Abstract

The development of smartphones and mobile internet technologies has promoted the development of mobile payments worldwide. The core purpose of this study is to ascertain what the main factors are which affect Dutch customers’ adoption and experience of mobile payments. This study first addresses the concepts of mobile payments and customer experience and then explores the current Dutch financial and banking systems, before attempting to understand the recent researches worldwide on mobile payments. Based on quantitative research methods, the study examines the factors that influence the adoption and experience of mobile payments and the impacts of the COVID-19 outbreak on payment methods due to social distancing rules in the Netherlands. It finds that perceived ease of use, perceived usefulness, safety and trust are the main factors that affect the adoption of mobile payments, and mobile-payment providers need to improve technical protection and offer some benefits to boost the mobile-payment business. The COVID-19 outbreak has caused the decline of cash payments and the increase of contactless payments in the Netherlands; mobile payments ensure people’s health and help slow down the spread of the virus.

Introduction

Financial technology (fintech) adoption across markets worldwide has been due to its proven ability to lower investment barriers (Hong et al., 2020). However, the rate of fintech adoption varies across advanced and emerging economies (Frost, 2020). Flood et al. (2013) extend the discussion on the benefits of fintech by covering the social impact on fintech consumers. There are various types of fintech services available for a wider consumer base, such as peer-to-peer (P2P) lending, marketplace lending and other fintech-based credit platforms. Emerging markets, however, are experiencing a surge in mobile payment–based fintech services; for example, big tech mobile payments made up 16% of Chinese gross domestic product (Frost et al., 2019). In comparison, the adoption of mobile payment–based fintech services is less clear (Flood et al., 2013).

Mobile payment is an innovative system from banks or proxy financial companies (e.g., Ideal, Paypal and Apple Pay) where customers can use the payment apps in smartphones or other mobile devices to buy goods or services or to pay bills (Lee, 2019). Smartphones or other mobile devices connect customers, payment providers and merchants to complete payments to merchants using apps available in smartphones or via a quick response (QR) code, along with authentication and authorization.

As a new payment model, mobile payments are a further step in cashless payments. Mobile payments have quickly become an important choice for users since their emergence, along with the development of technology and digitization. There are many types of research exploring mobile payments. Prior studies in this context have explored factors affecting the adoption and experience of mobile payments and the impact of mobile payments on the banking industry (Geerling, 2018).

Digitization is the process of transforming information into a digital format compatible with computers or compatible smart devices (Gigov & Poposka, 2017). Digitization has changed the banking industry fundamentally in recent years. Banks have adjusted their structures and operations, as well as launching various new services to customers, such as online banking, mobile banking and mobile payments (Raluca, 2019; Yanagawa, 2018).

Mobile banking enables customers to manage their accounts remotely through their smartphones or other devices. Customers can download an application from their smartphones and login with their details and passwords. Internet connection and mobile networks play a vital part in mobile banking adoption (McGovern et al., 2019). Before the advances of smartphones, mobile banking services required short message service (SMS) facilities on mobiles.

The success of the iPhone and other smartphones based on the Android system promoted a sharp increase in mobile apps. Such development let banks develop mobile banking apps to reach a wider customer group (Gupta, 2013). The mobile banking service has brought convenience to customers and has the ability to improve customer satisfaction. Especially in the context of Industry 4.0, mobile banking services are becoming more and more secure and convenient, changing the banking business model in the twenty-first century (Chakiso, 2019).

Due to the ease of use, usefulness and efficiency of mobile payments, customer experience on mobile payments has become a popular research agenda (Chiriac et al., 2018). Factors affecting mobile banking adoption vary across different economic, cultural and social contexts. Evidence on mobile banking adoption leans largely towards emerging economies, and limited evidence exists in the context of advanced economies. It is meaningful to study factors affecting customer adoption and experience of mobile payments in the context of advanced economies. Therefore, this study aims to explore customer adoption and understanding of mobile payments in the Netherlands and to understand the factors that influence the adoption of mobile payments in the Dutch market.

We believe our research is timely and could contribute to the existing literature. It is important to acknowledge the impact of the COVID-19 outbreak on the growth of mobile banking adoption across various economies. The pandemic has led to strategic and policy changes in financial industries around the world. In the USA, the COVID-19 outbreak has caused companies in all areas to establish remote working conditions, including most banks and financial service companies. They actively adopt various actions to ensure that people enjoy reliable financial and payment services. In China, the COVID-19 outbreak has promoted the rapid development of e-commerce models. Online shopping has accelerated the replacement of offline shopping, and many physical stores have switched to online sale, with mobile payment business increasing by 14.29% in the first quarter in China (Government of China, 2020). In India, the COVID-19 outbreak has promoted the development of digital payment and mobile payment.

In Europe, the COVID-19 outbreak has also accelerated digital finance services and the rapid development of fintech companies. Before the COVID-19 outbreak, mobile banking adoption was slow in Europe. However, the COVID-19 outbreak has speeded up the transition from the manual and paper-based process to digital finance and the process from traditional payment methods to cashless payments in a few months.

The COVID-19 outbreak has promoted the shift from offline payments to online payments in the Netherlands. Spending through credit cards decreased during the lockdown and increased again after the lockdown, starting mid-May. To implement social distancing rules and fight against the spread of COVID-19, Dutch banks and providers of payment terminals have increased temporarily the limit of contactless payment terminals at the points of sale such as supermarkets and other shops from 25 to 50 euros, and customers can pay with cards or smartphones without entering a personal identification number (PIN).

We present the rest of the article in nine sections. The second, third and fourth sections focus on discussing relevant studies, highlight the objectives of this study and establish the theoretical perspective of the current study, respectively. Next, we elaborate on the methodology in the fifth section. The sixth section provides a discussion on the results, where we compare our study findings with those of prior studies and theories to establish our unique contribution. The rest of the sections are dedicated to the conclusion, managerial implications and directions for future research.

Review of Literature

The launch of the iPhone 5S brought the fingerprint reader, which could improve the smartphone’s convenience and safety, as well as providing an opportunity for mobile payments. Apple Pay, created by Apple, simulates the process for customers to reach the services on apps. Later, Google Wallet was released as a mobile payment service to Android users. Apple Pay has been successful since its emergence; more and more banks have started to cooperate with Apple to supply mobile payments. There were more than 3,000 banks worldwide using mobile payments in 2019.

Apple Pay and Google Pay are ‘mobile proximity payments’, which mean the payment services offered by some other financial institutes or companies (instead of banks) with smartphones in-store or online (Gomber et al., 2018); these companies are called ‘proximity payment companies’. The proximity payment companies provide more opportunities for customers to adopt mobile payments, and their emergence has broken the monopoly of the payment market by traditional banks and financial institutions. Mobile payment apps released on smartphones also provide a new opportunity to serve customers (Bezhovski, 2016).

With the support of technical innovations and their features such as efficiency, transparency and convenience, mobile payments have attracted a considerable number of customers and become famous worldwide (Barbara & Lars, 2020). Many types of research have addressed mobile payment adoption in different countries (Gomber et al., 2018; Jun et al., 2018; Liao, 2018; McGovern et al., 2018).

Berg et al. (2020) explore fintech adoption in the European and Central Asian regions, following the high usage of mobile phones and government initiatives to provide better internet access to both urban and rural populations. In addition to the enormous potential of fintech in both Europe and Central Asia, Berg et al. (2020) outline the several challenges of fintech adoption in these areas, which include barriers of remittance flow, higher transaction cost and low level of access to finance for micro, small and medium enterprises (MSMEs). Fu and Mishra (2020) explore the global impact of COVID-19 on fintech adoption and find that market size and demographics are global drivers of fintech adoption.

Hasan et al. (2020) examine the importance of digital financial services to promote financial inclusion in China and make a valuable contribution by addressing the possible forces responsible for the promotion of digital financial services in the country. The study uses a qualitative method and applies a systematic literature review to provide the necessary evidence for the promotion of digital financial services in China. Chawla and Joshi (2020) provide evidence of digital financial service adoption in the context of India and find an attitude as a significant predictor of mobile wallet adoption.

Customer experience refers to the feelings about a product or service, which depend on the functions and performance of this product or service. Better customer experience can promote customer adoption of products or services. The successful development of mobile payments has attracted scholars worldwide to research on them. Several types of research discuss customer experience of mobile payments (Kumar et al., 2018;).

The researchers have explored customer experience of mobile payments in their respective countries, applied several related theories and addressed the factors that promote the adoption of mobile payments in the local social and economic context through qualitative or quantitative methods, such as the technology acceptance model (TAM), value-based adoption model (VAM), etc. They have found that mobile payments have improved payment speed and increased convenience and that young customers and customers who tend to accept new technology adopt mobile payments more rapidly.

Besides the two theory models mentioned above, other vital variables affect customer adoption and experience of mobile payments. Unnikrishnan and Jagannathan (2018) argue that trust is an important variable not included in TAM; they believe that trust could positively affect the adoption and experience of mobile payments, since when customers think mobile payment providers and their mobile payment apps are reliable, they prefer to adopt them. Trust is related to changes in customers’ payment habits.

Some studies explore how risk affects customer adoption and the experience of mobile payments. They argue that as a negative factor, perceived risks affect customer attitudes and trust and further cause different behavioural intentions towards mobile payments (Chakiso, 2019; Unnikrishnan & Jagannathan, 2018). Perceived risk causes feelings related to uncertainty and negative consequences. It involves the following types of risks: perceived privacy risk (personal information–related), perceived security risk (technical and system-related), perceived monetary risk (money lost) and some other uncertainties (unexpected issues, like COVID-19). All these risks could affect customer adoption and experience of mobile payments (McGovern et al., 2019).

When customers think none of the risks mentioned above is present, they believe using mobile payments is safe. Safety is another crucial variable that could affect the adoption of mobile payments, which is considered to be positively related to the adoption of mobile payments. When customers believe that mobile prices and their providers are safe, their intention of adoption will increase (Bezhovski, 2016). Many scholars have applied this theory in their researches and tried to explore how perceived usefulness and perceived ease of use affect the adoption of mobile payments. They have found that these two factors facilitate the adoption of mobile payments significantly (Shailza & Madhulika, 2019).

The value earned means that customers can achieve some discount or cashback by using mobile payments, and pleasure means the happiness of customers. Perceived cost means the financial loss to customers because of the use of mobile payments, and technical effort means the mental and physical efforts needed. Some studies have found that all these above factors affect customer intention and adoption of mobile payments (Lee et al., 2015). Other researchers have argued that customers tend to care more about the expected advantages of mobile payments instead of potential disadvantages; they think perceived value could positively affect customer adoption and experience of mobile payments (Jun et al., 2018).

Unnikrishnan and Jagannathan (2018) argue that trust was an important variable that was not included in the TAM model and conclude that trust could positively affect the adoption and experience of mobile payments when customers think mobile payment providers and their mobile payment apps are reliable, they prefer to adopt them. Trust is also related to the changes in customers’ payment habits.

Risk affects customer adoption customer adoption and experience of mobile payments. They argued that as a negative factor, perceived risks would affect customer attitudes and trust, and further cause different behavioural intentions towards mobile payments (Chakiso, 2019; Unnikrishnan & Jagannathan, 2018). The perceived risks mean feelings related to uncertainty and negative consequences. Perceived risk involves the following types of risks: perceived privacy risk—personal information-related; perceived security risk—technical and system-related; perceived monetary risk—money lost and some other uncertainties—unexpected issues. All these risks could affect customer adoption and experience of mobile payments (McGovern et al., 2019).

Safety is another important variable that could affect the adoption of mobile payments, which is considered positively related to the adoption of mobile payments. When they believe that mobile payments and their providers are safe, their intention of adoption would increase (Bezhovski, 2016).

Research Gaps and Study Objectives

The above discussion on prior research allows us to explore several research gaps. Studies on mobile banking focus heavily on emerging markets. The availability of a sound financial system often eludes research attention on mobile banking adoption in advanced economies. Malaquias and Hwang (2019) and Sajasalo et al. (2018) provide evidence of mobile banking adoption in the USA and Finland, respectively. However, evidence of mobile banking adoption in the context of the Netherlands is non-existent.

Therefore, the primary objective of this study is to explore the drivers of fintech adoption in the Netherlands. More specifically, we try to integrate a theoretical perspective in our quest to explore possible drivers of fintech adoption in the context of an emerging economy.

Theoretical Framework

One of the best-known theoretical frameworks is TAM. Fishbein and Ajzen put forward the theory of reasoned action in their studies in 1975 (Fishbein & Ajzen, 1975). TAM is one popular extension of the idea of reasoned action. It was proposed by Davis in 1989 and was used to describe the process of how users accept and use new technology (Davis, 1989; Davis et al., 1989). Scholars have widely used TAM. TAM includes two critical measures: perceived usefulness and perceived ease of use (Akhtar et al., 2019), which are two key variables that influence the customer’s attitude towards new technology. The relationship between the key variables and the attitude towards use is explained below. Many scholars have applied this theory in their researches; they have tried to explore how perceived usefulness and perceived ease of use affect the adoption of mobile payments and found that these two factors facilitate the adoption of mobile payments significantly (Shailza & Madhulika, 2019).

Another popular framework is the value-based adoption model (VAM). Kim et al. (2007) proposes this model in 2007 and indicates that the perceived value of the advantages and disadvantages of the use of new technology affects customer adoption of new technology (Jun et al., 2018), which refers to the values achieved from goods or services and the loss of using it. The perceived advantages are financial benefits earned and pleasure, etc., while the disadvantages are financial cost and technical effort. While perceived cost means the financial loss to customers because of the use of mobile payments, and technical effort means the mental and physical measures needed.

Lee et al. (2015) found that all these above factors affect customer intention and adoption of mobile payments. Other researchers have argued that customers tend to care more about the expected advantages of mobile payments instead of potential disadvantages; they think perceived value could positively affect customer adoption and the experience of mobile payments (Jun et al., 2018).

Research Methodology

Compared with qualitative methods, quantitative methods collect a larger number of samples and can more accurately estimate the correlation between independent variables and dependent variables (Saunders et al., 2016). As shown in the conceptual framework above, this study aims to explore the drivers of mobile banking adoption in the Netherlands based on the propositions of TAM and VAM. Therefore, we adopt a quantitative research method in this study following Akturan and Tezcan (2012) and Farah et al. (2018).

This study chooses convenience sampling to conduct quantitative research, which is a kind of non-probability sampling method. Convenience sampling is known as ‘accidental sampling’ or ‘opportunity sampling’; it is a kind of non-probability selection where researchers draw samples from the people that are close at hand (Etikan et al., 2016). However, there are some disadvantages of convenience sampling. For example, the results of the research cannot be generalized to the whole population; they are biased, because some people answer the questionnaire while others do not (Etikan et al., 2016). We use the convenience sampling technique prescribed by Cochran (2007) to determine that the final sample size for this study is 300. A similar technique has been adopted in recent studies on mobile banking adoption (Akinwale & Kyari, 2020; Talom & Tengeh, 2020) due to difficulties in determining a sampling frame.

We use a self-developed questionnaire to collect primary data on fintech adoption in the Netherlands. All respondents have prior experience in using a specific type of financial technology while performing online transactions. The questionnaire asks respondents to provide their opinion on various drivers of fintech adoption. Specific sections are exploring the safety and risk related to fintech usage that is linked with user trust in such platforms. Our questionnaire also requests respondents’ opinion on several constructs prescribed by TAM, such as perceived usefulness, perceived ease of use and perceived value earned and lost. Finally, we ask questions to explore fintech adoption among our respondents.

We distributed the link of an online questionnaire on social media platforms. First, the questionnaire was converted into a Google Form, and then links were created and distributed on social platforms, such as Facebook, Twitter, LinkedIn, etc. An online survey has several advantages compared with a traditional physical survey. First, it is faster and cheaper, the time needed for completing an online survey is less than that for traditional researches, and the response is almost instant. Second, it is more accurate and quicker to analyse; the researchers do not need to type all the results into the computer but just download the results directly after the respondents finish the questionnaire. Last, it is more honest and flexible; because the respondents are anonymous and not face to face with the researchers, they tend to answer more honestly, and the online links provide more flexible schedules and places to answer for both the researchers and respondents (Saunders et al., 2016). Two hundred and seventeen respondents participated in this survey. We collected 204 valid responses finally, at a response rate of 94%.

Reliability Statistics Regarding Adoption of Mobile Payments.

This study also uses the Cronbach’s alpha coefficient to detect the reliability of the correlation between the independent variables and dependent variables. Table 1 indicates that the Cronbach’s alpha coefficient is 0.705; the items are perceived ease of use, perceived usefulness, perceived value earned, trust, safety and risk. The Cronbach’s alpha coefficient is more than 0.7, which means the reliability regarding the correlation between the independent variables and the adoption and experience of mobile payments is high.

Data Presentation and Findings

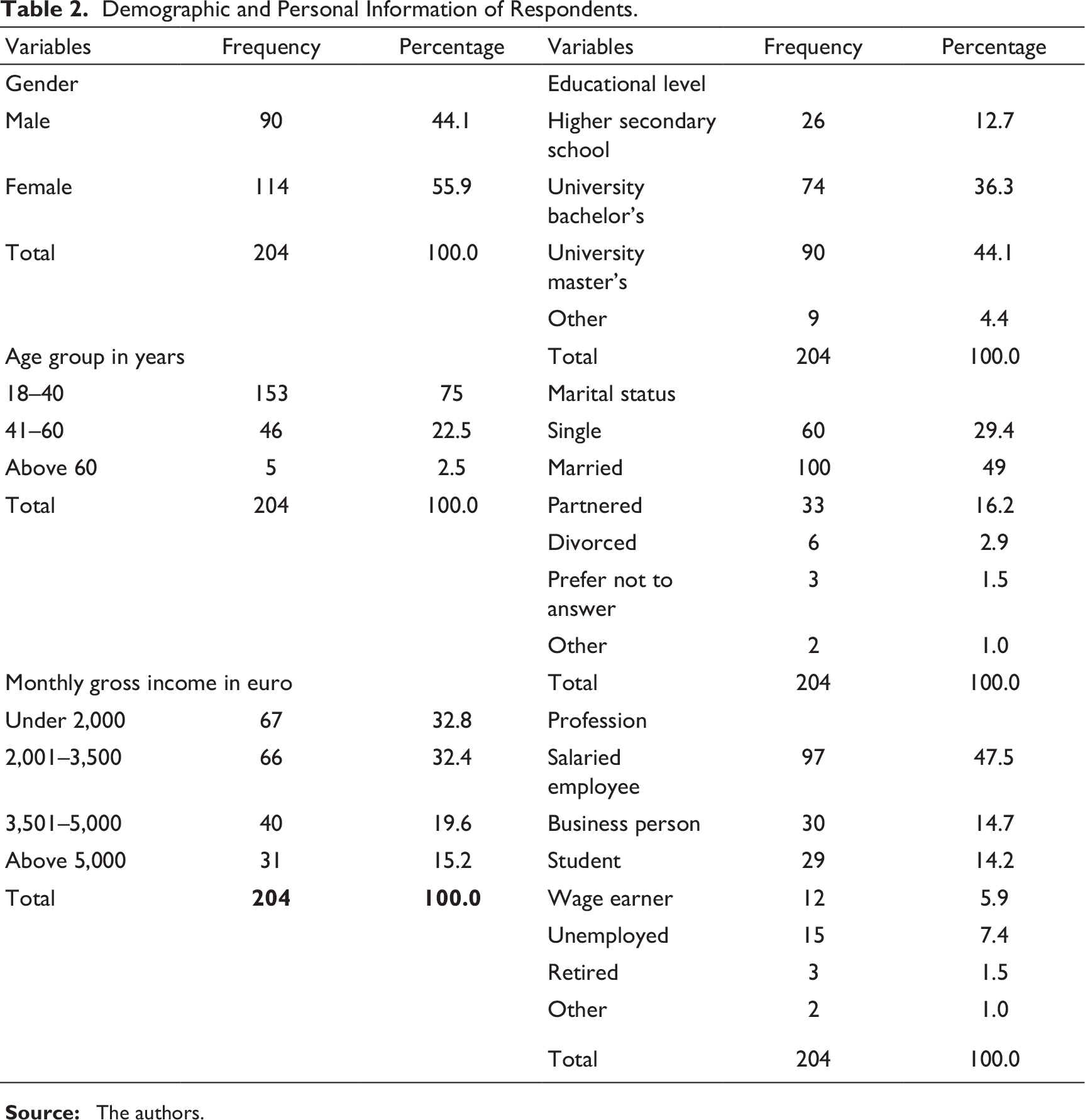

Demographic and Personal Information of Respondents.

Of the respondents, 33% earn under €2,000 in monthly gross income and 32% earn between €2,001 and €3,500. Fewer respondents earn a higher monthly gross income, 20% earning between €3,501 and €5,000 monthly, while only 15% earn more than €5,000 monthly. Of the respondents, 48% are salaried employees, 15% are business persons, 14% are students, 7% are unemployed and 6% are wage earners, and others and retired respondents account for 10%.

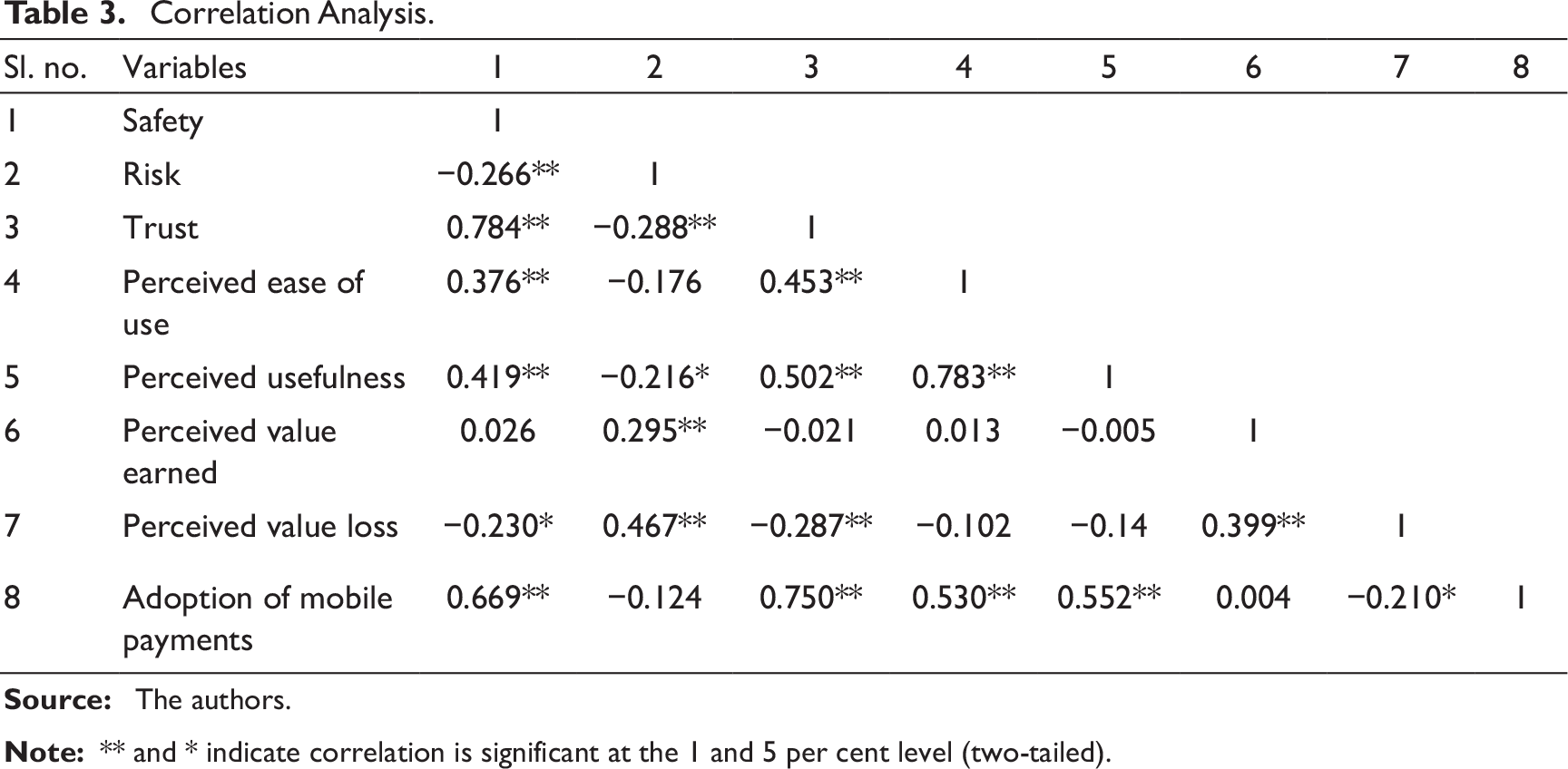

Correlation Analysis.

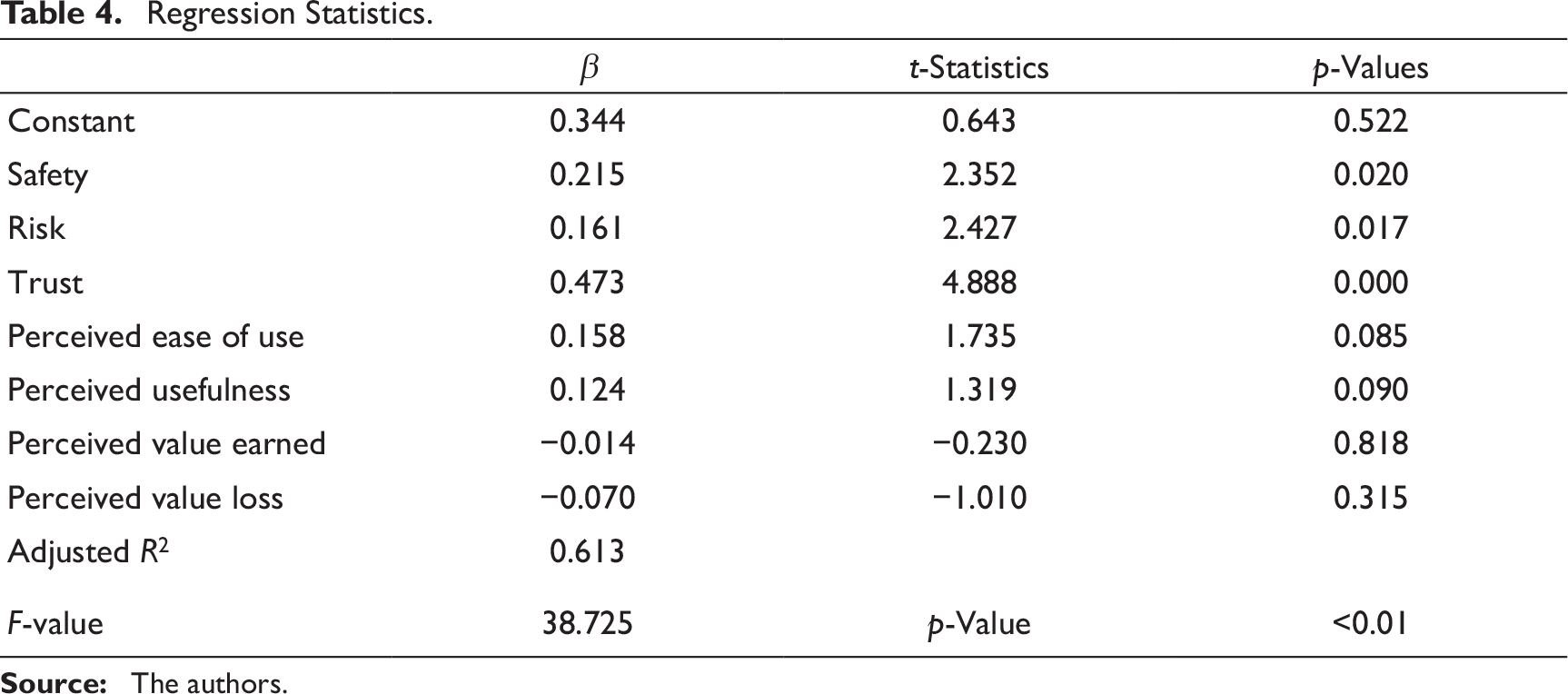

Regression Statistics.

The vast majority of respondents have experienced the convenience and simplicity of mobile payments, which are very easy to use. Perceived usefulness has a significant positive impact on the adoption of mobile payments (p < 0.10); most respondents think mobile payments are useful. This also reminds the providers that if they could provide customers with more useful mobile payment services, they would retain current customers and attract more new customers. Perceived value earned is not positively related to the adoption of mobile payments. Customers do not get any financial benefits from mobile payment providers, and they use mobile payments not because of expectation of benefits as well.

Perceived value loss is not significantly negative related to the adoption of mobile payments. Customers do not suffer loss from using mobile payments, and there are no concerns about value loss from mobile payments either. This is not in line with the correlation analysis, because the correlation analysis shows that perceived value loss has a significant negative correlation with the adoption of mobile payments. Here, this study agrees with the regression analysis results. Trust has a very significant positive effect on the adoption of mobile payments. It means most customers trust mobile payments and their providers very much. The regression coefficient indicates that safety has a very significant positive effect on the adoption of mobile payments; the p-value is 0.020, which is less than 0.05. Most customers think that mobile payments are safe; there is no concern about financial loss and personal information loss through using mobile payments.

When customers think mobile payments are not risky, they tend to choose them, and the opposite is also true. This is not in line with the correlation analysis because the correlation analysis shows that risk does not affect mobile payment. Here, this study agrees with the regression analysis results. Except for the two independent variables of perceived value loss and risk, the findings of the other five independent variables are aligned with the results of correlation analysis.

Surprisingly, the popularity and penetration rate of mobile payments is only about 61%, which is still relatively low compared with the penetration rate of smartphones and mobile phone networks in the Netherlands. This may be because Dutch customers are used to card payments. As per the frequency analysis, around 85% of the respondents use card payments very frequently; this finding is aligned with the studies showing that card payments are described as the primary payment method in the Dutch market. As a convenient payment method, card payments have released a contactless payment method that connects point-of-sale (POS) machines wirelessly in recent years. Customers do not need to insert a card and enter a PIN; they only need to take out the card and approach the POS machine to pay. This convenience makes people rely more on card payments.

According to the correlation analysis and frequency analysis, most respondents believe that mobile payments are very safe and not risky. They trust mobile payments and their providers, and the vast majority of respondents believe that mobile payments are very convenient and useful. The regression analysis regarding most of the variables is also consistent with the correlation analysis except for the variable of risk. Safety, trust, perceived ease of use and perceived usefulness are the main positive factors that affect the adoption and experience of mobile payments for most respondents. The regression analysis indicates that risk is a negative variable. Therefore, it is clear that the research findings in this study are highly consistent with the TAM theory. It is precise because customers all over the world like the characteristics of mobile payments and adopt them. Regarding risk, safety and trust, the findings of this study are also aligned with the previous survey.

Regarding the attainment of benefits from using mobile payments, most respondents held different views, while most respondents did not suffer an inevitable loss of services through using mobile payments. The variables perceived value earned and perceived value loss of the VAM theory did not show significant positive and negative correlations in the adoption of mobile payments in this study. This may be because the Dutch mobile payment providers did not provide customers with benefits, such as discounts or vouchers, to encourage customers to use mobile payments. When using mobile payments, there is no loss of fees or other related expenses. Therefore, these two variables have not a significant relationship with the adoption and experience of mobile payments in the Dutch market.

Conclusion

Most mobile-payment customers believe that providers should strengthen the technical protection of mobile payments and provide certain benefits to current and potential customers. For non-users, the concern of safety issues and difficulties in use are the main reasons why they do not try mobile payments. They are worried that mobile payments are not safe and will compromise their privacy or cause financial loss, and they are worried that they are challenging to use. More than half of the non-users indicated that they would try mobile payments in the future. Of the non-users, 25% said that if the bank recommended them, they would try to use mobile payments, and another 25% said they would try to use mobile payments in some extreme conditions. The providers also need to improve the safety level of mobile payments further, strengthen the technical protection of mobile payments, simplify the operating procedures of mobile payments and provide corresponding benefits for new and current customers. They would gain more and more customers.

Before this study, the previous researchers did not explore the various factors that affect mobile payments from the perspective of customer adoption and experience in the Netherlands. This study introduces the TAM and VAM theories and combines three critical variables to study the adoption and understanding of mobile payments in the Dutch payment market, and it finally finds that two variables from TAM and three important variables affect the adoption and experience of mobile payments in the Dutch market. It is also found that the penetration rate of mobile payments in the Netherlands is low. In addition, this study attempts to explore the impact of the COVID-19 outbreak on people’s payment methods and looks forward to the future contribution of mobile payments and contactless payments in fighting COVID-19 and ensuring people’s health.

As per the above analysis, new users of mobile payments are very few, accounting for only 7%. It shows that mobile payments have not been able to develop further in the Netherlands. Therefore, further research can focus on the reasons for the slow development of mobile payments in the Netherlands and how to improve the popularity of mobile payments in the country. Of the respondents who do not use or experience mobile payments, 25% chose ‘other reasons’ regarding the factors that hinder them from choosing mobile payments. However, they did not specifically indicate the reasons. In future research, it is worth studying what other reasons hinder them from trying mobile payments. In the context of the COVID-19 outbreak, the financial industry and the banking industry need to improve the services such as mobile payments and digital finance to provide safer and more convenient services to customers.

Managerial Implications

The Netherlands ranked third in the IMD World Digital Competitiveness Ranking 2019. The revolution in the fintech industry poses several challenges for the banking industry. While the fintech revolution offers faster and more convenient payment facilities through the use of information and communications technology (ICT), it also allows more opportunities for fraudulent transactions. Therefore, regulators and the banking sector need proactive measures to deal with the apparent threats posed by the fintech revolution in the Netherlands. One challenge is the implementation of efficient protection for online transactions in the form of biometrics and tokenization. Regulators could enhance fintech adoption in the Netherlands by developing better consumer protection for online financial fraud, which could protect both the consumers and the banking sector. In addition, there is a need for standardization of monitoring and reporting practices for fintech operations.

Limitations and Directions for Future Research

This study focuses on the drivers of fintech adoption in the Netherlands. However, there are several areas of fintech adoption that we could not cover in the study. One major event that has shaken the world is the COVID-19 pandemic. We expect future research to explore the impact of the COVID-19 pandemic on fintech adoption in both advanced and emerging economies. Also, further studies can discuss the effects of COVID-19 on the financial and banking industries on a larger scale.

Footnotes

Acknowledgement

The authors are grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article. Usual disclaimers apply.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.