Abstract

The socio-economic environment of a country may significantly influence the size and working of the country’s financial markets in the long run. Keeping this in mind, this study aims to analyse the long-run and short-run impact of COVID-19 cases, deaths, stringency index, and vaccinations on the US stock market. Daily time series data ranging from 22 January 2020, to 30 April 2021, was considered in this study. The ARDL bounds test approach was employed to examine long-run and short-run relationships. Our statistical evidence suggests that, in the long run, confirmed cases and stringency have a negative and significant impact on stock markets, whereas vaccinations have a positive and significant effect on the stock markets. This indicates that any public health emergency adversely affects the stock markets, such as a pandemic outbreak. The government should ramp up the efforts towards vaccinating their citizens in the earliest possible timeline. Such actions of resurgence from the pandemic instil confidence in the market. Policymakers should be thoughtful about formulating contingency measures to effectively safeguard the population while preventing the deterioration in investor confidence.

Introduction

Stock market prices reflect all available information and react rapidly to the arrival of new reports or events (Fama, 1970). In the past century, the markets have seen a number of pandemics. No prior infectious disease pandemic, on the other hand, has had such a substantial effect on the stock markets as the COVID-19 pandemic (Baker et al., 2020). Many researchers have studied the impact of pandemics caused by the Spanish Flu (1918–1920), Asian flu (1957–1958), SARS (2003), EBOLA (2013–2016) and COVID-19 (2019) on the economy or stock market returns or volatility. For instance, Angel et al. (2021), Barro et al. (2020), Bodenhorn (2020), Cortes and Verdickt (2021) and Karlsson et al. (2014) extensively studied Spanish flu in this context. The economic impact of Asian flu was explored by Chan-Lau and Ivaschenko (2003), Forbes (2004) and Girard et al. (2003). Likewise, for SARS, Chen et al. (2009), Chen et al. (2007), Min and Wu (2004), Nippani and Washer (2004) and Waugh (2003) carried out an exhaustive investigation. Donadelli et al. (2017) and Ichev and Marinč (2018) researched EBOLA’s adverse economic implications. In the recent times, COVID-19 related economic adversities have been unravelled by Al-Awadhi et al. (2020), Alfaro et al. (2020), Ashraf (2020), Bai et al. (2021), Baig et al. (2021), Baker et al. (2020), He et al. (2020), Just and Echaust (2020), Liu et al. (2020), Narayan et al. (2021), Schoenfeld (2020) and Zhang et al. (2020). The outbreak of a pandemic invokes negative sentiments among retail investors. This creates a leverage effect implying that negative news creates more volatility as compared to positive news. Due to the irregular movement between the return shock and volatility adjustment resulting in subsequent irregularity, investors have been suggested to be more conscious of negative news in the market.

Nonetheless, stock market integration is dynamic and time-varying during the crisis period (Chakrabarti & Roll, 2002; Gupta & Guidi, 2012; Huyghebaert & Wang, 2010; Joshi et al., 2021b; Longin & Solnik, 1995; Morana & Beltratti, 2008; Narayan et al., 2014; Patel & Patel, 2022). This is attributed to the diversification of foreign investors’ portfolios and their preference for emerging economies in the post-liberalization era (Joshi et al., 2021a; Modi et al., 2010). At the same time, institutional investors are required to protect their clients’ risk-adjusted returns. Rational investors behave in tandem with positive and negative news during the pandemic crisis. In response to higher reported cases across the globe, many governments resorted to adopting very stringent actions, including full or partial lockdown. Such stringent measures immediately reflect upon the market because rational investors demand a higher market risk premium while investing in the crisis period (Aggarwal et al., 2021). Additionally, the favourable economic signals might boost up the level of foreign investment, which in turn might increase the level of per capita income (Abosedra et al., 2021; Sharma et al., 2018, 2021; Sharma & Kautish, 2020a, 2020b, 2021). Higher stringency leads to greater difficulty in conducting the regular business activities, thereby hampering economic growth. At the same time, the successive clinical trials of vaccination bring positive news to the market (Chan et al., 2021). Hence, the rational investors believe that market reacts negatively with growth in cases, growth in deaths and increase in stringency; whereas vaccination drives garner positive reaction from the markets. The stringency index data used in our study has been sourced from

Since the stock markets react furiously to negative news as compared to positive news, the impact of a pandemic outbreak on the world’s largest stock market is of great academic and practical significance. Stringent government measures to curb the spread of the disease can have far-reaching economic ramifications, which could be perceived negatively by the investor community. While designing the policy responses to COVID-19, few of the African countries maneuvered around the potentially large trade-offs between public health and food security (Birner et al., 2021). Nevertheless, higher rates of vaccinations amongst the population can be considered as silver lining of economic resurgence. In modern civilization, the COVID-19 pandemic has been an unprecedented event that has raised many concerns and inquisition around the interplay of government measures and market performance in the midst of a raging public healthcare crisis. Given the recency of the event, there is a dearth of empirical economic research exploring these facets. Moreover, the use of measures or metrics such as vaccination in specific context remains schismatically unravelled. The objective of this research is to analyse the long-run and short-run impact of COVID-19 cases, deaths, stringency index and vaccinations on the stock markets for the US. The novelty of our inquiry stems from the fact that previous studies have researched the impact of various crises on the stock market performance, but rarely to a pandemic of such magnitude, and encompassing comprehensively such as case count, deaths, stringency and vaccinations.

The study contributes to the recent existing literature in several manners. First, by departing from the previous studies (Bakry et al., 2021; Birner et al., 2021; Díaz et al., 2022; Dragomirescu-Gaina, 2021; Dzator et al., 2021; Fu et al., 2021; Rouatbi et al., 2021; Xie et al., 2021), we investigated the possible association between confirmed cases, confirmed deaths, vaccination and stringency index of the US on its stock market. None of these studies has explored this association. We also presented a long-term policy framework to mitigate market volatility caused by the COVID-19 negative news, and here is where the current study’s novelty lies, as we used the ARDL bound test cointegration approach. This approach is advantageous, as it will reveal the market behaviour with the stringency and vaccination news.

In this article, we attempt to examine the effect of confirmed cases, confirmed deaths, vaccination and stringency index of the US on its stock market ever since the first case of COVID-19 was reported. Due to COVID-19, the microstructure of the US stock market observed increase in market illiquidity and volatility (Baig et al., 2021). Our contribution in this aspect is to investigate the US stock market’s response to the country’s COVID-19 related metrics. Hence, the following is the rationale of the study:

The study explores the dynamics of COVID-19 related metrics on stock price adjustments. None of the research examined the effect of vaccinations on stock market movements. The duration has been taken considering the index case of COVID-19 in the US until 30 April 2021. The first case of COVID-19 was reported to Centres for Disease Control and Prevention on 22 January 2020. Long-run and short-run relationship have been established with respect to COVID-19 metrics and the US stock market.

The essence of this article is structured according to the following sections. Section 2 discusses the literature review. Section 3 describes the data and model specification. Methodology is proposed in Section 4. Section 5 deals with results and discussions; Section 6 addresses the study’s conclusion and policy implications; while Section 7 lists the references.

Literature Review

EMH states that market discounts everything based on the information (Fama, 1970; Patel et al., 2012; Patel & Sewell, 2015). The outbreak of an epidemic or pandemic has a widespread impact on our society and the economy at large. The effect of COVID-19 on the Indian economy in the short and long term was addressed by Barbate et al. (2021). This attracts significant interest amongst researchers and practitioners alike. A wide range of studies has been conducted to understand the financial implications of an infectious disease outbreak on the economy. Capital markets, especially equity markets, have been largely driven by investor sentiments of greed and fear. In case of an unforeseen catastrophe or a black swan event, markets tend to react irrationally. The anticipation of government measures and interventions to curb the situation also causes investors to overestimate ground-level adversities. Due to this, market overreacts during pandemics but when more information is available in the market, the market corrects itself (Phan & Narayan, 2020). Rather than deploying strict lockdown measures, Dzator et al. (2021) advocated for boosting knowledge and full participation of all members of society in the implementation of public health policies. Historically, the world has witnessed numerous epidemics that were confined to specific geographies. A large scale, full-blown pandemic has been a rare sighting for the financial markets’ spectators. An epidemic outbreak causes clouds of pessimism to loom over the stock market due to the investors’ woes about dwindling future income and economic devastation (Jiang et al., 2017; Liu et al., 2020).

Extensive research has been conducted on the financial impact of SARS epidemic outbreak that occurred in the year 2002. Nippani and Washer (2004) found that the SARS outbreak had a negative impact on the stock markets of China and Vietnam. In the case of Taiwan, Chen et al. (2007) and Chen et al. (2009) observed the influence of SARS epidemic outbreak and found a negative relationship in the returns of tourism, retail, hotel, and wholesale businesses whereas the biotechnology businesses showed a positive relationship. Similarly, Jiang et al. (2017) studied the relationship between the Chinese stock market’s performance and H7N9 influenza outbreak. The results of the study revealed that the daily number of cases had a significant and negative impact on the broad market indices. The impact of Ebola virus outbreak on the US securities markets was assessed by Ichev and Marinč (2018). They observed that the companies having their operations in West Africa and the USA were adversely impacted by the Ebola outbreak in these regions. Moreover, the stock performance of smaller companies was relatively more dismal than larger companies. Goodell (2020) presented agendas for future research by conducting a comprehensive literature survey regarding the impact of COVID-19 on finance, breaking into sectoral impact. The effect of COVID-19 pandemic on the stock market has been extensively studied in recent times. Few researchers have examined the effect of a pandemic on market volatility (Bai et al., 2021; Baig et al., 2021; Baker et al., 2020; Bouri et al., 2021; Díaz et al., 2022; Just & Echaust, 2020; Song et al., 2021; Zhang et al., 2020); others have analysed the impact with relation to cross-section returns in the market or in industries (Al-Awadhi et al., 2020; Alfaro et al., 2020; Ashraf, 2020; He et al., 2020; Kanupriya, 2021; Liu et al., 2020; Schoenfeld, 2020).

Of lately, replete studies have been undertaken to explore the impact of COVID-19 pandemic on the stock market performance. Amongst these, Al-Awadhi et al. (2020) observed that the Chinese stock markets reacted negatively to the daily increase in confirmed cases and deaths pertaining to COVID-19 disease. In agreement, Burdekin and Harrison (2021) found that rising coronavirus cases have the predicted overall effect of worsening relative stock market performance, but have little consistent impact on rising mortality rates. Alfaro et al. (2020) observed a negative relationship between the US stock market returns and the detrimental effects of the COVID-19 outbreak. In a panel study encompassing 64 countries, Ashraf (2020) found an inverse relationship between stock market returns and rise in confirmed cases for respective countries. However, the news of growing death rate has a negative but not significant impact on the stock market. This indicates that the market had already reacted with the news of growth in the confirmed cases; hence, it did not react significantly with the growth in deaths. This was in line with the findings of similar studies performed by He et al. (2020), Baig et al. (2021) and Liu et al. (2020). However, Onali (2020) did not find impact of COVID-19 cases and related deaths in the US and six other countries in the first three months of 2020. Zhang et al. (2020) affirms the negative impact of COVID-19 outbreak on the stock markets of ten countries under study. They gathered that the standard deviations generated by the Chinese stock markets were highest in February and lowest in March, whereas the US stock markets witnessed the sharpest spike in standard deviations amongst all countries investigated. Borjigin et al. (2020) discerned that negative news about the pandemic has a greater effect on market volatility than positive news. Yang et al. (2021) evaluated the destination image and travel intention in China influenced by misleading media coverage.

In a sector-wise study, Schoenfeld (2020) found that the COVID-19 pandemic inflicted the gravest wounds upon the hospitality, automobile, logistics, machinery, oil and gas, and garment industries. Kanupriya (2021) observed the worst hit of the Indian textiles sector due to COVID-19. However, Al-Awadhi et al. (2020) observed a better performance of information technology and medicine manufacturing sectors while worst performance of beverages, air transportation, water transportation, and highway transportation in China during COVID-19 outbreak. Moreover, they also observed significantly more negative effect on returns of large market capitalization stocks as compared to small market capitalization stocks. Goodell (2020) claimed that COVID-19 induced a substantial withdrawal of deposits and disrupted cash flows of borrowers, consequently leading to mounting non-performing assets, which has severely impacted the financial sector.

There are major differences between developed and emerging markets with respect to investors’ interpretation of risk in response to new information related to COVID-19. These differences are in terms of national culture and the quality of governance (Bakry et al., 2021). From a governance perspective, authorities generally tend to handle infectious diseases outbreak on a war footing basis. This implies that stringent measures are often implemented in order to safeguard the population at the earliest. For example, Narayan et al. (2021) observed the positive effect of lockdowns, travel bans, and economic stimulus packages on the G7 stock markets. Likewise, the onset of COVID-19 led several countries in a complete lockdown. As the governments imposed sudden containment measures for limiting the spread of the virus, it triggered a global economic turmoil triggered by supply and demand shocks (Dragomirescu-Gaina, 2021; Eichenbaum, et al., 2020; Fetzer et al., 2020; Gormsen, & Koijen, 2020; Malden & Stephens, 2020). Consequently, there has been a shift in the aggregate demand and supply [AD-AS] curves primarily impacted by volatility in the workforce supply, diminishing income levels, spending, saving and investment levels, prices fluctuations across various asset classes such as oil, commodities, equities, dwindling industrial output, trade balance, investment, exchange rates, interest rates, and credit growth (de España, 2020; Malik et al., 2020; Maliszewska et al., 2020; Pak et al., 2020). Thangavel et al. (2021) addressed the effects of the pandemic on the future of globalization.

Not just official government announcements, but also unofficial beliefs, have an impact on financial markets (Xie et al., 2021). Stock markets were one of the most severely impacted segments of the financial markets. It nosedived immediately with the public announcement of the COVID-19 outbreak. This was primarily due to a sharp spike in volatility, withering liquidity, and value destruction of shareholders’ investments (Boissay & Rungcharoenkitkul, 2020). Baig et al. (2021) studied the impact of COVID-19 on the microstructure of the US stock markets and observed that increase in confirmed cases and deaths due to COVID-19 infection has a significant increase in market illiquidity and volatility. They also found that the liquidity and stability of the stock markets were further worsened by weak investor sentiments and the announcement of lockdowns. Xie et al. (2021) found a significant negative influence of the announcement of lockdown on most of the stock markets. Fu et al. (2021) investigated the gradual ease of lockdown based on vaccination progress. Rouatbi et al. (2021) provided convincing evidence in stabilizing the global equity market due to vaccination drives. They further found stronger impact of vaccinations within developed markets than in emerging markets. Nevertheless, an empirical analysis of 72 countries, Kizys et al. (2021) found that the investor herding phenomenon existed in the stock markets and that stringent government response, measured through Oxford’s Stringency Index, mitigated investor herding by reducing multidimensional uncertainty. Sinha (2021) analysed socio-economic attention searches using the keywords such as bank loan rate, COVID-19, economy, internal rate of return, risk-free rate of return, fear, economic crisis, gold price, donation, and loan moratorium. The researcher also proposes to re-examine the socio-economic attention searches using the keywords such as ‘Vaccine’, ‘COVID-19 Vaccine’, ‘COVAX’, ‘COVID Vaccine’, and so on.

Countries across the globe formulated an array of fiscal and monetary policies as corrective measures against the panic, paranoia, and palpable socio-economic depredation caused by the emergence of the pandemic and its subsequent containment response. Governments increased public spending by implementing direct cash transfers and economic stimulus packages, while Central Banks adopted an expansionary stance of reducing interest rates and executing quantitative easing policies in order to infuse liquidity into the economic system (McKibbin, & Fernando, 2020). Amidst this eruption of an unprecedented contagion, both biological and financial, the world stands at the crossroads of survival and growth. Scholastic inquisitiveness about exploring the holistic interplay between factors such as confirmed cases, confirmed deaths, vaccination and stringency index on the stock market of the USA has been the driving force behind this research endeavour.

Our research is the most recent and closely linked to the literature on COVID-19 metrics and the US stock market. None of these studies assesses the impact of vaccination campaigns in conjunction with other indicators on the US stock market. As a result, our research is the first to assess how COVID-19 pandemic-related metrics influenced the US stock market, adding to the existing literature on COVID-19 and stock markets.

Data, Variable Selection and Model Specification

The present study is unique in terms of the approach, threefold. First, we used the autoregressive distributed lag bound test approach (Pesaran et al., 2001) to study the long-run and short-run relationship among the stock market and COVID-19 related metrics. The rationale for using the ARDL method is that it outperforms other measures in terms of establishing the relationship between the variables even when they are at different order of integration. Nonetheless, due to the presence of an integrated stochastic trend of I(2), the approach would fail (Acquah, 2010). Second, the research attempts to investigate the long-run and short-run cointegration association among variables of interest due to the COVID-19 outbreak. Third, we investigated the market reactions after the first case of COVID-19 was reported in the United States of America. Hence, the duration of the period is from 22 January 2020 to 30 April 2021.

We have collected daily closing prices of Dow Jones Industrial Average (DJ) from Nasdaq and data related to confirmed cases, deaths, vaccination (Vacci) and stringency index (SI) from

Initially, the stationarity of the series is checked by performing unit root tests (Augmented Dickey Fuller test and Phillip-Perron) on the level as well as first differenced log series of the variables. The ARDL approach allows integration of order I(0) or I(1), which implies that the series can be stationary either at I(0) or I(1). Stock market adjustments are ephemeral because of cross border holdings of institutional investors (Patel & Patel, 2022); hence, the ARDL approach helps us to take different lags for the independent variables (Ozturk & Acaravci, 2011). This process ensures the pre-conditioning of the ARDL model, where no series are integrated at order (2). The second step comprehends the ARDL model specification, considering Akaike information criterion (AIC). We then use the bound test approach to investigate the cointegration between dependent and regressors to estimate the long-run and short-run relationship. The relationship among the variables is dynamic over time. The declines caused by panic are quite often temporary (Brounen & Derwall, 2010), indicating market sentiments or herding behaviour rather than rationality (Aggarwal et al., 2021). The Eq. (1) represents the DJIA as a function of the variables under study;

Where DJ represents Dow Jones Industrial Average, Cases and Deaths represent the total confirmed cases and total confirmed deaths. Vacci represents the total vaccination in the country and SI represents the Stringency Index developed by

Methodology

Several studies have used techniques such as Johansen cointegration, Engle and Granger cointegration, DCC-GARCH, Granger causality test, Vector autoregression, and others to capture the cointegration relationship (Sharma & Seth, 2012). However, Engle and Granger (1987), Johansen (1988) and Johansen and Juselius (1990) techniques are widely used to establish cointegration relationship. The majority of these statistical tests necessitate variables of the same integration order (Bekhet & Matar, 2013). We use the ARDL bound test approach in our research (Pesaran et al., 2001) as it supports the study of variables that are at level, or first difference, or a mix of both.

The expected relationship of total cases, total deaths and stringency index is negative whereas it is positive for total vaccination with index returns. Alfaro et al. (2020) examined the US market in response to pandemics such as COVID-19 and SARS; observed negative response to such pandemics. Similar to that Ashraf (2020) analysed stock markets’ reactions to COVID-19 cases. The author documented a negative response of the stock market with growth in cases. Further, they also observed a proactive response of the market with growth in cases as compared to growth in deaths. Few researchers have also examined the market volatility and financial risk due to pandemic (Baig et al., 2021; Baker et al., 2020; Zhang et al., 2020).

Hence, the error correction model is estimated as follows;

Where DJ indicates Dow Jones Industrial Average, and cases, deaths, Vacci and SI indicate the COVID-19 related variables as explained in section 3. Δ is the first differ- ence operator. α0 is the constant term, Ø1, ….., Ø5 are the coefficient of long run relationship and β6, …..,β10 are the coefficient of short-run relationship εt is the white noise error term. The null hypothesis for long-run relationship is Ø1 = Ø2 = Ø3 =Ø4 = Ø5 = 0 and for short-run relationship is β6 = β7 = β8 = β9 = β10 = 0 . To check the existence of long-run relationships, we conducted the bounds test using EViews. If the calculated F-statistic is over the critical value of upper bound, then the co-integration relationship occurs in the equation. In case, if it is under the critical value of lower bound, then the cointegration relationship does not exist. Nonetheless, the outcome of cointegration is inconclusive if the statistics fall between the critical limit.

Results and Discussion

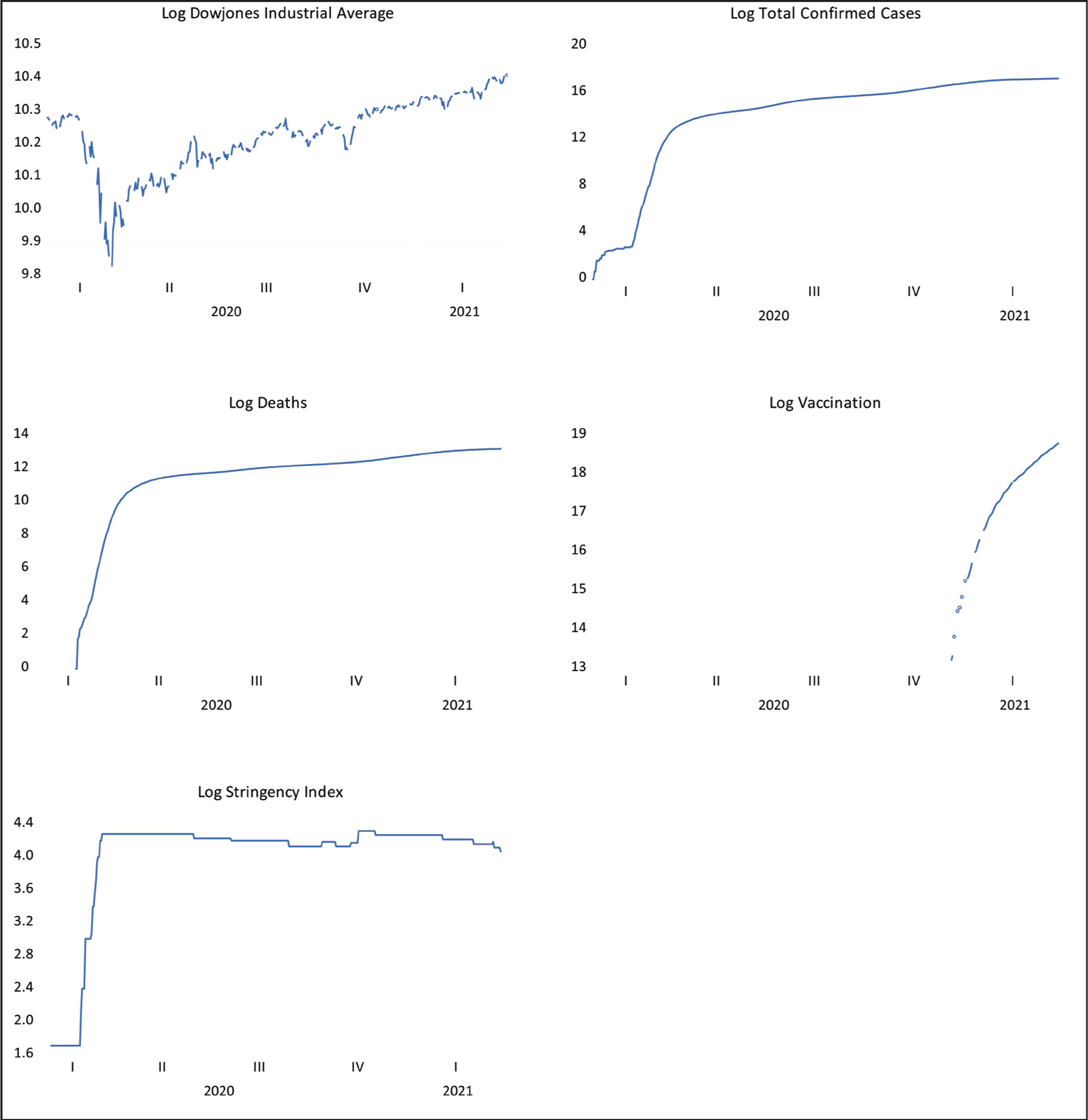

Figure 1 depicts the plot of the daily movement of variables under study for USA. A sharp dip has been observed in the movement of Dow Jones during the first quarter of 2020 as the market started to react negatively to the sudden increase in the confirmed cases and deaths related to COVID-19 in the same quarter. Though there has been an increase in the number of confirmed cases and deaths along with high stringency index, there was no notable downward movement in the Dow Jones as the markets had already factored in the situation of increasing cases and deaths of COVID-19. A spike in the Dow Jones has been observed after the fourth quarter of 2020, the market started getting positive information on vaccination trials and subsequently country started vaccinations drives.

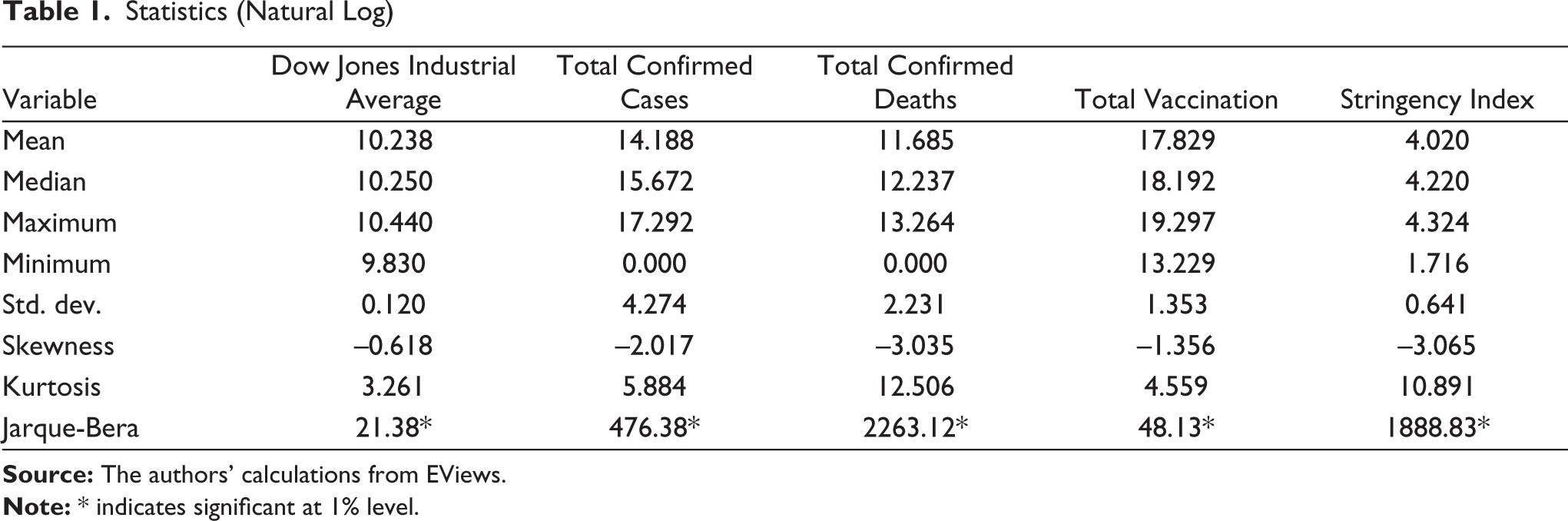

Table 1 shows the descriptive statistics between the vari- ables. Among the variables, highest volatility is observed in confirmed cases whereas lowest volatility is observed in the Dow Jones. The mean of the vaccination is highest amongst the variables under study. This indicates the massive efforts overtaken by the federal government towards the immunization of its citizens. The Jarque-Bera test shows that the variables are not normally distributed as the null hypothesis of normally is rejected. All the variables are negatively skewed, indicating that values are mostly situated towards the distribution’s right-side tail.

Statistics (Natural Log)

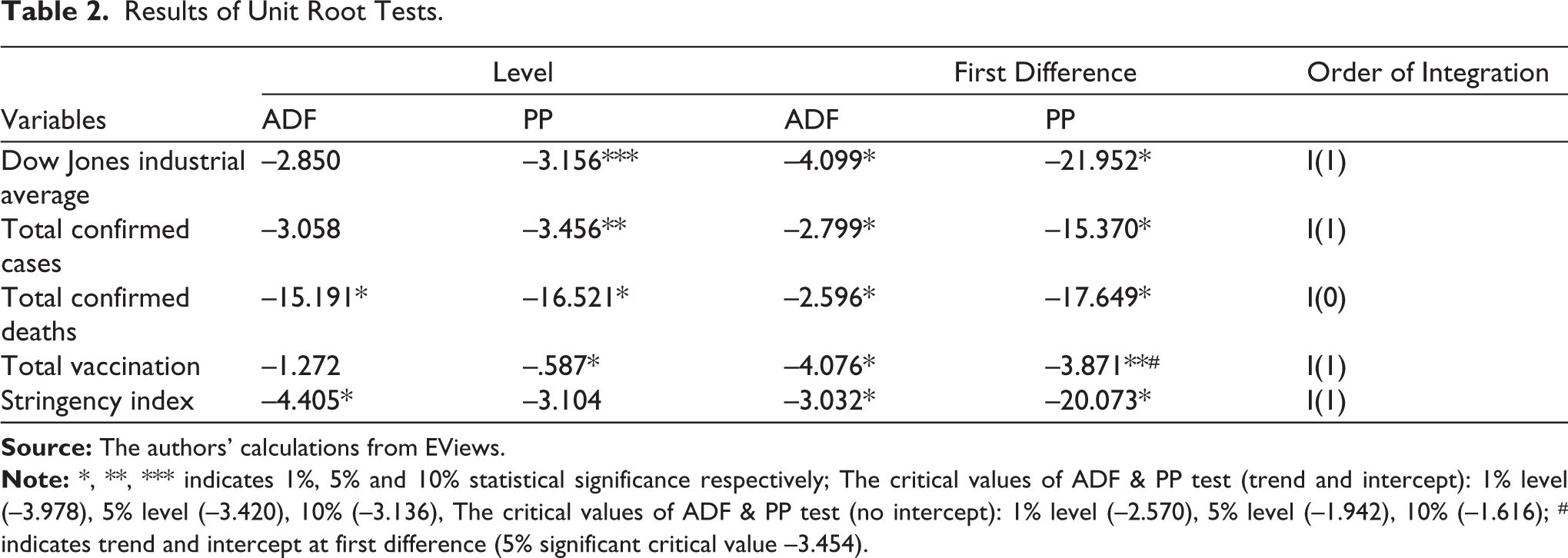

The primary condition of ARDL states that the series should not be integrated at order I(2) so to avoid spurious results. Two unit root tests, namely ADF and PP, are considered to confirm the null hypothesis of unit roots. These tests are applied on the levels by including trend and intercept; however, none was added at the first difference in the equation. In Table 2, we report the outcomes of unit root tests.

Results of Unit Root Tests.

Table 2 reports the results of unit root tests at level and first difference series. The null of ADF and PP is that there is a unit root in the time series. All the series are stationary either at level or at first difference. Results of these tests indicates that none of the series is I(2), which satisfies the first condition of ARDL.

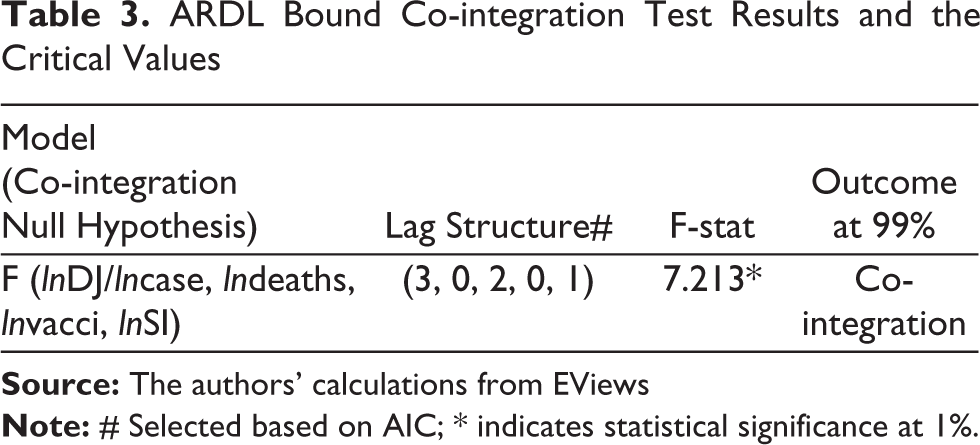

Table 3 reports the outcomes of ARDL bounds test using the AIC information criteria for optimum lag order. The estimated F-statistic exceed 99% upper bound, which rejects the null of no cointegration. Therefore, there exists a cointegration relationship amongst the variables.

ARDL Bound Co-integration Test Results and the Critical Values

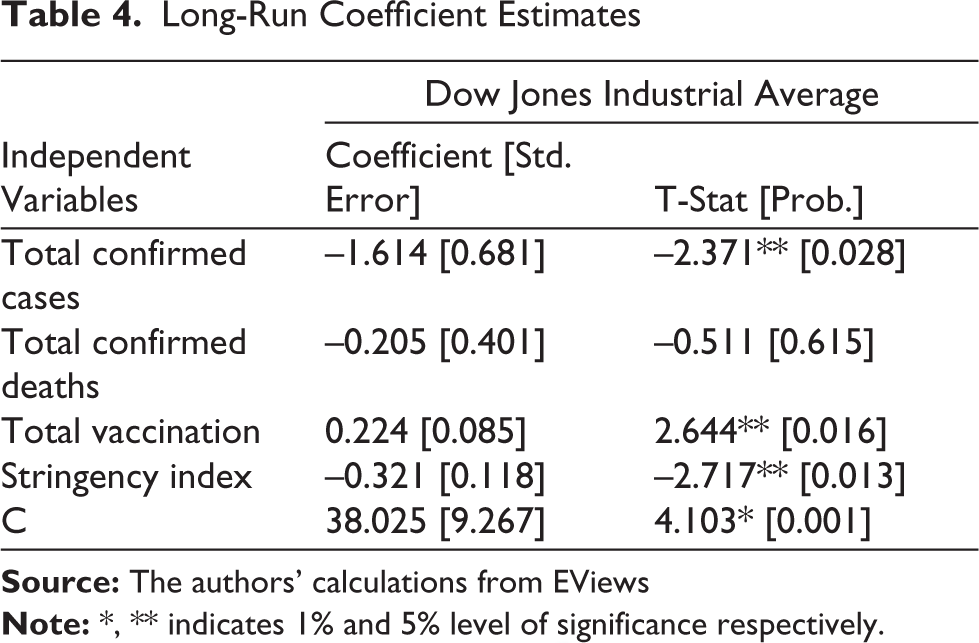

Table 4 shows the long-run cointegration results of the model. Total confirmed cases reported in the USA shows a significant and negative relationship with the Dow Jones movement. For every 1% increase in the confirmed cases, there will be a 1.614% decrease in the Dow Jones movement. News pertaining to pandemic outbreak instils fear and negative sentiments amongst the investors and given that negative news creates more volatility as compared to positive news, markets tend to nosedive. The outbreak of the COVID-19 pandemic created a substantial increase in economic anxiety (Fetzer et al., 2020). Our results are consistent with that of Al-Awadhi et al. (2020). Total deaths are showing an insignificant but negative relationship with the Dow Jones movement. This is because the confirmed cases had already created panic in the market. This was in line with the findings of similar studies performed by Ashraf (2020), He et al. (2020), Baig et al. (2021), Liu et al. (2020) and Burdekin and Harrison (2021). Vaccination is showing a significant positive relationship with the Dow Jones movement. For every 1% increase in vaccination, there will be a 0.224% increase in the Dow Jones movement, thus indicating that the market has factored this as a positive sentiment in expectation of a faster recovery. The stringency index is showing a significant negative relationship with the Dow Jones movement. For every 1% increase in the stringency index, there will be a 0.321% decrease in the Dow Jones movement. These observations are consistent with that of Eichenbaum, et al. (2020), Fetzer et al. (2020), Gormsen and Koijen (2020) and Malden and Stephens (2020). Due to the stringent lockdown measures, supply and demand shocks were triggered causing widespread economic turmoil (de España, 2020; Maliszewska et al., 2020; Pak et al., 2020).

Long-Run Coefficient Estimates

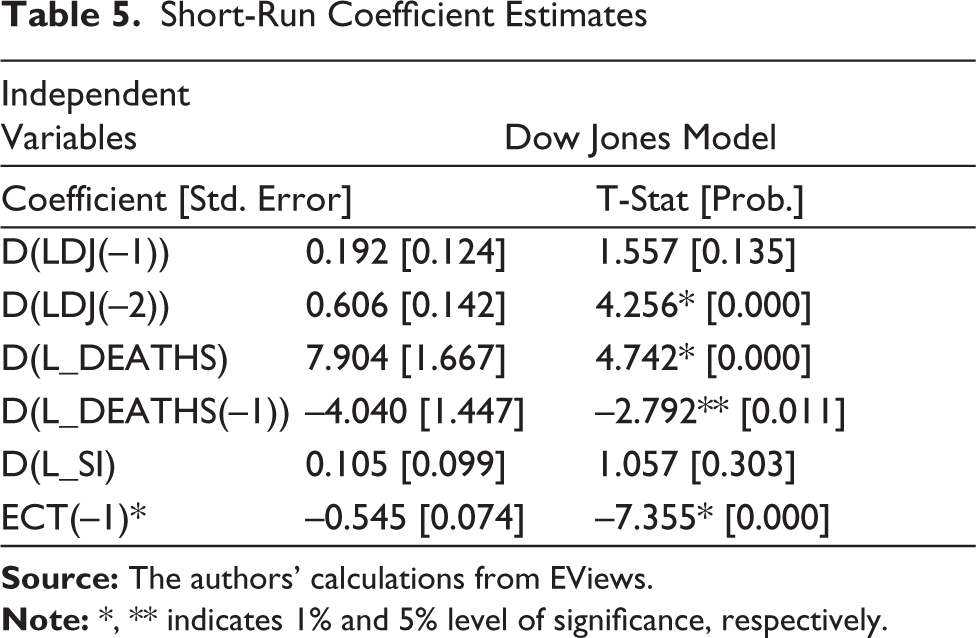

Table 5 presents the short-run dynamics equilibrium relationship of the model. The difference in death reported due to COVID-19 in the short-run has a significant positive impact on the Dow Jones. However, the change from the previous deaths has significant negative impact on Dow Jones movement. As reported in the long-run, market is more affected by the confirmed cases as compared to confirmed deaths. The change in stringency index is insignificant, indicating that market has already responded to the stringency measures adopted by the country in the long-run. The sign of error correction term (ECT) is negative, which confirms the existence of a long-run equilibrium relationship among the variables. The ECT coefficient of –0.545 indicates that any disequilibrium will be adjusted at the speed of 54.5% from the previous period. Table 6 reports various diagnostic tests adopted for checking the stability of the constructed model.

Short-Run Coefficient Estimates

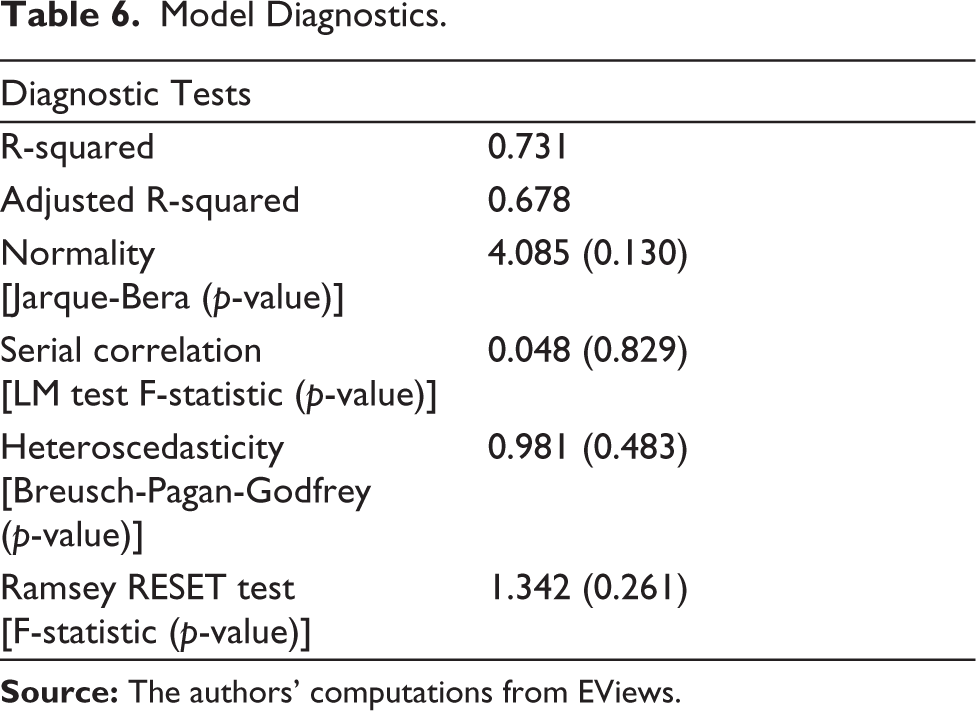

Model Diagnostics.

The Jarque-Bera test for normality assumption in the residuals is tested and the null hypothesis of normally distributed residuals is accepted. The serial correlation is tested using the LM test and the null hypothesis of no serial correlation is accepted. For testing the homoscedasticity, Breush-Pagan-Godfrey test is performed and the null of disturbance terms is homoscedastic is accepted. To test the structural stability of the model, the cumulative sum of recursive residuals (CUSUM) and the cumulative sum of squares (CUSUMSQ) are plotted in Figure 2. As the plots are between the 5% significance bounds, the model is considered stable.

Conclusion and Policy Implications

This research examines the long-run and short-run relationship between COVID-19 confirmed cases, confirmed deaths, vaccination, and stringency measures with the stock market in context to the US. The ARDL bounds test approach has been deployed for establishing empirical evidence. Daily time series data ranging from 22 January 2020 to 30 April 2021 was considered in this study. Our research is the most recent and is closely linked to the literature on COVID-19 metrics and the US stock market. None of these studies examined the impact of vaccination campaigns in conjunction with other factors on the US stock market. As a result, our study is the first to investigate at how COVID-19 pandemic-related metrics affected the stock market in the United States, thus contributing to the existing body of knowledge. Our results indicate that a negative and significant relationship exists between the returns of stock market, confirmed cases and stringency; whereas a positive and significant relationship exists between the returns of stock market and vaccinations.

In light of the aforementioned results, it becomes imperative for governments to formulate and implement policy measures such that it uplifts investor confidence, especially under such grim circumstances. Initially, controlling the spread of infections should be given paramount importance. Nevertheless, the authorities should act swiftly to gauge the leeway that could be exercised for the gradual easement of the lockdown. At the same time, the government should ramp up efforts towards vaccinating their citizens in the earliest possible timeline. Such efforts of resurgence from the pandemic instils confidence in the market. As a non-pharmacological measure, expansionary fiscal and monetary policies must supplement the governments’ pandemic response actions in order to provide support to the adversely impacted businesses and communities. Moreover, strong impetus should be provided for the development and administering of vaccines at a population scale so that the pandemic can be exterminated.

Despite the exhaustive insights drawn from this study, we are of the opinion that the enormity of challenges, which a public health emergency poses, to a country require a broader, multi-faceted contingency approach that encompasses epidemiological considerations at its core. Given that the time period of the study is short, hence the study singly explores the effect of COVID-19 on the stock prices for a short period of time. Secondary data used in this study has been sourced from readily available resources in public domain. Lastly, government efforts in the form of stimulus packages and the prevailing political set-up might have also influenced the stock markets. In purview of the aforesaid limitations, we believe the scope for future research may arise.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.