Abstract

Pantawid Pamilyang Pilipino Program (4Ps) is the Philippine version of the conditional cash transfer (CCT) program that measures human development through the provision of conditional cash grants to the poorest of the poor. This research determines the health expenditure and utilisation of the poor families in a low-income community under the CCT program. A cross-sectional research design was adopted using mixed methods of data collection from 177 households between May and June 2017. Results reveal that most families under CCT devote the largest portion of household health expenditure for inpatient health seeking. About 40% of the total expenditure is covered by the National Health Insurance Program and the cost for hospitalisation mostly comes from the out-of-pocket source. Moreover, the common problems encountered during health utilisation and spending are poor customer service of healthcare facilities and uncompensated hospital bill by health insurance.

Abbreviations

4Ps: Pantawid Pamilyang Pilipino Program

CCT: conditional cash transfer

DOH: Department of Health

DSWD: Department of Social Welfare and Development

FGD: focus group discussion

NHIP: National Health Insurance Program

PhilHealth: Philippine Health Insurance

SDG: sustainable development goals

SWS: Social Weather Station

UHC: Universal Health Coverage

Poverty is an economic issue that has long been a persistent problem in different nations, especially among developing countries. The issue of poverty alleviation became the focus of many political and socioeconomic reforms that have been undertaken in the quest to mitigate poverty. However, poverty is more than the lack of income and resources to ensure a sustainable livelihood. Its manifestations include hunger and malnutrition, limited access to education and other basic services, social discrimination and exclusion as well as the lack of participation in decision-making. Economic growth must be inclusive to provide sustainable jobs and promote equality (Kenny, 2015). According to a Philippine survey conducted in the year 2017, more than half of the Philippine household population belongs to poor and low-income families which is 6-point rise from December 2016. Furthermore, 8.1 million Filipino families are considered food-poor (SWS, 2017). Evidently, social inequity in the country has remained persistently large in much way that poverty is continuously occurring over time. According to the World Bank (2013), income inequality is highly associated with inequality in access to health services and there is a high degree of inequity in favour of the richest decile of the population for all indicators of health service utilisation. More importantly, there is a decline in overall utilisation of healthcare considering the non-poor who are less burdened by illness or diseases receive more healthcare services, while the poor who bear a greater burden of illnesses receive less healthcare (Son, 2009).

The notion that governments should use social spending to enhance the human capital accumulation of its citizens has caught on in social policy approaches from the developed to the developing countries, penetrating policy formulation in both contexts. The basic idea is that the beneficiaries and the society benefit when people are more skilled and able to support themselves (Jenson, 20xs09). Conditional cash transfer (CCT) programs provide cash payments to poor households that meet certain behavioural requirements, generally related to children’s healthcare and education. The combination of cash and conditionality allows programs to boost household consumption in the short-term while providing an incentive, and helping to offset the costs, for poor families to invest in long-term human capital development. By building healthier, stronger and more productive future generations, it aims to interrupt the intergenerational transfer of poverty. It became popular in the Latin America and considered as best practice and innovative program for the delivery of social services (Fernald et al., 2008; Rawlings & Rubio, 2005). The CCT program was anchored to the metaparadigms and key principles of the Theory of Change. A theory of change is a method that explains how a given intervention, or set of interventions, is expected to lead to specific development change, drawing on a causal analysis based on available evidence (De Silva et al., 2014). Several studies assess and evaluated the provision of CCT to assess its impact on social protection and health, especially in child nutrition (Leroy et al., 2009); food consumption and food security (Gitter & Caldés, 2010); and utilisation of health facilities and services (Akresh et al., 2013; Behrman & Parker, 2013; Benedetti et al., 2016).

Based on the previous literature, formal labour supply; home production; and depletion of specific assets respond to health risk. There is also an empirical evidence on the role of public health insurance in mitigating adverse outcomes associated with health shocks. Study revealed that household labour supply is an important insurance mechanism against health shocks. Access to health insurance helps households to maintain investment in children’s human capital during negative health shocks, which suggests that one benefit of health insurance could arise from reducing the use of costly smoothing mechanisms (Liu, 2016). Moreover, there is also clear evidence of the impact that deteriorating health can have on an individual, their household and their none co-resident family. It is shown that severe health limitations pose significant financial risk to individuals and their families and interplay between formal health insurance and family risk-sharing (Dalton & LaFave, 2017). Hence, economic costs of poor health transmit throughout a family network and interact with connections across generations and space that offer support in times of need.

A study estimated the impact of social health insurance on financial risk by utilising data from a natural experiment created by the phased roll-out of a social health insurance program for the poor. It was found out that insurance reduces out-of-pocket costs, particularly in higher quantiles of the distribution creating reductions in the frequency and amount of money borrowed for health reasons (Barnes et al., 2017). However, another study revealed that large proportion of family size results to high dependency rate and therefore increases the out-of-pocket expenditure by households (Gonzales & Ambong, 2018).

In the Philippines, CCT is known as the Pantawid Pamilyang Pilipino Program (4Ps) under the Department of Social Welfare and Development (DSWD). The program aims to exterminate extreme poverty in the Philippines through the provision of support for health, nutrition and education to children. To circumvent the disparity and to ensure an effective and well-targeted social protection program, all identified beneficiaries of the Philippine CCT program or 4Ps were entitled to the National Health Insurance Program (NHIP) benefits in all healthcare facilities. The Philippine government expanded social health insurance and upgrade health facilities in the entire region to achieve the expansion of access to healthcare services. Moreover, the Department of Health (DOH) has also begun to increase effective coverage through enrolment, utilisation and financial risk protection under the NHIP or PhilHealth (Philippine Health Insurance Corporation). The NHIP has a mandate to provide universal health insurance coverage to all Filipinos (World Bank, 2013). It covered 92% of our total population by December 2015 (DOH, 2015). In addition, as part of the commitment to the Sustainable Development Goal (SDG) 3: Ensure healthy lives and promote well-being for all at all ages, the country targets to achieve universal health coverage (UHC), including financial risk protection, access to quality essential healthcare services, access to safe, effective, quality, and affordable essential medicines and vaccines for all (United Nations, 2016). Also, in the National Health Agenda for 2016 to 2022, the government health system aspires to have a financial protection for Filipinos; especially the poor are protected from high cost of healthcare, best possible health outcomes with no disparity and offer Filipinos feeling of respect, valued and empowered in all their interaction with the health system (DOH, 2015). Consequently, 4Ps can create positive for the demand of health services by reducing financial barriers to access. Given the hopes to set strategic option in adopting, formulating and implementing viable national health insurance system for the poor; thus, there needs to guide the development of national consensus and action.

Given the goal of the DOH of creating a more feasible healthcare insurance system for the poorest of the poor in the country, this study attempts to create a clearer view of the health expenditure and access to health services of poor families after their enrolment in the NHIP. Specifically, the study determines the household health expenditure and utilisation of poor families in a low-income community under the Philippine CCT program.

Methods

Locale of the Study

The study was conducted in Barangay Labangan, Caminawit and Pagasa in San Jose, Occidental Mindoro, Philippines.

Research Design

This was a cross-sectional study design utilising mixed methods in data collection. The data was collected between May and June 2017 using a structured questionnaire that was administered through a survey interview. The study also conducted focus group discussions to explore common encounters on health utilisation and household spending.

Respondents of the Study

The participants of the study were the families covered by the CCT program dubbed as 4Ps. The study participants were part of a previous study on the health seeking behaviour of the 4Ps. The respondents were asked, ‘Is there any of your family members ever been sick, injured or hospitalised in the past 3 months?’ and those who answered ‘yes’ were included in the analysis. In addition, purposive sampling was done for the focus group discussions among the survey participants. There were 3 focus groups held in three (3) different locations in which each group was composed of 10 participants.

Research Instrument

The study used a survey questionnaire in gathering the following data: demographic data of the respondents such as educational attainment of the family head, average monthly income, household size and household expenditure. Other parts of the questionnaire were about the health condition reason for health seeking and the choice of healthcare provider. The questionnaire also includes the household health expenditure for inpatient and outpatient health seeking and sources of funds for health service utilisation. Moreover, to explore common encounters on health utilisation and household spending of the 4Ps grantees, focused group discussion (FGD) was conducted using the following components:

Health problems facing the community Problems encountered during health seeking, pattern of health expenditure and the use of Philhealth.

Data Analysis

Descriptive statistics was utilised to describe the demographic profile of the respondents. Frequency and percentages were used to analyse the ordinal and nominal variables. Mean and standard deviation were used to analyse the interval variables. Furthermore, the qualitative results of the FGD were also analysed using descriptive analysis.

Results

Demographic Profile of Families Under CCT Program

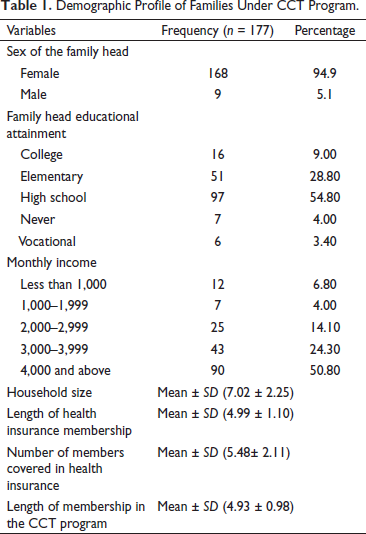

Table 1 presents the demographic profile of 177 family grantees surveyed in three barangays of San Jose, Occidental Mindoro, Philippines. It reveals that the majority or 94.9% of the household heads surveyed were female having formal education up to high school (54.80%). Moreover, 50.80% are earning a monthly income of not less than 4,000 pesos a month while the mean household size is 7 members, which can already be considered as a big household presenting a high dependency rate (Tabuga et al., 2013).

Demographic Profile of Families Under CCT Program.

When it comes to the length of membership in 4Ps, the grantees have been members for approximately five years (mean = 4.93 years) the same as the length of time when they became a member of the Philippine Health Insurance System (Philhealth) (mean = 4.99 years). Furthermore, the number of household members covered by health insurance per family is approximately six members (mean = 5.48 members).

Health Condition for Health Service Utilisation and Choice of Healthcare Provider

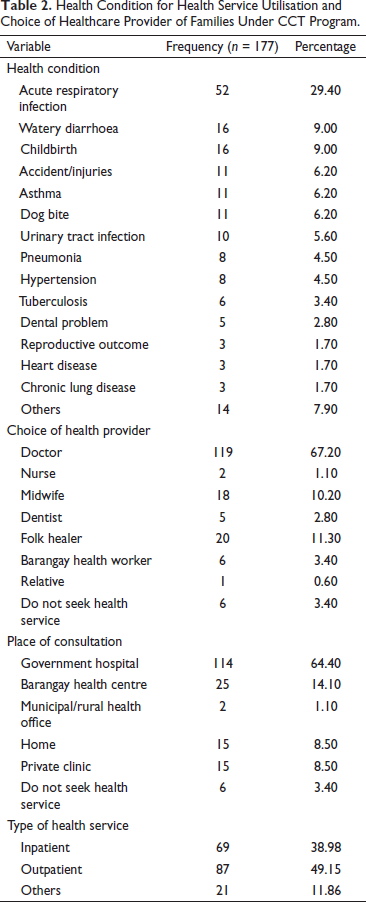

Table 2 reveals that the most common health problem encountered by the respondents is acute respiratory infection (29.40%). The healthcare providers they preferred were doctors (67.20%) from a government hospital (64.40%) providing an outpatient health service (49.15%).

Health Condition for Health Service Utilisation and Choice of Healthcare Provider of Families Under CCT Program.

Household Health Expenditure for Inpatient and Outpatient Health Seeking

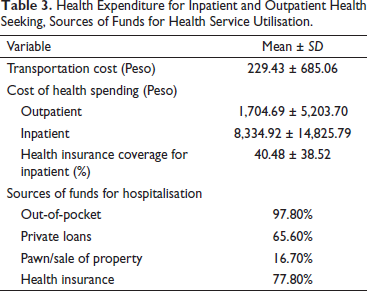

Table 3 shows the expenditure of a household based on the last consultation or hospitalisation. The findings revealed a high spending on the transportation cost (mean = 229.43 ± 685.06), which could be a high burden for a household belonging to the poorest sector relying on the daily income. It also revealed that the households spend an average of 1,704.69 for their outpatient consultation since most of the laboratory procedures and medicines are not free. Since there is a high use of financial risk protection in hospitalisation (77.80%), there is still high out-of-pocket (97.80%) spending in every household because most of the hospitalisation expenses were not covered by Philhealth. Hospitalisation costs tend households to rely on other sources of funds such as private loans (65.60%), pawning and sale of properties (16.70%).

Health Expenditure for Inpatient and Outpatient Health Seeking, Sources of Funds for Health Service Utilisation.

Common Encounters on Health Utilisation and Household Spending

Health Problems Facing the Community

A similar consensus was brought by household heads as the most common health problems in the community. Most of the group mentioned that respiratory tract infections, diarrhoea, dog bites and cardiovascular conditions. Consistently, focus groups mentioned that childbirth is common in the barangay as several pregnancies also increase. In majority of the focus group, the common illnesses experienced by the households are toothache, allergy, fever and headache. They purchased medicine from a retail store in the neighbourhood since drugstores are far from the village. Usually, infants were prone to illnesses such as cough, colds, diarrhoea and fever while athlete’s foot and skin allergies were often experienced by adults, especially during the rainy season when there is flooding. They are aware that infants are sensitive and prone to illnesses.

Problems Encountered During Health Seeking, Pattern of Health Expenditure and the Use of Health Insurance

Health Services

Conversely, negative experiences were much easier for all the groups to describe. An overwhelming majority of groups stated that, at the time of consultation in the public health facilities they commonly notice that the number of doctors is not enough to accommodate the bulk of patients causing a long queue and could also entail a long time for waiting. They also mentioned that most of their household chores or even their workplace are also affected by an all-day queue of patients.

Health Expenditures

An overwhelming majority of groups stated that most of the reasons for hospitalisation were not being covered by the Philhealth. The issue of no balance billing was also discussed in the group. No balance billing means that sponsored beneficiaries shall not pay fees more than the prescribed case rates for common medical and surgical services. However, the groups that had problem with their bills since most of the medicines and medical supplies were not available within the accredited facility tended to buy outside the hospital and were not able to reimburse it.

Discussion

Women are usually selected as beneficiaries of the cash transfers because they are believed to have more motivation in investing in the human development of their families, especially their children, than their male counterparts (Watkins, 2006).

In the year 2013, it was reported that the CCT program has not improved access to financial institutions (World Bank, 2013). In both CCT-covered and non CCT-covered barangays, only about 10% of households reported having a bank account. However, more poor households in CCT-covered barangays reported savings in all provinces. Furthermore, it also revealed that few differences were found in program impact across people in relative poverty, indigenous people status and gender. Among those identified as poor, the program was found to be equally effective for households who were relatively poorer and those who were relatively less poor. Likewise, few differences were found between households who identified themselves as having indigenous people status and those who did not. The program also appeared to be equally effective for boys and girls, with no gender differences found in program impacts on outcomes related to education and health service use (Chaudhury et al., 2013).

PhilHealth-sponsored program appeared to have successfully attained universal coverage over the targeted ‘poor’ population at the national level for the year 2011. However, coverage rates varied between provinces; gaps between the lowest and highest rates could be extremely wide and rates were highly skewed towards the leakage levels. Also, anticipate the potential risk for the ‘moral hazard effect’ of health insurance to take place. The ‘moral hazard’ issue occurring among the poorest and the poor may not be as disturbing as it is if caused by the behaviour emanating from non-poor and unqualified persons included in the program. By which, this type of health finance would cause strong incentive to consume more and ‘better’ healthcare and a disincentive to maintain a healthy life, which may pose a future challenge to the national and local government policymakers (Silfverberg, 2014).

A study on the determinants of children’s health services utilisation indicated that maternal education and a number of illnesses determine the decision to seek care. Once the decision has been made to seek care, the choice between a public and private provider is affected by the family’s economic status and size of the household (Thind & Cruz, 2003). An evaluation of the factors influencing healthcare utilisation in the Philippines revealed that pneumonia is the most common reason for health utilisation especially in the government health centre. Cost is the main factor influencing choice, followed by transportation availability and quality of care (Kim et al., 2014).

As part of the CCT, the Philippine government pursue better understanding of inequities in health and the level of effectiveness of a key poverty alleviation program about addressing access to health. Further, the program provides a strategic opportunity to provide technical support to help DOH manage changes and close the capacity gap towards a coherent implementation of universal healthcare. The health grant aims to promote healthy practices, improve nutritional status of young children and increase use of health services. Poor households with children 0–14 years old and/or pregnant women will receive PhP500 per month. However, this is only limit to the following conditions: all children under-five follow the DOH protocol by regularly visiting the health centre or rural health unit; pregnant women attend health centres or rural health units for health services per DOH protocol; all school-aged (6–14) children comply with the de-worming protocol at primary schools; and household grantee basically mothers and/or spouse to attend Family Development Sessions (FDS) at least once a month (Parrocho et al., 2013).

Private out-of-pocket expenditure constitutes the bulk of health spending and remains a financial barrier to access to health services. Based on the study on the distribution of out-of-pocket expenditures in the Philippines, half of the out-of-pocket spending went to medical products, of which almost two-thirds went to pharmaceutical products and almost three-tenths went to supplements. The share of medical products to out-of-pocket spending was higher among the poor than among the rich. The poor also incur catastrophic health payments leading to out-of-pocket health spending of over 40% of their income (Parrocho et al., 2013). It was agreed by a similar study revealing that subsidy for the poor covers a high proportion of the national health insurance fund, effectively subsidising healthcare service for other members, especially the informal sector. Hospitals also enrol the poor as well as the near poor in PhilHealth at point-of-care and may over-subscribe the poor given the higher reimbursement relative to the premium subsidy. The poor are covered by a No Balance Billing policy in which they are not liable to pay hospital fees over the case rate. However, out-of-pocket spending is still incurred by the poor due to other expenses, especially for medication (Ulep & Dela Cruz, 2013).

An issue escalated in most of the focus group was that in times of sickness in the family, they rarely go to see a doctor or visit a health clinic. They therefore do not enjoy the benefits covered by their PhilHealth membership. When the illness gets severe is the only time when they go to see a doctor. They usually consult a therapist and faith healer (manghihilot and albularyo).

Majority of the focus group raised an inquiry about the distance of a public hospital making affordable emergency healthcare inaccessible for them. For some groups, lack of time is one of the factors that disallowed them to seek consultation in health centres. Poor customer service was pointed out by the focus groups to public health institutions, especially in hospitals such as not being treated politely, not being listened to, having concerns go unnoticed or dismissed staff ignoring patients. They also agreed that the district hospital has a bunch of documents and procedures to process, long lines and slow queues. There are some issues in claims processing where the case is not compensable by PhilHealth, violation of the single period confinement rule and attendance by non-accredited doctors. One member in a focus group stated that she was not able to claim her benefits because at the time her other child was confined for the second time for a different case, it is still less than the prescribed recur usage of the benefit. Further one of the heads stated that she failed to claim her benefits because she did not meet the requirements for the coverage. One household head also mentioned that she was not able to claim the benefit when her child was hospitalised since she brought her child to the nearest hospital due to some emergency. Another problem revealed during the utilisation of health services and Philhealth is the reimbursement. Since most of the claims for medical expenses were ascribed for reimbursement. The out-of-pocket spending also exists which may affect their total household expenditure.

The result of the current study was similar to the study conducted in China about the effect of medical insurance schemes in health services utilisation. It reveals that the enrolment in a financial risk protection scheme has shown a positive but limited effect on increasing health services utilisation. The benefit package design of higher reimbursement rates for lower-level hospitals has induced the insured to use medical services in lower-level hospitals for inpatient services (Cabalfin, 2016). However, these results contradict the findings of a similar study which reveals that increasing health insurance coverage is likely to be an effective approach to increasing access to healthcare (Zhou et al., 2014). The findings suggest that when such coverage is subsidised, as is the case in the Philippines, women from poor and rural populations are likely to benefit the most.

Philippines is challenged by attracting and retaining staff in the underserved areas of the country. Furthermore, considerable inequities in healthcare access and outcomes between socioeconomic groups remain. The PhilHealth’s limited breadth and depth of coverage has resulted in high levels of out-of-pocket payments.

The implementation of the reforms in financing, service delivery and regulation which are aimed at tackling the inefficiencies and inequalities in the health system has been challenged by the decentralised environment and the presence of the private sector, often creating fragmentation and variation in the quality of health services across the country (Gouda et al., 2016).

A recent study quantifies the extent to which beneficiaries of the National Health Insurance System which is PhilHealth incur out-of-pocket expenses for inpatient care and examines the characteristics of beneficiaries making these payments and the hospitals in which these payments are typically made. The study found out that although the current NHIP reduces the size of out-of-pocket payments, NHIP beneficiaries are not completely free from the risk of large out-of-pocket payments, despite NHIPs attempt to mitigate this by setting different benefit ceilings based on the level of the hospital and the severity of the disease (Işık et al., 2015).

Footnotes

Acknowledgement

The authors are grateful to the Department of Social Welfare and Development MIMAROPA Region and the Provincial 4Ps for their support in the recruitment and coordination with research assistants and for providing supplementary data. Further, the authors are thankful to Mr Leoniel S. Bais, Dr Susanita Lumbo and Dr Arnold N. Venturina and to Occidental Mindoro State College-Research, Development and Extension Unit for their support in this research project.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Ethics Approval

This original research article was technically reviewed and approved by the Research and Extension Council of the Research, Development, and Extension Unit of Occidental Mindoro State College. The participation of the families under 4Ps was voluntary and with the consent and supervision of the Department of Social Welfare and Development MIMAROPA Region, through the Regional Director and Program Coordinator. The complete anonymity of the participants was considered, and they were informed of their right to confidentiality and privacy. Further, clarifications from the participants were entertained to facilitate ease of understanding of the instrument. Coding of the questionnaire was done and recorded to a separate sheet and was later matched after data collection. Data access was limited only to the researchers.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.