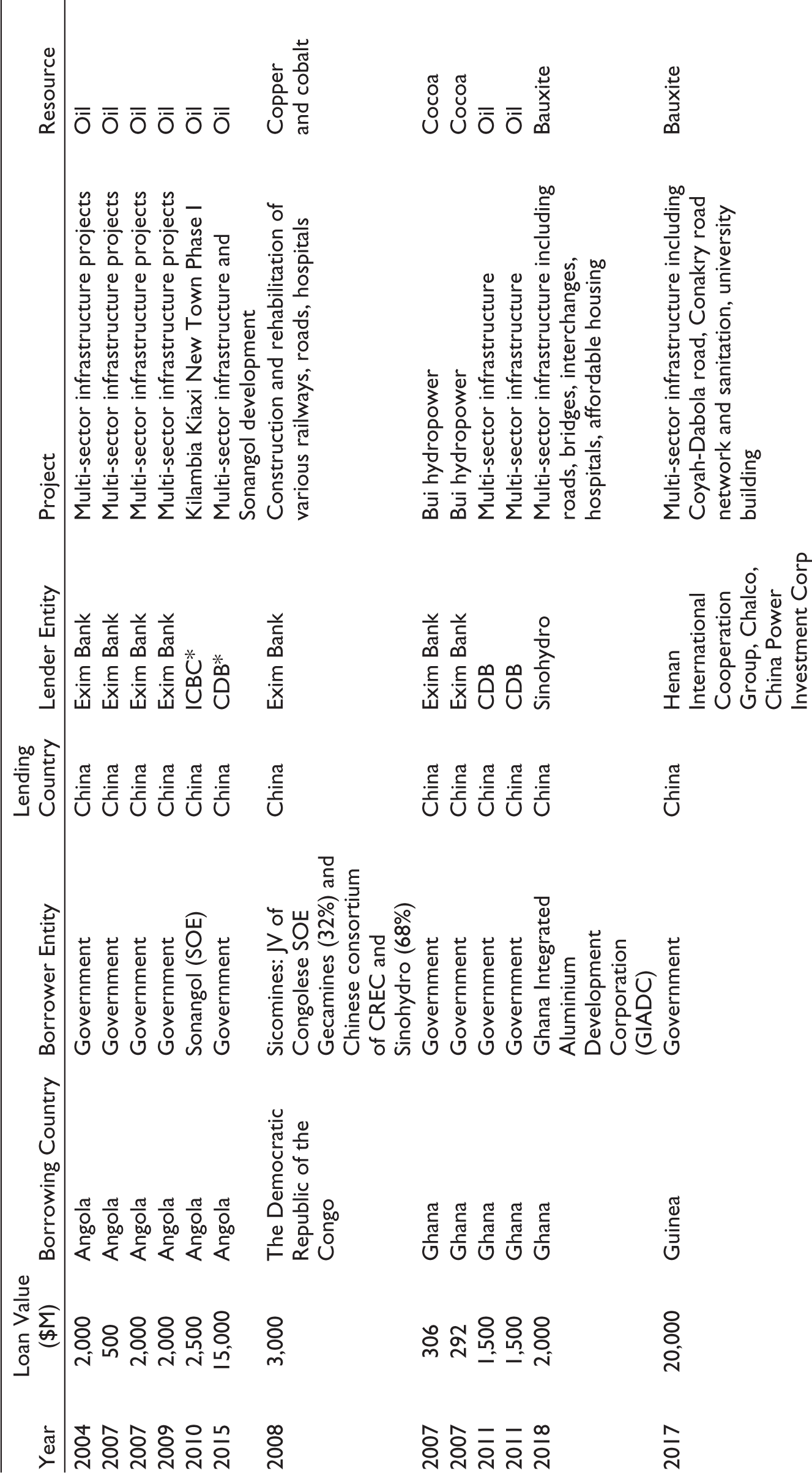

Chinese banks and companies began to lend a large amount of money to selected African (and Latin American) countries in exchange for their oil. The largest sectors financed by Chinese loans are transportation (US$24.2 billion), followed by energy (US$17.6 billion), mining (US$9.0 billion) and communication (US$6.5 billion) (Brautigam and Hwang 2016). Table 1 shows resource-backed loans between African countries and China, up to 2018. However, it should be clarified that most of these deals are backed with oil. Also, most of them are greenfield projects (Vasquez 2019). The Angola Model, as an agreement between governments and mainly state-owned development banks as lenders, is commonplace across the continent. However, there are some exceptions, such as Guinea, which can be seen as part of a new model and with private actors on both sides, the Sinohydro deal in Ghana.

Overview of Resource-Backed Loans Between African Countries and China Between 2004 and 2018

Nigeria is also an important oil exporter, but it is not listed above. The Chinese company Sinopec took over the company Addax Petroleum for US$ 7.2 billion in 2009. Sinopec received oil equity in Nigeria, Gabon and Cameroon (Vasquez 2019). Therefore, it is not a resource-backed loan from China.

The Literature on the Angola Model

For Konijn (2014), the resource-backed finance model has weak linkages to the local economy and therefore limits economic impact. Mihalyi, Adam, and Hwang (2020) highlight that Chinese banks often bundle loans with oil sector production or trading agreements. Also, they come with requirements regarding the use of Chinese construction companies. Alves (2013) highlights, as observed in the case of Angola, the increased participation of Chinese companies in upstream production (Mihalyi, Adam, and Hwang 2020). Furthermore, due to contract conditions, a major share of goods and services is produced in China, while African countries only export resources in their raw state. In the case of the deal between China and DRC in 2008, the former gained rights to extract 6.8 million tons of copper and 420,000 tons of cobalt (Jiang 2009).

The Angola Model has often been discussed as a strategic partnership or a marriage of convenience. Corkin (2011, n.d.) argued that the relationship between Angola and China seems to be maturing from a heady embrace of mutual convenience to a reassessment of each other’s strategic significance as partners. Begu et al. (2018, 1) define the model as cooperation and a source of economic growth and infrastructure development for Angola and a source of energy that fuels China. Konijn and van Tulder (2013) highlight that general criticisms are the lack of transparency, doubts if it is a fair deal, a potential conflict of interest, concerns about fraud and corruption as well as weak links with the local economy. Furthermore, Ezechukwu (2015) points out a number of challenges resulting from the irreversible damage done to the environment by infrastructure projects, as well as the rising debt profile of African countries. Brooks (2017, 228) notes that the Angola Model enables types of capitalist development that in the long run will bring greater benefits to Chinese capital than the Angolan people. Also, he states, African countries are now re-accumulating debts and deepening their dependency on China.

For Singh (2019), in terms of dependency on natural resource extraction among borrowing governments, is more concerned with the misconception (Singh 2019, n.d.) that China is using loans to take over natural resources. There is also a growing number of scholars, such as Brautigam (2019) or Lai, Lin, and Sidaway (2020), refusing to acknowledge the debt trap discourse. Carmody (2020), however, supports this idea and outlines that increasing dependencies are more a feature of uneven capitalist development rather than something unique to China. However, he also points out that China as an increasingly authoritarian state is not afraid of using its economic and geopolitical power. Moreover, Jureńczyk (2020) argues that western researchers and commentators criticise Chinas cooperation’s and investment in African countries. However, he points out the specific political circumstances in Angola. The political system in Angola is monopolised by the MPLA and the masses do not benefit from the contracts with China, it can be better labelled as a transparent looting by the elites (Hess and Aidoo 2015). In addition, authorities have silenced criticism of Chinas growing role in Angola. In 2017, Angola approved a new media law, that enabled the government to control and censor critical information online. Therefore, Jureńczyk (2020, 54) argues, that there is no confirmation in the data of the practice defined by the world media as land grabbing. Furthermore, he points out, that western commentators overstate the influence of China in Angola. Nevertheless, de Carvalho, Kopiński, and Taylor (2021) argue that China responded to the criticism of the Angola Model and evolved their lending practices. In 2019, China shifted lending away from African countries that had recently restructured or reprofiled their debt. Lending was cut to countries such as Angola, Ethiopia Cameroon or the Republic of Congo, and new borrowers were Ghana, South Africa, Egypt, Ivory Coast and Nigeria (Pilling and Schipani 2021). In addition, Acker and Brautigam (2021) conclude, based on 20 years of data on China’s Africa lending, that (a) Chinese loan commitments dipped by 30% in 2019 compared to 2018; (b) Commercial loans from China Development Bank raised and (c) the resource-backed finance model is evolving, especially in Ghana and Guinea.

The Sinohydro Deal in Ghana 2018

Origins of the Sinohydro Deal

Resource-for-infrastructure deals refer to those in which loans granted for infrastructure development are repaid with natural resources. The first kind of resource-for-infrastructure deal between Ghana and China was the construction of the Bui Dam in 2007, also with Sinohydro as a construction company. The cost of construction was covered by the government of Ghana and by loans from the China Exim Bank (Williams et al. 2017). Both countries settled on a cocoa sales agreement of 40,000 tons for 17 years as repayment for the construction of the dam (Konijn 2014). In June 2017, the People’s Republic of China and the Republic of Ghana entered into a $10 billion deal, stipulating that China would participate in the development of the integrated bauxite–aluminum industry in Ghana and invest heavily in infrastructure development. In addition to the construction of schools and hospitals, this agreement included the expansion of roads and railway lines as well as deep-water port at Tema (Oxford Business Group 2018). Finally, in September 2018, the two countries signed a Memorandum of Understanding on further cooperation under the Belt and Road Initiative. In this context, an agreement was signed between the Ghanaian government and the Chinese company Sinohydro, the latter of which invested $2 billion in the development of infrastructure and would receive refined bauxite in return for 15 years (Master Project Support Agreement [MPSA] 2018). Also, Ghana committed to expand its bauxite-mining activities and build refineries over the following 3 years (Kpodo 2018). While this agreement could be just another example of the Angola Model and a typical resource-for-infrastructure contract, there are debates about differences between it and the more common finance models.

A major challenge with oil-backed loans is the volatile nature of oil prices. Ghana experienced such problems with a US$ 3 billion oil-backed loan from the China Development Bank in 2011. On the one hand, the country struggled with falling oil prices (from US$ 115 in June 2014 to US$ 53 in January 2015) (Aidoo et al. 2017), while on the other hand, it also had a simultaneous problem with price declines in its other major export goods, that is, gold and cacao. The ability of Ghana’s government to repay the loan was restricted. In 2015, the CBD agreement ended (Chen 2016), and Ghana turned to the IMF to help its struggling economy. In 2015, the IMF approved a $918 million loan, to help the country. During that time, the nation’s opposition party, New Patriotic Party (NPP), accused the ruling National Democratic Congress (NDC) of making a one-sided deal with China and putting a lot of pressure on the administration (Aidoo et al. 2017). This was also an important narrative during the campaign in 2016 (NPP 2020), when Akufo-Addo’s NPP won the general election and started new loan negotiations with China. However, based on experiences, this time it was different.

Operational Characteristics

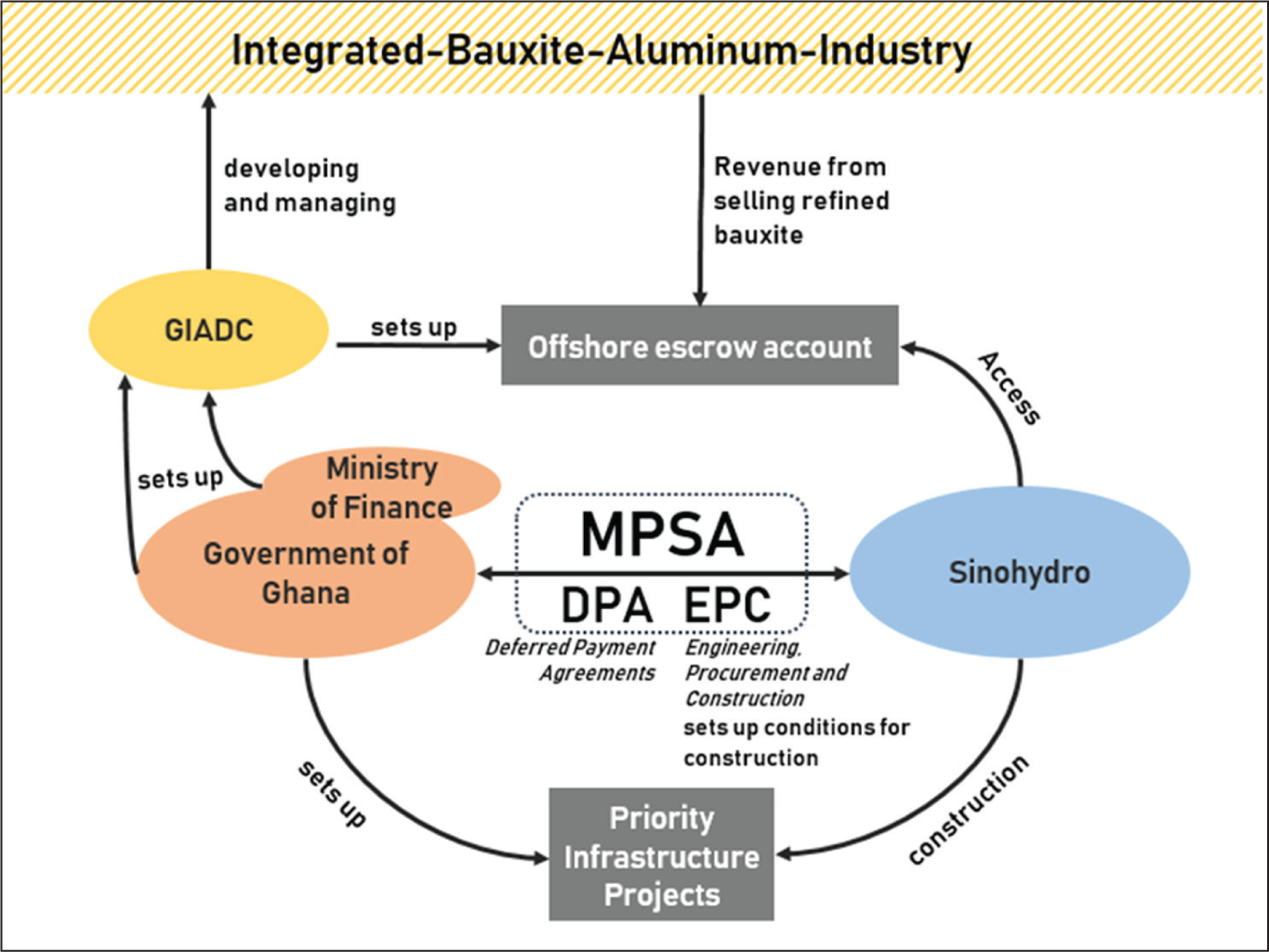

The Government of Ghana entered a finance arrangement with Sinohydro to develop infrastructure in the country. In July 2018, the master project support agreement (MPSA) was approved by Parliament. Following which, in November 2018, Parliament approved deferred payment agreements (DPAs) and engineering, procurement construction (EPC) contracts (IMF 2019). The latter of which are a particular form of arrangement whereby the contractor (in this case Sinohydro) is responsible for all activities, ranging from design, procurement and construction, through to the commissioning and handover of the project to the end-user or owner. Under an EPC contract, a single construction company agrees to provide a finished project, meeting certain technical and functional specifications, by a fixed time and for a fixed price. The Government of Ghana has undertaken to pay the total EPC contract price to Sinohydro, using proceeds from the sale of refined bauxite.

Sinohydro agreed to arrange project financing for deferred repayments by the government, which in turn would provide 15% of the construction and project costs. Under the MSPA, the government defined priority areas that need to be developed and executed by Sinohydro. Phase 1 consisted of ten road construction projects, at a total of 441.59 km and US$ 500 million and was scheduled to begin in March of 2020 (Republic Ghana Ministry of Finance 2020). According to the Republic Ghana Ministry of Finance (2020), four out of 10 road projects have already commenced; however, due to the Covid-19 outbreak in March 2020, construction stopped, and there are serious concerns of further delays. Defined priority areas for Phase II are road construction and bridges, as well as hospitals and affordable housing.

The Ghana Integrated Aluminium Corporation (GIADC) was set up by Parliament (established through an Act of Parliament in August 2018) as a commercially-based independent SPV (special-purpose vehicle) in charge of developing and managing the nation’s bauxite reserves (IMF 2019). While this was a required step, it is not defined in the Sinohydro deal. GIADC is in charge of organising bauxite mining in the country and for setting up plans to build refineries and relevant infrastructure. It is also in charge of entering into joint venture partnerships with investors for mining and refining. The GIADC board consists of representatives of the integrated aluminium industry, members of Parliament, a representative of the Ministry of Finance, the chief from Nyinahini, a representative of the Minerals Commission and a representative of the Association of Ghana Industries. GIADC has a Chief Executive Officer, who was a former Senior Vice President of Dell Corporation.

Under the DPAs, all financial obligations to Sinohydro are to be transferred from the Ministry of Finance to the Ghana Integrated Aluminium Corporation (GIADC) (see also Figure 2). Therefore, the government has no financial liability to Sinohydro, and the Chinese company is not directly involved in bauxite mining or the sale of the refined resource. However, GIADC reimburses Sinohydro with deferred payments and is responsible if payments are missed. As a result, GIADC has set up an offshore escrow account for revenue generated from selling bauxite. The government estimates that bauxite mining could deliver over US$500 billion in revenue. Although the Republic of Ghana has extensive bauxite reserves, the bauxite–aluminum industry has historically not been very significant, and the ore is only mined at one site near the city of Awaso. Since 2011, the mine has been owned by the Chinese company Bosai Mineral Group, which has fundamentally changed exports. Bauxite was mainly distributed to Europe and North America between 2008 and 2011, but since 2012, it has increasingly been exported to China (British Geological Survey 2018; Republic Ghana Ministry of Finance 2015).

Analysis and Discussion

As mentioned previously, transparency is often a problem, and it often limits studies on resource-backed loans, because not every detail is made public. In their study, for instance, Mihalyi, Adam, and Hwang (2020) found that out of 52 cases, only 19 provided basic information such as interest rates. However, Ghana has tried to be more transparent. While many details still remain somewhat vague, more openness in Ghana allows for a more detailed look at such deals. Nevertheless, the lack of transparency in other cases also limits research on this topic, especially when it comes to comparison.

One main argument offered by Johnston (2019) as to why the Sinohydro deal is different, is the new fixed interest rate development loan. However, according to Mihalyi, Adam, and Hwang (2020), 10 out of 19 loans they observed had fixed interest rates. For example, the loan made in 2009 to the Republic of Congo had a fixed interest rate of 0.25%, while in 2007, one of the two loans negotiated between Ghana and Exim Bank had a fixed interest rate of 2% (Brautigam 2011). Furthermore, the Sinohydro deal is London Interbank Offered Rate (LIBOR)-based, with an annual interest rate of LIBOR + 2.8%. As mentioned, the collateral is also refined bauxite. Herein, I concentrate on two different and unique aspects of Ghana’s Sinohydro deal: (a) privatisation, which refers to the involved actors and the new parastatal GIADC, as well as (b) the collateral itself and impacts for the integrated bauxite industry. However, in the end I also want to draw attention on (c) the environmental aspect, as it is a major concern when it comes to mineral extraction industry.

Privatisation Shift

Mihalyi, Adam, and Hwang (2020) highlight that out of the $164 billion in RBLs committed in sub-Saharan Africa and Latin America between 2004 and 2018, 77% of the amount came from two Chinese policy banks, specifically CDB and the China Exim Bank. The rest were a mix of state-owned companies of various nationalities and international commodity traders. Under the Angola model, Chinese loans are provided by its Export–Import Bank (Exim Bank) and are accompanied by an interest subsidy from the Ministry of Commerce (Foster et al. 2009; Kiala 2010). In the case of Ghana, the state-owned company Sinohydro, with the approval of Sinosure (China Export & Credit Insurance Corporation), signed the deal with the government of Ghana, which negotiated on behalf of the Ghana Integrated Aluminium Development Corporation (GIADC), but once the GIADC was set up, it would become the obligor under the Sinohydro arrangement. Compared to the construction of the Bui Dam, an agreement between China and Ghana in 2006, the government put the Bui Power Authority a government agency in charge. The Sinohydro deal is at this point a deal between a state-owned company (Sinohydro) and a commercial-based independent SPV (GIADC). The IMF (2019) argues that this structure seeks to ensure that the GIADC obligation will not add to the Ghanaian government’s debt stock. Also, the Sinohydro deal states that the Government of Ghana will have no financial liability to Sinohydro, nor will it provide any guarantees. Therefore, the IMF (2019) classified this project as commercial debt, thereby appearing to have ring-fenced possible government obligations. The only risk in that case would be a delayed transfer of obligations to the SPV. However, another advantage of this arrangement is that the GIADC is free to negotiate with possible investors in the bauxite sector, so they can also attract Western companies and limit Chinese influence in the mining sector.

The Sinohydro deal, as well as the example from Guinea, illustrates what has been observed recently, that is, China’s state-owned enterprises (SOEs) increasingly investing their own capital to build and operate infrastructure projects. Primarily, the SOEs serve as contractors responsible for engineering, procurement and construction (EPC). Chinese policy banks then finance the project with loans, and thereafter, projects are contracted to a Chinese construction firm (Foster et al. 2009). Leutert (2019) points out the evolution of Chinese SOEs, from contractors to operators and investors, which is the case with Sinohydro in Ghana. As mentioned earlier, in 2017 the Exim Bank promoted a more sustainable and innovative finance mechanism. This shift, and its implications for governments and economies, will require more attention in the future.

Collateral and Its Impact on the National Economy

When it comes to collateral, there are some differences. In the case of the Bui-Dam deal between Ghana and China, the latter guaranteed to purchase 30,000 tons of cocoa per year from the Ghanaian government at current world market prices (Odoom 2015). Similar to the $3 billion oil loan in 2012, which stated that 13,000 barrels of oil would be supplied daily for fifteen-and-a-half years to pay off the loan (Odoom 2015). In addition, the 2004 deal with Angola stated that the US$2 billion Chinese loan was tied to a delivery of 10,000 bpd of crude oil. Sinohydro deal documents define that the proceeds of the sale of refined bauxite should be used. Additionally, they state that receipts from the transfer of refined bauxite to its strategic partner, and where receipts from refined bauxite are not sufficient […] Government of Ghana shall use other sources for the repayment to Sinohydro, thereby allowing for the export of refined bauxite, or even bauxite in its raw state, into the global market. In comparison, a similar deal in 2017 between China and Guinea had bauxite as collateral, while Ghana has refined bauxite. Meanwhile, aluminium is becoming more and more important. Ghana’s government also hopes that with the integrated bauxite–aluminum industry, they can stimulate nationwide industrialisation. Ghana has mines as well as a smelter, and so only, the refiners are missing in the value chain. In addition, it already holds a 20% stake in the mining company, the smelter is 100% state-owned and a minimum 30% stake in any new mine, refinery or smelter will be held by the government. With the Sinohydro deal, the government argues, the country can now develop an integrated bauxite–aluminum industry, which has been the plan since the nation gained independence. This would also be in the interest of China.

As Schmalz (2018) suggests, China is trying to avert a possible financial crisis and is struggling with increasing industry overcapacity as well as rising indebtedness. By building infrastructure and connecting other countries, China exports its surplus while supporting economic growth. Thus, Ghana is increasingly embedded in China-based globalisation (Kanungo 2017) and, as a resource-rich country and fast-growing sales market, has aroused the interest in Chinese companies. Sinohydro is a state-owned enterprise, with the majority stake held by the Chinese central government. For Asche and Schüller (2008, 15), the impression of an overall strategy for the economic development of Africa is reinforced by the fact that the Chinese government formulates clear industrial policy goals and uses a mixture of market-based and interventionist instruments to achieve its goals. Therefore, it could be argued from the perspective of China, this is some kind of strategy diversification to invest in other countries, using not only their state-owned development banks, but also state-owned enterprises. However, due to the close interlinking of politics and the economy in China, targeted agreements between the administration and the company, as well as joint action on foreign markets, is possible. Also, from the perspective of Ghana, it seems that the administration tried to negotiate a different deal and may have learned from past experiences, especially recalling the oil-backed loan in 2011. Worth mentioning is the guaranteed 30% local content in the Sinohydro deal. It may appear to be not that much; however, it is an important step in limiting Chinese involvement, which has always been critical. Other deals have culminated in a lower percentage securing local interests, such as a loan to the DRC in 2007 at 12%. More often, China has a high percentage of its own companies, such as in Ghana in 2011 (minimum 60% Chinese companies) or Angola in 2004 with 70%.

One benefit of the Sinohydro deal is that the construction of infrastructure projects are starting very quick and results are getting visible in a short time. Less than 18 months after the negotiations, the road projects are getting underway. The important aspect here is that Ghana’s President Akufo-Addo needs to show very quickly that the Sinohydro deal is worth the critical environmental and financial risks. Looking at the location of the prioritised projects, it appears that almost every political region in Ghana benefits. If people see positive development in their region, they may be less concerned about the critic from national as well as international environmentalist and the media. Especially because 2020 is an election year and many roads will be finished or at least under construction within the first term of Akufo-Addos presidency. Parallel, the infrastructure for the integrated Bauxite–Aluminium industry needs to be set up, which is best done via railway. Therefore, Ghana signed several agreements with China Railway Wuju Group Corporation and China Civil Engineering Construction Corporation (Ministry of Railway Development 2019a; 2019b) in order to renew and extend the existing railway network. While the Sinohydro deal serves public infrastructure across the regions, the government agreed new loans in order to set up an infrastructure, which serves more the Bauxite–Aluminum industry. However, this may deepen the dependency on China as well as raise the pressure on being successful with these projects. The establishment of the bauxite refinery to complete the aluminium value chain is therefore an important aspect of his industrial projects in the presidential campaign of Akufo-Addo in 2020 (NPP 2020).

Environmental Concerns

The 2018 budget statement and economic policy of government promotes aluminium refineries and bauxite mines at Nyinahin and the Atewa range, Kyebi. Due to its processing, it makes sense to build refinery directly next to mining areas. However, Kyebi in particular attracted media attention, as an important forest could fall victim to the plans. According to the Minerals Commission (2015), the Atewa range hosts the second largest bauxite deposit in Ghana. The range of hills on which the bauxite occurs consists of flat or nearly flat-topped hills stretching 14.5 km from Apinamang in the west to Kyebi in the east. The bauxite deposits are covered by the tropical forest, which implies that the forest needs to be logged to some extent, if open pit mines are to developed (Schep et al. 2016). Like most extractive industries, bauxite mining which is usually striped-mined has significant effect on natural environment, like degradation or disruption of local wildlife and water flows. One of the by-products of the process for refining bauxite into alumina is a waste product, mostly known as ‘red-mud’ (Ingulstad, Storli, and Gendron 2013). The alkaline constituents in the red mud impose severe and alarming environmental problems, like soil or water pollution (Rai, Wasewar, and Agnihotri 2017).

According to Ingulstad, Storli, and Gendron (2013), in order to produce one tonne of aluminium, the mining process generates 10 tonnes of waste rock and three tonnes of toxic red mud. Environmentalists as well as the local officials criticise the plans for mining of bauxite in the Atewa forest (Purwins 2020). They fear deforestation, pollution of water and other environmental damage will affect especially the local population. The forest functions as the source of three important rivers the Densu, Birim and Ayensu rivers. A burden on the region could thus also lead to these rivers being heavily polluted. The Densu river belongs to the coastal river system of Ghana and is one of the two main sources of water supply for the Accra urban area (Schep et al. 2016). According to the Ghana Wildlife Society (2018), over five million Ghanaians depend on the water from the three rivers, Densu, Birim and Ayensu. However, the society calls for a protection of the forest and promotes different options like eco-tourism. A group calling themselves concerned citizens of Atewa Landscape was formed in 2018 to prevent bauxite mining in the forest. They constitute themselves from civil society organisations, youth groups, interfaith groups, farmer-based associations, opinion leaders and community leaders. In addition, the NGO A Rocha Ghana is an initiator and promoting the protest against the government plans. In March 2018, the group started a six-day walk from the eastern region to Accra in protest of mining in the Atewa forest reserve and to submit a petition to the government. By 2020, they intensified their protests in various ways. In addition, some youth groups within the Ashanti region have vowed to stop the mining of bauxite in the Nyinahin forest reserve, another major bauxite reserve in Ghana.

Nevertheless, most African countries require a type of environmental assessment, which is a formal process preventing environmental harm and aligning development activities with the interests of the general public. The environmental laws in Ghana come in the form of environmental impact assessments (EIAs) and strategic environmental assessments (SEAs), which are also very common in other African countries (TCI 2018). An EIA requires an analysis of the possible impacts that a proposed physical development would have on the environment, as well as on human well-being. In general, these assessments have to be done before starting a project. Based on the results, the project needs to guarantee certain changes and implementations. An SEA is the systematic and comprehensive process of evaluating the environmental effects of government policies, programmes or plans (EPA Ghana 1994; TCI 2018). The Environmental Protection Agency (EPA) permits projects (governmental as well as private) if they undertake an EIA and can prove that they will have no significant impact on the environment and public health. At this point, the question arises why the Ghanaian government has not undertaken a formal assessment of the agreement’s potential environmental impacts. The requirement for a formal assessment does not apply to negotiations of agreements; in addition, an SEA will only trigger if government plans are likely to affect the environment (Neal and Losos 2021). However, the Sinohydro deal is crafted in such a way that it does not mention at any time, the development of an integrated bauxite–aluminium industry it is only agreed that Ghana will use refined bauxite as collateral. Moreover, the Sinohydro deal does not describe how Ghana will meet its contractual obligations. EIA and SEA does not trigger, the Sinohydro deal has bypassed environmental laws.

Examples from Other Countries: The Case of Guinea

Acker and Brautigam (2021), point out that besides the critic of resource-secured lending, in some countries this practice declined, while in others it continued, for example, in the DRC, Guinea and as described in Ghana. In the DRC, copper is used to finance infrastructure under the Sicomines agreement. Very similar to the Sinohydro deal in Ghana is the resource-backed loan in Guinea, which is a good example because both were negotiated at the same time. Moreover, both deals are the only known loans backed by the commodity bauxite (Mihalyi, Adam, and Hwang 2020). In 2017, a consortium of Chinese banks, led by the Industrial and Commercial Bank of China (ICBC), announced $20 billion in loans, in return for which they would receive bauxite with Guinea. Compared to Ghana, in the case of Guinea, bauxite concessions were provided in exchange for infrastructure such as road projects. As part of these negotiations, Guinea entered into a concession agreement with the Chinese company Chalco. Under this agreement, further developments in the bauxite sector had been agreed upon, and it was planned to proceed further with bauxite and build refineries. According to Wingo (2020), China is shifting toward making a greater on-the-ground commitment to extraction as part of resource-backed deals in Guinea. However, it is important to note that the bauxite sector in Guinea is far more developed compared to Ghana. Ding et al. (2021, 3) argue, that on the other side, Ghana has a more diversified economy, a stronger legal and regulatory framework, and a more empowered civil society, giving Ghana an advantage in addressing the regulatory and environmental concerns of its natural resource for infrastructure agreement with China. Especially the aspect of a more empowered civil society, giving Ghana an advantage in addressing the regulatory and environmental concerns, as already described before. Compared to Guinea, the issue of biodiversity protection is a greater concern in Ghana (Ding et al. 2021). However, many details remain unclear, which makes it difficult to compare both cases. Nevertheless, the resource-backed deals in Ghana and Guinea illustrate that the trend of using metals as collateral continues (Wingo, 2020).

Conclusion

The Angola Model has ensured vast amounts of capital to build much-needed roads, bridges and other infrastructure in Africa under the narrative of a win-win-situation (Begu et al. 2018). However, the financial crisis and the crash in oil prices meant that Angola had to sell increasingly more oil to repay the Chinese debt. Commodity prices are inherently volatile, and African countries need to sell enough of their resources to avoid the same inflation trap. Mihalyi, Adam, and Hwang (2020) point out that the majority of resource-backed loans are earmarked for financing particular infrastructure projects. Since the provision of infrastructure is critical, many African governments justify borrowing if the social returns from these projects are higher than interest charges and risks associated with the loan. However, since 2014, commodity-backed loans have played a smaller role in China’s foreign policy, and some governments have also refused to use these finance models; for example, Angola announced in 2019 that it had decided to stop guaranteeing loans with oil (Macauhub 2019). Additionally, other commodities, such as cobalt and copper in the DRC, appear to be less resilient to price drops than originally hoped (Landry 2018). In the case of the Republic of Congo, the IMF approved a bailout worth nearly $449 million, after the country struggled with debts it owed to China (Bavier 2019).

The Sinohydro deal in Ghana is an example of a Chinese SOE being not only a constructor, but also an operator and an investor. This matches with the idea proposed by the Exim Bank in 2017 to develop new, innovative and sustainable finance mechanisms, including government–private capital cooperation. From the perspective of Ghana, the established GIDAC has ring-fenced possible government obligations. Also, what Hart (1977, 22) once described as the country’s most useful resource can now be developed into a promising industry. However, some challenges remain, similar to other cases, such as problems in transparency. Investments made by China in Africa, according to Ascensão et al. (2018, 207), increase negative environmental impacts. They are likely to affect disproportionately an already vulnerable population. Due to the lack of transparency, environmental issues and concerns, the Sinohydro deal increased a growing movement against bauxite mining in Ghana, especially at Atewa forest a possible extraction site (Purwins 2020). The Ghanaian government is therefore under a lot of pressure, not only from local but international NGOs, intellectuals (or actors like Leonardo DiCaprio) and major manufacturing companies as members of the Aluminium Stewardship Initiative openly opposing mining in Atewa forest (Birdlife International 2021). Finally, the COVID-19 pandemic across China and Ghana has also led to a delay when it comes to construction. In this regard, signing this deal without already constructed refineries and infrastructure seems a very risky undertaking.

In January 2020, the news website Ghana Web ran the following headline: Ghana’s Sinohydro deal touted as a new model for Africa to follow. In addition, likewise to the analysis of Acker and Brautigam (2021), I would argue, that the controversial resource-backed infrastructure financing model is still alive and has evolved in certain ways. As argued, the main differences are (a) the established para-state company charged with managing the extraction of bauxite and (b) the plans to develop an integrated bauxite–aluminium industry within Ghana. On the other side, environmental concern regarding bypassing regulations or possible pollutions remain the same. However, is too early to say if this kind of deal is something for which other African countries strive; in fact, it could be one of many different ways to approach construction deals in the African continent, rather than a strategic shift. On the other hand, Ghana is known in the African continent as having a strong economy, and so it may be in a better position when negotiating with China. In terms of the Sinohydro deal, the short-to-long-term extraction of bauxite, as well as the associated consequences on the local level, will prove if it is indeed a successful and sustainable model.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.