Abstract

This article focuses on the narratives that are developing in the household debt arena through a systematic and in-depth examination of the literature. The article used co-occurrence analysis to identify the major themes in the household debate followed by a review of the top 100 highly cited articles, which is supplemented with citation tracking. It is found that the past research mainly concentrates on the effect of financialization and deregulation of global markets, mortgages and housing bubbles, the upward trending inequality, the GDP growth and financial stability as well as the relationship between the household balance sheet and macroeconomic fluctuations. This study highlights the significant and upcoming trends in the study of household finances placing it at the centre of academic discourse on economic crisis and financial stability. It tracks the channels through which household debt could have potential impact on economic stability by summarizing the significant studies and deriving conclusions and direction for future research.

Introduction

Debt is generally believed to contribute to the long-term economic growth of the country extending its positive implications to households and businesses alike. For emerging economies, the influence of household debt on financial deepening is paramount enabling them to bridge the gap between their status quo and developed country status. At the same time, the recent narrative defined by the recurrent debt-led crises points to the devastating impact that the unsustainable rise in debt can have on the economy, polity and stability of the country. Household debt has multiplied rapidly over the past few decades, raising concerns over its sustainability and, therefore, its consequences for the financial system and the macroeconomy as a whole. In recent times, the massive proliferation of household debt in systematically important countries such as the United States, China, Japan, the United Kingdom and India are strong indicators of the need to investigate literature on excessive household debt. This topic has implications at both macro- and microeconomic levels. On the microeconomic level, household debt is a significant indicator of financial well-being, linked closely with stress, mental health, education and wealth(Albacete & Lindner, 2013; Berger et al., 2016; Heintz-Martin et al., 2022), while also associated with inflation, unemployment, exchange rate, inequality asset prices, fiscal position and monetary policy at the macroeconomic level (Aldashev & Batkeyev, 2023; Andrade et al., 2023; Floden et al., 2021; Sufi, 2023). The pandemic has further put the spotlight on households and their financial behaviour in response to shocks and uncertain future. Thus, household debt has become the cynosure in the current global position, shifting the narrative from public to private debt and its influence on the stability of the economy.

This article attempts to understand and bring together the various theories and perspectives relating to household debt, and overcome the existing gaps in the literature review in the household debt domain by answering the following research questions:

To identify the themes developing in the literature through co-occurrence analysis. To provide a theme-specific review of the highly cited articles in the field of household debt.

Research Methodology

Preliminary Search

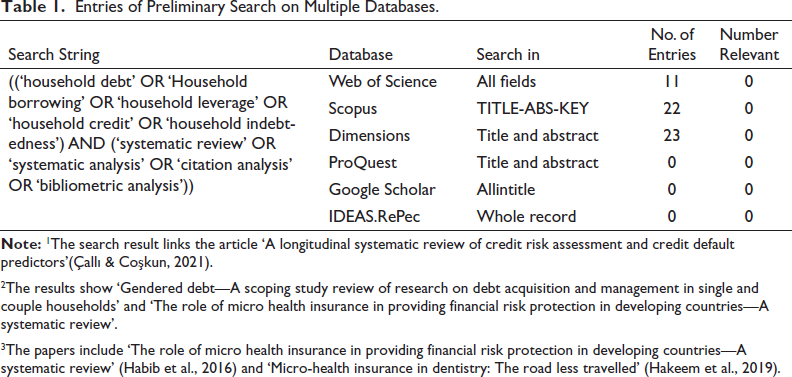

Before beginning the process of literature review in the area of household debt, it was important to establish that a prior attempt at systematic review was not done to ensure the relevance of our review. For this, a preliminary search was done in Web of Science, Dimensions, and Ideas.RePEc and Google Scholar. The results of the preliminary search are listed in Table 1 which shows that none of the articles extracted was relevant. The need for a review in this area was therefore identified.

Entries of Preliminary Search on Multiple Databases.

2The results show ‘Gendered debt—A scoping study review of research on debt acquisition and management in single and couple households’ and ‘The role of micro health insurance in providing financial risk protection in developing countries—A systematic review’.

3The papers include ‘The role of micro health insurance in providing financial risk protection in developing countries—A systematic review’ (Habib et al., 2016) and ‘Micro-health insurance in dentistry: The road less travelled’ (Hakeem et al., 2019).

Data Extraction

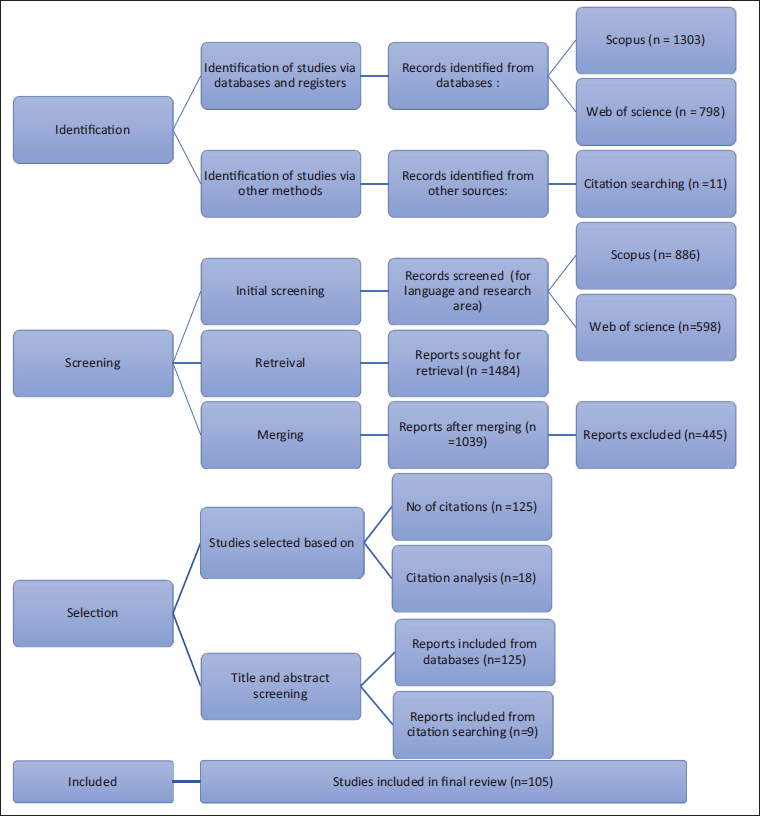

This systematic review extracts documents from the two major databases, Scopus and Web of Science, which cover a broader section of literature. It adopts the PRISMA (Preferred Reporting Items for Systematic Reviews and Meta-Analysis) guidelines to identify and extract the documents to be included which is detailed in Figure 1. The authors have included peer-reviewed articles to allow for systematic searchability based on similar terminologies and constructs as well as early access articles to include any recent shift in narrative. As a post-search criterion, citation tracking has been used to include influential and highly cited books and reports as well as relevant journal articles that have significantly contributed to this field.

Co-occurrence Network Based on Keywords.

Data Analysis

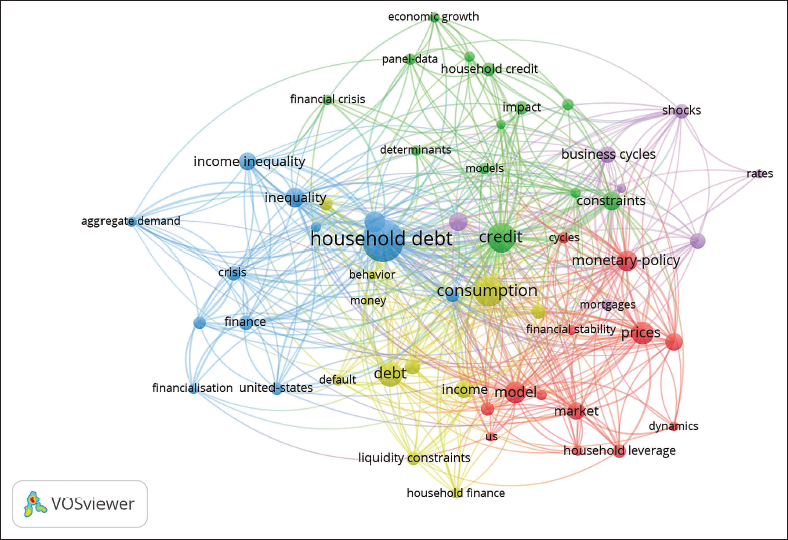

This article uses co-occurrence analysis to understand the themes and sub-themes of the household debt narrative which is performed on the merged file consisting of 1,039 documents. The co-occurrence frequency of the keywords is used to uncover linkages in the literature as well as understand the development of the field. The important steps in this analysis include extraction of keywords, calculation of keyword frequency, selection of high-frequency keywords, clustering them based on the co-occurrence index, followed by the formation of the networks. The visualization process also enables us to better define themes and draft clusters based on their correlation coefficient calculated by the software. In the network created by Vos-Viewer, the size of the nodes or vertex generally represents the occurrence or keyword frequency, while connecting lines depict that a relationship exists and that they are present in the same article. Similar coloured clusters usually form a part of the same theme or narrative.

Results

Themes Identified Through Co-occurrence Analysis

We use keyword co-occurrence analysis with a unit of analysis as all keywords (authors and keyword plus, minimum number of occurrence of a word set at 10 to ensure that keywords with high total link strength are selected). A total of 56 significant keywords are selected and a network is created. The network developed is characterized by centrality and density. Centrality refers to nodes that form central poles of any network connecting it to other clusters through mediator keyword or otherwise and are important determinants of the cluster theme. For each colour code cluster, an overlapping theme can be analysed.

Five interlinked clusters are presented each defining a recurring theme from literature. 1

Cluster 1. (Red) studies the policy implications of household debt, with a focus on the role of monetary policy leading to and after the financial crisis.

Cluster 2. (Blue) represents the strand of literature that studies household debt in the context of emerging financialization and increased income inequality, linking it to a crisis.

Cluster 3. (Purple) studies leverage and business cycle in the context of shocks such as fluctuations in interest rates and mortgage markets.

Cluster 4. (Green) represents the interaction of credit with economic growth and financial stability highlighting the role of housing wealth.

Cluster 5. (Yellow) represents the consumption channel of household debt, focusing on income/household finances and the implications of default on account of liquidity constraints.

Theme-based Review of Literature

Conventionally, the quality of an article is judged based on the number of citations received. However, both Scopus and Web of Science provide another metric that measures the influence and interest generated by a paper: the usage count. The usage count indicates the number of users that visit a database for a specific paper. For presenting an elaborate literature review on the identified themes, an index is created such that the number of citations and usage count are both included, each weighted equally. The authors review the papers with the highest score on the index developed.

Household Debt and Policy Framework

The global financial crisis has highlighted the trade-off faced by governments and policymakers between increasing financial access to households and the risk associated with high household leverage. There are two aspects to household debt-policy linkage. First is that the federal policies supported the unsustainable growth of household debt, and second, detailing the available policies to manage a household debt crisis.

The household debt levels stand at $47 trillion or 60% of GDP fuelled by accommodative monetary policy, unprecedented stimulus and low-interest rates (Tiftik & Guardia, 2020). These market-oriented, neo-liberalist policies have led to a shift from profit-led growth to more unsustainable debt-led growth (Stockhammer, 2016). In their paper, Justiniano et al. (2019) attribute the housing boom preceding the Great Recession as a major cause of crisis. The housing boom was a result of accommodative monetary policy and laxer lending conditions, evident from falling mortgage rates, an increase in household debt levels, a rise in house prices and stability of loan-to-value (LTV) ratio. At the same time, the financial structure which ensures easy lending and borrowing conditions has no built-in feature of risk sharing between the players. So, in the event of a shock, the onus of default falls wholly on the borrower, who in most cases is the weakest link of the system ineffective to bear the burden making the outcome of these ‘regressively redistributive’ policies (Walks, 2014). The lenders on the other hand are safeguarded by their senior claim on the borrower assets held as collateral (Mian & Sufi, 2014). In the event of liquidation of collateral, even though the surplus has to be returned to asset owners, it is a rarity as the lenders have no incentive to maximize the borrower’s return. For instance, the current property exemptions allow the mortgage creditor to foreclose a loan if not fully repaid, adversely affecting borrowers but benefiting the lenders (Berkowitz & Hynes, 2015).

It is also recognized that when the 2008 financial crisis struck, the war chest of policymakers and governments was devoid of targeted regulations and statutes for a crisis that had its roots in the household sector. There had been no previous large-scale crisis that was attributed to the household sector specifically, leaving governments and policymakers in a state of frenzy. To bring the economy back on track the Federal Reserve and other central banks adopted a set of radical policies that in normal times would lie outside the Overton window, such as huge bailout packages, quantitative easing and near-zero bound interest rates (Aloui et al., 2011; Mendicino & Punzi, 2014). In their book Firefighting, Bernanke et al. (2019) justify the use of controversial policies such as Primary Dealer Credit Facility for bailouts or Troubled Asset Relief Program to buy toxic securities, etc. However, the criticism of the policymakers has been substantial as the use of such policies and instruments had serious trade-offs.

In their paper, Alpanda and Zubairy (2017) assess the effectiveness of three categories of policies in controlling household debt crisis and the subsequent recession—macro-prudential policies such as LTV, housing-related tax and ultimately monetary policy. The preferred order for policy use is a reduction in tax deductibility, tightening of LTV (macro-prudential), raising property taxes and finally monetary policy. Along similar lines, Cerutti et al. (2017a) studied 12 macroprudential policies to calculate aggregate macroprudential policy index (MPI) with two major subcategories—borrower-targeted and financial institution-targeted instruments. In the context of household credit, the adoption of borrower-based measures leads to lower credit growth. However, the policies to be adopted need to account for structural and cross-country differences. In countries with weak institutions and macroprudential frameworks, the expansion of household credit particularly the deepening of mortgage markets has to be done under caution (Cerutti et al., 2017b). In another paper, Gelain et al. (2013) suggest that establishing borrowing constraints with a focus on income rather than house price growth or LTV reduces volatility for both household debt and house prices. Raising the interest rates, however, had the implication of raising inflation and is a less preferred measure. Also, debt modifications of distressed borrowers to reduce the principal at the start of the crisis can be used to prevent potential gains, avoid defaults and have a positive effect on consumption (Ganong & Noel, 2020).

Household Debt and Inequality

In the last four decades, there has been a rise in inequality, decline in social mobility and growing political polarization which has shifted the debate to the inequality–fragility relationship (Cardaci & Saraceno, 2019; Jauch et al., 2011). Research over the years has pointed out that the inequality–crisis nexus works in two directions, inequality leading to a debt crisis and debt crisis leading to increased inequality.

In an attempt to answer whether income inequality contributed to the growth of household debt before the Great Recession, Cynamon and Fazzari (2016) the great recession. In his paper connect two trends prevalent after the 1980s—the doubling of household debt to income ratio and the rise of income share to the top income distribution. Given the unequal distribution of income since the 1980s, the consumption rate of the bottom 95% should have declined, which was not the case suggesting that the bottom 95 was using debt to support the current consumption, beyond sustainable levels, coinciding with the great recession. In his paper, Iacoviello (2008) constructed a model economy to show that the consistent and sustained increase from the 1980s can only be explained through a simultaneous rise in income inequality. Researchers also provide robust estimations to show that a 1% increase in inequality is associated with a 2–6% increase in household debt (Klein et al., 2015). In line with the Veblen (1899) theory of conspicuous consumption, Kapeller et al. (2015) find that households with smaller incomes use debt as an instrument for maintaining a societal benchmark of the standard of living or what Christen and Morgan (2005) called ‘Keeping up with the Jonases’. This inequality pressures the low- and middle-income groups to use equity release for supporting consumption; a factor frequently associated with bad debt, banking distress and 2008 financial crises (Cardaci, 2018). Similarly, in their paper, Kumhof et al. (2013) link the increase in income inequality to the possibility of a financial crisis through an increase in household debt to income ratio. This relation is significant even after controlling for factors such as regulation, monetary policy, investment inflows and expansionary monetary policy (Perugini et al., 2016).

Empirical evidence shows a positive relationship between income concentration and indebtedness in the private sector, suggesting income distribution as a determinant of macroeconomic stability. In his paper, Stockhammer (2015) highlights four channels through which income inequality contributes to increased household debt; the marginal propensity to consume (MPC) differential between income classes, liberalization of international capital flows, and consumption fuelled by debt and financial innovation. As the people at the top have low MPC, they save more money which is pushed into the market for lending (Hudson, 2019; Rajan, 2010). This is evident from the high debt-to-income ratio, debt-to-asset ratio and high debt-service ratio of low- and middle-income groups which reflects the tendency of substituting loans for wages in the face of stagnating wages (Barba & Pivetti, 2009). For the upper class, financial innovation such as derivatives enables them to increase their speculative tendencies, thus creating a ‘global financial casino’ for the affluent, while lower income distribution supports consumption through debt (Stockhammer & Wildauer, 2016).

An often-overlooked research question is whether household debt causes income inequality, rather than the other way round. The current debt-based system is believed to have redistribution effects of income and wealth, increasing both the share of income of people at the top as well as widening the gap between top- and middle-income groups (Wood, 2019). While it may be argued that debt causes financial development and therefore greater income, it has been found that household debt is not associated with declines in income inequality while business debt is (Beck et al., 2014). The dramatic rise in debt relative to income has been higher in the bottom quintile of income, which is also faced with growth in debt to assets ratio. The former observation suggests increased sensitivity of households to rising interest rates and negative income shocks, the latter indicates deterioration in the value of the collateral and subsequent difficulty faced by poor debtors to meet financial obligations through asset liquidation (Crawford & Faruqui, 2011). On disaggregating household debt into mortgage, consumer and other debt, find that the credit card or payday loans are accountable for increasing income inequality.

In their paper, Berisha et al. (2018) suggest that household debt cause income inequality, usually through a heightened probability of financial crisis. As Galbraith (1994) states, each financial crisis leaves ‘a tiny minority enriched by the total ruin of all the rest of the people’, suggesting that the credit booms and busts are linked to income inequality. The credit booms are linked to low-interest rates, economic expansion and income inequality, all complementary rather than mutually exclusive factors (van Treeck, 2014). This indicates that excessive debt events are related to inequality episodes with cross-country differences. The inequality–leverage–crisis nexus is significant in the financialized economies indicating that the sustainability of finance is challenged by increased inequality (Gu & Huang, 2014). As financial markets develop, credit growth becomes pro-cyclical, moving in line with the real economy at the aggregate level. However, when the income dispersion is high, credit growth becomes more erratic (Iacoviello et al., 2008). Thus, the relation between inequality and household debt is asymmetrically co-integrated, with evidence that increased inequality leads to changes in household debt while the result for falling inequality is not significant. This observation has important policy implications, as any attempt at declining income inequality will not bring down household debt levels.

Household Debt, Mortgage Market and the Business Cycle

After the 2008 financial crisis, research on the effect of credit-driven boom–bust cycles in the ensuing crisis started gaining momentum. The way in which financial cycles expand and contract resulting in changes in investment and consumption decisions, expectations and risks defines the relationship with business cycles (BIS, 2014; Moore, 2008). This strand of research places households at the centre of business cycle fluctuations, operating through the credit supply channel. As the supply of credit expands (supported by low-interest rates), households borrow extensively for both consumption and investment. In booms even the constrained borrowers characterized by low credit scores and high credit card usage behave as if they have high discount rates, stimulating them to borrow more aggressively (up to 40 cents against $1) (Mian & Sufi, 2010) . This growth in debt is stronger than the income growth required to make the debt service payments, thereby creating a bubble. To control the growing bubble, central banks tighten credit growth and increase interest rates, which makes debt servicing more difficult. When debt service cost becomes greater than the amount borrowed to finance spending, the upward cycle reverses, leading to a business cycle downturn (Dalio, 2018).

The increased use of debt also supports the exuberance in the housing market. In tune with the credit supply hypothesis, Mian et al. (2017b) find that sharp rise in household debt to GDP can be attributed to increased mortgage lending which is evident from the doubling of the share of mortgages on the balance sheets of banks in the second half of twentieth century with two-thirds of banking business consisting of loans for residential investment (Jordà et al., 2016). This growth in mortgage finance can be linked to increased financialization, supported by financial innovation and regulatory changes that have transformed the fixed real-estate asset into a quasi-financial asset possessing liquidity (Aalbers, 2019). Financialization has changed the nature of housing from a safe-secure asset to a highly leveraged debt vehicle whose value is contingent upon market swings. This interdependence augments the business cycle and the financial fragility associated with mortgage or hypothecary lending-based real-estate booms (Oikarinen, 2009). During booms of the house price surges, households tend to borrow excessively in anticipation of further gains. The increased demand for household credit, securitization and growth of shadow banking over traditional banks have fuelled over-borrowing and over-investment beyond sustainable levels. Financial innovation and collateral constraints lead to undermining of risks prevalent in credit markets and consequences of imperfect information, leading more households to leverage debt for residential investment (Boz & Mendoza, 2014). So, while some households are able to use the asset price bubble to their advantage, others are left lurking in financial stress and debt overhang (Montgomerie & Büdenbender, 2014). Thus, from a macroeconomic perspective, residential investment is the best predictor of where GDP is going, with housing as the main driver of economic activity before the recession. In the event of a crash, the impact of house price decline on balance sheets and aggregate demand is associated with deflation. In Japan, the early 1990s was associated with a decline in Japanese equity and land prices, followed by prolonged productive activity and a deflation slide (Koo, 2009). In the United States, the housing bubble burst resulted in a rise of defaults by at least 34% between 2006 and 2008 (Mian & Sufi, 2011).

Even though a high household debt to GDP ratio does represent a more leveraged and therefore less stable financial sector, the fluctuations in the business cycles caused by the presence of high household debt are not the same across countries, varying based on financial development, government policies and resource dependencies (Loukoianova et al., 2019). In his paper Walks (2013) shows that households in global cities are more vulnerable to debt-related risks associated with house price fluctuations amid urban growth. Following the Great Recession, a new trend in housing is evident, particularly in major cities and tourist destinations—the growth of the rental bubble is supported by increased household debt (Blanco-Romero et al., 2018).

Household Debt, Economic Growth and Financial Stability

It is recognized that debt, despite the odds, is the lifeblood of the economy with the support it provides to households and businesses in smoothening consumption and making investment decisions. High levels of private-sector debt, for example, are often interpreted as a sign of financial development, which leads its benefits to long-term growth (Rajan & Zingales, 1998). A well-functioning financial system in a country channels funds to the most productive uses and allocates risks to parties who can bear them. It propels economic growth and opportunity . On similar lines, the extension of household credit is often taken as a proxy of financial deepening tempting economists and policymakers to consider this growth in finance as welfare-enhancing, though there is evidence to the contrary. Advocates of debt counter the concerns over excessive leverage, suggesting the importance of net wealth of a country over the gross debt (Fatas, 2011). Others contend that since gross debt is ‘(mostly) money we owe to ourselves’, it would not matter on its own (Krugman, 2011).

However, it has been found that excessive debt weighs on the growth of an economy interacting through the market mechanisms of spending and investment. Studies suggest that in many economies’ total gross debt levels are excessive and need to decline. Reports by McKinsey (2010, 2012) underline the need for advanced countries to reverse the rise in total gross Debt to ‘clear the way’ for economic growth. In a study of 20 countries by Eichengreen and Mitchener (2003), the authors found that the intensity of the credit boom was highly correlated to the intensity of economic downturns. Increased exposure to debt erodes the ability to withstand economic shocks (or shocks of non-financial nature), resulting in disruptions of payment flows and magnifying financial instability (Friedman, 1986). The role that finances play for resource-dependent countries is essential, but it also makes them vulnerable due to governments and the private sector’s propensity to borrow abroad. It was observed that countries experiencing sudden large capital inflows are at a high risk of having a debt crisis (Reinhart & Rogoff, 2008). Indeed, an outcome of using foreign credit is greater exposure of the domestic financial system to global fluctuations as was the case during the 1997 crisis of Thailand (Ranttila, 2016). The high external credit exposure is responsible for ‘sudden stops’—the phenomenon of sudden reversals of current account positions, and following severe recessions in emerging economies (Mendoza, 2010). Even the most advanced financial systems such as the United States may fail as the problems associated with excessive leverage outplay the strengths. An example of this is the new Triffin dilemma where the continuation of the dollar as the world’s reserve currency will increase US deficits, but its replacement will increase the value of debt (Bordo & McCauley, 2017).

The paper by Benczúr et al. (2019) finds a ‘non-linear, hump-shaped impact’ of credit on economic growth, with the effect being positive for non-financial corporate credit but negative for household credit mainly over longer periods. For instance, one standard deviation increase in household debt to GDP ratio over t–3 is related to a 2.1 percentage point decline over the subsequent three years (Mian et al., 2017a). In their paper, Mian and Sufi (2010) cite household leverage as an early predictor of recessions, with sharp increases in household debt followed by a decline in durable consumption, residential investment and unemployment. Private credit is an early warning predictor of a banking crisis, with household debt expansion having negative implications for long-run income (Büyükkarabacak & Valev, 2010).

These observations are in cognizance of the ‘credit view’, which proposes that the magnitude and mechanism of bank credit matter, as opposed to the ‘money view’, which focuses on the level of bank money. In other words, the entire bank’s balance sheet—the asset side, leverage and composition, has macroeconomic repercussions. It could be based on the financial accelerator effect, 2 Bernanke and Blinder (1992) or the financial fragility effect 3 stimulated by the constrained collaterals (Bernanke et al., 1999).

Household Debt and Individual Financial Decision

The crux of this strand of literature can be explained through Mr Micawber’s principle of financial prudence, ‘Annual income twenty pounds, annual expenditure nineteen pounds, nineteen shillings, and six pence, results happiness, annual income twenty pounds, annual expenditure twenty pounds ought and six, results misery’ (Dickens, 1850).

Debt is frequently used by households to finance asset (or quasi-assets) ownership, which are expected to generate a stream of income in future or provide equivalent services. Since the asset ownership of average households is concentrated in the housing sector, the house prices affect and are significantly affected by the levels of household debt. Since residential real estate makes up a large share of the household wealth, it makes the households more vulnerable to house price volatility. In the event of a drop in house prices, highly indebted households face challenges in the form of sudden wealth decline and collateral effects (Capozza & Seguin, 1996). This is particularly true for recourse loans which allow lenders to expropriate the borrower’s assets to recover the value of the loan, leaving them worse off than before . If a shock leads to a decline in house prices, weak households fail to service their debt, followed by bankruptcy and foreclosure. Usually, household with a debt-to-income ratio of above 350% and debt servicing ratio greater than 40% are considered to be financially weak. In a study by Alter and Mahoney (2020), the authors show how house price risks are higher for highly indebted financially weak households. In general, they find that in the short-run household leverage lowers the house price risk, while exacerbating them in the long run. It has been seen that the expectations of house price appreciation are high at the start but decline towards the end of the boom (Landvoigt, 2017).

Debt is frequently used by households to finance asset (or quasi-assets) ownership, which are expected to generate a stream of income in future or provide equivalent services. Since the asset ownership of average households is concentrated in the housing sector, the house prices affect and are significantly affected by the levels of household debt. Since residential real estate makes up a large share of the household wealth, it makes the households more vulnerable to house price volatility. In the event of a drop in house prices, highly indebted households face challenges in the form of sudden wealth decline and collateral effects (Capozza & Seguin, 1996). This is particularly true for recourse loans which allow lenders to expropriate the borrower’s assets to recover the value of the loan, leaving them worse off than before . If a shock leads to a decline in house prices, weak households fail to service their debt, followed by bankruptcy and foreclosure. Usually, household with a debt-to-income ratio of above 350% and debt servicing ratio greater than 40% are considered to be financially weak. In a study by Alter and Mahoney (2020), the authors show how house price risks are higher for highly indebted financially weak households. In general, they find that in the short-run household leverage lowers the house price risk, while exacerbating them in the long run. It has been seen that the expectations of house price appreciation are high at the start but decline towards the end of the boom .

High levels of debt have also been found to be related to lower financial assets, as households choose to forgo investment opportunities in view of debt service obligation. For instance, in Becker and Shabani, (2010), the authors use a survey of consumer finance data to show that households holding mortgage debt were 10% less likely to own stocks and 37% less likely to own bonds in contrast to households that had no mortgage debt. The behaviour of households towards tax incentives also varies between mortgaged and non-mortgaged households, the mortgage households being more sensitive to tax changes reflected in consumption shifts as compared to non-mortgages (Cloyne et al., 2019).

The results for consumption are on similar lines where Ogawa and Wan (2007) find that household indebtedness measured as a ratio of debt to assets has significant negative effects on spending not only for durables like land and housing purchases but also semi-durables and non-durables, even after controlling for wealth effects. Using household-level data, Dynan (2012) finds that the higher the extent of leverage, the larger the decline in spending. It is also seen that the increase in household debt-to-income ratio relates to household interest rate risk preference. Those households which have higher risk preferences are usually headed by young males, own few financial assets and have a high debt-to-income ratio (Nagano & Yeom, 2014). These young households with low asset holdings and high-risk preferences are more vulnerable to increasing their indebtedness beyond sustainable levels as compared to older, asset-rich and risk-averse households (Daud et al., 2018). The level of risk aversion is inversely related to the level of household debt (Brown et al., 2013). Incidentally, we also find that perceived peer income may also contribute to increased use of debt and the likelihood of financial distress (Georgarakos et al., 2014).

In another paper, Klapper et al. (2013) argue that individuals reporting high financial literacy are less likely to face negative income shocks and have high unspent income. Higher financial literacy is also positively associated with financial market participation and negatively with informal borrowing. Feng et al. (2019) used a joint modelling approach to evaluate the impact of financial literacy on the financial health of Chinese households. Households scoring high on the financial literacy index preferred secured over unsecured debt and had a higher proportion of assets (housing and non-housing), allowing them to hedge in the event of a crisis (Brown & Taylor, 2008; Cox et al., 2002). Also, the expectations about inflations and interest rates influence household financial decisions and in turn household borrowing. Those households that have high inflation experiences tend to borrow via fixed-rate mortgages and refrain from investing in long-term bonds. This tends to influence the portfolio choices of the households and real-asset prices (Malmendier & Nagel, 2016).

Apart from the major themes highlighted, increased household debt has also been linked to decline in credit scores (Han & Li, 2011;,Stavins, 2000), internal migration (Cooke, 2013), conspicuous consumption (Georgarakos et al., 2014), gambling problem (Gainsbury et al., 2015), obesity (Averett & Smith, 2014), mental health issues (Hojman et al., 2016), stress and psychological well-being (Shen et al., 2014), reduced happiness (Liu et al., 2019) and an increase in male suicides (Reeves et al., 2015).

Conclusion

This article provides a comprehensive overview of the current state of academic research and a review of the significant works in the household debt arena. The bibliometric analysis reveals that the research on household debt has increased exponentially since 2008 following the Global Financial Crisis, with the upward trend rising sharply during the pandemic period. Prior to this the household debt was studied at micro/individual levels with little impact on macroeconomy. At the same time, it is realized that literature on household debt is dispersed with little collaboration at the author or organization level. At the country level, most of the research originates in the USA, England and Germany while countries such as China, Sweden South Korea, Turkey and Brazil are newer contributors. Interestingly, the latter countries are currently witnessing a dramatic rise in household debt levels, hence, the supporting research. Atif Mian and Amir Sufi emerge as the experts in this field with the highest aggregate citations.

From the co-occurrence analysis and the subsequent literature review, it can be concluded that the increase in household debt is related mainly to five major factors including GDP, household consumption, house prices, inequality, policy framework and financial crisis. Of course, the trend in household debt is not the same globally, which is why the narrative shifts between various contexts and domains. Finally, based on the extensive review of the selected papers, it is realized that despite identifying five broad areas of study, a clear demarcation between these pieces of literature does not exist. For instance, the decision at the household level has macroeconomic repercussions, influencing aggregate demand, inflation, production activity and growth. The balance-sheet position of the households is linked through demand and supply to house prices, the real-estate industry and real interest rates. Similarly, rising household debt and residential investment fuel consecutive asset bubbles, which may leave the economy with a large and burdensome debt overhang. This challenges financial stability. In a typical debt crisis, the central bank can lower the real and nominal interest rates, keeping the economy afloat; in severe debt crises (i.e., depressions), this is no longer possible. The episodes of recession and depression are caused by inequality and also exasperate inequality. For instance, most financial assets are held by the top of the income distribution while the middle class owes most debt. Inequality is in turn connected to policy framework with the effectiveness of monetary policies increasing as income inequality declines. The presence of these linkages makes the study of household debt both paramount and difficult. It is clear that household debt impacts the micro- and macro-side of the economy while also influencing the trajectory of economic growth and dynamics of societal development. The review finds two contrasting narratives regarding household debt, one which considers the stimulating effects of household debt on consumption, bank profitability and housing market vitality; the other, which connects household debt excesses to financial market instability, insolvency issues and negative impact on the real economy. Between the optimistic and pessimistic view of household debt, the more popular literature seems to support the negative consequences of excessive leverage in the household sector.

The article however is limited to articles in peer-reviewed academic journals which can be extended to include books, reports, policy papers and expert blogs in future studies. An article solely focusing on a systematic literature review can incorporate other databases such as PubMed or Dimensions. The future research can detail on each of the identified themes to gain valuable insights into the channels through which household debt impacts the economy. This systematic review can also be used as a precursor of quantitative analysis on the lines of exploratory sequential research design.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.