Abstract

This paper describes the funding and financial services provided by the Akiba Mashinani Trust (AMT) to support the Kenyan Homeless People’s Federation (Muungano wa Wanavijiji). Muungano is a federation of autonomous savings groups with over 60,000 members from informal settlements across Kenya. Savings are critical because they enable wealth accumulation, demonstrate the capacity of the community to repay loans and hence leverage additional resources, and build social capital among members. AMT is able to use these savings as seed capital for revolving funds at the community, city and national scales. The funds offer informal settlers a range of financial products, including community project loans, which allow savings groups to finance social housing, sanitation and basic infrastructure in an affordable way. Therefore, unlike formal banking and microfinance institutions, AMT positions its financial services within a broader effort to improve the physical and social fabric of urban informal settlements. The experiences of Muungano and AMT demonstrate the catalytic impact of establishing appropriate financial services geared towards low-income groups – and crucially, how the savings of low-income people can leverage government resources to achieve more inclusive cities.

I. Introduction

This paper describes the financial and non-financial services provided by the Akiba Mashinani Trust (AMT) to support the many housing, livelihood and other initiatives undertaken by the Kenyan Homeless People’s Federation (Muungano wa Wanavijiji, or Muungano) in informal settlements. It discusses measures taken to ensure greater equity, inclusion (especially for low-income groups), participation and community management, accountability, and cost-effectiveness. It demonstrates the importance of tailoring financial services to meet the needs of low-income groups, and how the savings of poor people can steer government resources towards marginalized urban residents. Ultimately, this paper aims to show the correlation between finance and urban transformation of low-income communities living on land with insecure land tenure and very little government investment in basic infrastructure and services.

This paper describes the results of a recent study of AMT’s and Muungano’s work, and contributes to the analysis of the effectiveness of decentralized finance in Kenya. The objective was to document the benefits of the alliance’s local-level finance. The study covers the financial and non-financial products that AMT and Muungano provide, for capacity building, in-situ housing, greenfield development, house improvements, and individual and group livelihood loans. This paper also includes three short case studies illustrating how these financial services have benefitted different communities in these areas.(1)

a. Informal settlements in Kenya

In Kenya, more than half of the urban population live in informal settlements.(2) Most of these settlements are built on private land that was allocated by the state for development purposes or on public land initially set aside for other uses.

The balance of landlords, owner-occupiers and tenants varies among settlements: for instance, 48 per cent of the residents of Kiandutu, a settlement in Kiambu, are tenants, compared to 92 per cent of the residents of Mukuru, a settlement in Nairobi.(3) Landlords typically build temporary units with minimal services and negligible infrastructure. The housing is ordinarily constructed from corrugated iron sheets; some of these houses have concrete floors while many have only earth floors. Almost all the housing is comprised of single-room units, often measuring 10 by 10 feet, with an average occupancy of three people per household. These single rooms are used by families for sleeping, cooking and bathing. Despite the low quality of housing, rents in most informal settlements are high, with residents spending about 20 per cent of their income on housing. In Mukuru, the majority of rent-paying residents pay between Kenyan shillings (KSh) 1,501 and 2,000 (US$ 14.4–19.20)(4) per month, with about 20 per cent paying between KSh 2,000 and 2,500 (US$ 19.20–24) per month. Most tenants aspire to live in a one- or two-bedroom house with running water and individual household toilet and bathing facilities.

Although county governments are supposed to provide safe drinking water to all residents, most county water systems rarely reach past the edge of informal settlements. The residents often rely on flimsy water pipes operated by illicit water cartels that charge exorbitant rates. This creates a staggering “poverty penalty”, where Mukuru residents pay 172 per cent more per cubic metre of water than residents living in formal areas.(5) As a result, slum(6) dwellers usually consume less water of lower quality at higher per-unit costs than their wealthier neighbours. The majority of households do not have access to toilets at home and are forced to use private commercial toilets in public areas, which are available at a cost of KSh 5 for an adult and KSh 3 (US$ .48/.29) for a child. The available toilets are normally pit latrines that fill up quickly and require constant emptying. The expense and poor state of these facilities push many to use tins and paper bags popularly known as flying toilets. The raw faecal waste is then tossed onto rooftops or into drains.

There is therefore an urgent need for investment in housing, infrastructure and services in informal settlements for those living or working there. For Muungano and AMT, the provision of financial services to low-income residents is key to unlocking the resources and capacities of communities. These organizations provide a wide variety of financial and non-financial products ranging from savings accounts to livelihood loans to housing development. Unlike formal banking and microfinance institutions, AMT couches its activities within a broader community effort to upgrade urban informal settlements and markets. Critical to the achievement of its goals has been the investment it has mobilized from local authorities. At the same time, AMT takes its financial responsibilities seriously and seeks to be a credible financial agency. This paper therefore aims to describe how finance or access to financial services is not an end in itself, but a means to achieving improvements in slums and informal markets. The paper also explores what is required to make this goal effective.

b. Introducing Muungano wa Wanavijiji

Muungano, an affiliate of SDI (formerly Slum/Shack Dwellers International), is a federation of autonomous but linked savings groups based in informal settlements. Savings are critical because they enable wealth accumulation, demonstrate the capacity of the community to repay loans, and build social capital among members. Collective savings facilitate strong communal bonds and the development of common goals for their settlements. These enable the savings groups to engage with local authorities and enter into discussions on improving settlements. One of Muungano’s slogans is “Shilingi shilingi, nyumba mpya Mathare”. It means “A shilling, a shilling saved is a new house in Mathare”.(7)

Muungano has over 60,000 members in over 1,000 groups from informal settlements across the country. The income of these members is generally low. For instance, the monthly income of residents in Mukuru is about KSh 12,000 (US$ 115.20), with women earning about 30 per cent less than men in similar occupations.(8) Each savings group draws its membership from the informal settlement or informal market where it is rooted. The groups hold weekly meetings where members deliberate on all issues affecting them, deposit or review savings, take out loans and make loan repayments. At district and city levels, the groups form regional, county or city networks. The savings groups offer a platform for community mobilizing, organizing and developing their capacities to engage with government towards improving conditions in the settlements.(9)

Muungano groups are self-selected and self-managed. Almost all the groups are registered as self-help groups and are therefore required to have a minimum of 10 members, a constitution and three officials: a treasurer, a chairperson and a secretary. Most Muungano groups have a membership of at least 30 to 40 members. All members are required to abide by the constitution of the group, attend meetings, purchase a passbook and be active savers. Savings groups ordinarily maintain a register of their members.

To become a member of a group, applicants are required to register with a fee, which varies among groups. For instance, an applicant is required to pay a membership fee of KSh 200 (US$ 1.92) to join the Matopeni self-help group or the Mukhwano disabled group, while the Shikamoo savings group charges applicants KSh 1,000 (US$ 9.60) to join. The initial fee set by the Shikamoo group was KSh 100 (US$ 0.96). However, many people joined the group but failed to attend meetings or participate in other group activities. The group raised the fee to deter those who were not serious about participating.

The groups’ main activities are mobilizing savings and share contributions, conducting welfare activities and issuing loans. Group activities and projects also include community organization, settlement planning, land purchase, construction of new affordable houses and house improvements.

c. Introducing the Akiba Mashinani Trust

AMT is the financing vehicle for Muungano, formed to raise and structure capital in order to achieve community and individual plans. The fund’s primary clientele is located in informal settlements and 70 per cent are women. AMT strives to work with the most vulnerable segments of society including clients who are female, young, disabled or living with HIV/AIDS (and thus likely to be among the trust’s poorest clients).

AMT is governed by a seven-member board of trustees, whose role is to provide strategic guidance, general supervision of the finances and general management of the organization. The board is appointed by the National Executive Council of Muungano. Board members are drawn from different communities, who collectively appoint a chairperson from among their number. These governance arrangements ensure that the members of Muungano retain oversight of AMT activities. Board members participate in institutional planning, approve plans and budgets, and receive reports on the performance of the organization. They also report to various Muungano teams on the performance of the trust.

Currently, AMT has 10 staff members: an executive director (appointed by the board), two finance officers, and seven field officers who are distributed across the various regions where AMT operates. The field officers’ main role is to help with the delivery of financial and non-financial products to Muungano members, particularly by building the capacity of local grassroots facilitators. The facilitators are responsible for training existing groups, mobilizing new groups, processing and recovering loans, filing reports, and communicating new information to the community.

The AMT methodology and experience are mirrored across 39 other African, Asian and Latin American countries that have comparable levels of urban informality and income disparities. This linkage is achieved through the Kenyan federations’ affiliation to SDI and by extension to an increasingly global way of accessing finance connected to urban development. Local funds such as AMT are called Urban Poor Funds. The unique and distinguishing characteristic of these Urban Poor Funds is the involvement of beneficiaries in the management of these funds. In the Kenyan case, the savings groups of Muungano act as intermediaries between AMT and individuals.(10)

AMT strives to achieve both operational and financial self-sufficiency. This is a challenge because delivery of financial and non-financial services to very low-income households is necessarily an expensive venture. AMT is working to overcome this challenge by rapidly growing its customer base and adopting efficient strategies and tactics for delivering services. It is also seeking to grow and diversify its portfolio and revenue sources to ensure that there are sufficient financial resources to serve its members. In addition to savings, these resources come from:

II. Methods

This study was carried out in August–October 2016. The research was conducted in five urban areas where Muungano has a strong presence: Nairobi, Kiambu, Kitui, Mombasa and Nakuru. The study covers the six financial products that the trust and the federation provide: capacity building, in-situ housing, greenfield housing development, house improvements, and individual and group livelihood loans.

Literature reviewed included AMT’s strategic and business plans, manuals of operation, project reports and group records. New evidence was generated through focus group discussions and individual interviews (using semi-structured questionnaires) with savings group members who have benefitted from these services. Individual member interviews also helped to track possible positive and negative impacts and the challenges that groups and individuals face in fostering inclusiveness, equity and member participation. To capture the interface and accountability systems between the beneficiaries and the various offices of the AMT–Muungano alliance, the research was carried out at three levels: the AMT, savings group, and individual member levels.

Field officers and federation members (from savings groups that were not part of the groups selected for research) played an important role in identifying the participants, developing the questionnaires, testing and administering the questionnaires, and conducting focus group discussions and interviews with the respondents. Most of the participants in this study joined their groups between 2006 and 2016. Some of the respondents founded their groups; others were introduced to their groups by Muungano leaders, other members of the group, friends or family.

Focus group discussions were conducted in 10 savings groups, as well as one with AMT staff and another with three members of the board and the executive director of the trust. Sixty-seven individual interviews were completed with members of the benefitting savings groups. As far as possible, the study ensured that these interviews represented different genders, ages, and particular needs such as disabilities. Participants were selected randomly from each group.

III. Providing Financial Services to The Urban Poor

Muungano and AMT offer deposit and credit services to all residents of informal settlements who are members. The majority of respondents to this study attested to the high quality of these services.

The financial services offered include:

Operational costs are covered by registration fees, fines for late attendance of meetings, and administration-fee contributions from members, which are collected from time to time when necessary (for example, to buy stationery or cover bus fares for conducting banking activities). These have a minimum cost of KSh 10 (US$ 0.096) or KSh 20 (US$ 0.192). Presently 50 per cent of AMT’s total operational costs are covered. The trust’s core financial goal is to cover costs while lending at affordable rates.

a. Deposit products

The formal banking sector in Kenya has historically catered to a select group who were mostly employed by government, and to formal business institutions. The conditions for opening accounts were too onerous for other people. For example, the initial deposit required for opening a bank account was too high for the majority of Kenyans, and a potential customer was required to obtain guarantees from at least two account holders from the same bank before they could open an account. As a result of these restrictions, low-income people did not have access to formal financial services. The microfinance institutions set up to fill this gap initially catered to organized, higher-income groupings. The informal savings groups established by Muungano members therefore helped to meet an important need.

Savings are voluntary and members save different amounts based on their incomes. The respondents in this study saved KSh 50–250 per week (US$ 0.48–2.40). The amount of money accrued in savings from each respondent was on average KSh 7,000 (US$ 67.2) for ordinary savings (for livelihood or day-to-day needs) and KSh 50,000 (US$ 480) for project savings (for housing or infrastructure projects).

Muungano savings groups practise either daily or weekly savings. A savings group that practises daily savings has a collector who moves from door to door at a given time collecting members’ savings. On collection, the savings are registered by the collector in both the member’s passbook and the collector’s book. The collector acknowledges receipt of the member’s savings by signing the member’s passbook. The collector then hands over all the money to the treasurer, who records the total amount in the treasurer’s book. The treasurer likewise acknowledges receipt of funds by signing the collector’s book. All savings groups meet on a weekly basis to ensure that money collected has been duly banked and no unauthorized withdrawals have been made.(11)

In groups that save on a weekly basis, members make a commitment to save every day and submit their savings to the group during their weekly meetings. The savings exercise is aided by three records: the treasurer’s book, the saver’s passbook and the minutes book. Members hand in their savings to the treasurer during the meeting. He or she records all the savings collected alongside each member’s name in the treasurer’s book and the savers’ passbooks and signs each with an acknowledgement of receipt. The minutes book, which is under the custody of the secretary, summarizes the meeting, from the number of people who saved that day to the amount of money collected. The money is banked after every meeting. All groups conduct monthly bank reconciliations by comparing the amounts reflected in the savers’ books with those in their bank account and the treasurer’s book. The treasurer’s book is audited by the group audit team on a monthly basis and also reviewed before the commencement of any project.

One of the earliest interventions of Muungano and AMT (in 2001) was to support these informal savings groups to bridge the divide with formal financial services. AMT entered into a partnership with Standard Bank, which agreed to open up subsidiary accounts for Muungano groups under a main account opened by the federation. Subsequently, other banks in Kenya began to open up. Local banking institutions like Equity Bank adjusted their regulations by drastically reducing the account-opening requirements and the bureaucracy of opening an account. Many low-income people were for the first time able to hold a bank account. However, despite this opening up, many of the lowest-income households were still left out.

A related and important deposit product is the welfare fund, into which a small proportion of each group’s savings is put aside. Generally, the group welfare programmes are of two types. The first is where members contribute an average of KSh 100 per month to assist each other in the event of a death of a member or their immediate family. The second is where the members make ad hoc contributions in the event of another member’s unforeseen crisis, such as death, fire or illness. In many instances, welfare contributions accumulate over time as they are not fully utilized. In such cases, the groups convert the unused funds into capital or use it to buy Christmas gifts or to finance group celebrations. Some groups like the Nakuru West Network also encourage their members to subscribe to the National Hospital Insurance Fund (NHIF),(12) providing an additional layer of security in the event of disaster.

b. Loan products

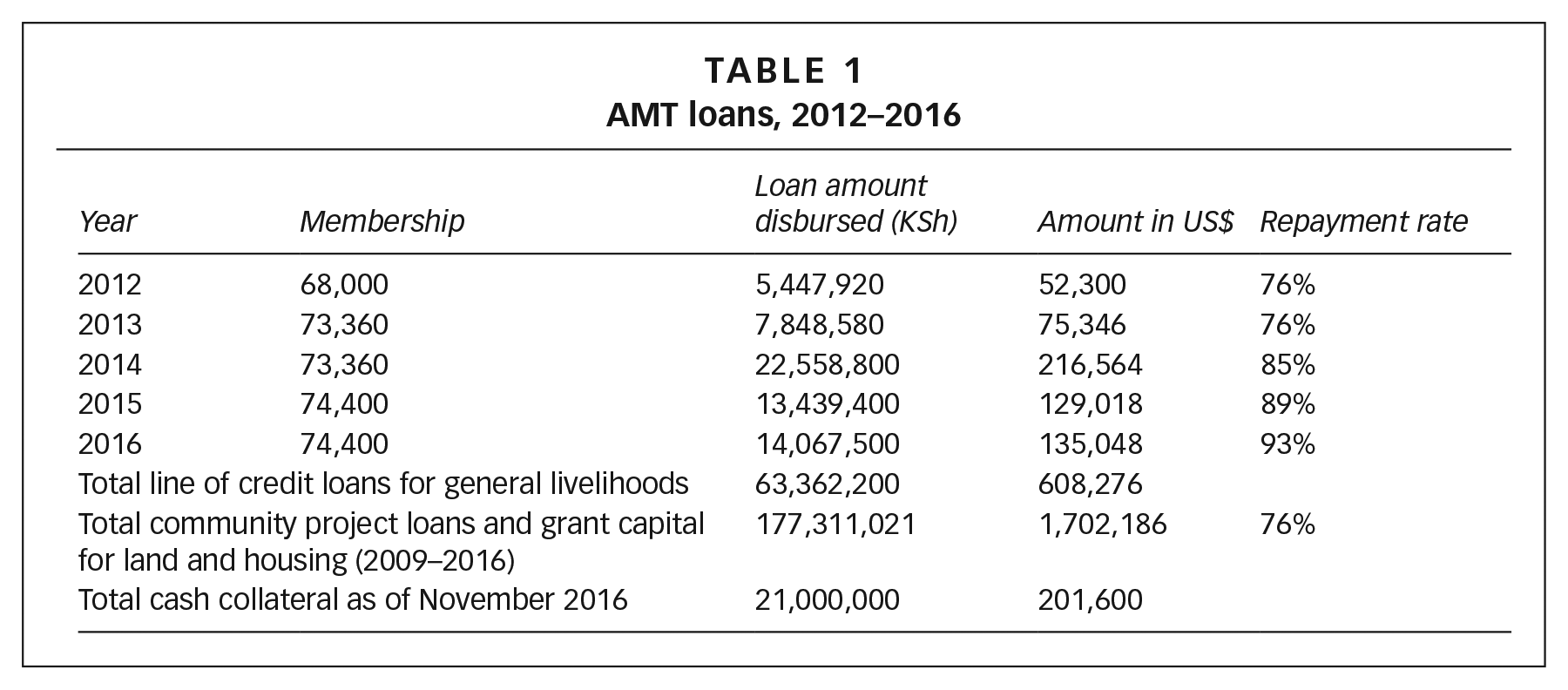

Although deposit products such as savings accounts and welfare funds are important, limited access to capital has continued to disadvantage low-income households. Mungaano groups have responded to demand by lending money to their members, drawing on those same members’ contributions in the form of savings. In most groups, almost all of the money deposited each week is lent out as soon as it is received.This revolving fund model ensures that the groups’ limited resources are used effectively, but also acts as an additional safeguard by ensuring that minimal cash is left in the treasurer’s hands. As of December 2016, 6,822 Muungano members had received financing from AMT for land and housing, while 6,174 members had benefitted from livelihood loans.

The amount a member can borrow from the group is to a large extent determined by the value of their savings, the character of the individual, and their credit history. Personal loan applications are appraised by the committee and approved by the whole group. Group loan applications require loan recommendation by an AMT officer and approval by the AMT head office. A loan contract agreement is then created, followed by a payment of cash collateral and a service charge to the AMT bank account. Loans are disbursed either to the borrower’s bank account or with a cheque, and loan repayments are made directly to the AMT bank account.

Different borrowing limits and processes are adopted depending on the savings group, the amount to be borrowed and the source of the money. Loan sizes are deliberately small in order to attract low-income groups. In Mukhwano, for instance, the respondents explained that the maximum sum that is lent from members’ savings is KSh 1,000 (US$ 9.6), which can be lent for a maximum period of one week. There are exceptions: in the H-Town savings group, internal loans range in size from a minimum of KSh 500 (US$ 4.8) to a maximum of KSh 25,000 (US$ 240). For the most part, however, members need to manage their expectations and recognize that they can only access loans in proportion to their savings.

Internal loans are taken out frequently by individual members. All the respondents in this study stated they had received loans from the group more than three times. 10 per cent of the loan amount is the standard rate for all group loans across the country, and is more affordable than rates of most formal institutions: microfinance lenders charge 22.6 per cent while commercial banks charge 16 per cent.(13) The interest collectible is the main source of income to the group. The repayment period also varies, depending on the loan size, from one month to a maximum period of three months. Internal loan application processes are generally very simple. One of the respondents explained the process of application:

“If I want to obtain a loan from the members’ savings, I apply verbally during the group meeting, the members vet my application, and if they approve it the money is issued and recorded by the treasurer at the meeting but I have to pay interest upfront.”

The use of loans is not restricted and client groups are assisted to develop financial services appropriate for them. For example, some groups have been assisted to develop express one-day loans and daily savings. Some of the groups interviewed also carry out table banking and run merry-go-round schemes,(14) whereby members rotate taking out loans or withdrawing savings.

When a group has insufficient funds to lend to its members, it applies for a loan from AMT. Individual applications are submitted to the group and – if approved – are bundled together into a single loan application. The group then applies to AMT on behalf of its members. On receipt of the applications, an AMT staff member appraises the group by going through its bank statements to establish its savings, internal loan and repayment records, and ensures that the group meets all the loan conditions. To qualify for an AMT loan, a group must be registered as a self-help group, with a group constitution and clear leadership. It must be actively saving, and have a group bank account.

This approach is much simpler than the processes adopted by most formal financial institutions. According to respondents, a formal institution will normally require a borrower to complete a loan application form, an asset form, an affidavit requiring them to take an oath that the loan will be repaid, a loan insurance form, and several other forms for opening individual accounts for each group member. In addition, borrowers bear the costs of loan applications and pay insurance, feasibility study and legal fees. Financial institutions also ask for asset collateral or solid guarantors (i.e. people with savings equivalent to the loan amount) before loan disbursement. In the event of default, the microfinance institution seizes and auctions the assets held as collateral for the loan. By comparison, Muungano groups and AMT cover for an individual’s inability to pay a loan instalment during times of crisis by using the groups’ savings. This greatly reduces the amount of stress that members bear in the event of default.

There are of course instances of loan delinquency and default. In such cases, the other members of a savings group either use the individual’s savings to pay the debt or need to make extra contributions in order to pay AMT. However, these are the exception: the repayment rate is 90 per cent for livelihood loans and 76 per cent for housing loans, and the repayment rate has improved each year (Table 1). The present arrears rate is 17 per cent.

AMT loans, 2012–2016

IV. Providing Non-Financial Services to The Urban Poor

AMT offers technical assistance to Muungano groups, including training in financial management, housing development and business management. Some of this training is embedded in the savings process, such as record keeping. Dedicated training may also be provided during group meetings, formal workshops, and learning exchanges and field visits between Muungano groups.

In some cases, education and training are provided through partnerships with other organizations. For instance, the Kijani Initiative is an organization that aims to empower disadvantaged youth in Kenya to “kick poverty” and build a greener future for themselves, their families and their communities. Kijani helped form the H-Town savings group; subsequently it trained group members in financial literacy and supported some group enterprises. For example, Kijani provided a grant of KSh 35,000 (US$ 336), which was augmented with a loan of KSh 50,000 (US$ 480) from AMT to enable the group to open an M-Pesa agency(15) and a food-vending business.

While individual training is valued, one of the primary goals of Muungano and AMT is to support collective decision-making and action by the urban poor. The structures and processes around savings are key to the development of the necessary social capital. The respondents reported that they felt a strong sense of ownership through the contribution of individual savings, welfare funds and shares. While the roles of the respondents varied depending on their position in the group, they were unanimous in saying they played a part in decision-making in the group.

With SDI Kenya’s support, Muungano adopts a range of non-financial practices that support the development of social capital. Enumeration and mapping are used to collect detailed information on households, buildings and infrastructure within informal settlements. The outputs – geo-spatially tagged maps, censuses and other information – enable informal settlement dwellers to be formally recognized by city authorities, who otherwise lack any robust data on the size, composition and population of these areas. Enumeration also helps to ensure every household is accounted for, and provides a platform to involve them in decision-making processes.(16) The collective design, implementation and operation of group projects has also proven an effective way to build social capital within informal settlements, as well as to establish constructive relations with government agencies. Across African cities, grassroots organizations have deployed co-production as an explicit socio-political strategy as much as a way to meet immediate basic needs.(17)

Many of the savings groups in Kenya were established with a shared purpose, which has allowed groups facing similar challenges to build their resources and support systems. The Mukhwano disability group members, for example, help one other to overcome stigma and discrimination in the community. Respondents noted that when they initially joined the group, many hid their disabled children at home and often saw disability as a curse. Through the support of the group, their attitudes towards disability have changed; they have even opened a day care centre to take care of disabled children instead of hiding them away. The Mukhwano group is a member of the Association for the Physically Disabled of Kenya (APDK), which offers rehabilitation services to persons with disabilities. The Mukhwano group has also been listed as a beneficiary of the National Fund for the Disabled of Kenya, an endowment fund mandated to use its income for the benefit of the disabled within Kenya.

In other cases, the groups have assumed a collective commitment to social and emotional support. The respondents from the Kakimeki group indicated that the other members provide advice when they face challenges at home, such as domestic violence. The women in the group encourage each other and all of them strive to be financially independent, especially as many have fragile marriages. In this instance, the financial services complement the non-financial services: the respondents explained that the welfare funds provide peace of mind, as the savers know that they will receive some financial support in the event of any calamities.

V. Case Studies

Boxes 1–3 outline three short case studies describing the experiences of Muungano savings groups in delivering certain projects: greenfield housing development, land allocation and in-situ slum upgrading, and housing/land relocation.

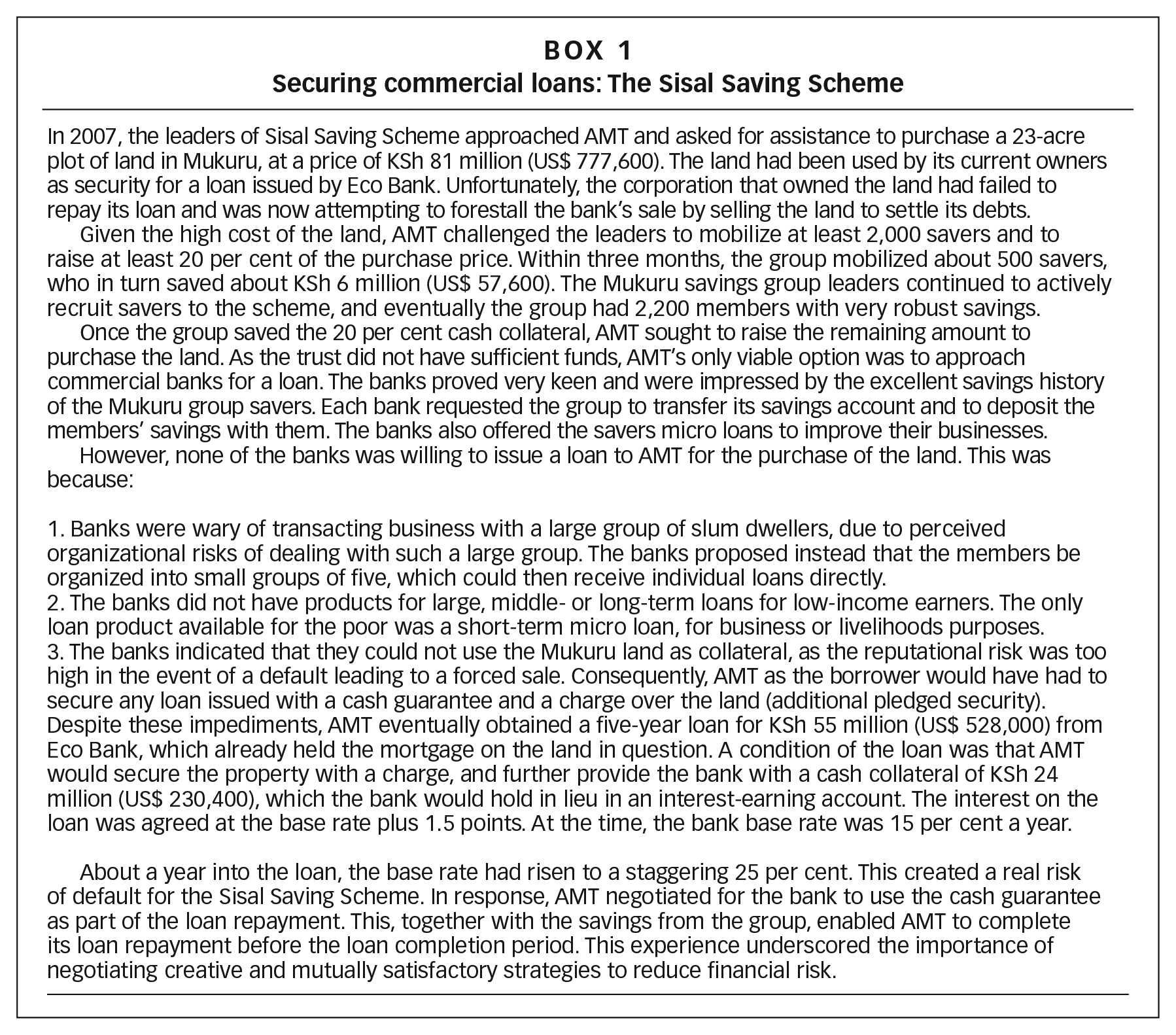

Securing commercial loans: The Sisal Saving Scheme

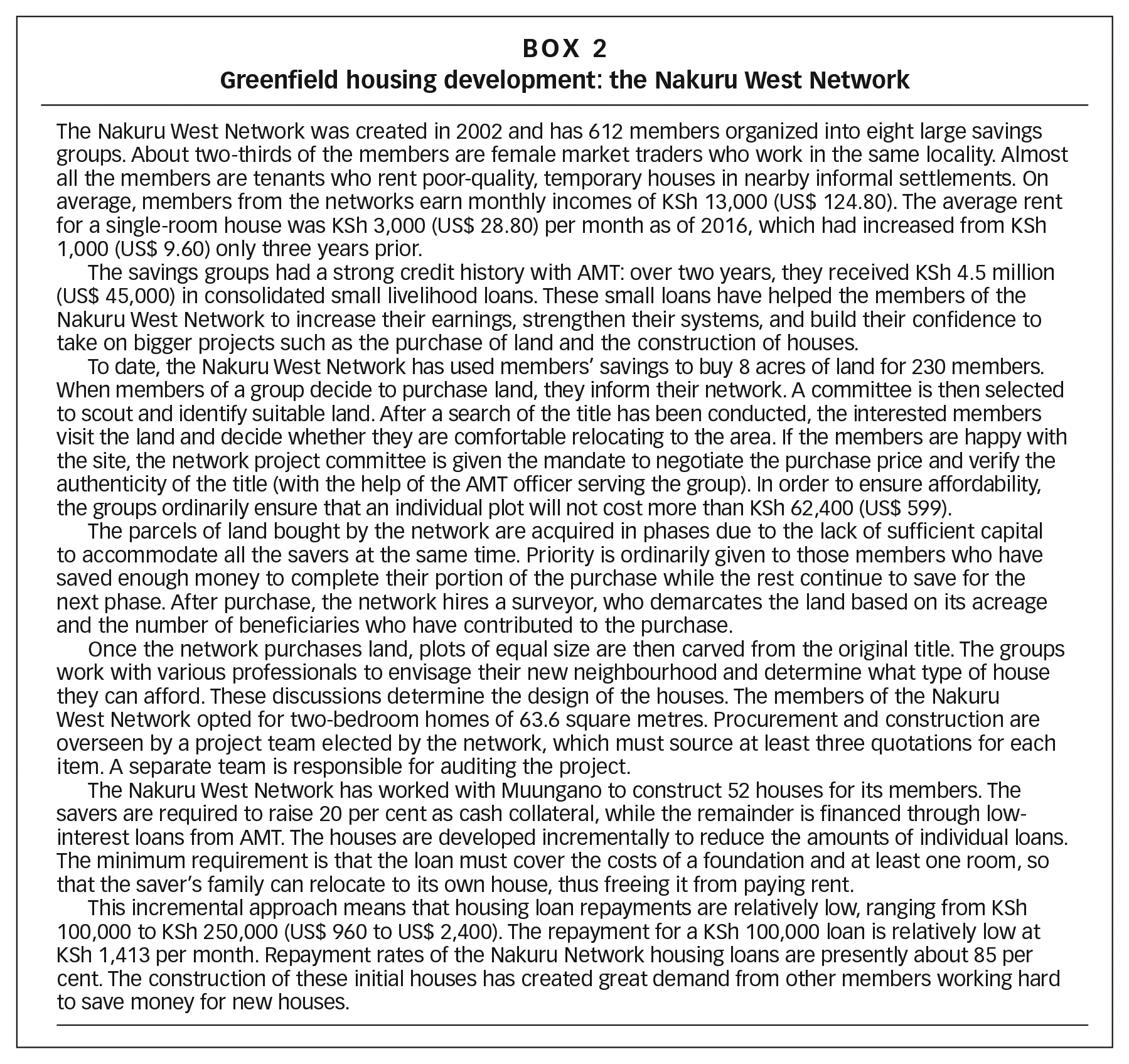

Greenfield housing development: the Nakuru West Network

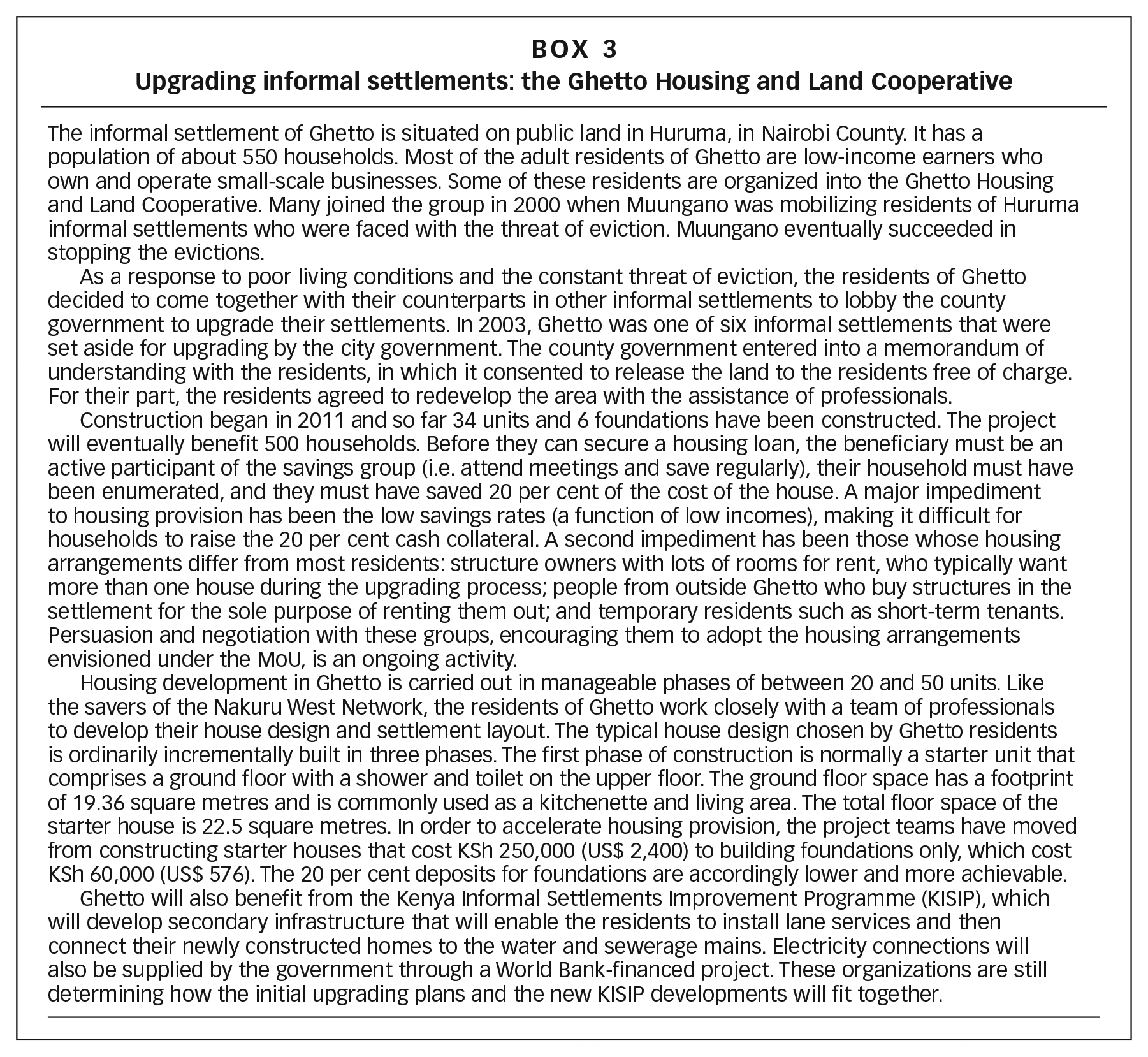

Upgrading informal settlements: the Ghetto Housing and Land Cooperative

VI. Conclusions

AMT and Muungano have been instrumental in providing opportunities for residents of low-income and informal settlements to form strong communal bonds and to create shared development goals for their settlements. These community initiatives have also enabled them to engage constructively with local authorities about strategies to improve the quality of life in informal settlements. A range of specific practices and policies has enabled Muungano and AMT to use financial services to achieve wider social and economic goals.

First, AMT has enhanced

AMT cannot always reach those on the lowest incomes. Even with regular savings and flexible financial products, some cannot afford all of the service conditions (such as the 20 per cent cash collateral for housing loans). This means the lowest-income households are often left out and enables better-off candidates to take advantage of community projects meant for the lowest-income groups. (The problem is worse in Nairobi since Nairobi has extremely low-income groups.) This makes strengthening settlement-based community mobilization even more important, as it enables Muungano and AMT to identify and ensure inclusion of all categories of people.

Second, AMT has promoted

Kenya’s innovations in mobile financial services create opportunities to further improve the efficiency and transparency of service delivery. AMT can use electronic systems like M-Pesa to improve the efficiency and integrity of its financial services, while also expanding its reach and appeal to new Muungano members.

Third, AMT has

To further build the financial capacities of Muungano savings groups, AMT could foster linkages to an increased range of existing services, such as the National Hospital Insurance Fund (NHIF), National Social Security Fund (NSSF), National Council of Persons With Disabilities (NCPWD) and collective investment groups. In the absence of substantially increased capital within the local fund, AMT could also partner with government funds such as the Women’s Enterprise Fund, Uwezo Fund and the Youth Fund. These funds offer low interest rates, ranging from 5 to 8 per cent per annum to low-income groups, and would allow AMT and Muungano to offer their services to more residents of informal settlements. This in turn could accelerate their efforts to transform Kenya’s towns and cities into more inclusive spaces, where low-income and other marginalized urban residents can secure the resources necessary to live healthy and fulfilled lives.

Footnotes

1.

2.

UN-Habitat (2016), Slum Almanac 2015 – 2016, Nairobi, available at ![]() .

.

3.

AMT et al. (2016), Unlocking the Poverty Penalty and Upscaling the Respect for Rights in Informal Settlements in Kenya, Joint project by AMT, Katiba Institute, Strathmore University and University of Nairobi; also ![]() , A Profile of Mukuru kwa Rueben, Mukuru kwa Njenga and Viwandani.

, A Profile of Mukuru kwa Rueben, Mukuru kwa Njenga and Viwandani.

4.

An exchange rate of KSh 1 to US$ 0.0096 was used, based on the daily rate on 1 August 2017.

5.

AMT et al. (2015), Improving access to justice and basic services in the informal settlements in Nairobi, Joint project by AMT, Katiba Institute, Strathmore University and University of Nairobi, available at ![]() .

.

6.

The term “slum” usually has derogatory connotations and can suggest that a settlement needs replacement or can legitimate the eviction of its residents. However, it is a difficult term to avoid for at least three reasons. First, some networks of neighbourhood organizations choose to identify themselves with a positive use of the term, partly to neutralize these negative connotations; one of the most successful is the National Slum Dwellers Federation in India. Second, the only global estimates for housing deficiencies, collected by the United Nations, are for what they term “slums”. And third, in some nations, there are advantages for residents of informal settlements if their settlement is recognized officially as a “slum”; indeed, the residents may lobby to get their settlement classified as a “notified slum”. Where the term is used in this journal, it refers to settlements characterized by at least some of the following features: a lack of formal recognition on the part of local government of the settlement and its residents; the absence of secure tenure for residents; inadequacies in provision for infrastructure and services; overcrowded and sub-standard dwellings; and location on land less than suitable for occupation. For a discussion of more precise ways to classify the range of housing sub-markets through which those with limited incomes buy, rent or build accommodation, see Environment and Urbanization Vol 1, No 2 (1989), available at ![]() .

.

7.

Mathare is a collection of slums in Nairobi and home to about half a million people.

9.

Lines, K and Makau, J (2017), “Muungano nguvu yetu (unity is strength): 20 years of the Kenyan federation of slum dwellers”, Working paper, International Institute for Environment and Development, London, available at ![]() .

.

10.

For earlier literature on these federated grassroots organizations of the urban poor, see Baumann, T, J Bolnick and D Mitlin (2004), “The age of cities and organisations of the urban poor: the work of the South African Homeless People’s Federation”, in D Mitlin and D Satterthwaite (editors), Empowering Squatter Citizen: Local Government, Civil Society, and Urban Poverty Reduction, Earthscan, London, pages 193–210; Weru, J (2004), “Community federations and city upgrading: the work of Pamoja Trust and Muungano in Kenya”, Environment and Urbanization Vol 16, No 1, pages 47–62; and Patel, S, C Baptist and C D’Cruz (2012), “Knowledge is power – informal communities assert their right to the city through SDI and community-led enumerations”, Environment and Urbanization Vol 24, No 1, pages 13–26.

11.

The accountability of any savings group is therefore dependent on active participation by its members, which can prove difficult when they have other responsibilities such as their livelihoods or childcare. One respondent noted, “In every meeting, we always have absent members. It’s a challenge as it delays our progress.” Most savings groups have adopted a range of mechanisms to ensure attendance: “choose another day, change the meeting time, encourage members to attend or increase the amount of penalties for absenteeism”.

12.

The NHIF is a Kenyan government corporation that provides health insurance to Kenyans. In order to benefit from the insurance, it is a requirement to remit monthly contributions. The contributions range from KSh 150–1,700 (US$ 1.44–16.32) depending on a person’s income.

13.

Ngigi, G (2015), “Microfinance banks charge high interest despite taking deposits”, Business Daily Africa, 10 February, available at ![]() .

.

14.

“Table banking” involves all members contributing a similar amount of money during the weekly group meeting. The money is placed “on the table” and the total amount contributed is taken by one or several members as a loan. The conditions on which these loans are given are agreed upon by the group. Most are generally short-term loans ranging from one to two months with an interest rate of about 10 per cent per month. The interest earned from internal loans is accumulated to increase the capital and for the payment of an annual dividend to members. A “merry-go-round” is where members regularly contribute a small amount of money to a fund. Each time money is collected, the full amount is paid to one of the members, who take turns in receiving the payout. After one full cycle, every member has had a turn. In this way, members are saving money until it comes back to them as a larger sum.

15.

According to the Communication Authority of Kenya, 80.5 per cent of Kenyans use a mobile phone. (Communications Authority of Kenya (undated), “Kenya’s mobile penetration hits 80 per cent”, available at ![]() .) M-Pesa, M-Shwari and Equitel are becoming popular mobile applications for making transfers, payments and loan applications, increasingly in partnership with commercial banks such as the Commercial Bank of Africa.

.) M-Pesa, M-Shwari and Equitel are becoming popular mobile applications for making transfers, payments and loan applications, increasingly in partnership with commercial banks such as the Commercial Bank of Africa.

16.

Karanja, I (2010), “An enumeration and mapping of informal settlements in Kisumu, Kenya, implemented by their inhabitants”, Environment and Urbanization Vol 22, No 1, pages 217–239; also Makau, J, S Dobson and E Samia (2012), “The five-city enumeration: the role of participatory enumerations in developing community capacity and partnerships with government in Uganda”, Environment and Urbanization Vol 24, No 1, pages 31–46.

17.

Mitlin, D (2008), “With and beyond the state — co-production as a route to political influence, power and transformation for grassroots organizations”, Environment and Urbanization Vol 20, No 2, pages 339–360; also Banana, E, B Chitekwe-Biti and A Walnycki (2015), “Co-producing inclusive city-wide sanitation strategies: lessons from Chinhoyi, Zimbabwe”, Environment and Urbanization Vol 27, No 1, pages 35–54; and Wamuchiru, E (2017), “Beyond the networked city: situated practices of citizenship and grassroots agency in water infrastructure provision in the Chamazi settlement, Dar es Salaam”, Environment and Urbanization Vol 29, No 2, pages 551–566.

18.

Moser, C O N (2007), Reducing Global Poverty: The Case for Asset Accumulation, Brookings Institute Press, Washington, DC.