Abstract

This study concentrates on the effect of foreign ownership of companies on worker wage distribution. Using an innovative methodological approach that combines the Oaxaca–Blinder decomposition and the modified DiNardo et al. reweighting approach, we estimate the wage gap between domestic-owned and foreign-owned firms. The study confirms that firm ownership (domestic or foreign) influences the wage distribution of workers, as a worker employed in a foreign-owned firm earns, on average, 5 percent more than a matched worker in a domestic-owned firm with similar characteristics. We link that gap with an origin of foreign capital. This analysis demonstrates that the origin of capital has an impact on wage distribution in the firm and may affect wages in the whole section.

Keywords

Introduction

Since the second wave of globalization, the worldwide economy has become more integrated, and globalization has supported income growth and poverty reduction, especially in less developed regions. It has also had strong impact on local labour markets. Stronger international trade, increased migration and the possibility to invest abroad have influenced labour markets, including employment and labour conditions. Specifically, the impact of foreign firms on wages has received increased attention from economists. Capital movements have been increasing constantly in recent years, and as a result, employment in foreign-owned firms has considerably increased, especially as foreign-owned firms pay higher wages than domestic-owned firms.

The two main strands of literature on the effect of foreign ownership on wages differ in the analysed effect. The first analyses the acquisition or privatization effect on wages and compares wages of workers before and after the foreign acquisition of a firm. The second analyses the presence of foreign capital in the firm or in the economy. Our work contributes to the latter.

There are several explanations for why foreign-owned firms offer higher wages, and the most plausible is that foreign investors as employers attract the best, usually highest skilled, candidates. If this hypothesis holds, foreign firms employing mostly low-skilled labour will pay market wages, while those employing high-skilled individuals will pay higher wages than their domestic rivals.

This study examines how foreign ownership of companies affects wage distribution of workers. Our main research hypothesis is as follows. Firm ownership (domestic or foreign) does not influence the wage distribution of workers. The existing differences in wages between domestic-owned and foreign-owned firms are attributed to factors other than ownership. This hypothesis is verified across the Statistical Classification of Economic Activities in the European Community (NACE) sections of the economy. We assess to what extent the wage premium of foreign-owned firms reflects selection, as they may cherry-pick workers and target the best domestic firms for acquisition and the most promising industries for greenfield start-ups.

This study concentrates on the effect of foreign ownership of companies on worker wage distributions, contributing to the research in several ways. First, we estimate the wage gap between the domestic-owned and foreign-owned firms and link that gap with the origin of foreign capital. To the best of the authors’ knowledge, this aspect has not been analysed in the literature. Second, this is the first study on a transition economy that shows the impact of foreign ownership on domestic firms’ worker wages in the same economic section. Third, our novel methodology involves studying differences in gross wages between workers in foreign-owned and domestic-owned firms using different econometric methods. We follow and adapt the innovative methodological approach of Majchrowska and Strawiński (2018) that combines two methods: Oaxaca–Blinder decomposition and the modified DiNardo et al. (1996) reweighting approach. The modification in the reweighting scheme is an adjustment for differences at two distinct levels: firm and individual. A two-step matching procedure verifies the main hypothesis.

Considering the regional dimension, we concentrate on the biggest representative among the Central and Eastern European countries: Poland. Before 1990, foreign participation in the Polish economy was restricted. As in other centrally planned economies, only after implementing new laws in the transition process could Poland benefit from foreign direct investment (FDI) inflows. Consequently, especially in recent years, employment in entities with foreign capital has been increasing at a faster pace than employment in the national economy. In 2017, about 10 percent of entities employing 10 or more employees in Poland were at least partially owned by foreign investors (Central Statistical Office (CSO), 2017, 2018).

Three main findings emerge from our study. First, we find observable differences in wage distributions between domestic-owned and foreign-owned firms. We confirm that firm ownership (domestic or foreign) does influence the wage distribution of workers in the sense that workers employed in foreign-owned firms earn, on average, 5 percent more than matched workers of domestic-owned firms with similar characteristics. Second, we show that the origin of foreign capital has an impact on economic sections in which investments are made, and they impact the wage premium of foreign ownership. Third, this is the first study on a transition economy that shows a larger share of foreign-owned firms in the NACE section and finds higher wages among workers of domestic-owned firms.

The structure of the rest of this article is as follows. Section ‘Literature review’ briefly reviews the relevant literature in this field. In section ‘Data treatment and description’, we present the data and conduct sample construction. In section ‘Methodology’, we present the methodology of the research. The empirical model and results are presented in section ‘Empirical model and results’. Section ‘Conclusion’ concludes.

Literature review

Several empirical studies have examined the effect of foreign ownership on wages. This section reviews the main contributions in empirical literature, presenting works by how they explain the wage premium from foreign ownership.

As mentioned, this literature is divided into two categories. First, many works concentrate on the acquisition effect on wages, showing that foreign acquisitions of domestic firms have positive effects on the average wages in acquired firms (Brown et al., 2010). Second, some authors concentrate solely on the ownership effect and find that workers in industries with greater foreign presence enjoy higher wages (Aitken et al., 1996; Feliciano and Lipsey, 2006).

Most economic research in both categories shows that foreign-owned firms pay higher wages than their domestic-owned counterparts. The estimates of the average wage effect for foreign ownership range between 10 and 70 percent (Heyman et al., 2007). The literature shows this persistence effect even after controlling for sectoral, regional and firm-level characteristics.

Regardless of the cause of foreign capital in a firm, several explanations of the wage premium are possible. First, there are substantial differences between domestic-owned and foreign-owned firms. A frequent finding in the literature is that foreign-owned firms are more productive (Brännlund et al., 2016), as higher productivity translates to higher wages. However, higher wages in foreign-owned firms may increase the equilibrium wage in the whole section and thus spill over into higher wages in domestic firms. Aitken et al. (1996) investigate wages paid by domestic-owned and foreign-owned firms in Mexico, Venezuela and the United States, showing that while foreign investment in a section leads to higher productivity and hence higher wages, in the same section, wages increase in domestic firms in Mexico and Venezuela. Girma and Görg (2007), studying the United Kingdom, find that foreign-owned firms pay higher wages than comparable domestic firms, and the magnitude of these wage premia differs for skilled and unskilled workers. Egger et al. (2020) provide evidence for a foreign ownership wage premium in Germany. They also show that this wage premium differs by skill group.

As such, labour market research has confirmed wage differences across industries and sectors (Krueger and Summers, 1988). Foreign-owned firms may be located in higher paying industries or sectors, especially as those firms that offer better pay tend to be more productive. Another reason for wage differences between foreign-owned and domestic-owned firms may stem from geographical location, as regional differences in wages are observed in many countries (Aitken et al., 1996). If foreign firms tend to locate in regions with higher wages, this may partially explain the analysed wage gap.

A relatively simple, but plausible, explanation of these wage differences may be due to larger firms paying higher wages, which empirical research confirms (Hollister, 2004). Foreign-owned firms tend to be larger than domestic firms, and this size effect may contribute to the wage gap.

Second, foreign-owned firms are often accused of cherry-picking acquisition objects and workers. Frequently, this issue is analysed in the context of foreign acquisition of a firm. For Portugal, Almeida (2007) shows that although the workforce in foreign-owned companies was better skilled and paid higher wages, these differences were entirely attributable to cherry-picking of acquisition objects by foreign investors. However, using Portugal data in a matched employer–employee panel, Martins (2004) shows that the foreign-firm premium is large and significantly positive but falls substantially when firm and worker controls are added. Moreover, using the difference-in-differences (DID) approach, no effect on individual wages was found after foreign acquisition of Portuguese manufacturing firms. These results suggest that the foreign-firm wage premium commonly documented in the literature may be exaggerated due to a combination of two factors: lack of a proper like-for-like comparison between domestic and foreign firms, and workers’ unobserved heterogeneity, though to a small extent.

While several studies find that part of the wage differential can be explained by firm and worker characteristics (Feliciano and Lipsey, 2006 (United States)), another part of it remains unaccounted. Bircan (2013) uses detailed plant-level data from Turkey and shows that up to 15 percentage points of the multinational wage premium can be explained by the level of foreign ownership per se.

Recent studies deal with the issue of the origin of the capital and its impact on wages. Setzler and Tintelnot (2019) disaggregate the foreign wage premium in the United States by country of origin and find larger premiums in origin countries with greater GDP per capita. Although they analyse multinational companies, which are defined slightly differently than firms with foreign capital are, their results suggest that the origin of capital matters. In addition, Hjort et al. (2020) find strong evidence that many multinational firms ‘anchor’ the wages they pay abroad to the wages at headquarters.

Considering empirical evidence of foreign ownership and wages in the Central and Eastern European (CEE) regions, most studies concentrate on the privatization (acquisition) effect on wages. Brown et al. (2010) analyse the effect of privatization on workers using data on manufacturing firms in four CEE countries for 1992–2004. Their results indicate positive effects on wages and no negative effects on employment. These effects are explained by enhanced firm efficiency. Considering Hungary for 1986–2008, Earle et al. (2018) study the wage effects of FDI and find that foreign acquisition of a firm raises average wages by 15–29 percent. The wage gains are larger for university-educated workers and those in high-skill occupations.

Using a standard supply and demand framework for labour, Faggio (2001) analyses the link between FDI and wages in Poland, Bulgaria and Romania. The study finds that in manufacturing in Poland, higher levels of foreign activity are associated with higher local wages, and there are positive FDI spillovers from foreign to domestic producers. Moreover, there is a link between the FDI impact on wages and the section of activity in which firms operate. Konings (2000) uses firm-level panel data to investigate the effects of FDI on the productivity performance of domestic firms in Bulgaria, Romania and Poland. Although it does not investigate wages, the study finds that, in Poland, foreign firms perform better than firms without foreign participation, and there are no spillovers to domestic firms in Poland. To some extent, these findings imply that a higher productivity performance could possibly translate into higher wages. Bedi and Cieślik (2002) analyse the overall impact of FDI on the economy while concentrating on wage determinants. They find that wages are higher in industries with greater foreign participation, and workers in those industries experience faster wage growth. However, they do not distinguish between domestic and foreign firms.

This study fills the gap in the literature by analysing the effect of firm foreign ownership on worker wages in Poland. We assume that, after 30 years of the decentralization of the Polish economy, the acquisition effect has been sufficiently analysed. To some extent, we expect analogous results to Almeida (2007), who study Portugal at the turn of the century, which has similarities to Poland 15 years after the European Union (EU) accession. We focus on firms that have foreign capital and not on the effect of acquisition.

Data treatment and description

The data on monthly salaries and individual characteristics of employees used in this study were obtained from the Structure of Wages and Salaries by Occupations (SES) database, provided by CSO Poland. It is a part of the Eurostat Structure of Earnings Survey, a large enterprise sample survey providing detailed and comparable information on the relationships between the level of remuneration and individual characteristics of employees and employers. It is conducted every 2 years. The database includes both full- and part-time employees who worked for the whole month of October in the surveyed years. The survey covers around 13 percent of enterprises in the national economy that have more than nine employees. 1 According to the CSO (2017) report on business activity of entities with foreign participation operating in the Polish economy, the share of employment in micro firms (up to nine workers) does not exceed 1.5 percent of total workers employed by foreign-owned firms. However, over two-thirds of the foreign capital is located in firms employing 250 or more workers and are responsible for the employment of three-fourths of the total workers employed by foreign-owned firms.

The underlying advantage of the SES data is the high reliability of information on salaries, as they are reported by the accounting departments. In addition, the size of the SES data is advantageous, with nearly 800,000 individual observations in 2016. The SES database contains information on individual salaries (in local currency: PLN); number of hours worked; and several personal characteristics, such as gender, age, education level, work tenure and occupational group. It also includes employer characteristics, such as ownership sector, size of enterprise and location, as well as the NACE section. There are two types of salary information: for October of the given year and for the whole year. In Poland, wages are paid monthly; therefore, as a dependent variable, this study uses the full-time equivalent monthly salary, which includes wages and salaries, overtime pay, bonuses, pay for piecework and shift work, allowances, fees, tips and gratitude, commissions and remuneration in kind. We use monthly salary as it is usually the monthly remuneration set in the employment contract.

The SES data are complemented with information on labour productivity and accident risk, which may be interrelated to foreign ownership. To control for the differences in productivity among economic NACE sections, we use labour productivity measured as gross value added in 1000 euros per employee provided by Eurostat. If foreign-based investors provide more efficient technologies, higher wages may occur due to new technology and not foreign ownership. Castelman (2016) argues that despite agreement on some measures, the relocation of hazardous industries to less restrictive countries continues to exist. As labour protection legislation and environmental protection law are less restrictive in Poland than in other EU-15 members, we control for accident risk. We use official register data collected from statistical cards on accidents at work in Poland to estimate serious or fatal occupational injury risk, as this measure explains a significant share of wage level and wage gap among workers (Strawiński and Celińska-Kopczyńska, 2019).

We impose some limitations on the dataset. First, to prevent results impacted by outlying observations, we remove individual wage observations below the 1st percentile, which are below the national minimum, and above the 99th percentile. Second, we exclude individuals working on contracts other than permanent and fixed-term contracts, that is, workers employed to perform a specific job and those undergoing a trial period, which constitute 1.8 percent of employees in the private sector. Third, as not more than 5 percent of workers in the private sector work on part-time contracts, we excluded them from the analysis. As the study is focused on foreign firms in the private sector, we limit the SES sample to private sector workers. The sample is drawn a year before the survey so that some workers employed in smaller firms could be surveyed, as the registered information may not be actual. We decided not to include that information as it is not representative of the economy. In addition, persons working in agriculture are not included in the final sample because they consist mostly of self-employed workers. Furthermore, we restrict the sample to persons aged 20–59 years. Most workers under 20 years in Poland are employed on short-term civil contracts. The upper-bound restriction is set based on the official retirement age so that workers in the pre-retirement age are protected.

Finally, NACE subsections with no foreign firms (water collection, treatment and supply; remediation activities and other waste management activities; veterinary activities; and creative, arts and entertainment activities) are excluded from the sample, which account for 303 observations. After all adjustments, the sample consists of 395,368 observations representing 4,679,063 workers (over 86 percent of private sector workers), of which 134,747 observations are for workers in foreign-owned firms, which correspond to 1,432,496 workers. The sample is reweighted to reflect the structure of the employee population.

The analysis focuses on foreign firms, and in the FDI literature, an investor is ‘foreign’ in terms of the residency address. There are three types of foreign ownership: (1) influence ownership – a single foreign investor directly owning at least 10 percent of shares in a company, with the purpose of gaining an effective voice in its management; (2) control ownership – more than 50 percent ownership; and (3) ultimate ownership – foreign investors possess 100 percent ownership. We distinguish only between the narrow definition (3) of foreign firms (foreign property only) and the wide definition (1). 2

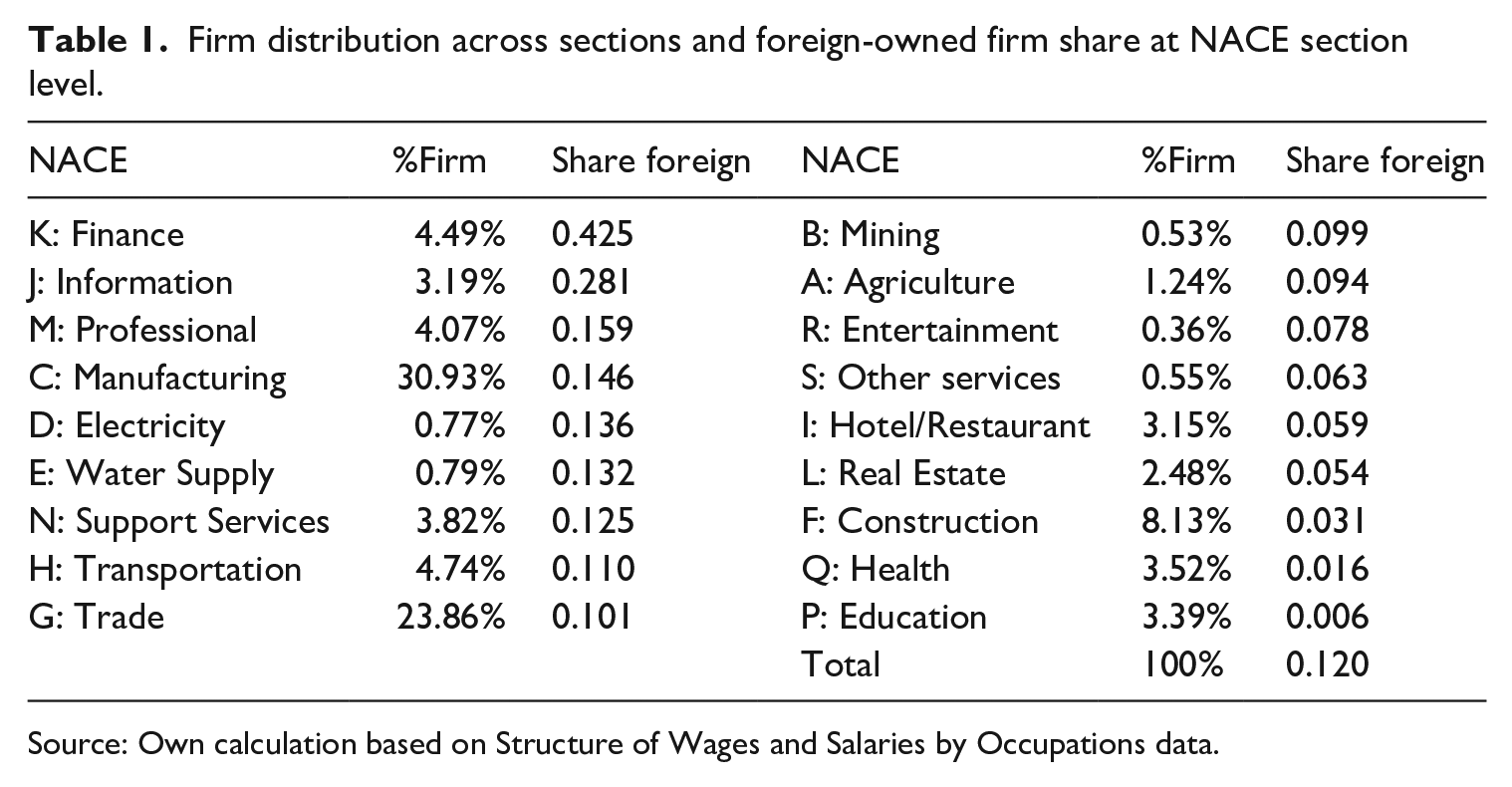

In the analysed dataset, the share of foreign firms varies across different economic activities. Table 1 presents the distribution of analysed firms among NACE sections (column %firm) and the share of foreign-owned firms in each section (column share foreign). Most of the analysed firms operate in the sections of Manufacturing (C) as well as Wholesale and Retail Trade and Repair of Motor Vehicles and Motorcycles (G, hereafter: Trade). The highest proportion of foreign-owned firms are in Financial and Insurance Activities (section K, hereafter: Finance) and Information and Communication (section J, hereafter: Information). Overall, 12 percent of firms (weighted by employment) are foreign-owned.

Firm distribution across sections and foreign-owned firm share at NACE section level.

Source: Own calculation based on Structure of Wages and Salaries by Occupations data.

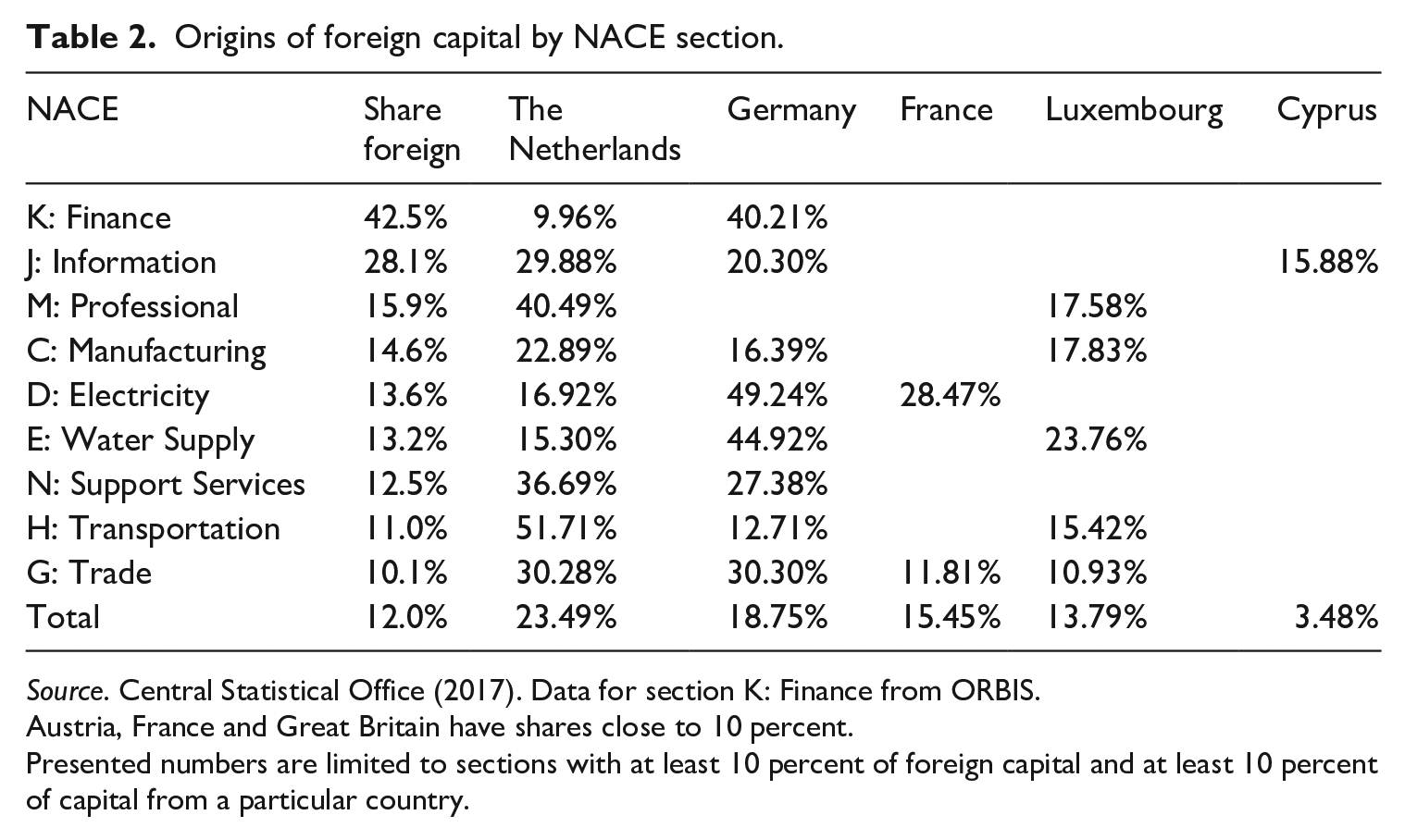

According to CSO (2017), more than 70 percent of foreign-owned capital invested in Poland came from four countries: the Netherlands, Germany, France and Luxembourg. The majority, over 55 percent of those investments, are in the Manufacturing and Trade sections. However, the sections with the highest share of foreign capital are Finance and Information. Clearly, the investment portfolio differs by country. Firms from two countries with the largest share in foreign investment in Poland (the Netherlands and Germany) have business activities across all economic sections. However, investors from France are focused on the Electricity, Gas Steam and Air Conditioning Supply (section D, hereafter: Electricity) and Trade sections. Capital from Luxembourg is invested mostly in selected areas of the economy (see Table 2).

Origins of foreign capital by NACE section.

Source. Central Statistical Office (2017). Data for section K: Finance from ORBIS.

Austria, France and Great Britain have shares close to 10 percent.

Presented numbers are limited to sections with at least 10 percent of foreign capital and at least 10 percent of capital from a particular country.

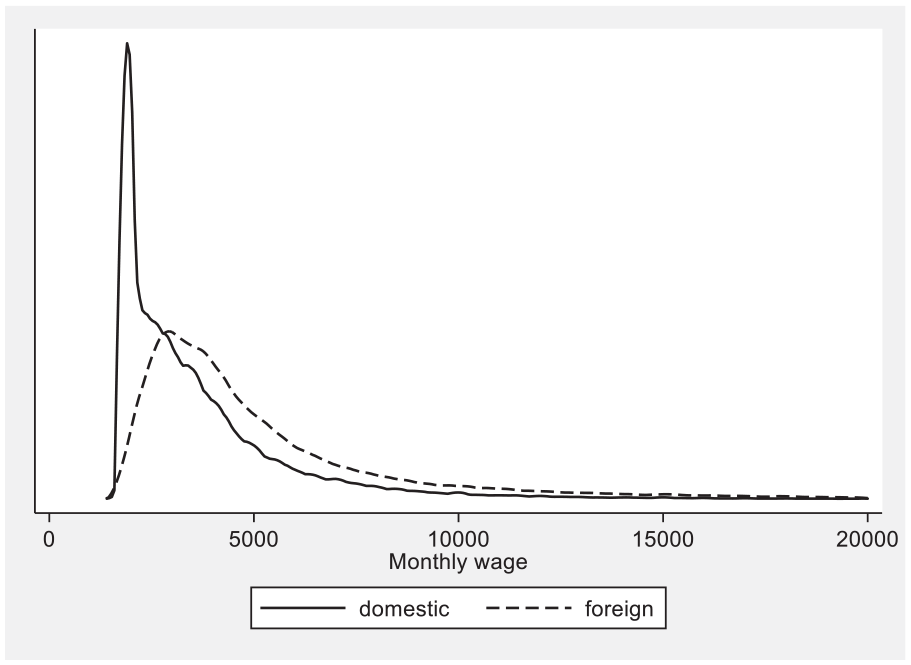

There is a visible discrepancy between domestic-owned and foreign-owned firms in terms of worker wage distributions (Figure 1). As worker wage distribution, we understand the distribution of wages within a given firm. The difference in the left tail of wage distributions stems from the fact that while a significant number of workers earn the minimum wage or just above in domestic-owned firms, few earn such wages in foreign-owned firms. However, the age distribution of the workers shows that foreign-owned firms are more likely to employ young and unexperienced workers, although the expectation would be for lower wages. This fact encourages us to pursue in-depth study of the phenomenon.

Wage distributions in the private sector (only firms with full domestic/foreign ownership; PLN).

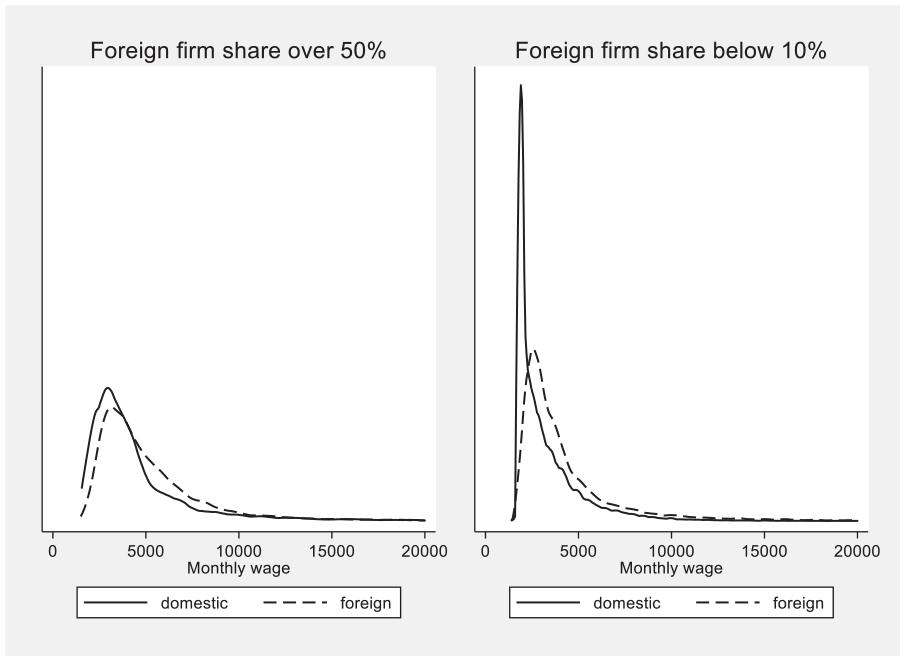

There are differences in worker wage distributions between domestic-owned and foreign-owned firms (firms with mixed domestic/foreign capital are excluded due to few observations), depending on the share of foreign-owned firms in the NACE subsection. Figure 2 (left panel) illustrates that in sections where more than half of the firms are foreign-owned, wage distributions of domestic-owned firms are similar to those of foreign-owned ones. Domestic firms seem to adapt wage policies to follow the majority in the section. However, in sections where the share of foreign firms is low, there is a discrepancy between wage policies of both types of firms (Figure 2, right panel). To some extent, wage policy of foreign-owned firms follows that of domestic-owned ones. However, a visibly larger share of workers in domestic-owned firms is concentrated on the left side of the chart, meaning that they earn wages close to the minimum wage level. For foreign-owned firms, the wage distributions move slightly to the right, implying that these firms offer higher wages, even if they are a minority in the section.

Wage distributions in domestic and foreign firms, depending on foreign firm share in NACE sections (PLN).

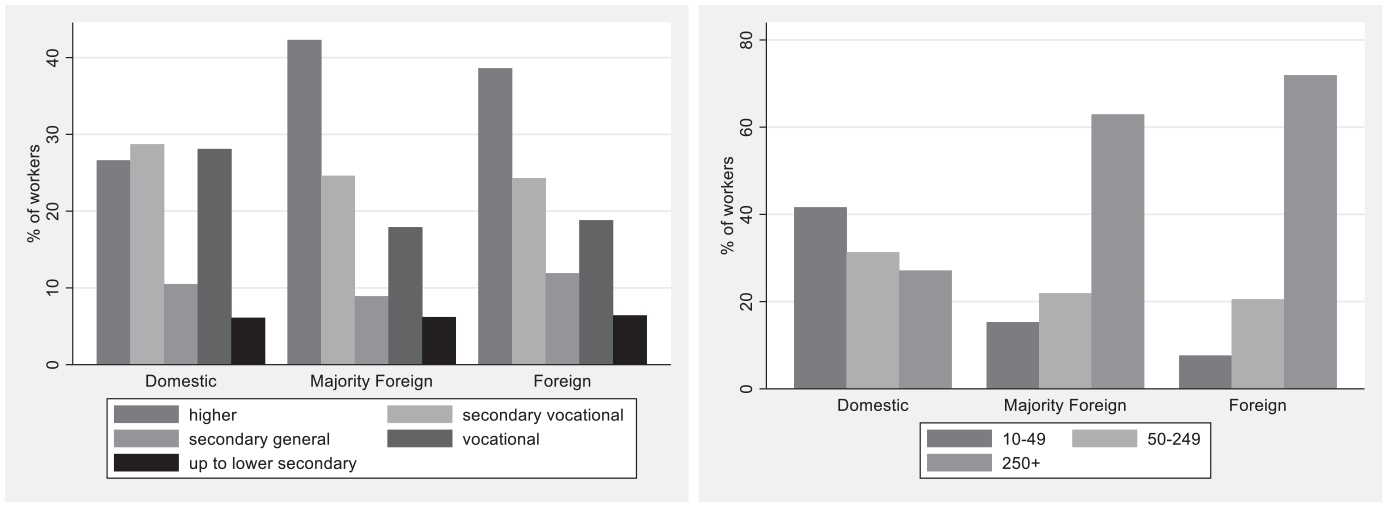

Another visible difference between domestic-owned and foreign-owned firms is the distribution of workers with different levels of education, particularly the share of workers with university or equivalent education (Figure 3, left panel). While they constitute about 28 percent of total employment in domestic-owned firms, university-educated employees comprise around 40 percent of the workforce in foreign-owned firms. This can be a side effect of younger workers, who are generally better educated than older workers, comprising a larger share of employees in foreign-owned firms. In addition, this means we may not reject that foreign-owned firms cherry-pick better educated employers.

Distribution of workers across educational groups (left panel) and firm size (right panel).

As foreign-owned firms are mostly large firms employing 250 or more workers, a majority of workers employed in foreign-owned firms are employed in large firms (Figure 3, right panel). The situation differs for domestic-owned firms. The smaller the domestic firm, the higher the share of employment.

Methodology

Our empirical approach follows Majchrowska and Strawiński (2018), who analyse some aspects of the Polish SES data. They propose a combination of the non-parametric method of DiNardo et al. (1996) and the Oaxaca–Blinder (1973) decomposition. With some modifications, this method can be implemented to identify the effect of firm ownership on wage distribution of workers. Formally, the wage gap can be written as the difference between the wage distributions of two groups

where subscripts A and B represent workers employed by domestic-owned and foreign-owned firms, respectively. As Mincer (1974) demonstrates, wage is a function of employee characteristics, employer characteristics and wage policy. The wage policy can differ between domestic-owned and foreign-owned firms. Considering this, one can write the wage for a group of workers as a function of individual worker characteristics (X), employer characteristics (E) and wage policy (P)

When compared with the existing literature, the proposed approach has some advantages. The authors assume that the functional form of the wage equation is identical; hence, differences in wage distributions are not imposed in the model, as is done, for instance, by Earle et al. (2018).

The standard approach in the literature is to perform the wage decomposition of Oaxaca (1973) and Blinder (1973). In this method, the wage difference is divided into a part ‘explained’ by worker characteristics and an unexplained one. Since our aim is to identify the eventual wage gap caused by the ownership difference, this approach is not sufficient, as the unexplained part cannot be simply interpreted as a gap caused by the difference in ownership. Different factors, such as the economic structure or the size of the firm, may be consequential.

In the extant literature, similar problems are commonly solved by conducting DID analysis (Card and Krueger, 1994). Rather than the traditional two periods, we have differences in two dimensions: worker characteristics (X) and employer characteristics (E). Therefore, the outcomes for two groups are observed

If individual characteristics and firm characteristics are the same for domestic-owned and foreign-owned firms (i.e.

In this study, it is not possible to directly estimate equation (3) for several reasons. First, there is a serious identification problem; the difference in the salary distribution between firms with different ownership might occur due to the difference in the wage-setting scheme, firm characteristics or worker characteristics. Second, it is likely that worker characteristics are correlated with characteristics of the firm for which they work.

In this research, to correct the wage distribution for these effects, we pursue the method of DiNardo et al. (1996), which allows for reweighting of the actual characteristics of firms and workers, with estimated propensity scores as weights, to receive the counterfactual distribution of worker characteristics. To circumvent the problem of potential correlations between worker and firm characteristics, the propensity scores are estimated in a two-step procedure. In step 1, firms are matched, and in step 2, workers included in the matched-firms subsample from the first step are matched. Consequently, the final weights are multiplications of firm and individual weights. Therefore, the wage distribution for the reweighted sample can be treated as if no difference exists in firm and worker characteristics between domestic and foreign firms. Specifically, reweighting factor wi, proposed by DiNardo et al. (1996), takes the following form

Weights wi are used to transform actual distributions

where

There are two key differences between the Oaxaca–Blinder decomposition and the method of DiNardo et al. (1996). Both are related to the counterfactual construction method, but in the Oaxaca–Blinder decomposition, it is fully parametric, while DiNardo et al.’s approach involves the weighted kernel density estimation. The second difference is the outcome of the analysis. The former approach informs of a change in the mean value of wages, while the latter indicates a change in the entire wage distribution.

To some extent, our approach follows Majchrowska and Strawiński (2018), where the two aforementioned methods are combined. Our extension of the method is a two-step procedure used to produce weights, which solves the problem of potential correlations between worker’s and firm’s characteristics.

The empirical strategy is divided into two steps. First, the DiNardo et al. (1996) reweighting approach is used. The propensity scores are generated from the logit model estimated on the pooled sample, as this distribution better handles long and heavy tails. The dependent variable is the firm ownership dummy. A set of independent variables for firm-level matching includes firm size, foreign firm share in NACE subsection, NACE dummies, dummies for dominant occupational group in the firm, firm average occupation-related accident risk, region dummies and sectional labour productivity. The domestic-owned and foreign-owned firms are matched on the propensity scores. Next, matching is conducted at the worker level. For the individual-level matching variables, we use age and its square, experience at current employer and its square, a gender indicator, education dummies, type of contract dummy, and NACE and International Standard Classification for Occupations codes. The dependent variable is employment in foreign-owned firm dummy. The estimated propensity scores are used as weights in the reweighting procedure. To prevent poor-quality matches with enormous weights, we discard observations with propensity scores below 0.01, which means that the probability that the observation is for a foreign-owned firm or worker employed by a foreign-owned firm does not exceed 1 percent.

Second, we employ the Oaxaca–Blinder decomposition with the Mincer-type wage equation. The counterfactual salary distribution with imposed worker characteristics from the second group is decomposed. This allows for the separation of the effect of a change in wage-setting schemes and that of changes in the characteristics of firms and workers. To avoid the problem of arbitrary selected reference categories for discrete variables, the authors follow Neumark’s (1988) proposal and use coefficients from pooled regression as an estimate for the non-discriminatory coefficient vector. The choice of reference category has no impact on estimating the explained and unexplained part (Jann, 2008). To calculate standard errors, we use three-level clustering on level of firm, section and section interacted with occupational groups.

Empirical model and results

This study examines how foreign ownership of companies affects the wage distribution in foreign-owned firms and in NACE subsections. The functional form of the wage equation used in this approach is presented as follows

where wi is the average gross monthly full-time equivalent salary of a worker i (PLN), AGE is worker age (in years), EXP is work experience at current employer (in years) and X represents worker and job characteristics:

NACE sections (19 dummies: manufacturing as base level);

Firm size (three dummies: 10–49 employees, 50–249 employees, 250 and more employees (base));

Sectional labour productivity (gross value added in thousands of euro per employed);

Occupation-related accident risk (accidents per 1000 employed in occupation);

Gender (1 female, 0 male);

Education level (five dummies: bachelor or above (base) secondary vocational, secondary general, vocational and up to lower secondary);

Major occupational groups (eight dummies: professionals as base level);

Type of contract (1 fixed-term, 0 permanent);

Regional dummies (16 regions, Mazowieckie (capital region) as base level).

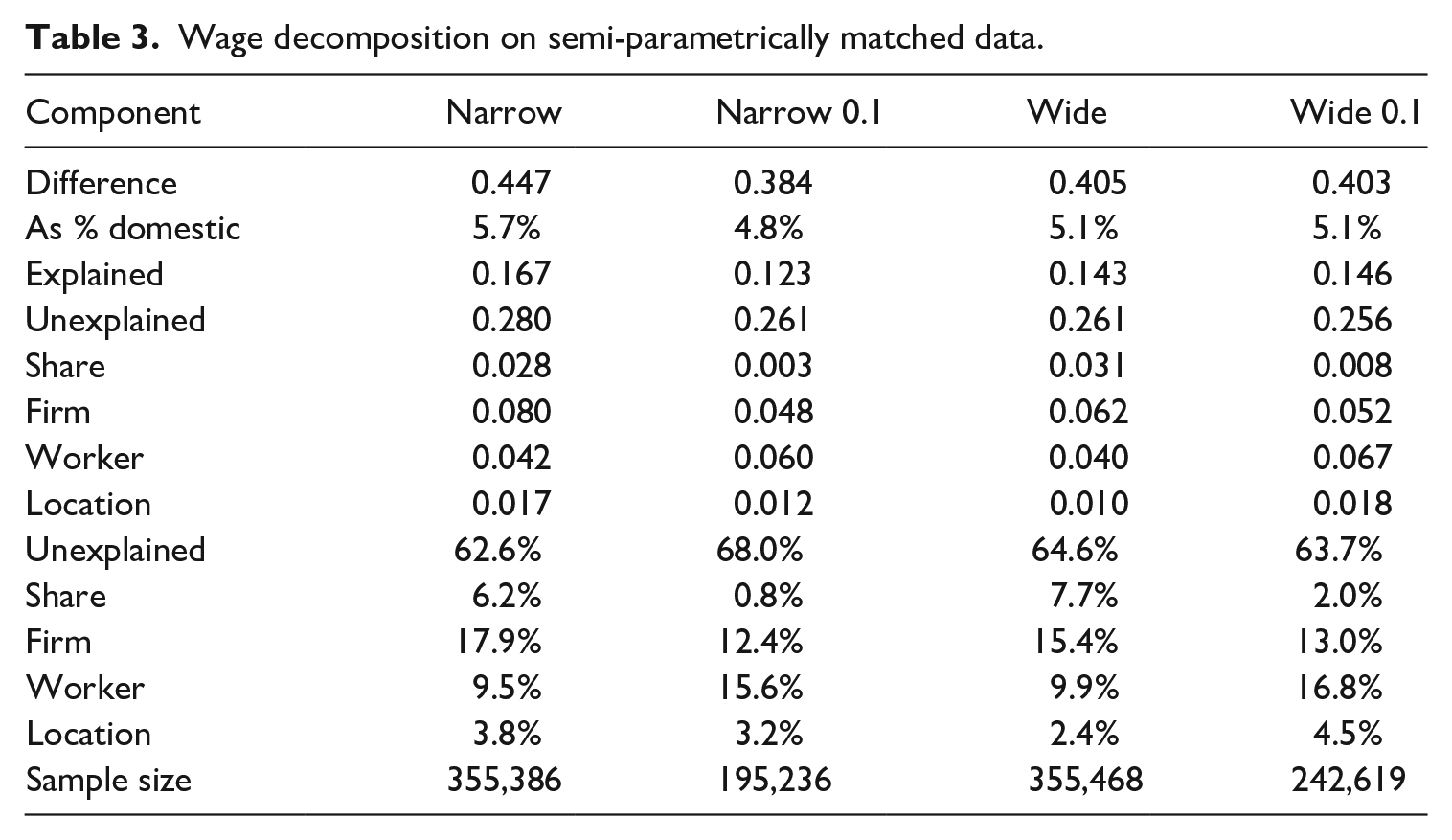

The results in Tables 3 to 5 are presented in the following ways. We estimate four versions of the model. They differ in foreign firm definition (narrow and wide) and scope of the sample: full and limited to firms in subsections with foreign firm share greater than 10 percent. We create four categories: narrow (narrow definition of foreign firm), narrow 0.1 (subsections with narrow foreign ownership at 10 percent or greater), wide (wide definition of foreign firm) and wide 0.1 (subsections with wide foreign ownership at 10 percent or greater). In the narrow definition, only ultimate ownership is treated as foreign ownership, while in the wide definition, foreign-owned firms have more than 50 percent of shares controlled by foreign investors.

Wage decomposition on semi-parametrically matched data.

Oaxaca–Blinder wage decomposition.

Wage decompositions for different origin of investor with semi-parametrically matched data.

Statistically insignificant results are in italics.

To present the results transparently and compactly, 3 the characteristics of employees and companies are grouped. Difference represents the difference in the logarithm of wage between worker of domestic-owned and foreign-owned firms. This difference is a percentage of the domestic-owned firm’s worker’s wage. In the narrow sample, the logarithm of foreign-owned firm wage is, on average, higher by 0.45 than for the domestic-owned firm wage. On average, a foreign-owned firm worker earns 5.7 percent more than a domestic-owned firm worker with similar characteristics.

Next, we present the explained and unexplained parts of the wage gap in log points. The explained part is divided into four components. Share represents the share of foreign firms in the NACE subsection. Firm characteristics include NACE, firm size, labour productivity in the section and occupation-related accident risk. Worker characteristics include gender, age, working experience, education, occupation and type of contract. Location is described by a set of regional dummies.

The results show that the estimated size of the wage gap between foreign-owned and domestic-owned firms is similar for all considered sub-samples. In each specification, the results indicate a wage premium from foreign ownership, which is up to about 5 percent of the average wage of domestic-owned firm worker and differs across firms and sections of the economy. Firm characteristics account for about 1 percentage point of the wage gap between domestic-owned and foreign-owned firms. The estimate of the wage gap is slightly lower for the sample restricted to subsections with foreign ownership of 10 percent or more (column Narrow 0.1). This indicates that, in this subsample, worker wage distributions are closer to each other than throughout the economy. The explained part is, on average, 35 percent of total wage gap between domestic-owned and foreign-owned firm workers, while 65 percent remains unexplained. However, in the explained part, we can distinguish some firm characteristics that are responsible for half of this part. About 15 percentage points are attributed to worker characteristics and the foreign firm share. More importantly, contributions of these two groups of factors are on similar levels, regardless of the sample. To some extent, this may support the cherry-picking hypothesis. When the magnitude of impact from foreign ownership is lower, the impact of worker characteristics is higher, and vice versa. Finally, the results confirm that the wage distribution of foreign-owned firms differs from that of domestic-owned firms. Generally, foreign-owned firms have fewer low earners and more high earners.

We show that foreign-owned firms pay higher wages than domestic-owned firms, even when controlling for firm and worker characteristics. However, foreign-owned firms tend to employ younger and better educated workers on average. What is not obvious is whether these higher wages are a consequence of foreign ownership or are associated with cherry-picking of worker and firm characteristics. The results of the analysis indicate that about 25 percent of wage differences is attributed to firm and worker characteristics. As we can attribute the remaining part to omitted factors and foreign ownership, this does not eliminate cherry-picking.

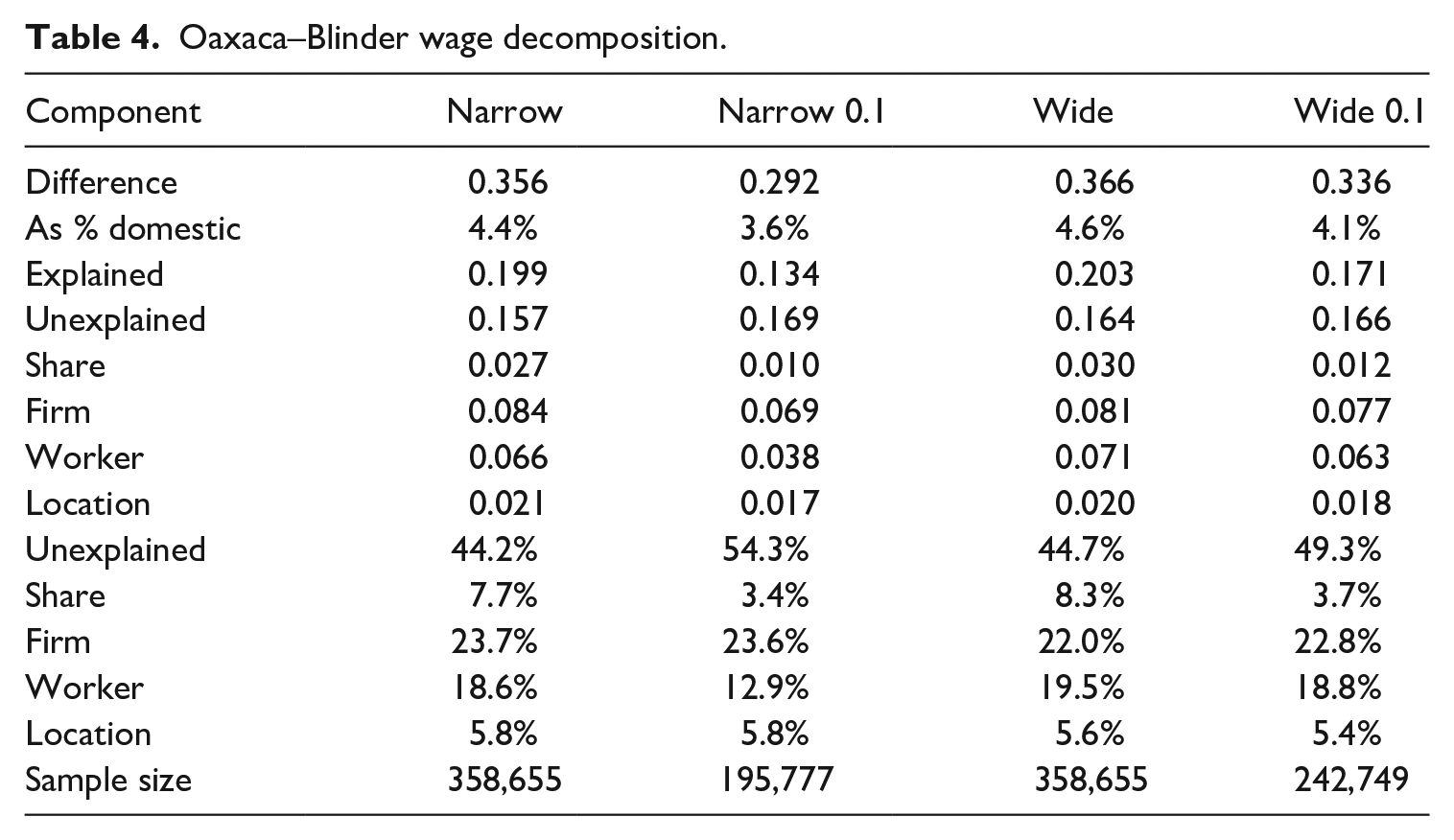

To provide robustness to the main results, we perform the standard Oaxaca–Blinder decomposition of the wage gap between domestic-owned and foreign-owned firms. The sample sizes are larger, which indicates that the matching procedure left out some workers unmatched due to non-existing counterpart in the second group. In presentation but not in estimation, firm and worker characteristics are combined into four groups as in non-parametric models. Again, four versions of the model are estimated that differ in foreign firm definition (narrow and wide) and scope of the sample: full and limited to firms in subsections with foreign firm at 10 percent or greater. The results are presented in Table 4.

Parametric estimates of the wage gap are slightly below the values obtained in the semi-parametric model. The estimate of the gap is about 4 percent and varies with the sample used. The explained part in the full sample accounts for over 50 percent of the domestic–foreign wage gap and about 45 percent in the restricted sample. In both cases, these figures are higher than in the non-parametric model. In addition, contributions from all four factor groups are larger. However, these results are obtained from samples larger by about 10,000–20,000 observations that were not matched in the previous specification. They account for about 5 percent of the entire sample but clearly affect the results. However, results of the robustness check indicate that the semi-parametric estimates are sound and correct.

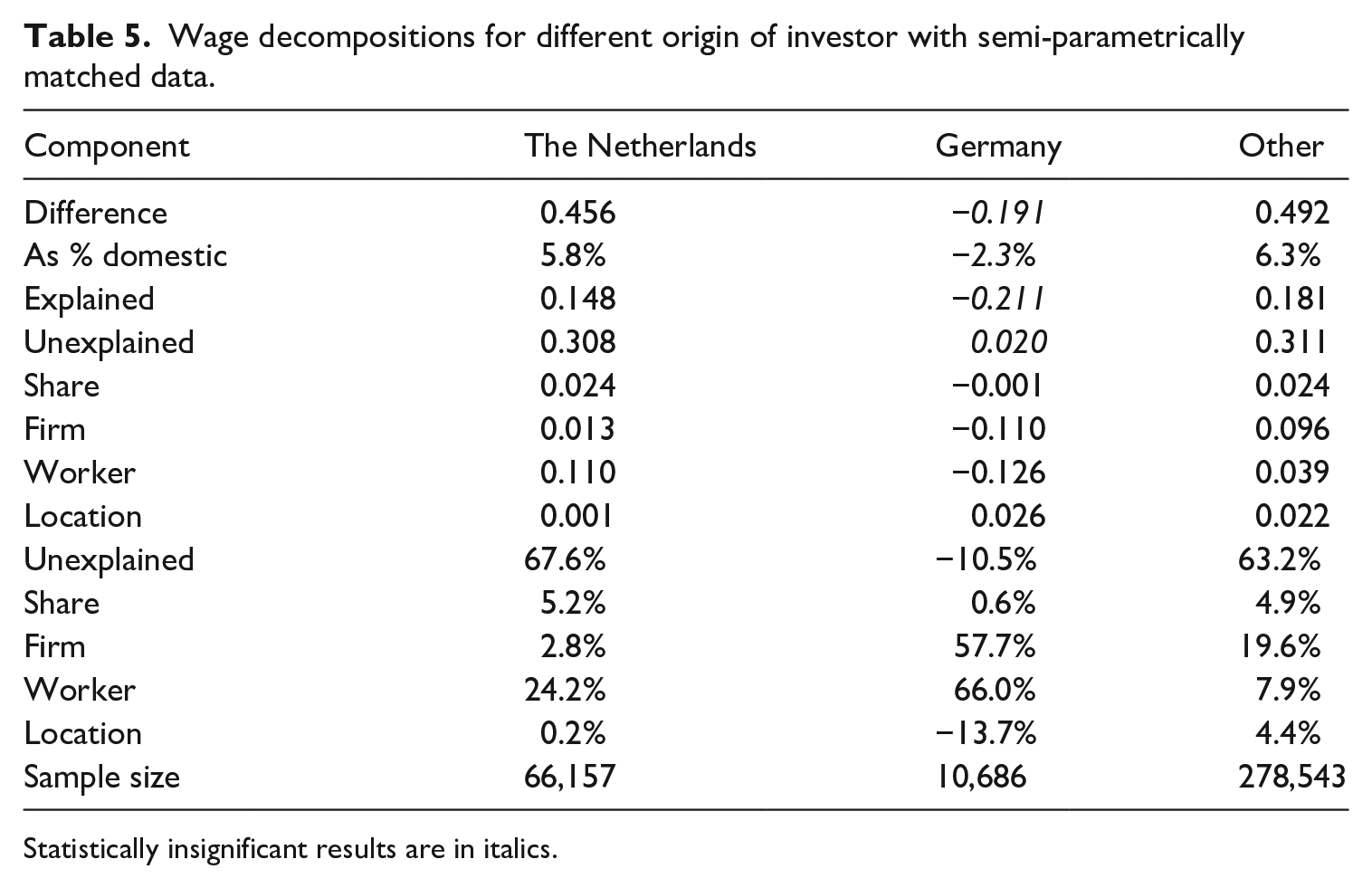

Examining further than the existing literature, our analysis explores the impact of the origin of foreign capital. However, detailed information at the firm level is not available for firms surveyed in the SES. To circumvent this problem, we employ a novel strategy by assigning all foreign firms in each economic section to a country, using the following method. If more than 50 percent of foreign-owned firms are from country A or the share of firms with capital from country A exceeds by at least 5 percent of the share from another country (with the second highest share), all foreign-owned firms are assigned to having capital from country A. This is economically justified, since foreign-owned firms tend to have wage-setting schemes akin to their home country, and this effect is particularly visible in emerging economies (Hjort et al., 2020). This may be partly due to the presence of collective bargaining in the home country, which may be implemented in the host country (Marginson and Meardi, 2009). In addition, investors from other countries tend to follow the leader, which we define as the country that has most foreign capital in the section.

In the transport section, firms from the Netherlands have more than a 50 percent share in invested foreign capital (Table 2), and so we assume that the worker wage distributions follow that of the Netherlands’ firms. Using the second rule, we link Information, Professional, Scientific and Technical Activities (section M) and Administrative and Support Services Activities (section N) with the Netherlands’ capital, and we link firms in the Finance (K), Electricity (D) and Water supply (E) sections with Germany’s capital, where we rely on the narrow definition of foreign and present the results of wage decompositions in Table 5.

Our results confirm that, in sections where capital has a diversified origin, wage premium for working in foreign firms is higher than that in other firms. In sections where capital from the Netherlands prevails, wage premium is slightly higher than the average wage premium to working in foreign-owned firms (5.8 percent vs 5.7 percent). Quite unexpected results are obtained for firms in sections with the advantage of German capital. The wage premium there is negative and not statistically significant. This implies that in those sections, workers in foreign-owned firms are paid similar wages to workers in domestic firms. However, there may be an economic explanation for this result, which may suggest that German firms have a tendency to locate economic activity in sections where they can benefit from lower wages of Polish workers. In addition, capital from other countries may be in sections where the best available work candidates for new technologies are available. To some extent, this may be confirmed, as much German investment in Poland is in sections where high qualifications are not key components in recruiting workers. To confirm this hypothesis, more detailed data on foreign investments in Poland are needed. This topic requires analysis and provides a promising field for future research.

In the last step, we divide the full sample into four parts, each containing workers at different job levels (basic jobs, qualified jobs, specialists and managers), and re-estimate the wage decomposition model on semi-parametrically matched data (Table 6). The wage gap between workers of foreign-owned and domestic-owned firms is lowest for basic jobs and highest for managerial jobs, and it increases along with qualifications needed to perform a job. In addition, the unexplained part is lowest for basic jobs and highest for managerial jobs. This may imply that low-skilled workers are paid equally in domestic-owned and foreign-owned firms. A positive wage premium for employment in foreign-owned firms may indicate support for the cherry-picking hypothesis.

Wage decompositions for different job levels with semi-parametrically matched data.

Conclusion

This study analysed the effect of foreign firm ownership on workers’ distribution of wages by using a large enterprise sample survey on remuneration and employer and employee characteristics. We adapted an innovative methodological approach of Majchrowska and Strawiński (2018), which combined a modified DiNardo et al. (1996) reweighting approach with the Oaxaca–Blinder wage decomposition. Specifically, we used matching at firm level and individual level to control for the differences between workers of domestic-owned and foreign-owned firms.

The results indicate that, on average and other factors being equal, foreign-owned firms pay higher wages. We confirm that firm ownership (domestic or foreign) influences the wage distribution of workers, whereby workers employed in foreign-owned firms earn, on average, 5 percent more than workers with similar characteristics employed in domestic-owned firms. While the novel methodological approach makes it difficult to compare our numerical results with other research in this field, the results generally correspond with most research, especially with studies for Hungary (Brown et al., 2010; Earle et al., 2018). In addition, this result aligns with Almeida (2007), who shows that, in Portugal, foreign firms pay higher wages than domestic firms do.

This study shows that, in most cases, there is a positive wage spillover. A larger share of foreign-owned firms in the NACE division implies higher wages among workers of domestic firms. Particularly, this finding is confirmed for firms owned by firms from the Netherlands, one of two countries with the largest share in foreign investment in Poland. However, this result cannot be confirmed for German capital, as the wage premium in sections with higher German capital is negative and statistically not significant. An interesting extension of this study is further research on wages regarding the origin of the foreign capital.

The wage differences among sections are negligible when controlling for other factors. To some extent, our results complement Faggio (2001), who found that, in manufacturing in Poland, higher levels of foreign activity are associated with higher local wages. Our work extends Bedi and Cieślik (2002), who found that wages are higher in industries with greater foreign participation and that workers in those industries experience faster wage growth. While we did not analyse wage growth, we distinguished NACE sections with greater foreign participation and showed that, in those sections, wages are higher for workers of foreign-owned and domestic-owned companies.

Our approach was similar to that of Earle et al. (2018), who found that, in Hungary, the raw foreign wage premium represents selection bias; nonetheless, foreign acquisition raises average wages. However, while Earle et al. (2018) use firm-level and employer–employee panel data, we focussed on one period and proposed the novel two-step matching procedure.

We aimed to assess the extent to which the wage premium to foreign ownership reflects selection, in particular, cherry-picking workers by foreign investors. We followed Vahter and Masso (2018), who indicate that foreign-owned firms have, on average, higher wages than domestic-owned firms, due at least in part to selecting high-wage industries and regions, taking over local firms with higher performance and wages, or foreign ownership having an effect on wages through a variety of channels (see also Arnold and Javorcik, 2009; Fosfuri et al., 2001). However, this result may be confirmed in some economic sections and should be interpreted with caution, as better pay grade in foreign-owned firms may result from different factors. For example, Almeida (2007) finds evidence of an important selection effect; however, it refers to ‘cherry-picking’ in the context of choosing firms for foreign acquisition, not employing the best workers. Moreover, the study states that there are no significant changes in the workforce composition following a foreign acquisition. As foreign firms tend to employ younger and better educated workers, this may confirm the cherry-picking hypothesis. However, foreign-owned firms tend to locate in places abundant in these workers (capital region and western Poland). Similar to the Portugal study, our study takes place several years after the EU accession.

Nevertheless, there are limitations to our study. First, it used repeated cross-sectional data, and we explored two dimensions – firm and worker – as the time dimension would have complicated the analysis due to firm takeover. Second, the study could not use information about firm financial performance. Statistical data protection rules make it impossible to directly match detailed wage data with firm financial performance measures. Even with an ideal dataset containing panels of linked workers and firms to estimate separate fixed effects for each worker and each firm (Abowd et al., 1999), the researcher would have to contend with non-random matching and switching behaviour of firms and workers. This issue calls for further research. Moreover, in the literature, there is agreement that foreign ownership positively influences productivity. We control for labour productivity, but only on an aggregate level.

Third, our research has limited availability of data concerning the origin of the foreign capital in certain sections of the economy. We partially solved this problem by using a proxy for ownership. While this method is economically justified, detailed data would be beneficial. However, for anonymity, there are no surveys on matched employer–employee data, and it is not possible to construct such data from existing sources.

Finally, we could not discriminate between greenfield investments and financial investments in ownership. However, we find this of little importance, and therefore, it is not a big concern in the case of this study. Heyman et al. (2007) state that a greenfield investor must attract new workers, which would force these types of investors to raise wages. However, Bircan (2013), who checked this relation empirically, finds no evidence for this mechanism. As greenfield investments constitute a small FDI in Poland, we doubt whether it would significantly affect the overall level of wages in the country. Moreover, the limited availability of data makes it difficult to check empirically.

Supplemental Material

sj-pdf-1-ejd-10.1177_0959680121996675 – Supplemental material for Foreign- and domestic firm ownership and its impact on wages. Evidence from Poland

Supplemental material, sj-pdf-1-ejd-10.1177_0959680121996675 for Foreign- and domestic firm ownership and its impact on wages. Evidence from Poland by Paulina Broniatowska and and Paweł Strawiński in European Journal of Industrial Relations

Footnotes

Acknowledgements

The authors are thankful to the participants of Euroasia Business and Economic Society 2020, Macromodels 2019 and World Finance Conference 2020 conferences, as well as the seminar and conferences at Warsaw University. The authors acknowledge Anna Białek-Jaworska, Ewa Cukrowska-Torzewska, Marco Barranechea-Mendez, Prof. Wassem Mina, Leszek Wincenciak and anonymous referees for insightful comments. All the views expressed in text are those of authors and shall not be related to institutions.

Data availability

Additional results and Stata do-files used to generate results presented herein are available from the lead author at

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship and/or publication of this article: This study was supported financially by the National Science Centre, Poland (Grant No. 2018/31/B/HS4/01562).

Supplemental material

Supplemental material for this article is available online.

Notes

Author biographies

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.