Abstract

Regressive consumption taxes - especially value-added taxes (VATs) - are often seen as a “money machine”: they raise substantial revenue while sparing mobile capital, and thus are thought to help governments sustain generous welfare states under fiscal pressure. Existing accounts largely treat this “regressive tax-welfare nexus” as a structural relationship that operates independently of political context. We revisit this assumption by foregrounding the role of partisanship. We argue that while regressive taxes provide substantial and stable revenue, only left-leaning governments tend to channel these resources into welfare expansion. Non-left governments may also raise regressive taxes, but typically allocate the proceeds elsewhere. Using panel data for 20 OECD countries over three decades, we show that increases in VAT rates are positively associated with welfare state generosity only under left governments. Our findings challenge structural interpretations of the tax-welfare relationship and demonstrate that partisan politics continues to shape how governments deploy regressive revenues.

Introduction

Existing research on the welfare state’s funding base has established an enduring connection between regressive taxation and welfare provision in rich democracies (Ganghof, 2006; Kato, 2003; Lindert, 2004; Prasad and Deng, 2009; Wilensky, 2002). This literature emphasizes the transformative role played by regressive taxation, and the Value Added Tax (VAT) in particular, in helping governments secure the financial resources necessary to maintain or expand welfare states. Regressive taxes have two crucial qualities setting them apart from other leading modern taxes. They are efficient revenue-raisers, being relatively easy to levy and administer and hard to evade; and critically, they are lenient on capital compared to income and property taxes, and are thus unlikely to provoke capital flight (Ebrill et al., 2001; Ganghof, 2006; Kato, 2003; Keen and Lockwood, 2010; Wilensky, 2002). The implications of this regressive tax–welfare nexus are potentially profound. Kato (2003: 3) argues that “tax politics ultimately explain the diversification of high-spending and low-spending countries,” as those which shifted toward regressive taxation were better able to maintain or even expand their welfare states than others that relied on progressive taxes (Steinmo, 1993; Kato, 2003: 22; Wilensky, 2002: 236).

In this article, we explicitly test the proposition that regressive taxation supports greater welfare generosity (Wilensky, 2002: 236; Kato, 2003: 22). A motivating puzzle for this enquiry is that countries relying most heavily on regressive taxation include some of the most comprehensive welfare states — such as Denmark, Norway, and Sweden — but also some of the least generous, like the UK and Ireland. This does not square well with the theory that regressive taxes are necessarily guarantors of generous welfare states.

The central hypothesis we advance is that the extent to which welfare regimes are sustained by regressive taxation is conditional on the partisanship of the incumbent government, rather than automatic (see Kato, 2003: 22; Wilensky, 2002: 236). Specifically, only left-leaning governments tend to use windfalls from regressive taxes for welfare expansion, while non-left governments are more likely to prioritize spending elsewhere. Left-wing parties have been ideologically committed to expansive welfare policies and have historically drawn support from constituencies that benefit directly from welfare programs, such as working-class voters and public sector employees, whereas non-left parties have generally favored a reduced public sector and/or prioritized other forms of expenditure (see Esping-Andersen, 1990; Huber and Stephens, 2001; Korpi, 1978, 1989). Our hypothesis about the differential impact of regressive taxation based on government ideology integrates insights from two key literatures: one identifying regressive taxation as a critical funding source for welfare states, and the other linking left-wing parties to higher levels of welfare state spending (Hicks and Swank, 1992; Huber and Stephens, 2001; Kittel and Obinger, 2003; Korpi, 1978, 1989).

Most empirical work has focused on explaining whether and when governments adopt regressive taxes, with some debate remaining as to whether this preference is universal across partisan lines. While many scholars agree that existing welfare state commitments push governments toward more regressive taxes due to their revenue-raising power (Beramendi and Rueda, 2007; Helgason, 2017; Kato, 2003), others — particularly those working in the “worlds of taxation” tradition — emphasize that tax policy is deeply political, shaped by distinct historical trajectories, institutional frameworks, and political coalitions (Campbell, 1993; Castles, 1998; Obinger and Wagschal, 2001; Obinger and Wagschal, 2012; Steinmo, 1993). While sympathetic to this view, we argue that even amid convergence on regressive taxation, partisanship continues to play a crucial role — not in the choice of tax instrument itself, but in how regressive tax revenue is allocated.

Our focus, therefore, is less on the determinants of tax adoption and more on the political consequences of regressive taxation for welfare generosity — a relationship that has received relatively little empirical scrutiny. Using panel data covering 20 OECD countries over three decades, we empirically test the proposition that the historical development of regressive taxation paved the way for greater welfare generosity over time (Wilensky, 2002: 236; Kato, 2003: 22). 1

Our analysis demonstrates that a strong reliance on regressive taxation, measured using the VAT standard rate, is only associated with higher welfare state expenditure when left-leaning governments are in power. This finding suggests that the positive relationship between regressive taxation and greater welfare state generosity is strongly conditional on government partisanship.

The results remain robust across a range of alternative empirical specifications, including different operationalizations of regressive taxation (Ganghof, 2006). Recognizing that the VAT is only part of a broader regressive tax mix (Ganderson and Limberg, 2021), we also use an index of broad-based regressive taxes — encompassing turnover and general sales taxes — to capture historical tax system evolution (Ganghof, 2006). The partisan effect persists even with this more expansive measure, reinforcing our conclusion that the regressive tax–welfare nexus is fundamentally partisan-dependent.

The remainder of the article proceeds as follows. The next section outlines the argument that the link between regressive taxation and greater welfare state resilience is conditional on government partisanship, illustrating the argument with the British experience. We then present data, econometric models, and estimation results, followed by robustness checks that offer further evidence supporting the partisan argument. Finally, we briefly conclude, summarizing findings and situating their scholarly and applied policy implications in historical context.

Regressive taxation, welfare state generosity and partisanship

By design, regressive sales and consumption taxes like VAT are imbued with a revenue-raising capacity that many other taxes lack. In contrast to corporate and income taxes, VAT spares capital and is therefore unlikely to induce capital flight. On average, it now generates 20% of OECD state tax revenue, rapidly becoming an indispensable part of the tax mix of almost all rich democracies (Ganderson and Limberg, 2021). An influential argument in the literature on the welfare state’s funding base suggests that countries which shifted their tax structure toward regressive taxes like VAT during the period of sustained growth following World War II were better able to secure the necessary revenue streams to maintain or even expand social security expenditures during the era of comparatively low growth that followed the 1980s (Kato, 2003: 22; Wilensky, 2002). An underlying assumption in this body of work is that, irrespective of ideology, governments can and do use regressive revenue to sustain welfare states (Ganghof, 2006; Kato, 2003; Prasad and Deng, 2009; Wilensky, 2002). 2

Yet the extent to which partisanship has shaped the evolution of governments’ reliance on regressive taxes remains disputed. Proponents of the “worlds of taxation” tradition argue that countries have developed distinct tax mixes shaped by their historical trajectories, institutional frameworks, and—most importantly—the partisan complexion of governments. Patterns of taxation often overlap with patterns of social spending and cluster into distinct families of nations (Campbell, 1993; Castles, 1998; Obinger and Wagschal, 2001; Obinger and Wagschal, 2012; Steinmo, 1993). More recent studies in this tradition suggest that partisan differences persist in the types of taxes governments prefer, despite a general shift toward more regressive taxation. Left-leaning governments remain more likely to rely on progressive taxes than their right-leaning counterparts—unless constrained by corporatist institutions (Beramendi and Rueda, 2007; Helgason, 2017).

While we share the assumption that partisanship matters, our focus shifts from explaining cross-national variation in countries’ tax structures—as in much of the recent literature—to examining how partisan politics shapes the allocation of regressive tax revenues. In other words, even in a world where many advanced democracies have converged on increasing regressive taxes like VAT—including continental corporatist models that historically relied more on social contributions—we argue that partisanship still plays a critical role in determining how this revenue is used. This interaction of regressive taxation and partisanship has received relatively little empirical attention and deserves to be revisited.

What motivates our inquiry is a striking empirical pattern: countries with similar reliance on regressive taxes display markedly different levels of welfare state generosity. This group includes some of the most comprehensive welfare states, such as Denmark, Norway, and Sweden, but also some of the least generous, like the UK and Ireland (Kato, 2003; Steinmo, 1993). The UK, for instance, shifted toward a regressive revenue structure relatively early. 3 VAT was introduced by a Conservative government in 1973 at a single 10% rate, and later raised to 15% under Margaret Thatcher in 1979 (Victor, 2010). One might expect such revenue to have shielded the British welfare state, which was comparatively well developed by the early 1970s (Starke, 2008). However, evidence of welfare expansion during the subsequent period of economic stagnation is lacking; in fact, major areas including housing and pensions experienced significant cuts (Starke, 2008; Clayton and Pontusson, 1998; Bonoli, 2001; Huber and Stephens, 2001; Pierson, 1996). Interestingly, the increase in VAT to 15% under the Thatcher government coincided with reductions in income tax rates—especially for high earners—suggesting that VAT revenue was used to finance other priorities, such as cuts to more progressive taxes (Backhouse, 2002; Manning, 2015).

The UK case also hints at a moderating effect of political partisanship in the tax–welfare relationship. VAT had been championed in the 1960s by British Conservatives with no welfarist motives, 4 whereas in Sweden, it was promoted by social democratic governments averse to income and capital taxation but eager to maximize regressive tax revenues for progressive welfare expansion (Andersson, 2022).

This contrast informs our core theoretical claim: we hypothesize that only left-leaning parties are likely to use VAT revenue to support welfare expansion. By contrast, non-left parties will either redirect this revenue to other spending priorities or use it to offset cuts to more progressive taxes.

This hypothesis connects to a large body of literature associating left-wing parties with greater welfare state expenditure (Hicks and Swank, 1992; Huber and Stephens, 2001; Kittel and Obinger, 2003; Korpi, 1978, 1989). Some authors emphasize electoral incentives, noting that left parties have historically drawn support from constituencies that benefit directly from welfare programs, such as working-class voters and public sector employees (Anderson and Beramendi, 2012; Lindvall and Rueda, 2018). Others, however, attribute this to the programmatic and ideological commitments of left-wing parties to principles of equality and social justice (Esping-Andersen, 1990; Huber and Stephens, 2001; Korpi, 1978, 1989). More recent approaches in this tradition show that political actors are indeed genuinely policy-seeking, rather than purely motivated by electoral incentives, a point reflected in the fact that elite preferences do not always align with those of voters (Wenzelburger and Zohlnhöfer, 2021). Whether due to policy-seeking commitments or electoral incentives, we therefore expect that left-leaning governments will use revenue from regressive taxation to expand the welfare state, whereas non-left governments will not.

To be clear, we do not claim that non-left incumbents necessarily pursue welfare retrenchment. Research has shown that even right-leaning governments are often reluctant to roll back welfare states, for fear of electoral backlash (Basinger and Hallerberg, 2004; Häusermann, 2012; Myles and Pierson, 2001; Pierson, 1996). However, we argue that the allocation of regressive tax revenue is partisan: left governments are more likely to use it to protect or expand the welfare state, while right governments will pursue alternative uses.

Data and measurement

We use the VAT standard rate as our main measure of regressive taxation and lag it by 1 year to partially address the challenge of simultaneity bias. The VAT standard rate is a widely used indicator which has the advantage that it measures direct policy change (Lierse and Seelkopf, 2016; Limberg, 2022). In contrast, alternative measures such as revenue yields or effective rates are more affected by prevailing macroeconomic conditions.

However, we recognize that there is a lively discussion in the tax policy literature on encompassing measures of regressive taxation, both statically and longitudinally. More recent studies suggest that VAT may constitute only one part of a co-evolving regressive tax mix that includes prior consumption taxes and payroll taxes (Ganderson and Limberg, 2021; Ganghof, 2006). For instance, in most countries VAT merely replaced an already-existing national General Consumption Tax (GCT), typically a turnover or general sales tax. GCT rivals VAT in revenue-raising power, while also sparing capital at the expense of burdening lower-income groups (Ganderson and Limberg, 2021) and in many ways was the original regressive ‘money machine’. As such, VAT was chiefly a technological and administrative innovation rather than a revolutionary leap that radically scaled up revenue streams (Ganderson and Limberg, 2021).

An incomplete operationalization of regressive taxation in the form of solely relying on VAT standard rates might skew our estimation of the tax-welfare nexus. Complementing VAT standard rates with a broader, more encompassing measure would allow us to account for cases in which countries might have relied on a set of alternative regressive taxes to achieve the same welfarist goals. Such a measure would also need to include payroll taxes and income taxes targeting lower incomes, which also have the advantage of keeping a moderate tax burden on capital while raising significant revenue (Brittain, 1971; Ganghof, 2006; Kemmerling, 2009; Saez and Zucman, 2019).

In addition to using VAT standard rates we therefore propose an additional variable based on a latent variable approach that allows us to incorporate a variety of different measures of regressive taxation. We construct our latent variable of regressive taxation using six indicators, including both statutory tax measures (Ahrens et al., 2020; Lierse and Seelkopf, 2016; Limberg, 2019; Scheve and Stasavage, 2012) and tax revenue measures that consider the size of the tax base (Adam et al., 2013; Osterloh and Debus, 2012). The composite indicator includes: (1) the VAT standard rate, as a signal of purposive policy intent (Lierse and Seelkopf, 2016); (2) the overall revenue from all consumption taxes (OECD, 2021b); (3) the average effective tax rate on consumption (McDaniel, 2007); (4) the average effective tax rate on payroll (McDaniel, 2007); (5) the income tax rate for citizens in the bottom income tax bracket (Lierse and Seelkopf, 2016); (6) the average effective tax rate on the bottom third of household wage incomes, which captures the tax burden from both personal wage income and social security contributions (Egger et al., 2019).

This indicator allows us to account for allowances, reliefs and other tax exemptions. All measures load positively onto the latent variable, but the correlation is strongest for the VAT standard rate measure (see Figure A2 in the Appendix).

5

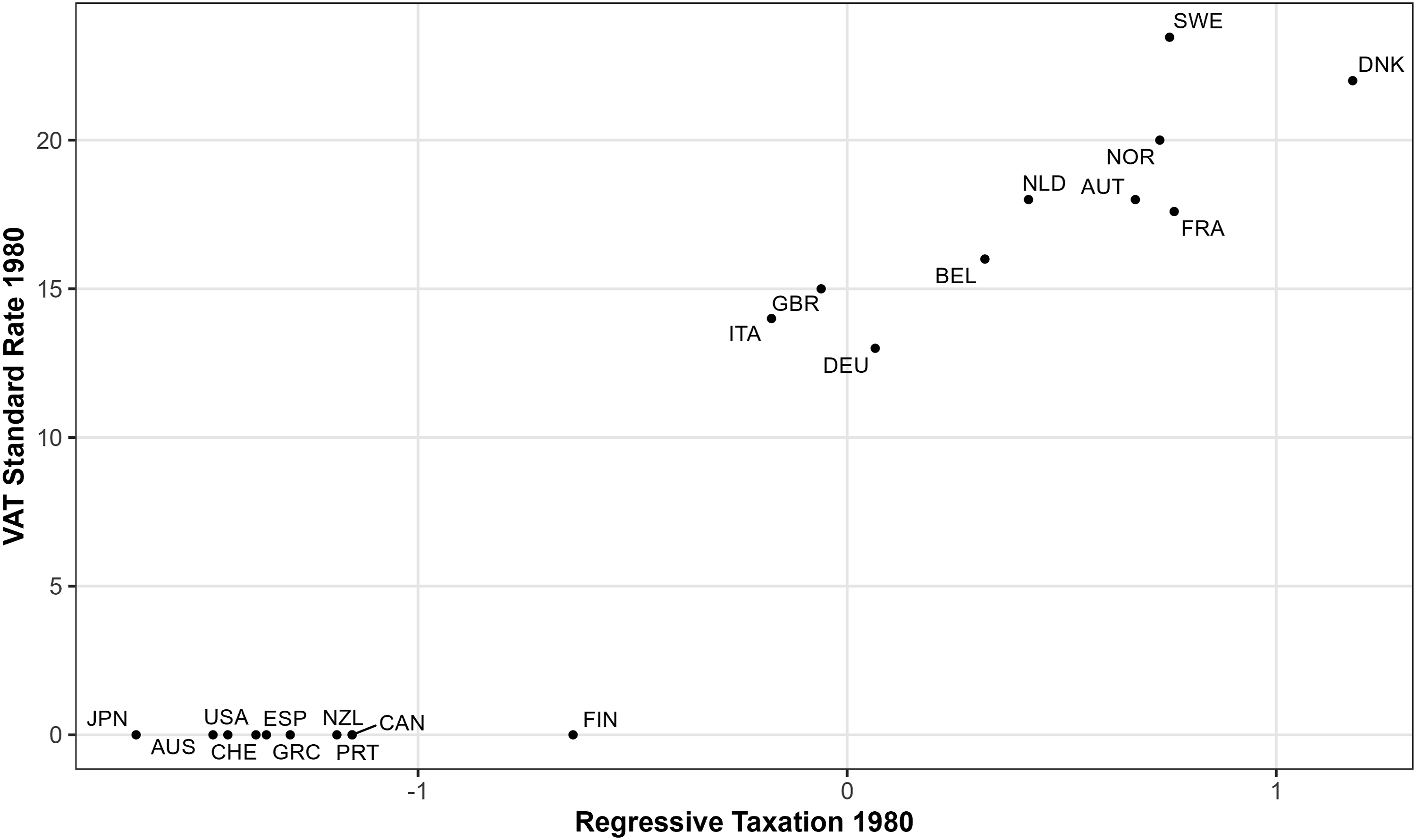

Our new indicator ranges from −1.7 to 1.5 with a mean of 0 and a standard deviation of 0.9. When we plot our new measure against the VAT standard rate for the first year of our observation period, we find that the two measures are highly correlated (Figure 1). This shows support for our main approach of using VAT rates as a proxy for regressive tax policy change. However, there is also some variation. For instance, Finland seems to be one of the very few countries that extracted substantial revenue from regressive taxes in the absence of a VAT. Thus, we present results for both the standard VAT rate, as a more conventional measure, and our new indicator of regressive taxation. New indicator of regressive taxation.

The operationalization of welfare state effort, our dependent variable, has also sparked an ongoing debate, with some researchers opting for policy-based generosity indices (Scruggs et al., 2013) and other authors relying on social spending as a share of GDP (see for instance Huber and Stephens, 2001). We operationalize our dependent variable using the general welfare state generosity index from the Comparative Welfare Entitlement Dataset (Scruggs et al., 2013), a policy-based measure. The index builds on the work of Esping-Andersen (1990) and uses data on replacement rates, eligibility criteria, and duration of benefit payments for three main social policy areas (unemployment insurance, sickness insurance, public pensions) to measure a country’s overall welfare state generosity. Using a policy-based measure, instead of a spending measure as previous studies on the tax-welfare nexus have done, is another step towards tackling the simultaneity bias inherent in the nature of the budgetary process. However, we also use spending measures as an alternative specification of our dependent variable to check the robustness of our findings (Table A5). Data come from the OECD’s social expenditure database and cover all 20 countries in the sample from 1980 onwards (OECD, 2021b).

Since we are interested in how partisanship moderates the relationship between regressive taxation and welfare state generosity, we include an interaction term between VAT standard rates and government partisanship. We measure government partisanship using the percentage of cabinet posts that are held by left parties in a given year (Armingeon et al., 2021). In line with the theoretical argument, we expect that value-added tax rates changes are only associated with welfare state generosity under leftist governments. In other words, left parties in power use VAT rate hikes to expand or sustain welfare state generosity. In contrast, we do not expect to see this positive association between VAT reforms and welfare state generosity under non-left governments. Because various measures of left party strength are often used in the comparative politics literature (Döring and Schwander, 2015), we also run our models using an indicator that measures the strength of leftist parties by looking at the share of parliamentary seats as a percentage of total seats held by the government (Armingeon et al., 2021), as well as a measure of ideological hegemony developed by Schmidt (1996). This measure ranges from ‘1’ indicating a hegemony of rightist and centrist parties to ‘5’ indicating a hegemony of leftist parties. Results hold when using these alternative measures (Table A1 and Table A2). 6 Furthermore we include measure of left-party strength from the PACOGOV dataset (Table A3) as well a variable that includes both leftist and Christian Democratic parties, which scholars have credited as key originators and mediators of welfare state development (Mares, 2003; Van Kersbergen, 1995) (Table A4).

We include a battery of covariates to control for other dominant explanatory factors in the comparative welfare state literature. First, higher welfare dependency ratios increase spending automatically, which can assert downward pressure on social policy. To account for this, we include a country’s unemployment rate as well as the share of people over 65 in our regression models (Armingeon et al., 2021). Second, we also control for a country’s wealth as well as economic fluctuations by including variables that measure GDP per capita (logged) as well as real GDP growth (OECD, 2021a; World Bank, 2021). Third, the economic openness of a country might impact both social policy and tax policy (Garrett and Mitchell, 2001). To account for this we include the total trade openness measured via imports and exports as percentage of GDP (Feebstra et al., 2015). Fourth, institutional veto points could affect policy-making by reducing a government’s room to manoeuvre (Immergut, 1990). Therefore, we include a time-varying index that measures institutional constraints (Armingeon et al., 2021; Schmidt, 1996). Finally, general fiscal problems and economic cycles might be driving social and tax policy making (Schäfer and Streeck, 2013; Steinebach et al., 2019). To account for the impact of fiscal problem pressure, we include a country’s deficit as a percentage of GDP (OECD, 2021a) as well as the yearly average of long-term interest rates on government bonds (OECD, 2021a).

Empirical analysis

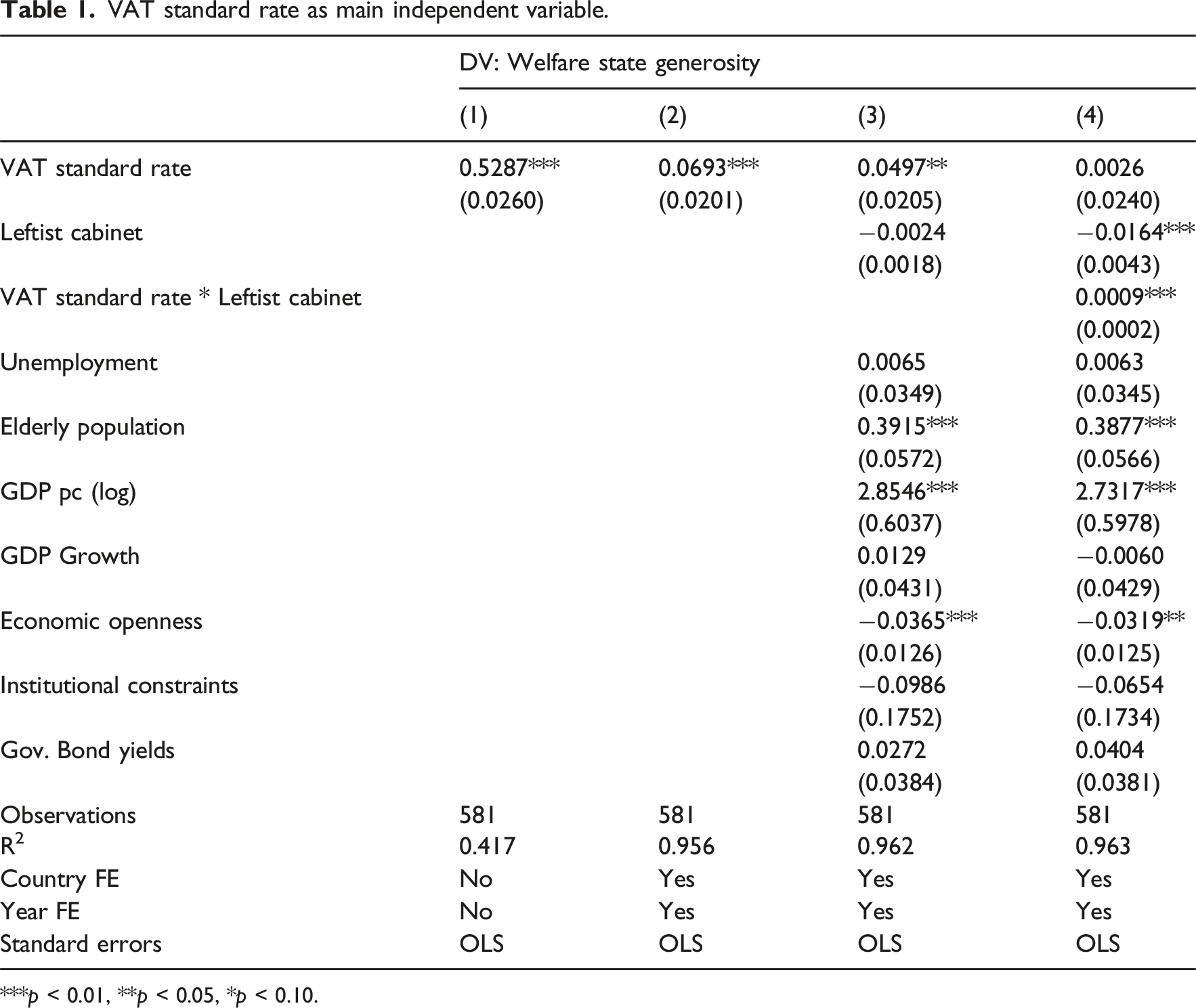

VAT standard rate as main independent variable.

***p < 0.01, **p < 0.05, *p < 0.10.

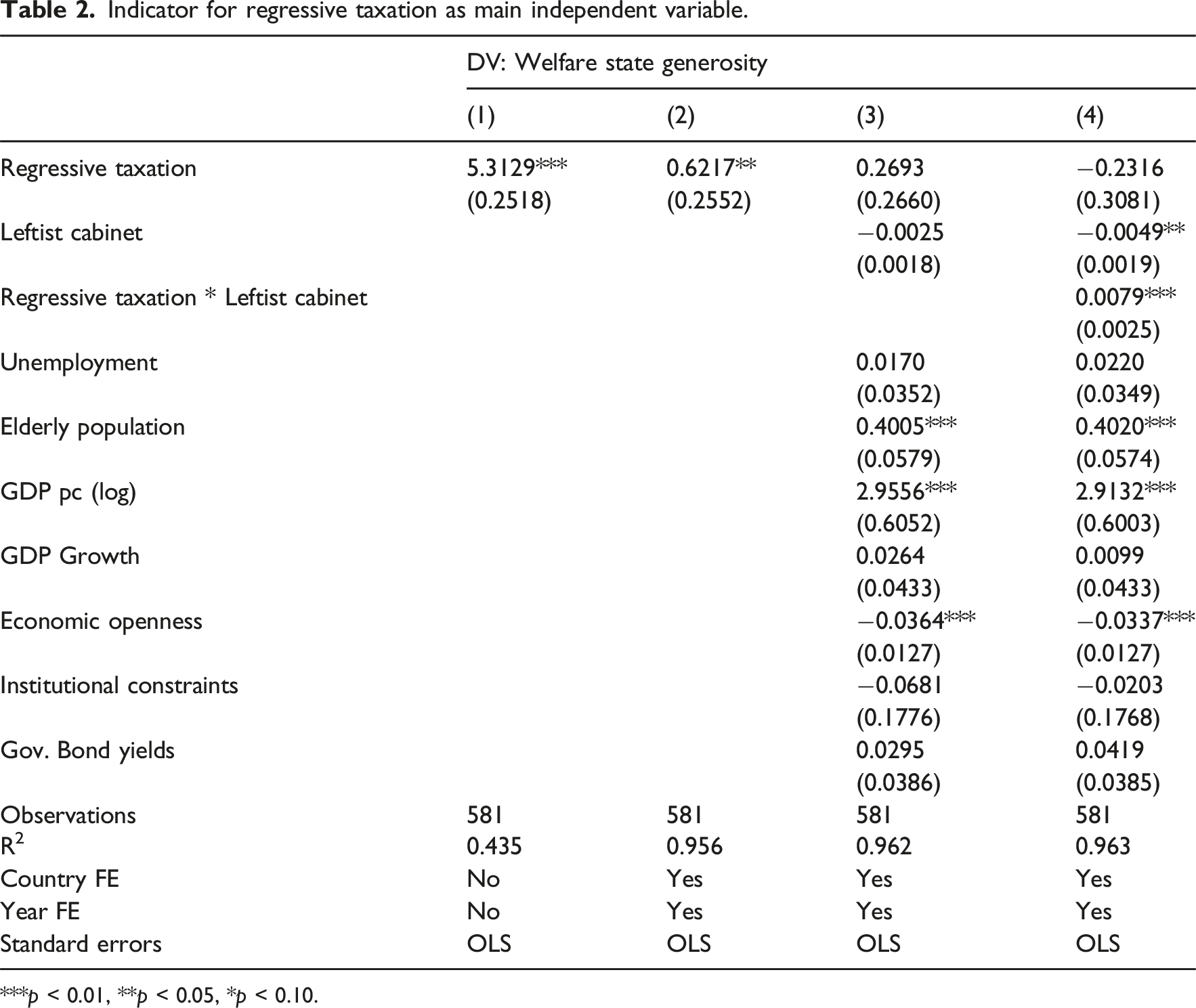

Model 1 shows that VAT standard rates are positively associated with welfare state generosity. This finding also holds when including two-way fixed effects (Model 2) and adding a battery of covariates (Model 3). These results support existing work that has theorized a strong positive relationship between regressive taxation and welfare state generosity (Kato, 2003; Steinmo, 1993; Wilensky, 2002). This average effect of regressive taxation does, however, conceal important variation. The interaction term between VAT standard rates and partisanship (Model 4) is positive and statistically significant. This indicates that the relationship between VAT rates and welfare state generosity depends on political partisanship. We can find the same pattern when using our novel indicator for regressive taxation instead of VAT standard rates (Table 2, Model 4).

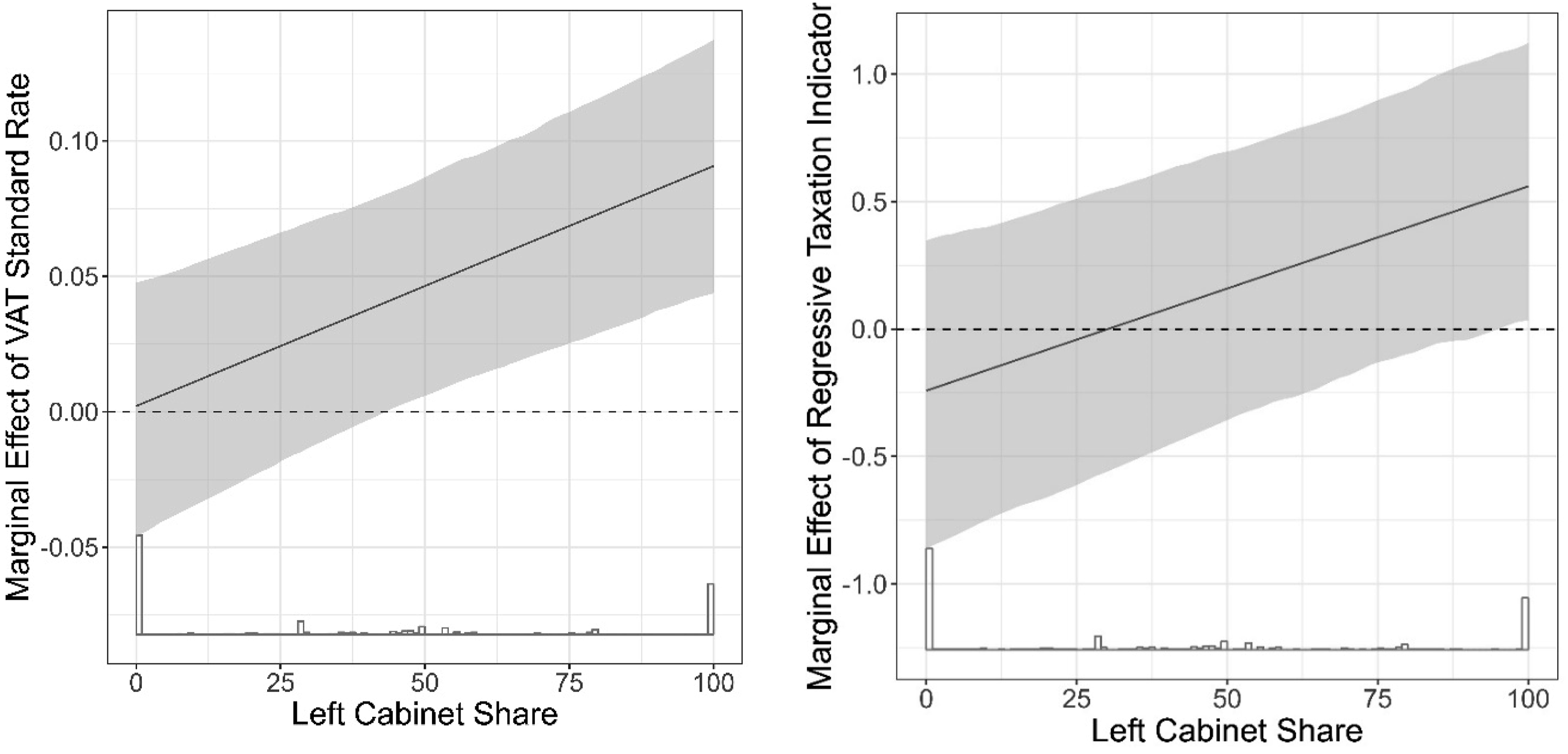

In order to interpret the results of the interaction term substantially, Figure 2 plots the marginal effect of the VAT standard rate (left panel) and our regressive taxation indicator (right panel) conditional on left cabinet share (Brambor et al., 2006). The histogram on the x-axis visualizes the distribution of our left cabinet share. Note that the majority of observations (around 80%) consist of governments that either include no ministers from left-wing parties or are composed entirely of left-wing party ministers. In line with our hypothesis, the marginal effects plot shows that the relationship between VAT tax rates and welfare state generosity depends on partisanship (left panel). In a cabinet that solely consists of conservative and centrist parties, there is no relationship between regressive taxation and welfare state generosity. In contrast, the relationship is positive and statistically significant for countries with a left cabinet share of more than 50%. For cabinets that are solely made up of left-wing party ministers, a 1-point increase in the VAT standard rate is associated with an increase in the generosity index by around 0.1 points. Furthermore, we can identify a similar pattern for our regressive taxation indicator (right panel). Here, the effect becomes statistically significant only for cabinets composed exclusively of ministers from left-wing parties. Indicator for regressive taxation as main independent variable. ***p < 0.01, **p < 0.05, *p < 0.10.

These findings support our argument that the link between regressive taxation and welfare state generosity is dependent on political ideology. In countries like Sweden, where social democratic governments adopted VAT and subsequently increased VAT rates, there is indeed a positive link between regressive taxation and welfare state generosity. However, this is not the case in countries where the incumbent government is not predominantly composed of left-leaning parties. This is not to say that non-left governments necessarily retrenched the welfare state. Rather our findings suggest that the revenue from VAT rate increases does not positively impact welfare state generosity when governments are mostly composed of cabinet ministers from non-left parties.

Robustness checks

As TSCS analyses can be sensitive to modeling choices (Kittel and Winner, 2005; Schmitt, 2016) and have recently been criticized for combining within-unit and cross-sectional variation in ways that may produce uninterpretable results (Kropko and Kubinec, 2020), we assess the robustness of our findings using alternative econometric approaches. First, we rerun our analysis using a Prais–Winsten estimator to account for potential serial correlation and find that our results remain stable (Table A15). As a further way of addressing serial correlation, we replace year fixed effects with unit-specific linear time trends. Unlike a pure correction to the error structure, time trends explicitly model systematic temporal dynamics within each unit, absorbing—albeit only partially—gradual changes over time that might otherwise manifest as serial correlation. We also rerun our models without any time trends. The results remain robust under both specifications (Tables A6 and A7). We also estimate a specification with two-way fixed effects, a lagged dependent variable (LDV), and PCSEs (Table A9, Model 1). While this specification does not yield statistically significant results, we view this outcome with caution given the well-documented limitations of this approach, including the absorption of substantively meaningful variation (Schmitt, 2016) and the risk of Nickell bias, which arises from correlation between the lagged dependent variable and the error term (Demetrescu et al., 2025; Gaibulloev et al., 2014; Hausman and Pinkovskiy, 2017; Keele and Kelly, 2006; Nickell, 1981; Plümper et al., 2005). To address these concerns, we therefore estimate an Arellano–Bond GMM model (Arellano and Bond, 1991), which mitigates Nickell bias by using lagged levels of the dependent variable as instruments. This dynamic panel estimator is specifically designed to address issues arising from the inclusion of a lagged dependent variable into fixed effects models while maintaining consistency. The results of the Arellano–Bond model confirm our main finding that partisanship moderates the effect of VAT tax rates on welfare state generosity (Table A9, Model 2).

To acknowledge that the budgetary process is not unidirectional, and that the causal relationship between regressive taxation and the welfare state can run either way (Ganghof, 2006), a common strategy used in existing empirical studies on the tax-welfare nexus involves a two-stage least-squares regression (Kato, 2003). This empirical strategy allows us to check whether our results hold when using a model that partially accounts for potential endogeneity. We use VAT rates in period t-2 as an instrument for our two-stage least-squares setup (Table A17). Again, findings hold. Crucially, however, our main argument is not about the causal direction, but about partisanship shaping the connection between regressive taxation and welfare generosity.

We also rerun our analysis using an approach proposed by Garritzmann and Seng (2020) that accounts for the clustering of country year observations into cabinets via random intercepts (Figure A8). We find that our results hold. In addition, we rerun our main model with a series of alternative standard errors to check whether results hold (Beck, 2001; King and Roberts, 2015). Instead of regular OLS standard errors, we use PCSEs which account for problems of heteroskedasticity (Beck and Katz, 1995). To ensure that our findings are not driven by influential cases we also apply a jackknife resampling procedure to estimate standard errors. Results hold when calculating these alternative standard errors (Tables A14 and A16).

Conclusion

While often assumed to go hand-in-hand, the relationship between regressive tax revenues and welfare state generosity is more conditional than widely acknowledged. Existing literature has frequently emphasized the importance of structural pressures that transcend partisan divides: a regressive VAT can help policymakers navigate the dual challenges of sustaining welfare commitments while accommodating capital mobility (Kato, 2003; Wilensky, 2002). This perspective suggests that certain regressive taxes may, paradoxically, support expansive welfare states. However, cases like the UK—where regressive tax adoption did not translate into sustained welfare generosity—challenge this assumption and highlight the need for a more nuanced explanation.

This article proposes a new theoretical framework that brings together insights from two key literatures: one that views regressive taxation as a critical funding mechanism for welfare states, and another that links left-party strength to more expansive social spending (Huber and Stephens, 2001; Korpi, 1978, 1989). Our central argument is that the partisan orientation of the government is a crucial mediating factor in the regressive tax–welfare state relationship. Specifically, only left-leaning governments tend to use windfalls from regressive taxes for welfare expansion, while non-left governments are more likely to prioritize spending elsewhere. We test this argument across multiple rich democracies over a period of more than three decades.

In sum, we find strong support for our hypothesis: partisanship conditions the effect of regressive taxation. Our results show that only left-wing governments devote the proceeds of VAT and other regressive taxes to welfare state retention. The connection between regressive VAT and the welfare state does not hold when non-left parties are in power. These parties often raise VAT rates while not expanding welfare, using VAT revenues for different types of spending or for cutting other taxes. These results are robust to multiple alternative model specifications and a variety of different measures. Most importantly, we find that our results hold when we examine whether different regressive taxes may act as substitutes for VAT, our main proxy for regressive taxation.

This analysis is not without limitations. First, more granular research may be conducted on the regressive tax–welfare nexus, drawing out the origins, mechanisms, and policy limits of the partisan effect in different historical eras and cases. More precisely, our findings suggest that VAT hikes under non-left governments are associated with a set of different priorities, such as cuts to other taxes. Second, due to data restrictions, our analysis is limited to the period since the 1980s and to core OECD countries. Therefore, it would be interesting to expand the historical coverage and investigate whether our findings show temporal variation, dependent on the varying growth of regressive, indirect consumption taxes (Ganderson and Limberg, 2021).

Our findings have important implications for policymakers. As fiscal consolidation and demographic pressures continue to reshape welfare models across advanced democracies, left-wing parties—historically more committed to welfare state expansion—may increasingly rely on regressive taxes to sustain social spending. However, the long-term sustainability of this strategy is uncertain, particularly given the rising inequality and wealth concentration often associated with regressive tax regimes. For non-left parties, this pressure is arguably less pronounced, as they tend to show more openness to austerity politics and may be less committed to preserving expansive welfare states. For the left, however, a new era may be emerging. If welfare systems come under intensified strain in the coming years, governments may no longer be able to rely on VAT increases alone to maintain them—potentially forcing a renewed turn toward more progressive taxation.

Supplemental Material

Supplement Material - Partisanship and the nexus between regressive taxation and the welfare state

Supplemental Material for Partisanship and the nexus between regressive taxation and the welfare state by Hanna Kleider, Julian Limberg, Joseph Ganderson in Journal of European Social Policy

Footnotes

Acknowledgments

We thank Olivier Jacques and Stefanie Moller for helpful discussions and valuable feedback on this project. We are also grateful to participants of the 2022 UNC Inequality Workshop at the University of North Carolina at Chapel Hill for their insightful comments, including Pablo Beramendi, David Brady, Evelyne Huber, Gary Marks, Bilyana Petrova, David Rueda, Daniel Stegmueller, and John D. Stephens. We further thank Sarah Niedzwiecki and Zoila Ponce de León for comments on earlier drafts. Finally, we appreciate the constructive suggestions provided by the two anonymous reviewers.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of conflicting interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.