Abstract

While debt is not problematic per se, it can become an additional burden when people experience negative life events–like unemployment, a severe disease, divorce, or their partner’s death–which can be detrimental for individuals’ subjective wellbeing. We investigate first, a potential moderating effect of economic resources or, better yet, lack thereof in the relations between negative life events and general life satisfaction, and second, whether this moderating effect is a function of state-level policies. We expect that, on average, debt has a reinforcing effect on the negative relationship between negative life events and general life satisfaction. Moreover, we expect that country-level policies protecting individuals from the negative consequences of experiencing a negative life event or indebtedness can explain the country differences in the moderating effect of debt. We test our assumptions among the population aged 50+ applying data from the Survey of Health, Ageing and Retirement (SHARE). We apply a two-stage fixed-effects regression approach to estimate the moderation effect of debt on the relationship between negative life events and general life satisfaction within and across countries. Although we find an almost zero average moderating effect of debt across countries, we find large variance in the moderating effects between countries. This variance can be explained by debt regime, but not by the generosity of the public unemployment and the public health systems, or the level of gender equality.

Introduction and previous research

Post-war era developments across the industrialized world provided larger shares of the population the opportunity to accumulate assets. These developments include rising real wages, policies encouraging homeownership, and an expansion of occupational pension plans. Coupled with increasing longevity and recent reductions in public pension spending, accumulated wealth became an essential component of individuals’ old-age provision (Skopek, 2015). On the macro-level, rising wages and wealth resulted in increased consumption and economic growth. On the micro-level, however, economic fortunes are distributed very unequally. The current generation of older persons uses different forms of credit to maintain the standard of living they have been accustomed to and is much more likely to be in debt than previous generations (Cynamon and Fazzari, 2008; Lewin-Epstein and Semyonov, 2016).

Debt is not problematic, per se. Instead, it is an important means to smooth out consumption over the life course (Modigliani and Brumberg, 1954). At old age, however, household income typically decreases, and individuals are more reliant on their savings. In addition, debt can become a burden, for example, when people experience negative life events such as unemployment, divorce, or severe disease. Such events are typically related to a decrease of subjective wellbeing–at least temporarily–(Lykken and Tellegen, 1996), but also to a drop in income. Individuals experiencing negative life events become more likely to have problems servicing their debt, and they are more likely to experience psychological stress. Because economic constraints and additional psychological stress caused by debt are likely to reinforce the negative relationship between negative life events and subjective wellbeing, debt can spiral out of control when experiencing a negative life event (see also Kuypers and Marx, 2021, in the current issue). Our first research objective is to identify the potential moderating effect of debt on the negative relationship between negative life events and subjective wellbeing, measured by its cognitive dimension ‘general life satisfaction’.

One question emerging from the increased personal debt of older persons but also most rich nations (Coletta et al., 2019) is whether countries profiting from the increased consumption also take measures to help their citizens cope with debt and the experience of negative life events. Thus, our second research objective is investigating the role of the state in decreasing the effect of experiencing a negative life event on subjective wellbeing of individuals who are also indebted and thus faced with a ‘double burden’.

Social (Liu et al., 2017), religious (Bjorck and Thurman, 2007), and personality resources (Yap et al., 2012) can reduce the negative effect of negative life events on subjective wellbeing. For buffering effects of economic resources, empirical evidence is mixed. Smith et al. (2005) find a buffering effect of net household wealth on the negative effect of becoming handicapped on subjective wellbeing (CES-D depression inventory). Kuhn and Brulé (2019) do not find a buffering effect of income or wealth on the negative effects of separation, death of a closely related person, unemployment and disability, on subjective wellbeing (general life satisfaction). 1

We look at a specific dimension of wealth, namely, debt–understood as indebtedness and measured as gross debt–as another potential moderator of the negative relationship between negative life events and subjective wellbeing, measured as general life satisfaction. We expect that, on average, debt has a reinforcing effect on the relationship between negative life events and general life satisfaction. Using an international comparative approach, we explore the possibility that the reinforcing role of debt depends on the policies countries implement to protect individuals from unexpected negative life events and other hardships.

The contribution of our article is twofold: first, just as Kuypers and Marx (2021) in the current issue, we expand previous research by changing the perspective from positive (for example, income and wealth) to negative economic resources (that is, debt). Second, unlike most previous studies that focused on a single country, in this study, we examine state-level mechanisms in determining the extent to which being in debt shapes individuals’ ability to maintain their general life satisfaction following a negative life event. Thus, we analyse the relationships between debt, negative life events, and general life satisfaction across different European countries, with different levels of welfare generosity, gender equality, and personal bankruptcy regulations.

For our empirical analyses, we use the SHARE, an international panel study representative of the population aged 50 years and over. SHARE is one of the few international comparative studies that provide high quality and detailed information on (self-reported) wealth, debt, respondents’ general life satisfaction, and numerous life events. The SHARE population is particularly valuable for our research interest for several reasons. First, most respondents in SHARE have already entered retirement or are close to retirement. Hence, they have already had plenty of time for wealth accumulation, and we can thus learn about how successful they have been in this task over their life course. Second, because many of these respondents are already out of the labour force, they are more likely to rely on wealth than income. At the same time, due to increased indebtedness within this population (Coletta et al., 2019), it is more likely that the negative effect of a negative life event on their general life satisfaction will be reinforced by debt as compared to the younger population (Niedzwiedz et al., 2015). The 50+ population are more likely to experience their partner’s death and a severe disease than the overall population but less likely to experience unemployment and divorce. If, however, they experience unemployment or divorce, these events can have a stronger negative impact on their general life satisfaction compared to the younger population.

Theoretical framework

Debt, negative life events, and subjective wellbeing

The literature on the relations between subjective wellbeing and economic standing relies mainly on the so-called set-point theory of wellbeing. This theory argues that the relationship between economic resources and subjective wellbeing is only short because the level of individual happiness oscillates around a certain set-point that is partly biologically given and partly determined in early life (Lykken and Tellegen, 1996; Easterlin, 2005). However, more recent findings (Fujita and Diener, 2005; Headey, 2008) showed substantial and permanent changes in individuals’ subjective wellbeing levels. Based on these results, Easterlin (2005) maintained that set-point theory might apply for events in pecuniary domains (for example, income and wealth) but is unlikely to apply for events in nonpecuniary ones (for example, family and health) where larger and more permanent decreases in subjective wellbeing are expected.

We rely on differences in available resources (see Cummins, 2000)–in our case debt–as a potential explanatory factor for heterogeneities in relationships between negative life events and subjective wellbeing. There are at least two reasons to expect debt to moderate the relationship between negative life events and subjective wellbeing. We summarize the first one under the term ‘psychological stress’. Cummins (2000), as well as Weinstein and Stone (2018), argues that there exist ‘second order personality traits’ (Cummins: self-control, self-esteem, and optimism) or ‘key psychological needs’ (Weinstein and Stone: autonomy, relatedness, and competence) that are positively related to subjective wellbeing. Both theoretical perspectives maintain that financial insecurity exogenously affects personal needs (that is, second order personality traits and key psychological needs) and hence subjective wellbeing. Following Dwyer et al. (2011), we argue that debt is a clear example of such financial insecurity as it implies consuming beyond one’s current income. Moreover, being indebted may also lead to social isolation (Kuypers and Marx, 2021; Oesterreich, 2008, in the current issue), undermining the need for relatedness, and it can harm one’s optimism and self-control (Hobfoll, 2002).

A second reason to expect a debt moderation effect is that indebted individuals are likely to find it harder to cope with the unexpected consequences of negative life events due to their inability to draw the material resources needed. This reasoning is based on the inverse of the function of income and wealth in buffering against the outcomes of negative life events (Tay et al., 2017). We summarize the second explanation for a reinforcing moderation effect of debt under ‘economic constraints’. Both explanations suggest that debt reinforces the negative relationship between negative life events and subjective wellbeing (hypothesis 1).

The comparative setting

The second contribution of our study is to investigate whether the moderation of debt in the relationship between negative life events and subjective wellbeing differs across institutional contexts. The welfare state has different instruments to affect the relationship between debt, negative life events, and happiness directly or indirectly. According to Pacek and Radcliff (2008), its most important instrument is the generosity of its services or decommodification, referring to the extent to which citizens in a country are economically independent of the market (Esping-Andersen, 1990). These services or state-sponsored social benefits safeguard against the negative consequences of unexpectedly exiting the labour market and other unexpected life events. Such benefits should alleviate both psychological stress and economic constraints induced by debt. Thus, we predict that debt’s moderating effect will be weaker in countries with a higher degree of welfare state generosity (hypothesis 2).

Negative life events do not affect men and women to the same extent. In line with the findings of Andress et al. (2006) and Leopold (2018), we expect widowhood and divorce to be financially more consequential for women than for men. The size of the widowhood and divorce effects in our analyses should at least partially depend on the level of discrimination of women in paid (labour market) and unpaid work in the different countries (Sierminska et al., 2010; see also Gornick and Sierminska, 2021, in the current issue, for gender differences in wealth accumulation and retirement preparedness). Role expansion theories (Brook et al., 2008; Nordenmark, 2004) suggest that small income differences between spouses (that is, high levels of gender equality) are an indicator for role expansion and women’s multiple social roles (Carr, 2004; Halleröd, 2013). These roles provide a wider social network and a higher experience of dealing with different practical situations, which help women to cope with spousal loss (Bennett et al., 2010) and probably also with divorce. We expect that high levels of gender equality will also reduce psychological stress and economic constraints induced by debt for the group that is mainly affected by these events, namely, women. We, therefore, suggest the moderating effect of debt as weaker in countries with a higher degree of gender equality (hypothesis 3). Finally, we also consider the countries’ regulations regarding personal bankruptcy. We expect a weaker moderation of debt in the relationship between negative life events and general life satisfaction in countries with friendlier personal bankruptcy laws (hypothesis 4). Figure A1 in the appendix illustrates our micro- and macro-level hypotheses.

Data, variables, and method

Data

We test our hypotheses drawing on data from the SHARE, 2 a multidisciplinary and cross-national panel database of microdata on health, socio-economic status, and social and family networks of individuals aged 50 or older for 27 European countries and Israel. So far, data from seven waves conducted between 2004 and 2017 is available. Respondents aged 50 years or more and their cohabiting partners are our units of analysis. For our micro-level analysis (hypothesis 1), we use only countries that participated in at least two waves, excluding the third wave that collected retrospective life histories. We had to exclude five countries (Greece, Hungary, Luxembourg, Poland, and Portugal) with too few observations for one or several of our negative life events. To test our contextual hypotheses (2–4), we further limit our analyses to countries with the required context information. Table A2 in the Online Appendix gives an overview of the available context information and our unbalanced country samples can also be found there.

Variables and sample

Our dependent variable is individual subjective wellbeing operationalized as general life satisfaction, measured on an 11-point single-item scale, with 0 meaning completely dissatisfied and 10 meaning completely satisfied. We decided for this single indicator of subjective wellbeing in line with Veenhoven (1993), stating that a simple single item to measure quality of life is generally agreed to perform as well or better than more complex formulations and allows easy comparison of life satisfaction across nations. 3 General life satisfaction represents the cognitive dimension of subjective wellbeing, to be distinguished from its affective (quality of life) and emotional (depression) dimensions (Amit and Litwin, 2009). It is the most stable dimension of subjective wellbeing over the life course (Eid and Diener, 2004; Oishi et al., 2001), and it is robust to social desirability bias and stable across countries (Pacek and Radcliff, 2008). In our statistical models, general life satisfaction is z-standardized to ensure that the coefficients across countries are comparable. Consequentially, a one-unit change in one of the independent variables results in a change in general life satisfaction of one country-specific standard deviation.

Our main independent variables are debt and negative life events. We operationalize debt as the actual amount that one owes (Tay et al., 2017), focusing on indebtedness rather than over-indebtedness. Unlike over-indebted households, indebted households can fulfill their debt obligations. Moreover, if the debt goes along with wealth accumulation, even a high debt burden is not necessarily related to restrictions in the fulfilment of physical or psychological needs. A high level of indebtedness (high debt-to-income ratio) can represent very different things: it can imply an involuntary need to cover costs but it can also indicate a preference for present over future consumption or myopic consumption (Betti et al., 2007). We argue that being in debt is likely to moderate the relationship between negative life events and general life satisfaction, especially among individuals aged 50+ who are in or close to retirement and thus rely on accumulated economic resources. Even if they can repay their debt and maintain a certain level of consumption, these indebted households are still likely to feel financially burdened (see also Kuypers and Marx, 2021, in the current issue). Considering only those households who are over-indebted, we might miss part of the story.

In line with the SHARE definition, we operationalize debt as the sum of the value of running mortgages and other debt on cars, credit cards, or towards banks, building societies, and other financial institutions (Christelis et al., 2005a: 311). We adjust this sum for differences in purchasing power across countries and time, that is, the values correspond to euros in Germany in 2015. Considering the skewed distribution of debt, we decided to logarithmize it. To simplify the interpretation of the regression coefficients, we centre the logged mean gross debt.

We acknowledge that mortgage is a wealth-generating debt form and might have less detrimental effects on general life satisfaction than liabilities. However, we contend that, especially for the elderly and the very old, a mortgage is more likely a problem than a wealth-generating mechanism. Households that had not yet finished repaying their mortgage might resort to increasing liabilities to do so (see Lewin-Epstein and Semyonov, 2016). In their study on the relevance of inheritance and gifts for the wealth accumulation of low-income households in the current issue, Morelli (2021) find that housing wealth is an important part of wealth for low-income households. This could apply the other way around: mortgage could be a (productive) form of debt, especially among low-income households. We therefore also estimated our models looking at the two debt components separately, in that they work in different ways.

Importantly, indebtedness might also be a direct consequence of negative life events (see Hochman et al., 2019; and Rodems and Pfeffer, 2021, in the current issue). In such cases, debt should work as a moderator and as a mediator of the relationship between negative life events and general life satisfaction. If debt and wealth are mediators on the effects of negative life events on general life satisfaction, controlling for them would artificially decrease the effect of the negative life events. As we are interested in the moderation role of debt and not the mediation, we decided to use long-term average debt and wealth as measurements that potentially affect the incidence of negative life events. Specifically, for each wave, we construct the mean log debt and wealth accumulated from the first wave available to the wave (t−1) preceding the wave (t) in which a respondent experienced one of the events we are considering. This operationalization avoids the over-control problem of time-varying wealth and debt, which might be affected by negative life events.

We analyse four negative life events, three of which are family events, and one is a work event that we measure with four event dummies. The first event is becoming unemployed since the previous wave. The second event is having been diagnosed with a stroke, cancer, hip or femoral fracture, or a heart attack since the previous wave. 4 The third event is the partner’s death since the previous wave, 5 and the fourth event is divorce since the previous wave.

We adjust for several control variables. We control for gross wealth, 6 which is constructed similarly as gross debt, that is, we use centred logged mean gross wealth adjusted for purchasing power with Germany 2015 as reference. We control for centred logged household net income, age, health, partner’s age and health, and months since the previous wave. To control for period effects, we include wave dummies. Health is measured on a 1 (excellent) to 5 (poor) scale. Our fixed-effects analysis design, explained in the section below, implicitly controls for all time-constant demographic variables, including gender and migrant status and personality traits. Table A1a–TableA1c in the Online Appendix show our summary statistics.

To test our country context hypotheses 2, 3, and 4, we combine the micro-level SHARE data with macro-level information from other data sets. To compare the generosity of social benefits, we use the Comparative Welfare Entitlements dataset (CWED2) (Scruggs, 2007; Scruggs et al., 2017). This dataset provides generosity measures (rather than relative expenditure) for 33 countries regarding each country’s healthcare, unemployment, and public pension systems. These sub-indices have a minimum value of 0, with higher values indicating higher generosity. They are calculated for an average production worker in the manufacturing sector who is 40 years old and has been working for 20 years preceding the benefit period. We include these generosity measures because they are designed to capture the countries’ welfare generosity, not the relative expenditure. In our analyses, we include the indices for the generosity of the unemployment and healthcare system, which we expect to affect the events of unemployment and severe disease, respectively. We calculate the mean generosity indices for 2003 (first SHARE wave) to 2011 (last CWED wave). 7

The overall generosity measures of the unemployment and healthcare system include four measures: qualification period (weeks of insurance needed to qualify for benefit), duration (weeks of benefit entitlement excluding times of means-tested assistance or long-term disability/invalidity pensions), waiting days (days one must wait to start receiving benefit after becoming unemployed/sick), and coverage (percentage of the labour force insured for unemployment risk/with sick pay insurance). The indices for unemployment and sick pay insurance are computed using the standardized (z-scores) values as (Scruggs, 2014: 9)

The level of discrimination of women in paid and unpaid tasks is depicted in the Gender Equality Index, initially developed by Plantenga et al. (2009) and provided by the European Institute for Gender Equality (EIGE, 2020). This index is calculated based on gender inequality in seven domains: work, knowledge, health, money, power, time, and violence. It produces a score that ranges between 1 and 100, where 100 stands for the best situation, with no gender gaps combined with the highest level of achievement. We calculate the mean Gender Equality Index for 2005 (first wave of the index) to 2017 (latest SHARE wave).

Finally, we account for the so-called debt-discharge regime in our analyses based among others on the work of Schönen (2009; 2010) and Hoffmann (2012) and applied, for example, in the work of Angel and Heitzmann (2015). These regimes are based on countries’ different debt-discharge procedures. Four regime types or country groups are differentiated: 8 first, countries with no or very weak discharge mechanisms; second, countries with partial discharge; third, countries with full discharge following the Scandinavian or German law approach; and fourth, countries with full discharge following the British or French law approach, which is quicker and considered more debtor-friendly than the third type. Countries within the first regime type either do not grant any possibilities for consumers’ debt discharge at all or they offer such possibilities that are bound to the fulfilment of strict conditions such as, for example, a positive court decision. The second regime type provides possibilities of consumers’ debt discharge but only to a limited extent. Usually, debtors must pay back a fixed percentage of their debt before discharge is granted, or the threshold of admission to a consumer insolvency proceeding is restricted to a maximum over-indebtedness of a certain amount of money. Countries within the third regime group offer full debt discharge after a fixed period in which the debtor tries to pay pack at least parts of his or her debt. France–that is, Alsace-Moselle–and the UK form the fourth regime type characterized by low admission thresholds and short procedures leading to an immediate and full debt discharge. As we have no regional indicators for France, the fourth type, however, is not represented in our sample. Table A2 in the Online Appendix shows the summary statistics for our context variables.

Method

To identify the effect of negative life events on general life satisfaction and the potential moderating effect of debt, we estimate for each country a linear fixed-effects regression of general life satisfaction on negative event dummies with interaction terms for each negative event with time-invariant log gross debt and log gross wealth, including the control variables specified above. Because we use centred debt and wealth, the main effects of the negative life events reflect the mean difference between the level of general life satisfaction after a negative life event and all other time points. Moderation should appear in the coefficients of the interaction terms. Standard errors are adjusted for clustering at the household sampling unit level.

To identify how the country-level variables affect the effects at the micro-level, we follow the two-stage approach by Lewis and Linzer (2005), that is, we estimate weighted linear regressions on the estimated main effects of the negative life events and the moderation effects with log gross debt for each country on the macro variables mentioned above. The standard errors of the estimates from the first stage are used as weights in the second stage. We also estimated all models with financial debt separated from mortgage debt.

Results

Micro-level results

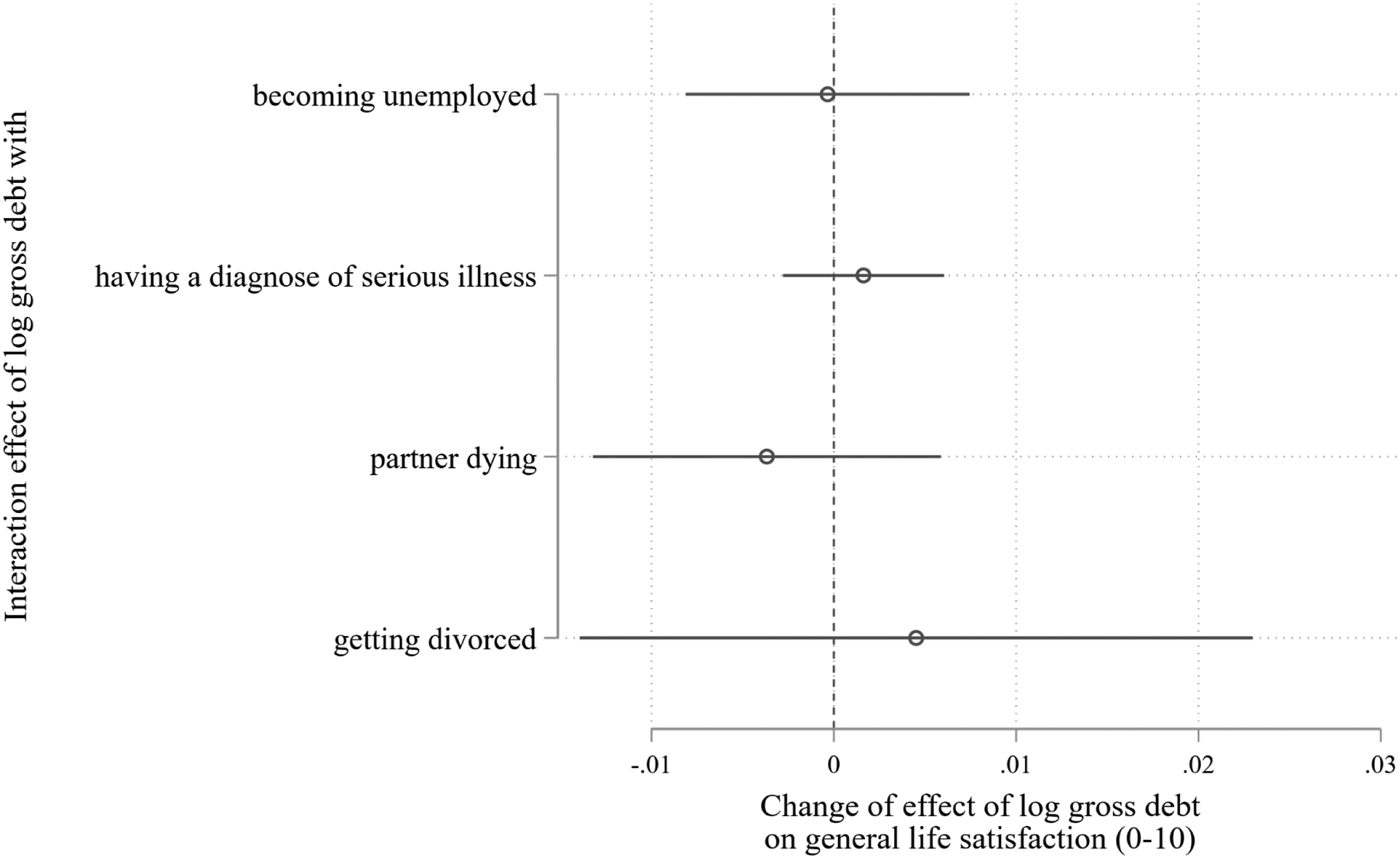

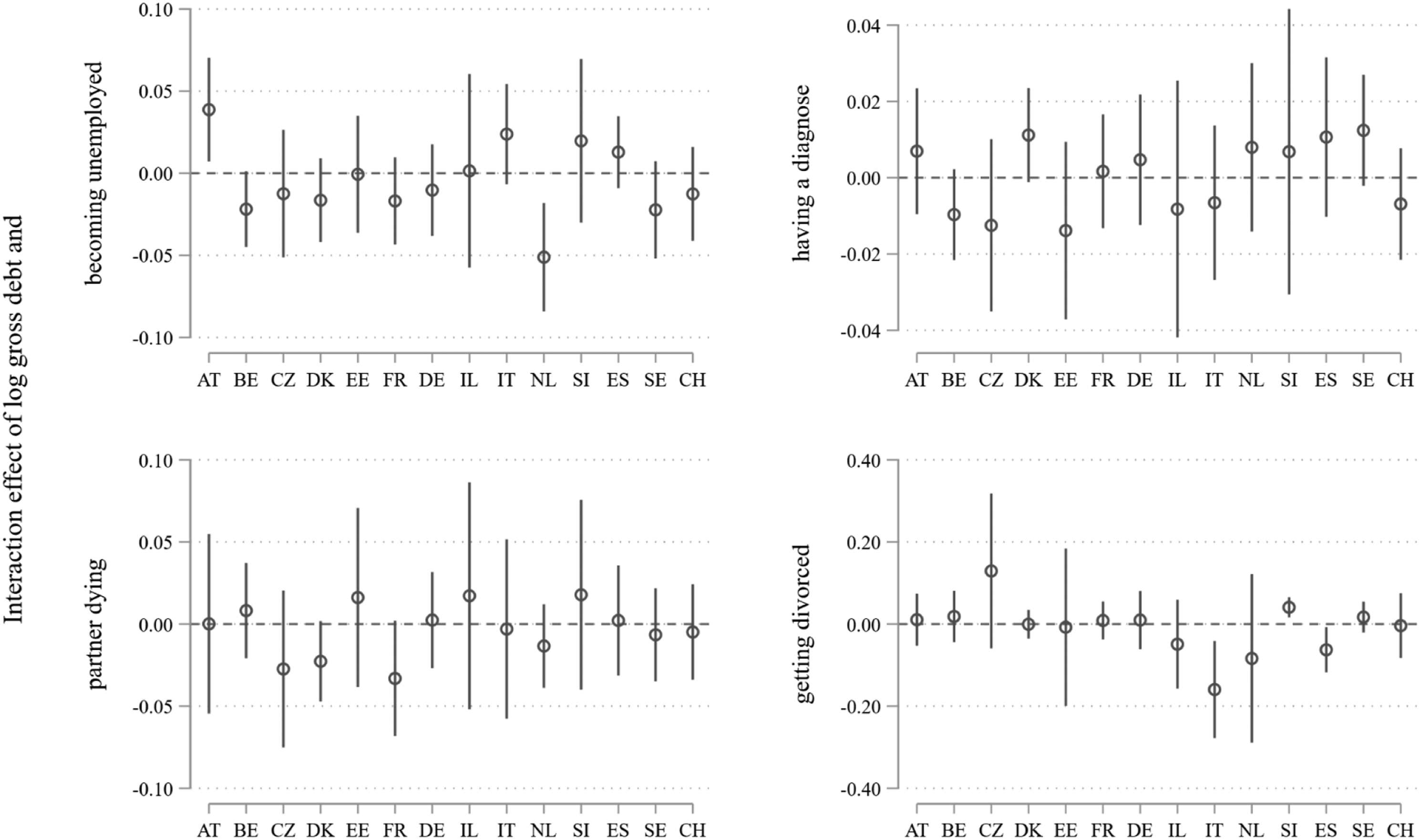

In hypothesis 1, we suggested that debt reinforces the negative relationship between negative life events and subjective wellbeing. We tested this expectation by running a fixed-effects regression of general life satisfaction on the negative life events moderated by gross debt and gross wealth with the control variables mentioned above. In Figure 1, we illustrated the average interaction effect of individual negative life events and gross debt among countries. The average interaction effects among all countries are close to zero and not statistically significant. Strictly speaking, we must therefore reject our first hypothesis. However, the average interaction effect says little about the debt moderation effects in the individual countries. In Figure 2, we thus illustrate the moderating effect of gross debt by country. Obviously, we find large variance in the moderating effects between countries. In about half of the countries of our sample, debt has–as expected–a negative moderation effect on the four negative life events we study. These moderations reach statistical significance for unemployment in the Netherlands and for divorce in Italy and Spain. Doubling debt reinforces the effect of becoming unemployed on subjective wellbeing by 0.05 standard deviations in the Netherlands. Doubling debt reinforces the effect of getting a divorce by 0.16 standard deviations in Italy and by 0.06 standard deviations in Spain. Especially for divorce and widowhood, many countries show a zero moderation effect of debt. For all four events, we also find some countries with positive debt moderation effects, especially for being diagnosed with a severe disease. The positive debt moderation reaches statistical significance for unemployment in Austria and for divorce in Estonia. Tables A3a and b in the Online Appendix contain our full regression results. Micro-level: Illustration of the average interaction effect of individual negative life events and gross debt among countries. Note: The dependent variable is general life satisfaction (0–10). According to our theoretical assumptions, we expected a negative interaction effect between negative life events and gross debt. Cluster-robust standards. Micro-level: Illustration of the moderating effect of gross debt by country (interaction effects of individual negative life events and gross debt). Note: The dependent variable is general life satisfaction (0–10). According to our theoretical assumptions, we expected a negative interaction effect between negative life events and gross debt.

As a robustness check, we estimated all models with financial debt (liabilities) separated from mortgage debt. Results from these models did not differ substantially from our joint measure of liabilities and mortgage, indicating that for households with at least one person aged 50+, relationships between debt, general life satisfaction, and negative life events do not depend on the type of debt (Tables A4a and b in the Online Appendix). This finding supports the appropriateness of using a joint debt measure in our main analyses (see, for example, Lewin-Epstein and Semyonov, 2016).

Macro-level interactions

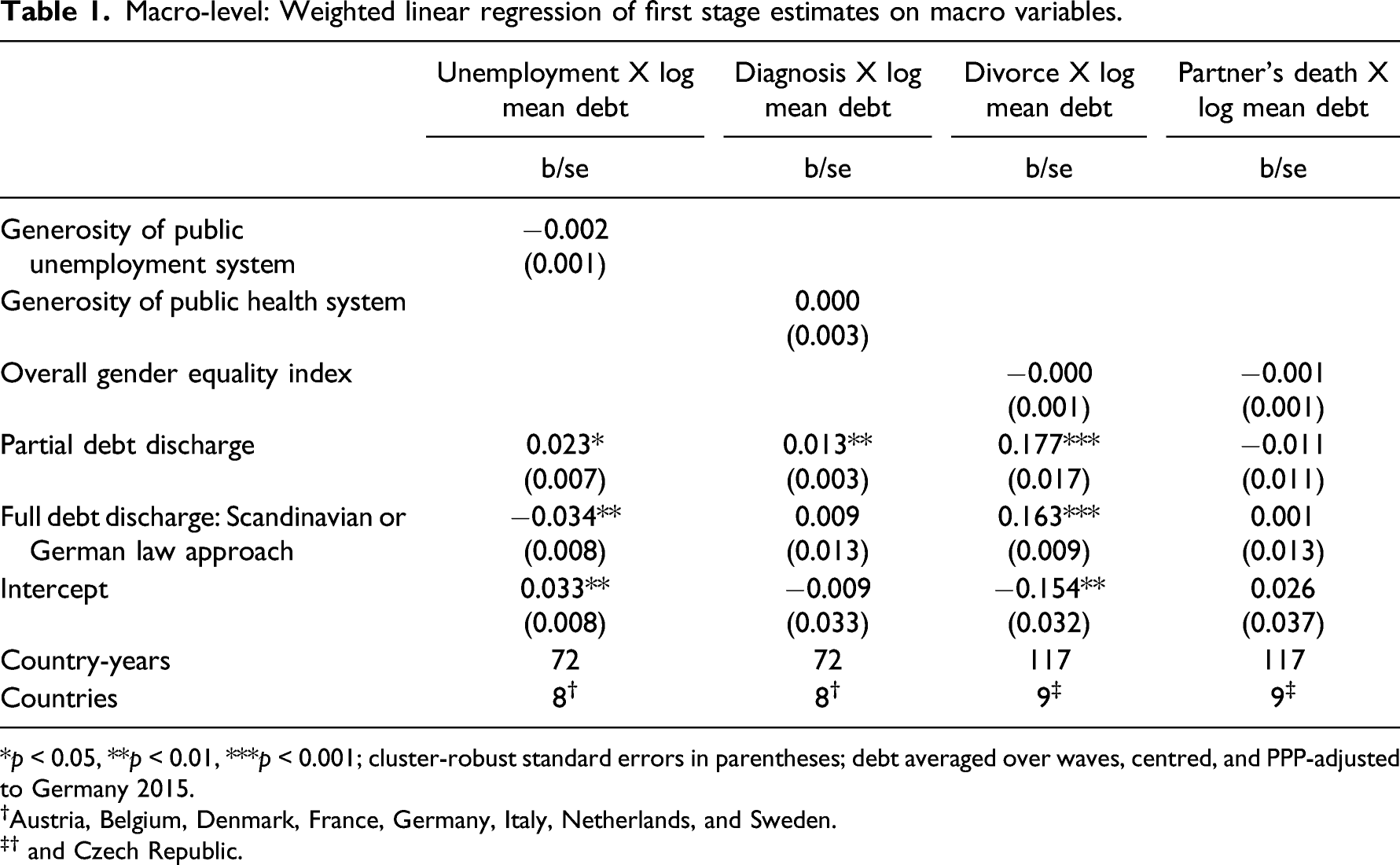

Macro-level: Weighted linear regression of first stage estimates on macro variables.

*p < 0.05, **p < 0.01, ***p < 0.001; cluster-robust standard errors in parentheses; debt averaged over waves, centred, and PPP-adjusted to Germany 2015.

†Austria, Belgium, Denmark, France, Germany, Italy, Netherlands, and Sweden.

‡† and Czech Republic.

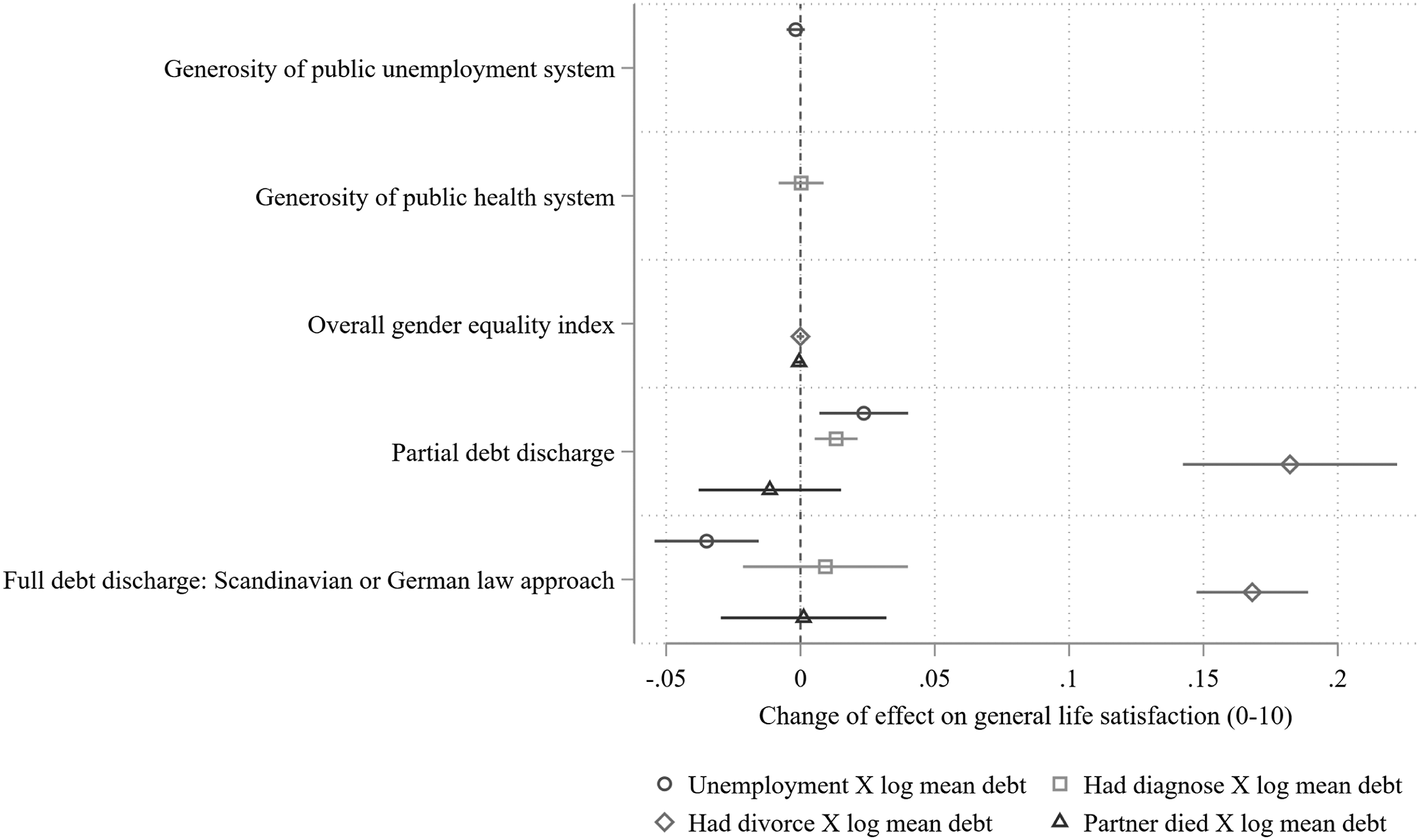

Macro-level: Illustration of the weighted linear regression of first stage estimates on macro variables. Note: The dependent variable is general life satisfaction (0–10). The reference category for the debt regime types is the type 1: no or very weak discharge.

In hypothesis 2, we expected a lower debt moderation for unemployment in countries with a more generous public unemployment system, and a lower debt moderation for being diagnosed with severe disease in countries with a more generous healthcare system. Our findings, as shown in Table 1, do not support our hypothesis. Effects of the generosity of the unemployment system on unemployment and the generosity of the healthcare policy on being diagnosed with severe disease are close to zero and not statistically significant. Our third hypothesis suggested a lower debt moderation for the events of divorce and partner’s death in countries with higher gender equality. Again, our findings do not support this hypothesis. The effects of gender equality on divorce and partner’s death are close to zero and not statistically significant.

Finally, in hypothesis 4, we suggested a weaker moderation of debt in countries with stronger debt relief for individuals. Comparing countries with no or very weak debt discharge to countries with partial debt discharge, we find that the moderation of debt in the relations between unemployment and general life satisfaction (b = 0.023), being diagnosed with a severe disease and general life satisfaction (b = 0.013), and especially between divorce and general life satisfaction (b = 0.177) are weakened in those countries with partial debt discharge. Looking at the contrast between countries with no or very weak debt discharge and countries with full debt discharge, results are less clear. As expected, in countries with full debt discharge, we find an attenuating moderation effect of debt for divorce (b = −0.163). Contradicting our expectations, we find the full debt-discharge regime to attenuate the debt moderation on unemployment (b = −0.034). This effect size, however, is very small as compared to the divorce effect.

Summary and discussion

Our study focused on the role of debt in shaping the negative relationship between negative life events and general life satisfaction. Our first aim was to establish debt as a moderator in the relationship between four negative life events–unemployment, severe disease, divorce, and partner’s death–and general life satisfaction. We hypothesized that debt reinforces the negative relationship between negative life events and general life satisfaction because being indebted is psychologically stressful and implies economic constraints. In other words, we expected indebtedness as an additional burden to negative life events in terms of life satisfaction.

While the average interaction effect over all countries was zero, we found ambivalent results between countries for the moderation of debt. While in some countries, indebted individuals who experienced a negative life event showed lower levels of life satisfaction, in other countries, such individuals showed no changes, or even higher levels of satisfaction with life. Overall, interaction effect sizes were small, indicating little differences in life satisfaction between households with different amounts of debt, who experienced negative life events. Going back to the theoretical discussion on the set-point theory, our findings show that negative life events can have a negative effect on general life satisfaction. Yet, in many countries, debt does not change the relationship between experiencing a negative life event and general life satisfaction. In line with Easterlin (2005), we see that unemployment as a reflection of an event with mostly pecuniary consequences has a weaker effect as compared to the family event of divorce.

In a second step, we tried to explain the variance in the micro-level moderation of debt, by looking at state-level policy measures that can assist individuals in coping with double burden circumstances in terms of debt and negative life events. We hypothesized that the reinforcing moderation effect of debt is weaker (1) for the events of unemployment and severe disease in countries where unemployment and healthcare policies are more generous, (2) for the events of divorce and partner’s death in countries where gender equality is higher, and (3) for all four negative life events in countries where more and faster ways of debt relief exist.

We did not find clear evidence for an effect of social welfare generosity and the level of gender equality either in the negative relationship between a negative life event and general life satisfaction nor in the moderation effect of debt on this relationship. This means that neither welfare state generosity nor the level of gender equality can explain the country differences in the moderation effect of debt on the relationship between negative life events and general life satisfaction. We did find that a county’s debt-discharge policy can reduce the negative effect of the interaction between debt and experiencing a negative life event, particularly in the case of divorce. When indebted individuals experience a divorce, easy ways to get out of debt seem to help them to cope with their reduced life satisfaction. An ad-hoc explanation for this finding might be that divorce in contrast to unemployment (unemployment insurance), death of the partner (widow pension), and being diagnosed with a severe disease (health insurance) has no direct protection or insurance policy at the institutional level, while at the same time divorce is usually related to a sudden decrease in household finances. Having debt and experiencing a divorce represents a double disadvantage for individuals in terms of their general life satisfaction, which can be relieved by a debtor-friendly law approach and reinforced by a strict or debtor-unfriendly law approach.

Our findings must be considered in the light of several shortcomings: first, the number of individuals who experience a negative life event is small. Second, in the SHARE, the measurement of divorce is prone to measurement error because of proactive dependent interviewing, which only measures reported changes. These error sources may decrease variance in our main independent variables, which would explain the large standard errors of our estimates. Third, our debt-discharge measure is not optimal because only one country in our sample belongs to the debt-discharge regime with weak or no discharge policies, namely, Italy. Moreover, our debt-discharge typology does not include information on how easy it is in different countries to take up loans. Finally, we did not analyse the actual individual mechanisms underlying the moderation effect of debt on the relationship between negative life events and general life satisfaction.

Summing up, our findings imply, on the one hand, that the individual mechanisms linking the experience of a negative life event to general life satisfaction are not relieved by welfare state policies. On the other hand, they show that countries can make a difference by supporting individuals who find themselves in a double disadvantage by being indebted and experiencing a negative life event. Installing mechanisms for debt relief may help indebted individuals cope with their double disadvantage of debt and experiencing a negative life event. However, the effectiveness of such measures seems to depend on the specific event type and country.

The policy instrument of debt relief might be very relevant also during the current COVID-19 pandemic and the economic recession emerging from it, acting as yet another burden. Individuals, especially entrepreneurs and self-employed people, are faced with a high risk of indebtedness or even insolvency. At the same time, individuals–especially those aged 50 years and older–are faced now with an even higher risk of experiencing all four of the negative life events we study. Supporting individuals who find themselves in such a triple disadvantage through laws granting easy debt relief might be more important now than ever (see DLA Piper, 2020 for changes in insolvency law in response to COVID-19).

Supplemental Material

sj-pdf-1-esp-10.1177_09589287211050505 – Supplemental Material for Double burden? Implications of indebtedness to general life satisfaction following negative life events in international comparison

Supplemental Material, sj-pdf-1-esp-10.1177_09589287211050505 for Double burden? Implications of indebtedness to general life satisfaction following negative life events in international comparison by Nora Müller, Klaus Pforr and Oshrat Hochman in Journal of European Social Policy

Supplemental Material

sj-pdf-2-esp-10.1177_09589287211050505 – Supplemental Material for Double burden? Implications of indebtedness to general life satisfaction following negative life events in international comparison

Supplemental Material, sj-pdf-2-esp-10.1177_09589287211050505 for Double burden? Implications of indebtedness to general life satisfaction following negative life events in international comparison by Nora Müller, Klaus Pforr and Oshrat Hochman in Journal of European Social Policy

Footnotes

Acknowledgments

We thank Ive Marx and Brian Nolan for editing this special issue on ‘Wealth and Social Policy’ and for their helpful comments on an earlier version of our article. We thank the two reviewers and the special issue super-referee for their great comments and suggestions. We thank Michael Gebel for sharing a modified version of the Stata ado edvreg, created by Jeffrey Lewis and modified by Eduardo Leoni.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Supplemental material

Supplemental material for this article is available online.

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.