Abstract

We analyse the different fiscal treatment of married and cohabiting couples across all EU Member States using microsimulation methods. Our article highlights important differences across EU countries’ tax–benefit systems, where seven countries show substantial bonuses for married couples and four exhibit marriage penalties. On a micro level, we find that these marriage bonuses/penalties differ substantially across household types and income. From a policy point of view, our results suggest that the abolishment of marriage-related tax–benefit components in countries with marriage bonuses would leave some households financially worse off but would increase governments revenues that could be spent to targeted support of specific groups. From both an equity and efficiency point of view, this abolishment would be desirable.

Introduction

In most western societies, household formation has changed rapidly over the past centuries. While the traditional form of marriage has been the dominant form of family households for decades, cohabitation is on the rise in many countries, as highlighted by Perelli-Harris and Gassen (2012). The marriage rate has dropped significantly in recent decades in the EU. According to EUROSTAT Marriage Indicators, 1 since 1964 ‘the crude marriage rate in the EU has declined by close to 50% in relative terms. At the same time, the crude divorce rate has more than doubled’. These marriage formation changes affect also children. More than half of divorced couples have minors 2 and also births outside marriage have been increasing rapidly. According to EUROSTAT Fertility Indicators, 3 in 2018 about 42% of births in the EU were outside marriage, which is 17% points more than in 2000. They relate this development to changing patterns of family formation.

Despite the changing family formation trends, many tax–benefit systems continue to treat married couples and cohabiting partners differently. In our article, we focus on couples who either live in a formal union or are cohabiting, and whether changing their civil status brings any financial gains/losses to a couple, as a result of the existing tax–benefit system. The concept of married couples also includes those in civil unions and registered partnerships. Registered partnership, similarly to marriage, is a legally recognised social contract between two people, indicating a permanence of the union that leads to the same tax–benefit treatment as marriage in many countries. 4 Non-marital cohabitation, 5 on the other hand, is a living arrangement between a couple without any legal contract. In the tax–benefit systems these couples are often treated as separate individuals.

We use EUROMOD, the tax benefit microsimulation model of the European Union. The model uses countries’ existing tax and benefit rules, 6 applies it to harmonised microdata on individuals and households, and calculates the effects of these rules on household income. It is based on EU-SILC (European Union Statistics on Income and Living Conditions) microdata and allows for the comprehensive assessment of unequal treatment between married and cohabiting couples across all EU countries, ensuring also cross-country comparability. 7 This allows us to estimate the marriage bonus or penalty for each household in the EU-SILC data.

In this article, we try to answer several questions. First, we give a cross-country overview of the treatment of marriage within the tax–benefit system. We show that in many European countries being in wedlock does not give any sizable financial advantages. However, there are some countries that treat couples differently based on their civil status, which is often related to taxation. Second, we use micro data to analyse the marriage bonus/penalty on a micro level. We show that in most countries the marriage bonus is strongly related to the labour market status of a spouse and the difference in a couple’s earnings. Third, we estimate the costs and distributional impact of unequal treatment. We show that offsetting unequal treatment may be complicated in practice.

While there is extensive literature on the US related to the marriage bonus and its consequences on income and family formation (Alm and Whittington, 1997; Fisher, 2013; Michelmore, 2018), research on the unequal treatment of married and cohabiting couples within the tax–benefit systems of the European countries is scarce. Therefore, we contribute to the literature in several ways. First, we are to our best knowledge the first to analyse the unequal treatment of married (including those in a civil union or registered partnership) and cohabiting couples across all EU Member States in a comprehensive way. Second, we show that this unequal treatment not only differs substantially across countries, but also within countries (by household type).

Our results point to important policy implications. First, the unequal treatment of couples solely depending on their civil status does violate horizontal and vertical equity principals (i.e., two financially equal couples may end up with different disposable incomes just because of their civil status; better off married couples may receive a tax rebate, while this rebate might not be available for cohabiting couples who are earning less). Second, although bringing up children in a family where parents are married provides benefits for children, in the light of the changing family formation trends, tax–benefit systems should ensure adequate support to all children or other dependants irrespective of the marital status of their carers, instead of providing fiscal benefits only to married people. The policy-makers should aim at the most efficient and effective use of limited financial resources, ensuring equity and fiscal sustainability in the long run.

The article is structured as follows: the second section provides an overview of the related literature; the third section discusses the marriage-related tax and benefit components in EU Member States; the fourth section describes the data as well as the methodology used for the analysis; results are presented in the fifth section; the sixth section discusses the results and the policy implications. In the seventh section we summarize and conclude.

Literature

While the general trend has been an increasing number of single households in Europe, also the composition of couple households has also changed substantially over the last decades. While in former times, couples were often married, the number of cohabiting couples is on the rise. Perelli-Harris and Gassen (2012) discuss the increase in cohabitation in the past few decades in Western Europe and give an overview of the legal framework. Additionally, Blau and Van der Klaauw (2013) and Lundberg and Pollak (2014) provide an overview of the changes in family structures in the US over the recent decades.

Marriage may provide many non financial gains for people who decided to get married, such as legal protection, greater psychological and physical wellbeing, greater risk-sharing and financial stability, among other things. Furthermore, the traditional married family often enjoys advantages over other family forms, which are due to certain tax advantages or higher benefit levels. The general tax structure and other tax–benefit components deliberately or unconsciously contribute to patterns of work, marriage, household formation, childbearing, unpaid labour division at home and more (see, e.g., McCaffery, 2009). Among other functions, taxation enacts a social function which is meant to redistribute incomes, but at the same time it modifies the social stratification, for example, by protecting vulnerable groups in society or encouraging specific behaviour. Marriage formation can well be encouraged by taxation in the form of tax rebates or specific spouse-related allowances (see, e.g., Leroy, 2008; Sainsbury, 1999). In many respects, this ‘social engineering’ by fiscal policies is the representation of social norms and values that exist in a society, and, at the same time, it further perpetuates those norms by continually applying unequal treatment within the fiscal systems (as shown, e.g., by Stotsky (1996) and Elson (2006)).

From the welfare state point of view, different tax treatments of particular groups by offering tax advantages or privileges hint to a hidden or invisible welfare state (see, e.g., Martin, 2020; Sinfield, 2012; Greve, 1994). The idea that taxes have not only a revenue raising function but also a social policy function is not new. Richard Titmus was the first to explicitly use the term fiscal welfare. Tax allowances, tax credits, reduced tax rates and tax exemptions are in essence savings for the individual and, despite the difference in the administrative method, are effectively transfer payments (Titmuss, 1958). However, the social function of tax reliefs has often been overlooked in the welfare state analysis. 8 Tax breaks offered to married people are deemed not to deviate from the standard system in many countries (Adema et al., 2011). As Sinfield (2012) nicely states, ‘the recognition of marriage and family is so institutionalised in many countries that reliefs are part of the benchmark system and so not regarded as tax expenditures’. 9

The different tax treatment of married couples is well known in the literature, at least regarding the negative incentive effects of such tax systems. Bick and Fuchs-Schündeln (2017), for example, quantify the negative labour supply effects of joint taxation (typically a main source of the marriage bonus) for 17 European countries and the US. Kabatek et al. (2014) show that for France, the change from joint to individual taxation would increase female labour supply substantially, while male labour supply would fall. Similarly, Crossley and Jeon (2007) find positive effects on female labour market participation of reform that reduces the jointness of the income taxation in Canada.

The impact of social (cash) benefits is not widely discussed in the literature, simply because social benefits are typically only a minor part (if any) of the marriage bonus. In most countries, for the eligibility to the means-tested benefits, incomes of all household members are assessed. Thus, as long as a couple lives in the same household, there is no difference if they are married or not. Although some countries initiated specific benefits for single mothers, it was noted that this led to unintended consequences, such as postponed marriages and increased births for cohabitants, especially among the least educated in France in the 1990s and to increased fraudulent claims of cohabiting women in the Netherlands (Perelli-Harris and Gassen, 2012). For this reason most countries try to clearly distinguish between cohabiting and single parents, meaning that cohabiting parents won’t receive extra benefits compared to the married ones. As shown by Montanari (2000), marriage bonuses ‘predominantly take the form of tax allowances’, reducing the tax burden of the married couple. It is important to mention that tax breaks are typically regressive which suggests that abolishing the marriage bonuses might be inequality reducing. However, neglecting cash benefits that are related to marriage might bias the results, not only in the size of the marriage bonus or penalty, but also on the distributional impacts.

Additionally, the existence of marriage bonuses or penalties, meaning that couples can be financially better or worse off by being married, raises the question of whether financial (dis)incentives matter for the marriage decision of a couple. There has been a considerable amount of research analysing how fiscal benefits affect marriage decisions (see, e.g., Alm and Whittington, 1997, 1999; Alm et al., 1999; Fink, 2020; Fisher, 2013; Michelmore, 2018).

While behavioural effects, both on the labour market and on the decision to marry, are out of the scope of our article, the information on the size and heterogeneity across households of the marriage bonus/penalty in the EU countries offers important insights into the tax–benefit systems and opens new areas for research in this field. So far, relatively few studies have focused on cross-country analyses of marriage bonuses using a microsimulation approach. A study by O’Donoghue and Sutherland (1999) focuses on 15 EU countries, but in their analysis they account for not only marriage but also the presence of children. Similarly, Immervoll et al. (2009) analyse marriage bonuses and penalties in 15 Member States using the EUROMOD microsimulation model, but by focusing only on a number of hypothetical households. In addition, they assess the labour supply effects, pointing to high taxation of secondary earners. A more recent study by Miho and Thévenon (2020) analyses differences in children’s economic security in relation to the marital status of their parents, as illustrated by the different impacts of tax–benefit systems on earnings of hypothetical families across the OECD countries.

In our article, we focus only on the different tax–benefit treatment of married (including those in civil unions and registered partnerships) versus non-married couples without assessing the impact of other family-related fiscal instruments that do not differ across marriage status, such as children tax allowances.

Marriage-related components of tax–benefit systems

Tax and benefit systems in the EU and the UK are highly varied. Without going into the depth of each country’s peculiarities, we focus on the elements within tax and benefit systems that are explicitly related to the marital condition. It is important to note that we separate two seemingly similar concepts related to taxation. We draw a line between family-based taxation and marriage-based taxation. Supporting children or other dependents through the tax system is reasonable since they represent additional needs and expenses for a family. This is the opposite of providing financial bonuses based on a mere marriage fact, which does not entail any specific needs nor additional expenses.

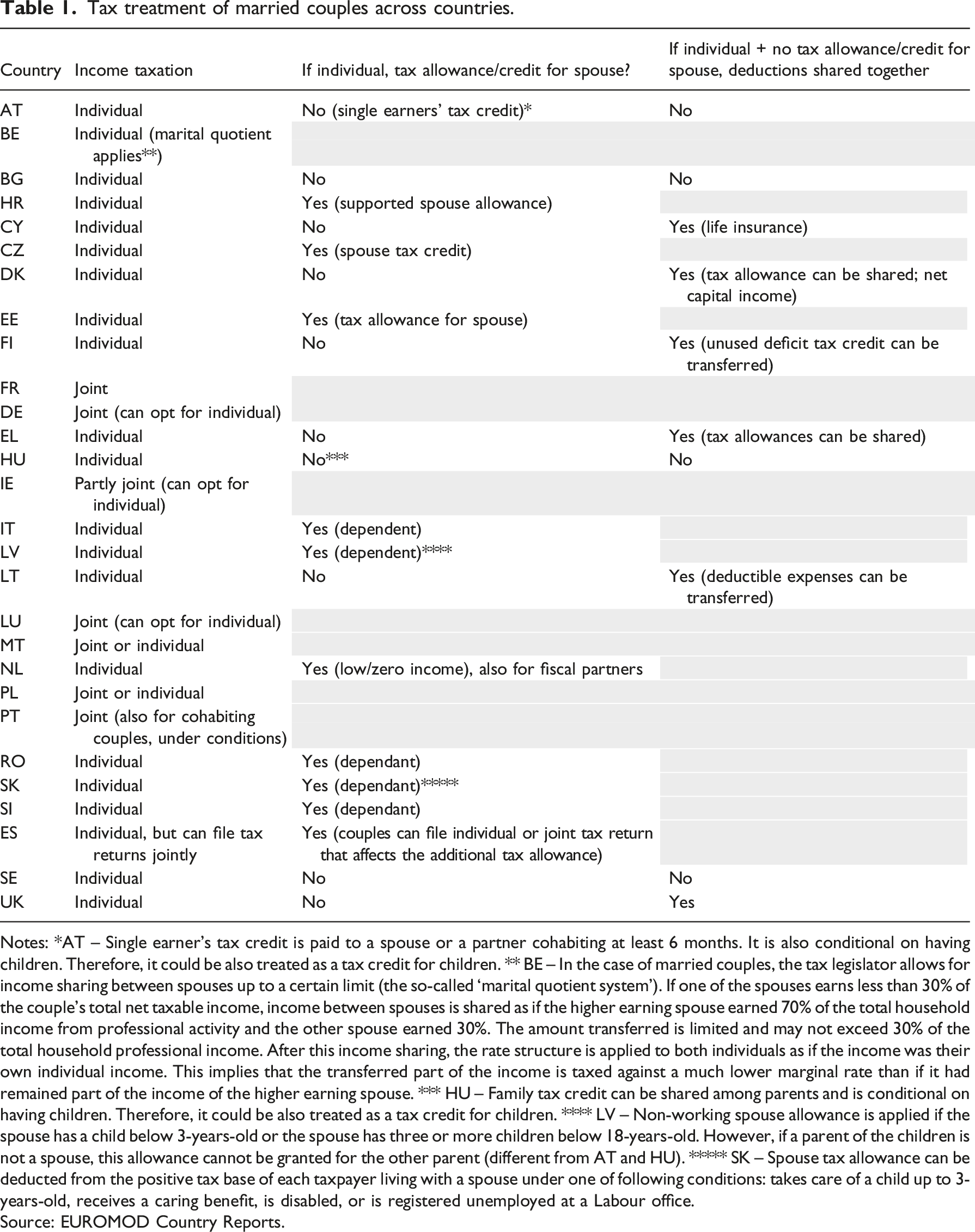

Tax treatment of married couples across countries.

Notes: *AT – Single earner’s tax credit is paid to a spouse or a partner cohabiting at least 6 months. It is also conditional on having children. Therefore, it could be also treated as a tax credit for children. ** BE – In the case of married couples, the tax legislator allows for income sharing between spouses up to a certain limit (the so-called ‘marital quotient system’). If one of the spouses earns less than 30% of the couple’s total net taxable income, income between spouses is shared as if the higher earning spouse earned 70% of the total household income from professional activity and the other spouse earned 30%. The amount transferred is limited and may not exceed 30% of the total household professional income. After this income sharing, the rate structure is applied to both individuals as if the income was their own individual income. This implies that the transferred part of the income is taxed against a much lower marginal rate than if it had remained part of the income of the higher earning spouse. *** HU – Family tax credit can be shared among parents and is conditional on having children. Therefore, it could be also treated as a tax credit for children. **** LV – Non-working spouse allowance is applied if the spouse has a child below 3-years-old or the spouse has three or more children below 18-years-old. However, if a parent of the children is not a spouse, this allowance cannot be granted for the other parent (different from AT and HU). ***** SK – Spouse tax allowance can be deducted from the positive tax base of each taxpayer living with a spouse under one of following conditions: takes care of a child up to 3-years-old, receives a caring benefit, is disabled, or is registered unemployed at a Labour office.

Source: EUROMOD Country Reports.

In recent years, some countries have moved from joint to individualised personal income tax structures, or at least they allow married people to opt for an individual taxation. 10 However, in 2020, only four countries had strictly individual income taxation: Bulgaria, Sweden, Austria and Hungary. 11 Another six countries (Finland, Denmark, Lithuania, Greece, Cyprus and the UK) do not apply any tax allowances or credits for a spouse but allow a transfer of unused tax allowances/credits between spouses, and some expenses can be deducted from a partner’s tax base/tax liabilities. In general, the financial benefits of being married in those countries are negligible. The biggest group of EU countries (Estonia, Latvia, Czechia, Slovakia, the Netherlands, Romania, Croatia, Slovenia, Italy and Spain) have individual tax systems but apply tax allowances or tax credits for a partner with little or no earnings. 12 Seven countries (Poland, Germany, Ireland, Belgium, Luxembourg, Malta and Portugal) have joint income assessments or the allocation of earnings between spouses.

Usually, benefits do not differ by marital status in most EU countries as either benefits are meant to replace individual’s earnings (e.g. unemployment benefits), are categorical (e.g., benefits for children), or means-tested, meaning that in most cases incomes of all household members are assessed. However, in some countries people are only eligible for entitlements to social benefits if married (e.g. supplements to unemployment benefits, survivor pensions) or not married (i.e., cohabiting couples with children might be treated as lone parents by the tax and benefit system). That implies that there is also an unequal treatment of married and cohabiting couples related to benefits. These benefits play a more important role for some households in Cyprus, Malta, Greece and Italy, mostly because of social pensions or means-tested benefits for non-married elderly people.

Data and methodology

Our analysis is based on EUROMOD, the microsimulation model for the European Union, which simulates personal income tax liabilities, social insurance contributions (SIC) and entitlements to social benefits for the underlying population of each Member State. We make use of EUROMOD because it is a unique tool for cross-country comparative analysis and it allows for simulations of hypothetical policy changes in each Member State (Sutherland and Figari, 2013).

Our analysis focuses on all standard components of tax–benefit systems that are simulated in EUROMOD, that is, direct taxes, SIC and cash benefits. 13 However, there are a few fiscal components that are usually not simulated, and the value is taken directly from the underlying EU-SILC data. This is due to the lack of some information needed for the simulation. 14 As an example, in many countries old-age pensions, or survivor pensions, are not simulated because of the lack of information on the contributory history. This is also the case of some minor benefits, such as disability benefits, because usually there is no information available in the data on the severity of the disability. In those cases we are not able to cover potential differences in the policy treatment of married and cohabiting couples.

As mentioned before, different treatment of cohabiting and married couples can stem from several components of the tax–benefit system. In countries with purely individual taxation, married couples are taxed as two different tax units, while in countries with joint taxation, the income of both spouses is taxed jointly. 15 In some other countries the withholding of personal income tax is applied at the individual level, but additional allowances or tax credits can take into account the incomes (or expenditures) of a spouse. Some differences are also observed in relation to benefit entitlements, especially of means-tested benefits and benefits for elderly people.

We define the

The tax–benefit function of a couple t

c

(y

i

, y

j

, X

c

…) (married or cohabiting) depends on the income of the individual y

i

and the income of their partner y

j

, as well as other characteristics of the couple X

c

, such as children, age, labour market status and others. If MB

c

is bigger than zero, couple c faces a

In our analysis, we use EUROMOD to simulate changes in taxes and benefits under two hypothetical scenarios: 1) in the first scenario, both married and cohabiting couples are defined as cohabiting. It means that all couples in the data would be treated by the tax–benefit system in the same way as non-married couples:

16

2) in the second scenario, both married couples and cohabiting partners are considered as married. So all couples would be treated by the tax–benefit system in the same way as married couples:

To simulate these two counterfactual scenarios, we first modify the input data, changing the marital status of couples living together. Then, we use EUROMOD to simulate the change in taxes and benefits in these two counterfactual scenarios and we compare it to the actual status.

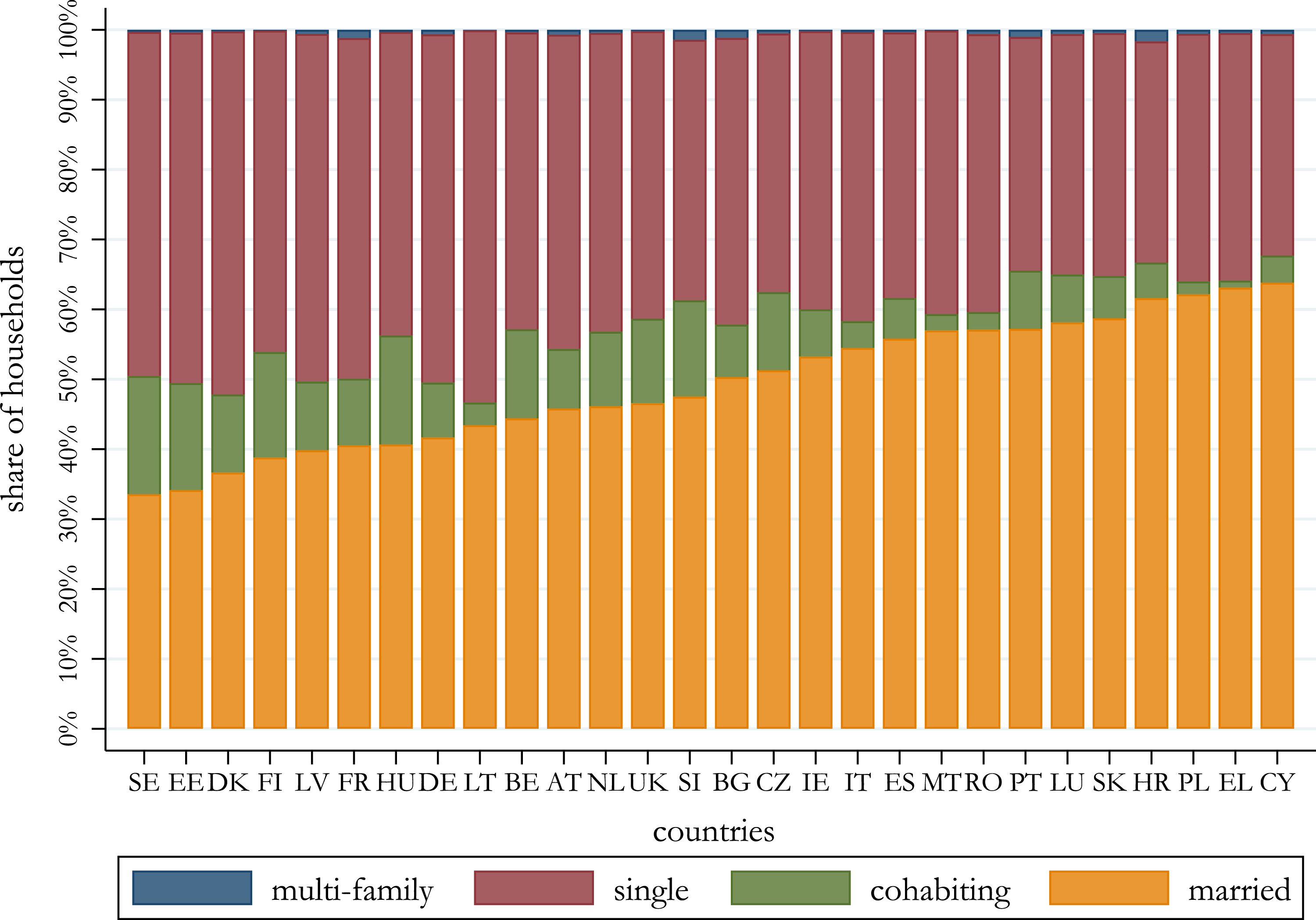

The analysis is based on the 2019 tax–benefit system using 2017 EU-SILC data. Uprating factors are applied to monetary variables in order to represent the year 2019. For the purpose of our analysis, we divide the population into four subgroups: (i) married couple households, (ii) households with cohabiting partners, (iii) single person households and (iv) multi-family households, indicates households with both a married and a cohabiting couple. Figure 1 gives an overview of household composition for each country. Household structure in the EU. Note: EUROMOD estimations based on EU-SILC; Households are divided in four groups: (i) married, indicates households with married couples, (ii) cohabiting, indicates couples, who are not legally married, (iii) singles and (iv) multi-family households, indicates households with both a married and a cohabiting couple.

Cyprus, Greece, Poland and Croatia are the countries with the highest share of married couple households (around 63%). On the opposite side, in Sweden and Estonia only 34% of the households are married couples, but the percentage of cohabiting partners is quite high. A relatively high share of cohabiting partners is also observed in Finland and Hungary, while in Greece, Poland, Malta, Romania, Lithuania, Italy and Cyprus it constitutes less than 5%. Although the share of cohabiting couples is relatively small, it has been increasing substantially over decades in Western Europe (see, e.g., Perelli-Harris and Gassen, 2012). Single person households constitute more than a half of the households in Lithuania. The multi-family households represent a negligible share of total households in all Member States and the UK.

Empirical results

Marriage penalty or marriage bonus?

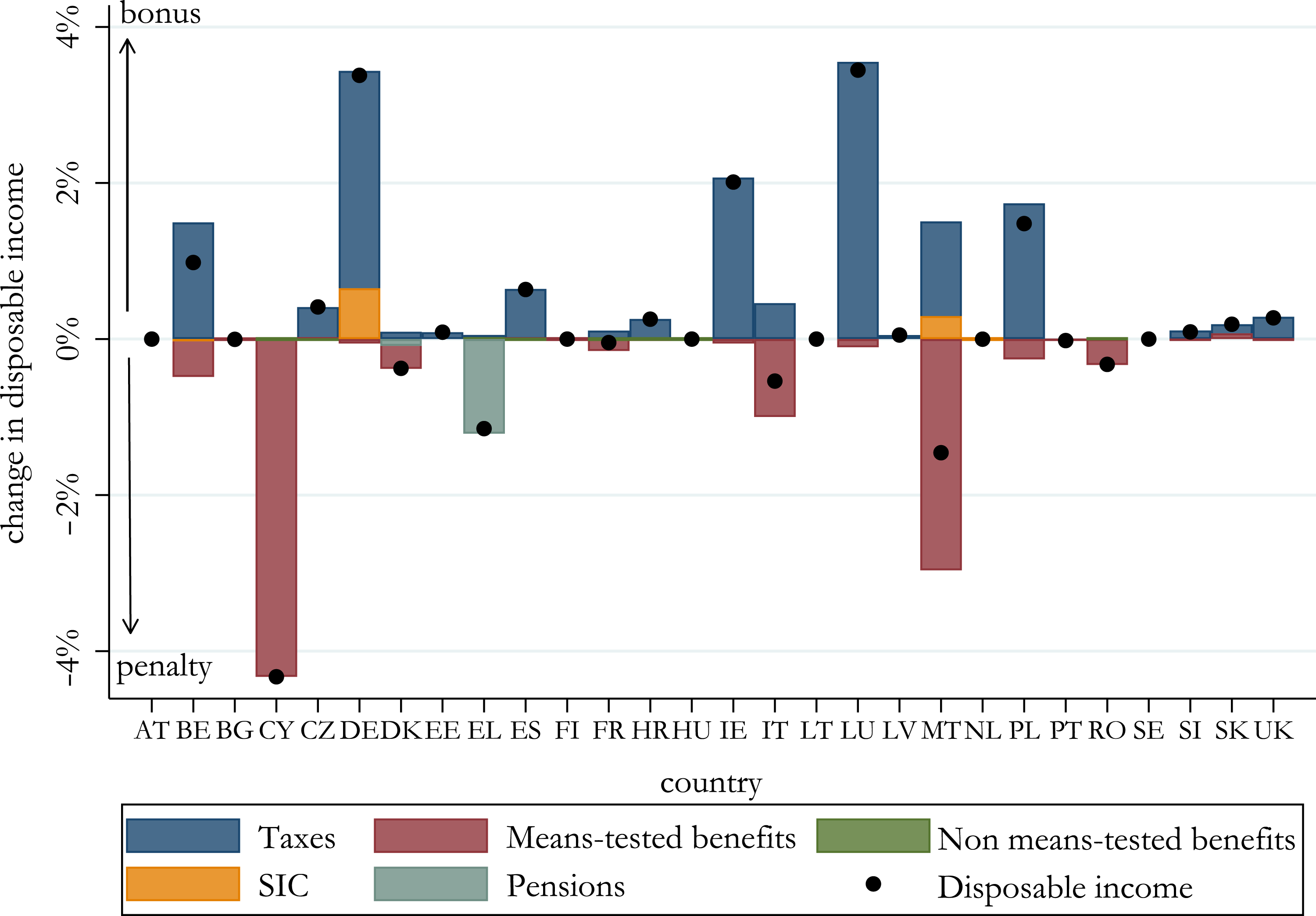

To identify the size of the marriage bonus or penalty across countries, we simulate the hypothetical situation in which all married couples are treated as cohabiting couples and then compare the changed to their actual situation (Scenario 1). Figure 2 shows the impact of marriage on disposable income for the subsample of married couples. Additionally, the change in disposable income is broken down into the main components of the tax–benefit system – personal income taxes, SIC, pensions, as well as social benefits (means-tested and non means-tested). Marriage bonus/penalty by income component (subsample married). Note: EUROMOD estimations based on EU-SILC. SIC are Social Insurance Contributions.

In countries such as Austria, Bulgaria, Estonia, Finland, Hungary, Lithuania, Latvia, the Netherlands, Portugal and Sweden, there are no, or very minor differences related to the tax–benefit system between married and cohabiting couples. However, we can see that in other countries, a couple is financially better off if married than cohabiting due to different tax–benefit rules. We find substantial differences in countries such as Luxembourg, Germany, Ireland, Poland and Belgium. Additionally, in some countries married couples would be, on average, better off if they were cohabiting, indicating the existence of a marriage penalty.

Focusing on the source of the bonus/penalty, we see that the bonus is mainly driven by a reduction in taxes. This effect is particularly strong in countries with marriage bonuses, and joint taxation can be identified as the main source for the marriage bonus. However, in Germany and some other countries, other components of the tax–benefit system (e.g. social insurance contributions) also lead to different treatment of married and cohabiting couples.

A different situation is observed in Cyprus, Malta and Greece, where marriage would lead to a penalty. On average, married couples face a reduction in their disposable income because of the reduced means-tested benefits and pensions. In Belgium, although in general marriage would lead to a bonus, which is due to taxation, there is a reduction in means-tested benefits because some married couples lose eligibility for income support due to higher after-tax earnings.

In the rest of the article, we will focus on the countries where the impact of marriage is economically relevant. Our analysis will therefore include the Member States where we find at least a 0.4% change in average disposable income due to marriage: Luxembourg, Ireland, Poland, Belgium, Germany, Spain, Czechia, Italy, Greece, Malta and Cyprus.

Who gains or loses by marriage?

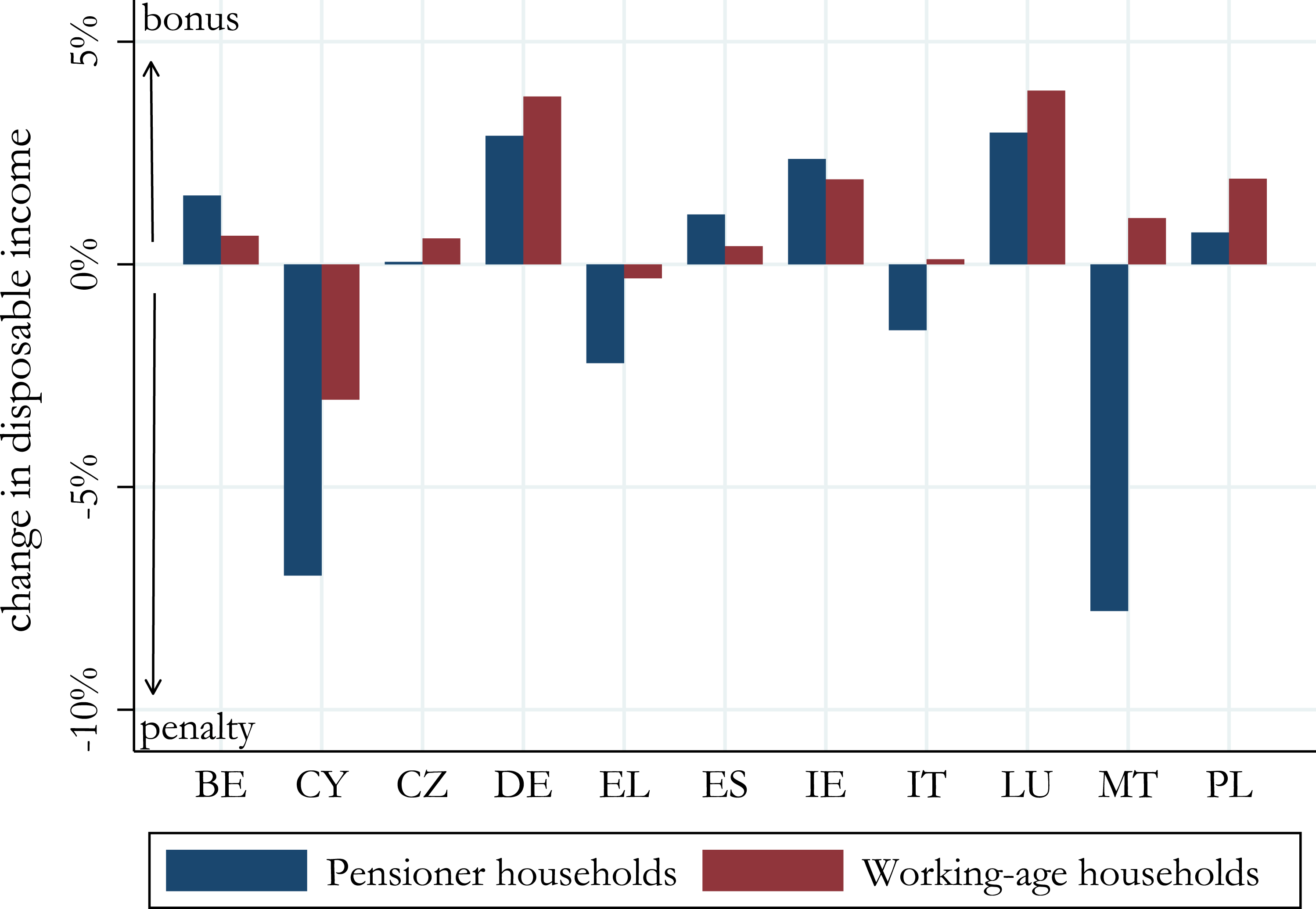

In this section, we look at the financial impact of marriage at the micro level and analyse which characteristics of couples are related to a higher or lower marriage bonus/penalty. In other words, we analyse which households benefit more from marriage. Given that incentives might be different for the working age population versus pensioners, we first look at the marriage bonus/penalty separately for the two groups. A detailed analysis about the amount of the marriage bonus for different household types can be found in the Supplemental Appendix.

Interestingly, and as highlighted in Figure 3, we find that in Malta and Italy, working age couples have positive incentives to marry, however, as soon as they retire, they face a marriage penalty. In Cyprus and Greece all couples face the marriage penalty, which increases in pension age. In these four countries, the marriage penalty for older people is driven by reduction in pensions or benefits targeted at elderly people.

17

Marriage bonus/penalty for pensioners and working-age households. Note: EUROMOD estimations based on EU-SILC data; Pensioner households include all couples with at least a partner older than 65 years old or receiving pensions.

Among countries offering a marriage bonus, pensioner households benefit more than working age married couples in Belgium, 18 Spain and Ireland. However, in these countries, the effect is not driven by specific benefits targeted at elderly people. On the other hand, in Czechia, Germany, Luxembourg and Poland, working age couples have a higher marriage bonus than pensioner households. This is mainly related to the higher taxable income of the former group compared to the latter.

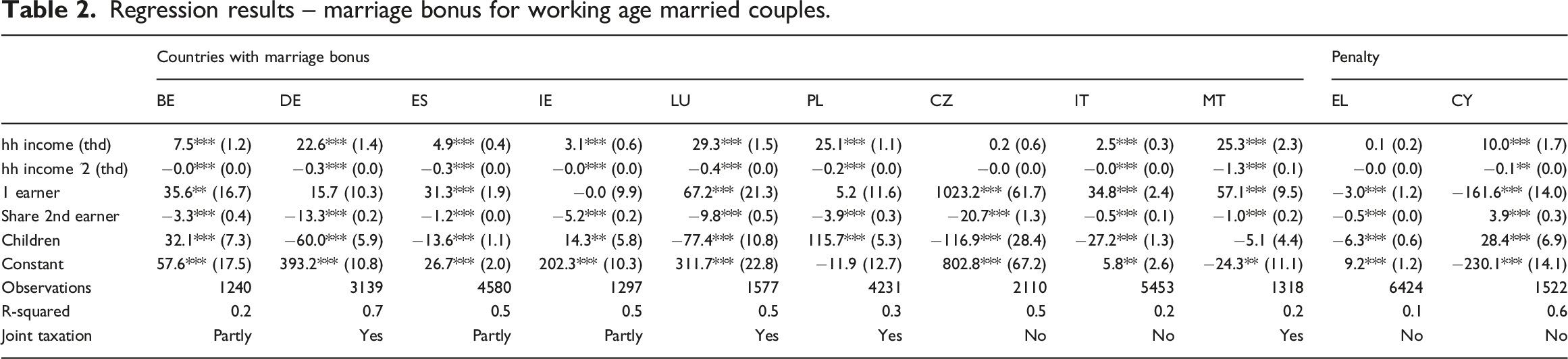

The incentives for the working age people to be married also depend on other characteristics of the household. To analyse the incentives for working age married couples, we set up a simple regression model where the dependent variable is the marriage bonus in euros and the explanatory variables are the household income, the number of earners in the household, the difference in earnings between the couple and the presence of dependent children in the household. We control for the total market income of the household. This analysis focuses on the sub-sample of households where there is one married couple with at least one earner. 19

Regression results – marriage bonus for working age married couples.

We also see a highly significant correlation with our earnings share variable, which is the percentage of earnings of the second earner relative to the total earnings of the couple. It indicates that the difference in earnings within a married couple is an important determinant of the amount of the marriage bonus. In most countries, even when controlled for the total income of the household, the bigger the difference in the earnings of the two household members (earnings of one spouse significantly exceed the earnings of the other), the higher the marriage bonus. In turn, this indicates that marriage could incentivize the second earner to reduce the number of hours at work or to leave a job in order to reduce the total taxes paid. This result is in line with Bick and Fuchs-Schündeln (2017), who find that joint income taxation in Belgium and Germany generates negative labour supply incentives for married women, who are typically the second earners. Similarly, Figari et al. (2011) show that countries with joint taxation introduce substantial disadvantages through the tax–benefit system for women compared to their partners due to lower incentives to work more intensively. This finding is not surprising, knowing that in many countries the difference between individual and joint taxation is almost nonexistent when both partners have similar earnings.

Financial incentives to marry are also different for couples with children. Some couples with children might receive higher benefits when cohabiting because of the lone parent definition. In some countries (e.g., Luxembourg) unmarried parents are considered as lone parents for tax and benefits purposes. In general, the interpretation of these coefficients has to be done with caution because with this simple regression model we are not controlling for other variables that can affect eligibility to some benefits.

The cost of equal treatment

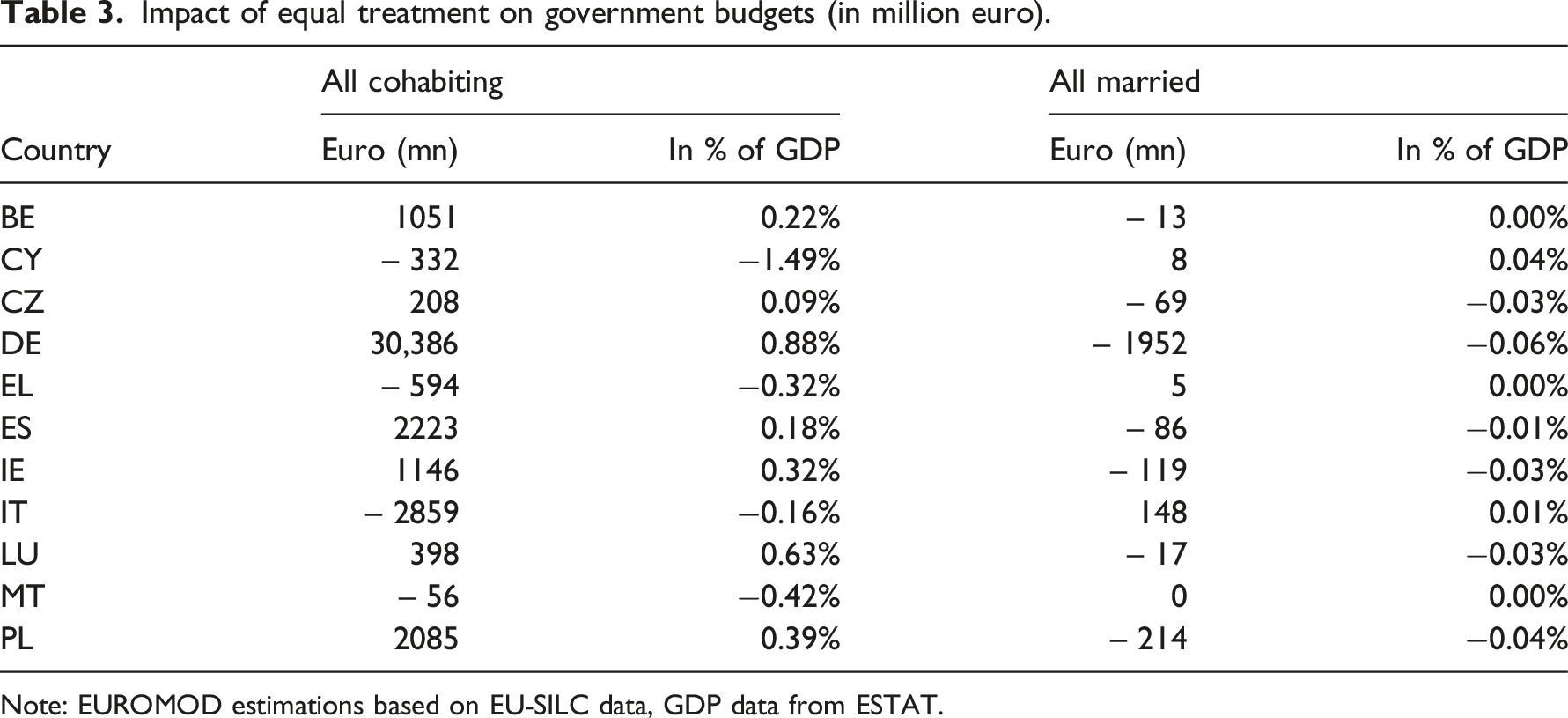

Impact of equal treatment on government budgets (in million euro).

Note: EUROMOD estimations based on EU-SILC data, GDP data from ESTAT.

If cohabiting couples were treated as married (all married), as expected, in countries with joint income taxation or where marriage-related tax allowances or credits exist, the governments would face a loss in their budget. The opposite is observed in Cyprus, Greece, Italy and Malta, where due to a reduction in benefits that are related to means-tested benefits for non-married pensioners, the impact on the government budget would be positive.

If we treat married couples as if they were cohabiting (all cohabiting), the opposite holds true. Most countries would increase their revenues substantially. For example, Germany would increase their revenues by almost €30 billion (0.88% of GDP), mostly driven by the effect of offsetting joint taxation. On the other hand, in countries with a marriage penalty, this change would require extra spending, which could be as high as almost 1.5% of GDP in Cyprus.

Our results highlight that, depending on the country, the impact of equal treatment of married and cohabiting couples within existing tax–benefit systems would have a substantial impact on government budgets.

The distributional impact of equal treatment

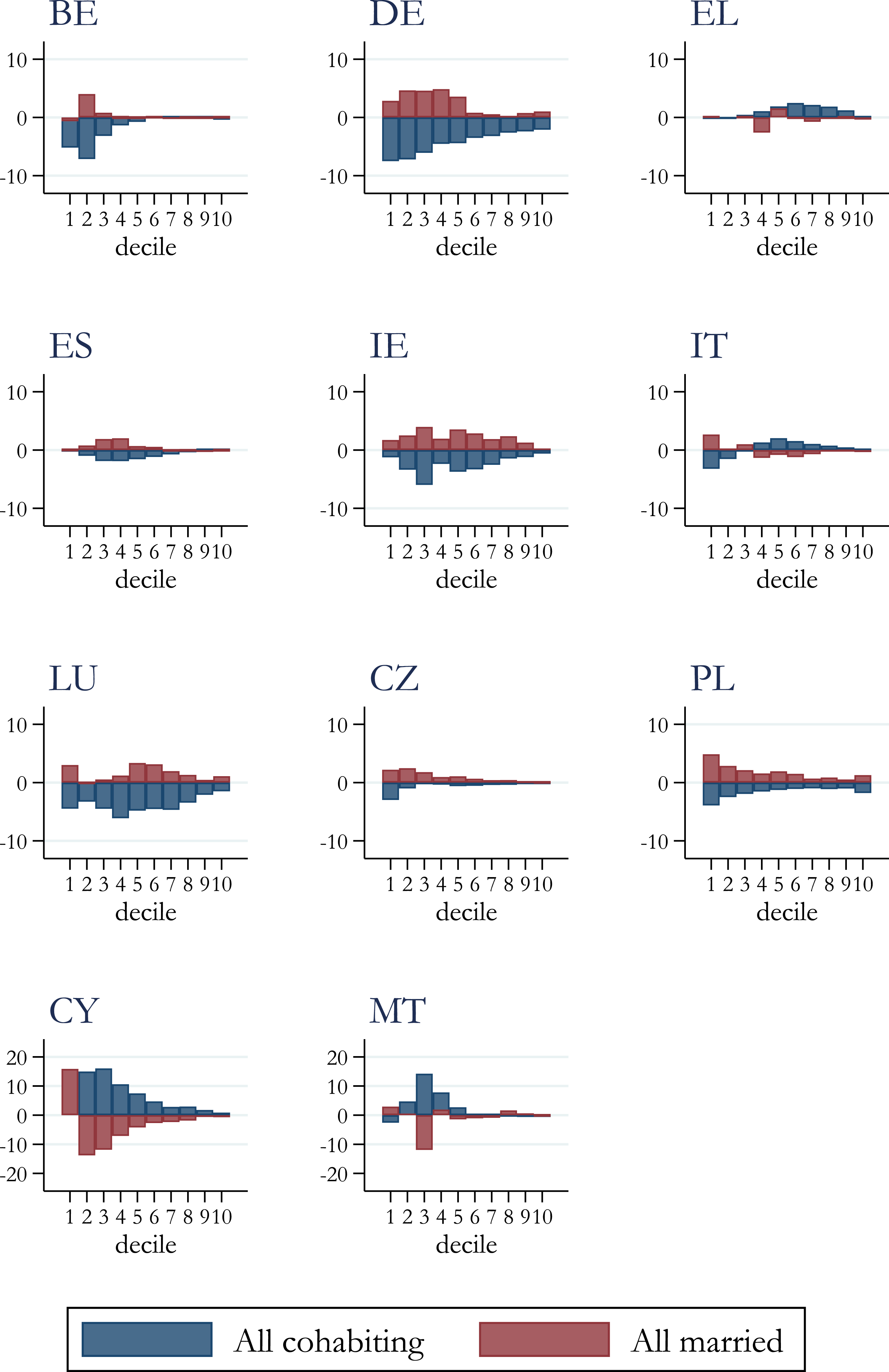

The implementation of an equal treatment for married and cohabiting partners would have a different impact on the income distribution across countries. Figure 4 shows the change in disposable income for the subsample of households with cohabiting partners and with married couples. If tax–benefit rules applied to married couples were also to be applied also to cohabiting partners (all married, red bars), in Belgium, cohabiting couples, especially in the second and third deciles would benefit and would experience a substantial increase in disposable income. In Germany, Spain, Czechia and Poland, the positive impact would be mostly for couples in the low and medium part of the income distribution. Meanwhile in Luxembourg and Ireland the impact is positive in all deciles, with the middle part of the income distribution benefiting the most. By contrast, in Cyprus and Malta, cohabiting couples in the lower part of the income distribution would lose their income due to a reduction in means-tested benefits, in particular for couples with children.

20

This finding is in line with the article by Immervoll et al. (2009), which shows that family-based transfers tend to create substantial marriage penalties at the bottom of the income distribution, which points to fairness and efficiency issues. Percentage change in disposable income in case of equal treatment (subsample couples). Note: EUROMOD estimations based on EU-SILC data. Deciles based on the disposable hh income over the whole population.

As expected, the opposite result is found if all couples were treated as not married (all cohabiting, blue bars), as shown in Figure 4. In Belgium and Germany the impact for couples would be regressive, meaning that married couples in the lowest deciles would lose more compared to more wealthy couples if they were treated as cohabiting. In general, we observe a small impact on the top deciles (except Poland) and a stronger impact on households in the low-middle part of the income distribution. It is likely that in these deciles there is a higher share of one-earner couples or two-earner couples with high difference in earnings.

Given the much lower share of cohabiting partners compared to married couples, it is also interesting to look at the impact on disposable income of the whole population. This also allows us to get insights on the impact on indicators, such as inequality, which are typically based on the whole population sample. Depending not only on the specific design of the tax system (joint taxation) and the design of benefits related to marriage but also the location of married and cohabiting couples in the income distribution, equal treatment can have different effects across the income distribution. As shown in Figure 8 in the Supplemental Appendix, treating married couples as if they were not married would have a substantially stronger effect on disposable income. Some differences are also observed on the impact by deciles. In Germany, for example, with the exception of the first decile, households would lose about 2–2.5% in disposable income across the income distribution if married couples were treated equally to cohabiting ones. This result is different from the one shown in Figure 4, and it suggests that in the first decile there are few married couples. On the other hand, for Greece and Malta we find a stronger positive effect in the lower part of the income distribution because some low income couples would start receiving means-tested benefits and pensions to which married people are not entitled.

Our results therefore also highlight that different tax–benefit treatments do not only affect individual households substantially, but can also affect policy-relevant indicators.

Discussion of results

As shown empirically, for more than half of the EU countries there are no (substantial) financial gains from being in wedlock. However, in some other Member States there is an important unequal treatment between cohabiting and married couples within their tax–benefit systems. Depending on the country, the strength of the unequal treatment varies substantially. In some countries cohabiting couples are, on average, better-off (Cyprus, Malta and Italy), while in other countries (Luxembourg, Germany, Ireland, Poland and Belgium) married couples have financial advantages compared to cohabiting couples.

Unequal treatment of couples has important implications. From an equity point of view, the different treatment of married and cohabiting couples within tax–benefit systems that exists in several EU countries violates both vertical as well as horizontal equity principals. First, at the individual level, it can easily happen in the case of joint taxation when a low-income earner pays more taxes than a higher-income earner due to their marriage status. At the household level, a tax break may be applied for a married couple with higher earnings, while a similar tax rebate will not be available to cohabiting couples despite their lower earnings. This clearly violates the principle of vertical equity.

Second, treating couples differently solely based on their marital status violates the principle of ‘marriage neutrality’, which is widely discussed in the US context analysing the tax code (see, e.g., Puckett, 2009; Listokin, 2013; Hemel, 2019). A couple’s tax dues or benefit entitlements should not be different depending on their civil status. Similarly, if couples are otherwise in the same financial and economic situation but are different in marriage status and have to pay different taxes, it violates the principle of horizontal equity. 21 Moreover, married couples with children, who, on average, are better off than single parent families, might be offered tax advantages that are systematically not available to single parents (see, e.g., Schechtl, 2021).

Generally, there are two ways to address unequal treatment of married and non-married couples. One is to apply the same tax and benefit rules to cohabiting couples as to married couples (tax allowances, tax credits or joint taxation), which is already done to a larger extent in some countries (e.g., Portugal, the Netherlands). 22 The second is to scrap out any fiscal benefits to married couples and move to more individualised taxation, keeping the support for dependants.

Our argument favours the second way of addressing the unequal treatment of married and non-married couples. Arguably marriage may provide many non-financial (e.g., legal, psychological, cultural) benefits for those who decide to marry. However, it is not evident that marriage implies any specific fiscal treatment by the state since marriage itself does not create any additional financial needs. What does indeed create additional financial needs is the existence of children or other dependants (elderly, people with disabilities) in households. Couples with dependent children, especially single parents, typically show a higher at-risk of poverty rates than couples without children. Children are increasingly more often being born out of wedlock. Even if born within a marriage, it does not mean that they won’t end up growing up with only one parent. More than half of divorcing couples do have children, which might leave children and a carer (usually a woman) in a financially precarious situation. 23 Coupled with the fact that not only married individuals have to take care of other dependants, the link of fiscal advantages to married couples seems to be discriminatory and not sustainable, and the tax–benefit system could probably be better adjusted by targeting those groups in need directly.

As shown before, unequal treatment of marriage and cohabitation with all the discussed consequences still exists in many European countries. Even though attempts have been made to eliminate these discrepancies in some countries, our analysis also highlights the issues related to the potential change of the current rules. Applying marriage-related tax and benefit rules also to cohabiting couples would lead to foregone revenues for the governments currently having different fiscal treatment of spouses. In addition, it might lead to further decreased revenues due to reduced incentives for the second earner to participate in the labour market. In turn, for the second earner, it translates into increased individual dependency of the family, lower entitlements to social security benefits and, more importantly, lower pensions in old age. Although applying marriage-related rules to all couples would ensure horizontal equity irrespective of marital status, the preferential fiscal treatment of couples vis-à-vis other household types (especially of single-parent families or households with other dependant adults) would put into question the fairness of the tax–benefit systems.

Moving to individual taxation seems to raise revenues for governments with marriage bonuses but leads to losses for governments with marriage penalties. At the same time, individual tax–benefit systems would be simpler, fairer and would interfere less with household decisions on paid and unpaid work distribution within a couple. Although this would mean that some households would be financially worse off, extra revenues collected might be better directed to specific population groups, such as households with children, poor households or the unemployed.

Conclusion

We analyse the unequal treatment of marriage and cohabitation within the tax–benefit systems of the EU Member States using EUROMOD, the tax–benefit model of the European Union. We contribute to the literature in mainly two ways. First, we provide the first comprehensive analysis on the unequal treatment of married and cohabiting couples across all EU Member States. Second, we also show that this unequal treatment differs substantially across countries and across household types.

In the majority of EU Member States, being married does not bring substantial financial gains or losses for a couple. For several countries we find important differences, mainly stemming from personal income taxation rules that either assess incomes jointly or apply marriage-related allowances or credits, and also from different benefit eligibility rules. While in seven countries married couples are substantially better off than cohabiting partners (marriage bonus) due to taxation, in four countries, the opposite holds true (marriage penalty), which is mainly related to social benefits.

We not only find substantial differences in the size of the marriage bonus across some countries but also across different household types. In countries with marriage bonuses, single-earner households or two-earner households with substantially different earning levels between partners typically receive a higher marriage bonus. For countries with the marriage penalty, it is the elderly households that are most affected.

From a policy-maker’s point of view, we highlight the budgetary costs that come along with eliminating the unequal treatment in some EU countries. For countries with marriage bonuses, applying the same policy rules to cohabiting couples that exist for married people would make cohabiting couples financially better-off but would result in a reduction in revenues for governments. Although couples were treated equally irrespective of their marital status, preferential fiscal treatment of couples vis-à-vis other household types (i.e., single parents) would put into question the fairness of tax–benefit systems.

Contrarily, abolishing the marriage-related tax–benefit components would lead to income losses for married couples but would result in increased government revenues that could be spent to targeted support of specific groups in need, regardless their marital status or the marital status of the carers. The policy-makers should aim at the most efficient and effective use of limited financial resources, ensuring equity and fiscal sustainability in the long run.

Our results should be interpreted with caution as they provide a static assessment of the different treatment of cohabiting and married couples within countries’ tax–benefit systems without any behavioural reactions. That is, we cannot draw any conclusion on whether a particular tax–benefit system encourages people to marry or if behavioural changes are due to the changes in the taxation or in social benefits’ eligibility rules. Please note, that the simulated impact is limited to the policies or their components that can be included and are modelled in EUROMOD microsimulation model (e.g. marriage bonuses stemming from survivor pensions or specific old-age pension rules that are different for married people cannot be simulated).

Future research could focus on answering the question as to what extent tax–benefit systems encourage marriage formation or dissolution in European countries, a question that is highly policy-relevant and so far not well developed in the literature. Another interesting follow-up could be the analysis of how tax–benefit systems influence work incentives within couples and whether and to what extent they could be responsible for differences in labour market participation between women and men.

Supplemental Material

Supplemental Material - Does it pay to say ‘I do’? Marriage bonuses and penalties across the EU

Supplemental Material for Does it pay to say ‘I do’? Marriage bonuses and penalties across the EU by Michael Christl, Silvia De Poli, and Viginta Ivaškaitė-Tamošiūnė Journal of European Social Policy

Footnotes

Authors’ Note

The findings, interpretations and conclusions expressed in this article are entirely those of the authors. They should not be attributed to the European Commission. Any mistakes and all interpretations are the authors and theirs only.The authors are grateful for the helpful comments from Salvador Barrios, Wouter Van der Wielen and María Teresa Álvarez Martínez. We are indebted to the many people who have contributed to the development of EUROMOD, especially to the EUROMOD team at JRC Seville.

Declaration of conflicting interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Supplemental Material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.