Abstract

This study examines 120 research papers on cryptocurrency adoption, investment, and investor behavior using preferred reporting items for systematic reviews and meta-analyses–guided systematic literature review. Further, it intends to illustrate the key trends, institutions, and country contributions to this field through a bibliometric analysis. The findings indicate that people’s decision to adopt cryptocurrencies is primarily facilitated by social factors and hindered by fluctuations, ease of buying cryptocurrencies, and jurisdictional issues. It also reveals an impact of psychology, which erupts in the forms of herding and instrumental sentiments. A conceptual framework of cryptocurrency adoption and investment intensity in fintech ecosystem is proposed. The study provides fresh insights into investment intensity, fintech-motivated investment trends, and investor behavior in cryptocurrency.

Introduction

Fintech and cryptocurrency innovations can be regarded as critical drivers in shaping and advancing the future financial system. Bitcoin, Ethereum, and comparable assets constitute a distinct class of decentralized digital currencies. They operate independently of traditional banking systems, allowing transactions without intermediaries, and instead relying on peer-to-peer networks and blockchain technology (Nakamoto, 2008). Simultaneously, financial technology (fintech) encompasses a broad and dynamic spectrum, extending from digital banking to blockchain innovations, and outperforms the traditional approaches toward the provision of financial services (Feyen et al., 2021). Altogether, it is creating new venturing opportunities as well as new risks for market actors, investors, and authorities (Shan et al., 2024). Global resurgence of cryptocurrencies denotes an increase in popularity and acceptance of cryptocurrencies after crashes which were experienced in 2018 and subsequent volatile market periods. Hence, cryptocurrencies promise to be a (fast, transparent, and cheaper) alternative to the traditional banking industry. This newly arising interest is mainly related to their ability to replace such banking services. As a result of these attributes, cryptocurrencies have become attractive substitutes to conventional financial services and are back in vogue among institutions, investors, and fintech innovators.

Nakamoto introduced a new era in the financial industry with the introduction of Bitcoin, which sparked the development of numerous other cryptos such as Ethereum, Litecoin, Ripple, and Dash (Almeida & Gonçalves, 2023; Nakamoto, 2008). As Feng et al. (2018) point out, these digital assets have gained great appeal over the course of a very short time, becoming rapidly traded in the global financial markets and attracting the attention of mainstream retail investors, institutional players, and regulators. A phenomenon that was existent only in the technology circles has now migrated into the mainstream business domain where institutions and corporations have willingly accepted cryptocurrency as an investment class (Taera et al., 2023). But this phenomenon has faced numerous challenges. This is because prices vary drastically in a short span of time due to regulatory crackdowns in most regions. Governments and regulatory authorities worldwide underwent various issues, especially in designing an environment that not only meets security and stability requirements but also fosters innovation in the finance sector (Zhang et al., 2023b). The combination of regulatory ambiguity and market volatility continues to limit the effectiveness of cryptocurrencies in formal financial system.

The crossing point between cryptocurrency and fintech is becoming increasingly complex, focusing on enabling financial services, particularly in areas where they are often unavailable. For instance, technologies such as decentralized finance (DeFi), blockchain, and cryptocurrency trading platforms are starting to transform the delivery of financial services, offering a cost-effective and efficient alternative to traditional banking services. These developments offer potential financial services to countries that have weak formal banking sectors. Moreover, fintech can extend banking services to populations previously without access to formal financial services (Shan et al., 2024). Furthermore, fintech advancements significantly contribute to expanding global financial inclusion by facilitating cross-border money transfers and suggesting new investment opportunities. In contrast to conventional markets, where basic, technical research primarily drives choices, cryptocurrency markets are more susceptible to behavioral biases such as the fear of missing out (FOMO), speculation, and herding (Kyriazis, 2020). When these behavioral patterns are combined with the high volatility of the cryptocurrency market, it creates a risky environment that poses a significant threat to both retail investors and institutional players to effectively manage investment risk and invest in the cryptocurrency market (Kouhizadeh et al., 2021). Scholars from various fields have explored the cryptocurrency market, especially to understand investor behavior, market volatility, and regulatory responses. Previous literature has studied numerous factors influencing investor behavior, including sentiment (Anamika et al., 2023; Drobetz et al., 2019; Guégan & Renault, 2021). From the above-mentioned perspective, it is clear that the distinctive characteristics of cryptocurrency markets have sparked a lot of scholarly interest in investor behavior.

Despite the rapid growth of cryptocurrencies and their increasing role in fintech, there are still critical knowledge gaps in relation to the reasons behind the adoption of cryptocurrencies and investor behavior in new markets. The wider usage of cryptocurrencies is hampered by regulatory issues like ambiguous regulations in various countries, which pose a big uncertainty to businesses and customers (Chohan, 2017). Meanwhile, emerging fintech technologies are exceeding the regulatory environment, which raises sustainability and risk management concerns (Kouhizadeh et al., 2021). Another critical area that is rarely studied is the investment intensity in cryptocurrency markets. Traditional financial markets have long benefited from studies of investors’ psychology and risk perception, but we have not even started applying these models to the relatively new and volatile cryptocurrency markets. Hence, this article aims to review and compare the adoption of cryptocurrency using the Scopus and Dimensions databases. While the search criteria did not impose any specific year limitation, the analysis predominantly focuses on articles published between 2018 and 2024. This time period indicates the increasing scholarly and business interest in the cryptocurrency adoption, investor behavior, and fintech innovations. Articles were screened based on the relevance to these topics and restrained to inclusion and exclusion. Unlike in previous studies, the articles included research from a variety of fields, as the issue was related to some primary topics— cryptocurrency investment, adoption, and investor behavior with crypto investments.

Methodology

The study follows a systematic review process guided by the preferred reporting items for systematic reviews and meta-analyses (PRISMA) framework, which provides a transparent and replicable structure to literature synthesis. In order to further guarantee the rigor of the sampling strategy, we utilized the studies by Jiang et al. (2021) and Yue et al. (2021) in drawing both the sampling strategy and the sampling procedure. Scopus and Dimensions databases were chosen, as they offer wide coverage of peer-reviewed research and extracted studies published between 2018 and 2024. This period reflects the recent surge in cryptocurrency adoption and investment intensity in the fintech sector. We focused on the period 2018–2024, as most studies on cryptocurrency and fintech innovation emerged during these years (AlQudah & Bariviera, 2025). In this regard, we adopted the protocol of the systematic review (Table 1) in accordance with the aim of the study and in reference to Briner and Denyer (2012). In this framework, it was set apart from the works of Flori (2019), Haq et al. (2021), and Jalal et al. (2021) by exploring a wider range of keywords, not limited solely to those related to behavioral finance. Instead, we employed a wide range of keywords, including “cryptocurrency,” “cryptocurrencies,” “Bitcoin,” “portfolio diversification,” “investment,” “investors,” and “alternative investment,” which allowed us to cover cryptocurrency adoption, investment, and investor behavior much more comprehensively. As a result, this stringent quality criteria aided us to identify the literature. Subsequently, we finalized the inclusion criteria by incorporating only English-language academic journal articles. Furthermore, we included not only peripheral studies in the cryptocurrency and fintech innovation investment area but also supplementary peripheral studies that incorporated broader insights into cryptocurrencies and fintech innovations, resulting in a larger depth and breadth within the review. In addition, we excluded articles that concentrated on blockchain technology, mining activities, and money laundering, as they did not pertain to the study’s focus on investor behavior and investment trends.

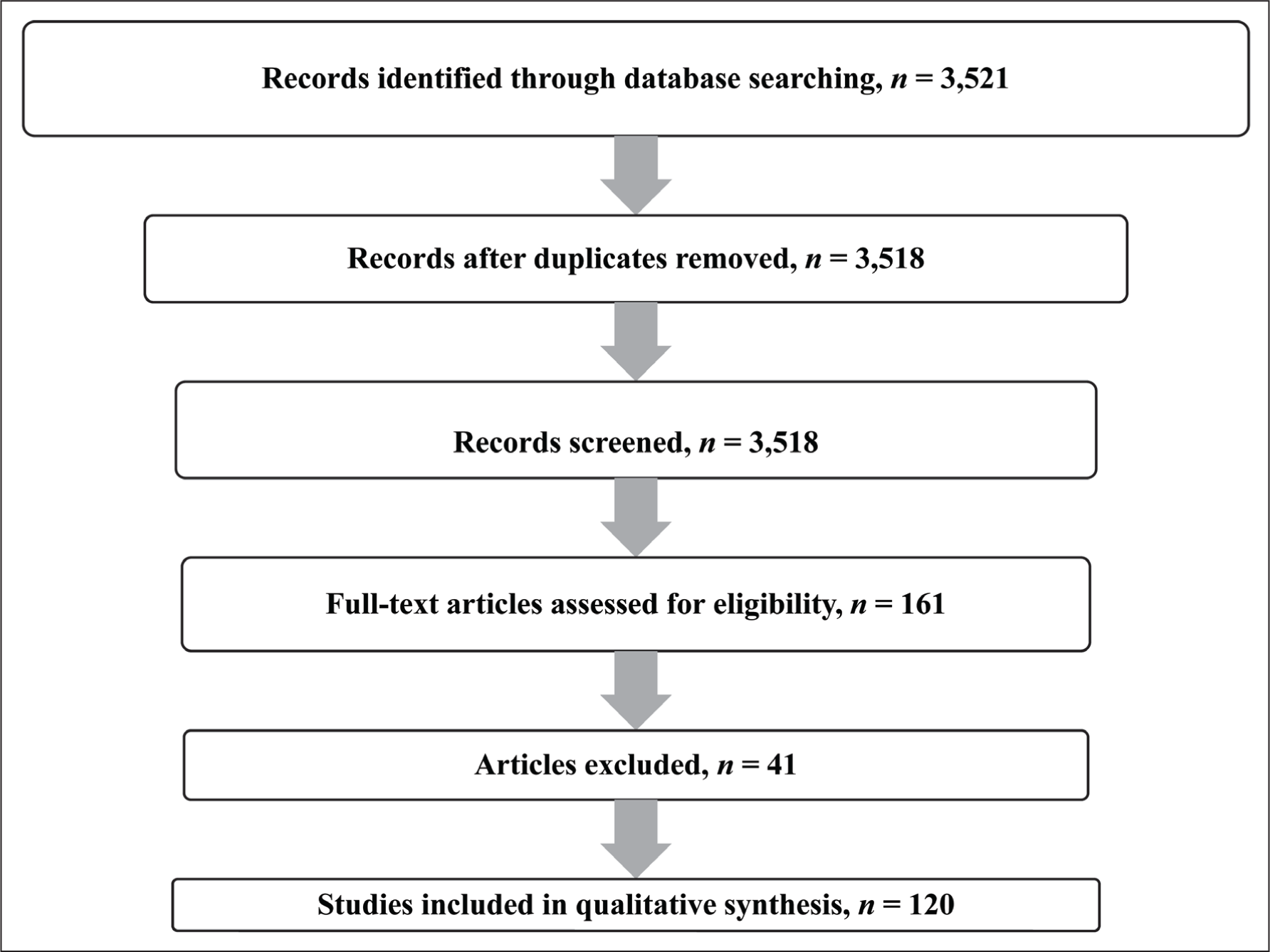

Protocol of SLR.

In this study, the PRISMA method was used as it is a widely and rigorously accepted tool for systematic literature review practices (Page et al., 2021). Completeness, replicability, and transparency in identification, screening, assessing eligibility, and inclusion of relevant studies have been clearly defined through a structured methodology. Hence, this study relies on PRISMA method to guarantee the methodological rigor and combines different studies on cryptocurrency adoption, investment intensity, and investor behavior within fintech literature. The PRISMA flow diagram (Figure 1) details the exacting path by which our cohort was narrowed by articles and analyzed. Thus, a keyword search for 3,518 articles was first conducted and later sifted through to yield a final list of 364 articles. Removing duplicates, these articles were screened preliminarily according to their title and abstract, to evaluate their relevance to cryptocurrency adoption and behavior of investors. And it was found that 161 articles had their field narrowed to required conditions, which were screened as full text and then screened in detail for eligibility based on our inclusion and exclusion criteria.

Following the full-text screening, studies that specifically examined the nuances of cryptocurrency adoption and the behavioral patterns of investors within the cryptocurrency financial sphere were retained for further analysis. This article also considers studies on investor behavior, investment decisions, or the psychology of investors. Additionally, this study also included specific research articles on fintech innovation or blockchain technology if they were related to cryptocurrency adoption or investment. However, our exclusion criteria were restricted to those articles that merely discussed the technological aspects of blockchain and cryptocurrency mining. The study also excluded the articles that do not contend with a direct facet of invoking investor behavior or the choice of conduct toward cryptocurrency markets. Also, the study excluded blogs or non-peer-reviewed publications and conference papers. It is from this critical assessment that 41 articles were excluded as they did not meet these stringent standards and we had a curated set of 120 studies that were incorporated into our qualitative synthesis.

Subsequently, the above selection was based on the aim to reduce the number of research articles to high-quality and high-impact studies that deepen the understanding of the dynamics of cryptocurrency markets and the behavior of investors. In addition, we deepened the analysis of the data with bibliometric tools (Bartolacci et al., 2019; Galvao et al., 2019; Rialti et al., 2019). In this process, the largest contributions in the field of high-frequency trade were identified, displaying the most-cited institutions and countries. The result also displays the trends in the relationship between the behavior of investors and market sentiments. As a result, the application of these analytical tools and rigorous methods provides new insights into the behavior of cryptocurrency investment strategies and market dynamics.

Bibliometric Analysis

This study has carried out a bibliometric analysis with the help of Biblioshiny (Table 2). The analysis of the selected articles was limited to predefined keywords. Hence, it reflects the core themes of cryptocurrency adoption and investor behavior in the fintech sector. Because of this systematic process, the study found the most relevant journals in this field of research. The journal Finance Research Letters has made a vast contribution to the field with 13 articles. With the Q1 Scimago Journal Rank (SJR), the journal had a high impact on the cryptocurrency research community. Following the Finance Research Letters, the International Review of Economics & Finance contributed six articles. The Journal of International Financial Markets, Institutions & Money and Research in International Business and Finance have contributed five articles each. In addition, four articles each were contributed by the International Review of Financial Analysis and the Journal of Behavioral and Experimental Finance. The Energy Economics has contributed to the domain with six articles. Further, other journals listed in Table 2 have each contributed two articles in the field. With the presence of diverse journals, this bibliometric analysis exhibits journals from various quartiles of the SJR, from Q1 to Q4. The review was mainly focused on such journals, since these journals had a significant and high impact on the themes related to Bitcoin and fintech.

Most Relevant Sources.

In this sense, the journals on the list are quite diverse: journals specializing in economics and finance are joined by more interdisciplinary journals, such as the Technology in Society and Human Behavior and Emerging Technologies, which indicates that cryptocurrency studies are interdisciplinary. The variety of this type will not only include all possible scholarly views about the cryptocurrency but will also make our review comprehensive enough. Therefore, applying a bibliometric method based on an objective and systematic distribution, our selection process proves that the choice of the articles is not biased toward special publications and, at the same time, covers the main contributions in the field. Thus, the integration of SJR quartiles adds to the substantiation of the validity and academic prestige of the literature basis, and therefore, our findings are grounded in legitimate and relevant research.

The bar graph in Figure 2 depicts the institutional affiliations that have contributed to studies about cryptocurrency adoption and investment intensity in the fintech domain. South Ural State University and the University of Lisbon are the most prolific contributors, with three publications for each. This concentration of output is an indication of a high degree of expertise concentrated in these institutions. Further, the University Sains Malaysia, University of Pretoria, and Uttaranchal University each contributed two articles, indicating they are emerging hubs. The remaining institutions contributed one article each, highlighting a skewed distribution where few dominate the output, per Lotka’s law patterns given in Figure 7.

Figure 3 shows the geographic pattern of research articles related to the adoption of cryptocurrency and the intensity of investment in fintech from 2018 to 2024. The analysis is concentrated in six nations, namely, Indonesia, China, the United States, Saudi Arabia, India, and the United Kingdom. Indonesia’s number of publications increased intensely from 1 in 2018 to 12 in 2024, an evidence of a strong momentum in an emerging market. The United States, after a weak beginning, increased their output to four publications in both 2023 and 2024. Saudi Arabia had no publications before 2020 but reached six by 2024. India has a steady overcoming curve, reaching the peak of five publications in 2024. Meanwhile, the United Kingdom had a consistent moderate growth with six publications in 2024. These developments together suggest a growing international interest, where emerging markets including Indonesia, India, and Saudi Arabia are increasingly challenging the leadership of established fintech hubs in the United States, the United Kingdom, and China.

Figure 4 describes the author collaboration network as produced by the bibliometric analysis and thus provides insights into relevant structural patterns in research productivity. A conspicuous red cluster, centered on Larisa Y.’s high-degree centrality, marks her as a key hub that is closely connected with John W., Akanksha J., Roman M., Imran M., and Shaen C.. This dense interconnection of the core supports the interdisciplinary diffusion of knowledge and demonstrates the group’s great influence on the field. Almeida J. appears to function as a broker, exhibiting high betweenness centrality and maintaining independent connections across different clusters. Smaller clusters, such as Chaubey D., Kala D., Al Maghrebi M., Kumar S., Alsomoush K., and Alsmadi A., are characterized by thematic or geographic modularity, with a low density but high clustering coefficients. Taken together, the network structure suggests limited global collaboration, where centralized collaboration structure concentrate influence within a few dominant groups while constraining broader knowledge exchange across the field.

A thematic map of research topics is presented in Figure 5, which classifies them in four quadrants: basic, motor, niche, and emerging/declining. Basic themes include Bitcoin, cryptocurrency, fintech, and effects of COVID-19 that form the basis of the fundamental core of the literature characterized by high centrality and comparatively low density. Motor themes which involve investment alternatives, portfolio diversification, and investor focus exhibit both high density and centrality, thus motivating much academic and practical progress. Niche themes such as behavioral finance, asset pricing, investor behavior, market volatility, and Bitcoin adoption occupy specialized quadrants with low density and low centrality, indicating maturation or decline. Consequently, the thematic transformation implies a foundational cryptocurrency conceptual shift to dynamic investment strategies.

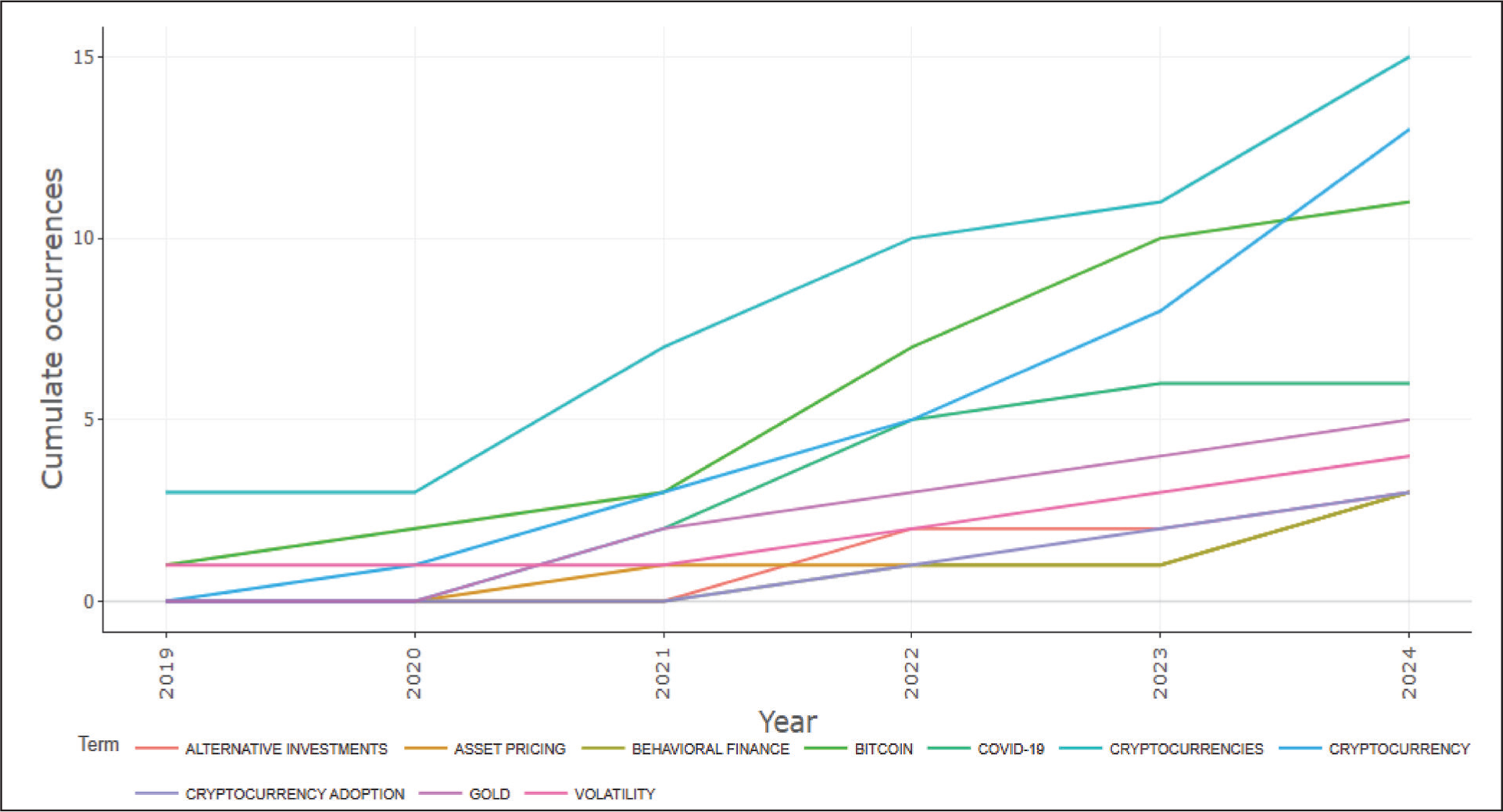

In Figure 6, occurrences of keywords from 2019 to 2024 are shown, thus revealing the dynamics of the research focus in cryptocurrency adoption and fintech. Terms such as “cryptocurrencies,” “adoption,” “Bitcoin,” “digital assets,” “asset price,” “alternative investments,” and “market volatility” show sharp rises, especially in the post-2021 period, thus capturing the ripeness of fintech and a heightened academic interest in the dynamics of digital finance. On the other hand, some keywords, such as “behavioral finance,” “COVID-19,” and “gold,” show little or flat growth, indicating a relative decline in scholarly focus in the face of the boom in cryptocurrency-related topics.

Figure 7 shows the application of Lotka’s law on the authors’ productivity in cryptocurrency and fintech research. The great majority of authors have only one publication, while a few elite authors have many times the average volume of output, thus highlighting underlying inequities of academic publishing. This core–periphery distribution is similar to the author network given in Figure 4, showing the importance of prolific researchers’ leading advances in the literature about the adoption and intensity of investment in cryptocurrencies.

Cryptocurrency Adoption and Investment Intensity Literature

Investment Motivation

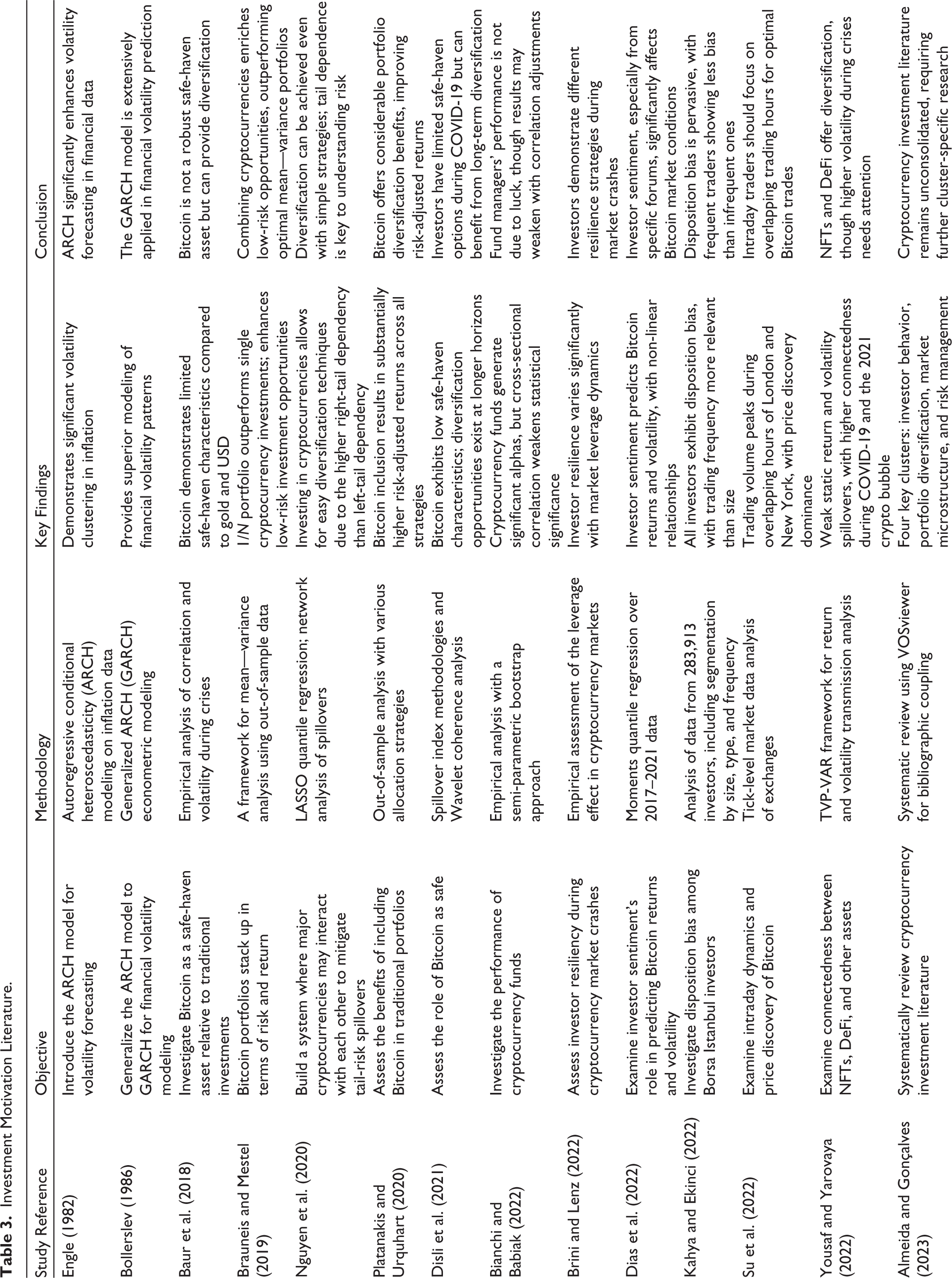

Cryptocurrency is an emerging asset class for investment that provides a wide array of incentives, such as high returns and diversification against financial stocks. As seen from Table 3, the primary motivation factor for investors is the performance of cryptocurrencies. Bianchi and Babiak (2022) show that cryptocurrency funds could generate positive alphas, thus attracting those investors seeking higher returns. Other significant facilitators include diversification and risk management. The relatively low correlation between the value of cryptocurrency and other traditional assets attracts investors to diversify their portfolios. However, such alpha performance will need to be put into perspective in terms of market cycles. Also, these funds may not be able to hold on to their profits during market downturns with high volatility. Therefore, cryptocurrency appeals to investors with high-return opportunities and diversification benefits. In addition, its performance tends to rely on market cycles and volatility. Hence, it is limited to ongoing gains.

Investment Motivation Literature.

Nguyen et al.’s (2020) study shows that tail-risk spillovers in the cryptocurrency market may be used as a diversification strategy. Thus, it may increase the risk–return profile of investment portfolios. This study also shows additional insights into the re-emergence of cryptocurrencies as possible safe-haven assets in times of crisis. Similarly, Disli et al. (2021) have revealed that Bitcoin is not a completely safe-haven asset, but it provides meaningful benefits in diversification during times of financial instability, such as the COVID-19 pandemic. During a highly volatile period, this dynamic would appeal to investors seeking alternative asset investments. Besides, as shown by Brauneis and Mestel (2019), the inclusion of cryptocurrencies can potentially be in portfolios to enhance the Sharpe ratio and strengthen the investors’ role in optimization strategies of risk and return. However, crisis behavioral patterns of investment are not determined solely by the behavior and sentiment of investors. Dammak et al. (2023) demonstrate that investor behavior significantly changes in the case of a crisis and is motivated by fear or the search for stability. Hence, their contribution has shown the significant role of sentiment on investment patterns. Similarly, Dias et al. (2022) find that there is a strong correlation between emotions and investor sentiment, returns, and volatility of Bitcoin. These psychological factors, such as FOMO and herd mentality, enhance speculative behavior in online forums and sentiment-oriented discourse about cryptocurrency and, as a result, investors’ participation in cryptocurrency markets. These emotional dynamics are characterized by the extreme change in prices and as such need to consider models that are capable of capturing such volatility. Therefore, the findings indicate the role of cryptocurrencies as diversifiers and connected to market dynamics and reactions of investors in moments of crisis.

Engle (1982) introduced the autoregressive conditional heteroskedasticity (ARCH) model and significantly contributed to volatility modeling, since it captures volatility clusters in financial data. From this framework, Bollerslev (1986) developed the generalized ARCH (GARCH) model that enhanced the ARCH approach by providing a more robust method for analyzing the financial market volatility. The GARCH has become a standard approach for modeling market fluctuations in the financial markets and is widely applied to assess the risk and flexibility of various investments. Further, Yousaf and Goodell (2023) examined the fall of the FTX exchange and showed that reputational contagion places profound constraints on investor behavior following such market crises. If a reputational crisis creates the fear of contagion, investors may begin to question the security of their digital asset holdings, influencing the market dynamics. Volatility is not solely a statistical phenomenon; it is also shaped by technical factors and investor sentiment, especially during a period of crisis when confidence in digital assets tends to weaken.

In this context, behavioral biases, such as disposition bias, also impact cryptocurrency investments. Psychological factors often surpass logical approaches in decision-making, which is where trust shocks come into play. According to Kahya and Ekinci (2022), investors retain underperforming assets for long periods of time in disposition bias, thereby influencing their decision-making processes. It demonstrates how the knowledge of psychological issues in cryptocurrency trading can help explain the propensity of investors’ biases to dictate suboptimal investment decision-making. Consistent with this, Platanakis and Urquhart (2020) discovered that adding Bitcoin into conventional stock–bond portfolios significantly enhances risk–adjusted returns. Thus, this finding aligns with the growing trend of integrating cryptocurrencies into the traditional financial market framework. However, investment behavior is not only determined by rationality but also influenced by emotions and trust dynamics, as well as behavioral biases like contagion effects that collectively shape market outcomes.

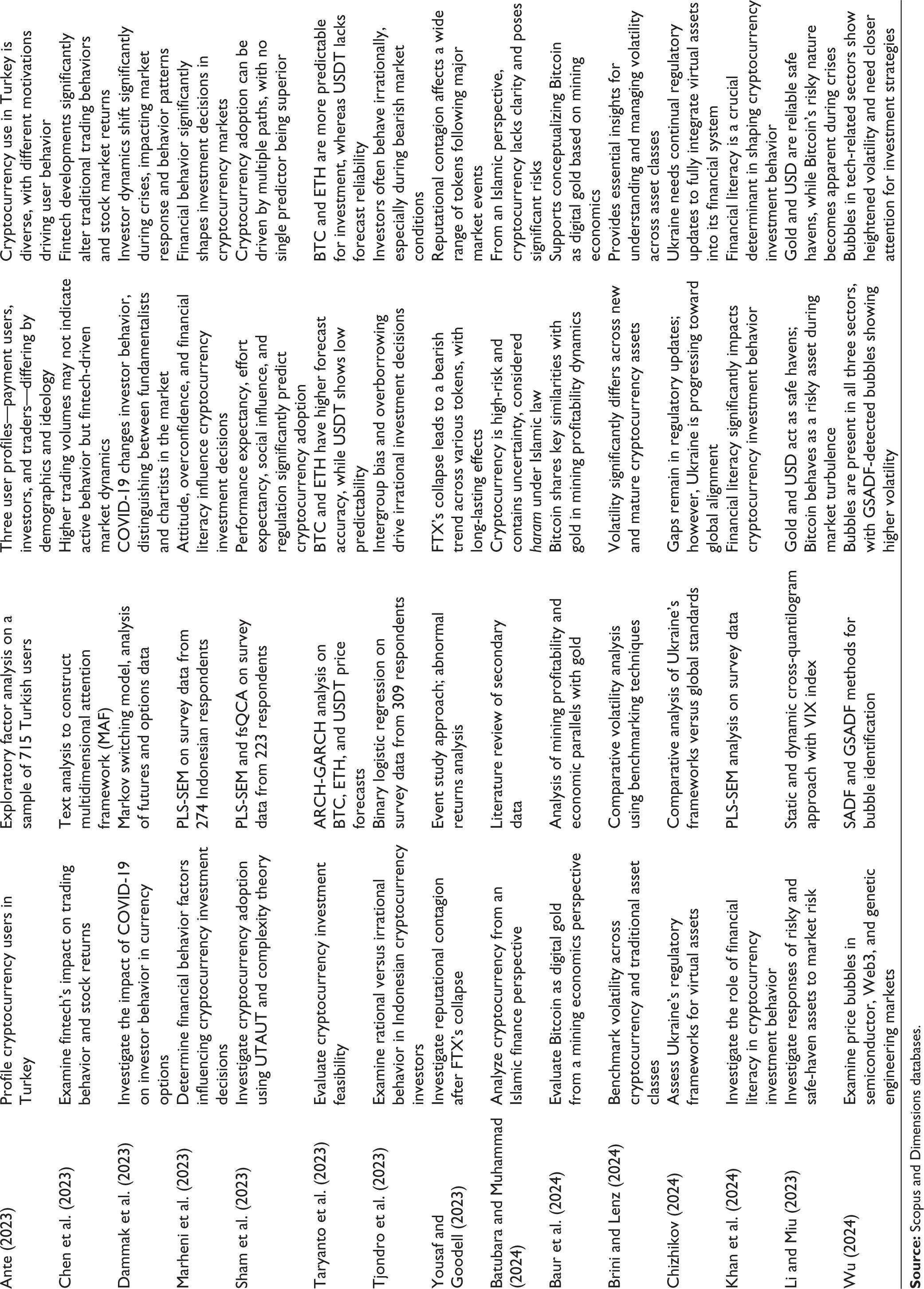

In this domain, recent literature has identified various factors that influence cryptocurrency investments to shed more meaningful light on the causes of these investments. The first motive may be speculation based on the price bubbles in emerging technologies like cryptocurrencies. Wu (2024) found that speculative bubbles occur often in industries such as semiconductors, Web3, and cryptocurrencies. And investors of these industries seek high-risk, high-reward but volatile opportunities. Integration of non-fungible tokens (NFTs) and decentralized finance (DeFi) with legacy assets such as oil and gold creates opportunities for diversification; investors become interested in investigating these new asset classes. In addition, Yousaf and Yarovaya (2022) show that traditional markets remain disconnected from NFTs and DeFi, providing investors with the benefit of diversification to hedge against their portfolio. Additional factors driving investor interest include a search for stability in a market that often sinks into chaos. According to Sokhanvar and Hammoudeh (2024), crypto coins act like a risky asset resulting from a prominent crisis, whereas traditional safe havens, such as gold and the US dollar, keep their stability. Thus, they influence the choice between risky and safe-haven assets. Sham et al. (2023) noticed, based on the unified theory of acceptance and use of technology (UTAUT) model, that these factors, both personal and technological motivators, are the primary impetus behind cryptocurrency adoption in Malaysia. The advent of fintech technologies has significantly shifted how investors operate. Chen et al. (2023) showed that the usage of fintech innovations, as in China, increases accessibility and new trading options. Therefore, it has brought more investors’ involvement into the market. Furthermore, the regulatory developments around virtual assets are another motivation for investors. Batubara and Muhammad (2024) and Chizhikov (2024) underlined the significance of the contemporary regulatory environment in Ukraine. Also, it is seen as a very important factor for investors because it gives clarity and confidence to the virtual asset market.

The ARCH and GARCH models motivate investors by helping them to forecast cryptocurrency prices more accurately. Taryanto et al. (2023) use these methods to forecast Bitcoin and Ethereum prices for investors who require data-driven insights to support their investment strategies. These studies demonstrate that cryptocurrency investments can be driven by various motivations, such as speculative opportunities, regulatory compliance, portfolio diversification, or the introduction of fintech innovations. Additionally, Brini and Lenz (2022) examined the leverage effect and tourists’ preparedness to face cryptocurrency market crashes with properties varying by country. Similarly, Brini and Lenz (2024) have classified the cryptocurrency volatility by new and already existing asset classes to understand cryptocurrency volatility more appropriately. Likewise, Baur et al. (2024) conducted a mining-focused study on Bitcoin, contributing to the discourse surrounding its characterization as “digital gold.” Extending this line of study, Baur et al. (2024) examined Bitcoin’s volatility in relation to the mining industry and demonstrated that its behavioral patterns align closely with traditional commodities, thereby reinforcing the notion of Bitcoin as the digital counterpart to gold. As a result, previous literature indicates that there a wide range of factors motivate investment in cryptocurrencies. Financial incentives, such as the potential higher returns, diversification benefits, and portfolio protection, remain the central motivations. In addition, psychological aspects, such as FOMO, herding behavior, and risk-seeking tendencies, also drive investors’ decision. Additionally, external factors such as government regulation and fintech advancements also exercise a substantial influence on investment motivations in the cryptocurrency market.

Investor Behavior and Investment Intensity in Cryptocurrency Markets

A thorough understanding of investor behavior is essential for assessing the adoption and degree of investor engagement in cryptocurrency. Existing literature indicates that social influence significantly shapes investors’ decision-making processes in the cryptocurrency market. In a similar manner, Gupta et al. (2021) exhibited that social networks and peer pressure have a large effect on investor intentions in the cryptocurrency market. Thus, social influence is not the only factor that influences investment decisions, but financial literacy, resource availability, performance expectancy, and perceived usefulness also influence the investor decision. In addition, the users of traditional financial market have a different perspective on the volatility of markets than investors in cryptocurrency. While a conventional market is more likely to be informed that the market is becoming volatile as a negative news, crypto investors see it as an opportunity to increase returns (Nadler & Guo, 2020). Besides, this peculiar behavior from investors shows just how high-risk, high-reward crypto investing can be. Short-term investors may execute high-frequency trading strategies using elevated sentiment periods and a high trading volume (Karaa et al., 2021). Additionally, they offer lottery-like payoffs, which attract investors who would not bother with stock market cash risks during a potential crash (Grobys & Junttila, 2021). Similarly, Pelster et al. (2019) also noted this risk-seeking behavior, observing that crypto investors are willing to engage in speculative trading, even in the face of significant risks, rather than accept low returns in the hope of achieving high ones.

The intensity of cryptocurrency investment is associated with both rational and irrational investor behavior. For instance, Gemayel and Preda (2021) have found certain tendencies of irrational learning of cryptocurrency investors the less-successful investors have the tendency to reinvest their losses, similar to gambling. A tendency toward risk-taking, which is actually an attempt to offset or recover losses, may exacerbate financial distress. On the other hand, successful investors tend to maintain their market positions, opting for continuous exposure to crypto assets and either withdrawing or depositing additional funds. The pattern of behavior indicates a high level of investment intensity due to ambiguity aversion, where investors prioritize familiar risks over uncertain outcomes (Luo et al., 2021). Sociodemographic factors also influence the crypto investment behavior. Australian females are less likely to invest in cryptocurrencies, while higher-income Australians are more likely to invest, in particular, in initial coin offerings (ICOs) with strategic long-term plans, according to Xi et al. (2020). Chinese crypto investors, on the other hand, are younger (18–30 years) and more concerned with the short-term, speculative gains at the expense of ICO strategic plans and white papers (Fahlenbrach & Frattaroli, 2021; Xi et al., 2020). This finding suggests that investors from different socioeconomic groups have varying levels of intensity and motivation: Australians prefer longer-term investments, and Chinese investors are looking to make short-term speculation. Moreover, most crypto investors are inclined to prefer centralized exchanges compared to decentralized exchanges because of the trading and liquidity powered by these platforms (Aspris et al., 2021). Investor sentiment significantly influences the behavior of the cryptocurrency market. Anamika et al. (2023) prove that investor sentiment in its microeconomic (personal indicators of financial well-being) or macroeconomic (general indicators of economic welfare) form can explain the price movement of cryptocurrencies. Burggraf et al. (2021) also observed that optimistic sentiment in the Bitcoin market leads to low returns, and pessimistic sentiment correlates with riskier investor behavior. According to Gaies et al. (2021), there is a tendency for cryptocurrency prices to rise when traditional equity markets exhibit bearish sentiment.

Market sentiment also determines different degrees of investment intensity. Bitcoin investors tend to engage in more transactions when people are more optimistic but in less during pessimism because they want to prevent any losses. In cryptocurrency markets, dynamic balancing of sentiment and investment intensity takes place, with optimistic investors eventually reducing their trading volumes if their sentiment does not align with their investment intensity, a scenario that is currently playing out. Due to the significant participation of individual investors in cryptocurrency, with trading peaks on weekends, its decentralized nature, and its potential for very high returns, its popularity has risen. In fact, local working hours more closely align with the timing of trading activity, suggesting rather that the cryptocurrency locality influences actual trading patterns (Jain et al., 2019). On the one hand, this observation also reminds us that cryptocurrency markets are truly global and even cross the globe, not just around the clock but also according to regional working hours. The cryptocurrency market is a sentiment-based market, where the sentiment component plays a crucial role in driving price movement and trading. As Hou et al. (2020) show, prices in the crypto market heavily correlate with popularity, emotions, and public sentiments. In particular, the returns on cryptocurrencies depend on optimism. Positive news about Bitcoin or another cryptocurrency disperses returns, converges expectations, and drives up prices (Caferra et al., 2021). The findings suggest that investor sentiment significantly influences the volatility and pricing of cryptocurrencies, and the impact of market emotions on cryptocurrency price movements can either increase or decrease, depending on the overall sentiment of investors. Mai et al. (2018) find that internet forum discussions have a greater impact on Bitcoin’s value than the tweets do (even if both are correlated to future price movements and particularly when there are more bullish posts). As per Kraaijeveld and De Smedt (2020), Twitter setiment predicts price returns on cryptocurrencies, with tweet volumes typically serving as an indicator for upcoming price movements. Similarly, Web search activities on platforms such as Google and Baidu predict cryptocurrency volatility. High search intensity related to Bitcoin price and fundamentals is therefore closely associated with subsequent volatility (Bleher & Dimpfl, 2019; Süssmuth, 2022).

In the light of the significance of sentiment and public information, social media have played a prominent role in reducing information asymmetry between investors and ICOs (Domingo et al., 2020). Through these channels, investors can understand the market sentiment and get a glimpse of various projections of cryptocurrency, which in turn can, at the same time, potentially influence their future investment decisions. In this respect, ICO issuers must minimize the information asymmetries by maximizing information about their projects to ensure the attraction of a wide range of investors (Thies et al., 2022). Finally, the sentiment analysis of white papers used in ICOs can be used to determine that there is a positive correlation between the tone of these documents and higher investor confidence, meaning that white papers can be effective in influencing investor perception. Although transparency will be improved due to soft information and voluntary disclosures, they are a risk since disclosures might be manipulated to deceive investors (Zhang et al., 2022). Surprisingly, the fast increase in market capitalization usually leads to the possibility of manipulation, specifically in smaller and less-developed digital assets (Gandal et al., 2021). These findings show that a stronger regulation framework is necessary to safeguard investors and maintain market integrity. Therefore, the behavior of information in cryptocurrency markets has a dual aspect, that is, openness and disclosure. These aspects may empower investor confidence and participation and, at the same time, introduce vulnerabilities, which can be used to manipulate the markets.

Financial intermediaries, such as institutional investors, that could play a major role in filling this regulatory void through providing market confidence and serving as trusted intermediaries would find it advisable to initiate trade. The participation of these investors can indicate the quality of ICO projects and will inevitably attract more retail investors, thereby increasing the stability of the market (Momtaz, 2021). From this perspective, sentiment, social influence, and the availability of information significantly affect both the behavior and the investment intensity of cryptocurrency investors. Cryptocurrency prices are strongly influenced by the public sentiment, especially as expressed through social media, and investor participation is closely linked to perceived transparency and trustworthiness of ICO projects. In the rapidly expanding cryptocurrency market, understanding these dynamics is vital for managing the investment risk and informing future regulatory developments.

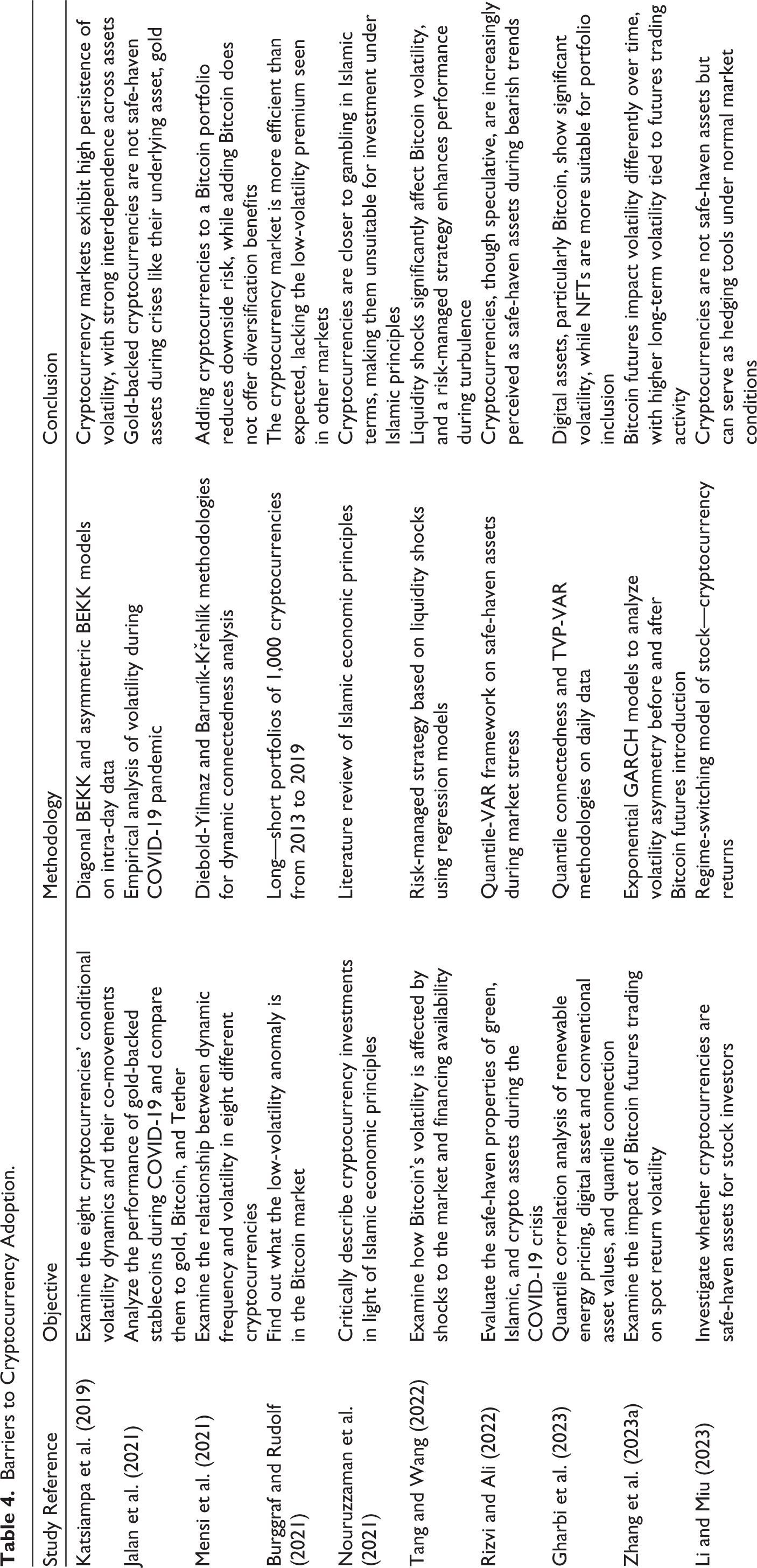

Barriers to Cryptocurrency Adoption

Cryptocurrency adoption has several barriers that include regulatory uncertainty, liquidity constraints, high volatility, and behavioral challenges among investors. These barriers continue to restrict the adoption beyond niche communities and innovative markets with the rising interest in cryptocurrencies. Moreover, these barriers also make cryptocurrency investment a complex and risky endeavor for both institutional and retail investors (Table 4). Likewise, Jalan et al. (2021) show that volatility is a crucial barrier to crypto adoption, thus noting that assets like gold-backed stable coins were introduced as a potential hedge against such instability of cryptocurrencies. However, these assets have shown volatility level comparable to cryptocurrencies like Bitcoin, hence making them inadequate as truly stable financial assets. These aspects indicate that even with technologies designed to mitigate volatility, it is difficult to address the broader challenges common to cryptocurrency adoption.

Barriers to Cryptocurrency Adoption.

Katsiampa et al. (2019) examined the conditional volatility dynamics of the most significant cryptocurrencies and their relationships. The results show that the volatility spillovers between cryptocurrencies are large, so shocks in one cryptocurrency can propel other cryptocurrencies, increasing the market risk. Mostly all analyses of the crypto ecosystem reveal a level of systemic risk in a crypto-related asset, not making it an ideal instrument for portfolio management. Mensi et al. (2021) further examined the interconnectedness of volatility among key cryptocurrencies such as Bitcoin, Ethereum, and Litecoin. The findings of their study signified that the volatility of cryptocurrency acts as a net transmitter of risk. During market downturns, the interconnected volatility increases the concern about the contagion effects. Thus, it limits the ability of the investors to realize effective diversification in the crypto market. In this context, the findings indicate that cryptocurrencies may increase rather than mitigate risks. Hence, the cautions investors found it discouraging to view them as reliable diversification tools.

During black-swan events, such as the COVID-19 pandemic and the Russia—Ukraine conflict, the performance of cryptocurrencies was examined by Kyriazis and Corbet (2024). The results presented in the study indicate that the Bitcoin possessed a certain level of hedging. However, in the case of other crypto assets, they were not serving the traditional safe-haven role. Besides, the role of cryptocurrencies becomes more complicated during times of market instability. On a similar note, Gharbi et al. (2023) studied the behavioral biases and macroeconomic factors that affected volatility spillovers in cryptocurrency markets during the COVID-19 pandemic. Their findings show cognitive biases such as overconfidence and herding behavior intensify market volatility during periods of financial instability. Thus, cryptocurrency adoption poses more challenges because of the interrelation between the conventional financial resources and the digital one. Further, this complexity is supported by a combination of behavioral and technological barriers, which collectively delay their broader acceptance.

In a similar vein, volatility spillovers between digital and non-digital assets were studied by Kayani et al. (2024). Their work has observed that cryptocurrencies, particularly Bitcoin, imply a major shock transmitter. The connection between the old financial system and cryptocurrencies adds systemic risks and bind cryptocurrencies as a useful diversification tool. Political and macroeconomic conditions, including financial and economic development, regulation, and broader institutional quality, have also been found to shape cryptocurrency adoption at the country level. The earlier work of Zhang et al. (2023a) revealed the fact that futures trading in Bitcoin generates the effect of decreasing short-term volatility and enhancing long-term volatility. The characteristics of volatility in cryptocurrency markets are not stable returns that are sought by long-term investors. Thus, the cryptocurrency markets must be multidimensional so that technological innovation, regulatory clarity, and enhanced financial literacy can address challenges and strengthen investors’ confidence. Simultaneously, the attractiveness and nature of cryptocurrency usage can be explained by its volatile nature, unpredictability of regulations, liquidity constraints, behavioral biases, market inefficiencies, and diversification benefits. All these elements of cryptocurrency make it a high-risk environment that will not attract potential users, especially those with lower risk tolerance or limited financial literacy. Hence, these obstacles and the need to promote the widespread use of cryptocurrency could probably require the reformation of regulations, the specific focus on education of the investors, and further technological advancements.

Momentum and Investor Attention in Cryptocurrency Markets

A phenomenon in cryptocurrencies where higher maximum daily returns correlate with higher future returns is termed the momentum effect (Li et al., 2021). Investor sentiment and underpricing may distort the level of cryptocurrency investment returns due to the momentum effect and its inherent risk, thus making such cryptocurrency investment very close to lottery stock behavior (Li et al., 2021). These lottery-style dynamics entice both speculators and tech-competence investors to trade according to market conditions (Lee et al., 2020). Investors are technologically competent and make their trading decisions based on the expected value of Bitcoin. Speculators tend to apply momentum strategies during periods of high volatility. However, they transit to contrarian positions when volatility subsides (Lee et al., 2020). Based on the literature, the future cryptocurrency trading markets will likely focus on technological advancements such as machine-learning models. These models are capable of accurately predicting cryptocurrency prices and trading volumes (Feng et al., 2018; Zhang et al., 2022).

In a similar manner, news and media contribute substantially to determining investor behavior in the cryptocurrency market. This evidence reflects how media attention affects Bitcoin demand. Besides, investors’ beliefs and responses to news events are the key drivers of market movement (Flori, 2019). However, slow-acting investors provide liquidity to the market, ultimately leading prices down to the sentiment. Negative news has a bigger impact on cryptocurrency investors than positive news, especially when the news is about the same regulatory developments. In this regard, da Gama Silva et al. (2019) found that crypto investors tend to react negatively to potential market regulations, considering them to be barriers to market freedom. However, illiquid cryptocurrencies, where information asymmetry risks are higher, significantly dampen this reaction (Chokor & Alfieri, 2021). This asymmetry is even more pronounced in ICOs than in initial public offerings (IPOs), since ICOs are, most often, not as highly regulated and much more prone to fraud. However, ICOs’ first-day returns tend to be higher (for relatively small token offerings) when the market sentiment is positive, and there are high expectations for expected trading volume (Felix & von Eije, 2019). Another challenge within the cryptocurrency market is media manipulation. On the same note, the occurrence of various pump-and-dump schemes and scams exposes investors to significant risks of deception on social media platforms. Moreover, these platforms were exploited by scammers to artificially inflate the cryptocurrency price, thus enticing inexperienced investors to purchase at inflated prices, only for them to incur losses when prices subsequently collapse d(Nghiem et al., 2021). Besides, due to the influence of social media trends, investors may engage in herd behavior, leading to irrational investment decisions (Yasir et al., 2023).

Efficiency of Cryptocurrency

This study demonstrates that a considerable body of research has examined the structure and functioning of cryptocurrency markets. Nevertheless, the evidence indicates that these markets continue to exhibit significant inefficiency, primarily influenced by speculative behavior and investor sentiment (Kankanam Pathiranage et al., 2021). Besides, Fousekis and Tzaferi (2021) also demonstrate that trading volume and returns exhibit a directional relationship, enabling investors to profit from past trading activities, which is an indication of informational inefficiency. Viewed as a whole, the evidence demonstrates that irrational and speculative trading patterns are common causes of inefficiency in the cryptocurrency market.

Furthermore, although the Bitcoin investment trust shows an average premium of 44%, it continues to display pricing inefficiency and a link between price and net asset value (Almudhaf, 2018; Kwok, 2020). Thus, market inefficiency is worsened when the global quantitative monetary policy is loosened (Huang, 2022). Therefore, the Bitcoin market is clearly immature and very speculative with an information utilization rate of only 10% (Kang et al., 2022). These studies indicate that crypto markets remain persistently inefficient, largely due to global monetary conditions and lack of reliable information. Moreover, potential arbitrage possibilities might arise when the cryptocurrency market is inefficient (Andrade et al., 2021; Tadi & Kortchemski, 2021). The Kimchi premium, which is the difference in the price of cryptocurrencies on different exchanges, is a proof of this (Eom, 2021). Bitcoin, in contrast to Ripple and Ethereum, has superior risk management capabilities and solid long-term investment prospects. Ripple and Ethereum are better investments for speculators (Celeste et al., 2020). In addition, it seems that triangle arbitrage between forex and cryptocurrency occurs during crisis times, leading to the outperformance of cryptocurrency investments.

Before 2017, cryptocurrencies exhibited relatively high efficiency, although transaction price did not represent all known information in the cryptocurrency market (Kang et al., 2022). Consequently, only a limited number of cryptocurrencies aligned with efficiency market hypothesis. However, the onset of the COVID-19 pandemic was associated with an improvement in overall cryptocurrency market efficiency. Although Bitcoin initially demonstrated stronger efficiency prior to the pandemic, Ethereum subsequently surpassed it in this respect (Mnif et al., 2020). Evidence from these developments signify that cryptocurrency market efficiency is inherently dynamic. In addition, it evolves in response to external shocks and shifting investor behavior. Hence, crypto markets are becoming more efficient as the number of links between them has increased, which is a good news for volatility and returns. Crypto markets seem to function autonomously according to the available data. One example is the fact that the Bitcoin market seems to be unaffected by the state of the economy as a whole (Glas, 2019).

There is no evidence that the cryptocurrency market is related to more conventional markets. Also, the fact that cryptocurrencies are distinct markets implies that their responses to big global events such as BREXIT and US elections could not be typical of other asset classes (Schaub & Phares, 2020). Further differentiating cryptocurrencies from more conventional asset classes is their synchronic development (Pele et al., 2023). Along these lines, research suggests that Bitcoin and other cryptocurrencies may be better understood as technological goods rather than traditional investments (Corbet, Lucey, et al., 2018; Corbet, Lucey, & Yarovaya, 2018) or alternatively as speculation bubbles (White et al., 2020) rather than as forms of money. In this view, the Bitcoin is distinct from fiat currencies while also differing fundamentally from gold (Baur et al., 2018). Moreover, this cryptocurrency is distinguished from other asset classes. Since this cryptocurrency sustains volatile price dynamic, high regime shifts, unique risk—return characteristics, and low correlation with other traditional assets classes (Tavares et al., 2021), therefore, it possesses a dual identity, causing its role in financial markets to be more complex.

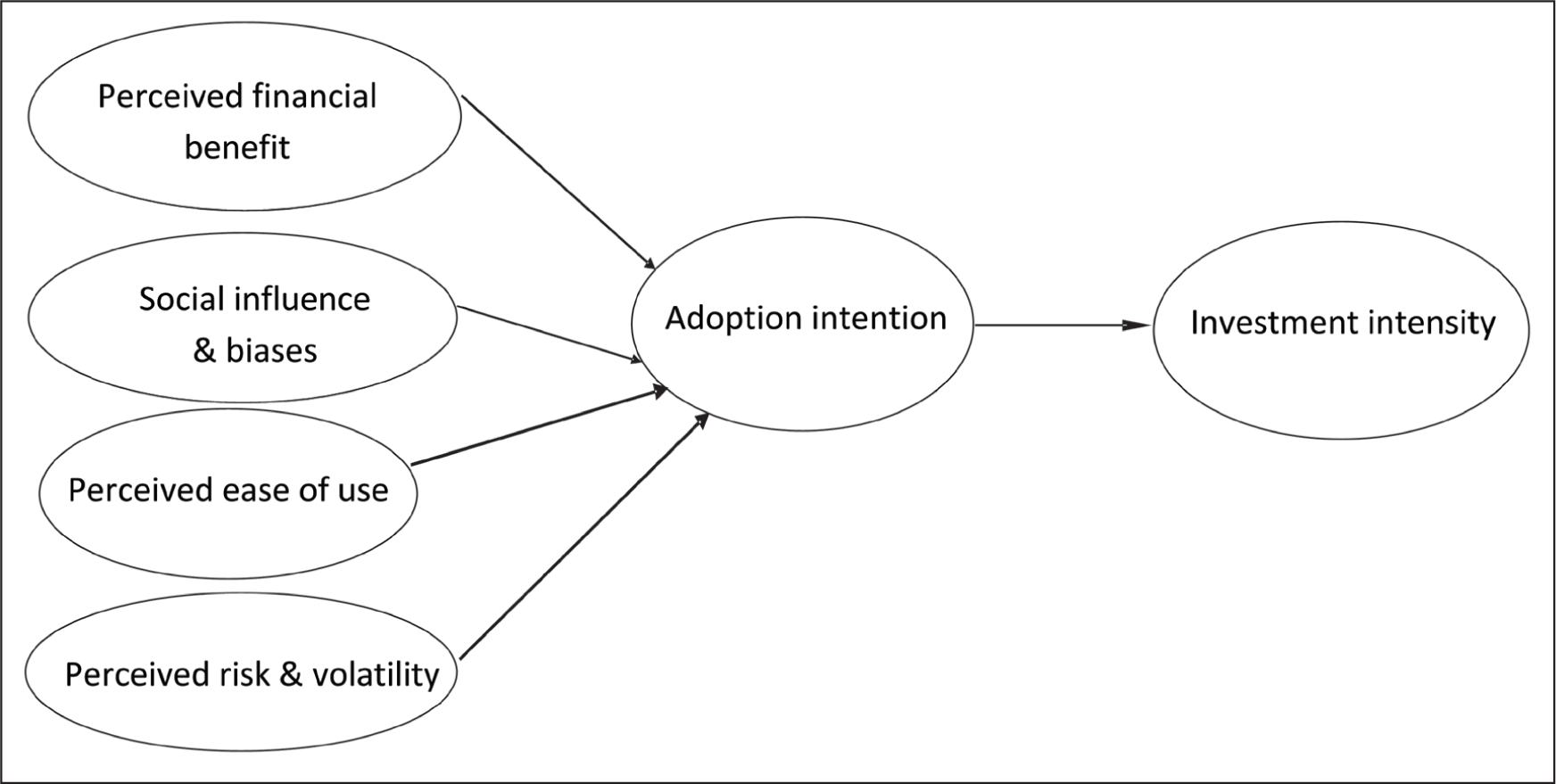

Theoretical Framework and Proposed Model

The theoretical framework for this study is grounded in the technology acceptance model (TAM) by Davis (1989) and extended by the UTAUT model by Venkatesh et al. (2003) with core concepts from the behavioral finance of Kahneman and Tversky (1979). TAM highlights rational technology acceptance based on perceived usefulness and ease of use, providing a parsimonious model of technology acceptance with good predictive power about people’s intended behavior; however, it does not account for social influences and psychological bias (Davis, 1989). UTAUT extends the framework by adding four constructs, that is, performance expectancy, effort expectancy, social influence, and facilitating conditions, thus generating a more complete model of adoption, without losing the rationality of decision-making (Venkatesh et al., 2003). Behavioral finance addresses these shortcomings by taking into consideration the irrational determinants that are true causes of the real-world deviations in volatile markets (i.e., emotions, herding behavior, and cognitive biases), even though it focuses enough on technology usability (Kahneman & Tversky, 1979). The current framework incorporates these strengths, in which TAM and UTAUT form the logical base of technology, while behavioral finance adds a degree of psychological realism, which results in a holistic model that works through the channel of adoption intention and invests in the intensity of cryptocurrency applications. The proposed model provides a robust lens for understanding investors’ adoption and the use of financial technologies in cryptocurrency markets.

The reviewed literature informed each of the four independent constructs in our proposed framework (Figure 8). Investment intensity was one of the outcome variables that became apparent across the reviewed literature and reflects the extent of investment in cryptocurrency markets. Research in the investment intensity stream has continually defined intensity in terms of the frequency of trading, portfolio share, and investment (Bleher & Dimpfl, 2019; Bowden & Gemayel, 2022; Fousekis & Tzaferi, 2021; Gaies et al., 2021; Luo et al., 2021; Süssmuth, 2022). In addition to financial returns, the existing studies have shown that behavioral, cognitive, and contextual factors are also determinants of the intensity of investment. Therefore, investment intensity, the dependent variable, absorbs the impact of psychological, technological, and social determinants observed in the systematic literature review.

Conceptual Framework of Cryptocurrency Adoption and Investment Intensity.

Empirical studies consistently indicate that perceived high-return potential, diversification benefits of portfolios, inflation hedging, and speculative profits are the main reasons that drive the cryptocurrency investment (Bianchi & Babiak, 2022; Dias et al., 2022; Disli et al., 2021; Nguyen et al., 2020; Wu, 2024). Such evidence supports the use of perceived financial benefits as a focal independent variable that determines the intention of adopting, which subsequently determines the degree of follow-up investment. Moreover, the perceived financial benefits align with the perceived usefulness of TAM and the performance expectancy of UTAUT, as evidenced by articles such as the one by Jariyapan et al. (2022), which shows that during volatile times, investors are willing to view cryptocurrency platforms as useful (Davis, 1989; Venkatesh et al., 2003).

Extreme price volatility, regulatory risks and uncertainty, and market manipulation are the recurrent features of cryptocurrency markets that are recorded in the literature (Baur et al., 2024; Brini & Lenz, 2024; Chohan, 2017; Chokor & Alfieri, 2021; da Gama Silva et al., 2019; Domingo et al., 2020). The nature of these risk perceptions has an adverse effect on investor confidence and adoption intention, in addition to modifying the level of capital commitment. In line with this, perceived risk and volatility are included as important independent variables in the systematic literature review that limit the intention formation process as well as the level of investment. Moreover, perceived risk and volatility are a combination of prospect theory and volatility aversion that humans are prone to through behavioral finance and fintech findings on the connection between perceived risk (e.g., hacks or price swings) and investing decisions (Chen et al., 2023; Kahneman & Tversky, 1979).

Empirical studies have indicated that cryptocurrency investments are heavily influenced by social interactions, herd effects, and cognitive biases (Gharbi et al., 2023; Gupta et al., 2021; Kahya & Ekinci, 2022; Yasir et al., 2023). Word of mouth on social media, celebrity recommendations, user-to-user influences, and the psychological phenomenon of FOMO are all contributing factors to the increased investor salience and faster market entry (El Haddaoui et al., 2023; El Hedhli et al., 2021; Gerrans et al., 2023; Wang et al., 2023). Therefore, these findings support conceptualizing social influence and bias as a discrete independent variable that shapes adoption intentions and moderates the desire for further investment. Specifically, social influence and bias represent an integration of UTAUT’s social influence, behavioral finance theories of herding, and investor sentiment (Baker & Wurgler, 2007; Banerjee, 1992; Chen et al., 2023; Venkatesh et al., 2003). In this context, peer actions, media hype, and cognitive biases drive cryptocurrency investment decisions.

The absence of user-friendly platforms and financial literacy are the factors that discourage participation. On the flip side, technological-acceptance-based studies show that the simplified interfaces, the accessibility to trading applications, and the availability of digital wallets contribute to investment (Chen et al., 2023; Feng et al., 2018; Lee et al., 2020; Sham et al., 2023). Therefore, the perceived ease of use has been conceptualized as one of the most important determinants of adoption intention, especially among retailers and novice investors, as supported by several reviewed studies. Besides, the perceived ease of use aligns with the essence of TAM and the effort expectancy under UTAUT (Venkatesh et al., 2003), which has been substantiated with scientific input through the notion that intuitive mobile banking interfaces eliminate the barriers in adoption (Alalwan et al., 2017; Davis, 1989; Venkatesh et al., 2003).

Implications

The analysis of the reviewed literature provides action-oriented information for the uptake of cryptocurrency by different players. Policymakers should focus on the development of sensible regulatory environments highlighting tax regimes, enforcing anti-money-laundering (AML) procedures and systems for investors’ protection, such as mandatory disclosure standards and risk warnings. Such measures are directly targeted at the literature’s emphasis on regulatory uncertainty as a major hurdle to adoption while promoting market stability and investor confidence. In addition, cooperation between government bodies and financial institutions can further standardize the licensing of cryptocurrency exchanges, thus reducing systemic risks and encouraging sustainable innovation. Investors are advised to incorporate behavioral finance insights into their decision-making processes by incorporating sentiment analyses of social media trends and peer-herding patterns in addition to traditional metrics such as perceived financial benefits and assessments of volatility.

The proposed framework emphasizes the importance of adoption intention, explicitly as a mediating construct, meaning that investors should calibrate portfolio allocations according to the perceptions of ease and difficulty of use, where they are more aware of cognitive biases, to best optimize the investment intensity without falling into the hype of investing in a market. Diversification strategies to include regulated stablecoins can balance between high-return potential and the perceived mitigation of risk. Fintech developers should focus on intuitive user interfaces that focus on perceived ease of use via features like one-click verification of AML compliance, showing real-time volatility dashboards, and even influencing the sentiment of the community through social nudges. Integrating elements of behavioral finance, including debiasing tools that may be designed to mitigate against overconfidence and herding, may be useful to improve platform stickiness and boost adoption intention, driving greater investment intensity. Rigorous usability testing in volatile cryptocurrency situations will ensure platforms reduce friction while adhering to the changing regulatory requirements.

Conclusion

The current research is a synthesis of the academic literature on the uptake of cryptocurrencies and investor behavior in the fintech industry. This systematic literature reviewed and classified the extant literature across five key thematic domains such as investment motivation, investor behavior and investment intensity in cryptocurrency markets, barriers to cryptocurrency adoption, momentum and investor attention in cryptocurrency markets, and cryptocurrency market efficiency. The findings have shown that behavioral sentiments determine cryptocurrency markets, thus causing volatility and speculative bubbles. In line with this, perceived financial benefit, social influences and biases, perceived ease of use, and perceived risk and volatility are relevant in explaining investment decisions. Bibliometric mapping reveals escalating publication trends and concentrated authorship networks in fintech hubs. Although the bibliometric analysis offers useful insights into cryptocurrency adoption and the intensity of investments, it is also vulnerable to critical limitations. Remarkably, its use of Scopus and Dimensions databases might omit other databases, grey literature, and non-English publications with relevant studies, thus restricting the ability to represent the world of scholarship in all its diversity, particularly underrepresented ones. In order to reduce the shortcomings of these, future studies must increase data retrieval in various databases and types of documents to better reflect new trends. Also, multi-source triangulation, temporal analyses, and the qualitative integration of results would help overcome the issues of self-citation bias, institutional and geographic skew, and scale sensitivity of productivity measures to make bibliometric results on cryptocurrency research more robust and generalizable. As a result, future research needs to focus on the formation of investment decisions by institutional investors in the cryptocurrency market and the cognitive biases that influence their allocation policies in a situation involving the analysis of the common macroeconomic variables. In addition, the contribution of cognitive bias in investor behavior (e.g., overconfidence, optimism, underreaction, overreaction, and disposition effect) is an area that should be addressed in future studies. This tendency makes investors recognize gains too early and continue holding assets that lead to losses (Gemayel & Preda, 2021; Shrotryia & Kalra, 2022). This article highlights the need to conduct future studies to investigate the effect of sociodemographic factors on investor behavior. It is also important to examine whether macroeconomic sentiment has a stronger influence on institutional investors than on retail investors (Burggraf et al., 2021; Gupta et al., 2021). Hence this review highlights forward-looking mandate for future research whose valuable insights can be useful for stakeholders in the multifaceted dynamics of cryptocurrency markets.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.