Abstract

The research on integrated reporting (IR) has grown swiftly over the past decade, and specific attention is given to the disclosure quality of IR information across the globe. The objective of this study is to investigate the association between board characteristics and integrated reporting quality. The analysis selected 46 Indian listed companies with 138 firm-year observations over three years. The study found a positive impact of board size, CEO duality, non-executive board members, financial leverage, the COVID-19 crisis and firm size on IR quality. The study found a negative effect of gender diversity, board activity and profitability on IR quality. This study is the first to examine the effect of board features on the implementation and adoption of IR in the Indian context. Moreover, the study offers key insights for researchers, practitioners, accounting bodies, government agencies, investors and policymakers into the use of integrated reporting and sound decision-making.

Keywords

Introduction

A conventional annual report mainly focuses on the financial and economic aspects of a business. Further, a few complementary reports on corporate social responsibility, corporate governance and business responsibility are also presented along with the annual report (Frías-Aceituno et al., 2013). Traditional financial reports follow certain accounting standards, regulations and rules. Therefore, corporates do not publish complete information as per stakeholders’ requirements (Alfiero et al., 2017). Individually drafted reports might provide overlapping information, lack of integration and absence of coherence, which leads to delay in decision-making (Frías-Aceituno et al., 2013; Vitolla et al., 2019). However, disclosing the information is seen as the best way to communicate valuable information to stakeholder groups (Alfiero et al., 2017). The topic of integrated reporting (IR) framework and quality disclosure has received significant attention from researchers, regulators and other professional bodies (Raimo et al., 2020). IR is a novel inclination in corporate sustainable reporting, representing a standard shift from traditional financial reporting to non-financial reporting and presenting these two combined documents in a single stand-alone report (Iredele, 2019; Veltri & Silvestri, 2020). The novel reporting creates value for the business (Vitolla et al., 2019) and improves decisions related to risk management and resource allocation (Frías-Aceituno et al., 2013). The IR framework creates an opportunity to meet the expectations of various stakeholder groups and enhance the stakeholders’ trust in the company (Eccles & Krzus, 2010; Vitolla et al., 2019). IR quality improves corporate reputation, increases earning quality, reduces reputational risk and cost of capital, increases analysts forecast accuracy and increases corporate value and financial performance (Dey, 2020; Erin & Adegboye, 2021; Esch et al., 2019; Flores et al., 2019; García-Sánchez & Noguera-Gámez, 2017; Obeng et al., 2020; Pavlopoulos et al., 2019).

The process of disclosing non-financial information gives a clear picture of economic capability and removes information asymmetry (Alfiero et al., 2017). The voluntary disclosure includes significant non-financial information beyond what is legally required (Ariff, 2013). The agency problem and information asymmetry are removed only with transparency via non-financial disclosure (Alfiero et al., 2017). Given these hurdles, companies began to combine individual reports into a single integrated report. Thus, the IR provides combined, structured disclosure about a company’s strategy, prospectus, governance and performance in broader aspects (Eccles & Kruz, 2010).

The corporate boards consist of both executive and non-executive members, and their role is to direct, run and control the company (Qaderi et al., 2022). The board establishes an internal governance mechanism to protect the stakeholders’ interests and strengthens corporate disclosure (Aladwey et al., 2021; Busco et al., 2019). The boards are meant for formulating corporate sustainable strategies (Orazalin & Baydauletov, 2020), looking after the company’s performance (Omran et al., 2021), supervising the manager’s actions (Songini et al., 2022), preserving the stakeholders’ interests (Songini et al., 2022), improving the connection between the company and external resource providers (Jamil et al., 2020) and taking actions for long survival of the company in the market (Qaderi et al., 2022). In keeping with the argument of agency theory, earlier studies have proved that the corporate board was crucial in maintaining effective observation techniques and minimising the agency problem and information asymmetry. The present study’s objective is to analyse the influence of board features on IR quality. Earlier studies focused on the relationship between board features and non-financial disclosure based on agency theory (Frías-Aceituno et al., 2013; Vitolla et al., 2020a). The present study is based on agency theory, as this theory enumerates the dynamics of voluntary disclosure (Frías-Aceituno et al., 2013). It contributes to the literature in the following manner: First, the study recognises the determinants of integrated quality standards. Second, the study extends the scope of agency theory. Finally, it examines the association between IR quality and corporate governance performance.

Growth of IR in India

The board structure has a key role in IR adoption, and IR disclosure has received significant consideration in most high-income countries. However, in emerging countries like India, the board’s role is still unexamined in disclosing IR information. The present study aims to fill the gap by examining the effect of board features on IR, as per an agency theory prospect. It focuses on Indian listed companies for several reasons. First, the Indian regulatory bodies (such as Securities and Exchange Board of India [SEBI]) and professional bodies (such as Confederation of Indian Industries [CII] and others) have paid much attention to IR adoption through the Integrated Reporting Framework Council (IIRC) in India (Abhishek & Divyashree, 2019). Second, the SEBI circular requested all listed companies to follow IR voluntarily as per the IIRC (Abhishek & Divyashree, 2019; Bal & Bal, 2019). Third, the IIRC members had an interactive section in India with Indian corporates and enumerated the emergence of IR (Vrushali, 2019). Fourth, a few well-established companies participated in the IR pilot programme, and corporate personnel are part of the IIRC (2013). Regular development of the IR framework makes India one among the few countries to follow IR voluntarily (Abhishek & Divyashree, 2019; Ghosh & Bhattacharya, 2020; Mishra et al., 2022). The growth of IR in India is improving, but its effect has not been examined (Prajapati et al., 2014). The study has not found much difference between IR and other reports (Kundu, 2017), the average score of IR by the selected firms significantly improved (Lohar & Soral, 2017), IR adoption enhanced the firms to disclose more information (Joshi, 2018) and the extensive business reporting language significantly improved the IR information (Ashok, 2019). Therefore, the present study examines the association between board features and IR standards for IR-adopting firms from India.

Trends of IR in India

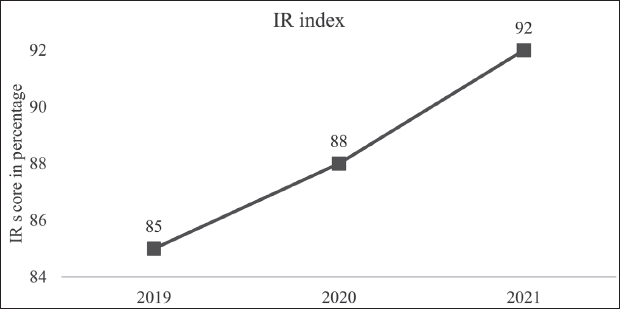

Figure 1 discloses the mean of IR quality scores measured by the total integrated reporting quality (TIRQ) index for three years. The mean score of the TIRQ index was 85 per cent in 2019, 88 per cent in 2020 and 92 per cent in 2021. The IR adoption in India was initiated by SEBI’s circular in 2017, which encouraged Indian companies to publish IR information on a voluntary basis. The disclosure quality of the sampled companies was found to be improving during the proposed period, especially under the pandemic conditions. The IR disclosure helps to maintain healthy relationships with stakeholders and meet various requirements. The companies might have improved IR disclosure as a mechanism to overcome the pandemic effect and to remain close to the stakeholders by publishing material non-accounting information.

Theoretical Background

A few studies have discussed the relationship between board characteristics and corporate disclosure (Vitolla et al., 2020a). The present study is theoretically supported by the agency theory. The agency theory enumerates the relationship between the agent and the principal. Further, in agency theory, an agent acts on behalf of the principal or stakeholders (Jensen & Meckling, 1976). A conflict of interest arises when the goals of the agent and principal are different. Due to opportunistic management behaviour and the presence of information asymmetry, conflict of interest arises (Jensen & Meckling, 1976). To solve this problem of the agency theory, it is suggested to upsurge the internal review system by appointing more independent directors or non-executive members and revealing more IR information (Vitolla et al., 2020a). The problem of information asymmetry will be overcome by having a positive association between agent and principal (Raimo et al., 2021). The IR adoption enables firms to disclose quality non-financial information to stakeholders and minimise information asymmetry (Vitolla et al., 2020b). Frías-Aceituno et al. (2013) justified that having effective board members minimises the problem of agency, reduces information asymmetry and maintains high transparency in reports. Vitolla et al. (2020a) found corporate boards positively respond to disclosure of high-quality information and justified that the IR disclosure reduces the agency issues and the information asymmetry problem. IR adoption by the firms postulates to improve both financial and non-financial information disclosure and gives importance to stakeholders. Hence, the present study strongly believes that the adoption and implementation of integrated reports by Indian listed companies might build a strong association between management and stakeholder groups.

The rest of the article is organised as follows: The second section deals with a review of the literature and hypotheses are proposed to find the relationship between board features and IR quality disclosure; the third section includes research design and model specification. The fourth section discusses empirical results and the discussion of analysis. The final section concludes the study with proper implications, findings and future scope.

Literature Review

Limited studies have analysed the association between board characteristics and IR standards. A few studies have explored the effect of board characteristics on the growth and quality of IR. The present literature has focused mainly on the influence of board characteristics on the disclosure of IR information. Similarly, it has examined the influence of board effectiveness on the adoption and promotion of IR information. Abeysekera (2010) examined 56 Kenyan listed companies and found that larger boards help to disclose significant capital information. Frías-Aceituno et al. (2013) examined the role of board features in publishing non-financial information by large multinational companies. The study found that growth opportunity, firm size, gender diversity and board size were statistically significant with non-financial disclosure. In contrast, board independence and board activity were negatively associated with non-financial information. Jizi et al. (2013) found a positive and significant association between board composition and corporate social responsibility (CSR). Samaha et al. (2015) examined the relationship between board characteristics and voluntary disclosure. The results found that board size was statistically significant with voluntary disclosure. Similarly, results from Lai et al. (2016) found a significant relationship between corporate board characteristics and IR practice.

Alfiero et al. (2017) investigated 1,047 European companies and found board size and females on the board had a significant association with the IR. In contrast, the study found a negative nexus between older board members and IR disclosure. Nadeem et al. (2017) found women on board were statistically significant with corporate sustainable disclosure. Kilic and Kuzey (2018) examined 55 non-financial companies and found that larger firms and the role of women on board significantly affected the forward-looking disclosure. However, larger boards, firms’ profitability and leverage have an insignificant association with forward-looking disclosure. A study by Ofoegbu et al. (2018) investigated 303 environmentally sensitive companies in two developing countries and found industry membership, board size, audit firm size and environmental committee were statistically significant with environmental disclosure for South African companies. Likewise, for Nigerian companies, only board size, audit firm size and independence of board members were significant with environmental disclosure. The results for the combined sample showed that most of the variables were found to be significant with environmental disclosure under IR guidelines.

Vitolla et al. (2020a) examined 134 international firms and found IR quality was positively affected by board size, board independence, board diversity, board activity, firm size, civil law and sustainable committee. The results showed that profitability was not significant with IR quality. Cooray et al. (2020) examined 132 Sri Lankan listed firms and found board size and risk management committee were significant with IR quality. In contrast, the study identified an insignificant relationship between CEO duality, board independence, gender diversity and an independent audit committee with IR quality. Lopes and Braz (2020) found that board features such as CEO duality, board size, board independence and gender diversity were statistically significant with IR information.

Vitolla et al. (2020b) examined 130 international firms and found board activity, diversity, size and independence of the board, firm size, profitability and CSR committee were statistically significant with intellectual capital disclosure (ICD). In contrast, the results revealed that firm age and environmental sensitivity were insignificant with ICD. Marrone (2020) investigated 139 international firms and found gender diversity, CEO duality, profitability (ROE), firm size, board dimension and environmental sensitivity were associated with IR disclosure. In contrast, the study found that the board average age, civil law, CSR committee and firm age were not associated with the IR disclosure. Hamad et al. (2020) examined the effect of sustainable reporting on the association between governance performance and IR disclosure quality for 100 top Malaysian listed firms. The results found that a sustainable report builds a strong relationship between a few board features and IR quality.

Omran et al. (2021) examined the top 50 Australian listed companies and reported that non-executive members, firm size, growth opportunity and profitability were significant with IR quality. In contrast, board size, board meetings and women on board were not associated with aggregate IR disclosure. Qaderi et al. (2022) investigated the impact of board characteristics and the existence of a sustainability committee on IR disclosure. The results disclosed that independent members, size of the board, gender diversity, non-executive directors’ remuneration and the existence of sustainable committees substantially affected the IR disclosure. Having multiple directors was found to be insignificant with the quality of IR disclosure. Songini et al. (2022) investigated the impact of board features on IR quality with 212 integrated reports of 55 listed companies. The study found the education level of board members and profitability had a substantial effect on IR quality. In contrast, IR quality was not affected by board size, women on board, non-executive members and financial leverage. Hasan et al. (2022) examined 138 listed firms from Pakistan and found a positive association of firm size, gender diversity, larger audit committees, growth opportunities and firm age with voluntary sustainable disclosure. In contrast, the number of subsidiaries, financial capacity, independent audit committee, foreign ownership and managerial ownership were insignificantly associated with voluntary sustainability disclosure. Hichri (2022) examined 120 French companies and found audit committees and diversity have a positive association with IR. However, the CEO’s duality and board size were found to be insignificant with IR quality.

Lee and Yeo (2016) examined 822 South African firms and found that IR quality has a significant impact on firm value. Cosma et al. (2018) examined listed firms from South Africa and found that IR has a substantial effect on firm performance. Nurkumalasari et al. (2019) examined 14 Asian firms and reported that IR has no effect on firm performance for highly levered firms. Zhou et al. (2017) found an insignificant association between IR quality and analyst forecast accuracy in the context of South Africa. Wahl et al. (2020) also found IR disclosure has an insignificant association with firm value and earnings forecast accuracy. Qaderi et al. (2023) analysed Malaysian listed firms and found IR disclosure levels and quality were significantly improved. Soriya and Rastogi (2023) examined 93 annual reports of Indian companies and found IR quality disclosure is considerably related to firms’ profitability while having an insignificant relationship with firms’ performance. The impact of IR quality has a varied impact on firm performance in different countries. Based on this review, the present study proposes five hypotheses.

Hypotheses Development

The present study investigates the impact of board features on IR quality. Specifically, the study considers board features such as board size, board diversity (women on board), duality of CEO (CEOD), role of non-executive board members and board activity represented by the number of board meetings held during the year.

Board Size and IR Practices

Board composition represents different opinions and perspectives of directors. The board composition improves the effectiveness of top management and endorses a strong relationship between agent and principal (Vitolla et al., 2020a). The board function depends on structure and board composition (Frías-Aceituno et al., 2013). The execution of corporate governance standards will improve reporting quality and transparency in disclosure (Kilic & Kuzey, 2018). The board composition indicates the combination of both executive and non-executive members or independent and non-independent members (Wang et al., 2020). The board members are reasons for framing corporate mechanisms and corporate policies to be performed by the managerial personnel (Vitolla et al., 2020b). Because of the monitoring role of directors, firms might disclose non-financial information (Kilic & Kuzey, 2018). On the other hand, board size is measured as a major element for the effective implementation of voluntary disclosure. And the inclusion of larger boards positively helps the firms to disclose quality IR (Marrone, 2020). Few empirical studies have provided a positive link between board size and IR quality. The effective board may positively impact the firm’s disclosure (Qaderi et al., 2022). In contrast, a few studies argue that board size has no impression on IR quality (Alfiero et al., 2017; Kilic & Kuzey, 2018). So, the following hypothesis is proposed:

H1: IR quality is positively affected by the board composition or board size (BS).

Board Diversity (Role of Women on Board) and IR Practices

Gender diversity is the most discussed topic in recent literature (Alfiero et al., 2017). The importance of diversity is rising due to cultural, social and ethical differences between men and women (Liao et al., 2015). A few studies have investigated the difference between men and women in terms of educational qualification, professional experience, personality and skills (Vitolla et al., 2020b). The presence of women on board creates a pleasant climate, more diligence and more commitment (Huse & Solberg, 2006). Moreover, female directors are less focused on their personal goals and focused more on board effectiveness (Frías-Aceituno et al., 2013). Similarly, women on board can enumerate the variance in information disclosure practices between different organisations. So, women on board favour the development of IR quality disclosure (Vitolla et al., 2020a). The women’s nature, values and behaviour are strongly linked to disclosing higher quality information and greater transparency within the company (Frías-Aceituno et al., 2013). The women on board pay attention to features linked with sustainable disclosure and have strong capabilities for monitoring managers’ activity (Vitolla et al., 2020a). The presence of women on board favours good working conditions and promotes higher disclosure (Frías-Aceituno et al., 2013). Some earlier studies have found a positive relationship between women on board and IR quality (Lopes & Braz, 2020; Qaderi et al., 2022). In contrast, a few studies argue that the presence of women on board has no impact on the disclosure of IR information (Omran et al., 2021; Songini et al., 2022). In the IR context, greater involvement by women on board could lead to the disclosure of high-quality IR. Therefore, we propose the following hypothesis:

H2: IR quality is positively affected by the percentage of women on board (%WOB).

CEO Duality

Conflict of interest and agency costs are higher when the CEO plays a dual role (Arora & Sharma, 2016). CEO duality comprises an absorption of dynamic decision-making power, which lessens the board’s independence, monitoring and control (Gul & Leung, 2004). Similarly, the CEO duality diminishes the board’s fairness (Krishnan & Visvanathan, 2009). The CEO duality causes a two-way situation that could positively or negatively affect the disclosure quality of information (Marrone, 2020). Entities with dual roles tend to produce more IR information (Lopes & Braz, 2020; Marrone, 2020). The presence of CEO duality can reduce the power of board members (Lopes & Braz, 2020). It is observed that one key person holding dual positions might influence the firm’s performance. The CEO duality can disclose and promote more non-financial information (Marrone, 2020). When the CEO holds a dual position in the company, the CEO carries out effective decisions without any bureaucratic rules (Arora & Sharma, 2016). The concentration of power with a single person leads to effective negotiation with board members to disclose more IR information. The centralised authority of the CEO helps to make quick decisions and influences the board members to have high standards of disclosure of IR information. A few studies have discussed that CEO duality increases bureaucracy and does not consider the size of the board in disclosing higher IR (Cooray et al., 2020). Hence, the study proposes the following hypothesis:

H3: IR quality is positively affected by the dual position of CEO (CEOD).

Board Activity (Number of Board Meetings Held During the Year)

Board activity is another important dimension of board operations, which tries to solve the agency problem and overcome the problem of conflict. The ability to monitor the managers’ movements is also connected with board activity (Vitolla et al., 2020a). So, frequent board interactions help the management to communicate valid information to interested parties. Lipton and Lorsch (1992) enumerated that a board with a larger number of meetings is more dynamic and reaches the expectations of stakeholders’ interests. Further, more board meetings involve the distribution of quality information to related stakeholder groups and capital providers. Further, Xie et al. (2003) found that increased board meetings involve dynamic supervision and low chances of reducing corporate earnings. The information asymmetry is reduced, due to frequent board activities (Vitolla et al., 2020a). Information connectivity and monitoring were only possible with a greater number of board meetings (Frías-Aceituno et al., 2013). The high attention and monitoring could lead the firms to disclose advanced IR information. A few studies found a significant association between IR and board activity (Ntim & Osei, 2011; Vitolla et al., 2020c). In contrast, few studies proved that there was an insignificant relationship between board activity and IR disclosure (Frías-Aceituno et al., 2013; Kantudu & Samaila, 2015). Therefore, the present study proposes the following hypothesis:

H4: IR quality is positively affected by the board meeting held during the year (NOBM).

Non-executive Board Members

The important aspect of corporate governance is to reduce agency costs, and it significantly depends on on-board composition (Frías-Aceituno et al., 2013). A board with more non-executive members is likely to closely watch the management activities diligently (Liao et al., 2015). The non-executive board members are not directly involved in business operations (De Villiers et al., 2011) and do not have any positions in the company; hence, they provide valid feedback regarding performance and management operations (Liao et al., 2015). So, the greater presence of non-executive members leads to effective observation of the operations of the company (Vitolla et al., 2020a). A board with more non-executive members guarantees the specific objective and positive behaviour of the company towards stakeholders (Vitolla et al., 2020a). The guarantee from non-executive members promotes the disclosure quality of information, and this will be directly impacted by the reputation and experience of members (Qaderi et al., 2022). So, independent members request the companies to disclose high-quality information to users (Qaderi et al., 2022). The presence of more independent members on board favours the higher disclosure of IR information and removes information asymmetry (Qaderi et al., 2022; Vitolla et al., 2020a). A few studies have enumerated that board independence enhances quality IR and removes information asymmetry (Lopes & Braz, 2020; Omran et al., 2021). In contrast, board independence has no positive impact on IR quality (Songini et al., 2022). Hence, the present study proposes the following hypothesis:

H5: IR quality is positively affected by the non-executive board members (NEBM).

Research Design

This section deals with suggested empirical research techniques for the study. These consist of the choice of a sample and a valid explanation of such a sample choice. In addition, it also includes model specification, model estimation and the types of variables and their descriptions.

Sample Construction and Source of Data

The sample selection is conditioned by the obligation and participation of firms in the adoption of the IR framework, for which this study followed the reports of Grant (2020), AICL (2020) and Vrushali (2019). The sample data (corporate governance and financial data) is collected from the Centre for Monitoring Indian Economy (CMIE) Prowess database and content analysis from the annual reports of sample companies. The initial sample size consists of 58 IR-adopted companies. This study has excluded banks and insurance companies, considering the specific intention of the IR framework for non-financial companies. Hence, the final sample consists of 46 IR-adopted companies with 138 firm-year observations. The period consists of three years, that is, 2019 to 2021; during this time slab, only 46 Indian listed companies disclosed at least three years of integrated reports. This sample time provides the opportunity to test whether corporate governance features contribute to producing high-quality IR disclosure or not.

Variables and Model Specification

Dependent Variable

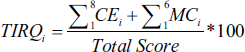

Few studies have proposed various approaches to assess the quality of IR. Alfiero et al. (2017), Agustia et al. (2020) and Pistoni et al. (2018) employed content elements as a proxy for IR quality. Kilic and Kuzey (2018) proposed forward-looking disclosure under the content elements, and Vitolla et al. (2020b) coined intellectual capital disclosure as a proxy for IR capital. Therefore, this study considers a dependent variable as total IR quality (TIRQ), which is a combination of eight content features and six capitals. Previous studies have proposed similar techniques to assess the existence of IR information through an annual report of the companies. This study evaluated the scoreboard or index under the presence of 14 constituents, that is, eight content elements and six capitals. The study analysed the existence of both quantitative and qualitative information under IR. This study allocates a score of 0 in the absence of individual features of capitals and content elements as developed in the scoreboard. Similarly, it allocates a score of 1 if the feature exists for the content element and capital in the integrated annual report. All individual content elements and capitals have a maximum score of 6 based on the scoreboard. The overall maximum score of content elements and capitals is 84; that is, the maximum score for content elements is 48 and capitals has a maximum score of 36. The TIRQ disclosure index is presented as the following mathematical equation:

Where TIRQi = Total integrated reporting quality of the firm, CEi = Scores allotted for individual content elements and MCi = Scores allotted for multiple capitals.

Independent Variables

The board size (BS) is considered as the count of members on the board (Marrone, 2020). The gender diversity, or %WOB, is denoted as the proportion of women participating on the board (Kilic & Kuzey 2018). The CEOD indicates the dual role played by the CEO, and it is a dummy variable that assumes a score of 1 if the CEO also holds another position in the company and 0 otherwise (Marrone, 2020). The board activity or the number of board meetings (NOBM) indicates the number of meetings held by the board members during the year (Vitolla et al., 2020a). The board independence or non-executive board members (NEBM) indicates the number of independent members on the board (Ofoegbu et al., 2018).

Control Variable

To increase the goodness of panel data analysis, the following control variables are incorporated. The natural logarithm of total assets is a proxy for overall firm size (Vitolla et al., 2019). Previous studies have reported that there was a positive association between firm size and voluntary disclosure of non-financial information, or IR information (Vitolla et al., 2020a). The profitability (return on assets) is measured as net profit/total assets × 100 (Kilic & Kuzey, 2018). The profitability (ROA) is included in panel data analysis as it represents the firm’s financial performance and it is one of the important elements to improve the quality of IR disclosure. Firms allocate different resources out of profitability to draft IR information (Vitolla et al., 2020a). The financial leverage (Solv) is measured as a ratio of debt to total assets (Songini et al., 2022). Another control variable is COVID-19 (CD), which is denoted as a dummy variable and gets a value of 1 if pandemics are presented in the annual report and 0 if not.

Model Specification

The present study used a regression model to test the proposed board features’ relationship with TIRQ, following the model of Vitolla et al. (2020c) and Kilic and Kuzey (2018). Specifically, the study used a balanced panel data analysis. The following equations elaborate the panel data analysis, including all five models:

TIRQit = Total integrated reporting quality; BSit = Board size; %WOBit = % of women on board; CEODit = CEO duality; NOBMit = Number of board meetings; NEBMit = Non-executive board members; Solvit = Financial solvency; Log TAit = Natural logarithm of total assets; ROAit = Return on asset; CDit = COVID-19 dummy variable; uit = Error term.

Results

Descriptive and Correlation Analysis

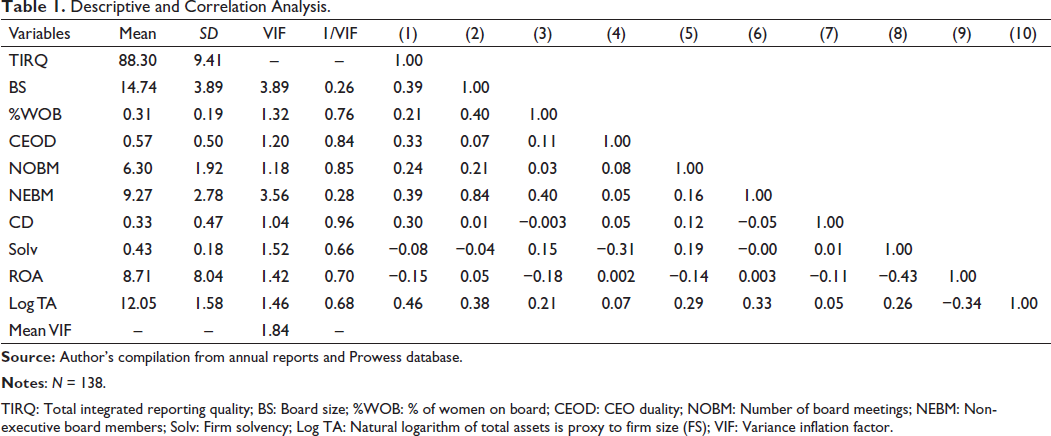

Table 1 presents the descriptive and correlation results. The dependent variable is TIRQ. It has an average score of 88.30, which indicates a high disclosure quality of information by the Indian listed companies. The average BS is 14.74. The board diversity has a low average score of 0.31, which indicates the diversity of the board is low and the role of women on board is limited. The CEOD has a low average score of 0.57, which demonstrates that only a few companies’ CEOs play dual roles. The NOBM’s average score is 6.30, which represents that every two months, one board meeting is conducted. The average of NEBMs is 9.27, which shows a reasonable degree of independence. The firm’s leverage has an average score of 0.43. The correlation results found a lack of multicollinearity in the results. Further, the multicollinearity results are also confirmed by the variance inflation factor (VIF) analysis. The minimum VIF is 1.04 for the COVID-19 pandemic, and the maximum VIF is 3.89 for BS. Hence, the VIF score is below the standard baseline point. The study has verified White’s test for normality check and found that the data is distributed normally for all five models.

Descriptive and Correlation Analysis.

TIRQ: Total integrated reporting quality; BS: Board size; %WOB: % of women on board; CEOD: CEO duality; NOBM: Number of board meetings; NEBM: Non-executive board members; Solv: Firm solvency; Log TA: Natural logarithm of total assets is proxy to firm size (FS); VIF: Variance inflation factor.

Multivariate Analysis

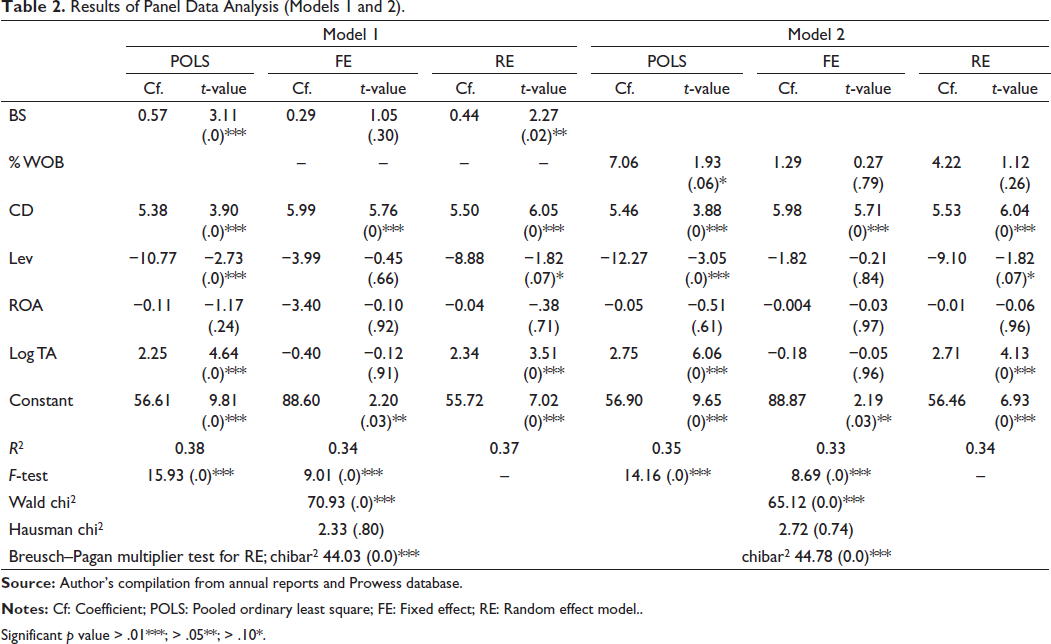

The panel data results for Models 1 and 2 are presented in Table 2; Models 3 and 4 results are presented in Table 3; and Model 5 results are presented in Table 4. The dependent variable for all five models is TIRQ, and it is fixed for all models. The detailed panel results are presented in Tables 2 to 4. To examine panel data, the study applied POLS, FE and RE methods for the analysis. The study found the RE method is more appropriate, as confirmed by the Hausman specification test for all five models. Further, the study has conducted the Breusch–Pagan multiplier test to choose between the RE model or POLS. Therefore, the results suggest analysing only RE model results. In Model 1, BS is an independent variable. The study found there is a strong positive connection between BS and TIRQ at a p value of .02. The result indicates that firms with strong BS help to promote TIRQ in India. So, the study accepts H1. Next, in Model 2, the independent variable is %WOB. The results did not support H2 and found that %WOB has an insignificant association with TIRQ at a p value of .26. Hence, the participation of women does not have much impact on the disclosure of TIRQ-listed companies. So, the second hypothesis (H2) is not supported.

Results of Panel Data Analysis (Models 1 and 2).

Significant p value > .01***; > .05**; > .10*.

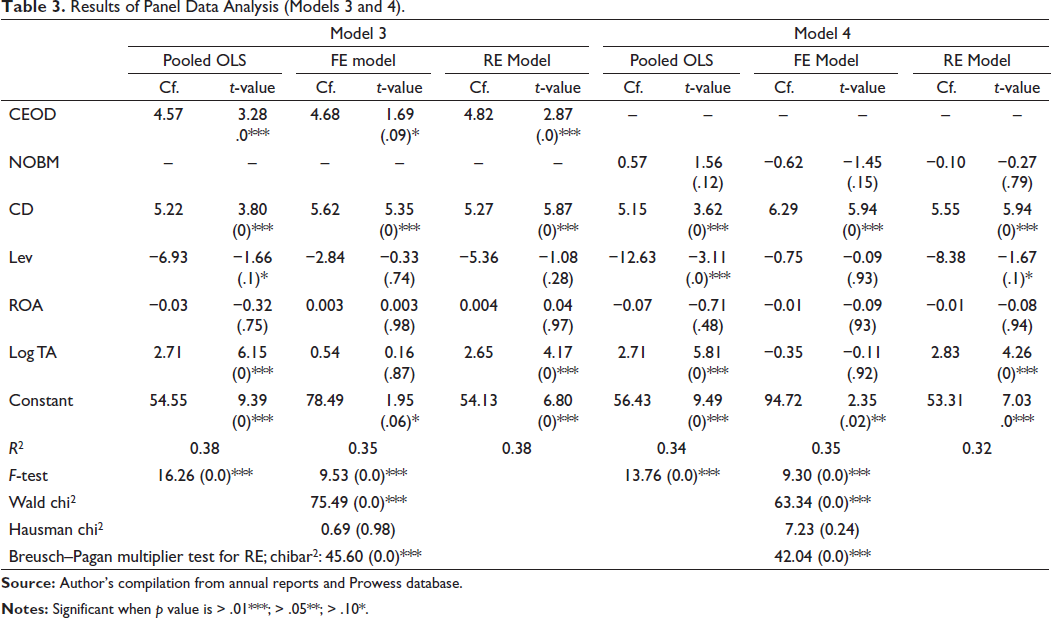

Results of Panel Data Analysis (Models 3 and 4).

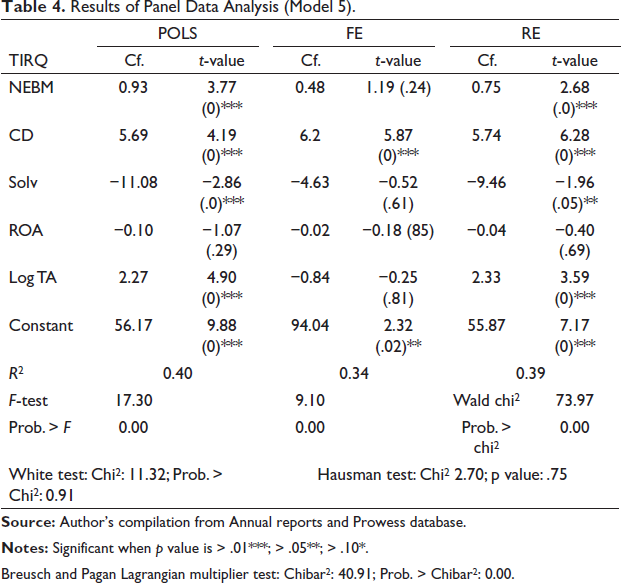

Results of Panel Data Analysis (Model 5).

Breusch and Pagan Lagrangian multiplier test: Chibar2: 40.91; Prob. > Chibar2: 0.00.

In Model 3, the independent variable is CEOD. The results found that CEOD has a positive and statistically significant relationship with TIRQ at a p value of .0. This enumerates that the duality of the CEO has a significant impact on disclosing high non-financial information, or TIRQ. So, H3 is supported. In Model 4, the independent variable is NOBM, or board activity. The results do not support H4. The NOBM is insignificant, with the TIRQ at a p value of .79. Frequent board meetings do not guarantee the disclosure of higher-quality information.

In Model 5, the independent variable is NEBM (board independence), as presented in Table 4. The results support H5. The board with a higher NEBM has a positive and significant impact on TIRQ at a p value of .0. This result indicates that the companies with higher NEBM favour disclosing high-quality IR information. Finally, the empirical results disclose that firm size has a significant effect on the disclosure of TIRQ for all chosen models. Usually, superior firms favour disclosing better IR information than small firms. Financial leverage has a negative but significant effect on TIRQ in almost four models. This means listed firms like to disclose more TIRQ information to stakeholder groups and do not consider restrictions from debt providers or credit providers. Another control variable, COVID-19, a dummy variable, is significant with the TIRQ for all the equations. The probable explanation could be that during a pandemic period, most of the listed firms are likely to disclose material non-financial information to various stakeholder groups. This includes the activities carried forward during the pandemic, such as employee safety and service provided under CSR. The profitability (ROA) is insignificant with the TIRQ, which indicates profitability does not have any impact on disclosing the TIRQ. The probability of the F-test is significant for all models. It denotes the considered models that are found to be more suitable. The R2 is found to be satisfactory for all models.

Discussion

The results of the present study confirm that only a few board features influence the IR disclosure positively. The results are interpreted with the help of the agency theory. The problem of information asymmetry is removed between owners and managers after the adoption of the IR framework (Vitolla et al., 2020a). The present study validates how NEBM, CEOD and BS favour the propagation of TIRQ disclosure. First, the study found positive linkages between BS and TIRQ disclosure. Larger boards have greater monitoring capacity and dynamic control over a firm’s operations, which reduces agency costs. Similarly, higher BS removes the problem of agency and minimises information asymmetry (Frías-Aceituno et al., 2013). Jizi (2017), Alfiero et al. (2017) and Kilic and Kuzey (2018) found higher BS leads to disclosure of greater IR quality, removes the agency problem, removes information irregularities and builds strong relationships with stakeholders. Hence, the study suggests that higher BS enables Indian listed firms to disclose more TIRQ in their annual reports.

Second, the %WOB has an insignificant relationship with TIRQ, meaning the presence of women on board has less impact on the TIRQ of Indian firms. Songini et al. (2022), Fasan and Mio (2017) and Omran et al. (2021) also found the role of women is insignificant and cannot influence the disclosure of IR. In contrast to our results, a few earlier studies have strongly suggested women’s role is crucial in promoting and disclosing the quality of IR information (Alfiero et al., 2017; Vitolla et al., 2020a). Our results may be because of the lower participation of women in corporate boards. Third, the CEOD is significant with TIRQ. This means holding two strong positions in a company by a single person might prompt quick and dynamic decision-making and go for disclosing a more reliable TIRQ. Lopes and Braz (2020) and Marrone (2020) strongly believed that CEO duality significantly improved the quality levels of IR information with less bureaucratic interference and quick decision-making. In contrast, Cooray et al. (2020) explained that duality has a negative effect on board monitoring, and concentration of power in one hand leads to a negative effect on firm performance and IR disclosure quality.

Further, the results found that NOBM or board activity is insignificant with TIRQ. Frequent board interactions do not guarantee the disclosure of higher-quality information. Frías-Aceituno et al. (2013) argued that irregular annual meetings do not influence the disclosure quality of IR information. Frequent board activities or discussions enable the firms to disclose high-quality IR information. Vitolla et al. (2020a) found board activity improves effectiveness in monitoring, greater diligence and more control in disclosing IR information. Finally, the study found a positive association between NEBM and TIRQ. The presence of NEBM is an effective tool for managing and monitoring the actions of management (Vitolla et al., 2020a). As the NEBM increases, the possibility of hiding material information will reduce and encourage managers to produce quality IR information. With reference to early studies, the presence of NEBM improves monitoring actions and IR quality and maintains strong stakeholder orientation (Lopes & Braz, 2020; Omran et al., 2021). Songini et al. (2022) found that NEBM cannot control the activities of managers. Moreover, these results confirm the prospects of the role of the board features as righteous to good governance approach. The features of boards such as BS, NEBM, %WOB, NOBM and CEOD favour strong bonds with interested groups. Strong corporate governance performance fuels more IR quality and transparent information. This leads to a strong competitive advantage for the company.

Conclusion

Traditional corporate reporting mainly focuses on past financial performance and usually lacks future forecasts for financial endeavours. At present, companies expect that disclosing integrated annual reports will incorporate more prospective information (Adams & Simnett, 2011). The current study has examined the effect of board features on the IR disclosure levels of Indian IR-adopting companies. Specifically, by using agency theory, the study verified the effect of BS, CEOD, % WOB, NOBM and NEBM as factors in disclosing TIRQ. The investigation is conducted on a sample of 46 Indian listed companies with 138 firm-year observations. The study unveiled that board size, CEO duality, presence of non-executive members, COVID-19, leverage and firm size have a positive and statistical impact on TIRQ. The present board features help to disclose high-standard IR information and promote transparency for the use of both stakeholders and shareholders. Similarly, % WOB, board activities have insignificant effects on TIRQ.

The results contribute, in several ways, to supplement the existing literature on IR quality by providing an investigation of TIRQ disclosure in early IR-adopting companies in India. This is one of the initial studies to introduce the concept of TIRQ disclosure under the IR framework. An important contribution to the existing literature is examining the features of IR disclosure by merging both eight content elements and six capitals. The study extends the scope of agency theory and enumerates phenomena related to the novel concept of IR. However, the literature focuses on board characteristics that are correlated with organisational structure, management control, transparency, IR adoption and IR quality, but this study extends the arena of the determinants of IR standards.

The findings of the study have unique suggestions for commercial executives, governing bodies and practitioners. Investors’ attention increased after the introduction of IR as a communication tool (Vitolla et al., 2020a). So, this study suggests that companies redesign their board features in such a way that righteous behaviour results in high-quality IR disclosure. The Indian listed companies should have a reasonably larger board to have better control, monitoring and support to develop IR. This approach could positively influence the reduction of information irregularities and agency costs. In addition, firms need to give high priority to NEBM and women on board. The NEBM and %WOB express positive insights, favour publishing IR standards and favour investment levels and dynamic stakeholder relationships. The dual role favours disclosing high-standard integrated reports. The IR movement will have positive implications for accounting education and corporate governance reporting. Perhaps, the top management of the organisations needs to deeply understand the novel reporting model of IR.

This work has a few limitations, which form the future agenda for IR researchers. First, it is limited to only Indian listed companies and does not compare the disclosure levels of Indian companies with those of other countries. Second, the sample size is restricted to only 46 Indian-listed companies. Third, this study is based only on panel data analysis and not on dynamic panel data analysis. Future research work can be carried out with the inclusion of banking and financial institutions and advanced panel data models. Also, future work could explore countries with different governance mechanisms. Further, the impact of other board features such as the presence of foreign ownership, directors age, directors’ colour and other institutional factors can be explored.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.