Abstract

Micro-entrepreneurs are the strategic assets of the nation, given their mammoth share in maintaining the socio-economic equilibrium and inclusive growth of the economy. Despite their contribution to India’s economy, they are still confronted with several on-ground hurdles, such as inadequate financial literacy among entrepreneurs, inaccessibility to affordable credit, financial mismanagement and lack of innovation. The extant literature has revealed that financial illiteracy and lack of innovation have raised pertinent concerns across the world, given the increasing rate of business failures. Nonetheless, the effect of financial literacy on organisational performance and innovativeness remains underexplored and fragmented. This study aims to examine the effect of financial literacy on the business performance and innovativeness of the micro-entrepreneurs in Delhi-National Capital Region (NCR) in India. Primary data were gathered from around 302 micro-entrepreneurs registered in Delhi-NCR through self-administered questionnaires. Data analysis was conducted through SmartPLS 4 software. The results indicated that financial literacy significantly impacts business performance and innovativeness among micro-entrepreneurs. Therefore, the study advocates wider participation of policymakers, financial service providers and managers in designing tailored strategies aimed to enhance the financial education of micro-entrepreneurs.

Keywords

Introduction

Micro, small and medium enterprises (MSMEs) are touted as the growth accelerators in India’s economy and play a pivotal role in nation-building through stimulating economic development by generating employment opportunities for the bottom-of-the-pyramid communities, narrowing regional economic imbalances, fostering entrepreneurial activities, boosting competitiveness and innovativeness among firms. Micro-enterprises constitute more than 99% of the total registered MSMEs followed by 0.52% small enterprises and 0.01% medium enterprises (MSME, 2020; MSME, 2021). The present contribution of this sector towards India’s GDP, total export and manufacturing output is reported as 29%, 45% and 33%, respectively (CII, 2019; MSME, 2021). Evidently, micro-enterprises have a strategic contribution, both in volume and value creation, to the Indian economy.

Though the statistics may differ across developed and developing economies and industry types, typically, about two-thirds of businesses do not survive within the initial 5 years (Agyapong & Attram, 2019; Arasti et al., 2014). Lack of innovation, less competitive edge, liquidity crunch, inadequate accounting records, low financial literacy among owner–managers and financial mismanagement are some of the empirically validated on-ground hurdles faced by micro-enterprises which further affects their business performance (Agyapong & Attram, 2019; Arasti et al., 2014; Hassan et al., 2018; IBM Study, 2017; Maheshkar & Soni, 2021). The former Federal Reserve Chief of the United States noted the rising significance of financial literacy in the twenty-first century as financial markets are becoming more complex (Hogarth & Hilgert, 2002).

In the Indian context, a survey by Standard and Poor revealed that 76% of the Indian population faces difficulty in comprehending fundamental financial concepts involving numeracy, inflation, calculation of compound interest and risk management (GFLEC, 2023). Indeed, research on financial literacy at household level and its effect on savings, investment decisions, stock market participation and risk tolerance is abundant (Lusardi & Mitchell, 2014), but the studies documenting the interconnections among financial literacy, business performance and innovativeness in the context of micro-entrepreneurs are underexplored in the academic literature, also the findings are fragmented. Given the vacuum in the studies pertaining to financial literacy and entrepreneurship, it behoves on academia to extend the probe on financial literacy from the perspective of consumers to entrepreneurs.

Evidently, financial illiteracy among entrepreneurs is widespread and has raised pertinent concerns all over the world (Zulaihati et al., 2020). Absence of adequate financial literacy among entrepreneurs is notably the root cause of business failures, as the personal characteristics of business owners have a profound effect on enterprise performance (Lukiastuti & Kusuma, 2020). Financial ignorance of entrepreneurs can lead to poor business decisions, which have social as well as economic impact, as the business failures can lead to crumbling of financial ecosystem of any economy. The adverse effect of the pandemic on micro-enterprises has highlighted, more than ever, the importance of financial knowledge and skills among micro-entrepreneurs, as they were most vulnerable to the crises. Henceforth, entrepreneurs should possess financial awareness, skills, attitude and behaviour to have a fundamental knowledge of financial terms and terminologies, be able to analyse the financial statements of their company and have knowledge of different financial products and services that exist in the financial marketplace, to ensure sustainable business operations (Hogarth & Hilgert, 2002; Liu et al., 2020; OECD, 2017). Merely starting a business is not enough; entrepreneurs should make holistic efforts to make the venture sustainable. Financial literacy of senior executives positively impacts the sustainability of small and medium enterprises (SMEs) as per the findings of Ye and Kulathunga (2019). Micro-entrepreneurs have to make complex financial decisions regarding planning, procuring, allocating resources and constantly innovating during different phases of the business lifecycle to achieve economic gains, for the purpose of which they need to be equipped with adequate financial literacy. If an entrepreneur is financially literate, they can make strategic investment decisions, identify market opportunities, have high-risk propensity in business and effectively manage the finances, leading to better strategic outcomes. Entrepreneurial skills such as bookkeeping, budgeting, debt management, monitoring financial ratios and interpreting audit reports are reported to have a positive effect on business performance (Julius Tumba et al., 2022; Mutegi et al., 2015).

The theoretical support of this study can be derived from the theory of resource-based view (RBV). The theory propounds that an organisation can achieve superior business performance through sustained competitive advantage if it possesses strategic resources that are rare, valuable, inimitable and non-substitutable (Barney, 1991; Wernerfelt, 1984). Building on RBV, the present study contemplates that financial knowledge and skills are some of the strategic intangible resources that can lead to superior business performance (Agyapong & Attram, 2019; Luo & Cheng, 2022). Given the remarkable contribution of micro-enterprises to India’s economy, measuring business performance in the present macroeconomic environment assumes greater significance for several stakeholders such as academicians, business owners, financial institutions and policymakers. Furthermore, financing is a critical pillar and central to the holistic development of a business enterprise. Even before the start of their entrepreneurial venture, notably, the primary challenge that strikes an entrepreneur is related with the finances. Having adequate financial knowledge and skills empowers an entrepreneur to manage their business finances effectively by being innovative in selecting financial instruments, which may further result in better debt management and risk diversification, thereby better control on business operations.

With this backdrop, the present research work aims to examine the influence of financial literacy on the business performance and the innovativeness in the context of micro-enterprises in the Delhi-National Capital Region (NCR), India. The selection of micro-entrepreneurs as a sampling frame in this study was motivated by the fact that, even though they have a larger pie in the nation building, they still face fundamental issues such as limited resources and scale of operations, constrained export potential, have low competitive advantage and face information asymmetry, all of which exposes a micro-entrepreneur to plethora of internal as well as external risks. For all the above-stated reasons, micro-entrepreneurs need to have enough financial knowledge as they take most of the business decisions themselves. In the light of above arguments, the article aims to achieve the above-mentioned objectives.

Literature Review

Micro-enterprises in Delhi-NCR

According to the Gazette of India, Ministry of MSMEs on 1 June 2020, notified the following revised criteria for micro-enterprises as a part of the Aatmanirbhar Bharat Package. It notifies the maximum limit of a micro-enterprise in respect of investment in plant and machinery or equipment and turnover, which are ₹10 million and ₹50 million, respectively.

As per the Economic Survey, 2022, Delhi-NCR is the emerging hotspot for industrial development due to the existence of myriad businesses, exponential rise in infrastructure development, a large consumer market, rising per capita income and employment opportunities, resulting in emerging entrepreneurial ecosystem. Delhi has 0.925 million estimated micro-enterprises as per the reports of MSME 2020–2021, whereas NCR has 4.19 million MSMEs according to the executive summary prepared by the NCR Planning Board. Henceforth, the authors were motivated to select the National Capital and the areas which are part of NCR as the sampling area of the present study.

Theoretical Literature Review

The present study embraces RBV, which views tangible and intangible endowments as sources of competitive advantage and key to superior organisational outcomes. This study construes financial skills and knowledge as strategic resources that an entrepreneurs must acquire to create a competitive advantage over its rivals. The past literature has empirically validated the RBV by concluding that financial knowledge and skills have a positive impact on business performance (Agyapong & Attram, 2019; Eniola & Entebang, 2015).

Empirical Literature Review

Financial Literacy of Entrepreneurs and its Influence on Business Performance

The concept of financial literacy rests on five pillars, such as knowledge, ability to comprehend fundamental financial concepts, having a knack of managing personal finances, appropriate skill and confidence while making future financial plans (Remund, 2010). Financial literacy is measured by financial knowledge and financial skills in the present study. Lusardi and Mitchell (2011), in their working paper, concluded that financial literacy is a lifetime skill that is needed to navigate the complex financial landscape. A financially literate entrepreneur can be defined as someone who makes informed financial decisions at the various growth stages of the business, has knowledge about financial products and services and confidently approaches financial service providers (USAID, 2009). According to Smith and Reece (1998), business performance is defined as ‘the operational ability to satisfy the desires of the company’s major shareholder’. Hurley and Hult (1998) defines business performance as ‘the achievement of organisational goals related to profitability and growth in sales and market share, as well as the accomplishment of general firm strategic objectives’. Findings by Njoroge (2013) found out that there is a positive relationship between financial literacy and the entrepreneurial success of business enterprises in Kenya. In the same vein, the work of Bruhn and Zia (2013) observed that high financial literacy among entrepreneurs resulted in improved sales and business performance. The studies by Eniola and Entebang (2015) and Wijewardena et al. (2008) concluded that possession of financial knowledge, financial awareness and financial attitude by the owners of SMEs enhanced their business performance. Agyei (2018) ascertained that there is positive relationship between firm growth and financial literacy. Tuffour et al. (2020) assessed the impact of determinants of financial literacy (awareness, attitude and knowledge) on the performance (financial and non-financial) of managers in Ghana. More so, this finding is in line with Julius Tumba et al. (2022), who examined the impact of financial literacy (financial education, cash forecasting, bookkeeping) on the business performance of female micro-entrepreneurs in Nigeria. Henceforth, the authors have formulated the following hypotheses in the light of above arguments.

H1a: Financial knowledge has a significant positive effect on the business performance.

H1b: Financial skills have a significant positive effect on the business performance.

Financial Literacy and Innovativeness

The past literature on the effect of financial literacy on innovativeness is underexplored in the academic literature. Innovativeness is the capacity of firm to involve in innovative activities, providing creative solutions to business problems and working on untapped opportunities crucial for the sustainable business performance and survival of firms (Hult et al., 2004). In the context of financial literacy, being innovative is when an entrepreneur chooses the most suitable financing instruments that facilitate the growth of enterprises by the existing financial information. According to the study ‘Entrepreneurial India’, carried out by IBM in collaboration with Oxford Economics, it was found that around 90% of Indian startups fail because of lack of innovation and unique business models. The literature suggests that finances have an instrumental role in enhancing the innovative activities in an organisation. Innovation requires financial resources, the inaccessibility of which can negatively affect the growth of businesses especially in the times of crisis. The firm that keeps innovating can adapt to the crises more efficiently. If an entrepreneur is financially literate, then they can utilise the financial products and services effectively to sustain innovation.

García-Pérez-de-Lema et al. (2021) observed that financial literacy of CEOs has a direct and indirect impact on the technological innovation in SMEs. MSMEs in India lack innovation, which hampers their development. Wahyono and Hutahayan (2021) concluded that there are positive interconnections among financial literacy, performance and innovation of entrepreneurs in Java and Bali. Hence, the authors have formulated the following hypotheses in this regard.

H2a: Financial knowledge of micro-entrepreneurs has a significant positive effect on innovativeness.

H2b: Financial skills of micro-entrepreneurs have a significant positive effect on innovativeness.

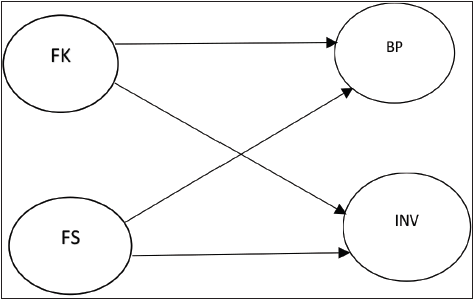

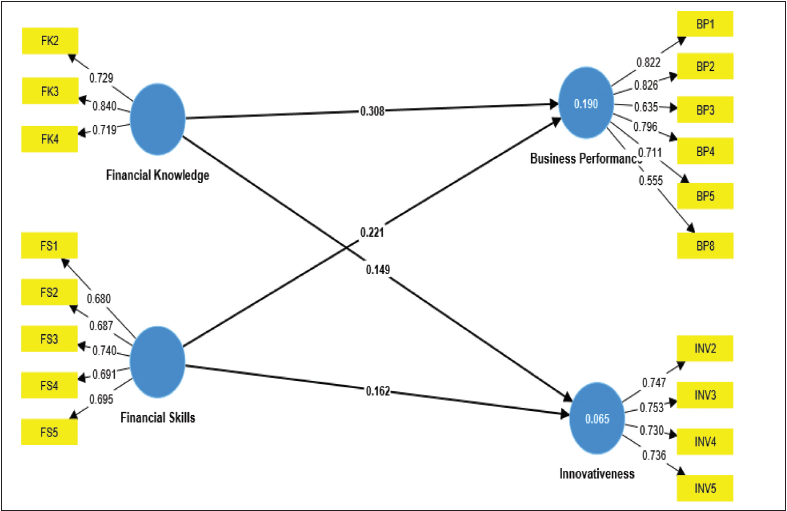

The hypothesized relationships are shown in Figure 1.

Objectives

This study aims to achieve twin objectives. The principal objective is to investigate the influence of financial literacy on the business performance. Furthermore, the study explores the influence of financial literacy on innovativeness in the context of micro-enterprises in Delhi-NCR.

Research Methodology

Research Design, Data and Sampling

The study was quantitative in nature, adopted a cross-sectional survey method and obtained data from 302 micro-entrepreneurs from industry associations registered with MSME on Udyam Portal in Delhi-NCR. The respondents constituted owners–managers of micro-enterprises in manufacturing, trading and service firms who provided primary information on the variables: financial literacy (financial knowledge and financial skills), business performance and innovativeness. The data from the micro-entrepreneurs were obtained through field survey from the period between November 2022 to January 2023 using structured questionnaires. Data analyses were carried out through partial least squares approach to structural equation modelling (SmartPLS 4) to analyse the hypothesized relationships among constructs. Non-probability method of sampling, convenience sampling, was employed in the process of collecting data. The size of the sample in this study was decided following the suggestions of Reinartz et al. (2009).

Data Collection and Instrument

The data on the variables of interest were gathered physically from the micro-entrepreneurs through self-administered close-ended questionnaires. The questionnaire comprised two sections. Section 1 captured demographic and business profile of the micro-entrepreneurs such as gender, age of the respondents, age of the organisation, nature of the firm and position in the organisation. Section 2 consisted of close-ended questions on the latent constructs such as financial knowledge, financial skills, business performance and innovativeness. The survey instrument was presented before five experts in the field, five professors in the department, three research scholars and three chartered accountants who were also the owners of micro-enterprises. Subsequent revisions were made in the instrument to make them more relevant in the context of micro-enterprises in Delhi-NCR. Therefore, face and content validity of the survey instrument was ensured. Responses sought on the hypothesized variables were collected on the five-point Likert scale (Likert, 1932), where ‘one’ was (strongly disagree) to ‘five’ was (strongly agree). To ascertain the reliability and validity of the questionnaire, a pilot test was also conducted among 32 micro-entrepreneurs in Delhi-NCR. In total, 302 micro-entrepreneurs participated in the survey, out of which 234 respondents provided useable responses for further data analysis (77.48%) after accounting for data entry errors, missing values and data cleaning. The authors assured the respondents that the responses obtained would be kept confidential as researchers collected data pertaining to their business performance.

Measurement of Variables

Financial Literacy

The authors have measured financial literacy variable through two proxies: financial knowledge and financial skills, adapted from previous studies to suit the context of present study. So, financial skills and financial knowledge are the exogenous variables in the study. The measure of financial knowledge and financial skills are adapted from van Rooij et al. (2011), Okello Candiya Bongomin et al. (2017), Kojo Oseifuah (2010), Sulaiman (2014), Dahmen and Rodríguez (2014), Barte (2012) and Reich and Berman (2014). Financial knowledge and financial skills in this study were measured by time value of money, knowledge of financial statements, financial ratios, working capital, debt and financial management as indicators of financial literacy.

Business Performance

In the present study, business performance is an endogenous variable in the context of micro-enterprises. The items are adopted from Covin and Slevin (1991), Watson (2007) and Mac an Bhaird (2010), who used growth in profit, revenue, sales, market share, number of customers and competitive advantage as indicators of business performance.

Innovativeness

The items measuring innovativeness are adopted from Hurley and Hult (1998) and Homburg and Pflesser (2000), which used creativity, new ideas, research and development as indicators.

Data Analysis, Findings and Discussion

The data analyses was performed through PLS-SEM (Smart-PLS version 4). The authors were motivated to utilise this technique because of its wide acceptability in multiple disciplines, including strategic management (Hair et al., 2012), less sample size benefits and its ability to test the theoretical framework with prediction. PLS-SEM exhibits great statistical power in case of exploratory research and underdeveloped or developing theories as per the suggestions of Purwanto and Sudargini (2021) and Hair et al. (2017). This study attempts to extend the theory of RBV, which hypothesises that financial knowledge and financial skills are the strategic intangible resources that are the sources of enhanced firm performance. As per Henseler et al. (2016), the analysis of PLS-SEM is conducted in two stages: first, we ascertain measurement model based on assessment of construct reliability and validity, and second, the hypothesized model path coefficients are verified, which is assessing the structural model.

Demographic and Business Characteristics

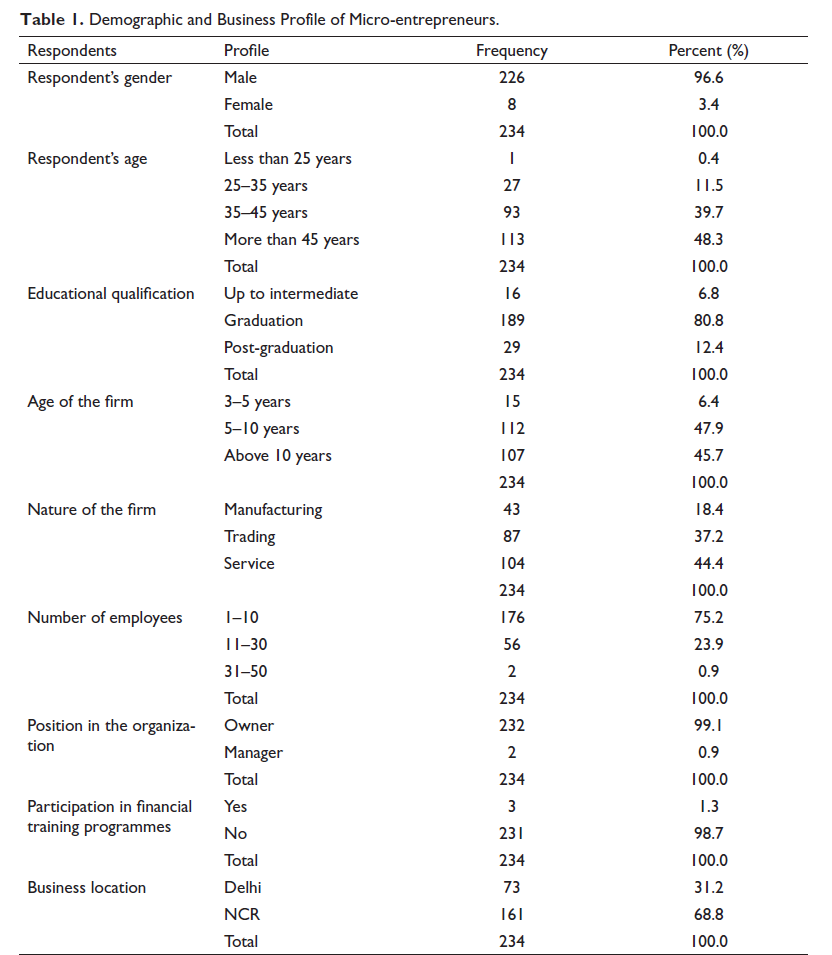

Table 1 depicts the demographic and business profile of the micro-entrepreneurs registered in Delhi-NCR. Of the 234 micro-entrepreneurs in the present study, 96.6% of the respondents were male, while 3.4% were female. Besides, 48.3% of the micro-entrepreneurs were above 45 years, 39.7% were between 35 and 45 years, 11.5% were between 25 and 35 years and 0.4% of the respondents were less than 0.4%. In addition, the findings revealed that 31.2% of registered micro-entrepreneurs were from Delhi, and 68.8% of micro-entrepreneurs were from NCR Region. 6.8% of respondents were up to intermediate, 80.8% of the respondents were graduates and 12.4% of the respondents were postgraduates. With regard to the age of the organisation, 6.4% of the firms were 3–5 years old, 47.9% micro-enterprises were 5–10 years old and 45.7% were above 10 years old. Majority (44.4%) of the micro-enterprises were from service sector, 18.4% were in manufacturing sector and 37.2% of the firms were registered as trading enterprises. The participants’ businesses spanned several industries that include the real estate, furniture, food and beverages, apparel, footwear, textiles, jewellery, restaurants, cosmetics, bakery products, travel, repairs of consumer electronics, flour milling, educational services and electricals. Around 75.2% of the micro-enterprises had employees between 1 and 10, 23.9% of firms had employees between 11 and 30 and 0.9% of the firms had employees between 31 and 50. Majority (99.1%) of the responses were filled by owners of micro-enterprises, and rest 0.9% responses were filled by managers. Merely 1.3% of the entrepreneurs had attended any financial literacy training/workshops, whereas a whopping 98.7% of the respondents did not participate in any such training. This finding calls for effective implementation of skilling programmes and other policies meant for micro-entrepreneurs. The next step is to move towards evaluating the measurement model.

Demographic and Business Profile of Micro-entrepreneurs.

Assessment of Measurement Model

Validity and Reliability

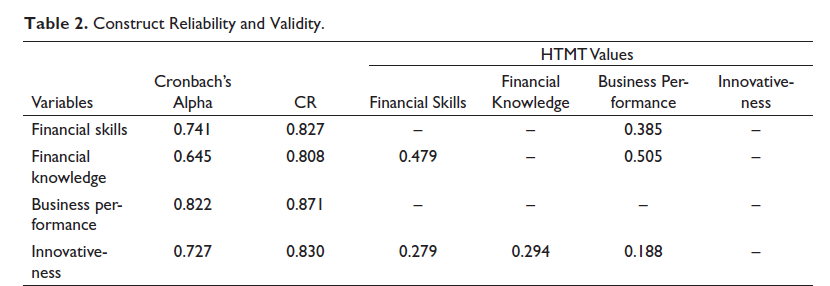

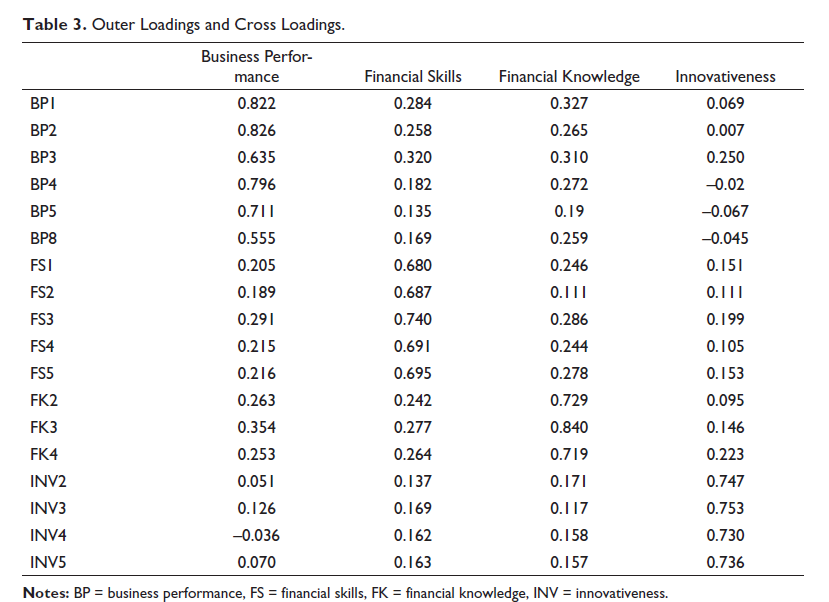

‘There is no one correct method of measuring a construct’ in social science research, and ‘measurement errors are part and parcel of social science research’ as suggested by Bandalos and Finney (2018). This study evaluated the overall measurement model through evaluating construct reliability and validity. The model in the study is reflective in nature. The authors examine convergent validity, construct reliability and discriminant validity to assess the adequacy of the latent constructs. Construct reliability in this study is measured through Cronbach’s alpha (CA) and composite reliability (CR), the recommended values for which are 0.70 in case of established research and 0.60 in case of exploratory research. Table 2 demonstrates that the values of CA and CR are above 0.60 and 0.70 for all the hypothesized constructs, respectively. Henceforth, internal consistency is achieved. Convergent validity can be evaluated by the inspection of CR and indicator factor loadings (Hair et al., 2011; Fornell & Larcker, 1981). The recommended values for the indicator factor loadings should exceed 0.7, but in empirical research, the loading factor value should be greater than 0.5 (Hulland, 1999; Purwanto & Sudargini, 2021). The results in Table 3 reveal that outer factor loadings for all the indicator items range from 0.554 to 0.840. Additionally, CR can also be considered to measure convergent validity (Hair et al., 2011), which in this study ranged from 0.808 to 0.871, establishing the convergent validity in the study. Discriminant validity in the present study is established through heterotrait-monotrait ratio (HTMT) correlation and cross loadings. When the variables in the study are conceptually distinct, the recommended HTMT values should be below 0.85 to establish discriminant validity (Hair et al., 2019; Henseler et al., 2014). In this study, all HTMT values are not above 0.85, which can be seen in Table 2; hence, discriminant validity is also established. Cross loadings values exceeded than all other cross loading values, confirming discriminant validity. The subsequent stage is to evaluate the structural model through path analysis.

Construct Reliability and Validity.

Outer Loadings and Cross Loadings.

Structural Model and Hypotheses Testing

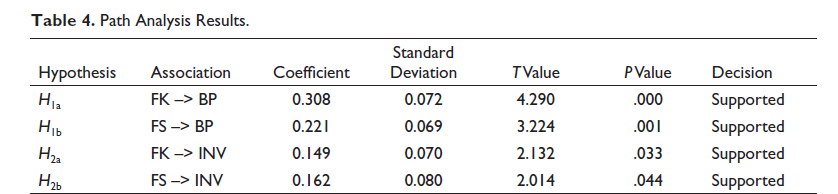

This study evaluates the inner model on the basis of significance value, R2, Q2 (predictive relevance) and multi-collinearity (Hair et al., 2017). The path analysis is depicted in Figure 2. In this study, the authors tested four hypotheses. Table 3 exhibits the path coefficients; running bootstrapping using 5,000 sub-samples at 95% confidence level was run to assess the statistical significance of each path coefficient. H1a stated that financial knowledge has a significant positive effect on the business performance (β = 0.308, t = 4.290, p < .05) as shown in Table 4. Henceforth, alternate hypothesis is accepted. Therefore, financial knowledge is a significant determinant of business performance.

Path Analysis and Hypotheses Verification.

Path Analysis Results.

H1b stated that financial skills are a determinant of business performance (β = 0.221, t = 3.224, p < .05). The results led to the acceptance of the alternate hypothesis H1b as shown in Table 4. This suggests that financial skills are a significant determinant of business performance in Delhi-NCR. The authors conclude that financial literacy (financial knowledge and financial skills) positively impacts business performance of micro-enterprises in Delhi-NCR. Thus, the more the micro-entrepreneurs are financially literate in terms of setting up a business plan, recognising the importance of time value of money, financial ratios, financial statements, setting funds for unplanned expenses, avoiding diversion of funds and working capital mismanagement, the more they can positively increase their business performance in terms of enhanced profits, revenue, sales and market size. Subsequently, it leads to sustainable business operations. The results are congruent with the past studies (Agyapong & Attram, 2019; Babajide et al., 2021; Eniola & Entebang, 2017; Julius Tumba et al., 2021; Tuffour et al., 2020; Usama & Yusoff, 2018).

Table 5 depicts the R2 value, which is 19%, concluding that the variances in the endogenous construct (business performance) can be moderately explained by micro-entrepreneur’s financial literacy (financial knowledge and financial skills) with regards to micro-enterprises registered in Delhi-NCR, as per the suggestions of Cohen (1988).

R-Square and Q-Square.

H2a tested the effect of financial knowledge on innovativeness of micro-enterprises (β = 0.149, t = 2.132, p < .05), and the findings resulted in acceptance of alternate H2a as depicted in Table 4. This can be interpreted as having adequate financial skills among micro-entrepreneurs is a determinant of innovativeness of micro-enterprises. It notes the fact that being financially aware can help an entrepreneur in utilising the financial resources in such a way that drives innovative activities critical for the survival and success of micro-enterprises.

The test of financial skills of micro-entrepreneurs as a determinant of innovativeness was tested in H2b (β = 0.162, t = 2.014, p < .05), and this lends support to H2b as shown in Table 4. Thus, the authors conclude that determinants of financial literacy (financial knowledge and skills) have a significant positive impact on innovativeness. Financial literacy among small business owners can act as a leverage to spur innovation capacity of the enterprise. Entrepreneurs have to be innovative to be competitive. The more financially literate an entrepreneur is in terms of making well-informed financial decisions, managing risk efficiently, having a fair idea of the cash flow, setting up funds for innovation during crisis and efficiently using the financial products and services instrumental in firm growth, the more the enterprise becomes innovative in terms of embracing creativity, conducting research and development, supporting new ideas from its employees and experimenting with the products and processes. This finding is congruent with the earlier studies (Campos Valenzuela et al., 2021; García-Pérez-de-Lema et al., 2021; Tian et al., 2020; Wahyono and Hutahayan, 2021).

Additionally, Table 5 shows the effect of financial literacy on innovativeness, calculated R2 value as 6.5%, suggesting that variances in innovativeness can be explained by financial knowledge and skills by just 6.5%. Although the R2 value is less than 0.1 and the effect is not very high, yet the relationship between the constructs is significant (p < .05). To avoid the multi-collinearity issues, the authors examined the variance inflation factors (VIF) values, the recommended values of which are 3.3 or lower (Kock, 2015). The VIF values can also be considered for checking common method bias (Kock, 2015). VIF values are given in Table 6, which shows that all the constructs in the inner model had VIF below 3.3, thus dismissing multi-collinearity issues and free of common method bias. Table 5 contains the Q2 values (predictive relevance), which are 0.153 and 0.039 (exceeds 0), respectively; hence, predictive relevance for both endogenous variables (business performance, innovativeness) is established. Those items whose factor loadings were below 0.5 were dropped from the study. The above-mentioned findings from the structural model establish that financial literacy of micro-entrepreneurs positively impacts their business performance and innovativeness.

Collinearity Statistics (VIF)—Inner Model.

Conclusion and Implications

The study concludes that the proxies of financial literacy, that is financial knowledge and financial skills, are the significant determinants of business performance and innovativeness with regards to micro-enterprises registered in Delhi-NCR, India. The study provided empirical evidence that having adequate financial proficiency among small business owners is critical in spurring sustainable business performance and innovativeness of firms. In a micro-enterprise, the owner does not have enough resources (be it financial, technical, managerial) at their disposal unlike their counterparts (medium enterprises) who have large pool of diverse resources, so it is of utmost importance for them to be financially proficient as they are the ultimate decision-makers in day-to-day business activities and any business decision can profoundly impact their businesses. Also, financial illiteracy among micro-entrepreneurs can have spill-over impacts in the business ecosystems as it can lead to business failures. The possession of financial knowledge, skills and attitude by small business owners can provide a competitive edge to them at different stages of the business cycle and also prepare them to function efficiently in the complex financial landscape. The empirical findings in the study expand the application of theory of RBV in the entrepreneurship studies, which contends that knowledge-based resources can give a competitive edge to entrepreneurs in improving their business performance. Given the volatile macroeconomic environment, aided by the pandemic crises, digital disruptions, financial scams, mounting non-performing assets and proliferation of sophisticated financial products and services in the financial markets, the outcome of this research work re-echoes the need of inculcation financial education among the entrepreneurs.

The findings of the study call for a collaborative approach among stakeholders including policymakers, financial institutions and entrepreneurship associations in Delhi NCR, managers to formulate, implement and execute initiatives to enhance financial literacy and innovativeness among micro entrepreneurs. Training programmes that include developing financial acumen to micro-entrepreneurs, providing them targeted counselling when facing financial challenges, hands-on training in adopting digitalisation and encouraging the participation of women entrepreneurs should be conducted by subject experts. Empowering micro-entrepreneurs through inculcating fundamental financial proficiency can make them aware of relevant financial products and services, aid them in accessing affordable and timely finance, subsequently helping them build huge business structures, that will significantly elevate the status of India globally.

Limitations and Future Research

Although the study contributes to the existing literature in manifold ways, yet it is fraught with certain limitations. First, the respondents that formed the sample were from different business types. The financial literacy level, innovation efforts and business performance vary from one sector to another, which can lead to generalisability issues. Findings would have been more consistent, had the data been collected from one particular industry. Second, the sample size is not large and data was collected from Delhi-NCR, so it may have some generalisability issues. Scholars should collect data from other geographical settings to get a better ground reality on the variables.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The authors received no financial support for the research, authorship and/or publication of this article.