Abstract

Global sustainability challenges have triggered a sense of accountability in society, culminating in the growing incorporation of sustainability into corporate operations. This article aims to investigate the influence of environmental, social and governance (ESG) disclosure on a company’s cost of financing in emerging markets. Furthermore, the article examines the criticality of separate pillars of ESG in determining the companies’ capital costs using a panel dataset of 192 non-financial companies drawn from the equity indices from the BRICS countries for 10 years, spanning 2011–2020. Pooled Ordinary Least Square and fixed-effect panel regressions are used to test the hypothesised relationships. The robustness of our findings is validated by the application of the System Generalised Methods of Moments approach. The results show that ESG disclosure scores and their individual component scores are positively associated with the cost of equity and weighted average cost of capital. In contrast, there is a negative relationship with the cost of debt. Results demonstrate the apprehensions of equity providers and the reception of debt providers towards the companies’ ESG adoption. The governance pillar has the most significant influence on capital costs. The study enables managers to evaluate the economically ideal capital structure for ESG-compliant enterprises strategically.

Introduction

Global climate change and rising human vulnerability have pushed sustainability to the forefront of the international agenda. The continuous rise in environmental and social challenges underscores the urgent need to change firms’ attitudes towards sustainability issues. The outcome of a firm’s negative externalities in the form of increased human vulnerabilities demands that businesses should progressively integrate sustainability into their policies and operations (Michaelis, 2003). Corporations are under growing scrutiny to publish comprehensive information about their initiatives to mitigate the adverse effects of their businesses on the environment and society (Bansal, 2002). Lately, there has been an abrupt transition in the company’s orientation from the narrow objective of financial profitability to the broader picture of sustaining in this dynamic environment (Schulte & Hallstedt, 2018). Increasing numbers of companies are committing to environmental, social and governance (ESG) principles to address these critical global issues and evolve with the changing business landscape (Wong et al., 2021). The ‘business rationale’ for corporate social responsibility (CSR), which prioritises sustainability, is cited as the driving force behind the transition from CSR to ESG. This transition represents a shift from morally driven societal obligations in CSR towards a risk management viewpoint within ESG, encompassing aspects that involve potential litigation and regulatory issues (Pollman, 2019). Several international initiatives have also fostered the notion of sustainability, such as the United Nations General Assembly’s endorsement of the sustainable development goals (SDGs) and the Paris Agreement to manage global temperature by cutting the emission of greenhouse gases.

Therefore, moving beyond conventional financial metrics, ESG has become an important criterion investors and analysts use to evaluate a company’s performance (Kiron et al., 2013; Schramade, 2016). Decision-makers are using ESG as a tool to monitor the degree of alignment of the company’s activities with their stated objective to achieve long-term sustainability (In et al., 2019). Although adopting and demonstrating sustainable business practices have some extra costs attached (Butler et al., 2011), these sustainable initiatives have also endowed many organisations with competitive leverage (LEV) (Esty & Winston, 2009).

A report released by the United Nations Global Compact 2004 discussed integrating ESG factors into investment decision-making as a new investment strategy (UNEP, 2004). Simply put, ESG investing is the holistic approach to investment decision-making wherein due diligence is paid to various ESG factors while determining the return and the risk associated with the firms. Previous studies have proved that ESG compliance has aided corporates not only in serving society ethically but also in enhancing their financial performance through the combination of greater returns and reduced risks (Aboud & Diab, 2019; Cerqueti et al., 2021; Chelawat & Trivedi, 2016; Kim & Li, 2021). ESG risk is one of the primary sources of overall risk enterprises face. Companies must anticipate the ESG risks likely to impact their business to curb the ramifications of forfeiting stakeholders’ confidence. ESG data has become a relevant source of information for financial market analysts (Leins, 2020) to build optimal and efficient portfolios. Investors’ rising adoption of ESG data is driven by its economic usefulness rather than ethical concerns (Amel-Zadeh & Serafeim, 2018).

The present research expands on the existing literature on ESG, especially concerning the setting of emerging markets. Previous research in this domain has catered mainly to developed markets; however, companies operating in emerging markets are equally vulnerable to ESG risks, if not more. This study is motivated by a lack of sufficient evidence from existing research that establishes a clear link between an ESG disclosure score (ESGS) and the companies’ capital financing costs in emerging markets. This study seeks to fill this research vacuum by investigating the influence of ESG disclosure on weighted average cost of capital (WACC), cost of equity (COE) and cost of debt (COD) in the fastest-growing BRICS economies. Together, the five nations account for around one-quarter of the global GDP and 42% of the global population (BRICS Investment Report, 2023). As the significance of BRICS nations grows in the global economy, it becomes imperative to scrutinise the impact of growing consciousness of sustainability in the business landscape and its repercussions on the capital costs of companies operating within these nations. This holds particular significance considering the relatively limited body of research addressing the collective dynamics of the BRICS consortium (Fandella et al., 2023). Therefore, this study examined a dataset of 192 non-financial companies derived from the primary equity indices of BRICS nations from 2011 to 2020. Furthermore, as the optimal capital structure of a company depends on attaining an ideal balance between equity and debt (Myers, 2001), it is imperative to thoroughly investigate the distinct impact of ESG ratings on both the COE and debt for the firm, aiming to ascertain its optimal capital structure. Consequently, our research introduces a comparative analysis delineating the responses of lenders and investors to ESG compliance within firms operating in emerging markets. The study seeks to precisely identify the ESG pillar that exerts the most significant impact on a firm’s financing costs by comparing the influence of various ESG pillars on COE, COD and WACC of the firms. The resultant insights hold financial implications for financial market players, policymakers and capital providers. These findings hold specific importance for managerial decision-making, facilitating the determination of an optimal capital structure for the firm. This involves a consideration of the impact of ESG compliance on the costs associated with each financing component, ultimately guiding the selection of the most economically efficient financing sources.

The article is organised into five sections. The second section reviews the existing literature and develops hypotheses based on our research objectives. The third section lays down the data sources and research methodologies employed. After discussing the results in the fourth section, section five concludes our research.

Literature Review and Hypotheses Development

Over the last decade, the ongoing debate about the impact of ESG disclosure on a company’s performance has garnered attention. Several studies have attempted to demonstrate the prominence of ESG (Díaz et al., 2021; Zumente & Bistrova, 2021). ESG investing is often mixed up with socially responsible investing (SRI). SRI is a negative approach that concentrates on weeding out sin stocks when making an investment decision. ESG investing, on the other hand, is a positive term that focusses on businesses that take the initiative to curb the adverse effects of their business activities on society (Alessandrini & Jondeau, 2020). ESG information influences the company’s valuation and performance, making it an effective indicator of financial performance (Giese et al., 2019).

Theoretical Background

Several organisational and management theories support the notion of ESG. Stakeholder theory, introduced by Freeman (1984), rationalises the growing prominence of ESG considerations in the corporate realm. It argues that companies should prioritise the well-being of all stakeholders beyond solely concentrating on shareholders. This approach not only fosters trust among stakeholders but also contributes to enhancing the firm’s reputation. Another theoretical paradigm, legitimacy theory (Deegan, 2002), is intricately linked to stakeholder theory. The need to attain legitimacy from stakeholders as a reciprocal gesture for utilising society resources is emphasised by legitimacy theory. Businesses are expected to operate within the confines and norms established by the community to achieve social legitimacy (Dowling & Pfeffer, 1975) by prioritising societal and environmental considerations beyond purely profit-oriented goals. Hence, adherence to ESG standards constitutes a holistic strategy aimed at securing stakeholder trust and upholding societal legitimacy, thereby facilitating the smooth operation of companies.

Some theories also provide a basis for exploring the potential connection between the growing notion of business sustainability and the financing cost of capital. The fundamental premise of agency theory is that managers and shareholders interact in a principal-agent dynamic, with managers acting as stewards of the firm’s welfare on behalf of shareholders (Jensen & Meckling, 1976). Agents may occasionally misuse their decision-making authority for personal benefit, resulting in agency costs between them and the principals. Likewise, agency costs can emerge when managers excessively allocate resources to ESG compliance efforts, resulting in higher operational expenses negatively impacting profitability (Cerciello et al., 2023), which may not correspond with shareholders’ core interests. As a result, shareholders may demand higher returns on their invested capital to compensate for the risk related to the reduced profitability owing to the company’s ESG activities.

Similarly, according to the trade-off theory, a trade-off relationship exists between sustainability and profitability, as articulated by Friedman (2007). The trade-off stems from the notion that a strong commitment to ESG principles results in substantial compliance expenditures for the firm, which could potentially exert adverse short-term effects on profitability. Thus, the trade-off and agency theories advocate a significant association between ESG issues and company capital costs, particularly the COE, given that shareholders may directly endure the repercussions of increased ESG compliance expenses.

ESG and COE

Previous research yielded contradictory results regarding the influence of ESG compliance on equity costs. While some studies conclude that ESG scores and COE are positively related (Dahiya & Singh, 2021; Nazir et al., 2022; Prasad et al., 2022; Richardson & Welker, 2001; Yeh et al., 2020) supporting the agency and trade-off theory, others report a negative association, demonstrating that a high ESGS results in a reduction in the COE of the companies (Breuer et al., 2018; Cornell, 2021; Dhaliwal et al., 2011; Ng & Rezaee, 2015; Ould Daoud Ellili, 2020; Reverte, 2012).

Richardson and Welker (2001) contend that while financial transparency is beneficial in lowering the COE, social disclosure has a detrimental influence as it raises the COE. Another study conducted in the Chinese capital market by Yeh et al. (2020) reported a positive relationship between the COE and an organisation’s CSR activities, stating that the plausible reason for this association could be the equity markets’ delayed adjustment to changes in CSR. Dahiya and Singh (2021) discovered a positive association between ESG scores and COE among Indian enterprises. Similarly, another Indian study by Prasad et al. (2022) found that enhanced social disclosure scores (SSs) increase the COE. Investors regard CSR spending and reporting as liabilities rather than assets.

On the contrary, several studies demonstrate that increased emphasis on ESG investment yields social benefits. Investors are now prioritising firms with high ESG ratings, leading to reduced COE (Cornell, 2021). El Ghoul et al. (2011) contend that increased investment in diversified CSR activities considerably reduces the company’s COE, especially when complemented with a high level of investor protection (Breuer et al., 2018). Ng and Rezaee’s (2015) study suggests that environmental and governance performance can potentially reduce COE. However, social performance has an insignificant effect on capital costs. Evdokimova and Kuzubov (2021) researched the BRICS nations and reported that non-financial reporting by a firm significantly reduced its COE. Upon reviewing the existing literature, it becomes evident that there is a lack of a definitive direction regarding the association between ESG and COE. This observation serves as the basis for formulating our initial set of hypotheses, as detailed below:

ESG and COD

Previous research on the relationship between ESG and COD (Carey et al., 2021; Eliwa et al., 2021; Raimo et al., 2021; Yeh et al., 2020) clearly demonstrates that ESG can effectively lower firm COD. Lending institutions are now increasingly integrating ESG information in their credit decisions by giving considerable attention to companies’ ESG performance and disclosure (Eliwa et al., 2021).

Francis et al. (2005) discovered that as firms’ disclosure policies become more comprehensive, their debt costs drop. Similarly, Bhuiyan and Nguyen (2019) suggest that the COD of the businesses decreases as their non-financial reporting increases. According to Yeh et al. (2020), the effective reduction in Chinese firms’ debt costs is mainly attributable to their improved CSR performance. Companies that adhere to SDGs and obligations can thus influence their creditors and control the COD financing (Yeh et al., 2020). Besides private information, sustainability assurance serves as an essential source of information for lenders, making debt financing more accessible to firms at a lower cost (Carey et al., 2021). Evdokimova and Kuzubov (2021) discovered a negative association between non-financial reporting and debt costs in BRICS countries. As a result, the proposed relationship of ESGS and its pillars with debt costs can be postulated as follows:

ESG and Cost of Capital

The results of previous studies testing the relationship between ESG and WACC have shown divergent views, making it difficult to draw any conclusion (Gholami et al., 2023; Kazemi & Rahmani, 2013; Kling et al., 2021; Nazir et al., 2022; Ould Daoud Ellili, 2020; Ramirez et al., 2022; Wong et al., 2021).

Nazir et al. (2022) asserted that investors perceive ESG costs not as value-additive but as an unnecessary burden on the company’s finances, resulting in an increased WACC. The study found that this association varies across sectors. Further, Kling et al. (2021) found that companies face a high cost of financing if they operate in climate-vulnerable countries.

Evdokimova and Kuzubov (2021) and Ould Daoud Ellili (2020) confirmed that companies adhering to ESG dimensions and disclosing ESG compliances exhibit improved transparency, leading to a lower WACC. Improvements in ESG compliance disclosure also help to reduce information asymmetry, which leads to lower risk for investors and a lower cost of capital (Kazemi & Rahmani, 2013). The governance score exhibits a significant adverse relationship with WACC, whereas the environmental and social pillars do not Ramirez et al. (2022).

Nonetheless, Johnson (2020) found no statistically significant relationship between ESG and WACC. According to the literature review, more research in this domain is needed to draw a conclusion. Thus, we propose our third set of hypotheses as follows:

Data and Research Methodology

Sample Selection and Construction of Variables

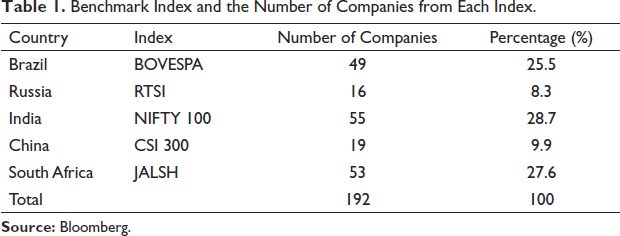

We focussed our research on emerging economies because the idea of ESG is still in its infancy in these countries, leaving this area of study largely untapped. As a result, analysing the nature and impact of ESG compliance on firms in emerging markets to provide investors and researchers with a better understanding of the problem becomes critical. Although several studies have scrutinised the relationship between ESG scores and financing costs in individual countries of the BRICS group, only a few have examined this relationship across the entire BRICS group. Therefore, our investigation focussed on the entire BRICS alliance, which encompasses the world’s five most prominent emerging markets. The data about ESG scores and other financial measures has been sourced from the Bloomberg database. The sample was drawn from the equity benchmark indices of each emerging market in the BRICS. Table 1 displays the index and the corresponding number of companies in each country.

Benchmark Index and the Number of Companies from Each Index.

We primarily chose firms in our sample that had consistently obtained ESG scores from 2011 to 2020, resulting in a limited sample as ESG is still burgeoning. Financial firms are omitted from our sample as the nature of their activities differs from those of other corporations, having a comparatively lesser impact on the environmental pillar of ESG. Furthermore, they are subject to different rules and regulations than non-financial enterprises. The Global Industrial Classification Standard was used to identify the sectors. The selection process yielded a preliminary sample of 557 non-financial enterprises from all five BRICS equity indexes. Nonetheless, due to insufficient ESG scores and financial data, several organisations were eventually excluded from the sample. As a result, we obtained a final dataset of 192 entities, yielding 1920 firm-year observations for our research.

Dependent Variable

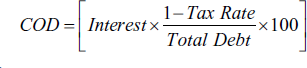

The primary dependent variable in our research is the WACC. The WACC is used to accurately measure a firm’s potential cost of financing from multiple funding avenues. It considers the COD and equity to determine a company’s present value for its capital providers and is critical in capital budgeting decisions. To better understand the relationship between ESG scores and WACC, we divided it into equity and debt costs and investigated their relationship with ESG scores separately. The COE is the minimum return investors require for assuming the risk of investing in a company’s stock. It predicts a company’s stock price by discounting its projected cash flows (Raimo et al., 2020). The company’s equity cost increases with the increase in investors’ required return. The COD represents the interest rate a company bears on funds borrowed from banks, financial institutions, private institutions and the bond market (Bartkoski et al., 2017). All three dependent variables’ data are extracted from the Bloomberg database. Bloomberg’s methodology for calculating the capital costs is described below:

Independent Variable

Our study’s primary independent variable is ESGSs. We expanded our research to gain a better understanding of the connection between different ESG pillars and capital costs by including ES, SSs and GSs as independent variables.

Data for the ESGSs and their pillars are sourced from the Bloomberg database. With the surging consciousness of sustainability, several organisations have created a database for ESG ratings. They evaluate companies’ performance across multiple dimensions and assign ratings/scores to them. Bloomberg covers the ESG data in extensive detail and offers ESGSs for more than 13,000 firms spread over 100 nations (Bloomberg, 2022). The scores are further categorised into three distinct pillars, namely the ESG pillars. Data for the ratings is obtained from an array of sources, including the company’s website, CSR reports, regulatory filings and corporate presentations. All information must be present to avoid a reduction in their disclosure scores. The criteria for assigning scores vary among the different sectors because they are tailored according to the requirements of a particular industry. The concept of ESG in BRICS countries is progressively gaining traction, as witnessed by the growth trajectory of mean ESG scores among the BRICS countries over the last decade. From 2011 to 2020, each BRICS member’s mean ESG disclosure ratings have improved steadily. Russia has made the most progress among the five nations regarding average ESG scores.

Control Variables

This study employs a variety of firm-level control variables identified through a review of the existing literature. The data for these variables is obtained from Bloomberg. Control variables limit the impact of potential confounding and other extraneous variables on the hypothesised relationship between dependent and independent variables (Schjoedt & Bird, 2014). They improve the precision of our estimates and minimise any bias stemming from the influence of other variables.

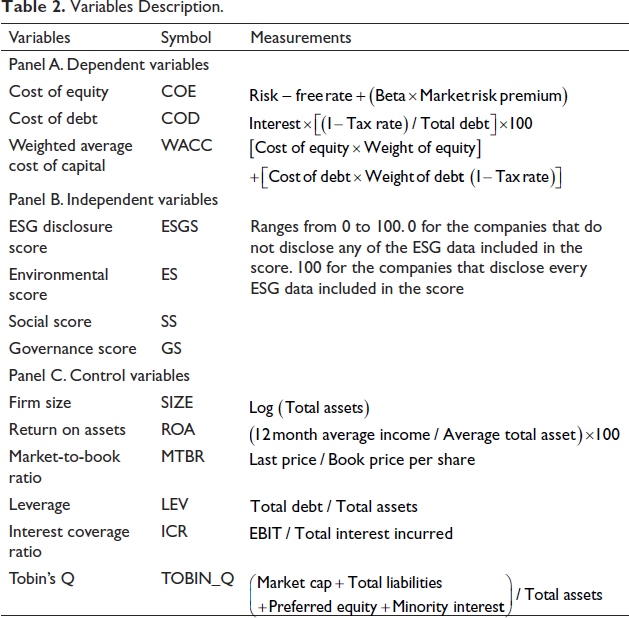

Variables Description.

Return on assets (ROA) serves as the essential variable to control a firm’s profitability (Raimo et al., 2021). Highly profitable firms are less prone to default risk, making capital access cheaper. Another control variable, LEV, is the ratio of total debt to total assets (Raimo et al., 2021). Highly leveraged firms exhibit a greater risk of default, affecting their capital financing costs. The natural log of total assets (SIZE) is a proxy for controlling the influence of firm size because larger firms have less information asymmetry, which usually leads to easier capital access (Raimo et al., 2021). The market-to-book ratio reflects a company’s potential for growth (Prasad et al., 2022). A lower ratio suggests that the business is currently undervalued, which raises the potential risk for investors. Finally, the interest coverage ratio, calculated by dividing earnings before interest and tax by the company’s interest expenses, represents how efficiently a company can service its debt obligations (Raimo et al., 2021). Besides that, Tobin’s Q is used to control the effect of firm value on its capital costs. Table 2 explains the measurement of variables in detail.

Empirical Models

This section highlights the empirical models used to test the relationship between our study’s independent and dependent variables. Fixed effect panel regression is applied to examine the proposed relationships. Fixed effects models can accommodate unobserved heterogeneities and yield more precise estimates of the model parameters. The following three estimation models are constructed using the study’s proposed hypotheses:

Model for H1: Our first model, M1, probes the relationship between the ESG score and the firm’s COE, with COE as a dependent and ESGS as an independent variable, in addition to several control variables previously addressed. Moreover, models M1a, M1b and M1c demonstrate a link between the COE and the ESG disclosure scores, respectively.

Model for H2: The second model explores the relationship between COD and the explanatory variables, which include the ESGS, environmental score, social score and governance score.

Model for H3: Our third model investigate the connection between the WACC and ESG and its pillars scores individually.

Empirical Results and Discussion

Descriptive Statistics

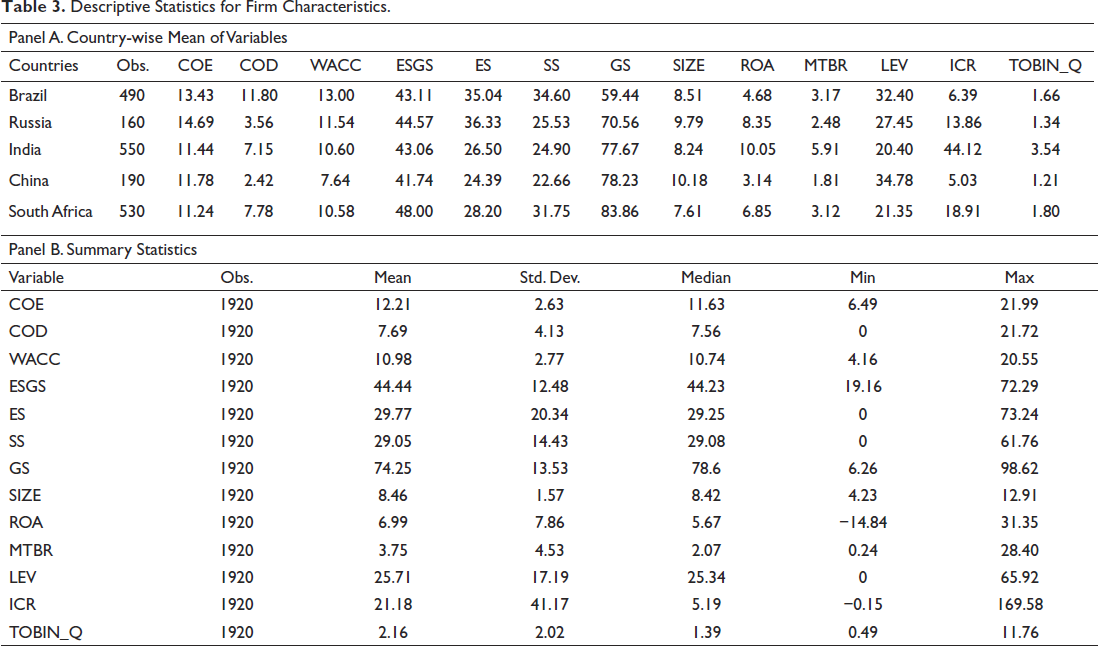

Table 3 displays the descriptive statistics for all variables. Some outliers were discovered in our data, which may have hampered the accuracy of our findings. Therefore, to reduce the influence of these outliers, variables are winsorised at 1%. Panel A presents the mean value for each variable at the level of each country in the BRICS. Panel B portrays the summary statistics of our entire sample.

The average ESG score of BRICS nations is 44.44, ranging from 19.16 to 72.29, revealing that enterprises in emerging markets are not satisfactorily adhering to ESG norms. The minimum environmental and social score is 0, implying that some corporations have entirely disregarded their obligations to the environment and society. The governance pillar has a better average score than the other pillars, indicating that organisations still need to recognise the significance of social and environmental factors completely. COD ranges from 0% to 21.72%, suggesting that some businesses are entirely financed by equity, with the average debt cost being 7.69%. Equity costs average 12.21%, ranging from 6.49% to 21.99%. The mean COE is higher than that of debt, in line with corporate finance theory, which holds that debt is relatively cheaper for firms. Firms’ sizes vary from 4.23 to 12.91 (logged values), and ROA ranges from −14.84% to 31.35%, with a mean of 6.99%. A high standard deviation of ROA indicates that returns vary significantly among firms.

Descriptive Statistics for Firm Characteristics.

Correlation Analysis

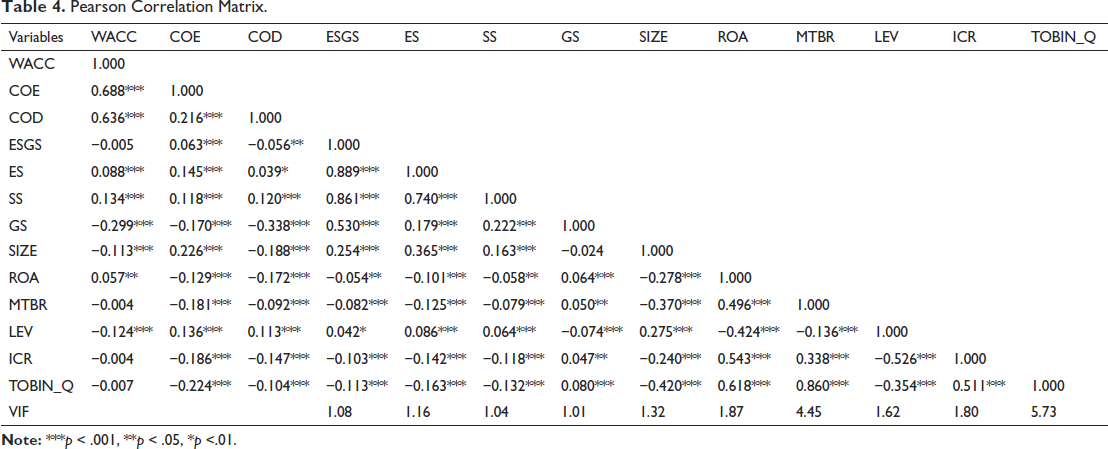

The correlation matrix for each variable is shown in Table 4. ESG scores have a significant negative correlation (Raimo et al., 2021) with the COD but a positive correlation with the COE (Dahiya & Singh, 2021). However, no significant correlation exists between ESG scores and WACC. ROA is significantly inversely correlated to both COE and COD (Yilmaz, 2022), as reduced profitability might increase the risk perception of the capital providers, prompting them to demand high returns for invested capital. The variance inflation factor (VIF) analysis is used to determine how multicollinear the explanatory variables are. A VIF score of less than 10 indicates that the explanatory variables are not significantly multicollinear (Gujarati, 1995; Hair, 2014). Our explanatory variables’ VIF values are below the upper threshold level, demonstrating that multicollinearity does not significantly affect the findings of our study.

Pearson Correlation Matrix.

Regression Results and Discussion

The current section discusses the results of all the regression models based on our study’s stated hypotheses. Pooled Ordinary Least Square (OLS) and panel regression were used to test the hypotheses. The Breusch-Pagan Lagrange Multiplier and Hausman tests were conducted to select the most suitable model for our study. Initially, a Lagrange Multiplier test was used to select the best model from the pooled OLS and random effects models. The null hypothesis in the Lagrange Multiplier test asserts that the error variances are all equal, so the pooled OLS model fits the data (Engle, 1984). However, the alternative hypothesis suggests the random effect model. The p value is below 0.5, inferring that the random effect model is preferable to pooled OLS. Subsequently, the Hausman test is performed to choose between random and fixed-effect models. In our case, a p value of less than .05 indicates that the alternative hypothesis, which suggests the fixed effects model, is accepted.

ESG Disclosure Score and Cost of Capital

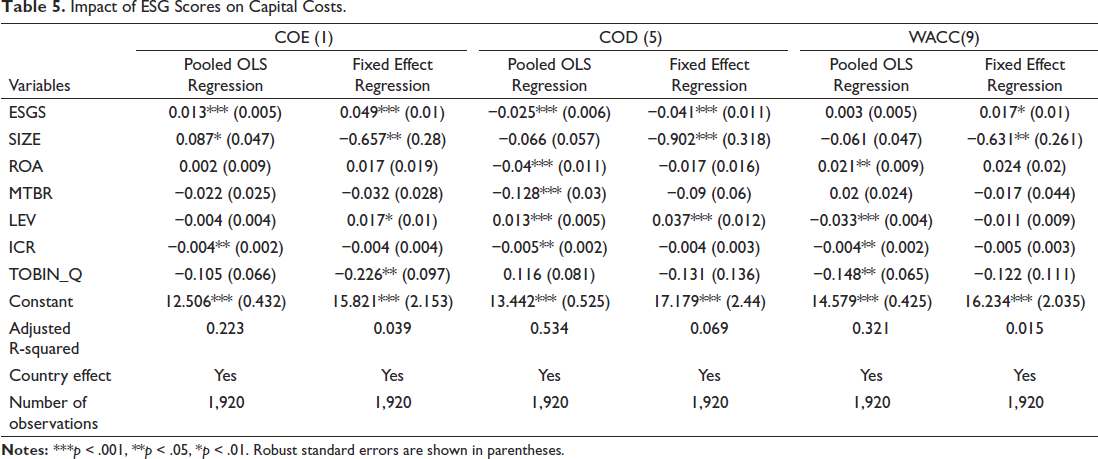

Table 5 exhibits the regression results for our primary models, which aim to determine the degree of linkage between the explanatory variable, ESGSs and the dependent variables, COE, COD and WACC. Fixed effect regression result for Model 1 shows a significant and positive association (β = 0.049, p < .01) between ESG scores and COE, implying that improved ESG disclosure raises a company’s equity cost. Our results are congruous with previous studies by Atan et al. (2018), Dahiya and Singh (2021), Nazir et al. (2022), Prasad et al. (2022), Richardson and Welker (2001) and Yeh et al. (2020). In China, Yeh et al. (2020) discovered a positive relationship between CSR (a precursor to ESG) and COE. Similarly, Dahiya and Singh (2021), in the Indian market, explored the linkage between CSR and COE using all the pillars of the ESG score and found a strong positive relationship between them.

Impact of ESG Scores on Capital Costs.

Fixed effect regressions for Model 2 show a significantly negative relationship between ESG score and COD (β = −0.041, p < .01), rejecting our second null hypothesis and emphasising that the debt cost decreases as the firm’s ESG scores improve. This indicates that lenders offer favourable terms to enterprises prioritising sustainability, resulting in a comparatively reduced rate of debt financing. In essence, heightened transparency in ESG disclosure corresponds to diminished costs associated with enterprise debt. Our model’s findings concur with earlier studies by Crifo et al. (2017), Prasad et al. (2022), Raimo et al. (2021), Yeh et al. (2020) and Yilmaz (2022).

Model 3 regression results indicate a statistically significant positive relationship between WACC and ESG scores (β = 0.017, p < .1), demonstrating that the overall capital cost increases with the increase in ESG scores. This phenomenon results from companies’ overreliance on equity capital, particularly in emerging markets. Several issues in emerging markets, such as infrastructure and regulatory challenges, a lack of investor access to credit information, the illiquidity of corporate bonds, and the predominance of financing from banks, cause the underdevelopment of the corporate bond market (Tendulkar, 2015). Size is significantly and negatively related to all sources of finance, consistent with the literature (El Ghoul et al., 2011), signalling that large firms pay a lower premium for raising finance mainly because lenders and shareholders are more optimistic about their prospects. Another variable, LEV, exhibits a significantly positive association with both COE (Gonçalves et al., 2022) and COD, consistent with the rational explanation that a firm with a high LEV ratio is more likely to experience a credit default risk, resulting in a higher expected premium by lenders and shareholders.

Several previous studies, particularly those involving developed countries, contradict our findings. Gholami et al (2023), Ould Daoud Ellili (2020) and Ramirez et al. (2022) .found a negative relationship between ESG scores and the COE and WACC. The paucity of research in this domain, especially in emerging markets, makes it challenging to draw conclusions from the literature reporting conflicting results. This disagreement of findings is plausibly the outcome of various attributes, such as diverse cultures, socio-economic character, statutes and ordinances, the extent of shareholder activism, institutional framework and others. Prior research has also suggested that the ESG policies of firms in emerging markets differ from those of advanced economies (Akhtaruzzaman et al., 2022; Martins, 2022).

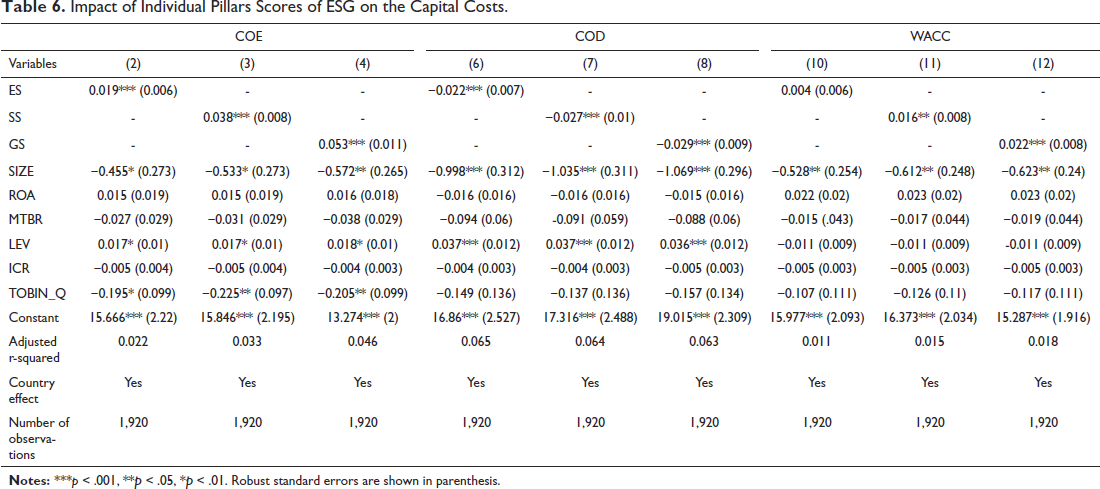

Additionally, an examination of each pillar reveals critical insights for investors. Our findings reveal that all three pillars of ESG scores, namely the ESG scores, have a significantly positive relationship with the COE. COD has a negative association with all of the ESG pillars. Table 6 demonstrates the impact of individual ESG pillar on the companies’ capital costs. Regarding WACC, the social and governance scores are significantly related, whereas the environmental score is not. The highest coefficient value of the governance score proves that the governance pillar is the most important of all the pillars that affect the firm’s financing costs.

Impact of Individual Pillars Scores of ESG on the Capital Costs.

Robustness Test

We conducted a robustness check to ensure that potential endogeneity does not make our estimators biased and inconsistent. Endogeneity is caused primarily by reverse causality, measurement errors, omitted variable bias and selection bias, among other things. The firm’s decision on the extent of its investments in ESG activities could be influenced by its cost of capital financing, resulting in reverse causality and an incorrect interpretation of the relationship between the variables.

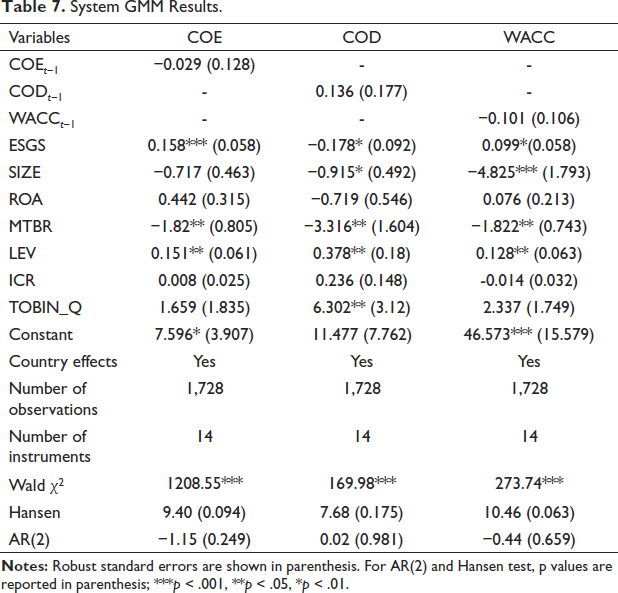

Although the fixed effect model helps eliminate endogeneity by controlling unobserved heterogeneity in the data, we nevertheless employed the two-step System Generalised Method of Moments (GMM) regression by Blundell and Bond (1998) to verify the robustness of our benchmark analysis results. Table 7 shows the system GMM results of the association between companies’ ESG scores and capital costs. In addition to the variables examined in our baseline regression model, the one-year lag of our key dependent variables, namely COE, COD and WACC, is also employed as an explanatory variable in GMM models. ESG scores have a positive relationship with COE that is significant at 1%, as opposed to a significantly negative relationship with COD at a 10% significance level. The WACC also displays a significantly positive relationship with the ESG rating. The GMM regression results match the findings of our baseline model, demonstrating the robustness of our conclusions. Wald χ2 is significant, indicating that the independent variables used in the analysis are significant for the model. The AR(2) test confirms that our models have no serial correlation problem. The validity of our instruments is affirmed by the statistics of the Hansen test of over-identifying restriction.

System GMM Results.

Conclusion, Implications and Limitations

In a dynamic regulatory environment, companies must embrace sustainability measures to stay competitive. ESG scores are a powerful yardstick for investors to evaluate and compare firms’ performance. ESG influences major corporate decisions, such as mergers and acquisitions, executive compensation and others (Brooks & Oikonomou, 2018). The growing integration of ESG considerations into financial decision-making by investors makes it even more intriguing to probe how ESG may affect company financing costs.

This article investigates the link between ESG ratings and the WACC, with detailed attention to their relationship with equity and debt costs separately. Furthermore, we investigated how individual ESG pillars influence financing costs, making it easier for managers to decide which pillar to prioritise based on their capital structure. The study examined 10-year panel data from 192 non-financial enterprises from BRICS nations. The fixed effect panel regression analysis reveals that ESG scores are significantly related to COE, COD and WACC. The findings revealed a positive relationship between ESG scores with COE and WACC, albeit a negative association with COD, corroborating earlier findings. The robustness of these relationships is further demonstrated by applying a two-step System GMM regression to our core model, which produced the same results as our benchmark regression results. One plausible explanation for the positive association between ESG ratings and WACC is that most enterprises in developing economies are primarily funded by equity, owing to the underdevelopment of their bond markets (Endo, 2008). For instance, over half of our sampled Indian firms had less than 10% debt capital in their total capital structure, relying primarily on equity capital (Bloomberg, 2022). As a corollary, the ESG score’s negative association with COD is overshadowed by its positive relationship with COE, resulting in an overall significant positive relationship between ESG scores and the WACC. By delving deeper into the interaction of different ESG pillars with the WACC and its components, we discovered that all pillars are positively associated with COE while negatively related to COD. The governance pillar proved to be the most influential since the emphasis on governance has increased in emerging nations due to several recent corporate scandals mainly attributed to a lack of effective governance standards (Hail et al., 2018), potentially causing financial and reputational damages to the organisations.

Our analysis helps fuel the present debate over the impact of non-financial disclosure on a firm’s financing costs. Investors in emerging markets are still apprehensive about the costs associated with improved ESG compliance by firms (Dahiya & Singh, 2021) and thus perceive the disclosure of ESG information negatively due to the associated risk (Johnson, 2020). The fundamental purpose of equity shareholders is maximising profits (Friedman, 2007), eventually leading to a higher firm valuation. Additional expenses to meet various ESG compliances will reduce the company’s profit. Therefore, increased ESG compliance, which reflects high ESG scores, is regarded negatively by the shareholders, who expect higher returns as compensation for the higher perceived risk. However, the equity cost might start decreasing in the long run with the shift in investors’ perceived notions.

On the contrary, debt providers appear more receptive to ESG disclosure and incentivise firms by providing discounted financing. Debt holders charge a predetermined interest rate, thus rendering them unconcerned about the company’s profitability. Instead, they value the reputational advantages conferred by highly ESG-compliant firms (Apergis et al., 2022). Also, the majority of companies in emerging markets typically rely on banks and other government financial institutions for debt financing instead of the corporate bond market (Hawkins). Governments in every nation are pressing businesses to embrace sustainability. The rising popularity of sustainability-linked loans and green bonds, which offer a lower interest rate, demonstrates the reward for sustainability provided by lenders. Sustainability-linked loans, trending nowadays, are a promising method of ensuring more substantial ESG considerations by firms because loan terms are directly linked with the sustainability profile of the business (The Rise of Sustainability-linked Loans). Lower borrowing rates are granted to businesses in consideration of reaching predefined sustainability targets (Vulturius et al., 2022). Companies in BRICS nations will take time to leverage their ESG performance to reap the advantage of sustainability-linked loans, as the concept is fresh to emerging markets. Another example is India’s recently announced green credit programme, wherein the government promises to incentivise firms that adhere to sustainable activities as per the Environment (Protection) Act.

This study carries substantial insights for various stakeholders. Managers can effectively use this information to compete in the marketplace by improving the quality of their corporate practices. Through effective and widespread dissemination of information in the financial market, managers can improve their ESG ratings. Investors value informational transparency; therefore, if the firm effectively informs the investor that being highly ESG compliant is not detrimental to its financial performance, the investor may be able to expect a lower rate of return on their invested capital. Credit providers may also track a firm’s degree of risk by evaluating its ESG behaviours and accordingly charge a reasonable interest rate.

Nonetheless, this article has several limitations. Our study used a limited sample derived from the indices of the BRICS nations for 10 years. More emerging markets in the sample will help to generalise the findings. Besides that, our research relies on secondary data. A future study based on primary data will help substantiate our findings. Furthermore, this article suffered from survivorship bias, as several firms failed to meet the sample selection criteria owing to the unavailability of ESG scores and other financial metrics. However, this limitation is not anticipated in future studies because of the growing availability of ESG rating providers, which would allow for even more sophisticated ESG data with broader coverage. Future studies comparing the impact of ESG disclosure on capital costs between highly ESG-compliant and less ESG-compliant groups would add to a more comprehensive understanding. Furthermore, investigating the impact of a country’s institutional framework on the relationship between ESG and capital costs will assist us in gaining insight into this intricate relationship.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.