Abstract

The study investigates the effect of institutional quality on the corporate governance–firm performance nexus across 39 listed financial firms in South Africa via annual data from 2015 to 2022. We apply Driscoll and Kraay’s (1998) robust standard error and generalised method of moment estimation techniques to correct for cross-sectional dependence, serial correlation and endogeneity issues in this study. The study reveals a substantial positive correlation between firm performance and corporate governance metrics, including gender diversity, ethnic diversity, board size and board independence. This implies that having a large, independent, gender-based and ethnically diverse board improves company performance. In addition, all the indicators of institutional quality are found to enhance firm performance, while the relationship between corporate governance and firm performance in the industry is found to be strongly and negatively moderated by institutional quality. This suggests that corporate governance has a favourable impact on financial performance, but poor institutional quality weakens the beneficial and enhancing effects of corporate governance on firm performance. This research offers new insights into the importance of institutional frameworks and national governance mechanisms on the nexus between corporate governance and financial performance in the financial industry in South Africa.

Introduction

The overall goal of every profit-making firm is to deliver superior returns to its fund providers. The achievement of this corporate objective depends primarily on the combination of various firm-specific factors, including the structure of governance instituted in the firm. Among the firm-specific variables identified in empirical studies to drive organisational performance is corporate governance (CG) (Mansour et al., 2022; Mertzanis et al., 2019). However, the importance of CG mechanisms for firm performance (FP) is an ongoing issue in the accounting and finance literature. This is because the sustainability of corporate firms depends on how they are managed and controlled. The role of CG in an organisation’s performance has received global attention with the establishment of many governance laws to regulate corporate behaviours (Gallego-Álvarez & Pucheta-Martínez, 2020). Examples of such laws include the Sarbanes–Oxley Act (2002) and Dodd–Frank Act (2010), which were implemented to regulate corporate conduct among US firms. In addition, recent financial scandals and corporate failures around the world have been attributed to the breakdown of CG (Bhagat & Bolton, 2019). Similarly, the bank crisis witnessed in South Africa between 2014 and 2018 has been attributed to the breakdown of CG, especially at the board level (Mupangavanhu, 2021). During the crisis, two major banks—the African Bank and VBS Mutual Bank—collapsed due to poor internal control and an ineffective and inefficient board structure (Mittner, 2016; Mupangavanhu, 2021). The implication of this is that CG plays a central role in the performance and continuity of corporate firms.

Nevertheless, it is unclear from a theoretical and empirical standpoint whether strong CG improves a firm’s financial performance. Theoretically, agency theorists contend that when ownership and control are not aligned, agency costs arise (Fama & Jensen, 1983; Shleifer & Vishny, 1997). Hence, the exponents of agency theory contend that sound CG alleviates agency costs and improves FP. On the other hand, stewardship theorists assert that managers will protect the interest of their principal and will not take any action that is detrimental to the corporate goal of the enterprise (Donaldson & Davis, 1991). Among the various governance mechanisms identified in the literature as strongly influencing organisational performance are board attributes and composition (Arora & Sharma, 2015; Haider & Fang, 2016; Rusyda & Priantinah, 2018; Shakil et al., 2019). However, in the empirical context, scholars have focused on different dimensions of board attributes, such as board size, board diversity and board independence, but with mixed findings (Al-Ahdal et al., 2023; Napitupulu et al., 2020; Nguyen et al., 2014; Pathan & Faff, 2013). Additionally, these studies have concentrated on firm-level CG without considering the influence of the external environment, which has been identified as a critical factor that drives corporate performance (Nguyen et al., 2023; Zattoni et al., 2020).

As noted by Nguyen et al. (2023) and Olawale and Obinna (2023), the efficacy and effectiveness of CG depend on the level of institutional quality (IQ) in a country. Similarly, Mertzanis et al. (2019) assert that the effect of CG on FP hinges on the structure of the social and regulatory environment where the firm operates, whereas Kumar and Zattoni (2013) contend that IQ has a strong effect on the CG behaviour of corporate organisations. Similarly, Al-Gamrh et al. (2020) contend that companies’ performance and CG are strongly influenced by the institutional environment within which they operate. Within an economy, sets of formal and informal rules, institutions and regulations guide and shape the conduct and performance of business entities. These institutions are referred to as the ‘rules of the game’, described as a legal framework that guides property rights and contract enforcement (La Porta et al., 1997; North, 1990). Comparably, transaction costs and contract enforcement costs are minimal in an efficient and successful institutional system, which boosts confidence among investors and economic performance (Bhaumik et al., 2012; Chikalipah, 2017). As argued by Zattoni et al. (2020), IQ may have direct, mediated or moderated effects on CG and firm outcomes. This implies that the structure of the institution in a country can interact with CG to enhance or constrain FP.

Despite the significance of IQ for FP, there is little to no empirical research on how IQ affects the nexus between CG and FP in the context of South African businesses. Rent-seeking, opportunistic and selfish behaviour on the part of managers to pursue personal goals that are detrimental to shareholders’ interests may be encouraged by a weak institutional environment marked by a high level of corruption, political instability, absence of the rule of law (ROL), and poor enforcement of law and order (Olaniyi et al., 2022). However, a robust institutional framework can avert management encroachment, suppress white-collar crime, discourage financial impropriety and embezzlement, and lessen corporate board fiduciary obligation violations (Kumar & Zattoni, 2015). Therefore, IQ can provide additional checks to company managers and directors to embark on shareholder-inclined decisions, which will improve the firm’s financial bottom lines. Essentially, the efficacy of CG in promoting organisational success can either be facilitated or hindered by an efficient or weak national institution (Aguilera & Jackson, 2003). The unique characteristics of a growing economy such as South Africa make it necessary to evaluate whether the quality of the institutional environment matters in the relationship between CG and FP.

On this basis, the present article responds to the call from previous studies (see Zattoni et al., 2017, 2020) and contributes to the discussion on the CG‒FP nexus in the following ways. First, in light of their vital significance in the economy, the study concentrates on listed financial firms. In any economy, the financial sector is critical to its development and progress. Specifically, the sector is perceived as an agent of growth owing to its role in financial intermediation in the economy. The financial system’s effectiveness also affects the state of the economy (Ajide & Ojeyinka, 2022; Irawati et al., 2019). Furthermore, South Africa’s financial sector has been acclaimed as the most sophisticated sector in Africa (Ajide & Ojeyinka, 2022; Olaniyi & Adedokun, 2022). Second, the study fills a major gap in the CG literature by exploring the role of national-level institutions in the relationship between CG and FP via data from listed financial firms on the Johannesburg Stock Exchange (JSE) between 2015 and 2022. To our knowledge, in the case of South African financial firms, this study appears to be the first to account for the influence of IQ on the relationship between CG and FP. Finally, the study considers the impact of cross-sectional dependence (CD) via a battery of estimation techniques, an aspect of methodology that has been neglected in the CG–FP literature.

The findings of this study reveal that board characteristics such as gender diversity, ethnic diversity, board size and board independence consistently improve financial performance. In the same way, overall IQ and its components, such as control of corruption (COC), regulatory quality (REG) and ROL, enhance the performance of JSE financial firms. Overall, the study reveals that the overall IQ index (INS) negatively moderates the relationship between board characteristics and the performance of listed financial firms in South Africa. The key implication of the study findings is that inefficient and weak IQ mitigates the favourable effect of governance indicators on the financial performance of South African financial firms.

The remainder of the article is organised as follows. After the introduction, the second section provides an overview of CG and IQ in South Africa; the third section presents the literature review and development of the hypotheses; and the fourth section discusses the methodology used to accomplish the objective of the study. The fifth section presents an analysis of the results and a discussion of the findings, and the sixth section concludes the study.

Overview of CG and IQ in South Africa

According to Tshipa et al. (2018) and Muniandy (2022), South Africa is considered one of the leading emerging economies with well-established CG frameworks that regulate business behaviour and safeguard the interests of shareholders. The former apartheid policy, which was in place until 1994, encouraged white people to dominate higher managerial positions in businesses (Dreyer et al., 2021; Gyapong et al., 2016). Following the resurgence of democracy in 1994, the nation implemented several policies intended to protect and promote the expansion and advancement of the private sector to attain targeted levels of economic growth and development. To accomplish this laudable objective, the South African government published rules on CG, such as the King I, II, III and IV reports, which were put into effect in 1994, 2002, 2009 and 2016, respectively. These codes govern the business practices and board conduct of listed businesses on the JSE. The issue of board composition, as a governance mechanism, is essentially at the heart of these reports (Muniandy, 2022). The subject of board diversity is particularly relevant in South Africa because it has occurred over the past three decades (Gyapong et al., 2016; Scholtz & Kievet, 2018). With the implementation of the CG code in 1994 and subsequent reforms and amendments, there has been increased concern about gender and ethnic diversities in the board composition of South African companies (Muniandy, 2022). To address this imbalance, several policies, including the Broad-Based Black Employment Act (2003) and Employment Equity Act (1998), are enshrined as CG mechanisms introduced to mainstream ethnic and gender diversities, respectively, in the board appointment of South African companies (Ntim & Soobaroyen, 2013). The recent code of CG, through the King IV report issued in 2016, mandates that the governing boards of South African companies have a greater proportion of non-executive directors, who must be substantially independent in their board structure and composition (Institute of Directors, 2016). Despite these measures, CG among South African companies has become a hot topic, particularly in light of the severity of crises witnessed in the country’s financial sector. For example, the crisis that struck the sector between 2012 and 2018 led to the collapse of the African Bank, one of the main banks in the nation. Similarly, in 2018, the VBS Mutual Bank failed (Mupangavanhu, 2021). The financial irresponsibility of management, failure of CG, ineffective and inefficient board structure, weak internal control, and weak governance systems are some of the factors that have been identified as the causes of the financial failure of the two banks (Mittner, 2016; Mupangavanhu, 2021). Consequently, it is imperative to assess the efficacy of CG, specifically the attributes of the board, in attaining superior financial results within the financial sector of South Africa.

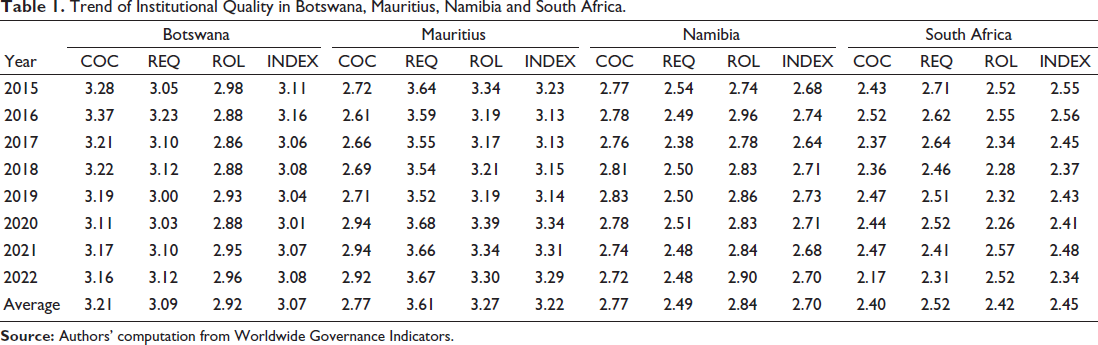

With respect to the institutional environment, South Africa’s IQ has not been impressive over the past few years, particularly compared with its neighbouring African nations, Botswana, Namibia and Mauritius. To highlight South Africa’s dismal performance in terms of institutional architecture, Table 1 shows the trend of three crucial IQ dimensions, COC, REG and ROL, in South Africa and three other African nations, including Botswana, Namibia and Mauritius, over the study period. Following the definition of the World Governance Indicators (WGI), the COC is defined as ‘the extent to which public power is exercised for private gain including the state capture by the elite and private interest’. On the other hand, REG captures ‘people’s perception of the ability of the government to formulate and implement sound policies that permit and promote private sector development’, whereas ROL is described as the ‘extent to which agents have confidence in and abide by the rules of society and, in particular, the quality of contract enforcement’. These institutional indicators’ initial values varied from –2.5 (weakest institution) to 2.5 (strongest institution). These indices are rescaled to 0.00–5.00, where 0.00 and 5.00 reflect the weakest and highest IQ, respectively, by adding +2.5 to the original value for ease of reading. Studies such as Ajide (2022) and Osinubi and Ojeyinka (2024) use a similar methodology.

Trend of Institutional Quality in Botswana, Mauritius, Namibia and South Africa.

At first glance in Table 1, South Africa clearly has the lowest scores across all three IQ dimensions that were taken into consideration, as well as in the INS that was produced by averaging the three components over the course of the study period. At the scale of 0.0–5.0, nations such as Botswana, Mauritius and Namibia consistently scored above the average of 2.5 over the study period. In contrast, South Africa only narrowly scored 2.52 in the REG dimension, performing below average on the other dimensions of IQ, including the ROL, the COC and the INS. Furthermore, over the course of the study period, South Africa’s IQ deteriorated. For example, the REG in the country decreased from 2.71 in 2015 to 2.31 in 2022, whereas the INS similarly decreased from 2.55 in 2015 to 2.34 in 2022. This is consistent with Olaniyi and Adedokun’s (2022) finding that South Africa’s IQ plummeted between 1986 and 2015. As mentioned previously, the government’s attempts to enact good CG to safeguard the interests of shareholders may be jeopardised by the nation’s poor IQ. Once more, these lax institutional standards may create loopholes that promote impropriety and corruption among company executives, managers and directors. Consequently, the following central research question is addressed by this empirical work: Is there a moderating effect of IQ on the relationship between CG and company performance among South African listed financial firms?

Literature Review and Hypothesis Development

The agency and institutional theories developed by Jensen and Meckling (1976) and Meyer (1977), respectively, constitute the main theoretical lens for this research. Institutional theory highlights the importance of the national-level institutional environment and architecture as powerful factors that explain corporate outcomes, whereas agency theory calls for sound firm-level CG mechanisms to mitigate the agency conflict that characterises the separation of ownership and control in the governance of corporate firms. Thus, these two theories serve as the workhorse for the study and provide the theoretical foundation for exploring the intricacy of CG and IQ in driving FP among the sampled firms. To situate the study from a proper perspective, we divide the empirical review section into three subheadings. In subsection ‘CG and FP Nexus’, we review studies on the nexus between CG and FP, whereas prior studies on the intricacies of IQ and FP are presented in subsection ‘Institutional Quality and Firm Performance’. Existing studies on the trilogy among CG, IQ and FP are reviewed in subsection ‘Corporate Governance, Institutional Quality and Firm Performance’.

CG and FP Nexus

The board of directors has been identified as the pillar and nucleus of internal CG in the management of corporate organisation (Saggar et al., 2022). The board is the highest decision-making organ saddled with the responsibility of monitoring and supervising firm activities and making strategic decisions towards the achievement of the organisational short- and long-term goals. Several studies have focused on one aspect of CG or the other, thereby making the outcomes and findings from such studies incomparable and lacking general applicability and acceptability. Following existing studies on CG (Boachie, 2023; Mertzanis et al., 2019; Tarighi et al., 2023), we focus on board attributes such as board independence, board size, gender and ethnic diversities as CG mechanisms and unravel their impacts on the performance of listed financial firms in South Africa while accounting for the role of IQ in the nexus between the target variables.

In the empirical setting, the debate over board size and the FP nexus is endless and unresolved. Based on the principles of agency theory, properly designed CG mechanisms can reduce the likelihood of an information gap between managers and other stakeholders, as well as the degree of conflict between shareholders and managers (Jensen & Meckling, 1976). Large boards have been recommended by some studies as a governance mechanism to increase business performance (García-Ramos & Diaz, 2021; Kahloul et al., 2022; Muchemwa et al., 2016; Tulung & Ramdani, 2018). This is because large boards have diverse skills, experiences and expertise that are critical to organisational performance. This line of research also contends that when board members oversee and regulate managers’ performance, they act as representatives of several stakeholders and shareholders. Furthermore, Ntim et al. (2015) contend that a larger board size encourages efficient oversight and monitoring, which forces management to act in the best interests of shareholders and increases the value and performance of the company. According to Kalsie and Shrivastav (2016), a large board with many directors strives to promote the interests of stakeholders and ultimately improve the performance of the organisation. However, other scholars, such as Altass (2022) and Kao et al. (2019), argue against large board size, claiming that it slows decision-making and negatively impacts board effectiveness, and consequently FP. According to Edogbanya’s (2019) findings, the listed Nigerian corporations have a lower firm value (Tobin’s Q) as their board size increases. Despite these contradictory results, we propose that, among South African listed financial firms, a larger board positively impacts FP.

H1a: Board size has a positive and significant effect on FP.

Another aspect of CG that has received scholars’ attention in the literature is board independence. Again, the argument on the effect of board independence on FP is keenly rooted in the dichotomy between agency and stewardship theories’ propositions. While agency theory supports a greater proportion of non-executive independent directors in the boardroom (Fama & Jensen, 1983), stewardship theory advocates for more executive directors due to their technical knowledge and experience in the operations of the firms. The exponents of agency theory contend that independent directors have no financial interests in the company and, as such, would ensure the protection of shareholders’ interests by influencing the board’s decision on matters that promote the well-being of all the stakeholders (Napitupulu et al., 2020). In this context, the empirical literature contradicts existing studies on the board independence and FP nexus; however, the findings are mixed and inconclusive. For example, Al Farooque et al. (2020) and Al Amosh and Khatib (2021) buttress the tenets of agency theory and find that firms with a greater proportion of independent directors record better financial outcomes. However, Edogbanya (2019) discovered that board independence reduces the performance of listed firms in Nigeria. Moreover, the Institute of Directors, South Africa (Institute of Directors, 2016), prescribes that the corporate board of South African firms must have a greater number of non-executive directors, a greater proportion of whom must be independent. Accordingly, we formulate the next hypothesis as follows:

H1b: Board independence strongly and positively promotes FP.

Recently, the topic of gender diversity has taken a central stage in the CG–FP literature. For example, researchers such as Chatterjee and Nag (2023) and Sarhan et al. (2019) have shown that having female directors in the boardroom offers essential and distinctive resources that increase company value. Their argument is based on resource dependence theory, which holds that female directors offer human resources capable of influencing business decisions in a way that maximises profit for shareholders. Furthermore, according to some authors, women are risk-averse and do not support board decisions on issues that are antithetical to their organisations’ corporate objectives (Seebeck & Vetter, 2021). Similar findings are made by Harris (2014) and Arora (2022), who find that gender diversity greatly increases return on equity (ROE), Tobin’s Q and return on assets (ROA). Similarly, Gyapong et al. (2016) and Scholtz and Kievet (2018) find a strong and favourable relationship between gender diversity and company performance in the context of South African listed companies. Their results validate the recommendations of the King IV report on CG, which advocates for more gender-balanced boards among South African corporations. Moreover, Edogbanya (2019) reported a favourable correlation between the number of female directors and firm value in Nigeria, measured by Tobin’s Q. In contrast, studies such as Solakoglu and Demir (2016) and Marquez-Cardenas et al. (2022) could not validate any significant association between the presence of women directors and organisational performance for listed firms in Turkey and Latin America, whereas scholars such as Adams and Ferreira (2009), Ujunwa et al. (2012) and Green et al. (2020) argued that greater gender diversity in the boardroom hurts FP. The present study aligns with the prescription of King IV reports in South Africa and hypothesises that the presence of female directors is expected to increase a company’s performance among financial firms in South Africa, as mentioned below:

H1c: Gender diversity is strongly and positively associated with FP.

In South Africa, the issue of ethnic diversity in board composition has received increased attention since the collapse of the apartheid policy in 1994. In an attempt to mainstream ethnic diversity in the board structure, several policies and reforms have been implemented by the South African government. The importance of ethnic diversity in the boardroom is of particular interest because the country has been described as one of the most ethnically diversified economies in the world (Gyapong et al., 2016; Muniandy, 2022; Ntim et al., 2015). To buttress this assertion, board ethnic diversity is one of the core aspects of the King IV report on the code of CG in South Africa. Although the report did not set any specific number or proportion for ethnicity in board composition, it encourages balance and equity in the representation of directors of indigenous origin for the effectiveness of corporate boards (Institute of Directors, 2016; Muniandy, 2022). Hence, the country serves as a good candidate for exploring the linkage between board ethnic diversity and corporate performance. However, delving empirically, there is no clear connection between ethnic diversity and FP. For example, using data on Fortune 1000 firms, Carter et al. (2003) find that firm value (Tobin’s Q) is enhanced with greater ethnic diversity. Similarly, Ujunwa et al. (2012) discovered a significant positive association between board ethnicity and the FP of 122 listed firms in Nigeria. Similarly, Gyapong et al. (2016) identified ethnic diversity as a positive influencer of FP (Tobin’s Q) among 245 listed firms in South Africa. However, their finding is refuted by the study of Carter et al. (2010), which failed to find any significant relationship between ethnic minority directors and Tobin’s Q among US S&P 500 index firms. Focusing on South African companies, Scholtz and Kievet (2018) employ data on the top 100 JSE-listed firms and document an inverse relationship between board ethnicity and a FP proxy with Tobin’s Q and ROA. Recently, a study by Muniandy (2022) asserts that the presence of black directors in the boardroom of South African firms strengthens board effectiveness and, in turn, produces performance. Therefore, the following hypothesis is formulated as follows:

H1d: Greater board ethnic diversity is strongly and positively related to better FP.

Institutional Quality and Firm Performance

In this study, we conceptualise IQ to incorporate the duty of national institutions to provide a regulatory structure that supports the private sector’s growth, adherence to the ROL, and provision of a conducive business atmosphere that discourages corruption and state capture (Chadee & Roxas, 2013). Our assumption is built on the intuition that the institutional environment is not only important for macroeconomic performance but also essential and fundamental for business performance. Moreover, extensive studies have been conducted on the effect of IQ on macroeconomic performance (Acemoglu et al., 2014; Olaniyi & Oladeji, 2021). All these studies argue that a better institutional environment leads to better economic outcomes. However, at the micro level, studies on the IQ–FP relationship are scarce and relatively underexplored, especially in the South African landscape. Since corporate firms exist within a set of legal, regulatory and macroeconomic frameworks, their success and performance are likely to be influenced by these institutional architectures. Starting with the path-breaking studies of North (1990) and La Porta et al. (1997), FP is enhanced in an environment with a strong legal system. Several studies have revealed the influence of institutional architecture on the performance of corporate organisations. Focusing on the manufacturing sector in India, Rajesh Raj and Sen (2017) reveal the effect of IQ on FP and find that greater corruption negatively impacts the total factor productivity of the sampled firms. Vanacker et al. (2021) identify intellectual property protection and institutions as strong predictors of the financial performance (ROA) of European firms. In a related study, scholars such as Karmani and Boussaada (2021) disclosed that high-quality institutions promote firm competitiveness. The authors further argue that government stability and enforcement of law and order stimulate FP, whereas an increase in corruption is detrimental to ROA and ROE among 814 European firms.

Focusing on developing countries, Hussen and Cokgezen (2021) analyse the response of firm innovation to regional IQ among 19 African countries and find that corruption control and adherence to the ROL promote firm innovation. Similarly, Nyamah et al. (2022) document a positive and significant influence of the institutional environment on the performance of 320 agri-food processing firms in Ghana. Focusing on 135 firms in Nigeria, Ojeka et al. (2019) demonstrated that an increase in corrupt practices and a weak institutional environment hurt the ROA and Tobin’s Q of non-financial firms. This finding is substantiated by the recent work of Kafouros et al. (2024), who establish a favourable effect of a strong institutional environment on the return on sales of listed firms in 16 emerging countries. Recently, Yen et al. (2023) analysed the impact of IQ on bank stability in Asian countries via panel estimation techniques such as fixed effects and random effects. The study revealed that a strong institutional environment, combined with political stability and adherence to the ROL, promotes bank stability in a region. Despite this, Faruq and Weidner (2018) find no evidence of a significant link between IQ and the performance of firms in the agriculture and service sectors. The authors conclude that the impact of IQ varies across different geographical regions. This outcome is supported by the study of Ahmed and Omar (2019), which failed to document any noticeable effect of institutional pressure on FP. On this basis, we hypothesise that a strong IQ has a positive and significant influence on the performance of listed financial firms in South Africa.

H2: Better IQ enhances FP among listed financial firms in South Africa.

Corporate Governance, Institutional Quality and Firm Performance

Specific studies on the trilogy among CG, IQ and FP are limited and scant. As presented in the preceding subsections, prior empirical studies have focused either on the influence of CG on FP or the interplay between IG and CG, whereas little or nothing is known about the joint and interactional effects of IQ and CG on FP, especially in an emerging economy such as South Africa. The institutional environment constitutes a macro environment within which firms operate, which in turn shapes the behaviour and performance of corporate organisations. In this context, Sugathan and George (2015) define governance architecture as ‘the country’s institutional fabric that supports the conduct of economic activities, facilitates efficient economic transactions, and restricts negative externalities from such transactions’. Similarly, Mertzanis et al. (2019) argued that the efficacy of CG in driving FP is strongly influenced by the social and regulatory environment within which firms operate. Thus, the growth, expansion and performance of corporate organisations can be influenced by the kinds of rules, regulations and legislation that emanate from the regulatory authority and the institutional environment within which the firm operates. For example, in a country where there is protection of private property and enforcement of contracts, investor confidence is increased, which in turn increases foreign portfolios and FP. Similarly, effective and efficient institutions can act as checks to discourage managerial entrenchment and board politics and thus enhance firm value. Along with this argument, Mertzanis et al. (2019) explore the impact of social institutions and CG on FP among 11 countries in the MENA region. Using the fixed-effects estimator, the authors discover that institutional variables such as COC, political stability and REG significantly drive FP in the region. However, the study considers only the separate effects of CG and IQ on FP. Relatedly, Lu and Wang (2021) argue that national law and culture play crucial roles in the relationship between the CG and the environmental performance of Iranian firms. Similarly, Nguyen et al. (2021) focus on 76 countries and find that the impact of gender diversity on FP is positive and stronger in countries with good national governance. Recently, Olawale and Obinna (2023) delved into the role of IQ in CG, that is, the FP of the oil and gas sector in Nigeria and disclosed that strong IQ provides an enabling environment for the stimulating effect of CG on the FP in the sector. In another study, Atugeba and Acquah-Sam (2024) examine the joint effect of national governance and CG on FP among 31 listed companies and discover that good national governance ameliorates the detrimental effect of CG to spur FP. Thus, the last hypothesis in this study is presented below:

H3: IQ positively moderates the effect of CG on FP in the South African financial sector.

Data and Methodology

Data

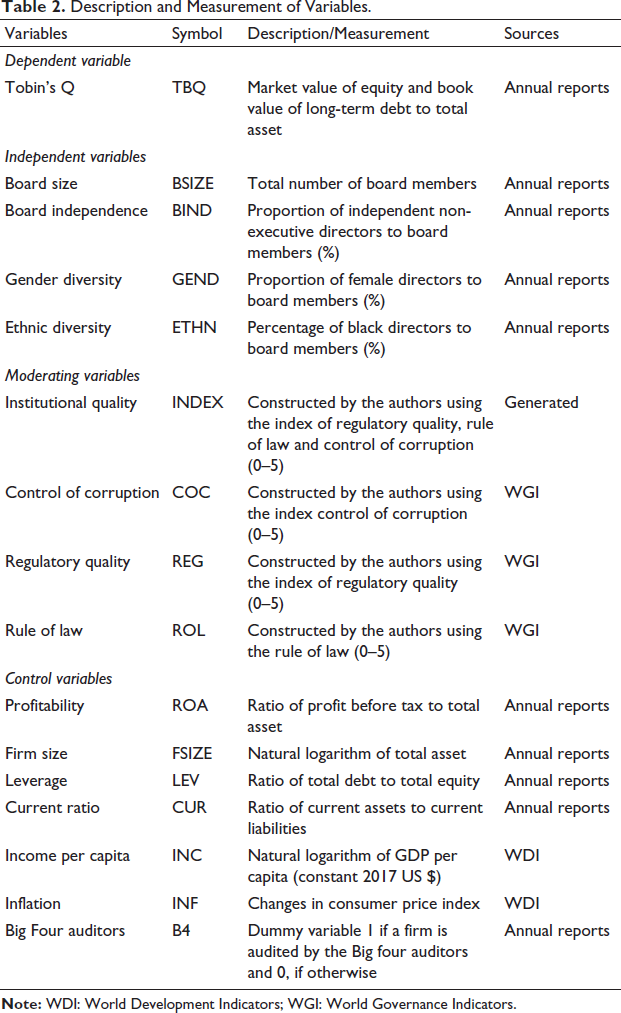

This study delves into the moderating role of IQ in the interplay between CG and FP among listed financial firms in South Africa from 2015 to 2022. The choice of the period (2015–2022) was informed by data availability at the time of the analysis, as some companies were yet to release their annual reports for 2023 and 2024. On the basis of information from annual reports of listed companies and published in the IRESS database, 45 financial firms are listed on the JSE as of December 2023. Initially, we intend to employ all financial firms as the units of analysis. However, six of these firms do not have complete data over the sample period; hence, they are excluded from the study. Importantly, these firms were not excluded at random but were strictly selected on the basis of continuous data over the sample period. Therefore, the study focuses on 39 firms (312 yearly observations) with data on the target variable. These firms are listed under the financial sector category and include bank institutions and non-bank financial institutions. Thus, the firms constitute approximately 87% of listed financial firms in South Africa, which is considered a good representation of the entire population. Hence, selection bias is not envisaged in this study, as the selected firms can be taken to represent the entire financial sector in South Africa (Ojeyinka & Matemane, 2024). This is because the data on CG indicators (board gender diversity, board ethnic diversity, board size and board independence) and firm-specific control variables (firm size, leverage ratio, current ratio and audit quality) are obtained from the annual reports (compiled in the IRESS) of the sampled firms. The IRESS is a specialised provider of financial and market survey data on listed firms on the JSE and other African markets. Data from the IRESS database are directly sourced and compiled from annual reports of listed firms, which are widely used by researchers from South Africa and other African countries (Du Toit & Lekoloane, 2018). Data on institutional variables (COC, REG and ROL) are sourced from the World Governance Index of the World Bank, whereas data on macroeconomic variables (income per capita and inflation) are obtained from the World Development Indicator of the World Bank. Table 2 provides detailed information on the definitions and measurements of the variables employed.

Description and Measurement of Variables.

Variables

Dependent Variable

The study employs Tobin’s Q as a measure of FP. Consistent with the studies of Al-ahdal et al. (2023), Ojeyinka and Matemane (2024) and Mondal and Sahu (2024), Tobin’s Q is preferred over other performance measures, such as accounting-based measures (ROA and ROE), which are based on historical data. Tobin’s Q is a forward-looking financial performance measure that provides information on the growth potential of a firm (Kyere & Ausloos, 2021).

Explanatory Variables

The second category of variables represents the governance indicators. In line with extant studies (Al-Shaer et al., 2024; Karmani & Boussaada, 2021), we employ board attributes such as board gender diversity, board ethnic diversity, board size and board independence as CG indicators. The selection of these governance variables is based on the assertion that the composition of the board plays a fundamental role in influencing FP (Boachie, 2023). Since the board of directors is described as the custodian of CG, the composition of the board in terms of diversity and independence will play a critical role in shaping organisational performance.

Moderating Variables

The third set of variables is the moderating variable—IQ indices. In this study, we follow existing studies by using four measures of the institutional environment, including the average IQ index, COC, REG and ROL, which have been established to influence FP (see Chadee & Roxas, 2013; Karmani & Boussaada, 2021). For example, weak REG, the absence of a ROL and large-scale corrupt practices at the upper echelon of companies encourage firm managers and directors to pursue self-oriented policies that deviate from shareholders’ welfare (Olaniyi et al., 2022).

Control Variables

The last set of variables is the control variables, consisting of firm-specific variables and macroeconomic variables. In CG studies, firm specifics such as firm size, the leverage ratio, the current ratio and auditor quality have been identified as crucial drivers of FP (see Kyere & Ausloos, 2021; Tarighi et al., 2023; Uribe-Bohorquez et al., 2018). Unlike previous studies, we also control for the influence of the macroeconomic environment on the dynamics of FP by incorporating South African per capita income and the inflation rate as macroeconomic variables in the model (see Boachie, 2020; Ojeka et al., 2019; Singh, 2023). All these studies identify inflation and per capita income as crucial macroeconomic indicators that affect FP.

Model Specification

The modelling method used to achieve the study objective is stepwise and is based on three steps. In the first step, we examine the primary effect of CG indicators on FP (Tobin’s Q). This is denoted as the baseline model. Second, the study expands the baseline specification by incorporating measures of IQ to uncover the direct effects of the institutional environment on the target variable (Tobin’s Q). Finally, the interaction term between CG proxies and IQ is used to investigate the moderating role of the latter on the nexus between CG and the financial performance of the financial firms listed on the JSE. Premised on the extant studies on the CG–performance nexus (Karmani & Boussaada, 2021; Singh et al., 2018), the baseline model is presented in Equation (1):

where FP is firm performance (Tobin’s Q).

where

In the second phase of the analysis, we extend Equation (2) by including indicators of the institutional environment, and the new model is specified as:

From Equation (3),

In Equation (4), INS stands for the overall IQ index, and COC, REQ and ROL represent the control of corruption, regulatory quality and rule of law, respectively. To prevent multicollinearity in the analysis, each of the institutional variables was entered into a separate model as explicitly presented below:

where Equations (5), (6), (7) and (8) describe the impacts of the INS, COC, REG and ROL on FP, respectively.

To establish the moderating role of the institutional environment, Equation (3) is augmented with the interaction term between the INS and CG indicators as specified below:

Here, If If If If

Analytical Techniques

To achieve the study’s objective, both descriptive and inferential statistics are employed. The descriptive statistics provide information on the salient attributes of the variables in the study. On the other hand, inferential statistics are employed to provide evidence-based outcomes on the moderating role of IQ in the relationship between CG and FP among listed financial firms in South Africa. Although the study utilised 87% of financial firms, inferential statistics are still necessary for hypothesis testing and for making concrete and evidence-based conclusions for policy formulation in the selected sector (Cochran, 1977; Kish, 1965). In addition, the outcome from inferential statistics can also serve as a guide for other sectors or industries listed on the JSE. The study employs panel estimation techniques to achieve the study’s objectives. The study conducts pre-estimation tests such as descriptive statistics and correlation analysis of the series. Thereafter, on the basis of the Hausman test, we apply the fixed-effects model as the primary estimation technique. Following the outcome of the Hausman test, we also conduct an endogeneity test via Durbin–Wu–Hausman test. The outcome clearly suggests endogeneity issues, which inform the usage of the instrumental variable technique as a technique of analysis. Specifically, we apply the two-step system generalised method of moments (GMM) to correct for endogeneity. The GMM is an instrumental variable technique that is robust to endogeneity bias in the regression. To confirm the reliability, authenticity and credibility of the study’s outcome, the study tests for the existence of CD among the sample firms, which motivates the usage of Driscoll and Kraay’s (1998) robust standard error as an alternative technique of analysis premised on the outcome from the CD test. As argued in the literature, Driscoll and Kraay’s (1998) approach produces a consistent covariance matrix estimator with robust standard error and is adjusted to be effective and efficient in addressing the problems of serial correlation, heteroscedasticity and CD in panel studies (Doku et al., 2023; Edogbanya, 2019; Hoechle, 2007; Ojeyinka & Akinlo, 2021; Olaniyi et al., 2022). For the robustness of the study’s outcomes, we employ feasible generalised least squares (FGLS) regression and panel-corrected standard error (PCSE) approaches. As argued by Wahba (2015), the FGLS method delivers superior and better results in the case of heteroscedasticity and serial correlation in the residual. Similarly, Tshipa et al. (2018) contend that the FGLS controls for heterogeneity and unobserved heterogeneity among the cross-sectional units in the panel. Finally, the GLS provides robust standard errors that account for the influence of serial correlation and heterogeneity in residual terms. As proposed by Beck and Katz (1995), the PCSE method is efficient in handling panel data with CD, heteroscedasticity and serial correction and thus produces robust standard errors (Onatunji, 2024).

Results and Discussion of Findings

Descriptive Analysis

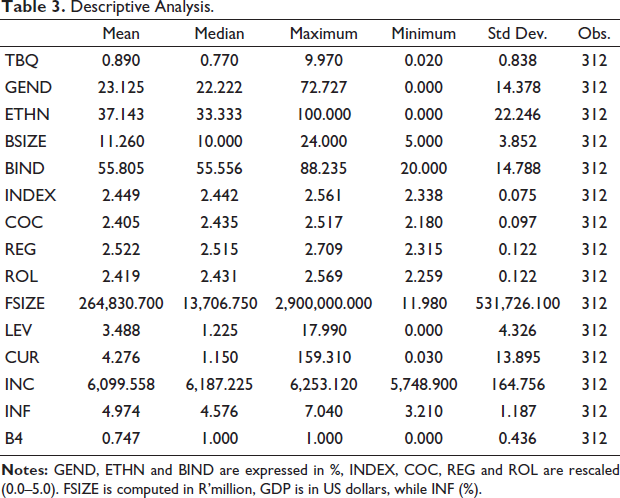

The emphasis in this subsection is to examine the salient characteristics of the series in the study to gain prior insight into their behaviours before the actual analysis is conducted. A summary of the outcomes is presented in Table 3. The average (mean) value of the target variable (Tobin’s Q) among the sample firms is 0.89, with the minimum and maximum values estimated to be 0.02 and 9.97, respectively. The value of the standard deviation of Tobin’s Q of the JSE financial firms is 0.83, which suggests little deviation of the actual data from the average value of the selected financial firms. For CG indicators, GEND, ETHN, BSIZE and BIND have average values of 23%, 37%, 11% and 56%, respectively, suggesting that the boardrooms of the sampled financial firms in South Africa are dominated by male and white directors despite the different CG initiatives implemented by the government to mainstream more female and black directors into the highest decision-making organ of South African firms. The implication of the average value of the proportion of the outcome is that fewer than 25% of the boards of the sampled firms are women directors, suggesting a low degree of gender diversity among the financial firms in South Africa. The standard deviations for GEND and ETHN are 14.4% and 22%, respectively, which implies a large deviation of the actual data from their average values. For the values of the institutional variables, the mean, median, minimum and maximum values of INS, COC, REG and ROL vary between 2.1 and 2.7 on a scale of 0.0–5.0. This suggests an average level of IQ in South Africa. With respect to the control variables, the average value of total assets, the leverage ratio, the current ratio, GDP per capita and the inflation rate stand at R264,830.7 million, 3.5, 4.3, $6,099.6 and 5%, respectively. The findings from Table 3 show that 75% of the selected firms were audited by Big Four auditors between 2015 and 2022.

Descriptive Analysis.

The study also examines the distribution of the data by testing whether the assumption of a normal distribution is satisfied. To address this, we conduct the Jarque–Bera (J–B) test for normality, and the outcomes are presented in Table 3. A variable follows a normal distribution if the probability value of the J–B test exceeds 0.05 (5%); otherwise, the distribution of the series is asymmetric. Considering the probability values of the J–B test in Table 3, the assumption of a normal distribution is rejected for all the variables. Hence, we conclude that the variables in the study do not follow a normal distribution pattern.

Correlation Analysis

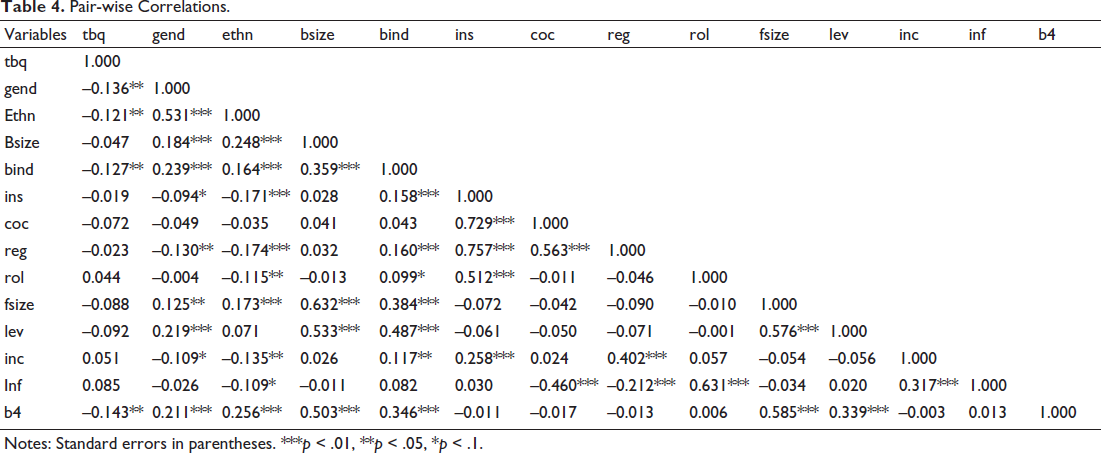

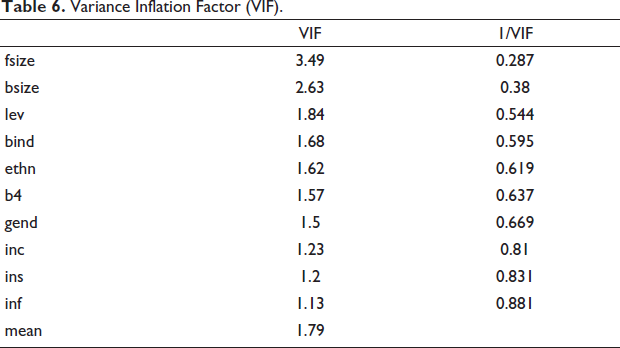

One major procedure to obviate the possibility of multicollinearity in any empirical investigation is to conduct a correlation analysis among the variables of interest. For robustness of the analysis, the Pearson correlation coefficient and variance inflation factor (VIF) are used to examine the level of association among the variables. The correlation matrix provides information on the direction of association between two variables, whereas the VIF measures the strength of the correlation between independent variables in a model. To rule out the possibility of multicollinearity, there must not be a high correlation (above 0.80) between two independent variables, and none of the independent variables should have a VIF above 10.0. The two measures are used to check for multicollinearity among independent variables in a regression analysis. Thus, for the robustness of the results, we apply two measures to test for multicollinearity in this study. Table 4 provides a synopsis of the Pearson correlation coefficients among FP, CG and the control variables used in the study. The study follows the prescription of Gujarati and Porter (2008) and applies the threshold of a correlation coefficient of 0.8 as a signal of multicollinearity. The outcomes from Table 4 reveal that the highest correlation coefficient is 0.759 between REG and INS, whereas the second highest correlation coefficient (0.729) is between COC and INS. However, this does not affect the reliability of the estimates because all the indicators of IQ are entered into separate models. This approach clearly explores the role of each IQ variable in the relationship between CG and FP (Nguyen et al., 2021). In addition, all the board attribute variables are negatively and significantly associated with the outcome variables at the 5% level, except for board size (BSIZE). Hence, none of the correlation coefficients exceeds the threshold of 0.8. This finding suggests that all the estimated models are immune and free from the threat of multicollinearity.

Pair-wise Correlations.

The study also calculates the VIF for the independent variables. Following the works of Lemma et al. (2022) and Ojeyinka and Matemane (2024), there is a multicollinearity threat when the VIF for any variable is greater than 5.0 and the average VIF exceeds 2.0. Focusing on the outcomes fromTable 5, firm size has the highest VIF (3.49), which is below the threshold of 5.0. Again, the average (mean) VIF of 1.79 is established in the study, which is below the threshold of 2.0 adopted. The outcomes reiterate the results of the Pearson correlation coefficient. On the basis of these tests, there is no multicollinearity problem in the estimated models.

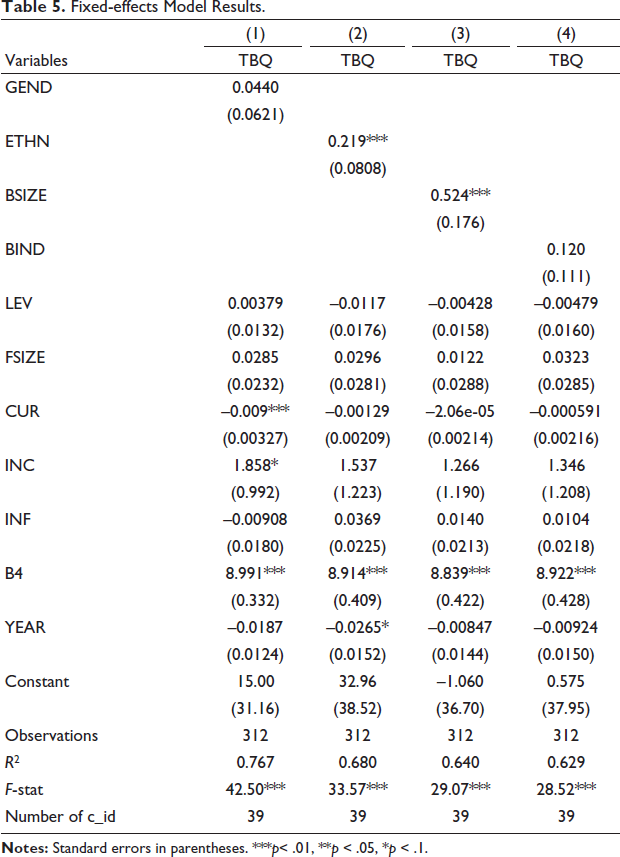

Fixed-effects Model Results.

Baseline Regression Model

The analysis is kick-started by applying the fixed-effects model based on the Hausman test (

Variance Inflation Factor (VIF).

Further Diagnostic Tests

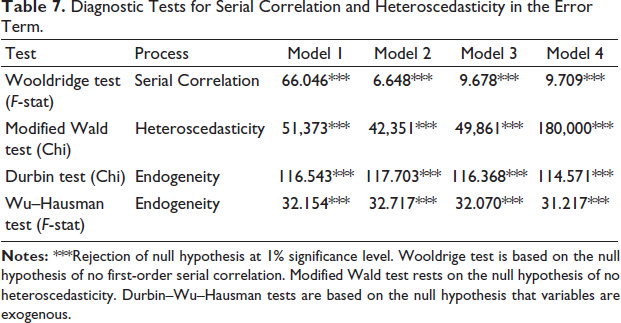

The outcomes of the fixed-effects models (Table 6) are based on the assumption that the error terms from the process are homoscedastic and are free from first-order serial correlation. However, Drukker (2003) suggested that the presence of serial correlation biases the standard error and renders the estimates inefficient. Therefore, it is crucial to subject the residual terms from the fixed-effects models to formal tests to obtain reliable, efficient and unbiased estimates. We proceed further by subjecting the residual recovered from the fixed effect models to first-order serial correlation and heteroscedasticity tests via the Wooldridge (2010) test and the modified Wald test proposed by Baum (2001), respectively. The results of the two tests are displayed in Table 5. The outcomes from the two tests validate the rejection of the null hypothesis of the absence of serial correlation and homoscedasticity, suggesting evidence of first-order serial correlation and heteroscedasticity at the 1% significance level. In addition, following the studies of Malik et al. (2021), we conduct a Durbin–Wu–Hausman test (Table 5) to assess the presence of endogeneity among the identified CG variables. The results of the Durbin–Wu–Hausman test reject the null hypothesis that CG variables are exogenous. Hence, it is imperative to adopt an estimation technique that addresses the observed endogeneity issue to deliver consistent and reliable estimates. We employ the GMM to control for the endogeneity challenge in this study.

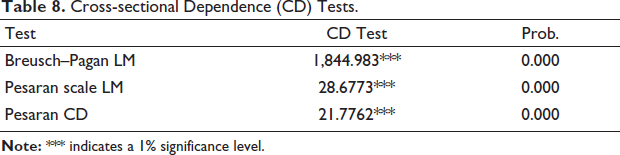

Furthermore, there is increased evidence of CD among listed firms, especially financial firms, due to the nature of their activities (Olaniyi et al., 2022). The conventional panel estimation techniques such as the fixed effect model presented above assume that the listed financial firms in the study are cross-sectionally independent. This implies that each firm makes decisions independently without recourse to other firms in the industry. However, in the real world, this might not be the case. Hence, there is a need to carry out a formal test to establish the presence or absence of CD among the firms in the study. Following this, the study subjects the outcomes from the fixed-effects models (Table 6) to CD tests via the Breusch and Pagan LM, Pesaran scale LM and Pesaran CD tests proposed by Breusch and Pagan (1980), Pesaran et al. (2008) and Pesaran (2021), respectively. The outcomes from the CD tests are displayed in Tables 7 and 8. The findings from the CD tests confirm the evidence of CD among the firms in the study. The outcomes are consistent across the three tests, which implies that the financial firms in South Africa are interdependent in their operations. Similar findings are reported by Olaniyi et al. (2022) for listed firms in Nigeria. Therefore, it is imperative to control for serial correlation, heteroscedasticity and CD in the study to ensure that the estimates are free from these econometric flaws. To achieve this, we adopt the Driscoll and Kraay (1998) robust standard error approach using the Stata command xtscc proposed by Hoechle (2007) as the primary estimation technique. To confirm the credibility and reliability of the estimates, we also employ the FGLS and PCSE as robustness tests.

Diagnostic Tests for Serial Correlation and Heteroscedasticity in the Error Term.

Cross-sectional Dependence (CD) Tests.

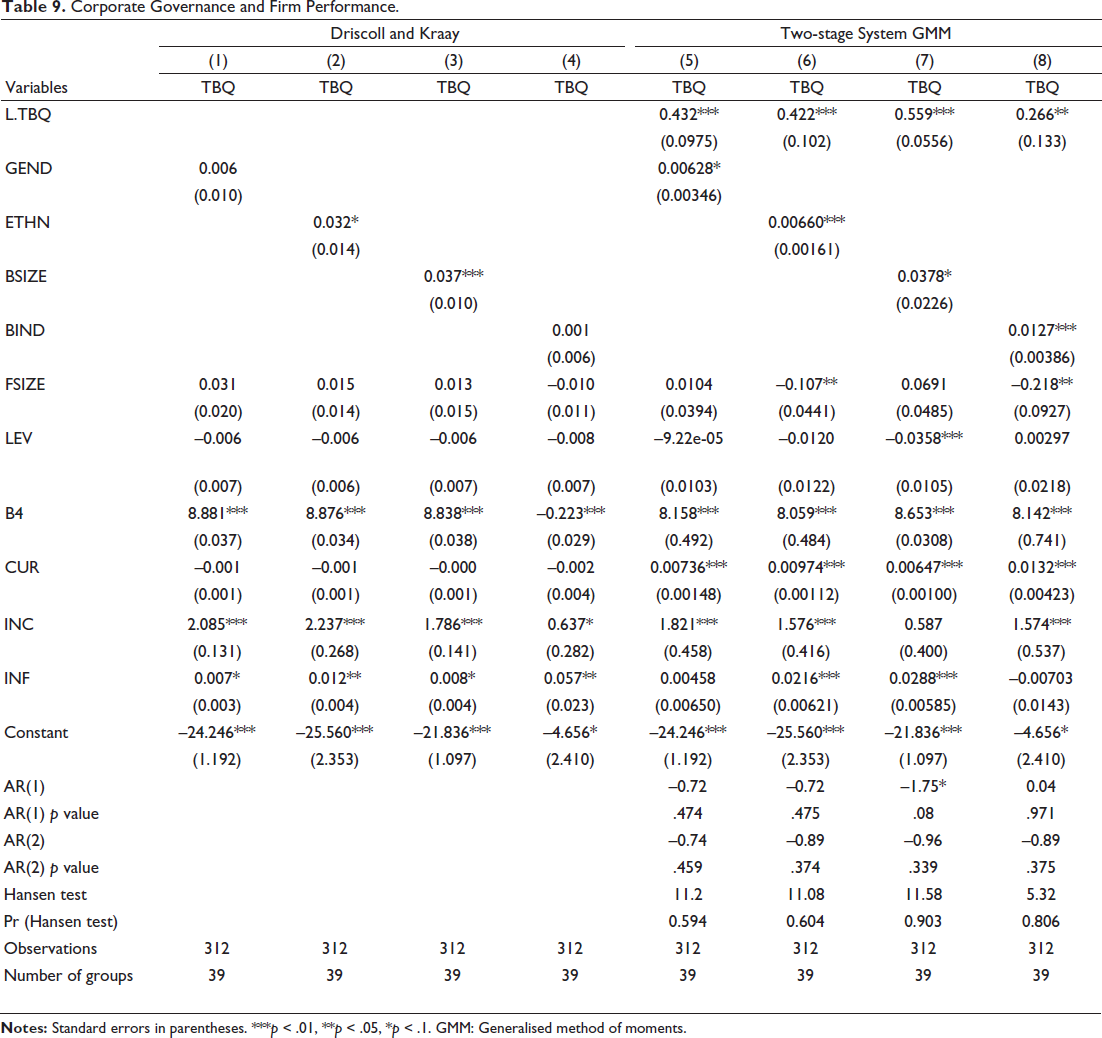

Effect of CG on FP

Following outcomes from the diagnostic tests, we re-estimate Equation (2) using the Driscoll and Kraay (DK) robust standard error to control for CD in the study. The outcomes of the DK approach are presented in Models 1–4 of Table 9. For the robustness of the findings, we also control potential endogeneity in the estimated models via the two-stage generalised method of the model, as displayed in models 5–8 (Table 9). Following the modelling style in Table 6, we estimate four models to account for the impact of the four metrics of CG under each of the two estimators. Specifically, Models 1–4 contain the outcomes from the DK approach, whereas the results from the GMM approach are presented in Models 5–8. Starting with the results from the DK specifications, income per capita (LGDP), inflation (INF) and audit quality (B4) have positive and significant effects on FP. The results imply that a favourable macroeconomic environment stimulates FP. In a similar manner, CG indicators such as ethnic diversity (ETHN) and board size (BSIZE) are discovered to enhance FP among the listed financial firms in South Africa in Models 2 and 3, respectively. Specifically, a unit increase in ethnic diversity and board size results in 0.039 (Model 2) and 0.035 (Model 3) increases in FP (TBQ), respectively. Again, the effects of gender diversity (GEND) and board independence (BIND) on FP (TBQ) are inconsequential, suggesting that the two corporate metrics fail to stimulate FP in the selected sector (Models 1 and 4). This suggests that the presence of women and independent directors has no significant effect on FP. A plausible explanation for this might be the proportion of women directors on the corporate board of the sample firms. For instance, the outcome from the descriptive statistics indicates that only 23% of the directors are female.

Corporate Governance and Firm Performance.

However, when the results from the GMM approach are considered, there is an absence of serial correlation in all the estimated models, as revealed by the probability values of AR(2), which are statistically insignificant (Models 5–8). Similarly, the values of the Hansen statistic for over-identified restrictions suggest that the instruments employed in all the estimated models are valid. The coefficients of the lag values of the dependent variable (L.TBQ) are positive and significant in all the GMM specifications (Models 5–8). Overall, the outcomes from Models 5–8 in Table 9 reveal that the GMM approach produces better and more consistent results than the DK specifications do. For instance, outcomes from the GMM models reveal that all the identified CG variables have a positive and significant effect on the outcome variable. Specifically, a unit increase in gender diversity, ethnic diversity, board size and board independence stimulates the performance of JSE financial firms by approximately 0.006, 0.007, 0.038 and 0.013, respectively. Overall, the outcomes reveal that large board size, board independence, gender and ethnically diversified boards are fundamental to achieving better financial outcomes among financial firms in South Africa. With respect to the control variable, the favourable effects of audit quality, income per capita and inflation on FP are persistent. Unlike the outcomes from the DK models, the results from the GMM specifications confirm a positive and significant effect of the current ratio on FP. Hence, we focus on the outcome from the GMM models under the discussion of findings in the subsequent section.

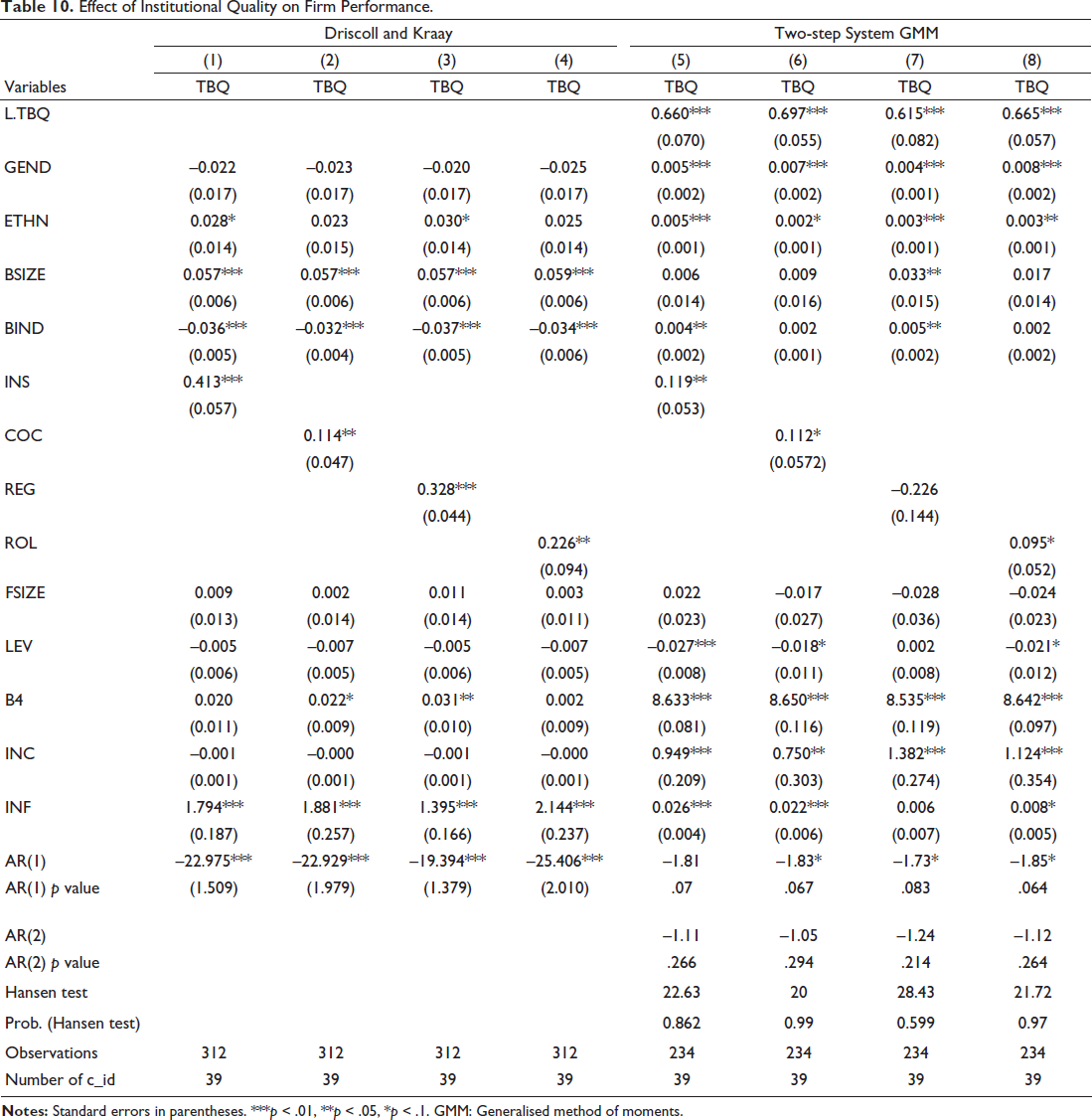

Institutional Environment and FP Nexus

In the second stage of the analysis, we explore the effects of IQ in South Africa on the performance of JSE-listed financial companies. To achieve this, we incorporate each of the three measures of IQ and the INS into the FP model in a stepwise manner, as presented in Equations (5)–(8). Similarly, we present the outcomes from both the DK and GMM approaches for the robustness of the estimates. The results of the estimates of the institutional environment are displayed in Table 10. Models 1, 2, 3 and 4 capture the effects of INS, COC (COC), REG and the ROL, respectively. The coefficients of all the institutional variables are positive and statistically significant. Similarly, all the estimated models pass the GMM diagnostic tests. The probability value of AR(2) is not significant, implying the absence of serial correlation in all the estimated models. Similarly, the probability value of the Hansen tests is not significant, confirming the validity and reliability of the selected instruments. All the indicators of CG significantly enhance FP in the sector except for Model 7, which is not statistically significant. This outcome underscores the importance of a good institutional environment in promoting FP. This further implies that the overall institutional architecture and framework in South Africa play crucial roles in driving the overall financial performance of financial companies. This again highlights the importance of good institutional infrastructure as a strategic driver of FP. In line with prior findings, income per capita (INC), inflation (INF) and audit quality (B4) persistently enhance FP across all the model specifications. However, with the incorporation of institutional variables, the impact of governance indicators on FP varies under the two approaches. For instance, board ethnic diversity (ETHN) and board size (BSIZE) consistently stimulate FP in Models 2 and 3, respectively. However, with the incorporation of institutional variables, the impact of governance indicator board independence (BIND) on FP is found to be negative and significant. Consistent with the outcomes from the DK specification, the magnitude of gender diversity (GEND) is not significant, suggesting that board diversity in terms of gender does not contribute to the increase in the value of the sample firms. On the other hand, under the GMM specifications, all the metrics of CG have positive effects on FP, although with different levels of significance.

Effect of Institutional Quality on Firm Performance.

Moderating Role of the Institutional Environment in the CG–Financial Performance Nexus

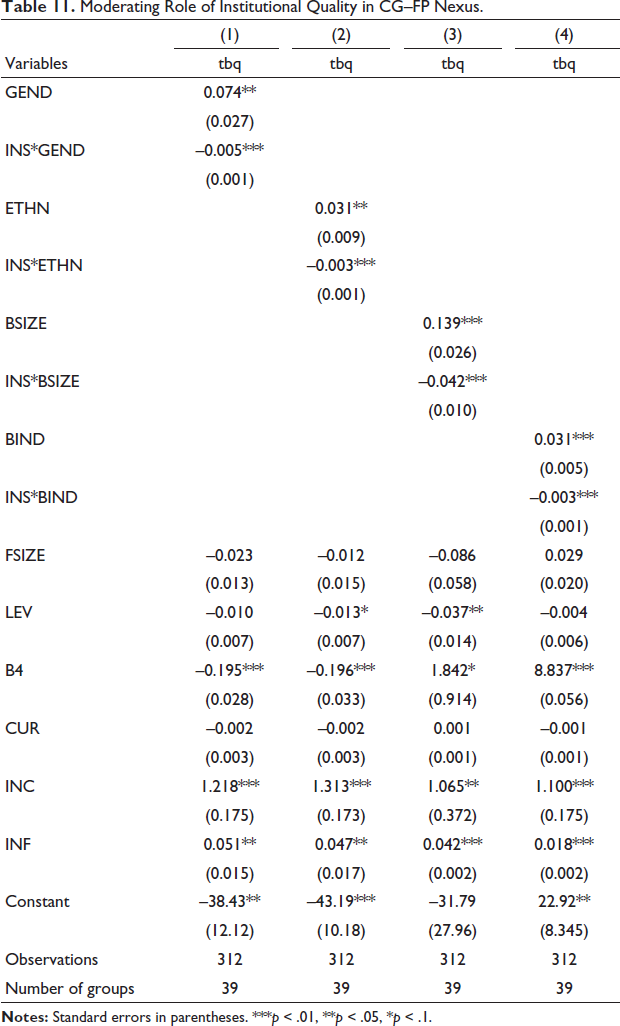

The third and final stage of the analysis delves into the moderating role of South African institutional architecture in the relationship between CG indicators and the performance of listed financial firms, based on Equation (9). In doing so, we incorporate the interaction term between the IQ index and CG indicators and examine their joint and combined impacts on FP, as depicted in Models 1, 2, 3 and 4 for GEND, ETHN, BSIZE and BIND, respectively. The outcomes of this analysis are presented in Table 11. The magnitudes of income per capita, inflation and audit quality are overwhelmingly positive and significant. Although the primary focus in this subsection is the coefficients of the interactive terms between IQ dimensions and CG measures, importantly, with the incorporation of the interaction terms, the magnitudes of all the CG indicators become positive and statistically significant, suggesting that FP is enhanced by an increase in the proportion of women directors, black directors, board size and board independence in Models 1, 2, 3 and 4, respectively.

Moderating Role of Institutional Quality in CG–FP Nexus.

However, the results for the focal variable suggest that the INS and the three dimensions of IQ, namely, COC, REG and ROL, negatively and significantly moderate the influence of governance metrics on FP. The outcome is robust and consistent across different model specifications and four measures of CG. This implies that the institutional environment in South Africa plays a strong moderating role in the relationship between CG and FP, suggesting that institutional variables and CG measures act as substitutes affecting the performance of selected financial firms in South Africa. This is, however, in conflict with our expectation, as IQ is expected to complement and enhance the impact of CG on FP. The results further prove that IQ in South Africa weakens and drains the positive effect of CG on FP.

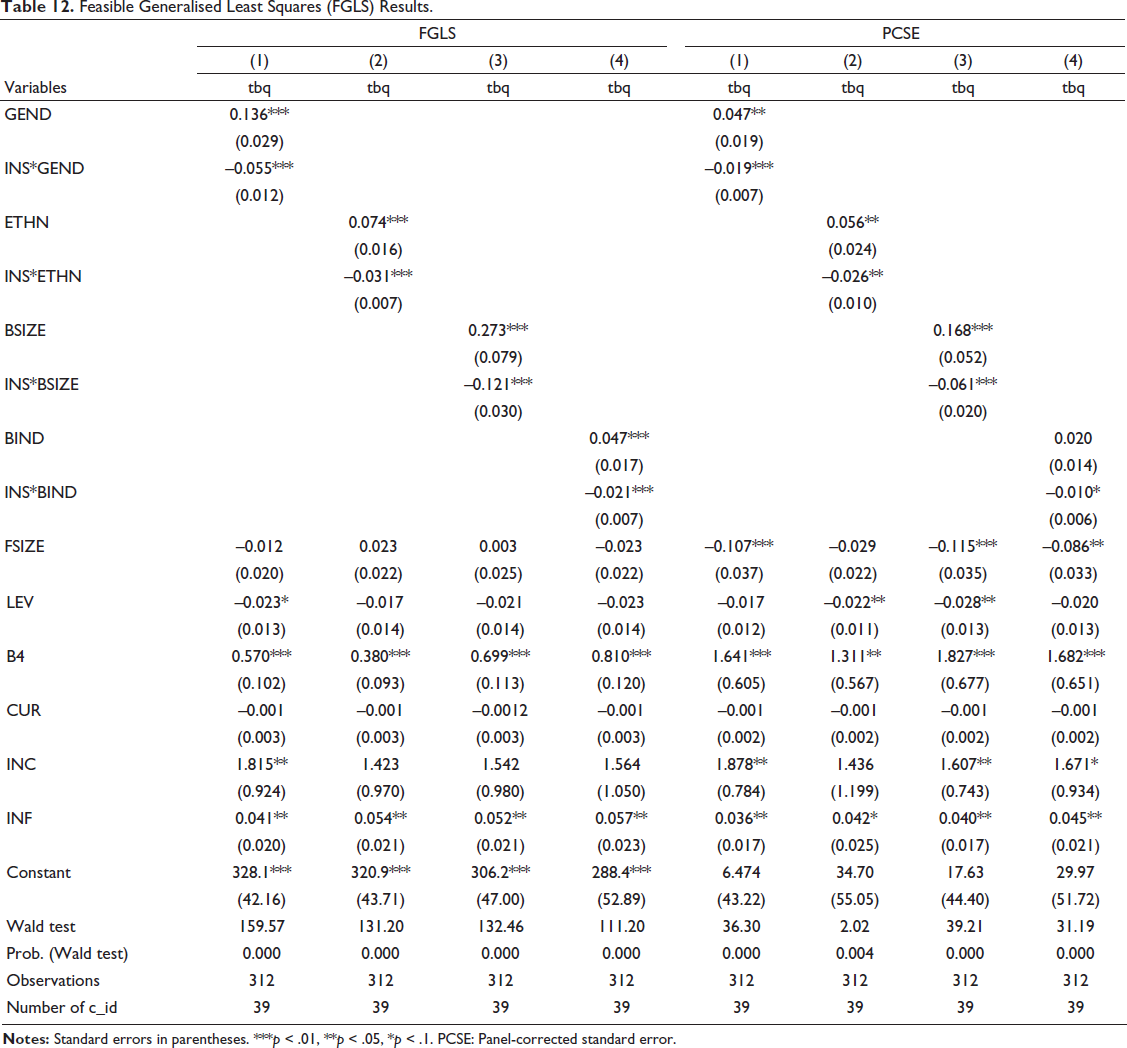

Robustness Using Alternative Estimators

To verify the credibility and reliability of the outcomes from the main analysis, we re-examine the moderating role of IQ on the connection between CG and FP in the financial sector via other estimation techniques. Specifically, we employ FGLS and PCSE as alternative estimation approaches for the robustness of the study’s outcomes. The results from the robustness tests are displayed in Models 1–4 and Models 5–8 for FGLS and PCSE in Table 12, respectively. Consistent with the prior outcomes, all the components of CG support better financial outcomes in the sector except board independence in Model 8, which is not significant. The outcomes validate the findings from the Driscoll and Kraay model (Table 11), indicating that sound CG promotes FP with strong IQ. Similarly, the coefficients of IQ and all the metrics of CG are negative and statistically significant. Consistently, all the control variables maintain their initial effect on the outcome variables with minor discrepancies. This finding reinforces and substantiates the outcome from the main estimation techniques, reiterating the detrimental effect of IQ on the interplay between CG and FP among financial firms in South Africa. In line with the previous results, control variables such as audit quality, income per capita and inflation significantly promote FP. Generally, the results conform to the initial findings when the IQ index is employed as a moderating variable.

Feasible Generalised Least Squares (FGLS) Results.

Discussion of Findings

This study probes into the moderating role of the institutional environment in the interplay between CG and the performance of listed financial companies in South Africa. With respect to the primary effect of CG on FP, CG indicators such as board ethnic diversity and board size have significant positive effects on market-based performance (Tobin’s Q) among listed financial firms in South Africa. The results are consistent across different model specifications and robust to alternative techniques. This implies that a more ethnically diverse board strengthens FP. This leads to the acceptance of H1d that ethnic diversity is positively and significantly associated with FP. This finding aligns with the resource dependency theory that the inclusion of directors of ethnic origin in corporate boards provides human capital and an external network to attract the critical resources that are needed to increase firm value and performance (Carter et al., 2010). Carter et al. (2003) find that board ethnic diversity is linked with an increase in the value of Tobin’s Q of the listed Fortune 1000 firms. This finding also confirms the outcomes of previous studies, including Ujunwa et al. (2012) for quoted firms in Nigeria and Cheong and Sinnakkannu (2014) and Chuah and Hooy (2018) in Malaysia. Similar findings are reported by Ntim et al. (2015) and Bin Khidmat et al. (2020) for South African and Chinese firms, respectively. All these studies document that ethnic diversity is a strong predictor of FP measured by Tobin’s Q. This finding has crucial implications for the performance of financial firms in South Africa, given the country’s antecedent orchestrated by the popular apartheid policy, where black firms are excluded and marginalised in the board decision-making process. With more black directors in the boardroom, firms can gain access to critical resources and garner stakeholders’ acceptance and confidence, which consequently boosts their legitimacy and enhances their financial outcome. However, our results negate the outcomes of Awaworyi Churchill et al. (2017) and Awaworyi Churchill and Valenzuela (2019), who discovered that ethnic diversity hurts FP.

Similarly, our study confirms that the board size of the sample financial firms promotes Tobin’s Q in South Africa, which aligns with the agency theory proposition, which advocates that a large board size is an effective governance mechanism to resolve agency conflict and stimulate FP, suggesting the acceptance of H1a on the board size–FP nexus. The outcome is in tandem with prior studies (García-Ramos & Diaz, 2021; Kahloul et al., 2022; Mertzanis et al., 2019; Queiri et al., 2021; Singh et al., 2018) that argue that a large board size provides firms with diverse human and material resources, skills, expertise and experience, which significantly promote firm financial performance. Similarly, Tshipa et al. (2018) support the finding that an increase in board size promotes firm value (Tobin’s Q) among listed firms in South Africa between 2002 and 2014.

In line with previous studies on South African firms (see Gyapong et al., 2016; Ntim et al., 2015), our findings reveal that gender diversity is a significant predictor of market-based performance, which implies the acceptance of H1c. This again highlights the importance of diverse gender boards in promoting organisational performance. The results support the findings of Okoyeuzu et al. (2021), who find that gender diversity promotes the performance of commercial banks in Nigeria. The implication of this finding implies that female board members use their human relational skills and are concerned with stakeholders influencing board decisions to promote FP in the sector. Similarly, the role of board independence in FP is positive and significant. This leads to the acceptance of H1b. The outcome aligns with the proposition of agency theory and the findings of existing studies (Al Amosh & Khatib, 2021; Al Farooque et al., 2020), which claim that the presence of independent directors in the boardroom influences board decisions in favour of shareholders’ interests and thus contributes positively to FP. In the same vein, this outcome upholds the proposition of the CG code in South Africa, King IV, which advocates for more independence in the composition of corporate boards. Since independent directors have little or no financial interest in the firm, they tend to be impartial and provide an assessment of the company’s activities.

Considering the metrics of the institutional apparatus, INS, COC and REG in South Africa significantly stimulate FP. The outcome supports H2 of the study. This finding corroborates the prediction of institutional theory that a favourable institutional environment provides the necessary stimulant for economic performance and market value. The outcomes confirm the conclusion of Singh (2023) that national governance enhances the profitability of microfinancing institutions in BRICS countries. This finding also corroborates the findings of Jabbouri and Almustafa (2021) and Kafouros et al. (2024) that national governance improves firm profitability by curtailing the negative effect of agency conflict within an organisation. The outcome also aligns with the outcome of Agostino et al. (2020), who document that institutional variables such as government stability and the ROL enhance firm productivity in the European region. The outcomes also align with the results of Again, Mertzanis et al. (2019), who find that institutional factors such as COC, REG and political stability are significant predictors of accounting-based financial performance for listed firms in the MENA region. The findings also reinforce the outcomes of Karmani and Boussaad (2021), who discovered that government stability and law order have a positive and significant effect on the performance of 814 European firms. Similarly, Lu and Wang (2021) find that the legal environment and country governance facilitate environmental performance. This outcome implies that when there are strict measures in place to check corrupt practices, managers and directors are discouraged from engaging in sharp practices that are detrimental to shareholders’ interest, which consequently increases firm value. Similarly, when the government implements sound policies and regulations, investor confidence is enhanced, and the protection of rights and private property stimulates the development of the private sector. With sound REG and control of corrupt practices, managerial entrenchment and selfish and opportunistic behaviour can be mitigated, which consequently results in better performance. This finding implies that the South African institutional environment plays a pivotal role in influencing business performance by providing the necessary infrastructure and a conducive environment that supports private sector development. Thus, the institutional environment provides an external mechanism to resolve internal agency problems by discouraging the tendency for self-promoting interests among managers and board members (Singh, 2023). Thus, the study argues that the institutional environment in South Africa supports the financial performance of financial companies in these countries.

However, when the interaction terms are incorporated into the analysis, all the indicators of CG positively and significantly enhance FP. With respect to the effect of IQ on the CG‒FP relationship, the INS in South Africa negatively moderates the nexus between the governance variables and FP, suggesting that underdeveloped and weak IQ undermines and mitigates the positive and favourable effect of CG on the performance of financial firms in South Africa. This, in turn, indicates the rejection of H3 that IQ complements and strengthens the effect of CG on FP. The outcome from the study implies that IQ fails to support CG to increase FP. The results, however, contrast with the findings of Uribe-Bohorquez et al. (2018), who observe a complementary relationship between the institutional environment and board independence for listed firms in America, Europe and MENA countries. Similarly, the results contradict the outcome of Nguyen et al. (2021), who document that IQ plays a strong moderating role in the relationship between gender diversity and performance of listed firms in 46 countries. The findings negate the outcome of Atugeba and Acquah-Sam (2024), which reveals that national governance complements the impact of CG on FP among 31 listed firms in Ghana. Moreover, none of these studies focuses on financial firms as a unit of analysis. This again highlights the need to examine the role of IQ in an emerging economy with a different institutional environment, such as South Africa. The outcome is, however, not surprising considering the poor performance of South Africa in terms of the indicators of institutional variables, where the country scores average values of 2.40, 2.52, 2.4 and 2.5 on the scale of 0.0–5.0 when COC, REG, ROL and INS, respectively. The result further implies that a weak institutional environment in the country promotes loopholes and encourages selfish and opportunistic behaviour among a company’s directors to engage in practices that undermine FP. Hence, this study finds that a poor institutional environment weakens the effectiveness of internal governance mechanisms in stimulating FP. This is because a weak and ineffective external institution increases transaction costs and discourages the enforcement of contracts, which increases contract firm value. Similarly, a loose regulatory environment encourages unethical practices and thus leads to poor financial performance. The study concludes that the institutional environment fails to complement CG to increase firm value among listed financial firms in South Africa. Alternatively, the outcome from the interaction terms suggests that institutional architecture and CG act as substitutes rather than complements to facilitate better financial performance in the financial sector. The results also imply that the separate enhancing impact of CG on FP is reduced and mitigated by weak IQ. Thus, we find that IQ in South Africa fails to stimulate and complement CG to achieve better financial outcomes.

Conclusion and Recommendations

Building on agency and institutional theories, the present study explores the moderating role of IQ in the nexus between CG mechanisms and the market-based performance (Tobin’s Q) nexus among listed financial firms in South Africa. In addition, the study accounts for the effect of the macroeconomic environment on the nexus between the two target variables by incorporating income per capita and inflation in the analysis. To further fill the lacuna in the literature, the study deepens its analysis by controlling for the influence of CD among the sampled firms via the robust standard error approach within the framework of Driscoll and Kraay (1998) to control for serial correlation and CD in the analysis. The findings from the main analysis are subjected to a number of robustness tests using the FGLS and PCSE as alternative estimators. As a preliminary procedure, the article confirms the evidence of CD among the studied financial firms, which suggests evidence of interdependence and interconnectivity among the firms in the sector.

The main findings of this study are as follows: (a) Focusing on the direct effect of CG on FP, CG metrics, such as gender diversity, ethnic diversity, board size and board independence, stimulate FP among financial companies in South Africa; (b) the INS, COC, REG and ROL in South Africa significantly promote FP; (c) in addition to incorporating the interaction term between IQ and CG variables, all the metrics of CG promote FP; (d) the INS negatively moderates the link between CG and FP and thus acts as a substitute for CG indicators to mitigate the performance of financial companies in South Africa; and (e) control variables, such as inflation, income per capita and audit quality, are significant drivers of the performance of the selected financial firms in South Africa. The overall implications of the outcome are that CG and institutional variables separately and individually enhance FP. However, the IQ index negatively moderates the interplay between CG and FP, implying that the beneficial effect of CG on FP is drained and eroded by weak and poor IQ in South Africa.

The outcomes from the study offer some policy recommendations to regulators and custodians of CG in South Africa, policymakers in the financial sector, firm managers, corporate investors and other stakeholders. For regulators, it is imperative to consider the gender mix of the corporate boards of financial firms to achieve balance and equity in board gender composition. In addition, CG regulators should ensure the strict enforcement of firms to achieve a certain minimum proportion of female directors in board composition, such as in countries such as Norway, where there is legislation on women’s representation in the boardroom. In the same vein, CG regulators in South Africa are advised to continue monitoring corporate firms to ensure that they adhere strictly to the prescription of the King IV code of CG in terms of board ethnicity and independence, as these are found to increase the overall performance of firms. Moreover, the appointment of independent directors should not be based on politics but on merit to be able to make significant contributions to board decisions that affect the welfare of shareholders. For policymakers, it is important to invest more in building a strong institutional infrastructure that discourages corrupt practices at the level of companies and guarantees stricter enforcement of the ROL to protect investor confidence. For investors, it is important to consider firms whose board composition promotes ethnicity and independence while making investment decisions to guarantee superior returns on their investment.

This study has advanced the frontier of knowledge in the CG–FP nexus by emphasising the importance of IQ, which has been relatively neglected in the finance literature. Similarly, the study focuses on the financial firms listed on the JSE because of the critical and fundamental role of the financial sector in economic growth and development. However, like any other study, some limitations can be identified that can provide a road map for future empirical engagement. First, the study focuses on board attributes as CG mechanisms, and future studies can consider other aspects of CG, such as board remuneration, board committee attributes and board qualifications. Second, the study concentrates on financial firms in South Africa, suggesting that the outcomes from the study may not be applicable to other emerging economies. Subsequent studies may consider a comparative study to gauge the influence of the institutional environment on the relationship between CG and FP for other countries with different regulatory and institutional environments.

Footnotes

Acknowledgment

The authors appreciate the invaluable contributions of the participants at the African Finance Conference held between 21 and 22 May 2024 at the University of Cape Town Graduate Business School, Cape Town, South Africa, towards improving the quality of the manuscript.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors gratefully acknowledge the generous financial support provided by the National Research Foundation of South Africa (Grant No. TTK2204062258).