Abstract

This research examines the effect of digital orientation on firm performance within the framework of organizational orientation theory. Focusing on a sample of Malaysian listed companies from 2012 to 2019, we employed robust panel regression alongside dynamic generalized method of moments panel and panel quantile regression models as supplementary analyses. The digital orientation was evaluated using Python-based text analysis. Surprisingly, our findings challenge conventional wisdom: Contrary to expectations, digital orientation exhibited no significant influence on firm performance metrics such as returns on assets, returns on equity and Tobin’s Q. This contradicts organizational orientation theory, suggesting that transitioning towards digitalization might not inherently enhance performance. Our study argues that adopting digitalized business practices may not ensure improved firm performance, particularly in emerging economies like Malaysia.

Introduction

Driven by the development of digital technologies, companies are locked in a cutthroat race to keep up with the competition by adapting their businesses to digitalization. Applying digital technologies, such as the Internet of Things, Big Data, Cloud Computing, Blockchains and Robotic Operation, facilitates the business process and affects the companies’ business dynamics. To stay ahead, they must embrace a digital-first ethos, reimagining their operations and processes for the digital age. Companies are forced to change their orientation to embrace digitalization (Matt et al., 2022; Urbach & Röglinger, 2018), which is famously known as digital orientation (DO). Yet, the pursuit has double-edged swords. On the one hand, several research findings show that revolutionary innovation, like digitalization, is a positive long-run investment for a firm (Nwankpa & Roumani, 2016; Westerman et al., 2012). On the other hand, it reminds us of the dot-com bubble, where intensive revolutionary innovation might result in financial distress (Bughin & Zeebroeck, 2017).

The government also encourages this DO. For example, under the Malaysian Twelfth National Plan, Malaysian companies are encouraged to pursue digitalization. Intriguingly, empirical research on the impact of DO on firm performance is rarely found, with notable studies emerging from developed countries (e.g., Jardak & Hamad, 2022). It leaves a significant research gap in understanding the performance of DO, particularly within the context of emerging countries, like Malaysia.

We built the argument based on the organizational orientation theoretical standpoint, positing firm orientation is crucial for firm performance (Kindermann et al., 2021; Tortorella et al., 2019). Imposing DO encourages companies to increase their operational agility (Lee et al., 2015) and boost their decision-making efficiency (Li et al., 2022). With a DO, companies can quickly respond to economic and market changes by utilizing real-time information and increasing production efficiency (Lai et al., 2023). It helps companies handle external challenges and uncertainties better, lowering their chances of financial difficulties (Kohtamäki et al., 2020; Li et al., 2022). Furthermore, DO reduces the information asymmetry between companies and the market (Wu et al., 2021), reducing their cost of financing.

Conversely, the proponents of the innovator dilemma (Nasiri et al., 2022; You & Brahmana, 2023) argue that when companies do pursue innovation, it may not always lead to immediate financial success and can sometimes even harm their current performance. Although a DO is thought to boost revenue, many companies have difficulty leveraging its potential and fail to achieve the anticipated revenue growth (Gebauer et al., 2020). Hence, would DO really enhance performance empirically?

This research uses those two theoretical arguments as rationalizations for research motivation. Malaysia presents an ideal research context to test the premises for other developing countries with similar institutional settings, based on three reasons. First, the positive theoretical channels driving the DO–firm performance relationship might not be dominant in developing countries due to their digital infrastructure and literacy. Second, the impact of DO on firm performance is more substantial for Malaysia, as the anecdotal evidence suggests Malaysian government, like other developing nations, imposed digital economy policy plan by introducing it as part of national policy. The Malaysian government provides incentives to encourage businesses to pursue digitalization. According to the Malaysia Investment Development Authority, Malaysia’s digital economy contributed 22.6% in 2020, amounting to USD 279 billion in 2021. Third, emerging countries like Malaysia present a corporate landscape where the business actively pursues digitalization at introduction or increasing business cycle phase. In this phase, most companies prepare themselves with a corporate orientation for their roadmap and strategic plans.

This study’s contribution is threefold. First, we enrich the theoretical framework of organizational orientation theory about the role of organizational orientation in digital firms. Second, we document the empirical findings that the impact of DO on a firm’s financial performance is trivial. Third, we lay a foundation for future research to explore DO by providing the measure and theoretical testing of its impact on a firm’s dynamics, especially in the context of emerging economies like Malaysia.

The article is organized as follows: In the second section, we formulate the hypothesis that will be empirically tested in this study. Meanwhile, the third section presents the measurements, model specifications and data information. The descriptive statistics and regression results are discussed in the fourth section. To deepen our understanding, we conduct further robustness tests in that section. Finally, we conclude with a summary of our key takeaways in the final section.

Literature Review

Organizational orientation theory is the foundation of how an organization’s goals and values affect the company (Kindermann et al., 2021; McGivern & Tvorik, 1997; Presthus, 1958). This theory frames how a firm’s transformation should be compensated given the change in its organizational orientation. The tenet is threefold. First, the orientation aligns the goals and values of employees within those of the organization, creating a common understanding of the organization’s priorities and focuses (Kindermann et al., 2021; Schweiger et al., 2019). This shared alignment leads to better firm performance as employees focus their efforts on activities that contribute to achieving the organization’s goals (McCroskey et al., 2005).

Second, organizational orientation shapes the decision-making processes within an organization, resulting in better strategic decision-making and better firm performance (Jogaratnam, 2017; Schweiger et al., 2019). Finally, organizational orientation influences an organization’s culture, shaping employees’ attitudes and behaviours toward work (Akinbode, 1973; Campbell, 2000; Cheema et al., 2020). A good orientation, therefore, can positively impact firm performance by creating a culture that supports better performance outcomes over time.

We define DO as an organization orientation that strategically utilizes digital technologies to optimize operations, enhance performance and maintain competitiveness in the digital era. With this logic, firms adopt digital technology as part of their strategic business ‘culture’ to optimize operations, improve efficiency, increase productivity and capitalize on new market opportunities. This aligns with the literature, where the adoption of digital technologies (Janowski, 2015; Weill & Woerner, 2018; Westerman et al., 2012) significantly influences firm dynamics (Bendig et al., 2023; Sun et al., 2022; Wu et al., 2022; Wen et al., 2022; You & Brahmana, 2023).

Unfortunately, the empirical research on the impact of DO on firms is dominated by qualitative or survey-based studies (e.g., Khin & Ho, 2018; Ponsignon et al., 2019;Zhao et al., 2023). Moreover, most of the research papers focus on competitive advantage (Kindermann et al., 2021), internationalization (You & Brahmana, 2023), innovation (Bendig et al., 2023; Wen et al., 2022) and firm risk (Tian et al., 2022; Wu et al., 2022). Accordingly, we lend this body of knowledge to build up our hypothesis.

The literature documents the importance of DO in enhancing the firm’s competitive ability. Firms capitalize on their digital resources and enhance their competitiveness using the DO embedded in the organization’s activities and management. The digital technology owned by the organization through its organizational orientation is a valuable and scarce resource that can be difficult to replace or imitate (Kindermann et al., 2021; Nambisan 2017). Those digital resources provide competitiveness for the companies and transform it into value creation (Matarazzo et al., 2021). Therefore, companies with a DO are more likely to earn better firm performance.

For instance, research from You and Brahmana (2023) reveals how DO may affect the firm’s internationalization. The findings surmise that DO drives innovation and boosts international operational efficiency. They reveal that DO helps firms leverage innovation for competitive advantage in international markets. Moreover, they argue that DO enables innovative companies to expand internationally by using innovation to open new factories, branches or subsidiaries abroad.

Using survey design, Tortorella et al. (2019) reveal that the DO’s of 147 Brazilian companies have a positive association with their performance. Their argument is that technology setup in business processes empowers employee engagement in technological processes; hence, it positively affects the value chain, resulting in better firm performance. Meanwhile, Rubbio et al. (2020) surmise the importance of DO in enhancing the digital capabilities of employees. It boosts the dynamic capability of the companies, resulting in better performance.

In short, DO enhances firms’ operational strategies by leveraging cutting-edge technologies. It provides companies with a roadmap, strategies and guidelines to navigate the digital landscape, consequently improving overall business performance. In practical application, firms utilize digital technologies by developing a comprehensive roadmap to integrate digital strategies into their business model. This transformation leads to heightened operational efficiency, cost reduction and a culture of innovation within companies (Kindermann et al., 2021; Kohtamäki et al., 2020; Lee et al., 2015; Li et al., 2022). Thus,

H1: DO has a positive impact on a firm’s performance.

Methods

Specification of the Baseline Model

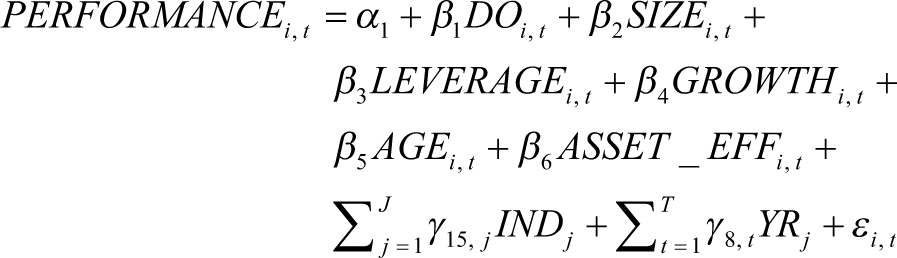

The finance literature has surmised that firm performance is a function of firm characteristics. The success or failure of a company is directly influenced by its inherent attributes, such as size, leverage, revenue growth, age and efficiency. These characteristics shape the company’s ability to adapt to market competition, resulting in performance and competitiveness within its industry. This explains the theoretical argument for utilizing firm characteristics as control variables to isolate their impact on firm performance from other factors, known as the baseline model of firm performance.

We then adopt the baseline model into the organizational orientation theory (McGivern & Tvorik, 1997; Presthus, 1958) by introducing DO as the main effect. The theory posits that DO influences firm dynamics by prioritizing activities based on their strategic DO (Weill & Woerner, 2018). Given that DO aligns organizational strategies with digitalization, leverages digital tools for the business process and management (Bendig et al., 2023) and promotes innovation (You & Brahmana, 2023), it improves performance.

Following previous research from You and Brahmana (2023) and Tian et al. (2022), we introduce the DO variable into our baseline model. The DO is the main effect, and performance is the dependent variable. We pooled the firm-level observations across the year and cross-sections to form the panel regression model. We specify the model as follows:

The performance is firm financial performance, measured by returns on assets (ROA), returns on equity (ROE) and Tobin’s Q (Q). Meanwhile, DO denotes the digital orientation. Size, leverage, growth, age and asset efficiency are the control variables. A detailed discussion about the measurement is provided in the next section.

It is noteworthy that INDj represents a set of industry-specific dummy variables devised according to the sector classification of Bursa Malaysia, aiming to mitigate time-invariant industry influences. Specifically, INDj equals ‘1’ if firm i is in industry j, otherwise ‘0’. j denotes the number of industries. Additionally, year dummies denoted as YRt are also introduced to the model to control for common shocks. YRt equals ‘1’ if firm i is in year t, otherwise ‘0’. t is the number of years. Before conducting panel regression estimation, it is essential to execute diagnostic tests, such as the normality test, multicollinearity, heteroscedasticity and autocorrelation. Subsequently, the Chow test, Breusch–Pagan LM test and Hausman fixed test were also estimated to select the best panel regression model.

Measurements

This research aims to explore the relationship between DO and financial performance. To achieve this objective, we provide an overview of the variables used in our analysis and their corresponding data sources. Following this, we outline the model specifications. Refer to Table A1 for a complete list of all variables.

The dependent variable of this research is financial performance. We use three financial measures: ROA, ROE and Q. ROA and ROE represent the accounting financial performance; meanwhile, Q represents the market performance. ROA is the ratio of net income to total assets, and ROE is the ratio of net income to total equity. Q is the ratio of the market value to its assets’ replacement cost. Theoretically, if Q surpasses one, it suggests that firms are incentivized to invest in the digital realm, as market expectations indicate that the benefits of these investments will exceed their expenses.

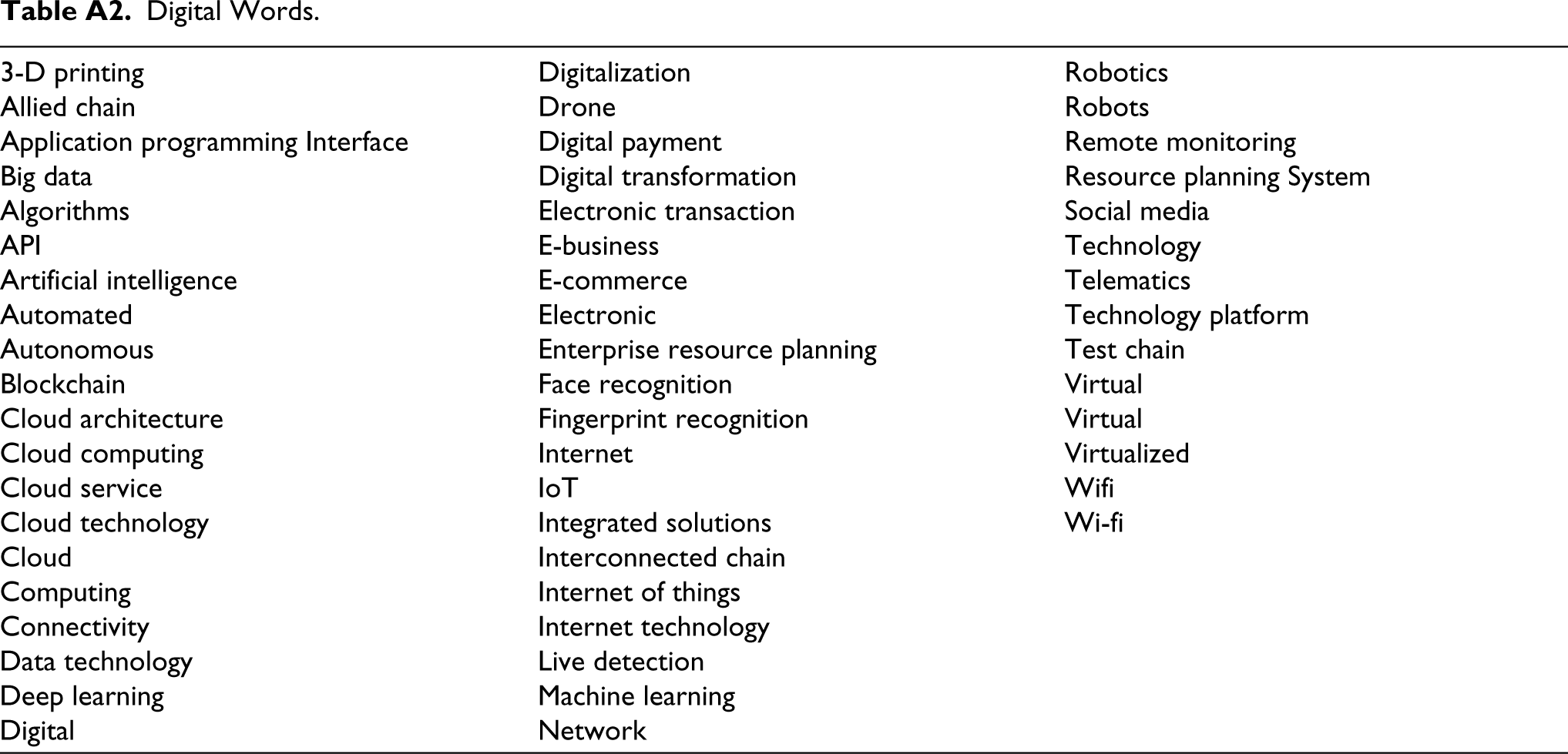

The main independent variable of this research is DO. To quantify a company’s DO, we draw inspiration from Tian et al.’s (2022) methodology, which assesses the tone of annual reports via text analysis. Our approach involves computing the DO using the number of occurrences of digital-related keywords within these reports, which are then subjected to a logarithmic transformation. Hence, DO is equal to the total number of occurrences transformed by taking the natural logarithm of 1 plus the total number of related keywords. The list of keywords is reported in Appendix B.

For the first step of retrieving the data, we used Python programming to count the occurrences of the words. For robustness reasons, we re-counted it manually to ensure the total words were not mistaken. Future research may use our Python coding, provided in Appendix C.

Finance literature has long explored the determinants of firm financial performance, and we thus control for those standard factors in order to isolate the main effect of DO. Our control variables consist of the firm’s size (SIZE), leverage (LEVERAGE), growth (GROWTH), age (AGE) and asset effectiveness (ASSETS_EFF).

SIZE is calculated by the natural logarithm of the firm’s total assets. LEVERAGE is the ratio of total debt to total assets. GROWTH is the yearly revenue growth of the firm. Then, AGE is the natural logarithm of years of a firm’s establishment. Meanwhile, ASSET_EFF is calculated by dividing total revenue by total assets.

Data

The data utilized in this study were retrieved from the annual reports of Malaysian-listed companies from 2012 to 2019. Out of the 929 companies listed on the Malaysia Stock Exchange, we collected data from 392 non-financial companies. This selection was made due to the distinct regulatory framework overseeing the Malaysian financial sector by the Central Bank of Malaysia. Furthermore, companies delisted during the research period were excluded from the analysis. The final dataset comprises 3,136 firm-year observations over the 8 years, representing 392 unique firms. All continuous variables underwent winsorization at the 1st and 99th percentiles to mitigate the impact of outliers.

Findings

Descriptive Statistics

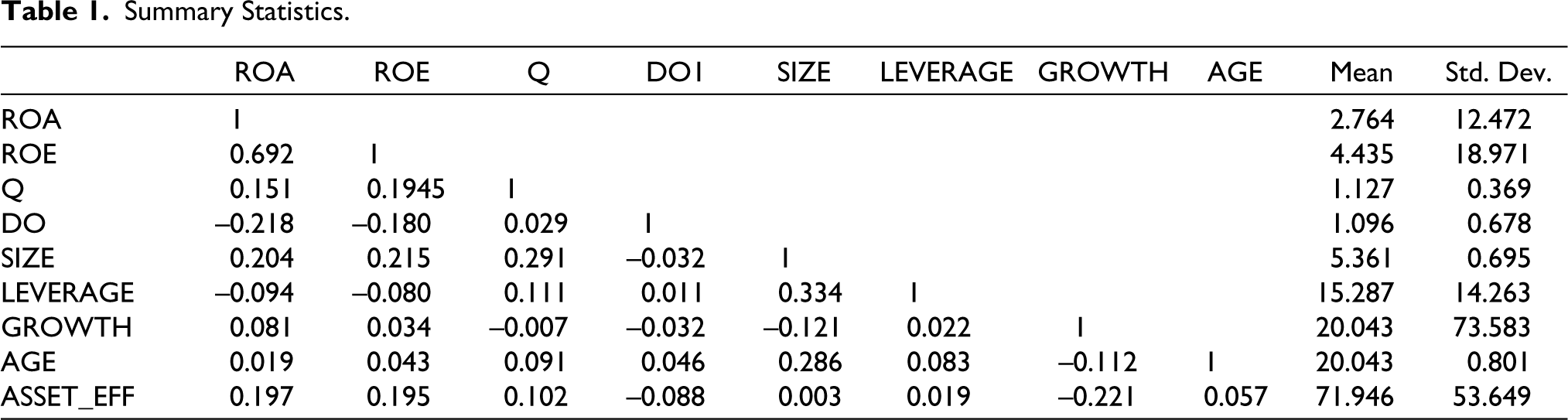

Table 1 summarizes statistics for all variables used in our estimation model. The main effect, DO, has an average value of 1.096. This is lower than the reported value of 2.9 by Tian et al. (2022) in context of China. The rationale is that China has a more advanced digital economy than Malaysia. The dependent variables, ROA, ROE and Q, show mean values of 2.764%, 4.435% and 1.127, respectively. It implies that the average profitability of Malaysian companies was 2.7% (ROA) and 4.435% (ROE), which is slightly lower than the mean value found by Brahmana et al. (2021) for 316 Malaysian companies from 2011 to 2016. Brahmana et al. (2021) reported that ROA was 5.4%. Meanwhile, Q is 1.127, indicating that the Malaysian companies are slightly overpriced as it is higher than 1. Our mean value is actually lower than the Q of 1.146 by Brahmana et al. (2021).

Summary Statistics.

Table 1 presents a correlation matrix showcasing the univariate relationship between the variables in our model specification. Our analysis reveals interesting findings about the association between explanatory and dependent variables. First, all control variables exhibit expected signs. We found that larger, low-leverage, high-growth and older companies are associated with high profitability (ROA and ROE). Meanwhile, when we use Q as the dependent variable, the sign of the association changes. The correlation between all control variables and Q exhibits expected signs, except for growth. Table 1 reveals that larger, high-leverage and older companies are associated with a high Q value, while high growth indicates a low Q.

The association between our main effect (DO) and firm performance (ROA, ROE and Q) has interesting findings. First, we found that high DO is associated with low profitability (negative association). Yet, it has a positive relationship with Q. It implies that companies with high DO generally have low profitability but high market value.

To validate our analysis, we assessed collinearity using the variance inflation factor (VIF). It shows VIF mean values below 10 for all estimation models. Based on these findings, we can assert that our model offers a robust framework for examining the relationship between DO and firm performance.

Regression Results

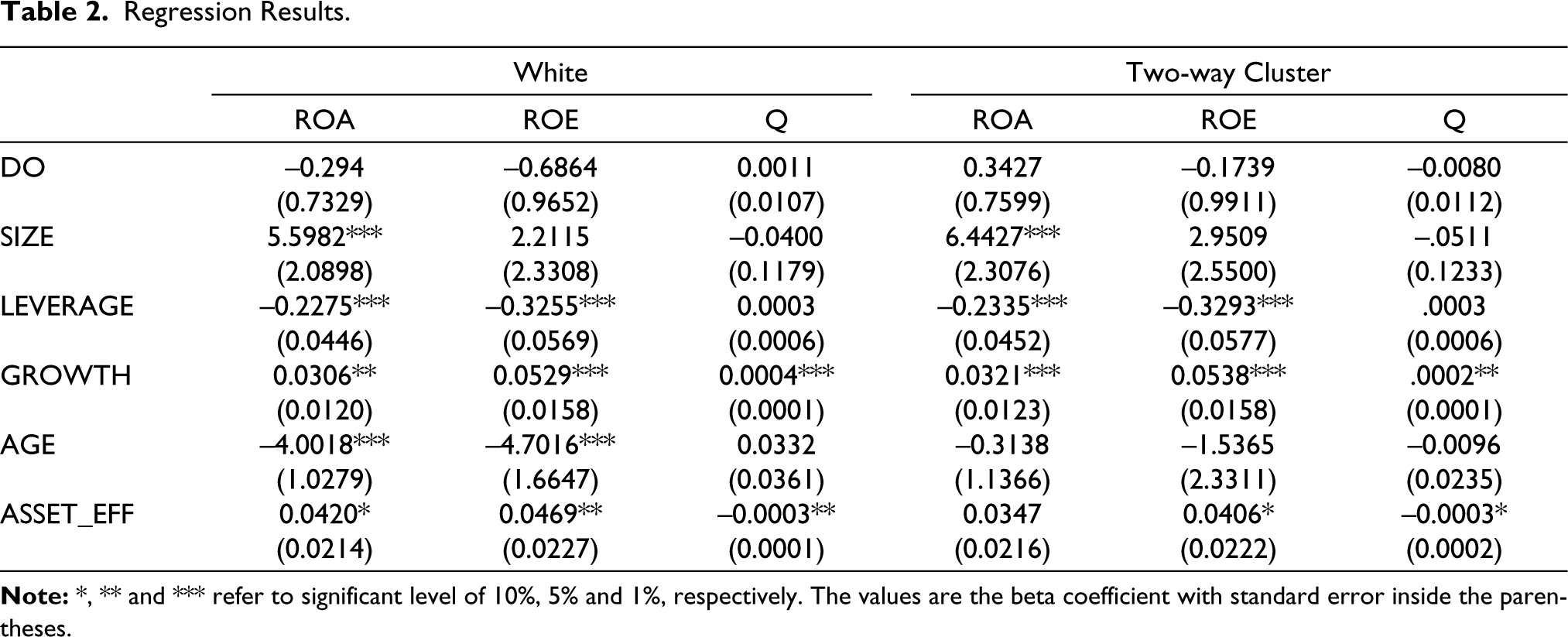

This section reports the hypothesis testing (H1) to determine the existence of DO effect on firm performance. We test it first on the accounting performance of ROA and ROE, and Table 2 presents the panel regression results. Following Petersen’s (2009) recommendation, we conducted the diagnostic tests for our pooled data using Breusch–Pagan LM and Hausman tests to account for potential within-cluster correlation and individual effects. It reveals that fixed-effect panel regression is much more appropriate for the analysis. We employ two fixed-effect-based panel regressions for robustness: fixed-effect White heteroscedastic-robust standard errors and two-way clustered standard errors. For brevity reasons and because all estimation models share the same conclusion, our statistical inferences are based on fixed-effect White heteroscedastic-robust model.

Regression Results.

For the ROA model, our analysis indicates no significant relationship between DO and firm performance. Specifically, the coefficient for DO is not statistically significant at the 5% level (β = –0.294, SE = 0.7329). Therefore, we reject the hypothesis by stating that there is no relationship between DO and ROA.

When using ROE as the dependent variable, the results also remain intact. Specifically, the coefficient for DO is not statistically significant at the 5% level (β = –0.6864, SE = 0.9652). Therefore, the findings reject the hypothesis and counter the organizational orientation theory. It is also consistent with prior research that has failed to establish a significant relationship between DO and ROE (Urbach & Röglinger, 2018; Weill & Woerner, 2018).

In sum, the results of our analysis suggest that DO is not significantly related to financial performance as measured by ROA and ROE. These findings have important implications for the literature because they imply that the DO of the company may not have any significant impact on firm performance, at least in the short term.

We proceed with our analysis by taking Q as the dependent variable. The purpose is straightforward: to examine the relationship between DO and firm market value. Table 2 shows no significant impact of DO on Q at the 5% level (β = –0.0011, SE = 0.0.0107). It indicates that the effort of the companies to transform the business digitally would have no impact on the firm value.

In short, we can conclude that DO does not significantly impact a company’s performance, as measured by ROA, ROE and Q. This discovery challenges conventional wisdom and has crucial implications for the business world. It suggests that companies may not experience immediate financial gains from digitalization.

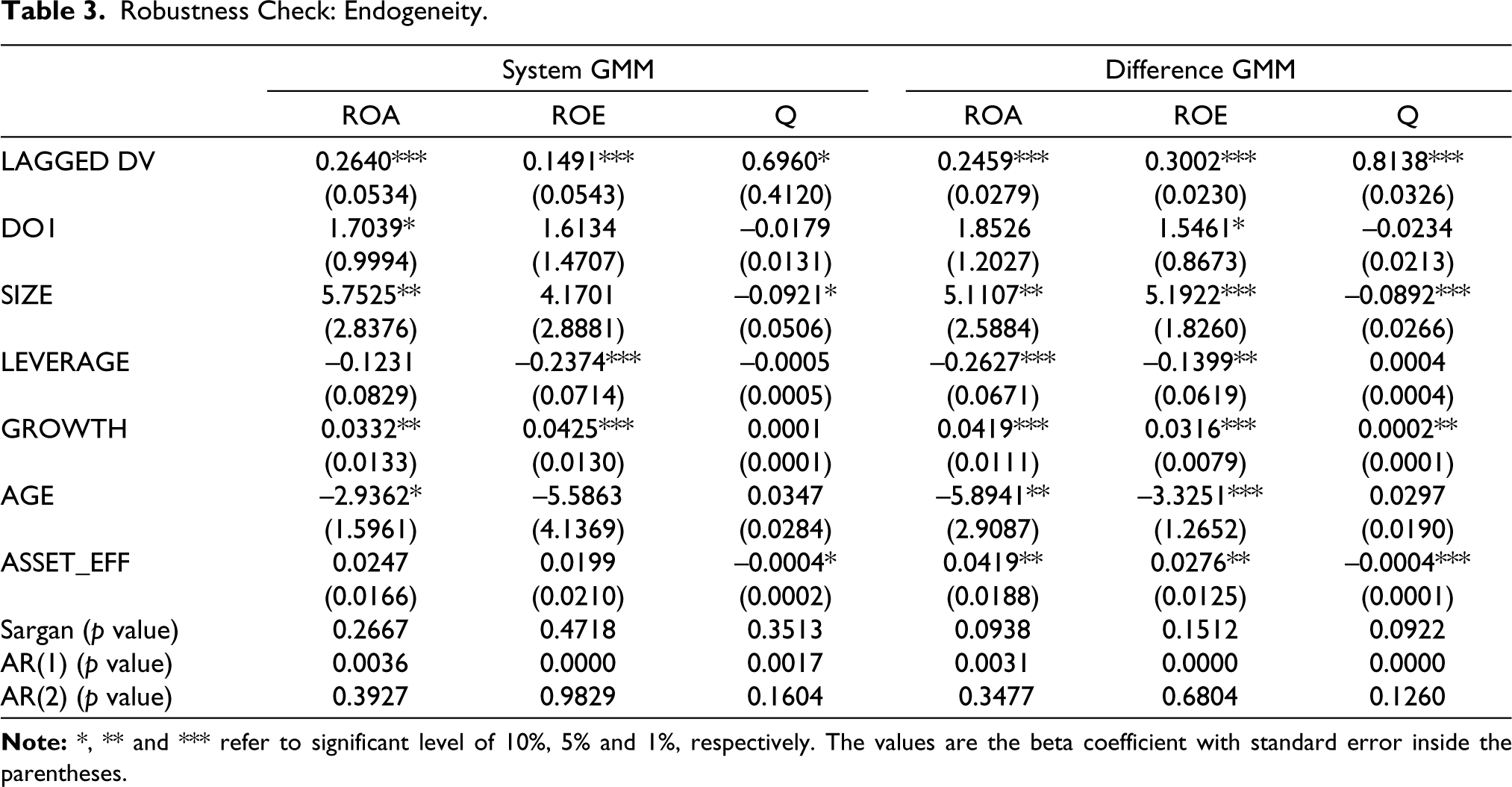

Endogeneity

Because it is challenging to select instrumental variables, we follow the methodology proposed by Wintoki et al. (2012), which recommends the utilization of the generalized method of moments (GMM) dynamic panel framework. This approach allows us to employ a panel GMM methodology to address concerns related to endogeneity. The results are presented in Table 3.

Robustness Check: Endogeneity.

We estimate the GMM using both Arellano and Bond’s (1991) difference GMM and Arellano and Bover’s (1995) system GMM models to ensure the vigour and rigour of our statistical inference. The first GMM model of Arellano and Bond’s (1991) uses a system of first-difference equations to eliminate the fixed effects and then utilizes a GMM estimation to control for the remaining endogeneity and autocorrelation in the error terms. Columns (1), (2) and (3) of Table 3 show that DO has no significant effect on the accounting performance (ROA and ROE) at a 5% significance level, supporting our earlier findings. The results remain the same when we take Q as the dependent variable. Therefore, DO has no significant relationship with firm value (Q). We proceed to the second robustness test, Arellano and Bover’s (1995) system GMM, allowing for more general forms of heterogeneity and dynamics across individuals. The results in the last three columns reaffirm that there is no causal relationship between DO and firm performance.

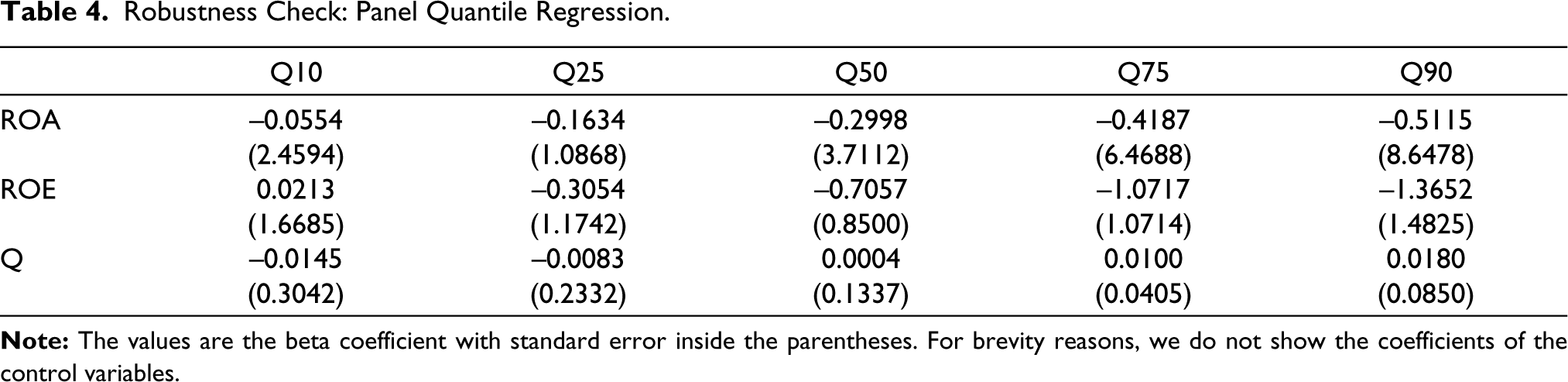

Alternative Estimation Model: Quantile Regression

We add another robustness check as an alternative estimation method: panel quantile regression. It was introduced by Koenker and Bassett (1978), offering an alternative to ordinary least square regression in addressing the limitations associated with estimating the conditional mean effect of DO on firm performance. Quantile regression might tackle the potential bias that arises from the non-normality issue due to data distribution. This model provides an advantageous alternative by allowing for the examination of the effects of DO across the entire spectrum of firm performance conditional distribution, particularly at the extreme upper and lower tails (for a comprehensive overview, refer to Koenker & Hallock, 2001). Table 4 reports the estimation results.

Robustness Check: Panel Quantile Regression.

We then present the regression estimates of the firm value conditional distribution at the 0.10th, 0.25th, 0.50th, 0.75th and 0.90th quantiles. The coefficients for DO are consistent across all the models, with no significant effect at the 5% level. It suggests that the non-existence effect of DO is widespread throughout the distribution of performance. Hence, the conclusion remains intact.

Discussion

Our findings conclude that there is no significant relationship between DO and firm performance, challenging the tenets of organizational orientation theory. We theorize the findings in three ways. First, a DO may not be enough to differentiate a firm from its competitors, particularly in industries where many firms have already adopted similar digital strategies. In these cases, firms may compete on price rather than innovation, and DO may not provide a sustainable competitive advantage. This is consistent with the argument from Nasiri et al. (2022).

Second, DO and maintenance costs can be significant, particularly for small or mid-sized firms with limited resources. You and Brahmana (2023) argue that the cost of digitalization may outweigh the potential benefits of DO, particularly in industries where digitalization is not as critical to customer enhancement (Nasiri et al., 2022). It only burdens the company with high capital expenditures and serves no value creation.

Finally, a DO may not address deeper organizational or strategic issues that can impact firm performance. For example, a firm may have a dysfunctional culture or ineffective strategy that hinders its ability to leverage digital technologies effectively. In these cases, a DO may not be sufficient to overcome these broader challenges. As a result, DO would not provide any enhancements for firm performance.

This result provides a good insight for policymakers, especially in the context of the Malaysian government. Embedding DO as part of national policy would not benefit the companies; it is merely a gimmick. Our results have shown that it is not a good period for Malaysian companies to have DO because it would not benefit company performance. The government should first provide the good infrastructure and ecosystem for the companies before pushing digitalization as part of national policy.

Conclusion

Our research objective is to investigate how DO may affect firm performance. We challenge the widely held belief that a strong DO leads to better firm performance, as our results suggest that a company’s degree of DO does not significantly impact its performance. Our results suggest that whether the companies have a lower or higher orientation towards digitalization does not matter for firm performance. These findings contradict standard recommendations based on organizational orientation theory.

It also implies that a DO is a complex matter, and it needs more than a roadmap, strategies and guidelines to navigate the digital landscape for better organizational performance. Theoretically, our study contributes to management literature by shedding light on the complex dynamics underlying the relationship between DO and firm performance. We support the innovation paradox argument, highlighting the complexity of DO for companies. This also implies the need for more firm-specific or industrial factors to understand digital technology’s impact on organizations.

From a practical perspective, our study provides valuable insight to companies regarding the digitalization process. Managers must carefully consider and plan digital investments, specifically transforming the company’s orientation into a digitalization framework. DO may only provide higher agency costs and capex for the companies. Furthermore, we also give policymakers insight into the fact that digitalization in business processes may not always provide positive results. It indicates the importance of government intervention, such as incentives, subsidies or creating a better digital ecosystem, before the companies transform into digitalized businesses.

While we offer a new perspective regarding the role of DO on firm performance, our study does have limitations. First, our study captures the DO using text analysis from an annual report, which may not fully grasp the extent of a firm’s DO. Even though it is the best-fit approach, future research could consider interviews with management to gain a more comprehensive understanding of a firm’s DO.

Related to that, one limitation of our study is that it did not consider organizational behaviour from the stakeholder’s perspective. The potential outcomes of digital transformation in a company are closely related to supplier–employee satisfaction or customer loyalty. Future research could investigate the impact of DO on a broader range of outcomes to gain a more comprehensive understanding of the benefits and costs of digital transformation.

Furthermore, organizational orientation is closely linked to a firm’s control and monitoring activities, suggesting that corporate governance could potentially moderate the relationship between DO and firm performance. Future research could explore how corporate governance factors, including board size, board capital, board diversity, executive compensation and controlling shareholders, may influence the impact of DO on firm performance. Additionally, future studies could examine the effects of external environmental factors, such as industry trends, market competition, technological advancements and financing costs, on the relationship between DO and firm performance.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.

Appendix A

Digital Words.

| 3-D printing | Digitalization | Robotics |

| Allied chain | Drone | Robots |

| Application programming Interface | Digital payment | Remote monitoring |

| Big data | Digital transformation | Resource planning System |

| Algorithms | Electronic transaction | Social media |

| API | E-business | Technology |

| Artificial intelligence | E-commerce | Telematics |

| Automated | Electronic | Technology platform |

| Autonomous | Enterprise resource planning | Test chain |

| Blockchain | Face recognition | Virtual |

| Cloud architecture | Fingerprint recognition | Virtual |

| Cloud computing | Internet | Virtualized |

| Cloud service | IoT | Wifi |

| Cloud technology | Integrated solutions | Wi-fi |

| Cloud | Interconnected chain | |

| Computing | Internet of things | |

| Connectivity | Internet technology | |

| Data technology | Live detection | |

| Deep learning | Machine learning | |

| Digital | Network |

Appendix B

All coding and data can be retrieved from: