Abstract

Managers of corporations are usually faced with several strategic decisions to make, including those related to capital structure and financial leverage. This study examines the determinants of leverage practices of listed non-financial firms, both local and foreign, and the moderating effect of foreign ownership. The study uses data from 61 listed non-financial firms over the period 2011–2021 and employs the generalized method of moments estimation technique to explore direct and moderating relationships. The key findings show that profitability, firm growth, liquidity, asset tangibility, capital expenditure, dividend and foreign ownership decrease leverage significantly, while holding more cash increases leverage practices significantly. In particular, firm growth, asset tangibility and dividend increase leverage insignificantly (significantly for cash), whereas return on asset and liquidity significantly decrease leverage in local firms (insignificantly for capital expenditure). On the other hand, all firm characteristics, except cash and dividends, significantly decrease leverage in foreign firms. Moreover, foreign firms have more debt financing compared to the local firms in Nigeria. It is also evident that foreign ownership moderates the relationship between return on asset, firm growth and leverage practices. Such findings should assist managers, investors and regulators in Nigeria to understand the determining factors of leverage and to consider the accruing benefits of debt financing over equity financing.

Introduction

Managers of corporations are usually faced with several strategic decisions to make, including those related to capital structure and financial leverage, which involve the right balance between borrowed and owner’s funds to embark upon, as the firm survival depends on such decisions (Danso & Adomako, 2014). Moreover, different, and sometimes conflicting, needs of debtholders and shareholders make finding such balance even harder (Singh et al., 2021) and has become a challenging debate for academics and practitioners. On the other hand, despite some benefits that debt might have, such as deductions of interest for tax purposes, other firms might prefer to have a substantial amount of cash held to finance their operations (Dangl & Zechner, 2021; Hando & Sharma, 2014), while Cuong et al. (2020) stated that firm operations are usually affected by its country’s economic environment. Several empirical studies and theories on capital structure have been developed following the work of Modigliani and Miller in 1958 about the irrelevance of capital structure (Rehman et al., 2016).

Debt financing practices from the perspective of firm-specific characteristics have received lots of attention, and even currently, by several scholars around the world, from the Asian region (Al-Ahdal et al., 2022; Gulzar & Haque, 2022; Zeitun & Goaied, 2021) to the European region (Bilgin & Dinc, 2019; Sikveland & Zhang, 2021; Yarba & Guner, 2019) and to the African region (Bolarinwa & Adegboye, 2020; Chipeta & Deressa, 2016; Munisi, 2017) and also the American region (Chen et al., 2021; El-Khatib, 2017).

The selection of Nigeria for the conduct of this study is very important for several reasons. First, Nigeria is known to be the biggest economy in Africa in terms of gross domestic product. Second, it is among the top two stock exchanges in Africa as regards to market capitalization and attracts a lot of foreign investors. Also, as a developing nation with lots of prospects, it is important to know the leverage practice from the perspective of a developing nation. There are similar studies in Africa but a limited number in Nigeria in particular. Munisi (2017) studied 12 sub-Saharan African countries but considered only 5 years (2005–2009). Chipeta and Deressa (2016) studied 12 sub-Saharan African countries but did not compare local and multinational firms in the selected firms. Bolarinwa (2020) studied several firms in Nigeria but did not consider the influence of foreign ownership on leverage.

However, to the best of the researchers’ knowledge, there is no literature on the moderating effect of foreign ownership on the relationship between firm-specific characteristics and corporate leverage of firms in Africa, Nigeria to be precise, and also comparing local and foreign firms. Therefore, this study aims to fill this gap by looking into the corporate leverage practices in Nigeria, taking into account the influence of multinational companies (MNCs), to answer this research question: What are the determinants of leverage in emerging markets, and does foreign ownership have any influence? A couple of objectives have been identified to help tackle this question:

To identify firm characteristics which have an impact on corporate leverage practices in Nigeria. To explore the role of foreign ownership and whether it has any moderating impact on how firm characteristics affect leverage in Nigeria.

This study has several contributions, including the construction of a manually collected data set of Nigerian non-financial firms for over 10 years. It also expands the literature on the determinants of financial leverage practices in Nigeria, and whether the use of debt financing differs between locally owned companies and MNCs. It further explores the moderating effect of such foreign ownership on the determinants of financial leverage and offers new insights to understand why such factors affect Nigerian firms differently.

The rest of the article is organized into four sections. The literature review is discussed next in the second section. Then, the third section consists of methodology, followed by results and discussion in the fourth section. The study ends with a conclusion, including a summary of key findings, policy implications, limitations and areas for further research.

Literature Review

Several theories have been used to explain leverage practices by several researchers, especially from the perspective of a firm’s specific characteristics. The tradeoff theory explains that firms consider the benefit from tax as well as the cost of bankruptcy when setting their leverage ratio target (Hang et al., 2018). In other words, the capital structure of a firm is a function of the cost and benefit of debt, and also a function of the attributes of the assets of a firm (Axelson et al., 2013; Gungoraydinoglu & Öztekin, 2011). Some of these benefits include the deduction of interest from tax (Onofrei et al., 2015).

On the other hand, the pecking order theory posits that a firm’s choice of financing is in preferential order; internal funds, debt financing and then equity financing (Adair & Adaskou, 2015). Companies prefer debt financing to equity (Hang et al., 2018). As regards to pecking order theory, debt follows after considering the retained earnings of firms, and then ordinary shares (Orlova et al., 2020). Table 1 shows a summary of previous literature on leverage that have been reviewed, including the title, country, methodology, and findings. Based on the aforementioned, this study contributes to the literature on the determinants of financial leverage practices in Nigeria, both in local and foreign firms. It further explores the moderating effect of such foreign ownership on the determinants of financial leverage and offers new insights to understand why such factors affect Nigerian firms differently.

2.1. Profitability and Leverage

The common belief is that profitable firms tend to have more debt financing, but most of the empirical evidence suggests otherwise (Eckbo & Kisser, 2021). Instead, highly profitable firms tend to borrow less (Frank & Goyal, 2014). Sikveland and Zhang (2021) clarify that there are more earnings retained from profitable firms, which will lessen the chances of embarking on debt financing because firms usually consider their internal funds first before external. The majority of the studies reviewed reported profitability as having a negative effect on leverage (Al-Ahdal et al., 2022; Duarte et al., 2021; Zeitun & Goaied, 2021). Although there are few other reported positive effects (Fitzgerald & Ryan, 2018; Gulzar & Haque, 2022; Jahanzeb et al., 2015). Based on the above previous studies and supported by pecking order theory, the below hypothesis is proposed:

H1: Profitability has a negative significant impact on leverage.

2.2. Growth and Leverage

There is a higher need for external funds for firms with high growth prospects (Ghose & Kabra, 2020). Munisi (2017) is of the opinion that lenders perceive high-growth firms as being able to generate future positive cash flow which will enable them to service their debt and as a result, they easily lend funds to those types of firms. The majority of the studies reviewed reported mixed results, as some reported positive effects (Kizildag & Ozdemir, 2016; Li & Stathis, 2017; Rehman et al., 2016) and others negative effects (Guner, 2016; Mateev et al., 2012; Sikveland & Zhang, 2021). Based on the above previous studies and supported by the pecking order theory of a positive effect, the below hypothesis is proposed:

H2: Growth has a positive significant impact on leverage.

2.3. Asset Tangibility and Leverage

Collaterals are usually involved in borrowing, and tangible assets serve as one in which firms place as collateral in a way to assure the lenders of recovering their borrowed finance from creditors, on one hand (Munisi, 2017). The majority of the studies reviewed, including more recent ones, reported a positive effect (Bilgin & Dinc, 2019; Bolarinwa & Adegboye, 2020; Hando & Sharma, 2014), while few others reported a negative effect (Jahanzeb et al., 2015; Mateev et al., 2012; Prime & Qi, 2013). Based on the above previous studies and supported by the pecking order theory and trade-off theory of positive effect, the below hypothesis is proposed:

H3: Asset tangibility has a positive significant impact on leverage.

2.4. Liquidity and Leverage

The pecking order theory explains that firms fund their investment using internal funds in the form of liquidity before opting for external funding/borrowing. This situation will see debt decrease with an increase in liquidity (Onofrei et al., 2015; Zafar et al., 2019).

The majority of the studies reviewed reported liquidity having a negative effect on leverage (Bhat et al., 2020; Bolarinwa & Adegboye, 2020; Dakua, 2018; Jahanzeb et al., 2015; Onofrei et al., 2015; Prime & Qi, 2013; Rehman et al., 2016; Serghiescu & Vaidean, 2014; Zafar et al., 2019), while few other studies have recorded positive effects (Al-Ahdal et al., 2022; Hando & Sharma, 2014; Zeitun & Goaied, 2021). Based on previous studies and supported by the pecking order theory, the below hypothesis is proposed:

H4: Liquidity has a negative significant impact on leverage.

2.5. Cash Holdings and Leverage

According to Sanchez-Vidal (2014), cash is an internally generated resource, which, if sufficient, would result in lesser external finance such as debt. With this regard, Lian et al. (2011), Sanchez-Vidal (2014), Proenca et al. (2014), Magerakis et al. (2015) and Jumah et al. (2023) found that more cash holdings are related to less leverage, which means that cash holding has a negative impact on financial leverage. Therefore, and supported by the pecking order theory, the below hypothesis is proposed:

H5: Cash holdings have a negative significant impact on leverage.

2.6. Capital Expenditure and Leverage

Capital expenditure is an outflow which will result in increased leverage (Kizildag & Ozdemir, 2016). A study was carried out in Jordan by Khasawneh and Staytieh (2017) using fixed effect regression. It was found that capital expenditure positively affected leverage. A similar study was carried out on firms in the United States by Kizildag and Ozdemir (2016) for the period between 1990 and 2015, and the same positive effect was reported. Chang et al. (2014) studied the capital structure of China firms and its determinants, covering the period between 1998 and 2009. The study revealed a negative effect between capital expenditure and leverage. This finding was supported by Li and Stathis (2017) who studied Australian firms and found negative effects as well.

Based on the above previous studies and supported by the pecking order theory (positive effect), the below hypothesis is proposed:

H6: Capital expenditure has a positive significant impact on leverage.

2.7. Dividends and Leverage

Dividends, which are sourced from internally generated funds, tend to reduce debt with an increase in dividends. Just like the pecking order theory posits that firms utilize internal funds for investment first before considering external funds.

A study was carried out on Pakistan firms by Jahanzeb et al. (2015) for the period between 2003 and 2012. The study looked at dividends and leverage and the findings reported the existence of a positive effect. Do et al. (2019) carried out a similar study on Taiwanese firms and found a positive effect. This was supported by the findings of Yamada (2019) who studied Japanese firms. Using quantile regression, Sanchez-Vidal (2014) carried out a study on leverage determinants in Spanish firms. The study evidenced a negative effect of dividends on leverage. This finding was supported by El-Khatib (2017).

Based on the above previous studies, the below hypothesis is proposed:

H7: Dividend has a negative significant impact on leverage.

2.8. Foreign Ownership and Leverage

Most of the reviewed studies reported foreign ownership has a negative effect on leverage (Gupta et al., 2020; Khasawneh & Staytieh, 2017). There are also some that recorded positive effects as well (Do et al., 2019). Based on the above previous studies and supported by the pecking order theory, the below hypothesis is proposed:

H8: Foreign ownership has a negative significant impact on leverage.

This study has several contributions, including the expansion of the literature on the determinants of financial leverage practices in Nigeria, and whether the use of debt financing differs between locally owned companies and MNCs. It further explores the moderating effect of such foreign ownership on the determinants of financial leverage and offers new insights to understand why such factors affect Nigerian firms differently.

Materials and Methods

3.1. Data and Variable Descriptions

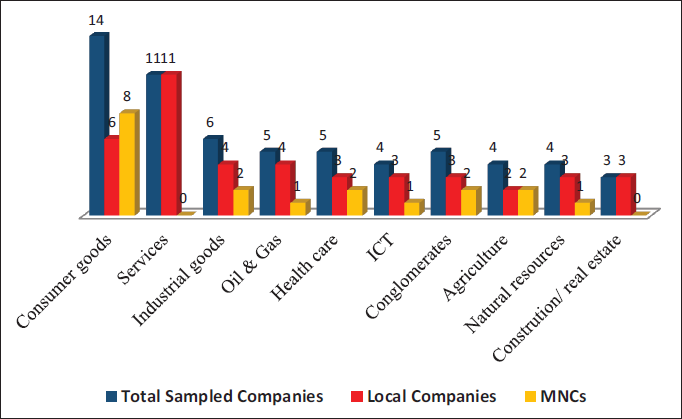

Quantitative research was employed, and secondary data were collected from the Nigerian Exchange Group (formerly Nigerian Stock Exchange) for the period 2011–2021. The chosen period of study was informed by the need to take into consideration the era of recession in Nigeria between 2011 and 2015. Also, at the time of data collection, most of the companies had 2021 as their latest annual report. The study considered all the companies listed in the Nigerian Stock Exchange, which amounted to 156 as of January 2023. The Nigerian Stock Exchange classified companies into 11 categories: conglomerate, healthcare, agriculture, construction/real estate, financial services, consumer goods, information and communication technology, industrial goods, natural resources, oil and gas and services. The criteria for the selection of the companies for the study were that the companies must have complete data, especially for leverage all through the period of study (2011–2021). Financial service firms were excluded from the study due to their peculiarities and also avoiding the mixture of both financial and non-financial firms (Ezeoha & Okeke, 2021). Using these criteria, the total sample amounted to 61 companies, out of which 42 are local companies and 19 are foreign companies (see Figure 1).

Number of Sampled Companies.

Number of Sampled Companies.

Figure 1 shows the classification of the non-financial firms (all firms, local and foreign firms) in Nigeria and also the number of firms selected from each classification based on the criteria. The empirical analysis was conducted to determine firm characteristics and their effects on corporate leverage, in which variable definitions and measurements can be found in Table 2.

Summary Table of Literature.

Variable Measurements.

3.2. Empirical Model

The study adopted a baseline model and implemented a panel regression analysis, since we have a panel data set of many companies over several years, proposing that leverage is a function of profitability, firm growth, liquidity, asset tangibility, capital expenditure, dividend per share, cash holding, foreign ownership, firm size and firm age. Below is the equation:

A second model was proposed to capture the interaction of foreign ownership. As pointed out by Baron and Kenny (1986), the moderating effect could take the form of an interaction, that is to say, the product of the independent variable and the moderating variable, and is stated below:

where,

Dependent variable: LEV: Leverage

Independent variables: ROA: Return on assets, GRW: Firm growth, TANG: Asset tangibility, LQ: Liquidity, CAPEX: Capital expenditure, DPS: Dividend per share, CASH: Cash holding

Moderating variable: FO: Foreign ownership

Control variables: FS: Firm size, FA: Firm age

Eventually, the generalized method of moments (GMM) was adopted. This was a result of the presence of endogenous variables and serial correlation from the estimated ordinary least squares (OLS) model (Bolarinwa & Adegboye, 2020; Gulzar & Haque, 2022).

It should be noted here that all variables have been winsorized to eliminate outliers so that outliers have no adverse impact on descriptive statistics and regression analysis below.

4.1. Descriptive Statistics

This section presents the descriptive statistics for all firms (61 firms) (see Figure 2), as well as for local firms (42 firms) and MNCs (19 firms) (see Figure 3) over the period 2011–2021.

Average Leverage for All Firms.

Average Leverage for All Firms.

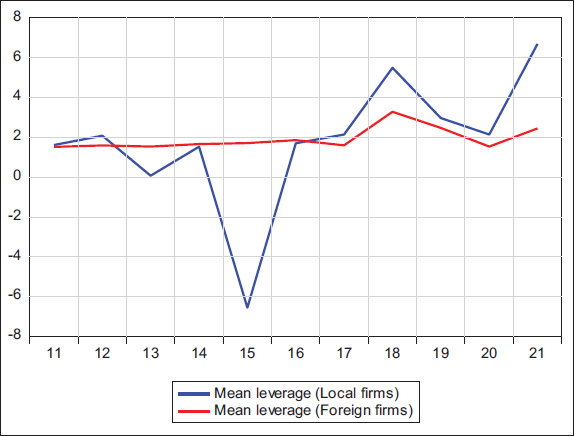

Average Leverage for Local and Foreign Firms.

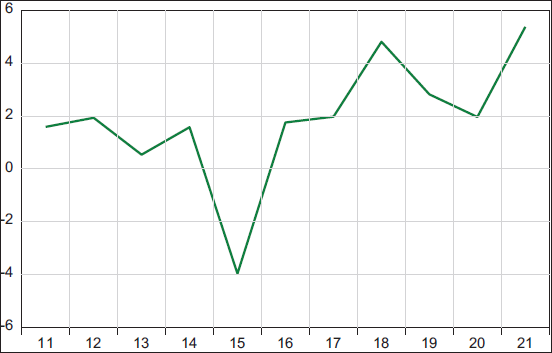

Figure 2 shows the average leverage of the total sampled firms under study from 2011 to 2021. From observation, there was an increase in debt financing from 2011 to 2012, then a reduction from 2012 to 2013, and increased again from 2013 to 2014. It dropped drastically from 2014 to 2015, recording the least debt financing period. An increase was experienced from 2015 to 2018 and dropped again from 2018 to 2020. Between the periods of 2020 and 2021, it increased again, and this time, experienced the highest level of leverage. This highest level of leverage can be attributed to the COVID-19 pandemic, which affected businesses adversely and resulted in the firms engaging in higher debt financing to relieve themselves from the shock of the pandemic. Notably, the debt financing practices of non-financial firms in Nigeria have an unstable pattern and this is due to the changing dynamics of businesses in Nigeria.

Figure 3 shows a comparison of the average leverage of local firms and that of foreign firms (MNCs) for the period between 2011 and 2021. From observation, the local firms had so many fluctuations in their leverage pattern when compared with that of the foreign firms which had quite a stable leverage pattern. Also, the local firms had the least leverage in 2015 and also the highest leverage in 2021.

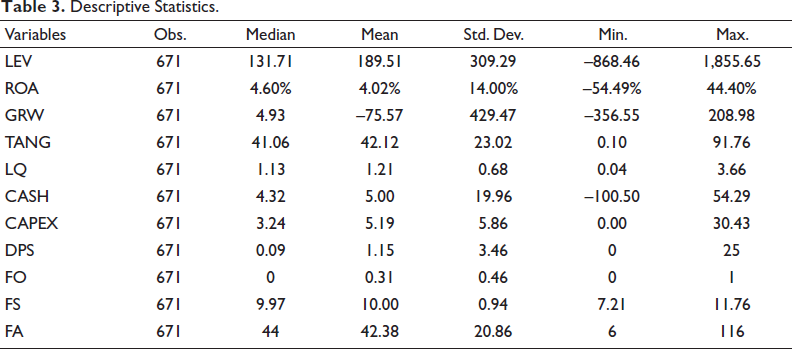

Table 3 reveals the summary statistics of the variables for all sampled firms. It can be observed that all non-financial firms have a leverage of 189.5 on average, which indicates a reliance on debt financing, while the average return on assets is around 4% for the whole sample. On the other hand, growth on average was –76, ranging from –356 to 209, which indicates huge deviations between firms, while liquidity has an average of 1.21:1 only across all firms, ranging from around 0 to 3.66:1. Foreign ownership averaged 31, while firm age averaged 42 years, ranging from 6 to 116 years.

Descriptive Statistics.

Asset tangibility averaged 0.421, ranging from 0.0008 to 0.966. Cash averaged 0.045, ranging from –1.961 to 0.688. Capital expenditure averaged 0.053, ranging from 0 to 0.655. The dividend per share averaged 1.345 naira per share, ranging from 0 to 68.197 naira per share.

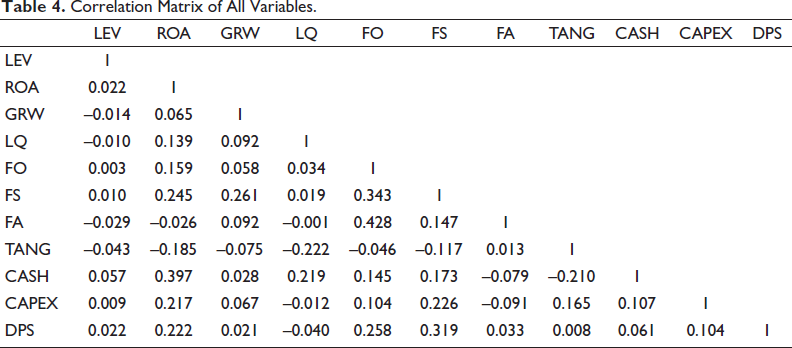

Table 4 shows the correlation matrix of all variables used in the study. All the variables reported values less than 0.08, as the highest correlation is 0.428 between firm age and foreign ownership. This implies the non-existence of a strong correlation among the variables under study (Okeke et al., 2022).

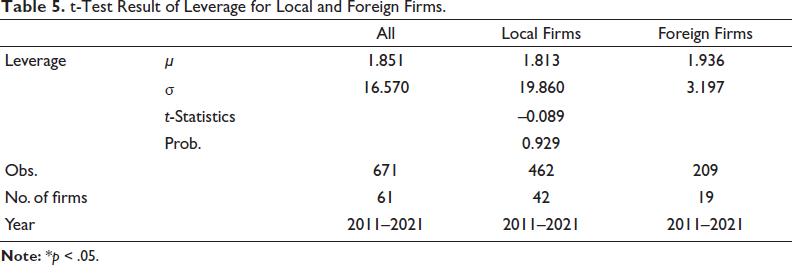

To determine the difference in the debt financing practices of local and foreign firms, and if it is significant, t-test statistics of mean difference were carried out. Table 5, which has the result in the display, revealed that the average leverage of local firms of 1.813 is not statistically different from that of foreign firms of 1.936 (t-statistic = –0.089, P<t> = 0.929). The implication is that both local firms and foreign firms in Nigeria do not employ different debt financing practices and also foreign firms employ more debt financing (1.936) compared to the local firms (1.813).

Correlation Matrix of All Variables.

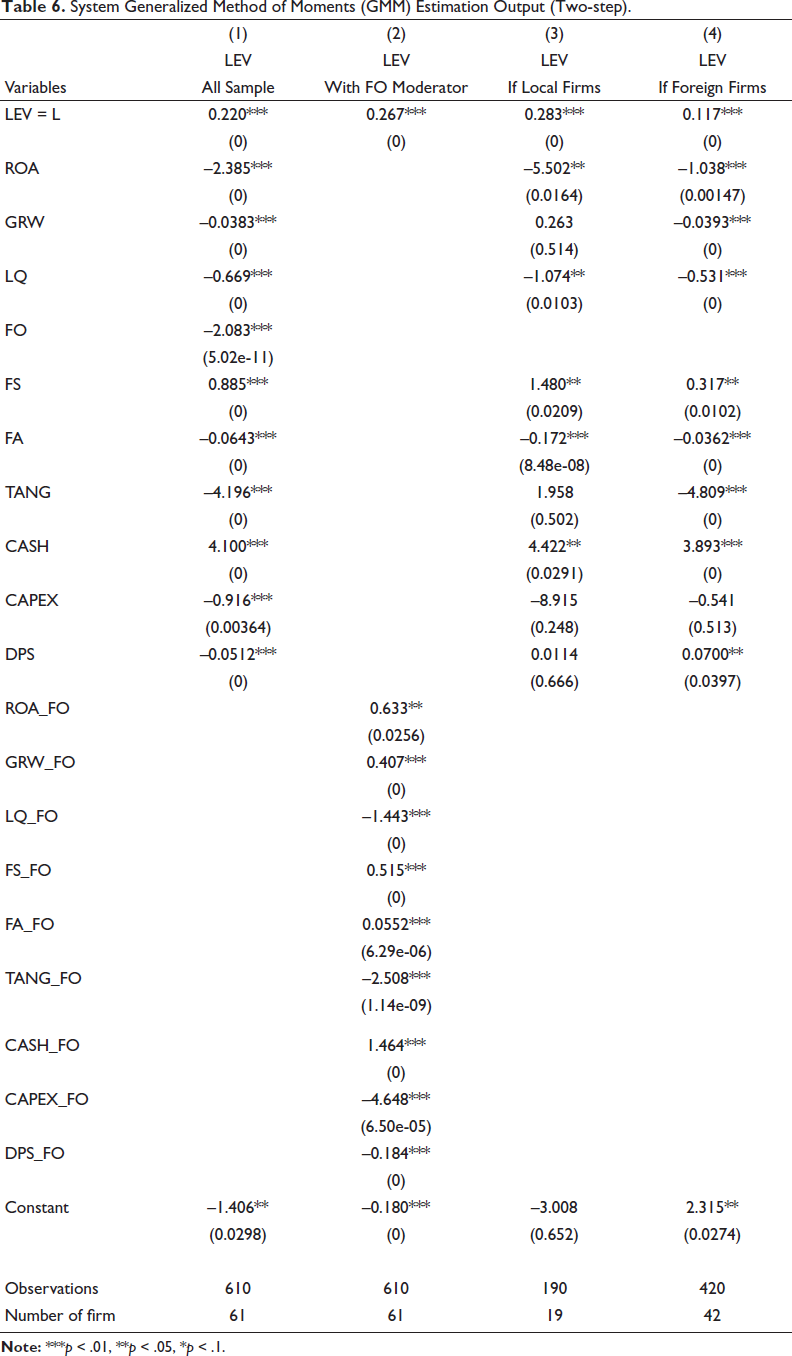

The GMM estimation, as shown in Table 6, indicates the assumptions of the GMM estimation were met. First, the number of cross-sections should be greater than the time (N = 61, 42, 19, for the different samples; T = 11) (Ezeoha & Okeke, 2021). Second, the use of instrumental variables must be exogenous variables and the number of instrumental variables greater or equal to the right-hand side variables (Arellano & Bond, 1991; Blundell & Bond, 1998). Also, the choice of GMM being the most appropriate regression model was informed by the works of previous studies and the understanding that the issue of endogeneity and multicollinearity are usually encountered by firm-specific characteristics variables (Gulzar & Haque, 2022; Yamada, 2019).

t-Test Result of Leverage for Local and Foreign Firms.

System Generalized Method of Moments (GMM) Estimation Output (Two-step).

Table 6 reveals the GMM estimation outputs for the main relationship, including those for the sub-samples (local/foreign firms), as well as the moderating effect of foreign ownership.

4.2. Discussion of Findings

Table 6 shows the regression results, where profitability was found to have a negative and significant effect on cash leverage, which indicates that 1% more profit motivates around 2.385% decrease in leverage. This result confirms the first hypothesis (H1), supports the pecking order theory and is consistent with most of the reviewed works (Bhat et al., 2020; Bolarinwa & Adegboye, 2020; Chen et al., 2021; Duarte et al., 2021; Ghose & Kabra, 2020; Gupta et al., 2020; Zeitun & Goaied, 2021). It is also clear that such a negative relationship holds in both local and foreign-owned firms, even that much higher impact has been noticed in local firms.

Firm growth, on the other hand, has a negative and significant impact on leverage, in which every 1% extra growth will lead to around 0.0383% less leverage. This result rejects the second hypothesis (H2), does not support the pecking order theory and is inconsistent with other studies (Rehman et al., 2016; Zafar et al., 2019). Having then compared the results based on foreign ownership, a similar impact was reported in foreign-owned firms, while a positive impact has been found in local firms. This might indicate that local firms with higher growth rates tend to rely more on debt rather than equity.

Table 5 also shows that asset tangibility affects leverage negatively, with an insignificant impact in local firms but a significant one in foreign-owned firms, which implies that firms tend to decrease their leverage 4% times as tangible assets increase by 1%. This result confirms the third hypothesis (H3), which does not support the pecking order and trade-off theory but is consistent with previous studies (Buvanendra et al., 2017; Munisi, 2017).

Liquidity has a negative and significant impact on leverage, which suggests that a 1% increase in liquidity surprisingly drives a 0.669% decrease in leverage. This finding confirms the fourth hypothesis (H4), supports the pecking order theory and is consistent with most of the previous literature (Bhat et al., 2020; Bolarinwa & Adegboye, 2020; Zafar et al., 2019).

Cash holdings, on the other hand, have been found to have a positive and significant effect on leverage in both local firms and foreign-owned firms, which implies that 1 unit higher cash holding increases leverage by 4 units. This result rejects the fifth hypothesis (H5) as well, supports the tradeoff theory and is not consistent with the findings of Lian et al. (2011), Sanchez-Vidal (2014), Proenca et al. (2014), Magerakis et al. (2015) and Jumah et al. (2023). This might indicate that rather than depending on excess cash for investment purpose, managers tend to accumulate it for a different purpose while depending on more debt financing for the firm’s investment.

Capital expenditure has been found to have a negative and significant impact on leverage, suggesting that leverage is decreased by 0.916 units with every 1 unit increase in capital expenditure. This finding rejects the sixth hypothesis (H6), does not support the pecking order theory and is inconsistent with previous literature (Khasawneh & Staytieh, 2017; Kizildag & Ozdemir, 2016). Again, this might be because companies with more capital expenditure avoid borrowing more money as it has already served its purpose of acquiring capital expenditure which can serve its purpose as an asset (generating income).

Moreover, dividends per share have a negative and significant impact on leverage, which implies that 1% extra dividends per share drives around a 0.05% decrease in leverage. This finding confirms the seventh hypothesis (H7) and is consistent with previous studies (El-Khatib, 2017; Sanchez-Vidal, 2014).

Finally, foreign ownership shows a negative and significant impact on leverage, which implies that leverage is 2% less in foreign-owned firms compared to domestic firms in Nigeria. This finding confirms the eighth hypothesis (H8), supports the pecking order theory and is consistent with previous studies (Gupta et al., 2020; Khasawneh & Staytieh, 2017). On the other hand, firm size has a positive and significant impact, while firm age has a negative and significant impact on leverage, for both local and foreign-owned firms in Nigeria.

Concerning the moderating impact on foreign ownership, measured by the coefficient of the interaction (Baron & Kenny, 1986), the results show that profitability, growth rate and firm age have now a positive impact on leverage when moderated by foreign ownership, while all other firm characteristics still have similar impact with/without moderating by foreign ownership, but with different coefficients. This indicates that foreign ownership moderates the way that firm characteristics affect corporate leverage practices.

This study sought to determine firm characteristics and leverage in Nigeria and the moderating effect of foreign ownership. Data were collected from 61 non-financial firms listed in the Nigerian Stock Exchange, with the exclusion of financial firms because of their peculiarity, for a period of 11 years (2011–2021). GMM estimation technique was employed, due to the existence of endogeneity and serial correlation from the OLS estimation technique. The study also separated the local firms from the foreign ones to look at the different practices and found out that foreign firms employed more debt financing than local firms. The key findings of the study show that all firm characteristics for the study influence leverage. Profitability, firm growth, liquidity, cash and capital expenditure drive leverage, whereas foreign ownership, asset tangibility and dividend negatively affect leverage in general. For local firms, more dividends, capital expenditures and cash result in having more leverage, whereas profitability, firm growth, liquidity and asset tangibility discourage leverage. For foreign firms, all firm characteristics except asset tangibility and dividend drive leverage. This study contributes to the literature on the determinants of financial leverage practices in Nigeria, both in local and foreign firms. It further explores the moderating effect of such foreign ownership on the determinants of financial leverage.

Concerning policy implications, the results will assist managers in Nigeria to understand the determining factors of leverage, and to consider the accruing benefits of debt financing which is to take advantage of interest for tax deduction purposes. It will also be insightful to lenders of capital who will be more informed in their consideration for lending capital to firms in Nigeria. Investors will also draw insight from the study and be more informed in their investment decisions. For regulatory bodies such as the Securities and Exchange Commission, Nigeria, the study will give them an insight into the regulation of non-financial firms in Nigeria as regards leverage, both local and foreign firms.

Finally, despite the significant findings and insights, this study has some limitations that further study should consider. One suggestion is to measure the ratio of foreign ownership rather than simply a binary measure. Also, this study has used foreign ownership as a moderator, and further research could use other macroeconomic moderators because debt financing is affected by the economic environment of a country.

Footnotes

Authors’ Contribution

Obiajulu Chibuzo Okeke: Conceived the research idea, designed the study, reviewed literature, and drafted the manuscript. Tony Abdoush: Conducted data analysis, drafted the results and discussion section, and provided critical revisions.

Alpha Shekwonya Jemutu: Collected data and contributed to manuscript writing.

Wisdom Okere: Contributed to manuscript writing.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Ethical Declaration

The authors abide by all the ethics involved in this academic work and have not submitted it to any other journal.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.