Abstract

Between half and three-quarters of new housing development in African cities has been taking place on land acquired through informal channels. This paper offers insights from a study of self-builders’ investments in informal land and housing in Dar es Salaam and Mwanza, two of the largest and fastest-growing cities in Tanzania. The findings demonstrate that self-builders’ investments in informal land and self-built housing are inextricably linked with household wealth accumulation processes and long-term security. In light of the research findings, the paper offers reflections on the potential impacts of ongoing land formalization processes. The paper argues that the informal housing system has far more advantages than appreciated by proponents of formalization, that the vision of bringing “dead capital” to life is misleading, and that the anticipated emergence of active formal markets for land and housing may not serve the needs or interests of low- and middle-income households.

Keywords

I. Introduction

African cities are growing rapidly, both demographically and spatially. UN projections estimate that Africa’s urban populations will double between 2015 and 2040,(1) while urban densities decline and urban land cover potentially triples.(2) Between half and three-quarters of new housing development in African cities has been on land acquired through informal channels, i.e. not in compliance with formal regulations for land-use planning, transfer of ownership or development control.(3) The pervasiveness of informal land development processes can be seen as a continuation or evolution of earlier practices, but also as a response to inefficient formal land delivery systems, along with exclusionary planning standards and regulations.(4) Formal land delivery channels commonly meet less than 10 per cent of effective demand.(5) It has been suggested that part of the reluctance to formally open up sufficient land for affordable housing lies in concerns about attracting yet more people to already overpopulated and underserviced cities.(6)

Prominent economist Hernando De Soto estimated that 85 per cent of all urban property in low and middle-income countries was held informally.(7) In many countries, the estimated value of household savings tied up in informal property is several times greater than the total value of savings and deposits in commercial banks, incoming foreign investments, and the value of formally registered companies and public enterprises privatized or about to the privatized.(8) De Soto dismissed the economic and financial significance of these informal assets, seeing them as “dead capital” that cannot easily be transacted outside narrow circles of trust or used as collateral for loans and for generating additional wealth.(9) In effect, De Soto argued that formal property rights are a precondition for going beyond the use of land and houses for shelter and getting out of poverty.

De Soto’s ideas have been prominent in urban development discourse in recent decades, lending support to an array of land formalization programmes.(10) The influence is reflected in the recognition given to secure property rights in Sustainable Development Goal 1 on poverty eradication and 11 on sustainable cities.(11) While land formalization remains high on the urban agenda, particularly in Africa, formal land and housing markets have not expanded commensurately. De Soto’s ideas have also attracted widespread criticism on conceptual, ideological and methodological grounds, particularly from researchers wary of the miraculous benefits he predicts for owners of informal property, when “dead capital” is brought to life.(12)

For the purpose of this paper, two critiques of De Soto are of particular relevance. First, urban livelihoods research has shown that households’ investments in informal land and housing are about more than meeting shelter needs. Even informal land and housing is often the most important economic asset for urban households,(13) commonly used for generating income, especially from home-based businesses and rental housing.(14) Longitudinal studies have also linked households’ investments in owner-occupied housing with long-term wealth accumulation and upward social mobility.(15) Households’ investments in land and housing may be shaped more by their perceptions of tenure security than by legal title.(16)

Secondly, there is little empirical evidence of land formalization programmes significantly improving low-income households’ ability to sell or use their property as collateral, i.e. as the basis for creating “live capital”. Even with their homes as collateral, financial institutions may be unwilling to lend to low-income households, which may find it difficult to meet the financial institutions’ income requirements. Indeed, predetermined and regular repayments on loans are ill-suited for households with low, irregular incomes and can put their homes at risk.(17) Furthermore, self-built housing is rarely transacted, even after formalization, due to limited demand from aspiring homeowners or other potential buyers, as well as sociocultural barriers to sale such as inheritance expectations of children and complex cross-generational tenure arrangements.(18)

While many specifics of De Soto’s celebration of land formalization have lost their salience, other justifications have emerged. In particular, Paul Collier and Tony Venables have been reviving the critique of informality on different grounds. While De Soto emphasized capital formation as the key benefit of formalization, Collier, Venables and others view formal property rights as a necessary precondition for the emergence of active formal markets for land and housing.(19) They see formalization as part of a multifaceted approach, which also entails efficiently enforced building regulations that are inexpensive to adhere to, innovative housing finance mechanisms, coordinated investments in complementary physical infrastructure and social services, and land-use planning, all of which support local employment creation.(20) This enables land formalization to fit neatly into a broader agenda around opening Africa’s cities up to world markets.(21)

This very different defence of formalization sees it as crucial for unlocking domestic capital, but also for attracting foreign investments and for generating revenue through property taxation. In this view, formalization encourages investments in more dense, efficient, productive land uses, while informal settlements cause urban sprawl and spatial fragmentation.(22) This, so the argument goes, has deprived African cities of the benefits of urban agglomeration, whose theorization launched the new “economic geography” in the early 1990s.(23) The emergence of active formal markets for land and housing is envisioned to encourage large-scale private investments in formal housing of standardized design, which can be efficiently developed to high densities and easily valuated, transacted on a market and used as collateral.(24) Formal land and housing markets are also anticipated to promote relocation of economic activity and formation of economic clusters,(25) as well as enabling connectivity and contributing to significant productivity gains.(26)

This paper contributes to the discussion of informal housing systems and these various critiques of informality raised by De Soto(27) and Collier, Venables and others.(28) The paper offers insights from a study of the investments of “self-builders” in informal land and housing in Dar es Salaam and Mwanza, two of the largest, fastest-growing cities in Tanzania. Self-builders are primary actors in opening up new peripheral land for residential development. Most self-builders acquire land through informal channels and engage in incremental construction for owner occupation, renting and other purposes. As such, they are key actors in the informal land development processes critiqued by De Soto(29) and the more recent proponents of formalization.(30) This paper examines how self-builders’ investments in informal land and housing are linked with household wealth accumulation processes. The findings confirm the importance of investments in owner-occupied housing for long-term wealth accumulation (as found in previous studies(31)) and also highlight the significance of multiple investments beyond household shelter needs. In light of these findings, the paper offers reflections on the potential impacts of ongoing land formalization processes on self-builders’ ability to deploy property as “live capital”. As efforts to formalize urban land intensify across Tanzanian cities,(32) it seems prudent to consider to what extent anticipated benefits are likely to materialize. The paper argues that the informal housing system has far more advantages than appreciated by the proponents of formalization, that De Soto’s vision of a bringing “dead capital” to life is misleading, and that the anticipated emergence of active formal markets for land and housing may not serve the needs and interests of low- and middle-income households.

II. Context

In recent decades, Dar es Salaam, with a population of 4.4 million people in 2012,(33) and Mwanza, with approx. 700,000,(34) have experienced continuously high population growth rates of around 5–6 per cent per year.(35) Informal land development processes are the dominant factors shaping urban expansion in both cities. Informal settlements are estimated to accommodate up to 75 per cent of residents in Dar es Salaam(36) and Mwanza.(37)

Expansion of informal settlements has been tacitly tolerated by Tanzanian authorities since independence.(38) The formal land allocation system is highly inefficient and subject to malpractice; it plays only a very marginal role in the provision of urban land.(39) Alongside this is a vibrant informal land market, with more accessible, affordable land, but also less tenure security and more insecurity about official plans. Most aspiring homeowners, across social groups, have no option but to acquire land on the informal market.(40) Though informal land is traded without titles, informal settlements are not generally considered illegal – residents enjoy a relatively high degree of de facto tenure security based on social recognition of ownership rights from adjoining landowners and elected local leaders.(41) Informal land transactions are commonly legitimized through informal sales agreements, legal contracts, and the practice of local leaders acting as witnesses and verifying that the seller is the rightful owner. These informal practices were also observed by De Soto in his commissioned assessment of the informal economy in Tanzania.(42) Decades of government policies focusing on regularization, rather than demolition, have ensured that development incentives are quite similar in informal and formal areas. Owners of informal land confidently build houses of permanent materials and connect to services.(43) Providers of formal services commonly provide services post-settlement in response to residents’ requests, applications and lobbying efforts.(44) Even property taxation is, at least in principle, payable also by owners of residential and commercial buildings in informal settlements.(45)

Regularization has been the main approach of the Tanzanian government towards informal settlements for the past decades. Regularization facilitates the recording, adjudication, classification, and registration of occupation and land use with the ultimate aim of formalizing property rights.(46) Urban Planning Act No 8 of 2007 and Land Act No 4 of 1999 provide for the recognition of informal settlements, if they are located in habitable areas. The government has been less tolerant of settlements occupying land without permission of existing claimants, but this applies to few informal settlements in Tanzania. Formal steps towards regularization are set out by the Ministry of Lands, Housing and Human Settlements Development. They include a public consultation on the scheme, a survey of existing conditions, development and local approval of a land-use plan, a cadastral survey and the issuing of title deeds.(47) An important objective is also to curb continued subdivision. Concerns have, however, been raised about the risks of over-emphasizing formalization of private property rights at the expense of public and communal land uses.(48)

Formalization of urban land is a central element in the National Programme for Property and Business Formalization (MKURABITA) launched in 2005 and influenced by De Soto’s ideas and assessment of the informal economy in Tanzania.(49) MKURABITA presumes a strong link between property and business, reflecting the government’s desire to raise capital for business investments through formalization.(50) Recently, the Tanzanian government has amplified efforts, launching an ambitious regularization programme, to an extent that Tanzania may be reaching “peak informality”.(51) The current Five Year Development Plan II (2016/17–2020/21) specifies ambitious targets, with regularized properties expected to rise from 380,000 in 2015/16 to 670,000 in 2025/26.(52) Regularization is presented as key to achieving higher levels of productivity and benefitting from agglomeration economies, echoing the ideas of Collier, Venables and other recent proponents of formalization.(53) Regularization could also ease collection of property tax, if it entails effective centralized registration of property.

There is considerable variation in the implementation of regularization projects in different neighbourhoods in Dar es Salaam and Mwanza. Generally, regularization is offered to, rather than forced upon, local neighbourhoods. Regularization focuses on delineation and registration of existing plot boundaries and private property rights. Regularization can also entail adjustment of claims considered unfounded or in contravention of land-use regulations, as well as negotiations regarding space for communal facilities. Regulations are sometimes adapted or eased, rather than strictly applied. For example, the smallest plot size accepted in the regularization guidelines is 90 square metres, while it is 300 square metres for planned high-density areas. There is little central funding, so ongoing projects are primarily financed through fees levied from the current landowners. Although significantly lower than individual registration costs, the costs for full regularization processes can be hard to cover locally. Ongoing regularization relies on the active leadership of local leaders at sub-ward and ward levels coordinating and ensuring local participation. The Tanzanian government increasingly supports private sector involvement in urban planning, which used to be the sole responsibility of municipal planning offices.(54) Several private surveying companies are licensed to carry out cadastral surveys and develop local land-use plans in regularization processes. These companies are motivated by profits extracted from the fees paid by current landowners. Perhaps as a result of the high upfront costs, regularization progress in both Dar es Salaam and Mwanza has been patchy in many of the areas covered. Speeding up regularization without undermining participatory processes or the positive aspects of the informal housing system remains a challenge. A better understanding of the informal processes will hopefully help to meet this challenge.

III. Methods

This paper is based on case studies of informal settlements, two in each city. One is a consolidated settlement close to the centre and the other a newly developing settlement towards the periphery (Map 1 and 2). All four areas could be considered “typical” residential areas in these cities, as they have developed largely informally and accommodate residents of mixed ethnic origins and socioeconomic backgrounds. During the early years of settlement, the land was neither surveyed nor planned for residential development (except a small area in Nyasaka). One area (Kiembe Samaki) was regularized post-settlement in the early 2000s as part of a World Bank-funded project. The remaining areas are undergoing regularization processes carried out by private surveying companies in collaboration with local ward and sub-ward authorities.

Mzinga is a newly developing settlement within the urban built-up area, approximately 15 kilometres southwest of Dar es Salaam’s city centre (Mzinga Ward, Ilala Municipality). The first self-builders settled in the area in the early 2000s.

Kiembe Samaki is a consolidated settlement with high densities and limited free space approximately 8 kilometres southwest of Dar es Salaam’s city centre (Barabara ya Mwinyi Ward, Temeke Municipality). The first self-builders settled in the late 1980s and early 1990s.

Nyasaka is a newly developing settlement on the urban fringe, approximately 5 kilometres northeast of Mwanza’s city centre (Nyasaka Ward, Ilemela Municipality). In the late 1990s a small part was surveyed for residential development. Many other self-builders settled in the surrounding areas during the 2000s.

Kiloleli B is a consolidated settlement with high densities located on steep hillsides approximately 3 kilometres northeast of Mwanza’s city centre (Nyasaka Ward, Ilemela Municipality). The first self-builders settled in the mid-1990s.

Data collection was carried out in November 2018 in Dar es Salaam and January–February 2019 in Mwanza. This consisted of semi-structured interviews with 112 households, 26 to 30 from each case area. Of these, 68 households are established self-builders who have built one or more houses in the city. Another 16 are in the process of building their first house in the city. The remaining 28 are tenants without property in the city, though some hold property elsewhere. All interviewees are adult household heads, both women and men, in charge of their households’ housing decisions and expenses. Most households are headed by married couples (of whom one participated in the interview). Others are headed by single women (20) or men (3), including never-married individuals, divorcees and widowers. In total 66 women and 46 men were interviewed. Household sampling was purposeful, and sought to capture variation in relation to housing type, size, quality and stage of completion – or for tenants, in relation to the type, size and quality of rental housing. Key informant interviews were also conducted with local leaders (4) and land brokers (11).

Locations of case study areas in Dar es Salaam

Locations of case study areas in Mwanza

IV. Findings

a. Meeting household shelter needs

Household shelter needs, and especially a desire to own their housing, is a central motivation for self-builders across case study areas. Most established self-builders (60 out of 68) live in their first family house in the city after previously living as tenants or with relatives elsewhere in the city. With a small payment for a piece of undeveloped land and investments in incremental house construction and improvements of services and infrastructure, they were able to establish themselves as homeowners. This is the primary route to homeownership for most low- and middle-income urban households, as formal land is limited in supply and difficult to acquire, even for those who could potentially afford it.

The self-builders interviewed are socioeconomically heterogeneous, and include self-employed, casual workers, business owners, and employees in government or private companies. Their occupations include informal traders, food vendors, craftspeople and security guards, as well as teachers, soldiers, nurses and engineers.

The primary attraction of acquiring land through informal channels is its availability and affordability. The vast majority of self-builders bought their land from the previous owner. Some connected with the previous owner through friends or relatives, others relied on informal land brokers. Undeveloped plots are purchased in many different sizes depending on the buyer’s preferences and ability to pay. Houses are commonly developed over several years and according to households’ ability to accumulate savings. Over time, many invest in such amenities within their compounds as on-site sanitation solutions, private boreholes or water storage facilities. They also seek to attract formal service providers through applications, lobbying efforts or co-financing for road improvements and extension of electricity, piped water and public transport services.

Self-built housing offers many advantages for the established self-builders, who value the stability, privacy and comfort of living in their own house. Homeownership is also a source of pride and prestige. Many highlight “not paying rent” and avoiding the “disturbances of rental life”, such as facing conflicts with landlords, sharing facilities and falling behind on rent payments. Despite substantial costs associated with land purchase and house construction, self-building offers more flexibility than paying rent. Investments can be made when resources are available and postponed during times of economic hardship. As an established self-builder in Mzinga explained: “Most of us feel secure only when living in our own house. Whenever you are sick or something goes wrong with the business, you know you have the house. That is why you see everyone is trying to find even just a small piece of land.” The lack of a land title does not detract from the strong sense of security associated with homeownership. Self-builders generally perceive themselves as legitimate owners of their land; they confidently build homes of permanent materials and invest in housing improvements and service connections.

Many tenants also aspire to homeownership, and the social distance between them and owners can be less about class than position in the life cycle. Out of 44 tenants interviewed, 16 are aspiring self-builders in the process of building a family house nearby (7) or in more peripheral areas (9). They have not yet been able to complete their house to a habitable stage, but hope to do so in coming years. Among the remaining tenants are many young people, who may be able to build a house later in their lives. However, not all tenants can do so, as explained by a long-term tenant in Kiembe Samaki: “I’m 44 years old and I have been living for more than 20 years in Dar es Salaam without having my own house. I cannot have any plans for my life, because I’m just renting all the time. Of course, I wish to build a house, but every time I see myself unable to attain the funds. I have a plot back home in my village, but I have not been able to develop it.”

b. Multiple investments beyond household shelter needs

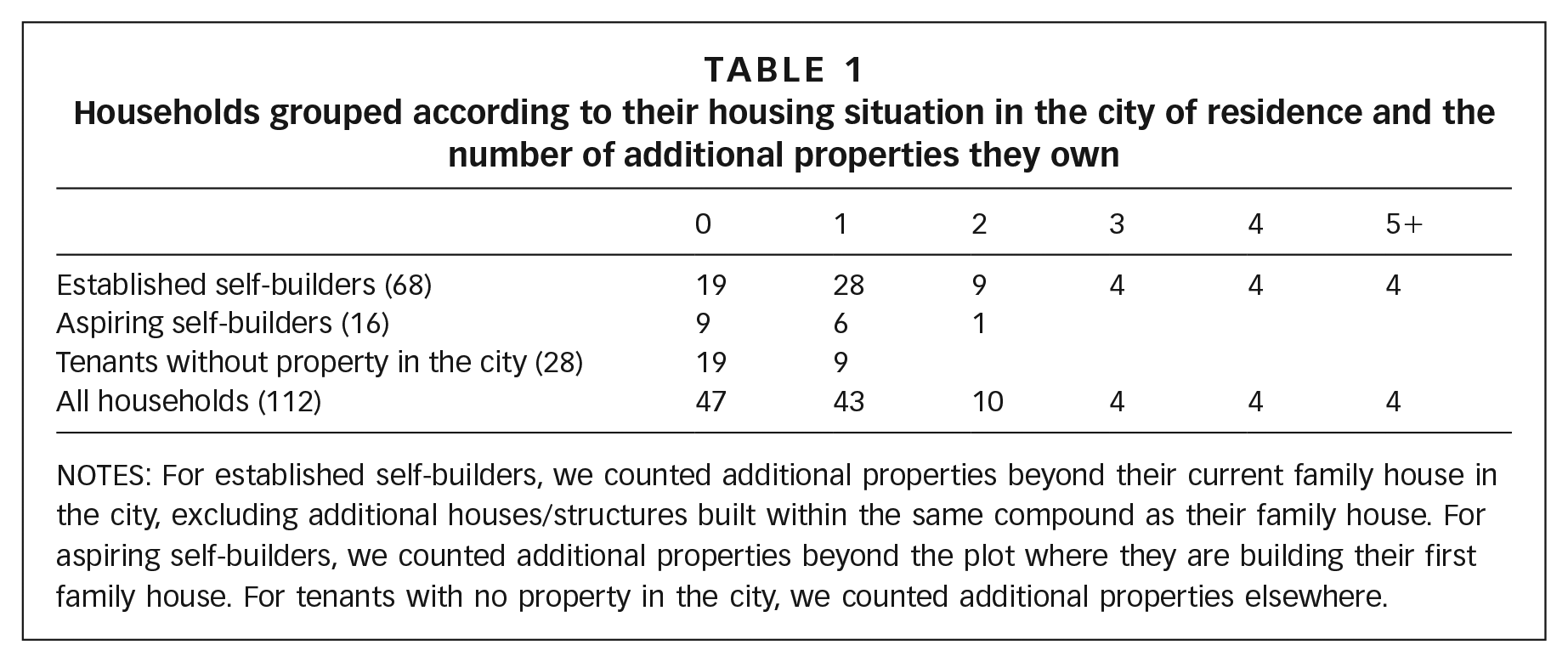

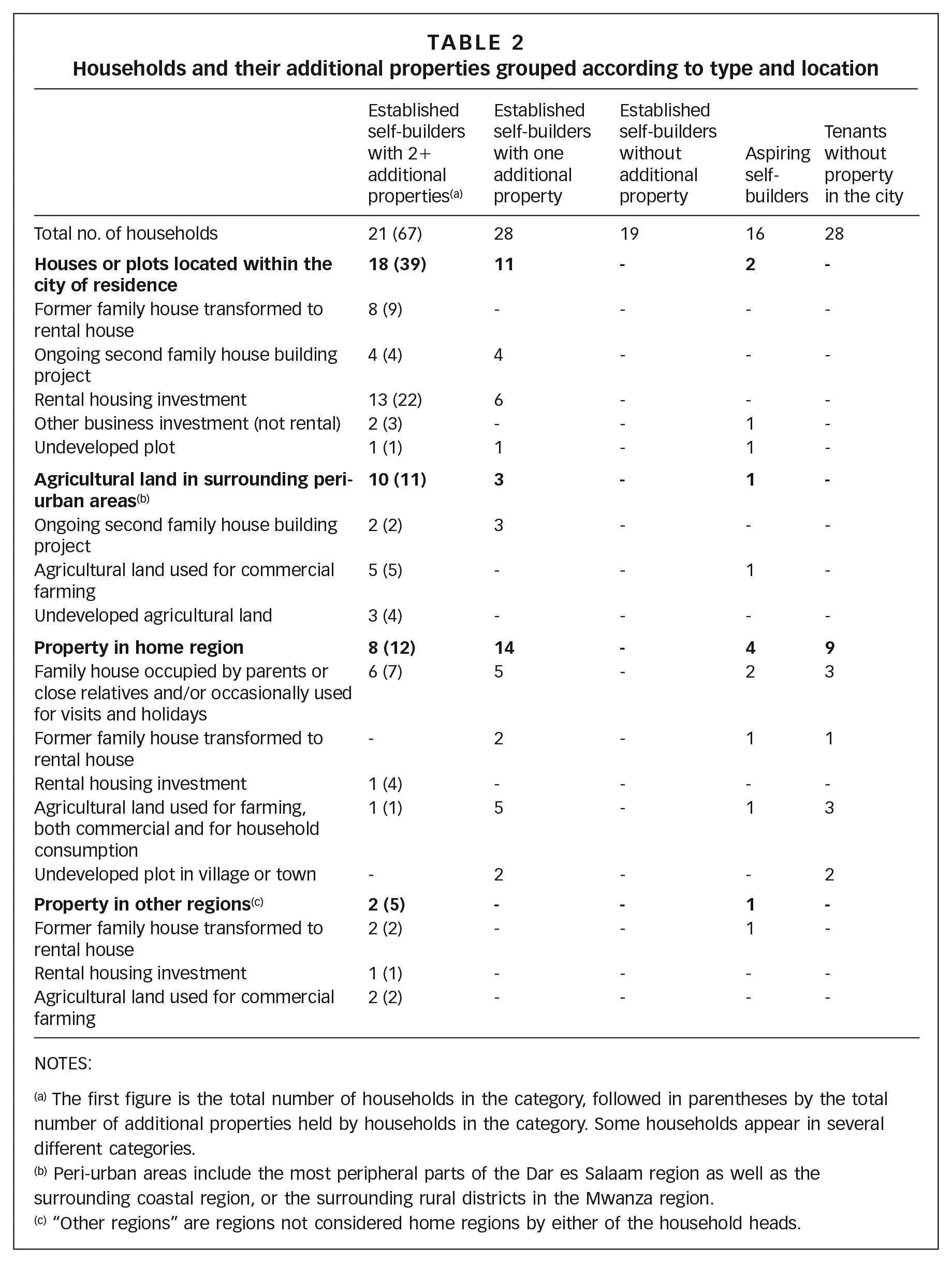

Of the 68 established self-builders, 49 own at least one additional house, undeveloped plot or agricultural landholding beyond their current family house (Table 1). Many (21) hold two or more additional properties. Most of these are located within the city (50 out of 95 additional properties) or in the surrounding peri-urban areas (14) (Table 2). Some of the additional properties are located in their home regions (26) or other regions where they lived previously (5). The additional properties fall broadly into four categories: second house building projects, rental housing investments, commercial farming investments and property “at home”.

Households grouped according to their housing situation in the city of residence and the number of additional properties they own

NOTES: For established self-builders, we counted additional properties beyond their current family house in the city, excluding additional houses/structures built within the same compound as their family house. For aspiring self-builders, we counted additional properties beyond the plot where they are building their first family house. For tenants with no property in the city, we counted additional properties elsewhere.

Households and their additional properties grouped according to type and location

NOTES:

The first figure is the total number of households in the category, followed in parentheses by the total number of additional properties held by households in the category. Some households appear in several different categories.

Peri-urban areas include the most peripheral parts of the Dar es Salaam region as well as the surrounding coastal region, or the surrounding rural districts in the Mwanza region.

“Other regions” are regions not considered home regions by either of the household heads.

Investing in a better house to live in

Having completed their first family house, some resourceful self-builders go on to build a larger, more comfortable house, which also frees up their first home for other uses. Eight established self-builders live in their second or third family house in the city. Their former family houses are located in more central areas and rented to tenants. Thirteen are in the process of building a second family house nearby (2), in other peripheral areas (6) or in peri-urban areas (5). The latter is typically to engage in farming and/or enjoy a more “natural lifestyle”. Most aspire to rent out their current family house, though a few (3) will use both houses for their own family, e.g. for second wives, adult children or ageing parents.

John, in his early 60s, lives in his second family house in Mzinga. He built the first in Buguruni in the early 1990s. In 2013 he was able to use his pension savings to buy a small, incomplete house in Mzinga, which he has expanded with extra rooms and space for his fumigation business. The Buguruni house is rented to a tenant. “Mzinga is a very nice area with plenty of space and a fresh breeze. Buguruni is much more dense and congested. Now I am looking for agricultural land in the coastal region, because I want to grow some crops and keep some animals.”

Investing in rental housing

Nineteen established self-builders have bought additional plots in the city specifically for rental housing (Table 2). Rental housing is perceived by many as an attractive investment and often generates substantial income, but most self-builders have other primary income sources. Only a handful of elderly retired people (5) derive their primary income from rental housing investments, made while they were still working.

Maria is in her 50s and has recently retired from nursing at a large hospital in Mwanza. She bought a plot in Kiloleli B in 1998 and was able to move into her own house in 2000. Later, she bought another plot in Nyasaka. “I finished construction on that house in Nyasaka in 2014. I don’t want to live there myself. It is just for renting purposes, to help raise money for tuition fees for my children. Right now, I have only one tenant family there, but I want to build another house for tenants there.”

Investing in commercial farmland

Some self-builders have invested in larger agricultural landholdings in the peri-urban areas around their city (8) for commercial farming, with no intention of settling there themselves. Others have invested in farmland in regions where they previously lived (2). Among those who have invested in commercial farming, many consider it a primary income source.

Zakaria identifies himself as a farmer. He owns a large piece of agricultural land in Buhongwa not too far from Mwanza City. He has also built a city house in Kiloleli B, where he has lived since 1996. “I built my house here in Kiloleli B, so my children could go to school more easily. Previously, I was also keeping livestock here, especially pigs. Nowadays I have many neighbours and some of the Muslims started complaining, so I decided to keep the animals on my farm in Buhongwa. Maybe I will build a rental house here instead, because I have a large compound.”

Investing in or holding houses and land “at home”

Of the established self-builders, 49 were born in a region other than their current region of residence. Quite a few (22) own land or houses “at home”, which can mean a village, a small town or a larger city in their home region. Some have inherited land or a house. Others built a house when they still lived “at home” or after moving to the city. Some of the houses “at home” are occupied by parents or close relatives, some are used occasionally for visits and some are rented to tenants. There are also migrants among aspiring self-builders and other tenants, who own property “at home”.

Suzana is in her early 20s and recently moved to Mwanza to join her husband, who teaches in a private school. They live in a rented room in Kiloleli B. “We do have a plot we inherited back home in our village in the Kishili highland area. Of course, we plan to build a house there at some point, but we don’t want to live there.”

c. Accumulating savings for investments

The primary sources of finance for self-builders’ investments in land and housing are accumulated household savings, extracted over many years from their salaries and profits from various businesses. Most established self-builders proudly declare that they have relied entirely on their own savings. A few have financed part of their investments through pension savings (6), land sales (4), or compensation from public land acquisitions or job terminations (4). Some (15) took loans from banks or microfinance institutions, mostly salaried employees or retired employees, who could use their salary as security. Such loans are not available for the many self-builders who are self-employed and/or engaged in small-scale businesses, trading activities or casual work.

The saving capacity of self-builders depends on the ability of household members to generate incomes, the relative weight of other household needs and their obligations towards extended family networks. Aspiring self-builders can find it a struggle to finance construction alongside rent payments. Successful completion of the first family house demonstrates a household’s ability to accumulate savings and may free up resources previously used for rent, so households can save even more. Continuous investments in land and housing beyond the first family house, especially in urban and peri-urban areas, are an indicator of a household’s sustained capacity to accumulate savings over time. Most of the 35 established self-builders who own additional properties in or around the city have experienced increasing or stable household incomes over the past 10 years, and are optimistic regarding future income. Quite a few (21) have one or two employees or retired employees in their households. Others (8) operate larger businesses within the hospitality, manufacturing, mining, agricultural processing or commercial farming sectors. Self-builder households with multiple (2+) additional properties within or around the city (19) are often visibly prosperous.

At the other end of the spectrum are established self-builders with no additional properties (19) or only additional property “at home” (14). Many (19 of 33) are unlikely to invest further in property, because of a declining capacity to save due to such factors as old age, retirement, health problems, loss of a spouse, growing household size, loss of a job or decreasing profits from their businesses. Some (7) have struggled for 15–20 years to finish constructing their current family house, often making hard choices, e.g. between sending their children to better schools and finishing house construction. The struggling self-builders highlight the risks associated with tying up their accumulated savings in incomplete structures for an indefinite time. This is exemplified by an ageing self-builder in Kiloleli B, whose family has lived in two rudimentary rooms since 1998, though foundation and incomplete walls outline the structure of a much larger house: “I am planning to improve my house, but my income is declining. Of course, times are tough for business, but I think it is also because I have spent a lot of my income on construction, so maybe I haven’t invested enough in my business.”

d. Building a reserve of wealth

More often, continuous investment in informal land and self-built housing builds a reserve of wealth, which can be passed on to children or mobilized in times of economic hardship. Income streams can be generated from rental arrangements if other income sources fail or if the ability to work or operate more demanding businesses is diminished by old age, retirement or ill health. Wealth can ultimately be released through property sales in severe emergencies, such as large hospital bills, personal injuries or loss of a spouse.

Investments in land and housing are associated with long-term protection and preservation of wealth. Among self-builders, land and housing is widely perceived as a secure place to put savings, a perception largely unaffected by the lack of titles to the land. Many highlight that land and housing are “fixed assets”, which cannot easily get stolen or lose value over time. This is often compared favourably with other investment options or businesses, which are considered riskier. Land investments may also constitute a hedge against inflation. The relative illiquidity of land and housing is part of the attraction, since it shields wealth from excessive consumption and some of the social obligations towards extended family networks. A relative in need might be able to make a socially legitimate claim on cash reserves, but only the most severe emergency would require someone to part with property, as explained by an established self-builder in Mzinga: “Selling our old house would not have been a good idea, because it will form part of the inheritance for my children. My children will not inherit the money in the bank. If I sell it now, I am not going to be able to keep the money. I also consider it as a security for my old age.”

Land investments may enable owners to passively accrue wealth through rising land values over time. Most of the established self-builders bought land cheaply during the early years of settlement and confidently assert that the value has increased since then. This perception is validated by land brokers, who have experienced substantial increases in land prices since the early years of settlement. However, brokers also reported that land prices had fallen in the three years prior to the study, which they explain with reference to the wider economic and political situation in Tanzania. Nevertheless, owners and brokers expect land prices to increase in the future due to growing local populations, limited availability of undeveloped land, and real improvements of services and infrastructure. Self-builders, who own land in more peripheral or peri-urban areas, anticipate rising land values as the city expands.

e. Reflections on the impacts of ongoing regularization processes

Three of the case study areas are currently undergoing regularization. These processes focus primarily on delineation and registration of existing private property rights. In a few cases, local leaders sought to secure land for communal purposes through negotiations between landowners, but were unsuccessful. Regularization processes are financed through fees from landowners ranging from TZS 250,000–300,000 per plot (approx. US$ 110–130). In all three areas, the initial survey had been completed at the time of fieldwork, but formal titles not yet issued. Local leaders said that only half to two-thirds of landowners had completed payment of all fees associated with regularization. Self-builders in these areas have diverse expectations regarding the impacts of regularization, including securing their rights against expropriation, solving boundary disputes and increasing land values. This subsection discusses the potential impacts of regularization on self-builders’ ability to use property as collateral and benefit from the anticipated emergence of active formal markets for land and housing.

The ability to acquire loans with property as collateral is key to De Soto’s vision of bringing “dead capital” to life.(55) This is also expected by local leaders and at least some of the established self-builders as an impact of regularization. However, some self-builders can already use their property as collateral for loans from banks or microfinance institutions, even without formal titles. Nine of the established self-builders have already done so, though five of them live in areas still undergoing regularization. They were able to use sales agreements or letters from local leaders as proof of ownership. Some of them acquired loans for house construction (1), tuition fees (1) or family emergencies (2). Others (5) acquired loans for investments in their businesses, more in line with De Soto’s ideas. The latter are entrepreneurs and larger business owners. As one explained: “Most people worry about losing their house, but when you use your house to take a loan for your business, it is not that risky. Loans are very expensive, so you need a good business to support the repayments.” This is perceived as less risky, because profits from the business investment contribute directly to repayments on the loan, whereas repayments on loans taken for tuition fees or family emergencies need to be extracted from other income sources. The findings suggest that many self-builders will remain disinclined towards using property as collateral even after regularization. Only three self-builders expressed an interest in doing so after regularization. Their reluctance is rooted in fear of losing their property, if they cannot make repayments. This is a real risk for self-builders with fluctuating and uncertain income sources, as observed by a self-builder in Mzinga: “The banks are not friendly. Not so long ago there were some houses around here that were being sold by banks, just because the owners failed to pay those high interest rates. Some were rescued by relatives, but others failed, and they just had to let their houses be sold.”

The emergence of active formal markets for land and housing is the key benefit of formal property rights in the view of Collier, Venables and other recent proponents of formalization.(56) Local leaders and land brokers expect regularization to facilitate smoother land transactions by establishing clear ownership rights, avoiding duplicate transactions, and resolving boundary disputes and ambiguous ownership rights. However, the findings indicate that informal land is already widely traded, not only inside the “narrow circles of trust” emphasized by De Soto,(57) but also outside them. Most established self-builders (65 out of 68) acquired their current plot through purchase. Only five bought directly from a relative or friend. Land brokers often play a central role in connecting unrelated buyers and sellers. Local leaders commonly facilitate transactions by verifying that the seller is the rightful owner of the land and that there are no ongoing disputes regarding ownership, e.g. in relation to inheritance, divorce or possible duplicate transactions in the past.

Relatively few established self-builders (11) have sold any of their land. Among those who have, some (7) cut off a piece of their own plot. Others (4) sold plots held elsewhere in the city. A few sold land to raise capital for investments in rental housing (2) or commercial farming (1), much in the spirit of De Soto. Others sold land to finance house construction (2) or to solve family emergencies (6). The latter is best described as a distress sale. Land sales are commonly viewed as a last-resort option to be taken up only for severe emergencies, as explained by a self-builder in Mzinga: “I have never sold any of my land. I have only been buying more. Whoever is selling land has their own reasons. The economic situation has been difficult in the past three years, so people who didn’t even think of selling land are now selling, but so far I haven’t experienced those types of emergencies that would require me to sell my land.” The aversion towards selling land might change if land values increase substantially after regularization, as is widely anticipated by brokers.

Regularization is expected to check further subdivision, but in Kiembe Samaki, which had already been regularized in the early 2000s, informal subdivision continued also after formalization. Local leaders can do little to prevent owners from subdividing and reselling land, and if they could prevent this, it would likely have adverse impacts for self-builders tackling difficult life events. Continuous unregulated subdivision could adversely affect land values, especially if vehicular and pedestrian accessibility is constrained within a settlement. Limited accessibility as result of subdivision is evident in the consolidated settlements, but much less so in newly developing areas. The higher rates of vehicle ownership in recent years may have made self-builders and local leaders more concerned about space for access roads, even if roads remain rough and unimproved for many years.

While there is an active informal market for land, house transactions are more complicated and less prevalent. Established self-builders have only vague notions about the value of their houses, reflecting the reality that most would neither want to nor be able to sell their house. According to brokers, there is a continuous demand for undeveloped land from new aspiring self-builders, whereas demand for complete houses is much more limited. Likely, there is only a narrow pool of aspiring homeowners who can raise the cash for a complete house. Few established self-builders (4) have experience with house transactions. Three initially bought a plot with a small house, primarily because they were interested in the plot, and either demolished or significantly rebuilt the original house. For house buyers the land is the long-term investment. According to brokers, self-built houses cannot necessarily yield sale prices that will cover the seller’s construction costs. House sales can be motivated by family emergencies or insurmountable debts, as a local chairman explained: “Houses are mostly sold when the owner is having economic problems, for an example when he has failed to repay a bank loan and he knows that the bank will soon come and sell his house for a low price. Then he might try to sell the house himself to get a better price.”

Regularization could make it easier to trade houses, if mortgage finance were more widely available. However, as Collier and Venables observe, transactions of self-built housing are also complicated by the difficulty of valuing such houses and verifying housing quality.(58) Furthermore, aspiring homeowners from similar socioeconomic groups as the established self-builders would probably be more inclined to engage in self-building to avoid regular mortgage payments. Regularization could potentially attract new groups of buyers previously discouraged by the lack of formal property rights, such as higher-income groups, commercial entities or private investors, as envisioned by Collier and Venables.(59) At present, the case study areas might be too peripheral and poorly accessible to attract such buyers, though coordinated investments in complementary physical infrastructure and social services could influence this.

V. Conclusions

This paper has contributed to the discussion of informal housing with a study of how and why “self-builders” invest in informal land and housing in Dar es Salaam and Mwanza. Most self-builders acquire land through informal channels and engage in incremental construction for owner occupation, renting and other purposes. As such, they are key actors in the informal land development processes critiqued by De Soto(60) and more recently by Collier, Venables and others.(61)

Our findings demonstrate that self-builders’ investments in informal land and self-built housing are inextricably linked with household wealth accumulation processes (as previously argued by others(62)) and also go beyond household shelter needs. The findings suggest that the informal housing system has far more advantages than appreciated by De Soto(63) and other proponents of formalization.(64) Investments in informal land and self-built housing function as a mechanism for saving, where small-scale savers have limited alternative options. This mechanism is well adapted to the fluctuating, uncertain income sources that many households rely on and provides a measure of protection from the precarious conditions of urban life. Continuous investments build a reserve of wealth, which can be transferred to children or mobilized in times of economic hardship. Land and housing investments are associated with long-term wealth preservation and passive accrual of wealth through rising land values, and may be a hedge against inflation. The relative illiquidity of land is a part of the attraction, as wealth fixed in land and housing is partly shielded from excessive consumption and obligations towards extended family networks.

While many of these benefits may also apply to investments in formal land and housing, it is remarkable that informal property is so widely perceived as a secure place for savings, even without land titles. This can be explained by the relatively high de facto tenure security in informal settlements in Tanzania. In other contexts, where lack of formal titles may be associated with greater risk and insecurity, the links between investments in informal land and wealth accumulation may be more tenuous and informal property owners may have more to gain from formalization.

The paper has also reflected on the potential impact of ongoing formalization processes, often considered synonymous with regularization in the Tanzanian context. The findings suggest that De Soto’s vision of bringing to life “dead capital”(65) is misleading. Formalization may improve self-builders’ ability to use their property as collateral, but many will be disinclined to imperil the advantages they associate with their investments – a secure place to live, the possibility to generate rental incomes if other income sources fail, and the option of selling land in case of adverse life events. Investments in informal land and self-built housing function as a primary source of security for low- and middle-income households where job security is limited, income sources are often unreliable and social security schemes are highly limited. This finding is in line with previous studies showing that formalization in itself will not make loans more suitable or appealing for households with low, irregular incomes.(66) This critique of De Soto will likely also have relevance in other contexts, where the lack of titles may be associated with greater insecurity.

The anticipated emergence of active formal markets for land and housing may not serve the needs and interests of low- and middle-income households. Increasing marketability might erode the long-term wealth protection offered by the relative illiquidity of informal land and housing. Rising land values may benefit established self-builders, but undermine affordability and make homeownership less attainable for aspiring homeowners. Regularization might stimulate redevelopment and attract new groups of buyers previously discouraged by the lack of formal property rights, as envisioned by Collier and Venables.(67) Indeed, regularization would probably need to attract new groups of buyers to realize their vision of sprawling, low-density, self-built housing giving way to higher density and more efficient and productive land uses that are expected to foster urban agglomeration economies.(68) New groups of buyers could displace low- and middle-income households from the most attractive locations, including tenants accommodated by established self-builders. The case study areas are likely too peripheral and poorly accessible to attract interest from new groups of buyers. Previous studies have found little evidence of market-led displacement after formalization, except in especially attractive locations.(69) Collier and Venables’ vision of large-scale private investments in formal housing of standardized design(70) could potentially offer new investment opportunities for resourceful households, but could also undermine incremental construction as a mechanism for saving for households, who remain unwilling or unable to assume the burden and risks associated with mortgage finance.

As efforts to formalize urban land grow across Tanzanian cities, it is prudent to ask whether some of the anticipated benefits are exaggerated, while the interests of those least able to afford higher housing costs are ignored. This paper has reflected on anticipated benefits highlighted by prominent proponents of formalization, notably the ability to deploy property as “live capital” through loans and resale. The findings suggest that the gains to current owners of informal property are questionable. There may be other benefits appreciated by current owners, such as securing their rights in the event of expropriation or increasing land values in the long term. There are, however, also high up-front costs associated with formalization, which will likely exclude many poorer self-builders and potentially decrease their tenure security. Partial regularization also makes it difficult to address collective issues and negotiate space for communal facilities and infrastructure. At the heart of regularization efforts should be community-based and participatory planning, before, during and after formalization. There is also a need to reconsider the fairness of expecting all current owners to bear the full costs of regularization, to provide sufficient support for those unable to bear the costs and to ensure adequate compensation for those willing to make land available for communal purposes.

Footnotes

Acknowledgements

We are grateful to the residents of Dar es Salaam and Mwanza who generously gave their time to participate in this research, to indispensable research assistants John Williams and Paul Mizzah Charles, and to three anonymous reviewers for valuable comments and critique.

Funding

The research of the lead author was carried out with the support of the Carlsberg Foundation.

The research for this paper is part of a project funded by the East Africa Research Hub (EARH) of the UK Department for International Development (DFID), titled “The Urban Land Nexus and Inclusive Urbanization in Dar es Salaam, Khartoum and Mwanza”, led by the Institute of Development Studies at the University of Sussex.

3.

10.

Durand-Lasserve (2007).

12.

A comprehensive review of the many different critiques of De Soto and the extensive literature on the impacts of urban land formalization is beyond the scope of this paper, but excellent reviews are provided elsewhere. See De Soto (2000); ![]() .

.

13.

14.

15.

17.

Durand-Lasserve (2007); Gilbert (2002, 2012); Lemanski (2011); Schmidt and Zakayo (2018); ![]() ; Hailu and Rooks (2006).

; Hailu and Rooks (2006).

18.

Gilbert (1999, 2012); Tipple (2015); Acheampong (2016); ![]() .

.

19.

20.

24.

26.

28.

30.

31.

35.

UNDESA/Population Division (2018).

39.

Kironde (2000, ![]() ).

).

40.

Kironde (2000, 2006); Namangaya and Kiunsi (2018); ![]() .

.

41.

Kironde (2000, 2006); Namangaya and Kiunsi (2018); Nnkya (2007); Kombe (2000); ![]() .

.

42.

This was commissioned by the Tanzanian government and carried out in 2004–2005 by researchers from Instituto Libertad y Democracia. De Soto (2006, ![]() ).

).

43.

Kironde (2000, 2006); Namangaya and Kiunsi (2018); ![]() .

.

47.

Ministry of Lands, Housing and Human Settlement Development (2016).

48.

Kyessi and Kyessi (2017).