Abstract

African countries have been hit by a dual shock of COVID-19 pandemic and global oil crisis, which have caused severe economic and social disruptions. Most studies shed light on the correlates between COVID-19 and the global oil crisis, including their economic impacts on oil producing/exporting countries. However, the objective of this study is to examine the effects of the global oil crisis on the implementation of World Health Organization’s (WHO) healthcare and public health measures to contain COVID-19 in Nigeria. Empirical data from Nigeria was collected and analysed using content analysis based on WHO’s methodology. There was low level of healthcare preparedness and emergency response capacities to contain the COVID-19 pandemic. Public health measures against COVID-19 such as lockdowns and social distancing policies were poorly implemented at the expense of the people without adequate countercyclical stimulus packages and palliatives.

Keywords

Introduction

Nigeria being Africa’s largest oil producing country is one of the hardest hit by the dual shock of COVID-19 pandemic and global oil price crash. Analysts indicate that the cumulative damage of the COVID-19 pandemic to Nigerian economy in the medium and longer term could be far more severe than its health impact (Devecioglu, 2020; The World Bank, 2020a). Nigeria is heavily dependent on oil export receipts and fiscal revenue—making up to three-quarters of government revenue (Ake, 1981; Ibeanu, 2002a; IMF, 2007). Hence, amidst disappearing oil revenues and rents Nigeria relies essentially on financial help/loan from the international community and charity donors to combat COVID-19 pandemic (IMF, 2020; Onyekwena & Ekeruche, 2020; Parkinson & Faucon, 2020). However, the strategic containment fight against COVID-19 in Nigeria has been twofold: to contain its further spread and to cushion the concomitant economic consequences. A key challenge is how to fix collapsed healthcare infrastructures and facilities as well as provide stimulus packages and palliatives for the people.

Many important studies and reports highlight significant linkages between the COVID-19 pandemic and the global oil crisis, and their short, medium and long term economic impacts on oil producing/exporting countries (Africa Newsroom, 2020; Akanni & Gabriel, 2020; Akrofi & Antwi, 2020; Arezki & Nguyen, 2020; Devecioglu, 2020; Gladstone, 2020; IEA, 2020a, 2020b; IMF, 2020; Maclean & Marks, 2020; Okonjo-Iweala, 2020; Onyekwena & Ekeruche, 2020; OPEC, 2020; Parkinson & Faucon, 2020; WHO, 2020a, 2020b; World Bank, 2020a, 2020b). However, there is little or no agreement among scholars, analysts and forecasters on the relationship between global oil crisis and the level of implementation of WHO’s healthcare standards, public health measures and social policies to contain further spread of the pandemic and cushion its economic effects. How did the global oil crisis impact on Nigeria’s adoption of World Health Organization’s (WHO) critical preparedness, readiness and emergency healthcare responses in the fight against COVID-19 pandemic? How does the implementation of COVID-19 public health measures/lockdown protocols, amidst the global oil crisis, implicate the level of stimulus packages and palliatives available to the affected people in Nigeria? These are critical issues that form the key objectives of this article.

This study adopts the WHO’s recommended methodology: ‘Critical preparedness, readiness and response actions for COVID-19’ (WHO, 2020d). The WHO methodology is used to assess the level of healthcare preparedness and emergency response capacities of Nigeria to contain the COVID-19 pandemic as well as the level of implementation of COVID-19 public health and social measures such as lockdown and social distancing policies. The study relies on qualitative methods of data collection and content analysis. Data was analysed based on WHO weighing factors on critical preparedness, readiness and response actions for COVID-19. This study makes two significant contributions. First, it shows that African rentier states (oil-export dependent economies) such as Nigeria lack the resource capacity to contain global health pandemics amidst any sustained global oil crisis. This is linked to the problem of low-export diversification among key oil producing countries in Africa. Second, the study makes a systematic case for an increased analytical and theoretical emphasis (especially leveraging the lessons from the dual shock of COVID-19 pandemic and global oil crisis) to mainstream oil-export dependent economies towards the path of economic and export-trade diversification and self-reliance.

Precarity of Crude Oil Production, Demand and Supply amidst COVID-19 Pandemic in Africa

African oil producing countries are among the hardest hit by a twin debacle of COVID-19 pandemic and declining oil price. They continue to face perilous times and significant threats each day amidst the threat of economic devastation and opprobrium (CNBC Africa, 2020; Parkinson & Faucon, 2020). It is important to examine the context, significance and implications of the COVID-19 tragedy on the global crude oil production, demand and supply regime as it affects key African oil producers such as Nigeria.

Crude Oil Price Crash

Crude oil prices crashed irredeemably in March 2020, recording their deepest monthly slump since the global financial crisis in 2008. This world economic crisis is linked to the ramifications of the COVID-19 pandemic as a driving force and global oil demand shock that impelled a massive sell-off in the world oil markets amidst surpluses in crude oil production and supply. The COVID-19 pandemic, together with the Saudi-Russia oil price tussle, has had a harsh impact on oil markets. The COVID-19 containment measures recommended by WHO and implemented by world governments, including lockdowns, travel restrictions and social distancing policies, currently affect over 40 per cent of the world’s population across 187 countries and territories (IEA, 2020b). These restrictive measures cut down fuel consumption, tear apart jet fuel markets and drive gasoline margins into negative threshold. The global economy faces severe contraction and uncertainties that will further sharply deplete overall GDP growth by 1.5 per cent in 2020 after a decelerating growth of 2.9 per cent in 2019 (OPEC, 2020).

Global oil demand averaged 98.84 mb/d in 2018 and 99.67 mb/d in 2019. It maintained at 98.75 in 1Q2019; 98.56 in 2Q2019; 100.53 in 3Q2019; and 100.79 in 4Q2019. However, it plummeted to estimated 92.92 in 1Q2020 and 86.70 in 2Q2020 (OPEC, 2019). Global oil demand in 2019 grew at 0.83 mb/d y-o-y to average 99.67 mb/d, but has tumbled uncontrollably in 2020, with global oil demand growth revised downward by a considerable 6.9 mb/d, depicting a historic decline of around 6.8 mb/d. Particularly, oil demand in the first quarter 2020 is revised lower by almost 12 mb/d y-o-y, with 60 per cent of the loss resulting from transportation fuels, primarily gasoline and jet fuel. The severity of the slump in global oil prices results in sharper contraction in oil demand in 2020, a gloomy and negative outlook that is forecast to escalate to 12 mb/d in second quarter 2020, about 6 mb/d in third quarter 2020 and about 3.5 mb/d in fourth quarter 2020 (OPEC, 2020). This plunging demand, for product markets, means refineries will cut production drastically, or even halt operations as economies of scale margins continue to stagger and slope downwards.

The saturation of physical market with large oil supplies, leading to excess storage of unsold cargoes forced crude oil spot prices to drop significantly than oil futures. Many crude oil sellers battle to make immediate sales amid the realities of steep drops in oil demand, especially for transportation fuels, jet fuels and gasoline. The sellers are forced to make deep concessions and discounts in order to attract buyers, leading to stark dips in crude differentials of all crude qualities and in all regions. Despite these trading frustrations, world crude oil production continued to rise, thus mounting more pressure to the already overstretched and worn-out oil market.

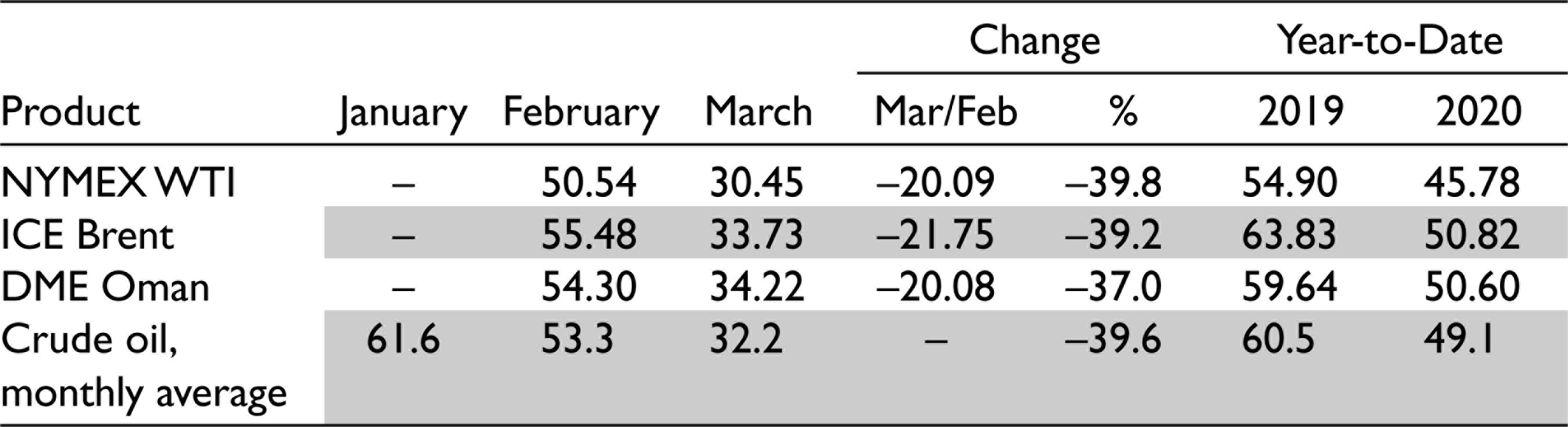

Table 1 shows the crude oil futures (prices) in 2020, indicating the unprecedented drastic and historic worst declines ever.

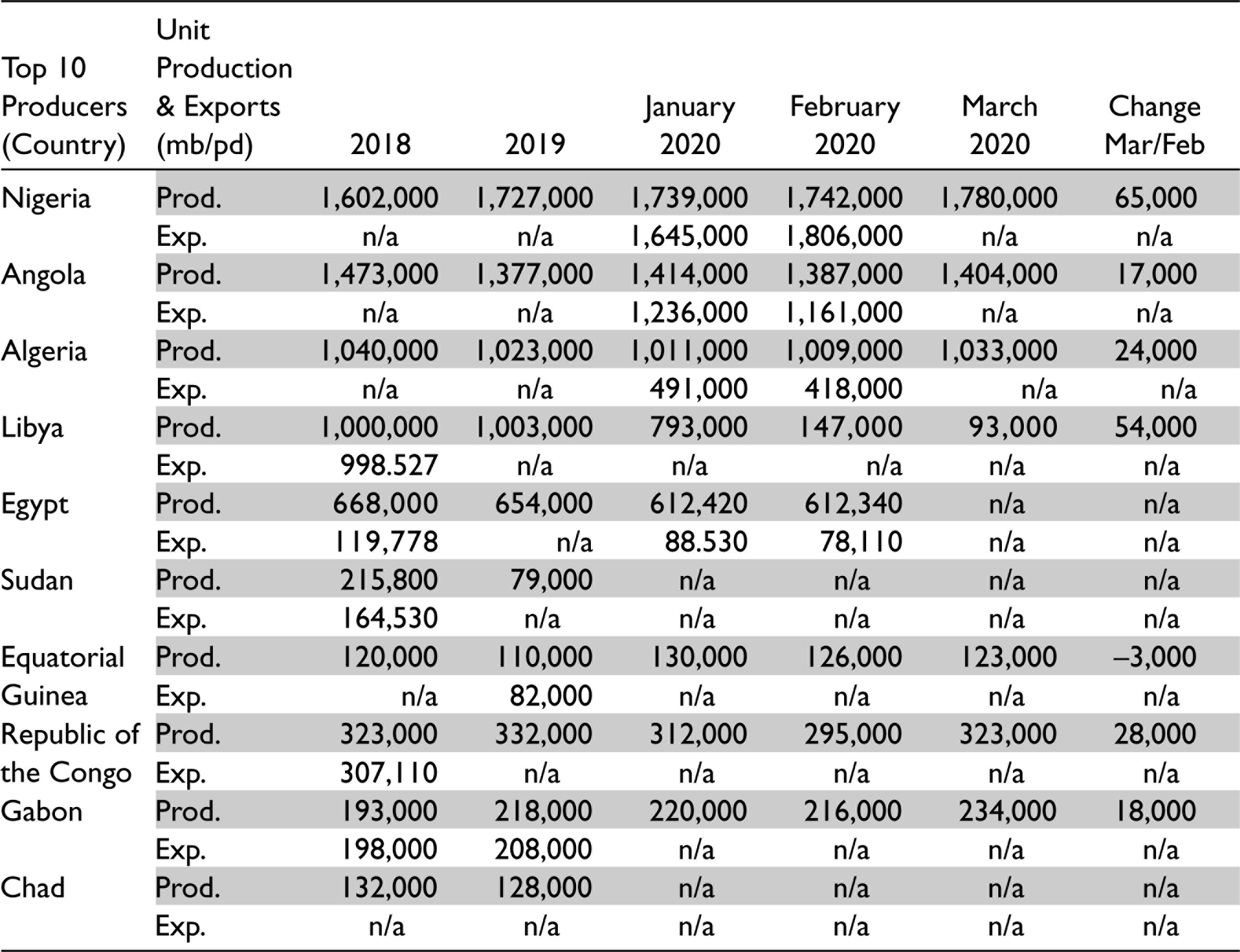

The potential damage of the global oil demand slowdown remains highly unpredictable, with some projections ranging between 8.0 mb/d and 15.0 mb/d decline in 2020 as against the same period in 2019 (OPEC, 2020). However, in an effort to stabilise the oil market and restore balance in the world oil market, the OPEC and non-OPEC crude oil exporting countries held two Extraordinary Ministerial Meetings, on 9 and 12 April 2020, and pushed for downward adjustments to their overall crude oil production by a historic 9.7 mb/d, beginning from 1 May 2020, for an initial two months period, and adjusted to 7.7 mb/d till the year end and 5.8 mb/d till 30 April 2022 (IEA, 2020b; OPEC, 2020). A sluggish rebound in world oil demand is predicted to an average annual growth rate of just below 1 mb/d between 2019 and 2025 (IEA, 2020a). Table 2 trends the impact of COVID-19 on crude oil production and exports in Africa, 2018–2020.

The table depicts a relatively stable trend in crude oil production levels for the top 10 African oil producing countries in the period, in stark contrast to a consistent decline in crude oil exports for the countries the same period. This trend portends the prevailing difficulty in making sales in the oil market in present times of COVID-19 and oil price free-fall.

Crude Oil Futures (Prices), 2020, in US$/b

The imbalances in the world oil prices impact the livelihoods of millions of people employed in the oil industry’s extensive value chain, including over 4 billion people trapped in COVID-19 lockdown, and strangle the economies of African oil producing countries where social stability is already fragile. A decline of 32 per cent or $335 billion is forecast in global capital expenditure by oil exploration and production companies, the lowest recorded since 13 years (IEA, 2020b). Global investment for exploration and production companies has flopped remarkably. For a low oil price scenario, where Brent crude averages $25/billion in 2020, global investments is forecast to plunge to $380 billion and decline further to about $300 billion in 2021, a 14-year and 15-year low respectively. Upstream spending which is forecast to drop between 15 per cent and 20 per cent in 2020 will force investments to shrink by $80 billion to $100 billion compared to the 2019 level. The international oil companies operating in Africa have cut their expenditure by an average of 20 per cent globally, despite the predicted negative effects on exploration and capital projects in Africa. ExxonMobil and BP have considered about 20 per cent reduction in operating cost and capital expenditure. Shell has already announced a reduction of underlying operating costs by $3 billion to $4 billion, with a reduction of cash capital expenditure of $5 billion. Total’s organic capex has been cut by over $3 billion, representing 20 per cent of its proposed 2020 capex. Chevron is also reducing capital and expenditures on exploration by 20 per cent, including a $700 million cut in upstream projects and exploration (Africa Newsroom, 2020). In October 2020, Chevron announced a 25 per cent cut in their Nigeria staff due to the pandemic’s impact on oil demand (Chinery et al., 2020).

Crude Oil Production and Exports in Africa, 2018–2020 (in mb/pd)

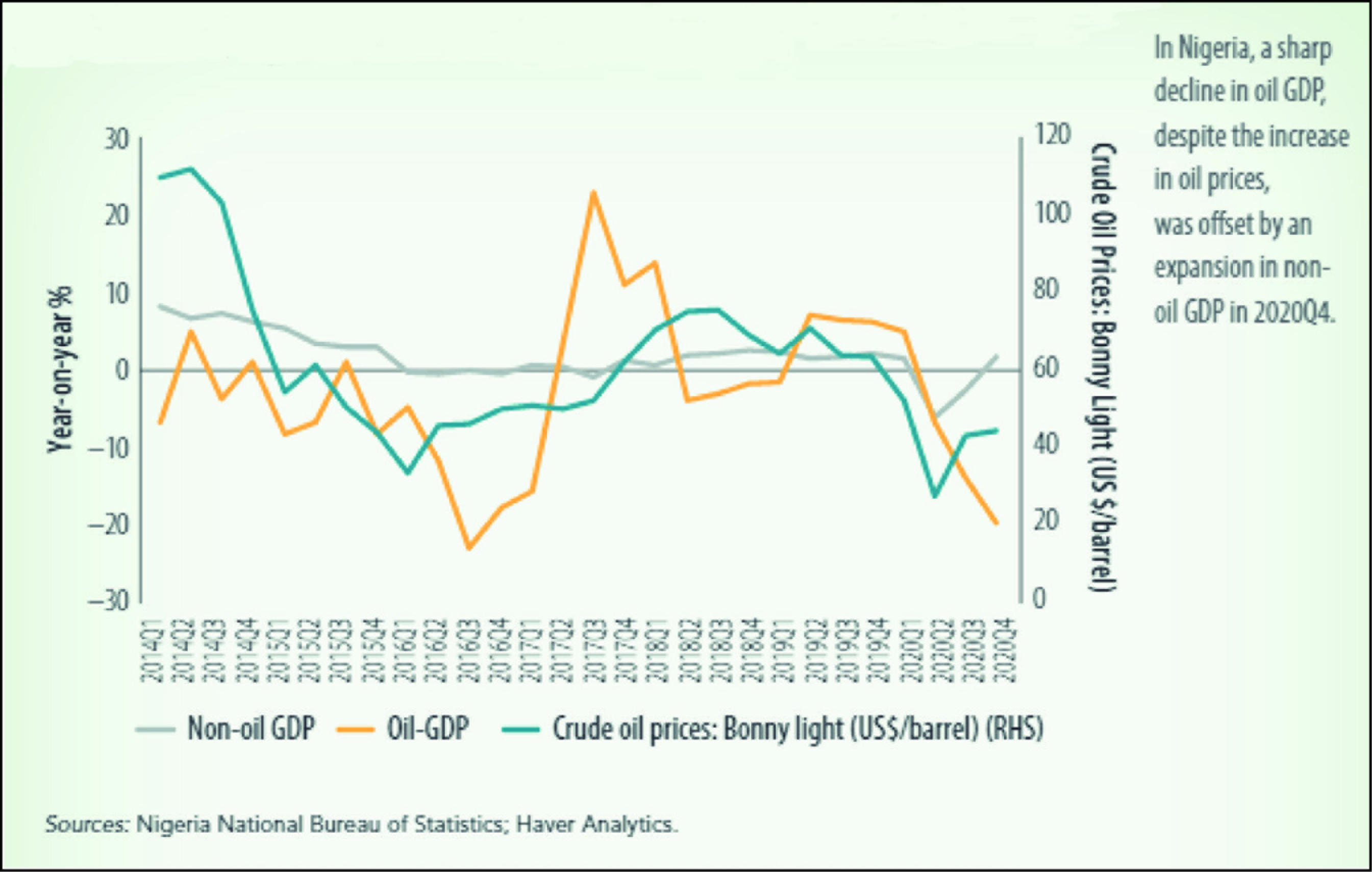

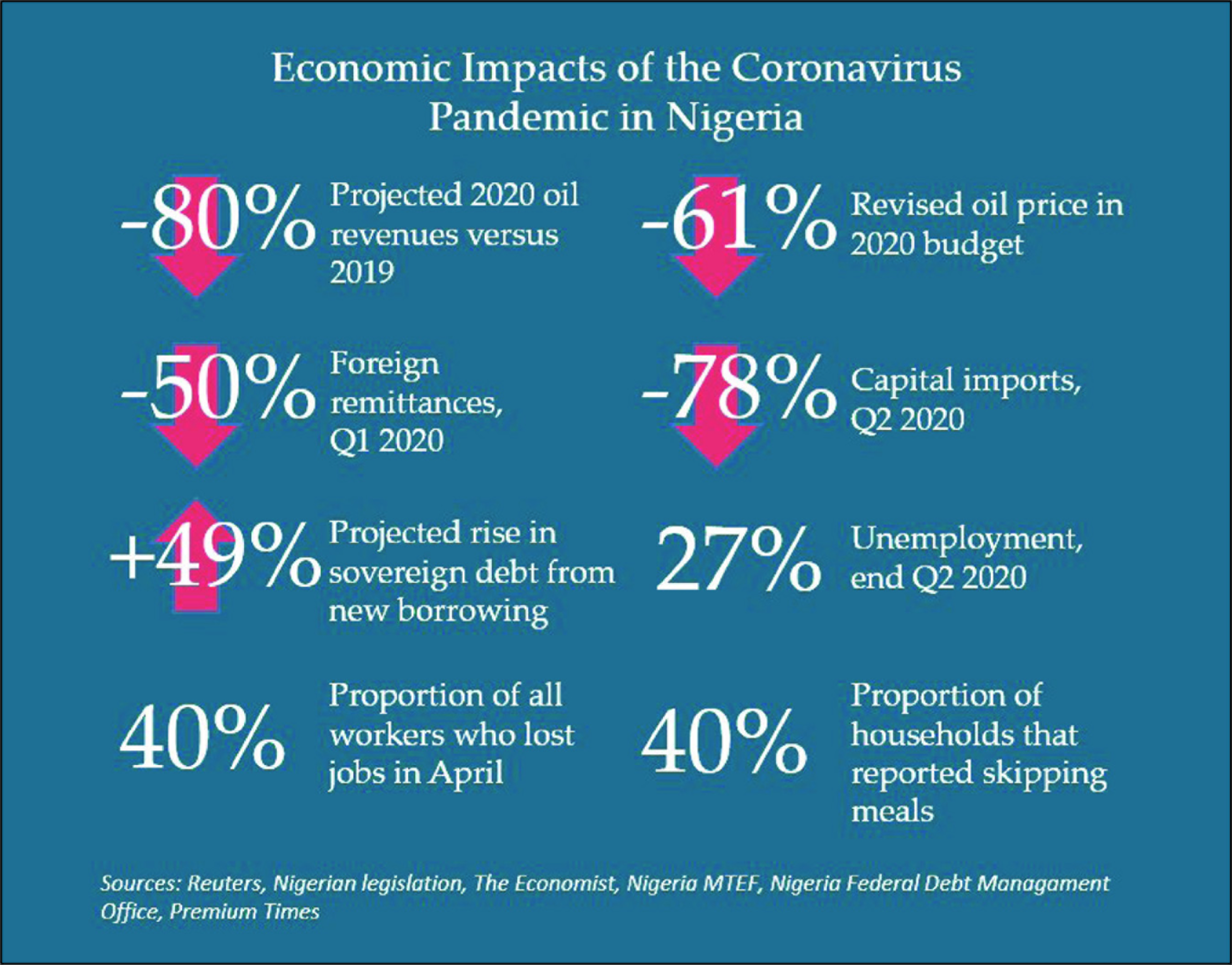

Following a historic crash in oil prices, more pressure has now been mounted on state budgets, testing the macroeconomic stability and resilience of the rich oil producing countries in Africa. Nigeria hinged its 2020 state budget on oil benchmark of $57 per barrel respectively, with the projection that oil prices will not fall below $30 per barrel for the rest of the year. Unfortunately, with the free fall in oil prices down to $20 and $22 per barrel—the highest drop in 18 years—the state budget was readjusted compelling a drastic cut on public spending (Africa Newsroom, 2020; Ireri & Mathai, 2021). Nigeria suffers the biggest loss on the continent with about $15.4 billion, even though the losses represent only 4 per cent of its GDP. Figure 1 shows the effects of the declining oil prices on Nigeria’s oil and non-oil GDP growth.

The figure shows that, at the early stage of the global pandemic, oil prices dropped significantly over the first half of the year then rose over the second half of the year—but remained far below those of the pre-COVID era. Despite a relative increase in the petroleum prices in mid-2020, Nigeria’s oil GDP continued on a consistent decline. The oil sector contracted by 13.89 per cent in the third quarter against the growth of 6.49 per cent achieved in the same period a year earlier. The drop in oil prices combined with the COVID-19 shock, thus caused Nigeria to slip into a recession in November 2020 (Al-Jazeera, 2020).

Nigeria has over $58 billion in oil projects set to suffer delays or cancellations. On March 18, Nigeria announced a 1.5 trillion naira ($5 billion) budgetary slash in nonessential capital spending (close to 1% of GDP) (IMF, 2020; OPEC, 2020; Parkinson & Faucon, 2020). Debt service already consumes over half of Nigerian government’s revenue and most fiscal buffers are depleted. In April 2020, Nigerian officials told the IMF that the country faced an external financing gap of $14 billion. Many of its 36 state governments have also become insolvent. To help support all this spending, the government sought about $11 billion in fresh loans from the IMF, domestic banks, the World Bank and others (Chinery et al., 2020).

Problem of Export Commodity Diversification

Nigeria operates a highly monolithic, reclusive and undiversified economy built on crude oil export-trade dependence, with only short-lived, unsustainable and sometimes, negative economic growth (Ake, 1981; Balistreri et al., 2015; Golub & Maybe, 2009; Saygili et al., 2018). The lack of export diversification on non-oil sectors of the economy worsen their recovery potentials for economic viability and rebounds amidst the COVID-19-induced volatile, convulsive and rapidly collapsing international oil market. An unstable export market economy without a sustainable export-trade and industrial diversification would be vulnerable to the potential impact of deteriorating export prices and stiffer competition at the world market that it cannot survive (IMF, 2007; Singer, 1950; World Bank, 2018).

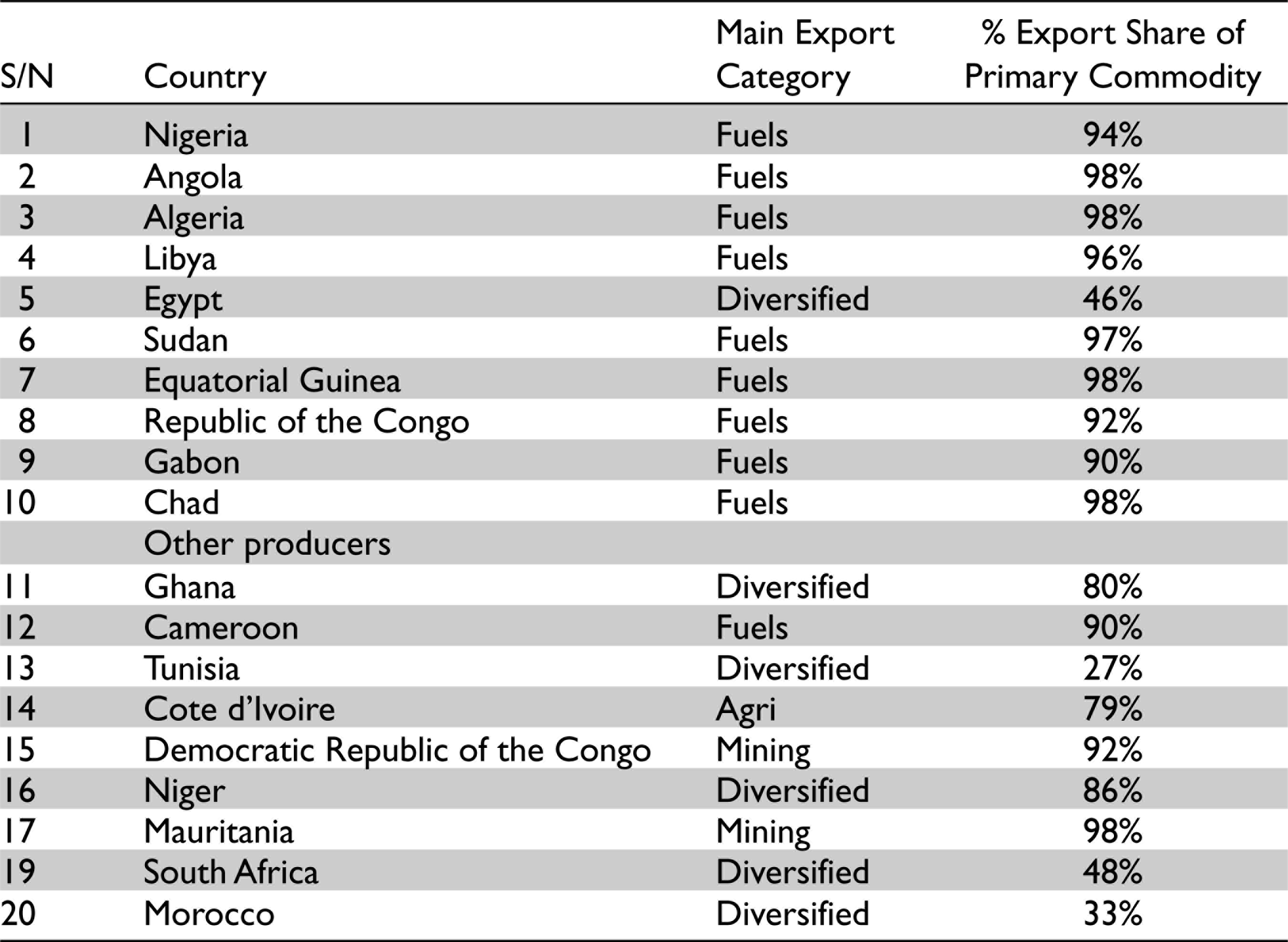

The risk in extreme fuel export-concentration is that the more the oil export-dependent economy experiences extreme price gains/cyclical boom, the more its effects repress the drive for export-diversification and development of all other sectors of the economy (Spatafora & Tytell, 2009; Stuart, 2019). This means that accruable oil rents in Nigeria have not been appropriately diversified in investments in other important sectors of the economy (Ake, 1981). Thus, Nigeria as a substantial oil export-dependent country suffers extremity of export-specialisation (i.e., on fuels: crude oil, natural gas and derivatives), with less developed or ‘upgraded’ secondary and services sector. Table 3 shows African oil rich countries’ export-specialisation category based on Trade Map 2018.

Export-Specialisation Category Based on Trade Map 2018

The table indicates that Nigeria is among top 10 oil producing countries in Africa that are not diversified and operate 90–98 per cent oil export-specialised economy. Only 6 out of 20 economies of oil producing countries in Africa are diversified. Figure 2 shows how the poor management of the economy amidst the ravaging coronavirus has negatively impacted on Nigeria’s economy.

The danger as portrayed in Figure 2 is that an excessively fuel-export dependent country such as Nigeria is extremely vulnerable to the world oil price crashes occasioned by the ravaging COVID-19 pandemic. Nigeria’s oil dependent status and the tendency of the oil industry to be volatile make it difficult to solely on the oil industry for economic recovery in post COVID-19 (Chinery et al., 2020). Hence, ‘The current fall in oil prices is limiting the ability of oil export dependent countries to respond to the multidimensional domestic pressures produced by COVID-19, at a time when more money is needed to finance service delivery, mitigate health risks and ease macroeconomic pressure’ (OECD, 2020, p. 4). Nigeria thus lost between 50 per cent and 85 per cent in net income for 2020 compared with 2019—this being the lowest in two decades. There has been a drastic decline in investor appetite for fossil fuel projects, and with the onset of COVID-19, oil companies in Nigeria have shelved new projects and permanently shut down high-cost operations in response to the oil price collapse (OECD, 2020).

The Rentier State and COVID-19 Containment Responses

The term rentier state has been used since the twentieth century. It is most frequently applied to states rich in highly valued natural resources such as petroleum. A rentier state is a state that derives all or a substantial portion of its national revenues from the rent of indigenous resources to external clients. This theory was first postulated by Hossein Mahdavy in 1970 (Mahdavy, 1970, p. 9). In rentier capitalism the predominance of capital derived from external rents and royalties of multinational oil companies for national economic development is significantly low, compared to the intensity of perceived exploitation of the rent-payers (Abulof, 2015).

Rentier state theory has some important assumptions. Hazem Al Beblawi and Giacomo Luciani put forward four characteristics of a rentier state:

Rent situations predominate. The economy relies on a substantial external rent—and therefore does not require a strong domestic productive sector. Only a small proportion of the working population is actually involved in the generation of the rent. Perhaps most importantly, the state’s government is the principal recipient of the external rent (Beblawi & Luciani, 1987, p. 8).

Nigeria depicts a rentier state which derives a substantial portion of its national revenues from ‘external rents’. The external clients involve the multinational oil companies that dominate the Nigerian oil sector. Since the 1970s, crude oil production accounted for about 80 per cent of Nigeria’s revenue and 95 per cent of export earnings. Beblawi and Luciani (1987, p. 8) further argued that ‘local laws often make it impossible for foreign companies to operate independently…. To do business, foreign enterprises engage a local sponsor who allows the company to trade in their name in return for a proportion of the proceeds—another type of rent. In addition, the oil rent leads to secondary rents, usually stock market or real estate speculation’.

The rentier state analysts posit that in resource-rich rentier states there is a challenge to national development and democratisation (Anderson, 1987, p. 1). In the case of Nigeria, for example, the process of award of oil blocks to cronies and cabals of the ruling elites in Nigeria are not ‘democratized’, transparent or are arbitrary to existing laws made by the same ruling elites (Nigeria Petroleum Act, 2004). This shows a connecting link between the lack of transparency, due process and corruption in the oil mining awards, and the inability to reinvest or diversify oil rents into other productive sectors.

Beblawi and Luciani identify several other characteristics associated with rentier oil states. They noted that while many states export resources or license their development by foreign partners, rentier states are characterised by the relative absence of revenue from domestic taxation, as the naturally occurring wealth precludes the need to extract substantial income from their citizenry. According to Douglas Yate (Yate, cited in Beblawi & Luciani, 1987, p. 8), the economic behaviour of a rentier state embodies a break in the work-reward causation…rewards of income and wealth for the rentier do not come as the result of work but rather are the result of chance or situation. This could create a ‘rentier mentality’. Hence, in rentier states like Nigeria where there is low export-diversification and overreliance on oil-exports, there is relative absence of substantial revenue from domestic investment and taxation. In the absence of having a well diversified productive economy the government is forced to ‘bribe’ the citizenry with extensive social welfare programs to the extent of becoming an allocation or distributive state. Noah Feldman argues that the government is forced to keep its people in line so that they do not overthrow it and start collecting oil rents themselves (Feldman, 2003, p. 10).

Kurtz and Brooks (2011) show that natural resource rents could be a curse or blessing depending on applicable public policy relating to human capital formation and economic development. Unfortunately, the oil rents collected in Nigeria are not properly reinvested to develop human capital, entrepreneurship and local capacity building for effective expansion of the productive base of the economy. The oil rents have been mostly misappropriated and used for political settlement between Nigerian oil actors and ruling elites. Schultze-Kraft (2013) contends that Nigerian oil actors (including top bureaucrats, political [party] leaders and ‘godfathers’, business moguls, retired military officers, Nigerian and international oil industry bosses) have vested interests in promoting or increasing their interests in Nigeria’s ‘oil sector’, which is lubricated via political settlement. Over many years, oil and the appropriation of oil rents by Nigerian oil actors and their international oil business partners have shaped this settlement (Ikein, 1990). The political settlement arrangements generally undermine transparency, accountability and due process in the oil sector. Smith (2004) concludes that there is apparent lack of success of democracy in rentier states.

Bayart et al. (1998) emphasise the predatory activities of Nigerian oil actors, which ‘criminalize’ the state, subvert it and enrich themselves (Iwuoha, 2021). The patrimonial political networks, corruption and state collapse thus strengthen the struggle for oil resources and the ungovernable nature of the oil economy.

This explains why some resource-abundant countries do not succeed in achieving national development (Torvik, 2009). A number of studies have established strong relationship between natural resource abundance and lower economic growth (Auty, 1993; Beblawi & Luciani, 1987; Havranek et al., 2016; Hodler, 2006; Ross, 1999, 2012, 2015; Sachs & Warner, 1995; van der Ploeg, 2011). Most oil resource abundance countries fail to achieve economic growth and national development as a result of some factors such as how resource wealth is spent, type of government, nature of resources, institutional quality (Mehlum et al., 2006), early/later industrialisation (Gylfason & Zoega, 2006; Torvik, 2009) and high volatility of export commodity prices (van der Ploeg, 2011), which make long-term planning difficult. High price volatility induces more real exchange rate fluctuations and less investment leading to lower productivity and growth rate (Aghion et al., 2009). Consequently, economic diversification is either delayed or neglected in expectation of massive resource wealth (Ross, 2015), or simply because abundant resources are crowding out other activities that could stimulate economic growth and development. The resource sectors only provide few jobs and often lack backward and forward linkages to the rest of the economy (Ross, 2012). In this light, the Dutch disease case describes how a natural resource revenue windfall results to a contraction of the manufacturing sector, and low economic productivity. The IMF identifies about 51 countries that derive at least 20 per cent of exports or 20 per cent of financial revenue from non-renewable natural resources as ‘resource rich’. These countries experience common features such as (a) extreme dependence on resource endowment for financial revenue, export trade or both, (b) low savings, (c) limited growth rate and (d) high volatility of resource revenues (Venables, 2016).

Rentier state theory foregrounds the precarity and vulnerability of states such as Nigeria that rely substantially on external oil rents in the event of a sustained global oil crisis. The outbreak of COVID-19 pandemic caused significant disruptions in global oil security with uncontrollable declines in oil prices thus tightening the demand and supply curve in the global oil market. The COVID-19 containment strategies adopted to control the spread of the COVID-19 pandemic, including lockdowns and travel restrictions altered or halted the global economy with sudden and sharp drops in global oil demand, supply and consumption. Falloff in road and air travel resulted to an estimated 10 per cent cut in oil consumption from 2019, or about 10 mb/d. The ravaging COVID-19 pandemic and the consequent lull in global oil prices became twin nightmare to Nigeria. Hence, the Nigerian economy could not withstand or resist the extreme dual shocks of global oil crisis and the COVID-19 pandemic. This is mainly as a result of its low level of export diversification and monolithic dependence on external oil rents. In other words, the tightening of oil rents as a result of exigent lockdown and social distancing measures critically affected the capacity of Nigeria to mop up adequate capital to fight COVID-19 pandemic. With much of the accruable oil rents squandered over the years as a result of oil corruption, political settlement and lack of transparency and due process in the oil sector, Nigeria was unable to develop its health sector and equip it with modern healthcare facilities up to global standards as to effectively fight the spread of COVID-19. Nigeria strictly enforced lockdown measures against dissatisfied and poor citizens without adequate palliatives and economic incentives to cushion the effects of these measures on them. This aligns with White (2021) and OECD (2020) convictions that due to Nigeria’s sole dependence on oil export revenues and the tendency of the oil industry to be volatile, it will be difficult for it to sustain the devastating shock of COVID-19 and achieve economic recovery in post COVID-19.

Implementation of COVID-19 Strategic Containment Policies

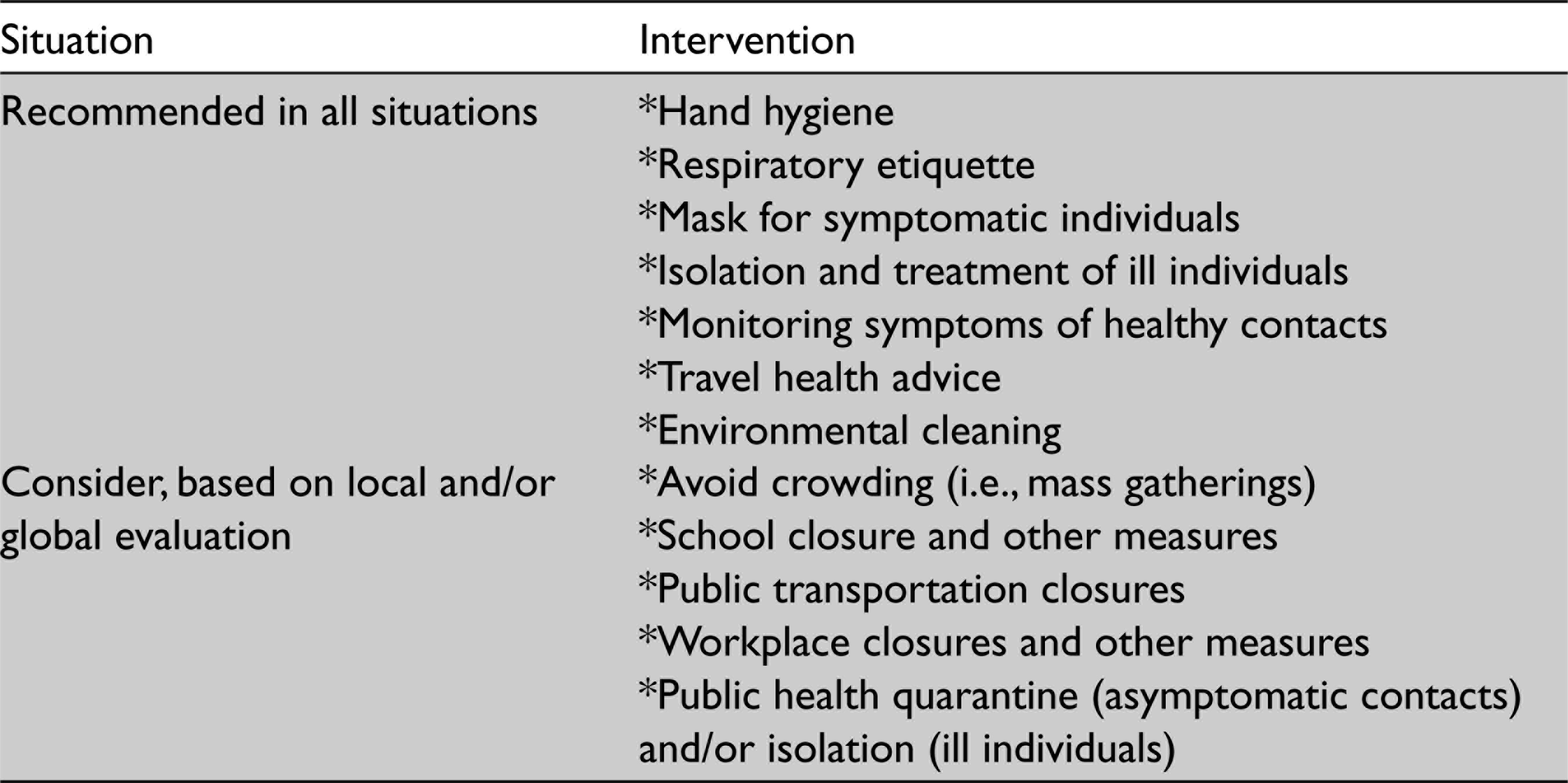

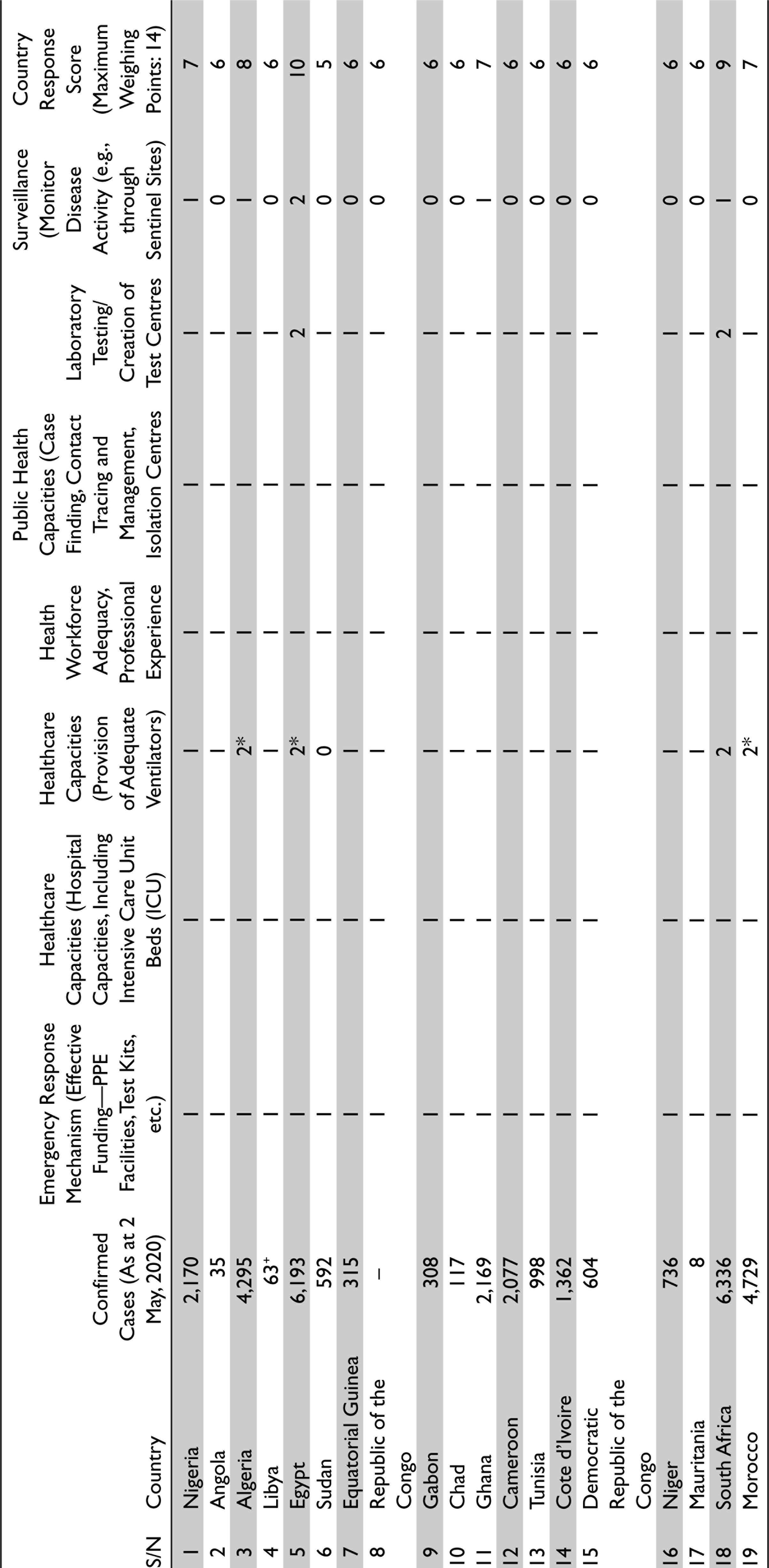

Amidst heavy oil revenue losses and massive budget cuts, Nigeria adopted and implemented some COVID-19 global measures such as ‘lockdown’, ‘social distancing’, travel restrictions, and so on (Table 4), in the form of ‘copy and paste’ without critically considering whether it could afford it (Soludo, 2020). Unfortunately, the containment measures were poorly implemented without proper recourse to the WHO COVID-19 public health risk assessment checklist. Table 5 assesses the level of Nigeria’s healthcare preparedness and emergency response capacities to handle and contain the COVID-19 pandemic at the early stage. Table 6 evaluates the level of implementation of COVID-19 public health and social measures, including the mitigation of its effects on the people at the early stage.

COVID-19 Public Health Measures

Table 5 shows lack of critical preparedness and readiness of the Nigerian public health system to handle COVID-19 crisis at the early stage. The Nigerian public health system lacks adequate capacity to trace, identify, test, isolate and care for cases and quarantine contacts as contained in the WHO assessment checklist on ‘Critical preparedness, readiness and response actions for COVID-19’ (WHO, 2020d). Nigeria scored 7 points against weighting factor of 14 points. Only Egypt could score 10 points against weighing factor of 14 points. South Africa and Algeria had 9 and 8 points each, respectively. Other African oil producing countries had less than 7 points, indicating less than 50 per cent preparedness in public health measures to contain COVID-19. Health professionals as well as medical equipment and personal protective gear are either lacking or in acute short supply. For example, with doctor to people ratio in Nigeria at one medical doctor for 6,000 thousand people, Nigeria needs 303,333 medical doctors to meet the World Health Organisation’s (WHO’s) recommendation on the doctor-to-patient ratio of 1:600 (Iwuoha et al., 2021b).

Africa’s Critical Preparedness, Readiness and Response Actions for COVID-19 (Based on WHO Methodological Framework/Weighing Factors on Public Health Measures)

Nigeria’s Minister of Finance, Budget and National Planning begged a South African-born American entrepreneur and business tycoon, Elon Musk, for ventilators through a tweet, ‘Dear @elonmusk @Tesla Federal Government of Nigeria needs support with 100–500 ventilators to assist with #COVID19 cases arising every day in Nigeria’ (Omilana, 2020). This shows that Nigeria could not afford the procurement of adequate ventilators, sold at between $15,000 and $24,000 each, to support COVID-19 infected people.

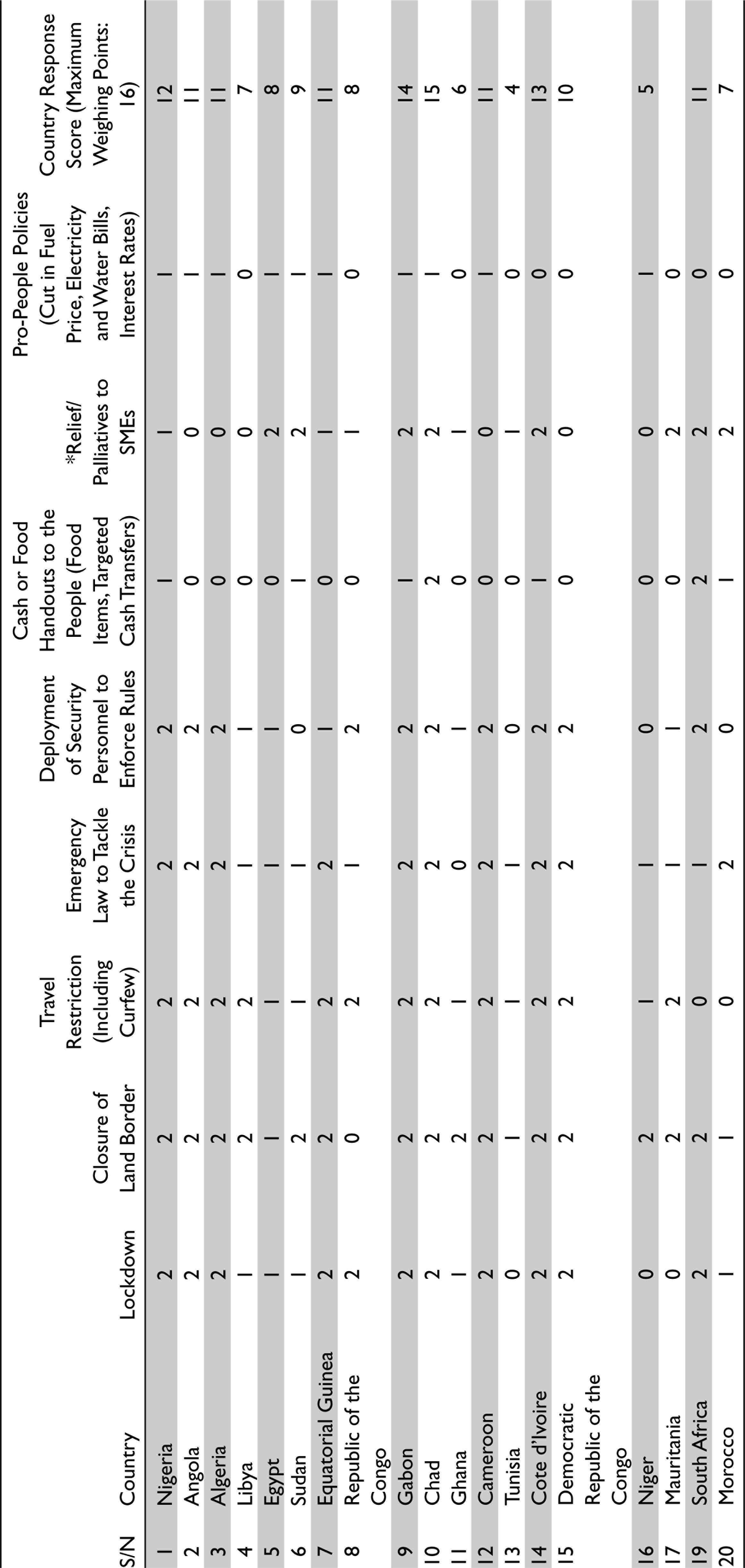

Critical Preparedness, Readiness and Response Actions for COVID-19 (Based on WHO Methodological Framework/Weighing Factors on Social Measures)

Table 6 indicates that Nigeria scored high points in implementation of social measures for COVID-19 containment. Nigeria scored 12 points against the overall weighing factor of 16 points—particularly on measures relating to the enforcement of lockdown, movement restriction, and deployment of security personnel to enforce rules; but scored very low or less than 20 per cent in the specific weighing for stimulus packages and palliative measures such as (i) cash or food handouts to the people, (ii) relief/palliatives to SMEs and (iii) pro-people policies. This shows that Nigeria deployed adequate security personnel to enforce strict lockdown measures and related protocols as recommended by WHO but failed abysmally in the aspect of implementation of robust stimulus packages and palliatives to cushion the economic effects of the lockdown policies on the people. Although the Nigerian government announced a stimulus package in May 2020, including food aid, direct cash transfers and loans for households, small- and medium-sized enterprises and key non-oil sectors early data showed that the actual outlays and numbers of people that benefited have been far lower than projections (Chinery et al., 2020; Onyekwena & Ekeruche, 2020; The World Bank, 2020a).

Nigeria slashed its 2020 budget by $5 billion and requested for $7 billion in emergency funding from the IMF (Parkinson & Faucon, 2020). By 16 April 2020, Nigeria had accessed N42.6 billion, including $50 million grant from the EU (IMF, 2020). With dwindling GDP growth for oil revenues which account for 90 per cent of Nigeria foreign exchange, Nigeria may face sever difficulties in its economic recovery measures in post COVID-19 (White, 2021). These realities show how Nigeria is boxed in, and trapped in the murky waters of economic uncertainties that may further bring it down to tatters in post-COVID-19. Public perceptions consider Nigerian government’s lockdown measures as elitist and not in the interest of the people, who are ‘forced’ to suffer the twin misfortune of the COVID-19 pandemic and excruciating hunger (Iwuoha et al., 2021a; Onuoha et al., 2021).

The contradictions and backlash from the inconsistency or inability to implement robust palliatives and economic stimulus alongside the COVID-19 lockdown measures have had a negative and reversal effect on the fight against COVID-19 pandemic in Nigeria (Iwuoha & Aniche, 2020). It has contributed significantly to the increase in the number of newly infected cases especially where the people are exposed to the infection while insisting on going out and finding a means to survive instead of remaining ‘locked-down’ at home and die of hunger. (Ibeanu, 2002b; Ikejiani-Clark, 2007).

Thus, critical healthcare facilities and infrastructures with which to fight COVID-19 pandemic are lacking thereby endangering the lives of millions of people. The investment climate is lacking with no capital formation, making it difficult for the manufacturing sector and SMEs to thrive. There are many poor people that need palliatives and economic stimulus packages in order cushion the effects of COVID-19 lockdowns and movement restrictions, but unfortunately the state lacks the financial resources to provide these. Instead, harsher and stricter economic measures and disempowerment policies are implemented such as salary cuts, public budget slashes, retrenchment, currency devaluation, etc., amidst unregulated commodity price hikes. This has further created structural pressures that undermine public compliance to the COVID-19 public health (containment) measures, thus escalating the number of infected cases.

Conclusion

This study adapts the WHO’s methodology: ‘Critical preparedness, readiness and response actions for COVID-19’ (WHO, 2020d), to flag the low level of healthcare preparedness and emergency response capacities of the African oil producing countries such as Nigeria to handle and contain the COVID-19 pandemic. It further showed that the COVID-19 public health and containment measures including the lockdowns were implemented at the expense of the people without adequate countercyclical stimulus packages and palliatives.

The study extracts the assumptions of the rentier state theory to flesh out the inherent contradictions in the articulation of African oil rich economies into the global oil economy as extreme oil-export dependent countries. There were many poor people amidst plenty oil wealth revenues in Nigeria, who need to receive some economic stimulus packages and palliatives in order to remain locked-down at home in the fight against COVID-19, but unfortunately the state lacked the financial resources to provide it adequately. This is mainly as a result of long years of mismanagement of oil rents, lack of accountability, transparency, due process and oil sector corruption—in which the ruling elites appropriate oil rents for political settlement and personal enrichment. With the disappearing oil windfalls and lack of financial resources to combat COVID-19 pandemic, Nigeria made some unhealthy sacrifices to the detriment of the people (national budget slashes, pay cuts for civil servants, harsh policies for SMEs, etc.) and relied on financial help/loan from the international community, philanthropist and charity donors to combat the spread of COVID-19 pandemic.

Theoretically, this shows that despite the bourgeoning oil rents, oil-export dependent countries such as Nigeria cannot effectively overcome the challenges of a sustained dual shock of global oil crisis and global pandemic put together. However, some lessons can be learned by African oil-export dependent countries from these developments. The dual shock of global oil crisis and COVID-19 pandemic inevitably provokes the need to look inwards towards the path of economic self-reliance and export-trade diversification in Africa. The study recommends that Nigeria should undertake structural reforms, including increased non-oil sector investments, strict government accountability, fight against institutional corruption, increased provision of healthcare facilities, and effective provision of stimulus packages and palliatives to support the people.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.