Abstract

After a risky choice, decision makers must frequently wait out a delay period before the outcome of their choice becomes known. In contemporary sports-betting apps, decision makers can “cash out” of their bet during this delay period by accepting a discounted immediate payout. An important open question is how availability of a postchoice cash-out option alters choice. We investigated this question using a novel gambling task that incorporated a cash-out option during the delay between bet and outcome. Across two experiments (N = 240 adults, recruited via Prolific), cash-out availability increased participants’ bet amounts by up to 35%. Participants who were more likely to cash out when odds deteriorated were less likely to cash out when odds improved. Furthermore, the effect of cash-out availability on bet amounts was positively correlated with individual differences in cash-out propensity for bets with deteriorating odds only. These results suggest that cash-out availability may promote larger bets by allowing bettors to avoid losing their entire stake.

Introduction

A common feature of everyday decision making under risk is that, having taken a risk, a decision maker must wait for time to elapse before learning whether the risk has paid off (Pope, 1983). People who bet on a horse race, for instance, typically must wait for the race to finish before the bet is settled; similarly, purchasers of lottery tickets must wait for the lottery numbers to be drawn, and investors in a fledgling start-up company may have to wait years before seeing any return. People typically find delayed outcomes aversive (e.g., Benoît & Ok, 2007), particularly if they must wait in uncertainty (Luhmann et al., 2011; Tanovic et al., 2018; Wu, 1999), and tend to prefer gambles that resolve uncertainty earlier (Bennett et al., 2016; Cabrero et al., 2019; Chew & Epstein, 1989). 1 Accordingly, some risky-choice settings, such as sports-betting apps, cater to this preference by incorporating a cash-out feature into the delay between choice and outcome: While waiting for the outcome, the decision maker is given the option to cash out of an original choice by forgoing any future winnings in exchange for a discounted immediate payout (A. Brown & Yang, 2017; Grant et al., 2021).

The cash-out feature is a prominent and prevalent feature of contemporary sports-betting apps (Lopez-Gonzalez et al., 2019; Lopez-Gonzalez & Griffiths, 2017; Newall et al., 2021), where it is marketed as a way for gamblers to “take control of [their] bets” (Bet365, 2023). To illustrate, consider a bettor who has placed a bet on the home team to win a soccer match. During the match, the bettor will be offered the ability to cash out of this bet for an amount proportional to its current value. For instance, if the away team immediately scores a goal, the cash-out offer will reduce to less than the initial bet amount, and the bettor might be motivated to cash out in order to ensure against the loss of the entirety of the original stake (Killick & Griffiths, 2021). Conversely, if the home team then rallies to lead 2–1, the cash-out offer will increase to more than the initial bet amount, and the bettor may be tempted to cash out to lock in a profit. Cash-out is typically offered at a discounted proportion of the true bet value, thereby ensuring a built-in profit margin for bookmakers on decisions to cash out (e.g., a bet with a current estimated value of $7 might have a corresponding cash-out offer of only $5; see worked example in the Supplemental Material available online, Section S1). This built-in margin increases the expected loss for bettors who use the cash-out offer frequently, which suggests that the cash-out feature may be a source of increased risk for gambling-related harm. Indeed, people who experience gambling-related harm report using the cash-out feature more frequently than those with less experience of gambling-related harm (Lopez-Gonzalez et al., 2019).

From a theoretical standpoint, postchoice cash-out availability means that decision makers are faced with two successive decisions: an initial risky choice followed by a subsequent choice about whether to cash out. Therefore, one way of conceptualizing risky choice with cash-out availability is as a kind of sequential risky decision-making (e.g., Fontanesi et al., 2022; Pleskac, 2008). However, standard laboratory paradigms for studying sequential risky decision-making (e.g., the Columbia Card Task, Figner et al., 2009; the Balloon Analogue Risk Task, Lejuez et al., 2002; the Devil Task, Slovic, 1966) differ from cash-out decisions because these tasks involve risks that always increase the longer a decision maker chooses to play. This is not the case in risky choice with cash-out availability, because the final outcome of a bet tends to become more predictable over time (e.g., the outcome of a soccer match becomes increasingly certain as the match goes on), and therefore less risky. 2 Separately, choices that share some features with the decision to accept or reject a cash-out offer also occur in the game show “Deal or No Deal,” where they have been analyzed as exemplars of real-world, high-stakes risky decision-making (Chen & John, 2018; Deck et al., 2008; Post et al., 2008). In this setting, the decision to take a deal may be similar to the decision to accept a cash-out offer in a sports-betting app; even so, however, analyses of “Deal or No Deal” choice data focus only on the second part of the choice sequence described above (the cash-out decision), without an initial risky-choice component. Deal or No Deal also takes place entirely in the gain domain because even a single dollar of prize money represents a profit relative to participants’ pre-game wealth; this is different from cash-out in sports betting, in which bettors who treat their initial bet as an investment in the future outcome of a match may be motivated to cash out by the aversive prospect of losing their stake.

Statement of Relevance

The past decade has seen a meteoric rise in the availability and use of gambling websites and smartphone apps. One notable novel product offered to users of these platforms is instant cash-out, which gives a bettor the option to “cash out” of a bet prior to its outcome in exchange for a discounted immediate payout. Instant cash-out is widely available across betting apps and websites and is marketed as a way for users to take control of their bets. However, the effects of its availability on betting behavior have not previously been studied. Here, across two experiments using a controlled experimental gambling task, we found that participants placed bets that were up to 35% larger when they knew they would be able to cash out of their bet prior to its conclusion. This finding suggests that cash-out availability may produce meaningful shifts in patterns of user engagement with gambling products.

In the present study, we investigated both phases of the cash-out decision. Our particular focus was on whether availability of a postchoice cash-out option would alter individuals’ initial risky choice. We reasoned that postchoice cash-out availability might increase risk taking in the initial choice phase (e.g., by increasing perceived control over the final outcome of the bet; Adkins & Paxson, 2017; Shaanan, 2005; Strickland et al., 1966). To date, the psychological literature has not considered how the availability of a postchoice cash-out option might influence initial choice behavior in decision-making under risk (although see Matthews et al., 2023, and Van Winden et al., 2011, for discussion of how other properties of the postchoice delay period influence the initial choice). To address this question, we developed a controlled card-betting task that incorporated both an initial risky choice (deciding how much to bet on the outcome of a random card draw) and a postchoice accept-or-reject cash-out offer. We then manipulated the availability of the cash-out option in two general-population online samples completing the task (Experiment 1: within-participants manipulation; Experiment 2: between-participants manipulation) to determine how cash-out availability altered participants’ betting behavior. We also collected data on participants’ self-reported experience of gambling-related harm to determine whether this moderated any of the observed effects of cash-out availability on behavior. In addition, our task design also allowed us to test how participants’ propensity to cash out varied as a function of four gamble-level factors: the value of the cash-out offer, the probability of winning, the ambiguity of this probability, and the time during the delay period when the cash-out offer was made. In a real-world betting context, these factors would correspond to features of a bet such as the size of the cut taken by bookmakers on cash-out offers, the probability that a bet will pay out, and the time during the event when the decision to cash out is made.

Method

Open practices statement

All data analyzed in this study, along with the preregistration document for Experiment 2, are publicly available in an Open Science Framework repository at https://osf.io/as8pw/. Except where otherwise specified, data-collection procedures and all analyses were preregistered for Experiment 2.

Design

Experiments 1 and 2 used the same behavioral task (the card-betting task) and manipulation of cash-out availability, but differed in their study design: Experiment 1 used a within-participants design (cash-out was available in half of all trials, and unavailable in the other half), whereas Experiment 2 used a between-participants design (participants were randomly allocated either to a group in which cash-out was available in all trials or a group in which cash-out was never available).

Because Experiments 1 and 2 used a very similar method, we describe the method for both experiments together below and then separately note the minor design modifications (and our rationale for these modifications) that were made between Experiments 1 and 2.

Participants

Participants in both experiments were adults recruited via the website Prolific (Experiment 1: N = 60; Experiment 2: N = 180). After applying exclusion criteria (see below), the Experiment 1 sample comprised 52 participants aged 20 to 65 (M = 39.9 years; 20 men, 30 women, 2 who did not indicate a binary gender), consisting of 12 participants from Australia, 12 from Canada, 6 from New Zealand, 17 from the United Kingdom, and 5 from the United States. In Experiment 2, the final sample after exclusions comprised 167 participants aged 18 to 65 (M = 36.3 years; 81 men, 83 women, 3 who did not indicate a binary gender), consisting of 46 participants from Australia, 37 from Canada, 7 from New Zealand, 55 from the United Kingdom, and 22 from the United States. Participants were eligible to participate if they had an account on Prolific with at least one previous study completion, had no vision impairment, could speak and read English, and resided in one of the countries mentioned above. Participants from Experiment 1 were excluded from participation in Experiment 2.

In Experiment 1, all 52 participants completed both cash-out-available trials and cash-out-unavailable trials of the card-betting task in a randomized order. In Experiment 2, participants were randomly allocated either to a group who completed the card-betting task with cash-out available in all trials (N = 80) or to a group for whom cash-out was never available (N = 87). Total time commitment in both experiments was approximately 30 min, and participants were compensated with a base payment of AUD$8 plus a performance bonus up to $2, depending on their winnings in the behavioral task (Experiment 1: M = $0.78; Experiment 2: M = $0.88).

Both experiments were approved by the Monash University Human Research Ethics Committee (#36452), all participants provided informed consent via a web-browser form, and all research was conducted in accordance with the 1964 Declaration of Helsinki. The sample size for Experiment 2 was selected according to a simulation-based bootstrap power analysis so as to give in excess of 95% power to detect a between-participants effect size estimated from permuted data from Experiment 1 (estimated between-participants Cohen’s d = 0.63).

Materials and procedure

All study components were presented to participants in their web browser using custom code written in JavaScript using the jsPsych package (Version 7.3.1; De Leeuw, 2015) and Python server code (Version 3.7.10) written using the Flask web framework (Version 1.1.2) and hosted on a Monash University virtual machine. All experiment code is available via the project Open Science Framework (OSF) repository.

Questionnaires

Before completing the card-betting task, participants first completed a short demographic questionnaire (assessing age, gender, country of residence, and education level) and the Problem Gambling Severity Index (PGSI; Ferris & Wynne, 2001) as an indicator of gambling severity and experience of gambling-related harm.

Card-betting task

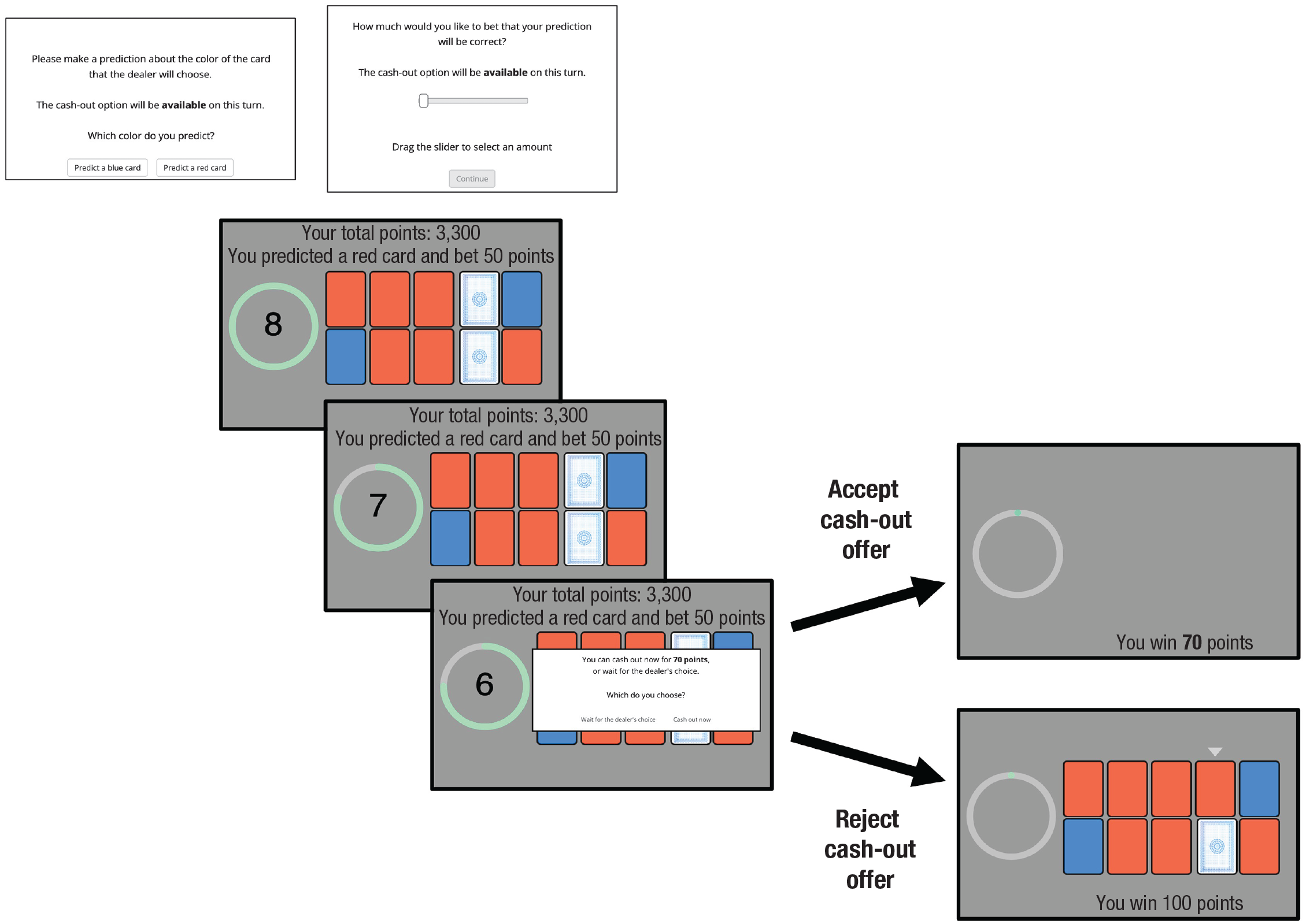

The card-betting task was designed as a modification of a prototype task previously reported by Bennett (2022) and was presented as a card game in which different cards were randomly selected by a fictitious “dealer” (see the project’s OSF repository for the exact instructions delivered to participants). In each trial of the task, participants made a prediction about the outcome of an uncertain future event, namely whether a single card randomly selected from an as-yet-invisible array of 10 cards would be red or blue. After predicting red or blue, the participant then chose how many points (the bet amount) to wager on their prediction. At this point, participants were shown for the first time an array of 10 cards (see Fig. 1), which were a mixture of face-up cards (red and blue) and face-down cards (color unknown). Participants were told that cards were drawn from a deck with equal numbers of red and blue cards (i.e., they were equally likely to be red or blue), and participants were explicitly instructed that the colors of face-down cards were independent of the colors of face-up cards. Participants clicked on a countdown timer using the mouse to initiate an 8-s delay period, 3 at the end of which a card was randomly selected from the array. If the card selected was face down, it was turned over so that participants could see its color. If the color of the selected card matched participants’ predictions, they won back double their bet amount; if their prediction was incorrect, they lost their stake.

Task schematic for the card-betting task. Prior to seeing the card array, participants first made a prediction as to whether a computerized dealer would randomly choose a red card or a blue card and staked a number of points on whether their prediction would be correct (range in Experiment 1: 5 to 50 points; Experiment 2: 5 to 100 points). Participants were then shown the card array and a countdown timer that indicated the length of the delay until the random selection of a card by a “dealer.” In trials in which cash-out was available, participants were given one opportunity to cash out of their bet during the delay prior to the selection of a card. No matter their choice, participants had to wait for the delay period to elapse before moving on to the next trial. In trials in which cash-out was not available (not shown), participants simply received an outcome depending on the accuracy of their prediction at the end of the delay period.

Trials varied in terms of whether cash-out was available or unavailable during the delay period prior to the selection of a card. In trials for which cash-out was available, participants were given one opportunity per delay period to cash out of their wager in exchange for an immediate payout of points (the cash-out offer). The offer amount was calculated by computing the expected value of the participant’s bet on the basis of the visible array of cards and offering either 80%, 90%, or 100% of this expected value (rounded to the nearest point) as a cash-out offer. If the participants accepted this cash-out offer, they received the number of points in the offer immediately, and the card array was hidden for the remainder of the delay period (thereby ensuring that participants could not reduce the overall duration of the task by choosing to cash out repeatedly). If the participants rejected the cash-out offer, the countdown resumed, and they received an outcome determined by the accuracy of their prediction about the selected card. In trials for which cash-out was unavailable, participants simply waited until the end of the delay period to learn whether their prediction was correct or incorrect. As described above, cash-out availability was manipulated in a within-participants design in Experiment 1 and in a between-participants design in Experiment 2.

Each participant completed four blocks of the card-betting task in total (Experiment 1: 20 trials per block; Experiment 2: 18 trials per block). These trials differed from one another according to four factors: (a) the probability of winning the bet, (b) the amount of ambiguity concerning this probability, (c) the value of the cash-out offer relative to the expected value of the participant’s bet (on cash-out-available trials only), and (d) the time point during the delay period at which the cash-out offer was made.

a. Pr(win): probability of winning the bet. Trials varied in the probability that the participant’s prediction would be correct upon seeing the card array (30%, 50%, or 70% probability of being correct, each approximately one third of trials). This manipulation was implemented by preallocating the card array in each trial so that the display of cards was consistent with either a 30%, 50%, or 70% probability of a blue card being randomly selected (taking into account that face-down cards were equally likely to be red or blue, as described above). Selection of cards on each trial was randomized using the JavaScript random number generator in the web browser. From the participants’ perspective, because the card array was not visible at the point in time when they made their bet, there was a 50% a priori probability of a blue card being chosen; as a consequence, participants were not able to gain any advantage by consistently predicting blue or red cards.

b. Amount of ambiguity. Ambiguity was manipulated by varying the number of face-down cards in the card array. Trials could be either low ambiguity (eight cards presented face up, two cards face down, as in Fig. 1) or high ambiguity (four cards face up, six cards face down). More information on the numbers of visible cards of each color for each combination of Pr(win) and ambiguity can be found in the Supplemental Material (Section S2).

c. Value of the cash-out offer. During the delay period, we calculated the true expected value (EV) of the bet as a function of its probability of paying out and the participant’s bet amount (

d. Cash-out offer time. The cash-out offer was made after either 2, 4, or 6 s of the 8-s delay period.

Different trial types were presented in a randomized order across participants, and the arrangement of the cards within the 10-card array was randomly determined on each trial. In both experiments, participants began with a one-time initial endowment of points with which to bet (Experiment 1: 3,000 points; Experiment 2: 3,600 points). At the end of the task, participants traded their final balance of points for a monetary bonus payment at a conversion rate of AUD$1 per 4,000 points. Participants were informed of this conversion rate before starting the task. In Experiment 1, participants could bet between 5 and 50 points on each of the 80 trials; in Experiment 2, participants could bet between 5 and 100 points on each of the 72 trials (see below for details and for the rationale regarding differences in method between Experiment 1 and Experiment 2).

Attention-check trials

In Experiment 1, eight trials (10% of total) were designated as attention-check trials. These trials were designed to ensure that participants were engaging adequately with the cash-out feature of the card-betting task rather than behaving at random when a cash-out offer was made. There were four attention-check trials in which a cash-out offer of 0 points was made (in which case the correct answer is always to reject the cash-out offer, regardless of the cards in the array), and four in which a cash-out offer of 100 points was made (in which case the correct answer is always to accept the offer). Attention-check trials were otherwise visually similar to the remaining 72 trials of the task and were pseudorandomly distributed within the running order of the task. Inattentive responding on attention-check trials was used as an exclusion criterion; see below for further details.

Modifications to method for Experiment 2

Although we sought to keep the basic design of the task as similar as practicable between Experiment 1 and Experiment 2, there were some minor differences between the two tasks. First, experiments differed in terms of how participants were provided information about the availability of the cash-out offer on each trial. In Experiment 1, because cash-out availability was manipulated trial by trial on a within-participants basis, information about cash-out availability was provided to participants at the start of each trial, thus ensuring that participants had access to this information at the point of placing a bet (see the Supplemental Material, Section S3, for the exact text as viewed by participants in each experiment). Although this mode of presentation is consistent with the way that cash-out availability is presented to gambling-app users, we reasoned that this may have been likely to induce demand effects by emphasizing the availability of cash-out at the point of making a bet. In Experiment 2, therefore, cash-out availability was manipulated on a between-participants basis so that all trials for a given participant were within the same condition, and no information statement about cash-out availability was provided on the prediction or bet screens. Indeed, for participants in the cash-out-unavailable group in Experiment 2, no mention of a cash-out feature was made anywhere in the task or instructions, and participants were not made aware that other participants were completing a similar version of the task with cash-out available. In addition, because the attention-check trials embedded in the task in Experiment 1 depended on participants’ advantageous use of the cash-out feature, we did away with the behavioral attention-check trials for all participants in Experiment 2 (while retaining survey-based attention checks; see below). This reduced the overall number of trials per participant to 72 trials in Experiment 2 (from 80 trials in Experiment 1); these 72 trials were identical to the 72 non-attention-check trials in Experiment 1.

We also made several minor design modifications to Experiment 2 that were informed by the results of Experiment 1. After observing that a number of participants in Experiment 1 showed ceiling effects in their bet amounts, we increased the upper limit of possible bet amounts from 50 points in Experiment 1 to 100 points in Experiment 2. To take this increased bet limit into account, we also gave participants a greater initial point endowment in Experiment 2 (3,600 points) compared with Experiment 1 (3,000 points). In addition, because we reasoned that cash-out offers within real-world betting apps are offered only at disadvantageous amounts because of bookmaker fees, we reduced the possible values of cash-out offers from 90% and 100% in Experiment 1 to 80% and 90% of the bet expected value in Experiment 2 to increase the ecological validity of the task.

Finally, to allow for exploratory analyses in the service of future hypothesis generation, participants in Experiment 2 also completed a brief posttask debriefing survey in which they used a five-point Likert scale (anchors: not at all, moderately, extremely) to rate the extent to which they felt various emotions (boredom, curiosity, stress, feelings of control, etc.) during both the betting phases of the task and the delay phases prior to observing an outcome. More details on this survey can be found in the Supplemental Material (Section S7).

Exclusion criteria

We sought to exclude participants who did not adequately engage with the experiment. In Experiment 1, participants were excluded from all further analysis if (a) they responded inaccurately to more than one of the attention-check trials embedded in the behavioral task, (b) they gave a logically impossible answer to an infrequency-item attention check embedded in the PGSI survey (i.e., an item for which there is a clear correct answer if participants are responding attentively to the survey; see Zorowitz et al., 2023), or (c) they reported experiencing a major technical issue during the task in the course of a postexperiment debriefing survey. In Experiment 2, we applied exclusion criteria (b) and (c), but we also excluded participants if (d) they self-reported not having engaged seriously with the task during the debriefing or if (e) they disclosed a country of residence that was not consistent with their reported country of residence on Prolific. All exclusion criteria for Experiment 2 were preregistered with the exception of (e), which was added post hoc upon inspection of participant demographics.

Data analysis

The card-betting task yields two dependent variables of primary interest: first, the amount that participants bet on the accuracy of their prediction prior to seeing the card array (the initial risky choice); second, in cash-out-available trials, the cash-out decision (i.e., whether or not participants chose to cash out).

Our first research question was whether the availability of a cash-out option altered participants’ bet amounts. To answer this question, we first computed the mean bet amount for each participant (and for each condition, in the within-participants Experiment 1 design) and compared mean amounts between bets for which cash-out was available and bets for which cash-out was unavailable. For Experiment 1, we found that residuals for a linear model of mean bet amounts across participants were normally distributed (according to visual inspection and a nonsignificant Shapiro-Wilk test), and we therefore analyzed data using a paired-samples t test. For Experiment 2, we found that residuals for a linear model of mean bet amounts across participants were not normally distributed (according to visual inspection and a significant Shapiro-Wilk test), and we therefore analyzed data using a nonparametric Wilcoxon rank-sum test.

Our second research question was how participants’ propensity to cash out varied as a function of different features of the card array and the cash-out offer value. We analyzed cash-out choices using a mixed-effects logistic regression analysis with cash-out offer acceptance as the dependent variable (offer rejected = 0, offer accepted = 1) and Pr(win), ambiguity, and cash-out offer value as independent variables. We selected random effects using a maximal to minimal-that-converges approach (Barr et al., 2013). Data were analyzed using the lme4 package in R, and the statistical significance of test statistics for mixed-effects analyses was calculated using type-III Wald tests as implemented in the car package in R. R code for all analyses presented in this manuscript is available in the project’s OSF repository, and a full description of the mixed-effects structure of regression models is available in the Supplemental Material (Section S4). For analyses of cash-out propensity, final regression models included random intercepts for all participants and random slopes for cash-out offer value, Pr(win) (linear), and Pr(win) (quadratic). Other random slopes (including the main effect of ambiguity, the main effect of cash-out offer time, and all two-way interactions) were excluded because their inclusion led to nonconvergence of regression models.

Results

Bet amount

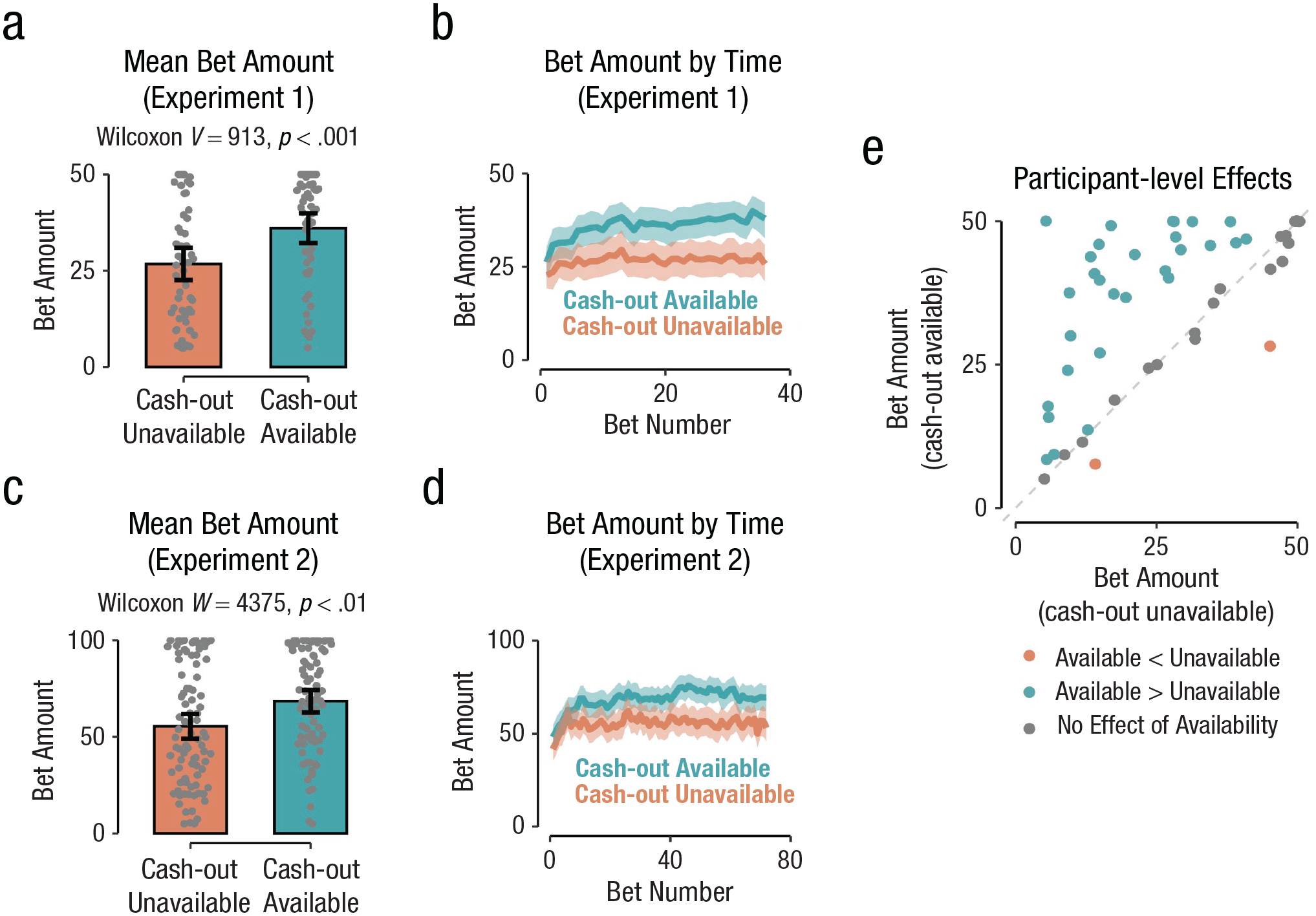

Our primary research question was whether the subsequent availability of a cash-out option altered participants’ initial betting behavior. We found strong evidence in support of this proposition: Participants placed significantly larger bets on the card-betting task when cash-out was available, both in the within-participants Experiment 1, t(51) = 5.38, p < .001, paired-samples t test (Fig. 1a), and in the between-participants Experiment 2, W = 4,375, p = .004, Wilcoxon rank-sum test (Fig. 1c). The effect size of cash-out availability was moderate to large: in Experiment 1, participants made bets that were 34.8% larger when cash-out was available (mean bet amount of 36.0 vs. 26.7 points; bootstrapped 95% confidence interval, or CI = [20.5%, 52.3%], within-participant Cohen’s d = 0.75). 4 Likewise, in Experiment 2, participants for whom cash-out was available placed bets that were 23.6% larger than participants for whom it was unavailable (mean bets of 68.5 vs. 55.4 points; bootstrapped 95% CI = [7.4%, 43.1%], between-groups Cohen’s d = 0.46). Furthermore, in the within-participants design of Experiment 1, there was evidence that this effect was also prevalent at an individual-participant level: Participant-level permutation tests revealed that even when participants were considered individually, a majority of the sample showed significant increases in bet amount when cash-out was available (29 of 52 participants, or 55.8% of the sample; see Fig. 2e). This indicates that the effect of cash-out availability on bet amounts was meaningful at the individual-participant level, not merely in aggregate at the group level.

The effect of cash-out availability on bet amount. On average, participants made larger bets when cash-out was available than when it was not available. Experiment 1 is shown in (a); Experiment 2 is shown in (c). This effect was initially smaller but increased in magnitude over time, as illustrated in (b) for Experiment 1 and (d) for Experiment 2. Plots depict mean group-level mean bet amounts; error bars (a,c) and shaded regions (b,d) represent the 95% confidence interval of the mean; gray points in (a) and (c) depict condition means for individual participants. In (e) are shown participant-level effects of cash-out availability on bet amount in Experiment 1 (within-participants design). Scatterpoints represent participant-wise mean bet amounts in trials for which cash-out was available (y-axis) and unavailable (x-axis). Points above the dashed diagonal represent participants who bet more when cash-out was available than when it was unavailable. Points are colored according to the significance of participant-wise permutation tests of the effect of cash-out availability on bet amount.

Notably, the effects of cash-out availability on bet amount were observed despite ceiling effects on participants’ bet amounts in both experiments (see Figs. 2a and 2c). Ceiling effects were particularly pronounced in Experiment 2 despite an increase in the maximum allowable bet amount in this study, suggesting that participants adapted their bets to match the range of available bet amounts. Nevertheless, the effect of cash-out-availability on bet amount remained significant even when excluding participants who consistently bet the maximum—Experiment 1: t(46) = 5.54, p < .001, paired-samples t test; Experiment 2: W = 3,619, p = .01, Wilcoxon rank-sum test—giving us confidence that the results reported above were not confounded by ceiling effects on bet amount.

We next conducted several exploratory mixed-effects regression analyses to unpack these effects further. These analyses indicated that there was a significant effect of time on task on bet amount in both experiments (Figs. 2b and 2d): Participants tended to make larger bets as time went on—Experiment 1:

Finally, we tested whether results were moderated by individual differences in the severity of problem-gambling symptoms. This analysis revealed a significant interaction between PGSI score and the effect of cash-out availability in Experiment 2,

Cash-out frequency

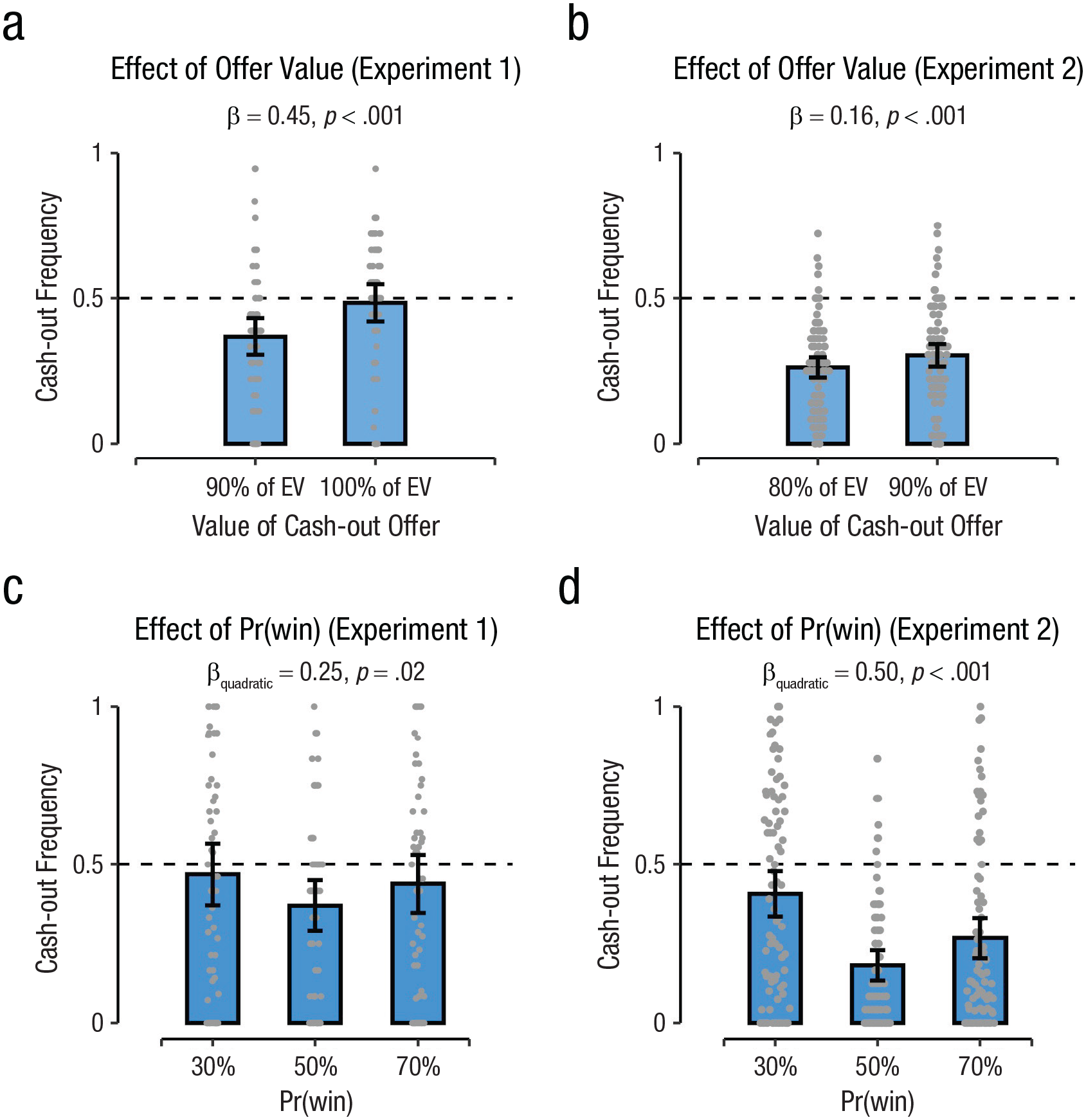

We next investigated the effects of trial-level factors on participants’ willingness to accept a cash-out offer. A mixed-effects logistic regression analysis revealed a significant main effect of the value of the cash-out offer on cash-out propensity. As expected, participants were more likely to accept cash-out offers that were more generous (relative to the expected value of their bet) in both Experiment 1,

Participants’ willingness to accept a cash-out offer. Willingness varied as a function of its value relative to the expected value (EV) of the bet. Participants in both Experiment 1and Experiment 2—see (a) and (b), respectively—were more likely to accept more generous cash-out offers. Participants’ willingness to accept a cash-out offer also varied significantly as a quadratic function of the likelihood of their bet paying off, as shown in (c) for Experiment 1 and (d) for Experiment 2. Plots depict group-mean cash-out frequencies plus or minus the 95% confidence interval of the mean; gray points depict condition means for individual participants. Pr(win) = probability of winning the bet.

We assessed both linear and quadratic effects of the probability of winning the bet, Pr(win), on the likelihood of accepting the cash-out offer. In both experiments, we found evidence for a positive quadratic effect of Pr(win)—Experiment 1:

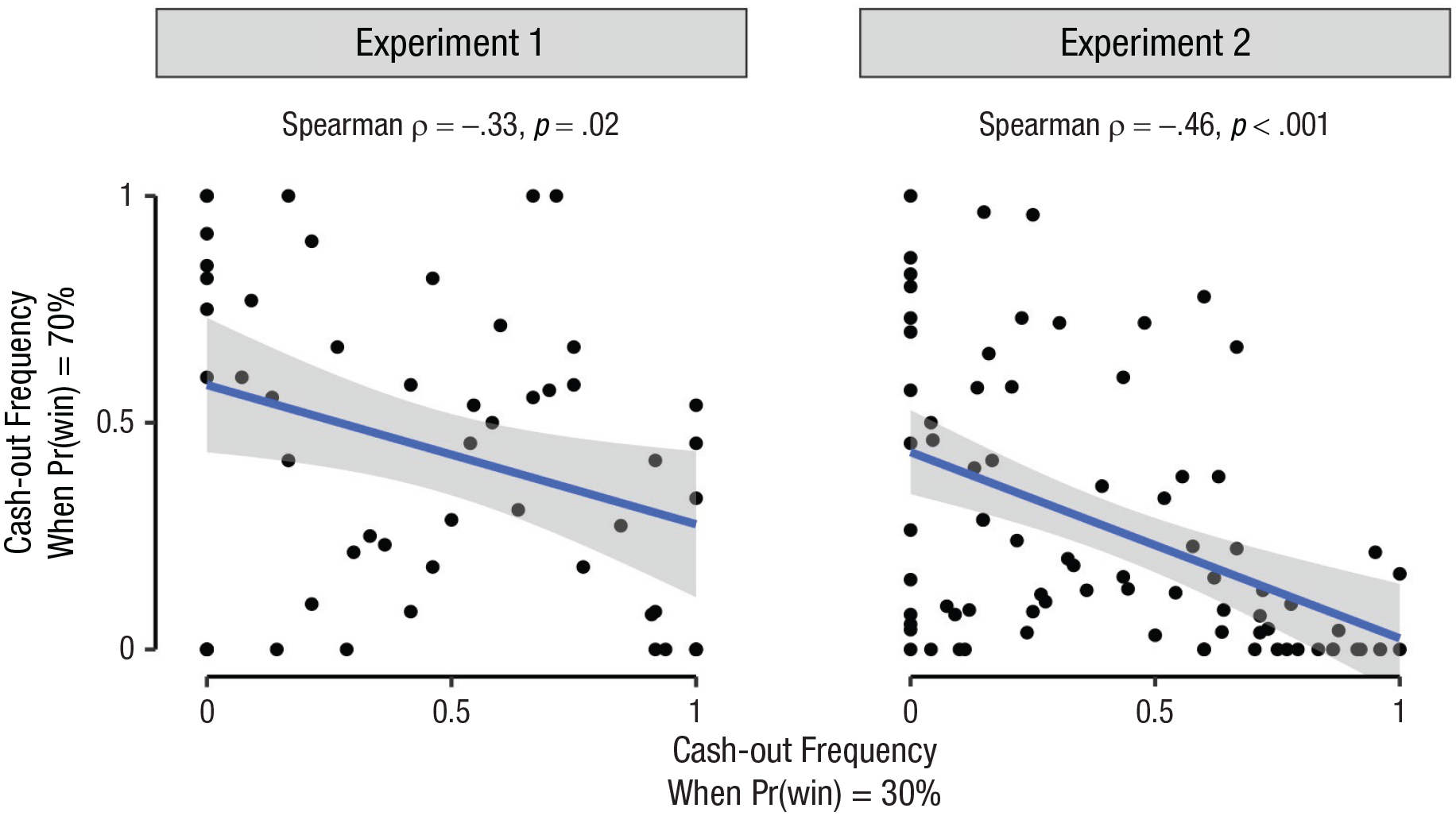

Cash-out frequency in Experiment 1 and Experiment 2. In both experiments, there was a significant negative correlation between participants’ willingness to cash out of bets that were likely to pay off and their willingness to cash out of bets that were unlikely to pay off. The x-axis shows the cash-out frequency on trials with a 70% chance of winning the bet; the y-axis shows the cash-out frequency on trials with a 30% chance of winning the bet. Points represent bivariate condition means for individual participants; overlaid regression lines depict the line of best fit and its 95% confidence interval (gray shaded region). Pr(win) = probability of winning the bet.

There was no main effect of ambiguity on cash-out propensity—Experiment 1:

We also conducted several exploratory analyses investigating whether participants’ PGSI scores moderated any of the observed effects. These analyses provided evidence (albeit at a trend level in Experiment 1) for an interaction between PGSI score and cash-out offer value—Experiment 1:

Finally, motivated by the substantial individual differences that we observed in the effect of Pr(win) on cash-out propensity, we conducted several exploratory analyses to investigate the consistency of cash-out behavior across different Pr(win) conditions. To our surprise, in both experiments we found a significant negative correlation between participants’ propensity to cash out when Pr(win) was 30% and their propensity to cash out when Pr(win) was 70% (see Fig. 4)—Experiment 1: Spearman ρ(50) = −.33, p = .02; Experiment 2: Spearman ρ(85) = −.46, p < .001 (full correlation matrices may be found in the Supplemental Material, Section S6). In other words, participants who were more likely to cash out of bets with improving odds, Pr(win) = 70%, were less likely to cash out of bets with worsening odds, Pr(win) = 30%.

This heterogeneity strongly suggests that different participants adopted different strategies for using the cash-out option in different task conditions—for example, avoiding losses when Pr(win) = 30%, and locking in gains when Pr(win) = 70%. Moreover, the within-participants design of Experiment 1 meant that in this experiment we were able to investigate how individual differences in cash-out propensity across the different Pr(win) conditions was associated with individual differences in the effect of cash-out availability on behavior. This analysis revealed that the effect of cash-out availability on bet amount (defined as the difference between a participant’s mean bet amount when cash-out was available vs. when it was unavailable) was positively associated with cash-out propensity when Pr(win) was 30% (Spearman ρ = .39, p = .004; Figure S4a), but not when Pr(win) was 50% (Spearman ρ = .0003, p = .99; Figure S4b) or 70% (Spearman ρ = −.06, p = .66; Figure S4c). In other words, the effect of cash-out availability on bet amount was strongest for participants whose behavior suggested that they were cashing out as a way of avoiding prospective losses. It is important to note, however, that our results do not conclusively identify loss aversion as the sole factor driving results, and further research would be required to dissect the relative contributions of different cognitive mechanisms (e.g., delay aversion, intolerance of uncertainty, loss aversion) to individuals’ decisions to cash out of their bets.

Exploratory analyses of emotion ratings

We conducted a posttask debriefing survey in Experiment 2 to explore participants’ subjective experience of the card-betting task. Analysis of survey data revealed a positive correlation between cash-out frequency and perceived control during the betting phase of the task, Spearman

Discussion

Some risky-choice settings (most notably contemporary sports-betting apps) offer a cash-out option to individuals who are waiting to learn the outcome of a previous risky choice. In the present study, we investigated how individuals’ risk preferences were influenced by the availability of this postchoice cash-out option. To do so, we developed a controlled behavioral task that allowed us to investigate the effect of cash-out availability on the prior risky choice, while also identifying features of the postchoice waiting period that influenced the likelihood of using the cash-out feature when it was offered. Across two experiments, we consistently found that the availability of a postchoice cash-out option increased the amount that participants were willing to bet on the outcome of an unpredictable future event. This was the case both when cash-out availability was manipulated within participants (Experiment 1; 35% increase in mean bet size on trials in which cash-out was available) and in the preregistered between-participants design of Experiment 2 (24% increase in mean bet size in participants for whom cash-out was available).

Our results showed that the availability of a postchoice cash-out option affected the amount of economic risk participants were willing to incur in the initial choice phase. This result held even when (as in Experiment 2) cash-out offers were systematically undervalued relative to bets’ true expected value. One possible explanation for this finding is that by encouraging participants to perceive the initial bet as partially reversible, cash-out availability may have increased participants’ perceived control over the outcomes of their bet (Adkins & Paxson, 2017; Shaanan, 2005), in line with the tendency for increased risk tolerance when decision-makers have greater perceived control over the outcomes of their bets (e.g., Davis et al., 2000; Strickland et al., 1966). Consistent with this explanation, exploratory analyses of subjective emotion-rating data collected in Experiment 2 revealed that participants who cashed out more frequently tended to rate themselves as feeling more in control during the betting phase of the task.

Cash-out availability also changed the profile of participants’ bets in two other ways. First, in both experiments, bet amounts increased more rapidly over time for trials in which cash-out was available. This is surprising, as one could expect that participants would correct their betting amount to reflect the undervalued cash-out offers. Yet the opposite was true, which could indicate that our participants were chasing losses incurred in the early stages of the experiment. Second, in Experiment 2 the effect of cash-out availability on bet amount was moderated by PGSI scores. Taken together, these results indicate that the cash-out feature might be a structural characteristic of sports-betting apps that appeals to inexperienced or low-risk gamblers, nudging them toward a higher-risk betting profile (in the sense of making bets that have a higher stake size and a lower expected value; see, e.g., Gray et al., 2012; Newall et al., 2021). We therefore suggest that the cash-out feature and its effects on betting behavior are important topics for consideration by policymakers and gambling regulators seeking to minimize gambling-related harm. To this end, further research using a longitudinal design is needed to investigate whether usage of the cash-out feature also results in changes in betting profiles over a more naturalistic timescale. Such a study would allow researchers and policymakers to determine whether higher usage of the cash-out feature is a behavioral signature that predicts a worsening trajectory of gambling-related harm over time, as our results suggest that it might be.

We found that cash-out propensity itself was sensitive to both the value of the cash-out offer and the probability of winning the bet. Specifically, participants were more likely to accept the cash-out offer when the offer was more generous relative to the expected value of their bet. Even so, however, cash-out rates remained considerable even when offers were made at less than the true expected value of the bet. This pattern of behavior might allow bookmakers to run a “Dutch book” on bettors with time-inconsistent risk preferences (cf. Ko & Huang, 2012), extracting profit from risk-seeking tendencies in the initial bet and then offering a cash-out option to profit from risk aversion during the preoutcome waiting period. There was also a quadratic effect of the probability of winning a bet on cash-out propensity, so that on average, participants were more likely to cash out of bets with a worse-than-even or better-than-even chance of paying out, compared with bets that had an even chance of paying out. We did not find any evidence that cash-out propensity was affected by the ambiguity of this probability or by the time point during the delay period when the cash-out offer was made.

One simple interpretation of our findings is that decisions to cash out are motivated by standard economic risk aversion. If this were the case, however, cash-out rates should be relatively consistent within an individual across the different win-probability conditions, because economic risk aversion is typically assumed to be a trait that depends only on the size of the stake and the variance of payouts (Holt & Laury, 2002). Our results suggested that this was not the case; instead, in both experiments we found an unexpected negative correlation between cash-out propensity in bets with deteriorating odds versus bets with improving odds. In other words, participants who were more likely to cash out in bets with deteriorating odds (thereby avoiding prospective losses) were less likely to cash out in bets with improving odds (thereby locking in their paper gains). This pattern is hard to reconcile with the explanation that cash-out decisions are simply motivated by economic risk aversion; instead, our results show that cash-out propensity depends in person-specific ways on whether the overall position of a bet is improving or deteriorating, similar to the path dependence observed in the game show “Deal or No Deal” (Post et al., 2008).

Moreover, we found that individual differences in the size of the effect of cash-out availability on bet amounts were positively correlated with individual differences in cash-out propensity for bets with deteriorating odds only. This indicates that participants who showed the largest effect of cash-out availability on their betting behavior tended to be those who most often used the cash-out feature in bets that were unlikely to pay off. This suggests that it was participants’ ability to cash out as a way of avoiding prospective losses that motivated their willingness to increase their bet amounts (rather than, e.g., cashing out as a way of locking in paper gains in bets that were likely to pay off). More broadly, these results underline the importance of understanding individual-level heterogeneity in cash-out decisions as a window on human risk-taking in dynamic choice environments, as distinct from the standard economic paradigm of static one-shot gambles (Gagne & Dayan, 2021; Lybbert et al., 2013).

Several limitations of the present study should be noted. First, the behavioral task that we used had lower monetary stakes and shorter timescales than would typically be the case in real-world sports betting. Consequently, further research is required to test whether results generalize to settings with higher monetary stakes and longer timescales. The behavioral task also offered only a single cash-out offer at a randomly determined point of the preoutcome delay period and hid the outcome of the original bet from participants if they accepted the cash-out offer. These features also differ from cash-out as a consumer product, which tends to be continuously available throughout the duration of a bet and which does not prevent bettors from learning the outcome of the original bet if they choose to cash out. Varying these task features to more closely match the experience of cash-out in the real world is therefore also important for future research; in particular, by manipulating the availability of post-cash-out outcome information we could test whether anticipated postoutcome regret (Zeelenberg, 1999) is a factor that influences the decision to cash out of a risky bet. Finally, the PGSI is only a proxy measure for gambling-related harm that may also capture interindividual variance in other factors, such as gambling exposure or experience. Further research with more fine-grained measures of gambling harm is required to determine how cash-out propensity might vary in those with high levels of gambling-related harm. Similarly, the generalizability of our results is limited in the sense that participants were adults recruited via Prolific rather than randomly sampled from the general population.

Although we have focused on the application of these findings to gambling, they also have bearing on a broader class of financial decisions. In many real-world financial choices, the owner of a risky asset (e.g., real estate, stocks, cryptocurrency) must weigh the guaranteed immediate returns of selling the asset (thereby cashing out) against the potential costs and benefits of retaining it into the future. There is an increasing convergence between the “gamified” product design of gambling apps and the design of stock-trading apps, which has been identified as a factor increasing risk-taking in consumers (Hüller et al., 2023). For this reason, our results also have bearing in understanding how people behave in these settings, and our finding that participants place larger bets when cash-out is available suggests that the frictionless opportunities to buy and sell financial securities in these apps may induce greater risk-taking by reducing the friction of trades and increasing perceived market liquidity (Keynes, 1936). As well as giving insight into gambling behavior more narrowly, therefore, the results of the present study also provide insight into the cognitive processes that underlie this broader class of real-world decisions.

Supplemental Material

sj-pdf-1-pss-10.1177_09567976241266516 – Supplemental material for People Place Larger Bets When Risky Choices Provide a Postbet Option to Cash Out

Supplemental material, sj-pdf-1-pss-10.1177_09567976241266516 for People Place Larger Bets When Risky Choices Provide a Postbet Option to Cash Out by Daniel Bennett, Lucy Albertella, Laura Forbes, Ty Hayes, Antonio Verdejo-Garcia, Lukasz Walasek and Elliot A. Ludvig in Psychological Science

Footnotes

Transparency

Action Editor: Lasana Harris

Editor: Patricia J. Bauer

Author Contributions

Notes

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.