Abstract

This exploratory study aims to provide insight into the audit expectation gap between companies and their auditors measured by the materiality for the financial statement as a whole, defined for the purpose of this paper as the materiality gap. This gap, conceived as a component of the audit expectation gap, is little examined in literature. In order to investigate the existence of a materiality gap, financial statement preparers of the selected companies were asked to estimate the materiality of their financial statement. This was subsequently compared with the outcome of the materiality used by the auditor based on the audit file. Moreover, to obtain more insight into the possible materiality gap, a survey was sent out to the partners of the audit firm involved. This study shows that materiality levels assumed by the preparers of financial statements were lower than the materiality actually applied by the auditors.

Keywords

Introduction

Although the audit expectation gap is a well-known concept and, generally speaking, a well-researched subject, it still remains a very complex concept with several dimensions. One of the dimensions often researched, mostly via surveys, is that of the auditor’s roles and responsibilities according to both auditors and the public (e.g., see Humphrey, Moizer & Turley, 1993; Koh & Woo, 1998). A less examined dimension is the materiality gap, that is, the gap in perceptions of materiality for financial statements as a whole between auditors, preparers and users. Studying this gap is important for two reasons: First, when looking at the audit opinion, it is quite clear that studying the materiality gap is an important research issue. An audit opinion states, among other things, that the financial statements are free from material mistakes. This raises the question whether preparers, auditors and users have the same view about what ‘free from material mistakes’ means, or whether there is, in fact, a so-called materiality gap (as part of the audit expectation gap). Second, the materiality for the financial statements as a whole forms the basis for the audit work to be carried out. So materiality plays an important role in the auditing process. However, there is no generally accepted definition of materiality. The International Standards on Auditing (ISA)

1

notes in Section 320.2 that different financial reporting frameworks tend to discuss materiality in very similar terms:

‘Misstatements, including omissions, are considered to be material if they, individually or in the aggregate, could reasonably be expected to influence the economic decisions of users taken on the basis of the financial statements;

Judgments about materiality are made in the light of surrounding circumstances, and are affected by the size or the nature of a misstatement, or a combination of both; and

Judgments about matters that are material to users of the financial statements are based on a consideration of the common financial information needs of users as a group. The possible effect of misstatements on specific individual users, whose needs may vary widely, is not considered.’

International Standards on Auditing states that both the amount (quantity) and the nature (quality) of the misstatements need to be considered. International Standards on Auditing also states that the auditor should determine materiality for the financial statements as a whole (ISA 320.10) and that (s)he should also document the materiality level, if applicable, for particular classes of transactions, account balances or disclosures (ISA 320.14).

While the materiality gap is an important research issue, the number of previous studies on this topic is quite small, and the research is limited in several respects. Important limitations include a tendency to rely on experimental methods as opposed to real-life situations and a general emphasis on the perceptions of users as opposed to preparers. Moreover, the object of previous studies was the materiality of individual items, and not the materiality for the financial statements as a whole. This article reports on an exploratory study of matched auditor and preparer perceptions of materiality in actual financial statements. The main finding is that preparers think of materiality in terms of lower thresholds compared to their auditor counterparts. This result is inconsistent with the general findings reported in literature, and recommendations are therefore made to pursue this line of research.

The remainder of this paper is organized as follows: the second section contains a brief review of literature on the materiality gap. In the third section, the research approach used in this paper, as well as the main findings, is described. The fourth section provides conclusions, limitations and suggestions for further research.

Review of Literature

The audit expectation gap (sometimes referred to as audit expectation–performance gap) is, generally speaking, well-researched in literature (see Best, Buckby & Tan, 2001). The gap is defined as the difference between society’s expectations of auditors and perceived performance of auditors (Porter, 1993). However, the concept of audit materiality as an element of the audit expectation gap is little noted in literature (Houghton & Jubb, 2011). In their research, Houghton and Jubb (2010) describe two ways in which the term materiality is used in the context of auditing. The first relates to ‘bigness’ and relates to the materiality of individual items in the financial statements. The second relates to the concept of materiality for the financial statement as a whole, which is the basis for (i) determining the nature, timing and extent of risk assessment procedures; (ii) identifying and assessing the risk of material misstatements; and (iii) determining the nature, timing and extent of further audit procedures (ISA 320.6) (Houghton & Jubb, 2011).

Messier, Martinov-Bennie and Eilifsen (2005) and Holstrum and Messier (1982) documented prior research on materiality (judgements), including comparative studies in which materiality and disclosure judgements between auditors, preparers and users, are studied. Based on their literature reviews and additional research, it can be concluded that while there have been many studies on materiality judgements of auditors and users separately, the number of studies published specifically on materiality as part of the audit expectation gap is limited. In this section, four published articles on this gap will be discussed. All studies deal with ‘bigness’ and relate to the question of whether a certain item, considered by itself, is material or not. As far as can be ascertained, no research has been published on the aggregated materiality level as part of the audit expectation gap, defined in the introduction as the materiality gap. Three of these studies (Boatsman & Robertson 1974; Firth, 1979; Jennings, Kneer & Reckers, 1987) are based on experiments, and one study (Jennings, Reckers & Kneer, 1991) is based on a survey. All studies examined the gap between auditors and users; additionally, the study done by Firth (1979) looked at the gap between preparers and auditors as well as at the gap between preparers and users. All papers examined the gap in respect to materiality attributed to disclosure items; in addition, Jennings et al. (1987) also examined the dollar threshold at which a misstatement or nondisclosure in the measurement of an item becomes material.

In essence, Boatsman and Robertson (1974) concluded that the judgement processes of CPAs and security analysts do not differ. Firth (1979) showed that there is wide diversity in opinions about whether items need to be separately disclosed or not. Chief accountants in industrial and commercial firms (as a proxy for preparers) wanted to disclose the least information. Auditors wanted to disclose more, and investment analysts and bank-lending officers (as a proxy for the users) wanted the most extensive disclosure. Jennings et al. (1987) assessed the degree of consensus on various disclosure issues. They tested both within and among three groups: CPAs, various user groups and officers of the court. Their findings suggest a great variation in all groups within as well as across cases. Jennings et al. (1991) researched materiality from the perspective of auditors and of lawyers and judges (where lawyers and judges are expected to be a reasonable proxy for users). Auditors had the lowest levels of disclosure, that is, wanted to disclose less. Lawyers and judges had the highest standards of disclosure.

According to Agrawal and Chatterjee (2015), the last decades the quality of financial information received increased attention. Surprisingly, based on literature, it can also be concluded that no research has been published on the materiality for the financial statements as a whole and that knowledge of materiality as part of the audit expectation gap is based on limited empirical research. Moreover, our knowledge is based on either experiments or on a survey and there is only one study that examined the gap between auditors and preparers. That paper found that preparers wanted to disclose the least information and hence had the highest materiality. In their review article, Messier et al. (2005, p. 157) summarized the results of research until 1982: 2 ‘There were considerable differences between users, preparers, and auditors with respect to materiality thresholds. In general, users demonstrated lower materiality thresholds than preparers or auditors; the materiality thresholds for auditors tended to be between those of preparers and users’.

The approach of using experiments or surveys to study materiality gaps as part of the audit expectation gap has several shortcomings. First, previous research may contain a bias because of the absence of real-world pressures, such as those associated with clients and liability (Boatsman & Robertson, 1974, p. 346). Power (2003, p. 379) expresses it as follows: ‘… very little is known about auditing in practical, as opposed to experimental, settings’. The reason why so little practical research has been done, according to Power (2003, p. 380), is: ‘There is very little of what is now called “field work” in auditing. The apparent reason for this is that professional service firms are reluctant to provide research access to client data and to live audit assignments.’ Second, experiments are typically based on a specific case description. The nature of the case, and the items for which materiality is assessed differ widely. In experiments, quite often it was asked if a specific situation was material or not. The nature of the items differs, with a wide range of situations, such as concerning write-down of inventory, price of a stock, etc. ‘With such a wide range of items or events examined, it is difficult to generalize these results because the relative importance of each of these items may vary significantly’ (Holstrum & Messier, 1982, p. 57).

Finally, it may be noted that earlier research focused on disclosure decisions to examine whether a certain item is material or not. This is another scope limitation, because as assumed by Messier (Messier, 1981, cited in Holstrum & Messier, 1982, p. 55) ‘materiality and disclosure were separated (though related) decisions’.

Objective and Rationale of the Study

This study investigates the audit expectation gap between companies and their auditors measured by the materiality for financial statements as a whole. Previous materiality gap research has focused on the user–preparer materiality gap and not on the preparer–auditor materiality gap, which is also an important aspect of the audit process. Outcome will indicate companies’ perceptions on the level of verification done by the auditor.

Methodology and Results

Research Approach and Data Source

In this study, the analysis of the materiality gap is based on a sample of auditor and preparer perceptions of materiality with respect to the same financial statements. To complement prior experimental research with real-life data, an attempt was made to obtain materiality assessments for a set of actual financial statements, inviting each preparer to consider materiality in terms of his or her company’s own financial statements.

Obviously, any research of this kind, though potentially highly relevant, is severely hindered by confidentiality requirements that are imposed on auditors (see, for instance, IFAC Code of Ethics for Professional Accountants, Section 140). It requires the cooperation of an audit firm which is willing to conduct most of the data gathering itself and to provide the data to the researcher in a format that guarantees the anonymity of the company.

This research is based on the 2007 financial statements of Dutch companies. At that time, materiality was defined by Dutch auditing standards using an exact translation of the definition contained in ISA 320 at that time. Cooperation was obtained from a Dutch member firm of the IFAC Forum of Firms member body. The data collection was carried out by an employee of the audit firm. The firm was willing to provide information for the year 2007 with respect to 29 companies, selected by the firm on the basis of general instructions by the researcher: cases were selected at random from among nonlisted companies with clean audit opinions. The audit firm excluded two companies from the original selection for reasons that cannot be disclosed because of confidentiality. The reasons were explained to the researcher, who concluded that there was no basis for assuming that these reasons were related to the companies’ or the auditors’ materiality judgements.

For each of these companies, the audit firm was asked to provide the following information:

Information on total assets, sales and results before taxes for the year 2007 in a format that ensured the anonymity of the company. The materiality level for the financial statements as a whole, applied in auditing these financial statements, as reported in the audit file (as mentioned in ISA 320.10). An assessment of the materiality level for the financial statements as a whole by the preparer of the financial statements.

The companies’ perception of materiality was based on a brief survey sent by the audit firm to the companies they audit. The audit firm was instructed to address the survey to the CFO or the financial controller of the company. In the survey, it was made clear that the survey had an academic purpose. As well as responding to some general questions, each preparer was asked to answer the following question with respect to their own company: ‘What amount, in Euros, do you think is material in your annual financial statements for the year 2007?’ (translated from Dutch).

In the end, 16 companies provided responses to the questionnaire, of which 12 were useable. Three respondents did not provide a number for materiality. One observation was omitted because it was clearly based on a misunderstanding of the question (the materiality threshold provided was greater than the balance sheet total of that company).

Two observations are noteworthy: one respondent turned out to be a former employee of the audit firm who knew the exact materiality threshold that was used, 3 and one observation was considered to be of doubtful value as the preparer reported a materiality threshold of zero. 4 Both observations have been retained, but it has been ascertained that the removal of these observations would not have significantly affected the results.

Finally, to obtain further insight, the audit partners were asked to answer some questions about materiality and the materiality gap.

Analysis

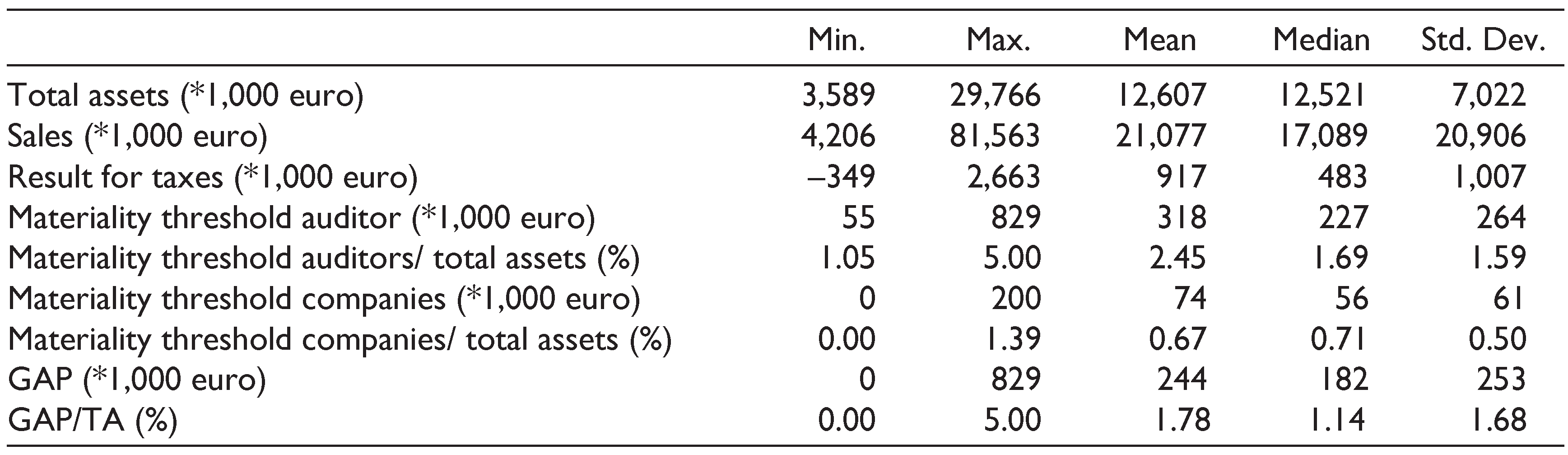

Table 1 provides descriptive statistics on the companies’ materiality levels of auditors and preparers as well as firm characteristics.

Sales, which is a measure for a company’s size, varies from 4 million euro to 82 million euro. The materiality threshold according to the auditors divided by total assets range from 1.05 to 5.00 per cent. The materiality threshold according to the preparers divided by total assets range from 0.00 to 1.39 per cent. This indicates that preparers have lower materiality thresholds. As a paired comparison, it appears that this result holds not just on average, but is true in all individual cases, with the exception of one case where the auditor and the preparer had the same perception of the materiality. When we define a variable GAP as (auditor materiality–preparer materiality), we find that this variable is never negative, although in one set of results it is equal to zero. GAP/TA ranges from 0 to 5 per cent. The mean is 1.78 per cent, which implies that the materiality threshold of the auditor scaled by total assets is on average 1.78 per cent higher.

To test whether the difference in materiality threshold between auditors and preparers is significant, a two-tailed Wilcoxon signed-rank test is used. As expected, because the materiality threshold of the preparers is always lower than the materiality threshold of the auditors, the difference between the two is highly significant (z-value of –2.934).

To assess the preparers’ understanding of the concept of materiality, the researcher also asked the preparers, with an open question, to provide a definition of materiality. Seven out of the twelve respondents gave a definition in line with ISA 320. Five preparers did not answer this question. Whether preparers responded to this question or not is unrelated to size of the firm, measured by total assets. (Tested by a Mann–Whitney test, p = 0.935.) This suggests that an understanding of the concept of materiality is unrelated to the size of the firm. The value of GAP/TA is, however, related to whether preparers did or did not give a proper definition of materiality. The value of GAP/TA of the subsample that gave a correct definition was higher than for the group that did not give a definition (tested by Mann–Whitney test, p = 0.030). If we assume that the group that gave a definition has, on average, a greater understanding of the concept of materiality, then the results suggest an understanding of the concept of materiality leads to a larger gap. Finally, tests were carried out to determine whether larger enterprises have a greater understanding of materiality and if—because of this—the reported gap would be smaller. If this is the case than one would also expect that the materiality gap scaled by total assets is negatively correlated with size. This turns out not to be the case. The Spearman correlation coefficient is 0.413 and is not significant (p = 0.183).

Descriptive Statistics

At the same time that the survey was sent to the companies audited by the audit firm, a survey was also sent out to the audit partners of the audit firm involved to acquire insights about materiality and about the communication of materiality by the audit partners. Ten surveys were sent out, and nine audit partners responded. It was not revealed to the researcher which of these audit partners were involved in the audits selected for the preparer survey. First, the audit partners were asked whether they communicate the level of the materiality to the companies audited. One audit partner answered ‘never’, four audit partners, ‘occasionally’ and four audit partners, ‘regularly’. None of the audit partners reported that they ‘always’ communicate the materiality threshold. Based on the answers of the audit partners, one would expect the materiality gap to be smaller: four out of the nine audit partners reported that they regularly communicate the materiality threshold to the companies audited. The next question asked was whether the audit partner expected a materiality gap to exist. Seven audit partners responded that they did; one partner indicated that (s)he did not. One audit partner did not reply to this question.

In the survey, some space was left blank for additional remarks. Two audit partners provided insightful comments: one audit partner responded that he does not communicate the materiality threshold because there are two possible reactions. In case the materiality threshold of the auditor is lower than that of the preparers, the response would generally be that ‘auditors are expensive’. The other feasible response could be that companies will be dissatisfied because they think that auditors do not pay (sufficient) attention to amounts below the materiality thresholds. One audit partner reported, correctly, as it turned out, that companies probably have lower materiality thresholds. This implies more work, but who would want to pay for that additional amount of work?

Discussion, Limitations and Suggestions for Further Research

Discussion

Whereas previous empirical research into the materiality gap has focused mainly on disclosure decisions, this study examines the materiality gap in the primary financial statements. This research examines the quantitative materiality threshold applied to the financial statements as a whole rather than to specific line items. The willingness of the audit firm to participate in this research provided a unique insight into the differences between materiality perceptions of auditors and the companies they audit. The cooperation of an audit firm also imposed significant restrictions on the research, especially with respect to sample size as well as the limited amount of information provided on the company’s characteristics and other relevant features in each audit that might have had an impact on materiality levels.

Nevertheless, the results are of interest. The findings of this research indicate that companies assume lower materiality levels compared to their auditors. On average, the materiality threshold of the auditors, scaled by total assets, was 1.78 per cent higher. Even though the number of observations in the current study is small, the fact that companies’ perceptions were lower (or equal) in all cases lends credibility to these findings concerning the materiality gap.

Three possible explanations for the difference in results compared to previous research are as follows: First, the difference may be caused by the fact that this study used real-life data as opposed to experiments. One might speculate that a greater familiarity with their respective organizations, including all the potential problems an auditor might encounter, would invite preparers to evaluate materiality thresholds at a lower level in their own organization as opposed to an hypothetical situation. When using real-life data, it is also possible that auditors, when faced with the cost constraints of a real audit, will respond differently to materiality issues than when answering hypothetical questions, where socially desirable responses may also play a role. A second possible explanation might be the time difference between this study and prior research. Preparers currently face an increasing number of legal claims, and the legal environment puts more emphasis on the responsibility of the preparer. Third, a possible explanation is in the nature of the materiality issue studied. Whereas previous research investigated disclosure issues, this study looks at the quantitative materiality threshold. With respect to disclosure, preparers may be more reluctant to disclose information because of proprietary information costs, but on the other hand, with respect to the reliability of the information provided they may be more demanding.

Taken at face value, the outcome of the current study suggests that companies expect auditors to engage in more detailed verification than they actually do. At the least, this indicates that the work of the auditor is not fully observable by the company. Whether it means that the auditor underperformed in the perception of the preparer, or that preparer perceptions are based on unrealistic assumptions about the nature and actual costs of auditing, cannot be determined on the basis of this research.

Though limited in scope, the research reported in this exploratory study provides sufficient indication that our understanding of the materiality gap as reflected in the existing research literature is incomplete. An important issue in any further research, of course, is to obtain the cooperation of more audit firms. This research shows that there are ways to allow firms to cooperate while respecting the need to maintain confidentiality. Although in the short term the outcome of this study—that companies expect higher materiality levels than auditors actually apply—does not seem to be in the interests of the audit firms themselves, in the long run the profession is likely to be strengthened by the removal of misunderstanding and ambiguity concerning the limitations and costs of an audit.

Limitations

The process of selecting companies is of vital importance. Given that the selection was carried out by the audit firm, it cannot be ruled out that the sample chosen for this study was not fully random. As far as can be ascertained by the researcher, however, the companies were selected randomly, and the process of eliminating two companies from the sample was made transparent to the researcher. If, nonetheless, selection had been to some extent nonrandom, the most likely result would have been that the findings understate the materiality gap. Given that the audit firm was aware of the research question, it might have been inclined to select companies expected to have a good understanding of materiality.

The preparers were not previously informed of the research question, but it is possible that they anticipated that their answers would be compared with those of the auditors. This might have led to a reporting bias if the preparers returned relatively low materiality thresholds to signal any belief they may have held that audits are too expensive.

While the sample includes a considerable size range, it does not include large, listed companies. It is conceivable that in larger, listed firms, there is a better understanding of audit matters so that any materiality gap between auditors and preparers will be smaller. Nevertheless, it is not likely that the findings of this study can be attributed solely to the level of knowledge. If that were the case, a negative relationship between size and the gap would have been expected.

The way in which the size of the audit firm influences the results is rather difficult to estimate. From literature, we know that auditors from large national audit firms have higher materiality thresholds compared to auditors from small audit firms (see Messier et al., 2005, p. 157): the audit firm which participated in this study is a member of an IFAC Forum of Firms, but not a big-4 audit firm.

Finally, the paper is based on 2007 data. However, I do not expect the outcome to be different in more recent years as no attempts have been made by neither the regulator nor the auditors to decrease the gap, for example, by better communication on materiality.

Suggestions for Further Research

Provided further cooperation from audit firms can be obtained, there are multiple avenues available for further research. Apart from research that confirms the existence of a preparer–auditor materiality gap, the results reported in this paper suggest that more work should be done to explore the determinants of the materiality gap:

Does the level of knowledge of audit procedures have an impact on the company’s perceptions of materiality thresholds? Does this differ for listed as opposed to nonlisted firms? It would also be interesting to split the gap into a performance gap and reasonableness gap (cf. Porter, 1993, p. 50). Who do auditors see as the users of the financial statement and who do preparers see as the users? Does this influence what they think to be material? Although it might be difficult to discern, it may be interesting to test whether the level of materiality thresholds is influenced by the rising number of lawsuits involving auditors and preparers. Does the fee structure (fixed fee or variable fee based on hours) influence the level of the materiality of the auditor? Based on the definition of materiality, fee structure should not be one of the determinants of the level of materiality, but real-life pressure in combination with fixed fee may influence the auditor’s materiality threshold.

If the existence of a materiality gap is confirmed, more general questions can be asked regarding the evaluation and economic significance of such a gap. The issue of which party is ‘right’ in its materiality threshold assessment should be answered by relating materiality threshold assessments to the perceptions of costs and the benefits of an audit. As it is not evident that consensus on the appropriate effort by the auditor already exists, an interesting question is whether the consensus can be encouraged by improving disclosure about materiality levels, or, more generally, enhancing communication on this point between auditor and the company audited. In general, it seems appropriate to conclude that, at any rate with respect to materiality, the contracting between auditors and companies audited is an area that requires further research.

Footnotes

Acknowledgements

The author is grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the paper. Usual disclaimers apply. I would also like to thank the employee of the audit firm for the data collection.