Abstract

This article studies the non-linear relation between family ownership and firm performance (FP) in the Indian context by taking firms listed on NSE 500. The sample firms are investigated for 11 years, 2011–2021. The article also tries to study the impact of various categories of external block holders on the performance of Indian family firms due to their capacity to pressure management and monitor their actions. The study results show a U-shaped relation between family ownership and Indian family firms’ performance, as depicted by ROA and TQ. The findings further suggest that two prominent kinds of outside block holders that have been observed to be related to greater performance in family firms are government and foreign institutional shareholders. Thus, it can be assumed that these external block holders’ greater monitoring ability is linked with reduced agency costs and increased FP. The study is unique in finding out the influence of the ownership and governance mechanisms in the sample of Indian family firms on their performance.

Keywords

Introduction

Family firms are distinct since family affairs are interwoven with business affairs in family businesses. A family business system consists of three sub-systems:

(1) the controlling family unit—representing the traditions, history and life cycle of the family; (2) the business entity—representing the strategies and structures utilised to generate wealth; and (3) the individual family member—representing the skills, interests and life stage of the participating family owners/managers. (Habbershon et al., 2003)

The interwoven and bilateral relationship between the business systems and family structures is a unique characteristic distinguishing the research on family firms and making it complex to study.

Even though much work has been done on research in family businesses recently, the question concerning the link between family and firm value continues to be unsettled, especially in emerging economies. Theoretical viewpoints of economics and management are differing and inadequate in describing family firm performance (FP), and the empirical analysis on family firms has provided contradictory results (Miller et al., 2007). The incongruity in family firms makes it complex to understand the family form of business organisations, standardised interactions between business structure and family, and the outcomes of such interactions.

This article examines the influence of ownership by family and outside block holders on the performance of Indian firms listed on the NSE 500 for 11 years (2011–2021). The objectives of this article are: (a) to investigate the non-linear relation between family ownership and the company performance; (b) to analyse the impact of the presence of outside block holders such as government, domestic institutional investors (DIIs) and foreign institutional investors (FIIs) on the listed Indian family firms’ performance.

Literature Review

Bearle and Means (1932) first described this concept of agency theory to illustrate large business organisations with diverse ownership resulting from conflicting interests between the agent and the principal, known as agency problems, emerging in cases where ownership and control are separated. Studies on family firms depict that these agency costs are primarily not an issue as ownership and control are not necessarily separated (Chrisman et al., 2010). Family owners usually take the role of managers and directors in their own family firms (Blanco-Mazagatos et al., 2007; Lubatkin et al., 2007). However, the traditional perspective that greater ownership by the family would lead to low agency costs because there is not much separation between control and ownership is problematic (Fama & Jensen, 1983). This is because the conventional agency theory does not adequately take into account the principal–principal agency costs that arise due to disagreements among majority family and minority owners (Young et al., 2008) and agency costs arising due to conflicts among family managers and non-family managers (Davis et al., 1997; Schulze et al., 2001).

Family ownership gives a family the capacity to impact a firm’s profitability. Family business literature shows that empirical research on how family ownership affects firm profitability in the context of different countries exists, but the majority of research has been undertaken in developed economies, and the knowledge of this relationship in developing countries like India is scarce (Kim & Gao, 2013; Wright et al., 2014). International ownership and control standards may not completely apply to Indian family firms because of the heterogeneity and diversity of Indian firms, including complex holding and ownership structures. Research on the extent of holding and control as factors affecting various performance parameters might offer new insights.

These results in previous empirical studies on developed markets like the USA and Europe exhibit an inverted U-shaped relation between family ownership and FP. But the studies on some emerging markets depict a U-shaped association between these two variables (Filatotchev et al., 2005; Lins, 2003). Better information on the relationship between these two variables in emerging nations like India is essential. In light of the above observation, to understand the non-linear relation, we hypothesise:

H1: The association between family ownership and FP is curvilinear (non-linear) in Indian family firms.

Further, various outside block holders in family firms, such as the government, domestic institutional investors and foreign institutional investors, can impact FP due to their capacity to pressure management to take certain actions (Jara-Bertin et al., 2008). The existence of such block holders might assist in curtailing the enforcement of poor business decisions and reduce moral hazard problems among the majority family owners and other minority shareholders, thereby improving firm value (Chen et al., 2022; Russino et al., 2019). The influence of the presence of these block holders on the performance of Indian family firms is explored in this study to understand whether they are acting as efficient invigilators of the company.

The purpose of hypotheses H2a, H2b and H2c is to explore whether the ownership of large external shareholders in the family firms impact Indian family firms’ financial performance. These large outside shareholders might have the ability and incentive to influence the firm’s management to make decisions in the company’s interests rather than enabling the owner–managers to pursue their personal gains. The three large outside shareholders whose impact on family FP are investigated in the study are the government, FIIs and DIIs. The hypotheses for the same are as follows:

H2a: DII shareholding in family firms is positively/negatively associated with their performance. H2b: FII shareholding in family firms is positively/negatively related to their performance. H2c: Government shareholding in family firms positively/negatively impacts their performance.

Data and Methodology

Sample Selection

The study has been conducted on public family firms in India. The sample for this study consists of companies listed on the NSE 500 Index as of 31 March 2021, for 11 years (2011–2021). Finally, the sample size is 301 firms, after excluding the financial & banking companies, government companies and firms with missing data, accounting for 3,311 firm-year observations. In the absence of any definite source of family firms in India, listed companies obtained from the NSE 500 have to be segregated into family and non-family companies based on the definition adopted in the study. In our sample, family firms constitute approximately 62% (186 firms) of the NIC codes, suggesting they are quite prevalent in India.

Definition of a Family Firm for the Study

This article takes the description given by Gupta and Nashier (2017) and Anderson and Reeb (2003) in their research on family firms. In India, the legal framework requires the listed firms to reveal their ownership structure every quarter. The Companies Act 2013 describes a promoter as an individual who has been denominated as such in the company’s prospectus or who oversees the company’s affairs either directly or indirectly. In India, family firms are promoted by Hindu Undivided Family (HUF), individuals, trusts and Indian body corporates. Indian law identifies a HUF as a legal body established by the members of a Sikh, Jain, Buddhist or Hindu family. HUF, as a separate legal entity and organisational structure, is extensively used by family firms in India to administer control over their businesses and is typical to India. Additional widely used modes to administer control over their firms are through shareholding in trusts and corporate bodies. Therefore, family businesses in India are usually a mixture of HUFs, individuals, trusts and corporate bodies.

Thus, we recognise a family firm to be one that is promoted by the HUF, individuals, trusts and corporate bodies belonging to the controlling family with at least 10% ownership of the family. For this study, a family firm is classified as the one in which at least 10% of the company’s outstanding shares are held by family, and at least one family member acts as a director on the board of the firm.

Research Variables

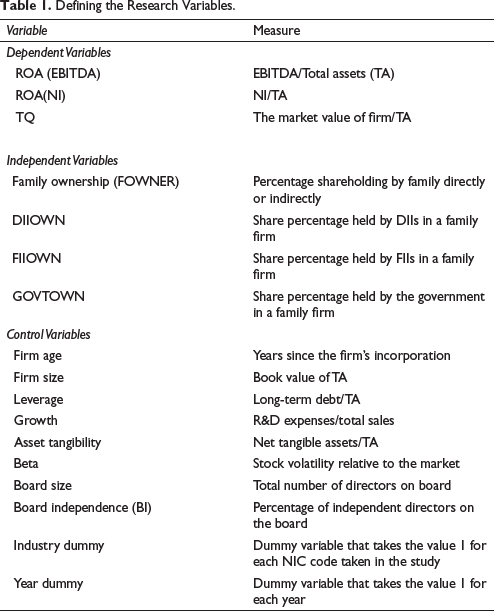

Studies on family businesses have pointed out that the accounting performance measure is return on assets (ROA), given by both net income (NI) and earnings before interest tax and depreciation (EBITDA). Tobin’s Q (TQ) is the market performance measure. Similar studies have applied these measures, for example, Andres (2008), Khanna and Palepu (2000), etc. The independent variables to study the models used in the article are family ownership (FOWNER), domestic institutional investors ownership (DIIOWN), foreign institutional investors ownership (FIIOWN), government ownership (GOVTOWN) and have been defined below in Table 1.

Defining the Research Variables.

The study introduces control variables drawn through a review of prior studies on the family business. These control variables will help to solve the problem of bias that might be caused due to omitted variables and endogeneity and are a part of the regression equation along with the independent variables. The control variables as derived from the literature (Anderson & Reeb, 2003; Gill & Kaur, 2016; Gupta & Nashier, 2017; Villalonga & Amit, 2006), are mentioned in Table 1.

Analysis

Descriptive Statistics

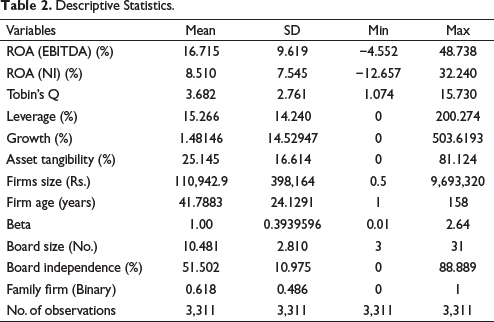

Descriptive statistics helps in getting a snapshot of the features of each dependent and independent variable. Table 2 gives descriptive statistics of the total sample of firms, presenting the mean, SD, min, and max values based on annual observations for variables of study. Table 2 indicates that the mean ROA based on EBITDA (NI) in the sample firm is 16.72% (8.51%). The mean value of TQ, which shows marked performance is 3.68.

Descriptive Statistics.

The mean age in the sample companies is approximately 42 years. The companies’ size varied from ₹ 0.5 million to ₹ 9,693,320 million in the 11 years taken for the study. The leverage value of an average company is 15.27%, and it ranges from 0 to as high as approximately 200%. The mean firm had a tangibility of 25%. An average firm has a beta value of 1, indicating that its security price tends to move with the market. The mean board size in the sample is 10 members, with independent directors being approximately 52% of the total directors.

Data Analysis

Panel data analysis is carried out to investigate the hypotheses of the study. The Hausman test is conducted to determine whether to use fixed or random effects. Fixed effects is accepted on the basis of the test. Variance inflation factor checks for multicollinearity among variables. All VIF values are less than 10 in our sample, suggesting no multicollinearity. In addition, we used the Huber White Sandwich Estimator (clustered) for variance to control for heteroscedasticity and serial correlation.

Non-linear Relationship Between FOWNER and FP

The link between FOWNER and FP is anticipated to be non-linear, as mentioned earlier in Hypothesis 1. In model 1, the family ownership square variable is introduced into the regression equation to explore the possible curvilinear relation between FOWNER and firm financial performance to test H1. Thus, the following regression model equation is developed to test H1:

Model 1—Equation (1):

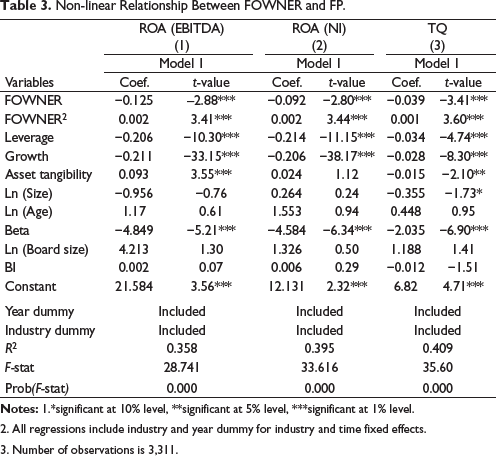

Table 3 depicts a non-linear relation between FOWNER and Indian family FP. It is observed that at low levels of family ownership ROA (EBITDA) decreases. Although, as family ownership becomes more concentrated, ROA(EBITDA) also rises. The positive and significant coefficient of FOWNER2 as given in part (1) (β = 0.002; p < .01) indicates that U-shaped relation exists between FOWNER and ROA (EBITDA) with R2 value of 0.358 and F-stat value of 28.74 (p = .000. The regression results for ROA based on NI are also similar, as given by column 2 of Table 3, suggesting that a U-shaped relationship exists between FOWNER and ROA (NI). The inflection point for the quadratic relationship is given by – β1/2 β2. The point where the gains connected to family ownership start to set in is at 23% using ROA(NI) as a performance measure.

Non-linear Relationship Between FOWNER and FP.

2. All regressions include industry and year dummy for industry and time fixed effects.

3. Number of observations is 3,311.

Part (3) shows the regression results using TQ as the response variable, which also depicts that Tobin’s Q declines at low levels of family ownership. Although, the positive and significant coefficient of FOWNER2 (β = 0.001; p < .01) indicates that TQ increases as the ownership of family members becomes concentrated in the firm, with an R2 value of 0.409 and F-stat value of 35.60 (p = .000). This signifies that at the higher ownership levels, family owners’ interests align with other shareholders. Therefore, as family ownership becomes concentrated, there appears to be a convergence of family owners’ and other shareholders’ interests. Thus, as family ownership increases in a firm and becomes concentrated, its value also rises. The inflection point is 19.5% using Tobin’s Q.

The inflection point using ROA and TQ as performance measures are quite close, consistently asserting FOWNER and FP have a non-linear relationship. These results are in contrast to those obtained in the case of the majority of developed countries, which show an inverted U-shaped relation between FOWNER and FP, indicating in these developed economies FP rises with the rise in family ownership up to a certain level beyond which performance begins to decline (Anderson & Reeb, 2003). Overall, the analysis indicates that FOWNER and FP does not have a uniform linear relation over the complete range of family shareholding; FP decreases with an increase in FOWNER up to a certain level as given by the inflection point ranging from 20% to 23%. Beyond this level, FP starts increasing with an increase in family ownership.

Impact of Other Large Block Holders Shareholding on Family FP

The purpose of hypotheses H2a, H2b and H2c is to investigate whether the ownership level of external shareholders in the family firms impacts the Indian family firms’ financial performance. These large outside shareholders might have the motive and ability to influence the firm’s management to avoid managerial entrenchment and focus on the company’s best interests. The three large outside shareholders that are investigated in the study are DIIs, FIIs and the Government. The specification model equation used to study the ownership of large external shareholders and its impacts on the performance of family firms in India to test hypotheses H2a to H2c is given below:

Model 2—Equation (2):

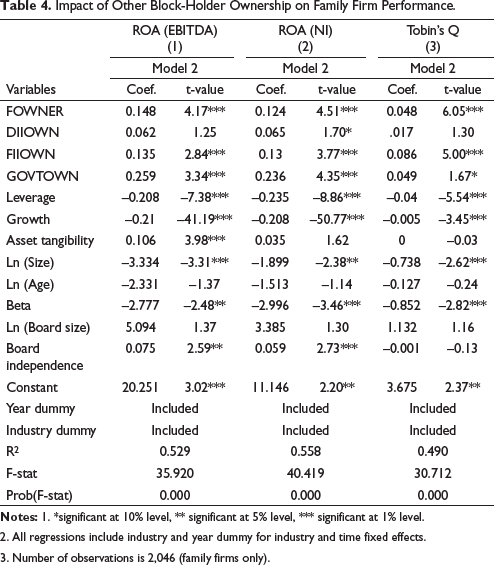

Table 4 investigates hypotheses H2a, H2b and H2c to understand whether the ownership level of large outside shareholders, namely, DIIs, FIIs and government ownership in the family-owned firms, influence the Indian family firms’ performance. In Model 2, DIIs’ shareholding in family firms (DIIOWN), FIIs’ shareholding in family firms (FIIOWN) and any shareholding by the central or the state government (GOVTOWN) are added as independent variables to examine their potential influence on family-owned firms’ performance in India.

Impact of Other Block-Holder Ownership on Family Firm Performance.

2. All regressions include industry and year dummy for industry and time fixed effects.

3. Number of observations is 2,046 (family firms only).

Column (1) in Table 4 shows regression results of the family firms’ performance based on ROA (EBITDA) on these three types of other large block holders using the fixed effects model. The findings show that FIIOWN (β = 0.135; p < .01) and GOVTOWN (β = 0.259; p < .01) have a significant and positive coefficient, implying that the existence of FIIs and government shareholders improves family FP. DIIs also lead to positive ROA(EBITDA), but the coefficient is not significant. The R2 value of the regression equation is 0.529, with the F-stat value of 35.920 (p = .000).

Column (2) of Table 4 depicts the findings using ROA(NI) as the response variable. The results depict that all three types of block holders have a significant and positive coefficient, DIIOWN (β = 0.065; p < .10), FIIOWN (β = 0.130; p < .01) and GOVTOWN (β = 0.236; p < .01), indicating that the presence of domestic as well as foreign institutional investors as well as government shareholders leads to positive ROA(NI). The R2 value of the regression equation is 0.558, with an F-stat value of 40.419 (p = .000).

Column (3) of Table 4 presents panel data regression results using market measure, TQ as the dependent variable. The findings depict that FIIOWN (β = 0.086; p < .01) and GOVTOWN (β = 0.049; p < .10) have a significant and positive coefficient, implying that the existence of FIIs and government shareholders in family firms lead to improved FP. The presence of domestic institutional investors also leads to positive ROA(EBITDA), but the coefficient is not significant. The R2 value of the regression equation is 0.490, with the F-stat value of 30.712 (p = .000).

The overall results indicate that the link between FIIs’ ownership in family firms and their accounting and market performance is significantly positive. This might suggest that collectively, foreign fund managers might create a significant force and are thus able to pressure and influence family owners and managers to enhance corporate governance and improve transparency in all the dealings of the firm. Thus, it can be concluded that these FIIs’ greater monitoring ability is linked with reduced agency costs and, therefore, higher ROA. Also, FIIOWN and TQ have a significant and positive relationship, implying that FIIs are careful in selecting firms with high TQ as they are concerned about their market return. The findings for the relation between DIIOWN and FP are positive but not significant for ROA (EBITDA) and TQ, implying that monitoring and influence of domestic institutional investors are not able to translate into notable enhancement in family firms’ performance in which they invested. Thus, it could be said that DIIs activism is neither beneficial nor harmful to family firms’ economic performance.

Further, the findings depict that GOVTOWN is significantly and positively related to the ROA and TQ, indicating that government ownership in family-owned firms enhances FP. The relation between the family and government could be beneficial for both, improving one another’s strengths and balancing for one another’s weaknesses. From the resource-based theory perspective, family firms that have government ownership have greater access to the government’s resources. Such association also aids in removing the incompetence often linked with the government-run companies.

Conclusion

The empirical research analysis confirms a U-Shaped relation between FOWNER and FP in terms of ROA and TQ. Family ownership is related negatively to the performance of a firm up to a certain level, as given by the inflection point ranging 20% to 23%. Subsequent to this, a further rise in family ownership is associated with an increase in family FP. These results are opposite to those obtained in previous empirical studies on developed markets like USA and Europe, which exhibit an inverted U-shaped relationship but are agreeable with the studies on emerging markets.

This signifies that at the higher ownership levels, family owners’ interests align with other shareholders. Therefore, as family ownership becomes concentrated, there appears to be a convergence of family owners’ and other shareholders’ interests. Thus, as family ownership increases in a firm and becomes concentrated, its value also rises. These results augment the extant viewpoint that markets in emerging economies have relatively weaker regulatory systems, which cannot check minority shareholders’ expropriation at the hands of the majority family owners who might want personal gains. But as family ownership becomes more and more concentrated, these family owners might realise that an increase in FP benefits them more. Hence, there might be no or lesser extraction of personal gains leading to higher FP at higher levels of family ownership.

The block holders are divided into three parts based on their identity so as to explore the effect of each category of large outside shareholders on FP. The outcome indicates that the link between FIIs’ ownership in a family firm and its performance is significantly positive. FIIOWN and TQ are significantly and positively related, implying that FIIs are careful in selecting firms with high TQ as they are concerned about their market return. In addition, the results also suggest that collectively, foreign fund managers might create a significant force and are thus able to pressure and influence family owners and managers to enhance corporate governance and improve transparency in all the dealings of the firm. Thus, it can be assumed that these foreign investors’ greater monitoring ability is linked with reduced agency costs and, therefore, higher ROA (EBITDA and NI).

The results for the link between DIIOWN and firm FP are positive but not significant for ROA (EBITDA) and TQ, implying that monitoring and influence of domestic institutional investors are not able to translate into notable enhancement in family firms’ performance in which they made an investment. Thus, it could be said that DIIs activism is neither beneficial nor harmful to family firms’ economic performance, as implied by the study’s empirical findings.

Further, the findings depict that GOVTOWN is significantly and positively related to both the ROA (based on EBITDA and NI) and TQ, implying that government ownership in family-owned firms enhances FP. Government ownership in family firms might suggest that the government is sincere regarding investment in family firms that are recognised to be more dedicated in the management of their business compared to the professional management of the government companies. The association between the family and government could be beneficial for both, improving one another’s strengths and balancing for one another’s weaknesses. From the resource-based theory perspective, family firms that have government ownership have greater access to the resources of the government, and such association also aids in removing the incompetence often linked with government-run companies.

Implications of the Study

This study can also help in drawing some implications for policymakers. The results indicate that corporate governance issues in emerging countries like India might necessitate solutions other than those given by the traditional agency theory context that disregards institutional distinctness. Adopting policies that are designed for developed economies might not be practical and efficient for developing nations. The outcome shows that a non-linear U-shaped relation exists between FOWNER and FP. These results add to the existing viewpoint that emerging markets like India have comparatively weaker regulatory structures that cannot check management entrenchment and expropriation of minority shareholders by the controlling family members (Gedajlovic et al., 2012). But as the family ownership in a firm rises, there is a convergence of family owners’ and other shareholders’ interests, generating improved FP.

The article depicts that the existence of non-family block holders like FIIs and government shareholders positively impacts FP. This is due to the fact that these large outside shareholders have the capacity and incentive to restrain family owners from withdrawing company resources for their personal gains, thus playing a crucial role in monitoring family owners. Although, the monitoring benefits of non-family large shareholders might be lost as the ownership of family members become more and more concentrated. Prior research states that family businesses evolve in accordance with society and the growth of the economy (Carillo et al., 2015). In emerging countries like India, pyramid structures are prevalent, the regulatory market is not fully developed, and the protection of shareholders is weak.

Thus, given the social and institutional settings in emerging countries, family business owners are more inclined towards nepotism than having entrepreneurial zeal among all generations and towards exploitation of minority shareholders. In such situations, the void in the regulatory system can be filled through optimal holding by non-family shareholders, thus monitoring the family owners and protecting minority shareholders. Developing economies require strict regulations and disclosure measures to check the exploitation of a company’s wealth by family business owners. A capital and regulatory market that is developed together with a steady institutional structure can extract the complete potential of family firms that form a large part of many developing countries like India. The governance and performance of family firms and the impact of family control can be examined more exhaustively if policymakers and regulators precisely define a family business and enforce relevant disclosure norms for them.

The current study examines the effect of the differences in the level of ownership concentration on FP. However, this study does not take into account psychological and social factors such as social and emotional ties, social networks, demographics, collective family commitment, education, and others, which can be significant for understanding the role of the family on FP through effective board and management. Such factors might influence the association between non-family and family members, the relation among members of the family, and the interaction between the business and the family as they can be important in driving stewardship behaviours which can be crucial for performance differences among family firms and also between family and non-family firms (Eddleston & Kellermanns, 2007). Thus, future research may explore these factors as well to have a more holistic view of how family influences FP.

Footnotes

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author received no financial support for the research, authorship and/or publication of this article.