Abstract

This paper examines the determinants of the income share of wage earners in the non-financial, private sectors of Greece since its introduction to the Eurozone in 1999. The main outcome of the integration of Greece into the Eurozone has been the financialisation of its economy, which has been particularly influential for households since it led to the rapid rise of household indebtedness. Building on recent research which shows that financialisation shape wage bargaining outcomes, we use quarterly data from the Eurostat and demonstrate that the relative size of the FIRE sectors and the increase in household debt have been negative drivers of the wage share in Greece over the last 22 years. Our findings also suggest that the employment-tied social benefits system and tertiary education provision have also been important determinants of workers’ income share.

Introduction

This paper examines the determinants of the income share of wage earners in the non-financial, private sectors of Greece since its introduction to the Eurozone in 1999. More specifically, this paper is contributing to the growing body of research within industrial relations, sociology of work and political economy that looks at whether financialisation is negatively associated with the wage share in the non-financial sectors of the economy. Recent studies provide compelling evidence that the growing dependence of non-financial corporations (NFCs) and households on credit and other financial instruments lead to wage cuts in both advanced and emerging economies (Alvarez, 2015; Gouzoulis, 2021, 2022; Gouzoulis et al., 2023; Köhler et al., 2019; Stockhammer, 2017). On the one hand, financialised NFCs face rising financial payments and target reducing costs related to the stakeholder with the least bargaining power, which is typically workers. On the other hand, indebted workers who face high default risk are likely to avoid aggressive wage demands and/or even accept a lower wage to avoid losing their job and defaulting. This study focuses on an overlooked case study within the labour share literature: Greece throughout its integration into the Eurozone. 1

Greece constitutes an ideal example to examine the financialisation-wage share relationship for two related reasons. First, in contrast to the export-oriented economies of the EU south, the main structural change that took place in Greece as part of its integration into the Eurozone has been the rapid financialisation of its economy, and, particularly of its households via the interbank market (Varoufakis and Tserkezis, 2016). Second, Greece has experienced one of the most aggressive supply-side-oriented economic adjustment programmes in recent economic history (Kornelakis and Voskeritsian, 2014; Koukiadaki and Kokkinou, 2016; Koukiadaki and Kretsos, 2012; Tourtouri et al., 2020). Part of these programmes has to do with financial deregulation which accelerated the financialisation process.

The first contribution of this paper is to offer a historical-institutional analysis of the relationship between the size of the Finance, Insurance, and Real Estate (FIRE) sectors, the household debt-to-GDP ratio, and the income share that accrues to wage earners in private NFCs in Greece since the launch of the Eurozone in the first quarter of 1999. Our analysis also traces parallel reforms related to wage bargaining structures and welfare provisions that are relevant to wage setting. The second contribution of the paper is that, building on this historical analysis, we test econometrically whether these financialisation indicators are indeed negatively associated with the private, NFC wage share using quarterly data from the Eurostat database (1999Q1–2021Q4). Indeed, our findings demonstrate that the relative size of the FIRE sectors and the increase in household debt have been the two main negative drivers of the wage share in Greece over the last 22 years. Notably, the coefficients of both financialisation variables are substantially large and statistically significant in all cases included.

This outcome highlights that the overall financialisation of the economy but also the self-disciplining effects of household indebtedness on Greek workers have been linked to a significant loss of income for them. Our results also show that the employment-tied social benefits system and tertiary education provision have also been important negative and positive determinants of workers’ income share over this period, respectively. From a policy perspective, since empirical research on the growth-wages nexus shows that increases in the wage share have positive effects on growth in a wide range of economies including Greece (e.g. Obst et al., 2020), our findings can also inform the public policy mixture of a more equitable, wage-led growth agenda.

The remainder of this paper is structured as follows. Section two discusses the literature on the drivers of the wage share. Section three analyses how Greece’s integration into the EU and the Eurozone shaped the employer-employee balance of power with a focus on financialisation. Section four discusses the econometric methodology of this study and section five reports and discusses the main findings. Section six concludes and discusses some implications of the findings.

Drivers of the income share of wage earners: Theory and evidence

The determinants of the balance of power between employers and workers has been a key focus of a number of studies across various social sciences (Gouzoulis, 2021, 2022; Gouzoulis, Constantine, et al., 2023; Gouzoulis, Iliopoulos, et al., 2023; Bengtsson, 2014; Kristal, 2010; Stockhammer, 2017). Evidence shows that the key drivers of fluctuations in the share of income going to workers are the (de-)regulation of the labour market, changes in public welfare provision, trade openness and the financialisation of the economy. 2 It is worth highlighting that due to the dynamic and context-specific nature of the employer-employee power differentials in a society, there is no framework for the analysis of capital-labour income distribution taking into account all factors in a unified way. Instead, different theories underline the importance of different complementary mechanisms that trigger such income shifts. This section presents the key mechanisms.

Labour power resources and wage bargaining

The Power Resources Theory (PRT) has been the key framework for the analysis of income shifts between employers and workers, focusing on changes in labour market regulation, labour market conditions and public welfare provision. This framework has roots to the influential works of Stephens (1979) and Korpi (1983) 3 and its main hypothesis is that when labour market slack exists, bargaining coordination becomes more decentralised, and/or union power decreases, employers become more powerful relative to workers and can impose wage restraint easier. Several empirical studies indeed show that since the late 1970s declining union density and strike activity as well as the widespread decentralisation of wage bargaining have been strongly associated with great earnings disparity and the decline of wage shares across countries (Bengtsson, 2014; Cowling and Molho, 1982; Dell’Aringa and Pagani, 2007; Devicienti et al., 2019; Kristal, 2010; Leslie and Pu, 1996; Pontusson, 2013).

The other main resource of labour power according to PRT is related to the relationship between welfare provision and the cost of job loss. In economies with increased universal public welfare provision and unemployment benefits, the cost of losing your job is comparatively lower as the differential between the average wage and the unemployment income is smaller. Thus, such safety nets strengthen the bargaining position of workers and enable them to demand higher wages and extract a bigger share of the value added in the economy. Regarding empirical evidence, it is well-established that, typically, the more egalitarian economies have more extensive welfare states with universal coverage (Esping-Andersen, 1990). Accordingly, the global policy shift towards welfare state retrenchment and employment-tied social insurance is closely linked to rising income inequalities (Esping-Andersen and Myles, 2009).

Further, also linked to welfare provision is the issue of educational attainment. An increasing share of the population having better education translates to a rising proportion of the workforce having more transferable skills. In turn, transferable skills give workers more employment opportunities, which increases their bargaining power and, consequently, their wages (Weisstanner, 2021). Thus, at the aggregate level, improving educational attainment can help reduce income disparities between high and low-wage earners as well as increase the share of wages.

Trade globalisation, price competitiveness and the relocation threat

The question of ‘who benefits from globalisation’? is far from new. Focusing on differences between advanced and developing economies, Stolper and Samuelson (1941) argue that since the demand for workers is lower in developing economies, the movement of capital to such regions will reduce unemployment and increase wages, generating a global ‘convergence’ in wages. However, several decades past the beginning of globalisation, there is significant evidence that the rise of global value chains and enhanced capital mobility encourages relocation to developing countries due to low wages (Gereffi et al., 2005). Under these circumstances, the capital mobility-related production relocation threat has given rise to a ‘global race to the bottom’ in terms of wages, with workers in advanced and developing countries accepting decreases in wages to avoid losing their jobs (Rodrik, 1997).

Another dimension of trade globalisation that affects the bargaining power of workers is price competitiveness in the context of a currency union, like the European Monetary System. In the absence of independent monetary policy that can affect exchange rates, internal devaluation policies – despite their ineffectiveness in most cases – have become the main public policy tool to improve price competitiveness and export performance (Armingeon and Baccaro, 2012). Hence, workers who work in export-oriented industries in such economies (e.g. the European South) are likely to accept lower wages over risking suppressing exports and losing their jobs. By this logic, in an economy whose main driver of growth is the external sector – which means that the majority of the workforce works in export-oriented industries – trade openness will likely generate downward pressure on its aggregate wage share.

Overall, evidence from time series and panel data analyses demonstrate that capital account openness, trade globalisation and increased FDI flows have reduced the wage shares of both emerging and advanced economies (Gouzoulis, 2022; Gouzoulis and Constantine, 2022; Böckerman and Maliranta, 2012; Stockhammer, 2017).

Financialisation and the labour market

The financialisation of the global economy constitutes one of the most influential structural developments of the last five decades. Financialisation is an umbrella term that describes the increasing direct and indirect influence of financial institutions and goals for the non-financial parts of society, both non-financial corporations (NFCs) and households. Both parallel processes have significant effects on labour management, industrial relations systems, and the bargaining between employers and workers (Prosser, 2014). Interestingly, many recent empirical studies find that the negative effect of financialisation on the bargaining of workers has been the key driver of the ongoing decline in labour shares across countries.

Regarding corporate financialisation, there are three distinct forms of it. The first is corporatist financialisation, where firms accumulate debt to finance their real investment. Second, the rise of shareholder value orientation, where managers of listed NFCs which are owned by a diverse group of shareholders are pushed to maximise dividend payments via share buybacks funded via business loans (Lazonick and O’Sullivan, 2000). In both cases, rising financial payments commonly lead NFCs to lay off employees, cut wages, and pursue workforce casualisation to reduce costs and improve their deteriorating balance sheets (Froud et al., 2000; Thompson, 2003, 2013). This process becomes more prominent in countries with already deregulated labour market (Darcillon 2016a, 2016b). Third, several (mainly large) NFCs have diversified their investment portfolios by investing in financial assets and instruments; hence, the financial profits of NFCs as a share of their overall profits are rising (Krippner, 2005; Tomaskovic-Devey and Lin, 2011). This portfolio shift makes profitability dependent on financial returns rather than real investment; therefore, demand for labour becomes less crucial for accumulation which leads to more labour market competition and lower wage shares (Lin and Tomaskovic-Devey, 2013). In summary, as outlined by Köhler et al. (2019), the financialisation of NFCs can induce decreases in the income share of the wage earners via: (a) providing more exit options to NFCs; (ii) pushing corporate managers to rise price mark-ups as a way of passing rising financial overhead costs to their workers; and (iii) putting pressure on corporate managers to cope with increased competition on capital markets via labour costs cuts to demonstrate firm efficiency and attract investors. Econometric studies on the effects of corporate financialisation on the wage share provide concrete evidence in favour of the aforementioned hypotheses (Alvarez, 2015; Dünhaupt, 2017; Köhler et al., 2019; Stockhammer, 2017).

Beyond the financialisation of NFCs, the post-1980 financial liberalisation includes lowering collateral and income requirement for access to credit, which has given rise to the financialisation of households/everyday life. The main development this process has brought is the steep increase in household indebtedness, particularly for low-income, wage earners (Köhler et al., 2019). Sociologists of finance argue that the accumulation of debt by poorer households makes them more self-disciplined and risk-averse on the fear of defaulting on their debt (Langley, 2007; Lazzarato, 2012). This argument has direct implications for labour market decisions since indebted individuals prioritise employment stability to secure repaying their debt over being militant in their negotiations about wages and working conditions, especially in economies with deregulated labour markets (Kim et al., 2019; Wood, 2017). Accordingly, indebted employees are commonly keen to accept lower pay and work under contingent contracts to avoid conflicts with their employers which includes the risk of redundancy and, consequently, personal default. Empirical evidence suggests that personal indebtedness is strongly associated with the decline of wage shares and the rise of underemployment across many advanced and emerging economies (Gouzoulis, 2021, 2022; Gouzoulis et al., 2023; Iliopoulos et al., 2022; Karacimen, 2015; Köhler et al., 2019; Wood, 2017). 4

EU integration, financialisation and the Greek labour market

The most notable examples of wage restraint during the last decades are the cases of the southern European economies of the Eurozone, namely, Portugal, Spain, Italy and Greece (Alfonso, 2019). The decline in the income share of workers in these countries has been the outcome of reforms related to EU integration that have both direct and indirect effects. Yet, given the major structural differences between these economies before their integration into the EU and the Eurozone, wage reductions have been the result of a distinct combination of factors in each case. A particularly interesting case among them is Greece, where the main outcome of its integration into the Eurozone has been the financialisation of its economy.

In contrast to export-oriented economies, like Spain and Italy, which were already large exporters of goods and the adoption of the common currency harmed their price competitiveness, Greece has never been a primarily export-oriented economy (Kornelakis and Voskeritsian, 2014). In this respect, in the absence of heavy industry, the relocation threat was minimalistic and, thus, trade openness has not been a major driver of economic performance or labour market outcomes (Varoufakis and Tserkezis, 2016). Simultaneously, especially after the Greek crisis and the related Economic Adjustment Programmes, Greece indeed decreased the size of certain forms of public welfare and the public sector, and implemented further labour market liberalisation (Ioannou, 2013; Tourtouri et al., 2020). Yet, given that public welfare coverage has already been limited and exclusionary, and the labour market has been fairly liberalised, the wage bargaining effects of both reforms have not been comparable to the negative impact of the major structural change in the Greek economy since joining the EU: the rapid financialisation of its economy. Joining the Eurozone, allowed commercial banks in Greece to take advantage of the liquidity provided by the more homogeneous EMU financial market, increasing cheap private credit provision (Lapavitsas, 2019). This led to a sharp increase in debt held by NFCs and households, with the growth rate of the latter being higher than the former (ibid.) and with housing loans being the main component (Placas, 2021).

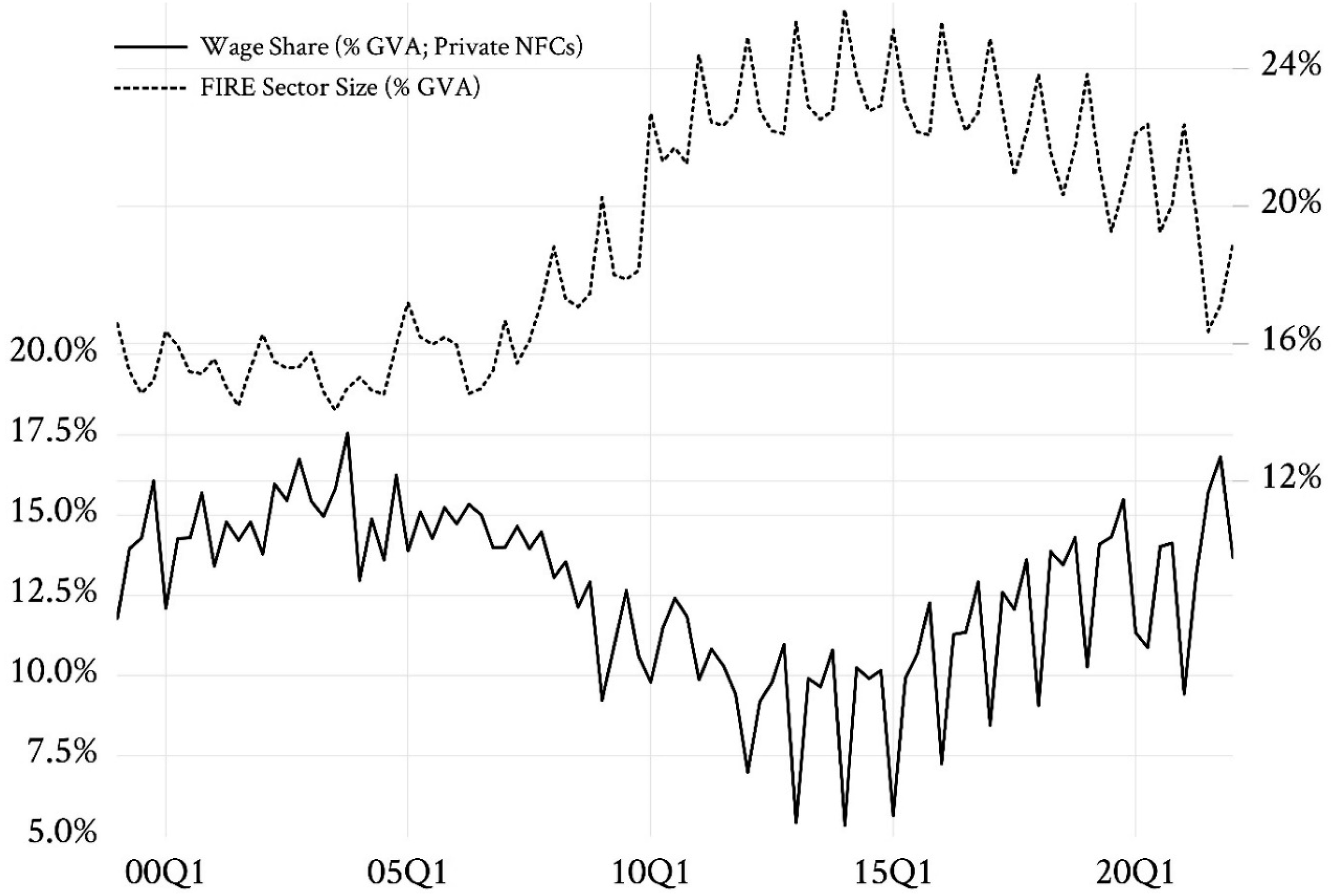

A common measure that roughly captures the overall extent of financialisation in a country is the size of the Finance, Insurance, and Real Estate (FIRE) sectors relative to the rest of the economy (e.g. see Gouzoulis et al., 2023). Therefore, given our focus on the relationship between financialisation and the labour share in Greece, Figure 1 reports the parallel evolution of the value added of the FIRE sectors (% of total value added) and the aggregated income share of wage earners in the non-financial, private sectors of the economy.

5

The period covered is from the first quarter of 1999 (the official launch of the Euro) to the last quarter of 2021 (the last data point available by Eurostat). FIRE sector size and the private, NFC wage share, 1999Q1–2021Q4. Notes. The data come from the Quarterly National Accounts of Eurostat (A*10 breakdowns). ‘FIRE Sector Size’ is the value added of the FIRE sectors as a share of the total value added. The ‘Wage Share’ is the sum of wages and salaries over the respective value added in the private, non-financial sectors of the economy (i.e. excluding [K] Financial and insurance activities, [L] Real estate activities, and [O-Q] Public administration, defence, education, human health and social work activities).

As shown in Figure 1, the negative correlation between the size of the FIRE sector size and the income share of wage earners in the Greek private NFCs between 1999 and 2021 is remarkable. From 1999 to the end of 2003, we can observe a small increase in the wage share from around 12.5% to around 16%, while the FIRE sector size remains relatively stable. During this period, Greece was governed by the centre (left) PASOK and a major construction boom took place in the context of the preparation for the 2004 Athens Olympics. The pre-2004 construction boom is important for this first stage of the financialisation of the Greek economy. In this early phase of integration into the Euro area, despite the size of the FIRE sectors expanding in real terms, the parallel growth of real sectors related to the temporary, Olympics-driven growth boom kept the relative share of the FIRE sector fairly stable until the end of 2004. Simultaneously, increased demand for labour driven by Olympics-related jobs temporarily decreased labour market slack. After the Olympics and up until the 2008 Global Financial Crisis, the wage share remained fairly stable at around 15%. The ruling party during this period, the (centre) right New Democracy, further facilitated financial integration within the Eurozone, which, combined with the contraction of value added in the NFC sectors following the 2004 Olympics, led to the beginning of the expansion of the FIRE sectors in Greece.

In 2008, Greece enters its great recession period initially triggered by the sovereign debt crisis and, subsequently, by the supply-side-oriented Economic Adjustment Programmes that were initially signed by a PASOK government in 2010 and were renewed by New Democracy-PASOK coalition governments in 2012. With respect to private sector-related policies, the key idea behind these programmes has been to make the labour market even more flexible at the expense of workers to attract investment. The key policy implemented was the decentralisation of wage bargaining in the first half of 2010, when Greece moved from a multi-employer, state-sponsored wage setting system to a liberalised government signal-setting system, and the ease of dismissals (Kornelakis and Voskeritsian, 2014; Koukiadaki and Kokkinou, 2016; Koukiadaki and Kretsos, 2012). In addition, since 2010, the duration and size of unemployment benefits have been restricted and the employment-tied model of social insurance in the country has become more pronounced (OECD, 2020, Ch. 2; Papadopoulos, 2016; Immervoll et al., 2022).

Also, part of the austerity-focused growth plans include cuts related to education, which have been particularly harmful concerning the quality of higher education provision (Koulouris et al., 2014). Last, major bank bailouts and the liberalisation of the financial sector aimed to maintain liquidity towards the real sectors of the economy and, thus, boost employment and growth (Bieling, 2014). Eventually, this policy agenda failed to achieve high or sustainable growth rates and, simultaneously, increased the financial commitments of NFCs and households (Psychogios et al., 2020). Under these circumstances, between 2010 and 2015, the relative size of the FIRE sectors in Greece grew from around 16 to around 25% of the total value added. At the same time, the wage share decreased to around 7.5% reaching not only the lowest point ever observed in Greece but also one of the lowest percentages observed internationally over the last 30 years.

After several years of recession and a failed pro-employer, supply-side agenda without any positive effects on growth, the election of SYRIZA in January 2015 – the first governing political party in Greece with radical left origins – marks a political and policy shift. During its first semester, the 2015 SYRIZA-led government rejected extending the Economic Adjustment Programmes. However, international economic and political pressure related to the threat of Grexit, pushed the government to ultimately implement a third Economic Adjustment Programme since August 2015 (Sheehan, 2017). The two major reforms that were enacted as part of it and came with the 2016 supplemental bailout agreement were the end of any government intervention in the wage setting process and the scrapping of the right of the Ministry of Labour to veto against collective dismissals (Tourtouri et al., 2020). Meanwhile, in June 2018, certain labour rights related to collective bargaining were partially restored (Ministerial Decree 32921/2175/2018), as the suspension period of the ‘principle of favourability’ and the ‘extension principle’ that was introduced by Greece’s creditors came to an end. Also, in February 2019, the minimum wage was increased by 10.9% for employees over the age of 25, and 27.2% for those below. During this period, we also observe the relative stabilisation of the Greek economy with low growth rates since 2017, the continuation of the deleveraging of the financial sector as part of the third bank recapitalisation processes that took place in December 2015, and the implementation of policy reforms that facilitated the reduction of non-performing loans. Overall, from 2015 to 2019, the share of the FIRE sector reduced to around 20% and the wage share reaches the 2005 levels at 15%.

Concerning the last period of our sample, 2019–2021, where New Democracy rose again in power, the share of the FIRE sectors becomes relatively stable and the wage share begins to slightly decline. Yet, due to the impact of COVID-19 that restricted business activity since March 2020, and the corresponding income support and debt relief policies for wage earners and corporations (EBA, 2020), this trend largely reversed with the wage share rising and the size of FIRE sectors decreasing. Taken together, overall, the robust association between increases in the size of FIRE sectors and reductions in the income share of wage earners in the private, NFC sectors since the introduction of the Euro in Greece is apparent.

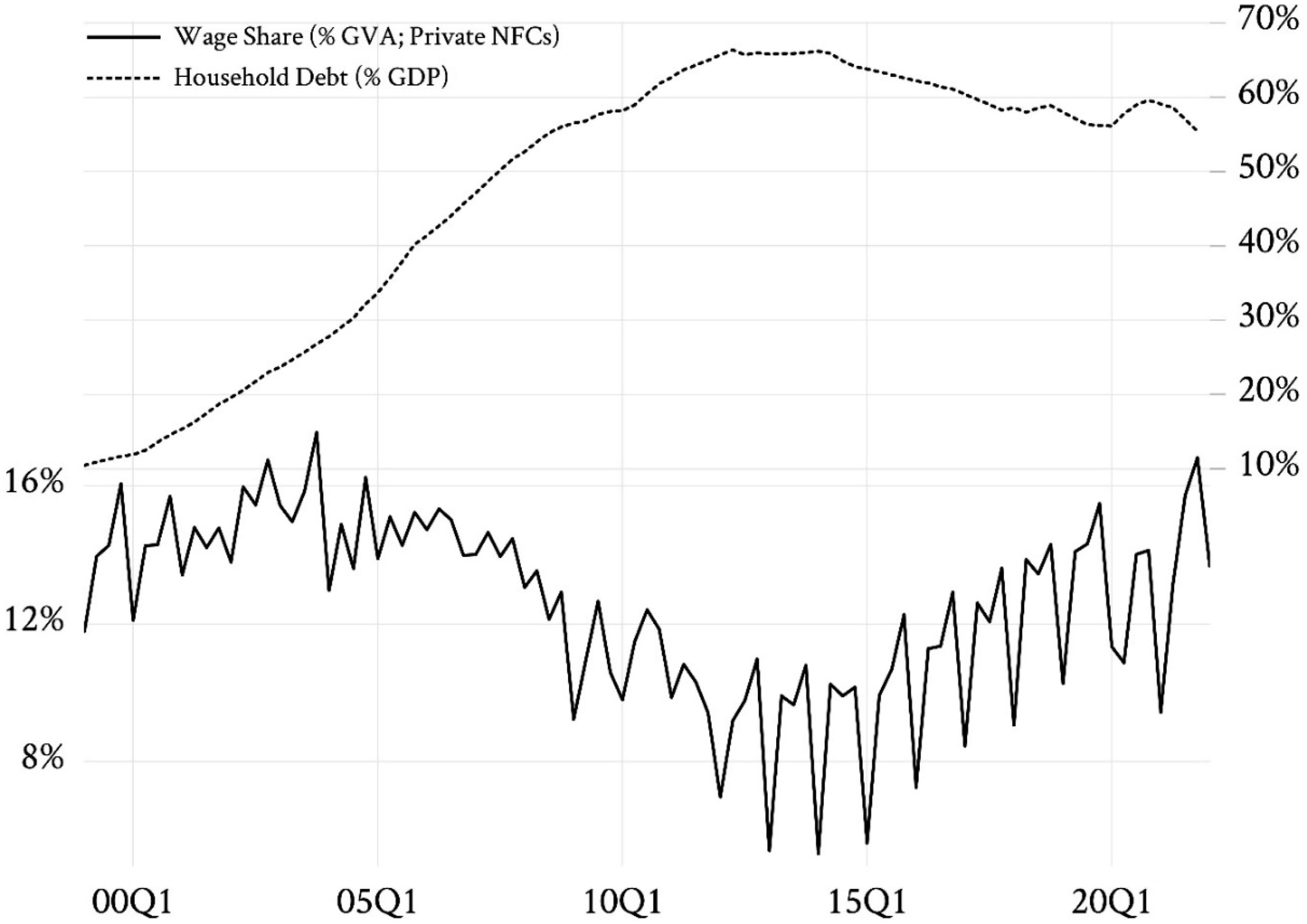

Beyond the overall extent of financialisation, as mentioned earlier, the main aspect of financialisation that grew rapidly during the period of integration into the Eurozone interbank market is the rise of household indebtedness (Placas, 2021; Varoufakis and Tserkezis, 2016). Therefore, exploring whether household debt-induced self-discipline is also negatively associated with the evolution of the Greek wage share is fundamental. Figure 2 presents the household debt-to-GDP ratio against the aggregated income share of wage earners in the non-financial, private sectors from the first quarter of 1999 to the last quarter of 2021. Household debt and the wage share, 1999Q1–2021Q4. Notes. The source for ‘Household Debt’ is the dataset of the Bank for International Settlements. The wage share is the same variable plotted in Figure 1.

Focusing on the household debt ratio itself, it is remarkable that since the beginning of Greece’s integration into the Eurozone market it has risen from 10.5% of GDP in the first quarter of 1999 to over 65.9% in the second quarter of 2014. Following this peak, it has become fairly stable around the ‘new normal’ of approximately 60% of GDP. While, admittedly, this ratio is lower than these of advanced economies (e.g. the Anglo-Saxon countries), where it often exceeds consistently 100% of GDP, the fact that such percentage change occurred in such a short period is extraordinary.

Contrasting the evolution of the household debt ratio with the income share of wage earners in private NFCs, similar to the wage share-FIRE sectors size relationship, the two variables appear to be loosely associated during the pre-2004 Olympics period. Following that, the association between increases in the household debt ratio and decreases in the wage share becomes stronger. The lowest point for the wage share over the whole period in the second half of 2014 (5.3%) coincides with the overall peak of household indebtedness during the same period. By the same token, the slight but steady reduction of the household debt ratio in the period after the peak also coincides with the recovery of the wage share until the last quarter of 2019. As regards the period of the latest New Democracy government that started in mid-2019, the household debt ratio began to increase again and the wage share started declining until the beginning of the COVID-19 period. As discussed earlier, lockdowns that restricted business activity as well as income support measures and debt relief schemes led to a slight reduction in household indebtedness compared to the previous two quarters and the recovery of the wage share. It is worth noting, however, that this peak of the wage share remains lower than the overall peak of the 1999–2021 period in 2003.

In terms of legal reforms that are related to the creditor-debtor relationship and the corresponding disciplinary effects on working-class households, despite all governments during this period adopting a market-oriented public policy agenda, certain forms of debtor protection were enacted. The most notable example is the ‘Katseli’ Law of 2010 (Laws 3869/2010 and 3816/2010) which allowed debt settlement for over-indebted individuals, offered protection for the primary residence of households, and included a debt restructuring scheme for business loans (Placas, 2021). 6 Post-2011 conservative coalition governments made the minimum requirements for the protection of primary residency and the penalties for repayment delays stricter (Law 4161/2013). Later, the post-2015 SYRIZA-led government followed a mixed approach with respect to the protection framework for borrowers (Laws 4336/2015, 4336/2015, 4549/2018). On the one hand, stricter requirements for the applicability of the protection of primary residence were imposed, and the establishment of electronic auctioning processes for the assets of bankrupt households and firms facilitated the process of selling non-performing loans to specialised distressed funds. On the other hand, it introduced debt service subsidies for poorer households and allowed repayment flexibility subject to personal economic conditions. According to Bank of Greece data on the ratio of non-performing loans to total loans in the Greek banking sector, the NPL ratio fell from 48.9% in March 2016, to 43.6% in June 2019. During this period, total household debt declined by approximately 10 percentage points (see Figure 2). The New Democracy government, soon after its re-election in July 2019, enacted the ‘Hercules/Heracles’ scheme (Law 4649/2019) to deal with the rising share of non-performing private loans in the country. This law allowed commercial banks in the country to reduce non-performing loans and improve their balance sheets by selling them even to offshore hedge funds. In practice, this has cancelled any benefits of previous debtor protection schemes and reinforced the disciplinary effects of household debt accumulation.

Empirical approach and methodology

Econometric specification and data

Building on sections two and three, this section presents the econometric specification and modelling approach used to examine the drivers of the income share of wage earners in the private, NFC sectors of Greece from 1999Q1 to 2021Q4 using quarterly from the Eurostat, the Bank for International Settlements, and Visser (2019). Our baseline equation is the following:

The measure of the Wage Share used is the series presented in Figures 1 and 2 calculated using data from the Quarterly National Accounts of Eurostat (A*10 breakdowns). That is the sum of wages and salaries over the respective value added in the private, non-financial sectors of the economy (i.e. excluding [K] Financial and insurance activities, [L] Real estate activities, and [O-Q] Public administration, defence, education, human health and social work activities).

Bargaining Coordination is measured by the categorical variable ‘Type: Type of coordination of wage setting’ from Visser (2019), which captures wage setting changes through a 6-point scale (from ‘1: No specific mechanism identified’ to ‘6: Government-imposed bargaining’). 7 As explained in the literature review section, more centralised wage setting coordination increases the bargaining power of low-income workers and, thus, increase the wage share. In the original dataset of Visser (2019), the series includes annual observations; therefore, we extend them in quarterly form by specifying the exact cut-off points of change. The cut-off dates that we use to transform the series from annual to quarterly are the following: (a) From 5 to 1 on May 2010 (First Economic Adjustment Programme); (b) From 1 to 0 on June 2016 (Supplemental memorandum of understanding with Greece – June 2016); (c) From 0 to 1 on August 2018 (Ministerial Decree No. 32921/2175/2018). In the case of Greece, as discussed in Section 3, most of the changes were minor between limited coordination and no coordination during this period; hence, its effects are likely to be negligible.

Education captures the share of tertiary educated employees (as a percentage of total employment). These series come from the Eurostat data portal and its original source is the European Union Labour Force Survey (EU-LFS). Higher education participation fosters a broader spectrum of transferable skills and competencies which are sought after by employers. As education is expected to significantly enhance employment prospects it has a positive effect on workers bargaining power and due to this, it is anticipated to positively impact the wage share. Given that austerity policies have been affecting tertiary education provision in Greece, this mechanism is likely to have contributed to the changes in the wage share observed over this period.

Regarding Social Benefits, we use social benefits in-kind and in cash (as a share of GDP). Both variables come from Eurostat’s Quarterly Non-Financial Accounts for General Government. The first variable is readily available, while the latter is calculated by subtracting social benefits in-kind from total social benefits. 8 While higher welfare provision is commonly associated with higher bargaining power and increased wages, given the employment-tied character of public welfare in Greece, it is likely that the signs of the respective coefficients will be negative. This is because obtaining any job, even a low-pay one, allows a household to access social transfers.

Trade openness is incorporated in the equations via three different quarterly indicators that are used interchangeably: trade openness (imports plus exports over GDP), the share of imports (% GDP), and the share of exports (% GDP) from Eurostat. These three variables are widely used measures of trade globalisation that capture potential downward pressure on wages due to an economy’s overall exposure to international trade, import penetration, and the effects of international price competitiveness as exports grow, respectively (Gouzoulis et al., 2023). While, in general, trade openness tends to increase the capital income share at the expense of wages in both advanced and developing economies, as discussed in section three, Greece was not an export-oriented economy before EU integration, hence, the effects of trade openness are likely to have been negligible in the absence of relocation threat (Varoufakis and Tserkezis, 2016).

Following the historical-institutional analysis of the previous section, Financialisation is captured via the inclusion of the size of the FIRE Sectors and the Household Debt-to-GDP ratio (see Figures 1 and 2). We expect both variables to exhibit significant negative effects on the income share of wage earners in Greece. As a robustness check for the main results, we also estimate an additional round of equations which incorporate the Corporate Debt-to-GDP ratio as an additional financialisation proxy. Further, as a robustness check for the potential impact of seasonality, we re-estimate all equations and include a binary, quarterly time dummy that controls for seasonal fluctuations related to short-term increases in employment and business activity during the summer months due to tourism (Q3). We prefer this approach to avoid losing information, which is a common disadvantage of seasonally adjusting the dependent variable series, even when the adjustment process is properly implemented (Lee, 2018).

Econometric modelling approach

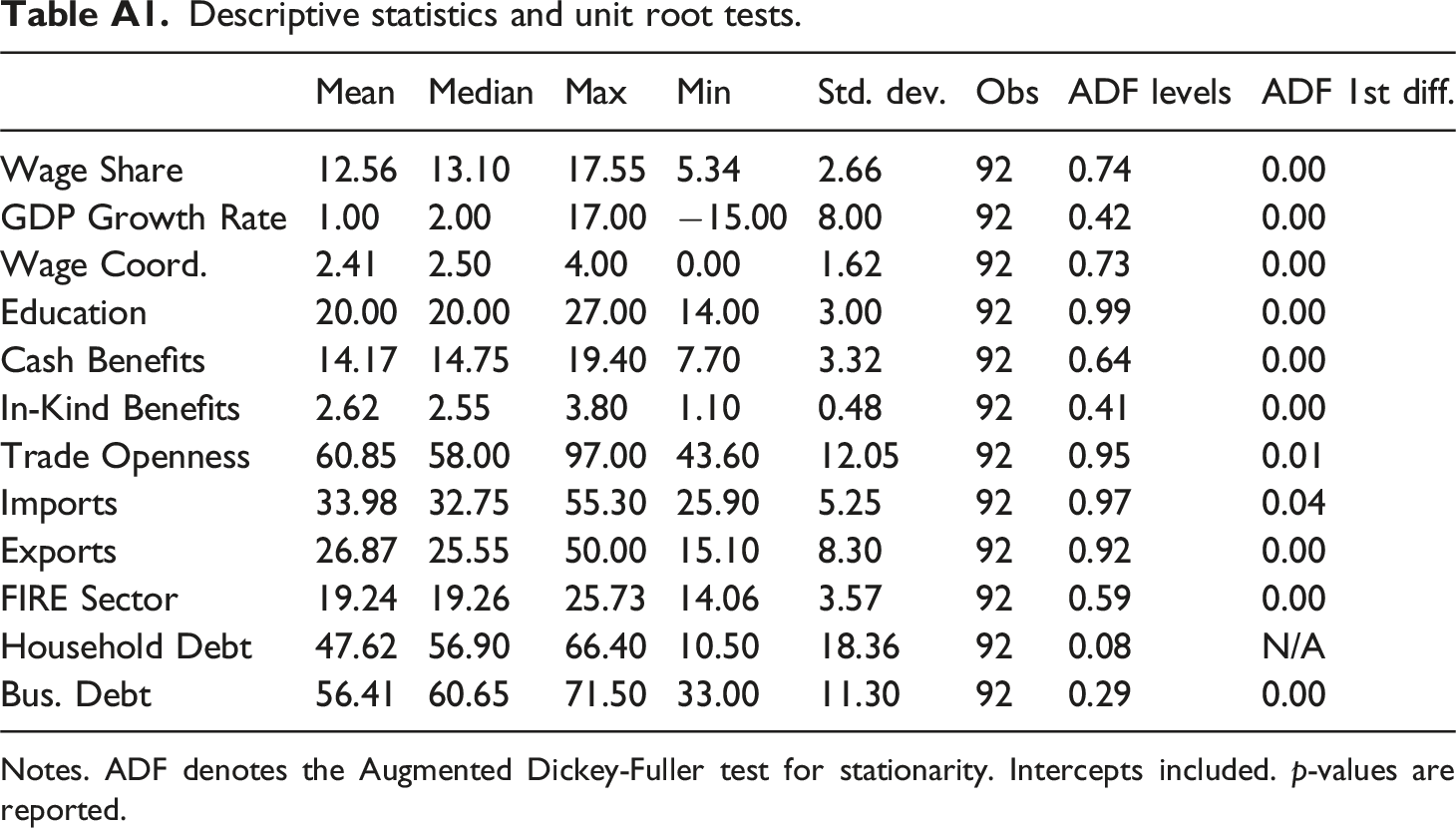

The choice of the appropriate econometric modelling approach is typically dictated by whether the respective series are stationary or not, that is, whether the statistical properties of each series change over time, and whether a cointegrating/long-run relationship between the dependent and the independent variables exists. According to the descriptive statistics and unit root tests reported in Table A1 of the appendix, all variables are stationary at either levels or first differences. Regarding cointegration, a common approach to evaluate this property is to run a stationary regression in levels between the dependent variable and the independent variables in each case, and test whether their residuals are stationary or not (Engle and Granger, 1987). In the case of our dataset, the residuals of these regressions are indeed stationary, therefore, we find evidence that a cointegrating relationship exists.

In cases where cointegration exists and the dataset includes a combination of stationary and non-stationary time series, the Unrestricted Error-Correction Model (UECM) is the standard modelling approach followed (Davidson et al., 1978; Lin and Tomaskovic-Devey, 2013; Sargan, 1964). The typical form of the UECM includes the explanatory variables in first-differences (short-run coefficients) and levels (level coefficients), and also the dependent variable in first lag both as a level and a short-run independent variable. One of the main advantages of this model is that it accounts for serial correlation, which is a frequent issue when econometric equations are estimated via the standard ordinary least squares (OLS) in levels. Furthermore, to address potential simultaneity biases, the level coefficients are typically included in first lags. This commonly used approach also creates a unidirectional mechanism that is comparable to the Granger causality test (see Godechot, 2016).

In reality, most economic variables may exhibit bidirectional relationships, which pose significant challenges related to identification and causality. ECMs are particularly useful in such cases as the error-correction term included essentially measures the degree to which the system is off its long-run equilibrium, allowing for correction toward that equilibrium in subsequent periods by capturing both feedback loops and the level effects. The alternative of Vector Autoregressive models with more complicated lag structures may struggle to properly identify long-run causal effects and very often leads to overparameterisation, and, thus, less efficient estimates (Sims, 1980). For these reasons, the UECM has become a very popular econometric strategy within industrial relations (see Bengtsson, 2014; Kristal, 2010, 2019). The UECM specification of the present study is of the following form:

Results and discussion

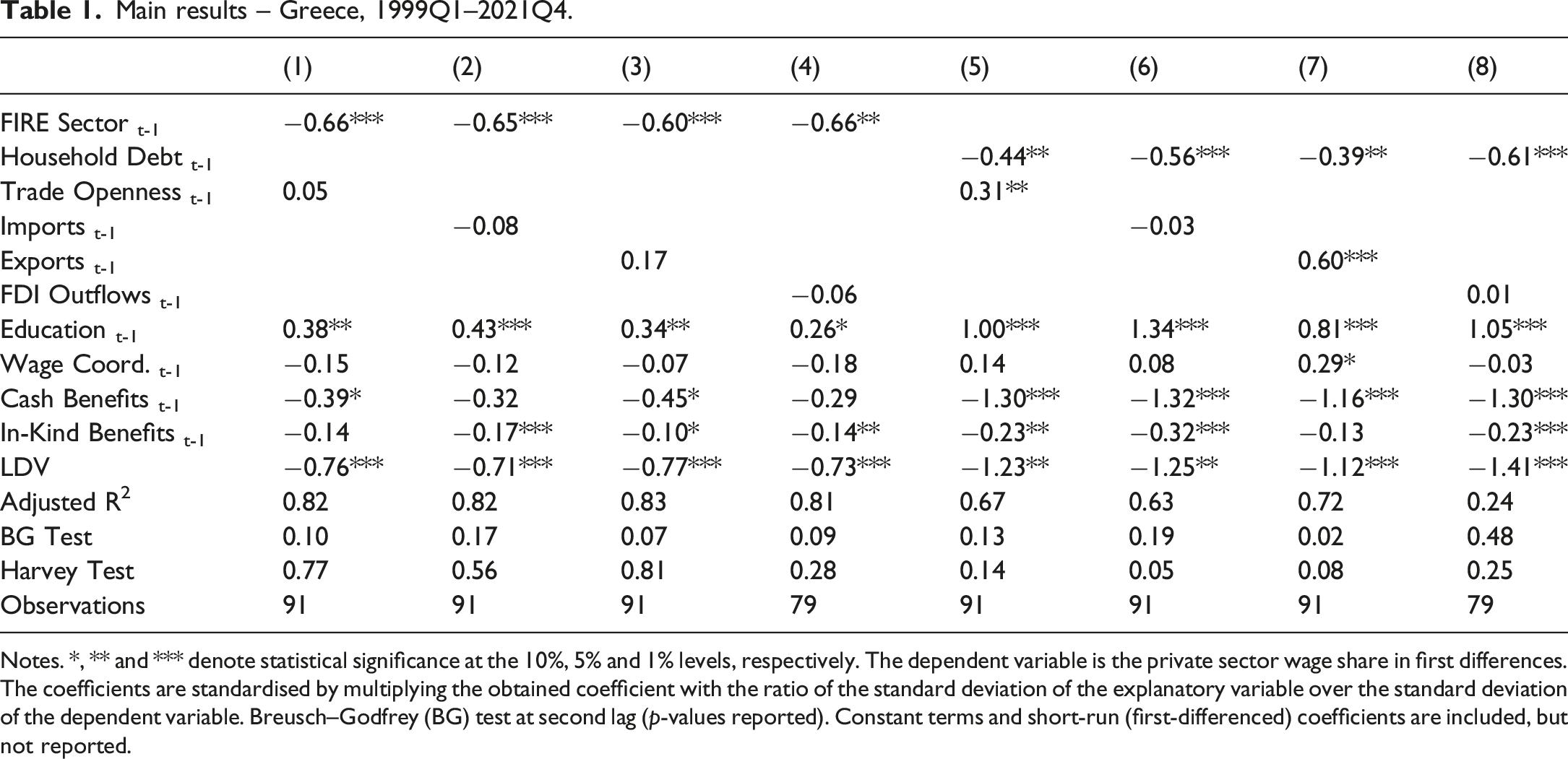

Main results – Greece, 1999Q1–2021Q4.

Notes. *, ** and *** denote statistical significance at the 10%, 5% and 1% levels, respectively. The dependent variable is the private sector wage share in first differences. The coefficients are standardised by multiplying the obtained coefficient with the ratio of the standard deviation of the explanatory variable over the standard deviation of the dependent variable. Breusch–Godfrey (BG) test at second lag (p-values reported). Constant terms and short-run (first-differenced) coefficients are included, but not reported.

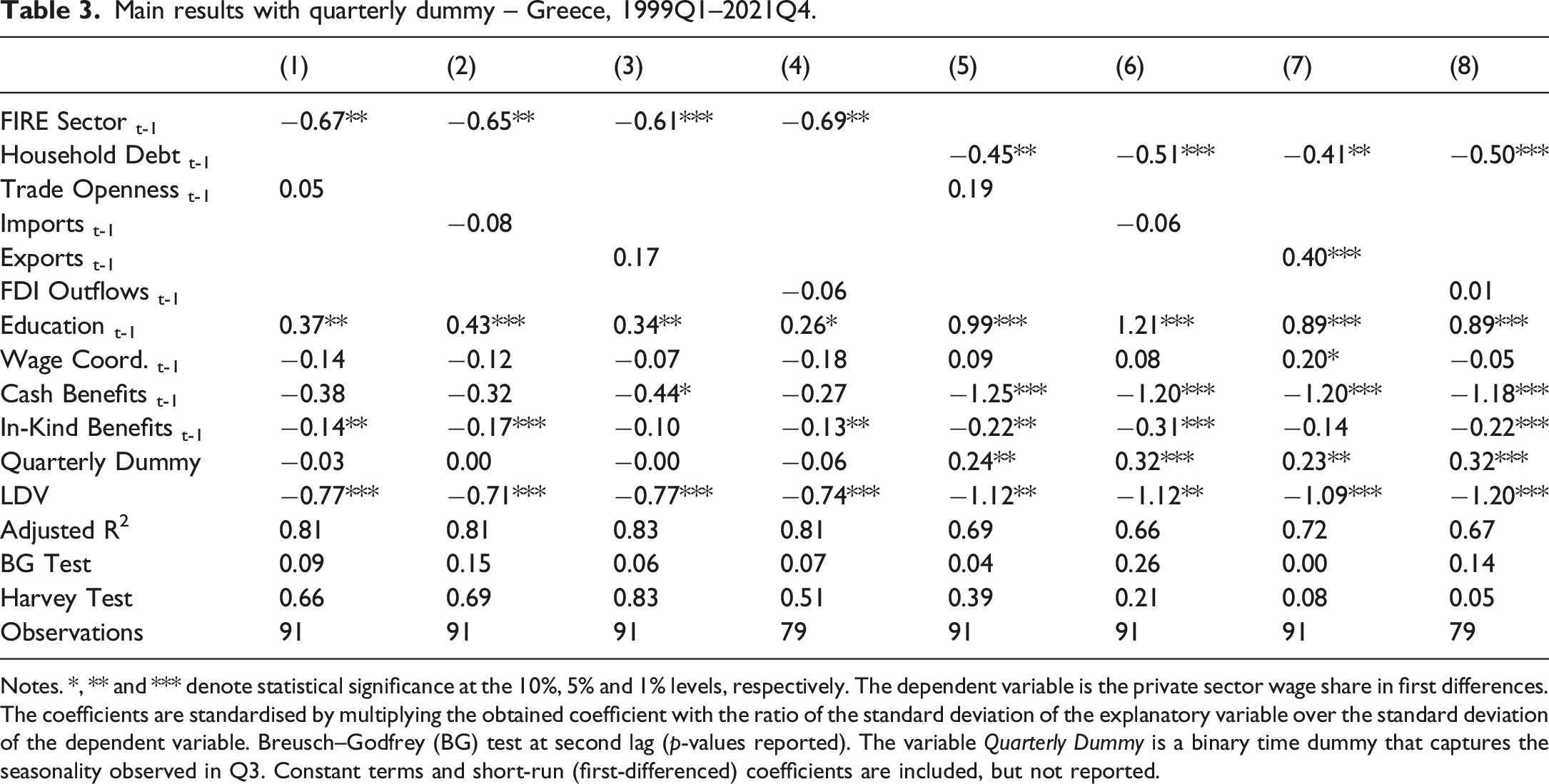

As it can be seen, all eight specifications employed, clearly show that the increase of the variables capturing the financialisation process, is associated with the wage share of the private, non-financial sectors of Greece from the first quarter of 1999 to the last quarter of 2021. We discuss each of the variables separately. The coefficient related to the relative size of the FIRE sectors (first proxy of financialisation), is consistently negative, fairly stable in size, and statistically significant in all four specifications included. This result is not surprising in the case of Greece where the country’s integration and alignment with the Eurozone economy were largely driven by extensive financial market liberalisation. This process was accompanied by unsustainable growth of the banking sector, leading to the provision of cheap credit to the private sector, and particularly low-income working-class households.

This leads us to the second and dominant form of financialisation in the Greek case after the adoption of the common currency, that of the household debt-to-GDP ratio. Its coefficients are also consistently negative, substantially large, and statistically significant either at the one or five percent levels in all four specifications included. This finding highlights the importance of this type of financialisation channel, namely, household financialisation. Increased level of indebtedness makes households more vulnerable to accept worse working conditions and/or lower wages. This decrease of bargaining power of labour impacts the distribution of income against labour. Taken together, Table 1 shows that the growth of the financial sector under the European Economic and Monetary Union and, particularly, its focus on credit provision to households has been the key negative driver of the Greek private, non-financial labour share.

Concerning the rest explanatory variables, the second consistent driver of the private sector, non-financial wage share of Greece is the share of tertiary educated workers. In all specifications, the coefficients for workers’ education are positive and statistically significant. Workers’ educational attainment allows them to increase their outside options, hence is expected to have a positive effect on their bargaining power. As such our finding shows that changes in educational provision and attainment over the last 22 years have been fundamental for changes in capital-labour distribution in the country. The spending cuts implemented during the official austerity years in Greece (2010–2019) will likely have a significant negative impact on the skillset and educational capital of the Greek labour force in the coming years, extending the downward pressures on the wage share.

Another worth-noting result is that, in most cases, social benefits in cash or in-kind are negatively related to the labour share. This finding is probably related to the employment-tied nature of social insurance in the country, which empowers employers disproportionately. As access to basic social welfare is contingent on having a job, workers are often compelled to accept even a low-paid job for basic access to social welfare, therefore increasing employers’ bargaining position. Last, the effects of trade openness and wage bargaining coordination are inconclusive and statistically insignificant in the vast majority of the cases. Given the discussion of domestic institutional change in the previous section, this is not a surprise since Greece was not an export-oriented economy before the introduction of the Euro. As such its wage bargaining was already fairly decentralised and trade openness does not have a significant effect on the bargaining power of workers.

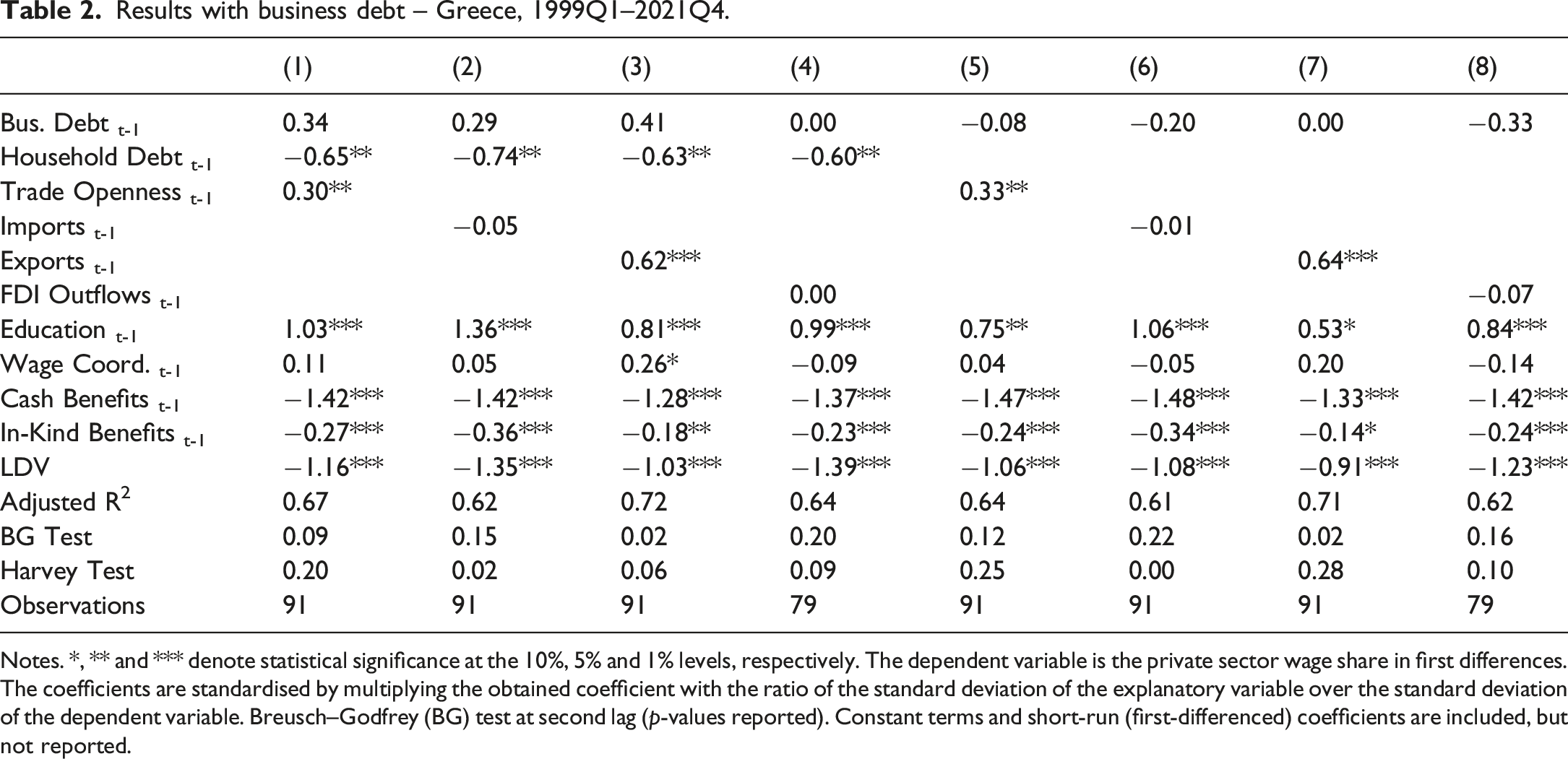

Results with business debt – Greece, 1999Q1–2021Q4.

Notes. *, ** and *** denote statistical significance at the 10%, 5% and 1% levels, respectively. The dependent variable is the private sector wage share in first differences. The coefficients are standardised by multiplying the obtained coefficient with the ratio of the standard deviation of the explanatory variable over the standard deviation of the dependent variable. Breusch–Godfrey (BG) test at second lag (p-values reported). Constant terms and short-run (first-differenced) coefficients are included, but not reported.

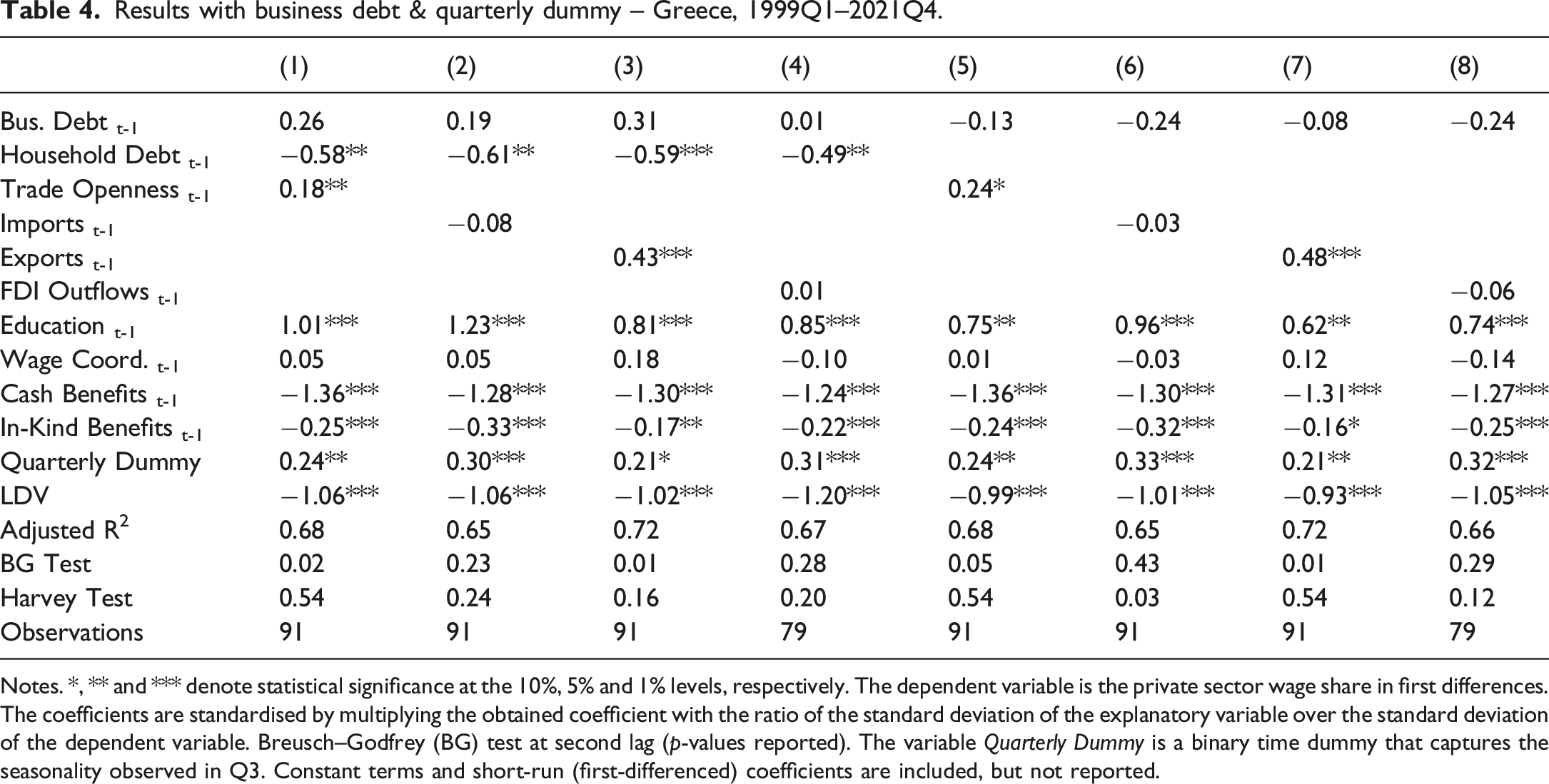

Summarising the key findings of our econometric analysis, the negative coefficients for the size of the FIRE sectors and the household debt ratio are statistically significant in all equations included. These results underscore the importance of understanding the phenomenon of financialisation as a crucial driver of wage dynamics in the context of Greece’s integration into the Eurozone. Further, they provide robust support that, similar to other financialised economies, in Greece, financialisation is a key negative driver of labour’s bargaining power and, thus, the wage share. Simultaneously, the impact of social transfers is also negative and robust, which is a strong indication of the employment-tied nature of the domestic welfare state, which, ultimately, disempowers workers as even a job with poor working conditions is essential to access basic social insurance. Lastly, the share of tertiary educated employees is also found to exhibit consistent positive effects, which, in line with our hypotheses, shows that formal qualifications and transferable skills related to educational attainment increase the bargaining power of workers and, consequently their income share.

Main results with quarterly dummy – Greece, 1999Q1–2021Q4.

Notes. *, ** and *** denote statistical significance at the 10%, 5% and 1% levels, respectively. The dependent variable is the private sector wage share in first differences. The coefficients are standardised by multiplying the obtained coefficient with the ratio of the standard deviation of the explanatory variable over the standard deviation of the dependent variable. Breusch–Godfrey (BG) test at second lag (p-values reported). The variable Quarterly Dummy is a binary time dummy that captures the seasonality observed in Q3. Constant terms and short-run (first-differenced) coefficients are included, but not reported.

Results with business debt & quarterly dummy – Greece, 1999Q1–2021Q4.

Notes. *, ** and *** denote statistical significance at the 10%, 5% and 1% levels, respectively. The dependent variable is the private sector wage share in first differences. The coefficients are standardised by multiplying the obtained coefficient with the ratio of the standard deviation of the explanatory variable over the standard deviation of the dependent variable. Breusch–Godfrey (BG) test at second lag (p-values reported). The variable Quarterly Dummy is a binary time dummy that captures the seasonality observed in Q3. Constant terms and short-run (first-differenced) coefficients are included, but not reported.

Concluding remarks

This study analyzes the factors that influence the wage share in the non-financial, private sector, of Greece, following its integration into the Eurozone. As we discuss in our paper, Greece’s integration into the Eurozone primarily resulted in the financialisation of its economy, notably affecting households by precipitating a rapid increase in household indebtedness. Our empirical analysis shows how the relative expansion of the FIRE sectors and the upsurge in household debt have negatively impacted Greece’s wage share since 2000. This connects directly to a growing body of research establishing both theoretical and empirical links between financialisation—at both household and corporate levels—diminished labour bargaining power, and the declining wage share. The key mechanisms driving these trends are (a) corporate financialisation increases the financial obligations of firms, which often shift this pressure onto their workforce by either directly reducing labour costs or indirectly weakening labour’s bargaining power; (b) corporate financialisation redirects firms’ investment priorities away from real, productive investments and towards financial assets that offer higher, more liquid and mobile returns. This reduction in real investment lowers labour demand, leading to higher unemployment and, consequently, a lower wage share; and (c) household financialisation raises indebtedness, particularly among low-income workers, which leads to more risk-averse and self-disciplined behaviour in both the labour market and the workplace, driven by the fear of defaulting on their debts. Furthermore, our findings highlight tertiary education provision has exhibited positive effects, whilst the employment-tied social insurance system has disempowered Greek workers and is negatively associated with the wage share.

Overall this work contributes to related research in two fundamental ways. First, our paper contributes to the growing literature on financialisation and wage bargaining outcomes by focusing on the Greek economy, which while it is an arguably interesting case due to recent reforms, it has not been studied on its own up to now. Second, examining the link between the financialisation of the Greek economy and the income share of wage earners in the private, Non-Financial Corporations (NFCs) sector since joining the Eurozone, our paper contributes on the broader literature regarding the political economy of Greece since the adoption of the Euro. Whereas our findings align with the broader global trends of financialisation and financial deregulation, there is space for further investigation in this area. For instance, the relationship between business debt and the wage share might be affected by broader structural characteristics of the Greek labor market. Most importantly, the effects of business debt might be conditioned by the structure of the economic and productive system in Greece which is highly skewed towards self-employed occupations and own-account workers (almost one third of the workforce). Further investigation of this channel building on our findings would allow a more nuanced understanding.

Several policy implications regarding wage recovery arise from these results. First, regulating financial institutions and easing the debt burden of working-class households would decrease their risk of defaulting and allow them to negotiate fairer wages. Second, the expansion of tertiary education provision to a larger share of workers would give them more employment options and, thus, more negotiating power. Third, making social transfer coverage universal by de-linking them from the employment contract would also empower working-class households and allow them to find jobs with better working conditions.

Footnotes

Acknowledgements

The authors are grateful to Yannis Dafermos and Yanis Varoufakis for their comments and suggestions on earlier versions of the paper.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: We are grateful to the Eteron Institute for their financial support, and Horizon Europe: DemoTrans The Interchange Between Democratic Institutions and the Globalisation of the Economy (101059288).

Notes

Appendix

Descriptive statistics and unit root tests.

| Mean | Median | Max | Min | Std. dev. | Obs | ADF levels | ADF 1st diff. | |

|---|---|---|---|---|---|---|---|---|

| Wage Share | 12.56 | 13.10 | 17.55 | 5.34 | 2.66 | 92 | 0.74 | 0.00 |

| GDP Growth Rate | 1.00 | 2.00 | 17.00 | −15.00 | 8.00 | 92 | 0.42 | 0.00 |

| Wage Coord. | 2.41 | 2.50 | 4.00 | 0.00 | 1.62 | 92 | 0.73 | 0.00 |

| Education | 20.00 | 20.00 | 27.00 | 14.00 | 3.00 | 92 | 0.99 | 0.00 |

| Cash Benefits | 14.17 | 14.75 | 19.40 | 7.70 | 3.32 | 92 | 0.64 | 0.00 |

| In-Kind Benefits | 2.62 | 2.55 | 3.80 | 1.10 | 0.48 | 92 | 0.41 | 0.00 |

| Trade Openness | 60.85 | 58.00 | 97.00 | 43.60 | 12.05 | 92 | 0.95 | 0.01 |

| Imports | 33.98 | 32.75 | 55.30 | 25.90 | 5.25 | 92 | 0.97 | 0.04 |

| Exports | 26.87 | 25.55 | 50.00 | 15.10 | 8.30 | 92 | 0.92 | 0.00 |

| FIRE Sector | 19.24 | 19.26 | 25.73 | 14.06 | 3.57 | 92 | 0.59 | 0.00 |

| Household Debt | 47.62 | 56.90 | 66.40 | 10.50 | 18.36 | 92 | 0.08 | N/A |

| Bus. Debt | 56.41 | 60.65 | 71.50 | 33.00 | 11.30 | 92 | 0.29 | 0.00 |

Notes. ADF denotes the Augmented Dickey-Fuller test for stationarity. Intercepts included. p-values are reported.