Abstract

‘Patient capital’ is presented by many policymakers as a panacea to address domestic (and sometimes city-level) gaps in financing urban development, particularly housing, that emerged in the post-2008 credit crunch. In this article, we analyse the complexities of patient investors’ entry into residential markets in London and their response to the first major, and unexpected, crisis of demand: the COVID-19 pandemic and immediate falls in market demand. We focus on how patient capital and the firms invested in the professionalised rental market, build to rent (BTR), have responded. We highlight three main responses: (1) advancing their lobbying efforts to secure a more supportive political environment; (2) protecting their income streams by offering new payment plans and adaptability to prevent void rates; (3) turning to a ‘reserve army’ of renters backed by the state – so-called Key Workers (KWs). We argue these demonstrate a continual and co-evolutionary dimension to policy promoting patient capital and the need for patient planning to govern patient investment in housing systems. Our findings are in ‘real-time’ and highlight the importance of structural uncertainties and the breakdown of long-term assumptions in shaping investment decisions.

Keywords

Introduction

Utilising ‘patient capital 1 ’ has become the preferred solution for global development bodies, national governments and local authorities to address gaps in financing (urban) development that emerged in the post-2008 credit crunch. A preference for long-term investment in cities is seen as a global challenge. The United Nations (2019), for instance, now calls on governments and regulators to ‘encourage asset managers to take a long-term approach’, while acknowledging that ‘shifting capital markets to a long-term horizon is challenging’. The solution is to find, what Crouch (2013) terms ‘institutional accommodations’ to attract more institutional capital and ‘asset owners with long-term liabilities, such as pension funds’ (p. 59). Other organisations such the World Economic Forum similarly present patient capital as a type of bridging finance that can unlock longer-term commitments from investors and channel resources into the provision of (new) built environments. Traditionally associated with banks and family holdings, in the years since the Global Financial Crisis of 2008 'patience' has been used to describe the activities of expanding groups of global investors such as Sovereign Wealth Funds (SWFs) and pension funds that have become vehicles for the transfer of finance across national borders (Alami and Dixon, 2020). In relation to housing and real estate, governments and supranational bodies have positioned such forms of capital as part of the solution to long-standing housing crises (European Commission, 2018). Efforts to boost patient capital sources include reshaping planning regulations to craft new market opportunities for potential investors; the liberalisation of financial regulations and codes of conduct; and selective marketing and political lobbying campaigns.

Academic research on patient capital has primarily adopted a comparative political economy approach. Such work focuses on how labour practices, governance structures and the origins of capital influence the time-frames within which investors operate (see Deeg and Hardie, 2016, for an overview). In an urban planning context, there is growing attention to the specifics of institutional investment in real-estate markets, as both commercial and residential buildings are more widely recognised as an asset class (Van Loon 2016). Our analysis builds on these insights, going beyond investor-centred research, to develop understandings of how states are enrolled in the long-term maintenance and sustainability of investments. While there is much discussion of the regulatory fixes used to entice investors, less is written on how the needs of such capital necessitates a long-term set of commitments within and among planning systems, regulators, policymakers and citizens. The mechanisms used to sustain and enhance returns for investors, in contexts of fluctuating and unpredictable political demands and market instabilities (or crises), represent a significant challenge. As we show, there is a continual and constant co-evolution of new accommodations and fixes to deal with changing circumstances, especially in market-driven planning systems such as those found in England in which value-capture models are well advanced (Ferm and Raco, 2020).

We advance this agenda by exploring the complexities of institutional investors’ entry into residential markets in London and their response to the first major, and unexpected, crisis of demand experienced in the emerging professionalised rental market: the COVID-19 pandemic. One of the most significant consequences of attracting patient capital has been the promotion of asset classes that are particularly receptive to such investment, whether or not those investments meet defined social policy needs. We examine especially the construction of Build to Rent (BTR) units that have come to play a pivotal role in both meeting the needs of investors and planning agencies, as they generate relatively secure returns, and enable local authorities to meet visible housing targets for the delivery of new units, even if the types of units constructed fail to tackle local housing market failures. We critically examine how patient capital investors and BTR firms responded to an unexpected drop in demand by (1) advancing their lobbying efforts to secure a more supportive political environment; (2) protecting their income streams by offering new payment plans and adaptability to prevent void rates; (3) developing agreements with public agencies to identify and mobilise a ‘reserve army’ of renters backed by the state – so-called Key Workers (KWs). The category of the KW has been a fluctuating focus for housing policy since 1945 and during the Covid pandemic it has been rediscovered to cover a range of mainly (although not exclusively) public sector professionals. We show how policy agendas and new forms of marketing are used to support the investment strategies of patient capital investors and enrol the state directly and indirectly in the provision of what is ostensibly branded ‘market’ housing. Our findings highlight the importance of structural uncertainties and the breakdown of long-term assumptions, in shaping investment decisions. The shift to KWs as housing consumers exemplifies the co-dependence and co-evolution of patient capital investors and urban housing planning systems. We begin with an overview of understandings of patient capital and housing regulation before discussing the London case.

We develop the argument that while patient capital appears to provide a resolution to some of the longer-running tensions associated with the market-driven provision of housing and social policy, its capture opens up new problems and systemic challenges. Patient capital investors require long-term revenue streams, so their divestment remains a threat for housing systems and their governance. This can happen in the wake of regulatory changes (either in recipient cities or places from which the investment originates) or because of shifting markets dynamics leading to lower than expected returns. Our discussion of the early impacts of COVID-19 on housing markets in London are indicative of how investors and planners have had to adapt to ensure that market returns are constantly maintained. Reliance on such capital is therefore fraught with tensions and difficulties, requiring constant regulatory attention – what we refer to as ‘patient planning’ – if objectives are to be met in the longer term.

Supply-side dominance and the role of patient capital in the urban environment

Policy responses to the failures of housing markets in countries such as the United Kingdom have prioritised the growth of new stock and the stimulation of private supply, often through a short-term focus on deregulation and the removal of planning burdens (Gallent et al., 2017). This has been coupled with, and is partly reliant on, the shift towards a market-led planning system that institutionalises the private sector’s role in the delivery of the whole housing system (including affordable homes). The planning system’s focus on supply-side stimulation relies on assumptions around a growing and consistent demand for property, which is enrolled to attract various private sector actors to the market (Brill and Durrant, 2021; see Stirling and Purves, this issue). An increasingly important part of governing housing is the rise of new types of funding and financing that differ from traditional bank or equity funded models of development. Alternative forms of finance are brought to the market by actors and firms who see urban housing markets, particularly professionalised rental markets or BTR, as an asset class that generates sustainable and consistent (financialised) income streams (Wijburg et al., 2018), which they match against their liabilities to pension funds backing them. As Özogul and Tasan-Kok (2020) argue, there is a need to unpack different forms of investor and management practices that hide behind the much-cited ‘wall of money’ now moving in to real-estate markets (Fernandez and Aalbers, 2016; Rolnik, 2019) and to move beyond generic and/or reductionist characterisations of what this process consists of and how it is regulated.

It is in this broader context that governments and regulators at multiple scales have become increasingly focused on the attraction of what is termed patient capital; that is, capital that is less disturbed by short-term or temporary shifts in the cash flow or profitability in non-financial market activity (Deeg and Hardie, 2016). There are a broad range of investors characterised as a part of the patient capital group, most notably families with ownership control, non-financial companies with mutual shareholdings and certain types of investments by banks (see Deeg and Hardie, 2016 for a full discussion). In this article, we focus on two particular forms of patient capital: pension funds and SWFs, since these have made the biggest investments in residential property in London. Moreover, both are considered to be more ‘patient’ than other forms of patient capital (Deeg and Hardie, 2016), yet remain under-analysed within the wider discussions of both the varieties of capitalism literature and within urban planning studies (Alami and Dixon, 2020). Pension funds are understood as patient because they are highly aware of their expected outcomes – their liabilities – as well as the likely future of their income streams. This longer-term, sometimes open-ended commitment, often serves as an anchor point to ensure the delivery of projects and long-term management. Moreover, because this institutional investment represents financing for further housing supply, it enables the continuation of supply-side governance solutions to the housing system’s failure, with housing policy thus becoming increasingly dependent on encouraging investment into the development of any kind of housing in order to meet housing targets.

For global development agencies, a patient capital model exists that ‘does not have a fixed investment period and spans across the stages of development [of a product] from early phase to later stage scale-up and growth’ (Dodgson and Gann, 2018: 1). In the aftermath of 2008, capital that could provide counter-cyclical forms of investment were seen an essential feature of recovery and resilience plans (Thatcher and Vlandas, 2016). In the real-estate sector, this was especially pertinent given the role of housing in causing the financial crash. Patient capital has previously invested in commercial property, rather than residential (van Loon, 2016), but since 2008 this has shifted as governments have actively courted patient forms of capital to address the funding gaps in housing supply chains. A UK Government Panel of private sector investors in 2017, for instance, noted that a stable regulatory environment and government backing was required to make the country a more attractive location for institutional investment. Particular kinds of patient capital were seen as having the capacity to limit the negative and destabilising effects of financialisation because its corporate governance structures do not fall prey to shareholder-driven, extractive short-termism.

Patient capital also fulfils an important ideological role, underpinned by claims that their presence has the potential to overcome some of the structural tensions of governability that plague market-led planning systems. Since the mid-1990s major cities have experienced consistent demographic and economic growth, with housing markets viewed as being in crisis and unable to deliver the quantity of units necessary to meet growing demands (Pike et al., 2019). States have sought to fuel urban growth as the basis for national economic development projects, with city authorities and planners required to ‘manage’ and promote further development by freeing up their planning systems and making them market-oriented. As Jessop (2016) notes, attempts to mobilise forms of capital in the pursuit of policy objectives, such as the supply of available and affordable housing, run up against the core dynamics found in private markets – notably the need to maximise and/or maintain profitable returns. For advocates of patient capital therefore, the presence and promotion of such forms of capital appears to transcend this contradiction. It promises to allow for both a degree of private profiteering and the delivery of social goods by changing the time-frames in and through which investors can expect returns. It is for this reason that supranational development agencies and territorial governments emphasise the importance of attracting investment through regulatory accommodations that meet their needs.

However, these idealised constructions of patient capital and a ‘different’ form of investment underplays some of the structural tensions that emerge when market actors are given a pivotal role in the delivery of housing. For Jessop (2016), their presence exemplifies a broader process of displacement in which ‘governance problems appear manageable [only] because certain ungovernable features manifest themselves elsewhere’ (p. 181). As he emphasises in earlier writing ‘the logic of capital accumulation is itself inherently contradictory and dilemmatic’ and attempts to draw on institutionally diverse capital to compensate for market failures and limitations ‘neither suspends these contradictions or dilemmas nor resolves them’ (Jessop, 2002: 238). Moreover, whatever the utopian narratives that surround ‘patience’, longer-term investment, especially in real-world property markets, is inherently risky and cannot be imagined away as a feature of markets dominated by short-term investments. As a range of writers on the real-estate sector has shown, property represents a highly illiquid and risky asset in comparison with others (Baum and Hartzell, 2012; Crosby and Henneberry, 2016). Property is always subject to fluctuations in value and broader regulatory and/or market changes. This is especially true in relatively new markets like those surrounding BTR in cities (Nethercote, 2020). The lack of legal protection for renters in many cases creates short tenancy lengths (relative to commercial property) and a high degree of churn, factors in tension with institutionalised investment demands and expectations.

What also remains under-addressed is what happens when market conditions change, in this case challenging the assumed strength of demand, and how this reveals faults more broadly in this system of governing housing from a supply-side perspective. There has been little consideration in idealised policy narratives of what would happen if this demand-driven model of supply-incentive based governance was threatened, especially given the established link between crises and housing investment (see Tasan-Kok et al., 2021 this issue). The perceived and actual threats to demand associated the COVID-19 pandemic across all types of urban residential markets represents a significant test for such an approach and the latest manifestation of the ways in which market tensions impact on the objectives of both public and private sectors (Batty, 2020). In the context of actively attracting capital assumed to be patient in its approach, and therefore able to endure economic cycles without leaving a site or city such that a project falls through or is bought by investors as a ‘distressed asset’, the question of whether capital will remain long-term (or whether it can) in the face of extreme economic uncertainty is unknown. In the immediate aftermath of 2008, for instance, it was noted by critical writers that pension funds and SWFs rely heavily on ‘good weather’ periods and were unable to deal with significant downturns – a lesson that features little in subsequent idealisations of patient capital (Corpataux et al., 2009). This COVID-19 moment represents a potential shock to the models of demand certainty that underpin patient capital strategies, especially in major cities with seemingly buoyant and growing housing markets.

We now turn specifically to the case of London and its BTR sites to develop insights into contemporary forms of planning and market change. We draw from extensive analysis of London’s residential property market and its governance over the past 3 years, with a particular focus on the response of the BTR market in 2020, during the unfolding of COVID-19. We analyse interviews with over 100 real-estate professionals, including developers, investors (ranging from private equity firms to large state backed pension funds), brokers, asset managers, public officials and planners (public and private). Of these interviews, half were conducted before March 2020 and half since that date. To address how the changes happened, we re-interviewed some investors periodically over the summer and autumn of 2020. Interviews were structured around discourse analysis from their annual reports (from UK inception to 2020). Throughout this article, interviewees are referred to by their profession and are numbered in the order they were interviewed, that is, investor 7 would be the 7th investor we interviewed. In addition, we draw from participant observation at industry events (in person and then online) which focused on developing BTR markets in the United Kingdom; discourse analysis of over 300 commercial reports produced and printed by the four largest real-estate consultancies (Savills, JLL, CBRE and Knight Frank) and business newspapers, and content analysis of public policy. In what follows, we initially discuss how institutional investors in BTR responded to the perceived (and partially realised) risk induced by the COVID-19 pandemic in 2020. We then focus on the response by firms such as LGIM, Legal and General (L&G) and M&G, who we take as representative examples of patient capital in London’s residential market.

The rise of BTR and the impacts of the Covid pandemic on London’s property markets

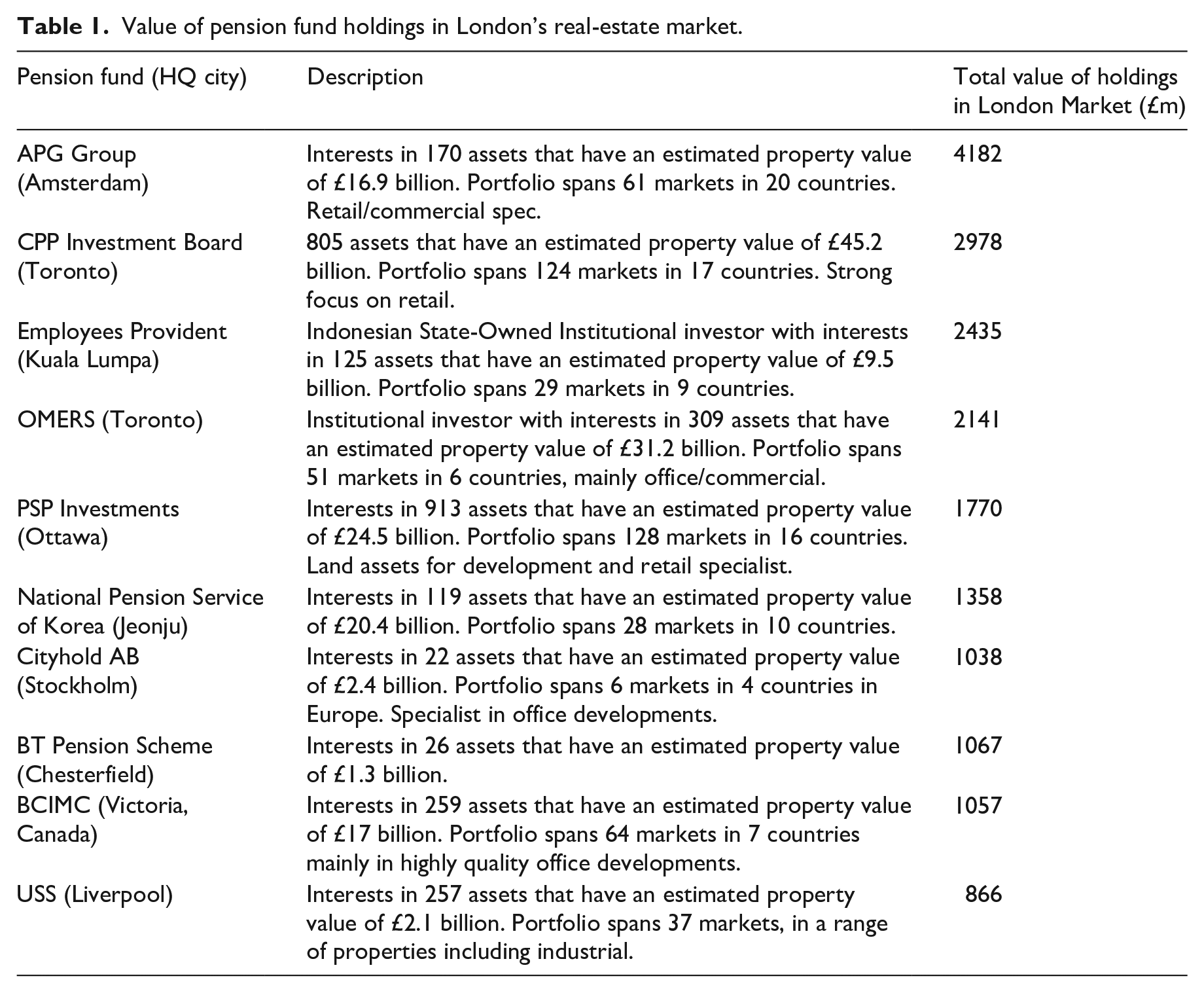

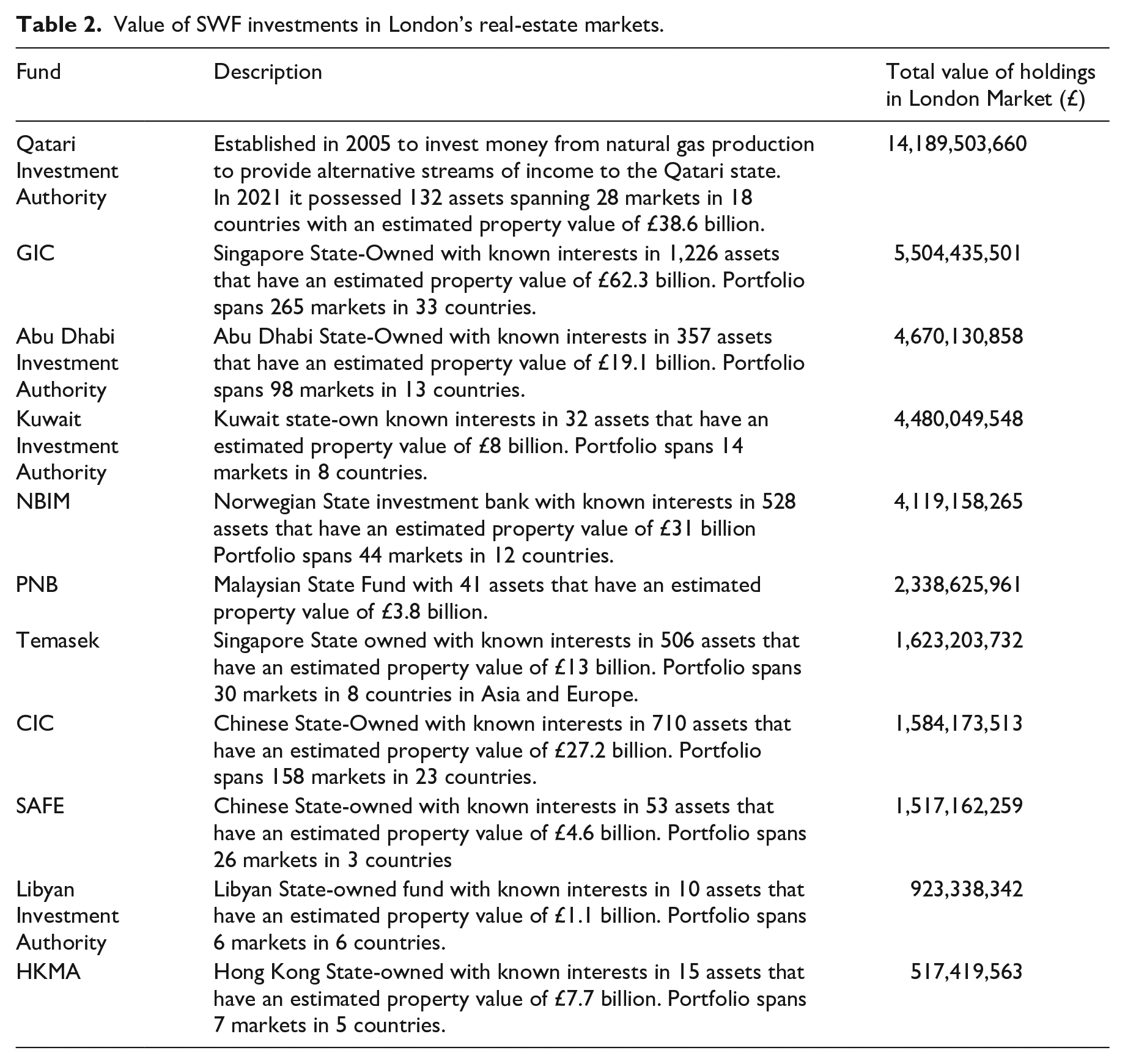

We use London as a critical case because policymakers have pioneered BTR in the city in order to facilitate patient institutional investment into the housing market to address the city’s housing problems. Since the Global Financial Crisis, efforts to attract patient capital as a whole have been relatively successful. In Tables 1 and 2 we have drawn on an analysis of data produced by Real Capital Analytics to list the top 10 pension funds investors (in 2021) in the real-estate sector in London by total value of holdings. The figures demonstrate the scope and scale of such investments but also highlight the challenges facing planners and regulators. 2 For at the same time as these forms of investment have grown, the availability and affordability of housing in the city has become a growing problem, with citizens and residents increasingly unable to access housing.

Value of pension fund holdings in London’s real-estate market.

Value of SWF investments in London’s real-estate markets.

Successive city and national governments have sought to make London’s residential sector, as an asset class, more attractive to pension funds and patient institutions. This reflects a wider policy orthodoxy around the perceived presence of a funding gap, in which indebted states are increasingly seeking private capital in the pursuit public policy ends (Pike et al., 2019). From the central government’s perspective, more investment could also address limits on the supply of housing and the failures of the private rental market in terms of poor quality and unaffordability. The private rental sector is an growing part of the housing system: it now accounts for around 20 per cent of new housing in England and 27 per cent in London. Yet the sector is often criticised for high rent-to-income ratios, low tenant rights, poor management of properties and the public realm, and for being dominated by small-scale private landlordism (Brill and Durrant, 2021; NEF, 2019). In this context of market expansion, investors have focused on BTR as an emerging asset class.

Market confidence has grown following regulatory changes outlined in a government report, the Montague Review 2012, that attempted to set out planning and financial market reforms which could elide the needs of patient, long-term investors, with emerging property market demand in cities like London (DCLG, 2012). The Review described a market, whose ‘underlying fundamentals are strong . . . and growing’ and underpinned by ‘pronounced imbalances between supply and demand’ (2012: 11). As rents across the sector, and especially in big cities, have ‘tended to rise roughly in line with real average earnings’, a degree of investor expectation has emerged that the market would be an ‘excellent match for liabilities arising in pension funds’ (DCLG, 2012). Moreover, it was claimed that an analysis of long-term returns ‘challenged the perception that yields in the sector would always be insufficient to attract investment’ (DCLG, 2012) with evidence of market trends over the previous 20 years used to show returns of 9.6 per cent, with the clear implication that future trends would follow the same path. The Review went further, calling for government to ‘share investment risk in the short term’ to boost private sector investment. Risks are thus perceived to be either political, with the risk of regulatory changes and associated compliance costs, or concerned with the supply of new sites for housing development. The report made little mention of demand risks, or even the possibility that demand for housing growth would subside in the wake of market changes. Conversely, it highlighted the certainties of future urban growth and under-supplied housing, with trend analysis used to predict the future returns and opportunities.

At the same time, in London, public policy and planning frameworks have been underpinned by a hubristic governmentality of expansion and growth, further fuelling expectations of high returns among investors. The city’s strategic planning framework, the London Plan 2021 confidently predicts that ‘London’s population is likely to continue to grow. By the 2020s there are likely to be more Londoners than at any time in the city’s history’ (paragraph 1.4). Or as the city’s long-term plan for employment predicted ‘the number of jobs in London is projected to increase from 4,896,000 in 2011 to 5,757,000 in 2036. This equates to annual average growth of just over 35,000 jobs per year and results in over 850,000 more jobs in London by 2036’ (London Enterprise Panel, 2013: 10). One way of addressing some of these challenges is to attract investment into the housing sector, especially BTR and the growth of a ‘quality’ rental sector. The Mayor’s public agencies, most notably, Transport for London, were required to use their land assets to promote development projects with BTR providers (TFL, 2020). The aim was both to generate financial returns to the public sector and instil confidence in the private market with state-backed assets underpinning the risks associated with new projects. To ensure a degree of investor longevity and commitment, the strategic planning framework, the London Plan 2021, introduced a clawback clause that ensures that BTR is held for at least 15 years. As with national-level analysis, the justification for policy development to create a supportive governance environmental for institutional investment marshals both the housing crisis, as understood as a crisis of supply, and the idea of the long-term commitment. For the Mayor, BTR forms part of meeting wider housing targets which are enrolled as a politicised measure of success during local elections, and are a governance tool for shaping the space of the city more generally.

These policy messages and initiatives have been further reinforced by private sector representative bodies, creating a cycle of narrative generation and encouraging a co-evolution between the public and private sectors. Support for BTR was justified based on both the capacity to address faults in the wider rental system and to help alleviate pressures, given the overwhelming demand, which are leveraged as a part of the lobbying efforts by the British Property Federation (BPF) and UKAA, the BTR sector’s representative body. For London-centred business actors, especially the pressure group London First, the idea of sustained population growth as an incentive to invest was front and centre of articulating the value of London’s BTR market: ‘London must significantly increase its rate of housebuilding if it is to adequately house its growing population. Failure to do so is not just a social issue: it poses a threat to the capital’s economic competitiveness’ (London First, 2019: 3). BTR in particular could act as a type of ‘asset fix’ facilitating more supply to cater for growth and finance, indirectly, for public projects. Indeed, in early interviews we carried out on London’s housing crisis, BTR as a model of housing delivery was repeatedly leveraged as an example of how further investment, particularly long-term focused patient capital, into the residential market was key in alleviating pressures in housing delivery more broadly as a part of attracting ‘talent’ for London’s businesses (Researcher 2, 2019). Designing and implementing institutional accommodations to support its growth and development should, according to business groups, be a priority for the planning system, especially in relation to urban development projects in key locations.

Across London’s real-estate industry, commercial reporting by leading consultancies reinforces the growth-centred message that there exists an insatiable demand for housing, particularly for rental property. For example, throughout the 2010s companies such as Savills (2017) have actively sought to use their research to create a market for BTR as a fundamental part of the ‘solution’ to the ‘delivery [of homes] not matching demand’ in London’s housing system. In the mid-2010s the focus was on delivering good-quality professionalised housing that attracted patient capital as a key funding source for developers, and saw the private rental market as one where units were getting smaller, more co-living and shared office space was growing and there was a great emphasis on access to transport links to get to work (Savills, 2017). In 2019, leading consultancies were all pitching BTR as an ‘exciting’ asset class for investors: something that could provide financial returns from a class of renters that were well-paid, in relatively secure positions, and looking for rental units that could be provided at high densities, with minimised construction and maintenance costs as a result of the scale and design approaches. Throughout our early interviews, there was a sense that BTR was an important part of addressing London’s affordability crisis because it would provide homes relatively quickly (Brill and Durrant, 2021).

In response, a market for BTR has emerged but its nascent nature and city location(s) meant that it was where the potential demand shock of COVID-19 was felt most keenly across the houisg system. The BTR market is made up of a mix of types of firms: some established American companies such as Greystar and Grainger entered the market through the development of their own purpose-built housing since 2012; home-grown niche firms spun out of large-scale UK consultancies such as Fizzy Living; and those backed by large-scale patient capital such as L&G, M&G and the Qatari SWF such as Get Living. The bulk of the 200,000 homes in the pipeline across the country is supported by investment from patient investors, who see the income streams as an essential liability matching device.

However, just as investments in BTR had grown to new levels, the COVID-19 pandemic hit the London market, with average rents in the centre falling by 18.3 per cent between March and June 2020 and by 8.3 per cent in the inner suburban areas (The Guardian, 2020). Trend-based research by Savills (2020b) indicated a rapid growth in workers looking for properties outside of the city and employers reassessing their commercial portfolios and requirements. Its World Cities Index also highlighted that market rates in London dropped by an unprecedented 2.4 per cent during that period (Savills, 2020a). Transactions slowed down significantly in the summer of 2020, with construction for large developments initially halted. This caused much investor anxiety among our interviewees, best exemplified by one’s claim that ‘nobody anticipated this kind of risk of Covid-19 . . . it was completely out of the blue’ (Market Economist 1, July 2020). Responding to this immediate change in circumstances was especially difficult as it corroded the models of expectation and returns that had fuelled new investments established both by market research and public policy framings.

In the immediate aftermath of the first lockdown (late summer 2020), respondents were concerned about whether London’s long-term growth was over-estimated and the impact this would have on their own strategies, especially given their 10 to 20-year time horizons and large up-front costs that had been invested over the past decade. In the months that followed, marketing events on BTR largely moved online and while the titles remained the same, for example ‘Getting into the Corridors of Power’, the threat of a demand shock was at the forefront of discussions, along with a growing focus on what housing measures could and should be taken by government to support demand, rather than opening up new sites for supply. By autumn 2020, this manifested as a core risk mitigation question for many investors, and in the months leading up the second lockdown in the winter of 2020, key actors across the BTR sector worked together with representatives such as BPF and UKAA to consolidate early political gains and put pressure on national and city governments to assist them with the threat of lower rental yields, decreased populations in city centres and high void rates.

An analysis of firm strategies and documents over this period reveals a growing concern with how government support could be used to maintain the profitability of BTR and ensure that drops in demand are mitigated through enhanced forms of direct and indirect state support. Firms such as Grainger, for instance, claim the impact of the COVID-19 pandemic on demand and the valuation of property assets had become a source of extreme risk and it was imperative that governments at multiple levels responded (Grainger, 2020: 99). Developers in London have long argued that the planning system’s requirement for them to pay a levy on their projects to provide city authorities with additional welfare finance (a form of value-capture), undermined their competitiveness and the viability of projects. The COVID-19 shock should be used to limit such payments and to adjust obligations to ensure longer-term profitability and the continued attractiveness of the sector for patient forms of capital.

These narratives were evident in interviews too, where investors who were previously emphasising the durability of their business strategies and the certainties of growth in the London market highlighted fears that were beginning to impact their ‘confidence’ in committing to further investments. There were particular concerns over unanticipated ‘void [rates] and arrears. I don’t know whether the industry is just being extremely naive or whether no one wants to talk about this at the moment’ (Investor 13, 2020). To even voice threats was seen as a potentially damaging blow to the sector’s marketing and consumer confidence. The focus of lobbying in the aftermath of the demand shock twins the housing supply narrative with the capacity of BTR to deliver: As a sub-sector of the Private Rented Sector, Build to Rent evolved out of the last global economic crisis as a new way to provide additional housing supply that was not reliant on consumer sentiment towards home sales, therefore continuing to build and support economic recovery. The same remains true today, and Build to Rent presents an opportunity for government, local authorities and industry to ensure the homes people need continue to be delivered, through expediting delivery of housing for the rental market. (BPF, 2021: 1)

The sustained emphasis on supply-side elements stands in stark contrast with the fears around a demand shock outlined above. The British Property Federation’s residential team, working alongside the UKAA, focused its narrative on the importance of institutional patient capital in sustaining residential property as a viable asset class in alignment with national economic recovery. This has been key to garnering wider government support for BTR and sustaining a supportive political environment deemed for patient capital actors: ‘just like in 2012, [patient capital] can be harnessed to support the Government’s objectives’ (BPF, 2021: 8).

In this regard, the governance of residential real-estate investment relies on the active political engagement of new forms of capital, such as more patient institutional investors. Moreover, this type of co-evolution of policy and market development speaks to the need for more long-term regulation and what we term here ‘patient planning’. The focus of planning systems to date, in terms of facilitating institutional investment, was on the moment of investment or the early stages of property development. This is a short-termist strategy that does not reflect the enduring nature of institutional investment in the market and the need for more long-term support, especially in the face of potential crises. While the government has actively endorsed patient capital as part of a post-2010 recovery plan, sustaining a supportive governance landscape in the face of both a nascent market and then a potential demand shock required BTR actors to actively engage in political action across multiple levels, often led by strategic business organisations. This action has to be both preemptive, that is, ahead of budget announcements, and rapidly reactive when policy changes that would adversely impact the market are raised. To govern the actions of investors, not just developers of housing for the for-sale market, requires recognising the different temporalities and risks actors involved in urban development work with (Brill, 2021; Geva and Rosen, this issue). As such, to govern patient capital, regulators must adopt a similar patient planning approach that reflects a long-term target and enables market regulation to mirror market attitudes towards income generating assets.

Altered corporate strategies: shifting rent collection and the reserve of renters

In this section, we show how the looming threat of a demand shock led to changes in corporate strategies in which patient capital investors sought to protect income streams by offering new payment plans and adaptability to prevent void rates. Beyond this, however, they have also relied on a turn towards a ‘reserve army’ of renters backed by the state, known as key workers – a trend that has been actively pushed by planners and government agencies across London who have rapidly redefined their priorities for housing in the wake of the COVID pandemic. These firms focus on providing space in relatively peripheral locations within the city, or at least on brownfield land where the value of the land is relatively low, to allow them to achieve sufficient economies of scale through large-scale redevelopment (DCLG, 2012). At the core is a heads on beds strategy: investors want occupation levels to be high to ensure they reduce the costs of under-occupation (such as surcharges on council tax), low levels of tenant churn because of the administrative burden of re-processing a flat and to create a sense of ‘buzz’. (Investor 6, 2019)

For example, for L&G, the focus was on ‘quality homes’. They differentiated themselves from dominant representations of poor quality buy to let landlords in the UK’s rental sector – a set of characterisations that are purposely reinforced by central government in an effort to bolster its broader drive towards the attraction of institutional investors (MHCLG, 2018). Respondents saw their long-term investments as contributing to the development of quality places and urban environments. In doing so they typically target young professionals, as they have relatively high incomes and who want to live in flats with high levels of amenities and equal-sized bedrooms.

As the threat of COVID-19 demand shock began to loom, adaptability and versatility were seen as key in managing the situation, particularly given the threat to their target market. As the BPF notes in their analysis, some companies responded by adjusting rent (plans): ‘including payment plans and rent reductions or deferrals for those tenants who have had income loss or other challenging circumstances affecting their ability to pay rent’ (BPF, 2021: 2). As noted above, vacancy or void rates are a huge risk for pension funds in particular and therefore minimising exposure to this, even if it means losing income in the short term, is key to managing the

The threat of a potential demand shock was not evenly experienced across the sector and manifested unevenly, as one investor described their changes: In London . . . we have seen a drop, for example, we have one built to rent asset in London which we have a direct exposure to and we’ve seen occupancy drop from 97 per cent during Covid-19 to 92% now (Investor 11).

For these investors, as with other prominent asset managers interviewed, there was a need to engage with and understand the underlying conditions that might drive a demand shock. The fear was that longer-term changes in working practices, such as working from home outside of urban centres, might undermine the business case for BTR investments. This was reinforced by early research in 2020 that indicated that the impact of Brexit and Covid combined had potentially led to a fall in London’s population of over half a million. For most investors the key was trying to predict how the wider macroeconomic situation would evolve: the rise in, and the potential continued rise in unemployment, particularly younger people and lower income families that generally occupy the private rented sector, is a major risk. My concern is that the almost overnight change can happen to a household’s income. It means that you’ll have someone who’s fully referenced, very happy living in one of your apartments, very easily meeting the rent and probably saving up, maybe, for a deposit for acquiring a house in the future, a flat in the future, who is no longer able to stay. (Investor 4)

Challenging this, sectoral organisations and individual firms focused on maintaining tenancies with younger people who remain unable to buy a home through flexible payment plans. This strategy appears to have been successful with firms across the city reporting relatively low void rates, although they admit in interviews that not everyone has been able to pay rent on time.

A second way in which vacancy rates have been reduced is by actively targeting those with assumed stable incomes and jobs who are less part of the demand threat: those considered KWs, and encouraging public sector agencies, such as local authorities and welfare sectors, to encourage their workers to support the sector. Within this category (which was very broadly defined at a national government level during lockdowns), investors were particularly keen to attract those with secure, stable, but modest incomes. State-backed KWs, who are directly employed by organisations such as the Civil Service or the National Health Service (NHS) quickly became what we refer here to as the ‘reserve of renters’, a group of tenants that did not feature significantly in corporate or public policy narratives around the demands for BTR pre-pandemic. Nurses were considered particularly attractive tenants because of their assumed stability and moderate incomes, making them less likely to move out of BTR units once they have moved in (Investor 4, 2019). KW have therefore become pivotal actors in making the market-investment models work, while also generating a wider political legitimacy for patient capital investment (Investor 4, 2021), with new investments presented as essential components of a wider strategy to support workers whose labour sustains key welfare infrastructure.

The history of KW housing schemes and the definition of KWs in the United Kingdom have been embedded in broader shifts in the nature of welfare reform, planning, and housing delivery. In the post-war period governments used the category of KWs to support regional policy programmes and provided housing directly to those whose presence was seen as necessary to urban and regional development (Raco, 2007). Since the 1980s, this approach has fragmented into a series of market-led piecemeal schemes of subsidised support to individuals or house-builders delivered through an un-coordinated patchwork of agencies including not-for-profit Housing Associations and/or individual local authorities or public sector employers acting to meet specific local needs. For example, the Peabody Trust in London continues to target key KW, employed by registered providers with a household income of less than £60,000 (Peabody Trust, 2020). The London borough of Kensington and Chelsea, one of London’s least affordable boroughs, similarly offers assistance to public sector KWs earning between £20,000 and £60,000.

However, in the wake of the COVID-19 pandemic, the narrative of the KW has re-emerged from a more marginal housing and spatial policy category to a widely lauded group of ‘heroes’ whose ‘essential’ work has enabled the continued functioning of social and economic systems (The Economist, 2020). This positive characterisation has been commodified by the real-estate sector, with BTR rapidly re-branded as KW-friendly, shifting the focus to their role as potential consumers. In our research, we found examples of where public agencies have started to support KW housing and to develop BTR projects, especially in regeneration areas in which earlier rounds of such investment have already taken place. There were three types of intervention that institutionalised the Mayor’s policies while also seeking to build confidence across the BTR sector.

First, some local authorities have started to channel public funds for social housing into subsidised rents in KW blocks within BTR sites, thus providing a direct connection between state spending and the investment. There is nothing new in welfare spending being used to supplement the provision of housing by private sector individuals and/or organisations. In 2019–2020, the UK government, for instance, spent over £17 billion on housing benefit – a direct payment to low income citizens to subsidise their housing costs in the private sector (Clark, 2021). In our research we traced developments across the city and analysed how their promotional material and interactions with local states had evolved. A clear example of the imprecision with which KWs was evoked, but also the importance placed on it was in a BTR development in the Borough of Waltham Forest where the local authority has provided a subsidy to enable discounted rents to 100 KWs, including nurses, doctors, teachers, police and firefighters. This site, Blackhorse Mills, is considered Legal and General’s (L&G) flagship development and the local authority have provided up to 20 per cent discount on rent for KWs. In some instances, third-sector housing associations have acted as conduits for subsidies and have focused new investments through Joint Ventures with BTR firms to provide new units for public sector workers. In our research we found evidence of long-established associations such A2Domain, who actively court KWs in sites near NHS hospitals and highlight the potential for some to access subsidised rental housing through them.

Second, in some instances, local authorities have even started to acquire and build their own BTR blocks to support both KWs and to generate demand across the sector. In the Borough of Brent the local authority has set up its own housing company to acquire existing BTR housing in regeneration areas or to finance the construction of new ones. A new BTR block utilising market-led finance has recently been constructed, housing approximately 150 KW residents. The local state’s active participation in the market establishes it as both a buyer of last resort for new blocks (from patient capital investors in need of sale) and a generator of demand in helping to establish and reproduce the sector. This is part of a broader trend in which welfare providers are now developing partnerships with local authorities and housing providers to fast-track new housing schemes, often involving BTR developments, to ensure a pipeline of new units and to maintain private sector investment in the sector. And third, the Mayor of London has promised investors that the political risks associated with new development projects will be reduced with the promise that ‘Planning guidance will be strengthened to enforce the expectation that KWs should be prioritised, with regard to local need’ (Mayor of London, 2021: 1). In echoes of post-war narratives over the importance of the presence of KWs in sustaining functioning cities and places, the Mayor will use public funds to create new markets for KWs and ensure that ‘NHS staff, police, firefighters, transport workers and teachers . . . put down roots in the capital’ (p. 1). This political commitment is important in giving potential (and existing) investors a degree of certainty in the London market.

The impacts of this support on the private sector investors and development companies that build and manage BTR developments has been significant in helping to realign existing strategies and bolster the attraction of the market for further investment. Interviewees saw the rise of KW support as an opportunity to recreate what they most desired – a stream of secure, preferably state-backed, tenants that would meet their longer-term patient models. One, for instance, noted that approximately 20 per cent of their tenants were already KWs in the wake of falls in demand from other (anticipated) sources and that this had become a core market for future expansion plans (Investor 10, 2020). What further complicates this is the under-defined nature of BTR’s role in the housing system before COVID-19, with some confusion about who the target audience was. In particular, some actors had seen their role in the wake of national and city-wide government policy that saw institutional investment as the key to the provision of more affordable rental housing. For the most part, our interviewees and contributors to industry events viewed KWs less as social or welfare actors and more as a government-backed consumer class whose enrolment could form an important part of their risk mitigation efforts in the face of a potential demand crisis. There is much less interest in building BTR housing for those defined by government as KWs in the private sector – such as delivery drivers and supermarket workers – whose work, despite their low income and precarious employment, continues to be pivotal in supporting place economies. It is the state-backed incomes that public sector workers draw on that are most attractive.

It is important to caveat these findings in two ways. First, these changes do not mark a swift departure from the dominant model of BTR provision and the role of patient capital in funding such forms of professionalised housing in London. However, they are a shift that will have a notable impact on what type of housing is provided in the rental market and for whom the housing targets. Second, the long-term impact of COVID-19 is unknown. This is true from the perspective of tenants and investors. As different companies announce their return to work policies, whether they will actively encourage workers to get back to the office and therefore re-centralise activities in to major cities such as London, or whether they will facilitate remote working more actively will heavily shape the demographic changes in London in the long run. Investors must remain attendant to these changes and how they will impact their long-term revenue streams from residential property. The governance of residential investment into housing must therefore be mindful that residential property remains a small part of most patient capital’s portfolio but that the realisation of a large demand shock, even over an extended period, will likely have major repercussions for the type of investor looking to buy, hold and sell professionally managed rental properties in London.

Conclusion

The article has used the example of BTR housing in London during the early part of the COVID-19 pandemic to explore broader questions over the governance and delivery of housing in contemporary cities. It has analysed one manifestation of a growing consensus that now dominates the agendas of supranational development agencies and national and city governments: the attraction of patient capital investment as a bridge to fix the gaps between existing funding and the construction of new housing and infrastructure. Such capital, it is claimed, is able to transcend some of the structural tensions that have plagued market-oriented forms of development planning in recent decades, in which short-term profiteering by investors has been responsible for failures in the delivery of social policy objectives.

However, we have argued that this approach represents a utopian, political-ideological framing of the efficiencies built in to market processes and how the benefits that investments bring can be (unproblematically) captured to meet social policy priorities. Drawing on patient capital for new housing appears to resolve one set of potential difficulties, but as we have shown it only displaces them to other arenas and requires new accommodations and planning arrangements to be put in place to sustain market returns. This co-evolution between regulatory systems and investment flows is significantly underplayed in policy framings that focus on the attraction of patient capital as a panacea, with the assumption that once situated in place, it will be reproduced without the need for much additional state support.

This article has analysed the reaction of patient capital actors in response to recent demand shocks. We have argued that the models of ‘patient capital’ that have driven new housing investment in BTR in cities such as London requires a continual stream of returns. Any disruption to such models, even over the short-term, has required rapid re-adjustments and a search for new strategies and models of return. While there is much rhetoric of patience, and stretched-out time-frames, the impacts of an immediate COVID-19 slowdown in interrupting incomes required rapid temporal realignments. We showed how patient capital actors and firms widened existing lobbying practices to secure a supportive political environment by tying their offering to economic recovery. Through a close examination of changing tactics at a city level we revealed how key firms have responded to the threat of a demand shock by adjusting rents and targeting KWs as the ‘reserve army’ of renters whose income are guaranteed by the state. This study offers an opportunity to analyse the ways in which particular classes or types of investors, heralded for their long-term views and associated stability, react to the threat (and potentially realisation) of a sudden change in the market condition(s). The COVID-19 demand shock made explicit some of the faults built into the UK’s market-led housing system and attempts therein to deliver policy aims through alignment with patient capital, it is critically important to understand these faults if policymakers are to navigate them as the private sector is increasingly relied on to provide solutions to the production and provision of housing globally.

For public sector planners, policymakers and planning systems, the potential threats of interruptions in expected demands also threatens established conventional wisdoms over the advantages of patient capital investment over other types. Much of the focus of policy has been on attracting patient capital to boost supply, with the assumption that once invested it will become established and take root in urban housing markets. There has been much less attention paid to how public policy also has to be ‘patient’ and to evolve alongside such investments, if stated policy objectives of creating attractive investment markets are to be met. In this sense a reliance on patient capital is little different to any form of market-oriented governance. There is a constant need to adopt measures that limit risks (to private returns) and generate market confidence so that future investors will continue to see housing and infrastructure as a market field with ongoing potential. We use the example of KWs to demonstrate one way in which public agencies have established new working relationships with patient capital investors to try to maintain demand across the sector while the sector itself relies on counter-cyclical state spending (in this example through the guaranteed employment of KWs) but there are also others. Fixes in taxation and social housing payments can also be used to maintain profitability. Here, the problems faced by investors become problems for the state, as the tensions and contradictions of market-driven systems are displaced to become planning problems (Jessop, 2016). Patient capital requires patient and continued financial and regulatory state support – both direct and indirect – in order to extract long-term and consistent financial returns from assets. Its deployment does not solve the financing and policy gap, but reinforces it as there is a need to make it work even if this only serves to displace problems. This article therefore reveals another dimension of a much wider set of trends and processes within which urban housing policies in countries such as the United Kingdom have become increasingly market-driven, with less direct provision and integrated forms of financing and control (Madden and Marcuse, 2016). The fault lines of such models of urban governance, explored here through regulator’s channelling of ‘patient capital’ into the emerging asset class of BTR housing, have been made explicit through the potential demand shock of COVID-19 and will continue to shape housing policy throughout its aftershocks.

Footnotes

Acknowledgements

This paper, in its original form asking ‘where did key workers go?’, was part of an AAG 2020 session which never happened because of the pandemic. We would like to thank those who were part of the initial panel for their continued engagement with the topics and for attending a virtual workshop in the summer of 2020. In particular, we appreciate the comments received from fellow What is Governed in Cities colleagues. We would also like to thank the reviewers for their comprehensive comments on the paper and Adrian Smith for his guidance.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This research was funded by ESRC, award number ES/S015078/1.