Abstract

Capital structure choice is a corporate decision which provides a combination of securities used to finance the investment requirements (Myers, 2001). That the ownership of a firm influences its decision-making process is a well-accepted economic proposition. Due to liberalization and continuous measures initiated by the Indian government to make India more business-friendly, foreign ownership has assumed a prominence in many Indian firms. In this regard, this article aims to examine the impact of foreign ownership on the financing mix, employing the data of non-financial firms constituting the Nifty 200 index, for the period 2007–2018; the data have been extracted from Bloomberg® and Ace Equity®. Using the generalized method of moments (GMM) technique for empirical analysis, the study observes that there is a statistically significant negative relationship between foreign ownership and leverage.

Keywords

Introduction

International trade and business activities have grown speedily due to rapid integration of world economies, which is a result of liberalization of their trade and payment regimes. Due to globalization, the notion of foreign direct investment (FDI) emerged (Kaur et al., 2013b). As defined by United Nations Conference on Trade and Development (UNCTAD):

Foreign direct investment (FDI) is an investment involving a long-term relationship and reflecting a lasting interest and control by a resident entity in one economy (foreign direct investor or parent enterprise) in an enterprise resident in an economy other than that of the foreign direct investor (FDI enterprise or affiliate enterprise or foreign affiliate).

1

Economics suggests that FDI enhances the growth of the recipient economy directly by way of adding to the capital formation and indirectly by intensifying competition, providing sophisticated technology and inducing human capital, which, in turn, is likely to increase productivity. To realize these potential benefits associated with FDI, both the developed and developing countries have become more receptive to the influx of FDI since 1980.

FDI in India

India welcomed FDI after the initiation of economic reforms in 1991 (Kaur et al., 2013a). The Government of India (GoI) is taking measures towards enhancing the sectoral limit of existing sectors, opening new sectors for FDI and simplifying the FDI policies. The revised FDI policies are directed towards enticing foreign financiers by creating conditions for ease of doing business, to garner investments. According to India Brand Equity Foundation (IBEF), to avail the benefits of relatively lower wages, special investment privileges such as tax exemptions, etc., foreign companies are attracted to invest in India. FDI acts as a catalyst in the economic growth of India and also provides (non-debt) financial resources for its economic development. 2 As per the latest database of UNCTAD, FDI flows to India have escalated by 6 per cent from 2017, and reached the level of US$42 billion, in 2018; India is among the top 20 destinations for FDI flows. 3

Foreign ownership has become a prominent feature of many Indian firms as a result of continuous endeavours by the Indian government to make it more business-friendly. It is usually believed that the ownership of a firm influences its decision-making process. Dunning (1988) posits that foreign companies are superior to domestic counterparts in certain areas, and with FDI flowing into their country, the domestic company’s output gets affected. Through FDI-related spillover effects, the FDI directly as well as indirectly impacts the output of domestic companies. The existing literature on FDI provides mixed evidence on productivity spillover effect associated with foreign investment; Branstetter (2006) and Meyer and Sinani (2009) established a positive link, while Aghion et al. (2009) reported a negative impact. Girma et al. (2015), examining the effects of FDI on firm productivity, show that these effects vary with different levels of foreign presence within a cluster.

With the advent of foreign companies, the level of competition in the host country’s market surges and, in turn, affects the domestic firms’ profitability and limits its growth opportunities. Further, several studies like Chakraborty (2010), Margaritis and Psillaki (2010), Kayo and Kimura (2011), Handoo and Sharma (2014) and Chadha and Sharma (2015) determine profitability and growth opportunities as crucial factors affecting corporate financing policy. ‘Capital structure refers to a mix or proportion of different sources of finance (debt and equity) to total capitalization’ (Khan & Jain, 2019). Financing decision holds a significant place in corporate financial management because of its impact on both risk and return of equity shareholders of the firm. Different companies have different objectives, which, in turn, influences their financing mix (the composition of debt and equity). There cannot be an optimal financial structure for all times; it evolves incessantly, and the top management must persistently take into account firm-specific, industry-specific, macroeconomic factors, the state of capital market and government regulations in this dynamic environment. Brander and Lewis (1986) have discussed the interconnectedness of financial decision and output. Wang and Wang (2015) have highlighted the financial benefits of foreign ownership.

Velde and Morrissey (2001) observe that the extant literature conventionally refers to FDI while identifying the effects of foreign ownership. Within the context of this article also, we analyse the impact of foreign ownership, focusing on FDI, similar to studies like Vishwasrao and Bosshardt (2001), Teixeira and Lehmann (2014) and Anwar and Sun (2015).

The rest of the study has been organized as follows: the second section reviews the relevant literature; the third section covers the objective and rationale of the study. The subsequent section describes the research methodology (the data source, sample frame, description of variables and the empirical model). The fifth section reports the results of the analysis, and the last section presents the discussion, concluding observations and managerial implications.

Literature Review

The global trends indicate that FDI flows to developing nations ballooned during the late 1990s. This could be attributed to the liberal laws (brought at a fast pace) related to the FDI laws of these nations. The foreign investment’s effect on the actions of domestic companies is rising in these emerging markets as a result of flooding foreign investment inflows (Vo, 2011).

Most of the earlier studies look into foreign ownership’s effect on productivity or firm performance. However, there is a dearth of research focusing on the link between foreign ownership and financing mix, especially in the Indian context. Bhaduri (2002), Chakraborty (2010), Handoo and Sharma (2014) and Chadha and Sharma (2015), among others, have explored the determinants of financial structure in the case of Indian firms, but hitherto, none of them has analysed the impact of foreign ownership on leverage.

The extant literature provides mixed evidence regarding the impact of foreign ownership on leverage. The following sections cover the summary of select studies.

Studies Showing a Positive Relationship

Phung and Le (2013) have investigated the effect of foreign ownership on financial structure, measured as total debt to market value, for Vietnam. They hypothesized a positive relationship between foreign ownership and leverage of Vietnamese listed firms, and their empirical results suggested the same. The result indicates that foreign investors are motivated to force firms to employ more debt to mitigate the agency problem because of the issue of high level of information asymmetry in Vietnam.

Sivathaasan (2013) assesses the effect of ownership (domestic and foreign) on leverage employing data of Sri Lankan listed manufacturing firms. The outcome shows a strong positive association of foreign ownership with leverage.

Another study supporting a positive link between foreign ownership and firm’s leverage is given by Mishra (2013) based on Australian firms’ data over the period 2001–2009.

Studies Reporting a Negative Relationship

Li et al. (2009) delve into the effect of ownership structure and institutional development on the financing decisions of Chinese firms. The results indicate a negative association between foreign ownership and all the measures of leverage used. Explanations used to justify the results are: (a) foreign-owned firms in China are to pay lower corporate tax rates than others due to which they are not incentivized to use debt for the purpose of tax-saving on debt (as interest on debt is a tax-deductible expense); and (b) firms with high foreign ownership, because of their relationship and reputation, enjoy more varied funding channels for accessing capital than others.

Gurunlu and Gursoy (2010) assess foreign ownership’s impact on Turkish firms’ leverage. As foreign owners bring in a lot more things apart from capital, like technology, know-how, access to a new market, new distribution channels and new creditors, the study expected a positive link between foreign ownership and market leverage and book leverage. However, their results indicate that foreign ownership is significantly and negatively related to long-term leverage.

Chen and Yu (2011) examine the effect of exports and FDI on debt–equity ratio for firms in emerging markets. The hypothesis for the study is formulated from an agency theory perspective and has been empirically tested on a sample comprising 566 Taiwanese firms. Their outcome suggests a negative interaction effect of export intensity and the extent of FDI on the MNCs’ capital structure, which points out to the fact that there is a steep rise is agency and monitory cost when companies’ international operations become excessively complicated.

Anwar and Sun (2015) analyse the effect of foreign presence on Chinese companies’ leverage. To prove association between foreign presence and firms’ leverage, they have proposed a theoretical model by combining aspects of international business and financial theory. Using different regression approaches for empirical analysis, they observe that foreign presence has a negative and statistically significant effect on leverage.

Le and Tannous (2016) study the impact of ownership structure (managerial, foreign, state and large ownership) on a corporate’s financing decision, of non-financial listed companies in Vietnam from 2007–2012. They conclude that foreign ownership negatively affects corporate leverage.

Studies Showing No Significant Relationship

Zou and Xiao (2006) examine the financing decision of Chinese listed companies over the period 1997–2000. They have hypothesized a positive effect of foreign ownership on firms’ leverage based on the belief that foreign investors are more vulnerable to the information asymmetry issue than the other investors in emerging economies, due to which foreign investors push firms to employ more debt, which can act as a monitoring mechanism of management. Nonetheless, they did not find a significant impact of ownership (foreign, state and legal person) on leverage.

Huang et al. (2011) have analysed the ownership structure’s effect by using the Chinese listed firms’ data for 2002–2005; they observe that ownership structure does not have any significant influence on corporate debt decisions. However, after segregating the firms based on leverage ratios (high and low), they report that foreign ownership positively influences corporate’s debt–equity ratio in highly leveraged firms. Nonetheless, they explain that foreign investors are usually institutional investors and can aptly monitor the managers. As an outcome, foreign ownership assists in controlling the overinvestment issue of managers or reducing the agency cost between shareholders and managers. Hence, leverage and foreign ownership might act as deterrents for the manager from indulging in activities that are not in the interest of the shareholders.

Objective of the Study

Among the corporate policies, the capital structure decision, relating to debt and equity, is one major decision (Brounen et al., 2006; Chadha & Sharma, 2016). Given the soaring inflow of FDI in the Indian economy, the study seeks to examine how foreign ownership is impacting the financial structure of Indian firms. While considerable attention is paid to analyse the link between ownership structure and firm performance, relatively less emphasis is placed on the assessment of its impact on the capital structure.

Considering the relevance of both FDI and financing decision, the objective of this article is to assess the foreign ownership’s effect on the financing mix of Indian companies.

Rationale of the Study

Vo (2011) finds that the effect of foreign investment on actions of domestic companies is rising due to burgeoning foreign investment flowing into emerging markets. Given that: (a) the financing decision and the output of the firms are interconnected; and (b) FDI impacts the firm output, it follows that the presence of foreign ownership in a company can also affect the firm’s capital structure through FDI-related spillovers. Kang and Stulz (1997) also indicate that foreign ownership is linked with leverage. By and large, in accordance with the above discussion, we can advocate that foreign ownership influences the leverage of domestic firms.

Generally, foreign ownership ensues when MNCs infuse long-term investments in a foreign country, commonly in the form of FDI. For the past three decades, India has been enacting several rules with respect to foreign ownership to attract more and more overseas investors. Consequently, foreign ownership has become an important attribute of Indian firms. Ganguli (2013) notably finds that ownership structure influences the capital structure in the case of Indian firms.

However, there is a paucity of research related to analysing the relationship between foreign ownership and financing mix. Hitherto, several studies have examined the determinants of capital structure in the Indian context, but none of the studies has examined this link.

Research Methodology

Data Source

The financial data for the study, such as short-term debt, long-term debt, total assets, tangible assets, operating earnings, sales, effective tax rate and percentage of foreign ownership have been extracted from Bloomberg® database. Ace Equity® database has also been used for collecting the data relating to incorporation date of firms.

Sample Description

We utilize a dataset comprising the top 200 companies listed on National Stock Exchange (NSE), the leading stock exchange of India. In general, large firms are more popular among foreign investors (Mishra & Ratti, 2011). Dahlquist and Robertsson (2001) notably find that firm size is a preferred trait amongst the foreign investors. They hypothesize that ‘large firms, measured by market capitalization, are better known abroad than small firms’. They are of the view that this measure is a broad proxy as size could be positively correlated with several other firm attributes that may attract foreign investors. Their results, using the data for Swedish firms, indicate that foreigners show a preference for large firms. Studies like Lin and Shiu (2003), Hiraki et al. (2003) and Kho et al. (2009) also confirm this relationship in the case of Taiwan, Japan and Korea, respectively. The NIFTY 200 Index of the NSE comprises large and mid-market capitalization companies, representing about 86.7 per cent of the free-float market capitalization of the stocks listed on NSE as on 29 March 2019. Hence, this dataset can be deemed adequate to study the relationship between foreign ownership and leverage. Non-financial firms listed on the Nifty 200 index have been considered for the purpose of the study. The study covers a time span of 12 years (2007–2018).

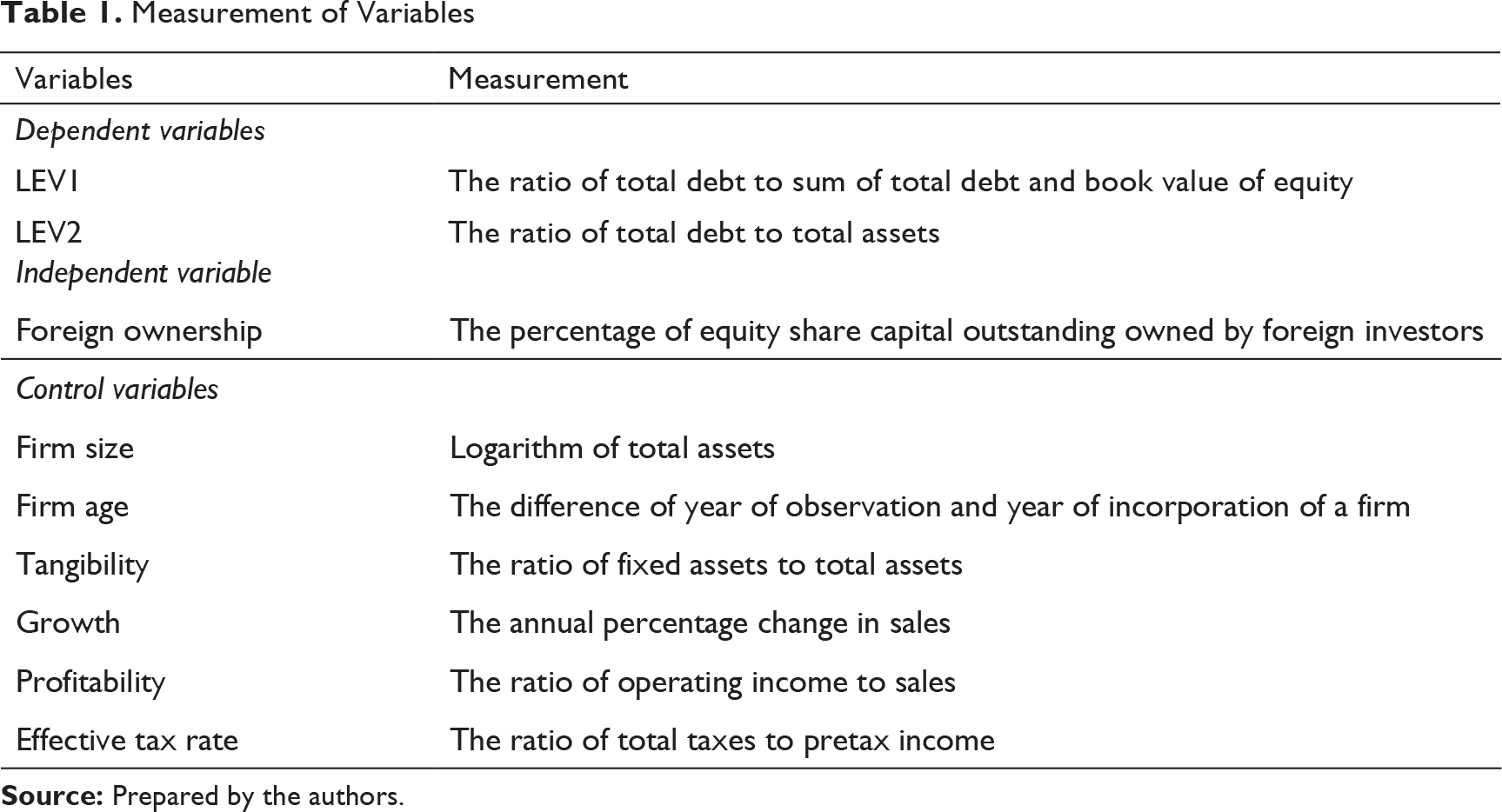

Definition of Variables

Dependent Variable

Leverage can be measured using various ratios including total debt to total assets, long-term debt to total assets and short-term debt to total assets (Céspedes et al., 2010; Chakraborty, 2010; Kayo & Kimura, 2011). Frank and Goyal (2009) employed four definitions of leverage using total debt, long-term debt, book value and market value of total assets. Rajan and Zingales (1995) defined leverage as the ratio of total debt to net assets.

Total Debt versus Long-term Debt

Most of the studies for financial structure include short-term debt; however, it forms a substantial part of total debt in the context of Indian firms. So it should be considered while measuring leverage. Also, it has been a tradition in India to employ short-term instruments, as they serve the purpose of long-term debt (Sen, 1979). This can be further substantiated with the help of Indian studies based on capital structure like Chakraborty (2010), Chadha and Sharma (2015) and Bajaj et al. (2018), which have used total debt while calculating leverage.

Book Value versus Market Value

As discussed above, various empirical definitions of leverage have been used in the literature. There exists a difference in the opinion regarding which measure is appropriate. One important distinction lies in whether the measures are based on book value or market value of equity.

There are several studies like Kayo and Kimura (2011), Mukherjee and Mahakud (2012) and Sharma and Paul (2015) that employ both book and market based measures of leverage, and some studies which only use a book-based measure of leverage like Ferri and Jones (1979), MacKay and Phillips (2005), Chakraborty (2010), Chadha and Sharma (2016), Bajaj et al. (2020), etc.

Myers (1977) suggests that managers pay attention to book leverage as assets in place can better hold up debt in contrast to growth opportunities. Barclay et al. (2006) give a similar argument supporting the view that current funds should finance assets in place instead of arbitrary growth option investments. Wide fluctuations in the financial markets and managers’ belief of uncertainty associated with market leverage reduce its usage for corporate financial decisions and encourage the application of book leverage. In line with managers’ views, Graham and Harvey (2001) note that existence of cost related to rebalancing of capital structure (as a result of equity market movements) deters firms from adjusting it regularly. Welch (2004) also notes that some authors prefer book values owing to the fact that they are less volatile as compared to market values.

In addition, book values are not only employed because of convenience, but they are also preferred over market values as while computing debt–equity ratio using market values one tends to create systematic bias in financial risk measures (Chakraborty, 1977). Moreover, book values can be employed with more certainty as compared to market values, as the latter could be influenced by many ancillary activities and the magnitude of which could be mostly unknown.

‘The ratio of total debt to total assets’ is a frequently used measure in the literature as a proxy for leverage. It signifies the percentage of assets that are financed by debt. A high percentage indicates high level of dependence on debt and, in turn, a high level of financial risk. Harvey et al. (2004) posit that it is reasonable to use debt measure based on book value as firms are more interested in book leverage ratios since bank loan covenants are written in terms of book value. Stonehill et al. (1975) observe ‘ratio of total debt at book value to total assets at book value’ as desired debt ratio by conducting a survey based on five countries. Numerous studies have employed this measure like Antoniou et al. (2006), Arslan and Karan (2006), Barclay et al. (2006), Frank and Goyal (2009), Chakraborty (2010), Chang et al. (2014), Handoo and Sharma (2014), Chadha and Sharma (2016), Bena et al. (2017) and Do et al. (2019). In view of the above, we have used book value of debt as well as book value of equity in our study.

Considering the above-mentioned points, this study has employed two measures of capital structure—the ratio of total debt to sum of total debt and book value of equity (LEV1) and the ratio of total debt to total assets (LEV2)—for checking the robustness. Here, total debt is sum of short-term debt and long-term debt; short-term debt includes short-term borrowings, lease liabilities and current portion of long-term debt, and long-term debt includes all interest-bearing financial obligations that have maturity of longer than one year.

Independent Variables

Foreign ownership is the key independent variable in this study, which is determined as a percentage of shares outstanding owned by foreign investors, consistent with most studies (Huang et al., 2011; Le & Tannous, 2016; Thai, 2017). Remmers et al. (1974) argue that different industries have varied situations; they suggest that firms within the same industry, because of similar growth rates, profitability, liquidity requirements and technology, might have similar levels of debt. Hence, industry dummies are included to subdue the industry fixed effects as a set of four-digit industry dummies; year dummies are also introduced for moderating temporal variations in the dependent variable.

Control Variables

Firm Size

The impact of firm size on debt–equity ratio is unclear. As per trade-off theory, larger companies are supposed to have a diversified business and have steady cash flows which make them less vulnerable to bankruptcy, suggesting a positive relationship between firm size and leverage (Frank & Goyal, 2009; Rajan & Zingales, 1995). Some of the other studies (Harris & Raviv, 1990; Narayanan, 1988; Poitevin, 1989; Stulz, 1990) have indicated that firm size impacts the company’s leverage positively. Empirical studies Wu and Yue (2009), Kayo and Kimura (2011) and Bhama et al. (2016) also support this positive association of firm leverage with the firm size. In contrast, as per the pecking order theory, large firms have less asymmetric information problems, so they tend to prefer equity to debt, suggesting that firm size is negatively related to leverage.

Firm Age

Frank and Goyal (2009) suggest that a firm’s age influences its financing mix through agency cost of debt. Older firms tend to enjoy low debt-related agency cost, which implies a positive link between firm age and debt level. Petersen and Rajan (1994) contend that it is comparatively easy for older firms to access debt when compared to young firms due to more networks or ties of the firm with creditors.

Tangibility

Contrasting effects of tangibility on debt ratio are provided by the existing literature. Tangible assets perform the role of collateral for borrowing money (Scott, 1977). On the one hand, both agency cost theory and trade-off theory estimate that tangibility is positively linked with leverage. On the other hand, an opposite suggestion emanates from the pecking order theory (Myers & Majluf, 1984). Empirically also, mixed indications are reported in the literature. Akhtar and Oliver (2009) concluded a positive association between tangibility and debt; however, Li et al. (2009) noted a contrasting link.

Growth

Regarding empirical evidence, mixed results are provided, while Rajan and Zingales (1995), Booth et al. (2001) and Chen (2004) report that growth positively impacts the debt–equity ratio; in contrast, Chakraborty (2010) and Kayo and Kimura (2011) conclude the opposite. As per the extant literature, there exists a relationship between growth and capital structure (Mouamer, 2011), though different theories point towards different directions. Firms having higher growth opportunities will require more funds. Agency cost theory asserts that firms with high growth opportunities may invest suboptimally, hence increasing the agency cost related to debt. This theory suggests a negative relationship between growth rate and debt; however, according to pecking order theory, growth opportunities are positively related to leverage. Myers (1984) suggests that firm with higher growth opportunities needing more funds would prefer debt, among the external sources of finance.

Effective Tax Rate

As per the theoretical estimation, a positive link exists between tax rates and tax savings in the case of debt. For this reason, tax influences leverage, and hence corporates facing higher tax rates employ additional debt for lowering the tax bills (Modigliani & Miller, 1958). Empirical studies (Gurcharan, 2010; Wiwattanakantang, 1999) also show a substantial impact of tax on leverage.

Profitability

Profitability is another element that affects a firm’s debt, but there exists theoretical disagreement regarding the link between profitability and financial structure. Internal sources of financing are used first, and then external sources of financing are employed, according to the pecking order theory. Hence, profitable firms will prefer internal financing over debt, which suggests that these companies tend to employ less debt. Most empirical studies support the pecking order theory (Booth et al., 2001; Chen, 2004). Based on the trade-off theory, Myers (1984) indicates that profitable firms can employ a higher level of debt as they have higher tax savings and lower costs of financial distress. Agency cost theory (Jensen, 1986) also predicts a similar relationship; it posits that debt can be used to govern the behaviour of managers.

Measurement of Variables

Model Specification

To empirically evaluate the effect of foreign ownership on leverage, the following dynamic capital model is adopted to circumvent the endogeneity problem:

where LEVit is the leverage of firm i at time t, LEVit–1 is the lag of leverage, FOit stands for foreign ownership of firm i at time t and Xit is a vector of control variables. This equation also includes industry dummies as dindustryi and year dummies as dyearit. Finally, an error time (εit) is also introduced to capture the effect of all omitted variables.

Analysis

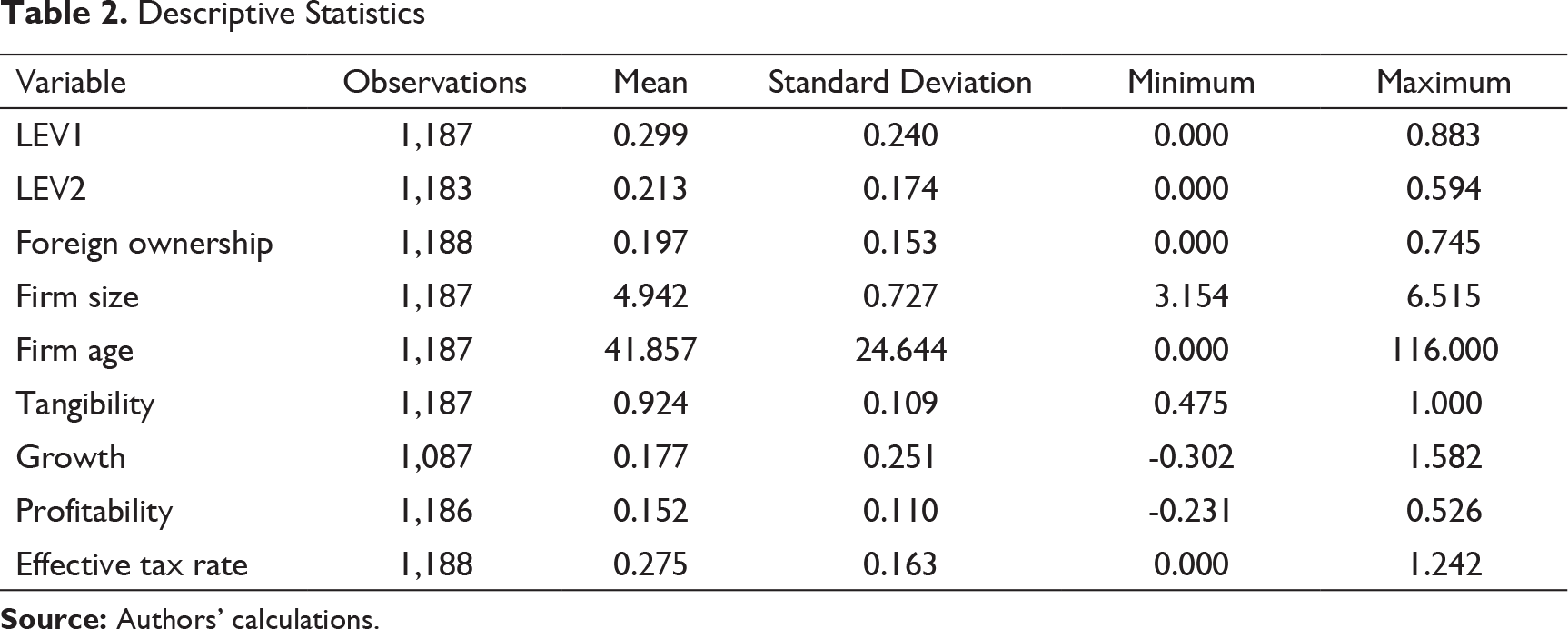

Descriptive Statistics

Table 2 gives the summary statistics for all variables used in our capital structure model for non-financial firms listed on the Nifty 200 index for the period 2007–2018. The data is strongly balanced. The means of both the measures of leverage, LEV1 and LEV2, are 0.299 and 0.213, respectively. The spread between the minimum and maximum leverage is relatively higher in the case of LEV1. The proportion of foreign ownership has a mean of 0.197, and it ranges from almost 0 to 0.745.

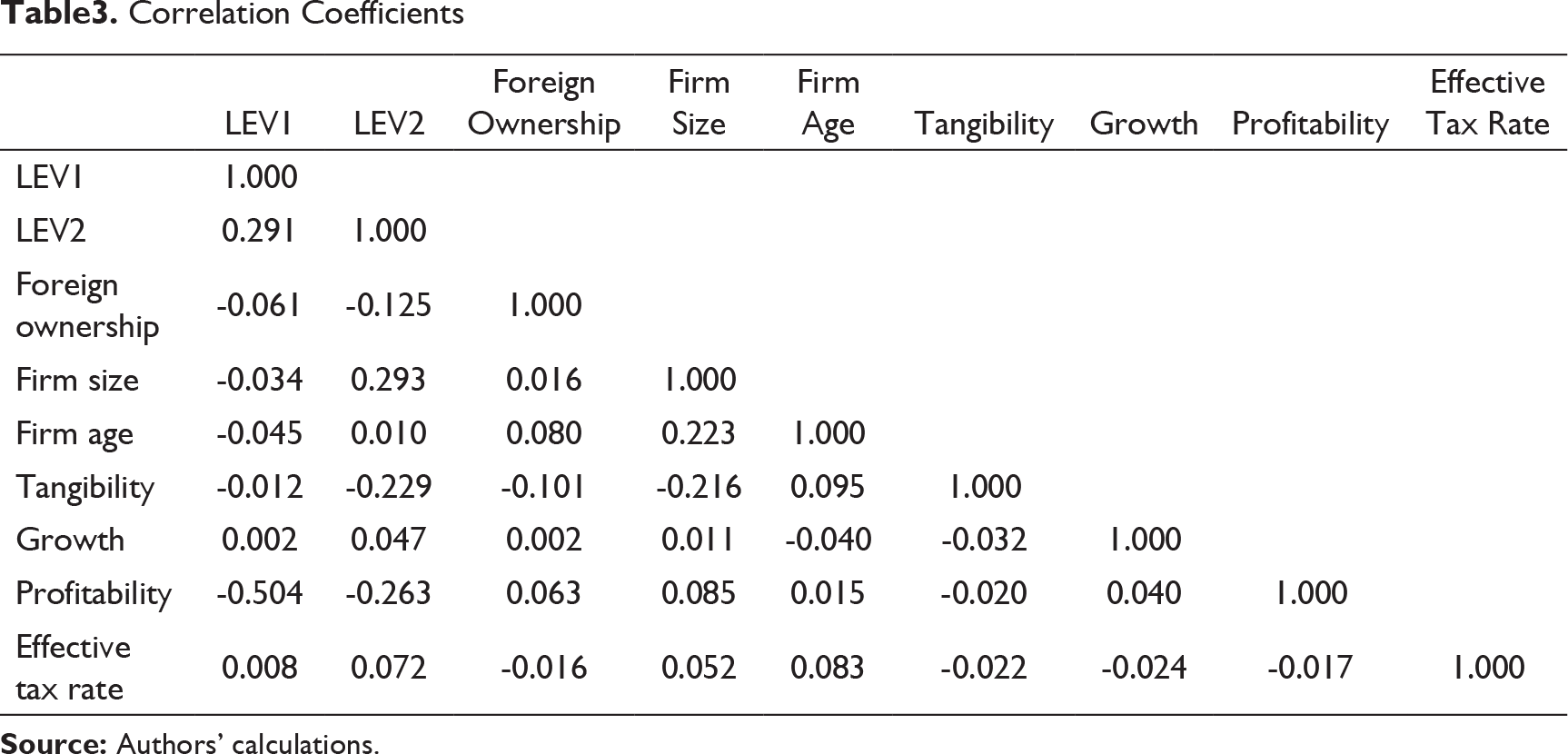

Correlation Analysis

Descriptive Statistics

Correlation Coefficients

Empirical Analysis

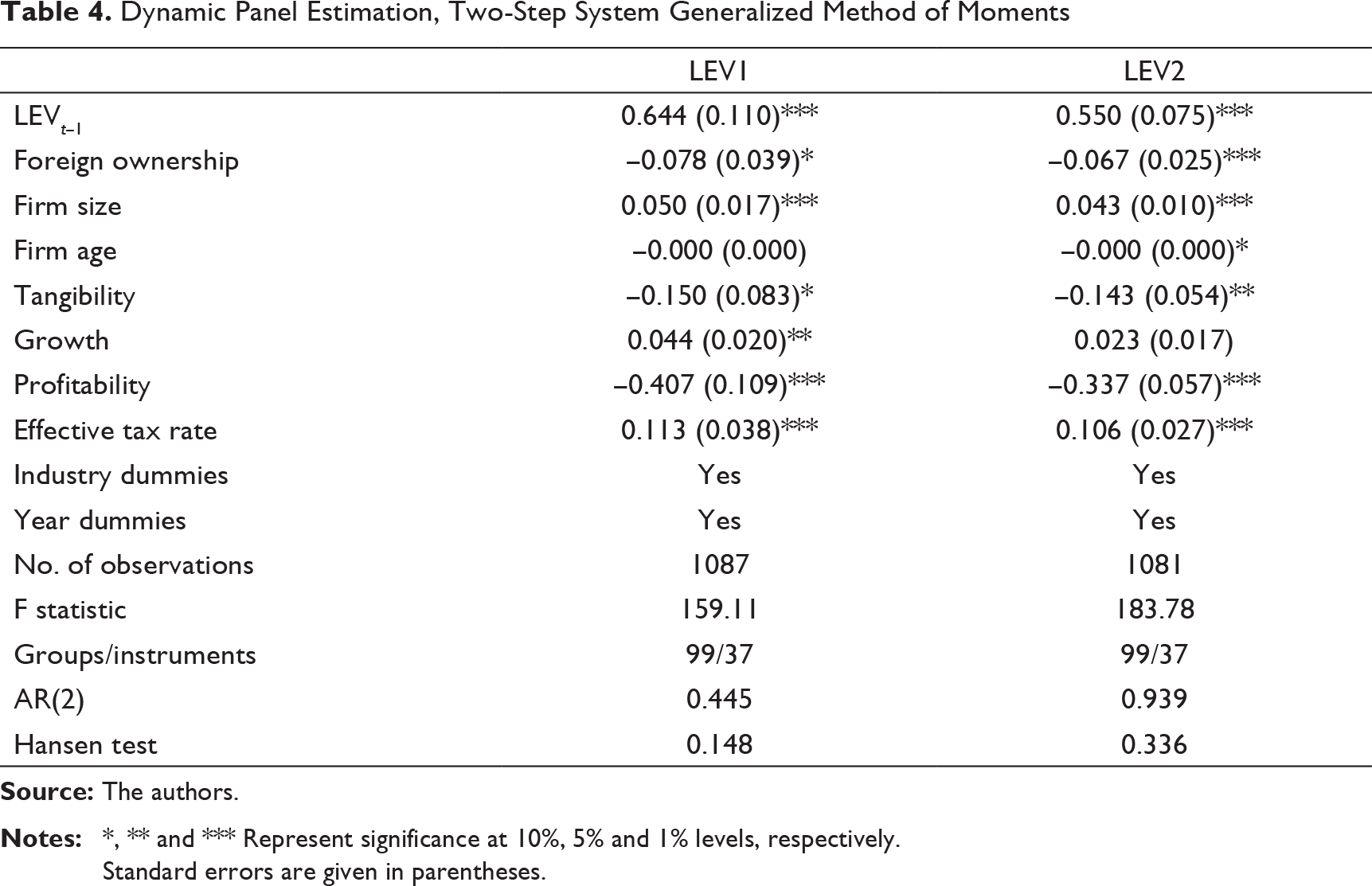

Wintoki et al. (2012) posit the presence of endogeneity while examining the relationship between ownership and financial structure. Most of the existing studies have assumed ownership structure as an exogenous variable that impacts the financing mix. However, this usual belief is being reappraised, and now it is accepted that many firm-specific factors, inclusive of leverage, influence the ownership structure. Cameron and Trivedi (2005) suggest that when the ownership framework is considered endogenous, the outcome of the earlier studies employing only pooled ordinary least squares (OLS), fixed or random effect models, to examine the link between ownership and leverage can be deceptive, notably for the short panel. To overcome this problem, some studies have advocated the adoption of instrument variables (IV) estimation. However, finding the valid instruments is not an easy task, and the IV estimators are likely to be biased in the case of weak instruments, that is, IV estimates with invalid instruments could have no improvement over OLS estimators. Hence, the Arellano and Bond (1991) method is considered as an appropriate technique for dynamic panel estimation, to avoid the endogeneity problem. However, difference generalized method of moments (GMM) is attributed to the use of poor instruments (Blundell & Bond, 1998). As a solution, Arellano and Bover (1995), as well as Blundell and Bond (1998), developed system GMM which provides more efficient estimators. Arellano and Bond (1991) state two key tests to check the validity of the GMM model: (a) the Hansen (1982) test of over-identifying restrictions; and (b) test for autocorrelation of the error terms.

Table 4 shows the outcomes of a two-step system GMM, with two measures of leverage as the dependent variable and foreign ownership as a key independent variable. Here, we have used the xtabond2 command developed by Roodman (2009). The standard errors reported here are robust and increase efficiency.

The results demonstrate a negative and significant link between foreign ownership and financing mix. Foreign ownership is negatively associated with LEV1 and LEV2, at 10 per cent and 1 per cent levels of significance, respectively. Moreover, the coefficient of the lag of the dependent variable (LEVit–1) is positive and significant, indicating that the current leverage is affected by the previous period’s leverage.

Dynamic Panel Estimation, Two-Step System Generalized Method of Moments

Standard errors are given in parentheses.

LEV1 is the ratio of total debt to sum of total debt and book value of equity. LEV2 is the ratio of total debt to total assets.

Discussion

Capital structure choice is a corporate decision which provides a combination of securities used to finance the investment requirements (Myers, 2001). Managers must choose the financing mix prudently so that it ensures the goal of maximization of shareholder’s wealth, which, in turn, impacts the long-term growth of businesses (Tripathi et al., 2018). By ameliorating the business climate and enforcing favourable policy framework, the GoI has ensured flourishing inflow of foreign investment. 4 This set of steps has induced a higher level of foreign ownership in Indian firms. With the entry of foreign firms, the domestic companies get affected either immediately or through the spillovers. With their induction, the level of competition in the host country’s market increases and, in turn, affects the domestic firms’ profitability and limits their growth opportunities. Through the FDI-related spillovers, productivity and the output of the company get affected. However, profitability, growth opportunities, productivity level and output certainly are accounted for while adopting the financing strategy. Therefore, corporate finance and international business literature clearly portray a link between foreign ownership and leverage. Nevertheless, the studies formally exploring this relation are nascent. Hitherto, none of the studies in the Indian context has examined this link. Against this backdrop, this article attempts to explore the impact of foreign ownership on the financing decision of Indian companies.

It concludes a negative and significant effect of foreign ownership on leverage. Results show that foreign ownership is negatively associated with both measures of leverage (LEV1 and LEV2).

The findings are consistent with that of Jain et al. (2013), which states: ‘The foreign-controlled companies in India use less debt than the domestic companies’. This can be substantiated with the following reasons: First, the foreign investors are primarily big investors and normally possess advanced monitoring skills (Huang et al., 2011) which enable them to subdue the issue of overinvestment by managers or lower the agency cost between shareholders and managers (Al-Najjar & Taylor, 2008). This way, foreign ownership and debt level might act as alternates for moderating the reckless behaviour of managers (Moon, 2001). Second, companies in which the level of foreign ownership is high usually have access to varied financing channels viz-à-viz others (Li et al., 2009). Further, the requirement for external financing can be lower in these firms due to the foreign investor’s equity contribution.

Moreover, the coefficient of the lag of the dependent variable (LEVit–1) is positive and significant, indicating that the current leverage is affected by the previous period’s leverage.

Almost similar relations are found for control variables as well, with regard to both the measures of leverage. The results suggest that firm size, growth and effective tax rate positively affect leverage. Size and tax rate have a significant impact on the financing mix under both measures of leverage. On the other hand, tangibility and profitability have a negative and significant effect on the capital structure.

Agency costs, information asymmetry and taxes are crucial factors while determining the financing strategy. The pecking order theory, trade-off theory and free cash flow theory, all are conditional theories of financial structure. Each of them underlines different features (costs and benefits) for alternative financing options. Myers (2001) states that there exists no single theory that can illustrate the financing choice, rather a mix of theories acts as an underpinning in justifying the financial structure. Hence, the outcome of our study suggests that a combination of the pecking order theory and the trade-off theory rationalize the capital structure choice in the Indian context. Indian-based studies like Chakraborty (2010) and Chadha and Sharma (2015) ascertained the same, while Bhama et al. (2017) backed the pecking order theory and Bajaj et al. (2018) supported trade-off theory.

Conclusion and Managerial Implications

Deciding the composition of debt or equity in the capital structure or how a firm finances its long-term investments is still one of the controversial issues in finance, and as per the above discussion, we advocate that it is impacted by the foreign ownership. The study uses the GMM technique for empirically testing this link, employing the data of non-financial firms constituting the Nifty 200 index, for the period 2007–2018. The study observes that there is a statistically significant negative relationship between foreign ownership and leverage.

Foreign capital could be in the form of debt or equity, which increases the domestic firm’s debt as well as the capital, so its impact on leverage cannot be clearly decided (Anwar & Sun, 2015). However, FDI flows into India occur primarily in the form of equity, so with the influx of foreign investment, increase in the numerator is lower than the increase in the denominator of the leverage (here measured as ratio of total debt to sum of total debt and equity). Hence, we can conclude from our results that with the increase in foreign ownership, the leverage of the Indian firms reduces.

From an operational viewpoint, a corporate should focus on maintaining a sound capital structure. There should be some balance between debt and equity; too much debt can be counterproductive. Debt-dominated firms face several disadvantages; they do not have financial flexibility as they have exhausted their debt capacity. Since firms having this kind of lopsided capital structure are considered very risky because of the high financial risk, obtaining/raising additional capital could be a challenge for them. However, equity-oriented capital structure does not enhance the financial burden of the company like debt does. Further, creditors and investors favour low debt–equity ratio as their interests are better guarded in the case of a business downturn.

Highly leveraged firms can pursue foreign investment, which has various advantages. Foreign investors not only bring in capital but also provide better technology and improve the human resource, which can lead to higher productivity, boost their international trade, etc. This way, they can benefit from the foreign ownership and concomitantly reduce their debt level.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

Surbhi Gupta receives financial support (Junior Research Fellowship) from the University Grants Commission, India.