Abstract

Purpose:

Investment decisions of investors are strongly influenced by their risk tolerance. Previous research suggests that risk tolerance is influenced by various social, economic, demographic and psychological factors. This research aims to extend the investigative line of inquiry regarding the influence of one such psychological factor, that is, personality, on the risk tolerance of small investors without limiting their asset class or classifying them into any groups.

Design/Methodology/Approach:

A quantitative research method is used to measure personality traits and risk tolerance in the investment decisions of small investors in Kashmir. The study uses a structured questionnaire adopted in parts from various established scales to collect data from small investors. Correlations and multiple regression have been used to arrive at the results.

Findings:

Results of the study indicated that extrovert and open-to-experience individuals showed tolerance to risk. In contrast, conscientious, neurotic and agreeable individuals were risk-averse in the geographical location considered for this study. The results imply that financial advisors must consider the personality traits of investors when giving investment advice to small investors.

Practical Implications:

It becomes essential for financial planners and advisors to follow an investor-centric approach wherein they consider the personal characteristics of individuals when giving investment advice, and they must design the portfolios/investment avenues according to the investors’ personalities. The results of this study show that investors with different characters have different risk-taking capabilities, and a particular investor will feel comfortable investing in a specific risk-class asset.

Originality/Value:

There is no study or research about the influence of personality traits on risk tolerance in investment decisions in this particular geographical area, that is, Kashmir. Therefore, this study will contribute significantly towards understanding investor behaviour and help financial advisors and investment bankers suggest appropriate investment avenues.

Introduction

The doctrine of home economics emphasizes that people constantly invest their assets to maximize their returns. However, investments are bound to carry some risk as they are inherently associated with every economic decision. Investment decisions are affected by various economic, demographic and behavioural factors (Prasad et al., 2021). Further, an investor’s investments are significantly affected by the attitude they have towards risk (Bali et al., 2009; Fellner & Maciejovsky, 2007; Hunter & Kemp, 2004). Furthermore, as suggested by the literature, psychological factors such as personality traits, emotions and past experiences and non-psychological factors like financial literacy are the critical determinants of risk-taking, which in turn affects investment decisions (see, e.g., Grable, 2000; Hunter & Kemp, 2004; Lin, 2012; Pak & Mahmood, 2015; Pinjisakikool, 2017). We attempted to examine the role of one of these behavioural factors, that is, ‘personality’, to understand whether it influences risk tolerance in the investment decision-making of small investors.

Personality combines all those traits and attitudes that differentiate a person from others. That is why when two individuals encounter a similar situation, their reactions and decisions differ from each other based on their unique personalities. Research suggests that an individual’s ability to tolerate setbacks and risk relates to their personality (Mathur & Nathani, 2019). Given the wide acceptance in management and psychological literature (see, e.g., Digman, 1990; Lee & Ashton, 2004; Weller & Thulin, 2012), this study uses the Big Five Factor (BFF) model of personality, which is based on five dimensions: ‘extroversion’, ‘agreeableness’, ‘conscientiousness’, ‘neuroticism’ and ‘openness to experience’.

In contemporary times, when behavioural finance is taking over traditional financial theories, it becomes imperative to study how investors, rather than acting rationally, get influenced by psychological factors while making investing and financing decisions. The present study builds on behavioural finance perspectives, which are pretty different from the traditional standard finance approaches and add to the field of behavioural finance research. Intending to explore how an investor’s personality influences their risk tolerance in investment decisions, the present study draws an overall picture of the investors’ decision-making process, that is, how personality plays a role in an investor’s risk preferences while making an investment decision.

Numerous researchers who have previously investigated the impact of personality of investors on their risk tolerance in investment decisions include Rai et al. (2021), Sadiq and Amna (2019), Pak and Mahmood (2015), etc. However, after an extensive review of the literature, a dearth of research in the North Indian context, especially Kashmir, was felt. This study was conducted in the region of Kashmir, which is different from the rest of the country in many aspects, such as culture and socio-economic conditions, unemployment, poor economic development and political turmoil (Bradnock & Schofield, 2010). These unique aspects of the people of this region may influence the psychology of investors, which in turn may impact the risk tolerance in investment decision-making.

It was also identified during the literature review that most researchers who researched this specific area of behavioural finance restricted the asset class for investing. That is, they took into consideration investing either in stocks or tt-bonds. However, it is known that these two are instruments of the capital market and the capital market in itself is considered very risky by investors. The aim of the present study is to assess the overall risk tolerance of investors while investing without limiting their asset class. Moreover, it was also found that most of the studies were conducted on a specific segment of investors, for example, University students (Harris et al., 2006) and/or people with basic financial literacy and investment experience (Dhiman & Raheja, 2018) and/or people employed in a specific profession, for example, IT professionals (Shankar & Kallarakal, 2018) and/or salaried investors (Rushdi, 2014) or investors investing through stockbrokers (Rai et al., 2021). The limitations of the investor class were again identified as a gap that the present study aims to fill.

Overall, what makes this research stand apart is that the study is expected to first investigate the role of personality on risk tolerance of small investors in Kashmir; second, to take into consideration the overall risk tolerance of investors while investing without limiting the asset class which studies in most of the literature have done; third, to consider the small investors without classifying them into any types/groups; and lastly, to assess if personality traits predict risk tolerance.

Personality Traits and Risk Tolerance: Background and Hypotheses Development

An individual’s behaviour results from their decision-making process, which involves judging the potential rewards and risks accompanying every action. Before deciding where and when to invest his or her savings, an investor weighs the risk and return of the available investment avenues. Thus, risk tolerance is believed to affect decision-making significantly in different financial/investment contexts (Cardak & Wilkins, 2009; Hariharan et al., 2000). Grable (2000) defines financial risk tolerance as ‘the maximum amount of uncertainty an individual is willing to accept while making a financial decision’. However, some researchers argue that even though people may generally be perceived as risk averse or risk takers, a person’s risky decision/behaviour in one area cannot reliably be made by considering one specific field (Wahl & Kirchler, 2020). As a subject in financial, social, ethical and psychological domains, researchers have profoundly explored risk tolerance. Researchers have distinguished between risk-taking in different areas, that is, financial, physical, social and ethical (Weber et al., 2002). Various researchers have attempted to study the relationship between personality and risk tolerance. For instance, Pak and Mahmood (2015) investigated the personality traits, risk-taking attitudes and investment decisions among potential private investors in Kazakhstan. After measuring the personality traits, risk tolerance level and investing decisions of respondents using the quantitative research method, the study revealed a positive influence of personality traits on an individual’s risk-tolerance behaviour and investment decisions. A similar study by Mehtab (2019) conducted on investors in metro cities of India revealed an association between personality and risk perception of investors. Using the MBTI personality assessment model, the study, among other things, revealed a significant relationship between personality types and risk aversion.

Using the BFF personality model, a similar study was conducted in India by Mathur and Nathani (2019) on young investors. The study found that extroverted young investors were less likely to take risks. The study further revealed that individuals who like to be on time and organized are unaffected by risk, and those and those who are curious and open to experience, love to learn new things and thus are high on risk tolerance. Thanki and Baser (2019) also studied the effect of personality type along with demographic variables on risk tolerance in Ahmedabad, India. Using convenience sampling while collecting data from 380 investors, the study revealed that personality type, marital status, gender, monthly income and source of earning, that is, occupation, were substantial in determining the risk tolerance level of investors. In the following sections, the present study focuses on investment risk tolerance concerning the personality traits of individual investors.

Extroversion and Risk Tolerance

Extroversion is one of the personality types proposed by the BFF model. As defined by Lucas and Diener (2001), extroversion is a personality trait that encompasses several characteristics such as sociability, assertiveness, high activity level, positive emotions and impulsivity. Extroverts also enjoy activities involving large social gatherings and thus enjoy time spent with other people and are intimidated by spending time alone. When extroverts are around people, they feel energized; when alone, they are prone to boredom. Multiple studies emphasize the potential impact of extroversion on financial decisions, particularly on the investors’ attitude towards risk-taking. However, the results of such studies are mixed. Filbeck et al. (2005), for instance, attempted to find whether individuals who differ in their personalities vary in their level of risk tolerance using the Myer–Briggs Type Indicator and found that ‘the trait of extroversion has no measurable impact on the risk tolerance of investors’. Similar results were reported by Rai et al. (2021). However, a study by Nicholson et al. (2005) on executives attending graduate courses examined the relationship between personality factors and risk-taking. The study found that extroversion and openness were positively associated with risk-taking. Given the above literature, we hypothesize the following:

Agreeableness and Risk Tolerance

Cooper (2003) states that ‘agreeableness is the trait referring to an individual being more forgiving, considerate and lenient’. ‘Agreeable individuals avoid conflicts with others. They positively consider any information provided by others without any critical assessment’ (Costa & McCrae, 1992). These individuals want to get along with others and have an optimistic view of human nature. On the other hand, those who score low on the trait of agreeableness are usually sceptical and curious. Sadiq and Khan (2019) believe that agreeable individuals struggle to make personal financial decisions. Thus, they rely on financial analysts’ judgement for the same. Individuals who score higher on agreeableness make ‘more calculated and cautious decisions and prefer to take fewer risks, which indicates a negative correlation with risk-taking’ (Chitra & Sreedevi, 2011; Sadiq & Amna, 2019). This negative relationship was further confirmed by a study by Pak and Mahmood (2015). In light of the literature, we hypothesize the following:

Conscientiousness and Risk Tolerance

The conscientiousness dimension of personality is meticulous, determined, arranged, disciplined, orderly, responsible, dependable and goal oriented (Costa & McCrae, 1992). Hence, conscientiousness is a tendency to show self-discipline, act dutifully, avoid trouble and aim for achievement, followed by planned rather than spontaneous behaviour. Mayfield et al. (2008) assert that the characteristics of conscientious individuals give them a firm confidence level in their ability to manage their finances. They go for thoughtful analysis, make well-defined investment goals and portray strong intentions for investments in long-term portfolios. Moreover, Tauni et al. (2017) and Rai et al. (2021) found a positive relationship between conscientiousness and investing behaviour. However, in their study, Mathur and Nathani (2020) conclude that young investors who possess the traits of conscientiousness are not much affected by risk tolerance. In yet another study by Ferreira (2019) on a clientele of a South African investment company, the researcher examined whether financial risk tolerance is influenced by personality and found a positive association between conscientious people and risk tolerance. Thus, we hypothesize the following:

Neuroticism and Risk Tolerance

Therasa and Vijayabanu (2015) state that ‘neurotic individuals tend to exhibit traits such as fear, anger, depression and are easily inclined to stress, unable to control their impulses’. Also, individuals who are neurotic are pessimistic, depressed and anxious and exhibit more fear of uncertainty and ambiguity (McCrae & Costa, 1997; Smith & Williams, 1992). Researchers have conducted various studies to assess the impact of neuroticism on financial decision-making and investors’ risk tolerance. However, the overall results of the studies regarding the impact of neuroticism on risk behaviour are mixed. Yalcin et al. (2016) assert that for long-term financial planning, two personality facets, that is, conscientiousness and emotional strength, affect an individual’s decision-making. Individuals who score low on neuroticism are better in financial planning and commitment to future goals. However, on the contrary, Vigil-Colet (2007) opines that ‘risk-taking is related to neurological impairments. Thus, those with low neuroticism feel greater anxiety when making risky decisions’. Following the literature, we hypothesize the following:

Openness to Experience and Risk Tolerance

Openness to experience refers to a trait in an individual’s personality that inspires him/her to be refined and to undertake new experiences. Costa and McCrae (1992) defined this personality trait using characteristics such as ‘originality, curiosity, ingenuity, and creativity. It involves active imagination, aesthetic sensitivity, attentiveness to inner feelings, preference to variety, intellectual curiosity and willingness to consider new ideas and try new things’ (as cited in Camps et al., 2016). Mayfield et al. (2008) state that openness ‘exerts a positive influence on long-term investments in business school undergraduates in the United States’. In yet another study, Nandan and Saurabh (2016) describe that open individuals tend to take higher risks than those who score low on this dimension. Rai et al. (2021), in their study, concluded that agreeableness, conscientiousness and openness traits have an effect on risk tolerance, whereas extroversion and neuroticism do not affect the risk tolerance of investors. In view of the literature, we hypothesize the following:

Methods

Data

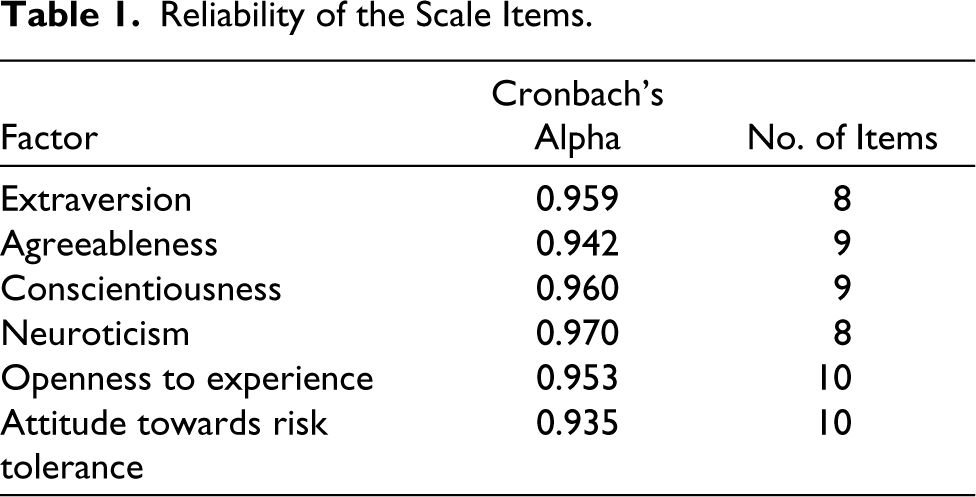

The study used both exploratory and descriptive research designs. Data were collected through mainly primary sources. However, secondary sources were also used. The data were collected using a structured questionnaire incorporating two established and validated scales (Big Five Inventory and the Risk-perception Scale). The Big Five Inventory, which is a 44-item questionnaire developed by John et al. (1991), is a reliable and validated scale that measures the five personality traits. Moreover, 10 questions regarding investment risk were asked using the Risk-perception Scale of Weber et al. (2002) to evaluate an individual’s risk-taking behaviour. The reliability and validity of the questionnaire were ensured by calculating the overall Cronbach’s alpha. The reliability of the scale items is presented in Table 1 below.

Reliability of the Scale Items.

Sample

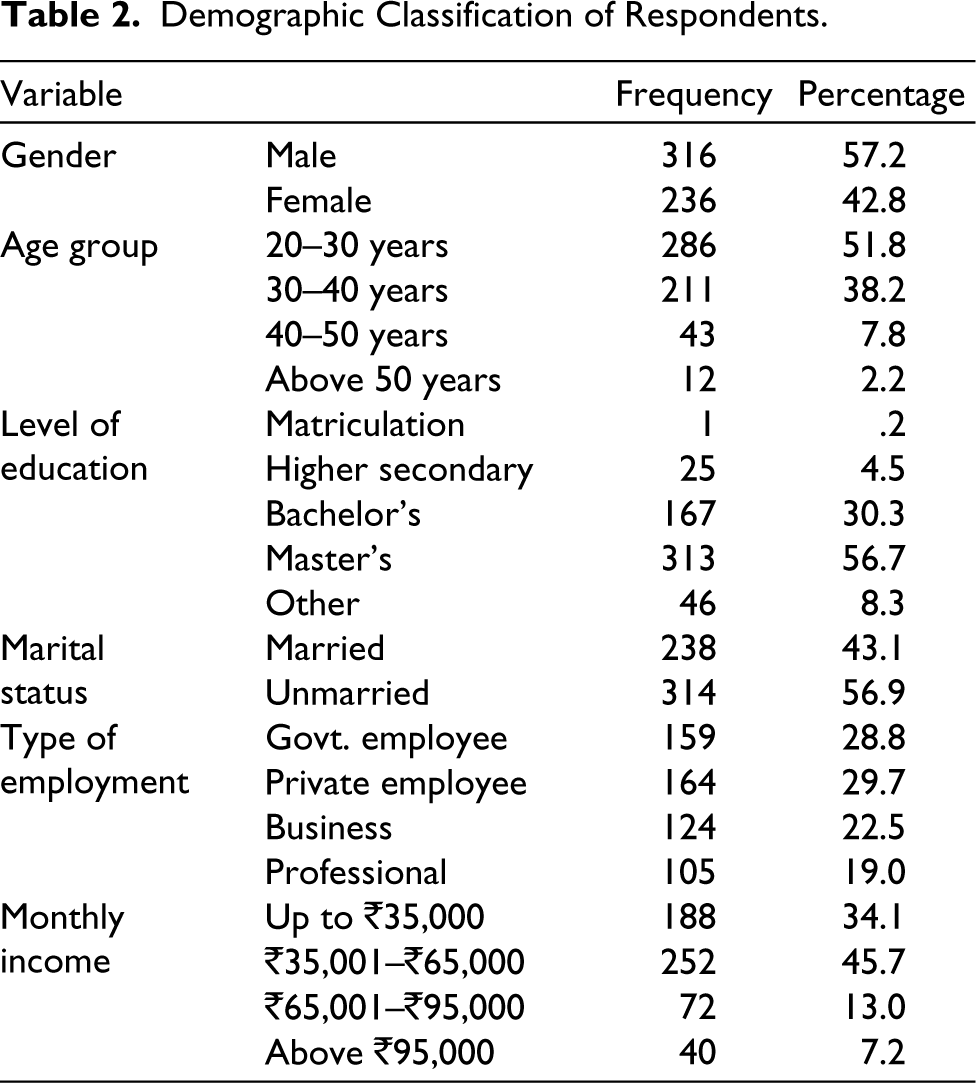

The population for the study comprised small investors in the age group 20 years and above with a stable income source. Since the study focused on small investors, it took only those respondents who had an investment for final data analysis. The reason for taking only small investors was that a huge portion of households in Kashmir have low incomes. As per a 2018 report provided by the Directorate of Economics and Statistics, Jammu and Kashmir (2018), ‘the monthly per capita income of J&K State for 2011–12 in rural areas was Rs. 891, while it marks Rs. 988 in urban areas’. These statistical figures indicate that most of the households do not earn much. So, when investors are faced with a situation like this, the investment decision becomes even more crucial. Because these small investors have little resources to put aside for investing, it must involve thorough thinking and mental exercise. Thus, only small investors, with little resources, invested for their own selves to increase their wealth, unlike institutional investors for whom investing others’ money is a job. Since the population was unknown and infinite, the sample size was determined using the itemized sampling method. Therefore, the research instrument contained 54 items, so the itemized sample was 540 (54 items × 10). Considering the likelihood of non-response and incomplete questionnaires, the calculated sample size was scaled up by 30%, that is, 702. After eliminating incompleteness and blank responses, the sample size was reduced to 552, which was considered and used as the final sample size. The sampling technique chosen was multi-stage random sampling followed by purposive sampling. The descriptive statistics in the form of frequencies are presented in Table 2 based on the characteristics of the sample (n = 552).

Demographic Classification of Respondents.

This section presents the inferential statistics of the collected data. It includes the statistical study of the association between the independent variable (personality) and the dependent variable (risk tolerance). For this, correlation and multiple regression techniques have been used.

Correlation

We performed a correlation analysis to ascertain the linear relationship between independent variables and risk tolerance. Table 3 displays the correlation results between the independent and dependent variables.

Pearson Correlation.

The results reveal a moderate positive linear relationship between ‘extroversion’ and ‘risk tolerance’ and ‘openness to experience’ and ‘risk tolerance’. This indicates a positive relationship between these two personality types and investor risk tolerance, indicating that a person who is extroverted and a person who is open to experience have higher risk tolerance.

However, the table reveals that ‘agreeableness’, ‘conscientiousness’ and ‘neuroticism’ report a negative relationship with risk tolerance. Most of the literature supports this finding (see, e.g., Anic, 2007; Pak & Mahmood, 2015; Sadiq & Amna, 2019).

Multiple Regression Analysis

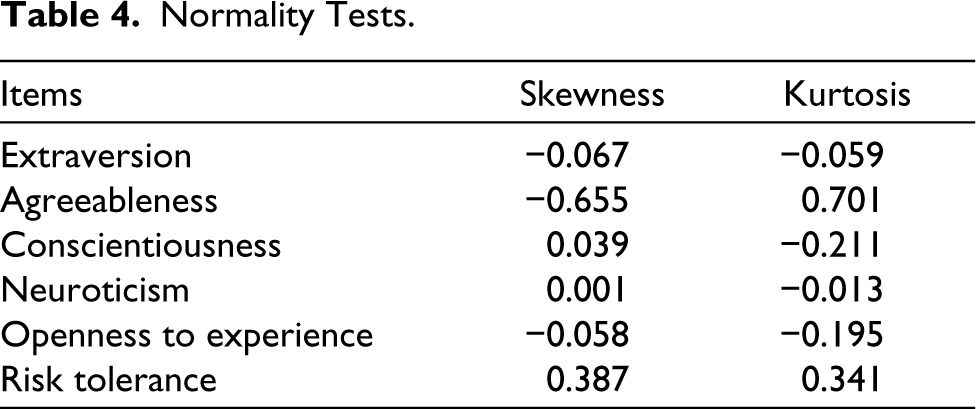

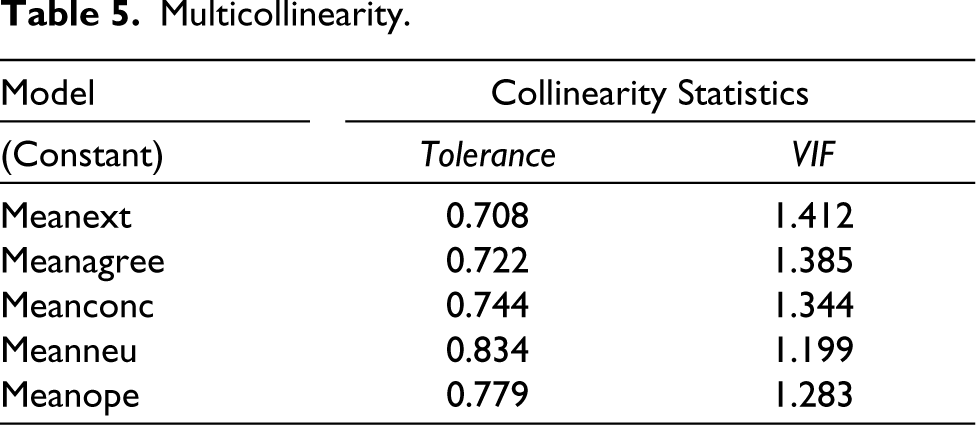

To verify whether the independent variables are statistically significant in predicting investors’ risk tolerance, the following regression equation was designed. However, before proceeding with regression, assumptions and prerequisites for analysing the data were tested, including data screening, normality, linearity, multicollinearity and homoscedasticity. The results for normality and multicollinearity have been presented in Tables 4 and 5 below:

Normality Tests.

Multicollinearity.

The applied regression analysis produced the results shown in Tables 6 and 7. The regression equation used for the analysis is presented below in equation:

Model Summary of Regression Equation.

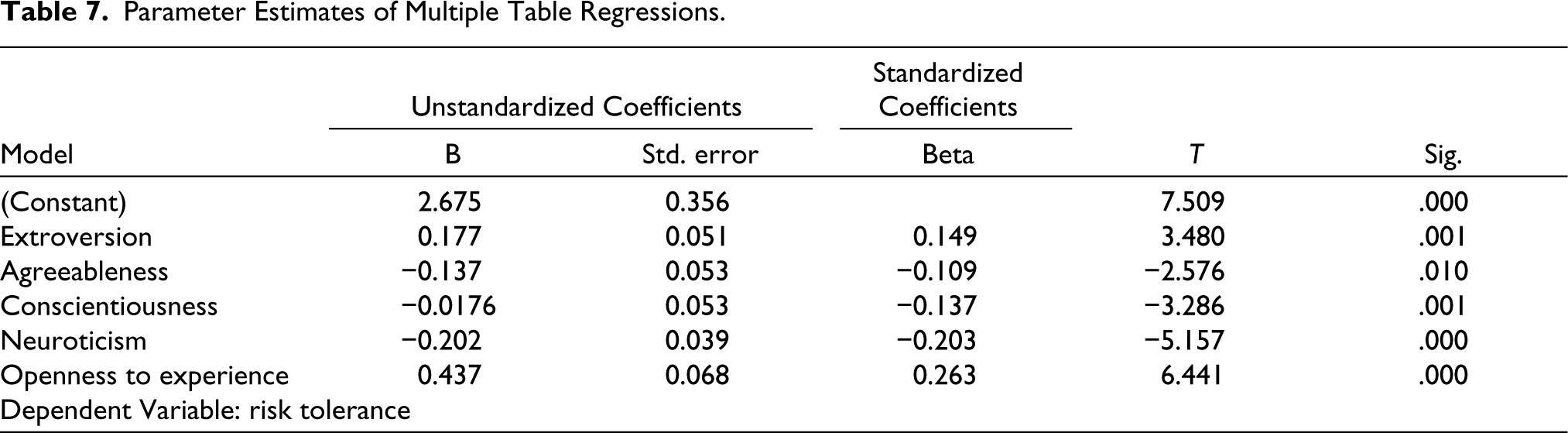

Parameter Estimates of Multiple Table Regressions.

Table 6 summarizes the regression equation and reveals that personality traits are statistically significant in predicting investor risk tolerance. Various factors may influence the dependent variable. However, the regression model explains only a limited proportion of the dependent variable’s total variance. Similarly, in this case, there can be various factors affecting an investor’s risk tolerance. However, the above regression model only aims to explain the variance in risk tolerance as a result of personality factors. Since the value of R (correlation coefficient) is 0.540, it can be deciphered that personality traits (extroversion, agreeableness, conscientiousness, neuroticism and openness to experience) do affect the risk tolerance of an investor. However, the value of R2 (coefficient of determination) was found to be 0.291, signifying that 29.1% of the variation in risk tolerance of investors is explained by extroversion, agreeableness, conscientiousness, neuroticism and openness to experience altogether.

Discussion and Limitations

The correlation and multiple regression employed to test the hypothesis (H1) of the study suggest a significant impact of personality on investors’ risk tolerance. The results indicate that personality traits significantly (positively/negatively) impact investment risk tolerance. ‘Extroversion’ and ‘Openness to experience’ are found to positively impact risk tolerance, as individuals scoring high on these two dimensions have a high tolerance for risk. Similarly, the dimensions of ‘agreeableness’, ‘conscientiousness’ and ‘neuroticism’ have a negative relationship with risk tolerance; that is, these individuals are not risk tolerant and try to avoid risk.

As reported in the model, the value of the beta coefficient (β1) for the independent variable ‘extroversion’ is 0.177 (p = .001), which is statistically significant at the 5% level. It implies that ‘extroversion has a positive and statistically significant influence on investor risk tolerance’. It can thus be concluded that individuals scoring high on extroversion are more risk tolerant. The results coincide with the findings of Dhiman and Raheja (2018), Pinjisakikool (2017), Pak and Mahmood (2015), Contessa et al. (2013), Mayfield et al. (2008) and Anic (2007). These researchers suggest that extroverts possess a positive attitude towards life due to their outgoing and optimistic nature. They find comfort in engaging in the world around them and taking risks. Lo et al. (2005) add that extroverts may consult financial advisors for investment but make decisions based on their overestimation of the market and underestimation of risks. Thus, an extrovert has high risk tolerance because of the inherent traits of self-confidence, dominance and optimistic attitude. Dalsky et al. (2008) suggest that these researchers feel that extroverts tend to be more receptive to positive information rather than negative information, as a result of which they always end up making optimistic and forward-looking decisions. Furthermore, Sadi et al. (2011) add that ‘extroverts’ take risks more impetuously, explaining the higher risk tolerance.

Similarly, the value of the beta coefficient (β5) reported for the independent variable of ‘openness to experience’ is 0.437 (p = .000), signifying that ‘openness to experience’ influences investor risk tolerance positively. Nga and Yien (2013) state that openness in individuals promotes their willingness to embrace unconventional financial decision-making methods and, therefore, could be one of the reasons for the high-risk tolerance of open individuals. Moreover, Kubilay and Bayrakdaroglu (2016) add that investors who are open to experience take more risks, confirming the present study’s findings. The study results align with the previous literature (see, e.g., Pak & Mahmood, 2015; Pinjisakikool, 2017; Sadiq & Amna, 2019). These researchers feel that since these individuals are open to new experiences and are adventurous, they would invest their money in avenues irrespective of the possible risk associated with the investment as they would like to bump into the thrill that lies in the investment, that is, either high profits or losses. Likewise, Soane and Chimel (2005) add that people who are strong on openness to experience traits are expected to be risk takers. Thus, the tendency to be more risk tolerant in open individuals comes from their traits.

Likewise, the value of the beta coefficient (β2) for the independent variable ‘agreeableness’, as reported in the model, is −0.137 (p = .010). Since ‘agreeable’ people tend to be cooperative and have good social relationships (Costa & McCrae, 1992), they prefer to get acknowledgement from others for their decisions. Agreeable people think thoroughly before making decisions as they have a low risk tolerance. However, some studies, for example, Dhiman and Raheja (2018) and Mayfield et al. (2008), contradict this relationship. They state that since agreeable individuals are cooperative and reliable and respect others’ opinions, they take more risks because they are more likely to rely on others’ opinions. Moreover, as stated by Schimtt (2004), ‘these people prefer to avoid arguing, disagreement and ferocity, and because these negative characteristics conflict with their personality’. These facts lead to a negative relationship between ‘agreeableness’ and ‘risk tolerance’. Numerous research studies confirm these study results (see, e.g., Chitra & Sreedevi, 2011; Kubilay & Bayrakdaroglu, 2016; Mathur & Nathani, 2019; etc.).

Last of all, the beta coefficients for ‘conscientiousness’ (β3) and ‘neuroticism’ (β4) are −0.176 (p = .001) and −0.202 (p = .000), respectively. Regarding this negative relationship, the plausible reason could be that conscientious individuals are meticulous, determined, arranged, disciplined, responsible and goal oriented (Camps et al., 2016). Moreover, Sadi et al. (2011) add that ‘conscientious investors do not rely on delusions and make their investment decisions prudently. This ability makes them more particular about their choice of investment and risk tolerance’. However, Ferreira (2019) and Dhiman and Raheja (2018) reported a positive relationship between ‘conscientiousness’ and ‘risk tolerance’. They believe that conscientious people have a certain degree of confidence, carefulness and clear goals when it comes to investment. So, they take calculated risks and thus have a positive relationship with risk tolerance.

Regarding the negative relationship between ‘neuroticism’ and ‘risk tolerance’, some previous studies have shown that people with a dominant trait of neuroticism have negative and weak emotions (see, e.g., McCrae & Costa, 1992). These individuals are pessimistic and exhibit more fear of uncertainty and ambiguity (Smith & Williams, 1992). Thus, neurotic individuals invest smaller amounts in risky assets (Mayfield et al., 2008) which is a result of these individuals’ risk averseness’. Various other studies confirm the study results (see, e.g., Niszczota, 2014; Vigil-Colet, 2007; Yalcin et al., 2016; Young et al., 2012).

A research study is seldom perfect, and without limitation, this study is no exception. Though utmost care has been taken while framing, designing and conducting the study, some limitations still exist. Future research can be conducted by overcoming the limitations. To begin with, the sample size of 552 can be a limiting factor for the research. However, a bigger sample size can be taken into account to make the studies more representative. Also, only one independent variable, that is, personality, and one dependent variable, that is, risk tolerance in investment decisions, have been used in the study. Future research can be extended by taking more variables into the study as it becomes evident that only personality cannot affect the risk tolerance of small investors. A number of factors, such as demographic characteristics, market conditions, individual goals, etc., work together to have an overall impact on an investor’s risk tolerance. Thus, it becomes important to study other variables as well. Also, a mediating or moderating relationship study could be established if the number of variables is increased. Moreover, the study has been conducted on small investors of Kashmir, wherein 92.7% of the investors taken in the study have had an income of less than ₹95,000 per month. In future, studies could be conducted on investors with higher incomes as the results obtained from those studies may broaden the horizons of this particular behavioural finance aspect with respect to Kashmir. Lastly, future researchers can use a different model to conduct the study other than the BFF.

Conclusion

The study results indicate that personality is one of the triggering factors in determining the risk tolerance in investment decisions of small investors of Kashmir. The results indicate that ‘openness to experience’ and ‘extraversion’ personality traits have a positive relationship with the risk tolerance of small investors, whereas ‘agreeableness’, ‘conscientiousness’ and ‘neuroticism’ have a negative relationship with risk tolerance. ‘Openness to experience’ displayed the strongest indication of proneness to risk taking. This can be attributed to the fact that open individuals tend to be curious, adventurous and open to new experiences (Chauvin et al., 2007; Chen et al., 2012). With regard to ‘extroversion’, a positive relationship with ‘risk tolerance’ was found. The reason for this can be attributed to the fact that extroverts, as opined by Sadi et al. (2011), are likely to be guided by external stimulators, as a result of which they take risks impulsively.

‘Neuroticism’ showed the strongest negative relationship with ‘risk tolerance’. The results are no surprise as this personality trait is characterized by upset ability, anxiety, moodiness, worry and envy (Camps et al., 2016). It was also found that the traits of ‘agreeableness’ and ‘risk tolerance’ are negatively related. Moreover, a negative correlation was also reported between the personality traits of ‘conscientiousness’ and ‘risk tolerance’. Individuals with this personality are characterized by traits of hard work, self-discipline, acting dutifully and aiming for achievement. They do not act spontaneously, and every action of conscious people is thoroughly planned. All these traits give these individuals a certain level of confidence in their financial abilities.

Thus, it becomes really important on the part of investors to assess their personality before making investment decisions because if they choose a risk-class investment that is above their appetite for risk tolerance, they may end up in distress. Investors, as per their personality type, invest in different investment avenues, and financial advisors must try to link investments with investors based on their risk tolerance levels. Moreover, it becomes essential for financial planners and advisors to follow an investor-centric approach wherein they consider the personal characteristics of individuals when giving investment advice. Thus, the investment advisors must design the portfolios/investment avenues according to the personality of the investors as it becomes utmost important after keeping in view the results of this study that investors with different personalities have different risk-taking capabilities and a particular investor will feel comfortable in investing in a particular risk-class asset.

Furthermore, investors must rely on expert advice rather than following a herd behaviour mentality regarding specific investments. As one shoe does not fit all, one investment avenue can be promising to one investor but not to another. So financial advisors must take extra precautions while giving investment advice because these investments are indeed vital for the development of a country. These investments make up the capital for industrialization in a country and, thereafter, decide the future of the country especially in lower-middle income countries like India, where finding sufficient capital for development efforts is an enormous task.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.