Abstract

Since the 1980s population ageing and economic change has led to cost-containing pension reforms in many industrialized countries. Research has focused on the institutional side of such reforms, but the impact of cost containment policies for real retirees’ pensions remains under-researched. This study addresses this gap. We use the change in projected pension replacement rates for average earners established by the OECD (2002–2019) as an indicator of institutional retrenchment and compare this with the change in the ‘relative pension level’ of real pensioners covering the period 1993–2020 across seven European countries. With data from five waves of the Luxembourg Income Survey and linear regression models we examine whether the average pension income from public and mandatory systems, expressed in relation to average wages (‘relative pension level’), of individuals in the earliest wave, least affected by institutional retrenchment, were significantly different from those of the later waves. The analysis was repeated for subgroups of men and women. We find that institutional change is no reliable predictor of relative pension level change. In the five countries where institutional retrenchment happened, real pension levels fell in only two, in the two countries where they increased no significant change in pension levels occurred. Women’s relative pensions have been more consistent with the expectations of the institutional reform literature than men’s. Our results suggest other variables have mediated the relationship between institutions and pension outcomes, most probably employment change. We conclude that outcome-based analysis is an essential complement to institutional approaches. For policymakers the long-term impact of pension reform is hard to predict, but our results suggest that relative real pension income has been more robust than feared by many.

Keywords

Introduction

Social scientists have demonstrated how populations age, with life expectancy increasing and birth-rates in decline globally (Baltes and Jimon, 2020; Bonenkamp et al., 2017). They agree that because of such trends the public and mandatory pension systems in the mature industrialized countries have been under cost pressure since the 1980s and that they had to become less generous to be financially sustainable (Hinrichs, 2021; Jang, 2019; Valls Martinez et al., 2021). Despite such agreement few studies investigate evidence for a link between pension reform and the actual retirement incomes of individuals from public and mandatory sources, and so far, there has been little comparative research on this matter. There are good reasons for this scarcity. First, there is a lack of suitable data owing to the delayed impact of institutional change on the pensions of retired people, the fact that for many years after a reform retirees’ pensions continue to be based to a significant extent on pension rights accrued under the pre-reform system. The second problem is the interrelatedness of institutional changes and other trends, particularly labour market activity rates, in determining pension incomes (see below).

Nevertheless, since the 1980s, when the period of cost containment began, almost a standard working-life has passed, and it is important for academics and policymakers to know to what extent austerity has actually affected the public/mandatory pensions of people, that is, those pensions which are the main welfare state guarantor of an adequate retirement income. Have those retiring on such pensions in recent years seen a decline in the adequacy of their income from this source compared to earlier cohorts of new retirees or is there evidence that other socio-economic factors, such as increased labour market activity, have mitigated the impact of institutional change? This is the question our article seeks to answer.

We will first give an overview of the literature outlining the change of public/mandatory pension institutions in rich democracies since the 1980s, followed by a review of research on the link between pension systems and retirement incomes. We then explain our analytical approach and the set-up of the empirical parts before describing the sample from the Luxembourg Income Study (LIS). The following section uses regression analyses to compare average relative pension levels for seven countries of two cohorts, one retiring around 1993, the other around 2018, allowing us to compare changing pension adequacy as retrenchment measures progress. We conclude with a reflection on the findings.

Literature review

The retrenchment of pension institutions

Policy responses to ageing populations since the 1980s have been the subject of substantial research, showing that governments found increasing pension costs unsustainable and aimed to contain contributions. They raised pension ages and reversed early retirement schemes (D’Addio et al., 2010; Ebbinghaus, 2015; Whitehouse et al., 2009); they moved towards multi-pillar systems as compensation for public retrenchment (Heneghan and Orenstein, 2019; Hinrichs, 2021; Orenstein, 2008; Kvist and Greve, 2011; Meyer et al., 2007); they adopted ‘financialization’, a shift in funding from pay-as-you-go towards capitalized pensions (Cutler and Waine, 2001; Ebbinghaus, 2019; Hassel et al., 2019); they modified indexing, such as de-linking pensions and inflation or earnings (Whiteford and Whitehouse, 2006); they introduced ‘notional defined contribution schemes’ to public pensions, and made benefits dependent on socio-demographic factors (Holzmann and Palmer, 2012).

Simultaneously, policymakers also adopted measures to increase coverage (Whitehouse et al., 2009), and increased or cut least the level of minimum income protection for retirees (Goedeme and Marchal, 2016; Grech, 2015; Meyer, 2017). Similarly, new care- and children-related pension rights for parents were introduced, potentially favouring women (Frericks et al., 2009; Häusermann, 2010; OECD, 2019).

While there is some evidence the adoption of these measures has varied by regime type, significant institutional reform has been a general feature of pension systems in the Global North in the last decades, including the post-socialist countries (Altiparmakov and Nedeljkovic, 2022; Häusermann, 2010; Hinrichs, 2000).

Overall, the reforms above mean that compared to an older individual who retired under a pre-reform system, a younger one would have to contribute for longer to receive a full public/mandatory pension, that is, their statutory retirement age would have risen. Their pension at that point would replace their wage at a lower level, affecting its adequacy, a gap they would be expected to fill by relying more on private pensions. Their public pension might also rise more slowly after retirement. Only those with an employment career interrupted by care responsibilities might have improved their situation under the reformed system compared to older cohorts; and the reforms may also affect marginalized workers less than high earners.

Thus, the literature on institutional change almost without exception regards the reforms as reducing the adequacy of the public/mandatory pensions received by most retirees on or near retirement, that is, they constitute a retrenchment.

The projected outcomes of institutional reform

Analysis that seeks to determine the scale and nature of the reforms above does not generally focus on the actual outcomes for real pensioners but calculates instead their impact on hypothetical individuals. This analysis assumes that policy change can be measured most precisely with invariant model individuals, instead of complex humans, an approach putting policy centre stage (Burlacu et al., 2014). The OECD has used biographies of hypothetical workers since the late 1990s to show the impact of public/mandatory pension reform (e.g., OECD, 2015). Research using this data projects the decline of individual pension replacement rates in 20 EU countries between 2002 and 2015 (Meyer, 2017) and a fall in pension wealth, that is, life-time mandatory pension benefits, for male and a rise for female retirees between 2005 and 2050 (Grech, 2015: 79–80). Similar micro-simulations suggest the shift towards multi-pillar pension systems would increase poverty risks in countries with voluntary savings (Bridgen and Meyer, 2007) and that the introduction of the sustainability factor in Germany 2004 significantly reduced the projected public pensions of the younger cohorts (Geyer and Steiner, 2014). The Comparative Welfare Entitlements Data Set is also based on ‘notional’ individuals but uses historical data and assumptions for national average replacement rates since the 1960s (Scruggs, 2022). On this basis Bridgen (2022) found that, contrary to expectations of the institutional literature, average replacement rates have remained steady or slightly increased in most countries over the last 20 years. Except for this finding, all other research using hypothetical individuals suggests that reforms have reduced the public/mandatory pension replacement rate which retirees can expect on retirement. It is therefore in line with the pension reform literature discussed in the first section.

The impact of broader economic and social trends on pension incomes

While much of the literature and projections of the impact of these reforms on public/mandatory pensions suggests that they have made systems less generous, the relationship between institutional change and the actual incomes of real pensioners is complicated. Less generous systems should mean lower replacement rates for individuals retiring under the reformed system, all other factors being equal. However, all other factors are never equal. The long-term impact of rule changes on real people also depends on how they respond to reforms, in the context of labour market opportunities, shifting gender norms and other welfare state changes.

Of these factors, employment change is likely to be most important given its centrality for pension accrual. Recent work has shown that cohorts coming of working age in the 1970s have fuller employment biographies and higher lifetime incomes than older cohorts, especially women (Geyer and Steiner, 2014; Glaser et al., 2022; van Winkle and Fasang, 2017). This will have inflated the public pension contribution of younger cohorts, potentially protecting them from the impact of the retrenching institutional reforms of the later periods of their working life (Hinrichs and Jesuola, 2012; Möhring, 2015; van Vliet et al., 2012). From the perspective of gender relations, moreover, it could be that women’s improved employment position has compensated for men’s equivalent pension losses when they retire, so that overall, couples’ households will be less affected by demographic changes and pension retrenchment than is often assumed (Möhring, 2015). Regarding the impact on retirement income of other welfare state arrangements, provision for minimum pensions is particularly important (Möhring, 2015; Ebbinghaus, 2021). 1

Some microsimulation models of the impact of pension reforms, such as Euromod, can allow for such economic and social factors (European Commission, 2024). However, it is only by considering evidence about actual outcomes for public/mandatory pension systems in the years since the reforms that we can detect whether these factors have in fact had an impact. In short, evidence that pension levels from these systems for real pensioners have not declined since the reforms, despite clear indications post-austerity that systems have become less generous, would indicate that compensatory behaviour by workers or other socio-economic factors mitigated the impact of institutional retrenchment. Before such mitigating factors are analysed, it is important to establish whether pension generosity has declined as expected.

Pension outcomes

Some studies have sought to establish the impact of pension reforms on actual outcomes over time, but they are not designed to analyse the adequacy of retirement income at an individual level, or they are flawed. Most work researches aggregate outcomes. Thus, based on data on public/private pension spending as a share of GDP and on income inequality and poverty of retirees between 1995 and 2011 in Western Europe, van Vliet et al. (2012) and Been et al. (2017) found that poverty and inequality declined in most countries. This is important because it suggests that despite declining pension system generosity indicated by institutional analysis, retirement income at an aggregate level has remained robust.

The only work linking reforms and real pensioners asks whether reforms since the 1990s affected the incomes of younger cohorts (born 1960) more than older ones (born 1927), in Austria, Germany, Hungary, Poland and Sweden (Chłón-Domińczak et al., 2020). It finds that pension generosity declined everywhere for cohorts born later than 1940, with the effect strongest for those born in the early 1950s. In contrast to the results on changes in aggregate outcomes, therefore, this study suggests less robust retirement incomes since the pension cost containment period began. Regarding our question, it indicates that if compensatory behaviours or other factors have mitigated the impact of institutional retrenchment this has not been sufficient to prevent decline in real pensions. However, the results of this study are distorted because two of its four cohorts had not reached statutory retirement age and it was unclear whether pension incomes between 2005 and 2013 were adjusted by inflation.

Summing up, the pension reform literature argues almost without exception that institutional changes have reduced system generosity. This is confirmed by most research using projected replacement rates of hypothetical individuals. Despite this significant body of work, research is lacking into whether pension reforms since the 1980s have affected the adequacy of public/mandatory pensions of real retirees. Addressing this gap is important to determine the impact of reform on public/mandatory pension levels and to help establish the extent to which institutional retrenchment has been mitigated by other socio-economic factors, such as increased labour market activity. Below we address these questions by showing the degree of institutional change in seven European countries since the early 2000s, which we then compare with the changing adequacy of the statutory pension income of one older and one younger cohort of new retirees.

Rationale, methods and data

The main aim of our study is to assess whether the general decline in the generosity of public/mandatory pension institutions has led to a decline in the actual incomes of real pensioners. To measure institutional pension system retrenchment in the seven countries of our sample we rely on the OECD’s regular assessment of how public/mandatory pension institutions affect the projected replacement rate of a hypothetical individual working on average wages until normal retirement age (e.g., OECD, 2005). In our definition institutional retrenchment occurred when changes to public/mandatory pensions led to a decline of the projected replacement rate. This happened in most of our countries, for gross and net replacement rates. Between 2002 and 2019 replacement rates fell for model full-time earners in Germany, Greece, Poland and the UK; reductions were projected for Austrian men only, female rates increased. In contrast, in the Czech Republic and Italy rates were projected to rise for all (Table A.1). Meanwhile, retirement ages also increased in all countries but Austria (Table A.2). The OECD has not done equivalent projections for part-time workers nor carers. To gauge the extent to which contributory periods for care times were newly institutionalized, potentially lifting the pensions of women, we analysed the Mutual Information System on Social Security (MISSOC) data base from their earliest data point, 1998 until 2017. New contributory periods for childcare or social care were introduced in Austria, Germany, Italy and the UK during that time. In the Czech Republic existing care periods remained relatively stable. In Greece, between 2003 and 2010 new contributory periods were introduced, but removed in 2012. Poland introduced care entitlements in 2004 and abolished them again in 2015 for those born after 1948 (Table A.3).

To measure real pensioner income during the period of institutional change we used the LIS which has harmonized person-level incomes dating back to the 1970s for 52 countries (LIS, 2021b, 2021a). The main measure of the pension level individuals accrued through their country’s state-owned, or state-regulated system is ‘public contributory pensions’ (value pi32). This captures public contributory pensions, mandatory individual accounts and occupational systems in countries where these schemes dominate. Included are pensions for old-age, disability and survivors. Where universal minimum pensions are part of contribution-based systems, they are included, too. We focus on the public/mandatory pension because they are the main welfare state guarantor of an adequate retirement income above the poverty line (Fouejieu et al., 2021: 49). We investigated whether Survey of Health, Ageing and Society in Europe (SHARE) and European Union Statistics on Income and Living Conditions (EU-SILC) data could be alternatives to the LIS. However, samples were too small for valid analysis in our age groups. Chłón-Domińczak et al.’s (2020) analysis of EU-SILC data uses a larger sample but includes a substantial cohort younger than retirement age whose public pension, if received at all, would be reduced due to early retirement.

To give us the longest possible period for comparison of pension income we included in our study the seven countries for which data was available from the earliest wave (4): Austria, Czech Republic, Germany, Greece, Italy, Poland and United Kingdom (UK). Our largest sample was drawn from the United Kingdom (N = 17,735, 37%), our smallest from Greece (N = 1,195, 3%). Altogether, our sample includes 47,648 individuals.

To determine the adequacy of real pensioners’ income and to make one cohort’s income comparable with another’s, we calculate the ‘relative pension level’ for each wave and country, that is, we compare the average annual income of each pensioner cohort with the average annual gross wages of the economically active population (OECD, 2021). According to the OECD the ‘relative pension level’ ‘is best seen as an indicator of pension adequacy, since it shows what benefit level a pensioner will receive in relation to the average wage earner in the respective country’ (2005:45; similarly: European Commission, 2023: 92). In technical terms we used LIS value pi32 and the formula: relative pension level = (pension/average wage)*100. LIS provides annual pension values in national currency units, mostly euros. For the Czech Republic, Poland and UK we converted national currencies into euros, using annual historical exchange rates.

To measure whether our cohorts’ pension adequacy has fallen during a period of institutional change we compare the relative pension levels of those most recently retired who will have accrued rights under the reformed systems for longest with those who retired at the earliest available point. We include public contributory pension data from LIS from wave 4 (collected 1993–1997) and compare this with wave 10 or 11 (2018–2020).

The LIS data is inconsistent regarding gross and net values. Pension income for Czech Republic, Germany and the UK are all in gross values, data for Poland are all in net values; data for Austria, Greece and Italy are net for waves 4 and 5 and gross for waves 10 (Greece, Italy) and 11 (Austria). To enable comparison between waves for these mixed countries, we adjusted the gross into net values for Austria (wave 11), Greece and Italy (wave 10) to correspond with the earlier waves 4 and 5, using OECD data. This conversion was the only option because data to convert average net to gross pension values for the 1990s is not available. Net pension replacement rates for individuals with average earnings are 13.4 percentage points higher than gross (wave 11) for Austria (OECD 2019); in Italy the equivalent difference is 10.1 percentage points (wave 10); in Greece gross and net replacement rates are identical (OECD, 2017). After these adjustments, we were able to use net data for Austria, Greece, Italy and Poland. The relative pension levels for all our countries are based on gross average wages; because net pensions are higher than gross pensions (Table A.1) our four net countries have higher relative levels than our three gross countries and therefore cannot be compared with each other. Given that our focus here is on changing adequacy in each country over time, it is nevertheless possible to have these different measurements. We can rule out that net pension levels changed only due to higher tax and other contributions and not because of pension system change, because we checked that gross and net pension levels developed in the same direction in all countries.

We selected from each cohort only those men and women who had reached the ‘normal pensionable age’ for their country and cohort at which they were eligible to withdraw full public pension benefits without actuarial reductions or penalties (OECD, 2017: 27) and those up to 2 years older, to augment our sample (Table A.2, appendix). We considered using the same age for all cohorts and countries, but if we had applied the ‘normal pensionable age’ of the older cohort to everyone we would have included many early retirees in the younger cohorts whose pension would have been reduced by penalties, given the ‘normal pensionable age’ for them had increased. Alternatively, if we had applied the ‘normal pensionable age’ for the younger cohorts (male 65 years, female 63 years) to all, the older individuals would already have been retired for up to 12 years (Italy), with pension levels affected by different indexation types. Thus, by selecting the normal national retirement ages for each country and cohort, we include individuals who only just became eligible to draw a public and/or mandatory pension without penalty, reflecting in the most undiluted way the pension system rules valid in that country at retirement.

Because of this decision the qualifying age of our younger cohorts increase with retirement age (except for Austria, where retirement ages remained static, Table A.2) and they vary between countries and genders. It is likely that individuals in the younger cohorts will have had to contribute for longer and more each month to reach a similar level of adequacy than previous ones. While such differences are significant, in this study we are focusing on adequacy at retirement age alone. The other side of what has been called the ‘pension policy equation’ (Economic Policy Committee, 2020: 6) considers matters of actuarial fairness and intergenerational equity, that is, changes in contribution periods, contribution levels during individuals’ active years, and/or life expectancy. These are important considerations, but it is also important to simply determine, as we do here, whether the likelihood of receiving an adequate public or mandatory pension at or close to normal retirement age, independent of all these other factors has declined for individuals during a period of cost containment. The OECD uses the same approach for their projections discussed above. They recognize that individuals’ length of career varies with statutory retirement age (e.g., OECD, 2005: 40; 2011: 116), but they, too, assume that comparing pension outcomes at this age with average wages indicates pension adequacy, suitable to be compared across countries and over time (OECD, 2005: 45). Our study emulates this approach, using real data.

Based on the rationale and approach outlined above, we offer two hypotheses. They would apply if the reform of pensions institutions quantified by the OECD projections in our seven countries translated directly into changes in pension outcomes:

Pension adequacy will decline in countries where pension reforms have reduced projected replacement rates for public/mandatory systems.

Pension adequacy will decline less for women than men in countries where pension reforms have reduced projected replacement rates for public/mandatory systems and increase more in countries where projected replacement rates for public/mandatory systems have increased.

Analyses

Using linear regression analyses we compared the relative pension levels for each country in wave 4 with the next available wave – wave 5 in most cases 2 – and the last available wave. For Czech Republic, Greece and Italy this was wave 10; for Austria, Germany, Poland and the UK it was wave 11. This choice provides the best test of our hypotheses. Thus, comparing changes in relative pension level from the earliest to the final wave meant that we included the oldest and youngest cohort for each country. The public/mandatory pension systems under which these two cohorts accrued pension rights would be expected to be the most different of all our cohorts, altered by all the institutional reforms made during the period. However, because wave 4 covered the period between 1994 and 1997, before OECD replacement rate projections began in 2002, we also included wave 5 (wave 6 in Poland), covering data from around the turn of the century. This enabled a more direct comparison between the OECD’s projected outcomes of institutional change and the results of our analysis.

To test hypotheses one (H1), we analysed the full country sample, controlling for sex, marital status 3 and education. To test hypothesis two (H2), we then conducted a sex-specific analysis, excluding the sex control variable.

Results

Descriptive results

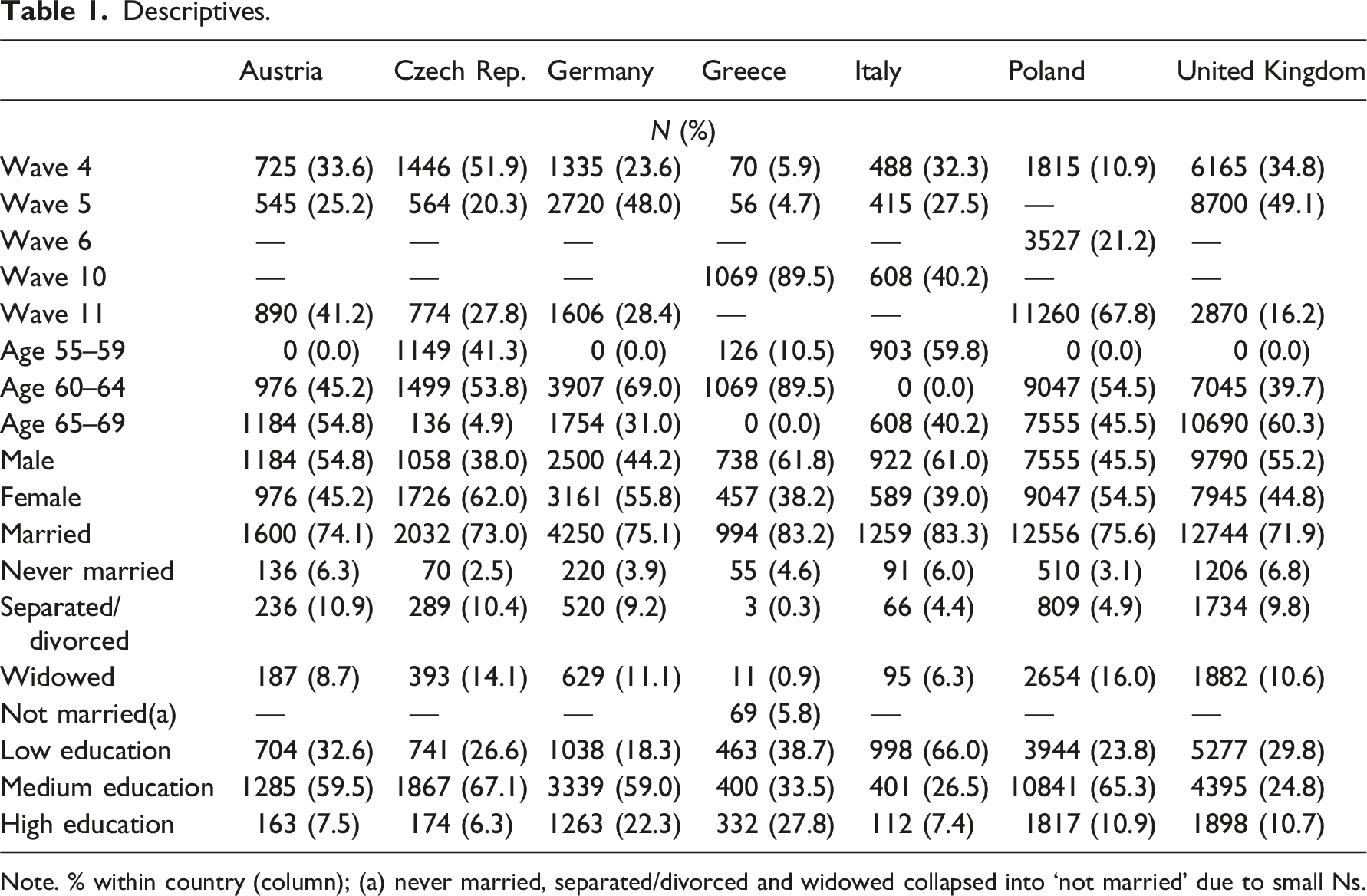

Descriptives.

Note. % within country (column); (a) never married, separated/divorced and widowed collapsed into ‘not married’ due to small Ns.

Due to national differences in normal pensionable age, the age distributions of respondents at the chosen ages (55–69 years) differed substantially. This was a product of our decision, justified above, to focus on the public/mandatory pension received in each country at the normal pension age for each cohort. For example, all Greek participants were under 65 and 60% of Italians were under 60, 55% of Austrian participants and 60% of UK ones were 65 or over. The samples contained more women in the Czech Republic (62%), Germany (56%) and Poland (55%) and fewer in Austria (45%), Greece (38%), Italy (39%) and the UK (45%). Most respondents were married, the highest percentage in Italy (83%) and lowest in the UK (72%). In Greece, Italy and the UK those with the lowest level of education formed the largest group; in Austria, Czech Republic, Germany and Poland the largest group was educated to a medium level. The highest percentage of highly educated respondents was observed for Greece (28%).

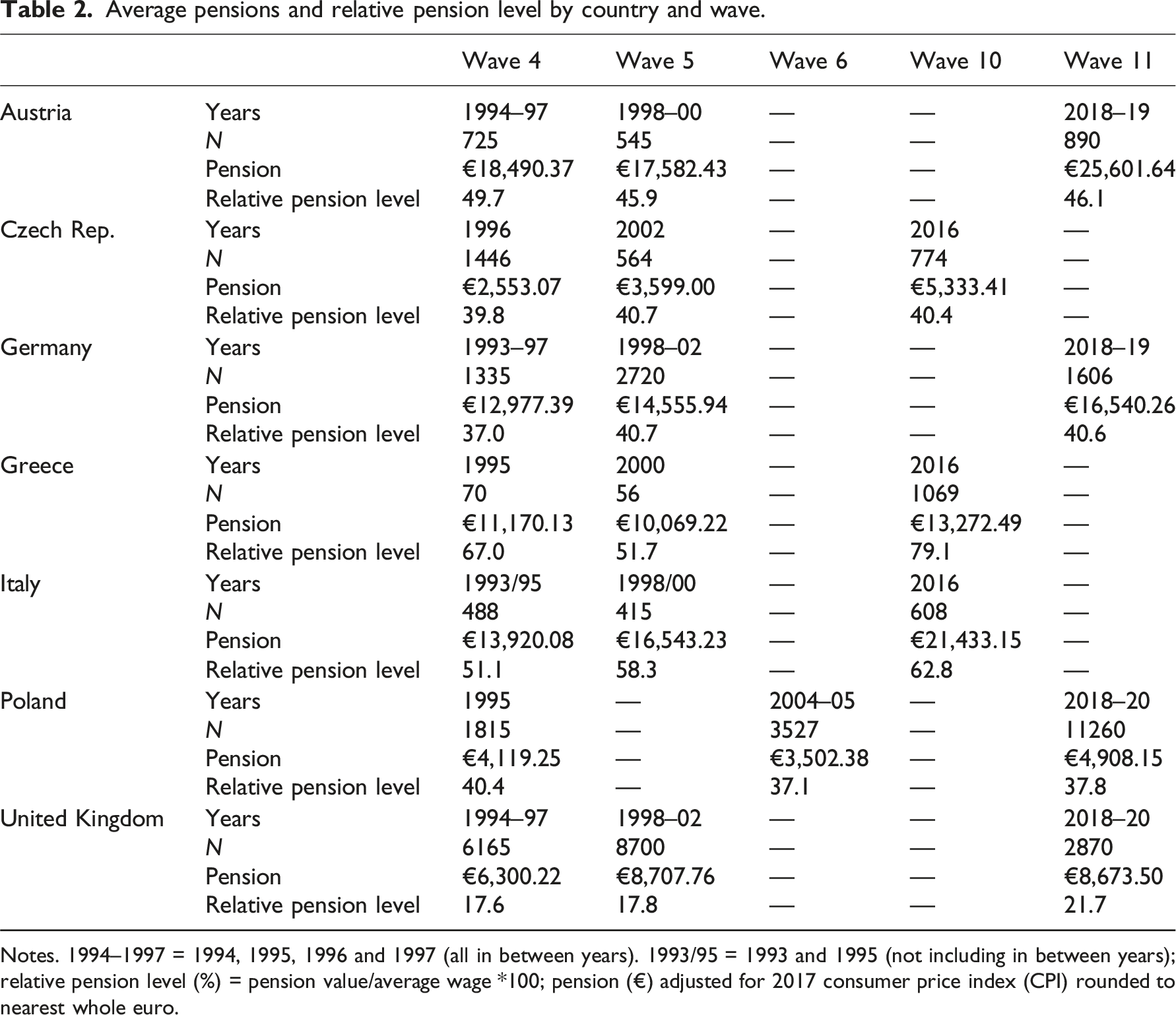

Average pensions and relative pension level by country and wave.

Notes. 1994–1997 = 1994, 1995, 1996 and 1997 (all in between years). 1993/95 = 1993 and 1995 (not including in between years); relative pension level (%) = pension value/average wage *100; pension (€) adjusted for 2017 consumer price index (CPI) rounded to nearest whole euro.

Regression results

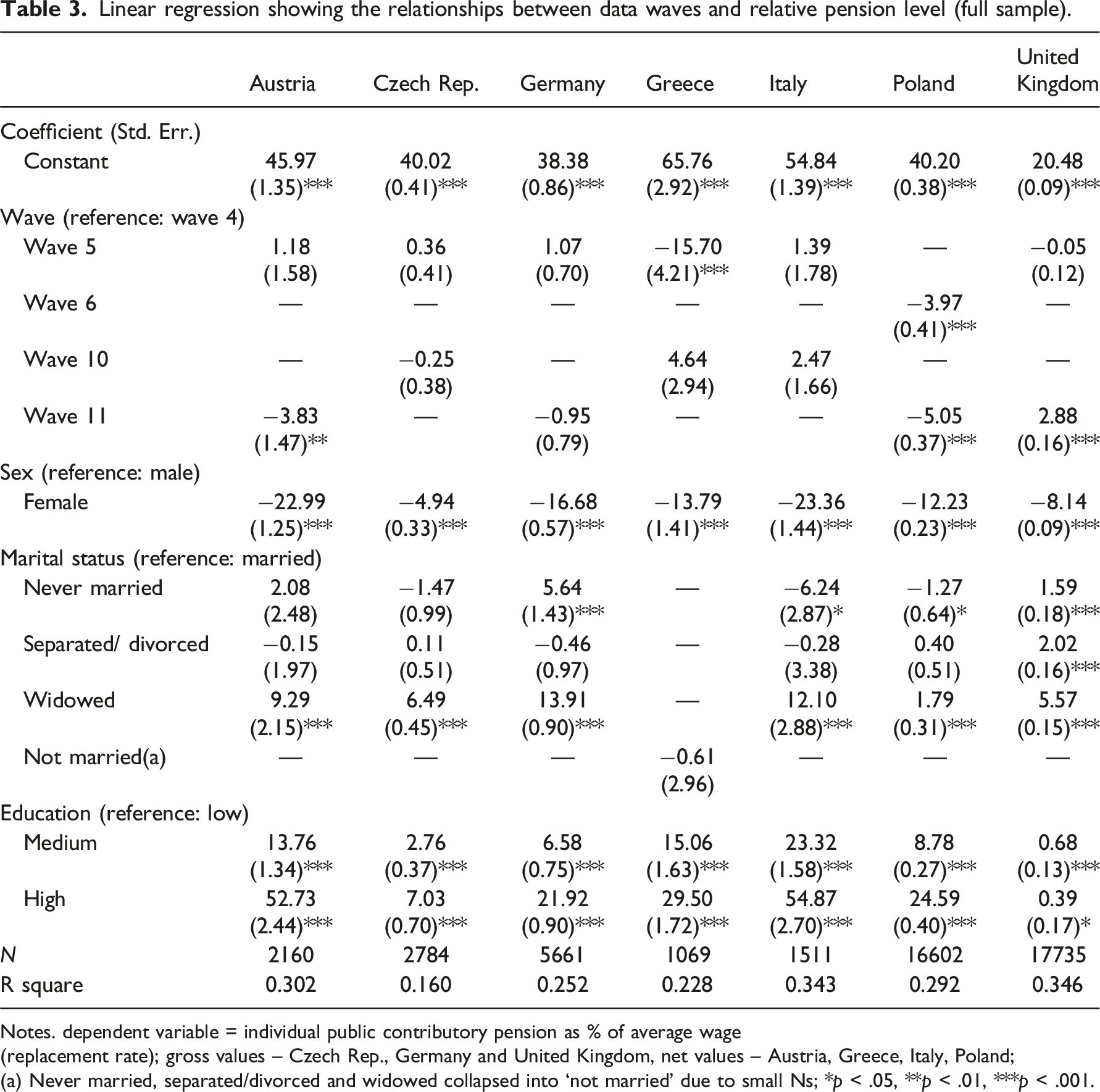

Linear regression showing the relationships between data waves and relative pension level (full sample).

Notes. dependent variable = individual public contributory pension as % of average wage (replacement rate); gross values – Czech Rep., Germany and United Kingdom, net values – Austria, Greece, Italy, Poland; (a) Never married, separated/divorced and widowed collapsed into ‘not married’ due to small Ns; *p < .05, **p < .01, ***p < .001.

Our results diverged significantly from these expectations. Of the five countries in which OECD-projected replacement rates fell, only Austria and Poland showed falls in our analysis of the LIS data. These falls were biggest in Poland. Here the relative pension level for our sample fell by 5.1 percentage points over the whole period, most of which occurred in the years up to wave 6. In Austria, the falls were smaller and less significant, the relative pension level for the sample declined by 3.8 percentage points over the whole period, having not fallen significantly in the years before wave 5.

In all other countries where OECD-projected replacement rates fell (Germany, Greece, UK), our analysis showed no decline in the relative pension levels of our sample across the whole period, although in Greece there was a significant fall between waves 4 and 5. Indeed, in the UK, relative pension levels rose significantly, by 2.9 percentage points across the whole period, an increase which occurred after wave 5. In Germany there was no significant change across either period.

In the two countries where OECD-projected replacement rates increased (Czech Republic and Italy), our results were again inconsistent with our hypothesis of significant increases in relative pension levels. In both countries no significant change was shown across either period.

Relative pension level by sex

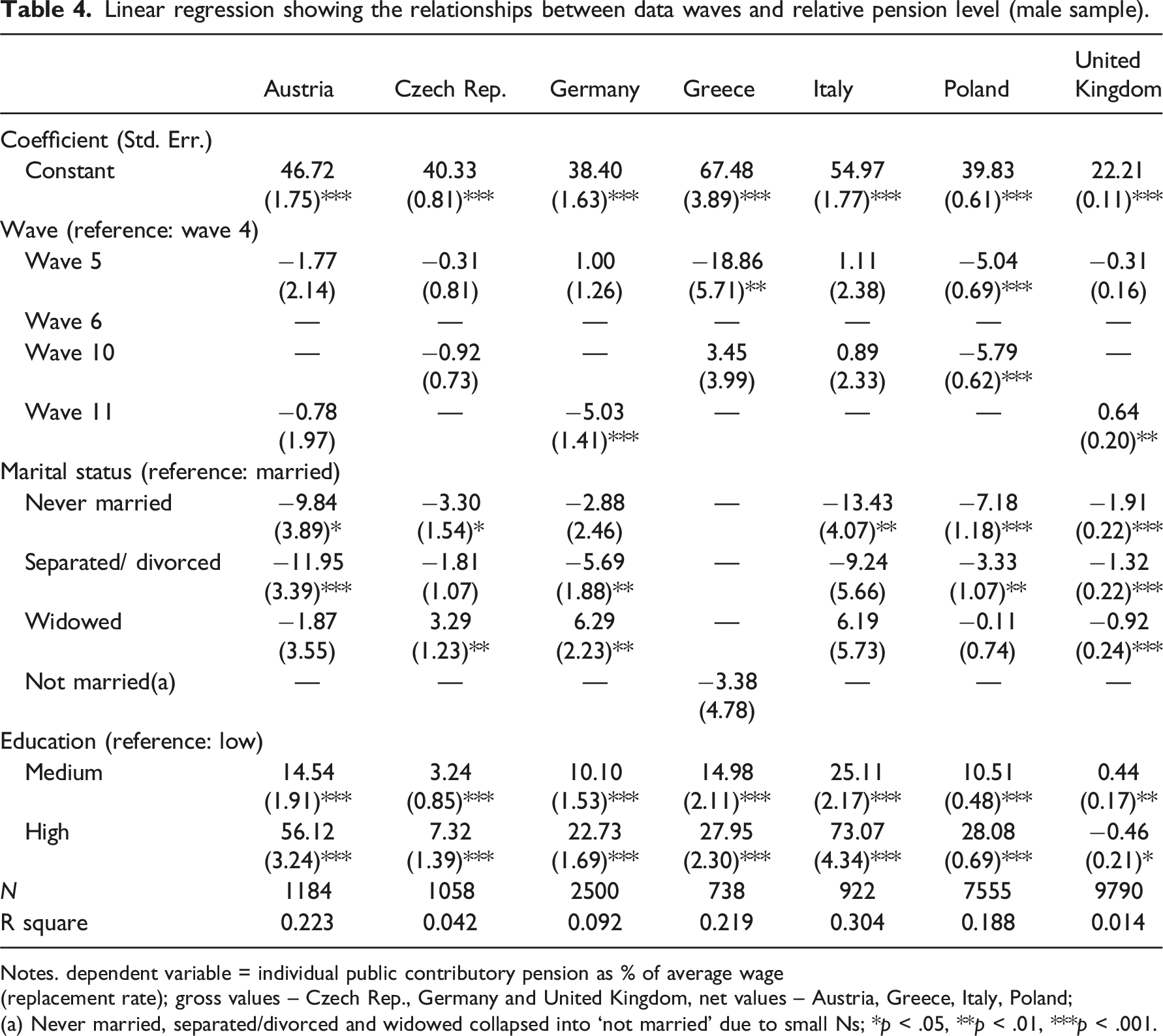

Linear regression showing the relationships between data waves and relative pension level (male sample).

Notes. dependent variable = individual public contributory pension as % of average wage (replacement rate); gross values – Czech Rep., Germany and United Kingdom, net values – Austria, Greece, Italy, Poland; (a) Never married, separated/divorced and widowed collapsed into ‘not married’ due to small Ns; *p < .05, **p < .01, ***p < .001.

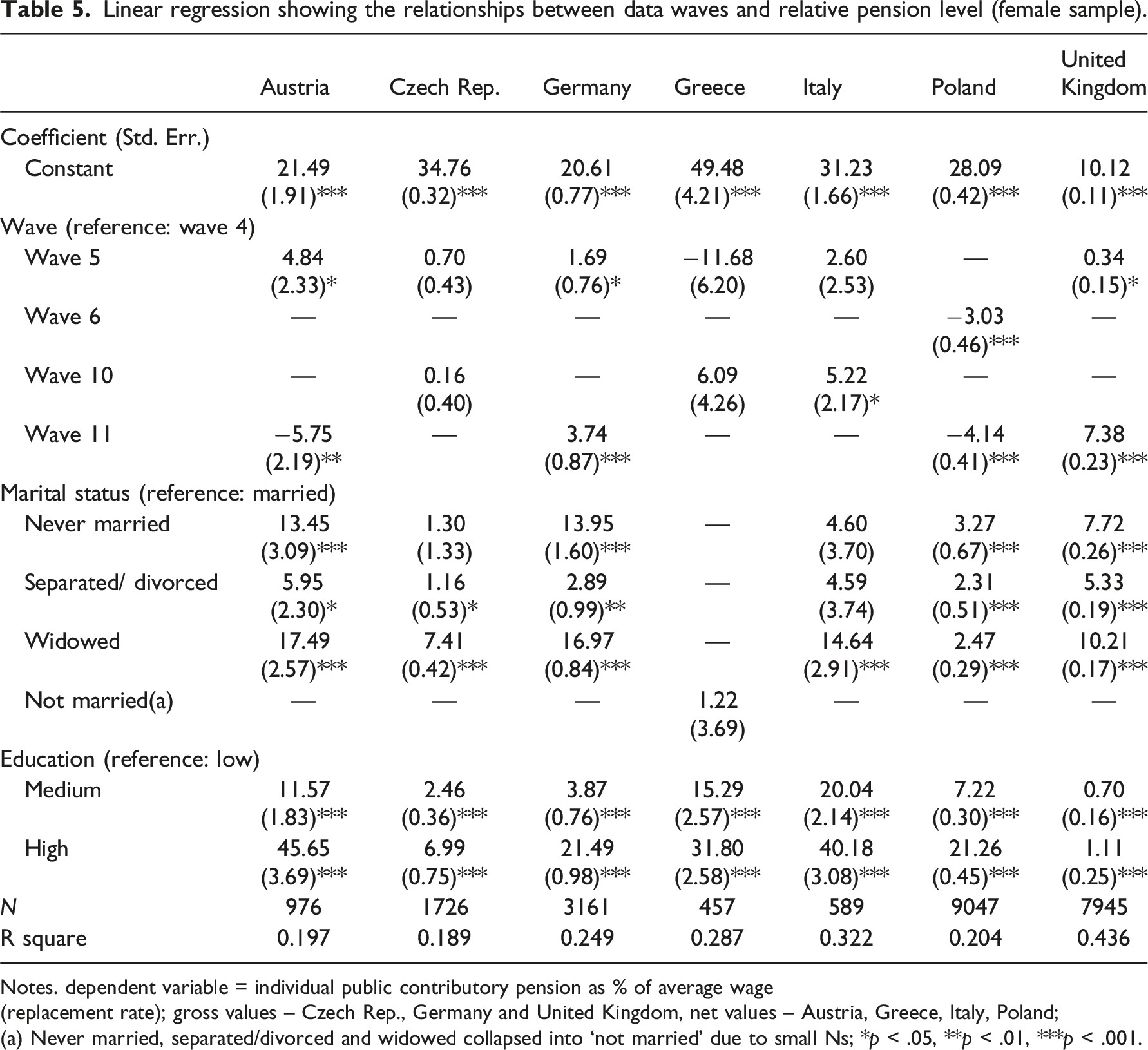

Linear regression showing the relationships between data waves and relative pension level (female sample).

Notes. dependent variable = individual public contributory pension as % of average wage (replacement rate); gross values – Czech Rep., Germany and United Kingdom, net values – Austria, Greece, Italy, Poland; (a) Never married, separated/divorced and widowed collapsed into ‘not married’ due to small Ns; *p < .05, **p < .01, ***p < .001.

In three of the countries where OECD-projected replacement rates fell (Germany, Poland, UK), our data showed more favourable results for women. The result most consistent with our hypothesis was in Poland where both men’s and women’s pensions declined, but men’s declined by slightly more over the whole period. In Germany, men’s pensions declined significantly, but women’s relative pension level rose significantly over the whole period, by 3.7 percentage points. In the UK, both men and women’s relative pension levels rose between wave 4 and the final wave but women’s rose by almost 7 percentage points more. In Greece, the final country where OECD-projected replacement rates fell, there was no significant change for either sex in the later period, but men’s pensions fell significantly in the earlier period.

Of the two countries where OECD-projected replacement rates increased (Czech Republic and Italy), the results for Italy showed a slightly better situation for women than men: women’s relative pension levels improved by a small and significant amount over the whole period while those for men showed no significant change. In the Czech Republic there was no significant change for either sex across either of the periods.

Discussion

The analysis above was designed to determine the impact of reforms to public pension institutions over the last two to three decades on actual pension outcomes in the most recent years that data are available since the reforms. Have the institutional retrenchments, generally highlighted by the OECD replacement rate projections, been clearly reflected in the adequacy of the pension citizens receive in the early years of their retirement or is there evidence that compensatory behaviours by workers or other socio-economic factors have significantly mitigated the impact of these reforms? Is there any evidence that women’s situation has generally improved, as some commentators have suggested?

Overall, our results show very little consistency with the OECD-projected replacement rates for our sample (Table A.1). The OECD projected declines in replacement rates between 2002 and 2019 in five of our countries (Austria, Germany, Greece, Poland, UK), based on their institutional reforms. In the other two (Czech Republic, Italy) only small increases were projected. In contrast, our results showed relative pension levels to have fallen over the entire period in only Poland and Austria. In four other countries they have remained static (Czech Republic, Germany, Greece, Italy), while in the UK they have risen.

In relation to sex, our results are not fully consistent with the OECD’s projections, but they do show women faring better than men in most cases when relative pension levels are compared across the whole period.

Conclusion

Little research has been undertaken to investigate whether the cost containment measures widely adopted by pension policymakers in recent decades have reduced the pension adequacy of recent retirees compared to previous cohorts, or whether other variables, such as tighter links to the labour market among more recent pensioners, have compensated them for less generous pension institutions. This is a major gap both for policymakers and academics. From the perspective of policymaking, it is crucial to know whether today’s individuals have become more vulnerable when they retire at statutory retirement age. From an academic perspective, answering this question allows insights into the extent to which long-term pension system change has a direct impact on income or will be mitigated by other factors.

One reason for this gap is insufficient and/or inadequate data. Only one comparative data set, LIS, offers sufficient longitudinal pension income information and here broadly suitable data is only available for some countries. Moreover, this data does not link pension income and employment biographies directly; and gross and net incomes are mixed in some countries, warranting adjustment. In undertaking the research on which this article is based, we took all possible, necessary steps to overcome these shortcomings to produce the only study that shows the impact of pension reform based on the real, not modelled, pensioner income recent retirees received from public/mandatory pensions in the first few years after the normal retirement age in their countries. Our results show that institutional change and pension income change are not systematically related. We demonstrated above that relative pension levels have remained static or gone up in countries where institutional retrenchment took place, and they remained static despite slight increases in system generosity in others. Institutional change and relative pension levels are most closely aligned with respect to females’ retirement income. Consistent with the expectations of the institutional reform literature, women’s pensions have been more buoyant than men’s in Germany, Italy, Poland and the UK.

These results suggests that other variables mediate the relationship between institutions and pension outcomes, most probably employment change. More research regarding the role of these variables is desirable, but without better data the prospect for such work is not good. Nevertheless, we have shown clearly that assessments of the impact of pension retrenchment on pension adequacy should not be based on institutional approaches alone. Outcome-based analysis is an essential complement to such approaches given the complexity of the relationship between the pension institutions, workers’ experience during their working lives and the pension they finally receive when they retire. For policymakers the results show that the long-term impact of reform on outcomes is hard to predict. However, overall relative real pension income has been more robust than feared by many.

Supplemental Material

Supplemental Material - Retrenchment without effect? Exploring the link between pension reforms and public pension adequacy of new retirees in seven European countries (1993–2020)

Supplemental Material for Retrenchment without effect? Exploring the link between pension reforms and public pension adequacy of new retirees in seven European countries (1993–2020) by Paul Bridgen, Traute Meyer and Lisa Davison in Journal of European Social Policy

Footnotes

Acknowledgement

The authors thank the editors of JESP and two anonymous referees for their excellent comments.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the ESRC Centre for Population Change.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.