Abstract

In conventional urban developments, land and property owners benefit from the uplift in land values that arises from the costly public investments by different levels of government in roads, water, sewerage, transport, education, hospitals and other services, as well as from private investments in production, trade, office, retail, entertainment, sporting and residential facilities. This paper describes the many benefits that come from cooperative land banks that make the development of new urban sites with infrastructure and services self-financing (reducing the need for public investment). They also lower the costs of housing and commercial investments by removing the cost of land. This is achieved by separating the ownership of land (now owned by the cooperative) from the ownership of buildings, and by making the rights of ownership conditional upon use (i.e. use it or lose it). Owners of dwellings get a “dynamic lease” that reflects the value of their investment and in addition obtain shares in the cooperative that capture the value of all sites and community assets. Cooperative land banks can also contribute to financing urban renewal initiatives, although, as the paper describes, this may need supportive legislation.

Keywords

I. Introduction

This paper describes the potential for making urban developments (and the infrastructure and services they need) self-financing. This can apply in substantial greenfield developments as well as significant urban renewal projects. Self-financing development can be achieved through a cooperative land bank (CLB) that separates the private ownership of buildings from land ownership, with all the land becoming owned by a cooperative controlled by its residents. The separate title for buildings can be in the form of a perpetual lease or a “strata title”, as developed in Australia.(1)

The duplex tenure created allows CLBs to capture the uplift in land values from urban development, which can then be used to make the cost of sites and services self-financing.(2) Self-financing urban development sites and services allows commercial investors and pioneer homeowners to avoid the cost of acquiring land. As the cost of land can be over half the cost of building a dwelling, the cost of housing can be halved in many cities.(3)

Eliminating the cost of land in CLB-hosted communities creates competitive advantages for attracting homebuyers, investors in rental housing, enterprises, shopping centres and other commercial facilities. The new investment then increases land values and thus also the equity of the CLB. In addition, the new investment increases the rent/rates paid to the CLB. The increase arises from both additional rent/ratepayers and increases in land values. A virtuous self-reinforcing process of self-financing civic improvement can thereby be achieved.

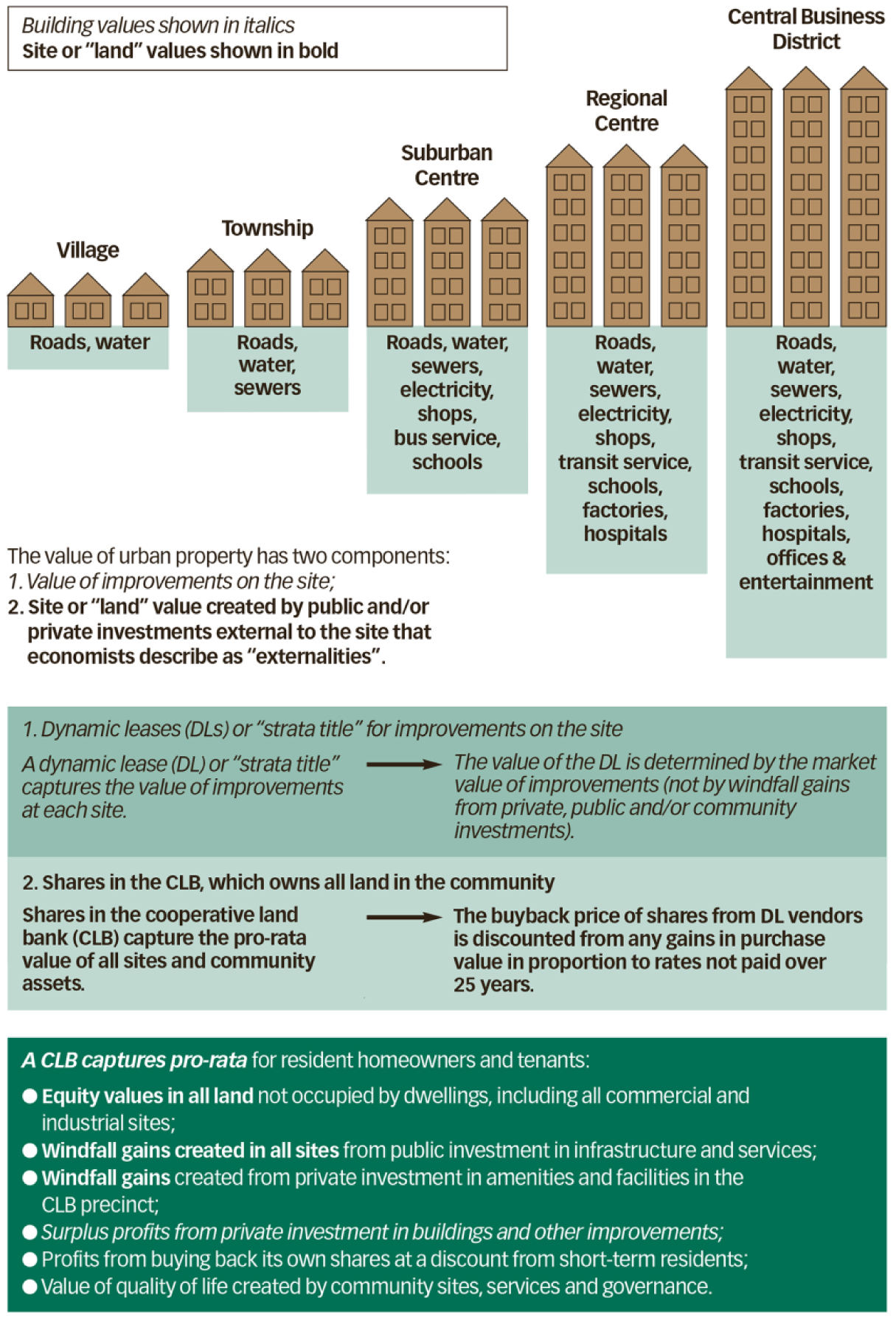

Owners of dwellings built on land owned by a CLB obtain two types of equity to create the “duplex tenure” system illustrated in Figure 1. One type of equity is the ownership of space occupied by the dwelling; this form of equity can be unilaterally sold or mortgaged. The other type of equity is shares in the CLB issued on the basis of, for example, one share for every square metre of land occupied by the dwelling. These two types of equity are connected or “stapled” so that one cannot be sold without the other. Shares in the cooperative can be used to provide both homeowners and tenants pro-rata equity in all the land owned by the CLB, which would include all public areas and sites occupied by trusts, corporations and non-residents. Tenants benefit because they acquire co-ownership interests in both the dwelling they occupy and its stapled CLB shares, which are held in trust until cashed out and/or converted into equity in another residency. Payment may be deferred until the dwelling has been fully depreciated for tax purposes. As residential land might only represent 20 per cent or so of all land in a typical mixed-use urban precinct, the share in uplifted land values accruing to residents in that case could be multiplied by a factor of four. A CLB can be thought of as a real estate investment trust (REIT) that may not necessarily own buildings on its land.

Cooperative land bank (CLB): Separating the ownership of land from the ownership of buildings

It is worth comparing this model to the community land trust (CLT) model. CLTs also remove the cost of land for homeowners.(4) Like CLBs, they imply perpetual ownership of the land by a communal entity. However, while both CLTs and CLBs hold their land in trust in perpetuity, CLTs do not issue shares. This denies CLT residents any negotiable share in the uplift in land values created by their occupation of the land, or of the land sites occupied by any associated infrastructure investments required to service their residency. Thus, by not issuing shares, CLTs can exacerbate rather than ameliorate wealth inequality. Sharing land ownership values associated with a CLT is denied because the formation of a CLT depends upon a gift of land and/or upon money to purchase its sites and services. The benefit of the gift or grant needs to be maintained in perpetuity for affordable housing to be maintained. The adoption of CLTs is limited by their dependency on gifts.

To introduce CLBs, planning officials need to change the business model of developers. Instead of acting as principals in buying, developing and selling realty, developers would need to compete for the right to manage the processes by which CLBs are formed. Development approvals for substantial sites are made conditional upon all the sites (but not buildings) being owned by the CLB. It is in this way that the CLB can capture most of the windfall gains generated by public investments to finance their development.

The ability of a CLB to become self-financing is enhanced when its precinct is sufficiently large to accommodate private investments in rental properties, places of employment, offices, manufacturing, retail, schools and health services. Not only do such investments increase the uplift in land value owned by the CLB, but they also allow the commercial sector to cross-subsidize the residential sector. This is illustrated by the self-financing development of the town of Letchworth, 35 miles north of London,(5) as well as by the many company towns established in the UK during the 19th century.

Letchworth was incorporated in 1903 as the “First Garden City Limited” (FGCL), in the year in which it first obtained a railway station. The FGCL acquired 15 square kilometres of farmland with finance organized by Quaker industrial interests that had earlier been associated with the establishment of UK company towns.(6) The finance was raised by FGCL issuing shares to the public and being listed on the London Stock Exchange. The equity raised was augmented by loans (secured by a floating charge over all the assets of the company) to fund improvements such as waterworks, gasworks, electricity and a public swimming pool.(7)

The Letchworth population grew from 96 persons in 1901 to 33,249 in 2011 on a self-financing basis. If FGCL had issued shares to its residents, as was originally intended,(8) it would have become a CLB. Letchworth provides proof of the self-financing concept even without the ability to capture “surplus profits”(9) or reduce the leakage of economic value in the form of interest exported to non-residents (as described in the following section).

The ability of a CLB to become viable as only a dormitory precinct without any commercial facilities, as commonly occurs with current CLTs, was illustrated in a feasibility study undertaken in Australia. The study was of an isolated rural community in northern New South Wales, whose sites and services were limited to roads and water for 80 self-built homes. The only bankable source of resident income was government welfare entitlements.(10) While the project was shown to be financially feasible, it did not proceed for other reasons.

CLBs are not likely to be viable in high-income urban economies at the scale of many current CLTs involving less than a hundred dwellings. CLBs require scale to integrate sources of added value through investments in infrastructure that would otherwise become what economists describe as “externalities”. Refer to the “infrastructure and community services” shown under the buildings in Figure 1. The economic, social, environmental and political payoff of CLBs is their ability to make a significant contribution to democratizing wealth, as explained in Democratising the Wealth of Nations.(11) While no special legislation may be required to introduce CLBs in greenfield precincts, facilitating legislation is likely to be required for political reasons in urban precincts. The facilitating legislation would transfer the decision-making process in forming a CLB from national, provincial and local governments to voters in the prospective CLB precinct (see Section III for more details).

The ability to make urban development self-financing can be considerably enhanced by adopting more efficient and fairer ways of owning property. These are considered in the next section. Section III provides details of how CLBs might be introduced in large urban renewal or greenfield sites. The concluding remarks in Section IV identify the compelling benefits from introducing facilitating legislation to allow cities to self-finance sustainable, affordable housing.

II. Limitations in Orthodox Economic Analysis

New rules for owning property could enhance self-financing urban development processes by improving the efficiency and equity of market economies. This opportunity is neglected because many economists accept that the nature of property rights is politically determined and thus outside the remit of their analysis. The “conventional wisdom” is that there are only two ways to distribute the wealth of nations – through work or welfare. This leads to a political imperative for maximizing employment to minimize welfare, taxes and the size of government. This is becoming less viable as citizens live longer in retirement, which reduces the percentage of their working life generating taxes.(12)

However, there is a third way to distribute national income – through property rights that provide rents, profit shares, dividends and royalties. Only a privileged minority of citizens are typically beneficiaries of property income. More efficient and fairer rules for owning property, such as those built into CLBs, could allow policies of full employment to be replaced with a policy of fulfilment in employment, community services and/or leisure. This approach would allow a reduction in taxes, welfare and the size of government.

There are three ways in which the “invisible hand” conceptualized by Adam Smith ends up overpaying investors with windfall profits, surplus profits and interest. First, competition for urban land generates unearned “windfall profits” in land values that may not be measured or reported.(13) These profits are described as “windfalls” because they are typically created by external parties. The external parties can be those seeking a home or neighbours improving their properties and the attractiveness of the neighbourhood. Second, uplift in value can also arise from commercial investors creating places of employment nearby or providing retail, leisure, recreation, and other facilities and amenities. Third, a major source of unearned uplift in land values arises from investment by different levels of government in roads, water, sewerage, transport, education, hospitals and other services. In all these cases, the value of nearby property will be enhanced. These windfall profits provide a compelling reason for land to be mutually owned by all within a precinct in order to share the gains widely to improve equity and fiscal efficiency.

The Jubilee line extension of the London Underground system provides an example of the extraordinary windfall profits for property owners who were close to one of the 11 new stations built in 1999. The cost of the public investment required to build the 11 stations was £3.5 billion (approx. US$ 5.5 billion as of June 1999). The uplift in site values created within 1,000 yards of each of the stations aggregated to £13 billion (approx. US$ 20 billion).(14) This meant that the windfall gains captured by landowners were 3.7 times the cost of the public investment! The size of the private windfall gains generated by public investment illustrates the extent to which the current system of property rights is inefficient and inequitable, and concentrates wealth in a way hidden from analysis.

There were no offsetting assets, goods or services to improve the wealth, income and wellbeing of citizens. If all of the £3.5-billion public investment had been borrowed against the security of the land and its rents in a number of CLBs, then the uplift in value would have increased the net worth of the land by £13 billion, less the amount borrowed of £3.5 billion. That is an increase in net worth of £9.5 billion. The average population density of London in 2000 was 11,560 people per square mile.(15) One square mile is approximately the area of 1,000 yards radius around each station. Using the density figure cited above, the increase in net worth per resident would be £74,700 (approx. US$ 117,720 as of June 2000).

Ideally, no major government expenditures should be undertaken to service any urban precinct without mutual ownership being established for all sites that will accrue material benefits from the proposed expenditures. Any government expenditures on improving urban services can be expected to increase land values and hence to make housing less affordable.(16) This explains why it is counterproductive for public funds to be expended on urban amenities before land ownership is held mutually in a CLB.

The uplift in CLB land values created by public investment can be used to generate shareholders’ funds for the CLB. These can then be used to provide additional collateral to support CLB loans, as occurred in Letchworth. A valuation of FGCL investments as of 26 November 1907 had increased by 32 per cent since 30 September 1903.(17) A virtuous self-reinforcing circle of increasing collateral with increasing sources of rent/rates to service the CLB debt arises from the values added by private investors in homes and/or commercial properties.

Uplift in land values is also increased by any government subsidies to homebuyers and/or tenants. While subsidies and grants to homebuyers and/or tenants can make housing more affordable, they do so on a basis that is not self-financing and in a manner that increases windfall gains for neighbouring landowners. The result is likely to exacerbate wealth inequality by directing the gains to owners only.

Owners of the means of production also get overpaid through “surplus profits” not identified by accountants and thus invisible to economists.(18) Surplus profits are those that continue to accrue after investors have already recovered the cost of their investment with a sufficient return to attract their investment.

As investors are not fortunetellers, their most urgent concern is not profit, but recovering all the money put at risk. Cash profits cannot be made unless the cost of the investment is paid back. For this reason, investors will not invest unless they expect to recover the full cost of their investment in the foreseeable future. Accounting doctrines do not require accountants to report when an investment has paid back its cost, or when the investment is providing profits beyond the time period required to provide the incentive to invest. Depreciation is a non-cash so-called “expense” that is used to reduce the size of reported profits and so also the tax liability. Rather than being an expense, depreciation is the opposite because it is a way for investors to obtain back tax free a return of their investment. This return of the investment is used to reduce the reported return on the investment.

Cash obtained by investors beyond the time horizon required for obtaining the incentive to invest represents a surplus incentive. A surplus incentive, or “surplus profit”, is by definition inefficient as it means investors are being overpaid. Surplus profits exacerbate inequality and may be significant. They can be orders of magnitude greater than the original investment.(19)

Owners of money also get overpaid from interest payments when neither the money owner nor the money is creating value for society.(20) Removing the export of interest payments outside of the CLB area can considerably enhance the self-financing ability of communities.(21) For instance, homebuyers may typically spend up to a third of their income servicing their home loans. The value of interest paid over the life of a long-term home loan may be as much as or more than the value of money initially borrowed.(22) Local currencies are also ways to enhance self-financing urban development.(23) While establishing a proprietary local currency can provide significant benefits, it is an optional feature when forming a CLB. It is the capture of windfall and surplus profits that is the inherent feature of CLBs. How a CLB captures and distributes overpayments to investors is described in the following section.

III. Establishing a Self-Financing Urban Development Process

The threshold challenge in establishing a self-financing process in any context is to assemble a sufficient area of land to create a viable CLB community. A viable size is best determined by a feasibility study. The precinct needs to be sufficiently large to accommodate supporting education (for non-professional occupations and entry-level to advanced education), health care, employment, retail, sporting and recreation, and other amenities. Long-term sustainability also requires access to energy, water and food resources. While some internal self-sufficiency may be possible from some renewable energy sources, water tanks and community gardens, many compromises may be required in large cities. The above requirements are broadly consistent with the UK government announcement in April 2014 about funding “Locally-led Garden Cities”.(24) The UK Department of Communities and Local Government (DCLG) invited projects that would provide “land value capture for the benefit of the community”, “green belts”, and the “opportunity for residents to grow their own food” for communities with at least 15,000 new dwellings. The aggregate target of new dwellings over five years was 250,000. Allocated government spending over this period was over £12 billion (approx. US$ 20.3 billion as of April 2014). It included £1 billion (approx. US$ 1.7 billion) on “Large Sites Infrastructure” in “recoverable loans” and £2 billion a year of “mainly grant funding, some recoverable”.

Neither the government announcement nor the DCLG official in charge of the proposal specified how such substantial loans would become “recoverable” or whether government expenditures would be conditional on the government first establishing a process for “land value capture for the benefit of the community”.(25) Founding members of the New Garden Cities Alliance (NGCA) were informed that some infrastructure expenditure had already been undertaken in prospective sites without any process in place for land value capture. Such expenditure is counterproductive as it increases site values and so exacerbates the difficulties of producing affordable housing.

The conversion of agricultural (greenfield) sites, as occurred in Letchworth, is one approach to assembling a viable precinct. The low-cost aggregation of industrial sites, informal settlements or inner-city precincts, whose land and buildings have reverted to councils from non-payment of rates and taxes, provides another opportunity for introducing self-financing urban development. Other prospective situations are the conversion of old dockland areas, airfields and rundown brownfield areas.

Two generic types of sites are considered below. The first are precincts that may not require any special facilitating legislation, like greenfield, brownfield or redevelopment sites or informal settlements. The second are urban precincts that require facilitating legislation to provide a politically acceptable basis for aggregating existing built-up areas into a precinct of viable size. A viable size is likely to involve thousands or even tens of thousands of dwellings, sufficient for the area to become a ward of a local government body or even an incorporated suburb owning all its own land.

a. Self-financing urban development without special legislation

The basic steps required in precincts that do not require special legislation are as follows:

The arrangements also provide the means for the CLB to expand organically over time by acquiring additional sites, through issuing RPPS in exchange for acquiring contiguous sites without expending cash. The need for cash can also be reduced and/or eliminated by not acquiring any buildings on the land. Instead, the site vendor (for instance the original owner) would retain ownership of buildings through a DL.

If the site acquired included a mortgaged building, the replacement security available to the existing lender should be of at least equal value. This is because the value of both the building and its site would be reflected in the value of the DL and the RPPS. The development values created should improve the lenders’ security. In addition, the risk of the existing lender liquidating its security should be reduced through the market-making role of the CLB in buying back only any stapled shares of a DL when it is sold.

The DLs would specify that after the building had been written off for tax purposes, its ownership would become vested in the CLB. This would limit the overpayment to investors of surplus profits. In this way, surplus profits, with any associated residual market equity value of buildings, is transferred to citizen residents through their CLB shares.

In the event that the buildings being written off contain rental housing, the CLB would distribute co-ownership equity of each dwelling to each of the tenants who occupy the dwelling, proportionate to their length of occupancy, the area they occupy, and the tenure of the landlords’ DL, plus such residual value as may be determined by the CLB. Similarly, the CLB would grant tenants pro-rata co-ownership equity in the CLB shares associated with the dwelling they occupy. This creates an incentive for housing tenants to take responsibility for the repair and maintenance of their dwellings to reduce the maintenance costs for investors. This arrangement also: (a) provides a basis for investors in CLB rental housing to obtain enhanced returns; and (b) ensures that citizen residents in a CLB become shareholders on a pro-rata basis. Tenants acquire CLB shares without cost so as to democratize the wealth of cities.

Investors have an incentive to invest in CLB rental dwellings through DLs because they avoid the cost of buying land. This significantly reduces the size of their investment relative to similar properties in non-CLB precincts. In this way, a CLB can provide enhanced returns for rental housing investors with significantly less money put at risk, so a higher rate of return can be obtained over that available from investing in non-CLB precincts.(28) There is no need to provide investors with any agreed minimum rate of return. Investors already obtain a higher return in a CLB because for the same rental income their investment is less, as they do not need to expend money on buying land. This also means that instead of surplus profits accruing to investors, these are transferred to citizens through their CLB shareholding. Likewise, citizens would obtain pro-rata equity in the residual market value of all commercial buildings written off for tax purposes. The pro-rata equity accruing to resident citizens could include supermarkets, shops, office buildings, manufacturing plants, government and recreational enterprises. New investors who do not have to purchase CLB shares cannot share in any uplift in value of the land they occupy. So any uplift in value of their site also accrues to the common CLB voting shares that are only held by resident citizens.

The CLB can admit residential members from government housing waiting lists and/or other applicants who meet certain criteria to buy and/or build homes and/or become tenants in rental properties. As the CLB removes the cost of land for homebuyers, it also removes the usual deposit gaps, so it is likely that the financial outlay for mortgage servicing will be less than that for renting. The CLB allows both the DL and the shares owned by homeowners to be registered as security for obtaining home loans.

Pioneer homebuyers acquire shares in the CLB at no cost, pro-rata to the space occupied by their DL. Tenants acquire deferred co-ownership CLB shares at no cost, pro-rata to the tenure of their occupancy as a proportion of the tenure of their landlord’s DL.

Voting rights would be allocated as for a local government body. A CLB could become a formal political unit of a local government ward, suburb, town or city.

The ownership of CLB common voting shares is restricted to citizens. RPPS issued to acquire property would not come with votes. This eliminates any external or corporate ownership, as well as control or loss of local political or economic sovereignty of the CLB precinct. It also minimizes the export of windfall gains and surplus profits.(29) Members raise mortgages on the security of both their DL and CLB shares to finance the purchase of their homes from traditional sources of housing finance.

If a homeowner did not occupy their property and rented it out, then their tenant would acquire co-ownership interests in both the dwelling and its associated CLB shares. The same “use it or lose it rule” would apply if the dwelling was not occupied, but the co-ownership rights would then accrue to the CLB. This use it or lose it rule would create an incentive for homeowners to negotiate a lower price to sell their property. The period of dwelling vacancy could be tied to the period of residency required by local government to be eligible to vote in local government elections. The rate at which homeowners lost equity in their DL could be tied to the tax depreciation rate for commercial buildings, or say 4 per cent per year.

If the purchase cost of CLB shares rose high enough to discourage homebuyers, then home seekers could still obtain equity in both a dwelling and the CLB by becoming a tenant in a rental property. In this way, market forces are created to establish long-term housing affordability by creating pressures for homeowners to reduce their selling price to avoid losing equity in both their homes and CLB shares.

b. Self-financing urban development with facilitating legislation

A major problem in large cities like London, neglected by the “Locally-led Garden Cities” initiative in the UK, is that low-income workers who are required to maintain cities cannot obtain affordable accommodation near their places of work. Examples are police, fire service, teachers, nurses, child minders, aged care workers, bus and train drivers, and others providing essential services. Instead of exacerbating this problem by introducing new settlements or “garden cities” on the outskirts of large cities, affordable housing is ideally required in their inner cities or suburbs. This would reduce the need for transit services like buses and trains. Self-financing redevelopment of inner-city precincts would also be supported by other well-established infrastructure.

Changing the rules of ownership in greenfield or in aggregated brownfield sites is unlikely to be politically contentious when market mechanisms are involved. However, obstacles remain in established inner urban precincts of large cities in nations with democratic forms of government. Many advanced democracies have lost their integrity around representing the interests of the many by becoming subject to powerful private minority interests.

Changes in the nature of ownership might only become politically feasible in democracies with facilitating legislation that transfers decision-making to the voters who are affected. The more concentrated the ownership of urban land (including by foreign investors), then the more likely that citizens would vote to change the rules to provide them all a “piece of the action”. The cost of facilitating legislation would be trivial in relation to the proposed “non-recoverable” expenditures on supporting infrastructure services the UK government announced in 2014. In addition, there are substantial macroeconomic benefits. These arise because CLBs own the land and so reduce or eliminate the export of rents, windfall gains and surplus profits outside of their jurisdiction. Other politically compelling outcomes would be to reduce inequality without increasing taxes, central government welfare, or the size and cost of government.

The facilitating legislation required would allow citizens to petition their local government body to hold a referendum to convert all existing title deeds in a viable precinct to duplex tenure. As in certain political elections, only individuals recognized as citizens would be entitled to vote. To protect the electability of politicians introducing such legislation from any un-represented vested interest, the requirement to approve the adoption of duplex tenure could be raised from 50 per cent of voters to say 75 per cent.

As noted above, property owners and lenders using their property as a security should not suffer any diminution in value. However, their entitlements to future windfall gains and surplus profits become diminished. It is the inclusive sharing of these gains with all voters that could provide the basis for at least 75 per cent of residents voting to establish a CLB. This could occur whether or not redevelopment was also undertaken to create new affordable housing. It should be remembered that the area of land occupied by residents could be a minor proportion of the CLB precinct. If residents only occupied 10 per cent of the precinct, the uplift in gains accruing to the resident shareholders could include those arising from the other 90 per cent of the precinct, less the limited allocation of gains to service the RPPS.

The facilitating legislation could specify some minimum number of residents, say 100, lodging a petition for a referendum to establish a CLB by this means. The petition would identify the boundaries of the proposed precinct that would determine which residents are entitled to vote. Advice for UK citizens in determining prospective boundaries would be available from nonprofit organizations like the NGCA and developers seeking to be involved in redevelopment to create new affordable housing.

Holding the referendum could be made conditional upon there being competing redevelopment proposals from property developers. The development process would no longer depend on the private capture of windfall gains and the associated risks for developers. Each redevelopment proposal would be required to provide an economic impact statement regarding the precinct’s conversion to duplex tenure. Residents could then vote on whether to form a CLB, as well as which developer should undertake the redevelopment.

The facilitating legislation could also be used to define a special purpose legal structure for forming the CLB. In this way protection for residents and other stakeholders could be introduced with the option for the CLB to become recognized as a political unit of local government. The tax implications of a CLB could also be clarified or determined in the facilitating legislation.

Overall, the efficacy of the UK government’s 2014 proposal for “Locally-led Garden Cities” could be very much increased and spread geographically with such facilitating legislation.

IV. Conclusions

CLBs introduce a more efficient and fairer way of financing and sharing the costs of urban developments. Their “use it or lose it” feature, as found in squatter settlements, creates a way to enrich local sovereignty and democracy by allowing resident citizens to control their neighbourhoods.

CLBs resolve the concerns of Henry George,(30) who wanted to tax urban land that was underutilized by owners seeking to obtain speculative windfall gains while denying the use of the site to others. The purpose of the tax was to: (a) recover the costs expended by governments that made land more valuable; and (b) encourage the better use or development of underutilized urban land. CLBs meet both aims by: (a) transferring the costs of urban infrastructure from governments to the CLBs while eliminating speculative private windfall gains; and (b) transferring the decision on how each site might be developed from the individual site owner to the best interests of all owners represented by the CLB. The Georgist land tax is socially unacceptable as it forces low-income homeowners to redevelop their site or sell it to those who have the means to do so. These options are onerous for low-income residents, especially those who do not want to change either their homes or the location where they have their social support networks. A Georgist land tax also introduces the cost of undertaking valuations of each individual site and estimating the degree to which it is being underutilized. In comparison, the cost of evaluating CLB shares would be relatively minor, as these would be similar to those routinely carried out for publicly traded REITs.

CLBs provide a modern way to implement the idea of Thomas Spence, who proposed that a parish-based corporation own all land, with its citizens as members.(31) But unlike the approach proposed by Spence, the 2004 report prepared for the UK government by Kate Barker did not consider the option of changing the nature of property rights for “securing our future housing needs”.(32) Barker, like Thomas Piketty, is an economist, and policy options of economists are generally limited to suggesting changes in the tax system rather than changing the nature of property rights. The taxing away of unearned gains has been the traditional solution.(33) Rather than taxing unearned gains, this paper identifies the benefits of communities sharing and preserving the gains.

One theoretical contribution of this paper is to highlight how wealth inequality is created in three ways that are not systematically reported by accountants, so as to inform economists, policymakers and lawmakers. An important policy insight is that it is counterproductive for any public spending or tax relief to be introduced to promote affordable housing unless the ownership of land is mutualized so as to capture development values for the common good. The public spending that should be avoided includes government-owned housing, first homeowner grants or other subsidies to rent or buy dwellings.

The policy practice recommended is that urban development should not be undertaken based solely on designing the visible structures, but also on the invisible architecture of owning, controlling, governing and financing urban development. In particular, it is recommended that governments make any substantial expenditure on urban development conditional on the affected sites becoming mutually owned and controlled by resident citizens through the “use it or lose it” policy introduced for property rights in the development precinct.

Footnotes

2.

Angel, Shlomo, Raymond W Archer, Sidhijai Tanphiphat and Emiel A Wegelin (editors) (1983), Land for Housing the Poor, Select Books, Singapore, page 29; also Doebele, William A (1987), “The Evolution of Concepts of Urban Land Tenure in Developing Countries”, Habitat International Vol 11, No 1, pages 7–22 (pages 18–20); Johnson, Thomas (1987), “Land Banks Open Possibilities”, Town & Country Planning Association Journal Vol 24, January; Solowoway, Scott and Thomas Johnson (1986), “The Use of Co-operative Land Banks & Other Alternative Forms of Public Finance to Promote Community Economic Development”, Unpublished thesis for a Master’s Degree at the Massachusetts Institute of Technology, Cambridge, USA; Turnbull, C S Shann (1973a), “New Modes of Land Tenure”, Australian Government Commission of Inquiry into Land Tenures, Transcript of proceedings, Sydney, 23 July, pages 598−617; Turnbull, Shann (1975), Democratising the Wealth of Nations, The Company Directors’ Association of Australia, Sydney, pages 65–70, available at: https://ssrn.com/abstract=1146062; Turnbull, Shann (1977a), “A Peaceful Path to Real Reform: Self-financing Suburbs”, Royal Australian Planning Institute Journal Vol 15, No 3, pages 81–84; Turnbull, Shann (1977b), “Landbank: A Way Out of the Land Price Spiral”, Real Estate Journal Vol 27, No 8, pages 10–11; Turnbull, Shann (1977c), “Cutting the Price of New Housing”, The Australian, 9 May; Turnbull, Shann (1983), “Co-operative Land Banks for Low-Income Housing”, in Shlomo Angel, Raymond W Archer, Sidhijai Tanphiphat and Emiel A Wegelin (editors) (1983), Land for Housing the Poor, Select Books, Singapore, pages 511–526, available at http://papers.ssrn.com/abstract_id=649642; Turnbull, Shann (1984), Multiple Occupancy Development: Feasibility Study by the Land Commission of NSW, Sydney; Turnbull, Shann (1985, unpublished), Pilot Multiple Occupancy at Wadeville: Acquisition Feasibility Report for the Land Commission of NSW, Sydney; Turnbull, Shann (2008), “Affordable housing policy: Not identifiable with orthodox economic analysis”, Paper presented to the American Real Estate and Urban Economics Association conference, Istanbul, 6 July, available at http://papers.ssrn.com/abstract_id=1027864; and Turnbull, Shann (2016a), “How might the funding of infrastructure land taxes affect housing affordability?”, Economic Papers Vol 35, No 3, pages 292–296.

3.

Davis, Morris A and Michael G Palumbo (2007), The Price of Residential Land in Large US Cities, Finance and Economics Discussion Series, Federal Reserve Board, Divisions of Research & Statistics and Monetary Affairs, Washington, DC, available at http://www.federalreserve.gov/Pubs/feds/2006/200625/200625pap.pdf; also Moran, Alan J (2006), The tragedy of planning: Losing the Great Australian Dream, Institute of Public Affairs, Melbourne, page 60, available at ![]() .

.

4.

Davis, John E (2014), Origins and evolution of the community land trust in the United States, Center for New Economics, available at http://berkshirecommunitylandtrust.org/wp-content/uploads/2015/02/Origins-Evolution-CLT-byJohnDavis.pdf; also Harrington, Catherine and Rose Seagrief (editors) (2012), The community trust handbook, National CLT Network, London, available at http://library.uniteddiversity.coop/Community_Land_Trusts/CLT_Hankbook/CLT_Handbook-Chapter_1-Introduction.pdf; Monro-Clark, Margaret (1982), Alternative modes of land tenure: A comparison of two models, University of Sydney; Swann, Robert (1997a), “Alternatives to ownership: Land trusts as land reform”, in Ward Morehouse (editor), Building sustainable communities: Tools and concepts for self-reliant economic change, Second revised edition, The Bootstrap Press, New York, pages 47–51, available at ![]() ; and Swann, Robert (1997b), “The cooperative land bank concept”, in Ward Morehouse (editor), Building sustainable communities: Tools and concepts for self-reliant economic change, Second revised edition, The Bootstrap Press, New York, pages 23–25, available at http://ssrn.com/abstract=1128862.

; and Swann, Robert (1997b), “The cooperative land bank concept”, in Ward Morehouse (editor), Building sustainable communities: Tools and concepts for self-reliant economic change, Second revised edition, The Bootstrap Press, New York, pages 23–25, available at http://ssrn.com/abstract=1128862.

5.

See reference 2, Turnbull (1977a and 2016a); also Howard, Ebenezer (1946 [1902]), Garden Cities of To-morrow, Faber and Faber, London; and Purdom, Charles B (1913), The Garden City - A Study in the Development of a Modern Town, J.M. Dent & Sons Ltd, London, available at ![]() .

.

6.

Purdom, Charles B (1963), The Letchworth achievement, J.M. Dent & Sons, Letchworth, pages 24–36.

7.

See reference 6, page 233.

8.

See reference 6.

9.

Turnbull, Shann (2006), “Grounding economics in commercial reality: A cash-flow paradigm”, in Peter Kreisler, Michael Johnson and John Lodewijks (editors), Essays in Heterodox Economics: Proceedings of the Fifth Australian Society of Heterodox Economists Conference, pages 438–461, available at ![]() .

.

10.

See reference 2, Turnbull (1984 and 1985). An earlier feasibility study of a Western Australian mining town of 5,000 people, which serviced what was then the largest iron ore mine in the world, is set out in Appendices 3 and 4 of Turnbull, Shann (1976), Land Leases without Landlords, Paper presented to the United Nations Habitat Forum, Vancouver, 8 June, available at ![]() .

.

11.

See reference 2, Turnbull (1975); also Turnbull, Shann (2015), “Sustaining society with ecological capitalism”, Human Systems Management Vol 34, No 1, pages 17–32, available at ![]() .

.

13.

Hagman, Donald G and Dean J Misczynski (editors) (1978), Windfalls for Wipeouts: Land value capture and compensation, American Society of Planning Officials, Chicago.

14.

Riley, Don (2002), Taken for a Ride, Centre for Land Policy Studies, London.

17.

See reference 2, Turnbull (2016a), page 29. This uses data from Purdom; see reference 5, ![]() , page 238.

, page 238.

18.

See reference 9.

19.

Turnbull, Shann (1973b), “Time-Limited Corporations”, ABACUS Vol 9, No 1, pages 1–28, available at ![]() .

.

20.

Gesell, Silvio (2002 [1916]), The Natural Economic Order, available at ![]() .

.

21.

Gesell inspired the introduction of negative interest rate money so that money would not create inequality or become an asset class that misallocated productive resources. Keynes described Gesell as an “unduly neglected prophet”. Keynes, John M (1936), The General Theory of Employment, Interest, and Money, Harcourt Brace Jovanovich, New York, Chapter 23, Part VI, available at ![]() .

.

22.

Kennedy, Margrit (1988), Interest and Inflation Free Money: How to create an exchange medium that works for everybody, Permakultur Institut e.v., Steyerberg.

23.

24.

Clegg, Nick and Eric Pickles (2014), Locally-led Garden Cities, Prospectus, UK Department of Community and Local Government, available at ![]() .

.

25.

26.

Details of self-financing self-liquidating currencies are provided in Turnbull, Shann (2016b), “Terminating currency options for distressed economies”, Athens Journal of Social Science Vol 3, No 3, July, pages 195–214, available at ![]() .

.

28.

See reference 2, Turnbull (1975), Appendix; also Lewis, Michael and Shann Turnbull (2012), “The Cooperative Land Bank: A solution in search of a home”, i4, November, Canadian Centre for Community Renewal, available at ![]() .

.

29.

This is to avoid what Penrose described as “unlimited, unknown foreign liability”. Penrose, Edith T (1956), “Foreign investment and the growth of the firm”, Economic Journal Vol 66, June, pages 220–235, page 235.

30.

George, Henry (1912 [1879]), Progress and Poverty: An Inquiry into the Cause of Industrial Depressions and of Increase of Want with Increases of Wealth: The Remedy, Doubleday, Page & Co., New York, available at ![]() .

.

31.

Spence proposed this during a period when thousands of private acts were passed by the UK Parliament to enclose public land for private use. His idea was that parish members would elect members of Parliament, with the government funded by the parishes from the rents collected from their residents. As Parliament was elected at that time by only 5 per cent of all males, this proposal would have made all males with an interest in land eligible to vote through their parish, consistent with the views of John Locke (1632–1704). Spence, Thomas (1775), Property in Land is Every One’s Right, Presented to The Philosophical Society, Newcastle upon Tyne, 8 November, published in 1793 as The Rights of Man, available at http://www.thomas-spence-society.co.uk/rights-of-man/. See reference 30; also Mill, John S (1848), Principles of Political Economy, Book V, Chapter II, available at http://www.econlib.org/library/Mill/mlP.html; Barker, Kate (2004), Delivering stability: securing our future housing needs, Final report, HM Treasury, London, available at http://news.bbc.co.uk/nol/shared/bsp/hi/pdfs/17_03_04_barker_review.pdf; and Piketty, Thomas (2014), Capital in the Twenty-First Century, Harvard University Press.

33.

See reference 30; also see reference 31, Mill (1848), Barker (2004) and ![]() .

.