Abstract

Purpose:

Environmental, social, and governance (ESG) is becoming a key concept of sustainability around the world. There is a tremendous increase in academic interest in ESG. It is difficult for researchers to structure a large quantity of unstructured data through a structured literature review or meta-analysis. Although, in recent years, many visualization tools have been invented for structuring or visualization of large quantities of literature, yet, there is currently a lack of bibliometric and visualization studies on this subject. To fill this lacuna, this study is conducted to analyse the publication metrics on the ESG literature and to give a research agenda for future research. This study will clarify the conceptual underpinnings of the ESG field serving as a reference for ESG development to help researchers and stakeholders quickly grasp the fundamentals of this subject.

Design/Methodology/Approach:

An extensive literature review was carried out on ESG spread over the period between 2008 and 2022 published journals identified from online academic databases of Scopus. A total of 701 conceptual and empirical articles were analysed. To achieve the objectives of the study, bibliometric analysis was used. To conduct bibliometric analysis, Biblioshiny application of RStudio and VOSviewer software was used.

Findings:

This study highlighted key trends, emerging themes and sub-themes by analysing the statistical profile of ESG literature, most productive ESG research journals, authors, countries, keywords and their collaboration status using bibliometric analysis.

Research implications:

By providing the distribution schema of ESG articles based on different criteria and by providing the future research areas, the present study would help future researchers to understand the current status of ESG research in the business industry as well as in academia and take this research area forward.

Originality/Value:

This bibliometric analysis provides a holistic view of ESG literature highlighting major research themes and their related sub-themes addressed in the research studies to date.

Introduction

Over the past 10 years, many nations have raised concerns about sustainable development and as a result. This has led to growing environmental consciousness among international legal authorities, and the idea of a green economy has drawn the attention of researchers and policymakers. This has led to a focus on the concept of environmental, social, and governance (ESG) in the past decade. The focus and importance of the concept can be understood by the fact that in 2004, the United Nations Global Compact and the Swiss Federal Department of Foreign Affairs published a report “Who Cares Wins”, where they focused on ESG. Since then, it has become a crucial component of investors’ financial decisions as it provides strong evidence of businesses’ commitment to environmental and social transparency (Chauhan & Kumar, 2018; Esty & Karpilow, 2019). Over the years, the focus has increased, and Morgan Stanley in a study in 2019 pointed out that, 85% of individual investors and 95% of millennials in the United States were interested in sustainable or ESG information (GSIA, 2020). Similarly, the Chartered Financial Analyst Institute Trust Survey conducted in 2020 showed that 76% of institutional investors and 69% of retail investors in India are interested in ESG investing and information.

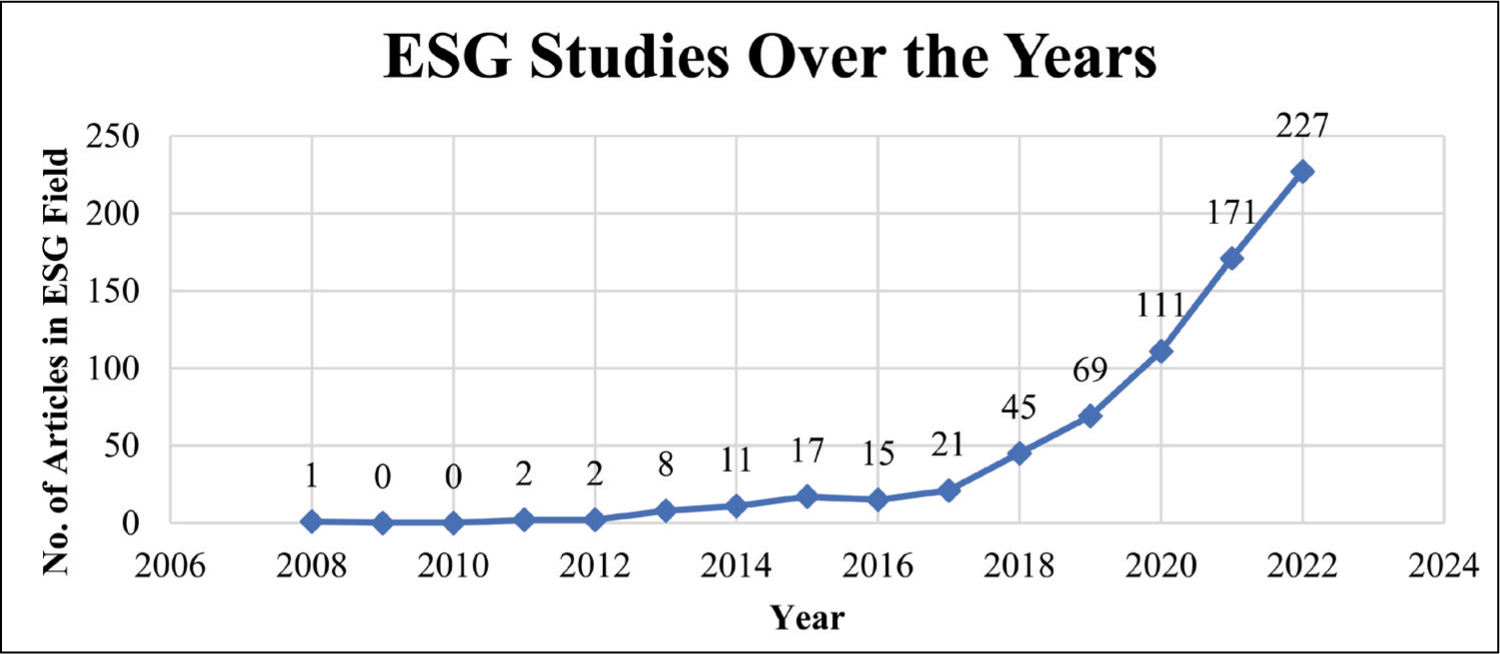

As is the case with most of the concepts, as the focus of the practitioners increases on a concept, the research activity around it also increases. ESG research has also gained momentum after 2010. Bibliometric analysis indicated that the number of papers on ESG research increased from a mere 2 in 2011 to 227 in 2022 (Figure 1). However, a preliminary bibliometric analysis resulted in 1,764 keywords. This is a huge number for any researcher to understand, comprehend and provide a structure to understand. Further, to the best of our efforts, few comprehensive studies could be found to help structure the existing literature and identify the trend of present research and future areas of research. It is with this motivation that the present study was undertaken to provide structure to the existing literature on ESG through a bibliometric analysis. The article started by discussing the research question and research methodology for bibliometric analysis.

Growth in ESG Research.

Research Questions

This study used the approach given by previous researchers (Durieux & Gevenois, 2010; Ellili, 2022; Gao et al., 2021; Senadheera et al., 2022; Wan et al., 2023). Based on their approach, this bibliometric analysis is provided by four research questions. These will help in determining the current situation and potential future research directions. These research questions are the following:

RQ1: What is the statistical profile of ESG literature and how it has been addressed in the existing literature? RQ2: What authors, journals, and countries have contributed the most to the research on ESG? RQ3: What are the most frequent keywords and topics of ESG disclosure documents and their evolution over time? RQ4: What are the gaps in the existing literature on ESG and what are the potential research questions for the future?

These research questions will help provide not only structure to existing research literature but also help identify future areas of research, and the following methodology was adopted to meet these objectives.

Literature Review

Due to the ESG field’s rapid expansion, various bibliometric reviews of the ESG concept have been done by academics to offer insights into this field of study. Galletta et al. (2022) conducted a bibliometric examination of ESG-related performance in the context of the banking sector. Similarly, Ellili (2022) used a bibliometric study to investigate the knowledge structure of ESG disclosure. These studies have provided insights into the state of ESG development in a particular industry (such as the banking sector).

Additionally, Gao et al. (2021) and Singh et al. (2022) used a bibliometric technique to provide an overall grasp of the ESG concept in the academic sector, in contrast to the aforementioned review studies. Both researchers suggested that socially responsible investment (SRI) and corporate social responsibility (CSR) were the ancestors of the ESG concept. These two studies used citation analyses to determine how well citations performed in the ESG field. Both citation analysis and co-citation analysis are crucial for a better understanding of citation performance in particular disciplines (Boyack & Klavans, 2010; Kleminski et al., 2022).

Bosi et al. (2022) examined literature on ESG and sustainability reporting over the last 24 years (1998–2022). They have also employed the Gephi technique, version 0.9.5 of bibliometric analysis, and combined the articles in four clusters, i.e., CSR and sustainability reporting, benefits and corporate social responsibility rewards, cost of equity and ESG disclosure and cost of capital and governance in CSR. Other studies (i.e., Diwan & Amarayil Sreeraman, 2023; Senadheera et al., 2022) used the Scopus database for the analysis. Senadheera et al. (2022) revealed that there were fewer specified metrics on governance pillars as compared to the environment and social pillars. On the other hand, Diwan and Amarayil Sreeraman (2023) suggested the need for framework-centric research on Carbon Disclosure Protocol (CDP), Global Reporting Initiative (GRI), Task Force on Climate-related Financial Disclosures (TCFD), and more empirical studies on ESG parameters relating to operational performance.

Saini et al. (2022) conducted a study including both systematic and bibliometric reviews of ESG articles and found that stakeholder, legitimacy, and signalling theories are the foundation for ESG and financial performance. They also found four clusters, namely, “CSR/ESG determinants and firm performance”, “Moderators and Mediators”, “Investors’ perception”, and “CSR in the tourism sector”, as the hottest topic in ESG research. Similarly, both Wan et al. (2023) and Zhao et al. (2023) conducted a bibliometric analysis of ESG literature using the Web of Science database and used CiteSpace and VOSviewer software for the analysis. Jain and Tripathi (2023) conducted bibliometric analysis on ESG research using both Scopus and Web of Science databases and found four intellectual themes, i.e., ESG investing, ESG disclosures and integrated reporting, ESG performance and firm value, and corporate governance and ESG performance. According to their analysis, the impact of ESG on firm value and ESG investment were the prominent themes, and the effect of ESG on the cost of capital and ESG audit and assurance were the emerging themes in this domain. On the other hand, Jain and Tripathi (2022) also conducted a systematic literature review on sustainability reporting for a better understanding of sustainability reporting as a tool of ESG. Studies of Cruz et al. (2023) and Yadav and Saini (2023) are also related to the same area of bibliometric research. Therefore, it can be seen that much research has been conducted to systemiz the ESG literature. However, in the study discussed above, co-citation analysis has been done on the state of ESG research to address the inadequacies of the earlier studies. In contrast, the studies by Gao et al. (2021) and Singh et al. (2022) have also carried out a literature citation analysis to investigate the hottest subjects and trends in the ESG area.

Need and Uniqueness of the Study

A literature review shows that a number of bibliometric studies have been conducted on ESG. However, few comprehensive studies could be found to help structure the existing literature. For example, some bibliometric studies on ESG only conducted citation analysis to evaluate the ESG literature (Gao et al., 2021; Singh et al., 2022). The other studies only used literature and keyword citation analysis to evaluate ESG literature using VOSviewer and CiteSpace (Ellili, 2022; Zhao et al., 2023). Therefore, this study was undertaken by using two different software, i.e., Biblioshiny and VOSviewer for the analysis. Along with this, the study used multiple co-citation analyses (i.e., author co-citation analysis, journal co-citation analysis) and bibliographic coupling (i.e., countries bibliographic coupling). Therefore, this study significantly advances our understanding of the knowledge structures of the ESG field.

Research Methodology

The main objective of this study was to conduct a bibliometric analysis to provide structure to the existing body of ESG literature and to identify gaps and future areas of research. Therefore, an exploratory research design was used. Data were retrieved from the Scopus database. The Scopus database was shortlisted for the study for two reasons. First, the Scopus database is more skewed towards business and management journals as compared to the Web of Science database (Gao et al., 2021; Karafil & Akgul, 2021; Senadheera et al., 2022). Second, Web of Science requires manual operations to export more than 500 papers, whereas the Scopus database helps in the selection of a large number of articles on “ESG”. Therefore, based on the scope of the article and past research, the Scopus database was used for bibliometric analysis in the current study.

Initially, in the bibliometric analysis, four different keywords, i.e., “ESG”, “environment social governance”, “ESG disclosures”, and “ESG reporting”, were used. The keywords “ESG reporting” and “sustainability reporting” are used interchangeably, and similarly “CSR reporting” is also used in this context. However, the searches on the database were limited as the true depth of literature could not be mined. Therefore, only two very broad keywords, i.e., “ESG” or “environment social governance”, were used. Also, using these two broad keywords resulted in papers related to sustainability. The search extracted a total of 6,598 documents spanning the period from 2008 to 2022 (Table 1). The retrieval procedure is as follows: (title-abs-key (“ESG”) or title-abs-key (“environment, social and governance”)) and (limit-to (doctype, “ar”)) and (limit-to (subjarea, “busi”) or limit-to (subjarea, “econ”) or limit-to (subjarea, “soci”)) and limit-to (language, “English”).

To further refine the search, three in-built filters were used, i.e., “type of source”, “type of publication” and “language”. The first filter, i.e., “type of source”, was used to shortlist only “articles” from the list of 6,598 results. This was done based on past research, which indicated that open-access articles are the most reliable source. The second filter, i.e., “type of publication”, was used to select only “business, management & accounting” and “social sciences”, as these journals were highly rich in “ESG” literature as compared to other journals like “engineering” and “economics”. The third filter, i.e., “language”, was used to select only “English” articles as these are easily understandable.

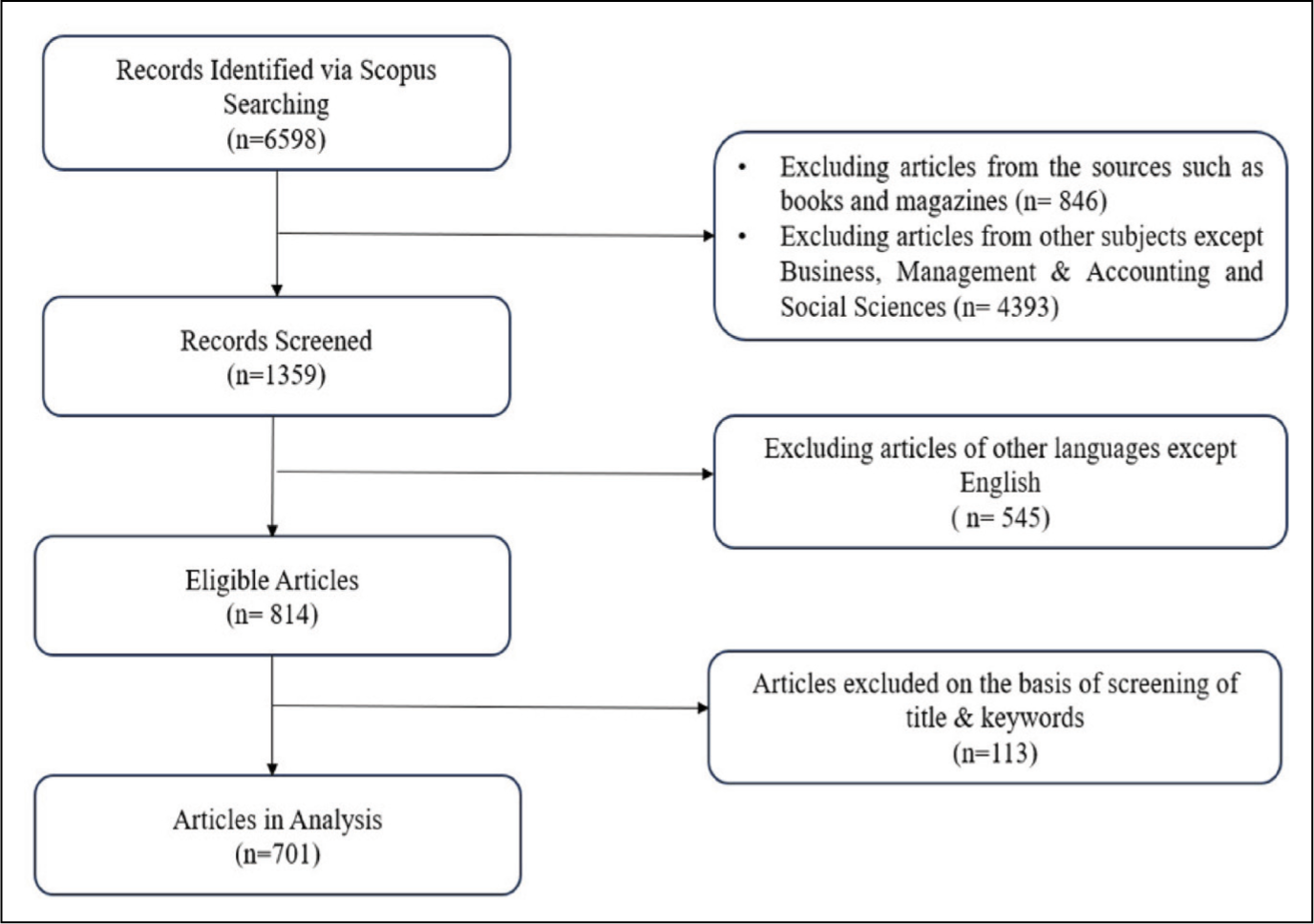

The PRISMA flow diagram of screening the articles is presented in Figure 2. The first filter reduced 846 articles and refined the search to 5,752 articles. The second filter resulted in 1,359 articles by removing 4,393 articles from other subjects except business, management and accounting, and social sciences. The third filter reduced the articles to 814. After the screening of the title and keywords of the articles, the final number of articles selected for the bibliometric analysis was 701 (Figure 2). Therefore, analysis in the current paper has been done on the 701 papers.

PRISMA Flow Diagram.

Indicators/Software and Technique

In order to conduct a bibliometric analysis of 701 articles, the methodology given in previous studies (Durieux & Gevenois, 2010; Ellili, 2022; Gao et al., 2021; Senadheera et al., 2022; Wan et al., 2023) was adopted, where performance analysis and science mapping were undertaken. The methodology for conducting a bibliometric study was based on the method by Durieux and Gevenois (2010). The study has used both Biblioshiny and VOSviewer for the analysis. Also, the study used multiple co-citation analyses (i.e., author co-citation analysis, sources co-citation analysis, and co-occurrence of keywords) and bibliographic coupling (countries bibliographic coupling) for analysing ESG articles.

Results

Before analysing the 701 articles in depth, a preliminary analysis to generate a descriptive summary of the article published was conducted. These 701 research articles (documents) were published in 221 journals over approximately 15 years (from 2008 to 2022). The results indicated that 1,670 authors were working in the area of ESG globally. Furthermore, out of the 701 documents, only 104 (14.83%) were single-authored, indicating that a major trend in the ESG field was co-authored papers belonging to multi-disciplinary approach in “business, management & accounting” and “social sciences”. Furthermore, the analysis indicated that the average number of citations per document was 15.81.

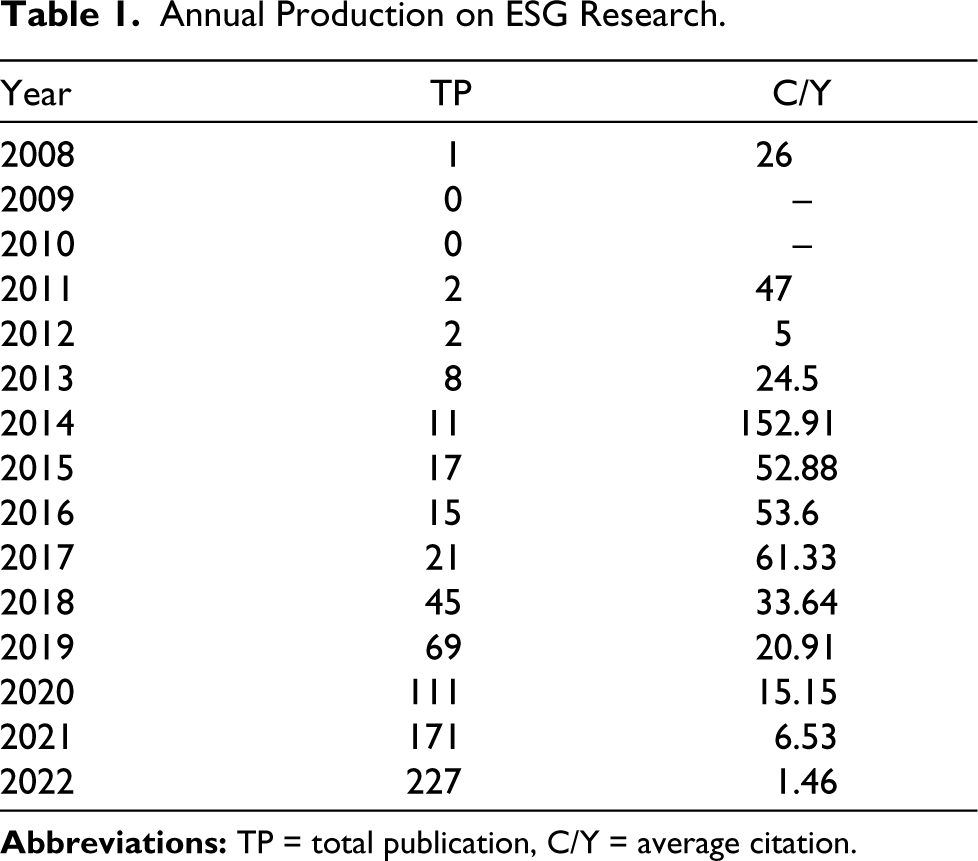

Annual Production on ESG Research

An annual production of ESG papers indicated that the research on ESG gained momentum after 2011 (Table 1). However, in 2018, there was a surge in publications on this topic, and the number of ESG papers increased from 45 in 2018 to 227 in 2022 (Table 1). Therefore, though the ESG term was first used by the United Nations Global Compact and the Swiss Federal Department of Foreign Affairs in 2004, it was after 2018 that the research in this area picked up yet the field of ESG research is in the nascent stages of development.

Annual Production on ESG Research.

Table 1 shows that the works published between 2020 and 2022 received the greatest citations. Only 8.70% of the papers have 50 or more citations, while only 33.67% have 10 or more. In addition, 90.89% of the papers on ESG have received at least one citation.

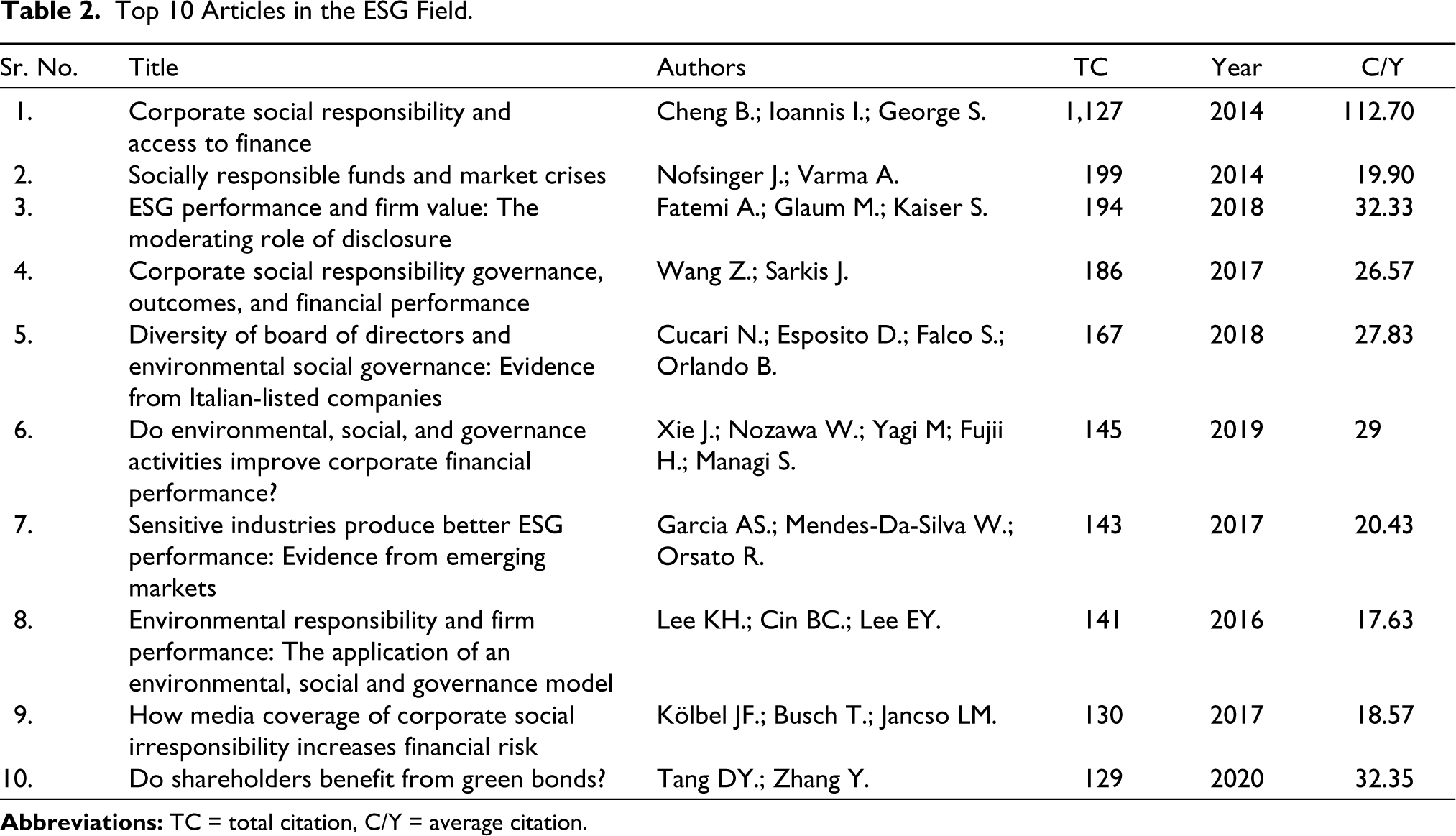

Top 10 Articles in the ESG Field.

Most Productive Articles in ESG Research

An analysis identifies the key authors and articles contributing to ESG research. Table 2 lists the 10 highly cited papers from 2008 to 2022. The most highly cited paper was written by author Cheng B. in 2014, who identifies the role of CSR in the access to finance by the organization, which in turn is helpful for the growth and profitability of the business. The total number of citations received by author Cheng B. is 1,127. The second most cited paper belongs to Nofsinger and Varma, who compared conventional mutual funds with socially responsible mutual funds and found that companies implementing socially responsible investing strategies in mutual fund management are less risky in the market crisis period.

Additionally, the citation structure was classified and counted from 2008 to 2022. There are highly cited papers almost every year, but the publications published in 2014 were the most cited (C/Y = 112.70). Out of the total papers, 11.09% have received more than 100 citations. 44.17 % of the papers received more than 10 citations and 93% received at least 1 citation.

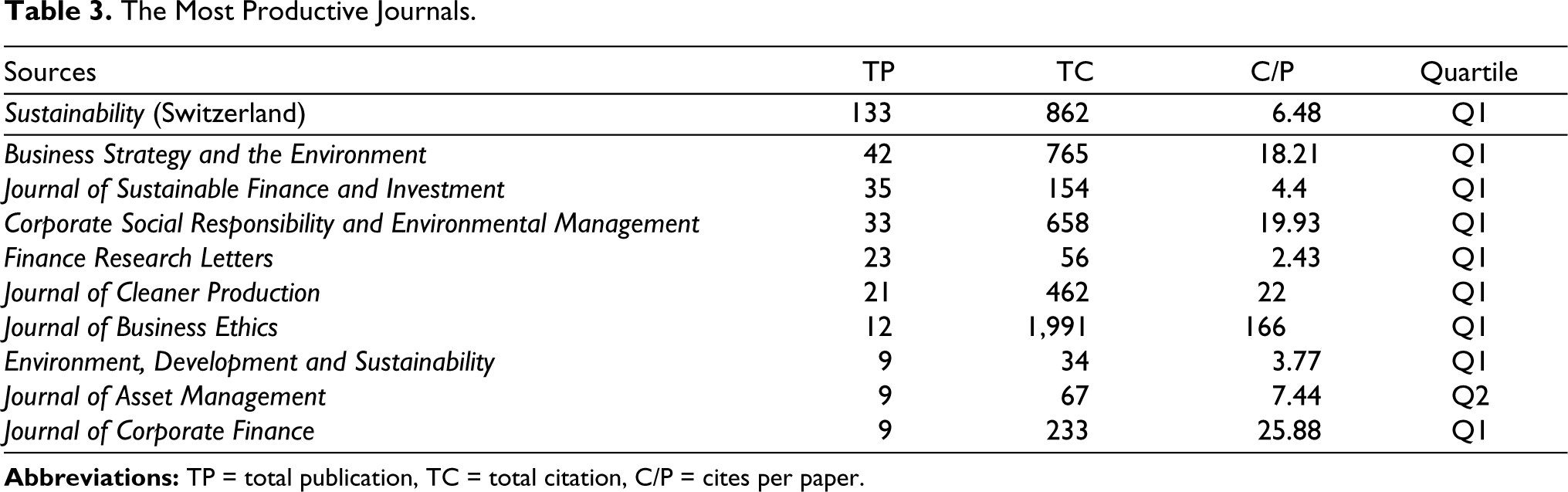

Most Productive Journals in ESG Research

The descriptive summary related to journal-wise distribution of articles was generated to find the most productive journal in the area of ESG research. All the journals were categorized based on Q1, Q2, Q3, and Q4 quartiles of the Scopus database. The quartile of the journal is determined on the basis of its impact factor or CiteScore, which reflects how many times articles from that journal have been cited in other scientific publications over a certain period. It was found that 64% of the articles (448) belong to the journal of Q1 category, indicating the most prestigious journals in the ESG field with the highest number of citations. Similarly, Q2 covers 19%, and Q3 includes 13% (91) of the total articles. On the other hand, Q4 includes journals with lower impact factors and those that have recently been included in the database. In our sample, only 4% of the total articles fall in the Q4 journal category. It shows that 80% of the articles in the bibliometric analysis belong to a highly influential publication. This would help the new researchers to find out the most relevant journals for ESG literature.

Out of these high-impact journals, the top journals that were found to be published in the area of ESG were Sustainability (133) and Business Strategy and the Environment (42). The ratio of the top 10 cited journals to the total number of papers was 46.50%. All the top 10 journals belong to the Q1 and Q2 categories of Scopus as well as showing highly influential publications (Table 3).

The citation of the journals was also analysed. The journals with the most cited articles are Journal of Business Ethics (1991) and Sustainability (862), indicating the leading position of these journals in the area of ESG research (Table 3). The citations of the top 10 journals accounted for 67.08% of the total citations.

The Most Productive Journals.

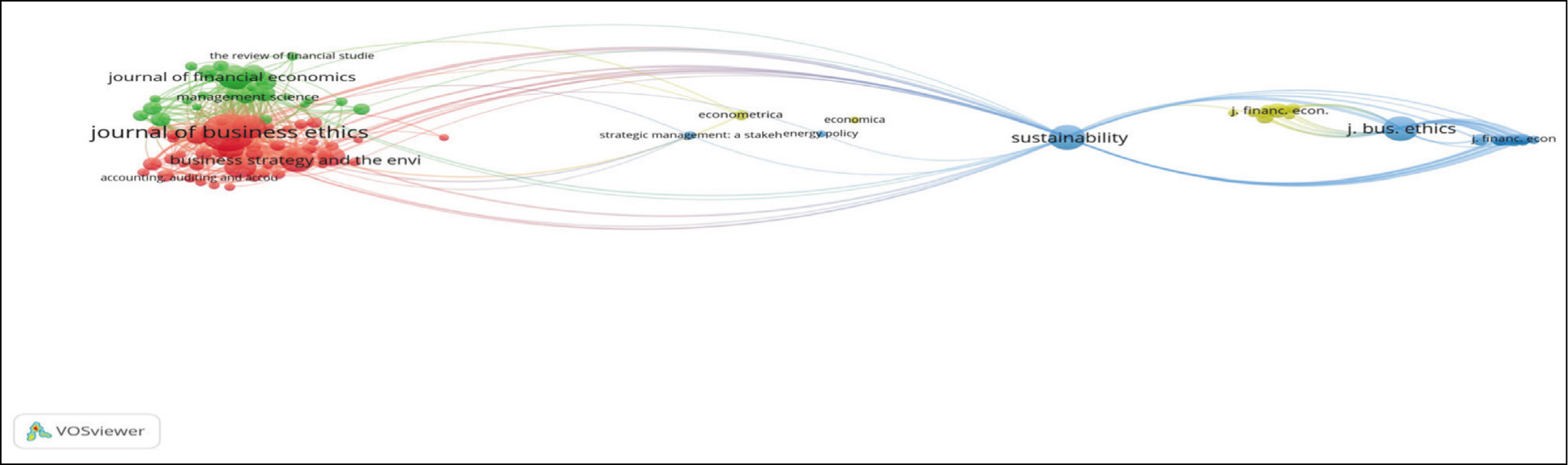

To further examine the relation between the journals, co-citation analysis of the referenced sources has been done using the VOSviewer software. The co-citation network of cited sources is shown in Figure 3. A total of 108 records meet the threshold out of 11,225 sources, satisfying the criterion when the minimum number of citations for each source is equal to 50. Similar-coloured nodes in Figure 3 belong to the same cluster.

Journal Co-citation Analysis.

The number of citations per document is shown by the area of each node. A larger node indicates a higher number of citations. The documents published in the Journal of Business Ethics, Corporate Social Responsibility and the Environment Management, Business Strategy and the Environment have the highest number of co-citations, as shown in Figure 3, indicating that the journal with the highest publication and citation also has the highest co-citation, thus indicating influential sources of ESG-themed papers.

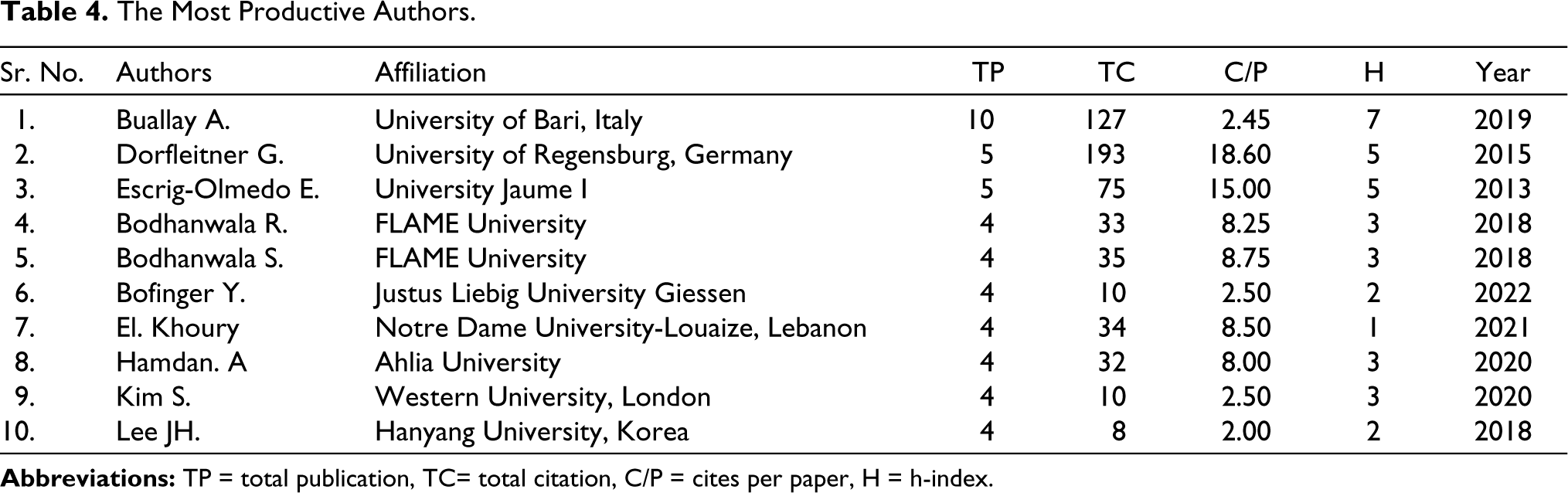

Most Productive Authors

The study also analysed the most relevant authors in the ESG field. From Table 4, it can be seen that Bullay A. is the most influential author with 10 publications. An analysis of Scopus data reveals that his first paper, “Between cost and value: Examining the implications of sustainability reporting on a firm’s performance” was published in the Journal of Applied Accounting Research in 2019. The impact of Bullay A. on the ESG field in just three years is amazing. He mainly discusses sustainability reporting and how it relates to financial performance in the banking, tourism, and agriculture industries. However, because of his recent entry into the field of ESG research, he is not the most influential (TC = 127).

The Most Productive Authors.

In second place for highest publication and the highest citations is author Dorfleitner G. from the University of Regensburg, Germany. He has published five papers and has received 193 citations in total. In 2015, the Review of Financial Economics published his first article titled “The wages of social responsibility: Where are they? A critical review of ESG investing” (Halbritter & Dorfleitner, 2015). It has received 170 citations in total, which is the highest among all his publications. He had mainly studied areas such as ESG investing, CSR, and financial performance and risk of CSR. The list also shows some other authors having high C/P such as Escrig-Olmedo E. (15.00) and Bodhanwala S. (8.75). Also, the authors having the highest publications also have high h-index such as Bullay A. (h = 7) and Dorfleitner G. (h = 5). Therefore, in general, interestingly, the most productive authors are also the most influential. It can be inferred that the majority of the productive and impactful authors have been active for comparatively more years.

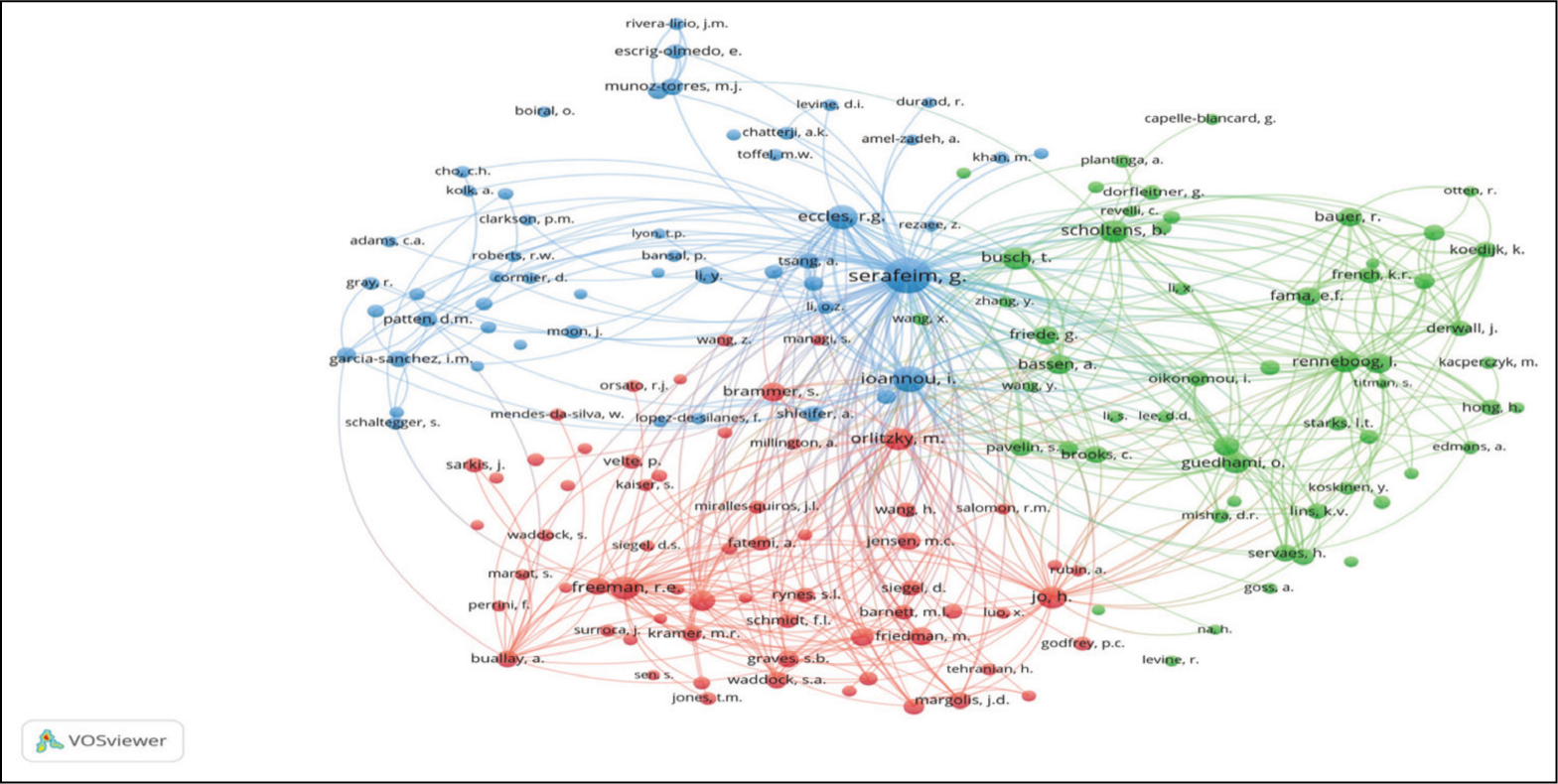

Authors’ Co-citation Analysis.

Author’s Co-citation Analysis

To further examine the relationship between the authors, the co-citation network of cited authors has been done using VOSviewer and is shown in Figure 4. The cluster shows 170 cited authors with at least 50 citations out of 32,194 cited authors. Figure 4 shows the most common clusters in red, green, and blue. The authors Serafime, Ioannou, and Eccles are placed together in the blue cluster, signifying that they conducted research in the same related field of study. The most well-known authors working on similar topics in the green cluster were Renneboog, Scholten, and Bush, whereas the most frequently mentioned authors in the red cluster were Freeman, Brammer, and Orlitzky, indicating working on similar themes related to ESG research. Importantly, the co-citation analysis shows different influential authors in ESG themes as compared to authors with the highest publications and citations.

Most Influential Universities in ESG

Table 5 lists the top 10 universities where the most influential productions have been published. As shown, Sapienza University of Rome was ranked first, with 24 publications, followed by Ahlia University, with 21 publications. Even if the other universities such as the Brno University of Technology, University Utara Malaysia, and University Jaume I are ranked low, they have the publication of 12 articles each.

Most Influential Countries in ESG

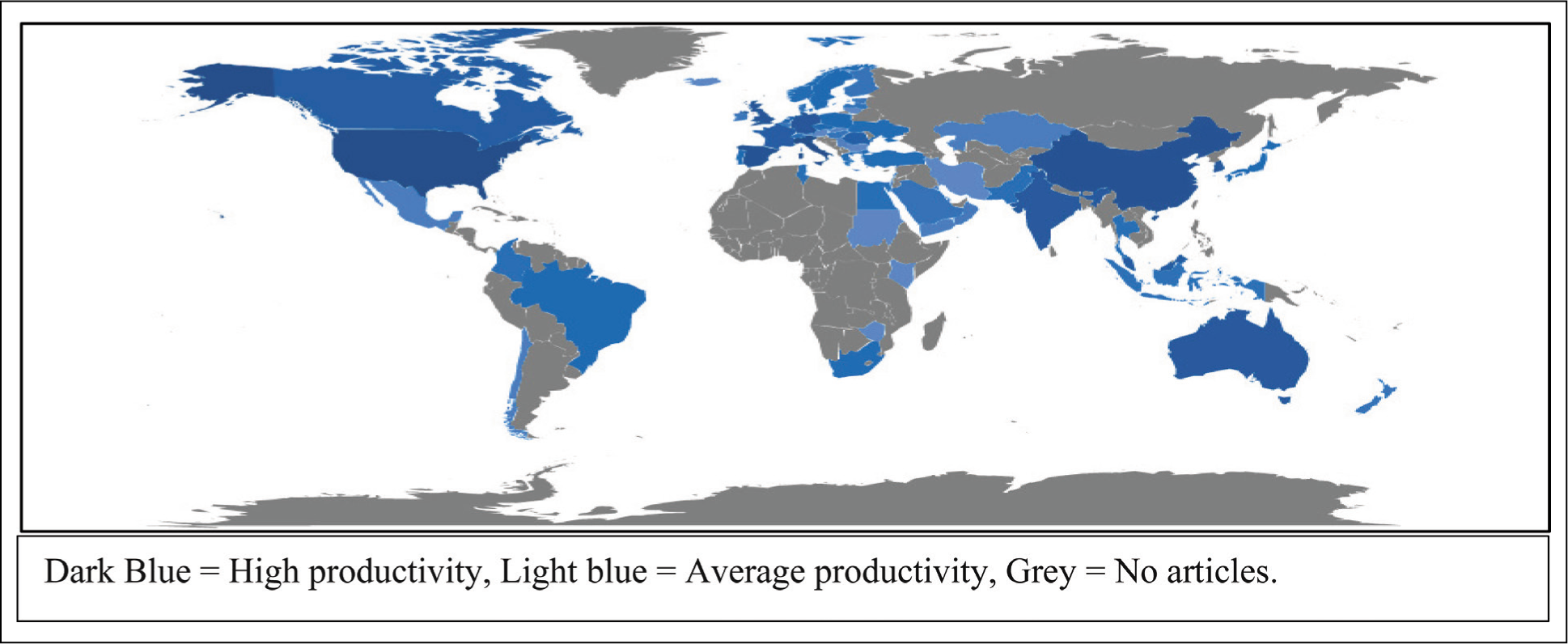

In the next step of bibliometric analysis, the papers were analysed for the most influential countries of research. This was done not only to identify the countries which were leading the ESG research and ESG policymaking but also to identify the countries which had a higher degree of awareness of ESG responsibilities. The analysis indicated that the research was skewed towards a few selected countries. The majority of the studies in ESG have been conducted in the United States, i.e., 205 articles followed by Italy (193 articles), China (134 articles), Spain (128 articles), and the United Kingdom (111 articles), which are mostly developed countries. In the case of emerging economies, i.e., developing countries such as South Korea (81 articles), India (80 articles), Japan (20 articles), and Indonesia (11 articles), the research on ESG was found to be average (Figure 5).

The Most Influential Universities in ESG.

Figure 5 shows that, although both developed and developing countries have published ESG-themed research papers, the publications are more skewed towards developed countries. The analysis of selected articles also indicated that there are many countries (Russia, Mongolia, Peru, Argentina, Bolivia, Chile, Denmark, Nigeria, Nepal, Bhutan, and Myanmar) where few works on ESG has been done. It may or may not be true because of the methodological limitation because articles are selected based on keywords. Therefore, it indicates that some cross-comparison and cultural studies would be helpful in providing future areas of research.

Leading Countries in ESG Research.

Interestingly, a manual review of 709 articles indicated that out of 709 documents, only 56 were related to cross-country comparison, and these too were between developed and developing nations. A plausible reason for lower cross-cultural study is the difference in ESG norms in different countries, thereby making it difficult to compare the ESG norms. The review indicated that most of the research from Asia Pacific, Canada, Europe, Latin America, the Middle East, the United States, and Africa mainly use GRI and Sustainability Accounting Standards Board (SASB), while countries like the United Kingdom and Hong Kong use the CDP, and recommendations of the TCFD for ESG, which mainly focus only on environment norms. Therefore, these differential ESG norms indicated that (i) cross- cultural studies were possible within a cluster using similar norms. (ii) There was a need for a standardization of the norms for research purposes globally.

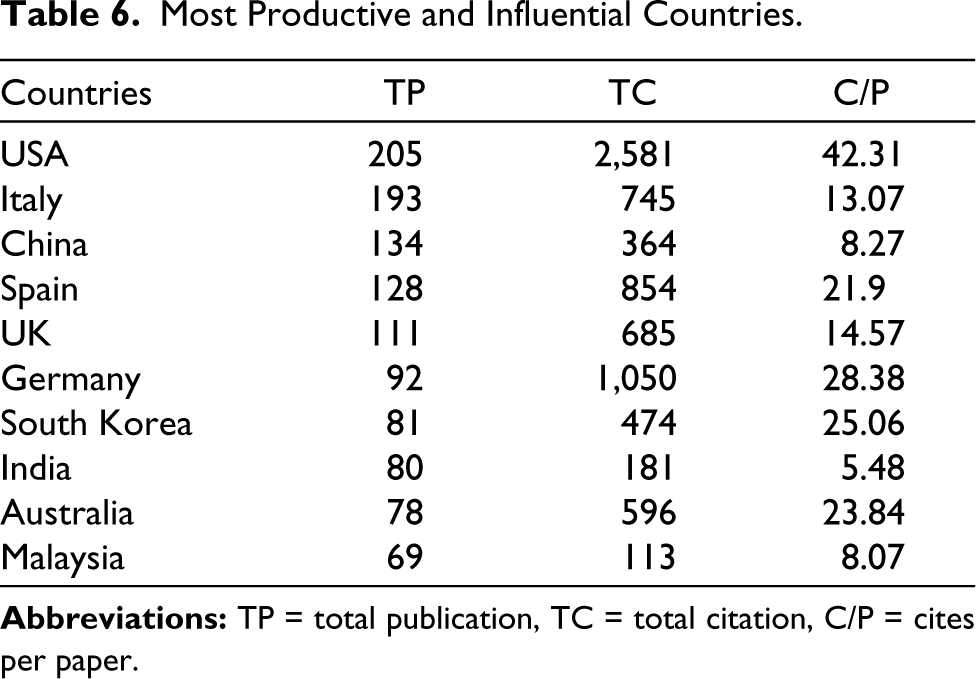

To further analyse the research by the most influential countries, the citation of the papers was analysed. Citations affect the research’s influence on other researchers. Data indicated that the citations for the US research were highest at 2,581 (Table 6) with an average of 42.31 citations per paper. Other countries such as Germany (1050), Spain (854), Italy (745), and the United Kingdom (685), were also indicated higher citations, indicating a higher relevance and quality of research. To further understand the research relevance and quality of research to help other researchers, a collaborative and thematic analysis was conducted on shortlisted papers.

As the citations for research from a few countries were higher, an attempt was made to understand the reason and similarity of research among the countries. Therefore, in the first step, a collaborative analysis was done, where clusters are made on the basis of the bibliographic coupling of the countries.

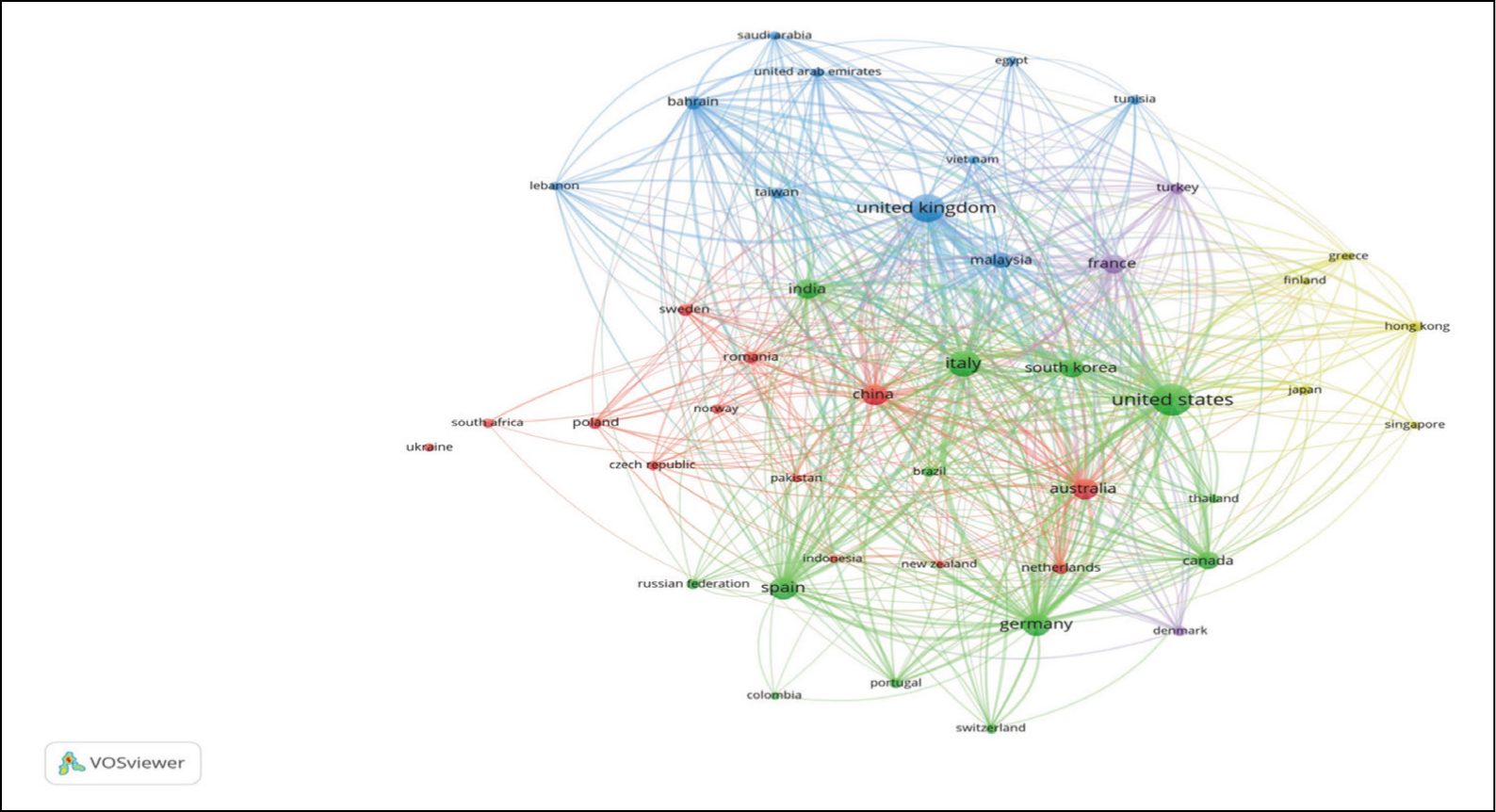

Bibliographic Coupling of Countries

As mentioned above, the bibliographic coupling of countries has been conducted to explore the similarities of research in different countries. It also helps to understand how other countries use similar literature in their publications and focus on a similar point. Figure 6 shows that countries such as the United States, Germany, Italy, Spain, and India are working on similar research themes. Similarly, the United Kingdom, Malaysia, Bahrain, Lebanon, and Egypt are working on the same issue. The results indicated that most studies originating from the United States were collaborative studies, with researchers from Germany, Italy, Spain, and India indicating the possibility of a cross-disciplinary approach benefitting the research quality.

Most Productive and Influential Countries.

Authors Keyword Analysis

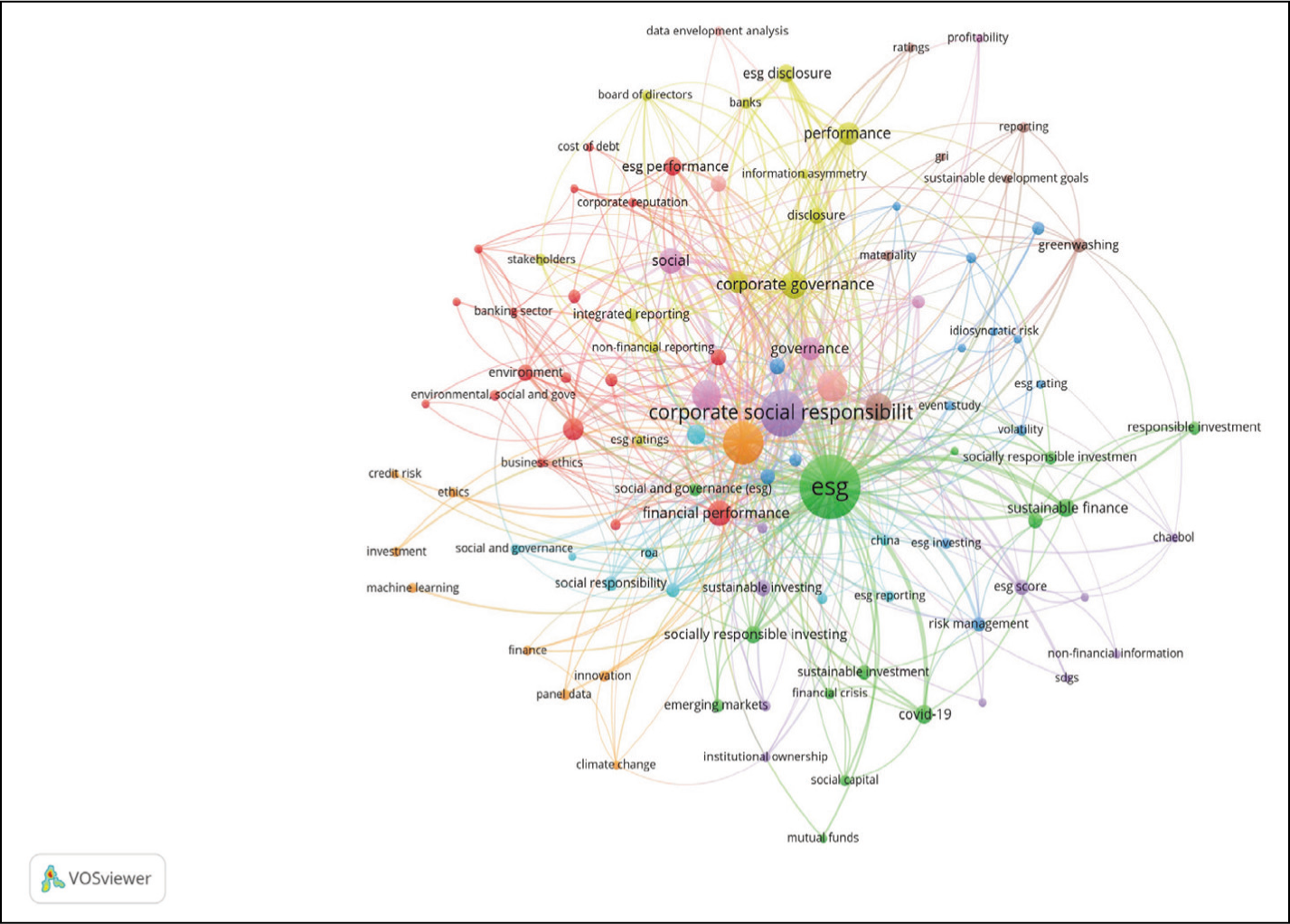

In the second step to understand the research literature and quality of research coming out of different countries, a thematic analysis based on the author’s keywords in different countries was done. This would help in identifying the most relevant themes in the ESG area, which helps in higher citation as well as quality of the papers. Using VOSviewer, a co-occurrence analysis of the author keywords was conducted to visualize the keywords (Figure 7). There were a total of 1,764 keywords, out of which only 102 met the threshold when the minimum occurrence of keyword limit was set to 5. According to the analysis, the term “ESG” occurred 386 times, while “corporate social responsibility” occurred 179 times. Furthermore, the term “sustainability” occurred most frequently in the 153 documents.

Collaboration Network of Countries.

Figure 7 shows six important co-occurrences in six different colours. The two major co-occurrences are around the concepts of ESG in green and CSR in purple. The keywords ESG and CSR have a large number of related minor concepts or themes. For example, as seen in Figure 7, ESG is linked mainly with sustainable finance, sustainable responsible investing, and terms such as social and environment. However, no link was found between ESG and governance. Similarly, CSR is mainly related to ESG performance and disclosure, indicating a large number of studies on this theme. Another important keyword, i.e., sustainability, is shown in orange. Furthermore, there are two minor themes: one in red, about ESG performance, and one in yellow, involving corporate governance that almost acts as an emerging concept in the literature.

Co-occurrence of Author’s Keywords.

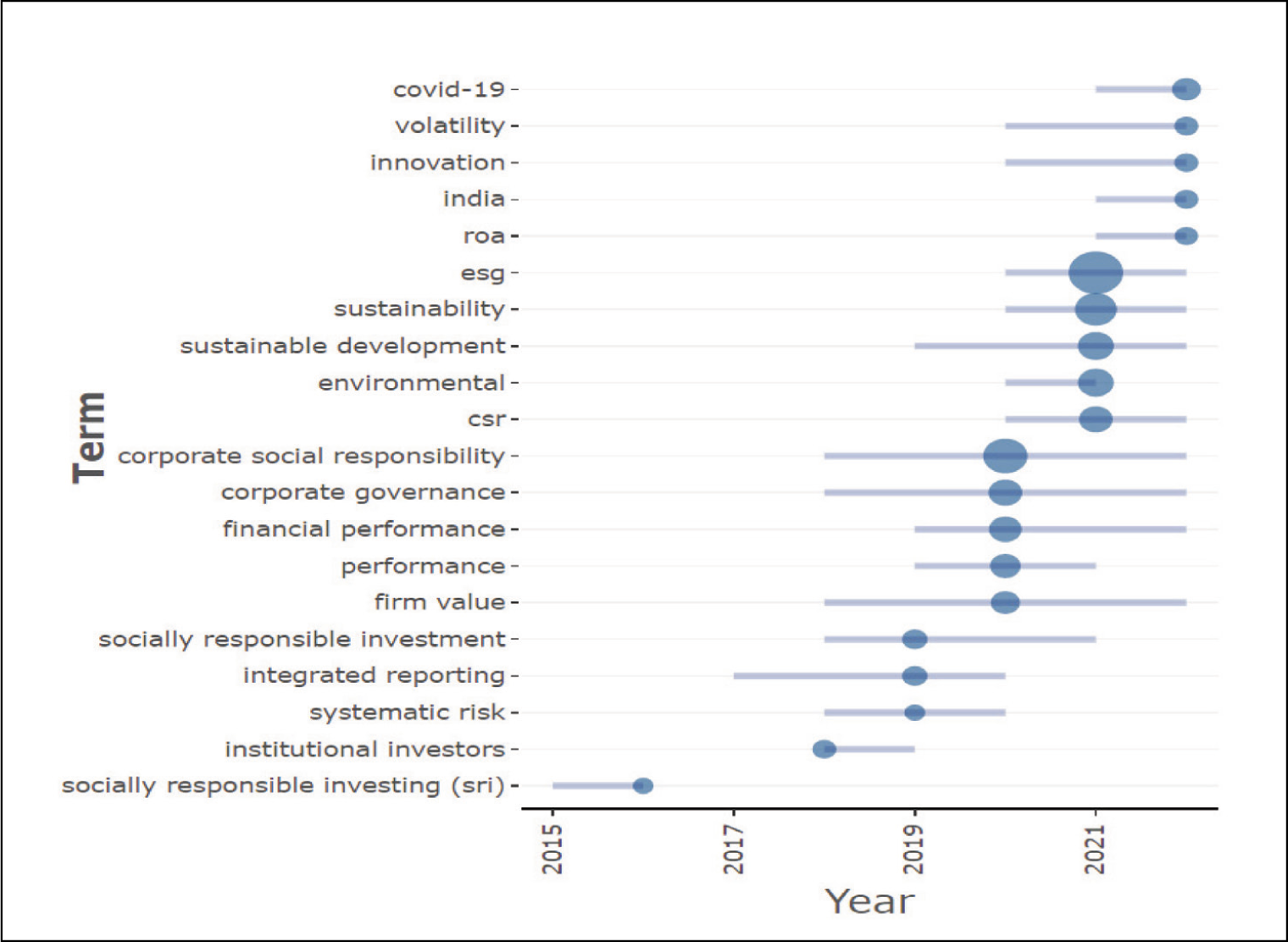

In the third step, the trend in the author’s keywords used throughout the time was analysed. This was done to identify the period of relevance of different keywords in ESG literature. Along with thematic mapping, this keyword trend analysis would help in forecasting future keyword trends for ESG research.

Similar to other descriptive, the analysis of the author’s keywords trend highlighted that the ESG research was stagnant from 2008 to 2015 (Figure 8). Extensive research in the field of ESG accelerated from 2015 onwards with the paper “Should Islamic investors consider SRI criteria in their investment strategies?” by Erragraguy and Revelli in 2015, published in the Finance Research Letters. From 2015 to 2018, institutional investors and socially responsible investing were trending a lot in ESG research. In 2019, SRI, integrated reporting, and systematic risk, were among the study topics of interest. In 2020, papers on CSR, corporate governance, and firm value were published in high volume. At present, sustainable development, sustainability, ESG, COVID-19, and volatility were the main keywords/hot topic of research as the COVID-19 pandemic sensitized the management and academician regarding the impact of COVID-19 on the company’s sustainability. Therefore, researchers should try to collaborate current trends with ESG for publishing and in ESG areas.

Thematic mapping

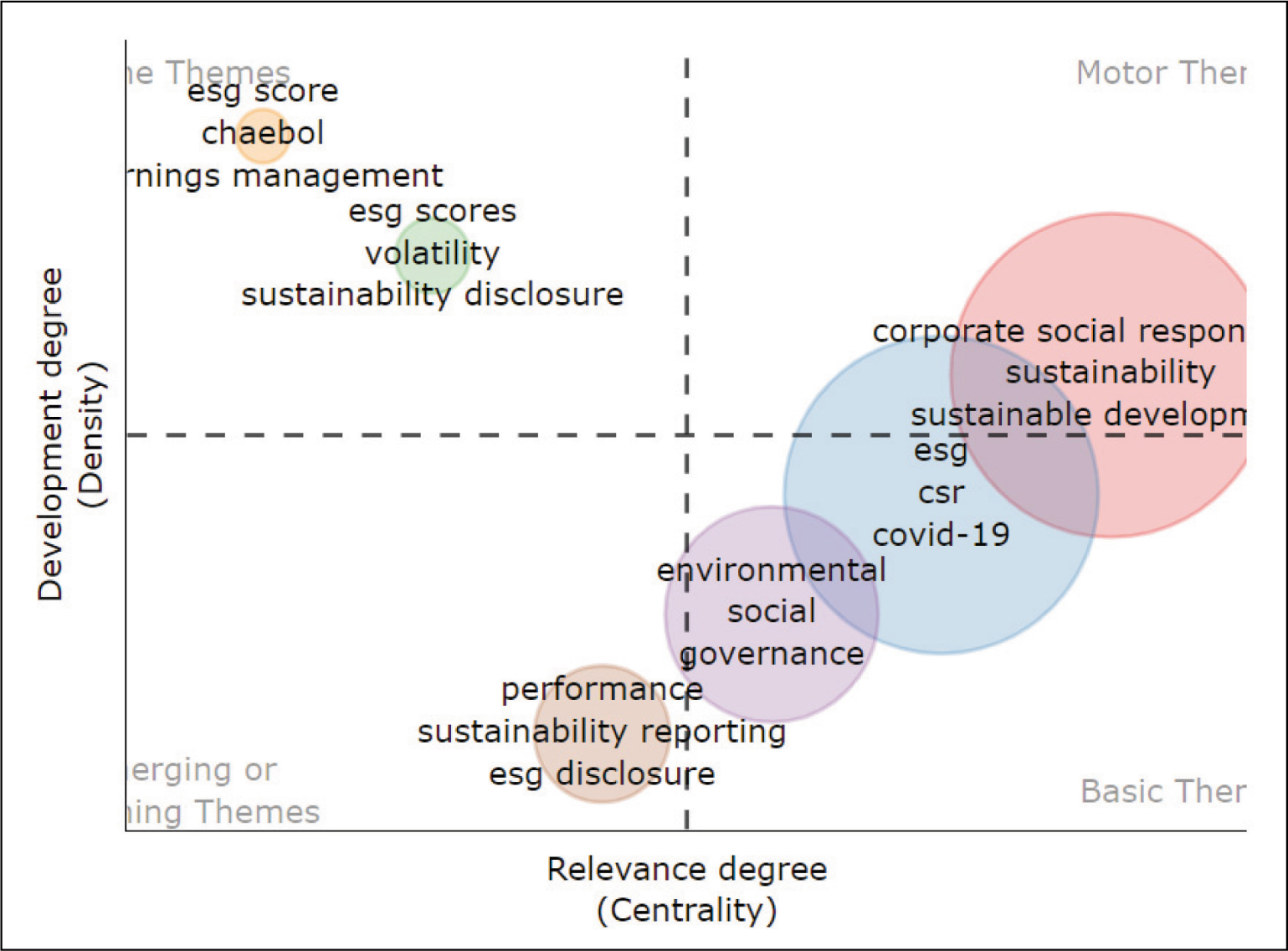

After keyword analysis, following the methodology of previous studies (Bosi et al., 2022; Diwan et al., 2023; Gao et al., 2021; Saini et al., 2022; Senadheera et al., 2022; Zhao et al., 2023), thematic mapping was done to identify general, niche, and emerging themes in textual data of ESG literature. This would help the researchers to identify the gap in ESG literature and areas for future direction. The thematic mapping presented in Figure 9 has been done based on the author’s keywords.

Themes of ESG Research.

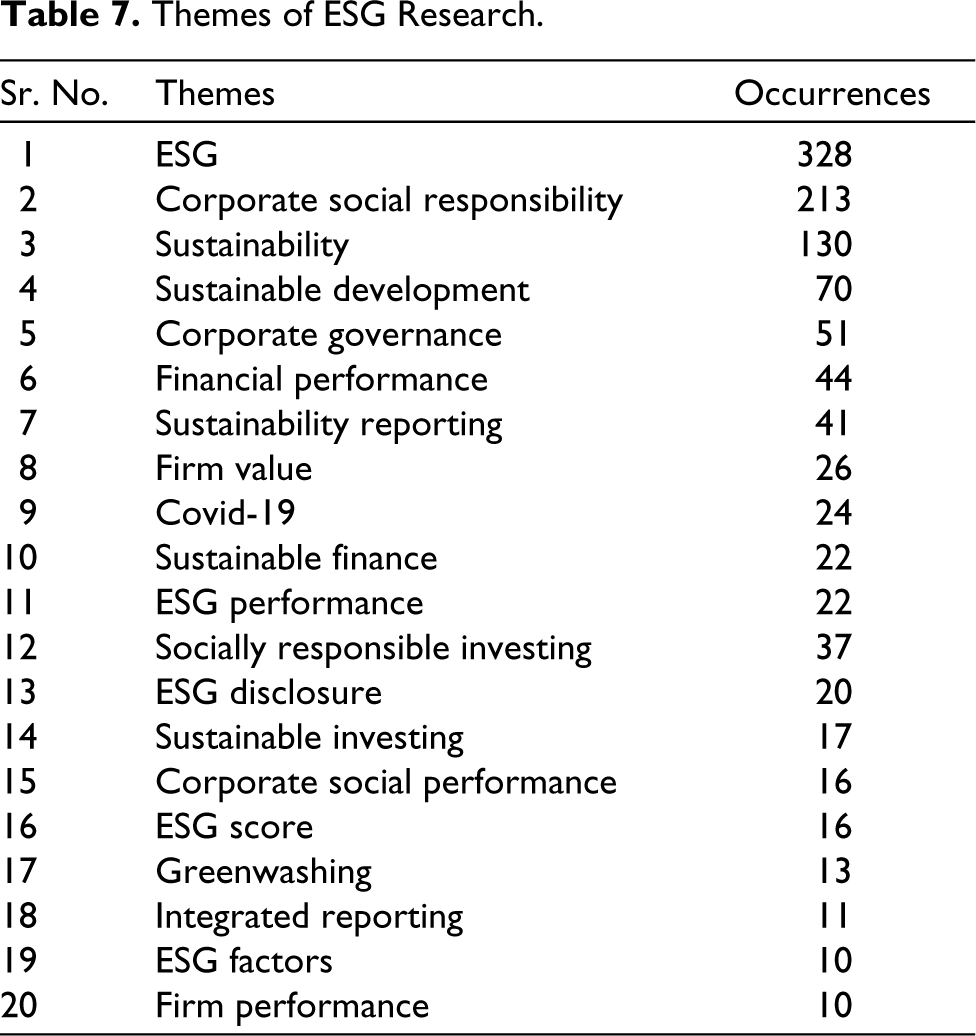

However, few terms have been used by different researchers differently, i.e., some researchers have used CSR whereas some have used CSR to denote CSR activities. It resulted in the falling of the same theme in different quadrants. To overcome this problem, a table is prepared to show the different themes with their number of repetitions, and then the same theme is clubbed together. Therefore, in the analysis part, it is taken care of and the themes with the highest number of repetitions are explained in their quadrant, respectively. Table 7 is presented to show the repetition of themes.

Table 7 represents the emerging themes in ESG research. CSR has been the most researched area, whereas greenwashing, integrated reporting and earnings management are the least researched themes. It shows the frequency of each theme in the ESG literature.

Future Research Directions

Based on overall publication metrics and thematic mapping, the study proposes the future scope of research in ESG as follows:

The most recent development in the field of standardization of ESG norms is Value Reporting Foundation (VRF). VRF is in collaboration with the GRI working to create a new standard that will combine both IIRC and SASB frameworks. On the other hand, the International Sustainability Standards Board builds on the work of market-led investor-focused reporting initiatives, including CDSB, TCFD, the VRF’s Integrated Reporting Framework, and industry-based SASB standards, as well as the WEF Stakeholder Capitalism Metrics. It all indicates that there is no one uniform way of ESG reporting, and at present, every country is following its customized methodology of reporting. Even if various initiatives are taken to standardize the ESG disclosures, they are still in the process and the countries follow the different standards as per their need and requirements. Therefore, the lack of cross-cultural studies highlighted that there is a need for a standardization of the norms for research purposes globally. Further, future research can explore the costs and benefits of developing a single, global ESG assurance framework. Much research has already been conducted on ESG and firm performance, but it is regardless of the industry. Therefore, this area can be looked at for future research in different industries along with cross-comparison of different industries in one country as well as among different countries. For example, most studies on ESG disclosure consider listed companies in different financial markets. It would be interesting to include other types of organizations (such as family businesses and small and medium enterprises) as well as other types of industries (such as education, tourism, and real estate). Also, most of the previous studies have investigated the direct relationships between ESG disclosure and other corporate and financial aspects, while few studies have taken it as a moderating and mediating variable. Therefore, it would be interesting to analyse the moderating role that ESG disclosure can play in other relationships, such as the relationship between corporate governance and financial performance. Future research should also focus on examining the connections between the environmental (E) and social (S) dimensions, enhancing the interaction between the environmental (E) and governance (G) dimensions, and highlighting the significance of each dimension separately in business financial performance. In addition, new environmental and social dimensions of ESG performance need to be identified. However, while the governance (G) dimension is the emphasis of ESG research, there are not many studies that look at how it affects economic outcomes. In the future, we should further explore the research of governance (G) regarding the impact of ESG on economic consequences.

One of the emerging themes in the ESG literature is ESG ratings. ESG rating agencies, such as Bloomberg, MSCI, and Sustainability Analytics, compile publicly accessible ESG data, analyse it thoroughly and uniquely, and assign an ESG score to the organization. However, till now, different ratings provided by different agencies have been taken into consideration for analysis, which makes the result incomparable. Future studies can look into standardizing the scoring criteria (Senadheera et al., 2022). Studies can be done to develop a better understanding of the utility of ESG information by retail and institutional investors and stakeholders. There is a need to explore ESG beyond the regulatory issue and unearth the different aspects of risk–return and investment preferences of retail and institutional investors from developed and emerging economies. Future research can be carried out to identify the effect of company digitization on ESG adoption. Furthermore, future studies can also analyse how ESG performance adoption by businesses affects their eligibility for government credit rationing.

From the analysis, it can be seen that ESG is an important factor affecting the investment and return of the businesses. Therefore, the importance of ESG in the process of sustainable development should be explored from a more specific and detailed perspective in future research.

Conclusion and Discussion

The discipline of ESG research has expanded quickly over the past 15 years and produced many significant study findings. Therefore, in this study, bibliometric analyses have been done to present the publication metrics of existing ESG literature, their collaboration status, hot areas, and trends of ESG research as well as to identify the future research gap.

First, the annual production of the ESG literature was analysed. From 2008 through 2022, a large number of ESG articles were published and a steep increase in the ESG literature was seen after 2018. The main reason for this growth is the trend of sustainability around the world. In terms of countries, the United States, Italy and Spain are the top three countries contributing to the ESG research. Out of the top 10 countries, most of them are developed nations, indicating higher trends of ESG in those countries. Developing nations should also focus on ESG concerns as environmental and CSR aspects spread around the globe. Second, in terms of authors, Bually A. and Dorfleitner G. are the authors with the most articles, making them the main contributors to ESG research. In terms of journals, Sustainability (Switzerland) (133) and Business Strategy and Environment (42) are the top publications that have an interest in ESG themes.

Literature review shows that existing ESG hot topics include ESG, CSR and sustainable reporting. The current research hotspots in ESG literature are ESG disclosure, ESG ratings and the relation of ESG performance to ESG investing volatility and ESG’s role in earnings management. This article evaluates the study outcomes and trends for ESG while summarizing the previous published research and conclusions. On the one hand, this research can offer direction to researchers who are unfamiliar with the subject, allowing them to quickly obtain crucial and necessary information and develop a basic understanding of it; on the other hand, this article can organize the body of literature for researchers who have already begun their own ESG research and increase the effectiveness of their scientific research. In the end, our research provides additional insights for companies and investors to effectively engage with productive and influential institutions or academics in the ESG field to help develop more effective ESG strategies.

Limitations of the Study

Despite various implications, this paper has several drawbacks. First, the study’s data have been retrieved from the Scopus database only. In the future, bibliographic information can be extracted from other databases like the Web of Science. Second, the terms of the search results often contain comparable duplicate data, such as the same keyword used in both the single and plural or the usage of hyphens in the same compound phrase, which somewhat compromises the validity of the findings. Therefore, future studies should also use various retrieval techniques, such as more related searches. Third, this study focused solely on open-source articles. Thus, other forms of publications, such as conference reviews and book chapters, were excluded, which may be an important source.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.