Abstract

It is often assumed in housing and urban studies scholarship that the roots of Sweden’s present housing discontents are to be found in a neoliberal ‘system switch’ following the early-1990s banking crisis. This paper offers a different account, identifying and expounding how insuperable contradictions in Sweden’s complex of housing production, distribution and finance, from the 1970s onward, led to a marked deterioration in its much-lauded housing model. Advancing a historical institutionalist framework, the paper seeks to historically couch the processes and outcomes commonly associated with the contemporary neoliberal era and position them more concretely in relation to actors and their social relations through time. Using a range of data pertaining to housing finance, subsidies, house prices and building output, as part of a mixed-methods analysis, the paper explores how macroeconomic factors, mediated by interactions between the state and sectoral cleavages, influence urban and regional development aspects. The paper’s conceptual and methodological relevance to housing and urban studies scholarship thus extends beyond Sweden.

Keywords

Introduction

Sweden’s housing system during the mid- to late twentieth century was very much the darling of the housing world. Attracting ‘wonder and admiration’ (Sahlin, 2008), Sweden’s social market system (Kemeny, 1995) constituted a core pillar of its much-lauded welfare state, guarded against speculation (Elander, 1991: 30) and was said be, ‘among the best measured in terms of access, cost and quality’ (Dickens et al., 1985: 49).

Following the early-1990s banking crisis – dominant scholarly accounts maintain – we witness a ‘system switch’ (Clark and Johnson, 2009: 179–180). Sweden experienced a ‘rapid transition from a regulated and subsidized, social democratic housing system to a deregulated, market-based system’ (Andersson and Turner, 2014: 4) in which ‘neoliberal politics . . . rapidly transformed the provision of housing’ (Hedin et al., 2012: 460).

Thus, the origins of many of the present-day housing discontents in Sweden (i.e. the seemingly ever-growing tendencies toward worsening housing affordability, socio-spatial inequalities, segmentation, segregation, residualisation and privatised planning) are commonly said to be found in the ‘neoliberal policies promoting marketization’ (Wimark et al., 2020), which are assumed to be the result of changes ‘in the last 20 years’ (Wimark et al., 2020).

This paper offers a different account, arguing that the roots of Sweden’s present housing discontents have a much longer pedigree than many assume. Where this account differs is in identifying insuperable contradictions in Sweden’s model of housing and finance during the 1970s and 1980s. By locating the roots of Sweden’s ‘system switch’ to the breakdown of its mid-twentieth-century housing industrial complex (Jonung, 1993), the paper seeks to historically couch the processes and outcomes commonly associated with the post-1980s era of neoliberalisation and position them more concretely in relation to actors and their social relations through time.

The paper’s focus is, significantly, the two decades preceding the early-1990s banking crisis – not the crisis or its aftermath per se – and its task is threefold. First, to illustrate how and why the post-War Swedish housing model generated contradictions which led to its deterioration from the 1970s onward. Second, to highlight how the aforementioned contradictions and subsequent deterioration of the Swedish housing model, in turn, links to – and partly explains – the process of neoliberalisation, which was manifested most keenly during the 1990s (Clark and Johnson, 2009). And third, to show how, by focusing on ‘neoliberal politics’, and the state’s agency in regulating housing therein, scholars all too often ignore the importance of finance and production in shaping micro- and meso-level urban and regional development outcomes, below the level of the nation state.

The deterioration of the Swedish housing model during the 1970s and 1980s, as detailed in the following pages, is mapped along four, interrelated vectors. First, in urban areas with high demand, an era of high inflation helped to reshape urban investor identities toward speculation in (and conversion of) the inner-city rental stock as rent gaps were identified and (in many cases) successfully closed. Second, households, using mortgage interest tax deductions, were able to borrow at negative rates, undermining an intricate system of subsidies which had been designed to be ‘tenure neutral’ and driving demand toward commodified tenure forms (reinforcing the first vector). Third, the structure of supply-side subsidies created an oversupply of rental housing in regions of low demand, leading to high vacancy rates and losses for municipal housing companies (MHCs). And, finally, a concentrated construction industry was able to mobilise ever greater power and influence over municipal authorities, in the context of intensifying regional competition and fiscal restraints.

In mapping these vectors, the paper poses a challenge to existing accounts which treat rapacious speculation within the inner-city rental housing stock; displacement of tenants through renovations and rent hikes (renovictions); sales of public housing; soaring house-price and rent inflation; burgeoning household debt; the privatisation of planning; and the deregulation of the housing and finance sectors more generally, as post-1980s novelties. Rather than contradicting this body of work, however, the analysis attempts to provide a complimentary framework, which captures the complexity of housing and finance system interactions, as well as the range of sectoral actors and interests which contribute to housing system change at various spatial scales over time.

The analysis integrates primary and secondary sources (quantitative and qualitative), both in the form of data extracted manually from Riksbank statistical yearbooks, and newspaper archives located at the National Library of Sweden’s electronic database: Svenska Dagstidningar.

Conceptually, the paper attempts to combine an analysis of how macroeconomic factors, mediated by interactions between the state and sectoral cleavages (regionally and nationally), influence urban and regional development aspects. Furthermore, it advances a lens which treats housing not as an institutionally isolated sphere, but as a complex of production, distribution and consumption (Dickens et al., 1985: 1) inextricably linked to the evolution of finance through time. I argue, in line with Rudolf Meidner, that the perceived ‘switch’ toward a neoliberal housing politics in the early 1990s, was more akin to a formal confirmation of an ongoing process rather than its cause (Meidner, 1993: 220).

The neoliberalisation of housing in Sweden. What’s missing?

The banking crisis of the early 1990s was a dual crisis of real estate and finance, producing an economic dislocation which was both steep and deep. Gross domestic product (GDP) declined for three consecutive years, private investment plummeted (Englund, 1999), commercial and residential house prices declined precipitously, and government debt soared, as the state nationalised swathes of the banking system and unemployment burgeoned.

Curiously, the lead-up to the banking crisis is seldom explicitly expounded in housing and urban studies literature pertaining to Sweden’s ostensible neoliberalisation (Christophers, 2013; Clark and Johnson, 2009), but Swedish housing is said to have been rapidly transformed in the crisis’ aftermath. Such accounts hold that Carl Bildt’s conservative-led government was responsible for dismantling the folkhem model (Wimark et al., 2020), and a line is drawn between the social democratic housing paradigm of the mid-twentieth century and the new, marketised, deregulated, post-1980s one (Andersson and Turner, 2014; Hedin and et al, 2012).

Other accounts of Sweden’s housing system transformation during the late twentieth and early twenty-first centuries are more attentive to earlier developments (Grundström and Molina, 2016), with Christophers (2013: 4) arguing that Swedish housing’s ostensible neoliberalisation began earlier than commonly acknowledged. This paper builds upon this insight but departs from Christophers in important respects.

What unites many of the above accounts is a focus on ‘neoliberal politics’, and the government’s role in regulating housing therein – what Aalbers and Christophers (2014) have termed ‘housing-as-policy’ (i.e. scholarship with a focus on policy, not markets). However, by privileging political agency, scholars, all too often, ignore pivotal changes in the spheres finance and production, and, more importantly, how said changes influence urban and regional development aspects below the level of national housing policy. As a result, the decades leading up to the banking crisis of the 1990s are largely marginalised and, instead, the aftermath and reactionary post-banking crisis reforms, such as the closure of the Department of Housing and the reduction in supply-side subsidies (Clark and Johnson, 2009: 180), become the fulcrum of analysis.

Such focus on political processes is entirely understandable and, to be sure, the reforms of the early 1990s represented pivotal changes (Christophers, 2013). However, the joint crises of housing and finance which culminated in the early-1990s banking crisis were not produced in a vacuum and in order to understand the housing discontents of the post-crisis period, we need a framework better suited to understanding changes in Sweden’s housing system in the lead-up to the crisis itself.

The build-up to this crisis has been studied by economists in great detail (Jaffee, 1994), where the centrality of financial deregulation, expansive macro policy (Englund, 1999) and poor macroprudential oversight in leading to an unsustainable housing boom (Jonung et al., 2009) are emphasised. Concepts such as neoliberalism are absent in such analyses where, instead, the boom-and-bust dynamics of the housing cycle (1985–1993) are viewed principally through a macro-financial lens, with housing generally treated as an ancillary analytical category. Instead of housing-as-policy, then, we get ‘housing-as-market’ (Aalbers and Christophers, 2014).

As will become evident in the following pages, macro-financial accounts are helpful in filling some of the gaps in the literature which focuses on housing-as-policy. However, the housing-as-market literature has a tendency to treat housing politics as a mere reflection or legitimisation of economic structures and processes. This too, is problematic.

What is missing from all of the above accounts is an integrated, politico-economic analysis of what was occurring in the main cities and regions in the two decades preceding the banking crisis. This paper advances a synthesis of the two approaches considered above – one which views the development of housing systems, and the wider urban and regional systems in which they are nested, as neither reducible to political agency nor macroeconomic restructuring per se, but as coevolving spheres whereby the underlying macro-financial milieu creates the fulcrum around which class and sectoral struggles express themselves. What such an analysis can reveal is that the regulatory and subsidy frameworks governing housing, and the financing of consumption and supply therein, had, during the 1970s and 1980s, been fatally undermined (Meidner, 1993).

Sweden’s housing industrial complex

During the post-War years, Sweden amassed what Jonung (1993) termed a ‘housing industrial complex’, underpinned by credit controls and a system of wide-reaching supply-side subsidies which were wielded toward the mass production of housing at low marginal costs (Blackwell, 2019). It was promoted and sustained by sectoral and class cleavages, and mediated by the state, in the form of the so-called Popular Movements Coalition (Gustavsson, 1980: 180), which consisted of the cooperative housing sector, the union movement, MHCs and the private construction industry (Jonung, 1993: 358).

During its peak in the early 1970s, Sweden built more housing per capita than the Soviet Union, during the Million Programme, as the housing shortages of yesteryear turned to surplus. Rigorous financial controls, supply-side subsidies, municipal planning monopolies and rationalisation, promoted by the National Housing Board (NHB), were deployed to achieve this building effort.

‘Strict demands’ regarding design, equipment and methods of construction (NHB, 1960: 131) were made under the aegis of the NHB in order that housing production assisted by state loans would be as ‘rational as possible’ (NHB, 1960). MHCs and, in particular, the housing cooperatives, pioneered standardised construction techniques, but Skånska Cement and other private construction firms rapidly gained market share. By 1970, 20 private construction firms accounted for 75% of all housing completions (Duncan, 1989: 166).

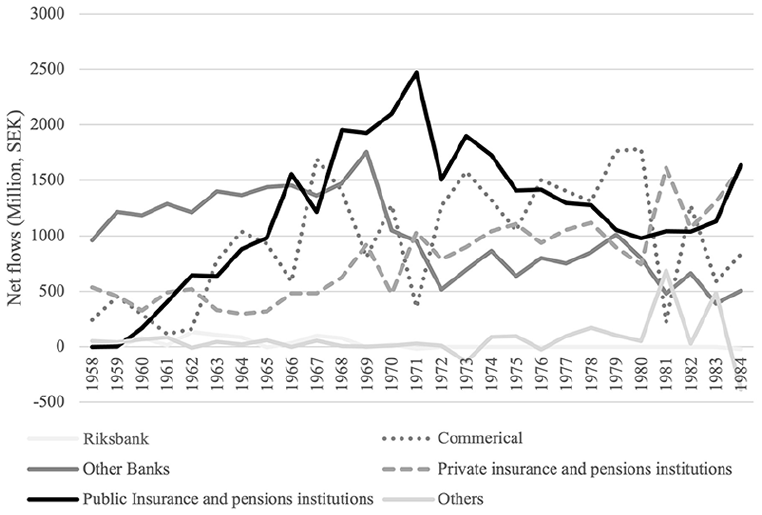

The state buttressed the creation of this complex by bolstering the supply of credit and mitigating investment risk, and this system was significantly augmented with the creation of the National Pension Fund’s Boards (AP funds) in 1960, which implied the socialisation of the nation’s savings (Jonung, 1993: 356).

The rules governing the Boards only permitted investment in fixed-income securities, and grew to become the largest investors in mortgage bonds, channelling Swedish households’ savings into housing construction on an unprecedented scale. The solid black line in Figure 1 illustrates the scale of investment.

Real net flows to housing construction on the organised credit market, 1958–1984 (1958 prices).

The AP funds were innovative instruments of capital mobilisation and state financial control and the synchronisation of credit and monetary policy was key to the facilitation of the Million Programme (Ryner, 2002: 90).

The political commitment to universality and tenure neutrality (Bengtsson et al., 2017: 74), a large public rental sector, an established national tenant movement, and a uniquely large cooperative housing sector (Bengtsson et al., 2017) coalesced with this system of regulation, finance and production to produce a ‘social democratic success story’ (Headey, 1978: 16). According to Grundström and Molina (2016: 320), ‘by the early 1970s, the entire Swedish population had obtained decent housing conditions as well as a high housing standard’.

Much has changed. Today, the rental housing shortage has reached crisis levels (Grundström and Molina, 2016) and ‘Swedish big cities have become among the most segregated in Europe’ (Sernhede et al., 2016). An affordability crisis is widely acknowledged (Lind, 2016) and, for many, Sweden’s housing system ‘palpably does not work’ (Christophers, 2013: 3).

To understand the disjuncture between Swedish housing as ‘success story’, and the perceived crisis of accessibility and affordability today, we need to trace the lineages of the present-day discontents back to the mounting contradictions within the housing industrial complex during the 1970s and 1980s. In an era of high inflation, housing consumption played a much more central role, and speculation within the existing inner-city rental housing stock flourished. By the mid-1980s, the decommodified, egalitarian system of housing, which characterised Sweden’s housing system during post-War years, had, to paraphrase Meidner (1993), been fatally undermined.

The focus on the 1970s and 1980s in this paper is warranted principally because the scholarly approaches explored above pay insufficient heed to the supply-side (construction and development) and finance – and their micro- and meso-level interactions at the urban and regional scales. This often leads scholars to rely on punctuated equilibrium models (Streeck and Thelen, 2005: 1), which ignore the actors and interests which help to shape the rules of the game.

The aforementioned accounts too often overlook core transformations and actors beyond the realm of government housing policy. In contrast, following Streeck and Thelen (2005), this analysis is attentive to the fact that ‘intuitions are not only periodically contested; they are the object of ongoing skirmishing as actors try to achieve advantage by interpreting or redirecting institutions in pursuit of their goals, or by . . . circumventing rules that clash with their interests’ (Streeck and Thelen, 2005: 18). Indeed, it is on actors’ ongoing skirmishing and the circumvention of rules at varying spatial scales that the focus of this paper lies.

Speculation in the city

The economic backdrop to the 1970s in Sweden was not as rubicund as it had been in the preceding two decades. In the era of oil price shocks, Swedish GDP growth lagged behind most Northern European economies, the current account was in deficit, and consumer prices rose more sharply than the Organisation for Economic Co-operation and Development (OECD) average in seven of the ten years of the 1970s (Caprio, 1982: 26).

This section returns to the historical record, relying on newspaper archives from the electronic Svenska Dagstidningar database to assess the impact of this macroeconomic turbulence on housing and the built environment. Searches were conducted involving key terms 1 and hundreds of newspaper articles were screened, covering a period of more than 15 years (1970–1985) as part of an iterative data collecting approach (Palinkas et al., 2015).

The mid-1970s marked the end of the Million Programme. Many argued that housing supply had been brought into balance with demand (Jaffee, 1994: 11), and an influential Housing Committee argued that, in a balanced housing market, price and rent controls were unwarranted (Sørvoll, 2013: 161). Sweden had, it seemed, built away its housing crisis of yesteryear.

By the early 1970s, however, demand for rented, Million Programme-era apartments collapsed (Hall and Vidén, 2005: 321), while, contemporaneously, demand for suburban, single-family housing and inner-city cooperative apartments soared. It was at this time that speculation within the existing inner-city rental housing stock in Sweden’s largest cities began to flourish.

The modus operandi of speculative investors varied, but their targets were essentially the same – centrally located private rental buildings and commercial premises. From the early 1970s, real estate companies connected to the Wallenberg family, such as Drott and Providentia – with established property portfolios – reportedly began purchasing rental apartment blocks en masse in inner-city Stockholm (Boman, 1973).

During this same time, a new cohort of speculators emerged alongside the established propertied interests. Their methods varied, but most involved highly leveraged purchases of run-down inner-city real estate. One method was to purchase apartments, with a view to renovating them and increasing rents subsequently, or converting them into cooperatives (Olivecrona, 1984: 114). Another strategy involved buying up entire multi-dwelling rental buildings, reducing running costs and hiking up rents.

The latter strategy was adopted by Adam Backström (Alfredsson, 1973; Palmér, 1972, who became infamous after becoming the dominant shareholder in one of the largest real estate companies in Stockholm – Credo (Palmér, 1972). After reducing maintenance costs and increasing rents, Backström would then sell entire multi-dwelling units within short timeframes. In one such sale to municipally owned Svenska Bostäder, Backström purportedly made 2.5 million kronor in less than a year (Alfredsson, 1973).

Such activities, particularly in Stockholm, were highly profitable, and soon banks were lining up to invest in these highly leveraged acquisitions. Backström’s privately owned Presidium purchased the real estate company Mälardrott, only to sell it 10 days later to (again) Svenska Bostäder (Expressen, 1974). As part of this deal, which involved Sweden’s largest cooperative, HSB, Backström reportedly pocketed ‘100,000s of kronor in a matter of days’ (Expressen, 1974). Furthermore, to assist Svenska Bostäder and HSB in their purchase of Mälardrott’s property portfolio, Backström reportedly loaned them 5.2 million SEK (DagensNyheter, 1974). Backström had seemingly identified rent gaps in the inner-city rental stock and, curiously, it was a municipality helping him close them.

The pace of these activities continued unabated until the mid-1970s where, following political outrage, the Riksdag introduced a new acquisition law for rental buildings. Such was the extent of Backström’s inner-city dealings, that this new law became synonymous with his name (Malmström, 2011). Following this, all acquisitions of rental apartments had to be subject to the approval of local rental committees. In the short term, this curtailed speculation in rental buildings, and commercial real estate became the preferred option for investors.

Rental housing was still in the sights of city speculators, however. But instead of acting as landlords, now investors in Sweden’s largest cities would convert rental buildings into cooperatives or andelslägenheter (a tenure which functionally created a form of owner-occupation).

Peder Wallenberg, son of Swedish industrialist, Jacob Wallenberg, was allegedly an exponent of such strategies. Jacob reportedly bought several multi-dwelling rental buildings for 8.3 million SEK in 1977 in one of Stockholm’s most desirable districts (Östermalm) and subsequently gifted them to his son (Melin, 1979). Because the purchase was for ‘private use’, the Backström law did not apply. Peder then apparently carved up these multi-dwelling units and sold each apartment unit for over one million kronor (Melin, 1979). One address, Karlaplan 1 in central Stockholm, contained 11 apartments, and was established as a cooperative in 1978.

These practices soon became commonplace throughout Sweden, with households opting to collectively convert their tenancies into cooperative ownership. In 1982, a new law was passed formally allowing private rental tenants to convert their apartments into cooperatives. These conversions represented an institutionalisation of the city speculators’ modus operandi, and were soon extended to public housing. During the 1980s nearly 3% of the MHC stock was privatised (Blackwell and Bengtsson, 2021); a trend which, while little reported on at the time, would accelerate thenceforth.

Why were these speculative practices and behaviours flourishing now? The changes in rent regulations of the late 1960s and early 1970s were certainly conditioning factors. Bruksvärdessystemet, or ‘soft’ rent control system, as Turner (1997) refers to it, was phased in between 1969 and 1978, replacing the rent control system introduced during the War (Turner, 1997: 485). This system temporarily depressed rents at the national level, which made the private rental stock less attractive to prospective contractors and landlords. Regionally, however, these developments played out differently, and Backström (and others) successfully pushed through rent increases in Stockholm during this time, without recourse to renovations.

The law change allowing cooperative owners to transfer their occupancy rights without price controls in 1968, however, was even more significant. This, combined with the inflationary dynamics of the 1970s, created the perfect storm for speculation and would have a direct impact on the composition of the entire Swedish housing system. As the Director of Housing at Stockholm Municipality, Stig Johnson, pointed out in an interview in December 1973, ‘[i]nvestment in housing is among the safest that exists today . . . A better protection against high inflation would be difficult to find’ (Expressen, 1973).

The share of households living in private rental accommodation plummeted throughout the 1970s, at the same time as owner-occupation burgeoned. Cooperative ownership increased also, significantly aided by conversions of private rentals. Indeed, the cooperative share of total housing completions during the 1970s was 11% – far lower than the replacement rate. The 1970s heralded a fundamental shift. This would have implications for future housing supply, as well as the flow of subsidised finance to the Swedish housing system.

State-sponsored housing demand

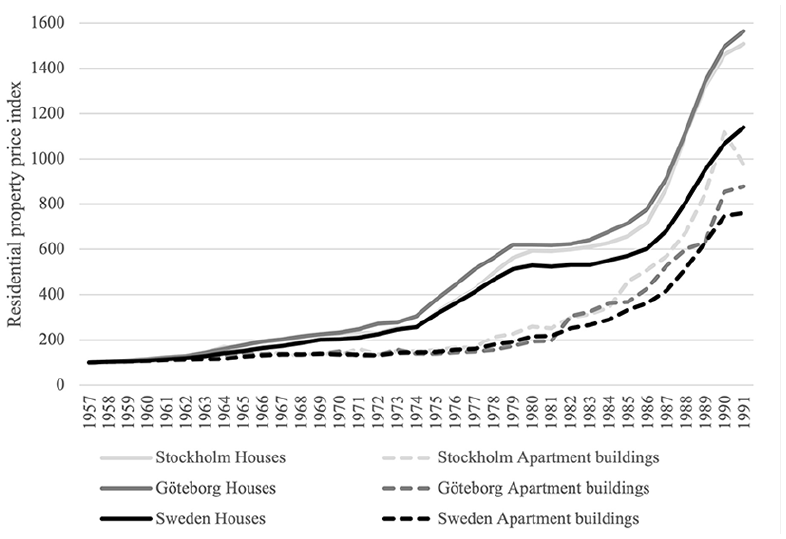

Throughout the 1970s, Swedish households had the lowest savings ratio of any of their Nordic neighbours (Berg, 1994). Equity withdrawal became more common, and house prices increased at levels not witnessed hitherto during the post-War period, reinforcing the investment trends discussed in the previous section. But what were the determinants driving the price rises observable in Figure 2?

Indices of residential property prices in Stockholm, Göteborg and Sweden, 1957–1991 (1957 = 100).

Wage growth was certainly a conditioning factor. The growth of the credit stock was also key and, from the 1970s onwards, households were amassing ever-greater volumes of debt. Levels of household debt were high even before the lifting of credit ceilings and tax reforms in the 1980s, as lenders and borrowers were increasingly able to meet outside of formal banking channels (Jonung, 1993: 364). During this time households, assisted by the banks, developed new ‘creative financing’ techniques. Sellers would ‘agree . . . not to receive the full sum demanded, but rather h[o]ld a certificate with a mortgage on [their] old house[s] as collateral’ (Boleat, 1985: 263). Banks would act as brokers in this process (Englund, 1999: 83) – not unlike Backström’s deal with Svenska Bostäder and HSB in 1973.

Swedish households became ‘among the least credit-constrained within the OECD’ (Englund, 1999: 83) and real interest rates were strongly negative throughout the 1970s (Englund, 1999), which spurred credit demand substantially. A study by Sandelin and Södersten (1978) used the following example: If a high-income household were to take a mortgage loan with a nominal interest rate of 10% when inflation was roughly 8%, then the real interest rate before tax becomes 2%. The real rate, when deducting interest payments from a marginal tax rate of 60%, then produces an after-tax interest rate of minus 4% (Sandelin and Södersten, 1978: 48). As Bergh (2014: 38) notes, the actual progressiveness of such a system (a variant of which remains today) is much lower than the marginal tax rate would imply.

Mortgage interest tax deductibility was not intended to skew incentives decidedly toward homeownership, but the system was not designed to accommodate inflationary tendencies, and, whilst the policies and institutions had remained broadly the same, the underlying macroeconomic conditions and incentive structures had changed. For middle- and high-income groups, this meant that debt-financing was incredibly attractive and, throughout the 1980s, household consumption was an important driver of GDP growth (Englund, 2015). The Social Democrats were aware that the mortgage interest tax relief system was increasingly becoming fiscally burdensome, but it was seen as ‘politically too risky’ to undermine homeowners (Bengtsson et al., 2017: 75).

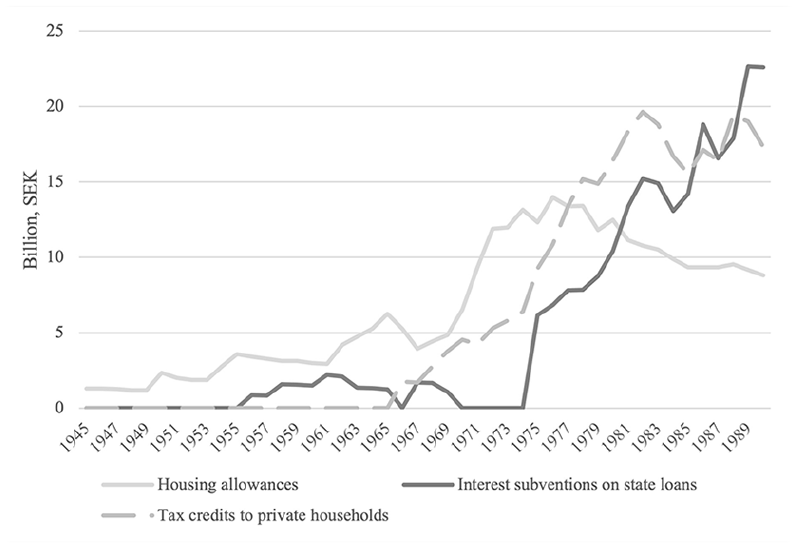

Figure 3, below, provides a summary of the evolution of state housing subsidies from 1945 to 1990. By 1980, tax credits to owner-occupiers amounted to over 40% of government housing subsidies. Swedish households were being institutionally encouraged to encumber themselves with debt.

State housing subsidies in billion SEK (1990 prices).

The state’s financial exposure to the housing system increased unprecedentedly from the 1970s onward. Ballooning mortgage interest tax deductibility, fuelled by the increased demand for owner-occupation and cooperative ownership, coalesced with the building boom and financial deregulation of the mid-1980s, leading to a phenomenal – and ultimately, unsustainable – rise in outlays.

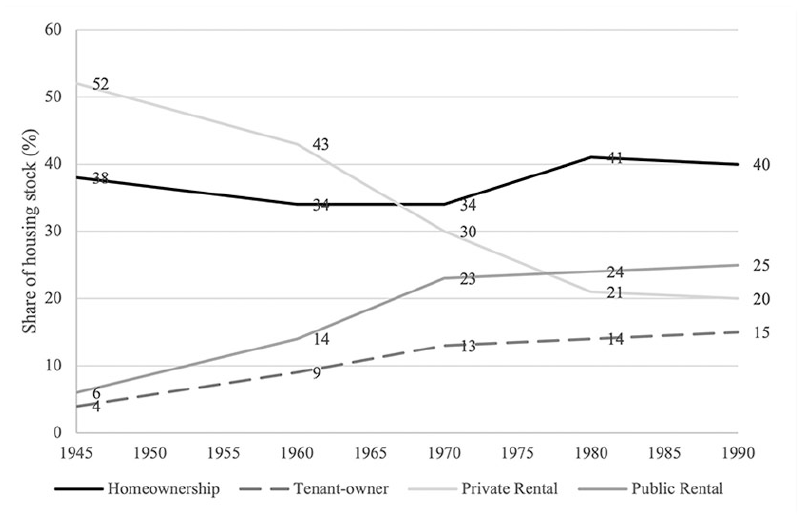

As evidenced in Figure 4, the biggest tenure shifts occurred during the 1970s. Households used tax incentives and higher wages to their advantage, and conversions of private rental accommodation to cooperatives continued apace. Further, as I explore, construction consortia and developers were having a greater say over urban development, helping to facilitate, and augment, these trends. Why do we witness no dramatic change in tenure composition during the 1980s? Chiefly because the credit that did flow into the housing system from the banks and finance companies following the financial deregulation of the early to mid-1980s served not to increase the homeownership and tenant-owner franchises, but to inflate prices (see Figure 2).

Forms of tenure in Sweden, 1945–90 (%).

Regional imbalances between supply and demand

One effect of this shift in aggregate household demand was that the number of vacant dwellings in multi-dwelling rental units soared, reaching a peak of nearly 40,000 in the early 1980s (Blackwell, 2019), of which some 40% were MHC stock (Sveriges Riksdag, 1981). Sweden was in the novel position of having too much housing, or, at least, too much of the ‘wrong’ type of housing in the ‘wrong’ place.

Even in those areas with vacant housing, new construction of both private and municipal rental units continued unabated (Wiklund, 2016) throughout the 1970s and 1980s, albeit not to the same extent as the Record Years of the Million Programme . While housing construction volumes fell in absolute terms from their early 1970s highs nationally, the increases in construction that did take place during much of the late 1970s and 1980s were in municipalities with fewer than 30,000 residents (ESO, 2002: 80).

This construction appears to have been driven neither by need nor demand and requires explanation, some of which can be understood through an analysis of construction output data. Figure 5, below, provides a regional picture of housing supply. Following Jaffee (1994), it depicts the ratio of housing completions to population growth in the 1980s in various counties in Sweden. For the purpose of this particular analysis, the analysis is restricted to regions where the population grew throughout the decade.

Housing completions/population growth (1980s).

This ratio is by no means a perfect gauge of housing supply and demand. However, when one considers the housing shortages of yesteryear were said to have been eliminated (see above), and that the headship rate (ratio of households to population) hovered around 0.45 during the 1980s in Sweden as a whole (Jaffee, 1994: 57), it becomes evident that, in all cases, the ratio of housing completions to population growth exceeded this rate and, in some cases, markedly so.

What such an analysis cannot accommodate is the even more extreme cases where the population declined over the decade. In Västernorrland County, despite a 2.5% population decline, 12,743 housing units were built, and a very similar (but less extreme) pattern played out in the counties of Norrbotten, Kalmar, Blekinge, Värmland, Västmanland and Gävleborg, leading Ola Nylander, of the National Association of Swedish Architects, to declare that: ‘Surprisingly they had caught up enough to resolve the housing crises of the past too’ (Wiklund, 2016).

The housing supply nexus and the balance of power

What explains this oversupply of housing? And why were the state, municipalities and construction companies so keen to support the steady supply of housing in areas after housing surpluses had been identified? This section explores how the changing power relations between local and national governments, the building materials industry and the construction industry impacted housing supply.

Municipal war

One answer could lie at the municipal level. Swedish municipalities have an extraordinary degree of tax-raising powers. Throughout the 1970s and early 1980s, local government taxation as a share of overall taxation was around 30% (OECD, 2017), and, today, Sweden has a municipal tax share of over 36%.

Svensson notes that ‘in the case of places to work, all authorities in principle are at war with each other, trying to obtain as many job opportunities as possible’ (Svensson, 1975: 66). Indeed, from the commencement of the Million Programme, and even more so throughout the 1980s, commercial urban development and the building of new homes was increasingly viewed as a means of encouraging inward investment, jobs and growth by municipal authorities. This was especially the case in areas and regions whose industrial base had become obsolete (Svensson, 1975).

The principle of local autonomy vis-à-vis municipal planning and land use meant that it was principally for municipalities to decide how land was to be used and developed. While plans had to be approved by the NHB who could, in theory, supersede planning decisions, in practice this seldom happened (Svensson, 1975: 53). Given practically free rein and operating under the assumption that any investment in housing and infrastructure was necessarily sound, municipalities used their planning powers to drive residential and commercial property development. As housing construction was so heavily subsidised by the state, the short- to medium-term financial outlays and risks, particularly for MHCs, were borne principally by the central state.

Housing subsidies and perverse incentives

The impetus behind the subsidy and state loan system (which, in essence, allowed municipal housing companies and cooperatives to meet the entirety of their initial capital outlays at heavily subsidised rates) was to promote non-speculative housing construction in a time of housing shortages, and to improve housing standards (Elander, 1991).

This arrangement constituted a quid pro quo between developers, cooperatives, municipalities and the state. In return for a degree of control over what was built and where, (as well as general standards), housing providers, whether municipalities, cooperatives or private developers, would be provided with stable access to loans at subsidised rates, as well as developable land and a guaranteed market (Newman and Thornley, 2002: 209). This had been a key component to the success of the housing industrial complex hitherto.

By the late 1970s, the national housing situation that the subsidy system had been designed to ameliorate had changed beyond recognition. In such a system, with general building subsidies provided centrally, this provided perverse incentives for both municipalities and construction companies, applying, as it did, wholesale throughout Sweden.

Municipalities and developers used these subsidies to their advantage, demonstrably choosing to build in areas where land was cheaper. Warsame et al. (2010: 242) note: ‘subsidized interest rate [was] more important in regions where demand [was] weak, such as in population contracting regions, than in growing regions’. This was not sustainable, and, by the mid-1970s, several MHCs in areas of population decline were facing heavy losses, as the numbers of vacant dwellings soared.

Poor targeting of subsidies was not only a problem for new builds, however. With mounting concern about unemployment in the construction industry, the state introduced an initiative designed to promote dwelling improvement in rental and tenant-owned apartment (Boverket, 2007: 91). The so-called ‘ROT programme’ (dubbed the ‘million programme for rebuilding’) was a subsidy that made repair, conversion and extension work on rental and cooperative dwellings tax deductible, and was indicative of the state’s willingness to stimulate the construction industry in an era of low productivity growth (Boverket, 2007). However, much like the interest subsidy and state loan system, the ROT programme led, in many cases, to questionable (and expensive) investments. Renovations, which in some cases fed into rent hikes of up to 60% (Jacobson, 1986: 183), drew heavy criticism from the NHB and other consultative bodies (Boverket, 2007: 91; Elander, 1991). Elander described the programme as a social and economic ‘disaster’ for ‘vulnerable groups’ (Elander, 1991: 37), and the scope of the programme was eventually curtailed in 1988, as new production boomed (Boverket, 2007: 91).

The ascendency of construction capital

By the late 1970s and throughout the 1980s, the relationship between municipalities and developers underwent profound change. Declining tax revenues (particularly in regions of population decline) and caps on state grants created a pincer movement on municipalities.

Following the Record Years it was, increasingly, not simply the case that private developers and construction companies were awarded contracts by local authorities to build on municipal-owned land. Following the completion of the Million Programme, developers and construction firms had developed sizable land banks which would threaten the whole strategy of providing masses of cheap housing (Dickens et al., 1985: 56). Construction firms, then, were no longer simply acting as building contractors as they had previously (Barlow and King, 1992: 392). They were having a greater say over what was being built and where.

Barlow and King argue that firms were now ‘“initiating” large schemes, often on their own land, for the profitable commercial sector but with a social housing component as “bait” for the communes’ (Barlow and King, 1992: 392). The balance of power had shifted, and large private sector construction firms were increasingly ‘setting the housing agenda’ (Duncan and Barlow, 1991: 216). This was a fundamental shift in dynamics and would have enduring implications for Sweden’s housing system. What is more, it occurred much earlier than many scholars assume (cf: Clark and Johnson, 2009; Olsson, 2018).

These were curious developments, and ones the central state had, initially at least, sought to avoid. Duncan and Barlow note that, ‘in the face of increasing evidence of land assembly by large building firms’ a ‘Land Condition’ (markvillkoret) was enacted (Duncan and Barlow, 1991: 213) in order to insulate housing land from the overall land market (Duncan and Barlow, 1991). Housing production receiving subsidies would, or so the Land Condition stipulated, only take place on land released by the municipality (Vedung, 2001: 69). Yet, as Vedung argues, ‘the actual development in the targeted outcome area, when the land stipulation existed between 1974 and 1991, went in the opposite direction’ (Vedung, 2001: 70). The exception of single-family dwellings in the Land Condition can perhaps explain this trend, and also (in part) the evident shift in production. Indeed, ‘housing production on land supplied by municipal authorities decreased’ (Vedung, 2001).

It is worth noting here that, while less was being built on municipal land, municipal landholdings were still considerable by international standards, and remain so today (Caesar and Kopsch, 2018). However, construction firms were now gaining more control over the types of projects municipalities engaged with and financed, and they were also providing more of their own capital (and land) to realise these projects. As Hall notes: [A] consortium, consisting of building contractors and insurance companies, negotiates with the municipality. The consortium provides something which the municipality wants, while the municipality exploits its planning monopoly in granting generous building permits, and the insurance company takes care of the financing (Hall, 1991: 272).

The largest construction firms, from the late 1970s onwards, were attracting new sources of finance – from insurance companies, finance companies and banks – and this was changing the rules of the game vis-à-vis residential housing investment.

With increasing sectoral concentration, spiralling building costs, and new financial channels undermining the tacit quid pro quo between developers and the state, this model came under severe strain by the 1980s. A mere five companies controlled nearly 60% of building land by 1988 (SOU, 1990: 99), and the level of concentration would only increase in the construction sector, with mergers, acquisitions and vertical integrations (OECD, 1992). The housing supply nexus, throughout the late 1970s and 1980s, was being dominated by an ever-decreasing pool of highly powerful actors, and this had ramifications for housing and urban development which are still felt today.

In 1990, an official government report noted that ‘significant concentration has occurred . . . at the same time as extensive open cooperation exists between companies when bidding’ (SOU, 1990: 13). It is difficult to assess precisely the degree to which these anticompetitive behaviours impacted on public procurement or building costs. However, with this industry accounting for the most revealed and suspected cases of cartels in Sweden, and with price fixing the most common misdemeanour (Konkurrensverket, 2004: 30–40), it is difficult to imagine that industrial concentration would have had benign effects. Anas et al. (1991: 46) note that the returns on working capital in the building materials industries were abnormal during the 1980s, with the highly monopolised ready-mix concrete industry recording returns of 20% or higher. They pointedly comment that ‘price setting in this industry can defeat the purpose of cost-covering rental control’ (Anas et al., 1991: 47).

Such a degree of concentration was one means by which construction firms were able to augment their power vis-à-vis the municipalities, allowing firms to ‘manipulate production costs through increased vertical integration of the building process’ (Barlow and King, 1992: 392). With the oversupply of residential housing generated throughout the 1970s and early 1980s, then, commercial property became the most lucrative form of investment and, from the mid-1980s onwards, construction firms were increasingly able to promote this type of development, while dictating the housing agenda.

Before concluding, a brief summary of this section is warranted. This section has explored how municipalities and construction firms adjusted to the post-Million Homes era, and how confluent factors on the housing supply-side steadily eroded the quid pro quo which had sustained the housing industrial complex hitherto. I identified four main dimensions to this. First, municipalities during the 1970s and 1980s saw investments in commercial and residential property as a means of promoting regional growth and increasing the tax base. Second, the structure of state housing loans and subsidies provided compelling incentives for municipalities to draw on their land banks in order to promote commercial and residential development, irrespective of demand. Third, although, local authorities still retained their planning monopolies, their fiscal positions had weakened throughout the 1970s, and their land resources reduced relative to private land holdings. Negotiations concerning the provision of commercial property development (and the residential housing mix therein) thus occurred in the context of strained municipal finances. With dwindling resources, municipalities increasingly looked to construction consortia to finance urban development and the construction industry was increasingly able to set the development agenda. Finally, the level of concentration within the Swedish construction industry fuelled anti-competitive behaviours (Bejrum et al., 1995, in Newman and Thornley, 2002: 213). The era of mass housing programmes had come to an end.

Conclusion

This paper has interrogated a simple problem: once a state, and almost an entire financial system, as well as a domestically oriented industrial supply system, has been geared toward the mass production of housing (with all the ancillary social, political and economic nexuses which have been mobilised to realise such as system) what happens when said system reaches saturation point?

By the late 1970s, the differences between owner-occupation and cooperative ownership were largely semantic: rents were pulling away from consumer prices; house-prices were increasing unprecedentedly; the subsidy system, which had been designed to promote tenure neutrality, was subsidising owner-occupiers to ever-greater extents; housing supply was out of step with demand; speculative tycoons were buying up swathes of inner-city rental stock and displacing tenants; segregation, particularly in MHC estates, was increasing (Linden, 1989); and planning decisions were being determined, to ever larger extents, by private interests.

Why are these pre-1990s dynamics important to emphasise? Simply because they highlight the importance of positioning phenomena such as neoliberalism within their specific socio-historical and spatial contexts. Many of the tenets that can be said to constitute the neoliberalisation of housing in Sweden highlighted above existed way before the supposed ‘system switch’ of the 1990s, but this can only be appreciated if, as Streeck and Thelen note (2005: 18), one is attentive to the fact that ‘major change in institutional practice may be observed together with strong continuity in institutional structures’.

As private firms and households increasingly utilised rising asset values as collateral for further leveraged investment (Jonung et al., 2009: 18), the state’s ability to control the flow and direction of credit to housing was checked. Meanwhile, construction firms and developers were utilising their burgeoning capital reserves and land banks in order to exert ever-greater influence over planning decisions. A key component to this growing influence was the increasing concentration and anticompetitive behaviours evident in this sector, and rising building costs. New financial channels empowering both the construction industry and middle- and high-income households assisted in generating insuperable tensions and contradictions in the subsidy system. This, in turn, undermined the capacity of the state to buffer the pre-existing system of financial controls, which had been so central to the creation of the housing industrial complex.

This paper has attempted to show that rapidly expanding housing supply to meet sharp increases in demand is not without consequence. As Ball (2003: 901) notes, when a house building boom is over, all those resources have to be redirected elsewhere, which generates substantial re-adjustment costs. The quantifiable ‘costs’ during the 1970s and 1980s have been relatively easy to assess: the state’s financial support to housing, by the 1980s, was being heavily directed to the demand-side (homeowners) in the form of mortgage tax relief, and, on the supply-side, multi-dwelling rental units were built in areas where there was no commensurate level of demand.

The period under investigation was one of profound flux, in which substantive qualitative and quantitative changes on both the demand- and supply-side altered Sweden’s housing and finance systems irrevocably. The mounting contradictions generated by Sweden’s housing industrial complex led to the embryonic emergence of a palpably different system of housing production, distribution and consumption. The housing industrial complex was not succeeded by a new system overnight, and the re-adjustment costs in the wake of the Million Programme took time to filter through.

This period of interregnum would evolve quickly, and when the housing system changes explored here coalesced with changes in the constitution of finance and regulation during the 1980s, the results would be explosive. When these changes fused onto the new demand- and supply-side dynamics explored here, financial practices and modes of speculation which had been (somewhat) legislated against hitherto would, gradually, become institutionalised. Seen in this light, the 1990s ‘system switch’ becomes not so much a dissolution of the social democratic mode of regulation, but an accentuation of a path already embarked upon, supported by new financial means.

This paper has argued that many of the most profound housing and finance system changes occurred in the lead up to the early 1990s banking crisis, not its aftermath. If scholars truly want to understand today’s housing discontents – and the context of the so-called neoliberal turn in the 1990s – then they would do well to extend their time horizons, focus on a wider range of actors, and look below the level of the nation-state.

Footnotes

Acknowledgements

I thank Don Mitchell, Brett Christophers, Sebastian Kohl and Alexander Kalyukin for their engagement with the topics and themes discussed in this paper. I also extend special thanks to Samuel Knafo and Andreas Antoniades for their generous help and support, and the anonymous referees for their constructive feedback. Any errors or omissions as may exist in this paper are my own.