Abstract

Industrial policy is witnessing a global resurgence. We propose that well-designed industrial policy must consider an industry’s regional structures, global linkages, and (variegated) exposures to geopolitical dynamics. In 2023, the UK government published a National Semiconductor Strategy. The National Semiconductor Strategy aims to grow this high-value sector, mitigate supply chain disruptions and protect national security. However, the strategy relies on an incomplete portrait of the industry’s regional geography, global integration and geopolitical exposures. Using newly available commercial data, this commentary examines 61 leading UK semiconductor firms to offer a far more comprehensive mapping of the UK’s semiconductor ecosystem than the National Semiconductor Strategy. Our analysis reveals overlooked aspects of the UK semiconductor industry. The Midlands and North West emerge as potentially under-recognised semiconductor hubs, with a significant workforce and revenue share. Heavy reliance on US suppliers, customers and investors creates vulnerabilities not addressed in the current strategy. Strong European ties exist, but Brexit-related trade barriers may harm UK firms. Last, we detect a subtle, though probably uncoordinated, pattern of Chinese investment in the sector that could expose UK firms to growing US-China tensions. We recommend that the new UK government take four steps. First, revise the National Semiconductor Strategy based on an up-to-date and systematic survey of the industry’s global linkages. Second, it will enhance its supply chain resilience strategy to address geopolitical risk and Brexit-related frictions. Third, track foreign investment patterns in high technology sectors especially regarding incremental changes in Chinese ownership. Fourth, to do so on the basis of close attention to regional clustering dynamics.

Keywords

Introduction

Turbulent economic, technological, geopolitical and climate dynamics are prompting the global emergence of a ‘new industrial policy’ (Kamin and Kysar, 2023). As states begin to pour resources into supporting private industry, they often neglect to carefully consider (1) the heterodox subnational/regional geographies of production (Johnston and Huggins, 2023); (2) how national industries are exposed to globalised supply chains and ownership structures (Smith, 2023); and (3) the growing risks to firms and industrial sectors posed by growing use of economic measures to pursue geopolitical goals (Farrell and Newman, 2023).

This commentary builds on a Digital Futures at Work (Digit) policy brief to explore these issues in the context of the UK’s evolving industrial strategy in the semiconductor industry (Rolf et al., 2024). As the foundational technology of complex modern economies, semiconductor technologies are at the forefront of this drive. For the United Kingdom, a robust semiconductor industry is essential for driving a net-zero green and digital transition, creating high-value skilled jobs and maximising opportunities for technological sovereignty. However, the industry faces formidable challenges, including vulnerability and fragility in global supply chains, rapid technological advancements requiring substantial ongoing investment, and increasing geopolitical tensions.

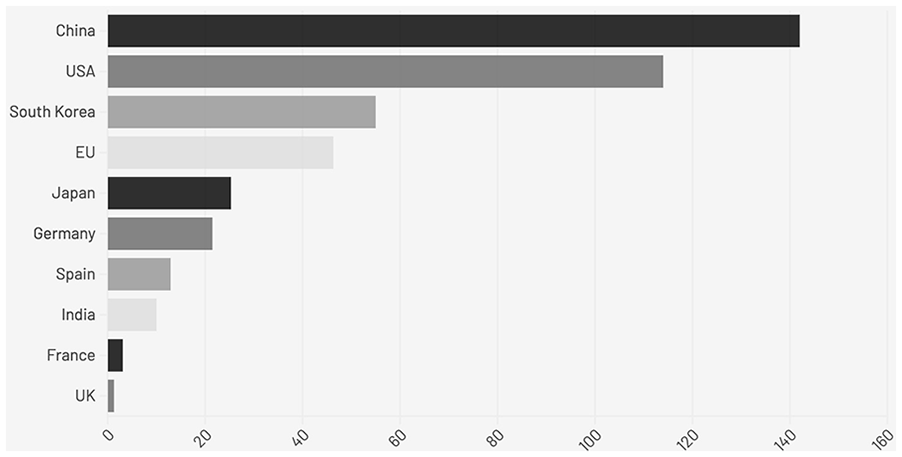

The United States and the European Union have implemented significant measures to support their semiconductor industries. The US CHIPS and Science Act commits $39 billion (plus $75 billion in loans/tax breaks) to enhance domestic semiconductor manufacturing, promote innovation and reduce dependency on foreign sources. Similarly, the €43 billion European Chips Act aims to double the EU’s global semiconductor market share to 20% by 2030 through public and private investments and establishes early warning systems for supply disruptions . China, India, South Korea and Japan have each also committed tens of billions of dollars’ worth of subsidies and other forms of support to their chip sectors (Goldberg et al., 2024).

The current UK National Semiconductor Strategy (NSS) (UK Department for Science, Industry and Technology [DSIT], 2023) is limited in comparison with the scope and scale of these initiatives (Figure 1). While the United States and EU make substantial investments to build end-to-end domestic capabilities across the entire semiconductor supply chain, the UK strategy devotes a modest £1 billion over the next decade to already existing areas of strength, in intellectual property and compound semiconductors. Measures to improve supply chain resilience are limited to issuing guidance for the sector and consultations with industry and allied countries and do not assess or address specific risks to supply chains and national security. A review of investment screening and export controls is mentioned but lags behind the more robust measures already taken by the United States and EU.

Global chip sector financial support, $bn.

The NSS aims to grow the UK semiconductor sector by leveraging existing strengths in research and development, chip design and compound semiconductors. But the success of such a highly targeted approach depends on the reliability of the underlying data. While the relative merits of other countries’ semiconductor industrial strategies can be debated, a critical distinction is that the United States and EU (among others) are investing in detailed mappings of semiconductor supply chains to inform their policies (U.S. Department of Commerce, 2024; European Commission, n.d.).

In contrast, the data sources and methodology underpinning the UK strategy are unclear. The referenced research indicates that recommendations are based on pre-existing and generic market analyses, as well as unspecified ‘close work with industry’. This approach may overlook important nuances in the sector’s geographic distribution, ownership structures and supply chain relationships, potentially leading to gaps in policy formulation. A new semiconductor sector analysis from DSIT (2024) confirms the limits of the original study supporting the NSS. The new sector analysis incorporates data on a far larger number of firms, better maps the industry’s regional structure, provides a supply chain taxonomy and provides (limited) data on UK firms’ international operations. However, the picture is far from comprehensive and significant gaps remain across all of these dimensions – particularly in terms of risks stemming from supply chain structures and foreign ownership.

Our analysis focuses on 61 leading semiconductor firms operating in the United Kingdom. Relevant companies were selected from the Fame database and the National Microelectronic Institute membership lists, with annual revenues over £10 million and with research & development (R&D) or manufacturing facilities in the United Kingdom. We incorporated ownership data from Bureau Van Dijk and Refinitiv Eikon to provide a comprehensive picture of these firms’ financial and operational structures. We also gathered detailed data on company facilities from company websites, Google Maps and job listings, as well as customer and supplier relationships from Bloomberg Professional. 1 In addition, we present data on foreign direct investment in the UK semiconductor sector.

This firm-level analysis offers new insights into the United Kingdom’s semiconductor sector and its regional distribution, depth of integration with key partners, and extent of exposures to deepening US-China trade and tech conflict. A revised NSS would benefit from such improved visibility into supply chain linkages and vulnerabilities.

Geographic distribution of industry: the need for reliable data

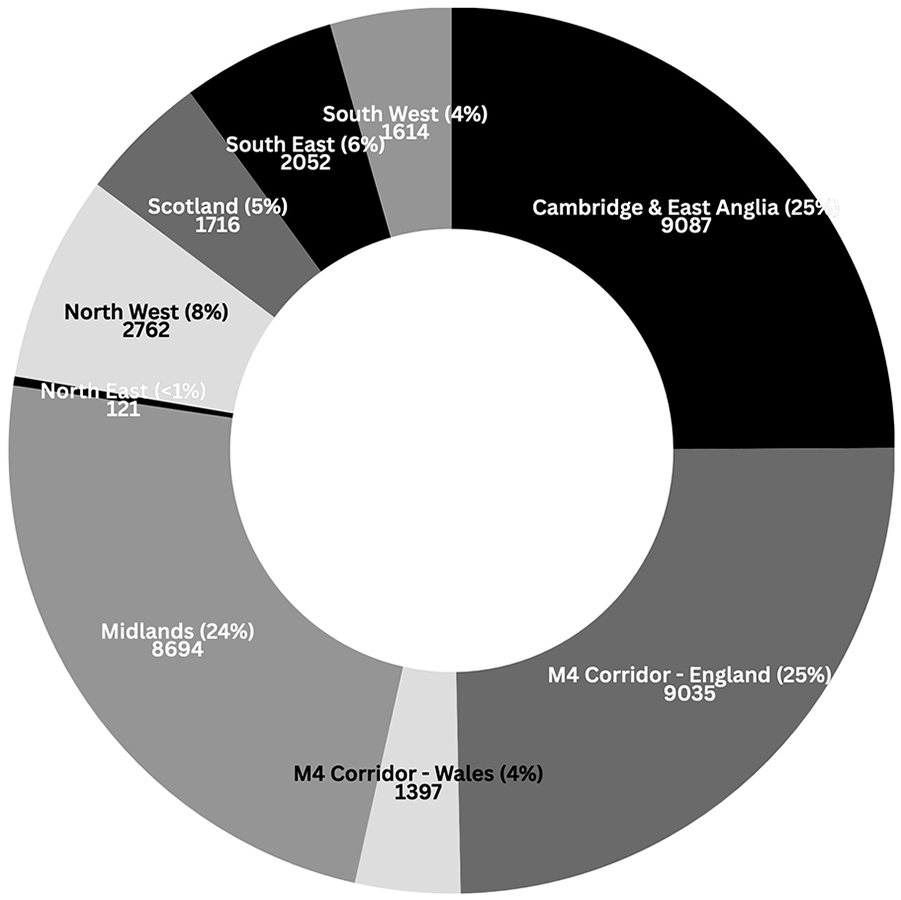

One area where the original NSS strategy may rely on an incomplete analysis of the industry landscape is its regional geography. While the NSS correctly identifies chip clusters in Cambridge, Bristol, the North East, South Wales, Scotland and Northern Ireland, it overlooks two important areas (subsequently flagged in the 2024 sector analysis): the Midlands and the North West. DSIT’s (2024) sector analysis provides much more fine-grained data, but its sample remains limited. 2

The Midlands hosts a substantial portion of the United Kingdom’s semiconductor workforce and generates a significant share of the sector’s revenue. Specifically, it accounts for 24% of jobs and 18% of revenue of the 61 major UK semiconductor firms. Moreover, with 7% of these firms’ workforce, the North West ranks fourth among UK regions for semiconductor employment, above recognised clusters like ‘Silicon Glen’ (5%) in Scotland (Figure 2).

Employment levels by major UK semiconductor firms’ main manufacturing/R&D location.

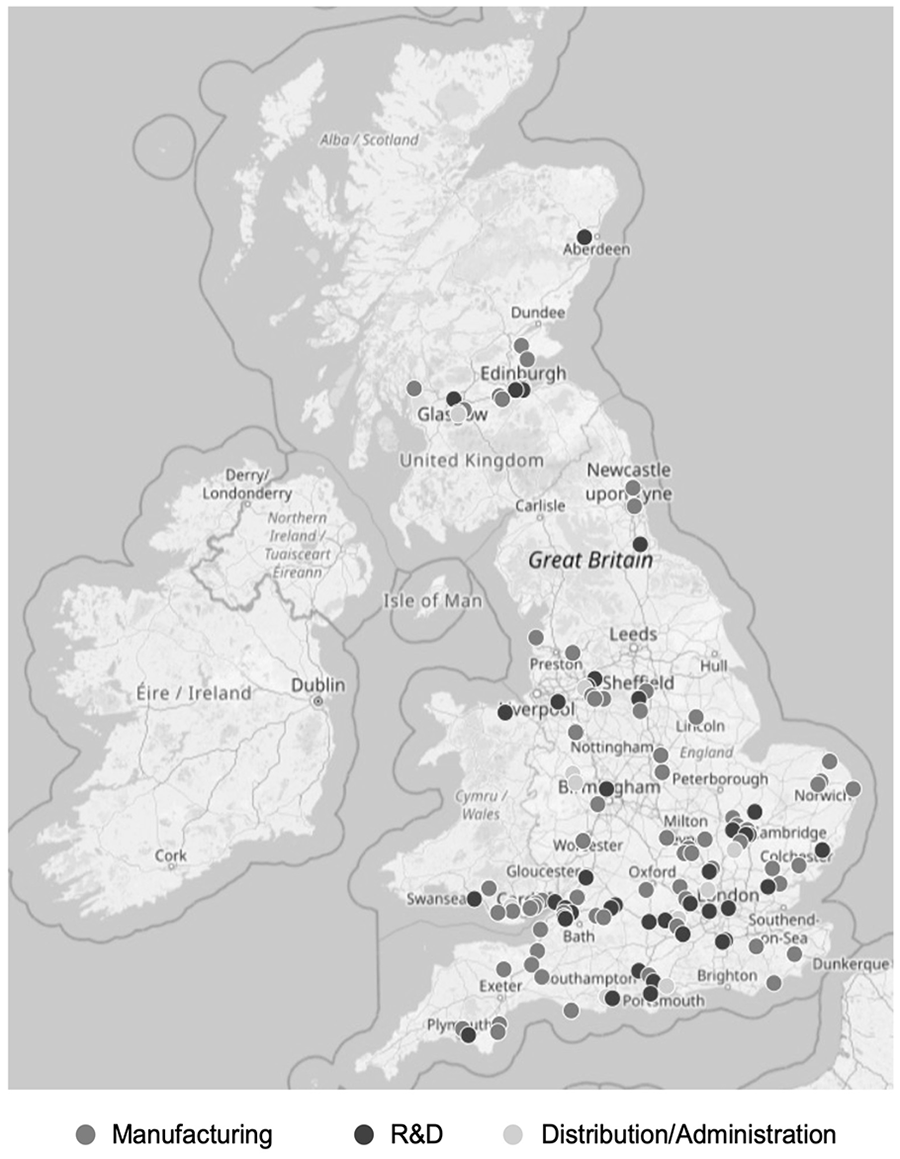

Furthermore, an in-depth look at the available facilities data of 61 major UK-based firms reveals that manufacturing and R&D are considerably more dispersed than commonly thought or acknowledged in the strategy. Significant clusters of manufacturing and R&D facilities exist in Bristol and Scotland, as noted in the strategy, but importantly they also extend to the North West – a region not mentioned in the government’s original assessment (Figure 3).

The geographic location and principal function of major UK semiconductor firms’ facilities.

Without a thorough and continually updated understanding of the entire semiconductor ecosystem and its regional distribution, the strategy risks misallocating resources and missing opportunities for growth.

Supply chain vulnerabilities: beyond Taiwan

The NSS primarily focuses on supply chain vulnerabilities related to East Asia, particularly Taiwan. While concerns about disruptions involving TSMC, Taiwan’s flagship fabrication company, are justified, our industry analysis reveals a more complex and potentially fragile supply chain landscape within which UK-based semiconductor firms are integrated. This supply chain landscape extends well beyond Taiwan to include key UK partners elsewhere.

The dominant role of the United States in UK semiconductor supply chains

Our detailed analysis of ownership patterns and supply-chain linkages makes clear the outsized role that the United States plays in the United Kingdom’s semiconductor ecosystem, which the NSS overlooks: 3

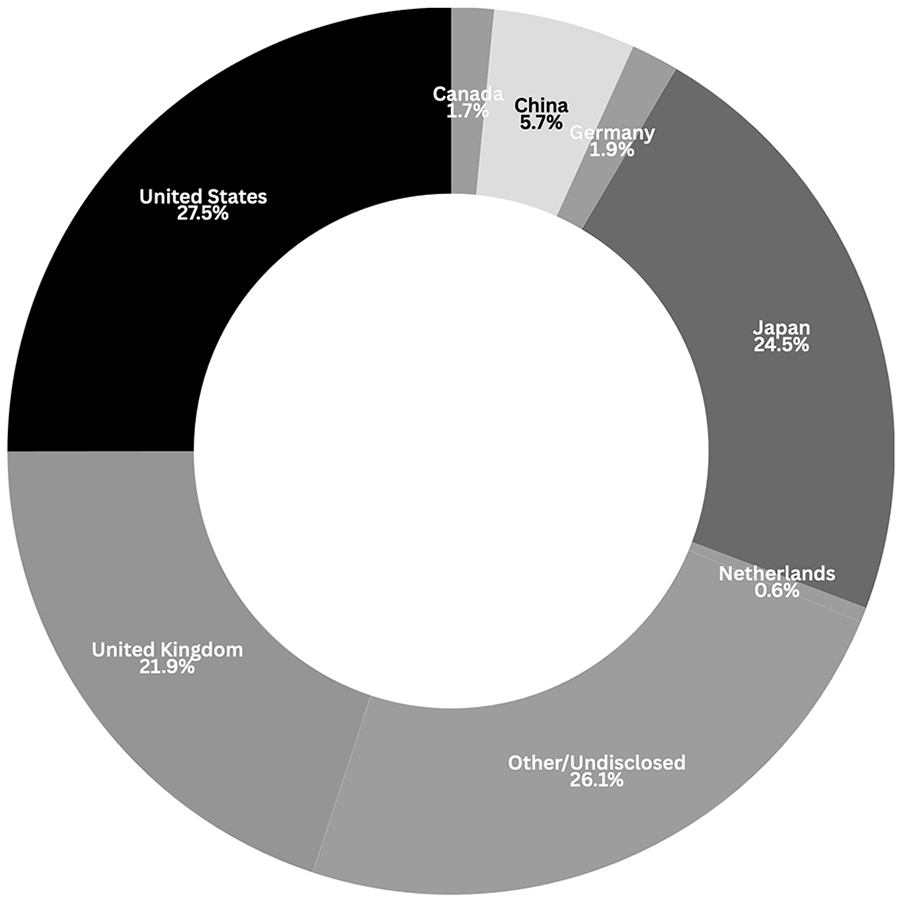

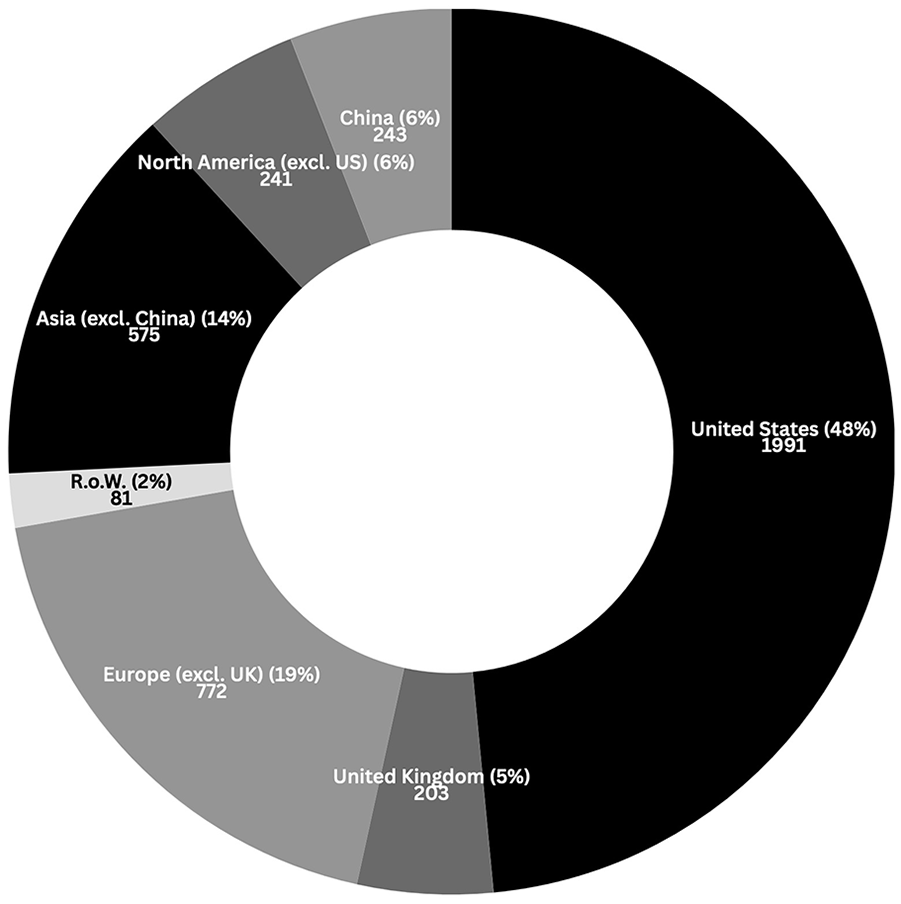

Ownership (Figure 4): US investors on average hold a 27.5% share in the 61 major semiconductors firms we examined – the largest share among foreign investors and larger than the equity share held by UK investors (21.9%).

Facilities (Figure 5): For the 17 firms with detailed data available, 48% of supplier facilities are physically located in the United States, and 51% of their customers are domiciled there.

Percentage of major UK semiconductor companies’ equity held by investors by country of domicile.

Geographic distribution of supplier facilities.

While the United States is a close ally, over-reliance on any single country – even a friendly one – can pose risks to supply chain resilience. As the US-China trade and technology conflict deepens, UK firms that heavily rely on US components and technology could be affected by US export restrictions and other measures (Germann et al., 2024). Firms such as the Netherlands’ ASML and Japan’s Tokyo Electron have already faced robust US measures targeting their business with China (Furukawa et al., 2024). Foresight over whether and how UK firms may be impacted is vital to sustain competitiveness and market access.

In view of this escalating conflict, the EU is pursuing an agenda of technological sovereignty which aims to reduce dependencies on both the United States and Asia (Poli, 2023). Given strong US bipartisan agreement to curb China’s tech advancement, the United States will likely tighten trade rules and restrict technology exports, disrupting global chip supply chains. However, the otherwise growing polarisation of US politics could lead to unforeseen, even more severe consequences – potentially crippling government functions or sparking widespread domestic unrest.

Integration with European semiconductor markets: risk and opportunity

Figure 5 also reveals that 15% of all facilities supplying the subset of 17 UK-based semiconductor companies are physically located in the EU and 19% of customers domiciled in EU member states. This substantial integration with the European semiconductor market represents both a risk and a potential opportunity that the NSS overlooks.

Brexit has introduced new supply chain vulnerabilities, including potential disruptions due to trade barriers and regulatory divergence and limiting access to skilled workers. While the United Kingdom has negotiated access to €1.3 billion in EU funds dedicated for research, development, and innovation (via the Chips Joint Undertaking), UK companies remain generally ineligible for direct funding or subsidies under the wider European Chips Act. This potentially puts them at a competitive disadvantage. While leveraging benefits from the EU’s massive new investments is possible, particularly given the United Kingdom’s geographical proximity and relative regulatory alignment, these opportunities require improved relations between the United Kingdom and EU, targeted agreements and efforts to uphold harmonised regulations.

Protecting national security: tracking foreign investment

The NSS aims to protect the United Kingdom’s national security interests in the semiconductor sector by strengthening investment screening processes for significant acquisitions and export controls for core technologies. However, analysis of ownership patterns in the UK semiconductor industry suggests a more granular and proactive approach is necessary.

Recent Chinese investment in the UK semiconductor sector has sparked controversy, such as over the 2021 acquisition of Newport Wafer Fab by Nexperia, a Dutch subsidiary of Chinese-owned Wingtech Technology. Citing the risk of technology leaks, the UK government ordered Nexperia in late 2022 to divest at least 86% of its stake in the facility, a decision that has recently been implemented with the sale to US-based Vishay Intertechnology.

Chinese ownership extends to other key players subject to similar security concerns (especially from the United States): Imagination Technologies was fully acquired by Chinese venture capital firm Canyon Bridge in 2017. In the same year, the US blocked Canyon Bridge from buying US-based Lattice Semiconductor, citing funding from Chinese state-owned enterprises and the potential transfer of intellectual property. Dynex Semiconductor Limited is wholly owned by China’s state-owned CRRC group, which has been blacklisted by the US Department of Defense since 2022 for allegedly being controlled by the Chinese military.

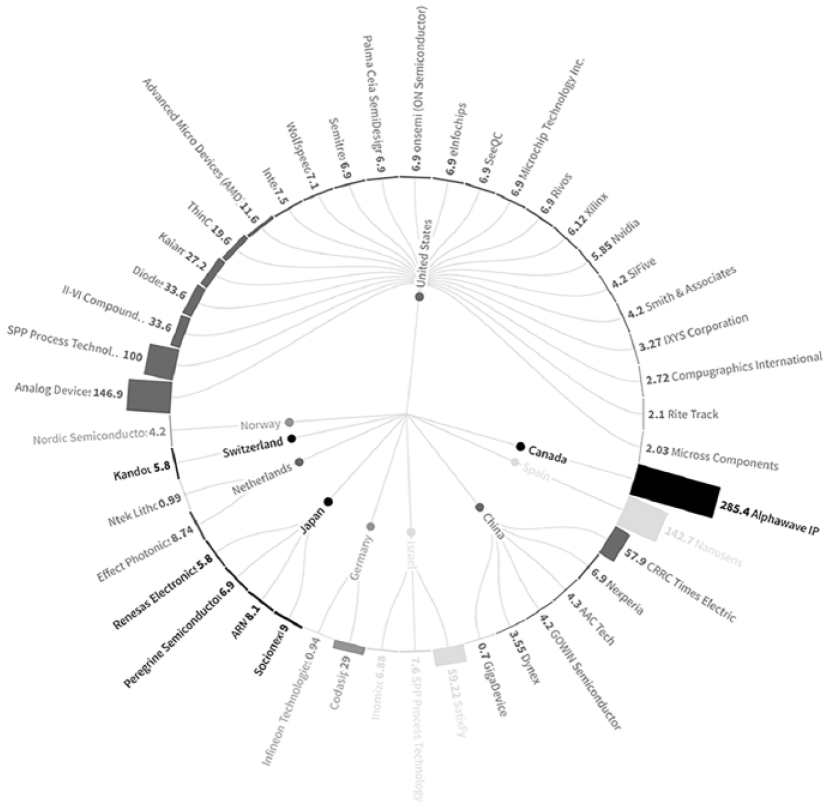

Beyond these high-profile cases, Chinese influence in the sector may be more pervasive – though not necessarily more coordinated – than is commonly understood (Figure 6). Between 2014 and 2024, Chinese firms accounted for some 7% of all greenfield investments in the UK semiconductor sector, principally in research and development. Chinese interests also permeate smaller firms below the £10 million revenue threshold of our industry analysis, such as Broadex Technologies UK Limited and eXception PCB. Scottish firm Future Technology Devices (which specialises in software and silicon for USB devices) is 80% owned by Chinese firm Dongguan Feite Semiconductor. Moreover, Huawei maintains a 3.72% stake in XMos Ltd and operates a significant R&D centre in Cambridge. Perhaps most notably, our analysis uncovered that Chinese investors hold equity positions in 36 of the 61 major UK-based semiconductor firms we examined – with the majority being stakes of under 1%, likely too small to trigger regulatory scrutiny.

Greenfield FDI projects in UK semiconductor industry by source and value (£m), January 2015–June 2024 present.

This complex web of investments underscores the importance of ongoing, careful monitoring of Chinese investment patterns and the cumulative effect of many smaller stakes across the industry. Entanglements with Chinese investors and supply chains poses risks that the United States will implement unilateral measures which damage the prospects for UK firms and the ecosystem as a whole. The case of Arm is illustrative: US export controls have forced it to restrict the sale of its most advanced chip designs to China, and to make considerable layoffs in its Chinese operations (Bohn, 2022).

Conclusion

The global return of industrial policy poses major challenges to states in the context of regionally-specialised, globally-interlinked, and (consequently) geopolitically vulnerable industrial structures which have emerged during recent decades. The UK’s National Semiconductor Strategy fails on these counts. The United States, EU and other states are not only investing heavily in bolstering their semiconductor industries, but also developing new data analytics to monitor semiconductor supply chains.

In view of such initiatives, the new UK government should revise the NSS along four lines. First, it should commission a systematic analysis of the UK semiconductor ecosystem’s global linkages, examining geopolitical risks surrounding supply chains and ownership. This survey should include detailed analyses of supply chain linkages and ownership structures. This updated analysis will enable more targeted and effective policy interventions. Second, it should broaden supply chain resilience measures beyond East Asia: Given the UK’s heavy reliance on US suppliers, customers and investors, a revised NSS should include specific measures to address potential disruptions stemming from unexpected political shifts in the United States and deepening US-China tensions. Following Brexit, the government should work on improving relations and streamlining customs procedures for semiconductor-related trade with the EU. Third, it should establish a high-technology foreign investment observatory. This should go beyond screening large acquisitions to assess the cumulative impact of multiple small investments in the semiconductor sector, particularly involving Chinese entities and considering US sanctions risks. Regular reports should be provided to relevant government bodies to inform policy decisions. Fourth, it should pay greater attention to regional clustering of the UK semiconductor industry and tailor interventions according to local economic, research, and institutional strengths (Johnston and Huggins, 2023). National economies are made up of regional industrial clusters with functional specialisations. These clusters are often differentially embedded in very different ways within global production networks (Yeung, 2021; Zhang and Peck, 2016). The UK semiconductor industry is no exception. As such, its regional clusters may be vulnerable to different kinds of geopolitical pressures and also require tailored interventions to achieve industrial upgrading.

Footnotes

Data Availability Statement

The data that support these findings are derived from commercial sources in the public domain (Google Maps, Indeed) or available from Bloomberg Professional, fDi Markets, Refinitiv Eikon and Bureau Van Dijk’s FAME databases, subject to commercial restrictions. The authors’ methods of analysis are available within the article (and outlined in the footnotes), and further clarification on our calculations is available upon request.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Steve Rolf would like to gratefully acknowledge that, as part of the Digital Futures at Work Research Centre (Digit), this work was supported by the UK Economic and Social Research Council (Grant No. ES/S012532/1).

1.

Bloomberg Professional contains data on 490,000 active buyer–supplier relationships, linking together approximately 28,000 companies. Refinitiv Eikon and Bureau Van Dijk’s FAME database contain extensive ownership and company financial data, including for private firms.

2.

Our threshold of including firms with >£10 m in revenue excludes many small and micro-sized firms that ![]() semiconductor sector analysis samples. However, DSIT’s regional analysis only considers dedicated semiconductor firms (meaning firms specialising only in semiconductors) headquartered in the United Kingdom. Most firms in its sample (109 out of 137) are micro-sized or small firms that account for only 5% of revenue and 14% of employment. Not counting Arm (which single-handedly represents 54% of revenue and 32% of employment), the study’s regional portrait is, then, largely shaped by only 18 firms. By contrast, our parameters include diversified and non-UK headquartered firms which nonetheless play an important part in the UK semiconductor industry. These lead us to examine 61 major semiconductor firms (including UK subsidiaries of foreign firms), offering arguably a more complete and balanced view of the sector’s regional geography.

semiconductor sector analysis samples. However, DSIT’s regional analysis only considers dedicated semiconductor firms (meaning firms specialising only in semiconductors) headquartered in the United Kingdom. Most firms in its sample (109 out of 137) are micro-sized or small firms that account for only 5% of revenue and 14% of employment. Not counting Arm (which single-handedly represents 54% of revenue and 32% of employment), the study’s regional portrait is, then, largely shaped by only 18 firms. By contrast, our parameters include diversified and non-UK headquartered firms which nonetheless play an important part in the UK semiconductor industry. These lead us to examine 61 major semiconductor firms (including UK subsidiaries of foreign firms), offering arguably a more complete and balanced view of the sector’s regional geography.

3.

DSIT (2024) captures the extent of UK firms’ direct operations in the United States but does not map UK firms’ third-party supplier facilities. Doing so reveals a far deeper reliance upon US producers.