Abstract

The article compares the process of digitalisation and outcomes from work restructuring in two banks from the United Kingdom and Luxembourg. The banking sectors in both countries have been challenged by digitalisation pressures such as online and mobile banking, pressures from ‘Fintech’ banks, and the automation of back-office operations. Yet, the adjustment paths in the two countries differed. In Luxembourg, there is an adjustment via limited lay-offs, and increased training and reskilling; however, in the United Kingdom, the main outcomes revolve around branch downsizing and offshoring of employment. These outcomes are explained by differences in institutional supports for collective voice institutions, as well as the role of the state. The findings demonstrate that the embedded employment relations’ institutions and actors have shaped distinct paths of adjustment to digitalisation; and show how the impact of technology on work is neither deterministic nor unidirectional.

Introduction

The debate around the impact of digitalisation on service work is relatively polarised between pessimistic and optimistic perspectives among academics, practitioners and policymakers (Grimshaw, 2020; Ilsøe, 2017; O’Reilly et al., 2018). The more pessimistic and alarmist perspectives emphasise the likely effects of automation in job losses and massive technological unemployment (Frey and Osborne, 2017). By contrast, the optimistic perspectives underline the potential for job creation that can counterbalance job losses (Grimshaw, 2020) and the opportunities for work-life balance and reskilling (EU Economic and Social Committee, 2015). There is a sizeable body of literature that examined the challenges that the platform economy poses for workers in terms of their precariousness (Gandini, 2019); the flexibility and autonomy (Wood et al., 2019); and their representation (Borghi et al., 2021). However, there is still limited research that explicitly examines how collective voice institutions respond to the challenge of digitalisation in established services sectors that are not part of the platform economy.

The purpose of the article is to fill this gap and explain the divergent trajectories of change in response to digitalisation pressures in the banking sector. To this end, we draw on comparative analysis of two internationalised banks in the United Kingdom and Luxembourg. Our findings suggest that – despite similar pressures – the responses to digitalisation in large part diverged and the role of embedded collective voice institutions and actors’ ability to tap on their power resources explains this variation. In Luxembourg, the consensual social partnership approach moderated the pace towards cost-cutting measures and mass lay-offs through legal prevention mechanisms (i.e. social plans, early retirement schemes), and the government enabled the adjustment via reskilling. By contrast, in the United Kingdom, cost-cutting measures were not contained, and job losses were accompanied by branch closures based on unilateral management decisions, which in turn prompted union campaigning and local lobbying initiatives.

The rest of the article is structured as follows. The second section reviews recent debates in the employment relations and sociological literature and sketches the conceptual frame through which we can analyse the actors’ responses to digitalisation. The third section outlines the overall research design, case selection criteria, as well as the data collection and analysis approach. The fourth section presents the findings from the comparative case studies of BNP Paribas (Luxembourg) and HSBC (United Kingdom). The final section discusses the findings, outlines the contribution to the literature and proposes avenues for further research.

Theoretical framework: A variety of adjustment paths to digitalisation

Conventional wisdom in the recent literature is playing up the probability of job losses (i.e. displacement of labour by technology) as one of the likely effects of automation in the next 10–20 years (Frey and Osborne, 2017). This is in line with the expected motivation behind technological changes, to cut costs and improve efficiency and productivity. However, a historical perspective suggests that earlier periods of intense technological change have also shown that jobs disappear and at the same time new jobs appear (Grimshaw, 2020). In addition, we should expect that the rate of job losses and reskilling in technologically modernising sectors (Ilsøe, 2017) will depend inter alia on job security legislation which varies cross-nationally corresponding to different historical paths of employment and production regimes (Gallie, 2007: 97–99).

Furthermore, the extent of job losses should also depend on the relative power dynamics of sectoral/local employment relations actors. As the ‘power-based’ explanations in industrial relations have shown (Benassi et al., 2016; Ibsen, 2015; Kornelakis and Voskeritsian, 2018; Lloyd and Payne, 2021) the ability of trade unions to draw on their resources is critical for their capacity to resist or accept organisational and institutional changes. This institutional support for collective voice is critical, for instance, to encourage upskilling processes and practices (Doellgast, Holtgrewe, et al., 2009). This is more likely to appear in settings with strong labour market actors who use their associational power to produce public goods of training. But upskilling is also a process that can take place ‘in-house’ as part of internal labour markets (Grimshaw et al., 2001) and reflect a strategic choice of employers to provide re-training for existing staff. In other words, unions or strategic employer action can potentially counterbalance the technologically induced decline in the real skill content of jobs.

Finally, the introduction of new digital technologies can lead to an increase in work intensification, for example, by altering the tempo and pace of work in the platform economy, which is structured by algorithmic management (Gandini, 2019; O’Reilly et al., 2018; Wood et al., 2019), by the request for universal availability and reachability through mobile or virtual working (EU Economic and Social Committee, 2015) or by increased monitoring and surveillance capabilities of new digital systems (Gandini, 2019). Similarly, the power of the trade unions is quite important even in the platform economy, where platform workers’ power depends on organising to resist a degradation of working conditions and to build solidarity (Borghi et al., 2021).

These works cast doubt to the perspective that the digitalisation dynamics and technological developments would invariably lead to convergence in work organisation and job losses. The technological unemployment thesis embodies a new ‘technological determinism’ that ignored the social shaping of technology (Holtgrewe, 2014) and adjustments to technology as socio-political choices (Grimshaw, 2020). Following this frame of thinking, we also propose that technology is not deterministic, but socially negotiated by key actors at various levels of governance and we hypothesise that any change should reflect the ‘power resources’ of the constellation of actors (Benassi et al., 2016), who are able to shape a variety of adjustment paths to digitalisation.

Indeed, recent work suggests that there are strong national differences in union power that affect the implementation of robotics and automation in the food processing industry between the United Kingdom and Norway (Lloyd and Payne, 2021). Similar studies suggest that resistance or acceptance of the digitalisation drives do vary across industrial relations contexts in the European steel industry (Stroud et al., 2020). More specifically, we hypothesise that distinct adjustment paths to digitalisation will also depend on the support of the state (Doellgast, Nohara, et al., 2009) as well as the employers’ associations capacities and power (Brandl and Lehr, 2019; Kornelakis, 2014). Overall, the result of interactions between the organisational-level strategies and sectoral level institutions and collective actors should largely shape the trajectory of change in response to digitalisation.

Research design and methodology

Our overall research design follows the comparative case study approach (George and Bennett, 2005). The choice to focus on the United Kingdom and Luxembourg is theoretically motivated: these countries are examples of two different models of capitalism with distinct institutional configurations in their employment relations systems (Hall and Soskice, 2001; Witt et al., 2018). On the one hand, the United Kingdom belongs to the category of Liberal Market Economies (Gospel and Edwards, 2012), whereas Luxembourg is identified as a country close to Coordinated Market Economies’ neo-corporatist model (Kirov and Thill, 2018). While distinct institutionally in the employment relations’ realm, both countries have a comparative advantage in the financial services industry and operate as global financial hubs in Europe.

The selection of the banking sector as our sectoral context is based on the following criteria. First, the sector has been central to debates on technology and industrial relations for a long time. Already in the 1990s, the sector was introducing massively Automated Teller Machines (ATMs), which was the first step towards less reliance of clients on networks of bank branches. This shift has been well documented in earlier work (Regini et al., 1999) which showed how the introduction of new technologies essentially reshaped the nature of work of banking employees, fragmented their career structures and pushed their work towards greater attention to sales and performance.

Second, the sector is at the forefront of the most recent wave of technological change in European services (Eurofound, 2014: 21). Several concurrent technological developments have a systemic impact on the sector, for example, the broadening of online and mobile banking products, the focus on internet-mediated interaction with clients, the implementation of artificial intelligence and bots, and the focus on Fintech and crypto-currencies like the Bitcoin. Digitalisation is transversal, impacting not only back-office and IT services, but also the provision of front-line banking services with a mix of online-mediated and offline activities and with the involvement (either cooperation or competition) of new Fintech players to make operations faster and cheaper. Banks also increasingly engage in the introduction of Robotic Process Automation (Lacity and Willcocks, 2016). As a result, digital robots now can handle part of the customers’ queries, which has up until recently been conducted by bank employees, thus leading to a reconfiguration of jobs in banks. The technological transformation in banking has already impacted the number of branches and people. According to data from the European Banking Federation, the number of branches has fallen by 31% since 2008 (EBF, 2020). In 2019, the United Kingdom counted more than 400,000 banking employees compared to 430,000 in 2009, while in Luxembourg in 2010, the number of employees was 26,146 or almost similar to the present day. At the EU level, the overall evolution of the employees in the banks only over the last 10 years is alarming – from over 3.1 million jobs in 2009, EBF counts 2.6 million in 2019.

Third, the sector remains relatively unionised at the cross-country level, with employees being represented by trade unions at company, sectoral, or national level (Eurofound, 2019). The union density is similar in both countries, ranging between 20 and 25% according to the local unions’ estimates. Employers’ or business associations also represent banks in several European countries. Collective bargaining and social partnership have therefore the potential to shape the process of technological adoption. Therefore, the overall sectoral and institutional setting provides a very good context to examine whether and how employment relations’ institutions shape the responses to digitalisation pressures.

Finally, we focus our analysis on two highly internationalised banks, HSBC and BNP Paribas, which are also well-embedded in their domestic banking systems. Unlike other local or regional banks, they have similar international pressures to digitalise and restructure and appear at the forefront of digitalisation. HSBC and BNP Paribas are the two leading banks in Europe by total assets in 2020 (Statista, 2021) among the two largest banks in Europe. Both banks are highly internationalised as HSBC’s network covers 64 countries and territories, while BNP Paribas’ network covers 68 countries and territories. The timeframe of the case studies is focused on restructuring initiatives in the five-year period between 2014 and 2019.

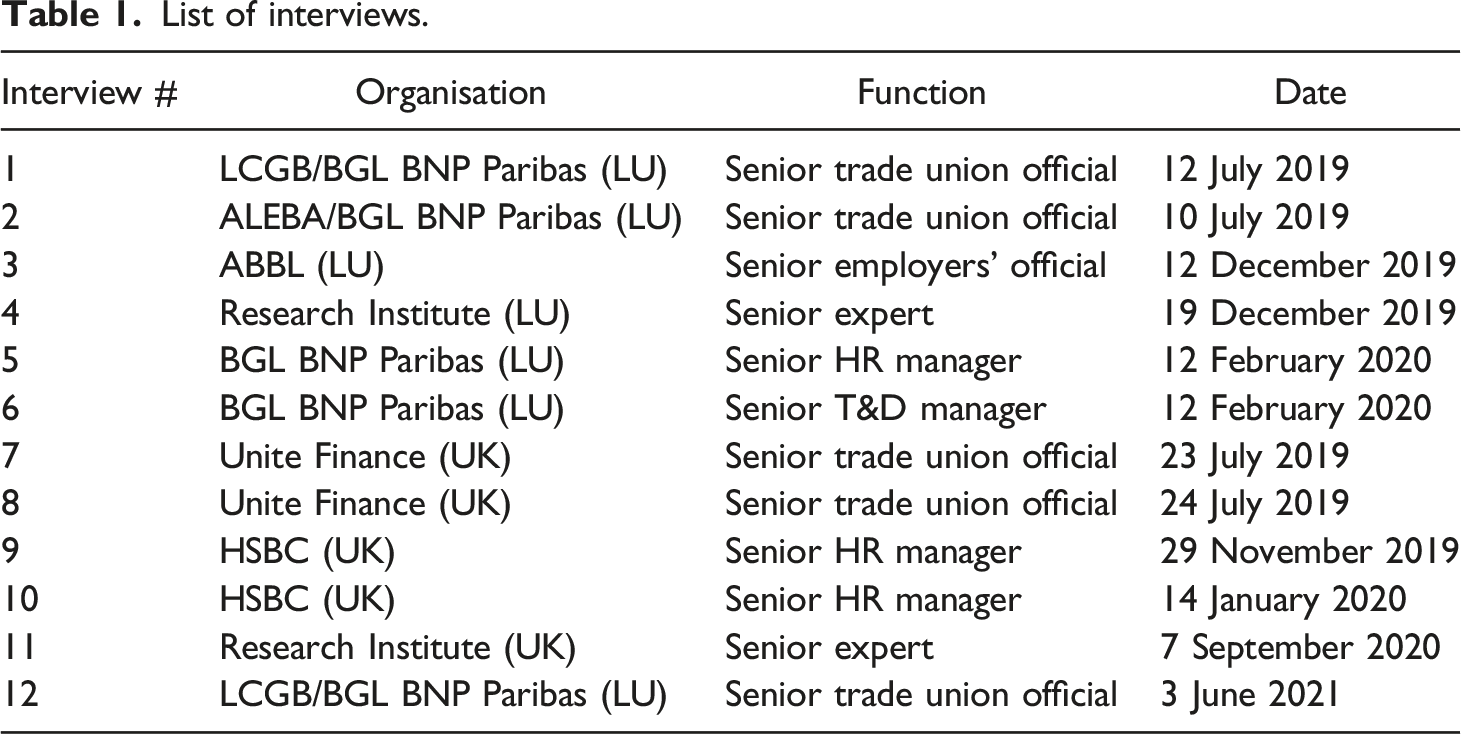

List of interviews.

The interviews were either recorded with permission or notes were taken where permission to record was not granted. All the data (primary sources, documents, and interview notes and transcripts) were read iteratively with the literature themes and processed via a thematic content analysis approach (Braun and Clarke, 2006). They were interpreted and categorised using initial themes that emerged from the literature. The themes were compared and contrasted with each other and with the literature so that relations are established. Then they were refined during the analysis and discussed within the team to ensure validity. The main themes that organise our thematic analysis and emerged from the literature and the data are the following: Digitalisation pressures and disruption; job losses and branch downsizing; and skill-formation and training.

Digitalisation of service work in banks: Luxembourg and the United Kingdom

The institutional context in the banking sector of Luxembourg

Historically, the financial sector has constituted one of the largest employers in Luxembourg. Employment in banking has remained relatively stable from 27.205 employees in 2008 to 26.317 in 2018 despite that the number of banks (companies) decreased from 156 in 2007 to 127 in2019. 1 Luxembourg has a long tradition of multi-level collective bargaining with corporatist institutions originating in the German Customs Union (Wey, 2003) and consecutively enforced by laws in the 1970s instituting a national tripartite collective bargaining arena as a crisis instrument. Each bargaining arena has a specific mission based in law and conducted by a multitude of actors negotiating within a legal framework and the government acting as a coordinator or legislator. One of the main objectives of collective bargaining is to seek to prevent major unemployment levels.

Collective bargaining at sector level is embedded in a 2004 legal framework on governing labour relations. This coexists with more informal practices between the various bargaining levels, which is due to small administrative pathways and close relations between the actors, and results in a common awareness regarding the volatility of the sector in an international competitive environment and the resulting imperative to act collectively in key economic sectors. Based on the right to sign collective labour agreements (CLAs), the law-based employee representativeness in banking is endorsed by the largest trade union the private Association Luxembourgeoise des Employés de Banque et Assurance (ALEBA); followed by the OGBL Syndicat Banques et Assurances (OGBL) sector union; and the Christian-democrat LCGB-Syndicat des Employés du Secteur Financier sector union.

On the employers’ side, the Luxembourg Banker’s Association ABBL (Association des Banques et Banquiers, Luxembourg) negotiates CLAs. Social partners negotiated the latest CLA, which was signed in July 2018 after 18 months of negotiations. The agreement details the wage rates for the six categories of personnel and includes an increase of the allocated budget for training from 1% in 2018 to 1.5% in 2019 and 2020 of the reference wage bill available for training purposes. These difficult sector-level negotiations highlight a broader tendency in collective bargaining marked by conflict-ridden agendas because of a diverging analysis of the socio-economic environment since the 2010 crisis.

At the company level regarding worker participation, a pooling of responsibilities occurred in 2015 with a law on social dialogue that suppressed the works’ councils (comité d’entreprise) in larger companies and defined the staff delegation (délégation du personnel) in companies of more than 15 employees as the central negotiator. This latest reconfiguration also represents a major change in banking, as a trade unionist emphasises: ‘The staff delegation was the advocacy body and the joint committee was the co-management body. Today the delegation has all the competences’ (Interviewee 1, Senior Trade Union Official, 12/07/2019).

Staff delegations continue to be composed of representatives elected among the banking employees and include employees and trade union delegates. In banks with more than 1000 employees, the staff are entitled to have representatives on the board.

Digitalisation pressures and disruption in the Banque Générale du Luxembourg BNP Paribas

Banque Générale du Luxembourg BNP Paribas is a Luxembourg bank founded by Société Générale of Belgium in 1919 under the name of Banque Générale du Luxembourg (BGL). Since May 2009, the bank has become a member of the BNP Paribas Banking Group. More recently, the bank has witnessed a technological and digital transformation reflected on projects such as the Direct Bank Initiative, which is responsible for remote service activities and providing daily online banking solutions to customers. Other digital business strategies included mobile banking with the launch of an iPhone mobile application, the launch of its Digicash payment application for individuals, and the online loan applications. Further investments in digital products were conducted at private banking level with the MyPortfolio iPad app supplemented by a smartphone version. In November 2015, due to cost considerations, the bank changed the historic core of its IT system, called Mainframe by migrating all the data and applications to a new decentralised platform (BGL BNP Paribas, 2015).

The cost factor in banks remains a fundamental and difficult to anticipate issue of concern. Interviewed employee representatives insist that while the digital products were initially implemented to reduce costs, in fact, they have increased costs. This creates a dilemma, as banks which do not invest at the right time for cost purposes into digital products, face difficulties to remain competitive in an international market. ‘[Digitalisation] is expensive (…). If you are a manager of a bank, one has to know if you have the necessary money to buy [digital products] or not. If you do not have the money, then you wait another year to do the investment, but in digitalisation, time goes by so quickly, that waiting could also make you lose money’. (Interviewee 2, Senior Trade Union Official, 10/07/2020)

The digitalisation strategy of the bank is based on multi-channel distribution services and products, through the telephone (call centres), the internet, the mobile and the physical branches (Interviewee 5). The bank also has much more ‘data’ and the big data will be exploited gradually by employees who are more comfortable with digital tools. At global level, BGL BNP Paribas works on 30 target profiles identified as jobs of the future. To address this pressure, the bank launched a programme called Digital Data Agile Academy (DDAA) and focused on training, skills and recruitment at the global level, but also in Luxembourg. Examples of new and future jobs and professions include growth hacker; data analysts; data scientists and agile project managers.

Moreover, in BNP BGP Paribas, as in the Luxembourg banks in general, increasing pressure and competition have been witnessed by a growing industry of Fintech companies. Fintech companies, including Amazon, eBay and PayPal, are regarded as a key pillar of economic diversification efforts. Representing both a competitive and invigorating actor, Fintech companies have received the support of employer associations which facilitated the cooperation between the banks and Fintech companies (Interview 3). They have developed digital-based solutions traditionally offered by banks: from compliance and risk-management, blockchain and cryptocurrency, security and authentication, automated investment services, Big Data analytics, to mobile and e-payments.

Job losses and branch downsizing in the Banque Générale du Luxembourg BNP Paribas

Over the years, there has been a general practice of the bank neither to dismiss employees not to resort to social plans to avert mass lay-offs. This practice is traced back to industrial relations in the sector in Luxembourg, characterised by a strong collaboration between the three representative trades unions, which collaborate not only at the sector level but also at the bank level. For BGL BNP Paribas, internal and tailor-made solutions discussed by the management and staff representatives were identified in this research as viable alternatives. BGL BNP Paribas remains the fifth largest employer in Luxembourg with a total of 3.830 employees in 2020. Two major restructuring processes occurred in 2010 and 2014: in 2014, 170 employees benefitted from voluntary early retirement schemes. The number of employees decreased by 400 between 2013 and 2016. 2 Yet, the overall number of employees has only decreased from 4060 in 2013 to 3830 in 2020. Similar to other long-established banks in Luxembourg, BGL BNP Paribas has avoided to implement mass dismissals and provoke employee insecurity. Unlike in the United Kingdom, before proceeding to mass layoffs, banks generally comply with law-based, but cumbersomely negotiated social plans that could fail if no agreement is achieved (Interview 12).

In the case of BGL BNP Paribas, job losses due to digitalisation dynamics and offshoring of digital services were in the past cushioned by instruments such as voluntary early retirement and reskilling schemes, internal mobility or tailor-made informal practises, such as keeping the employee in the paid job until early retirement starts; or favouring package-based voluntary exit. Even if occurring unevenly and with conflict-ridden agendas in banking, staff representatives, with the expertise of trade unions as background support, are involved and consulted in the negotiations of favourable solutions.

Nonetheless, branch closures have remained an integral part of cost-cutting strategies before and after the 2010 international crisis. Closures have been limited in our case study and followed a general strategy in the sector as a result of automation processes and a decreasing attendance because clients increasingly accepted web-banking tools (Interview 12). The branch closures have not led to dismissals, but employees moved to other departments within the bank or branches. (Interview 5).

Furthermore, the insecurity encountered by handling technological change and keeping up with the pace of digitalisation requires anticipation efforts from all involved actors. This entails that employee representatives insist to reinforce awareness towards stronger social responsibility from bank employers with the objective to avoid economically driven layoffs. This strategy is highlighted by one of our interviewees: ‘If the employer’s policy is (…) not to go through dry redundancies (…) we have to anticipate, we have to prepare employees’ (Interviewee 1, Senior Trade Union Official, 12/07/2019).

Beyond the avoidance of massive layoffs, as interviewees underline, the involvement of employees through co-decision is a fundamental source of their power: ‘…it is an area that must go through co-decision (…) but if you are on the board of directors of course you are in the process much earlier before any final decision has already been taken, then you can already negotiate’ (Interviewee 1, Senior Trade Union Official, 12/07/2019).

Hence, employees in Luxembourg are empowered through worker participation, including staff delegations and the information and consultation process, together with boards in larger banks and the European Works Council. In a nutshell, the involvement of collective voice institutions is fundamental in the adjustment process of Luxembourgish banks to digitalisation.

Skill-formation and retraining in Banque Générale du Luxembourg BNP Paribas

A challenge for trade unions in banking is to address through efficiently mobilised corporate instruments the employability and keeping in employment of staff. Our research identifies the deployment of compulsory and digital training schemes (Interview 2) at the bank level as a bulwark against de-skilling processes. This strategy is identified as a broadly applied neo-corporatist strategy, which requires the mobilisation of government actors and funding schemes such as the National Employment Fund (Fonds pour l’Emploi) and the appropriation by social partners who contribute with gained sector expertise.

An example is the New Digital Skills Bridge

3

pilot project initiated by the Ministry of the Economy and the National Employment Agency (ADEM) under the supervision of the tripartite Conjuncture Committee (Comité de conjoncture). After having consulted their staff delegation, companies can apply for funding and assistance with the objective to reskill employees by enhancing their digital competences that could favour their reorientation and avoid their dismissal. Simultaneously, it provides the government with an anticipation tool to measure the impact of digitalisation. ‘They [the government] are interested to see where tomorrow’s jobs are, where today’s skills are, what tomorrow’s skills are going to be and try to see with us how we can participate in this change by training our own people’ (Interviewee 5, Senior HR Manager, 12/02/2020).

In addition to anticipation efforts, the reinforcement of training skills is a requirement when banks face digital transformation processes. Training budgets in Luxembourg have been substantially increased and employers together with employees define on an annual basis training needs and elaborate annual career developments plans (plan de développement individuel de carrière). Supported by the government through the deployment of subsidies if banks organise training, the sector employer association ABBL has launched 16 digital skills courses organised by the House of Training of the Chamber of Commerce.

The institutional context of the banking sector in the United Kingdom

Employment relations in the United Kingdom banking sector have gone through a turbulent period that spans the last four decades. In the mid-1980s, sectoral collective bargaining broke down and the employers withdrew from national negotiations moving to a decentralised system. The unions and staff associations in the sector went through a period of instability that was characterised by industrial disputes and intense merger activity (Morris et al., 2001). Since the late 1990s, the sector has become a prominent example of the new style ‘partnership agreements’ in UK employment relations (Johnstone, 2016). Most of these agreements were established on the basis of bringing the unions ‘back on board’ to work through ongoing programmes of workforce restructuring and organisational change, and to re-establish good and harmonious industrial relations (Stuart and Lucio, 2008).

The main trade union representing employees in the finance and insurance sector is Unite the Union. It represents over 130,000 members throughout all major employers in banking and insurance. More recently, the wave of mergers has continued and BSU merged with Unite, DGSU merged with Nationwide Group Staff Union, UFS merged into Community, while SURGE and YISA merged into Aegis.

There is no employer association, and the main business association is the UK Finance that integrated the British Bankers Association (BBA). BBA was a trade association for the UK banking sector with 200 member banks and did not engage in collective bargaining. However, it was very active in shaping policy and practice as regards key issues such as Brexit and digitalisation. Since 2017, the BBA merged with another five business associations in the wider insurance and banking sector (Asset Based Finance Association, Financial Fraud Action UK, Payments UK and the UK Cards Association) and has now become UK Finance.

The estimated coverage in the sector is in the range of 20–25% (estimate by Unite) and all collective agreements within the sector are agreed at the firm level. The four most important firm-level agreements in terms of employees covered include those negotiated between Unite and HSBC, Barclays, Lloyds, and RBS. The scope of collective bargaining agreements encompasses issues such as: Equality, appraisal, flexible working, recruitment, disciplinary and performance systems.

Digitalisation pressures and disruption in HSBC UK

Technological change was quite important in the 2000s reflecting the shifts towards phone banking and Internet banking (Stuart and Lucio, 2008). More recently, the major shift has occurred towards mobile banking leading to fewer people using the branches (HSBC, 2017). HSBC has rolled out a ‘hugely ambitious’ digital transformation programme since 2015 and on 9 June 2015, HSBC announced plans to axe 25,000 jobs globally and radically re-structure, so as to achieve up to $5 billion in transformational cost savings. Increased digital and self-service capabilities would enable the bank to axe around 2000–3000 existing service roles. The attribution of these restructuring initiatives has been largely based on the shifts in consumer behaviour towards mobile banking and fewer needs to visit local branches (BBA, 2015).

In addition, the new players from the Fintech sector, such as Atom, Starling and Revolut, are challenging the incumbents. In the past, the segments between the boundaries of the sector were redrawn with the entrance of large retailers such as Tesco Bank (Stuart and Lucio, 2008). In recent years, the appearance of Fintech has accelerated digitalisation and has intensified the competitive pressures further disrupting the banking industry. The new players are not only innovating, but they are also cost leaders because unlike the large banks which have tens of thousands of employees, the new players have only a few hundreds of employees, which gives them a huge advantage in terms of cost-base (Diginomica, 2015).

Finally, digitalisation pressures are associated with the new capabilities of automation of work processes due to progress in artificial intelligence software. HSBC is, for example, already using AI technology to process documents related to international trade. At the time when the bank announced this in 2017, about 100 million pages of documents, such as invoices and insurance documents, were manually reviewed and processed by staff. Instead, now using optical character recognition (OCR) and robotics technology, HSBC’s Global Trade and Receivables Finance (GTRF) automates the review of documents and then sends them automatically to the bank’s transaction processing systems. While this improves accuracy and gives staff more time to do ‘value-adding activities’, it also makes such manual roles redundant.

Job losses and branch downsizing in HSBC UK

Since 2011, the job reductions have involved more than 11,000 jobs, while the job creation for the same period was around 1500 jobs (European Monitoring Centre on Change, 2020). HSBC UK remains the fourth largest bank in the United Kingdom (after Lloyds, Barclays and RBS) and currently has 625 branches. The number of branches has more than halved in the period 2011–2017, with its high street presence in June 2011 standing at 1301 branches (The Guardian, 2017). The most important restructuring event took place in the period 2015–2017. HSBC announced the implementation of a massive restructuring plan that affected 7–8000 British jobs by 2018, and this would see the end of a three-year restructuring plan (The Guardian, 2017).

The combined workforce in retail and commercial banking in the United Kingdom dropped from 37,901 employees in 2015 to 30,805 in 2018 (HSBC, 2019). The disappearing roles can be attributed to two processes that run in parallel: Offshoring and digitalisation. ‘…at the time they announced it they were 38,000 job losses worldwide, but of those a good 8,000 in the UK, most of those were IT workers, and they had this massive programme of investment in technology, named something like “Earth and Moon”, many of them lost their jobs, for many of them they lost their jobs because they went to India or China, just because they were cheaper to do. There was some automation in some of that. (…) This had nothing to do with the branch closures.’ (Interviewee 8, Senior Trade Union Official, 24/07/19)

Overall, the bank shifted about 5000 operational roles to low-cost locations, including software development roles. On the software development front, 50% was being done in India and China and that percentage increased to 75% under the new strategy.

In parallel another 3000 roles were automated in the United Kingdom (Diginomica, 2015). The digitalisation and automation process included inter alia: Implementing tools for front-line staff to make better use of their time; automating more operations to get more out of high-quality low-cost service centres; increase use of agile development; elimination of legacy systems; use of cloud platforms for non-business critical systems (e.g. HR); reduce in-country data warehouses (Diginomica, 2015). Interestingly, the discourse around digitalisation concerns more the impact on consumer behaviour (using online banking, smartphone banking, etc.) and less on the automation of work of employees. As one informant said: ‘The digital disruption is mostly outward looking changing the customer-facing functions, such as online banking, mobile banking etc. Internally, the workplace is less digitalised, banks have moved from customised IT solutions to proprietary solutions moving to the cloud relying on the Big Three [Oracle, Workday, SAP].’ (Interviewee 9, Senior HR Manager, 29/11/19).

The immediate effect of the change in customer behaviour has intensified restructuring leading to branch downsizing. According to employers, the branches are supposed to be now ‘right-sized’, but as one union informant said: ‘Well, until recently, in most branch closures, the next branch has been 5 miles, 10 miles, 2 miles away, so people have been able to move, and instead of working here, they now work there. So that works fine for most people. So in fact, until recently, there weren’t many redundancies from branch closures. But now that branches, particularly in rural areas, the number is so small, that if you decide to close a branch in the Scottish Highlands, the next nearest branch might be 50 or 60 miles away. Well obviously that person can’t now work in the other branch instead, so they are made redundant.’ (Interviewee 8, Senior Trade Union Official, 24/07/19).

But even this branch downsizing, which is direct outcome of online banking, does not lead to significant redundancies. The branch closures are largely dealt with a combination of redeployment into other branches and internal mobility where possible or voluntary redundancies: ‘If you are in a branch and it’s closing you can either move to the next nearest branch or you leave, there’s nothing else of course, because there’s nowhere else to work. If you are in a big office, like Canary Wharf, and your job is being affected because part of it is going to India, well then there’s opportunities for redeployment for other jobs in the bank. But you can’t do that if you are just in one branch on your own.’ (Interviewee 8, Senior Trade Union Official, 24/07/19).

On the collective bargaining front, the union has been working in partnership with the banks and there is regular consultation for changes. There is a process of annual/regular negotiation and agreement of wages at company level with the ‘Big Four’ although that does not lead to formal contracts. ‘We have collective bargaining agreements [with the Big Four] on all matters of terms and employment, and we are consulted on restructuring etc. What tends to happen is that because we have long-standing working relationship, we have almost day-to-day interactions. The discussions include all matters of terms and employment, e.g, grievance, sickness absence, pay salaries, hours of work, job security, bonus arrangements, pensions,’ (Interviewee 7, Senior Trade Union Official, 23/07/19).

In contrast to Luxembourg, there is not so much anticipation of change or a sectoral response to digitalisation. The main exception is a Toolkit for local branch closure that Unite published recently. There are however consultations and open communication channels with other actors in the sector, such as the UK Finance (incl. British Bankers Association): ‘We meet with UK Finance twice a year and we are discussing issues such as gender pay, gap, executive pay, we always talk about branches. But there is no formal relationship. (…) In an ideal world we would have sector-level bargaining and we would be negotiating at sector level for terms and conditions, like a basic floor, and maybe we do that we the equivalent of the BBA (…) But it’s Labour Party policy to have sector-level bargaining, so under a Labour government that’s the sort of thing that could come back’ (Interviewee 8, Senior Trade Union Official, 24/07/19).

The changes are employer-led and the unions are on the responsive mode. The union finds it hard to resist technological change per se, it is difficult to make the argument against it. ‘Employment has been on the decrease in banks, mainly because of the financial crisis, and now with technology changes it’s very hard to put up a fight against, for example, branch closure. So there’s a high street bank branch that is closing, it’s closing because people don’t go there so much anymore, and they don’t go there so much anymore, because they all do their banking on their smartphone or online. It’s very difficult to have an argument against that.’ (Interviewee 8, Senior Trade Union Official, 24/07/19).

One of the achievements of the unions was to negotiate a generous severance package (on top of legal minima) for dismissed employees and actually, that becomes attractive and incentivises senior employees to follow the route of voluntary exits. ‘But the other element is that whenever there’s these job losses because of stuff like that [technology], getting members to actually want to take [industrial] action is quite a big step (…) partly because they don’t see themselves as that kind of person, they are conservative with a small c, but also because there’s a big number of employees who always see redundancy as a right, you know, I’ve worked for this God-awful bank for 30 years and now I am just waiting to be made redundant so I can get my redundancy package. (…) And this is one of the sad facts about having negotiated a good redundancy agreement, is that whenever there’s job losses, we often get people who are kind of queuing up to be made redundant we are not campaigning for you to be made redundant.’ (Interviewee 8, Senior Trade Union Official, 24/07/19).

In response to the persisting branch closures across the banking sector, Unite launched a campaign in late 2019 to save bank branches, emphasising the detrimental impact on local communities, older customers with no access to mobile banking and SME. At the same time, Unite developed the Bank Branch Closure Tool Kit as a guide to anticipate change and help local branches to fight back for their survival.

Skill-formation and retraining in HSBC UK

Training and reskilling measures are wholly at the discretion of the employers. One impact of digital transformation is that it shifts demand to new digital skills, which are in shortage in the sector and there is no way to find them in the external labour market: ‘However, to fully harness the possibilities of these solutions one needs to have change in the culture/mind-set, operations and capabilities. Some of the digital skills of the workforce are missing (data science, analytics, digital customer experience) and these cannot be found in the external labour market, they cannot be ‘recruited away’, but can only be developed in-house.’ (Interviewee 9, Senior HR Manager, 29/11/19).

The skills shortages are exacerbated by the lack of any government funding, in sharp contrast to the case of Luxembourg. Until recently, unions’ voice and BBA’s voice were represented in a tripartite body called the Financial Services Skills Council, which addressed the issue of skills and lifelong learning within the UK banking sector (Stuart and Lucio, 2008). However, this body has become defunct and has not been replaced by another structure in recent years. The Financial Services Skills Council funding was cut as part of austerity programmes in the Conservative governments. ‘The Financial Services Skills Council basically was taken over by the Legal Skills Council but when all the funding was cut by the government I have never heard anything from them’. (Interviewee 8, Senior Trade Union Official, 24/07/19).

On the bright side, one of the positive consequences of digitalisation in automating dull and repetitive tasks is also acknowledged here. As one informant said: ‘We have had at the EWC and the UK level discussions about digitalisation plans and we are also included in consultation of change, for example, Invoice Finance. […] It is a fairly dull job’ (Interviewee 8, Senior Trade Union Official, 24/07/19).

Some processes that were mentioned as examples (e.g. Automatic processing of email invoices) seem to be positive developments, they do not extinguish – in the short run – whole jobs, just remove some repetitive tasks, also contributing to job quality. ‘What they have come up with is what they call a robot, which will read these invoices, and then populate the computer system, meaning that there is no employees needed. (…) They think they can get a high accuracy, or higher than people, to do that specific job. If you try to expand out into some of the more complicated jobs, it’s going to be quite a long time before you get to that stage’ (Interviewee 8, Senior Trade Union Official, 24/07/19).

Comparative discussion and conclusion

The case studies enhanced the plausibility of the argument that embedded employment relations’ institutions and actors shape the direction of adjustment paths to digitalisation. Although the market and technological pressures (Batt et al., 2009) in both countries’ services sectors were rather severe, the ultimate process of work restructuring varied. In both countries, the banks had to adjust to the massive introduction of online and mobile banking, the automation of processes, and the entry of new Fintech players in the sector; similar systemic legacies; and new tight regulations following the 2008/9 global financial crisis.

In Luxembourg, the adjustment to digital transformation was not left entirely to market forces. Instead, the unions and the employers relied on sectoral bargaining, informal tailor-made solutions and the mobilisation of law-based neo-corporatist tools, such as social plans, to shape the direction of change towards a softer transition and avoiding mass lay-offs. Collective labour agreements acted as institutional constraints (Doellgast, Holtgrewe, et al., 2009) to convergence and a technology-driven race to bottom. Instead, policies such as internal mobility and increase in the spending for retraining constituted avenues to cushion digital transformation effects and maintain job quality for employees. The role of the state (Doellgast, Nohara, et al., 2009) was also critical, as the social partners were able to tap on the resources of the state and engage in extensive reskilling and retraining programmes. By contrast, in the United Kingdom, the supporting role of the state (Doellgast, Nohara, et al., 2009) is missing, as the government withdrew its support for the institution of sectoral skill formation that could facilitate reskilling. This exacerbated the legacy of broken-down sectoral bargaining and created an institutional void. The adjustment to digitalisation was unilaterally employer-led with the union mainly being informed about planned changes; and fragmented responses such as union campaigning against local branch closures.

Overall, our analysis highlights the persisting importance of institutional differences and ‘power resources’ (Benassi et al., 2016; Ibsen, 2015; Lloyd and Payne, 2021) and how they are also relevant to moderate the wide-ranging effects of digitalisation. Although digitalisation pressures were similar, the persisting institutional differences in regard to the role of the state in supporting reskilling (Doellgast, 2010) and capacities of employers’ associations (Brandl and Lehr, 2019) for consensual bargaining explains the degree and path of adjustment.

Finally, our analysis suggests that the driving force of job losses is still offshoring rather than automation and digitalisation, at least for now, and concurs with the perspective that expected job losses due to automation are exaggerated (Grimshaw, 2020). Previous waves of technological change in the banking sector, such as the introduction of ATMs and debit cards, transformed the career structures and refocused jobs on performance and sales, but did not have a severe impact on levels of employment (Regini et al., 1999). By contrast, this wave of digitalisation is accompanied by branch downsizing and job losses. The jobs are not changing, but they are moving elsewhere. Yet, the differences between liberal and coordinated models of capitalism (Batt et al., 2009; Witt et al., 2018) are still important while sectoral specificities also matter (Lloyd and Payne, 2021). Further research could helpfully enrich this debate by examining the role of collective voice institutions in shaping digitalisation in other country contexts and white-collar services sectors.

Footnotes

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research has benefited from partial funding from a Visiting Scholar research scheme from the Luxembourg Institute of Socio-Economic Research (LISER) and a small grant from the King’s College London SSPP Research Fund.