Abstract

The current focus emphasizes the difficult choices faced by Indian management of the impossible trinity to manage import-led growth. The management highlights two mechanisms by which FDI (foreign direct investment) flows are easily substituted for short-run FII (foreign institutional investment) flows. First, GDP and its growth in an open economy framework and the associated international trade participation can clarify this substitution prospect. Specifically, this study develops reasoning whereby imports under the trilemma management can give some decisive advantage to FII at the cost of FDI to manage Indian import-led growth. Second, it underlines how the related policies, especially the sterilization interventions, constrain the interactions of higher domestic investments (domestic savings), spillover impacts of imports of intermediate and capital goods, and specialized FDI. If so, the Indian economy’s import-led growth can indicate FII and FDI tradeoffs. The study uses the ARDL regression method. The results show that the Indian policy-led macro environment can limit the scope of specialized FDI that aims to induce advanced domestic investment, exports, and FDI interactions. India’s focus on import-led growth thereby underpins how FII substitutes FDI.

Keywords

Introduction

India’s post-1991 market reform period witnessed an import increase that exemplifies the economy’s status as an import surplus. This indicates savings–investment imbalances that must be supported by capital inflows. The inflows should also help reduce possible stress created by the lack of adequate foreign exchange reserves. The purpose of the article is to develop an argument underscoring how the Indian management of imports could highlight a bias toward short-term portfolio capital flows that can come at the cost of more important foreign direct investment (FDI) types of flows. The basic Indian policy stance and the issues and research interests it raises need elaboration.

The Indian policy recognizes that imports are essential in removing supply constraints and supporting a competitive-led restructuring of Indian industries (Srinivasan, 1998). Additionally, the imports of intermediate and capital goods make possible the transition to a higher technological frontier with the capacity to produce greater varieties of sophisticated products (Goldberg et al., 2010). New endogenous growth (Romer, 1986; 1990) suggests that continuity of the imports comes with technological progress and can support serious growth. The higher income (and profitability of firms) would induce non-debt type of portfolio capital inflows and sustain higher investments to permit growth. India has witnessed capital inflows dominated by portfolio investments of foreign institutional investments (FIIs) (Errunza, 1986; Mohan & Kapur, 2009).

However, periodic higher FIIs unrelated to trade imbalances can exert pressure on foreign exchange rates. An appreciation of the domestic currency with the resultant increased trade imbalances could leave the economy at risk of over-dependence on capital inflows. Facing excessive capital inflows, developing countries such as India have periodically opted for policies that regulate the foreign exchange rate via the purchase of foreign currencies, which also adds to the much-needed foreign exchange reserves.

The Mundell-Fleming “impossible trinity” thesis suggests that such interventions in the foreign exchange market would be accompanied by a higher injection of base money and, therefore, a money supply that could cause both lower interest rates and higher inflationary pressures. Such developments can, in turn, negate capital inflows. The monetary policy in India and other Asian countries, however, manages the trilemma by relying on a sterilization process to negate the increased money supply (Frankel, 1999; Grenville, 2011; for Indian perspectives, see Mohan & Kapur, 2009; Reserve Bank of India [RBI], 2003; Sengupta, 2015). In doing so, the policy can regulate foreign exchange rates aligned with the fundamentals of the balance of payments (BoP) without sacrificing an independent monetary policy. This can manage possible inflation arising from an excess money supply or overheating of the economy.

Allowing for price stability as the critical Indian policy focal point that best maintains savings-led growth, the present article holds on to a strict but perhaps internally consistent version of the management of the trilemma in India. Assuming that import surplus-led growth necessitates capital flows to supplement domestic savings and domestic interest rates are set to maintain a low inflation regime, the trilemma management entails specific domestic demand management. It strives to maintain the identity: imports (M) –− exports (X) = investment (I) –− domestic savings (S). This price stability-centric macro balance provides the best adjustments to imports and the resultant growth prospects. However, one implication is that capital flows more than M –− X would then mean fewer incentives for higher domestic investment that correlate with domestic savings.

Research Gaps and Interests

Existing Indian literature in dealing with the management of a trilemma focuses more on the efficacy of the management. According to Mohan and Kapur (2009), the management has resulted in the non-debt types of capital flows that can support import-led growth. There are, however, instances of capital flight. Eichengreen and Gupta (2014) and Basu et al. (2014–2015), argue that periodic capital flights could be due to the tapering of security purchases by advanced countries, especially the US. Additionally, the import-led growth can be maintained or its volatility contained if an economy has the advantage of enough foreign exchange reserves, a depreciating rupee aligned to the fundamentals of the BoP, and an independent and proper money and credit policy that keeps inflation adequately anchored. On the contrary, Patnaik and Shah (2012) believe that the sterilization policy is a partial success; the real rate of interest in the period has seen a declining trend. Therefore, interventions in the foreign exchange markets could be the main reason behind capital flight; the trilemma logic still holds.

What this literature neglects is that the management of the trilemma is a workable option when FIIs are guided not solely by interest rate differentials but by other dominating factors, such as relative profit rates (Grenville, 2011). If interest rate differentials are the only factor at play, Patnaik and Shah could be right that Indian capital control causes capital flights. It is just not possible to completely control bank lending through sterilization.

Effective management of the trilemma, therefore, demands that imports open up a transition to a new technological frontier. Higher growth and a higher Indian profit rate can guide capital flows despite the low interest rates. This possibility raises another issue. If imports add to working capital and semi-processed or final goods inventories, the import surplus can depend on short-run capital flows. On the contrary, if the focus remains on the imports of durable fixed capital goods, which explains the higher profits, long-run capital flows would be crucial and should accompany the indicated import surplus.

Montiel and Reinhart (1999) argue that the need for foreign exchange reserves, the interventions in the foreign exchange markets, and especially the attendant sterilization policy aimed at M − X = I − S could translate into a preference for capital flows that would be short-run in nature. To elaborate, the basic policy focus remains on regulating credit via a higher interest rate. In doing so, it primarily considers the capital inflows as short-run flows, and the close substitution between debt and portfolio flows remains relevant.

Recourse to the sterilization policy is also problematic. One way or the other, it translates into banks’ holding more liquid government bills that are used to mop off the excess money supply. These are, in a way, money waiting in the wings. Banks flushed with liquid, risk-free assets tend to take higher risks elsewhere. Since the regulation of the money supply or short-term interest rates to manage inflation is in place, short-run working capital loans would have to move in tandem with long-term fixed capital-based loans. There is then an incentive for banks to focus more on long-term lending while holding short-term deposits (for more on the financial crisis implications, refer, Dasgupta et al., 2000).

This asset and liability mismatch and the problems with risks could be expected to be less severe in the high growth phase, which can ensure higher returns to the fixed assets and the underlying long-term loans. However, the policy focus shifts to how best to manage long-run growth prospects. Therefore, the policy should focus on a preference for long-run capital flows, FDI, which closely connects with the aspirations for more stable and developed growth prospects.

One issue is that the current policy views FDI as merely market-seeking, quite similar to the objective of FII; hence, import-led growth in an open economy framework can help guide both FDI and FII flows. What is neglected in this discussion is the policy stance that provides the best import-led market outlook, and a greater incentive to FIIs can come with some costs in the form of the sacrifice of long-run FDI inflows (refer the next section on the costs of policy stance I).

Furthermore, while FDI is market-seeking, Dunning (1993) differentiates between resource (and cheap labor)-seeking FDI and efficiency and asset-seeking FDI. The recent pattern of FDI in emerging countries (Dunning, 2002; Noorbakhsh et al., 2001) suggests domination by the latter types that seek locations or countries with advanced domestic production bases providing advantages to specialized FDI.

In this focus, import-led growth or import spillovers can induce domestic investments that are more productive and define an advanced domestic production status. The advanced development status induces advanced FDI, which can reinforce the domestic production base (refer the section on the cost of policy stance).

This article highlights how the current management of Indian import-led growth neglects the advanced domestic investment prospects that can induce specialized FDI. The current policy stance demonstrates a preference for FII flows and an FII-centric aggregate demand management-led macro balance in which a higher FII than an import surplus is accompanied by sterilization intervention and liquidity management that must target fewer domestic savings. This, in turn, negates possible higher domestic investments that can correlate with higher domestic savings, seen as the spillover impacts of imports.

Put differently, the current policy stance adopts a narrow, static, and short-term view. Every situation of “higher” domestic investments greater than domestic and foreign savings, allowing for an import surplus, is problematic and seen as an overheating situation. Therefore, it neglects the dynamic issues of how imports can create spill-over and induce higher domestic investments that add to the potential output and domestic savings. The policy stance then closes out a transition to a more advanced domestic developed status reinforced by interactions with specialized FDI and macro balance that can replace FII with FDI flows.

In this sense, the inquiry into the specificity of the nature of capital flow remains an important policy focus. Specifically, the prospects of the long-run capital flows can strengthen the domestic long-run capital market aligned more with productive domestic investments and FDI interactions. Does the management of the Indian import-led growth neglect this? To discuss these issues, the article is organized as follows. First, the two mechanisms by which the current policy stance can underpin the tradeoff between FII and FDI are discussed. Subsequently, the empirical hypotheses and methodology are presented. This is followed by a discussion of the results. Finally, the conclusions are presented.

Costs of Policy Stance I: Imports and FDI and FII Trade-Offs

The Indian management of the impossible trinity targets liquidity management and foreign exchange rate aligned with the trade deficits that allow the needed capital flows. The resultant investment takes place in a low inflation regime and enables the economy the best possible adjustment to import-led reallocation of resources.

This has an important implication for long-run FDI. Heckscher-Ohlin-Samuelson’s international trade framework, assuming production functions are identical, suggests that international trade involves a direct exchange of production factors and can substitute FDI (Liu et al., 2001; Mundell, 1957). The Indian policy of maintaining a favorable environment towards imports could mean less FDI.

Indian imports-led growth and the policy stance also support a substitution between FII and FDI from another perspective. Goldstein and Razin (2006) maintain that the choice between liquidity and profitability determines whether investors in the source country choose FDI or FII capital flows. Suppose the expected payoff from investment is guided by

Where k is the investment commitments and C is the production costs in a host country. A higher k with an unchanged or lower C permits a lower payoff in this functional relation. Further, it is assumed that productivity shocks, p, permit lower C, or p = 1/C

The advantage of FDI is that the investors are also managers and can control p to control both optimal k and C. Then, the payoff to FDI would be higher than the payoffs associated with FII, or we have:

At the same time, FDI involves some costs. There is a fixed cost, lc, relating to the expertise needed to manage liquidity costs. A liquidity constraint is operative when the investors have to sell their project at a given time. However, this decision is guided by higher C and therefore fetches a lower selling price (or higher lc). The greater the liquidity shocks anticipated by the firm and the lower the prospects of recovery of the assets by a sell, the lower would be the incentive to commit to FDI 1 . The higher the fixed and liquidity costs, the lower would be the incentive for choosing the FDI route.

Given this understanding, the nature of FII in India could highlight how the Indian policy stance provides it with relative advantages. The FII targets domestic firms with access to imported intermediate and capital goods. Indian policy permits firms the best advantage to adapt to the import-led new technological frontier and realize higher profits. In other words, FII, indirectly, through the management of Indian firms, best manages the productivity shocks and the uses of the optimal capital stock. If it is (reasonably) assumed that Indian firms are in a better position to manage the local conditions for making the technology operational, say with lower c and C, the payoffs for FIIs would also be higher than FDI. The policy stance that permits the profitability of Indian firms and growth prospects of the firms and aligns the depreciating rupee with the trade imbalances tilts the balance in favor of FIIs. Higher FIIs would substitute FDI.

With less restrictive assumptions, Dunning’s (1980) eclectic approach also suggests that FDI is market-seeking per se. Higher local transactions and production costs make global firms anxious about moving from FDI to exports. Trade can substitute FDI.

Costs of Policy Stance II: Growth and FII and FDI Trade Off

The relationship between FDI and trade is also a function of the motives of the firms that undertake FDI. If the motive is market seeking, FDI and trade are substitutes, as discussed previously. The situation changes dramatically if FDI refers to an efficiency and assets-seeking global firm that aims to locate in a country providing the best advantage to reinforce its assets (and efficiency), adding to its competitive advantage (Dunning, 1993). Import of intermediate and capital goods can add to the advanced domestic “growth” that provides an advantage to FDI. FII supporting the imports-led domestic advantages and FDI can play complementary roles.

To elaborate, imports of capital and intermediate goods add to advanced growth that typifies the constant coming up of new varieties of products (Goldberg et al., 2010). Following Aghion and Howitt’s (2009, pp. 77–78) growth accounting, productivity parameter A and labor force L define an effective supply of labor force AL. If varieties of intermediate goods zit are bounded from 1 to V and elasticity of substitution between the intermediate goods e is greater than unity but low, the production function is:

where “a” is the share of labor that incorporates returns to specialization, a market power-based return specific to monopolistic competition. If inputs are used with same intensity, z, we have:

Since inputs are used one-for-one (i.e., each input requires specialized machinery specific to it), and we have capital goods, K = Vz, then:

Taking logs, we have the growth accounting as follows:

In this reformulated Solow residue form, if “A” denotes the contribution of quality and V denotes the contribution of variety; the contribution of variety is guided by the values of “e” and “a”. Lower “e” and higher “a” would reflect a greater contribution of varieties that denotes the advanced status of Y.

The specification of “e” indicates an advanced status that comes with a love for varieties. Suppose a specialized labor force indexed to varieties of specialized intermediate inputs adds to new varieties of products, a greater preference (and substitution) for them would be associated with a higher share of varieties. Further, if the specialized labor force permits more effective production of varieties, the greater share of varieties would also be associated with a higher share of wage income. Taking specialized labor force as the only input results in a higher aggregate income (for a different specification involving capital and labor, see Grossman et al., 2017; Rodriguez-Clare, 1996).

The specification of the elasticity of substitution parameter indicates increasing returns to specialization. Addition to specialization implies higher returns to specialized inputs. This provides the incentive for higher domestic and FDI investments that involve more productive and specialization-seeking investments.

Taking up prospects of FDI first, it should not be guided solely by an import-based growth of varieties. If FDI brings in similar types of imports and has a domestic market orientation, as in case I seen earlier, FIIs would have a decisive advantage over FDI.

The focus should be on how import-led growth adds to an advanced status of human and knowledge capital-intensive domestic industrial base. This would provide the FDI-specific firms an opportunity for complementary specializations or carrying out their specializations more cost-effectively (Bandick & Hanssson, 2009; Morgan & Wakelin, 2001; Slaughter, 2002). If domestic capabilities are in place, FDI could also outsource many specialized tasks to domestic firms if it is cost-effective and this adds to a more significant competitive advantage. In addition, following Krugman (1991) and Gray (1998), a focus can be on specialized FDI aiming at greater specialization in a variety of products. Its preference would be locations that provide specialized labor force-related advantages. FDI in these instances can reinforce prospects of domestic advanced investments creating a growth impact (Alfaro et al., 2006).

The greater specialization or cost-effective specification also permits export-oriented FDI, making it complementary to trade (Krugman, 1991). A greater specialization, and greater competitive advantage on a global scale, allow FDI to take advantage of exports. FDI can be viewed as bringing in imports of intermediate and capital goods that can be used for exports (Liu et al., 2001).

Beyond permitting transitional growth to a higher technological frontier, the imports will also add to domestic capabilities. As discussed earlier, Aghion and Howitt also model that if imports induce advanced growth with a love for varieties, with the elasticity of substitution parameter being greater than one, then imports-led growth can induce new domestic investment opportunities that aim at greater specialization.

This needs further elaboration. Imports can confer Scitovksian higher profitability and pecuniary external economies’ advantages to domestic and reallocated international savings-led expansions (Krugman, 1991). Perhaps more importantly, imports can create knowledge spillover and new investment opportunities. A focus can be on how imports (and FDI) support Youngian (Young, 1928) technological external economies in the sense that the introduction of new specializations by a few firms induces others to adopt these methods (Padhi, 2019). Such investment-led expansions demand some financial arrangements that permit these macro investments more than what would be allowed by existing savings. 2 An important condition is that the investment should be productive and should increase income and savings to make the financial arrangement workable and stable.

Much, therefore, depends on whether imports permit the spill-over impacts that define advanced domestic specializations and whether the financial arrangement allows these new investments. As Alfaro and Chauvin (2020) cautioned, the availability of finance that can support higher induced domestic investments and capabilities plays a key role in bringing into play the growth impacts of FDI.

However, the financial arrangement under the trilemma management and the sterilization interventions might not permit the new investments. In addition, it is possible that increased imports of intermediate and capital goods (Goldberg et al., 2010) stipulate higher fixed costs-led expansions to realize higher scale economies (and higher market power-based compensations to the fixed costs) (Murphy et al., 1989). The current Indian policy stance and aggregate demand management aims at this full employment outcome. However, the underlying financial arrangement, a (domestic and foreign) savings-led adjustment to imports, can only indicate a “full employment” outcome in which expansion by some would have to be associated with contraction in others. Moreover, the full employment outcome, the realization of market power, not only makes the concerned firms more domestic market-oriented (Padhi, 2013) but also, the resultant market structure in favor of the importing firms could negate potential competition and such new investments may be seen as spill-overs of imports.

Therefore, a policy stance that visualizes FII-led macro balance to allow the best adaptation to imports can neglect the imports-led spill-overs. This inattention to import-led expansions by all firms, both importing and others, that involves new investment opportunities and higher domestic investments (savings) can highlight FII and FDI trade-offs.

Empirical Hypotheses, Data, and Methodology

Empirical Hypotheses

Existing Indian literature mainly focuses on how a higher growth of GDP, perhaps in an open economy framework that comes with a capital flow-centric macro balance (and such credit rating) and a foreign exchange rate aligned with the balance of payments, would guide FDI (Bhanumurthy et al., 2014; Dua & Garg, 2015; Suri, 2008). This literature also underpins the additional roles of institutions, especially in emerging economies (Asongu et al., 2018; Paul & Jadhav, 2019; Walsh & Yu, 2010). The related Indian studies also highlight the related roles of export processing zones augmented by skilled labor forces and cheap raw material availability and the provision of fiscal benefits that specifically target export-oriented FDI (Ahluwalia, 2006; Ministry of Commerce and Industry, 2011).

The studies cited earlier suggest both FII and FDI are market-seeking and the market size, GDP, and its growth, become the main determinants. Assuming that Indian growth is ascribed mainly to imports (Maitra, 2020) and that the related policies provide the best incentives for firms to make import-based adjustments to obtain higher profits, this international trade participation can favor FII types at the expense of FDI (see, the previous section on the costs of policy stance I).

The Indian economy conforms the macro-economic determinants to an open economy framework. The present study limits itself to demonstrating how international trade participation explains the nature of capital flows. Hence, the empirical specification is:

In this equation, in Indian policy-making, depreciation that is aligned with BoP is the main policy option that signals capital flow. It is expected that such a policy would induce both FII and FDI. However, the section on the costs of policy stance I holds that trade or import supported by portfolio capital flows (or FII) would show trade substituting the FDI hypothesis.

Another important policy focal point is the management of import-led growth through managing the trilemma that can negate advanced domestic investments and export-successes’ interactions. This can favor FII at the cost of advanced FDI.

Therefore, the empirical evaluation of the present Indian management of trilemma also focuses on whether import-led technological dynamism creates spillovers and supports advanced domestic growth of varieties that can induce higher FDI. Such growth prospects will be associated with both advanced domestic investments and export successes. The present focus is not on the higher domestic investments that equal FIIs or capital flows and domestic savings, which is the case under the management of the trilemma policy options. If the policy negates import-led spillovers and such higher domestic investments, it should cause higher portfolio capital flows to domestic investment ratio. It can also cause less export success. Both, as discussed earlier in the section on the costs of policy stance II, can reduce FDI inflows or cause FII to substitute FDI. On the contrary, a greater scope of actualizing import spillovers and such dynamism can support FII and FDI complementarity.

An evaluation of the Indian import-led growth then is whether it supports:

The focus here is not only on the export possibilities that can guide FDI, but also, on imports adding to spill-over advanced investments, and such advanced growth of varieties should translate into higher manufacturing exports. The presumption is that the higher the share of manufacturing exports, the higher would be advanced intermediate goods and specialized tasks. Such opportunities would induce FDI as a specialized firm. The share of manufacturing exports could become important in explaining export-based FDI.

Data and Period of Analyses

The main data on FDI, FII, exports, and imports were obtained from the Reserve Bank of India (rbi.org.in). The study relies both on RBI and EPWRF (epwrf.in) for the national account-based data on the net domestic capital formation (2004–2005 base year). The choice of the period relates to the study’s focus on how effective was the management of India’s import-led growth and the technological dynamism under the trilemma management. The management of trilemma is held to be workable when capital inflows are guided not by interest rate differential, but by higher profitability that comes with higher growth. A related issue is whether the high growth phase induces advanced domestic investments and FDI, or if under the management of trilemma this causes a preference for FII at the cost of FDI.

India has seen a proper revival of growth in the post-1991 market reform period attributable to the role of imports. The period also saw a high growth phase from 2004 to 2008. Later, in response to the 2008 global financial crisis, there was a sudden reversal of capital flows and higher inflationary pressures, marked by a growth slowdown. Though growth effects were not immediately discernable, growth momentum was maintained till 2010. The post-2010 period marks a slowdown with a major reversal of capital flows. As held in the article, a slowdown phase indicates lower profitability, and since capital flows are expected to be primarily guided by interest rate differentials, the management of the trilemma becomes problematic. Further, the tapering of US security purchases in 2013 saw a capital flight and highlighted the volatility of capital flows-centric growth. Therefore, changes in the capital flows in the post-2010 period may not be directly related to the Indian import-led growth and using this period for the study could demand a much broader framework of analysis that goes beyond the scope of the present study. Hence, given the adopted framework of studying how Indian import-led growth is managed, the present study focuses on the period from 1991 to 2010.

However, to compare how the results of the period stand in comparison to a more extended period that includes post-2010 periods, the present study also incorporates the period from 1991 to 2019. Despite the prospects of independent capital flights, how capital flows and their structure relate to some basic variables is taken up in the study to compare the results in the growth phase with the slowdown trends.

Regarding FDI flows, the Reserve bank of India (rbi.org.in) provides two sets of data: an old series available for the 1991–2010 period that refers mainly to equity investments and long-run debts transitions to define FDI by the old methodology; and a new series from 2001 to recent times that follows the IMF BoP Manual which provides a new calculation of FDI including retained earnings and all types of debt transactions between parent and affiliates. The new series data is available only after 2001 and is not comparable to the old ones (The Times of India, 2003). Therefore, the present study uses the old series data that is also available for a longer period. In addition, the old version of the FDI data can distinguish between equity and debt components that are not available separately in the new series data.

The data reveals a decrease in the share of FDI inflows in total private foreign investment inflows in India, from 97% in 1991 to 19% in 2010. This indicates a decrease of 6.36% per annum during the period. The decline in the ratio may be due to a phenomenal increase in FII in recent years, a growth of 5.24% per annum between 1991 and 2010 that could outpace the possible “normal” growth of FDI. The higher growth recorded for FII could also be due to its low level of inflow in the initial years. However, as held in the present article, the decrease in the ratio could be a cause for concern. The focus then is on how the reduction in the share of FDI in total capital flows could be accounted for by the policy stance that maintains the imports and portfolio capital flow nexus and comes with a depreciating domestic currency. Further, the post-2010 slowdown of imports-led growth (and FIIs) shows an increase in FDI to total capital flows. Therefore, the current focus on a study of import-led growth and how it is managed assumes importance.

Methodology

One constraint that time series regression analyses face is the prospect of spurious results, especially when time series data move together and some correlation is expected. The related variables are non-stationary: means and variances of variables are not constant but depend on time. The solution suggests using data of a more extended period or using a larger sample equal to or greater than 30 observations that can rely on unit root-based cointegration techniques to show stationarity and, therefore, avoid spurious relationships. However, the methods (e.g., Johansen cointegration tests) face some significant constraints, such as strict pre-determined lag structures and stationarity properties of the data (in which variables have to be stationary at levels or at their first difference), the presence of multiple cointegrating vectors, etc. In these instances, the inferences drawn from the methods might not be reliable (Ghouse et al., 2021; Nkoro & Uko, 2016).

The present study uses time series data, but as the sample size is relatively small, the ARDL method provides some specific advantages. The technique provides a bound test (Pesaran et al., 2001), a test of cointegration that identifies a single non-spurious long-run relationship between the underlying variables (otherwise the ARDL method is inapplicable). The determination of such long-run relationship in a small sample size less than or equal to 30 observations, is robust (Haug, 2002; Narayan, 2005; Nkoro & Uko, 2016). Second, another advantage is that Johansen cointegration demands all variables to be integrated to the same order, stationary at level I(0) or at first differences I(1), while ARDL can be used when some variables are I(0) while others are I(1).

Instead of relying on larger samples and normality of the data to generate cointegration, ARDL’s method using a small sample size suggests that cointegration can be generated by the incorporation of lagged values (of both dependent and independent variables). Further, since for a small sample (less than 30 observations), the normality test is violated, the critical (lower and upper bound) values of the bound tests for identifying significant cointegration need adjustments. Narayan (2005) and Kripfganz and Schneider (2018) suggest that the requirements of bound tests can be lower when used in small samples; they cite numerous studies that use a small sample of around 20 annual observations.

The critical values may vary according to sample size. In such cases, sufficient care should be taken to avoid distortion of cointegration tests due to specification errors arising in serial correlation (Pesaran et al., 2001). This demands a proper specification of lag-length. Instead of a pre-determined lag length, which is otherwise important to control non-normality, serial correlation, etc., the ARDL method gives more options concerning the lag-lengths. It relies on the Akaike information criterion or Schwarz information criterion (SIC) to arrive at the optimal lag lengths of both dependent and independent variables (Nkoro & Uko, 2016).

The present study uses the SIC that stipulates two lag lengths. In addition, if the bound test shows a single long-run relationship, in applying the ARDL method, this selection of the maximum of two lags gives attention to the degree of freedom and the power of tests. Further, since it uses a small sample, maximum of two independent variables are used to control the degree of freedom. Given the small sample size, higher lags, and a larger set of explanatory variables would decrease the degree of freedom. This may be a greater problem when the ARDL method involves lagged values of both dependent and explanatory variables. In the results relating to a long period, from 1991 to 2019, taken up in the study, a lag length of four is chosen.

Taking Equation (1) in the section on the empirical hypotheses, for instance, an ARDL regression representation would require the estimation of how the share of FDI in total capital flows is dependent on the behavior of imports, conditioned by policy option for a depreciating rupee aligned with the BoP. The empirical specification would be:

where, εt is a random “disturbance” term and in particular, it should be serially independent.

A similar ARDL specification of Equations 2 and 3 in the same section then permits an empirical evaluation of the policy options facing the management of trilemma: Does it permit the dynamism associated with domestic investments, exports, and FDI interactions?

The lagged values would denote short-run dynamic growth effects, capturing higher standard deviations in the data. The focus is on whether the lagged effects of both independent and dependent variables generate a stable long-run association. The lagged terms denote short-run disequilibrium impacts, but if these converge to long-run associations, the relationships would be stable. This is tested by the significance of error correction mechanism (ECM) coefficient.

The present article reports ARDL results only when the bound test (F-statistics greater than upper bound) is significant and shows long-run stable relationship among the variables, that is, the ECM term is negative and significant. These statistics, along with the short-run dynamic results are not reported but can be made available on request. Similarly, the augmented Dicky–Fuller tests show the variables concerned are either I(0) or I(1) and demand the use of the ARDL method; these results along with the growth rates of the variables can also be made available on request.

Results and Discussions

Imports and FDI

Indian higher imports-led growth with trade imbalances and the consequent openness to capital flows also translated into managing the impossible trilemma. The immediate impact of the underlying interventions in the foreign exchange markets is a depreciation of the rupee (or maintenance of such managed deprecation aligned to the BoP). Whether or not depreciation adds to exports (Bhanumurthy et al., 2014), the greater need for imports that comes with a higher income elasticity of demand implies that depreciation will not negatively impact the growth of imports. Taking the log of the variables, the correlation coefficient between imports and depreciation is positive (0.79). The depreciation signals capital flows, especially inducing higher portfolio investment inflows and the correlation coefficient between portfolio capital flows and imports is 0.88.

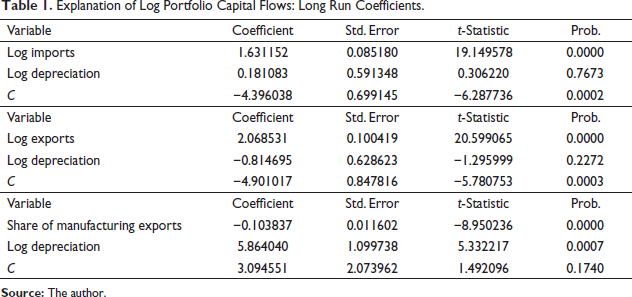

ARDL results suggest that imports positively and significantly explain the portfolio capital flows (Table 1). The coefficient of depreciation is positive but statistically not significant. That is, despite the Indian policy stance of keeping a depreciating local currency, as discussed earlier in the text, FII continues to be guided by import opportunities.

Explanation of Log Portfolio Capital Flows: Long Run Coefficients.

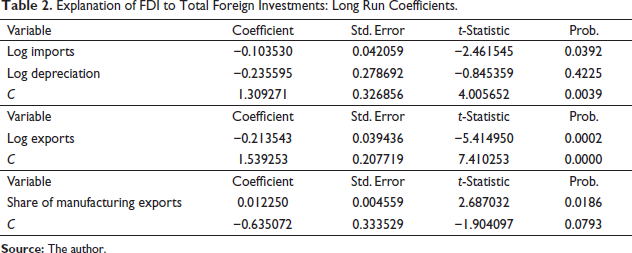

Perhaps more importantly, the results of Table 2 show imports negatively and significantly affect the share of FDI in total capital inflows. In this result, depreciation has a negative impact which supports the decrease in the share, but the coefficient is not statistically significant. Results (not reported) show imports, taken independently have a significant negative impact on the share of FDI in total foreign investments.

Explanation of FDI to Total Foreign Investments: Long Run Coefficients.

Exports and FDI

Taking depreciation as a conditional variable, the ARDL results in Table 1 indicate exports significantly and positively explain FII. However, Table 2 results show their impact on the share of FDI in total capital foreign investments is negative and statistically significant. As reasoned in the article, depreciation adds to exports that would come with higher import and trade imbalances. This explains why exports indicate higher FII capital flows as they sustain the trade imbalances.

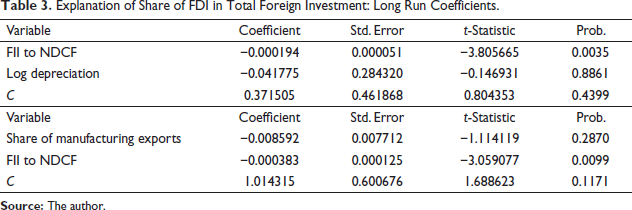

ARDL results in Table 1 indicate that the share of manufacturing exports negatively and significantly affects portfolio investments; while, Table 2 shows it positively and significantly affects the share of FDI. In other words, the decrease in the share of manufacturing exports is an important policy focal point and explains why Indian capital flows are more of portfolio types rather than export-orientation of FDI. One of the present arguments is the lack of both a higher share of manufacturing exports and FDI, which can be traced to the lack of a higher pace of domestic investments. Does the Indian experience show an interaction between FDI and domestic investments? The article hypothesizes that managing the trilemma associated with the sterilization policy (and such maintenance of macro balance) should translate into a higher portfolio to domestic investment ratio. Does this adversely affect FDI? Table 3 shows that FII to net domestic capital formation (NDCF) ratio has a negative and significant impact on the share of FDI to total foreign direct investment.

Explanation of Share of FDI in Total Foreign Investment: Long Run Coefficients.

Results for Period 1991–2019

To analyze a longer period inclusive of post-2010, one must consider the 2008 financial crisis. The impact of this was felt later, that is, after 2010, which includes the tapering of US security purchases, its adverse impact on capital flows to emerging countries, and a continuing slowdown of growth in India. How do such changes impact the earlier results? Despite these trends and volatility, how the nature of capital flows relates to some basic factors taken up in the study assumes importance because the data shows (not reported), that though exports, imports, and capital flows have decreased, however, the decrease in imports is more pronounced than the decrease in exports. Moreover, unlike the pre-2010 period, the share of manufacturing exports in this period witnessed an increase. In addition, the structure of capital flows tilted in favor of FDI.

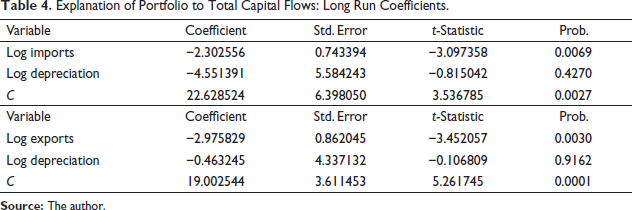

The ARDL results (not reported) show that, compared with the pre-2010 period results, there is a lack of significant explanatory influences of imports on FDI to total capital flows. However, Table 4 shows that the impact of imports, as the dependent variable is significant and negative on the portfolio to total capital flow ratio. This result is expected because the post-2010 capital flights could be ascribed to factors other than some indicators of well-functioning macro fundamentals in India.

Explanation of Portfolio to Total Capital Flows: Long Run Coefficients.

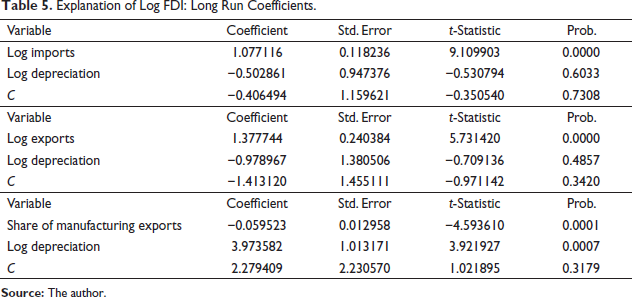

What is more important, in the period inclusive of the post-2010 slowdown of imports-led growth, is that imports positively and significantly explain FDI as indicated in Table 5.

Explanation of Log FDI: Long Run Coefficients.

Taking exports as the explanatory variable, Table 5 shows that exports positively and significantly influence FDI. In contrast, Table 4 shows that they have a negative and significant impact on the ratio of the portfolio to total capital flow. As held in this article, a greater export orientation or a slowdown of imports and import-led growth can shift the structure of capital flows in favor of FDI.

However, Table 5 shows that manufacturing exports have a negative and significant influence on FDI and therefore, a positive impact on the structure of capital flows in favor of FIIs (not reported). This result, contradicting the pre-2010 results, needs further elaboration. Taking all the relevant variables, such as exports, imports, capital flows, and so on, manufacturing exports is the only variable that shows an increase in the post-2010 period. Why has the revival of manufacturing exports not positively impacted FDI prospects? Perhaps, as has been held in the article, a mere revival of manufacturing exports, especially during the slowdown, might not be essential in explaining a higher FDI. The revival should be embedded in greater dynamism emanating from a higher pace of domestic investments. The interaction between these underpinning advanced domestic capabilities is the key to FDI. Table 6 shows that portfolio to the net domestic capital formation hurts FDI to total capital flows while controlling for exports.

Explanation of FDI to Total Capital Flows: Long Run Coefficients.

Put differently, managing the trilemma that favors a higher FII to domestic investment negatively impacts FDI. It can explain why the revival of manufacturing exports has not induced higher FDI. Therefore, the current management of the Indian import-led growth that negatively impacts the dynamism of domestic investment is significant in explaining the pattern of capital flows with a lower incidence of FDI.

Long-Run FDI Positions

FDI is mostly concerned with long-run positions in an economy. The financial arrangement underlying the maintenance of such positions could inform whether it is domestic market-oriented or exports oriented. FDI is not only a specialized firm in production but a multinational entity that decides the nature of intra-firm transactions to define its position in a country. Foreign investment capital inflow refers to the totality of capital inflows (or various instruments) by which foreign parents augment their assets in the affiliates in a country. Besides equity capital involving existing affiliates, it also includes the retained earnings of the affiliates assigned to the foreign parent and other “direct” capital (inter-corporate debt transactions involving the affiliates and their parents).

Equity flows could be driven by FDI seeking profitable domestic markets and how its stock market valuation signals prospects of higher availability of local loans or other sources of finance at favorable rates or attractive terms, respectively.

When one examines how existing FDIs strengthen their positions via retained earnings and within firm-specific debt flows, they represent a reallocation of foreign currency-denominated financial assets in favor of some specific country. Such expansion plans are associated with certain risks. Supposing a dollar gives a return of 5% in local currency, but higher import costs in the face of depreciation with less export earnings make the return to local currency riskier. The higher the prospects of trade imbalances, the greater the risk. The risk represents lower returns to a “loan” in foreign currency which also implies a lower risk-adjusted capital base of the foreign parent. A higher risk would either negate or cut back on its future expansion plans. If the loan or debt instrument were to be traded in the international capital market, local depreciation, higher import costs, and lower export earnings in a host country would mean lower returns in the foreign currency in which the loan is denominated. This implies a reduced assessment of what the securities are worth—a downgrading of foreign parents’ capital value (Friedman, 2000).

In other words, the fewer the export-related opportunities a country provides, the fewer the debt/retained earning commitments would be. The FDI flows would have a more significant bias towards equity flows which translates into how much finance in foreign currency is equivalent to domestic assets in local currency. The opportunities in the domestic markets would guide such domestic asset preference. The implication is that if the Indian policy stance sustains the nexus between portfolio capital flow, imports, and trade imbalances, they provide the incentives to FDI to become domestic market-oriented. A foreign parent would rely more on imports or equity that targets domestic markets. Taking the period from 2000 to 2010, the Economic Intelligence Service (2006; 2012) data shows that although equity investment (both FDI and FDI capital inflows) as a percentage of FDI capital inflows increased over time, the shares of re-investment capital inflows and debt inflows decreased, reflecting a lack of growth (exports) orientation of existing affiliates.

The data on this financial structure underlying FDI is only available for the period 2000–2010 which does not permit detailed analysis. This article relies on OLS estimates, recognizing that the focus would just be on the estimates of coefficients that come with no significant inferences. The results, taking equity to total FDI-related flows as the dependent variable, show.

Log (Equity/FDI) = −1.413 + 0.080 (2.300) Portfolio; R2 = 0.47 Log (Retained earnings/FDI) = −0.010 − 0.101 (−2.366) portfolio; R2 = 0.48 Log (Debt/FDI) = 4. 708 −0.653 (3.580) portfolio; R2 = 0.68 The R2 and t statistics (in brackets) show portfolio inflows, particularly, adversely impacting (FDI) debt inflow.

Conclusion

This article aims to assess the Indian management of import-led high-growth phases that can mark a transition to technological frontiers. Specifically, it evaluates the Indian management of import-led growth by managing the impossible trinity. The article’s primary contribution illustrates that the management favors capital flows of the portfolio types at the expense of a more dynamic FDI. Portfolio investment adds to domestic savings to define the desired higher investments in growth that come with an import surplus. However, imports and import-led growth provide a greater advantage to FII at the cost of FDI. In addition, the management undermines the spillover impact of imports of capital and intermediate goods that can support higher advanced domestic investment more than what would be supported by the existing domestic savings and import surpluses. This can also constrain possible export successes. Doing so gives a much-reduced scope to specialized FDI that aims at domestic investment and export interactions.

This evaluation also examines other policy implications. First, the sterilization policy underlying the trilemma management should not be stretched too far to offset import-led spillovers that would otherwise revitalize advanced domestic investment and ensure export success. The results suggest that if imports have spillovers and add to export successes or higher domestic investments, they can support higher FDI. Second, India should not rely only on GDP and its growth in an open economy framework to attract FDI. Such policy orientations are essential, but the open-economy framework should distinguish between FII and FDI flows or the nature of capital flows. FDI is guided mainly by the existence of developed domestic capabilities that can add force to its specializations. Third, even if debt types of portfolio investment show more volatility, policymakers should distinguish between such volatile debt flows and those related to long-run FDI positions. The present discussions show the considerations of long-run positions in a host country, which help guide higher prospects of FDI, and involve debt types of capital flows.

This study also clarifies why FDI in India remains domestic market-oriented (Agarwal, 2002; Ministry of Finance, 2003–2004). Imports remove the supply constraints facing an economy or target better supply chains, better inventory management, etc., embedded in higher technological dynamism. However, the Indian policy suggests that FIIs supporting domestic import-led growth also come with depreciation. Supposing the imports are price inelastic and come with higher income elasticity of demand without hinting at the underlying causation. The depreciation then results in higher import costs, leading to higher costs for advanced supply chains. Firms, domestic and FDI, who incur imports-based higher fixed costs become domestic market-oriented at the expense of the export market (Padhi, 2013). Imports do not translate into advanced domestic supply chains to feed exports. Porter (1992) and Rodriguez-Care (1996), echoing Stigler (1951), underpin how developing countries can rely on imported technology to adapt, but continuous dependence on imports is a costly affair. According to them, countries without domestic capabilities and relying exclusively on imports would always lag.

If depreciation does not result in significant export success (Bhanumurthy et al., 2014) and Indian imports remain insensitive to relative prices, comparable growth in exports and imports could translate into higher trade imbalances. This would continue to maintain the demand for more FIIs. In other words, the Indian policy stance may foster an environment that sustains the imports, trade imbalances, and the FII nexus, all of which can harm export-oriented FDI.

The neglect of higher domestic investments independent of import-led reallocations makes clear the trade-offs. In addition, such a policy stance adversely affects the generation of advanced domestic capabilities, skills, and dexterity and sources of increase in real domestic savings. This inattention could be problematic on another count. The lack of these capabilities and domestic specializations may constrain the economy’s ability to continue to adjust to the newer flow of imports embedded in the fourth generation technologies, thus limiting import-led growth. Goyal (2018) explains how the macro demand management underlying import-led growth is causing the progress of potential output (and such exponential growth) to slow.

These discussions on the problems facing trilemma management do not suggest that adopting a policy stance that adheres to the trilemma logic would be the best option. The article also explores the literature that questions the broader Hick’s ISLM-based trilemma that posits foreign and domestic currencies as (perfect) substitutes (for different perspectives, see Grenville, 2011; Taylor, 2020). The article alludes to the view that trilemma management can become more effective through proper management of growth which also brings in more enhanced FDI and advanced domestic investment interactions. Suppose the economy, faced with “higher” foreign capital inflows, maintains a depreciating rupee to start with. The resultant purchases of foreign currency would lead to a higher money supply and lower interest rates. The article raises the issue as to why this should be a problem. If for instance the Indian imports chiefly refer to the accumulation of inventories for working capital needs and indicate short-run financial assets, a lower rate of interest-led overheating can become a problem. Given the structure of demand and investment opportunities, a mere transition to the lower one can be a problem. However, the focus can be on how lower rates can support a transition to a higher pace of investment and expansions embedded in new, better supply responses and the development of long-run capital markets. This transition can come with low-interest rates and low prices (Padhi, 2018; 2018a). Learning by doing dynamism and spill-over impacts of imports could define more productive domestic investments, and the resultant higher growth brings in increases in savings. A macro balance of savings and investments can still be maintained when domestic investments (and savings) correlate with capital flows (in line with excess imports).

Policies should recognize that imports can create dynamic external economies and reinforce advanced domestic investment that embodies new specializations. Following a broader Keynesian perspective, the increased supply of money (and the lower interest rate) can support higher domestic investments. Low-interest rates would indicate low liquidity constraints facing such finance-led new investments. The advanced growth is expected to add to higher exports, FDI, and export interactions. The increased money supply and foreign currency inflows play a complementary role, and possibly higher, long-run capital inflows are not negated by the lower interest rates. The lower interest rate becomes a factor that can reinforce a more desirable substitution of FDI for FII.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest concerning research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article. The data used are freely available in public repositories mentioned in the text.