Abstract

The present research aims to analyse the effect of environmental, social and governance (ESG) disclosure on firm value using a sample of Indian-listed firms. The current research adopts cross-sectional regression analysis approach to analyse the financial data of 940 sample firms. The market-to-book value ratio and Tobin’s Q ratio are considered as market value indicators whereas ESG disclosure has been measured as indicator variable from annual report. The results conclude that ESG disclosure has significant positive effect on the market value of the sample firms. Further, the study also analyses the effect of carbon-sensitivity on this relation and found that carbon-sensitive firms experience lower intensity of the positive effect on firm value as compared to others. The findings provide significant implications for managers who can use ESG related disclosures to enhance the firm value. Besides, policymakers can also use the present findings to convey the positive impact of ESG performance and thereby improve the adoption of sustainable and socially desirable business practices. The present study provides pioneering evidence on the firm value effect of ESG disclosure in the context of one of the largest growing economies. The ESG disclosure and firm value nexus has been underexplored in emerging countries, and hence present research adds value to the existing literature.

Introduction

In the present era, stakeholders of firms are becoming thoughtful about environmental damage and its impact on the financial performance of the firms (Kumar & Firoz, 2019; Saka & Oshika, 2014; Wang et al., 2023) and therefore business organisations face increasing pressure to disclose their plans to reduce greenhouse gas (GHG) and overall climate change strategy and save the planet (Alsaifi et al., 2020). As a result, business corporations are experiencing the significance of adopting and disclosing sustainability practices as it could increase the financial status of the firms (Abdi et al., 2022). The mandatory disclosure of non-financial information such as environmental, social and governance (ESG) practices provides several benefits to firms, investors as well as the society (Wang et al., 2023). It may reduce information asymmetry (Easley & O’Hara, 2004), agency conflicts (Yu et al., 2018) and adverse selection problems (Bushman & Smith, 2001; Verrecchia, 2001). Further, it enhances operating efficiency and firm value as supported by Freeman (1984). However, according to Fridman (1970), mandatory disclosure may also add some costs that are nontrivial to the firms such as additional exposure, proprietary cost of disclosure and the uncertain reaction of stakeholders to such disclosures. Though the debate on mandatory ESG disclosure is ongoing, several countries have enforced regulatory guidelines to compulsorily disclose ESG-related information along with other financial data. In the given context, the Security Exchange Board of India (SEBI) has issued a mandate for the top 100 listed companies (according to market capitalisation) to file a business responsibility report (BRR) as a part of their annual report to show ESG information in 2012 (SEBI, 2012). Considering the increasing awareness about ESG among stakeholders, in 2015, the number of companies increased to 500 and lastly, SEBI made it compulsory for the top 1000 firms to disclose ESG-related information. Further, in 2021 SEBI revised the BRR framework as the Business Responsibility and Sustainability Report (BRSR) and issued a detailed format for the same. The BRSR includes general disclosures, management and process disclosures as well as states nine principles including ethics, transparency, accountability, sustainability, well-being of employees, promoting human rights and protecting and restoring the environment. Though ESG disclosures are becoming compulsory, managers are sceptical about their impact on firm performance. Research scholars have attempted to draw a meaningful relationship between ESG disclosure and financial performance (Abdi et al., 2022; Duque-Grisales & Aguilera-Caracuel, 2021; Li et al., 2018); however, most existing studies have been conducted in a developed nation and little evidence exist for emerging countries. Further, ESG disclosure norms are linked with the regulatory framework of specific nations, and hence extant results cannot be generalised. Besides, it is important to note that the extant literature provided mixed outcomes about ESG disclosure and firm performance. Freeman (1984) supported the positive effect of disclosing ESG-related information as it provides a better understanding of firms’ business, whereas Fridman (1970) and Vance (1975) opposed this concept by showing the thing is that disclosing ESG information is time-consuming as well as costly (Li et al., 2018; Wang et al., 2023). Hence, disclosure of ESG practices could be advantageous to the firms only if the firms could have more benefits than costs associated with disclosing the information (Zhang et al., 2020), it would hurt the firms’ value.

Provided the need for research-based evidence for the adoption of ESG reporting, the present study purports to analyse how ESG disclosure affects the market value of Indian companies. As stated earlier, ESG reporting is mandatory from fiscal year 2022–2023; however several firms were disclosing it voluntarily before this regulation. Hence, current research considers a sample of 940 companies for the financial year 2021–2022 to analyse how ESG reporting affects firm value. Besides, the study also examines the role of carbon-sensitivity in determining the nexus between ESG and market value. The findings describe that ESG reporting and firm value are significantly and positively related to Indian firms. Further, it is also found that the magnitude of the positive effect reduces for carbon-sensitive firms and thereby the results confirm the moderating effect of carbon-sensitivity.

The remaining manuscript has been structured as follows. The second section describes the review of theoretical as well as empirical literature along with hypothesis development. The third section presents the methodology of research whereas the fourth section explains the results and discussion. Lastly, the fifth section concludes the research along with limitations.

Literature Review

Theoretical Review

Disclosure of non-financial information has been governed by several theories such as stakeholder theory, signalling theory and resource-based theory as discussed in the subsequent section.

Stakeholder Theory

Stakeholder theory is based on the concept of acceptance of firm actions by all interested parties and not only shareholders (Abdi et al., 2022). The firms have a greater responsibility not only to their shareholders but also to a variety of associated groups (Ebaid, 2023). The theory suggests that mutual trust and cooperation between management and stakeholders can help reduce implicit and explicit costs (Eccles et al., 2014; Li et al., 2018). The disclosure of ESG information acts as a means to show the sustainability initiatives (Aouadi & Marsat, 2018) wherein firms create value for stakeholders through ESG investments (Behl et al., 2022; Saeidi et al., 2015). Through socially responsible behaviour, firms can address the needs of various groups of stakeholders (Fatemi & Fooladi, 2013) which further assists the firms in getting new paths to flourish their business and would be able to reduce risk (Fatemi et al., 2018).

Signalling Theory

Signalling theory has been developed by Akerlof (1978) and further extended by Spence (1973) and Stiglitz (1985). As per this theory, information asymmetry between managers and owners can be lowered by voluntary information with external stakeholders (Hahn & Kühnen, 2013; Yekini et al., 2012). Management groups convey information regarding firms’ better performance to outsiders through the lens of voluntary disclosure as it could be beneficial to the firms to increase their reputation and position in the market (Vitezić et al., 2012). Therefore, voluntary disclosure should be in the annual report of the firms to reduce information asymmetries as could be explained by the signalling theory (Vitezić et al., 2012). Several past studies (Ching & Gerab, 2017; Taj, 2016) have concluded that through disclosure of long-term sustainability initiatives, managers tend to provide signals of their commitment to society, the environment and stakeholders.

Resource-based Theory

The concept of resource-based theory was introduced by Birger Wernerfelt (1984) and later developed and refined by Jay Barney in 1991 (Gallego-Álvarez et al., 2011). It points out that resources and capabilities possessed by enterprises provide a foundation to exercise lasting competitive advantages (Wernerfelt, 1984). For instance, better ESG performance obtained by managing environmental issues and investing in new environmental protection technologies act as significant resources for firms to gain competitive advantages (Zhou et al., 2022). Resource-based theory helps firms to use ESG performance as a resource that can be used to enhance productivity and sound financial health as well as abate environmental pollution. Further, a firm’s endowment of resources such as high ESG performance is difficult to accumulate or replicate by competitors (Barney et al., 2011; Surroca et al., 2010) which creates sustainable competitive advantages leading to outperformance.

ESG Disclosure and Firm Value: Empirical Review and Hypothesis Development

Consolandi et al. (2022) examined the influence of ESG materiality on equity returns over 3,000 US companies from January 2008 to July 2019. They found a positive relationship between ESG and equity performance as well as a favourable market response for companies dealing with high levels of concentration of ESG materiality. Ashwin Kumar et al. (2016) have studied the linkage between ESG performance and the volatility of the stock market. Their study revealed that companies with ESG incorporation had lower volatility in their performance of stock and could generate high returns. Similar results are concluded by Chen et al. (2022) who examined the impact of COVID-19 and ESG ratings on the reaction of the stock market of the US airline industry using an autoregressive jump intensity trend model. They concluded that firms with high ESG ratings/scores experience lower volatility during a pandemic. Another pandemic-linked study was conducted by Broadstock et al. (2021) who investigated the role of ESG performance of firms during COVID-19 global pandemic as there was a market-wide financial crisis. They pointed out that ESG performance could abate financial risk during the financial crisis period and a high ESG portfolio had higher returns than a low ESG portfolio. Wu et al. (2022) have examined the relationship between ESG and pricing efficiency of the Chinese listed firms and found a positive relationship between ESG and pricing efficiency. Lööf and Stephen (2019) examined the association between ESG scores of the firms and their downside risk on the stock market of five European countries for the period of 2005–2017. The result revealed that higher ESG scores could reduce the downside risk of stock return.

Another strand of literature argued that ESG disclosure and performance cannot increase the firm value or ESG cannot help firms enhance their financial performance. Takahashi and Yamada (2021) tried to find out the factors that affect the stock returns of Japanese companies during COVID-19 by taking a sample of 360 firms. They pointed out that the firms with high ESG scores had a negative relationship with abnormal returns. Lue (2022) investigated the impact of ESG on the stock return of UK securities from 2003 to 2020 and found a negative relationship between ESG and stock return means that low ESG score companies earned more return than the high ESG score companies. Edmans (2023) conjectured that investing in ESG has not been any special or worse thing; instead, it has been an intangible asset only to the firms. Firms with higher ESG should not be given more admiration for spending more for better ESG performance than other intangibles the firms have and high ESG performance should not be only the value drivers of the firms.

Based on the above discussion, it can be inferred that the relation between ESG disclosure and firm value is significant; however, the direction of this relation is inconclusive. Hence, the present study frames the following hypothesis.

ESG Disclosure and Firm Value—Indian Perspective

Few studies have explored the firm value and ESG disclosure nexus in the Indian context (Behl et al., 2022; Chelawat & Trivedi, 2016; Dalal & Thaker, 2019; Rastogi & Agarwal, 2023; Sharma et al., 2020) though majority of them were constrained by limited data set due to voluntary reporting framework. Chelawat and Trivedi (2016) have investigated the impact of ESG performance on the financial performance of 93 listed companies from the NSE CNX Nifty 100 index. Based on panel regression, they concluded that better financial performance is associated with improved ESG performance. Another research from Behl et al. (2022) and Ray and Goel (2022) aimed to investigate the time-varying relation between the market value of the firm and ESG disclosure for Indian companies. Their findings commensurate the results of Chelawat and Trivedi (2016) and supported the positive impact of ESG disclosure. In a similar vein, Maji and Lohia (2023) have used cross-sectional ESG data of 222 Indian firms from CRISIL and analysed its impact on financial performance. Based on the pooled OLS regression, they supported positive relation between component-wise as well as overall ESG score and financial performance. Besides the direct effect of ESG scores, a study from Mendiratta et al. (2023) focused on the controversial news related to firm’s ESG performance and its effect on the corporate valuation. Based on the panel estimates, they concluded adverse effect of media coverage of ESG controversy on the firm value whilst the media reach is high and severity is low. Further, past studies from Rastogi and Agarwal (2023) and Mishra et al (2024) have extended the ESG-firm value literature by incorporating the corporate governance factors such as ownership concentration, board size and board independence. Overall, the findings were congruent with the extant studies and supported the positive impact of ESG disclosure on the firm performance.

Company-specific Determinants of Market Value

Apart from ESG-related disclosures, the market value of the firm also depends on several company-specific determinants such as firm size, leverage, return on assets (RoA), tangibility and dividend payout (Abdi et al., 2022; Pulino et al., 2022; Wong et al., 2020) whose effect should be controlled for. Firm size represented by the total assets (El-Deeb et al., 2022) indicates the ability of the firm to achieve economies of scale (Brinette et al., 2023), which further enhances the firm value by improving the operational efficiency (Buallay, 2020). Besides, asset tangibility assists in accessing the long-term finance by lowering the bankruptcy risk and thus reduces the cost of capital and improves firm value (Wong et al., 2020). On the other hand, leverage (measured by the debt-asset ratio) posits a significant bipolar effect on the firm value as the existing studies provided mixed results with positive (Dalal & Thaker, 2019; Wong et al., 2020) as well as negative effect (Abdi et al., 2022; Pulino et al., 2022). Finally, dividend payout has been extensively used as a significant predictor of firm value (Kengatharan & Dimon Ford, 2019; Nautiyal & Kavidayal, 2018; Sharif et al., 2015). Higher dividend payout represents the earning power of the firm which boosts the confidence of shareholders and thereby augments the market value of the firm (Abdi et at., 2022). Thus, following the past studies, the present research considers the selected firm characteristics as determinants of market value of the firm.

Research Methodology

Sample and Data Collection

The present study is based on the BRSR framework issued by SEBI which applies to the top 1,000 companies as per the market capitalisation. Therefore, the initial sample consists of these companies and the final sample arrived based on the availability of data. Current research uses a multi-stage sampling approach wherein (a) firms with missing information about the selected variables are removed, and (b) financial firms are also excluded due to distinct operating norms (Kumar & Firoz, 2019). Hence, the final sample has been arrived at 940 companies. Further, as the BRSR framework is mandatory from the financial year 2022–2023, we have selected a prior year in which it is voluntary for the sample companies to file ESG reports. Hence, the financial data has been taken for the fiscal year 2021–2022. Here, it is important to note that the preceding financial years, that is, 2019–2020 and 2020–2021 possess abnormal characteristics due to the COVID-19 pandemic and therefore have not been considered in data structure. Finally, the sample comprises cross-sectional data from 940 companies for the financial year 2021–2022. To collect financial data about the selected variables, the PROWESS database of the Centre for Monitoring Indian Economy (CMIE) has been used. It is one of the most used sources of data in past studies focusing on Indian companies (Anantha Krishnan & Sengupta, 2023).

Variables of Study

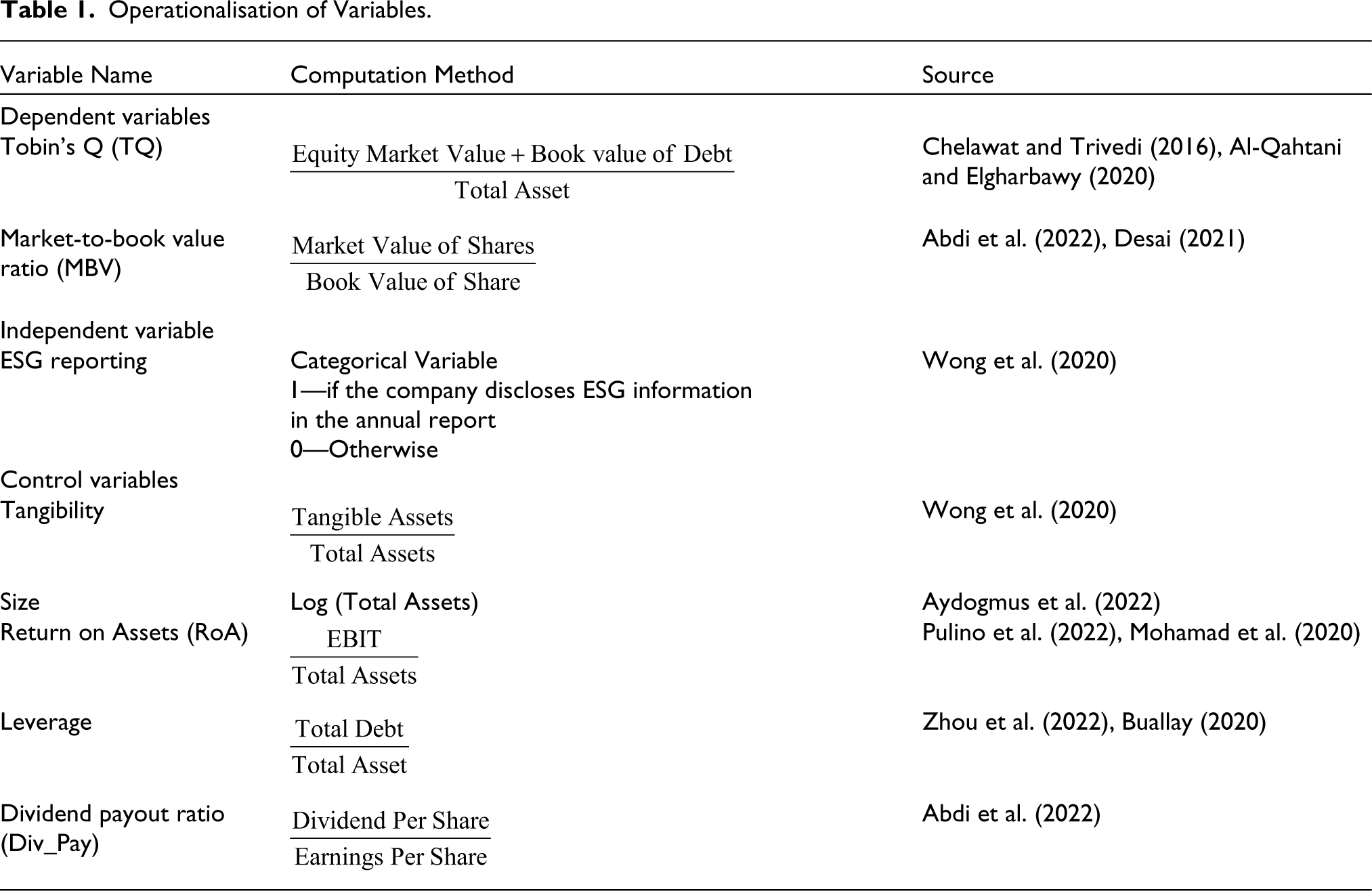

The present research aims to examine the effect of ESG reporting on firm value considering the same as independent and dependent variables respectively. Further, Table 1 presents the operationalisation of the variable along with the computation method and source.

Data Analysis Methods

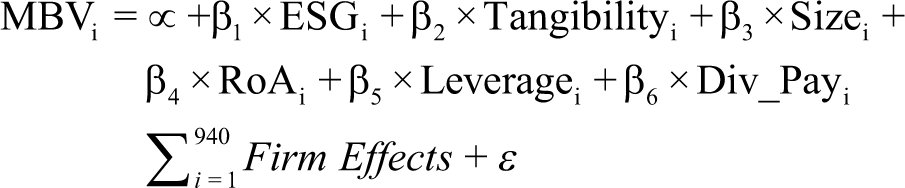

Financial data collected has been analysed using descriptive as well as inferential techniques. The present study is based on a cross-sectional regression model considering firm value as the dependent variable and ESG reporting as the independent variable. Further, the variance inflation factor (VIF) has been used to check multicollinearity. Eqns (1) and (2) represent the models to be estimated using a pooled regression approach.

Results and Discussion

Descriptive Statistics

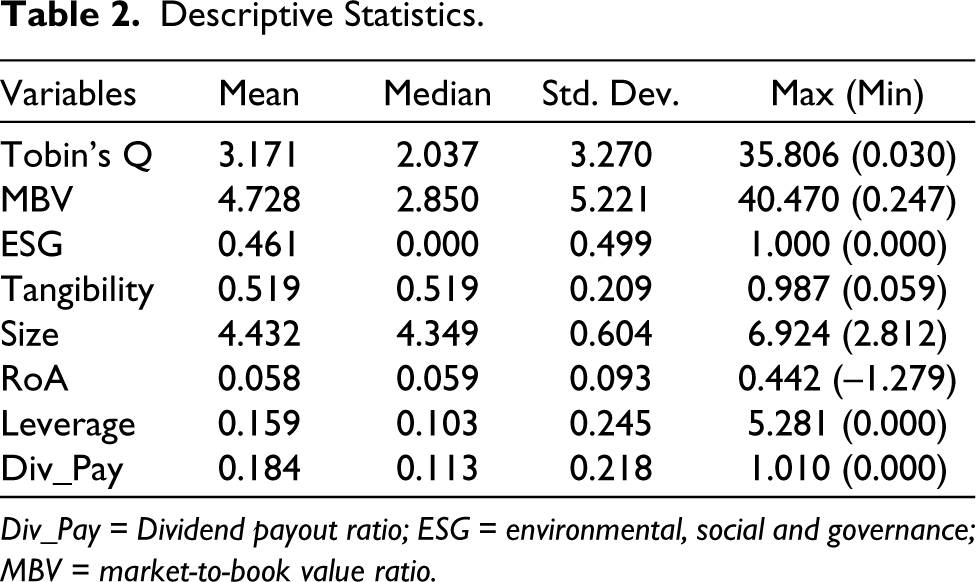

Table 2 presents the descriptive results of the sample financial data. The mean value of Tobin’s Q and MBV are 3.17 and 4.73 which reflects the higher market value of sample companies compared to book value as well as assets. However, both measures of market value have a greater standard deviation (Q ratio = 3.27; MBV = 5.22) value as compared to the mean which signifies a high degree of volatility. Referring to ESG results, 46.10% of firms have integrated ESG report out of the sample companies which indicates low-to-moderate adoption of ESG disclosure practices in the Indian context. Provided this, ESG disclosure has also observed inconsistent results as indicated by higher standard deviation values. Analysing the control variables, it can be inferred that sample companies hold approximately 52% of total assets as tangible with an average asset size of ₹32,170 million. Further, the mean RoA value is 5.80% which reflects low profitability, and the leverage ratio depicts only 16% of total assets are funded by debt. The average dividend payout of sample firms is 18.4% showing that the majority of profits are reinvested. Overall, descriptive statistics characterise the sample companies as high value, moderately disclosing, less profitable and low leveraged.

Operationalisation of Variables.

Descriptive Statistics.

Div_Pay = Dividend payout ratio; ESG = environmental, social and governance; MBV = market-to-book value ratio.

Correlation Analysis

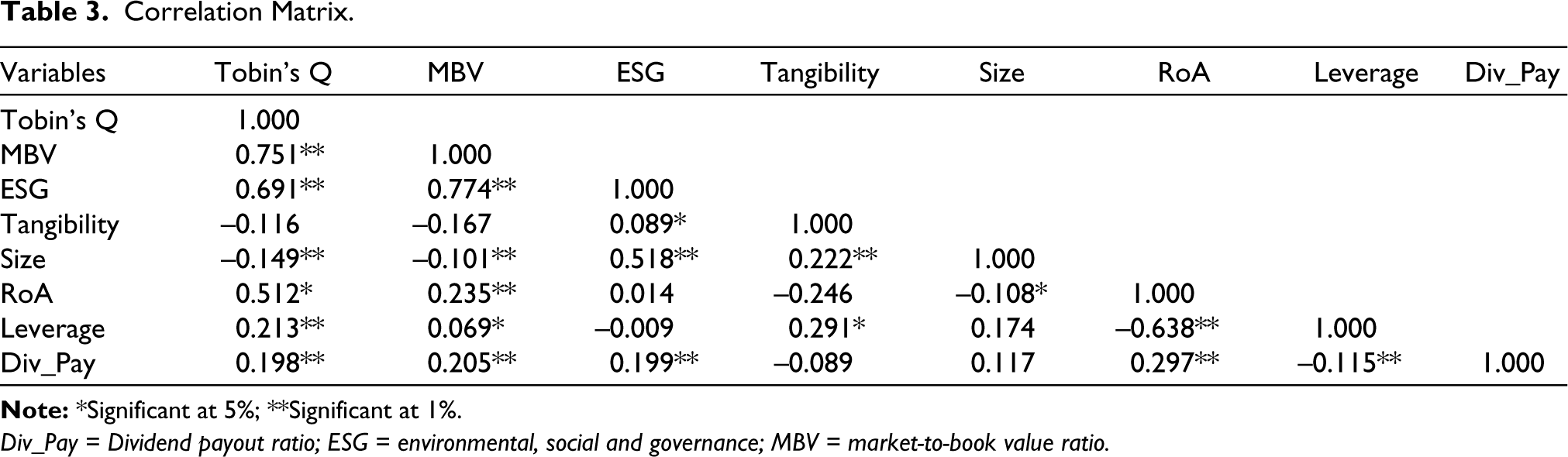

Table 3 summarises the results of Pearson correlation among the selected variables. Results show that ESG reporting has a significant positive relation with market value. The coefficient of correlation between ESG and Tobin’s Q ratio as well as MBV is 0.691 (p value < .01) and 0.774 (p value < .01) and both are statistically significant. Further, all control variables except tangibility are significantly correlated with both measures of market value. Size has a negative effect on firm value whereas RoA, leverage and dividend payout have significant positive relation with market value. Apart from market value, some independent variables are also correlated with each other significantly such as tangibility, size and leverage which may lead to multicollinearity issues. Hence, the study uses VIF measures to control the same and the results are discussed in the subsequent section.

Correlation Matrix.

Div_Pay = Dividend payout ratio; ESG = environmental, social and governance; MBV = market-to-book value ratio.

Regression Analysis—Full Sample

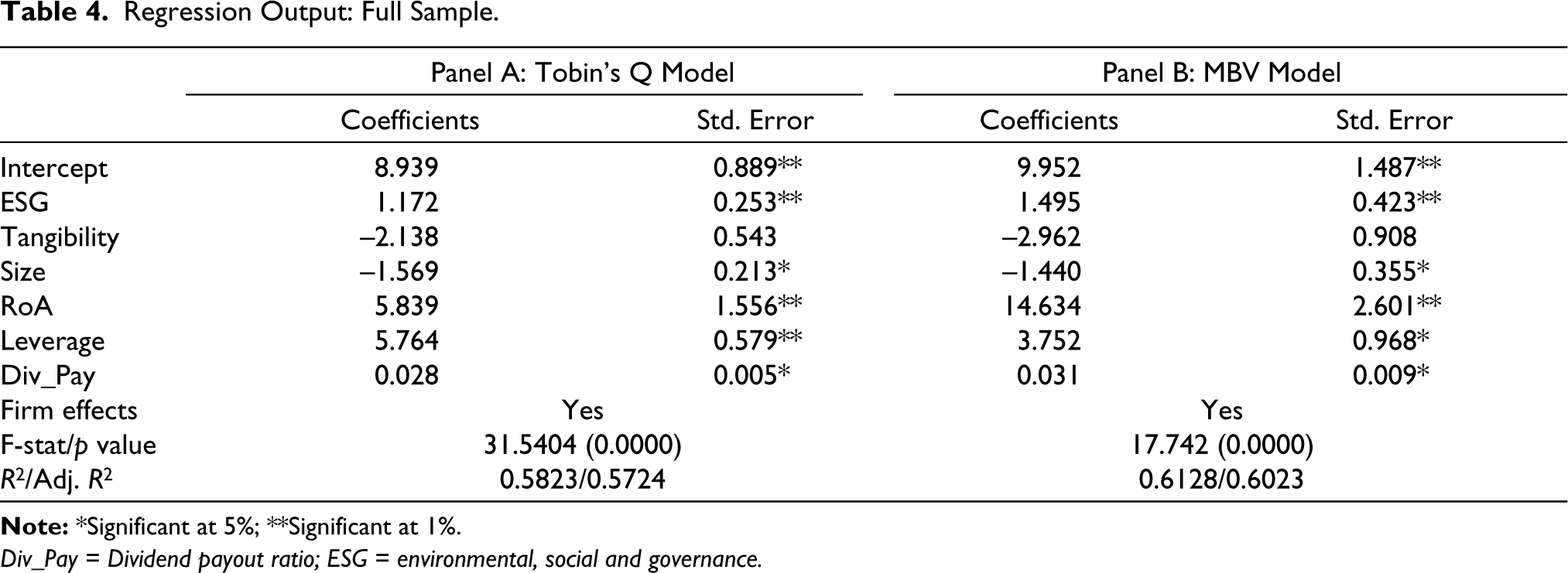

Table 4 describes the outcome of regression analysis considering Tobin’s Q and MBV as dependent variables. The overall significance of the regression model has been tested using F-test and results indicate that both models are statistically significant as p value < .01. Further, the regression coefficient, as shown in panel A of Table 4, indicates that ESG disclosure has a significant positive impact on Tobin’s Q ratio with β = 1.172 (p value < .01). Besides, except tangibility other control variables, that is size (β = −1.569, p value <.05), RoA (β = 5.839, p value <.01), leverage (β = 5.764, p value < .01) and dividend payout (β = 0.028, p value < .05) have a significant effect on Q ratio. The adjusted R2 value of the model indicates that 57.24% of changes in the Q ratio are explained by the estimated model. Apart from Tobin’s Q ratio, the present research also considers the MBV ratio as an alternate measure of market value to examine the robustness of the results. The regression outcome of the second model is also described in panel B of Table 4 and the overall model is significant and explains 60.23% changes in the MBV ratio. The impact of ESG disclosure and other control variables is congruent with that of Tobin’s Q ratio which confirms that findings are robust.

Regression Output: Full Sample.

Div_Pay = Dividend payout ratio; ESG = environmental, social and governance.

The current study purports to analyse the effect of ESG reporting on firm value and therefore cross-sectional regression analysis has been applied. The primary endogenous variable, ESG disclosure, has a significant positive impact on the firm value and contradicts the conclusion of the extant studies from Takahashi and Yamada (2021) and Edmans (2023). However, the findings are congruent with several past studies of Broadstock et al. (2021), Consolandi et al. (2022) and Chen et al. (2022). The positive effect of ESG disclosure can be explained as higher disclosures impedes information asymmetry between the investors and the managers. Further, shareholders can use such non-financial information to better evaluate the firm performance and correctly value the firm. Referring to the firm-control, except asset tangibility, all variables have a significant impact on firm value. The positive impact of profitability and dividend payout corroborates with the past studies of Qureshi et al. (2019) and Seth and Mahenthiran (2022) as it reflects the higher earnings of the firm. Further, leverage also enhances the market value of the firm as higher debt proportions reduce the overall cost of capital and thus increase the value of the benefits available to shareholders. The findings are consistent with Alsaifi et al. (2020). Finally, firm size has a significant negative effect on the firm value which contradicts the findings of Aydogmus et al. (2022) and can be explained as large firms require greater efforts to manage their internal operations which may hamper the efficiency.

Effect of Carbon Sensitivity

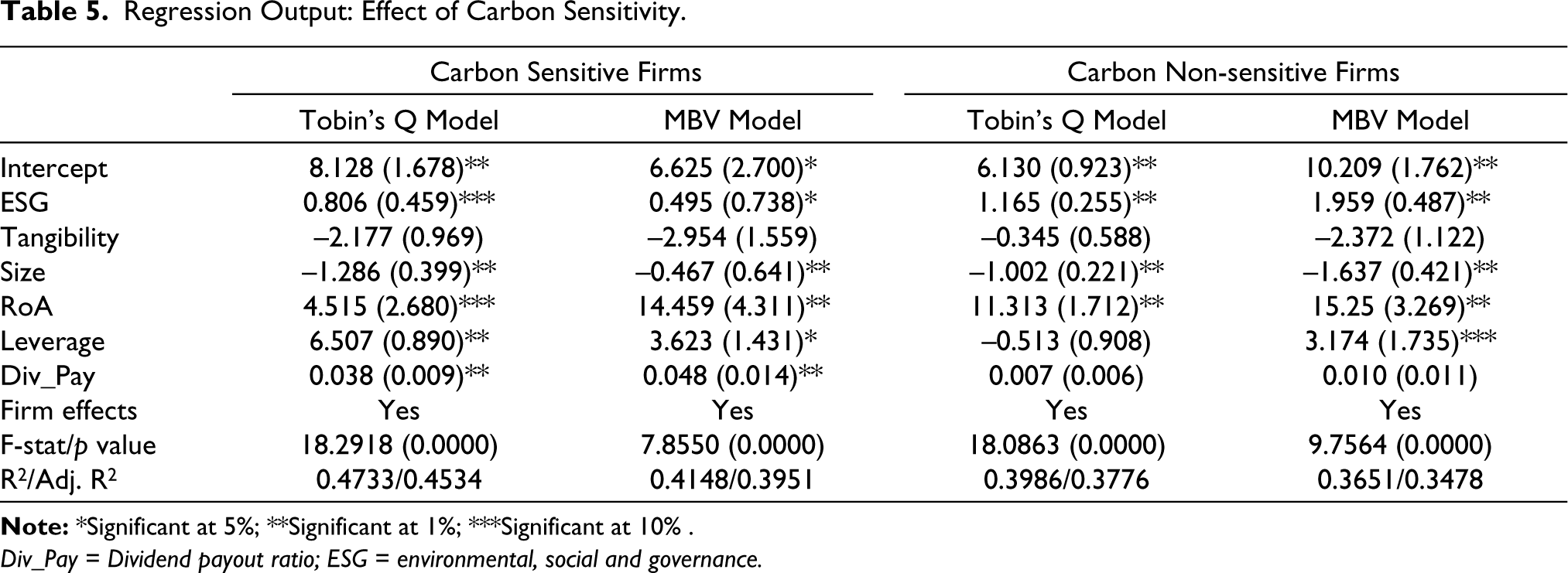

Besides the overall effect of ESG reporting, current research also proposes to examine the moderating effect of carbon sensitivity on the relation between firm value and ESG disclosure. Companies that operate in high-polluting industries such as coal, oil and gas, petroleum, energy, automobile and cement are considered as carbon sensitive, whereas non-sensitive firms operate in low-polluting industries such as banking, FMCG and food and agro products. Based on the extant studies of Kumar and Firoz (2019) and Kumari et al. (2022), the current research adopts CMIE industry classification codes to classify sensitive and non-sensitive firms. The industry-wise results are summarised in Table 5 where panels A and B describe the regression outcome for carbon-sensitive and non-sensitive companies, respectively. Though sub-sample results indicate a positive effect of ESG reporting, Tobin’s Q ratio of carbon-sensitive firms has a low beta value (0.806) as compared to non-sensitive firms (1.165). A similar conclusion can be drawn for the MBV model as well with beta values of 0.495 and 1.959 for carbon-sensitive and non-sensitive companies, respectively. The findings indicate that carbon-non-sensitive companies experience an amplified positive impact of ESG reporting as compared to sensitive firms. The results are congruent with the past research from Matsumura et al. (2014), Choi et al. (2021) and Ghose et al. (2023). This finding can be explained as carbon-sensitive firms face greater exposure to the pollution risk as well as environmental litigations (present as well as future) which may affect their legitimacy. Thus, investors discount the positive effect of ESG reporting for such companies (Choi et al., 2021).

Regression Output: Effect of Carbon Sensitivity.

Div_Pay = Dividend payout ratio; ESG = environmental, social and governance.

Robustness Analysis—Alternate Method and Controlling for Endogeneity

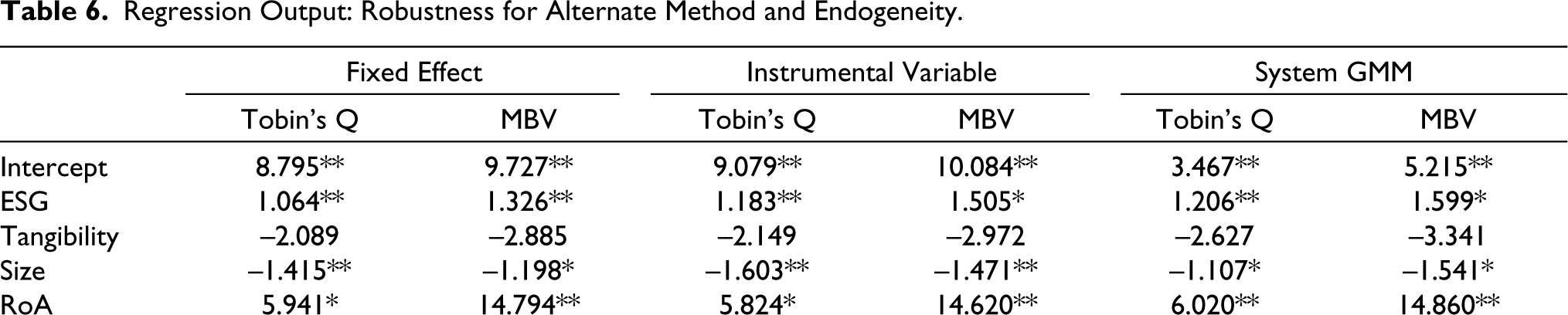

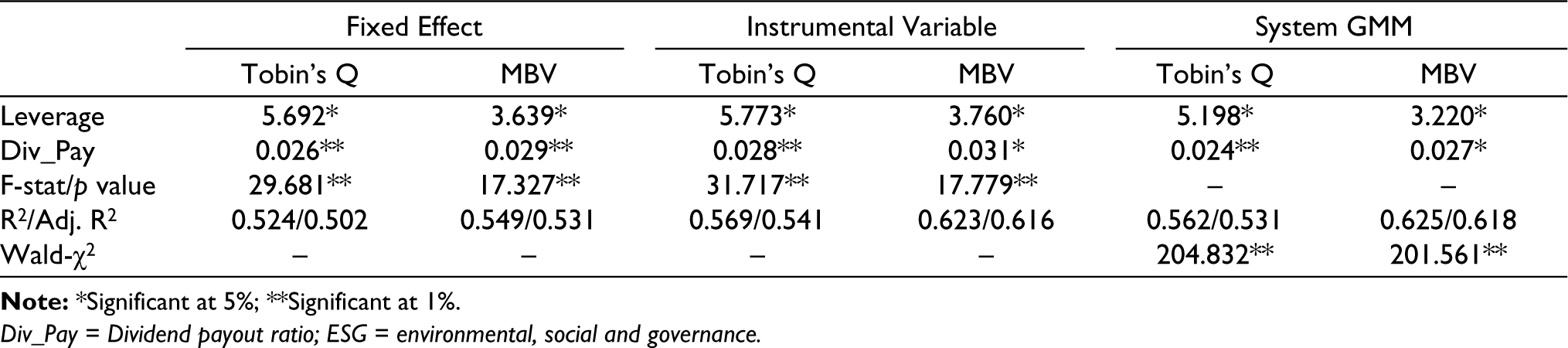

The current research adopts a battery of tests to enhance the robustness of the results and control for unobserved heterogeneity, omitted variable bias and potential endogeneity which commonly occurs in corporate finance studies (Alsaifi et al., 2020; Saiedi et al., 2015). Endogeneity issues may arise as the firms with higher value can have higher ESG scores as they are more noticeable among the investors. Such ability of the dependent variable to predict independent variable has been termed as ‘reverse causality’ which requires to be controlled. Thus, besides pooled OLS method, the present research conducts a fixed-effect regression model (to control for cross-sectional firm effects), instrumental variable and system generalised method of moments (GMM) (Arellano & Bond, 1991) (to control for potential endogeneity) and the results are portrayed in Table 6. Congruent with the OLS model, the results indicate a significant positive impact of ESG reporting on both measures of the market value. Conclusively, the findings of alternate estimation methods are congruent to the earlier results and the conclusions are analogue.

Regression Output: Robustness for Alternate Method and Endogeneity.

Div_Pay = Dividend payout ratio; ESG = environmental, social and governance.

Conclusion and Limitations

As per SEBI guidelines, Indian companies are mandatorily required to file ESG reports along with annual financial statements from the financial year 2022–2023. A novel framework of BRSR has been proposed by SEBI as an ESG report which motivates the current study. The present research aims to examine the effect of ESG disclosure on firm value of Indian firms. Tobin’s Q and MBV ratio has been used to measure firm value, whereas ESG disclosure has been measured by indicator variables. Considering the sample of 940 listed companies, the current study adopts a cross-sectional regression approach to analyse the hypothesised relationship. The results of data analysis reveal a significant positive effect of ESG disclosure on both indicators of firm value. Further, the study also performs regression analysis for sub-sample firms by classifying firms as per industry to examine the moderating role of carbon sensitivity. The results indicate that the positive effect of ESG on firm value is magnified for carbon-non-sensitive firms as compared to firms operating in sensitive industries such as coal, power, energy, etc. The findings of the current study will provide several implications for policymakers and managers. As the study elucidates a positive association between ESG and firm value, policymakers can promote the adoption of ESG reporting among business firms to promote transparency. Further, managers can use ESG performance and disclosure to enhance stakeholder confidence and reduce information asymmetry among investors and managers. This can further increase the market value of firms. However, managers of carbon-sensitive firms have to practice ESG reporting more intensively to diminish the environmental effect of their business operations on market capitalisation.

Current research attempts to provide comprehensive evidence for ESG disclosure and firm value in the context of emerging nations. However, a few limitations can be addressed by future research. The current study is based on a cross-sectional approach as the SEBI’s regulation is announced in May 2021 but future research can be conducted using a longitudinal approach. Future research can be conducted on assessing the effect of consolidated ESG score as well as its components (E, S and G) on the firm value. Finally, besides financial factors, governance-related factors such as board size, board independence and CEO duality can be tested on firm value to obtain robust results.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.