Abstract

Job reallocation is a key driver of aggregate wage growth, but its role in different economic systems remains understudied. This paper takes a comparative view and analyses the role of job mobility in job reallocation and aggregate wage growth in Norway, comparing it to published results for the United States. The results show first that, as expected, overall job mobility is much lower in Norway compared to the United States, likely reflecting the compressed wage distribution. However, the speed of job reallocation from low-wage to high-wage firms is similar to or even higher than in the United States. Second, in both Norway and the United States, the process of job reallocation is strongly pro-cyclical. This is entirely driven by the pro-cyclical nature of net job-to-job mobility from low- to high-wage firms. Third, for Norway, the bulk of aggregate wage growth reflects on-the job wage growth, while its cyclicality is largely driven by net job-to-job mobility from low to high-wage firms. This paper shows that reallocation is not necessarily less efficient in more egalitarian societies with lower mobility and different wage structures.

Introduction

Understanding the role of different ‘varieties of capitalism’ for economic and labour market performance is a crucial issue in the social sciences. Several ideal-typical models of policies and institutions have been identified that tend to be associated with good economic and labour market outcomes. These include the market-based model of the United States and several other mainly English-speaking economies, as well as the corporatist model of Norway and other Northern European countries (Hall and Soskice 2001). However, both models have recently come under pressure as it is proving increasingly challenging to sustain high productivity growth while containing wage inequalities (Hijzen et al. 2021).

This paper seeks to shed light on the way these different ‘ideal types’ generate sustained increases in living standards through higher wages, and the extent to which worker reallocation drives such changes. While not addressing specific aspects of the institutions assumed to affect these differences, we make use of the difference between these two ‘ideal types’ of the welfare state.

The two countries featured in this study are characterised by radically different wage-setting systems. While wages in the United States are largely determined through bargaining between individual workers and their employers (or unilateral wage-setting by employers), supported only by a modest statutory minimum wage for the most vulnerable; in Norway wages tend to be negotiated collectively through multiple levels of bargaining at the sector and firm level. Given the allocative role of wages in capitalist societies, these starkly different approaches to wage setting, associated with big differences in mobility, could potentially lead to differences not only pertaining to wage inequalities, but also for the operation of labour markets, the process of job reallocation and the way economic growth is generated.

This paper primarily focuses on the role of job mobility in Norway and the United States for efficiency-enhancing reallocation as well as aggregate wage growth. The key questions are, first, how reallocation along the wage ladder differs between the two countries given their very different wage distribution and institutional set-up, and second, how this reallocation contributes to aggregate wage growth relative to other components such as on-the-job growth and wage growth due to changes in workforce composition.

We make use of linked employer–employee data for Norway to track worker mobility across firms from the late 1990s to the early 2010s. These findings are compared to existing estimates for mobility and reallocation between low and high wage firms for the United States. Importantly, the analysis distinguishes job-to-job mobility from mobility in and out of employment. Moreover, we analyse how job mobility and job reallocation vary over the business cycle by differentiating between periods with high and low cyclical unemployment. The paper concludes by drawing out the implications of job mobility for aggregate wage growth and its evolution over the business cycle.

Conceptual framework

The main model linking job reallocation to aggregate wage growth and the business cycle emphasizes transitions between jobs as well as between employment and non-employment. Further, poaching of workers by firms higher up the job ladder drives aggregate wage and productivity growth (Moscarini and Postel-Vinay 2018). However, the spread in wages between firms, and therefore the extent to which differences along the job ladder incentivize mobility, differs strongly between countries (see e.g. Card et al., 2017; Criscuolo et al., 2020). This job ladder can be an important driver of aggregate wage growth and especially of its cyclicality and the cleansing of labour markets in a recession (Haltiwanger et al., 2021).

Expected differences between Norway and the United States

Norway and the United States are comparable rich economies providing strong, but declining, aggregate wage growth. However, the structures of their economies are very different, with Norway offering a much more egalitarian wage structure due to stronger labour market institutions and regulations.

We do not attempt to carry out an exhaustive analysis of the institutional differences between the Norwegian and US labour markets in this paper, but rather view them as two different ideal typical ways of organizing the economy, be it in the varieties of capitalism framework, where they exemplify the coordinated or liberal market economies respectively (Hall and Soskice 2001) or as growth and welfare regimes (Hassel and Palier 2023). These literatures make salient specific aspects of how growth is managed and how the economy and welfare state relate, of which we think the following are particularly relevant. First, Norway is characterised by a much more highly organised and coordinated bargaining system, while in the United States bargaining happens more at the individual level or at the firm-level. The latter is expected to lead to larger pay differences between workplaces in the latter, and increase incentives for changing firms. Second, Norway has relatively strict employment protection legislation reducing the insecurity for workers and lowering the risk for dismissal which again reduces mobility relative to the US (OECD 2020). Finally, through the more substantial social security safety net in Norway than in the United States there would be greater options to find a good match in Norway, with less of a move to only the worst-paying positions than in the United States.

Linking mobility, reallocation and wage growth

As job-to-job mobility along the job ladder drives workers’ wage progression and efficient allocation of jobs (Berson et al. 2020; Hahn et al., 2017; Haltiwanger, Hyatt, and McEntarfer, 2018), a decline in job mobility would result in a slowdown in aggregate wage or productivity growth (Azzopardi et al., 2020; Haltiwanger, Hyatt, Kahn et al., 2018; Moscarini and Postel-Vinay 2018). In their study on the United States Decker et al. (2020) document a decline in job mobility as job reallocation traces productivity less closely over time, which they link to lower aggregate productivity growth.

The job ladder is operationalized in different ways: through firm size and/or firm age, firm productivity, or (a function of) average earnings. In our paper, we follow Haltiwanger, Hyatt, Kahn et al. (2018) and classify firms according to their average earnings or wage premia. While a direct measure of productivity would allow for a closer measure of productivity-enhancing and thereby efficient reallocation this paper focuses on the wage distribution, as productivity information is not available for Norway in this data. This means that our results directly reflect mobility that enhances average wage growth, rather than productivity-enhancing mobility which are likely to be overlapping but also somewhat distinct (Bertheau and Vejlin 2023). However, the focus on wages is relevant here as it allows a direct link with average wage growth, relates to the literature on firm premia incorporating rent sharing (Card et al., 2017), and is consistent with the US work allowing for a comparison.

Cyclicality of mobility

During recessions jobs are primarily shed at low-wage and low-productivity firms (Bertheau et al. 2020). This generally results from the poaching channel – through which higher-wage firms grow – drying up during a recession. In that way, the job ladder contributes to the cleansing of the labour market during bad economic times (Bachmann and Bechara 2019; Haltiwanger et al., 2021). Comparative research is needed to indicate whether these patterns are the same in different economic systems. A sullying effect, where the most productive firms do not grow, can counteract a possible cleansing effect of recessions which happens at the lower end – where the less productive firms shed workers that can then move to more productive firms (Haltiwanger et al., 2021). Importantly, this entails that flows to non-employment and job-to-job flows have opposite reactions to recessions.

Findings in line with this argument were supplied by Bertheau et al. (2020) for Denmark, while Berson et al. (2020) find that net job-to-job mobility is much less pro-cyclical in France and Italy. The strong pro-cyclicality of employment in high-wage firms in the United States raises important questions about the optimal degree of labour hoarding during recessions and the role of policies and institutions in shaping incentives for labour hoarding, for example, through the use of job retention schemes (OECD 2021).

Methodology

This section describes the methodology for the empirical analysis of job mobility, reallocation and aggregate wage growth. We follow the approach of Haltiwanger, Hyatt, Kahn et al. (2018) [HHKM] and Haltiwanger, Hyatt and McEntarfer (2018) [HHM]. To facilitate a more relevant comparison we do not include the flows to and from the public sector in the baseline analysis. We further assess the implications of job mobility and job reallocation for aggregate wage growth in Norway.

Job reallocation is defined here as the change in the structure of private-sector employment between low and high wage firms measured quarterly. Following HHKM firms are divided into low-paying (20%), middle-paying (40%) and high-paying (40%) based on their employee-weighted full-quarter earnings, with and without adjusting for worker composition. 1 To the extent that higher-wage firms are more productive, the reallocation from lower to higher-wage firms is efficiency-enhancing, as well as contributing to aggregate wage growth. We first use average wages at the firm level, without adjustments for differences in worker composition. This allows us to compare the results for Norway with those for the United States. In a second step, we assess how the results for Norway change when ranking firms based on wage premia where firms’ workforce composition is accounted for. Wage premia are captured by means of the firm fixed effects obtained in a regression of log quarterly earnings, estimated year-by-year, that also include flexible earnings-experience profiles by gender and education profiles (with gender and education each interacted with a cubic in age) and quarter fixed effects (Barth et al., 2016; Card et al., 2017) 2 .

When considering the implications of job reallocation for aggregate wage growth, we also compare the contribution of job reallocation based on three firm-wage groups with that based on the full firm distribution.

The rate of job aggregate mobility is defined as the sum of hires [h] and separations [s] that has taken place between the previous quarter [t-1] and the current quarter [t] over employment [e] in the current quarter [t]. Further, job mobility may contribute to job reallocation by bringing about changes in the structure of employment between low and high wage firms, but not all job flows bring about such changes. Job flows that do not affect the structure of employment are referred to as excess turnover (Davis et al. 1998). Consequently, one can decompose the overall rate of job mobility (gj) for low, medium and high-wage firms – denoted with subscript j – into the rate of excess worker turnover (xj, twice the minimum of hires and separations over employment) and the rate of net employment growth (nj, the difference between hires and separations over employment). Time subscripts are removed for ease of exposition.

Moves are identified between consecutive quarters. As such job-to-job mobility may be over-estimated relative to more fine-grained timings (Bertheau et al. 2020).

The rate of excess turnover (xj) in turn can be decomposed into different flows that cancel each other out: the job-to-job mobility rate between firms of the same type (xjj), the job-to-job mobility rate between different types of firms j and k(xjk), and the employment mobility rate between firms of type j and non-employment n (xjn).

Similarly, net employment growth (nj) can be decomposed into the net rate of job-to-job mobility between firm type j and k (njk) and the rate of net employment mobility between firm type j and non-employment (njn).

Equation (3) shows that job reallocation between low and high-wage firms can take place through job-to-job mobility, for which wage incentives may play an important role, and employment mobility, for which flexibility-enhancing policies may be particularly important (e.g. employment and product market regulations, active labour market policies).

The implications of job mobility and job reallocation for aggregate wage growth in Norway are analysed by decomposing aggregate wage growth into the parts due to job stayers, job-to-job movers, and moves from and to non-employment, following the formulation in Hahn et al. (2021, 8). Here, st indicates job stayers, qt job-to-job moves, nt moves from nonemployment to employment and rt exits to nonemployment. The total number of each type is expressed by a capitalised letter, with D the total number employed. Equation (4) below expresses overall wage growth as the part due to the on-the-job wage growth, job-to-job moves and the difference between entrants to employment and those exiting from one quarter to the next, where w refers to the log real wage.

In this paper, we focus on overall earnings and do not consider the role played by part-time work and hours worked, which is likely to be substantial. This is partly due to data limitations and in order to compare the two countries, but it also reflects our choice to focus on overall earnings regardless of the hours worked. The hours do of course play a role as for instance the lowest-paid firms and sectors are likely to rely more on part-time work, and some of the measured mobility and wage growth may reflect a move from part-time to full-time work.

Data

Longitudinal Employer-Household Dynamics for the United States

The analysis for the United States in this paper draws directly from published results by HHKM and HHM based on the Longitudinal Employer-Household Dynamics (LEHD). The LEHD is an administrative dataset with quarterly data on the universe of workers in the United States. It combines worker-level data on earnings drawn from social security records with establishment-level data drawn from the Census of Employment and Wages. Their data covers 28 states for the period 1998 to 2011. We rely on the analysis of detailed quarterly information in HHKM on mobility and wage gains along the firm wage distribution; as well as the quarterly information on mobility and wage gains by age, education and firm-wage type in HHM.

Norwegian registry data

The Norwegian data are obtained from merging two registries: (i) the State Register of Employers and Employees (Aa-registeret), which contains all employment arrangements in Norway, and (ii) the End of the Year Certificate Register, containing information on annual wages, including bonuses and extra payments, for each worker in a firm. As the registry data include information on the time worked in each quarter, earnings are equivalised to full-quarter earnings. In order to minimise the role of outliers, we restrict the data to workers who stayed in the same job for at least 1 month in the quarter and earned more than 25% of the median wage, and winsorize the top 1% of earnings (Haltiwanger, Hyatt, and McEntarfer, 2018).

As in the case of the United States, the analysis includes workers aged 18 to 64 and their main job, defined as the one with the highest earnings in a quarter. Age is divided into four categories: less than 25 years; 25–34 years; 35–44 years; and 45–64 years. Education is divided into four categories: less than upper secondary; upper secondary; post-secondary non-tertiary; and tertiary (corresponding to a US college degree). Time series are seasonally adjusted and wage data are converted in real terms using CPI deflators. 3

The analysis is restricted to firms in the non-agricultural private sector in mainland Norway, excluding the offshore oil sector as well as the mining/extraction industries, as wages in this sector are substantially above the rest of the country and depend heavily on external variation, for the period 1998 to 2011. The public sector is generally excluded from the baseline analysis as was done for the United States. However, since the public sector plays a more important role in Norway, we test whether our findings change substantially when including the public sector as a third state in addition to private-sector employment and non-employment. The analysis consists of 4,949,282 worker observations in 1998 and 5,148,873 worker observations in 2011. Descriptive statistics are shown in table A1 in the appendix.

Results

This section documents the role of job mobility in reallocation and how this varies over the business cycle in Norway and the United States. To allow for a reasonable comparison between the two countries, the baseline analysis is restricted to the private sector and firms are ranked based on average wages. In Section 5, the analysis for Norway is repeated while accounting for differences in worker composition across firms by ranking firms based on wage premia, while, in Section 6, the analysis is repeated by taking account of the public sector as an additional state.

Overall job mobility

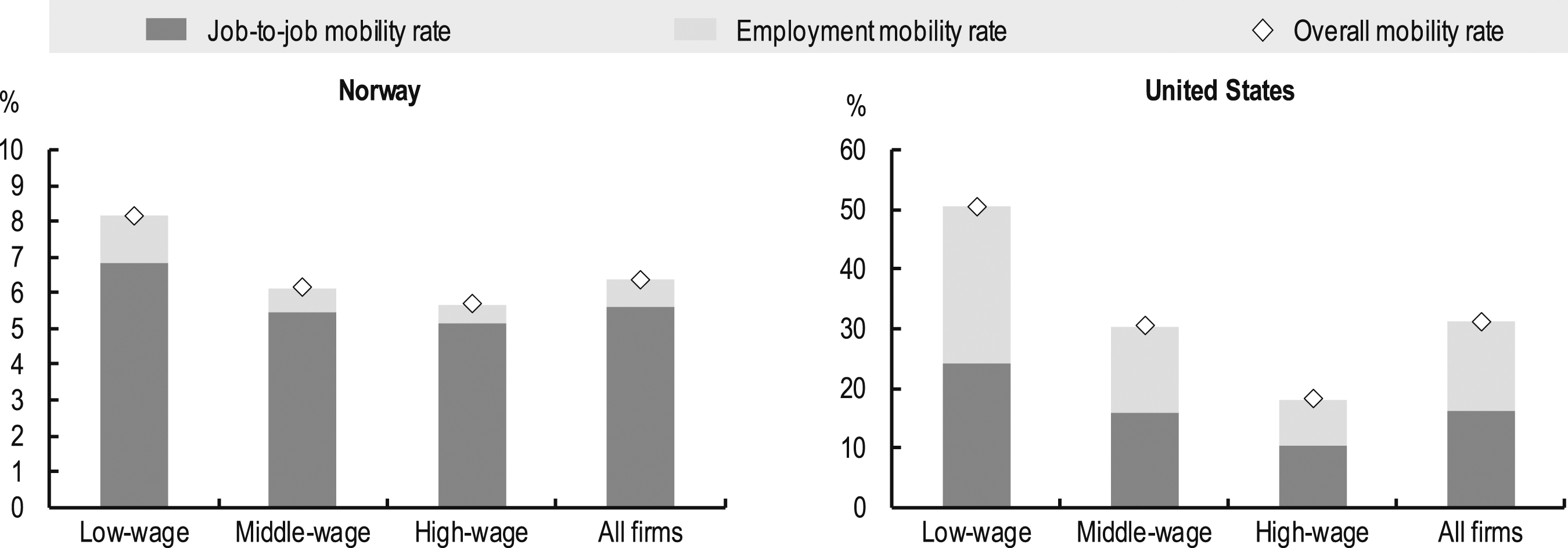

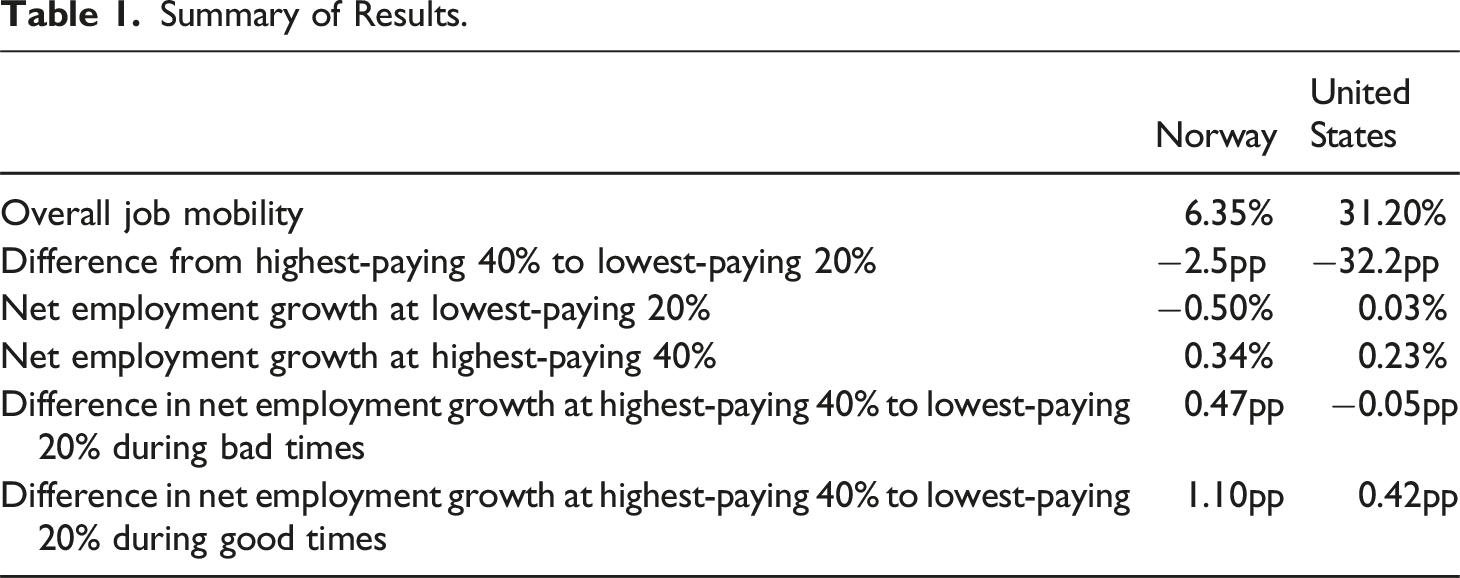

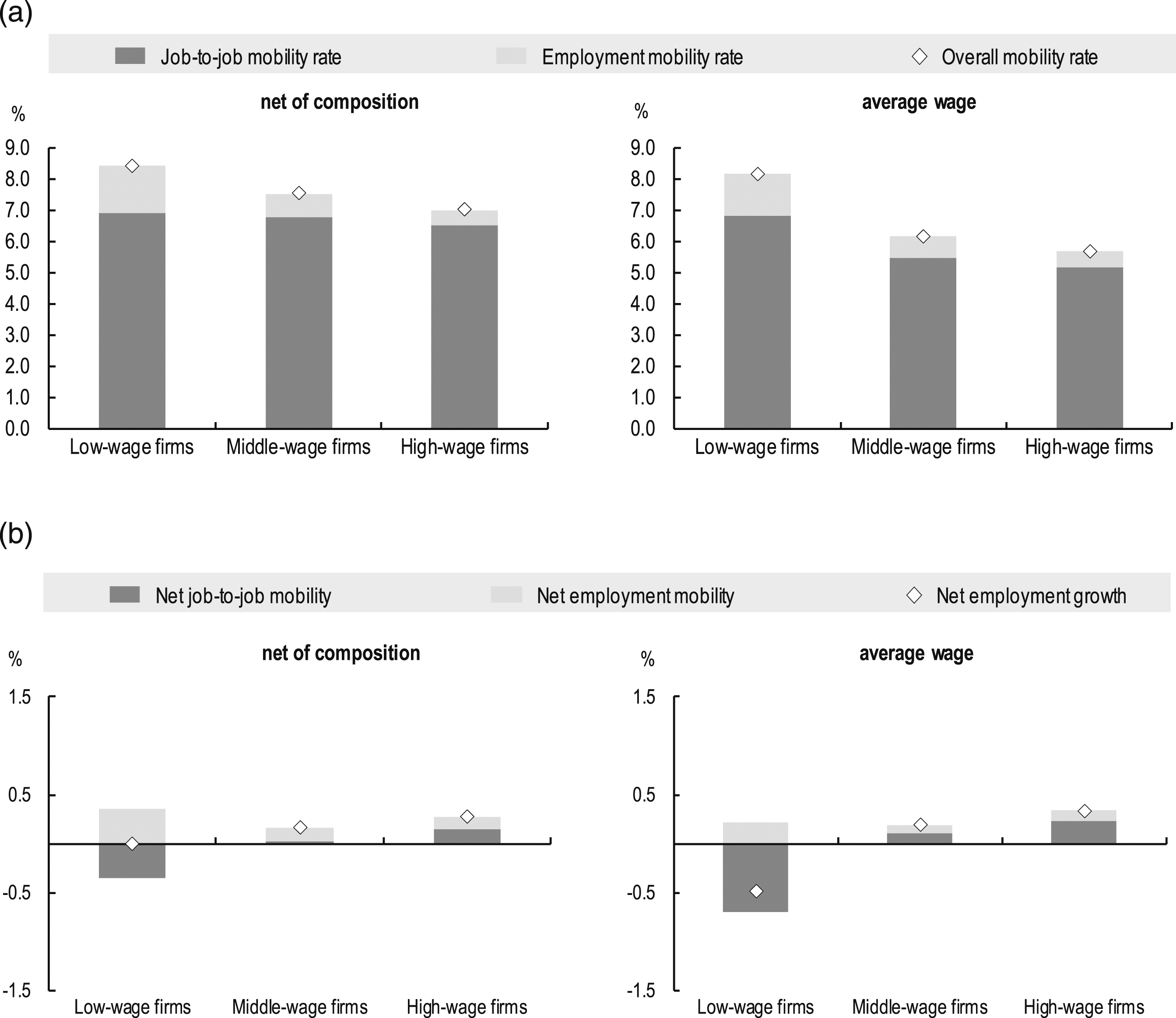

Overall job mobility is significantly lower in Norway than in the United States (Figure 1, all firms). The quarterly job mobility rate, defined by the sum of hires and separations in employment, equals 6% in Norway and 31% in the United States. In other words, overall job mobility is about five times as high in the United States as in Norway

4

. Lower mobility in Norway essentially reflects lower employment mobility, as the rate of job-to-job mobility is similar and may even be slightly higher in Norway. Low employment mobility in Norway may indicate that Norwegian workers face a much lower risk of job loss relative to their counterparts in the United States. Overall job mobility is low in Norway compared with the United States. The overall quarterly job mobility rate, the job-to-job mobility rate and the employment mobility rate by firm type, average the period 1998Q1-2011Q4. Note: Job-to-job mobility rate: the sum of hires and separations associated with direct job-to-job moves as a percentage of employment; Employment mobility rate: the sum of hires and separations associated with movements in and out of employment as a percentage of employment; Overall mobility rate: the sum of hires and separations as a percentage of employment. Low-wage firms: firms with average pay in the bottom quintile of the firm-wage distribution; Middle-wage firms: firms offering average pay in the second and third quintiles of the firm-wage distribution; High-wage firms: firms offering average pay in the top two quintiles of the firm-wage distribution. Source: Employment and poaching flows in the United States are based on Haltiwanger, Hyatt, Kahn et al. (2018). Calculations for Norway are based on employer-employee registry data (Aa-registeret) and the end-of year certificate register (lto-registeret).

Overall job mobility is higher in low-wage than in high-wage firms in both Norway (1.3 times) and the United States (about 2.3 times). For Norway, this is mainly due to the lower rate of mobility among low-wage firms than in the United States, as the rate of overall job mobility is more similar across countries among high-wage firms. Looking at the two components of job mobility separately, we observe that the gradients in job-to-job mobility and employment mobility over the firm-earnings distribution are less steep in Norway than in the United States. The rate of employment mobility is lower in all groups of firms in Norway than in the United States, but the difference is particularly large among low-wage firms. In both countries, employment mobility is relatively more important at the bottom of the wage distribution, but particularly so in Norway. Employment mobility accounts for 16% of all job flows in Norway for low-wage firms and 9% for high-wage firms compared with 52% and 42% respectively in the United States.

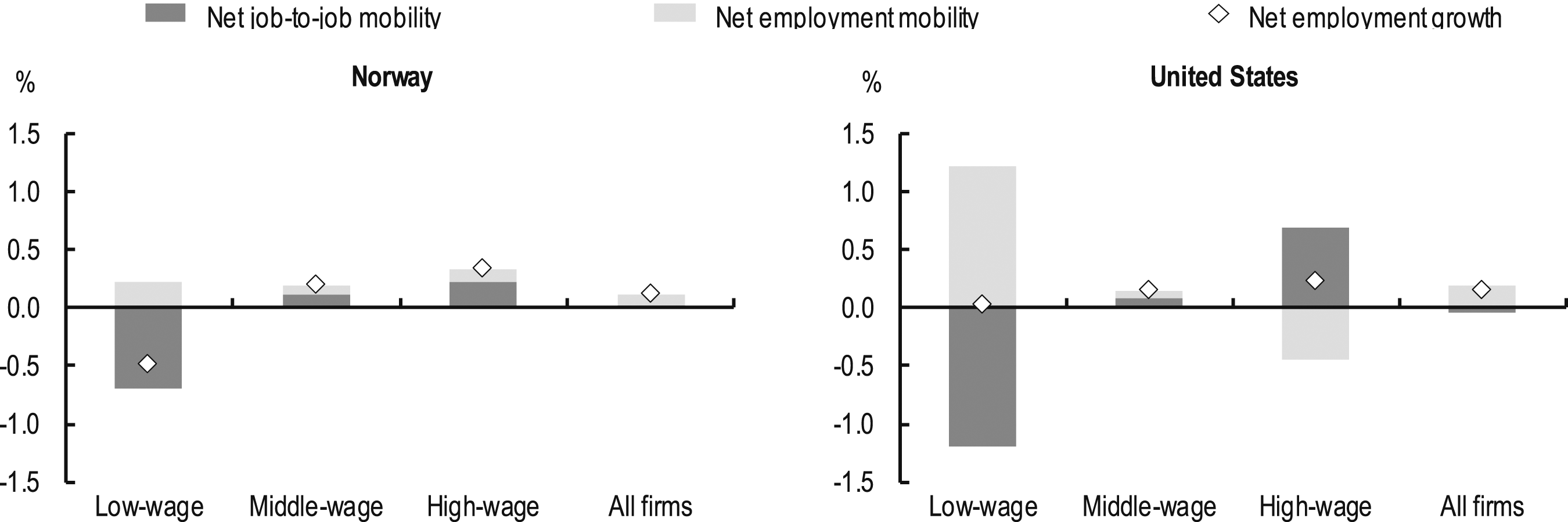

Importantly, overall job mobility in Norway and especially the United States overwhelmingly reflects excess turnover, that is, it does not result in changes in net employment or the structure of employment between firm types. Net employment growth by firm type, and the flows contributing to it, are tiny compared with the overall rate of job mobility (Figure 2). Consequently, the level of overall job mobility says little about the role of job mobility for the efficiency of job reallocation towards higher-wage firms. The key aspect is the direction of such mobility, and the ratio of directional moves out of all mobility seems to differ strongly between countries. Reallocation from low to high-wage firms equally fast in Norway than in the United States. Quarterly employment growth by firm type and the contributions of net job-to-job mobility and net employment mobility, average over the period 1998Q1-2011Q4. Note: Net job-to-job mobility: the differences in hires and separations associated with direct job-to-job moves as a percentage of employment; Net non-employment mobility: the difference in hires and separations associated with movements in and out of private sector employment as a percentage of employment; Net employment change: the differences in hires and separations as a percentage of employment. Low-wage firms: firms with average pay in the bottom quintile of the firm-wage distribution; Middle-wage firms: firms offering average pay in the second and third quintiles of the firm-wage distribution; High-wage firms: firms offering average pay in the top two quintiles of the firm-wage distribution. Source: Employment and poaching flows in the United States are based on Haltiwanger, Hyatt, Kahn et al. (2018). Calculations for Norway are based on employer-employee registry data (Aa-registeret) and the end-of year certificate register (lto-registeret).

Job mobility and reallocation

The rate of job reallocation jobs from low- to high-wage firms, is actually higher in Norway than in the United States (Figure 3). The quarterly net employment growth in high wage firms is 0.8 percentage points higher than low wage firms is in Norway and 0.2 percentage points higher in the United States. This is surprising considering the much greater degree of job mobility in the United States and the presence of larger pay differences between firms. Reallocation slows down in downturns, but generally higher in Norway than the United States. Net quarterly job-to-job and employment flow rates over firm types, average over periods where cyclical unemployment is below or above the HP-filtered trend, 1998Q1-2011Q4. Note: Net job-to-job mobility: the differences in hires and separations associated with direct job-to-job moves as a percentage of employment; Net non-employment mobility: the difference in hires and separations associated with movements in and out of employment as a percentage of employment; Net employment change: the differences in hires and separations as a percentage of employment. Low-wage firms: firms with average pay in the bottom quintile of the firm-wage distribution; Middle-wage firms: firms offering average pay in the second and third quintiles of the firm-wage distribution; High-wage firms: firms offering average pay in the top two quintiles of the firm-wage distribution. Good economic times are those with a negative or 0 deviation from the cyclical trend in unemployment (HP-filtered) while bad times are those with a high unemployment rate. Source: Employment and poaching flows in the United States are based on Haltiwanger, Hyatt, Kahn et al. (2018). Calculations for Norway are based on employer-employee registry data (Aa-registeret) and the end-of year certificate register (lto-registeret).

This apparent puzzle is due to the balance between job-to-job mobility and employment mobility. In the United States, high-wage firms exhibit both high rates of poaching and high rates of labour shedding. By contrast, in Norway high-wage firms grow relatively less by poaching workers from low-wage firms, and rely more on recruiting workers from non-employment. As a result, high-wage firms on average grow somewhat faster in Norway than in the United States. By the same token, low-wage firms downsize in Norway, while they remain stable in the United States. Low-wage firms in Norway tend to lose more workers to high-wage firms than that they can attract from non-employment. In the United States, low-wage firms fully offset the loss in workers due to poaching from higher-wage firms by hiring new workers from non-employment. The key difference therefore lies in the role of mobility in and out of private sector employment across high and low-wage firms.

Job-to-job mobility contributes to job reallocation in both countries because high-wage firms expand by poaching workers from lower-wage firms. The contribution of job-to-job mobility to job reallocation is more important in the United States because larger wage differences between firms make it easier for high-wage firms to poach workers from lower-wage firms. Employment mobility reduces the pace of job reallocation in both countries because low-wage firms stem the effects of poaching by high-wage firms on employment by hiring workers from non-employment. In the United States, this offsets most of the contribution of job-to-job mobility to reallocation. In other words, job ladders are more important in the United States for the wage progression of workers and channelling workers to their most productive use but are also less secure as workers are more likely to lose their jobs.

The role of the business cycle

Job-to-job and employment flows are expected to behave differently over the business cycle. The job ladder based on job-to-job mobility tends to be pro-cyclical, collapsing in bad economic times due to the decline in hiring, resulting in a sullying effect on efficiency-enhancing job reallocation and hence overall productivity and wage growth. On the other hand, flows in and out of employment tend to be counter-cyclical, with recessions potentially being associated with a cleansing effect whereby poor performing firms shrink or even leave the market (Haltiwanger et al., 2021). Consequently, the effect of the business cycle on job reallocation is ambiguous.

Figure 3 analyses reallocation between low and high wage firms separately in periods with positive and negative cyclical unemployment (obtained after removing the trend of unemployment with a Hodrick-Prescott filter). It shows that job reallocation is strongly pro-cyclical in both countries, with employment in high-wage firms expanding more strongly in good times and employment in low-wage firms remaining stable in the United States and declining more strongly in Norway. As expected, the strong pro-cyclicality of job reallocation is almost entirely driven by the pro-cyclicality of net job-to-job mobility.

Moscarini and Postel-Vinay (2012) argue that the strong pro-cyclicality of high-wage employment in the United States reflects the weaker incentives of high-wage firms to hoard workers during bad times. Since high-wage firms tend to be more productive, they can poach workers from lower-wage firms during expansions relatively easily by offering higher wages. In Norway, where wage differences between firms tend to be smaller, high-wage firms do not shed more workers than low-wage firms, even during periods of high cyclical unemployment.

The relationship between job mobility and reallocation over the business cycle is analysed more formally by regressing the differential net job flows between high and low wage firms (and its components) on cyclical unemployment as measured by the deviation of unemployment from a HP-filtered trend (same as in Figure 3). The results confirm that job reallocation is pro-cyclical in both countries and largely driven by job-to-job mobility (Annex Table 1). Figure A1 in the appendix presents the seasonally adjusted unemployment rate and the overall job-to-job and employment mobility rates over time.

Summary

Summary of Results.

Additional results unpacking workforce composition and the public sector

Workforce composition

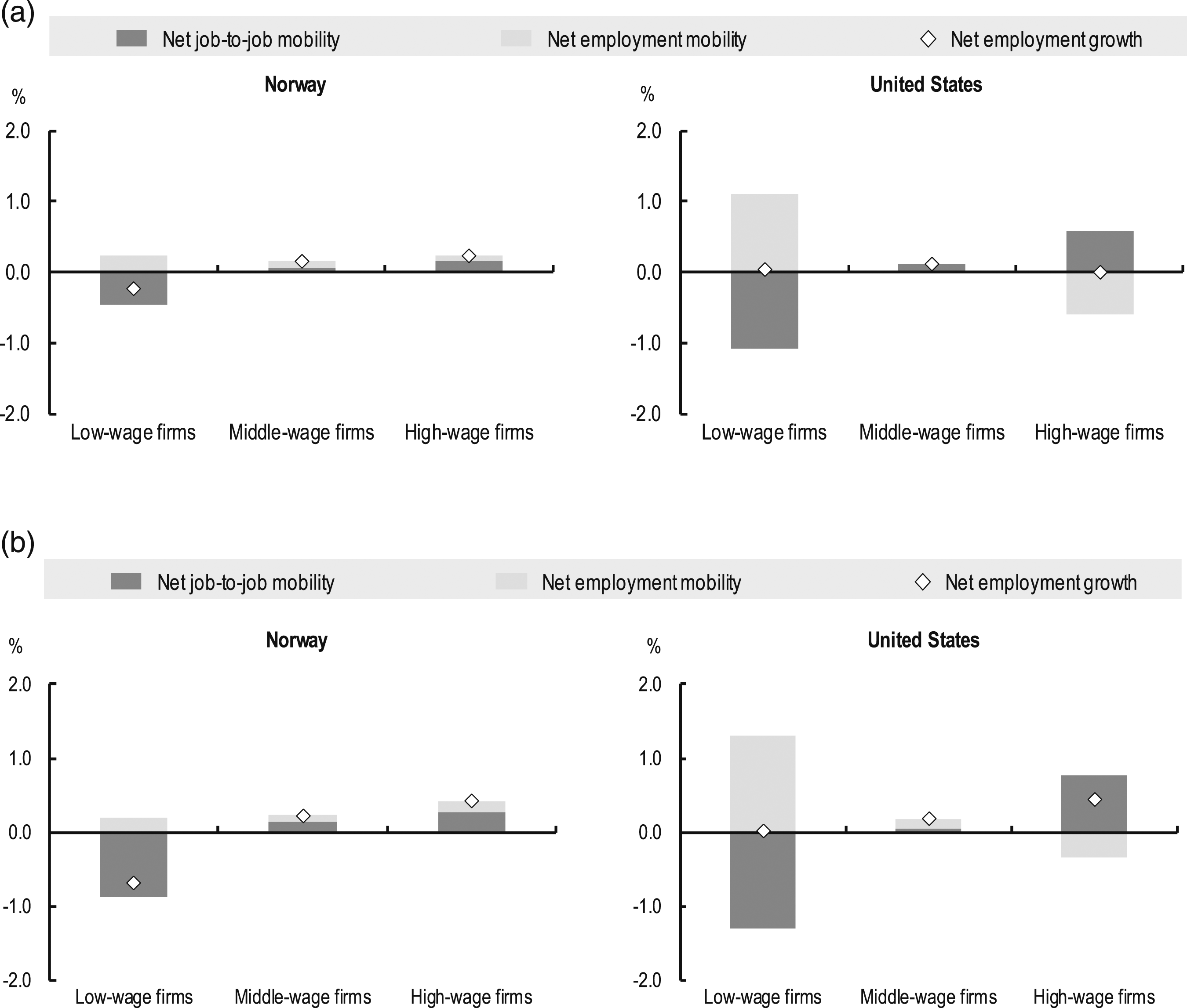

A key assumption in the baseline analysis is that average firm wages reflect at least to some extent firm wage premia and not just differences in worker composition. In a first step, we document how worker wages change as they transition between firms paying different wages using data for Norway (Annex Figure A2). This shows that, indeed, workers moving from high to low-wage firms experience significant earnings declines, whereas workers moving from low-wage to high-wage firms experience significant earnings increases.

In a second step, we repeat the baseline analysis in the previous section while ranking firms based on the part of wages that is determined by the characteristics of firms rather than the observed composition of their workforce, that is, instead of unadjusted average firm wages.

5

We find that results are qualitatively unchanged (Figure 4 and Annex Figure A3), although the speed of reallocation is somewhat lower indicating workers do not just move to better paying firms but also firms with more skilled workers as they advance in their careers. As before, we also find that job reallocation is strongly pro-cyclical and that this is entirely driven by the cyclicality of job-to-job mobility. Overall mobility and net flows when accounting for composition in Norway. The overall quarterly job mobility rate, the job-to-job mobility rate and the employment mobility rate (a) and net flows (b) by firm type based on firm premia (left) or average wage (right), average for the period 1998Q1-2011Q4. Note: The figure shows total quarterly mobility and net flows as defined in the text, when classifying private sector firms based on their firm premia. Low-wage firms: firms with average pay, accounting for worker composition in the bottom quintile of the firm-wage distribution; Middle-wage firms: firms offering average pay, accounting for worker composition, in the second and third quintiles of the firm-wage distribution; High-wage firms: firms offering average pay in the top two quintiles of the firm-wage distribution, accounting for worker composition. Source: Calculations for Norway are based on employer-employee registry data (Aa-registeret) and the end-of year certificate register (lto-registeret).

The role of the public sector

The analysis so far excluded the public sector, consistent with the work by Haltiwanger, Hyatt, Kahn et al. (2018) for the United States. However, the public sector is much more important in Norway than in the United States, accounting for 31% of employment in 2019 versus 15% in the United States (OECD 2021). The analysis is therefore repeated while accounting for flows between the private and the public sector. Note that doing so does not affect the components associated with job-to-job mobility and employment mobility in the private sector. Flows between the public sector and non-employment are ignored for the present purposes.

Job flows between the private and public sector are quantitatively important and reduce the overall speed of job reallocation as flows from the public sector primarily go to low-wage firms in Norway, as shown in figure A4 in the appendix. After taking account of the public sector, the speed of job reallocation is slower than that in the private sector in the United States. However, it is not clear how including the US public sector would change these results. Even if the speed of job reallocation would not be affected though, it would still be true that job reallocation is relatively high in Norway given the much lower rate of overall job mobility. Large net inflows from the public sector to an important extent reflect the transition of young workers, who start their career in the public sector (perhaps as part of their national service or as part time jobs in conjunction with education) and subsequently move to the private sector (see figure A5 in the Annex). Finally, figure A6 in the online annex shows net inflows from the public sector are strongly pro-cyclical in Norway, particularly at high-wage firms. While in good years, employment among high-wage firms grows by 0.5% on average per quarter due to net inflows from the public sector, this drops to zero during bad economic times. While net inflows from the public sector also decrease in low-paying firms, they remain strongly positive. The public sector then seems to hold an important reserve of labour that is not as sensitive to the business cycle as employment in the private sector.

From a reallocation perspective, the public sector plays a similar role in Norway as non-employment in the United States. Partly, this may reflect the use of these jobs as a labour market policy aimed at reaching high employment rates (Berglund et al., 2010). The use of these labour market policies has declined over time (Nekby 2008) which is consistent with what we see in our data. Indeed, we find substantial flows from non-employment to public sector employment and larger inflows for lower educated and young workers than higher educated and older.

The role of job mobility and reallocation for aggregate wage growth

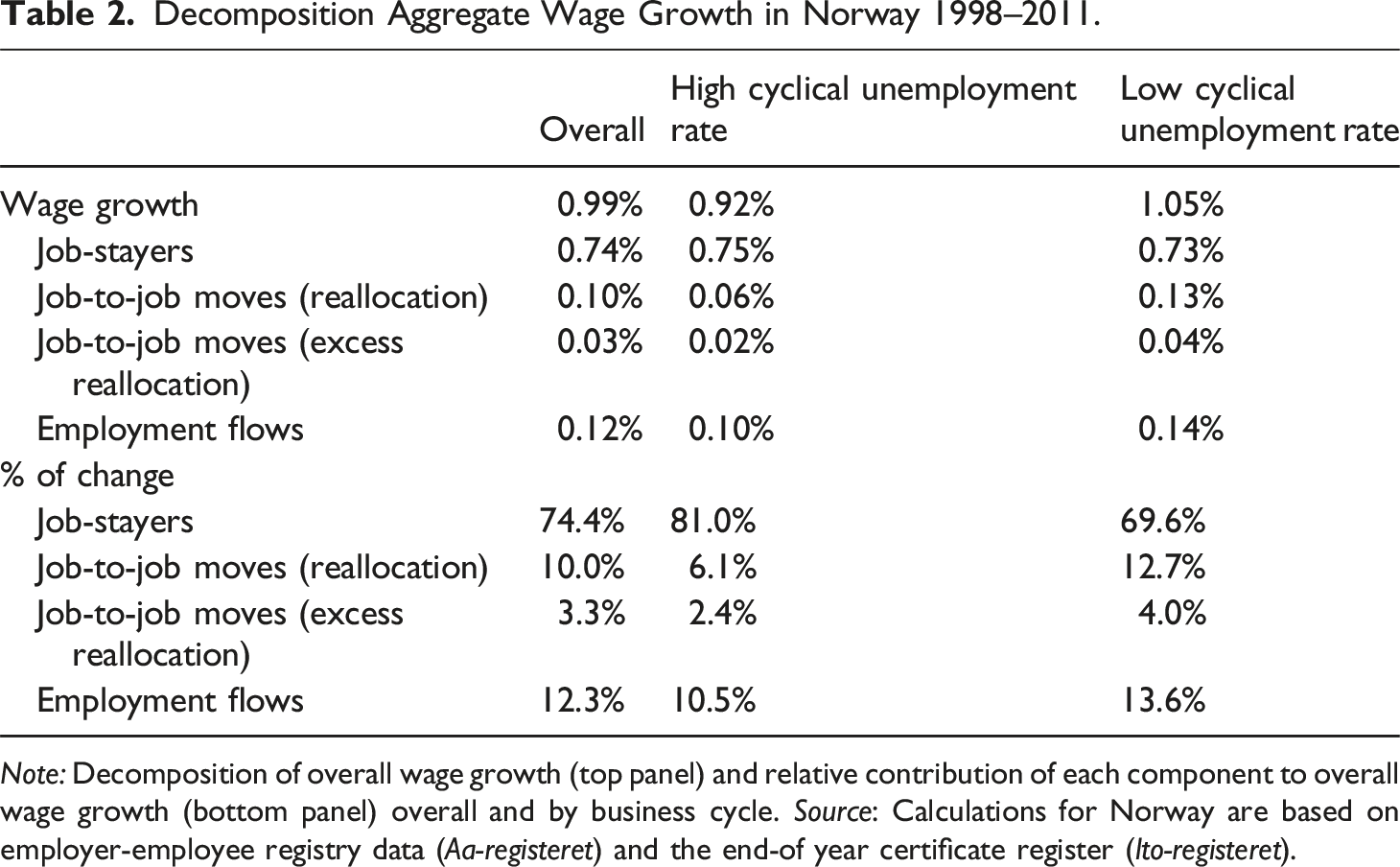

Decomposition Aggregate Wage Growth in Norway 1998–2011.

Note: Decomposition of overall wage growth (top panel) and relative contribution of each component to overall wage growth (bottom panel) overall and by business cycle. Source: Calculations for Norway are based on employer-employee registry data (Aa-registeret) and the end-of year certificate register (lto-registeret).

Real average aggregate quarterly wage growth during the period 1998–2011 in Norway amounted to about 1%. Three quarters of this was due to on-the-job wage growth, while the remainder reflected different forms of job mobility. Thirteen percent of aggregate wage growth was made up of job-to-job mobility between and within firm-wage groups, with the main part of this being due to moves between groups of firms rather than within a group of similarly paying firms. When using five quintile groups rather than the three groups the relative importance of job-to-job flows rises slightly from 10 to 12%. Employment mobility also contributes to average wage growth as there is an overall inflow from non-employment to employment, and especially among the higher-paying firms the wage of new entrants tends to be somewhat higher than that of those that leave the workforce.

As one would expect, wage growth slows in periods of high cyclical unemployment, and this is almost entirely driven by a lower contribution of job-to-job mobility (both with and between firm wage groups). Wages of job stayers appear largely to be a-cyclical. Third, the contribution of employment mobility to aggregate wage growth also is slightly pro-cyclical.

These findings are in line with Haltiwanger, Hyatt, Kahn et al. (2018) and Hahn et al. (2017) for the United States, which show that the breakdown in this job ladder has a negative impact on overall wage growth and that these flows are more susceptible to the business cycle than on-the-job wage growth.

Discussion and conclusion

In an effort to enhance our understanding of the way economic and social progress materialises under very different institutional settings, this paper focuses on the role of job mobility for reallocation in Norway and the United States using detailed linked employer-employee data. The main findings can be summarised as follows: • The speed of worker reallocation from low to high-wage firms is at least as high in Norway as in the United States, despite the much lower rate of overall job mobility in Norway. There is therefore no indication that wage compression in Norway slows job reallocation. While job-to-job mobility indeed moves fewer workers from low- to high-wage firms in Norway than in the United States, employment mobility complements such job ladders in Norway while it counteracts them in the United States. This may reflect more successful activation and guiding unemployed to better matches. • In both Norway and the United States, the process of job reallocation is strongly pro-cyclical and this is entirely driven by job-to-job mobility. In the United States, high-wage employment is pro-cyclical as high-wage firms face weaker incentives for labour hoarding during economic downturns, whereas employment in low-wage firms tends to be a-cyclical. In Norway, low-wage employment is counter-cyclical as low-wage firms have difficulty replacing poached workers by workers from non-employment. In fact, low-wage firms mainly hire workers from the public sector to maintain employment. • In Norway, on-the-job wage growth accounts for the bulk of aggregate wage growth but job-to-job mobility accounts for most of its cyclicality. While we do not have comparable results for the United States, Haltiwanger, Hyatt, Kahn et al. (2018) and Hahn et al. (2017) report qualitatively similar findings. While the speed of job reallocation may be similar in Norway and the United States, wage differences between firms are much larger in the United States, making this a potentially much more important channel of aggregate wage growth.

From a policy perspective, this paper shows that policy makers should not seek to promote overall job mobility, but instead make job mobility more effective as a channel for career progression and achieving a more efficient allocation of resources. In this respect, two points are worth highlighting. First, the example of Norway suggests that having a compressed wage structure does not necessarily have to be a major impediment to the efficacy of worker reallocation. Second, there could also be too much job mobility when firms have weak incentives for labour hoarding in the context of temporary shocks. Excessive employment mobility could result in higher job insecurity for workers and undermine the efficient allocation of resources. Job retention policies provide one way to support labour hoarding during a recession (OECD 2021).

Supplemental Material

Supplemental Material - Job mobility, reallocation and wage growth: A tale of two countries

Supplemental Material for Job mobility, reallocation and wage growth: A tale of two countries by Alexander Hijzen, Mats Lillehagen, and Wouter Zwysen in European Journal of Industrial Relations.

Footnotes

Acknowledgement

This paper is a revised version of ![]() , which benefited from comments by Erling Barth, Sebastian Barnes, Stephane Carcillo, Harald Dale-Olsen, Philip Hemmings, Michael Koelle, Urban Sila and Ola Vestad, as well as from the feedback of the editor and anonymous reviewers. The views in this paper are those of the authors and cannot be attributed to the OECD or its member countries. Any remaining errors are the responsibility of the authors.

, which benefited from comments by Erling Barth, Sebastian Barnes, Stephane Carcillo, Harald Dale-Olsen, Philip Hemmings, Michael Koelle, Urban Sila and Ola Vestad, as well as from the feedback of the editor and anonymous reviewers. The views in this paper are those of the authors and cannot be attributed to the OECD or its member countries. Any remaining errors are the responsibility of the authors.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Research Council of Norway [Grant 202479 and grant 287016].

Supplemental Material

Supplemental material for this article is available online.

Notes

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.