Abstract

The conceptualisation and measurement of benefit coverage is muddled with considerable confusion. In this forum contribution, we propose a new consolidated framework for the analysis of benefit coverage. Three sequential steps in measurement are suggested, involving the calculation of coverage rates, eligibility rates and take-up rates in social protection. Each step of the analysis focuses on particular aspects of programme legislation and implementation, and together the new framework will substantially improve the possibilities of research to inform policymaking. We provide an empirical illustration of our approach based on Swedish data, and highlight how our new consolidated framework for analysing benefit coverage provides a reorientation of the research agenda on benefit coverage.

Keywords

Introduction

The difficulties involved in the conceptualisation and measurement of welfare states and social policy are well known (Clasen and Siegel, 2007; Green-Pedersen, 2007; Gilbert, 2009; Goodin et al., 1999). This article introduces a new consolidated framework to analyse the intricate relationships between coverage, (non-)eligibility and (non-)take-up in cash benefit programmes. We also highlight specific areas of programme coverage where new research is needed. Cash benefit programmes are complex and their (in)effectiveness can depend on a number of very distinct factors. Three aspects are typically in focus in international analyses and in policymaking: financing, income replacement and coverage.

Financing is perhaps the most straightforward aspect of analyses of cash benefit programmes, as it involves the share of costs carried by employers, employees and the individuals themselves (Sjöberg, 1999). Income replacement concerns an assessment of the degree to which benefits replace work income during periods of joblessness, and pertains to questions of ‘what people get’ from the welfare state. The validity of replacement rate indicators is continuously discussed in research (Danforth and Stephens, 2013; Ferrarini et al., 2013; Kunißen, 2019; Kvist et al., 2013; Scruggs, 2013; Wenzelburger et al., 2013).

Coverage refers to the capacity of cash benefits to reach people in need, and pertains to questions of ‘who gets what’. The conceptualisation and measurement of benefit coverage is surrounded by considerable confusion, as detailed below. Sometimes the term is used to describe very different aspects of policy, and it is often difficult to understand how the concept is used without clearly studying the footnotes used to describe how the empirical analysis is constructed.

The purpose of this article is to provide a new consolidated framework for analysing benefit coverage in the area of social protection, drawing on insights from previous research. To what extent are existing approaches to analyse benefit coverage insufficient? How can the analysis of benefit coverage be improved to better identify exactly where policies are failing? Questions of ‘who gets what’ in social policy should not be approached too narrowly, but from various viewpoints. To better inform policymaking, we suggest that issues of benefit coverage are approached in a stepwise manner, using multiple – but distinct and clearly defined – concepts and indicators. Although our consolidated framework is developed primarily with respect to cash benefits, it is in principle also applicable to (the analysis of) public services.

This forum contribution is structured as follows. In the next section, we review earlier research to analyse programme coverage, and highlight the different ways in which coverage has been conceptualised in that literature. We then present our new framework for analysing benefit coverage, which integrates different concepts and indicators in a coherent way. The application of this new consolidated framework is then empirically illustrated based on Swedish data. In conclusion, we highlight areas where additional research is needed.

Coverage as potential and actual recipients

Several different approaches to conceptualise and measure benefit coverage exist. Korpi and Palme (1998) defined benefit coverage in terms of rights to get enrolled into a particular programme. Immervoll et al. (2014) used a definition including only those in receipt of a benefit, an aspect of social policy which Flora (1986) previously had used to calculate eligibility rates, and which Esping-Andersen (1990) referred to as take-up. In terms of clarity and uniform definitions, the conceptualisation of benefit coverage in comparative social policy research certainly did not have a good start.

The discussion is complicated further by various efforts to distinguish between different types of coverage, such as pseudo-coverage (Immervoll et al., 2014), observed and implicit coverage (Hernanz et al., 2004; OECD, 2018), as well as formal and effective coverage (European Council, 2019). The definitions often overlap, but are not always fully identical. However, a clear dividing line is between approaches focusing on potential recipients and approaches focusing on actual benefit recipients (Maquet et al., 2016). Both approaches face empirical challenges and conceptual limitations, as outlined below.

Coverage as potential recipients

Coverage in terms of potential recipients pertains to everyone who is exposed to a particular social risk (such as unemployment) and will have a legal right to apply for compensation once that risk occurs. This definition of coverage is mostly used in relation to social insurance, where eligibility is linked to contributions paid by either the employee or the employer, or a combination of both. For non-contributory benefits, coverage defined as potential recipients is typically 100% (compare universal child benefits or means-tested social assistance).

Data on the number of potential recipients of contributory programmes are often extracted from various social insurance funds, showing the number of insured persons as a percentage of a relevant reference population. The denominator – referring to everyone who is potentially at risk – sometimes differs between benefit programmes. For unemployment benefit (Carroll, 1999), sickness benefits (Kangas, 2004) and work accident insurance (Väisänen, 1992), the total labour force is often used. For old age benefits, the denominator is often people above the normal pension age (Palme, 1990).

The empirical focus on potential recipients used to be the dominant approach in analysing benefit coverage in comparative welfare state research. Among others, Korpi (1989) used the potential-recipients approach in one of the earliest large-scale investigations of social citizenship rights in OECD countries. Esping-Andersen (1990) followed the same procedure in defining and measuring benefit coverage in his seminal study of the three worlds of welfare capitalism. At least two well-known comparative social policy databases use the potential-recipients approach in calculating benefit coverage: the Social Policy Indicators Database (SPIN) and the Comparative Welfare State Entitlements Dataset (CWED). 1

A conceptual limitation of the potential-recipients approach is that not all who are formally included in a programme will actually receive a benefit, for a number of reasons. To some extent this limits analyses of the consequences of policies, as an increase of coverage (as potential recipients) may not necessarily result in more people benefiting from the policy (and vice versa). One of the main reasons for the discrepancy between potential and actual recipients is that people often need to fulfil certain eligibility criteria before an unemployment, sickness, parental leave or pension benefit is paid. People may need to sign up with the employment office and show that they are actively looking for a job in order to be eligible for an unemployment benefit. Parents may need to have made a minimum amount or period of contributions to receive a leave benefit, whereas people on sick leave may need to comply with regular health check-ups. Pensioners may lose their old-age benefit, or see it substantially reduced, if they have work income and so forth. In addition, among those who are covered and would be eligible, a number of people do not claim the benefit – a phenomenon referred to as non-take-up.

Coverage as actual recipients

In recent years, both the European Commission and the OECD have published data and analysed the coverage of social protection systems, mostly in the area of out-of-work benefits. This renewed interest is not surprising. The global financial crisis beginning in 2007/2008 painfully revealed that benefits in many countries were incapable of protecting people against the earnings loss of unemployment. As such, the social protection system also failed to fulfil its role as an effective automatic stabiliser (OECD, 2009). However, the European Commission and the OECD tend to focus their analyses of benefit coverage on actual recipients. Potentially, this takes us closer to the realities experienced by vulnerable groups in society (De Deken and Clasen, 2013; Finn and Goodship, 2014; Otto, 2018a; Van Oorschot, 2013).

The empirical approach is to relate the number of actual benefit recipients from socio-economic surveys or administrative records to the relevant target group of interest (e.g. working age population or the unemployed). Due to differences in the structure and the particular properties of the underlying data, coverage as actual recipients can differ widely between studies (Maquet et al., 2016). A consequence of this mismatch is that coverage rates based on actual recipients are sometimes above 100%. The OECD uses the prefix ‘pseudo’ to coverage as actual recipients precisely because the populations in the numerator and denominator do not always fully overlap, not because the measurement is based on actual recipients (OECD, 2018).

For policymaking, pseudo-coverage rates have at least one notable conceptual limitation: observed changes in coverage can either be the result of policy reforms or changes pertaining to the reference population. For instance, if fewer people receive unemployment benefits, this could be because of stricter qualification criteria, or an increase in the number of unemployed people with weaker employment histories. Although there are various weighting techniques to reduce this bias (Otto, 2018b; Otto and van Oorschot, 2019), the difficulty in disentangling ‘policy supply’ and ‘policy demand’ limits our understanding of policy. The exact reasons for incomplete coverage are obscured further as we typically lack information about those eligible, but who for one reason or the other do not receive a benefit. Non-take-up of this kind may be caused by a multitude of factors at the programme level (e.g. complex rules or vague qualification criteria), administrative level (e.g. poor quality of communication or administrative procedures) and client level (fear of stigmatisation, ignorance or insufficient knowledge) (Van Oorschot, 1991).

Towards a consolidated framework for analysing benefit coverage

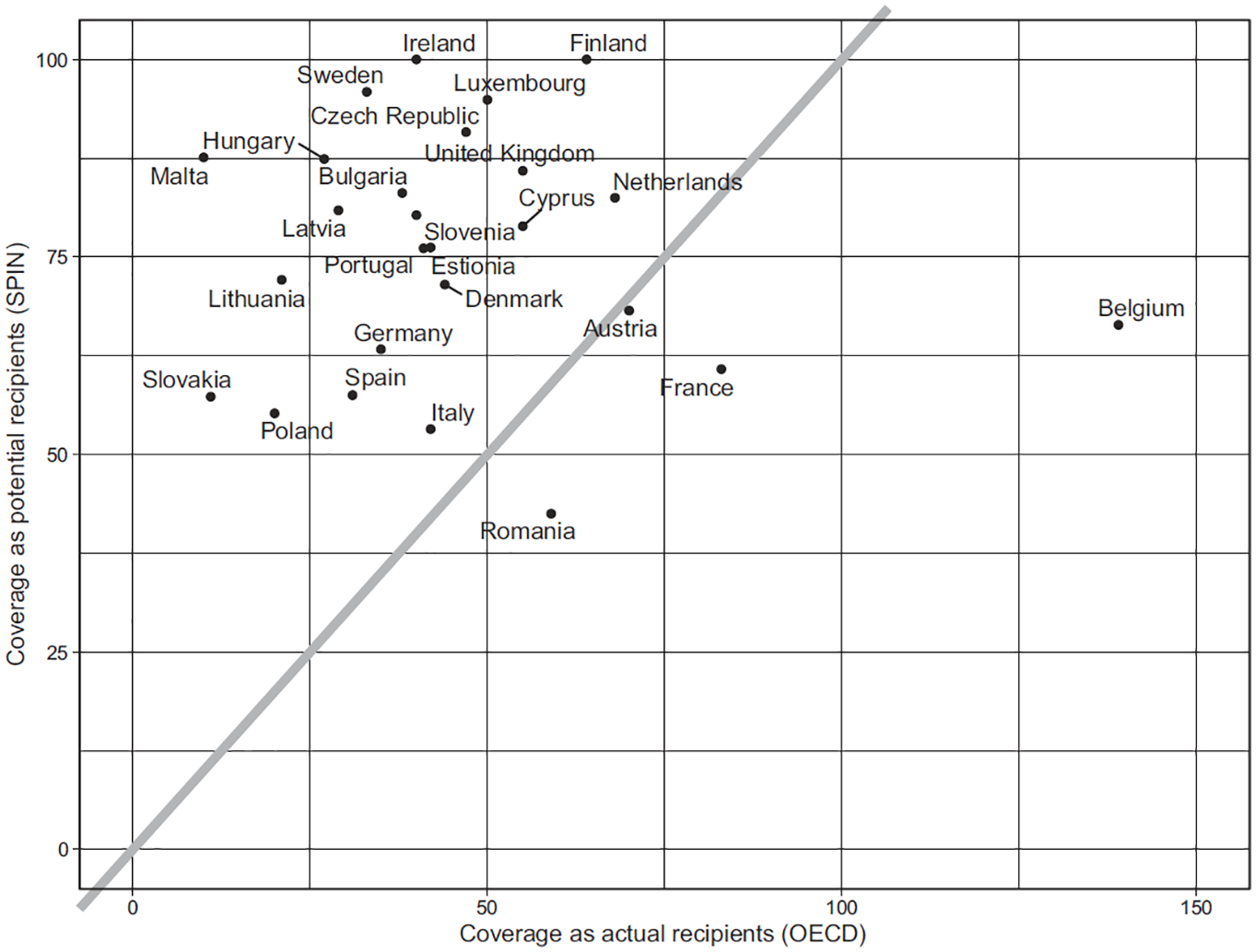

Despite the conceptual limitations outlined above, the increased focus on actual recipients in analyses of social policy and benefit coverage is a welcome and important addition to research (Van Oorschot, 2013). However, it is not a substitute for an analysis of potential recipients. Consider the data in Figure 1, which show unemployment benefit coverage rates as potential and as actual recipients in 26 European countries in 2010. For the former, we use data on unemployment benefit coverage in SPIN (Nelson et al., 2020). For the latter, we rely on OECD SOCR administrative data on pseudo-coverage. In OECD SOCR, we have excluded means-tested benefits to resemble as much as possible the data in SPIN.

Coverage rates of unemployment benefits as potential and actual recipients in 26 European countries, 2010.

Note the countries scattered in the upper-lefthand corner, including Bulgaria, the Czech Republic, Ireland, Finland, Hungary, Latvia, Luxembourg, Malta, Slovenia and Sweden. 2 In each of these countries, the share of those who are unemployed receiving unemployment benefits (indicated on the horizontal axis by coverage as actual recipients) is below 50% and even down to 10% in Malta.

Assume that we only have the information on how many people actually receive unemployment benefits on the horizontal axis showing the coverage rate as actual recipients (thus, no information about how many people are insured against the loss of earnings in case of unemployment – i.e. how countries are scattered along the vertical axis showing the coverage rate of unemployment benefits as potential recipients). In terms of policymaking, it would then be easy to reach the conclusion that the countries in the upper-lefthand corner of Figure 1 need to do better in terms of extending unemployment benefits to larger fractions of the labour force, making sure that more people are insured against losses in earnings. In a voluntary system, this can be accomplished by reducing the fees. In a compulsory system, it may involve an extension of the programme to encompass those in non-standard forms of employment, such as the self-employed, part-time employed and employed with zero-hour contracts (Spasova et al., 2017).

The scattering of countries along the vertical axis, however, suggests a very different policy diagnosis for these particular countries as the number of potential recipients is comparatively high. Thus, the problem may not primarily be that large fractions of the labour force are excluded. This insight is important as it helps us to identify potential weaknesses in the policies put in place. If a substantial part of the labour force is insured against losses in earnings in case of unemployment, while a large number of the unemployed evidently do not receive benefits, there are only two plausible, but very different, explanations: either eligibility criteria are too strict, or there is substantial non-take-up among those who qualify for benefits. Each problem requires its specific set of policy solutions.

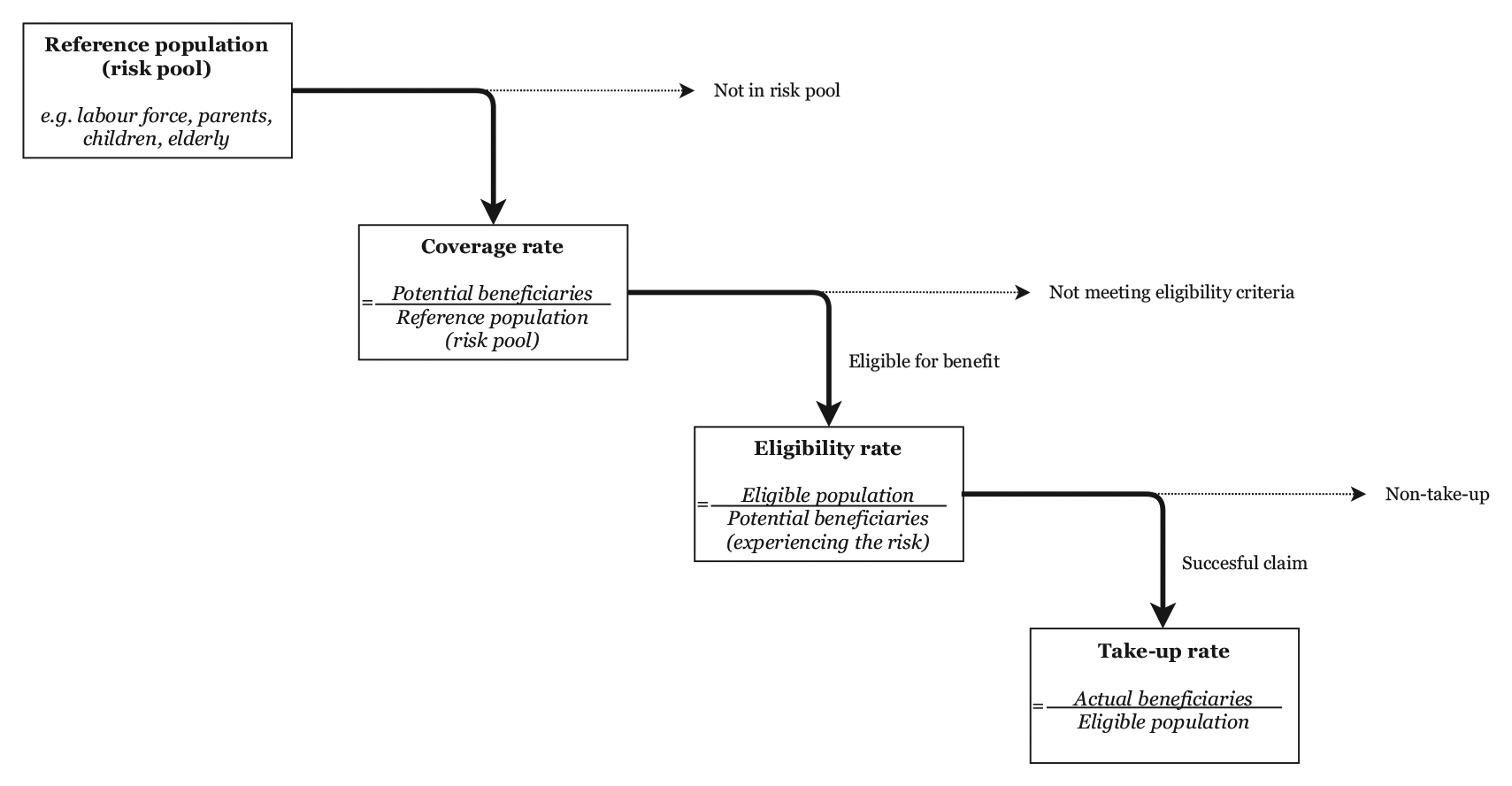

By combining the two approaches of analysing potential and actual recipients we narrowed down the problem of incomplete access to unemployment benefits quite substantially, but we still lack information to develop more clear policy guidance. Instead of the pseudo-coverage rates of unemployment benefits used above, we would have been better off by introducing a distinction between eligible persons with and without benefits. In our consolidated framework for the analysis of benefit coverage, issues of eligibility and non-take-up are explicitly addressed, as outlined in Figure 2.

A multidimensional framework for the analysis of benefit coverage.

The analysis begins by defining the appropriate reference population, depending on the research topic addressed. If the major concern is with insufficiencies in unemployment benefits, a natural reference population is the labour force. If work–family reconciliation policies are in focus, people who are in their fertile years may be a relevant starting point, and so forth. Hence, the crucial issue is to exclude those people who are not defined as being in the risk pool.

Once the appropriate reference population has been decided upon, the actual analysis begins. Three indicators are suggested for measurement, following a sequential order of analysis: the coverage rate, the eligibility rate and the take-up rate. Each step of the empirical analysis concerns particular aspects in the functioning of social protection, and is thus designed to maximise possibilities for policy inference. Note that for each stage of the analysis, the numerator of the previous stage is the denominator of the next stage.

The first stage of the analysis focuses on coverage as potential recipients. We restrict the use of the term coverage exclusively to this stage as a means to improve conceptual clarity. The reference population of the earlier stage defines the denominator used to calculate the coverage rate. For unemployment benefits, the coverage rate simply shows the share of potential recipients (those insured) in the labour force (or the reference population chosen for analysis).

The next stage of the analysis is to calculate the eligibility rate. Some of those who are insured will not receive compensation because they fail to meet eligibility criteria. For those who are insured, we calculate the eligibility rate as the share of people who qualify for benefits according to the programme rules.

Some people, who are eligible for a benefit, will not receive it (i.e. non-take-up). For those with successful claims, the final stage of the analysis includes calculating the take-up rate, which is the share of actual recipients in the eligible population. It should be noted that the take-up rate differs notably from the beneficiary ratios typically used in analyses of coverage as actual recipients, which use as denominator those in the relevant risk pool (e.g. the labour force or the working-age population) or currently experiencing the risk (e.g. unemployment). The take-up rate in our consolidated framework relates the number of people receiving benefits to those who are eligible according to programme rules and legislation. The take-up rate as we define it here is more precise than the beneficiary or recipiency ratios used elsewhere, as it takes into account issues of (non-)eligibility.

An empirical illustration: Sweden

For illustrative purposes, we will apply our consolidated framework for analysing benefit coverage to unemployment benefits, parental leave benefits and social assistance in Sweden. Sweden has high-quality data based on both surveys and population registers, as well as benefit programmes that are relatively easy to administer and therefore analyse. Nonetheless, it will become clear that even in Sweden, a complete analysis of benefit coverage is not always possible due to data limitations.

Together, the three programmes selected for empirical analysis illustrate the fruitfulness of analysing benefit coverage in a step-wise manner. Table 1 shows the coverage rate, eligibility rate and take-up rate of the Swedish earnings-related unemployment benefit, the earnings-related parental leave benefit and social assistance (försörjningsstöd) for selected years for which data is publicly available. For the earnings-related unemployment benefit we have relied on register data from Swedish authorities. For the earnings-related parental leave benefit and social assistance, we have used the European Union Statistics on Income and Living Conditions (EU-SILC).

Coverage, eligibility and take-up of social benefits in Sweden.

Source: Swedish Statistics (www.scb.se, last accessed 19-1-2021), the Swedish Employment Agency (https://arbetsformedlingen.se, last accessed 19-1-2021), the Swedish Unemployment Insurance Inspectorate (https://www.iaf.se, last accessed 19-1-2021), the Swedish Social Insurance Office (https://www.forsakringskassan.se/statistik/social-insurance-in-figures, last accessed 19-1-2021) and the European Union Statistics on Income and Living Conditions (EU-SILC) (https://ec.europa.eu/eurostat/web/microdata/european-union-statistics-on-income-and-living-conditions, last accessed 19-1-2021).

For the earnings-related unemployment benefit, the labour force is used as reference population for the coverage rate. The reference population for the earnings-related parental leave benefit and social assistance is women of fertile age (16–49 years) and single person households 18–64 years, respectively.

The Swedish earnings-related unemployment benefit is a voluntary, state-subsidised programme. To be included in the programme, people need to become a member of an unemployment insurance fund and pay a monthly fee. Thus, the programme suffers from incomplete coverage as not all of the labour force (reference population) are insured. After a substantial increase of the membership fee in the mid 2000s (Nelson, 2017), the number of insured workers dropped from around 85% to slightly below 70% of the labour force.

Far from all unemployed members of an insurance fund are eligible for a benefit. To qualify for benefits, unemployed members need to have been insured for 12 months and to have had a stable foothold in the labour market. 3 In parallel with a rise in precarious work, fewer unemployed members qualify for the earnings-related benefit (Alm et al., 2020). In 2000, the eligibility rate was slightly above 80%. In 2019, it was down to around 50%. The benefit may be withdrawn or substantially reduced if those who are unemployed are not actively looking for a new job. However, the sanction rate is only around 6%, the majority of which concerns withdrawal of the basic unemployment benefit (Inspektionen för arbetslöshetsförsäkringen, 2017). 4

Data do not allow an empirical assessment of the take-up rate of the earnings-related unemployment benefit among those who are eligible. A major problem is that currently available micro-level data lack information on membership of an insurance fund. However, the voluntary character of the earnings-related unemployment benefit, low stigma and hardly any administrative errors suggest that take-up is likely to be very high. 5 It is likely that some unemployed members who are between jobs may choose not to apply for benefits, especially if they know that they only will be unemployed for a week or so. After consulting the statistical units of the Swedish Employment Agency and the Swedish Insurance Inspectorate, we find it reasonable to set the take-up rate of the earnings-related unemployment benefit at 95%. For obvious reasons, this number should be interpreted cautiously until it can be determined empirically.

The Swedish earnings-related parental leave is compulsory, and it can be used by both mothers and fathers. In this analysis, we use women of fertile age (16–49 years) as the reference population, which gives us complete coverage. Six months of employment before giving birth are needed to qualify for the earnings-related benefit. Calculations based on EU-SILC show that around 50% of all mothers giving birth qualify for the earnings-related parental leave benefit, and that this share has been stable since the mid-2000s. Due to the low number of mothers giving birth in each wave of EU-SILC, we used 3-year moving averages.

It should be noted that eligibility for the earnings-related parental leave benefit is underestimated as there are special rules for the unemployed and self-employed that we could not simulate due to lack of data. 6 Similar to the earnings-related unemployment benefit, it has not been possible to estimate non-take-up among those qualifying for earnings-related parental leave. One reason is that EU-SILC income data does not distinguish between different forms of family benefits. 7 As all mothers who gave birth stay home for at least a few months, we expect that all previously working mothers will apply for parental leave. Similar to the unemployment benefit, administrative errors are probably low since most information needed in the application process is derived from national registers.

For social assistance, we also used EU-SILC, and report 3-year moving averages. In order to simplify the calculations, the analysis is restricted to single persons aged 18–64 years. As social assistance in Sweden is a general means-tested benefit programme, everyone is included. Coverage is therefore 100%. Having a low income, below the national social assistance scale rates, is the risk to be addressed. However, not all poor people are eligible. Under normal circumstances, full-time students cannot receive social assistance, nor can people with capital or other assets that can relatively easily be converted and used for consumption. If we included these two groups, the eligibility rate for social assistance was slightly below 70% in 2017, and somewhat above 70% in 2005. If students are excluded, the eligibility rate is close to 100%. Thus, hardly any people in these income brackets have registered capital income.

Notably, take-up among those eligible is very low, probably due to a combination of stigma and administrative procedures. Considering the latter, some evidence suggests that social assistance case-loads at municipal level in Sweden are related more to characteristics of the social welfare office than economic or demographic factors (Minas, 2006). The law on social assistance presupposes a considerable amount of discretionary power at the local level, providing high degrees of autonomy of individual case workers. Although take-up has increased in recent years, only 28% of those single persons who were eligible did receive a benefit in 2017.

Conclusion: An agenda for research

We have introduced a new consolidated framework for analysing benefit coverage. Questions of ‘who gets what’ in social policy cannot be fully addressed by conventional approaches to analyse coverage as potential and actual recipients. In our consolidated framework, coverage as potential recipients is complemented by analyses of eligibility and take-up. The two latter aspects are intertwined and cannot be separated using existing approaches to analyse coverage as actual recipients.

The empirical illustration based on Swedish data shows that our consolidated framework for analysing benefit coverage provides more detailed guidance for policymaking. Our analyses clearly show that the Swedish earnings-related unemployment benefit, the earnings-related parental leave benefit and social assistance fail to reach all those in need, but for different reasons. Our results should be interpreted cautiously. Nonetheless, it is clear that eligibility criteria raise obstacles in the inclusiveness of the earnings-related unemployment and parental leave benefits, whereas non-take-up among those eligible seems to be a major issue for social assistance. The latter needs to be investigated further, but suggests changes to reduce the discretionary character of social assistance in Sweden, thereby reducing stigma and streamlining administrative procedures.

Although our consolidated framework is a major step forward in terms of informing policymaking, it raises empirical challenges. Each stage of the analysis involves multiple decisions in measurement that are likely to affect the indicators and consequently the research findings. Whereas there is an ongoing discussion of measuring potential and actual recipients that has brought research forward, more efforts are needed to discuss how we can identify eligible persons in and without receipt of benefits.

Analyses of eligibility and take-up are mostly conducted in relation to means-tested benefits, where policy frameworks can be simulated with reasonable levels of accuracy based on individual-level and household-level income data (Bargain et al., 2012; Frick and Groh-Samberg, 2007; Fuchs et al., 2020; Gustafsson, 2002; Matsaganis et al., 2010; Van Oorschot, 1991). It is trickier to analyse eligibility in relation to contributory benefits or public services, which often requires information not always included in socio-economic surveys. We therefore suggest that research is concentrated on this particular aspect in the measurement of coverage.

Footnotes

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: the authors received financial support from the InGRID-2 project “Integrating Research Infrastructure for European expertise on Inclusive Growth from data to policy”, funded by the European Union’s Horizon 2020 research and innovation programme under grant agreement No 730998.