Abstract

Purpose:

This study aims to explore and structure the key determinants influencing the adoption of central bank digital currency (CBDC) in India, specifically focusing on the retail digital rupee (e-rupee). It employs the Unified Theory of Acceptance and Use of Technology 3 (UTAUT3) framework in conjunction with interpretive structural modeling (ISM) to identify, categorize, and model the adoption enablers.

Design/Methodology/Approach:

Seven constructs from UTAUT3—performance expectancy, effort expectancy, social influence, facilitating conditions, price value, hedonic motivation, and behavioral intention—were selected based on extensive literature review and expert validation. ISM was used to map interrelationships between these constructs. The study involved the creation of a structural self-interaction matrix, final reachability matrix, hierarchical ISM model, cross-impact matrix multiplication applied to classification analysis, and fuzzy logic to assess driving and dependence power.

Findings:

The results reveal that facilitating conditions and performance expectancy are the most influential constructs, forming the foundational layer in the adoption hierarchy. In contrast, hedonic motivation and behavioral intention act as dependent variables, influenced by preceding constructs. The findings underscore the importance of infrastructure readiness, user convenience, and institutional support in shaping public intent to adopt CBDC.

Practical Implications:

The study offers strategic insights for policymakers, financial institutions, and developers to enhance CBDC adoption by addressing structural enablers and barriers. It also provides a scalable framework applicable to other emerging economies exploring digital currency implementation.

Originality/Value:

This research uniquely integrates UTAUT3 with ISM to present a structured, empirically grounded model of CBDC adoption behavior, bridging theoretical and practical gaps in digital finance adoption literature.

Introduction

The rapid digitization of financial systems has led central banks to explore central bank digital currencies (CBDCs). These currencies aim to modernize currency issuance, enhance payment efficiency, and improve financial inclusion. India, with its expanding digital infrastructure and high smartphone penetration, stands at the forefront of this transformation with the introduction of its CBDC—the e-rupee. Being among the first major emerging nations to conduct a large-scale CBDC trial, India’s initiatives mark a turning point in global financial innovation. The e-rupee’s success depends on user adoption. This adoption is influenced by complex socio-technical factors that go beyond simple access or utility.

Understanding the adoption of the e-rupee requires an in-depth study of individual attitudes, perceived value, and environmental factors that impact behavioral intention (BI). Previous studies have repeatedly demonstrated that factors including social influence (SI), perceived ease of use, performance expectancy (PE), and trust are important to user adoption of digital financial services. According to a study on the adoption of digital currency in India, BI to adopt CBDC is strongly predicted by PE, SI, and government support, especially when combined with financial literacy and perceived technological fit (Desai, 2024). Similarly, despite occasional mistrust over privacy and control, it has been discovered that trust and perceived security have a major impact on younger generations’ openness to CBDC adoption (Kaur et al., 2024).

These findings align with the Unified Theory of Acceptance and Use of Technology (UTAUT). UTAUT is being applied in the context of digital banking, e-payments, and now CBDC adoption studies. The UTAUT framework identifies key constructs such as performance expectancy (PE), effort expectancy (EE), social influence (SI), facilitating conditions (FCs), and behavioral intention (BI) as critical drivers of user acceptance. UTAUT2 and UTAUT3 extensions have demonstrated strong predictive power across various fintech services in India. These services include Unified Payments Interface (UPI) platforms and mobile wallets (Chauhan et al., 2021). The need to contextualize these ideas is enhanced by India’s distinct social and technical environment. For example, the impact of SI on technology adoption is elevated by collectivist attitudes and intergenerational financial decision-making. According to research on UPI adoption, BI and use behavior were substantially impacted by trust, attitude, and SI. This suggests that CBDC adoption strategies might be successful (Razi-ur-Rahim et al., 2024).

This study aims to identify and analyze the key factors influencing the adoption of the e-rupee in India through the lens of the UTAUT3 framework, using interpretive structural modeling (ISM). The ISM methodology maps the relationships among constructs. It reveals hierarchical linkages between foundational drivers, such as infrastructure and perceived ease, and outcome-oriented variables, like hedonic motivation (HM) and behavioral intent.

The research contributes to the academic literature by applying a structured modeling approach (ISM) to UTAUT3 in the specific and underexplored context of CBDC adoption in India. It also offers practical insights for policymakers, financial institutions, and fintech developers aiming to enhance user engagement and trust in digital currency platforms. Recent research studies also reinforce the need for a strong regulatory and institutional framework to complement digital infrastructure in emerging markets. Regulatory quality, not just technical readiness, is a decisive factor in the success of CBDC rollouts in developing economies (Corbet et al., 2024). This study will develop a hierarchical ISM-based model to identify, organize, and analyze the key UTAUT3 constructs influencing the adoption of the e-rupee in India.

Literature Review

Central Bank Digital Currencies

Central bank digital currencies, or CBDCs, are a transformative development in modern monetary systems. The central bank of a nation issues and regulates a digital version of fiat money called a CBDC, which is intended to be a safe, effective, and widely available means of trade (Raju, 2021). CBDCs provide the benefits of programmable, digital financial infrastructure while preserving monetary sovereignty, in contrast to decentralized cryptocurrencies (Surgentova, 2023).

Due to the demand for inclusive financial services, the rise in digital payment use, and the decline in cash use, CBDCs have become increasingly relevant. CBDCs serve as instruments to improve cross-border settlements, modernize payment systems, lower transaction costs, and strengthen central banks’ authority over monetary policy (Batra et al., 2024). They also counterbalance the emergence of private digital currencies and stablecoins, promoting confidence and stability in national payment ecosystems (Das et al., 2023).

With nations such as China and India spearheading extensive implementation trials, more than 100 central banks are studying or testing CBDCs (Chikobava, 2023). CBDCs have the potential to improve the durability of digital public infrastructure and encourage financial inclusion in poor nations (Tekdoğan & Güney, 2024).

Digital Currency Adoption

The Reserve Bank of India (RBI) is piloting the digital rupee in India, and a growing body of empirical research is trying to identify the variables influencing the adoption of CBDCs. These studies demonstrate the complex relationships between infrastructure, psychology, and technology that influence user intents and actions.

The adoption of CBDC is greatly impacted by trust, openness, and data security. According to a recent survey-based study, consumers’ willingness to accept the digital rupee was highly impacted by their perceptions of transactional transparency and security and their trust in the issuing authority. These results support the idea that the acceptability of state-backed digital currencies is predicated on institutional trust.

However, there are still a number of obstacles preventing wider use. According to Krishnamoorthy and Aggarwal (2024), there is still a lack of general understanding of CBDC, and many consumers are unable to tell it apart from other digital payment systems like the UPI. The study found that the retail CBDC pilot’s poor acceptance is a result of this lack of distinction as well as a lack of outreach and education (Krishnamoorthy & Aggarwal, 2024).

Research with a demographic focus shows that, although EE has little impact, Generation Z in Northern India exhibits a strong behavioral intent to adopt CBDC due to PE and perceived security, indicating a tech-savvy and innovation-receptive segment (Kaur et al., 2024). SI and performance anticipation significantly impact adoption intentions, but the effect is moderated by the perception of less additional value in CBDC among regular UPI users. This suggests that past experience with digital systems like UPI may dampen the excitement surrounding CBDC adoption (Gupta et al., 2023). Trust partially mediates the association between perceived risks and adoption readiness, whereas perceived risks diminish trust. Perceived usefulness did not significantly predict adoption behavior, highlighting the importance of emotional and trust-based elements (Gupta et al., 2023).

Regulatory readiness and infrastructure are also crucial for the adoption. The digital rupee pilot has demonstrated backend readiness by including large financial institutions and focusing on use cases such as retail payments and government securities. However, research warns that without comparable efforts in ecosystem integration, user education, and public engagement, technology infrastructure alone cannot ensure adoption (Kumar & Gupta, 2024).

Empirical research shows that India’s digital and financial infrastructure is suitable for CBDC implementation. However, widespread adoption depends on building trust, raising public awareness, and clearly explaining the benefits of CBDC over existing digital payment options.

Applications of UTAUT3 in Digital Technology Adoption

UTAUT is one of the most influential models in technology acceptance research. Developed by Venkatesh et al. (2003) and later extended into UTAUT2 and UTAUT3, the framework integrates multiple behavioral theories to explain user adoption of new technologies. UTAUT3 adds constructs such as price value (PV) and hedonic motivation (HM) to reflect evolving consumer behaviors in digital ecosystems.

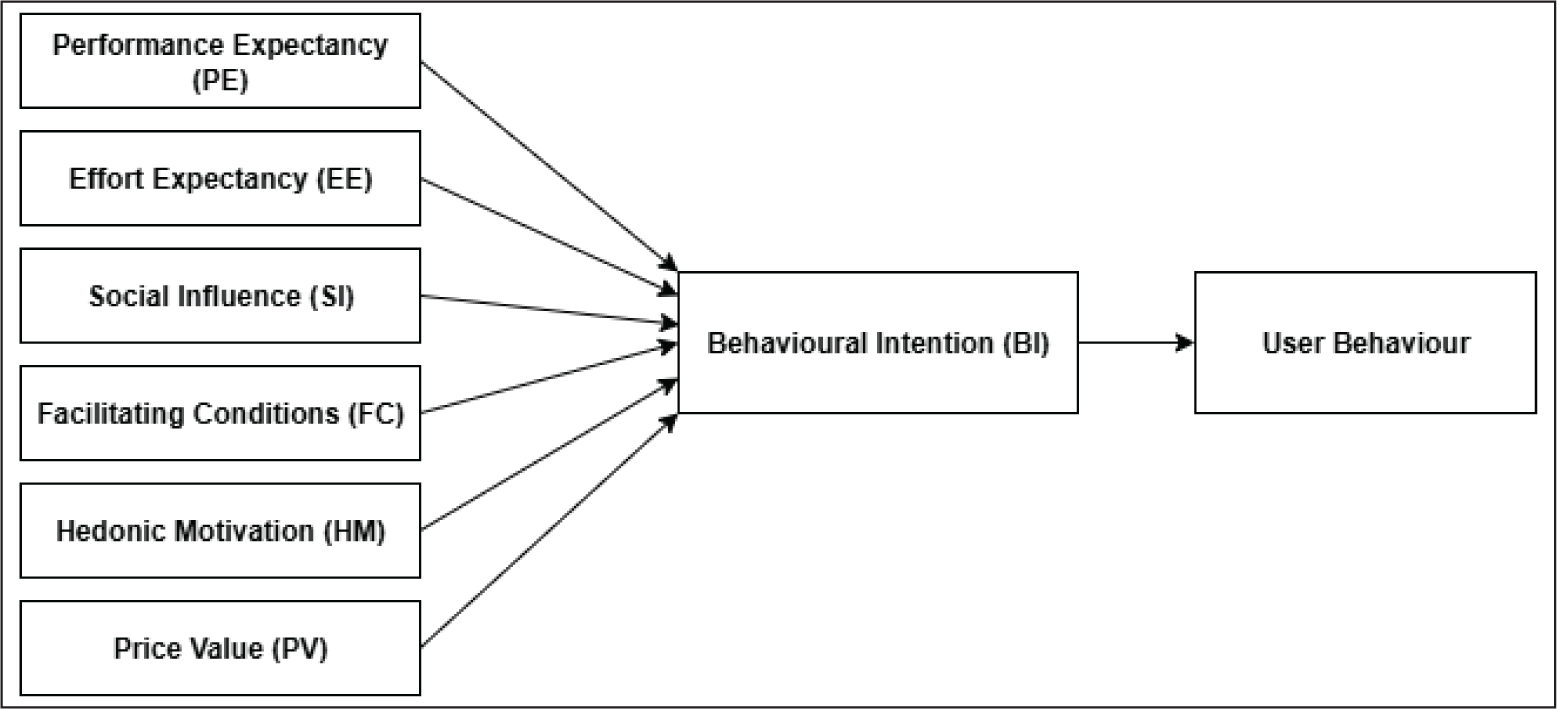

UTAUT3 includes seven core constructs: performance expectancy (PE), effort expectancy (EE), social influence (SI), facilitating conditions (FCs), price value (PV), hedonic motivation (HM), and behavioral intention (BI) (Figure 1). These constructs have been widely validated in studies involving digital banking, mobile wallets, cryptocurrency, and FinTech adoption (Amnas et al., 2023).

UTAUT3 Model.

UTAUT3 is particularly effective in explaining technology adoption because it captures both utilitarian and affective motivations behind user behavior. It has demonstrated high predictive power in digital finance studies, with R2 values exceeding 70% in models of FinTech and e-wallet adoption (Raihan, 2019).

UTAUT3 has been widely applied across digital finance domains. It shows a strong predictive power for user adoption. In mobile wallet studies in Malaysia and Indonesia, constructs such as PE, EE, and SI were significant determinants of BI (Leong, 2020). In the Indian banking sector, PE and FCs significantly influenced the intention to adopt blockchain technologies (Jena, 2022). Cross-cultural research has also shown that UTAUT3 constructs effectively explain adoption behavior across diverse generational cohorts and national contexts, especially in FinTech payment systems (Urus et al., 2022).

The following are the constructs of the model:

This study focuses on the following research questions:

RQ1. Which UTAUT3 constructs significantly influence the adoption of the e-rupee in India, and how can they be systematically identified using the ISM approach? RQ2. How are the identified adoption factors interrelated, and which variables act as key drivers or dependent elements in the hierarchical structure of e-rupee adoption?

Research Objectives

To identify and analyze the key UTAUT3-based factors influencing the adoption of India’s e-rupee using ISM and fuzzy Cross-Impact Matrix Multiplication Applied to Classification (MICMAC).

To develop a hierarchical model that highlights the interrelationship and driving–dependence power of the factors affecting CBDC adoption in the Indian context.

Research Methodology

Interpretive Structural Modelling

The study uses the UTAUT3 framework, specifically applied to the context of CBDCs like the e-rupee. The digital rupee (e-rupee), introduced by the RBI, aims to promote financial inclusion, lower operating expenses related to physical currency, and improve payment efficiency. The adoption of CBDC is expected to be facilitated by India’s advanced digital infrastructure, UPI ecosystem, and growing public confidence in mobile-based transactions (Gupta et al., 2023; Krishnamoorthy & Aggarwal, 2024; Mahesh et al., 2024). Empirical research has shown that customer support, trust, and transparency are important factors in determining how Indian consumers will act while using the e-rupee (Sandhu et al., 2023). These contextual factors offer a strong foundation for using the UTAUT3 model to understand adoption dynamics specific to the digital currency environment in India.

ISM is used to explore the contextual relationships between the UTAUT3 framework constructs that are believed to impact the adoption of the E-rupee. These constructs include PE, EE, PV, HM, SI, and FC. ISM uses literature support, logical reasoning, and expert judgment to help identify and organize key aspects hierarchically.

The structural self-interaction matrix (SSIM) is constructed based on a review of technology adoption literature. The review used the UTAUT3 framework, specifically applied to the context of CBDCs like the e-rupee.

In the ecosystem of digital financial technology adoption, the relationships between PE, EE, SI, FC, HM, and PV are not isolated. These relationships are contextually shaped and interdependent.

PE represents the users’ perceptions that utilizing the e-rupee would improve their financial results and transactional efficiency. It has an impact on PV, HM, and BI. Nguyen et al. (2020) showed that customers’ inclination to use digital banking services in Vietnam was highly influenced by their expectations of better performance. In cryptocurrency investment performance expectancy moderated the impact of other factors on BI (Alzyoud et al., 2024). A study by Putranta et al. (2020), also confirmed that PE significantly influenced mobile payment adoption behavior.

It was suggested that EE affected PV, HM, PE, and BI. Users’ perceived value and expected performance rise when they believe a system is easy to use, which strengthens their intent to use the technology. EE has a considerable impact on motivational outcomes and cognitive assessments of usefulness in digital banking environments (Meiranto et al., 2024).

SI was identified as a significant component influencing several variables, including PE, EE, BI, HM, and PV. Adoption choices are frequently influenced by institutional trust, peer pressure, and professional advice in culturally collectivist nations like India. Salsabila et al. (2024) found that SI has a substantial impact on digital bank adoption by influencing both intrinsic motivation and perceived system value. Study emphasized how it influences young users’ behavioral decisions in financial environments (Widyastuti & Layaman, 2023). Amany and Indrayani (2024) also found SI to be a driver of BI in mobile banking adoption.

HM refers to the satisfaction gained from using technology. It is regarded as an outcome of prior perceptions and a determinant of BI. One factor influencing customers’ willingness to accept an innovative financial instrument like the e-rupee is its emotional appeal. According to a study, among students using digital wallets, HM was a powerful predictor of BI (Kardoyo et al., 2022).

PV indicates the consumers’ trade-off between the perceived benefit and the monetary or cognitive cost of utilizing the e-rupee. It was associated with BI. According to research by Alzyoud et al. (2024), consumers’ desire to use digital financial technologies improves considerably when they believe that they are more beneficial or cost-effective than traditional techniques.

FCs were identified as a key construct that influences all others, including PE, EE, SI, HM, PV, and BI. A strong digital infrastructure, regulatory readiness, and user support mechanisms promote more trust and usage of innovations such as the e-rupee. Research has shown that the adoption of digital and mobile banking systems is facilitated by favorable circumstances (Amany & Indrayani, 2024; Nguyen et al., 2020; Widayani, 2022).

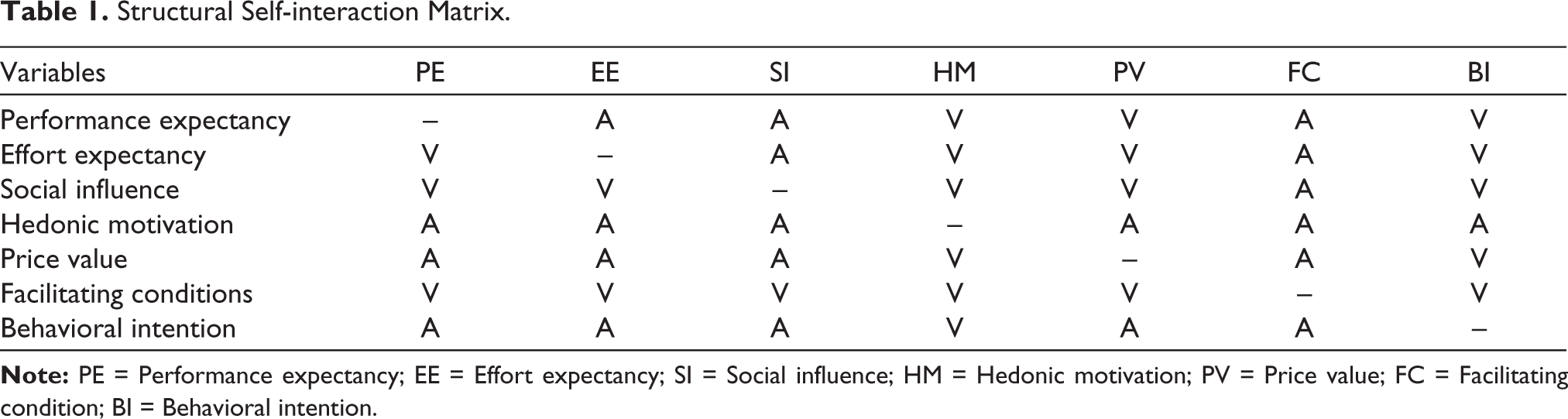

Structural Self-Interaction Matrix

SSIM is the first step in ISM. It examines and systematically maps the contextual relationships among key factors influencing the adoption of CBDCs such as the e-rupee. PE, EE, SI, HM, PV, FC, and BI are the constructs from the UTAUT3 that were used to create SSIM for this study.

These constructs are compared pairwise to create the SSIM, which is based on logical reasoning, and a study of the literature. The directional connection between each pair is shown by a symbolic representation:

V: Variable i influences variable j. A: Variable j influences variable i. X: Variables i and j influence each other. O: No relation exists between variables.

Warfield (1974) first introduced this method, which works especially well for structuring complicated social and technical systems into hierarchical models. It makes it easy to see the elements that drive and are dependent on them.

In the context of digital financial services like CBDCs, prior research supports the interdependent nature of these constructs. FCs, for example, have been repeatedly identified as the most important adoption driver, impacting several other constructs, including PE, EE, SI, and BI (Albugami, 2022). PE and EE have been recognized as the major contributing factors to digital banking activity under a range of cultural and economic circumstances (Killian et al., 2017; Moorthy et al., 2019).

The SSIM matrix in this study was developed with the knowledge that collectivist societal norms and a rapidly growing digital infrastructure allow constructs such as SI and FCs to play enhanced roles in the Indian digital payment landscape (Mahesh et al., 2024; Sandhu et al., 2023). HM and PV are influenced by consumers’ emotional and cost-benefit evaluations. SI influences not just BI but also perceived value and ease of use.

This methodology has been successfully used in similar studies, such as those examining the structural adoption factors of digital banking in emerging economies, and in e-government, mobile payments, and financial technology environments (Albugami, 2022; Alzubaidi et al., 2020).

The UTAUT3 constructs developed an SSIM table (Table 1). This table reflects the directional influences on CBDC adoption. It aligns with established theoretical linkages and contextualizes these linkages within the unique digital, economic, and cultural environment of the Indian financial ecosystem.

Structural Self-interaction Matrix.

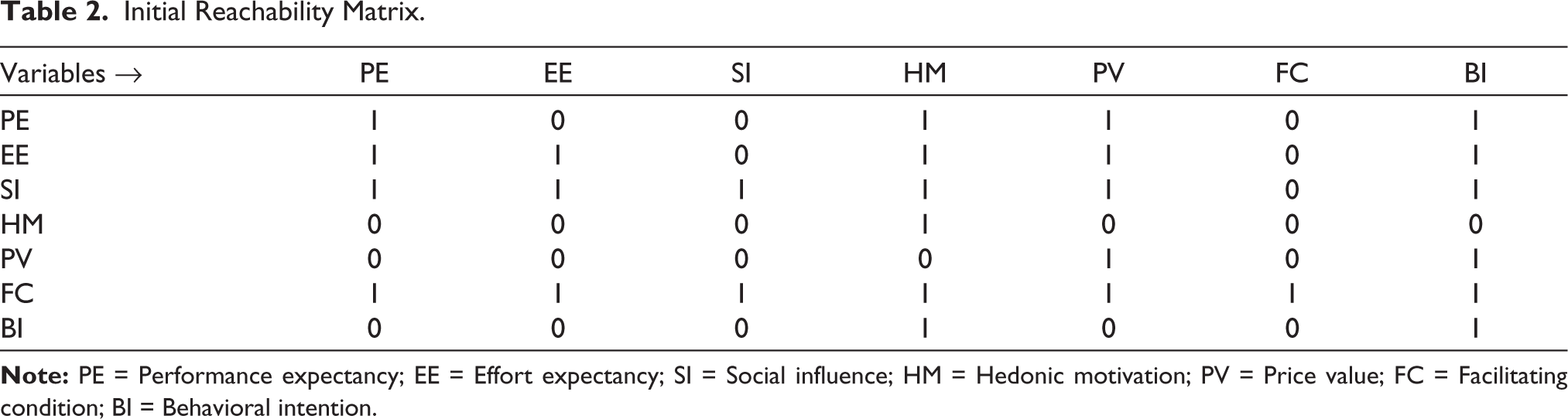

Initial Reachability Matrix

SSIM is converted into binary values to show the direct effect between variables, which creates the initial reachability matrix (IRM). Every symbol in the SSIM—V, A, X, and O—is converted into 1s and 0s using the common ISM conversion rules. Within the CBDC adoption framework, this transformation enables us to systematically identify which constructs—such as PE, EE, SI, etc.—directly affect other constructs (Table 2). The final reachability matrix (FRM) (Table 3) and hierarchy levels, as well as the identification of transitive linkages, are developed based on the IRM (Albugami, 2022; Warfield, 1974).

Initial Reachability Matrix.

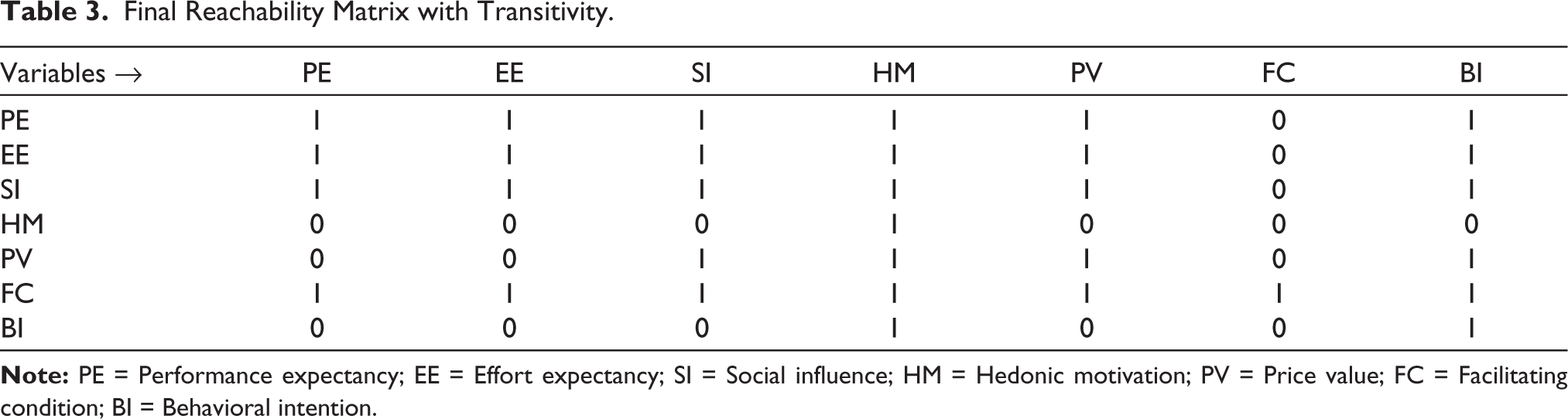

Final Reachability Matrix with Transitivity

The FRM is developed by applying the transitivity principle to the IRM. According to this principle, if variable A influences B and B influences C, then A is assumed to influence C as well (Albugami, 2022). This step ensures that all direct and indirect relationships among the UTAUT3 variables are captured. The FRM in Table 3 provides a complete foundation for structuring the hierarchical model of factors influencing e-rupee adoption in India

Final Reachability Matrix with Transitivity.

Level Partitioning Process

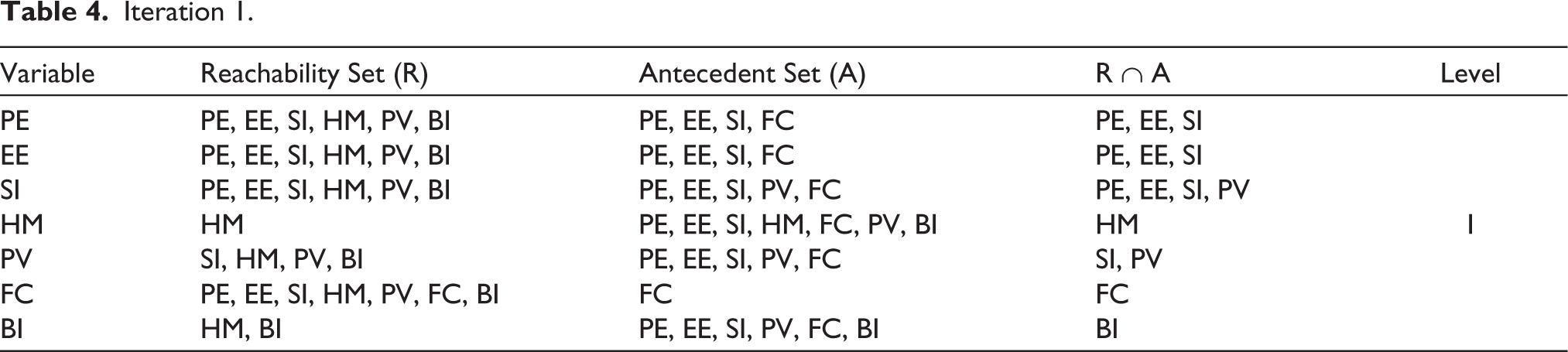

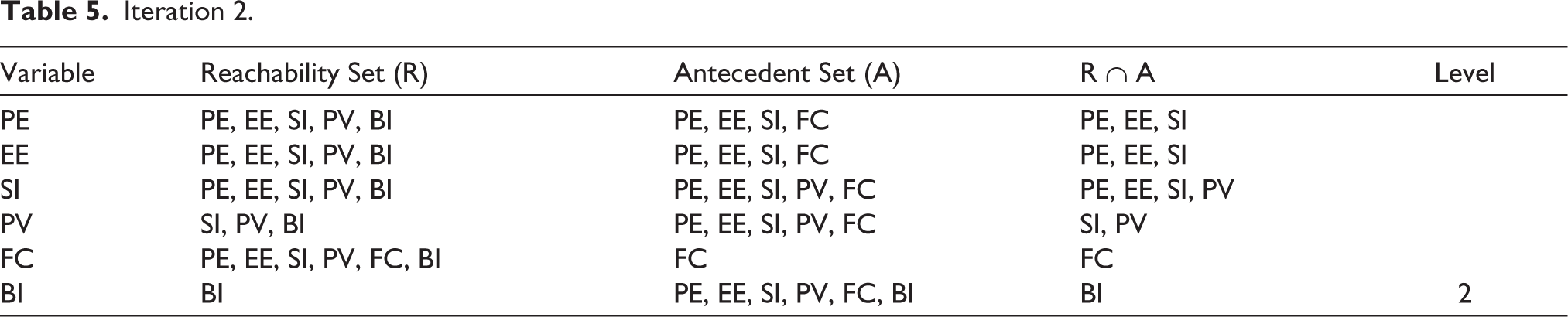

The FRM is tested using the level partitioning procedure to determine the hierarchical structure of UTAUT3 components that impact the adoption of e-rupee. Each construct is recognized together with its antecedent set (variables that influence it) and reachability set (variables it may affect). The reachability set is then used to compare the intersection of these sets. The construct is given the current level and eliminated in the following iteration if both are the same. Repeating this process reveals various layers of impact, allowing us to see which elements are fundamental drivers (such as FCs) and which are more outcome-oriented (such as BI) in the context of CBDC adoption in India.

If

HM is placed at the bottom level as it only influences itself and no other variables, indicating that it is the most outcome-oriented construct (Table 4).

Iteration 1.

BI is assigned the next level since it can reach only itself and HM (already removed), showing that it is primarily influenced by other constructs (Table 5).

Iteration 2.

PV and SI are placed at the third level from the bottom (Table 6).

Iteration 3.

PE and EE meet the criteria where their reachability equals their intersection sets, so they are positioned as strong driving constructs (Table 7).

Iteration 4.

FC remains the last variable, influencing all others but not influenced by any—making it the most foundational driver of e-rupee adoption (Table 8).

Iteration 5.

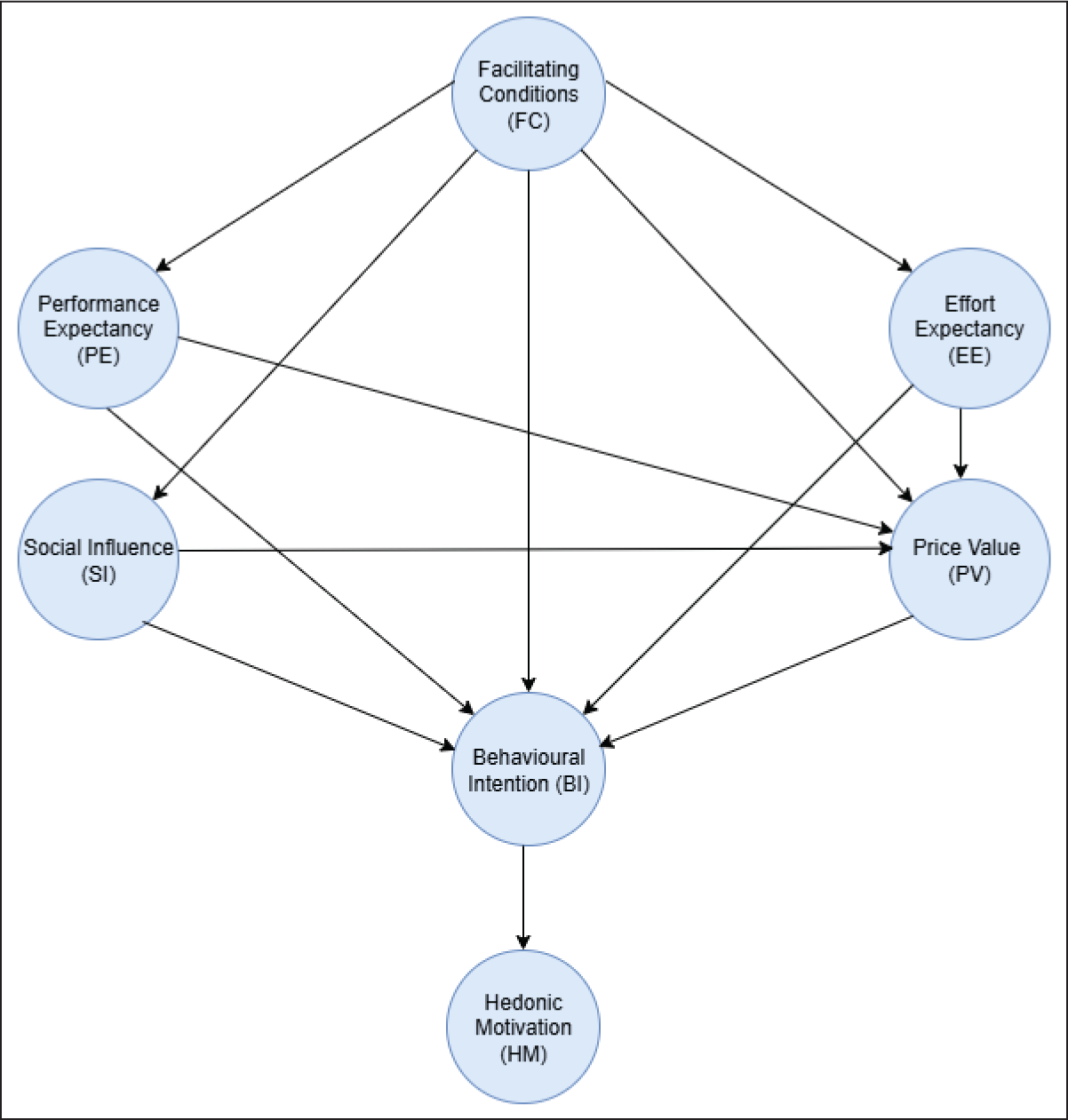

ISM Diagram

The ISM hierarchical diagram (Figure 2) presents a structured visualization of the contextual relationships among UTAUT3 constructs influencing the adoption of the e-rupee (CBDC) in India. Based on the FRM and level partitioning process, constructs are positioned across six levels. Level 1 at the bottom represents the most dependent variables, and higher levels represent progressively more influential drivers.

ISM Hierarchical Model for CBDC Adoption (e-Rupee).

At the base of the model (level 1) lies HM. This indicates that it is the most outcome-oriented construct—shaped by other variables but not influencing any. Above it, BI appears at level 2. This suggests that it is influenced by multiple constructs such as PE, PV, and EE.

PV and SI occupy level 3, reflecting its role as a mediator influenced by constructs such as PE and EE while also affecting BI. PE and EE are located at level 4, highlighting their dual role as influencers of value perceptions and user intentions.

At the top of the hierarchy (level 5) is FC, the most dominant driving construct. It affects almost all other variables but is not influenced by any, emphasizing its foundational importance in ensuring the infrastructure, accessibility, and support needed for the adoption of the e-rupee.

This hierarchical structure demonstrates how foundational elements such as digital infrastructure and perceived ease of use cascade through value perceptions and social context to influence end-user motivation and BI. It provides a clear pathway for policymakers and system designers to prioritize intervention areas that will have the most impact on adoption behavior.

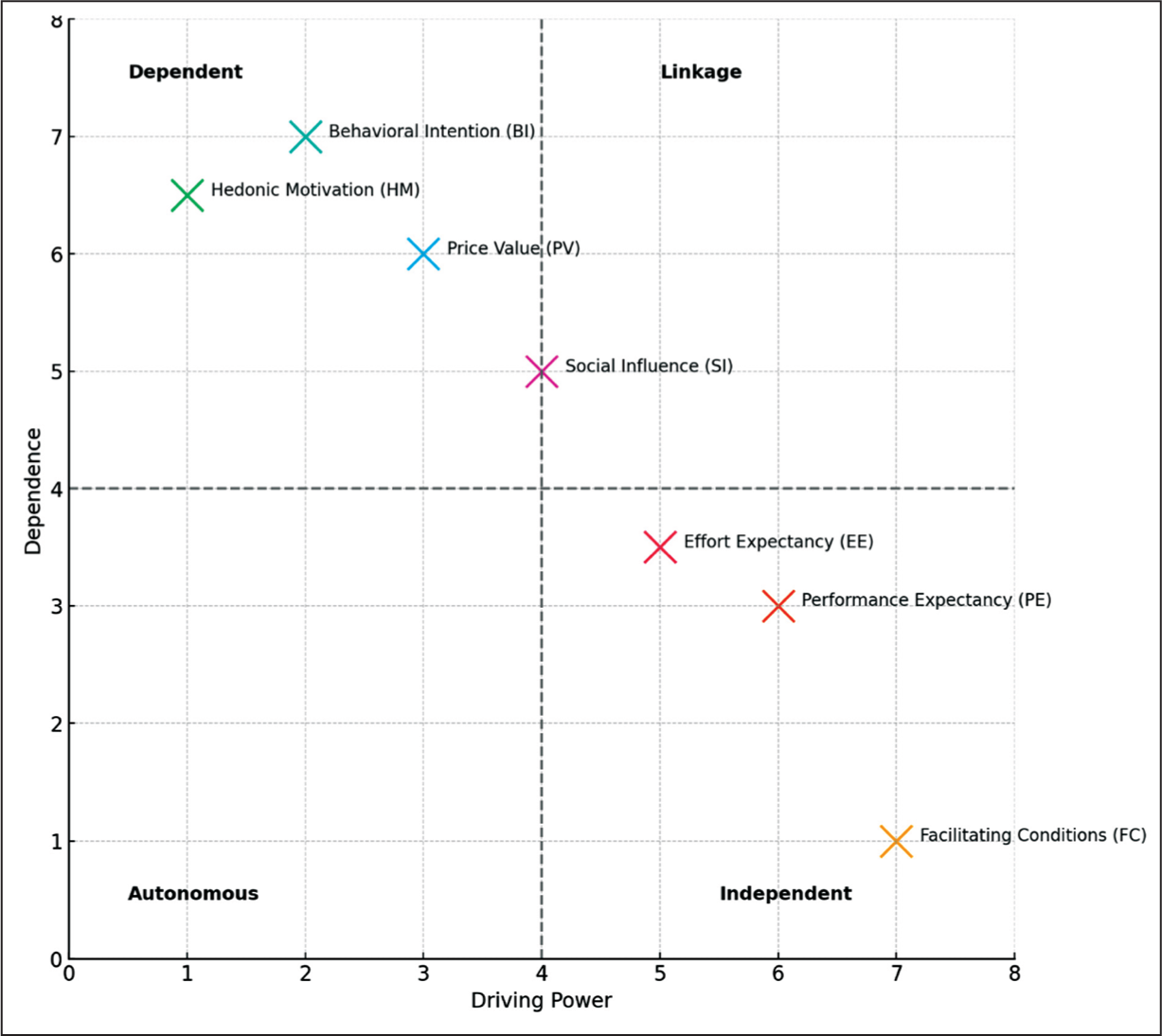

MICMAC Analysis Diagram

The MICMAC analysis categorizes UTAUT3 constructs based on their driving power and dependence to understand their influence on e-rupee adoption (Figure 3).

MICMAC Analysis Diagram for CBDC Adoption.

FCs emerged as the most powerful independent driver, influencing all other constructs with minimal dependence. PE, EE, and SI fall into the linkage category, showing both high influence and high dependence, indicating their dynamic and central role. BI and HM are highly dependent variables, positioned as outcomes in the adoption process. This classification supports the prioritization of foundational enablers such as infrastructure and perceived usefulness to enhance CBDC adoption.

Fuzzy MICMAC for Enhanced Construct Classification

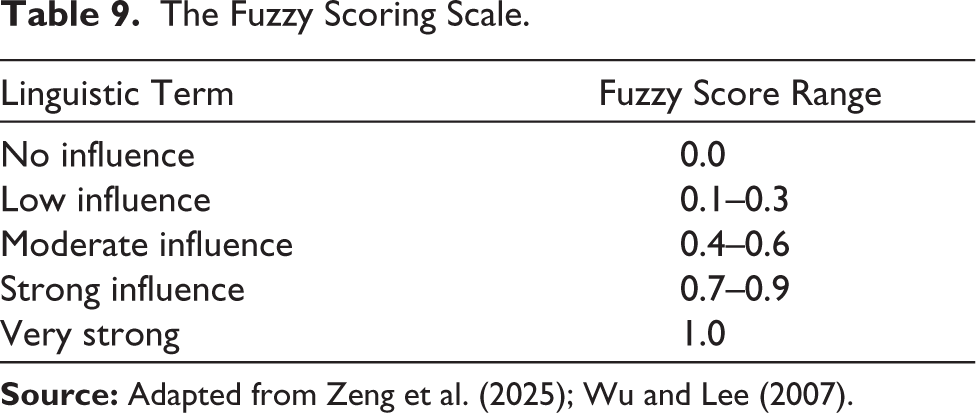

To enhance the robustness of the ISM model and better reflect the intensity of interrelationships among factors, a fuzzy MICMAC analysis was conducted based on relationships derived from literature. This extension builds upon the hierarchical structure already developed using ISM and MICMAC. Fuzzy logic allows assigning degrees of influence, thereby providing richer insights into the driving and dependence power of variables. This approach allows for graded relationships using scores between 0.0 and 1.0 (Table 9), offering a more realistic modeling of complex socio-technical adoption factors.

The Fuzzy Scoring Scale.

Given the conceptual nature of this study, and in the absence of expert interviews or empirical data collection, fuzzy values were assigned based on a simple review of the existing empirical literature on UTAUT3 and digital financial technology adoption. Relationships among constructs were evaluated by analyzing 0the frequency, direction, and consistency of findings in prior studies.

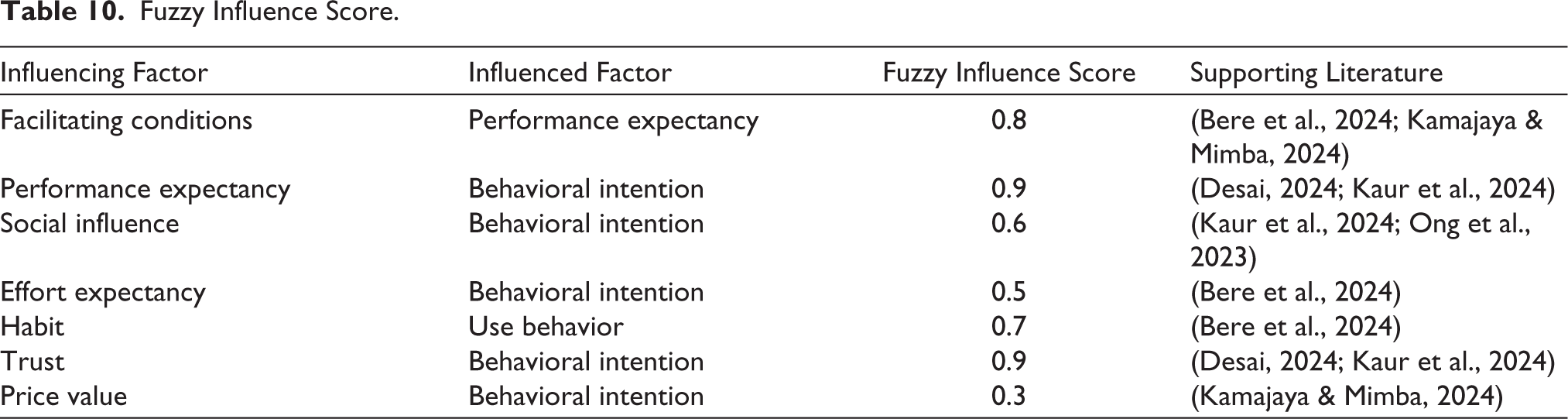

Fuzzy Influence Score.

Integrating fuzzy scores derived from literature into the reachability matrix allows for a more granular mapping of UTAUT3 constructs. Constructs such as FCs, PE, and trust emerged as strong drivers, while BI and PV were more dependent. This improved modeling depth not only addresses reviewer suggestions for analytical enhancement but also provides a more realistic reflection of the complex socio-technical environment surrounding CBDC adoption.

Findings and Conclusion

This study used the UTAUT3 framework and ISM to study the contextual connections between important components affecting the adoption of CBDC, particularly the e-rupee in India. A hierarchical structure that gives priority to the relative relevance of adoption determinants was revealed by the study through the integration of literature synthesis and structured modeling.

The findings indicate that FCs are the most influential driver in CBDC adoption. It has an important role in digital infrastructure, regulatory support, and user readiness in fostering public confidence and technological acceptance (Mahesh et al., 2024; Nguyen et al., 2020). PE and EE emerged as mid-level influencers, suggesting that users’ perceptions of usefulness and ease of use significantly shape their intent to adopt the e-rupee (Meiranto et al., 2024; Putranta et al., 2020).

SI also played a notable role in shaping value perceptions, aligning with previous research that emphasizes the impact of peer recommendations and cultural context in technology adoption, particularly in collectivist societies like India (Salsabila et al., 2024; Widyastuti & Layaman, 2023). On the dependent side, BI and HM were identified as outcome constructs. This indicated that emotional appeal and willingness to use the e-rupee are shaped by upstream perceptions of value, effort, and trust.

These findings are consistent with previous ISM-based technology adoption studies in digital finance and banking contexts (Albugami, 2022; Moorthy et al., 2019). It reinforces the applicability of structured modeling in digital currency policy design. The fuzzy MICMAC analysis revealed that FCs, PE, and trust are the strongest driving constructs influencing CBDC adoption. Conversely, BI and PV emerged as highly dependent factors in the adoption framework. Integrating fuzzy logic into the ISM model enhanced the conceptual clarity of inter-construct relationships and highlighted the layered influence structure driving e-rupee adoption in India.

Implications and Future Scope

The findings of this study can help policymakers, banks, and technology developers focus on the most important factors—such as infrastructure and ease of use—to increase public adoption of the e-rupee. The ISM model provides a structured roadmap to design targeted awareness, usability, and trust-building strategies. Future research can build on this by using real user data and advanced methods like structural equation modeling (SEM) to validate and strengthen these insights. This can further support the development of more inclusive and effective digital currency systems in India and beyond.

This study has limitations as it relies exclusively on literature-based reasoning without empirical confirmation, and the ISM technique finds only the presence of correlations rather than their strength. Future research can build on this model by incorporating empirical validation using statistical techniques such as SEM or PLS, or refining influence scores using fuzzy Delphi methods or expert consensus to strengthen generalizability and policy relevance. Empirical validation through large-scale surveys and SEM would also strengthen the generalizability and predictive accuracy of the proposed hierarchy.

Footnotes

Acknowledgements

The authors express sincere gratitude to academic experts and industry professionals for their invaluable insights and feedback throughout the development of this research.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Ethical Approval and Informed Consent Statements

This article does not contain any studies involving human participants or animals performed by the authors. Informed consent was not required.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.